by daniel l. edelstein

TRANSCRIPT

Copper—2004 21.1

Copper

ByDanielL.edelstein

Domestic survey data and tables were prepared by Hema Edupuganti, Michael V. Leahy, and Wanda G. Wooten, statistical assistants, and the world production tables were prepared by Regina R. Coleman and Glenn J. Wallace, international data coordinators.

In2004,mineproductionofrecoverablecopperintheUnitedStatesrosebyabout40,000metrictons(t)(4%)to1.16millionmetrictons(Mt),thehighestlevelsince2001.Aglobalshortfallinproductionthatbeganin2003andgainedmomentumin2004,ledtoasharpdeclineinglobalrefinedcopperinventoriesandariseincopperprices.Higherpricesandprojectionsofasustainedshortfallinproductionencouragedtherestartofidlecapacityatseveraloperatingminesinthelatterpartoftheyearandrestart,undernewownership,ofamineidledsince1999.

Downstreamsmelterandrefineryproductionwereessentiallyunchangedfromthatof2003,inpartowingtoincreasedexportsofconcentratesandanodecopper.electrowonproductionfromtheleachingofcopperores,whichdeclinedbyabout7,000t,accountedfor50%ofmineoutputand47%ofprimaryrefinedcopperproduction.reporteddomesticconsumptionofrefinedcopperin2004rosebyabout5%to2.41Mtandwasatitshighestlevelsince2001.Chinawastheworld’sleadingconsumerofrefinedcopperwithanestimated20%marketshare.

Globalmineproductionofcopper,whichhadbeenessentiallystagnantduringthepreceding2years,rosebyabout6%toarecord-high14.6Mtin2004.TheUnitedStatesaccountedforabout8%ofworldproductionandretaineditspositionastheworld’ssecondleadingmineproducer.Chile,wheremineproductionrosebyabout10%toarecord-high5.4Mt,remainedtheleadingmineproducerandaccountedformorethan37%oftotalworldproduction.Globalsmelterandrefineryproductionrosebyonlyabout3%and4%,respectively.TheUnitedStatesfelltosixthplacebehindpolandinworldsmelterproductionandremainedfourthinrefineryoutputbehindChile,China,andJapan.

U.S.GeologicalSurveyestimatesindicatedworldcopperreservesof470Mtandacopperreservebaseof940Mt.TheUnitedStateshadabout7%eachoftheworld’scopperreservesandreservebase.

TheprincipalminingStates,indescendingorderofproduction,Arizona,Utah,NewMexico,andMontana,accountedfor99%ofdomesticproduction;copperwasalsorecoveredatminesinIdaho,Missouri,andNevada.Althoughcopperwasrecoveredat22minesthatoperatedintheUnitedStates,just14minesaccountedformorethan99%ofproduction.Theremaining8mineswereeithersmallleachoperationsorbyproductproducersofcopper.

Duringtheyear,3primarysmelters,4electrolyticand3firerefineries,and12solventextraction-electrowinning(SX-eW)facilitiesoperatedintheUnitedStates.Thethreefirerefineriesprocessedscraptorecoverunalloyedcopperproducts;oneoftherefineriesoperatedonlyduringthefourthquarter.Scrapwasalsoconsumedinrelativelysmallquantitiesatseveraloftheprimarysmelters.

U.S.smelterandrefinerycapacityremainedessentiallyunchangedatabout900,000t,and2.25Mt,respectively,andcapacityutilizationratesremainedunchangedat60%and58%,respectively.In2004,copperrecoveredfromrefinedorremeltedscrap(about80%fromnewscrapand20%fromoldscrap)composed29%ofthetotalU.S.coppersupply.Theconversionofoldscraptoalloysandrefinedcopperdeclinedbyabout8%to191,000tofrecoverablecopperandwasataboutthesamelevelasin2003.Copperrecoveredfromnewscrap(774,000t)rosebyabout5%,andtoalargeextentwasareflectionofincreasedmanufacturinglevels.

Copperwasconsumedasrefinedcopperandasdirect-meltscrapatabout30brassmills,13wire-rodmills,and500chemicalplants,foundries,andmiscellaneousoperations.owingtosustainedlow-capacityutilizationatU.S.refineries,thenetimportrelianceforrefinedcopperasapercentageofapparentconsumptionincreasedforthethirdconsecutiveyeartoarecord-high43%.Chile,Canada,andperu,indescendingorder,accountedfor92%ofthe807,000tofrefinedcopperimportedforconsumption.Inadditiontoimports,domesticinventories,whichdeclinedby522,000t,providedsignificantsuppliestothedomesticindustry.

Legislation and Government Programs

In2003,theU.S.environmentalprotectionAgency(epA),aspartofitsreviewofexistingdrinkingwaterstandardsfor69substances(includingleadandcopper)forwhichNationalprimaryDrinkingWaterregulations(NpDWrs)wereestablishedpriorto1997,affirmeditsconclusionthattheestablishedmaximumcontaminantlevelgoal(MCLG)forcopperof1.3milligramsperlitershouldberetainedpendingcollectionofadditionaldataonhealthrisks.TheepAfurtherconcludedthatutilitieshadsufficientflexibilityundertheexistingleadcopperrule(LCr)toadoptnewcontrolstrategies.TheepArecognized,however,thattheexistingLCrmaylimittheabilitytoadoptneworemergingtechnologiesandstatedthatitwouldcontinuetomonitornewdevelopmentsandmayconsiderrevisionsattheendofthenext6-yearreviewcycle(U.S.environmentalprotectionAgency,2003).In2004,theepAheldaseriesofworkshopstodiscussissuesassociatedwithcompanyimplementationoftheLCr,includingworkshopsonLCrMonitoringprotocols,simultaneouscompliancewiththeLCrandNpDWrs,andpubliceducationrequirements(U.S.environmentalprotectionAgency,2004a,b).

onApril7,theBureauofIndustryandSecurity(BIS),U.S.DepartmentofCommerce,receivedajointpetitionfromtheCopperandBrassFabricatorsCouncil,Inc.andtheNonferrousFounders’Societythatrequestedtheimposition

21.2 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

ofexportmonitoringandexportcontrolsoncopperscrapandcopper-alloyscrapandthatrequestedapublichearingontheissue.ThepetitionwasfiledunderprovisionsoftheexportAdministrationActof1979,asamended,thatallowedforanindustry,orasegmentthereof,thatprocessesmetallicmaterialscapableofbeingrecycledtofilesuchapetition(U.S.DepartmentofCommerce,2004).Intheirpetition,thecopperandbrassindustrycontendedthattherapidriseofscrapexportstoChinahadcreatedashortsupplyofscrapmaterialsfordomesticconsumersandhadcontributedtohigherpricesforavailablesupplies.Thepetitionersarguedthatnotallsectorsoftheirindustrywereabletosubstitutecoppercathodeforscrapasafeedmaterial,andwherepossible,suchsubstitutionimposedeconomicpenaltyowingtothehighercostofcathode.Thepetitionersfurtherclaimedthathigherrawmaterialcostscouldnotbepassedthroughtoconsumers,andthatscarcitylimitedtheirproductionandharmedtheircompetitiveposition.Accordingtothepetition,totalscrapexportsfrom1999to2003roseby138%,andexportstoChina,whichroseby515%duringthesameperiod,accountedforessentiallyalloftheincrease.Thepetitionersrequestedthatexportquotasforcopperandcopper-alloyscrapbesetatthemeanvolumeofexportsfortheperiod1996-2000,380,000t,whichwasabout50%ofthe2003level(U.S.DepartmentofCommerce,2004b§1).

InJuly,BISissueditsrulingonthepetitioninwhichitdeterminedthattheshortsupplycriteriahadnotbeenmet,andthatneithermonitoringnorcontrolswerewarranted.Initsdetermination,Commerceconcludedthat:

• Thoughthevolumeofexportsofcopper-basescrapincreasedsignificantlyduringthestudyperiod,theincreasewassomewhatlesssignificantwhenconsideredinrelationtodomesticdemandandtheerosionofthesecondarysmeltingindustry.

• Copperscrappricesdidincreasesignificantly,buttheworldmarketforcoppercathode,notthelevelofU.S.exportsofcopper-basescrap,wasthemostimportantdeterminantinthefluctuationsofdomesticscrapprices.

• Theevidencedidnotdemonstratetheexistenceofascrapshortage,nordiditdemonstrateasignificantadverseeffectonthenationaleconomyorsectorthereof.TheCommerceDepartmentindicated,however,thatitwouldworktorefinescheduleBclassificationsforcopper-basescrapexportsinordertobetterdelineatethevarietiesofscrapbeingexported;reviewthenewscrapexportdatainthecomingyear;andworkcloselywiththeofficeoftheUnitedStatesTraderepresentativetoaddressanyforeigngovernmentpracticesthatmaybedistortingtradeincopper-basescrap(U.S.DepartmentofCommerce,2004a§).NewscheduleBclassificationsweresubsequentlyimplementedfor2005.

Production

In2004,inresponsetoaprojectedsustainedshiftintheglobalsupplybalance(fromoneofoversupplyofrefinedcoppertoaproductiondeficit)andtheprecipitousriseincopperprices

1References that include a section mark (§) are found in the Internet References Cited section.

atyearend2003,the7-yeardownwardtrendindomesticmineproductionwasreversed,andmineproductionrosebyabout4%.AttheendofJanuary,inresponseto“highercopperpricesandindicationsthattheimprovedmarketforcopperissustainable,”phelpsDodgeCorp.announcedplansforincreasingproductionatseveralNorthandSouthAmericanoperations.phelpsDodgechosespecificoperationsforincreaseinparttomaintainabalancebetweenitsmininganditsdownstreamprocessingfacilities(phelpsDodgeCorp.,2004).

Smelterandrefineryproductionwereessentiallyunchangedin2004.Threeprimarysmeltersandfourprimaryelectrolyticrefineriesoperatedduring2004.TheChinosmelterinNewMexicoandtheMiamielectrolyticrefineryinArizonathatclosedin2002wereretainedoncare-and-maintenancestatus.Duringthefourthquarter,thesecondarysmeltingandrefiningindustry,whichhadenduredacontinualdeclineinrecentyears,receivedaboostwhenAmericanIron&MetalCo.Inc.(Montreal,Quebec,Canada)restarteditsWarrenton,Mo,firerefinery,theonlyremainingnonintegratedsecondarycopperrefineryintheUnitedStates.AmericanIron&MetalacquiredWarrentonfromphilipServicesCorp.,ofHouston,TX,in2000andoperatedtherefineryintermittentlyuntilyearend2002.operatingasthenewlyformedWarrentonCopperLLC,theplanthopedtofilladomesticnicheasa“stableconsumercapableofconsuminglargeamountsofNo.2copper(scrap).”Thefacilityincludedwire-choppinglines,andplanscalledforaddingapreshredderandgranulator(McCann,2004§).

Company Reviews.—ASArCoIncorporated[ownedbyGrupoMéxico,S.A.deC.v.throughitssubsidiary,AmericasMiningCorp.(AMC)]begananacceleratedwasterockremovalprograminAprilatitsMissionandrayMinesinArizona.Asaresult,wasteremovalin2004increasedbyabout65%comparedwiththatin2003.AccordingtoAsarco,theprogrambegantobearfruitinthethirdquarter,withtotalcompanyproductionrisingto36,200t,anincreaseof30.2%comparedwithproductionduringthesecondquarter.GrupoMéxicoprojectedasignificantmineturnaroundbymid-2005thatcouldboostAsarco’stotalmineproductioncapacityto220,000metrictonsperyear(t/yr)ofcopper.productionfromU.S.operationsinArizonatotaled141,000t;theMissionMineproduced22,200tofcopperinconcentrate;therayMineproduced65,600tinconcentrateand34,000tofelectrowoncopper;andtheSilverBellMineproduced19,500tofelectrowoncopper.Asarcoexpectedthatareturntoapositivenetincomein2005wouldallowforinvestmentinprocessimprovementsandenvironmentalremediation(GrupoMéxico,S.A.deC.v.,2005,p.11-15;plattsMetalsWeek,2005).

CopperproductionfromBHpBilliton’sresidualArizonaleachoperationsatMiamiandpintovalleytotaled9,500tin2004,downfrom10,200tin2003(BHpBilliton,2005,p.10).BasedonanagreementsignedwithBHpin2001,rioTintoplcearneda55%controllinginterestintheresolutionCopperCompanybyinvesting$25millionindrilling,exploration,andremediation(BHpretaineda45%interest).resolutionwasformedbyrioTintotoevaluatealargecoppersulfidedepositlocatedabout2,000meters(m)belowthesurfacebeneathBHp’sshutteredMagmaMineinthepioneerminingdistricteastofSuperior,AZ.Bymidyear,drillinghadachievedat

Copper—2004 21.3

least5interceptswiththeorebody,oneofwhichwasreportedtoextendforabout300mandgrading1.9%copper.Ifminedevelopmentwastoproceed,thenrioTintodidnotanticipateproductionpriorto2014(Dillard,2004).

ConstellationCopperCorp.announcedinJunethatitsboardofdirectorshadapproveda$40milliondebtfinancingpackagefortheconstructionoftheLisbonvalleyopenpitandheap-leachSX-eWprojectinUtah(ConstellationCopperCorp.,2004a).InSeptember,ConstellationreportedthatdismantlingofthecrushingandSX-eWprocessingfacilitiesthatitpurchasedfromequitorialTonopahInc.’sclosedTonapah,Nv,minewascomplete,andthattheplantequipmenthadbeenrelocatedtotheLisbonvalleysite.InNovember,ConstellationannouncedthatithadbegunreconstructionofthecrushingandSX-eWprocessingfacilities.TheLisbonvalleyprojectwasdesignedtoproduce24,500t/yrofcoppercathodeataprojectedaveragecashoperatingcostof$0.47perpound(excludingminingfleetcosts).Theprojectedtotalcostof$0.72perpoundincludedalllife-of-minecapital,reclamation,andclosurecosts(ConstellationCopperCorp.,2004b,c).

InNevada,GoldSpring,Inc.reportedearlyintheyearthatitwasproceedingwithitsBigMikeproject,nearWinnamucca.Theprojectcalledforusingthecompany’seco-vatleachingsystemtoprocessabout1.1Mtofstockpiledoreduringa5-to6-yearperiodtorecoverabout11,300tofelectrowoncopper(GoldSpring,Inc.,2004§).Byyearend,however,nofurtherdevelopmenthadbeenannounced.

NordresourcesCorp.announcedthatithadissuedtender/contractdocumentstofourminingcontractorsforminingatthecompany’sJohnsonCampMinelocatedinSouthernArizona.operationsatJohnsonCampwouldinvolveremovalof4,500metrictonsperday(t/d)ofoverburdenandminingabout8,000t/doforetoproduceanominal9,000t/yrofelectrowoncathode.Actualproductionofcoppercathodewasanticipatedtobeginwithin3monthsofarestart(NordresourcesCorp.,2004).

In2004,phelpsDodgereportedcopperproductionof1.20Mt,whichincludedminorityparticipants’shareof204,000t,fromitsworldwideoperations,comparedwith1.18Mtand223,000t,respectively,in2003.U.S.productionin2004was683,000tofcopper(515,000telectrowonand168,000tinconcentrate),anincreaseof31,000tfromthatproducedin2003(phelpsDodgeCorp.,2005,p.8).

productionof381,000tofelectrowoncopperattheMorenciMinecomplexinArizonawasessentiallyunchangedfromthatofthepreviousyear.Thecomplexcomprisedanopenpit,aconcentrator,foursolventextraction(SX)facilities,andthreeelectrowinningtankhouses.WhiletheMorenciconcentratorremainedoncareandmaintenance,theMetcalfcrushingfacilityprocessedabout77,000t/dofore(phelpsDodgeCorp.,2005,p.8).

productionattheBagdadMineinArizonarosenominallyto99,900tofcopper(74,500tinnetconcentrateproductionand25,400telectrowon).ThoughphelpsDodgebeganincreasingmillthroughputandreportedthemilloperatingatfullcapacitybytheendofthesecondquarter,netproductionofcopperinconcentratewasessentiallyunchangedowingtolowermillheadgrade(0.41%copperdownfrom0.43%in2003)andtheprocessingof52,600tofconcentratethroughademonstrationleachplant(commissionedin2003)toproduce15,800tof

electrowoncathode.In2003,thedemonstrationleachplantprocessed40,000tofconcentrateandproduced11,000tofelectrowoncopper.In2002,priortostartingtheconcentrateleachplant,conventionalleachproductionwasonly14,000tfromresidualleachingoforepiles.Between1999,theyearphelpsDodgeacquiredtheproperty,andyearend2003,lessthan1Mtofleachorehadbeenaddedtothestockpiles.In2004,morethan21Mtoforegradinganaverage0.9%copperwasaddedtotheleachstockpile(phelpsDodgeCorp.,2005,p.3-8).

AttheSierritaMineinArizona,copperinconcentrateproductionroseto66,700tfrom60,100tin2003followingrampuptofullcapacityduringthefourthquarter.electrowonproductionplummetedto3,600tfrom8,400tduring2003,astheplantwasshutteredformostoftheyear.Thoughitwasrenewedduringtheyear,productionhadbeeninterruptedbyexpirationofalandleaseforthepropertyuponwhichtheelectrowinning(eW)tankhousewaslocated.phelpsDodgealsocompletedconstructionofan18,000t/yrcoppersulfateplantatSierritatosupplementcapacityatitsplantinelpaso,TX(phelpsDodgeCorp.,2005,p.3-8).

AttheChinoMineinNewMexico,miningandmillingofsulfideore,whichhadbeencurtailedsinceMarch2001,resumedduringthesecondquarteroftheyear,andbytheendofthethirdquarterthemillreportedlywasoperatingatabout80%capacity.Copperinconcentrateproductionwas27,000tfortheyear,aboutone-thirdofthelevelin2000.productionofleachore,whichhadbeennegligiblein2002,resumedduringSeptember2003,androsetothepre-curtailmentlevelof28millionmetrictonsperyear(Mt/yr)during2004.electrowonproductionin2004roseto56,000t,thehighestlevelsince1998,from36,000tin2003(phelpsDodgeCorp.,2005,p.10).TheCobreMineinNewMexicoproducednocopperin2004despitetheannouncedintentiontoreopentheminethathadbeenshutteredsince1999,thoughlimitedminerehabilitationactivitiestookplace.AttheTyroneMine,alsoinNewMexico,productionofelectrowoncopperdecreasedto39,000tfrom52,000tin2003followingpartialcurtailmentofproductioninSeptember2003.In2004,16.5Mtoforewasplacedinleachstockpiles,mostofwhichwaspreviouslyminedmaterialthathadbeenconsideredwastematerial(phelpsDodgeCorp.,2005,p.3-10).

AtMiami,AZ,phelpsDodges’selectrolyticrefineryremainedshuttered,whileelectrowonproductiondecreasedto8,900tofcopperfrom16,100tin2003.Miningofleachmaterial,whichlasttookplacein2001,remainedsuspended.Smelterproductionroseto195,000tofanodefrom182,000tin2003,andthefacilitywasreportedlyoperatingatfullcapacityduringthefourthquarter.productionofrefinedcopperatitselpaso,TX,refineryroseto280,000t,yetremainedwellbelowcapacityofabout400,000t(phelpsDodgeCorp.,2005,p.3-10).

QuadraMiningLtd.(vancouver,BritishColumbia,Canada)announcedthattheconcentratoratitsrobinsonMinenearely,Nv,hadbegunprocessingoreonSeptember1,andbytheendofthefirstweekinSeptemberitwasoperatingatabout60%ofitsdesigncapacityof38,000t/dofore.Themineoperatingcompany,robinsonNevadaMiningCompany(awhollyownedsubsidiaryofQuadra),contractedwithWashingtonGroupInternationaltomineapproximately67Mt/yroforeandwaste

21.4 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

atrobinsonduringa5-yearperiod.oreandwasteremovalwasexpectedtorampupfrom80,000t/dto200,000t/dbyJanuary2005.QuadrapurchasedrobinsonfromBHpinApril2004for$18million(QuadraMiningLtd.,2004b).BHp,whichbuiltanewmilltoprocessorefrompitsfirstdevelopedbywhatisnowkennecottUtahCopperCorp.,operatedtherobinsonMinefrom1996-99.UpdatedreserveestimatesandmineplanspublishedbyQuadrainAugust2004indicatedcopperreservesatitsfourpitsof133Mtoforegrading0.69%copperand0.285gramspermetrictonofgoldandcontaining747,000tofrecoverablecopperand18,700kilogramsofrecoverablegoldatrecoveryratesof82%and49.3%,respectively.Theoverallminelifewasprojectedtobe10yearsatanaverageproductionrateof75,000t/yrofcopperand1,170kilogramsperyearofgold,andhaveanaveragelife-of-the-minecashcostof$0.80perpoundofcopper.Concentrateswereexpectedtobesoldoffshore(QuadraMiningLtd.,2004a).

AtrioTinto’sBinghamCanyonMineinUtah,productionofcopperinconcentratedecreasedto264,000tfrom282,000tin2003owingtolowermillthroughputandloweraveragemill-headgrades(0.63%copper).Despitea2-weeksmeltershutdownformaintenanceduringthefourthquarter,productionofrefinedcopperroseto247,000tfrom231,000tin2003,yetremainedwellbelowcapacityofabout300,000t/yr.earlyin2005,parentcompanyrioTintoapprovedtheeast1pushbackproject,budgetedtocost$170million,toenlargetheBinghamCanyonopenpitandextendthelifeofthepituntil2017.previousplanshadcalledforexhaustionofopenpitreservesanddevelopmentofanundergroundmineby2013(rioTintoplc,2005a,p.17;2005b,p.48).

Inoctober,SouthernperuCopperCorp.(SpCC)announcedthatithadexecutedamergeragreementwithAMC,thenetresultofwhichwasthatGrupoMéxico,throughAMC,wouldincreaseitsownershipinSpCCtoroughly75.1%.previously,AMCowned54.2%ofSpCCwiththebalanceheldbyCerroTradingCompany(14.2%),phelpsDodgeCorp.(14.0%),andothercommonshareholders(17.6%).AccordingtoGrupoMéxico,afterthemergerithadthesecondlargestcopperreservesofanycompanyintheworldandthelargestreservesofanypubliclytradedcompany(GrupoMéxico,S.A.deC.v.,2004,p.2;SouthernperuCopperCorp.,2004).InadditiontoitsU.S.operations,GrupoMéxicooperatedtheCananeaandLaCaridadMinesinMexico,andSpCCoperatedtheToquepalaandCuajoneMinesinperu,thefourmineshavingacombinedcapacityofmorethan750,000t/yrofcopperinconcentrateandelectrowoncopper.

Consumption

reporteddomesticconsumptionofrefinedcopperin2004reversedits2-yeardownwardtrend,risingbymorethan5%tothehighestlevelin3years.Buoyedbycontinuedstronghousingconstruction,consumptionofrefinedcopperinthefirstquarterof2004rose6%aboveconsumptioninthepreviousquarterandwasupbymorethan8%comparedwithconsumptionduringthefirstquarterof2003.Wire-rodmillsaccountedformostoftheincrease,withconsumptionrisingbymorethan7%comparedwiththatofthepreviousquarter

andmorethan10%comparedwiththatofthefirstquarterof2003.AccordingtodatacompiledbytheAmericanBureauofMetalStatistics,Inc.(ABMS)(2004),U.S.shipmentsofwirerodinMarch2004were24%higherthaninMarch2003,andfirstquarter2004shipments,whichwereatthehighestlevelsincethefirstquarterof2001,were13%aboveshipmentsinthefirstquarterof2003.ApparentconsumptionofwirerodintheUnitedStates,whichincludednetimports,was15%higherthanthatforthefirstquarterof2003.Inventoriesofwirerodatproducerswereatthelowestlevelsinceatleast1996,providingfurtherevidenceofrecoveryindemand.

reportedconsumptioninthesecondandthirdquarters,thoughdownnominallyfromthatinthefirstquarter,remainedabout9%abovethatfortheequivalentperiodsof2003.BySeptember,however,themarketsshowedsignsofweakening,andduringthefourthquarter,reportedconsumptionofrefinedcopperdecreasedby10%fromthatofthethirdquarterandwas5%belowtherelativelystrongfourthquarterof2003.AccordingtoABMS(2005b)data,domesticwirerodshipmentsfor2004totaled1.79Mt,andwereupbyalmost9%fromthatofthepreviousyear.Apparentconsumptionofwirerodwasupbyabout7%.Similarly,ABMS(2005a)dataon2004brassmillproductsshipmentsbydomesticproducerswereupby7.3%comparedwith2003shipments,despitea12.3%dropduringthefourthquarterof2004(3.3%fourthquarteryear-on-yeardrop).Allcopperandcopperalloyproductsectorsrosein2004—plate,stripandsheet(11.9%);rodandbar(7.7%);andtube(3.4%).

AccordingtopreliminarydatafromtheCopperDevelopmentAssociation,Inc.(2005,p.18-20),thetotalsupplyofcopperandcopper-alloyproductstotheU.S.marketbyfabricators(brassmills,wiremills,foundries,andpowderproducers),whichincludednetimports,reverseda2-yeardeclineandroseby5.1%in2004toaboutthesamelevelasin2001.Brassmillproductsaccountedforabout49%oftotalshipmentstothedomesticmarket;wiremillproducts,49%;andfoundryandpowderproducts,2%.Inbuildingconstruction,whichwasthelargestendusesector,shipmentsroseby5.4%andaccountedforabout49%ofthemarket.Buildingconstructionincludedproductsusedforairconditioning,architecturalapplications,builder’shardware,buildingwire,commercialrefrigeration,andplumbingandheating.Shipmentsforelectric/electronicproducts(21%marketshare),transportationequipment(11%share),andconsumerandgeneralproducts(11%share)increasedby3%,12%,and8%,respectively.Shipmentsforindustrialmachineryandequipment(9%share)declinedbyabout2%.

Prices and Stocks

Thecopperpricerallyatyearend2003,thatwasencouragedbyaproductiondeficit,stockdrawdowns,andannouncementsofpotentialsupplydisruptions,continuedalmostuninterruptedthroughthefirstquarterof2004.TheCoMeX(theCoMeXDiv.oftheNewyorkMercantileexchange)pricereachedapeakof$1.38onMarch19,andaveraged$1.34forthemonth,thehighestmonthlyaveragesinceNovember1995.ThoughtheplattsMetalsWeekaverageproducerpricepremiumremainedunchangedintheJanuarytoMarchperiodat4.2centsperpound

Copper—2004 21.5

overCoMeX,theNewyorkdealerpremiumrosefrom4.2centsperpoundinJanuary,to4.8centsinFebruary,to5.5centsinMarch,andwasindicativeoftighteningcoppersupplies.

Thoughcopperpricesmoderatedduringthesecondquarter(theCoMeXpriceaveragedonly$1.21inJune),themarketwasvolatileandwassensitivetoindustryannouncements,includinganannouncementthatFreeportMcMoranCopperandGoldInc.’sGrasbergoperationinIndonesiahadrestartedmininginthehigh-graderegionofitspit(aseriesofslopefailureshadalteredmineplansandreducedproductionprojections)andreportsofpanicsellinginChina.ConcernoverapossibleslowdowninChina’seconomicgrowthsentpricesplungingonApril28to$1.18(Francis-Grey,2004§).Similarly,initiallaborconcernsatthe470,000-t/yrCollahuasiMineinChileandatAsarco’sminesinArizona,andtheirresolutionwithoutproductiondisruption,ledtopricevolatilityinJune(plattsMetalsWeek,2004a).

pricevolatilitywascloselytiedtothetighteningglobalsupplyofcopper.Globalcommodityexchangeinventories(CoMeX,LondonMetalexchangeLtd.,andShanghaiFuturesexchange)haddeclinedto806,000tatyearend2003from1.29Mtatyearend2002.exchangestockscontinuedtheirdownwardtrendduringthefirst6monthsof2004,andbytheendofJunehaddecreasedto242,000t.TheUnitedStatesaccountedformostofthedecline,withU.S.locatedexchangeinventoriesdecliningto152,000tattheendofJune,downfrom590,000tatyearend2003.

FollowingadipinAugust,atraditionalperiodoflightsummerdemand,tighteningsupply,laborunrest,andconcernoverotherproductiondisruptionsledtoanearsteadyriseinpricesduringtheremainderoftheyear.TheCoMeXpricepeakedat$1.54perpoundonDecember28andclosedtheyearat$1.49perpound.InDecember,theplattsMetalsWeekaverageNewyorkdealerpremiumforcathoderoseto5.5centsperpoundovertheCoMeXspotpriceandtheproducerpremiumrosetoabout5.3centsperpound.Thiscomparedwith3.0centsperpoundand4.2centsperpound,respectively,inDecember2003.kennecottUtahCopperindicatedthatpremiumswerelikelytocontinuetorisewhenitannouncedthatitsfirstquarter2005premiumforcathodedeliverytoU.S.locationswouldrisebybetween1.4centsperpoundand1.7centsperpounddependingonlocation(plattsMetalsWeek,2004b).Copperinventoriescontinuedtheirdownwardtrend,andbyyearendglobalcommodityexchangeinventorieshaddeclinedtoonly124,000t,thelowestlevelsincemid-1990.AccordingtoInternationalCopperStudyGroup(ICSG)data(2005a,p.9),totalyearendglobalinventories(commodityexchanges,consumer,government,merchant,andproducer)declinedto922,000tfrom1.78Mtatyearend2003,andattheprevailingrateofconsumptionequaledlessthana3-weeksupplyofcopper.

Copperscrappricesgenerallyfollowedtheupwardtrendinrefinedcopperprices.Withhigherrefinedprices,however,thediscountofmostgradesofcopperscraptorefinedcopperincreased.AccordingtoAmericanMetalMarketdata,theaveragediscountforrefinersNo.2scraproseto21centsperpoundfrom11centsperpoundin2003andthediscountforbrassmillNo.1scraproseto2.6centsperpoundfrom1.2

centsperpoundin2003.ThepricediscountforNo.2copperscrapincreasedsharplyinAprilto21.3centsperpoundfromanaverageofonly11.5centsperpoundduringthefirstquarter.TherisecoincidedwithindustryreportsthatChina,whichwastheleadingdestinationfordomesticscrapexports,hadessentiallyexitedfromtheNo.2scrapmarket,andthatshipmentsofscrapwerebackedupatChineseports(McCann,2004).

Trade

AccordingtoU.S.CensusBureaudata,netrefinedcopperimportsof689,000tweredownbyabout13%fromthosein2003.owingtoalargedrawdownininventories,however,U.S.importrelianceasapercentageofapparentdemandrosetoarecord-high43%.Canadaremainedthemostsignificantsourceofunwroughtcopperproductsfrom2000through2004andaccountedfor31%ofunmanufacturedimports,followedbyChile,28%,andperu,21%.refinedcopperaccountedfor75%ofunwroughtcopperimportsduringthesameperiod.In2004,theUnitedStateswasnominally(lessthan1,300t)anetexporterofcopperinconcentrates,havingbeenanetimporter(17,000t)in2003.Thistookplaceinlargepartbecauseofincreasedconcentrateproductionatnonintegratedminesthatexportedtheirconcentratesforprocessing.

AccordingtoU.S.CensusBureaudatacompiledbytheCopperandBrassFabricatorsCouncilInc.(2005,p.1-9),U.S.importsof328,000tofcopperandcopper-alloysemifabricatedproducts(excludingwire-rodmillproducts)wereupby22%fromthoseofthepreviousyear,andexportsroseto143,000tfrom122,000tin2003.Consequently,netimportsroseto184,000tfrom146,000tin2003.CanadaandMexicocollectivelyaccountedfor74%ofsemifabricatedcopperexportsand30%ofimports.

exportsofcopperscrapfor2004totaled714,000t,upfrom689,000tin2003.China(includingHongkong)wasthedestinationfor67%ofdomesticscrapexportsand,basedonimportdata,accountedfor65%ofreportedglobalscrapimports.TheUnitedStatesremainedtheleadingsourceofscrap,accountingfor19%ofglobalscraptrade(basedonreportedexports).

World Review

Whileworldproductionofrefinedcopperroseto15.8Mt,anincreaseofabout560,000t,worldcopperuse,accordingtoICSGdata(2005a,p.9),increasedbymorethan1Mttoalmost16.7Mt.Asaresult,theglobalproductiondeficitthatdevelopedduring2003continuedthroughout2004.Thecalculateddeficitfor2004reachedalmost900,000tofrefinedcopper.ThiscorrelateswellwiththeICSGreportedglobaldrawdownintotalinventories(860,000t)to920,000tatyearend2004from1.78Mtatyearend2003.Theaccumulated2-yeardeficitandstockdrawdown(2003-04)totaledabout1.3Mtand1.13Mt,respectively.Thediscrepancybetweencalculateddeficitsandstockdrawdownscanreadilybeaccountedforbythereleaseofunreportedinventories,especiallythoseinChina,thelargestglobalconsumerofcopper.

21.6 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

Whileworldrefineryproductionrosebyonlyabout560,000t,worldmineproductionrosebyabout860,000tto14.6Mt,withalloftheincreasecomingascopperinconcentrate.Smeltersreportedlyweretakingadvantageofasurgeinconcentrateavailabilityandariseintreatmentandrefiningchargestorebuilddiminishedinventoriesratherthanboosttheiroutput.ThiswasreportedtobemostprevalentinAsia,wherethedeclarationofaforcemajeureonconcentrateshipmentsfromtheGrasbergMineinIndonesiainlate2003hadcausedseveresupplyshortages,andsmelterswereseekingtoreducetheirvulnerabilitytofuturesupplyshortages.AccordingtoBloomsburyMineralseconomicsLtd.,smelterstocks,whichhadbeendecliningduringthepreceding3years,wereapproaching2001levelsbyyearend2004(plattsMetalsWeek,2004c).Underperformanceatsomenewsmelters,includingthoseinIndiaandThailand,alsocontributedtothefailureofincreasedmineoutputtotranslateintoincreasedrefineryproduction.AccordingtoICSG(2005b,p.62-67)data,smeltercapacityrosebyabout600,000tin2004to15.4Mt,whereascapacityutilizationdeclinedto82%fromabout83%in2003.AccordingtoCrUInternationalLtd.(2005,p.42-45),atightsupplyofconcentrateearlyintheyearthatresultedinspottreatmentandrefiningchargesfallingtozero,oreventonegativevalues,gavewaytosharplyrisingchargesatmidyearandbyyearendwereabout30centsperpoundofcopper.yearendtermcontractswerereportedtobeabout22centsperpoundofcopper.

Incontrastto2003,whenonlyAsiashowedapositivegrowthincopperuse,ICSG(2005a,p.19-20)dataindicatethatallthemajorcopperconsumingregionsoftheworldreportedsignificantgrowthincopperuse.InNorthAmerica,copperuseincreasedbymorethan6%to3.09Mt,upfrom2.90Mtin2003,andinAsia,copperuseincreasedby7.5%to7.7Mt.ThoughallthesignificantAsiancopper-consumingcountriesexperiencedgrowth,China,theworld’slargestconsumerofcopper,ledthewaywithanalmost8%increaseinapparentgrowth.releasesfromChina’sstrategicstockpile,forwhichdatawerenotavailable,mayhavesuppliedadditionalcoppertotheChinesemarket.Ineurope,copperuseincreasedbyabout5.3%to5.0Mtonthestrengthofrussianuse,whichincreasedbyabout30%to582,000t.ApparentconsumptionintheeuropeanUnionincreasedbyonlyabout2.3%.russianexporttariffsfavoredtheexportofvalueaddedproducts,resultingingreaterdomesticconsumptionofrefinedcopper,andanincreaseinexportsofcopperandcopper-alloysemifabricates,whichroseto305,000tin2004from185,000tin2003and59,000tin2001,whilerussianexportsofrefinedcopperdeclinedto339,000tin2004from395,000tin2003andmorethan580,000tin2001.U.S.importsofrussianwirerodwereonly29,000t,downfrom52,000tin2003,butstillsignificantlyhigherthan2001importsoflessthan3,000t.

Mine Production.—In2004,accordingtoICSG(2005b,p.2-60)estimates,worldminecapacityresumeditsstrongupwardgrowth,increasingbyalmost600,000t(3.9%).Capacityin2003hadrisenbyonlyabout130,000t(0.8%)toabout15.2Mt.Thisfollowedaperiodofstronggrowththatbeganin1995andsawcapacitygrowthof42%duringthe1994-2002period.estimatedcapacityutilizationincreasedin2004

fromabout90%inthepreceding2years,toalmost92%in2004,yetremainedwellbelowthatfor2001whentheutilizationrateexceeded94%.

In2004,capacitygrowthinChile(475,000t),China(20,000t),Congo(kinshasa)(30,000t),kazakhstan(40,000t),Mexico(30,000t),peru(105,000t),andZambia(34,000t),waspartiallyoffsetbyreductioninIndonesia.InIndonesia,effectivecapacitywasreducedbyabout280,000tfromitsengineeredcapacitywhenlandslideslimitedaccesstohigh-gradeoreintheGrasbergMine(InternationalCopperStudyGroup,2005b,p.12-60).

InAustralia,capacityandproductionwerepoisedtoincreasein2005followingthepurchaseoftheMt.GordonMinefrombankruptWesternMetalsLtd.byIndia’sAdityaBirlaGroup,andtheconversionofproductiontocopperinconcentratefromSX-eWinordertofeeditsDahejsmelterinIndia.TheBirlaGrouphadpreviouslypurchasedtheNiftyMineandwasplanningasimilarconversiontocopperinconcentrateandexpansionby2006(Clarke,2004§).

InChile,thereweremajorexpansionsatCorporaciónNacionaldelCobrédeChile’s(Codelco)NorteandTenientedivisions,andattheCollahuasiandescondidaMines.TotalproductionfromCodelco’sminesroseto1.84Mtfrom1.67Mtin2003.AtCodelcoNorte,productionroseto983,000tin2004from907,000tin2003followingaconcentratorexpansionin2003.WorkprogressedtowardopeningtheMinaSurnorthernexpansion,a120,000-t/yrrefinedcopperleachprojectslatedtobeginproductioninthelatterpartof2005.DevelopmentoftheMinistroAlejandroHalesMineandassociatedexpansionofconcentratorcapacityby50,000t/doforewasbeingstudied.AtelTeniente,productionroseto435,000tfrom339,000towingtomillandinfrastructureexpansionthatraisedmillingcapacityto131,000t/dofore(CorporaciónNacionaldelCobrédeChile,2005,p.25-42).AttheescondidaMine,productionroseto1.2Mtfrom993,000tin2003followingimprovedperformancefromthenewLagunaconcentrator.Mill-headgraderoseto1.51%from1.43%in2003andthroughputroseto82Mtfrom70Mtin2003.productionin2003hadbeensuppressedintentionallybymininglower-gradeoreinordertolimittheglobalcoppersurpluscarryingforwardfrom2002(rioTintoplc,2005b,p.14,45-48).

AttheCollahuasiMine,productionroseto481,000tofcopper(423,000tcopperinconcentrateand58,000telectrowon)fromatotalof395,000tin2003,followingcompletionofa$584millionexpansionprogramthatwasintendedtogivetheminealong-termcapacityof500,000t/yrofcopper(AngloAmerican,2005,p.124;Mining-technology.com,2005§).AttheelAbraMine(phelpsDodge,51%andCodelco,49%),productionofelectrowoncopperdeclinedbyabout9,000tto218,000t,andattheCandaleriaMine(phelpsDodge,80%andSumitomoCorp.,20%)concentrateproductiondeclinedby12,700tto200,000t(phelpsDodgeCorp.,2005,p.9).

InNorthernperu,productionattheAntaminacopper-zincproject(BHpBilliton,MitsubishiCorp.,NorandaInc.,andTeckComincoLtd.)rosetoarecord-high362,000tofcopperinconcentratefrom272,000tin2003.efficiencyimprovementsresultedinan18%increaseinmillthroughput,andcompletionofsedimentremovalfromthebottomofthepitallowedaccess

Copper—2004 21.7

tocopper-onlyore.Asaresult,averagemill-headgradesroseto1.34%copperfrom1.19%in2003,whilezincgradesdeclinedto0.97%zincfrom1.86%in2003(TeckComincoLtd.,2005§).

AtSpCCoperations,mineproductionfor2004increasedby6.1%to397,000t.Copperinconcentrateproductionroseby22,600tattheToquepalaMineandby9,800tattheCuajoneMine,whileSX-eWproductiondecreasedbyabout5,600t.MillthroughputattheToquepalaconcentratorincreased3%,establishinganewfacilitymillingrecordof19.8Mt/yr(SouthernperuCopperCompany,2005).

Smelter Production.—Worldsmeltercapacityrosebyabout600,000ttoarecord-high15.4Mt/yr.InChile,modernizationofNoranda’sAlnortesmelter,includinganewNorandafurnace,wascompletedin2003andboostedfull-yearcapacityin2004to270,000t/yrfrom165,000t/yrin2002.replacementofthereverberatoryfurnaceatCodelco’sSalvadorDivision(potrerillossmelter)boostedcapacitytoabout200,000t/yrfrom170,000t/yr(InternationalCopperStudyGroup,2005b,p.62-67).

InChina,expansionsoftheGuixi(JiangxiCopperCorp.),theJinchuanNon-ferrousMetalCo.,andtheJinlong(TonlingNonferrousMetalsCorp.)smeltersaccountedformostofa160,000-t/yrincreaseincapacity.AnewsmelterwasunderconstructionbyJinchuanthatcouldaddanadditional200,000t/yrofcapacitybyyearend2005.Atyearend,a30,000-t/yrsmelterwascommissionedbyBoatouHuadingCopperCo.,andphase2construction,whichcouldbringitsultimatecapacityupto200,000t/yr,wasunderconstruction(InternationalCopperStudyGroup,2005b,p.65-66).

InIndia,theBirlaGroupinstalledAusmelttechnologyin2003toexpanditsoutokumpufurnaceto250,000t/yrin2004from150,000t/yrin2002,andtheSterliteIndustriesLtd.,Isasmeltsmelter,whichstartedupin1996,reacheditscapacityofabout210,000t/yrin2004,upfrom180,000t/yrin2003.CapacityattheBirlasmelterwasexpectedtodoubleto500,000t/yrin2006,whilecapacityattheSterlitesmelterwasscheduledtoincreaseto300,000t/yrin2005.InIndonesia,afirst-phaseexpansionoftheGresiksmelterwascompleted,boostingcapacitybyabout25,000t/yrto245,000t/yr,andasecond-phaseexpansionwasanticipatedtocomeonstreamin2006.In2004,Iranemergedasamajorsmeltingcountrywithstartupofan80,000t/yrflashsmelterinkhatoonAbadandexpansionoftheSarChesmaehsmelterto200,000t/yrfrom145,000t/yr,bothownedbytheNationalIranianCopperIndustryCo.(InternationalCopperStudyGroup,2005b,p.68).

Refinery Production.—Worldrefinerycapacityrosebyabout530,000t/yr(3%).WiththeexceptionofonenewrefineryinChina(ZhongtiaoshanNonferrousMetalsCo.),nonewelectrolyticrefinerieswerecommissionedin2004,andforthemostpart,expansionsfollowedexpandedsmeltercapacities.Chinaaccountedforalmost340,000toftheincreasedglobalcapacity.InBelgium,thesecondaryrefineryinLiege,withacapacityofabout80,000t/yroffire-refinedcopper,closedearlyintheyear.Afterfallingin2003owingtoaglobalshortageofconcentrates,capacityutilizationatglobalrefineriesrosetoabout82%from81%in2003,butwasdownfrom88%asrecentlyas2001(InternationalCopperStudyGroup,2005b,p.96-106).

Outlook

Despiteamorethan3%estimatedgrowthinworldmineandrefineryproductionin2005,productionwasinsufficienttomeetglobaldemand,andtherefinedcopperproductiondeficitthathaddevelopedduringthepreceding2yearscontinuedthroughatleastthefirst3quartersof2005.Globalinventoriesofrefinedcopperheldinmetalexchangewarehousescontinuedtheirdownwardtrend,fallingbelow100,000tduringthethirdquarterof2005.Thisshortfalldevelopeddespiteanestimateddeclineinglobalconsumption,which,accordingtotheICSG(2005a,p.19),declinedbyalmost2%duringthefirst9monthsof2005comparedwiththatforthesameperiodin2004.StronggrowthinChinaandIndiawasmorethanoffsetbyreducedusebyothersignificantconsumers.Thoughglobalminecapacitywasprojectedtoincreasebyabout860,000t(5.5%),globalmineproductionfellshortofitsanticipatedgrowthowingtoproductionshortfallsintheUnitedStatesandSouthAmerica,andminecapacityutilizationwasprojectedtofalltoitslowestlevelinrecentyears.Newcapacityandincreasedcapacityutilizationwasexpectedtoreversetheglobalproductiondeficit,andamodestproductionsurpluswasanticipatedfor2006.

IntheUnitedStates,mineoutputwasprojectedtodecreasetoabout1.15Mtin2005owingtounusuallyheavyspringrains,equipmentshortages,andastrikebyworkersatAsarcothatbeganinJulyandextendedthroughthesecondweekinNovember.year-on-yearU.S.consumptionofrefinedcopperdeclinedduringthefirst9monthsof2005owingtoweakerdemandandasurgeinimportsofwirerodinthefirsthalfof2005.U.S.mineandrefineryproductionwereexpectedtoincreasein2006followingsettlementofthestrikeandtheexpectedstartupofaneweWfacilityinUtahearlyintheyear.

References Cited

AmericanBureauofMetalStatistics,Inc.,2004,UScopperwirerodmarket—ABMSreport4:Chatham,NJ,AmericanBureauofMetalStatistics,Inc.,May27,8p.

AmericanBureauofMetalStatistics,Inc.,2005a,Brassmillinventories,receiptsandshipmentsoftheUnitedStates—ABMSreport3:Chatham,NJ,AmericanBureauofMetalStatistics,Inc.,March24,12p.

AmericanBureauofMetalStatistics,Inc.,2005b,UScopperwirerodmarket—ABMSreport4:Chatham,NJ,AmericanBureauofMetalStatistics,Inc.,February22,6p.

AngloAmericanplc,2005,Annualreport—2004:London,Unitedkingdom,AngloAmericanplc,124p.

BHpBilliton,2005,Annualreport—2004:London,Unitedkingdom,BHpBilliton,55p.

ConstellationCopperCorp.,2004a,ConstellationCopperCorporationarrangesUS$40milliondebtfinanceforLisbonvalleyandreceivesintenttoapproveairqualitypermit:Denver,Co,ConstellationCopperCorp.pressrelease,June8,2p.

ConstellationCopperCorp.,2004b,ConstructioncommencesattheLisbonvalleySX-eWcopperproject:Denver,Co,ConstellationCopperCorp.pressrelease,November16,1p.

ConstellationCopperCorp.,2004c,UpdateonLisbonvalleySX-eWproject:Denver,Co,ConstellationCopperCorp.pressrelease,September29,1p.

CopperandBrassFabricatorsCouncilInc.,2005,Import/exportreport:Washington,DC,CopperandBrassFabricatorsCouncilInc.,January,121p.

CopperDevelopmentAssociationInc.,2005,Annualdata2004—Coppersupplyandconsumption:Newyork,Ny,CopperDevelopmentAssociationInc.,21p.

CorporaciónNacionaldelCobrédeChile,2005,Annualreport—2004:Santiago,Chile,CorporaciónNacionaldelCobrédeChile,102p.

21.8 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

CrUInternationalLtd.,2005,Copperquarterlyindustryandmarketoutlook:London,Unitedkingdom,CrUInternationalLtd.,January,66p.

Dillard,Gary,2004,NewhopeforSuperior:payDirt,November,p.3-5.GrupoMéxico,S.A.deC.v.,2004,GrupoMéxico,S.A.deC.v.reportsits

resultstodaycorrespondingtothethirdquarterandninemonthsendedSeptember30,2004:MexicoCity,Mexico,GrupoMéxico,S.A.deC.v.Ceo’sreport,october24,20p.

GrupoMéxico,S.A.deC.v.,2005,Annualreport—2004:MexicoCity,Mexico,GrupoMéxico,S.A.deC.v.,46p.

InternationalCopperStudyGroup,2005a,Copperbulletin:Lisbon,portugal,InternationalCopperStudyGroup,v.12,no.12,December,55p.

InternationalCopperStudyGroup,2005b,Directoryofcopperminesandplants:Lisbon,portugal,InternationalCopperStudyGroup,January,105p.

McCann,Joseph,2004,ChinesenoticeablyabsentfromUScopperscrapmart:AmericanMetalMarket,v.112,no.11-1,March15,p.6.

NordresourcesCorp.,2004,NordresourcesinvitestendersfromminingcontractorsforJohnsonCampcoppermine:Dragoon,AZ,NordresourcesCorp.newsrelease,July19,2p.

plattsMetalsWeek,2004a,FearsofstrikesatAsarco,Collahuasipushcopperhigher:plattsMetalsWeek,v.75,no.27,July5,p.1,6.

plattsMetalsWeek,2004b,kennecottpremiumsupmorethan1.40¢:plattsMetalsWeek,v.75,no.51,December20,p.15.

plattsMetalsWeek,2004c,refinedcopperdeficittotop1-milmtin2004—BMe:plattsMetalsWeek,v.75,no.46,November15,p.9.

plattsMetalsWeek,2005,Asarcoaimstohikeoutputto220,000mt:plattsMetalsWeek,v.76,no.4,January24,p.7.

phelpsDodgeCorp.,2004,phelpsDodgeisincreasingcopperproductionin2004,2005:phoenix,AZ,phelpsDodgeCorp.newsrelease,January29,2p.

phelpsDodgeCorp.,2005,Annualreport—2004:phoenix,AZ,phelpsDodgeCorp.,152p.

QuadraMiningLtd.,2004a,QuadraMiningLtd.reportssecondquarterresults,increasedmineralreservesandrevisedmineplan:vancouver,BritishColumbia,Canada,QuadraMiningLtd.pressrelease,August11,4p.

QuadraMiningLtd.,2004b,robinsonMineupdate—Concentratorbeginsprocessingore—Miningcontractsigned:vancouver,BritishColumbia,Canada,QuadraMiningLtd.pressrelease,September8,2p.

rioTintoplc.,2005a,Fourthquarter2004operationsreview:London,Unitedkingdom,rioTintoplcpressrelease,January19,23p.

rioTintoplc.,2005b,rioTinto2004annualreportandfinancialstatements:London,Unitedkingdom,rioTintoplc.,155p.

SouthernperuCopperCorp.,2004,SouthernperutoacquireMineraMéxicoinastock-for-stocktransaction:Lima,peru,SouthernperuCopperCorp.pressrelease,october21,1p.

SouthernperuCopperCorp.,2005,SpCCreportsfourthquarterandfull-yearresults:Lima,peru,SouthernperuCopperCorp.pressrelease,March14,2p.

U.S.DepartmentofCommerce,2004,requestforpubliccommentonthereceiptbytheDepartmentofCommerceofawrittenpetitionrequestingtheimpositionofshortsupplyexportcontrolsandmonitoringonrecyclablemetallicmaterialscontainingcopper:Federalregister,v.69,no.78,April22,p.21815-21816.

U.S.environmentalprotectionAgency,2003,Nationalprimarydrinkingwaterregulations;announcementofcompletionofepA’sreviewofexistingdrinkingwaterstandards:Federalregister,v.68,no.138,July18,p.42907-42929.

U.S.environmentalprotectionAgency,2004a,Leadandcopperrule;expertpanelworkshoponpubliceducationandriskcommunication:Federalregister,v.69,no.153,August10,p.48491-48492.

U.S.environmentalprotectionAgency,2004b,Leadandcopperrule;expertpanelworkshopsonsimultaneouscomplianceandmonitoringprotocols:Federalregister,v.69,no.79,April23,p.21958.

Internet References Cited

Clarke,Jo,2004(January26),India’aBirlaindealtobuysecondAustraliancopperminefor$14.3,accessedoctober5,2005,viaUrLhttp://www.amm.com.

Francis-Grey,paul,2004(April21),CoppertriggersLMeplunge,pricesdecrease,accessedApril22,2004,viaUrLhttp://www.amm.com.

GoldSpring,Inc.,2004,TheBigMikeproject,accessedJuly9,2004,viaUrLhttp://www.goldspring.us.

McCann,Joseph,2004(June18),Missouricoppersmelterismakingacomeback,accessedJune21,2004,viaUrLhttp://www.amm.com.

Mining-technology.com,2005,Collahuasicoppermine,Chile,accessedDecember18,2005,atUrLhttp://www.mining-technology.com/projects/collahuasi.

TeckComincoLtd.,2005,Antaminayearinreview,accessedJanuary20,2006,atUrLhttp://www.teckcominco.com/operations/antamina/review/htm.

U.S.DepartmentofCommerce,2004a(July21),CommerceDepartmentannouncescopperscrapandcopper-alloyscrapdetermination,accessedJuly22,2004,atUrLhttp://www.bis.doc.gov/news/2004/copperJuly21.htm.

U.S.DepartmentofCommerce,2004b(April7),petitionfortheimpositionofmonitoringandcontrolswithrespecttoexportsfromtheUnitedStatesofcopperscrapandcopperalloyscrap,accessedApril12,2004,atUrLhttp://www.bis.doc.gov/pdf/ocpa-final.pdf.

GEnERaL SOuRCES Of InfORMaTIOn

u.S. Geological Survey Publications

Copper.Ch.inMetalpricesintheUnitedStatesThrough1998.Copper.Ch.inMineralCommoditySummaries,annual.Copper.Ch.inUnitedStatesMineralresources,professional

paper820,1973.Copper.MineralIndustrySurveys,monthly.TheNatureandUseofCopperreserveandresourceData,

professionalpaper907-F,1981.

Other

AmericanBureauofMetalStatistics(ABMS)Non-FerrousMetalData.

TheAvailabilityofCopperinMarketeconomyCountries,U.S.BureauofMinesInformationCircular9310,1992.

Copper.Ch.inMineralFactsandproblems,U.S.BureauofMinesBulletin675,1985.

InternationalCopperStudyGroup,Lisbon,portugal,monthlyCopperBulletin.

InternationalCopperStudyGroup,Lisbon,portugal,quarterlyDirectoryofCopperMinesandplants.

WorldBureauofMetalStatistics(WBMS,London),monthlyWorldMetalsStatistics.

Copper—2004 21.9

TABLE 1

SALIENT COPPER STATISTICS1

(Metric tons unless otherwise specified)

2000 2001 2002 2003 2004

United States:

Mine production:

Ore concentrated thousand metric tons 202,000 148,000 104,000 114,000 139,000

Averag y er2e ield of copp percent 0.44 r 0.48 r 0.52 r 0.46 r 0.38

Recoverable copper:

Arizona 929,000 879,000 767,000 741,000 723,000

Michigan, Montana, Utah W W W W W

New Mexico 195,000 141,000 112,000 87,800 122,000

Other States 322,000 318,000 263,000 287,000 312,000

Total 1,450,000 1,340,000 1,140,000 1,120,000 1,160,000

Total value millions $2,810 $2,270 $1,910 $2,100 $3,420

Smelter production, primary and secondary 1,000,000 919,000 683,000 539,000 542,000

Byproduct sulfuric acid, sulfur content thousand metric tons 830 813 695 590 600

Refinery production:

Primary materials:

Electrolytic from domestic ores 865,000 808,000 725,000 532,000 531,000

Electrolytic from foreign materials 163,000 192,000 116,000 130,000 140,000

Electrowon 556,000 628,000 601,000 591,000 584,000

Total 1,580,000 1,630,000 1,440,000 1,250,000 1,260,000

Secondary materials (scrap), electrolytic and fire refined 209,000 172,000 69,900 53,300 50,800

Grand total 1,790,000 1,800,000 1,510,000 1,310,000 1,310,000

Secondary copper produced:

Recovered from new scrap 955,000 833,000 840,000 r 737,000 r 774,000

Recovered from old scrap 358,000 317,000 190,000 r 207,000 r 191,000

Total 1,310,000 1,150,000 1,030,000 r 944,000 965,000

Copper sulfate production 55,500 55,200 49,200 32,100 25,100

Exports:

Refined 93,600 22,500 26,600 93,300 118,000

Unmanufactured3 650,000 556,000 506,000 703,000 789,000

Imports:

Refined 1,060,000 991,000 927,000 882,000 807,000

Unmanufactured3 1,350,000 1,400,000 1,230,000 1,140,000 1,060,000

Copper stocks, December 31:

Blister and in-process material 122,000 98,000 44,400 56,800 51,400

Refined copper:

Refineries 14,800 28,600 11,700 12,100 10,400

Wire-rod mills 39,900 37,600 23,000 29,700 20,300

Brass mills 23,600 25,500 28,700 20,200 21,500

Other industry 4,390 4,860 4,800 4,240 r 3,230

New York Commodity Exchange (COMEX) 58,700 244,000 362,000 255,000 43,700

London Metal Exchange (LME), U.S. warehouses 204,000 617,000 601,000 335,000 35,000

Total 345,000 957,000 1,030,000 656,000 r 134,000

Consumption:

Refined copper, reported 3,020,000 2,620,000 2,370,000 2,290,000 2,410,000

A p p y p4pparent consum tion, rimar refined and old scra 3,090,000 2,510,000 2,610,000 2,430,000 2,550,000

Price:

Producer, weighted average cents per pound 88.16 76.85 75.80 85.25 133.94

COMEX, first position do. 83.97 72.57 71.67 81.05 128.97

LME, Grade A cash do. 82.24 71.57 70.72 80.68 129.96

World production:

Mine thousand metric tons 13,300 r 13,700 13,700 r 13,700 r 14,600 e

Smelter do. 12,300 r 12,800 r 12,600 r 12,500 r 12,700 e

Refinery do. 14,900 15,600 r 15,400 r 15,200 e 15,800See footnotes at end of table.

21.10 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

TABLE 1—Continued

SALIENT COPPER STATISTICS1

eEstimated. rRevised. W Withheld to avoid disclosing company proprietary data; included in "Other States."1Data are rounded to no more than three significant digits, except prices; may not add to totals shown.2Yield calculations are for concentrated ore only.3Includes copper content of alloy scrap.4In 2000, 2001, 2002, 2003, and 2004, apparent consumption is calculated using general imports of 1,020,000 tons, 1,200,000 tons, 1,060,000 tons, 687,000 tons, and 704,000 tons, respectively.

TABLE 2

LEADING COPPER-PRODUCING MINES IN THE UNITED STATES IN 2004, IN ORDER OF OUTPUT1

Capacity

(thousand

Rank Mine County and State Operator Source of copper metric tons)

1 Morenci Greenlee, AZ Phelps Dodge Corp. Copper ore, leached 390

2 Bingham Canyon Salt Lake, UT Kennecott Utah Copper Corp. Copper-molybdenum ore, concentrated 300

3 Ray Mine Pinal, AZ ASARCO Incorporated Copper ore, concentrated and leached 180

4 Bagdad Yavapai, AZ Phelps Dodge Corp. Copper-molybdenum ore, concentrated and leached 120

5 Chino Grant, NM do. do. 125

6 Sierrita Pima, AZ do. do. 100

7 Tyrone Grant, NM do. Copper ore, leached 80

8 Continental Pit Silver Bow, MT Montana Resources Copper-molybdenum ore, concentrated 45

9 Mission Complex Pima, AZ ASARCO Incorporated Copper ore, concentrated 70

10 Silver Bell do. do. Copper ore, leached 22

11 Robinson Mine White Pine, NV Robinson Nevada Mining Company Copper ore, concentrated 60

12 Miami Mine Gila, AZ Phelps Dodge Corp. Copper ore, leached 73

13 Pinto Valley do. BHP Copper Co. do. 10

14 Miami Mine do. do. do. 121The mines on this list accounted for more than 99% of U.S. mine production in 2004.

TABLE 3

MINE PRODUCTION OF COPPER-BEARING ORES AND RECOVERABLE COPPER CONTENT

OF ORES PRODUCED IN THE UNITED STATES, BY SOURCE AND TREATMENT PROCESS1

(Metric tons)

2003 2004

Gross Recoverable Gross Recoverable

Source and treatment process weight2 copper weight2 copper

Mined copper ore:

Concentrated 114,000,000 518,000 139,000,000 533,000

Leached NA 591,000 NA 584,000

Total NA 1,110,000 NA 1,120,000

Copper precipitates shipped, leached from

tailings, dumps, and in-place material 1,210 684 1,270 2,360

Other copper-bearing ores3 3,320,000 r 6,060 4,780,000 37,200

Grand total XX 1,120,000 XX 1,160,000rRevised. NA Not available. XX Not applicable. 1Data are rounded to no more than three significant digits; may not add to totals shown.2In 2004, 9,706 kilograms of gold and 171 metric tons of silver were recovered from concentrated ore. The average value of gold and silver per metric ton of ore concentrated was $1.18.3Includes gold ore, lead ore, silver ore, silver-copper ore, zinc ore, and ore shipped directly to smelter.

Copper—2004 21.11

TABLE 4

CONSUMPTION OF COPPER AND BRASS MATERIALS IN THE UNITED STATES, BY ITEM1

(Metric tons)

Foundries, Smelters,

chemical plants, refiners,

Item Brass mills Wire-rod mills miscellaneous users ingot makers Total

2003:

Copper scrap 840,000 2 W 85,900 r 187,000 r 1,110,000

Refined copper3 587,000 1,640,000 59,500 r 4,550 2,290,000

Hardeners and master alloys 6,060 -- 1,750 -- 7,800

Brass ingots 1,180 -- 98,700 r -- 99,900 r

Slab zinc 65,600 -- (4) (4) 86,200

2004:

Copper scrap 880,000 2 W 80,700 183,000 1,140,000

Refined copper3 573,000 1,780,000 57,400 4,560 2,410,000

Hardeners and master alloys 10,000 -- 2,040 -- 12,100

Brass ingots 1,470 -- 95,200 -- 96,600

Slab zinc 68,300 -- (4) (4) 95,500rRevised. W Withheld to avoid disclosing company proprietary data; included with "Brass mills." -- Zero.1Data are rounded to no more than three significant digits; may not add to totals shown.2Includes item indicated by symbol W.3Detailed information on consumption of refined copper can be found in table 5.4Withheld to avoid disclosing company proprietary data; included in "Total."

O R

TABLE 5

NSUMPTION OF REFINED COPPER SHAPES IN THE UNITED STATES, BY CLASS OF CONSUME

(Metric tons)

Ingots and Cakes and Wirebar, billets,

Class of consumer Cathodes ingot bars slabs other Total

2003:

Wire-rod mills 1,630,000 -- -- 8,730 1,640,000

Brass mills 439,000 14,900 41,800 91,400 587,000

Chemical plants -- -- -- 959 959

Ingot makers W W W 4,550 2 4,550

Foundries 3,320 r 7,440 r -- 11,100 r 21,900 r

Miscellaneous3 W W W 36,700 r, 2 36,700 r

Total 2,070,000 22,300 r 41,800 153,000 2,290,000 r

2004:

Wire-rod mills 1,770,000 -- -- 8,860 1,780,000

Brass mills 389,000 15,100 57,000 112,000 573,000

Chemical plants -- -- -- 1,200 1,200

Ingot makers W W W 4,560 2 4,560

Foundries 3,470 6,230 -- 11,300 21,000

Miscellaneous3 W W W 35,200 2 35,200

Total 2,160,000 21,400 57,000 173,000 2,410,000rRevised. W Withheld to avoid disclosing company proprietary data; included with "Wirebar, billets, other." -- Zero.1Data are rounded to no more than three significant digits; may not add to totals shown.2Includes items indicated by symbol W.3Includes consumers of copper powder and copper shot, iron and steel plants, and other manufacturers.

21.12 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

.

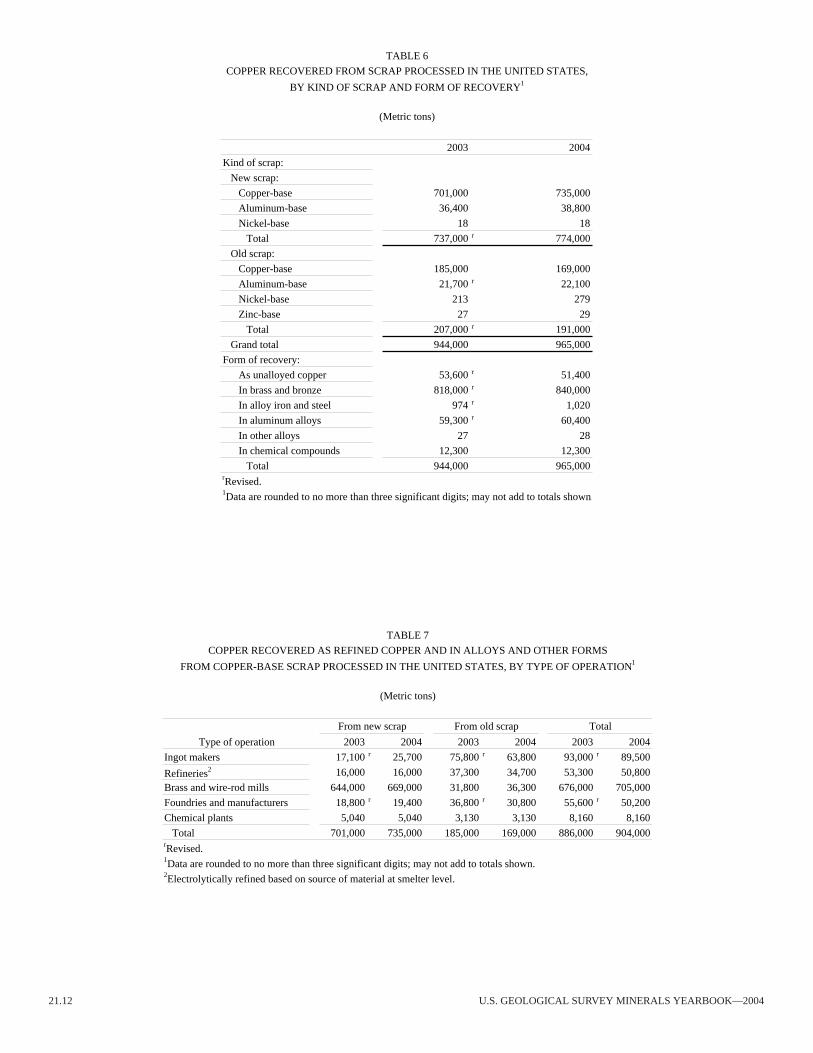

TABLE 6

COPPER RECOVERED FROM SCRAP PROCESSED IN THE UNITED STATES,

BY KIND OF SCRAP AND FORM OF RECOVERY1

(Metric tons)

2003 2004

Kind of scrap:

New scrap:

Copper-base 701,000 735,000

Aluminum-base 36,400 38,800

Nickel-base 18 18

Total 737,000 r 774,000

Old scrap:

Copper-base 185,000 169,000

Aluminum-base 21,700 r 22,100

Nickel-base 213 279

Zinc-base 27 29

Total 207,000 r 191,000

Grand total 944,000 965,000

Form of recovery:

As unalloyed copper 53,600 r 51,400

In brass and bronze 818,000 r 840,000

In alloy iron and steel 974 r 1,020

In aluminum alloys 59,300 r 60,400

In other alloys 27 28

In chemical compounds 12,300 12,300

Total 944,000 965,000rRevised.1Data are rounded to no more than three significant digits; may not add to totals shown

TABLE 7

COPPER RECOVERED AS REFINED COPPER AND IN ALLOYS AND OTHER FORMS

FROM COPPER-BASE SCRAP PROCESSED IN THE UNITED STATES, BY TYPE OF OPERATION1

(Metric tons)

From new scrap From old scrap Total

Type of operation 2003 2004 2003 2004 2003 2004

Ingot makers 17,100 r 25,700 75,800 r 63,800 93,000 r 89,500

Refineries2 16,000 16,000 37,300 34,700 53,300 50,800

Brass and wire-rod mills 644,000 669,000 31,800 36,300 676,000 705,000

Foundries and manufacturers 18,800 r 19,400 36,800 r 30,800 55,600 r 50,200

Chemical plants 5,040 5,040 3,130 3,130 8,160 8,160

Total 701,000 735,000 185,000 169,000 886,000 904,000rRevised.1Data are rounded to no more than three significant digits; may not add to totals shown.2Electrolytically refined based on source of material at smelter level.

Copper—2004 21.13

TABLE 8

PRODUCTION OF SECONDARY COPPER AND COPPER-ALLOY PRODUCTS

IN THE UNITED STATES, BY ITEM PRODUCED FROM SCRAP1

(Metric tons)

Item produced from scrap 2003 2004

Unalloyed copper products:

Refined copper 53,300 50,800

Copper powder 6,850 r 48

Copper castings 338 574

Total 60,500 r 51,400

Alloyed copper products:

Brass and bronze ingots:

Tin bronzes 8,820 r 10,200

Leaded red brass and semired brass 64,700 r 68,400

High leaded tin bronze 9,840 r 10,400

Yellow brass 4,370 r 5,890

Manganese bronze 7,860 r 8,270

Aluminum bronze 5,030 r 6,010

Nickel silver 2,270 r 2,140

Silicon bronze and brass 4,190 r 5,900

Copper-base hardeners and master alloys 5,420 5,500

Miscellaneous 6,130 r 4,940

Total 119,000 r 128,000

Brass mill and wire-rod mill products 829,000 865,000

Brass and bronze castings 42,800 r 44,000

Brass powder 102 71

Copper in chemical products 12,300 12,300

Grand total 1,060,000 1,100,000rRevised.1Data are rounded to no more than three significant digits; may not add to totals shown.

TABLE 9

COMPOSITION OF SECONDARY COPPER-ALLOY PRODUCTION IN THE UNITED STATES1

(Metric tons)

Copper Tin Lead Zinc Nickel Aluminum Total

Brass and bronze ingot production:2

2003r 100,000 3,400 5,290 9,540 221 12 119,000

2004 107,000 4,140 6,110 10,600 224 14 128,000

Secondary metal content of brass mill products:

2003 677,000 491 5,820 144,000 W W 829,000

2004 706,000 475 6,160 150,000 W W 865,000

Secondary metal content of brass and bronze castings:

2003 38,000 r 1,510 r 1,080 1,950 r 121 r 75 r 42,800 r

2004 39,100 1,520 1,130 2,030 182 62 44,000rRevised. W Withheld to avoid disclosing company proprietary data; included in "Total."1Data are rounded to no more than three significant digits; may not add to totals shown.2Includes approximately 97% from scrap and 3% from other than scrap in 2003 and approximately 96% from scrap and 4% from other

than scrap in 2004.

21.14 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

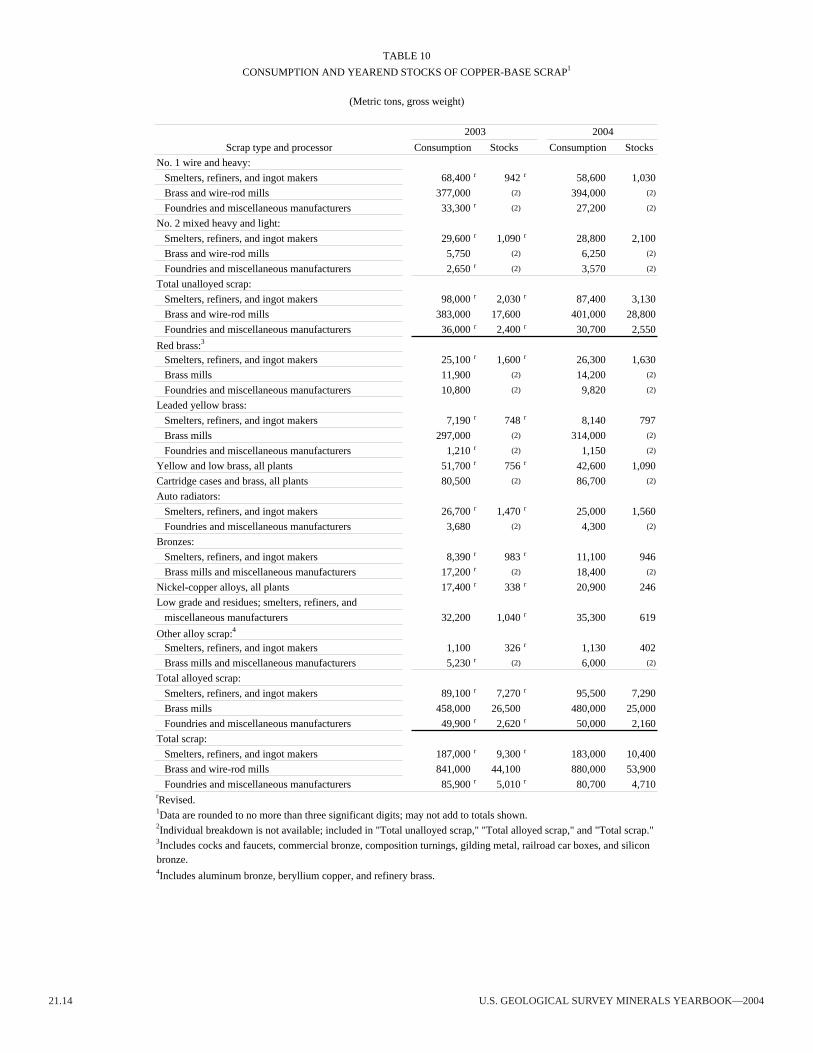

TABLE 10

CONSUMPTION AND YEAREND STOCKS OF COPPER-BASE SCRAP1

(Metric tons, gross weight)

2003 2004

Scrap type and processor Consumption Stocks Consumption Stocks

No. 1 wire and heavy:

Smelters, refiners, and ingot makers 68,400 r 942 r 58,600 1,030

Brass and wire-rod mills 377,000 (2) 394,000 (2)

Foundries and miscellaneous manufacturers 33,300 r (2) 27,200 (2)

No. 2 mixed heavy and light:

Smelters, refiners, and ingot makers 29,600 r 1,090 r 28,800 2,100

Brass and wire-rod mills 5,750 (2) 6,250 (2)

Foundries and miscellaneous manufacturers 2,650 r (2) 3,570 (2)

Total unalloyed scrap:

Smelters, refiners, and ingot makers 98,000 r 2,030 r 87,400 3,130

Brass and wire-rod mills 383,000 17,600 401,000 28,800

Foundries and miscellaneous manufacturers 36,000 r 2,400 r 30,700 2,550

Red brass:3

Smelters, refiners, and ingot makers 25,100 r 1,600 r 26,300 1,630

Brass mills 11,900 (2) 14,200 (2)

Foundries and miscellaneous manufacturers 10,800 (2) 9,820 (2)

Leaded yellow brass:

Smelters, refiners, and ingot makers 7,190 r 748 r 8,140 797

Brass mills 297,000 (2) 314,000 (2)

Foundries and miscellaneous manufacturers 1,210 r (2) 1,150 (2)

Yellow and low brass, all plants 51,700 r 756 r 42,600 1,090

Cartridge cases and brass, all plants 80,500 (2) 86,700 (2)

Auto radiators:

Smelters, refiners, and ingot makers 26,700 r 1,470 r 25,000 1,560

Foundries and miscellaneous manufacturers 3,680 (2) 4,300 (2)

Bronzes:

Smelters, refiners, and ingot makers 8,390 r 983 r 11,100 946

Brass mills and miscellaneous manufacturers 17,200 r (2) 18,400 (2)

Nickel-copper alloys, all plants 17,400 r 338 r 20,900 246

Low grade and residues; smelters, refiners, and

miscellaneous manufacturers 32,200 1,040 r 35,300 619

Other alloy scrap:4

Smelters, refiners, and ingot makers 1,100 326 r 1,130 402

Brass mills and miscellaneous manufacturers 5,230 r (2) 6,000 (2)

Total alloyed scrap:

Smelters, refiners, and ingot makers 89,100 r 7,270 r 95,500 7,290

Brass mills 458,000 26,500 480,000 25,000

Foundries and miscellaneous manufacturers 49,900 r 2,620 r 50,000 2,160

Total scrap:

Smelters, refiners, and ingot makers 187,000 r 9,300 r 183,000 10,400

Brass and wire-rod mills 841,000 44,100 880,000 53,900

Foundries and miscellaneous manufacturers 85,900 r 5,010 r 80,700 4,710rRevised.1Data are rounded to no more than three significant digits; may not add to totals shown.2Individual breakdown is not available; included in "Total unalloyed scrap," "Total alloyed scrap," and "Total scrap."3Includes cocks and faucets, commercial bronze, composition turnings, gilding metal, railroad car boxes, and siliconbronze.4Includes aluminum bronze, beryllium copper, and refinery brass.

Copper—2004 21.15

TABLE 11

CONSUMPTION OF PURCHASED COPPER-BASE SCRAP1, 2

(Metric tons, gross weight)

From new scrap From old scrap Total

Type of operation 2003 2004 2003 2004 2003 2004

Ingot makers 23,000 r 40,200 110,000 r 91,700 133,000 r 132,000

Smelters and refineries 16,200 16,200 37,600 34,900 53,800 51,100

Brass and wire-rod mills 808,000 843,000 32,600 37,700 841,000 880,000

Foundries and miscellaneous manufacturers 41,600 r 42,600 44,200 r 38,200 85,900 r 80,700

Total 889,000 r 941,000 225,000 r 202,000 1,110,000 1,140,000rRevised.1Data are rounded to no more than three significant digits; may not add to totals shown.2Consumption at brass and wire-rod mills assumed equal to receipts.

TABLE 12

FOUNDRIES AND MISCELLANEOUS MANUFACTURERS CONSUMPTION OF

BRASS INGOT, REFINED COPPER AND COPPER SCRAP IN THE UNITED STATES1

(Metric tons)

Ingot type or material consumed 2003 2004

Tin bronzes 23,500 r 22,800

Leaded red brass and semired brass 57,300 r 55,300

Yellow, leaded, low brass2 5,460 r 6,440

Manganese bronze 5,640 r 3,940

Nickel silver3 2,850 2,260

Aluminum bronze 3,580 r 3,590

Hardeners and master alloys4 1,750 2,040

Lead free alloys5 377 864

Total brass ingot 100,000 r 97,200

Refined copper 59,500 r 57,400

Copper scrap 85,900 r 80,700rRevised.1Data are rounded to no more than three significant digits; may not add to totals shown.2Includes brass and silicon bronze.3Includes brass, copper nickel, and nickel bronze.4Includes special alloys.5Includes copper-bismuth and copper-bismuth-selenium alloys.

TABLE 13

AVERAGE PRICES FOR COPPER SCRAP AND ALLOY-INGOT, BY TYPE

(Cents per pound)

Dealers' buying (New York)

Brass mills Refiners No. 2 Red brass turnings

Year No. 1 scrap No. 2 scrap scrap and borings

2003 80.17 70.42 52.70 38.65

2004 126.41 107.62 86.86 55.14

Source: American Metal Market.

21.16 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

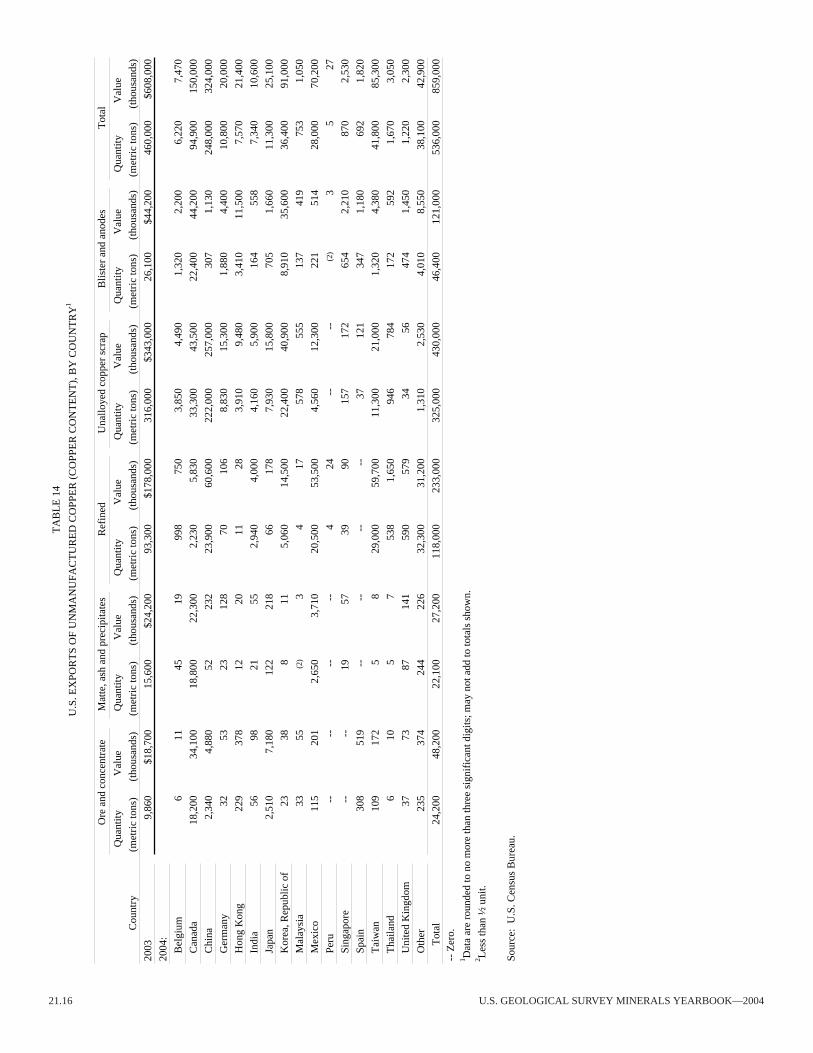

TA

BL

E 1

4

U.S

. EX

POR

TS

OF

UN

MA

NU

FAC

TU

RE

D C

OPP

ER

(C

OPP

ER

CO

NT

EN

T),

BY

CO

UN

TR

Y1

Ore

and

con

cent

rate

Mat

te, a

sh a

nd p

reci

pita

tes

Ref

ined

Una

lloye

d co

pper

scr

apB

liste

r an

d an

odes

Tot

al

Qua

ntity

Val

ueQ

uant

ityV

alue

Qua

ntity

Val

ueQ

uant

ityV

alue

Qua

ntity

Val

ueQ

uant

ityV

alue

Cou

ntry

(met

ric

tons

) (t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

) (t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

) (t

hous

ands

) (m

etri

c to

ns)

(tho

usan

ds)

2003

9,86

0$1

8,70

015

,600

$24,

200

93,3

00$1

78,0

0031

6,00

0$3

43,0

0026

,100

$44,

200

460,

000

$608

,000

2004

:

Bel

gium

611

4519

998

750

3,85

04,

490

1,32

02,

200

6,22

07,

470

Can

ada

18,2

0034

,100

18,8

0022

,300

2,23

05,

830

33,3

0043

,500

22,4

0044

,200

94,9

0015

0,00

0

Chi

na2,

340

4,88

052

232

23,9

0060

,600

222,

000

257,

000

307

1,13

024

8,00

032

4,00

0

Ger

man

y32

5323

128

7010

68,

830

15,3

001,

880

4,40

010

,800

20,0

00

Hon

g K

ong

229

378

1220

1128

3,91

09,

480

3,41

011

,500

7,57

021

,400

Indi

a56

9821

552,

940

4,00

04,

160

5,90

016

455

87,

340

10,6

00

Japa

n2,

510

7,18

012

221

866

178

7,93

015

,800

705

1,66

011

,300

25,1

00

Kor

ea, R

epub

lic o

f23

388

115,

060

14,5

0022

,400

40,9

008,

910

35,6

0036

,400

91,0

00

Mal

aysi

a33

55(2

)3

417

578

555

137

419

753

1,05

0

Mex

ico

115

201

2,65

03,

710

20,5

0053

,500

4,56

012

,300

221

514

28,0

0070

,200

Peru

----

----

424

----

(2)

35

27

Sing

apor

e--

--19

5739

9015

717

265

42,

210

870

2,53

0

Spai

n30

851

9--

----

--37

121

347

1,18

069

21,

820

Tai

wan

109

172

58

29,0

0059

,700

11,3

0021

,000

1,32

04,

380

41,8

0085

,300

Tha

iland

610

57

538

1,65

094

678

417

259

21,

670

3,05

0

Uni

ted

Kin

gdom

3773

8714

159

057

934

5647

41,

450

1,22

02,

300

Oth

er23

537

424

422

632

,300

31,2

001,

310

2,53

04,

010

8,55

038

,100

42,9

00

Tot

al24

,200

48,2

0022

,100

27,2

0011

8,00

023

3,00

032

5,00

043

0,00

046

,400

121,

000

536,

000

859,

000

-- Z

ero.

1 Dat

a ar

e ro

unde

d to

no

mor

e th

an th

ree

sign

ific

ant d

igits

; may

not

add

to to

tals

sho

wn.

2 L

ess

than

½ u

nit.

Sour

ce:

U.S

. Cen

sus

Bur

eau.

Copper—2004 21.17

Bd

TA

BL

E 1

5

U.S

. EX

POR

TS

OF

CO

PPE

R S

EM

IMA

NU

FAC

TU

RE

S, B

Y C

OU

NT

RY

1

Pipe

s an

d tu

bing

Plat

es, s

heet

s, f

oil,

bars

are

wir

e, in

clud

ing

wir

e ro

Wir

e an

d ca

ble,

str

ande

dC

oppe

r su

lfat

e

Qua

ntity

Val

ueQ

uant

ityV

alue

Qua

ntity

Val

ueQ

uant

ityV

alue

Qua

ntity

Val

ue

Cou

ntry

(met

ric

tons

)(t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

)(t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

)(t

hous

ands

)

2003

23,9

00$7

6,70

020

,300

$73,

600

115,

000

$243

,000

28,0

00$1

42,0

002,

070

$1,9

40

2004

:

Aus

tral

ia8

715

774

122

127

2,49

0--

--

Bra

zil

8331

672

1,25

027

504

6169

2--

--

Can

ada

9,25

040

,400

9,55

043

,500

14,0

0044

,500

6,23

023

,800

818

934

Chi

na34

109

1,03

03,

930

472

1,30

01,

720

5,83

013

414

3

Den

mar

k(3

)17

(3)

412

467

66--

--

Fran

ce13

048

088

602

232

2,60

081

2,15

0--

--

Ger

man

y5

8756

73,

660

150

4,33

016

74,

340

5345

Hon

g K

ong

1040

2,06

09,

040

9284

019

12,

150

----

Ital

y11

446

334

247

817

049

317

----

Japa

n37

163

411

2,11

017

878

396

3,37

012

717

8

Kor

ea, R

epub

lic o

f1

1113

683

929

210

299

3,44

016

20

Mal

aysi

a21

51,

140

3433

748

384

2128

0--

--

Mex

ico

13,4

0051

,500

13,1

0039

,300

130,

000

398,

000

17,3

0092

,100

3650

Net

herl

ands

565

3936

223

509

114

3,32

015

12

Saud

i Ara

bia

271

2,52

015

9--

--15

348

7--

--

Sing

apor

e8

6118

41,

180

3919

269

1,22

05

10

Swed

en--

--10

165

1630

813

486

----

Tai

wan

5922

783

64,

100

4117

587

801

1632

Tha

iland

457

609

3,07

043

365

3536

3--

--

Uni

ted

Kin

gdom

5034

511

01,

550

5440

397

2,21

09

9

Oth

er1,

090

4,36

070

24,

890

2,08

08,

790

5,16

024

,900

212

280

Tot

al24

,800

102,

000

29,6

0012

0,00

014

8,00

046

4,00

032

,400

175,

000

1,44

01,

710

-- Z

ero.

1 Dat

a ar

e ro

unde

d to

no

mor

e th

an th

ree

sign

ific

ant d

igits

; may

not

add

to to

tals

sho

wn.

2 Tot

al r

evis

ed e

xpor

ts o

f w

ire

rod

in 2

003

wer

e 10

0,01

4 m

etri

c to

ns (

t) v

alue

d at

$19

7 m

illio

n, a

nd in

200

4, w

ire

rod

expo

rts

wer

e 12

8,53

6 t v

alue

d at

$38

9 m

illio

n.3 L

ess

than

½ u

nit.

Sour

ce:

U.S

. Cen

sus

Bur

eau,

adj

uste

d by

the

U.S

. Geo

logi

cal S

urve

y fo

r m

iscl

assi

fied

wir

e ro

d sh

ipm

ents

to M

exic

o.

21.18 U.S.GeoLoGICALSUrveyMINerALSyeArBook—2004

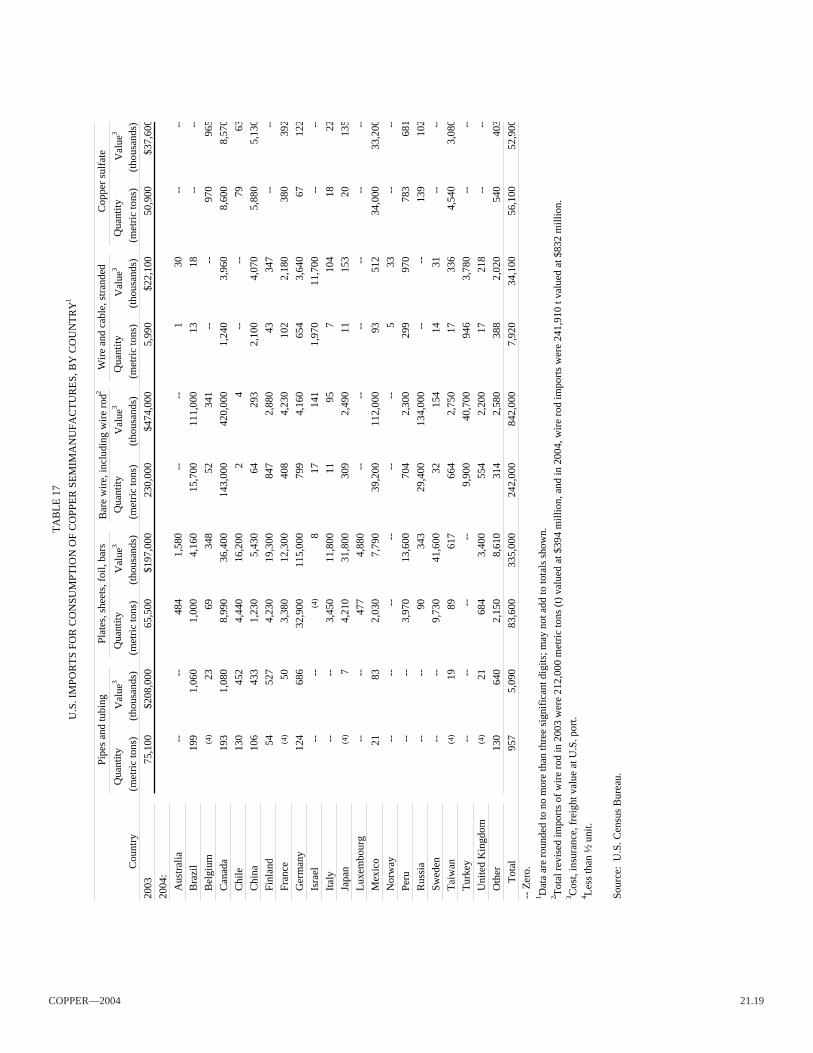

s

TA

BL

E 1

6

U.S

. IM

POR

TS

FOR

CO

NSU

MPT

ION

OF

UN

MA

NU

FAC

TU

RE

D C

OPP

ER

(C

OPP

ER

CO

NT

EN

T),

BY

CO

UN

TR

Y1

Ore

and

con

cent

rate

Mat

te, a

sh a

nd p

reci

pita

teB

liste

r an

d an

ode

Ref

ined

Una

lloye

d sc

rap

Tot

al

Qua

ntity

Val

ue2

Qua

ntity

Val

ue2

Qua

ntity

Val

ue2

Qua

ntity

Val

ue2

Qua

ntity

Val

ue2

Qua

ntity

Val

ue2

Cou

ntry

(met

ric

tons

)(t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

)(t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

)(t

hous

ands

)(m

etri

c to

ns)

(tho

usan

ds)

2003

27,1

00$1

6,60

01,

500

$2,0

3015

7,00

0$3

93,0

0088

2,00

0$1

,580

,000

19,6

00$2

4,60

01,

090,

000

$2,0

20,0

00

2004

:

Bra

zil

----

----

----

15,6

0047

,700

----

15,6

0047

,700

Can

ada

516

881

9934

875

,500

223,

000

278,

000

666,

000

6,37

013

,600

360,

000

904,

000

Chi

le--

----

--48

,900

130,

000

311,

000

875,

000

----

360,

000

1,00

0,00

0

Cos

ta R

ica

----

----

----

----

1,40

01,

260

1,40

01,

260

Dom

inic

an R

epub

lic--

----

----

----

--44

644

444

644

4

Finl

and

----

----

----

9427

2--

--94

272

Ger

man

y--

----

----

--21

,000

68,3

0048

1221

,000

68,3

00

Hon

dura

s--

----

----

----

--1,

430

1,98

014

31,

980

Japa

n--

--(3

)3

1940

4,38

015

,700

6569

54,

460

16,4

00

Mex

ico

22,4

0024

,100

206

115

8,63

029

,500

19,3

0055

,900

10,3

0013

,000

60,7

0012

3,00

0

Nam

ibia

----

----

7,71

022

,600

----

----

7,71

022

,600

Peru

----

----

10,2

0018

,300

152,

000

429,

000

5816

916

2,00

044

7,00

0

Tai

wan

----

1,33

03,

290

----

(3)

2--

--1,

330

3,29

0

Uni

ted

Kin

gdom

----

----

382

2718

055

42,

240

584

2,50

0

Oth

er--

--45

9313

976,

000

8,56

02,

770

3,61

010

,100

12,4

00

Tot

al22

,900

25,0

001,

680

3,85

015

1,00

042

3,00

080

7,00

02,

170,

000

23,4

0037

,100

1,01

0,00

02,

660,

000

-- Z

ero.

1 Dat

a ar

e ro

unde

d to

no

mor

e th

an th

ree

sign

ific

ant d

igits

; may

not

add

to to

tals

sho

wn.

2 Cos

t, in

sura

nce,

fre

ight

val

ue a

t U.S

. por

t.3 L

ess

than

½ u

nit.

Sour

ce:

U.S

. Cen

sus

Bur

eau.

Copper—2004 21.19

Qua

ntity

Val

ue3

Qua

ntity

Val

ue3

Qua

ntity

Val

ue3

Qua

ntity

Val

ue3

Qua

ntity

Val

ue3

Cou

ntry

(met

ric

tons

) (t

hous

ands

) (m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

) (t

hous

ands

) (m

etri

c to

ns)

(tho

usan

ds)

(met

ric

tons

) (t

hous

ands

)

2003

75,1

00$2

08,0

0065

,500

$197

,000

230,

000

$474

,000

5,

990

$22,

100

50,9

00$3

7,60

0

2004

:

Aus

tral

ia--

--48

41,

580

----

130

----

Bra

zil

199

1,06

01,

000

4,16

015

,700

111,

000

1318

----

Bel

gium

(4)

2369

348

5234

1--

--97

096

5

Can

ada

193

1,08

08,

990

36,4

0014

3,00

042

0,00

01,

240

3,96

08,

600

8,57

0

Chi

le13

045

24,

440

16,2

002

4--

--79

63

Chi

na10

643

31,

230

5,43

064

293

2,10

04,

070

5,88

05,

130

Finl

and

5452

74,

230

19,3

0084

72,

880

4334

7--

--

Fran