california municipal wastewater treatment & reuse

TRANSCRIPT

ADVANCED WATER TREATMENT & DESALINATION INSIGHT SERVICE GREENFIELD + WATER = BLUEFIELD

DATA INSIGHT California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook May 2015

Water Shortage / Flickr / Source: Andrew Hart / CC BY-SA 2.0

California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook

ADVANCED WATER TREATMENT & DESALINATION

DATA INSIGHT

2

1. Summary 2. Intensifying Drought Conditions Across California 3. Sizing California’s Water Use By Sector 4. Regulatory Environment Evolves in Face of Deteriorating Conditions 5. Population Growth Heightens the Long-Term Challenge 6. California’s Demand-side Challenge 7. California Municipal Wastewater Reuse In Broader US Context 8. Reclaimed Water Utilization by Sector 9. Wastewater Reuse Growth Hinges on Urban Water Suppliers 10. Shifts Along the Technology Adoption Curve 11. Wastewater Treatment Plant Capacity and Unused Effluent Flows by County 12. Ocean Outfalls Reflect Untapped Reuse Potential 13. Cost Competitiveness of Reclaimed Water 14. Planned Wastewater & Reuse Project Pipeline, 2014-2035 15. Planned Wastewater & Reuse Project Pipeline by Development Stage 16. SoCal Represents Market Epicenter

Exhibits • April 2015 Drought Intensity • Top 10 Counties by Forecasted Population Growth • California Urban Water Outlook, Forecasted Demand Impact 2015-2040 • California Water Use by Sector • State Legislation, 2009-2014 • Urban Water Usage Reductions via Voluntary Restrictions, 2014-2015 • Reused Wastewater Flow in the US • Reclaimed Water Applications by Sector • California Urban Water Supplier Current & Planned Sources, 2010-2035 • Relative Technology Adoption and Applications of Reclaimed Water • Planned Project Technology Selection, 85 Projects • Wastewater Treatment & Reuse Capacity Segmentation by Plant • Wastewater Volume Discharged (Not Reused) by County • California Ocean Outfalls by Region and Flows • Supply Comparison: MWD Rates vs. Alternative Sourcing Costs • Bottom-Up Reuse Project Pipeline by Capacity, 2014 - 2035 • Planned Reuse Projects in California by Development Stage and Year • Planned Reuse Projects in California by County

Appendix: Planned Wastewater Treatment & Reuse Plants

• This Data Insight highlights the following: - Critical water & environmental policies shaping the

California wastewater reuse market going forward.

- Identification and analysis of planned projects and their impact on market growth.

- Analysis of more than 479 existing projects, including reused water application, capacity, reuse vs. disposal rates, and location.

- The outlook for advanced water treatment technologies and primary drivers for their adoption.

• This report draws on Bluefield Research’s Advanced Water Treatment & Desalination Insight Service and its ongoing deliverables and research team.

Data Insight Details Insight Analysis

Data Analyzed • State policies 2009 to present impacting municipal

wastewater reuse • 479 municipal wastewater treatment plants • Wastewater flows by county • Reclaimed water use by sector & region • 372 water supplier plans, 2010-2035 • 85 planned municipal wastewater reuse systems–

upgrades, expansions, and greenfield • Analysis of wastewater flows from 50 ocean outfalls • Population forecasts by county

California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook is part of Bluefield’s Advanced Water Treatment & Desalination Insight Service.

About This Data Insight

California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook

ADVANCED WATER TREATMENT & DESALINATION

DATA INSIGHT

3

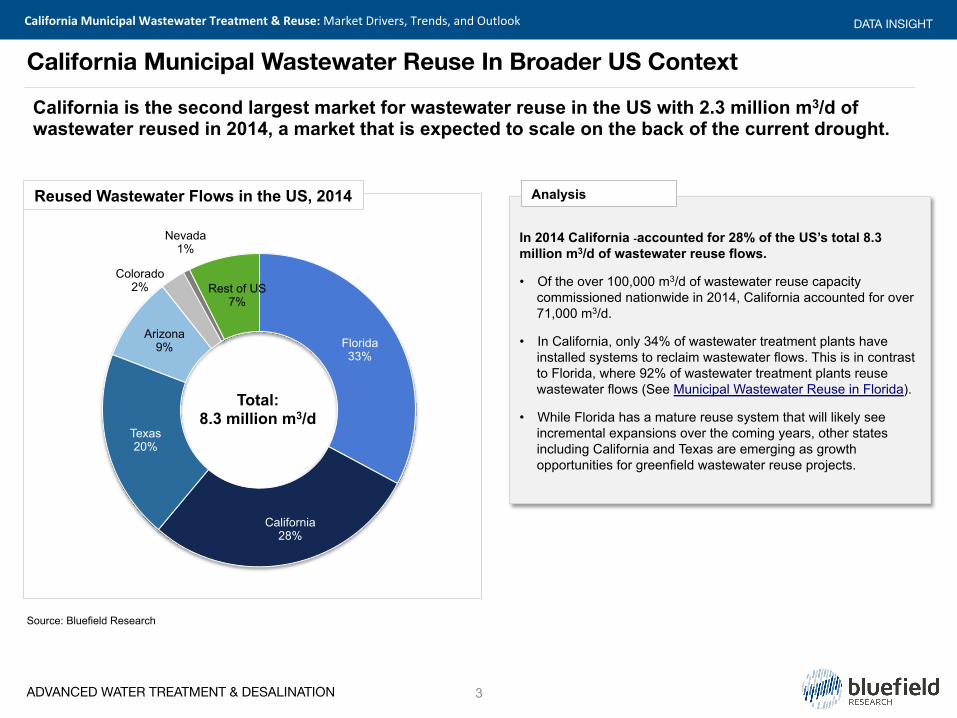

In 2014 California accounted for 28% of the US’s total 8.3 million m3/d of wastewater reuse flows.

• Of the over 100,000 m3/d of wastewater reuse capacity commissioned nationwide in 2014, California accounted for over 71,000 m3/d.

• In California, only 34% of wastewater treatment plants have installed systems to reclaim wastewater flows. This is in contrast to Florida, where 92% of wastewater treatment plants reuse wastewater flows (See Municipal Wastewater Reuse in Florida).

• While Florida has a mature reuse system that will likely see incremental expansions over the coming years, other states including California and Texas are emerging as growth opportunities for greenfield wastewater reuse projects.

Analysis

California Municipal Wastewater Reuse In Broader US Context

California is the second largest market for wastewater reuse in the US with 2.3 million m3/d of wastewater reused in 2014, a market that is expected to scale on the back of the current drought.

Florida 33%

California 28%

Texas 20%

Arizona 9%

Colorado 2%

Nevada 1%

Rest of US 7%

Total: 8.3 million m3/d

Reused Wastewater Flows in the US, 2014

Source: Bluefield Research

California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook

ADVANCED WATER TREATMENT & DESALINATION

DATA INSIGHT

4

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

m3 /d

of C

apac

ity

Conceptual

Feasability

Planned

Tendered

Design

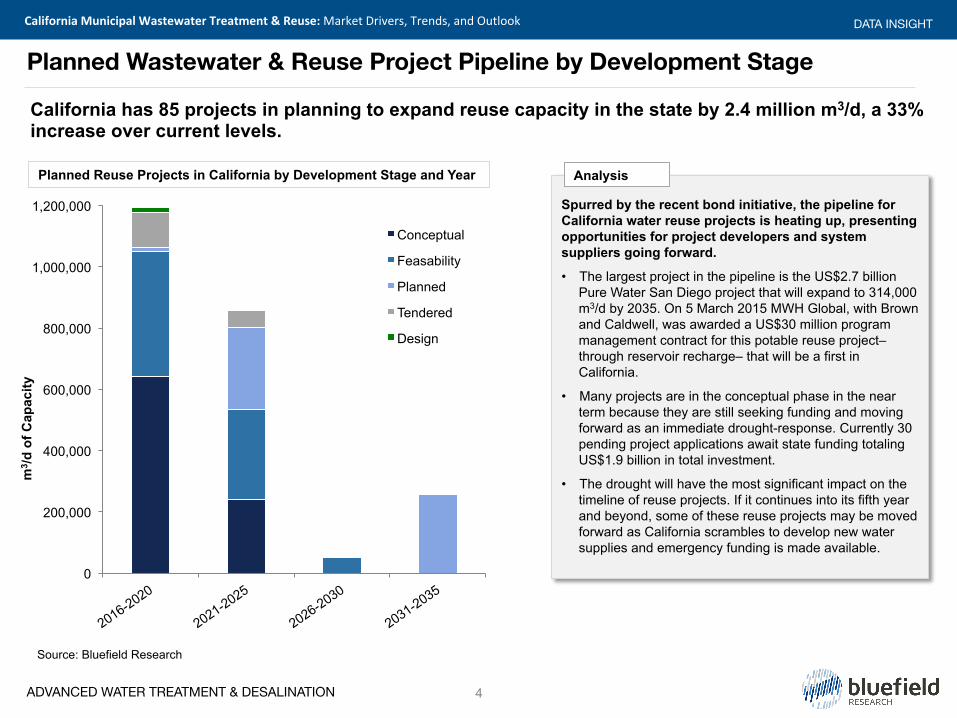

Spurred by the recent bond initiative, the pipeline for California water reuse projects is heating up, presenting opportunities for project developers and system suppliers going forward.

• The largest project in the pipeline is the US$2.7 billion Pure Water San Diego project that will expand to 314,000 m3/d by 2035. On 5 March 2015 MWH Global, with Brown and Caldwell, was awarded a US$30 million program management contract for this potable reuse project– through reservoir recharge– that will be a first in California.

• Many projects are in the conceptual phase in the near term because they are still seeking funding and moving forward as an immediate drought-response. Currently 30 pending project applications await state funding totaling US$1.9 billion in total investment.

• The drought will have the most significant impact on the timeline of reuse projects. If it continues into its fifth year and beyond, some of these reuse projects may be moved forward as California scrambles to develop new water supplies and emergency funding is made available.

Analysis Planned Reuse Projects in California by Development Stage and Year

Planned Wastewater & Reuse Project Pipeline by Development Stage

California has 85 projects in planning to expand reuse capacity in the state by 2.4 million m3/d, a 33% increase over current levels.

Source: Bluefield Research

California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook

ADVANCED WATER TREATMENT & DESALINATION

DATA INSIGHT

ADVANCED WATER TREATMENT & DESALINATION INSIGHT SERVICE

CLIENT FOCUS: This Insight Service is designed for companies involved in the supply, purchase or integration of water and wastewater treatment technologies, including:

• Municipal and water utilities tracking new players and technologies • Business development and strategy executives at manufacturers and

integrators of water and wastewater treatment systems, components • EPC and water project developers seeking new supply relationships or

strategic or vertical partnerships • Large industrial water users searching for optimal supply solutions • Investors targeting new business models in water treatment and re-use

RESEARCH COVERAGE: a 12-month cycle of data- and analytics-driven research provided in multiple formats to support client strategies, covering:

• Desalination market trends including new projects, emerging brackish water applications, and cost drivers

• Growth of water and wastewater treatment markets by segment (membrane, chemical, thermal, etc), by vertical market, and by region

• Water re-use strategies and market acceptance by sector • In-depth insight into industrial treatment markets including mining, oil &

gas, fracking, power, agriculture, and manufacturing • Technology trends in materials, processes, and energy efficiency • Supplier rankings and market share by segment and region • Supply chain shifts and tracking of new entrants

METRICS: primary research and analysis is supported by proprietary market, project and company databases updated continuously:

• WT, WWT and desalination project databases ( technology, supplier) • EPC and equipment supplier databases • Industrial segment project databases (mining, O&G, power, etc) • Rigorous market forecasts detailing models, assumptions, and detailed

scenarios

Insight Service Description

WATER SOLUTIONS COVERED:

Business Models

Cost Drivers

M&A Activity

Regulatory Activity

Market Share

MARKET SEGMENTS COVERED:

Industrial Water Municipal Water • Power Gen • Oil & Gas • Mining • Chemicals • Food & Beverage Water Reuse

Water Treatment

Wastewater Treatment Desalination

Agriculture

SELECT LIST OF COMPANIES COVERED:

5

California Municipal Wastewater Treatment & Reuse: Market Drivers, Trends, and Outlook

ADVANCED WATER TREATMENT & DESALINATION

DATA INSIGHT

© 2015 BLUEFIELD RESEARCH, LLC.

Global companies across the value chain are developing strategies to capitalize on greenfield opportunities in water -- new build, new business models, and private investment. Bluefield Research supports a growing roster of companies across key technology segments and industry verticals addressing risks and opportunities in the new water landscape. Companies are turning to Bluefield for in-depth, actionable intelligence into the water sector and the sector's impacts on key industries. The insights draw on primary research from the water, energy, power, mining, agriculture, financial sectors and their respective supply chains. Bluefield works with key decision-makers at utilities, project development companies, independent water and power providers, EPC companies, technology suppliers, manufacturers, and investment firms, giving them tools to define and execute strategies.

Contact Bluefield Research

NORTH AMERICA 34 Farnsworth St // Floor 3 Boston, MA 02210 T +1 617 963 5114 EUROPE C/de Santa Eulàlia 5-9 // 3a

08012 Barcelona Spain T +34 617 464 999 [email protected] www.bluefieldresearch.com

WWW.BLUEFIELDRESEARCH.COM GREENFIELD + WATER = BLUEFIELD 6