calibrating performance measures in the challenging

TRANSCRIPT

Calibrating Performance Measures in the Challenging Economic Environment

Stephen Charlebois

Mercer, Geneva +41 22 918 1027

Contents

The Paradigm Shift Selecting the Right Performance Measures Setting the Appropriate Performance Targets Validating Pay-for-Performance Outcomes Closing Remarks

The Paradigm Shift

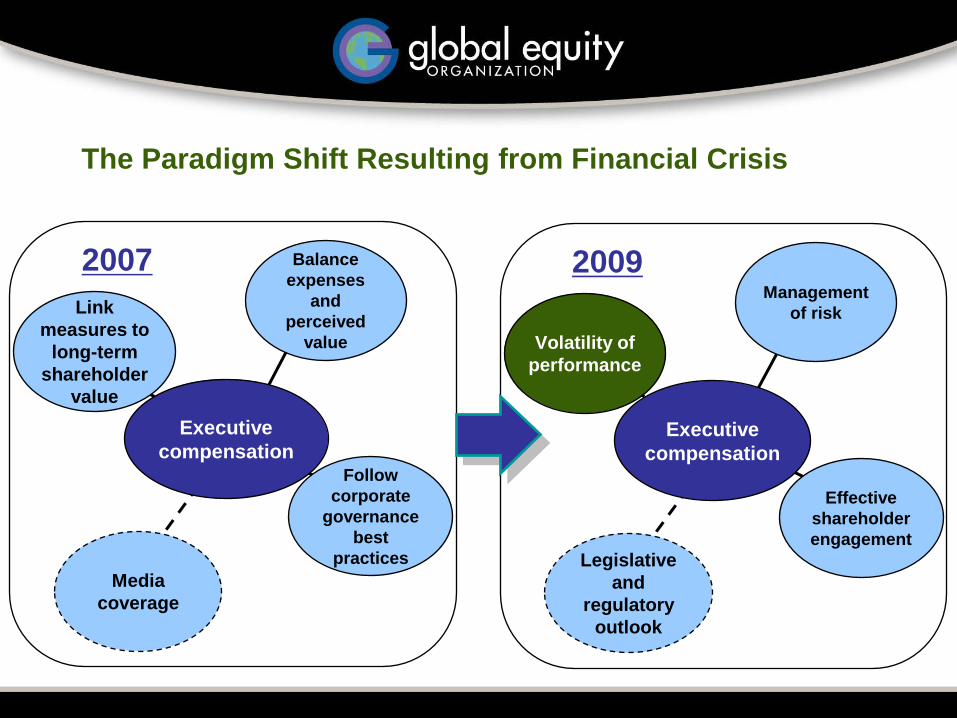

The Paradigm Shift Resulting from Financial Crisis

Follow corporate

governance best

practices

Balance expenses

and perceived

value

Executive compensation

Media coverage

Link measures to

long-term shareholder

value

2007

Effective shareholder engagement

Management of risk

Executive compensation

Legislative and

regulatory outlook

Volatility of performance

2009

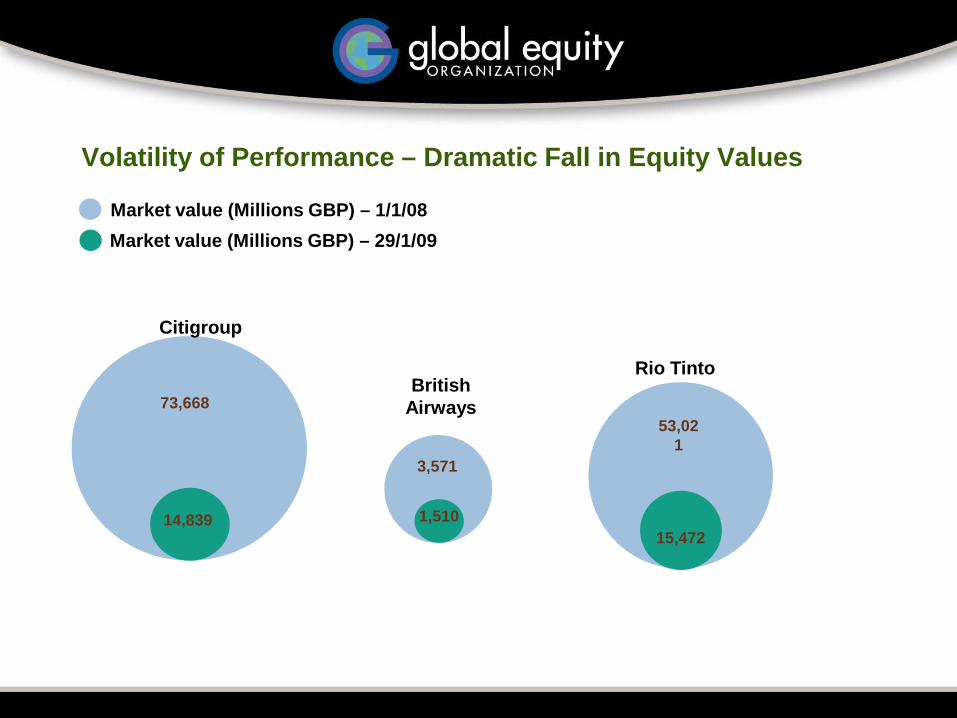

Volatility of Performance – Dramatic Fall in Equity Values

Market value (Millions GBP) – 1/1/08Market value (Millions GBP) – 29/1/09

73,668

Citigroup

British Airways

3,571

1,51014,839

53,021

15,472

Rio Tinto

Volatility of Performance – Impact of Economic Cycles

0

10

20

30

40

50

60

70

80

90

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Time

Econ

omic

Out

put

Economic Cycle Industry Cycle Company Cycle

Volatility of Performance – Impact of Industry Segment

Utilities

Pharmaceuticals

Oil & Gas(up-stream exploratory)

Financial Services

TelecomsConsumer Goods

Construction and real estate

Mining

Travel & Leisure

Retail &

Aerospace and Defence

Reward

Vola

tility

of P

erfo

rman

ce

Volatility of Performance – Impact of Industry Segment

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Y93 Y94 Y95 Y96 Y97 Y98 Y99 Y00 Y01 Y02 Y03 Y04 Y05 Y06 Y07 Y08

Year

3-Ye

ar S

ales

CA

GR

Source: S&P Research Insight, Mercer Analysis

LegendSample 75th %ileSample 50th %ileSample 25th %ileEnergy IndustryConsumer StaplesConsumer DiscretionaryHealth Care

Selecting the Right Performance Measures

Stakeholder Objectives of Performance Measurement

What Investors Want What the Board Wants What Management Wants

Strong line of sight to individual behaviour

Alignment with the business strategy and organizational culture (one size does not fit all)

Motivational goals that contain the right amount of stretch

Simplicity and ease of communication

Reasonable, defensible pay and performance outcomes

Flexibility to address both retention and measurement challenges as they rise

Clear and transparent disclosure of performance standards and compensation decisions

Direct linkage to shareholder value creation

Meaningful performance contingencies (no surprises) and fair calibration between results and payouts (no free rides)

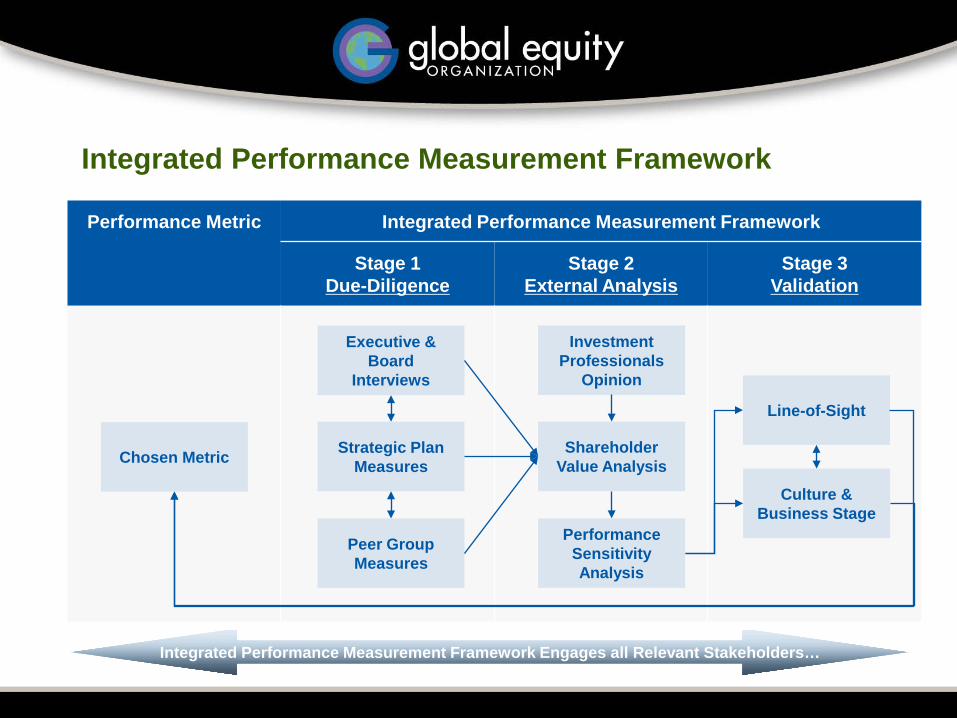

Integrated Performance Measurement Framework

Performance Metric Integrated Performance Measurement Framework

Stage 1Due-Diligence

Stage 2External Analysis

Stage 3Validation

Chosen Metric

Executive & Board

Interviews

Strategic Plan Measures

Peer Group Measures

Line-of-Sight

Culture & Business Stage

Investment Professionals

Opinion

Shareholder Value Analysis

Performance Sensitivity Analysis

Integrated Performance Measurement Framework Engages all Relevant Stakeholders…

Stage 1 – Due Diligence

Key questions in the current economic environment include: Executive and Board Interviews: Where is the industry moving?

How might your operating model change in the future? How is your financial strategy changing?

Strategic Plan Measures: What is your profit model and how do we create value today? How might that model change in the future? What key activities in your plan will make you successful?

Peer Group Measures: What measures have your industry and peer group historically used? How have those measure changed over time? Has there been a specific focus on particular measures during different point in economic cycle? How can these measures be adapted to your culture and reporting systems?

Stage 2 – External Analysis

Shareholder Value Analysis - Uses regression analyses to determine key financial measures that drive shareholder value over time

Performance Sensitivity Analysis – Identifies underlying sources of share price volatility by measuring volatility of stock price that is attributable to stock market, peer group and company-specific factors

Stage 2 – External Analysis – Sample PSA Analysis

LTI Cash PlanShare Options + Performance SharesShare Options

Potential Long Term

Incentive Mix

Company Specific Volatility High LowMedium

0%

20%

40%

60%

80%

100%

Perc

ent o

f Mon

thly

Var

ianc

e in

TSR

Exp

lain

ed b

y:

Market Volatility

Peer Volatility

Company Specific Volatility

Stage 3 - Validation

This stage is comprised of a more qualitative review to ensure the metrics chosen are appropriate, key questions include: Line-of-Sight: Does the metric align with organizational level? Is

the metric relevant for a profit centre vs. investment centre? Culture & Business Stage: How do we ensure people understand

the metric and reinforce it in managerial decisions? Does this metric incentivise the appropriate risk taking behaviour?

This is the time to step back and reflect on the appropriateness of the metric…

Annual Bonus Performance Measures – Emerging Trends

Using a basket of measures reduces the incidences of bonus payouts at the extremes - zero and maximum bonuses have become less likely

Increased use of non-financial performance measures, i.e. customer satisfaction, employee engagement, health & safety, strategic objectives, etc.

Make changes to performance metrics used to reflect the new priorities for companies most affected, i.e. increased focus on cashflow, costs, etc.

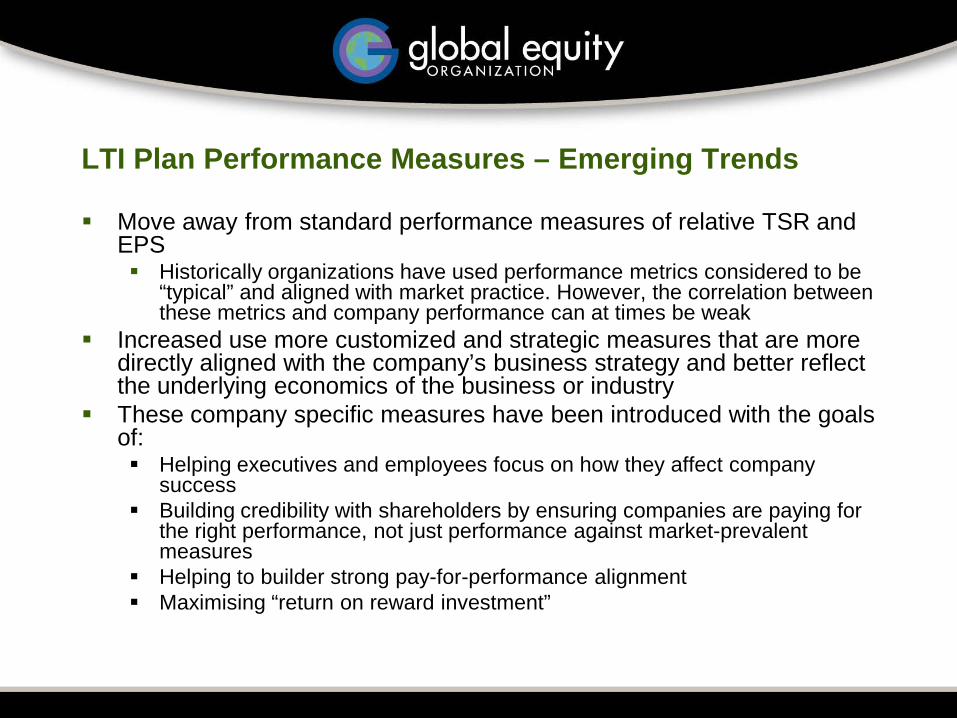

LTI Plan Performance Measures – Emerging Trends

Move away from standard performance measures of relative TSR and EPS Historically organizations have used performance metrics considered to be

“typical” and aligned with market practice. However, the correlation between these metrics and company performance can at times be weak

Increased use more customized and strategic measures that are more directly aligned with the company’s business strategy and better reflect the underlying economics of the business or industry

These company specific measures have been introduced with the goals of: Helping executives and employees focus on how they affect company

success Building credibility with shareholders by ensuring companies are paying for

the right performance, not just performance against market-prevalent measures

Helping to builder strong pay-for-performance alignment Maximising “return on reward investment”

Setting the Appropriate Performance Targets

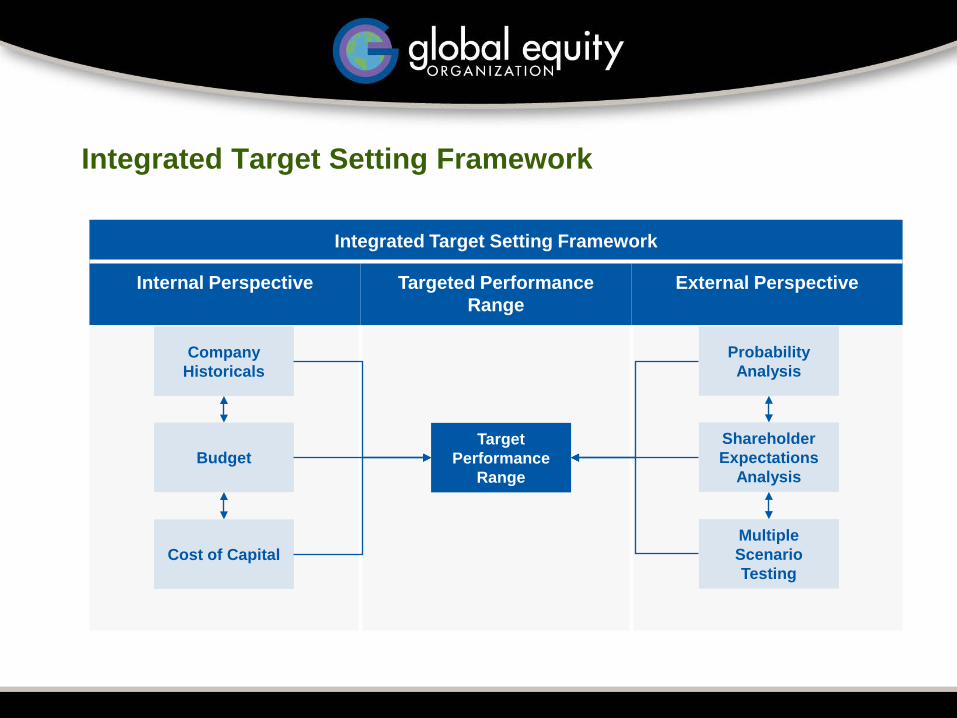

Integrated Target Setting Framework

Integrated Target Setting Framework

Internal Perspective Targeted Performance Range

External Perspective

Target Performance

Range

Probability Analysis

Shareholder Expectations

Analysis

Multiple Scenario Testing

Company Historicals

Budget

Cost of Capital

Target Setting - Internal Perspective

Companies that set performance targets by the internal approach alone usually place great stock in their ability to measure and analyze historical performance and use it as the principal basis for planning and predicting future performance

The internal perspective is generally a good starting point, however, solely relying on internal perspectives may lead to: Built-in, budgeted incentive payments even in a downturn Expected level of performance may not be achieved given general

or industry market opportunities Internally driven process can sometimes fail to incorporate

shareholder expectations, leading to goals that are not meaningful from a shareholder value creation perspective

Target Setting – External Perspective

The external perspective is generally used to complement the internal budgeting process and to re-confirm the assumptions made are correct and reflect economic, industry and company life-cycles. Typical analysis includes: Industry Analysts Expectations to directionally assess the

difficulty of a target. Macroeconomic Indicators to gauge the direction of demand for

products or growth in specific regions or industries. Shareholder Expectation Analysis for growth and option on the

company strategy and competitive positioning. Probability Analysis to test the relative difficulty of achieving a

certain level of performance. Scenario Testing to fully understand the potential implications of

“extreme” outcomes.

Target Setting – Emerging Trends

Increased use of forward looking scenario testing to determine the behaviour of the selected performance measures under different performance scenarios

Setting targets relative to external economic and market indices Review of typical 3-year performance periods

Some companies have moved to annual performance measurement, i.e. 3-year plan with 3 annual periods due to difficulty in setting 3-year targets in current economic environment

Calibrating Pay for Performance Outcomes

Calibrating Pay-for-Performance Outcomes

Calibrating incentive awards to performance results ensures that threshold, target and maximum payout opportunities are appropriate for commensurate performance results

2. Kinked (emphasis on target-max)

Steep slope above target

PerformancePerformance

Threshold

Target

Max

Rew

ard

Size

Threshold

Target

Max

Rew

ard

Size

1. Linear(equal emphasis on threshold-

max)

Executives receive a small bonus when performance is below target, with payments increasing in exact proportion as performance improves

The payout threshold is lower than under linear payout curve, but payments increase at a faster rate as performance exceeds the target

Review of Payout Curves – Emerging Trends

Flatter pay for performance correlation, less upside but lower targets for threshold performance

Increased use of an S-shaped payout curve: Provides reduced incentive for falling near the plan threshold and

maximum Motivates executives to reach target, but does not encourage them

to “shoot the lights out”

Closing RemarksStrategic Alignment

Right Performance Focus Do we have the right

measures? Are they consistent with our

strategic priorities? Do we have appropriate line of

sight?

Compensation Policy

How Much to Pay Pay Positioning

How to Pay Pay mix Leverage Vehicles Eligibility

For What to Pay Measures Targets Linkage Time-horizon

Right Behavior Are our performance goals

difficult enough? Does the compensation

program incent the appropriate risk- taking behavior?

Your Questions…