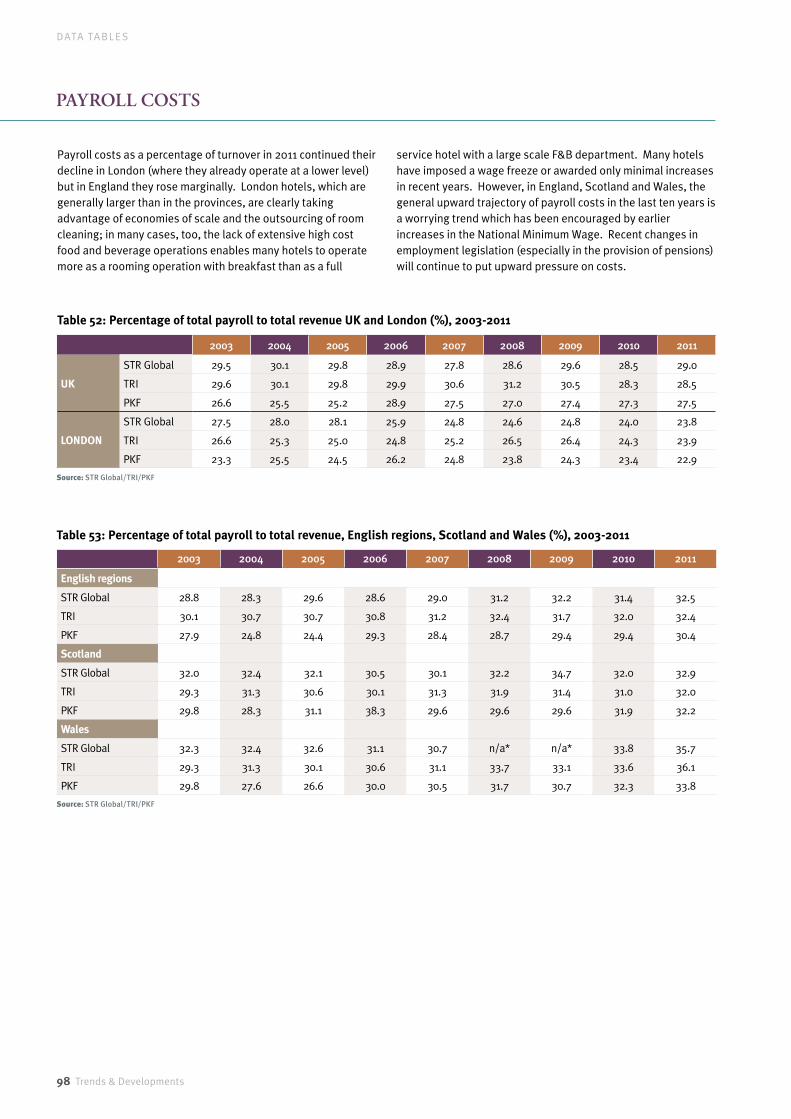

british hospitality: trends &...

TRANSCRIPT

BRitish hospitality:tRends & developments2012 REPORT

In association with

I N A SS O C I AT I O N W I T H

The association’s report – Creating Jobs in Britain: A Hospitality Economy Proposition – called on the government to work as a positive partner with the hospitality industry to realise the following objectives:

• To create 236,000 additional jobs throughout the hospitality industry by 2015.

• To make Britain a world-class destination for hospitality, tourism and business.

• To work in partnership with industry to propel hospitality’s contribution to economic recovery, rebalancing growth and the regeneration of local communities.

• To harness the knowledge and capabilities of members of the BHA to help transform the efficiency and commercialism of the public sector, without additional burdens of cost on government or industry.

BHA’s Aims And OBjEcTivEs

Compiled for the British Hospitality Association by Wordsmith and Company

Editors: Miles Quest and Diane Needham

Designed by: Creative Heads Ltd

British Hospitality Association Queens House 55-56 Lincoln’s Inn Fields London WC2A 3BH Tel: 020 7404 7744 Fax: 020 7404 7799 Email: [email protected] www.bha.org.uk

The British Hospitality Association, incorporating the Restaurant Association, the national trade association for the hotel, food service and leisure industry, celebrated its centenary in 2007. It has in membership almost every publicly quoted hotel group, many independent hotels, restaurants and clubs, major food and service management companies, motorway service operators and many local hotel associations. In total, it represents over 45,000 establishments, including 350,000 hotel rooms.

The association promotes the interests of the entire industry to government ministers, Members of Parliament and officials in Westminster, Edinburgh, Cardiff and Brussels, to other relevant organisations, the City and the media. In this capacity, it focuses on the potential impact of proposed UK and European legislation and seeks to ensure that the industry’s concerns are fully taken into account in the consultative process.

The association also aims to lead the industry towards better business practices, thus improving quality and, more specifically, to support members in order to make their businesses more efficient and more profitable.

Although every effort has been made to check the accuracy of the information in this publication, the association does not accept responsibility for any errors or omissions.

Trends & Developments 1Trends & Developments 1

3 Shaping informed operations, investment and strategic decisions UfiIbrahim,chiefexecutive,BritishHospitalityAssociation

5 Harnessing the power of the online world MarkRoper,AmericanExpress

6 TOURism

12 UK HOTEL indUsTRY

13 Economic outlook: a long and winding road back to the recovery DavidFenton,SeniorEconomist,RBSGroup

15 Total UK hotel construction exceeds £20bn in past decade MelvinGold,Consultant

18 2012 – A year of activity AndrewTaylor,HeadofLeisureforCommercialBankingatNatWestandRBS

28 Is the UK hotel industry stuck in the middle of a ‘lost decade’? JeremyHill,director,Christie+Co

31 Branding is key to hotel growth MelvinGold,consultant

36 UK cATERnG indUsTRY

37 Bright spots after a disappointing four years PeterBackman,managingdirector,Horizons

44 Eating-out continues – but few property transactions SimonChaplin,director,Christie+Co

47 PUBs

48 An undervalued sector stimulates investor attention NeilMorgan,director,Christie+Co

52 cOnFEREncEs And mEETinGs

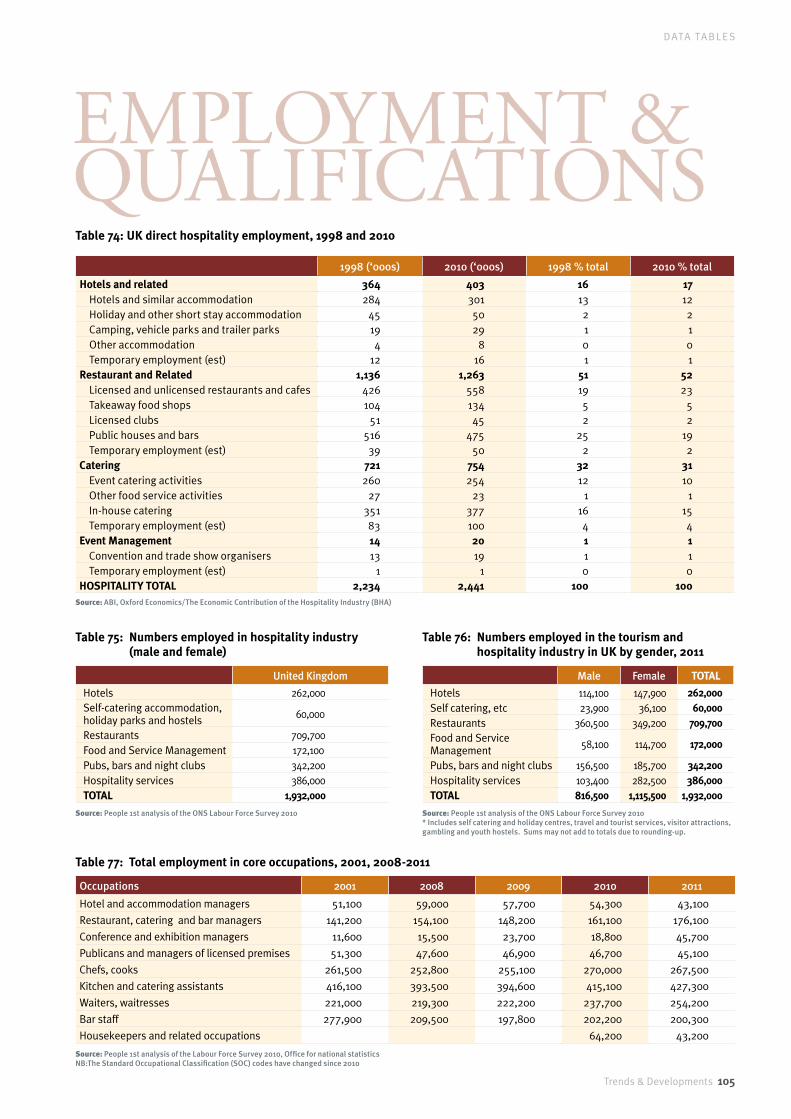

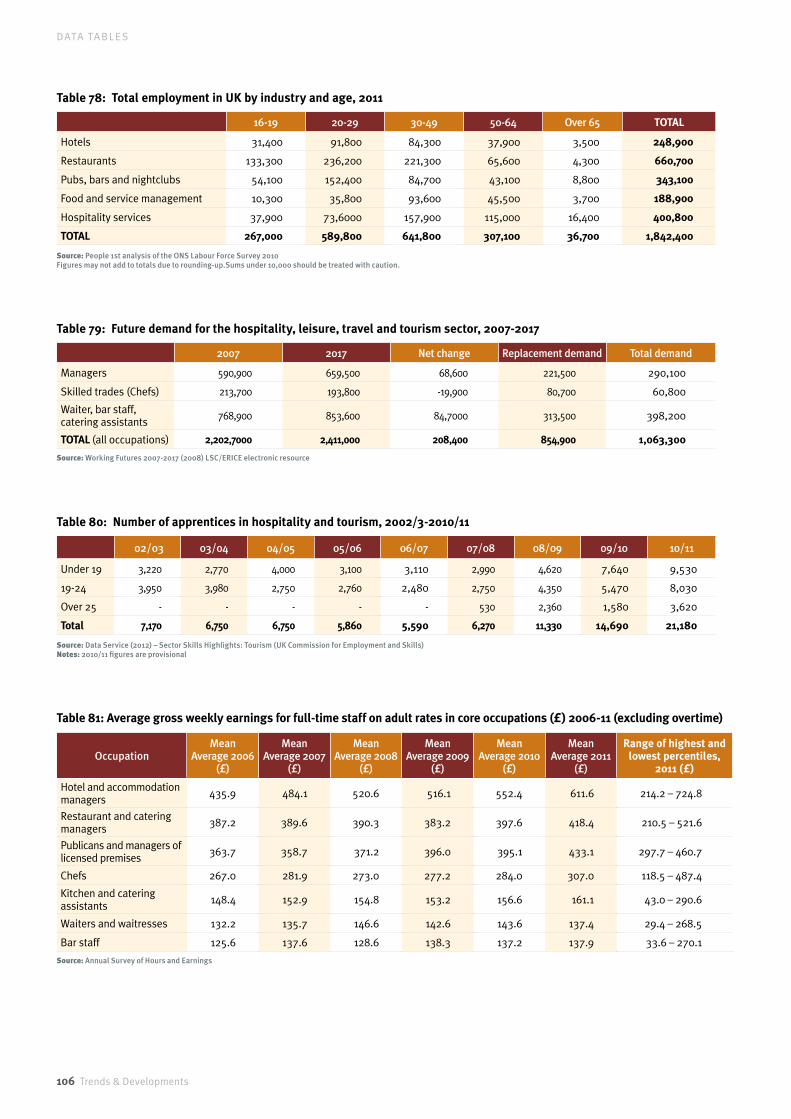

54 EmPLOYmEnT And QUALiFicATiOns

60 TimEsHARE

61 UK market strong for shared-holiday ownership product AndyMiln,regionaldirector,RCI

65 dATA TABLEs

66 Tourism: Tables1-17

71 UK hotel industry: Tables18-62

102 UK catering industry: Tables63-73

105 Employment and qualifications: Tables74-83

108 BiBLiOGRAPHY And AddREssEs

cOnTEnTs

2 Trends & Developments2 Trends & Developments

I N T RO DU C T I O N

I N T RO DU C T I O N

Trends & Developments 3Trends & Developments 3

Ufi Ibrahim, Chief Executive, British Hospitality Association

sHAPinG inFORmEd OPERATiOns, invEsTmEnT And sTRATEGic dEcisiOns

Appreciation of short, medium and long-term trends in the business environment is critical to shaping informed operations, investment and strategic decisions. Trends & Developments is the British Hospitality industry’s unique reference tool, amalgamating year-on-year data, tracking change across the restaurant, food service, accommodation, timeshare, and meetings sectors of the United Kingdom.

At the outset, I would like to express my sincere thanks to all the industry experts who contributed data, research and insights. I’d also like to underline our appreciation for the support of the sponsors of this publication – American Express, Christie & Co, Natwest and RBS. With their backing and input, this issue of Trends&Developments offers the user a comprehensive appreciation of a broader range of changes that are shaping British Hospitality.

Looking back to 2012 - an extraordinary year for the UK and for the Hospitality industry - exceptional events including the Queen’s Diamond Jubilee, and the Olympic & Paralympic Games, affected business performance at varying degrees. While not all Hospitality & Tourism related sectors saw a short term gain, there is an opportunity to reap rewards in the medium term.

By showcasing British Hospitality at its best on a global platform, coupled with the heightened visibility enjoyed by the UK during the Games and thereafter through the GREAT campaign, the UK aims to maximize the Hospitality & Tourism returns of the Olympics investment.

Fourteen million meals were served by Hospitality businesses during the Games, 70,000 Games-makers were recruited and trained, thousands of athletes and members of the Olympic family were accommodated and catered for. Some 4 billion global viewers tuned into some part of the Games, including the Olympics Closing Ceremony during which the President of the International Olympic Committee praised British Hospitality for our outstanding welcome and service.

There is no doubt that British Hospitality is world leading in many regards, and increasingly the world’s attention turns not only to what, but also how our industry responds to major events, evolving consumer behavior, the digital revolution, branding, as well as the development of talent and skills. As our industry context becomes more complex, so too will the challenge of staying ahead of the curve. The role of information, and the effective application of this intelligence will become even more critical in advancing competitive growth.

2012 also recorded a breakthrough in the number of international arrivals worldwide which reached 1 billion for the first time in history. The UNWTO forecasts continued growth, averaging some 43 million additional international trips per year. Much of this growth emanates from the rising incomes per capita in emerging economies. The more wealth people have, the more they want travel and enjoy the hospitality offered by international destinations. This trend bodes well for our industry in the UK. There is a real opportunity for export-led growth, which in turn can create new jobs and economic growth across the entire UK.

However, growth cannot be taken for granted. Just as businesses must become more responsive and effective in tackling change in a competitive and complex global market, so too must government. Public policy can make or break the ambition of our industry to generate employment and prosperity across the UK.

Over the past year, the British Hospitality industry rose above several challenges, not least the sluggish economy and continued squeeze on real household disposable incomes. Public expenditure cuts affected government spend on meetings and conferences, while uncertainty impacted on some B-to-B markets.

In his recent budget statement (5 December 2012), the UK Chancellor of the Exchequer warned that the ‘period of austerity’ was expected to continue to 2015. The Treasury appears to be unwavering on efforts to tackle the budget deficit and to reduce the size of the state. Sound policy decisions are dependent on evidence, intelligence and understanding of the consequences on UK plc.

The BHA is the authority on British Hospitality, and we are committed to delivering much needed research, and ensuring that businesses, investors and policy-makers, may be equipped with the facts necessary to make informed decisions to unlock Hospitality’s potential to create 475,000 jobs by 2020.

4 Trends & Developments4 Trends & Developments

I N T RO DU C T I O N

I N T RO DU C T I O N

Trends & Developments 5Trends & Developments 5

by Mark Roper, Vice President & General Manager, UK Merchant Services at American Express

HARnEssinG THE POwER OF THE OnLinE wORLd

The past few years have been notable for the speed at which technology has shaped and changed our industry, and 2012 has been no exception. Social media, online marketing and digital partnerships continue to take precedence as merchants look to communicate with their customers on a much larger scale, in newer and more innovative ways.

Whilst the advent of these new forms of communication might initially seem overwhelming we need to recognise that they’re here to stay – and we need to work out how we’re going to make the most of the possibilities that they offer. Some parts of the industry have already embraced the opportunity: exciting partnerships between businesses in the sector are thriving, and the prospect of a much larger online audience is proving difficult to ignore.

Over the past few years, social media has become an increasingly important part of our lives, especially for Generation Y who look to their social networks to remain connected at all times. Bloggers have become a widely-read and well-respected source of information for everything from holiday destinations to the latest restaurant openings; Twitter provides a channel for people to share their recommendations and experiences with one another instantly.

These new forms of communication have the power to revolutionise the way we all do business.

As a result, those in the hospitality industry have a new medium through which to attract and service customers, by being able to receive and manage bookings online, facilitating global bookings with an unprecedented level of simplicity for the customer. Online channels provide a golden opportunity to small merchants, who might not have resources for expensive marketing campaigns, to get their message across to a wider audience than traditional marketing mediums; and big and small companies alike are able to engage more efficiently and effectively with their customers.

American Express is continuing to focus on partnerships and has embraced innovative digital ventures delivering value to merchants though Cardmember spend in 2012.

One example is our partnership with FourSquare. This innovative new collaboration in the UK offers our Cardmembers exclusive location-based deals with a variety of businesses

across the country, including some of the best-known restaurant chains.

Realise the Potential London, an online magazine and iPhone & iPad app, was launched in Q2 2012 to help local and visiting Cardmembers make the most of their time in London. With compelling information and merchant offers, the campaign enabled businesses to be promoted to local Londoners, incoming tourists and business travellers.

For our partners in the restaurant sector, we’ve continued our support of Top Treats in partnership with Toptable, as well as the London Restaurant Festival to drive awareness and footfall to some of the capital’s most exciting restaurants. Rewarding Cardmembers for restaurant spend has encouraged them to dine out and dine out more frequently, visiting personal favorites and trying something new.

Social media enables American Express to bring our support of the industry, and the partnerships, to a much wider audience. Through online channels, we’re able to communicate these opportunities to both our merchants and our Cardmembers.

As we head into 2013 and beyond, and the influence of digital and social media increases even further, ways of working together to harness the power of the online world will become increasingly significant. Social media has made its presence felt in the hospitality industry, and it’s undoubtedly here to stay. With the enormous potential that the digital sphere has to revolutionise the way we all do business, embracing these times of change and making use of strong partnerships and innovations will help us all make the most of the opportunities at our fingertips.

We’re very pleased, once again, to sponsor BritishHospitality:TrendsandDevelopments. The BHA provides important support and insight throughout the year to those of us working in the hospitality industry, and this report continues to be vital reading as we plan for the year ahead.

6 Trends & Developments

TO U RISM

touRism

Trends & Developments 7

TO U RISM

Recovery has come at different speeds – stronger in emerging economies (up eight per cent) than in developed economies (up five per cent). This recovery is continuing into 2012 with international tourist arrivals growing by five per cent in the first half of 2012 to 467m and on track to reach one billion tourists by the end of the year.

The majority of destinations that had not exceeded pre-crisis levels in 2010 did so in 2011. Contrary to the long-term trend, advanced economies (+4.9 per cent) posted higher growth than emerging economies (+4.3 per cent) due largely to strong growth in Europe and the setbacks in the Middle East and North Africa.

The annual average growth rate of over four per cent in the number of travellers between 1970 and 2000 is forecast to moderate in the period 2010-2030, with the number of international tourist arrivals worldwide rising by an average 3.3 per cent per year. As a result, an average of 43m additional international tourists will join the tourism marketplace every year.

International tourism receipts continued their recovery in 2011, reflecting the increase in arrivals during the year, reaching a record US$1 trillion for the first time. Growth is estimated at 3.9 per cent in 2011, measured in real terms. By region, the Americas (+5.7 per cent) recorded the largest increase followed by Europe (+5.2 per cent), Asia and the Pacific (+4.4 per cent) and Africa (+2.2 per cent). The Middle East was the only region posting negative growth (-14 per cent).

In 2011, Europe attracted 51.3 per cent of tourism arrivals but 45 per cent of tourism expenditure in 2011 – up 6.2 per cent on 2010.

The rise of China as a tourist destination is noticeable. Having overtaken both the UK and Italy in recent years in terms of arrivals, it has now overtaken Spain to third place, while it is fourth in terms of receipts. If Hong Kong and Macao were included, China would be second only to the USA in terms of receipts, and third (after USA and France) in terms of arrivals.

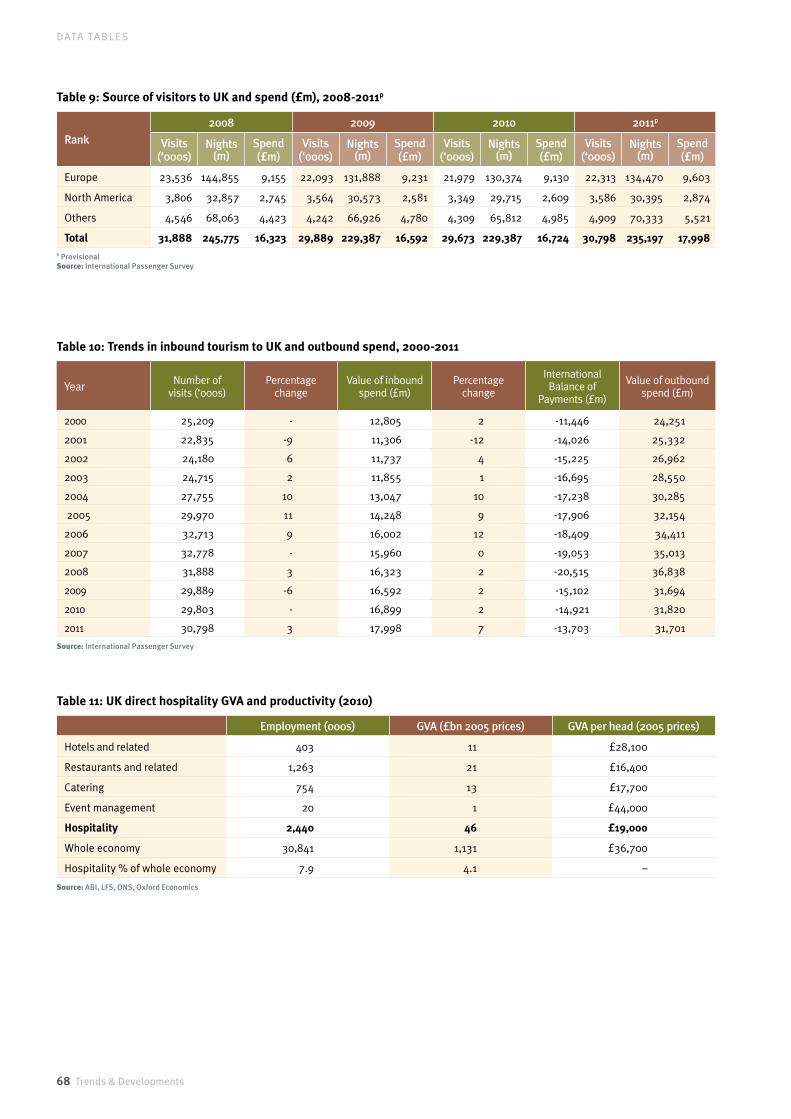

(Tables1-4,page66)

In 2011, world tourism continued to rebound from the setbacks of 2008/2009. In 2009 the number of international arrivals fell back to just above 2006 levels, dropping by 4.2 per cent with receipts falling by 9.5 per cent. A strong rebound in 2010 – up 6.6 per cent on 2009 figures – saw arrivals reach a record 940m, which again increased in 2011 by 4.6 per cent to reach a further record of 983m with receipts more than US$1 trillion in 2011.

wORLd TOURism GROws APAcE

43m additional international tourists will join the tourism marketplace every year.

1990

451 million

983 million

2011

118% increase

International tourist arrivals

Growth rate in 2011

4.6%

$1 trillionInternational arrival receipts in 2011

TO U RISM

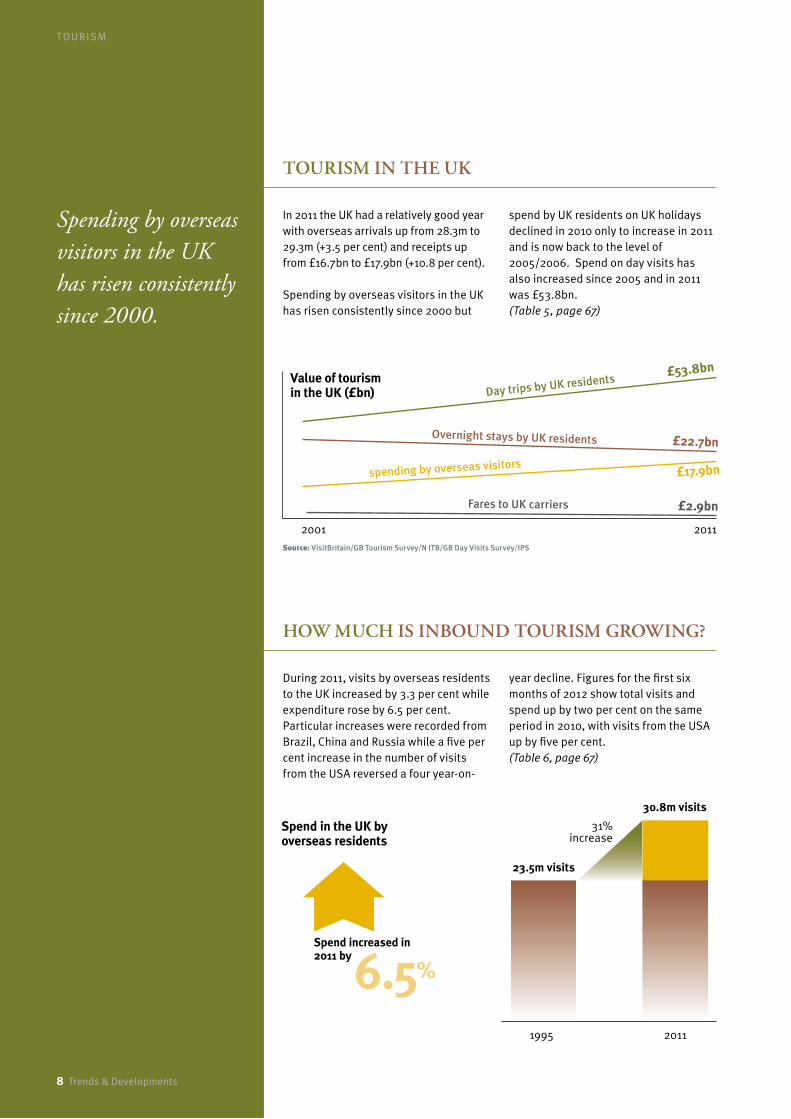

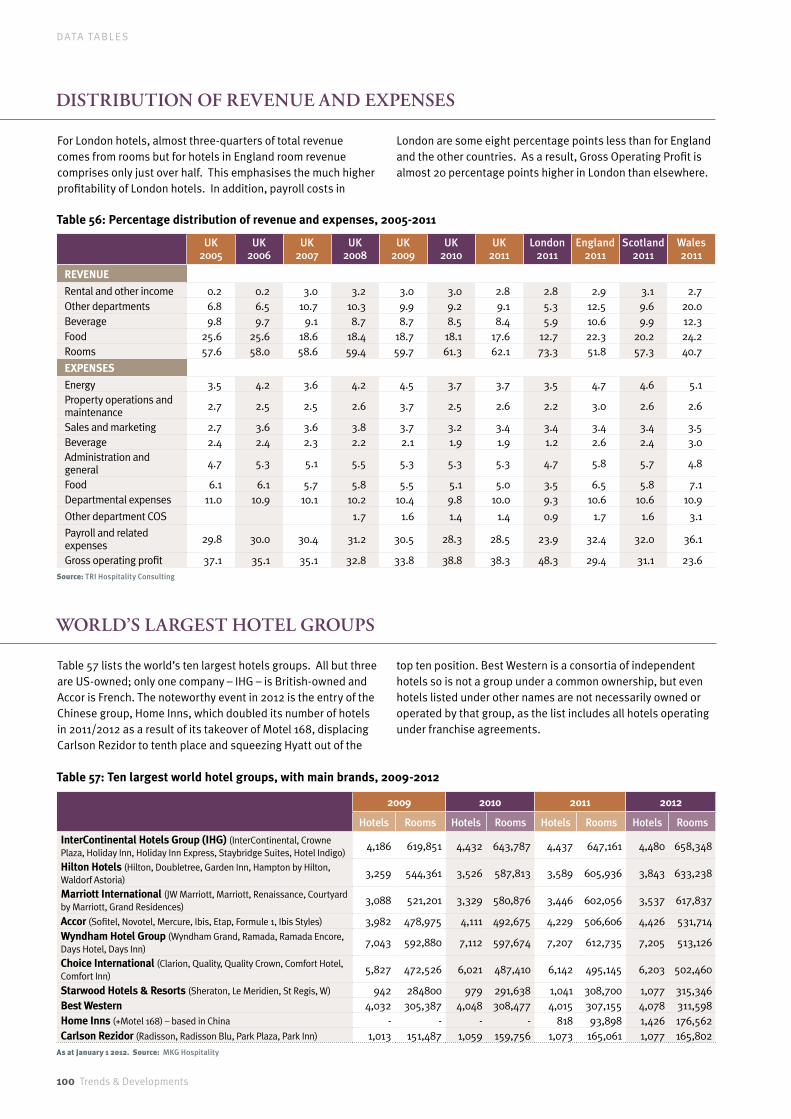

Spending by overseas visitors in the UK has risen consistently since 2000.

TOURism in THE UK

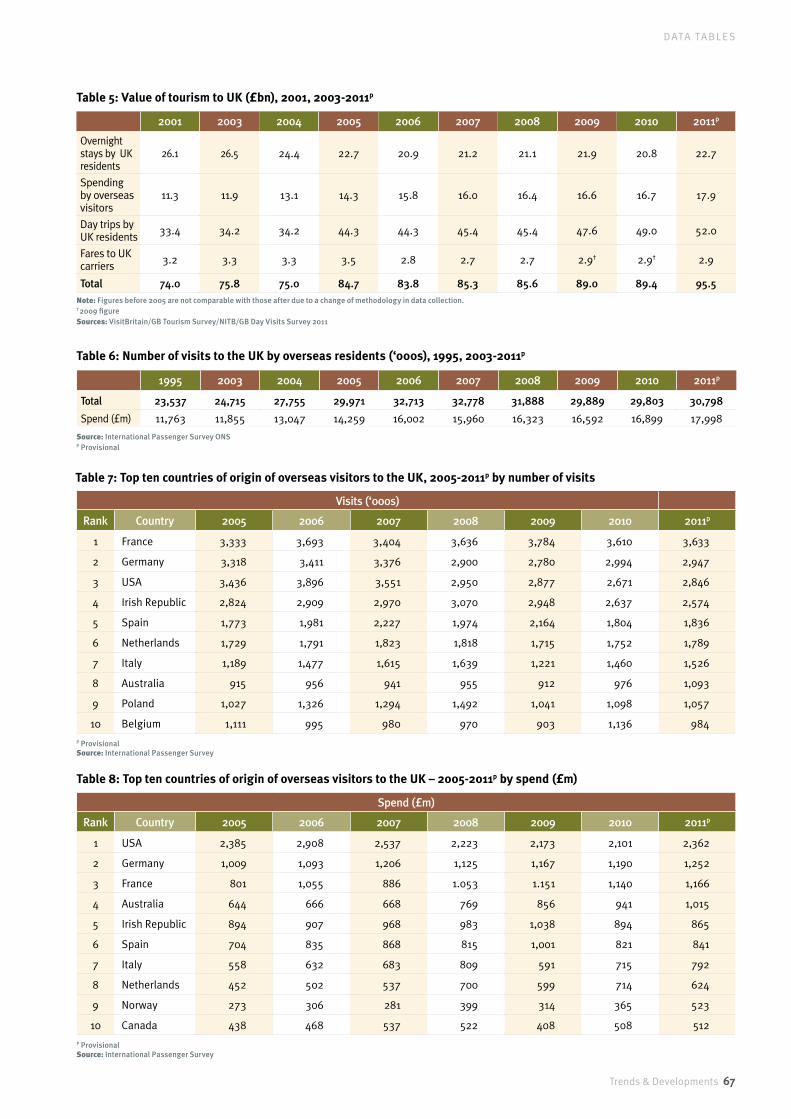

In 2011 the UK had a relatively good year with overseas arrivals up from 28.3m to 29.3m (+3.5 per cent) and receipts up from £16.7bn to £17.9bn (+10.8 per cent). Spending by overseas visitors in the UK has risen consistently since 2000 but

spend by UK residents on UK holidays declined in 2010 only to increase in 2011 and is now back to the level of 2005/2006. Spend on day visits has also increased since 2005 and in 2011 was £53.8bn.(Table5,page67)

1995

23.5m visits

2011

30.8m visits

6.5%Spend increased in 2011 by

HOw mUcH is inBOUnd TOURism GROwinG?

During 2011, visits by overseas residents to the UK increased by 3.3 per cent while expenditure rose by 6.5 per cent. Particular increases were recorded from Brazil, China and Russia while a five per cent increase in the number of visits from the USA reversed a four year-on-

year decline. Figures for the first six months of 2012 show total visits and spend up by two per cent on the same period in 2010, with visits from the USA up by five per cent. (Table6,page67)

2001

spending by overseas visitors

Overnight stays by UK residents

Fares to UK carriers

2011

£17.9bn

£22.7bn

£2.9bn

Day trips by UK residents£53.8bn

Value of tourism in the UK (£bn)

31% increase

Spend in the UK by overseas residents

8 Trends & Developments

Source: VisitBritain/GB Tourism Survey/N ITB/GB Day Visits Survey/IPS

Trends & Developments 9

TO U RISM

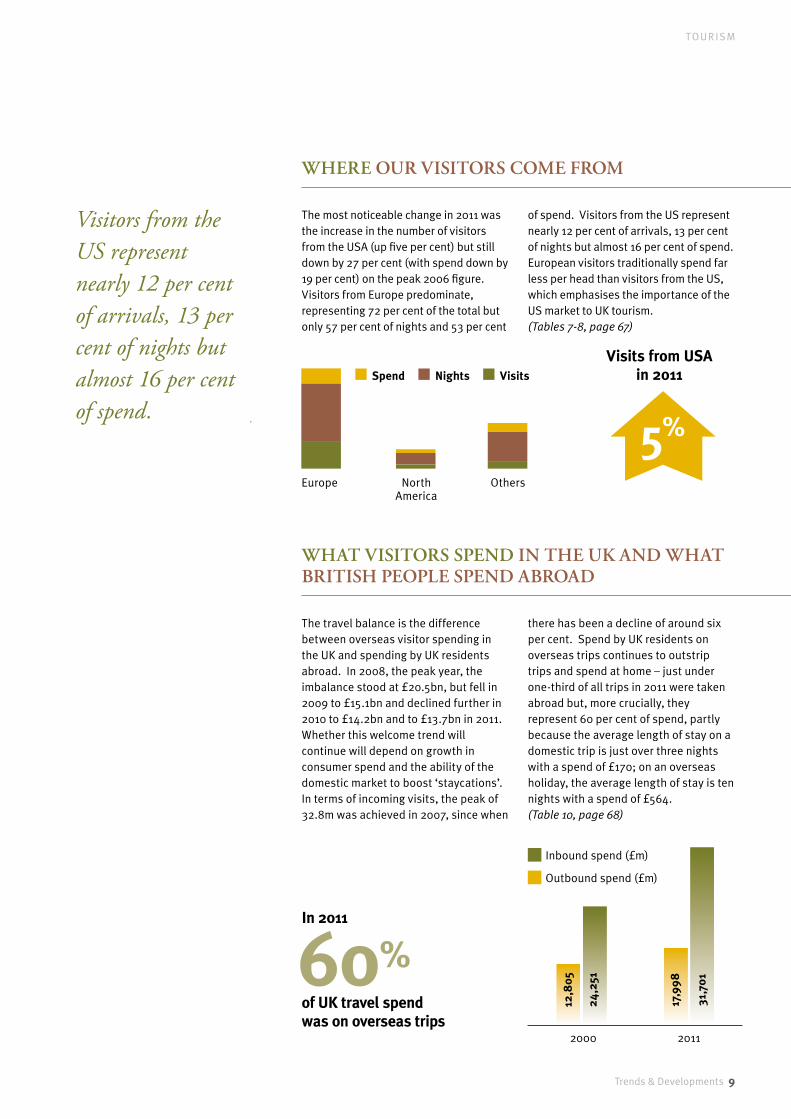

Visitors from the US represent nearly 12 per cent of arrivals, 13 per cent of nights but almost 16 per cent of spend.

wHERE OUR visiTORs cOmE FROm

The most noticeable change in 2011 was the increase in the number of visitors from the USA (up five per cent) but still down by 27 per cent (with spend down by 19 per cent) on the peak 2006 figure. Visitors from Europe predominate, representing 72 per cent of the total but only 57 per cent of nights and 53 per cent

of spend. Visitors from the US represent nearly 12 per cent of arrivals, 13 per cent of nights but almost 16 per cent of spend. European visitors traditionally spend far less per head than visitors from the US, which emphasises the importance of the US market to UK tourism.(Tables7-8,page67)

wHAT visiTORs sPEnd in THE UK And wHAT BRiTisH PEOPLE sPEnd ABROAd

The travel balance is the difference between overseas visitor spending in the UK and spending by UK residents abroad. In 2008, the peak year, the imbalance stood at £20.5bn, but fell in 2009 to £15.1bn and declined further in 2010 to £14.2bn and to £13.7bn in 2011. Whether this welcome trend will continue will depend on growth in consumer spend and the ability of the domestic market to boost ‘staycations’. In terms of incoming visits, the peak of 32.8m was achieved in 2007, since when

there has been a decline of around six per cent. Spend by UK residents on overseas trips continues to outstrip trips and spend at home – just under one-third of all trips in 2011 were taken abroad but, more crucially, they represent 60 per cent of spend, partly because the average length of stay on a domestic trip is just over three nights with a spend of £170; on an overseas holiday, the average length of stay is ten nights with a spend of £564.(Table10,page68)

Visits from USA in 2011

2000

Europe North America

Others

Spend Nights Visits

2011

12,8

05

24,2

51

17,9

98

31,7

0160%of UK travel spend was on overseas trips

In 2011

5%

Inbound spend (£m)

Outbound spend (£m)

10 Trends & Developments

TO U RISM

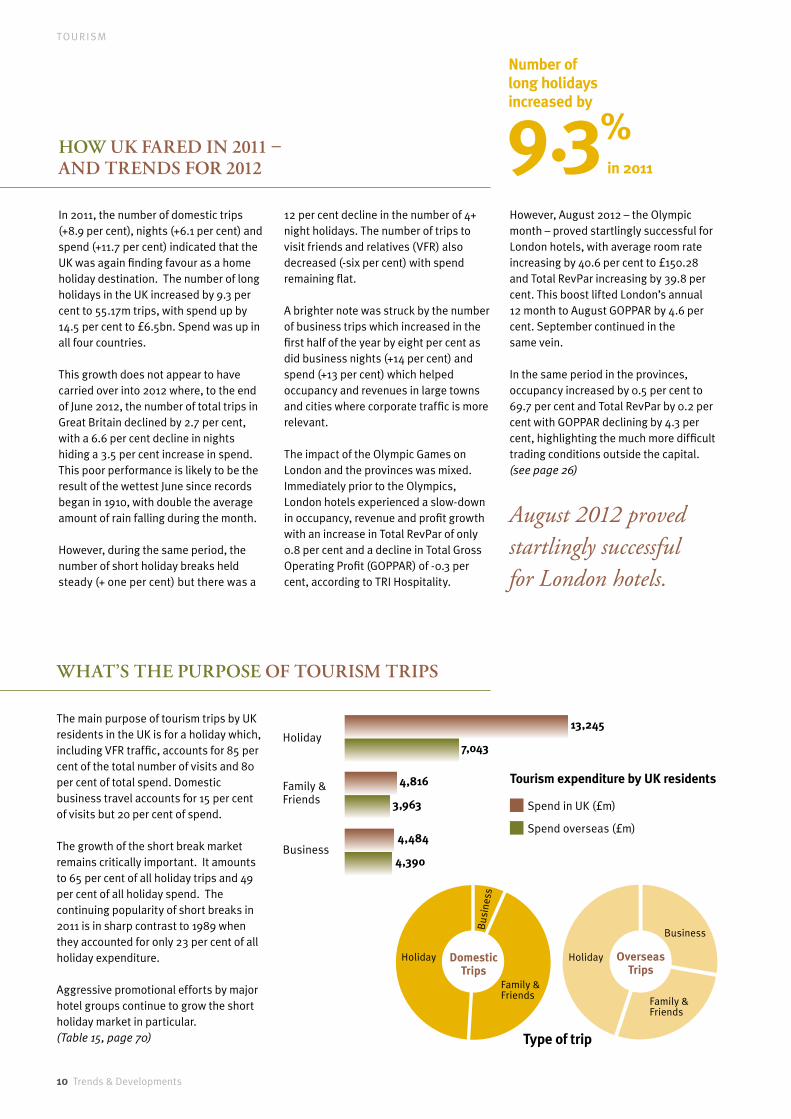

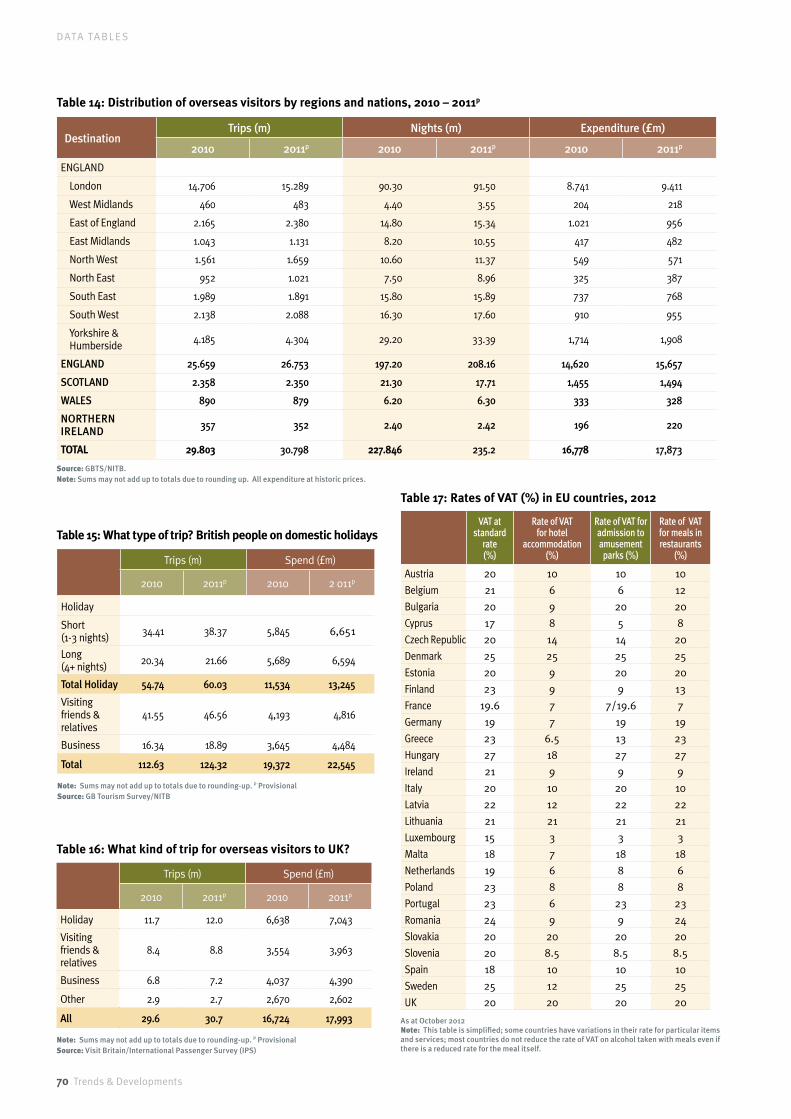

The main purpose of tourism trips by UK residents in the UK is for a holiday which, including VFR traffic, accounts for 85 per cent of the total number of visits and 80 per cent of total spend. Domestic business travel accounts for 15 per cent of visits but 20 per cent of spend.

The growth of the short break market remains critically important. It amounts to 65 per cent of all holiday trips and 49 per cent of all holiday spend. The continuing popularity of short breaks in 2011 is in sharp contrast to 1989 when they accounted for only 23 per cent of all holiday expenditure.

Aggressive promotional efforts by major hotel groups continue to grow the short holiday market in particular. (Table15,page70)

HOw UK FAREd in 2011 – And TREnds FOR 2012

In 2011, the number of domestic trips (+8.9 per cent), nights (+6.1 per cent) and spend (+11.7 per cent) indicated that the UK was again finding favour as a home holiday destination. The number of long holidays in the UK increased by 9.3 per cent to 55.17m trips, with spend up by 14.5 per cent to £6.5bn. Spend was up in all four countries.

This growth does not appear to have carried over into 2012 where, to the end of June 2012, the number of total trips in Great Britain declined by 2.7 per cent, with a 6.6 per cent decline in nights hiding a 3.5 per cent increase in spend. This poor performance is likely to be the result of the wettest June since records began in 1910, with double the average amount of rain falling during the month.

However, during the same period, the number of short holiday breaks held steady (+ one per cent) but there was a

12 per cent decline in the number of 4+ night holidays. The number of trips to visit friends and relatives (VFR) also decreased (-six per cent) with spend remaining flat.

A brighter note was struck by the number of business trips which increased in the first half of the year by eight per cent as did business nights (+14 per cent) and spend (+13 per cent) which helped occupancy and revenues in large towns and cities where corporate traffic is more relevant.

The impact of the Olympic Games on London and the provinces was mixed. Immediately prior to the Olympics, London hotels experienced a slow-down in occupancy, revenue and profit growth with an increase in Total RevPar of only 0.8 per cent and a decline in Total Gross Operating Profit (GOPPAR) of -0.3 per cent, according to TRI Hospitality.

However, August 2012 – the Olympic month – proved startlingly successful for London hotels, with average room rate increasing by 40.6 per cent to £150.28 and Total RevPar increasing by 39.8 per cent. This boost lifted London’s annual 12 month to August GOPPAR by 4.6 per cent. September continued in the same vein.

In the same period in the provinces, occupancy increased by 0.5 per cent to 69.7 per cent and Total RevPar by 0.2 per cent with GOPPAR declining by 4.3 per cent, highlighting the much more difficult trading conditions outside the capital.(seepage26)

wHAT’s THE PURPOsE OF TOURism TRiPs

Holiday

Family & Friends

Business

13,245

7,043

4,816

3,963

4,484

4,390

Spend in UK (£m)

Spend overseas (£m)

OverseasTrips

Holiday

Family & Friends

Business

Holiday

Family & Friends

Bus

ines

s

DomesticTrips

9.3%in 2011

Number of long holidays increased by

Type of trip

Tourism expenditure by UK residents

August 2012 proved startlingly successful for London hotels.

I N T RO DU C T I O NTO U RISM

Trends & Developments 11

UK REsidEnTs And visiTORs: wHERE THEY sTAY, HOw mUcH THEY sPEnd

TOTAL vALUE OF UK TOURism And LEisURE indUsTRY

vAT – And HOw THE UK is UncOmPETiTivE

In 2011, the south west, south east and north west remained the most popular regions of the country for domestic visitors in terms of trips, nights and spend, although London still earns £2.4bn from domestic visitors. The distribution of overseas visitors to Britain is markedly

different. London is by far the favourite destination and accounted for 53 per cent of all their expenditure (£9.4bn), followed, distantly, by the south east of England and Scotland.

(Table13,page69)

In 2011, the value of the total tourism and leisure industry increased by 2.2 per cent to £113.5 bn. Our definition of the industry includes all forms of catering, serviced and self-catering accommodation, food and drink consumed away from home, shopping on holiday, sports, gambling and domestic air travel (but not other transport costs associated with UK holidays).

Drinking accounts for about one-third of the market as does eating-out and overnight accommodation combined. But the strength of the sector is also demonstrated by the range of other significant activities, such as gambling and shopping, that form a part of this important sector of the UK economy.

(Table12,page69)

The rate of VAT varies throughout the EU but, more significantly for the hospitality industry, all but four countries – Denmark, Lithuania, Slovakia and the UK – provide a reduced rate for hotel accommodation and many have a reduced rate for meals and attractions. These include the UK’s key European competitors – France, Spain and Italy.

Lower rates in the EU disadvantage UK tourism, making it uncompetitive with the rest of Europe; a reduced rate would also encourage lower prices and greater consumer demand, thus creating more jobs. Tourism is the only export on which the UK government imposes a domestic tax.

Despite the economic recession, few countries have significantly increased

their rate of VAT on hospitality services, which appears to recognise the price sensitivity of world tourism and the need for countries to support their tourist industry.

In 2011, Greece increased VAT for restaurant meals from 13 per cent to 23 per cent while in 2012 France raised its rate from 5.5 per cent to seven per cent for hotel accommodation and restaurant meals; in the same year the Czech Republic increased the rate for hotel accommodation from 10 per cent to 14 per cent, Portugal raised the VAT level for restaurant meals from 13 to 23 per cent (but retained its six per cent rate for hotel accommodation) and Sweden actually reduced its VAT rate for meals from 25 per cent to 12 per cent.(Table17,page70)

VAT rate for Hotel Accommodation

20%

9.7%

VAT rate for Amusement

Parks

20%

14.8

%

VAT rate for Restaurant

Meals

20%

15.3

%

Average VAT rate in Europe

VAT rate in UK

11.8 £billionValue of tourism to London in 2011

Value of the tourism and leisure industry

in 2011 increased

to £113.5 bn

2.2%

Trends & Developments 11

12 Trends & Developments

H OT E L I N DUS T RY

hotel industRy

Trends & Developments 13

H OT E L I N DUS T RY

Is 2012 a turning point? David Fenton, Senior Economist, RBS Group, says that there is still a long and winding road ahead.

Let’s start with the good news:

the UK came out of its double-dip recession in Q3 2012, with the strongest growth since 2007 (+1.0 per cent q/q). As well as some truly unforgettable moments, the Olympics and Paralympics also delivered a boost to economic activity, across many sectors – including hospitality. Hotels showed greater

activity in Q3, according to National Statistics, albeit mainly in London. This continues an encouraging trend, which has seen the hospitality sector comfortably outperform the wider economy over the last couple of years.

Even so, let’s not get carried away. Economic growth was still flat in year-on-year terms in Q3, and another contraction in Q4 cannot be ruled out. The bottom line is that even if the UK economy has moved out of intensive care, it is to the high-dependency unit, and only an incurable optimist would expect a speedy recovery in 2013.

EcOnOmic OUTLOOK: A LOnG And windinG ROAd BAcK TO THE REcOvERY

by David Fenton, Senior Economist, RBS Group

KEY UncERTAinTiEs in THE GLOBAL EcOnOmY...

Looking forward, the outlook depends crucially on what happens in the global economy. That’s not because conditions at home don’t matter; far from it. Consumer spending accounts for almost half of final demand, and will be vital to the prospects for the hotel sector. But the fact is that a sustainable recovery in the UK requires a rebalancing of growth towards exports and investment. That seems almost impossible in the current environment.

There are two key uncertainties in the global economy: the US “fiscal cliff” and European debt crisis.

Of the two, the fiscal cliff is the more pressing. So pressing, in fact, that we will know the outcome by the time you read this. The fiscal cliff refers to a set of tax hikes and spending cuts, scheduled to come into effect on 1 January 2013, that would be big enough to tip the US economy back into recession. The UK

wouldn’t escape either: the global after-shock would probably be big enough to shave up to one per cent point off UK growth, according to the IMF. For an economy that’s currently flat in year-on-year terms, that could be enough to trigger a “treble dip” in 2013.

Our hope and expectation is that, by the time you read this, Congress will have done a deal. But even if the US steps back from the brink, the fiscal position will remain precarious and a source of uncertainty unless a credible plan to balance the books in the medium term has also been agreed.

If the fiscal cliff is the most pressing risk, the European debt crisis is the most worrying. Collectively, the euro area countries are the UK’s biggest trading partner and provide around half of overseas visitors, according to the International Passenger Survey.

Recent steps by the European Central Bank (ECB) have provided some welcome respite for countries like Spain and Italy. But the ECB cannot fix the crisis by itself. A sustainable solution could take many forms, including euro bonds and a banking union, which will ultimately see members acting more like a single country than a bunch of countries that happen to sit on the same continent.

Forging a stronger union won’t be easy. Germans are worried about the costs of bailing out governments in other countries, which is likely to be a key issue in the 2013 election. Meanwhile, opposition to austerity is growing in “peripheral” countries, as evidenced by strikes and violent protests in Spain and Portugal. Whatever happens, I think we can confidently predict that the European debt crisis will remain a key uncertainty for the UK in 2013.

14 Trends & Developments

H OT E L I N DUS T RY

...And cLOsER TO HOmE

PUTTinG iT ALL TOGETHER

As if that’s not enough, the UK also has plenty of home-grown uncertainties to contend with. For example, fiscal austerity has still got a long way to run. Of spending cuts, 88 per cent had yet to come into effect as of April 2012, according to the Institute for Fiscal Studies. And the debate about the effect of these cuts on the wider economy remains unsettled.

Recent research by the IMF suggested that so-called “fiscal multipliers” might be much higher than previous estimates (fiscal multipliers measure the effect of a tax or spending change on the wider economy). If so, austerity would be more costly. The key take-away from all of this

is that the public finances will continue to cast a shadow over the economic outlook.

Finally, it’s worth mentioning the rate of inflation. Consumer price inflation fell back in 2012, but was still higher than expected, higher than the two per cent target and – crucially – higher than growth in average earnings. This leaves consumers facing the toughest squeeze on real take-home pay for 30 years. ‘Short breaks’ has been one of the main areas where consumers are making cutbacks, according to the Deloitte Consumer Tracker, though the pressure has eased over the past year.

So where does all of this leave us?

Most economists – including us – expect 2013 to be a better year than 2012: +1.3 per cent from -0.1 per cent, according to Consensus Forecasts in November. Given that the hospitality sector is closely correlated with UK GDP, that should lead to an improvement in key metrics like RevPar.

Nevertheless, that would represent another sub-par performance for the UK economy, with expectations for 2014 also subdued. When it comes to the UK economy’s direction of travel, it would appear that the best we can hope for is a long and winding road back to recovery.

Most economists expect 2013 to be a better year than 2012: +1.3 per cent from -0.1 per cent.

88% of spending cuts have yet to come into effect as of April 2012

Public finances will continue to cast a shadow over the economic outlook.

Trends & Developments 15

H OT E L I N DUS T RY

TOTAL UK HOTEL cOnsTRUcTiOn ExcEEds £20bn in PAsT dEcAdE

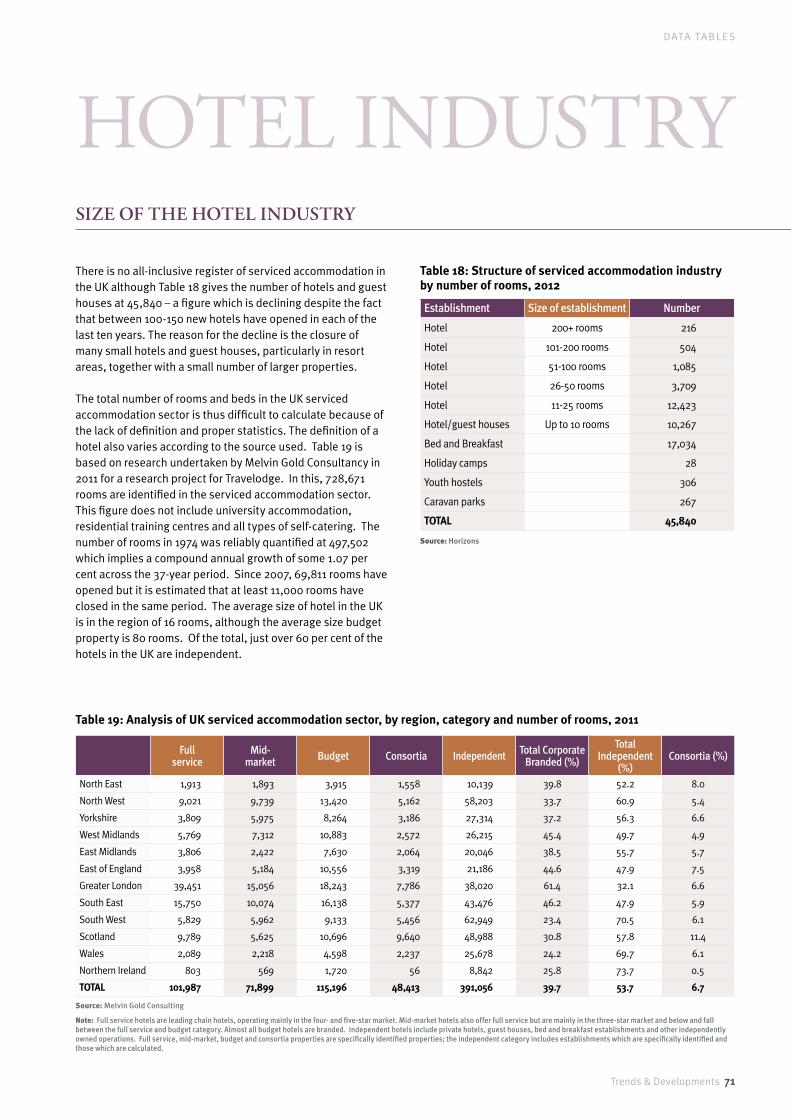

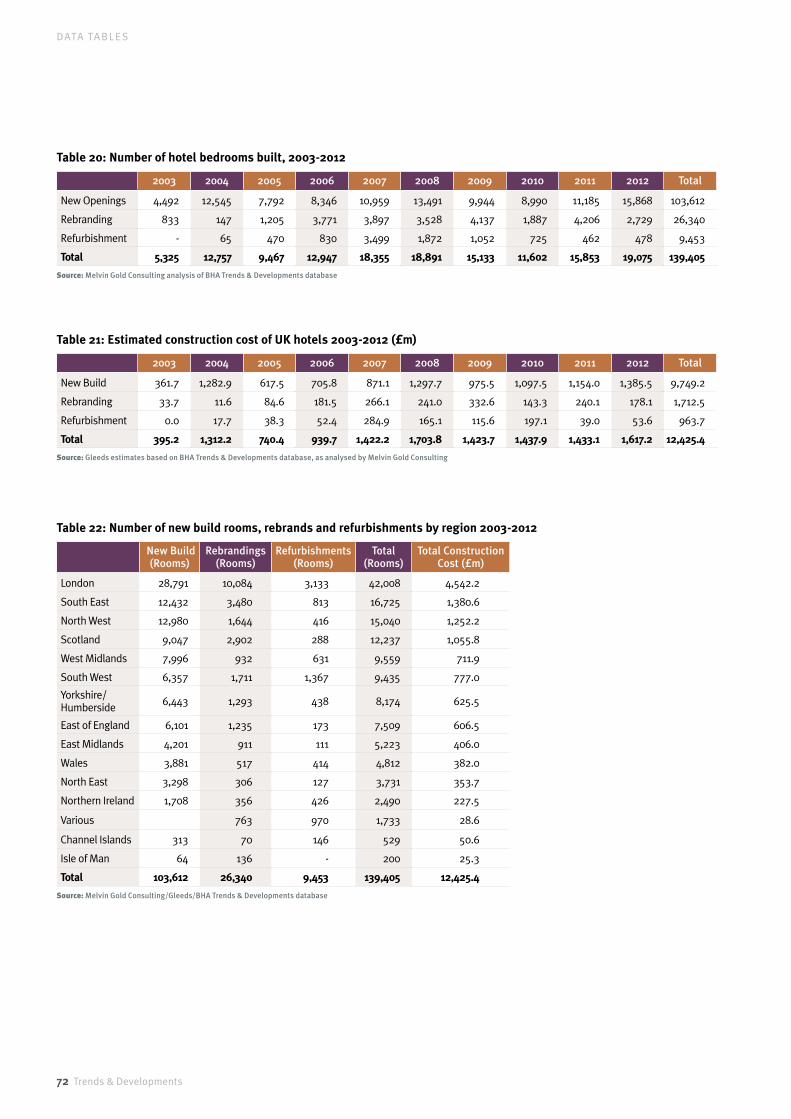

Over 100,000 new hotel rooms have been built in the UK in the last decade, plus extensive refurbishment in leading properties and rebrandings. With total investment at well over £20bn, the industry is a key player in the UK economy.

How much has been spent building all these new hotel rooms in the UK over the past decade? Using the listing that, for well over a decade this publication has annually published, and collaborating with Gleeds, I have sought to answer that question. Although there are almost certainly some omissions in this publication’s database, it is the most comprehensive available.

From that excellent start we incorporated into the database the ability to analyse the database by brand, by region and by city as well as by the number of bedrooms.

Gleeds then took the database and incorporated construction costs on a consistent basis, taking due account of location, brand and size of hotel. They also adjusted for timing so that the end value reflects what it would have been had all construction taken place in Quarter 4 of 2012. Of course the resulting estimate is broad, so there is a risk of incompleteness or inaccuracy, but it does provide a sound basis to estimate the construction worth of the UK hotel sector over the period.

As the table on page 16 shows, the database tracks 103,612 rooms (in 983 hotels) that opened between 2003 and 2012, 26,340 (219 hotels) that have switched brands and a further 9,453 (96 hotels) that have undergone significant refurbishment. In the case of rebranding a level of capital expenditure is assumed to be spent to bring a hotel to the new brand standards when it changes brand.

This does not always amount to a full refurbishment but is usually more than simply changing the signage and costs have been estimated on a suitable basis.

It also depicts the development cycle: the highest level of new openings will be this year (2012), largely due to the Olympics. 43.3 per cent of newly opened rooms were in London. Prior to that, the peak year was in 2008, followed by 2004, 2007 and 2011.

It is a reminder that so frequently the hotel development cycle is mis-aligned with the economic cycle: the development and build period is long, and much happens in the economy from conception to opening. In recent years and, indeed, currently, it has been hard to find bank funding for new developments. Thus, in the coming years, the pace of hotel openings will most likely slow (but not stop entirely) yet the cycle will resume again and chances are that the peak number of new openings will once again align with the top of the cycle.

Using Gleeds analysis of the database we are also able to express this in financial terms which is illustrated in the following table and shows an overall estimated construction cost of £12.4bn, predominantly in new build hotels (including conversion to hotel use of existing buildings). In seven of the ten years, the construction value of completed projects in the sector exceeded £1bn, the peak in this case being in 2008 when value exceeded £1.7bn. The Olympic Year fell only slightly short of that level.

This estimate of cost takes account only of construction cost, including fit-out. It excludes the professional fees which might be up to 10 per cent of total project cost for budget and midscale properties, or 15 per cent for full service or upscale properties with a larger interior design element. The value of the land on which the hotel stands can also vary significantly and might range from 20-100 per cent of construction cost.

Thus the overall economic impact of hotel development in the UK is well beyond the £12.4bn of construction value that we estimate here; it probably stretches beyond £20bn over the past decade although it is not possible to quantify accurately.

by Melvin Gold, Hotel Industry Consultant (in collaboration with Steve Lacey, Director, Gleeds)

20 £billiontotal investment in the last decade

2003 2012

Refurbishment (Total 9,543)– 478

Rebranding (Total 26,340)

8332,729

New openings (Total 103,612)15,868

4,492

Number of bedrooms built Average number of bedrooms

built per annum 2003-2012

8,634

H OT E L I N DUS T RY

Almost certainly these figures are understated, especially for refurbishments. They include only the most significant of these, and even then only the construction elements omitting professional fees etc. Also under the radar is the regular refurbishment capital set aside by hotels to upkeep their facilities. In the management agreements of the larger brands, for example, there is a requirement to set aside 4-5 per cent of annual revenue to upkeep the property. That is not included. So the refurbishment element only includes projects that have significantly

repositioned a property, rather than maintained its standards.

In the table below Gleeds have presented some summary data of ‘rule of thumb’ per room costs that are applicable for UK hotels. However for this analysis they have applied their more detailed industry expertise and knowledge of hotel construction costs, taking account of factors such as brand, location and project size to make a (still broad) estimate for each of the projects in the database, rather than relying solely on these ‘rule of thumb’ figures.

The predominant force has been the budget hotel sector as shown in the table left, which shows that 58,612 rooms, 56.6 per cent of total new openings, have been in the budget sector with the two largest players, Premier Inn (19,311 rooms) and Travelodge (18,433) being the driving force; the next largest, Holiday Inn Express, opened 5,588 rooms (referencing this publication’s database).

The database further reveals that only 12,619 unbranded hotel rooms have opened in the UK in the past decade (including some in small chains), which further supports the article on branding and franchising on page 31 of this publication. The emergence of niche sectors such as boutique hotels and Aparthotels is also revealed. Some of the unbranded hotels fall into these sectors as well as country house and the pub sectors, so not all are the traditional independent hotel by any means.

Analysis also shows that there were only two brands in the UK that drove construction values of more than £1bn – the budget giants Premier Inn (£1.3bn) and Travelodge (£1.05bn) exceeded that mark and unsurprisingly are now the largest hotel brands in the UK. These brands are also the only ones that tend to reach those parts of the country that others cannot reach – their development strategies featuring a wider variety of locations than any other brands in the UK market today.

More surprisingly, among the multi-brand global players it is Carlson (Radisson, Park Plaza, Park Inn) that has had the greatest impact on UK construction with a cost of almost £1.4bn although this was especially driven by some large Park Plaza developments in London including the city’s largest recent opening, the 1,021 room Park Plaza Westminster Bridge.

Sector Budget bedroom Midscale bedroom Upscale bedroom

Size of room Up to 22m² 24-30m² 28-50m² +

Construction Costs 34,000-50,000 50,000-130,000 135,000-325,000

Fees 4,000-6,000 7,000-20,000 20,000-40,000 +

Furniture, fittings & equipment 4,000-6,000 8,000-20,000 25,000-35,000 +

TOTAL 42,000-62,000 65,000-170,000 180,000-400,000 Source: Gleeds (Q4 2012)NB. Figures exclude utility connections, land cost, pre-opening costs and finance during construction

Hotels RoomsEstimated.

Construction Cost (£m)

Budget 580 58,612 3,366.8

Mid Market 97 16,880 1,664.7

Full Service 67 14,609 2,503.9

Independent 139 5,868 915.8

Boutique 47 3,593 592.3

Aparthotel 23 1,407 96.4

Upscale 9 1,356 463.4

Hostel 5 435 13.4

Resort Lodges/Apts 3 383 61.6

Country House 7 297 63.5

Pub 5 151 5.2

Beach Hut resort 1 21 2.2

TOTAL 983 103,612 9,749.2

Source: Melvin Gold Consulting/Gleeds/BHA Trends & Developments database

Estimated construction costs (£)

New openings (2003-2012)

12.4 £billionestimated construction cost of UK hotels 2003-2012

78% of construction costs are for new builds

57% of new openings have been in the budget sector

16 Trends & Developments

Trends & Developments 17

H OT E L I N DUS T RY

InterContinental Hotels, with six different brands under development, was the only other company to generate development of over £1bn. Accor is estimated to have generated £760m of construction and Hilton is estimated at £610m.

Regional and city analysis shows that London has had the greatest number of new hotels as well as rebrandings and refurbishments, proving once again that it is one of the most dynamic hotel markets in the world.

As the chart (right) shows, the North West had the next highest level of new openings but, when taking account of rebrandings and refurbishments, as well as new build, the South East had the second highest number of overall rooms. Scotland and the West Midlands were next in the rankings.

In construction cost terms, the differences were also stark. London drew £4.5bn of construction value, whereas only two English regions – the South East and the North West – exceeded the £1bn mark, as well as Scotland. This is also partly driven by the type of hotel and also by varying regional costs of construction.

In London, having a lower proportion of budget hotels and more upscale and full service, cost per room (taking account of new, rebranding and refurbishment) averaged £109,951 per room whereas the average cost in the South East was £85,460 per room and in the North West and Scotland it was £83,374 and £87,350 respectively.

In terms of cities, London had 25,681 new build rooms, with a further 3,370 at Heathrow, 1,125 at Stansted, and 386 near Gatwick. This is substantially more than the total supply in any other UK city. Nonetheless growth of 5,303 rooms in Manchester, 3,698 in Birmingham, 3,244 in Liverpool and 3,238 in Edinburgh were substantial increases. In fact there were 14 UK cities which had more than 1,000 rooms added during

the decade (as well as Heathrow and Stansted).

Rebrandings were especially prevalent in Scotland with Glasgow and Edinburgh having 1,159 and 744 rooms changing brand, respectively. These were in third and fourth place, only surpassed by London and Gatwick. Apart from London, significant levels of refurbishments were reported in Bournemouth and in Cardiff.

Putting the UK hotel industry’s impact on the construction sector in context, the £12.4bn of construction in a 10-year period indicates that this is 6.1 per cent of total UK Private Commercial Construction across the period. In overall terms, the Office of National Statistics estimates that new orders for Private Commercial Construction placed from mid-2002 until mid-2012 (most recent 10 years) was £204.1bn at current values.

It is remarkable that in 1969 the then government introduced the Hotel

Development Incentives Scheme (HDIS) which gave developers a grant of up to £1,000 per bedroom (£1,250 in London) – a significant contribution in those days. Such was the stimulus then required by the sector which sparked construction of 54,772 rooms (including extensions) between 1969 to April 1973, when the scheme ended.

Now, without incentives, and largely unloved by government, the hotel sector has developed 103,612 rooms in 983 new hotels in a decade that has included the worst recession in the country’s history. It has driven a construction value of £12.4bn, excluding professional fees and the value of the land, and has played a major part in stimulating regeneration.

Further proof that the hotel sector, and UK tourism in general, is a vibrant industry and is a significant contributor to the UK economy, creating both direct and indirect jobs, is hardly needed.

MelvinGold,FIH,isaleadingindependenthotelindustryconsultant.Moredetailsofhisservices,andhiscontactdetailscanbefoundatwww.melvingoldconsulting.com.

Gleedsisaworldclassmanagementandconstructionconsultancywithover125years’experienceinthebuildingandconstructionindustry.Ithasaparticularspecialisminthehotelsector.Contact:SteveLacey,Director([email protected])

Furthersupportingtablesforthedatapresentedinthisarticlewillbeincludedatwww.melvingoldconsulting.com/UK%20Hotel%20Supply.html

Total construction costs (£m)(forfulldetails,seeTable22,page72)

Lond

on

Sout

h W

est

Nor

th E

ast

4,5

42.2

777.

0

353.

7

Sout

h Ea

st

York

shire

/Hum

bers

ide

Nor

ther

n Ire

land

1,38

0.6

625.

5

227.

5

Nor

th W

est

East

of E

ngla

nd

Vario

us

1,25

2.2

606.

5

28.6

Scot

land

East

Mid

land

s

Chan

nel I

slan

ds

1,05

5.8

406.

0

50.6

Wes

t Mid

land

s

Wal

es

Isle

of M

an

711.

9

382.

0

25.3

18 Trends & Developments

H OT E L I N DUS T RY

by Andrew Taylor, Head of Leisure, RBS/NatWest Commercial Banking2012 – A YEAR OF AcTiviTY

This year saw significant events impacting the UK’s hospitality industry – from the success of the Queen’s Jubilee and Olympic and Paralympic games to Travelodge’s entry into CVA. But what is the true impact, both in and outside London? And how does the future look as results point towards economic recovery? Andrew Taylor, Head of Leisure for Commercial Banking at NatWest and RBS, takes a closer look.

After an encouraging start, the Jubilee was the first of the year’s historic events, bringing with it an extra bank holiday and a predicted influx of visitors to the capital, both foreign and domestic. But while the festivities created the illusion of a packed London in June, hotel occupancy struggled as the city was primarily filled with day visitors.

Ironically, hotels in London recorded the worst financial performance of 2012 in June for many years. Revenue per room (RevPAR) across the central London hotels declined by 10.8 per cent in the month to £117.30, while total revenue per room (TrevPAR) fell by 8.1 per cent to £148.00, on the back of a 6.6 per cent decline in room occupancy to 82.9 per cent. The extended holiday for the Queen’s Diamond Jubilee, combined with warnings of transport disruption and fears over accommodation, led to a detrimental decline in business. Nevertheless, despite this slow-down prior to the Olympic and Paralympics, the Games delivered a boost to hotel performance in London, although arguably less than predicted.

The Office for National Statistics recorded a drop of five per cent in visitor numbers in August although this was outweighed by an estimated nine per cent increase in spend per visitor compared to last year with the average hotel room costing £210 – an increase of 26 per cent compared to the same period in 2011.

Substitution seemed to be the leading factor, with business travellers and regular visitors avoiding the city amid fears of rocketing prices and travel and congestion chaos. This also had a knock-on effect on central London restaurants with takings in some restaurants not near Games venues down 40 per cent or more, although clearly this issue was short-lived.

London hoteliers also managed to buck the traditional post-Olympic slump as occupancy levels rose by 3.1 per cent to 89.5 per cent in September according to TRI Hospitality Consulting’s latest figures (Page26). These figures can be attributed to one of the most successful Paralympics in history and an increase of late visitors.

But while London and other host cities rode the crest of the Olympic wave, provincial cities suffered a decline in both occupancy and room revenue throughout August with year-to-date gross operating profit per available room down by three per cent while London’s GOPPAR rose by 6.6. per cent over the same period. This is not, however, a new struggle for the provinces. Those inside the London bubble have seen occupancies creeping up since early 2000 while occupancy in the provinces stays more or less static. Now, with the expected increase in food prices due to adverse weather conditions hitting UK harvests and the above-inflation energy increases, there seems to be no respite for provincial hoteliers.

Over the same period the UK restaurant and pub sector saw sales growth of 5.8 per cent in the year to September 2012 with sales inside the M25 increasing by 6.7 per cent. Competition remains strong both within the industry and against the supermarket “dine in” style offers. Consumer discretionary spend remains under pressure and customers are still looking for value alongside an enjoyable dining experience.

Although the proportion of budget hotels in the UK is still lower than in Europe and the US, over 17,000 new hotel rooms opened in the UK in the past year – 70 per cent of which were in the budget market. Interestingly, the London market grew by circa 8,000 rooms of which around 58 per cent were budget, whilst in the provinces nearly 86 per cent of new room stock came from the budget sector with the largest new room concentration being in Edinburgh. This will continue to put pressure on independent operators. With 15,000 new rooms projected for 2013 – highly driven by the branded and budget space – the future looks bright.

However, Travelodge’s entry into company voluntary agreement (CVA) with creditors threw a different light on the otherwise optimistic outlook. The chain, the second largest in the budget hotel sector behind Premier Inn and the third biggest hotel chain in the UK by number of bedrooms, is shedding one in ten of its hotels under a major overhaul which means that £709m of debt will be written off and new equity of £75m provided by the lenders.

Room rates for regional hotels predicted to

rise in 2013 by

Occupancy for regional hotels predicted to

fall in 2013 by

-0.3%

2.4%

Hotel recovery from the recession has been faster than the rest of the economy.

Trends & Developments 19

H OT E L I N DUS T RY

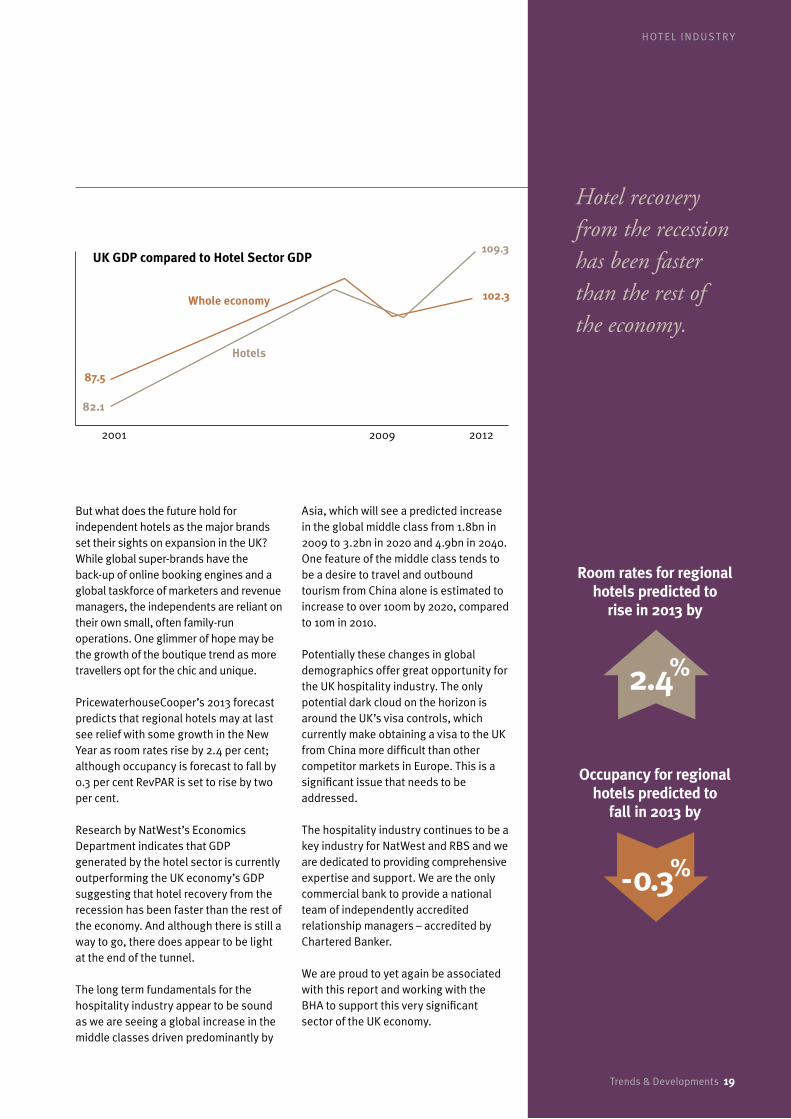

But what does the future hold for independent hotels as the major brands set their sights on expansion in the UK? While global super-brands have the back-up of online booking engines and a global taskforce of marketers and revenue managers, the independents are reliant on their own small, often family-run operations. One glimmer of hope may be the growth of the boutique trend as more travellers opt for the chic and unique.

PricewaterhouseCooper’s 2013 forecast predicts that regional hotels may at last see relief with some growth in the New Year as room rates rise by 2.4 per cent; although occupancy is forecast to fall by 0.3 per cent RevPAR is set to rise by two per cent.

Research by NatWest’s Economics Department indicates that GDP generated by the hotel sector is currently outperforming the UK economy’s GDP suggesting that hotel recovery from the recession has been faster than the rest of the economy. And although there is still a way to go, there does appear to be light at the end of the tunnel.

The long term fundamentals for the hospitality industry appear to be sound as we are seeing a global increase in the middle classes driven predominantly by

Asia, which will see a predicted increase in the global middle class from 1.8bn in 2009 to 3.2bn in 2020 and 4.9bn in 2040. One feature of the middle class tends to be a desire to travel and outbound tourism from China alone is estimated to increase to over 100m by 2020, compared to 10m in 2010.

Potentially these changes in global demographics offer great opportunity for the UK hospitality industry. The only potential dark cloud on the horizon is around the UK’s visa controls, which currently make obtaining a visa to the UK from China more difficult than other competitor markets in Europe. This is a significant issue that needs to be addressed.

The hospitality industry continues to be a key industry for NatWest and RBS and we are dedicated to providing comprehensive expertise and support. We are the only commercial bank to provide a national team of independently accredited relationship managers – accredited by Chartered Banker.

We are proud to yet again be associated with this report and working with the BHA to support this very significant sector of the UK economy.

2001 2012

Hotels

109.3

82.1

Whole economy 102.3

87.5

UK GDP compared to Hotel Sector GDP

2009

H OT E L I N DUS T RY

Whitbread, with its Premier Inn budget brand, continues to remain the largest hotel operator in the UK, with InterContinental’s various brands second and Travelodge third. In spite of the impact of the recession, all three companies maintained their growth during 2012, with Premier Inn adding 30 hotels (3,900 rooms) InterContinental adding 13 hotels (1,800 rooms) and Travelodge adding 39 hotels (4,000 rooms).

During the year, however, Travelodge entered a Company Voluntary Arrangement (CVA) with its creditors as it sought to reduce the level of rent it pays on 109 hotels, and announced plans to shed 49 hotels which it now considers unviable. It is raising £75m of new money to inject into the business and plans to invest £55m in a major refurbishment programme; bank debt of £235m, is being written off and £71m repaid reducing bank debt from £635m to £329m, with repayment extended to 2017. Accor and Hilton both added to their portfolios with more openings planned for 2013.

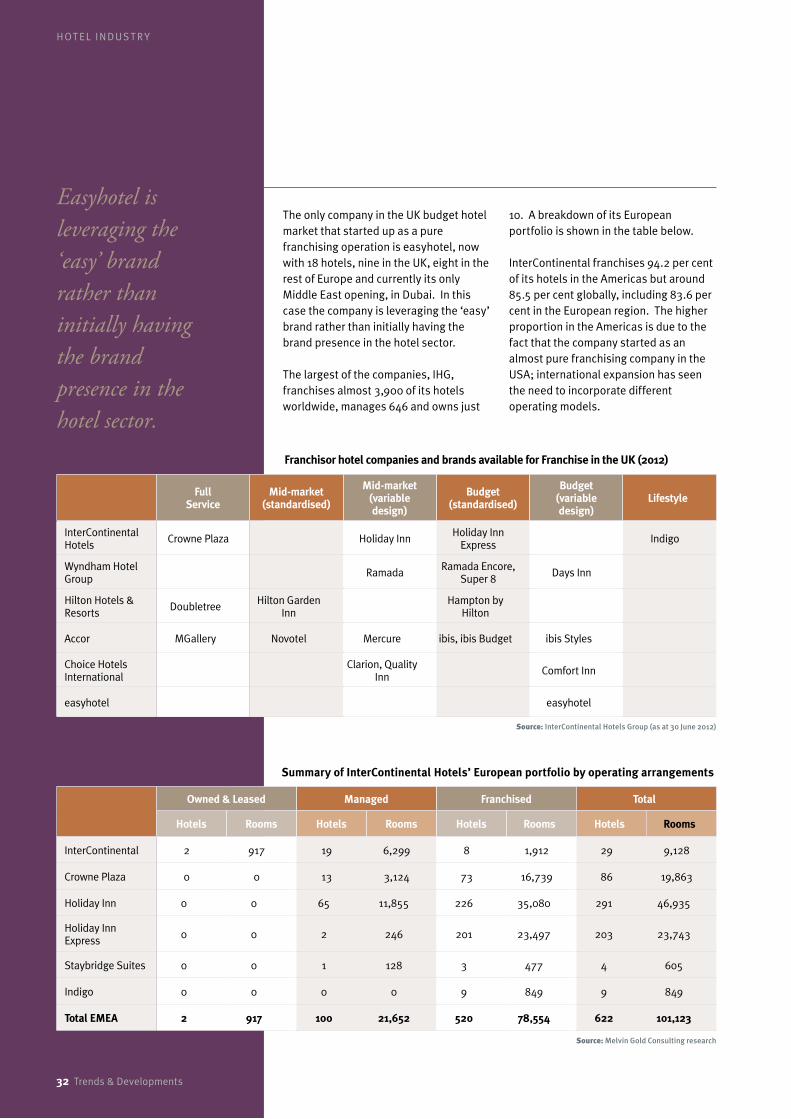

Of the ten largest companies, only Whitbread and InterContinental continue to remain in British hands; however, InterContinental is a truly international company with strong links to the US and Travelodge, though now owned by US investors, operates almost exclusively in UK and Ireland. Hilton, Marriott, Carlson and Wyndham are US-based and so is Best Western, though the UK franchise is a collection of quintessential three/four star British hotels. Guoman in based in Singapore with the majority of hotels in the UK.

Apart from Premier Inn and Travelodge, neither of which franchise in the UK, the majority of new developments continue to be franchise-led with Holiday Inn, Holiday Inn Express, Doubletree by Hilton, Hampton by Hilton, Ramada and Accor leading the way. All but Accor are US-based franchises so, to this extent, the UK hotel industry continues to be strongly influenced by US styles and standards, only slightly amended for the

UK market. The introduction of franchising and their brands, as well as the eagerness of hotel companies to change from ownership to hotel operations, remain the most significant trends in the UK hotel industry.

Independent ownership will continue – and the best will thrive – but branded hotel groups are increasingly influencing the industry’s development. Almost all the new-build properties are branded (Table29,page82), of which Premier Inn and Travelodge continue to be the most noticeable examples.

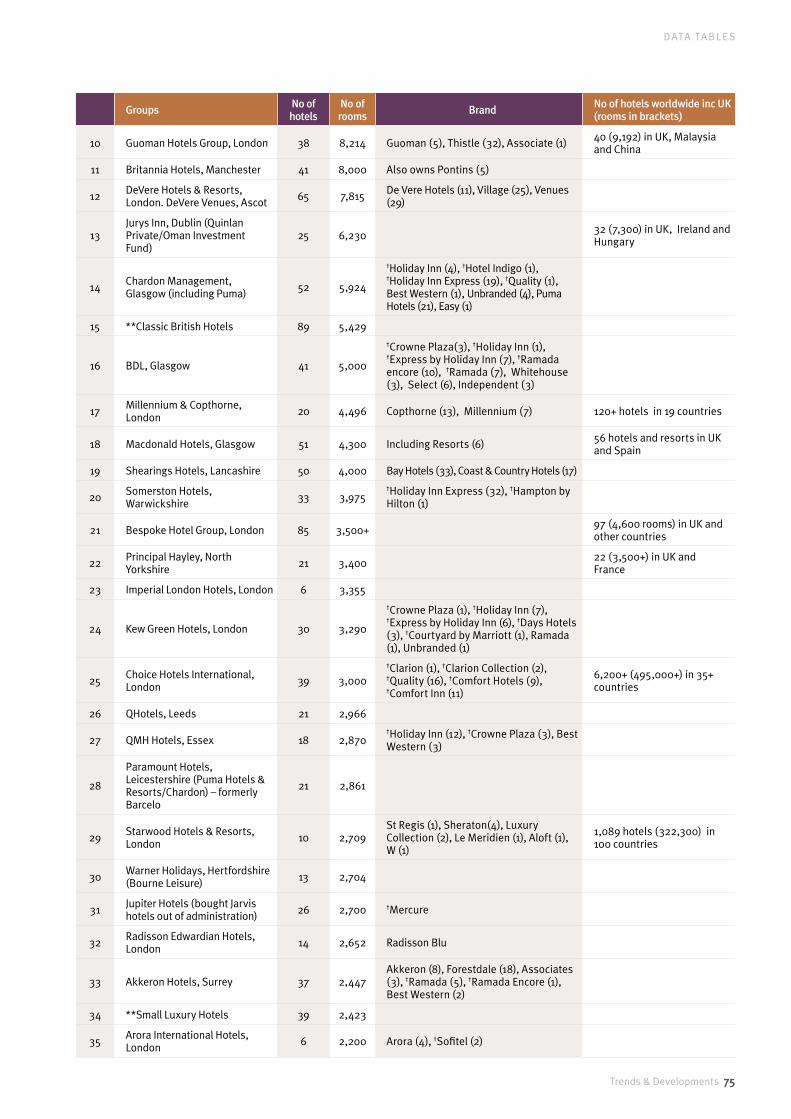

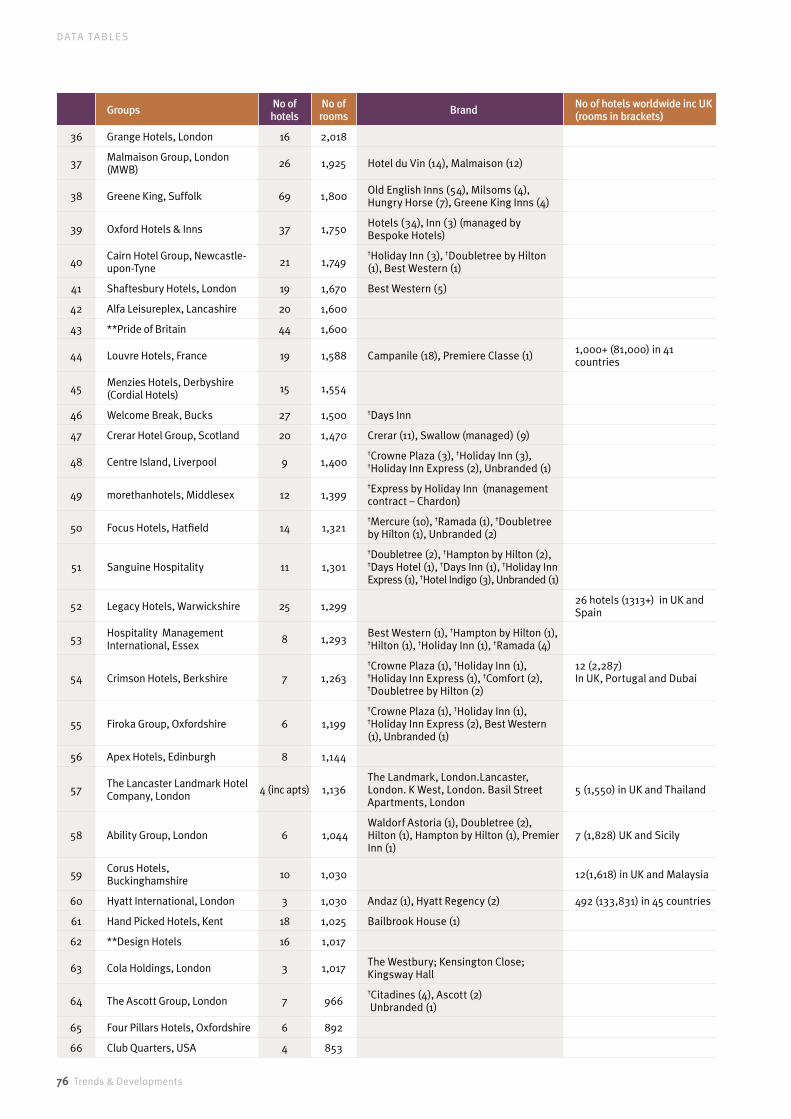

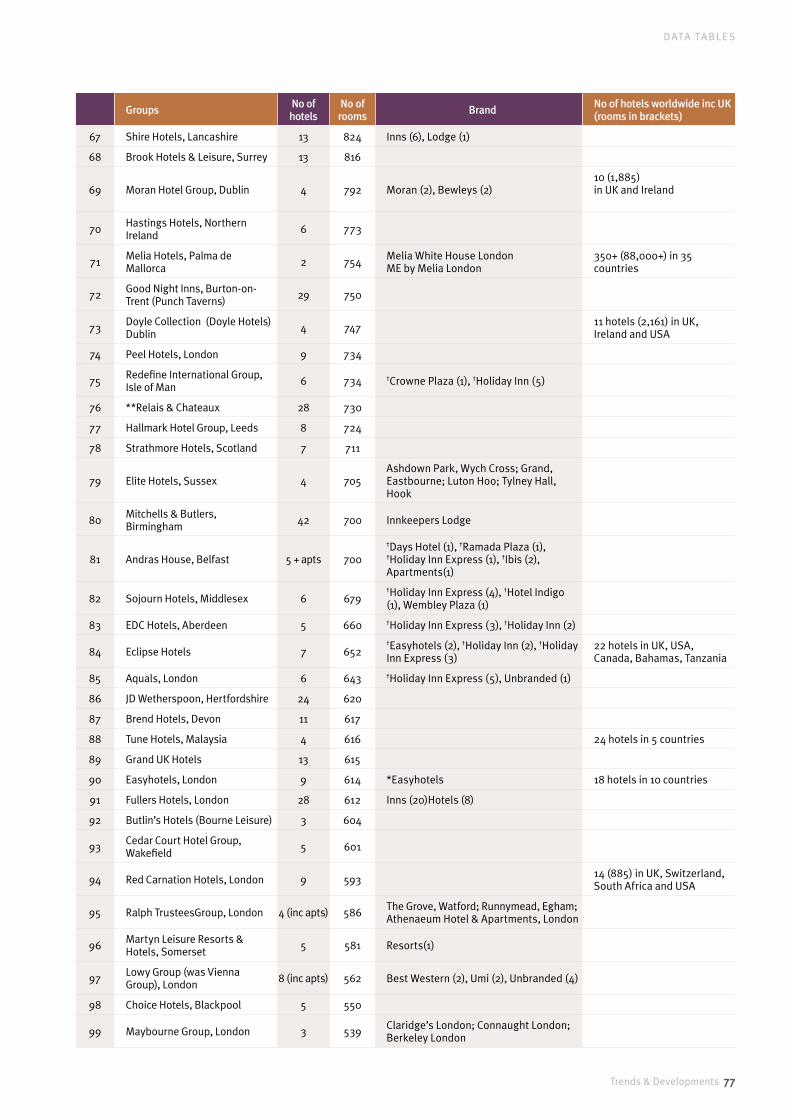

With the branded sector growing, the private sector has to hold its own in a difficult market though one company, Britannia Hotels, has moved from 13th to 11th on the back of a number of acquisitions (Table28,page79). Consortia such as Best Western, Classic British Hotels, Small Luxury Hotels of the World, and Pride of Britain maintain their position but are having to compete against the growth of major franchisees such as Chardon Management with 2,800 rooms added (now operating the 21 former Barcelo hotels for Puma) and BDL (plus 900 rooms).

Uk’s ten largest hotel companies and number of rooms(for full list, see Table 26, page 74)

1 Whitbread Hotel Company, London 48,383

2 InterContinental Hotels Group, Buckinghamshire 40,100

3 Travelodge, Oxfordshire 36,898

4 Accor, London 26,500+

5 Hilton Worldwide, London 23,500

6 Best Western, York 15,900

7 Carlson Rezidor Hotel Group, Brussels, Belgium 12,812

8 Marriott Hotels, London 11,943

9 Wyndham Worldwide, USA 10,010

10 Guoman Hotels Group, London 8,214

as at November 2012

With the branded sector growing, the private sector has to hold its own in a difficult market.

2012: GROwTH cOnTinUEs dEsPiTE REcEssiOn

New hotels in 2012

13 30 39

InterContinental

Premier Inn

Travelodge

20 Trends & Developments

Trends & Developments 21

H OT E L I N DUS T RY

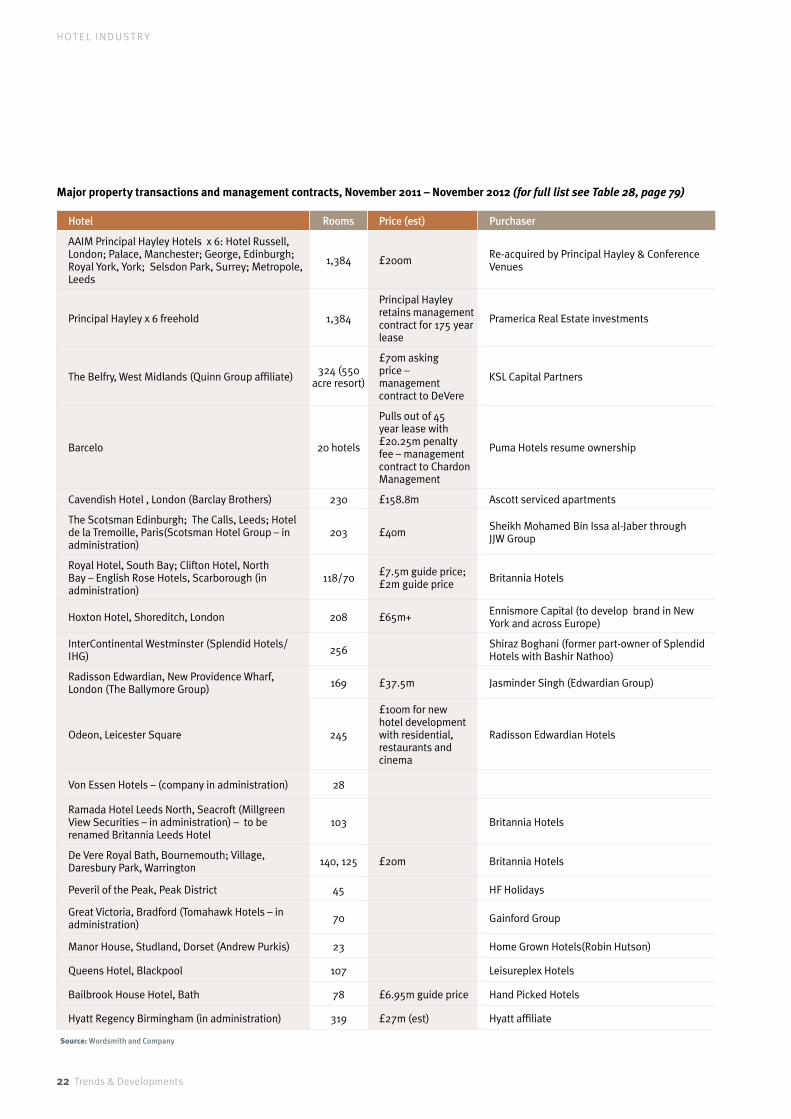

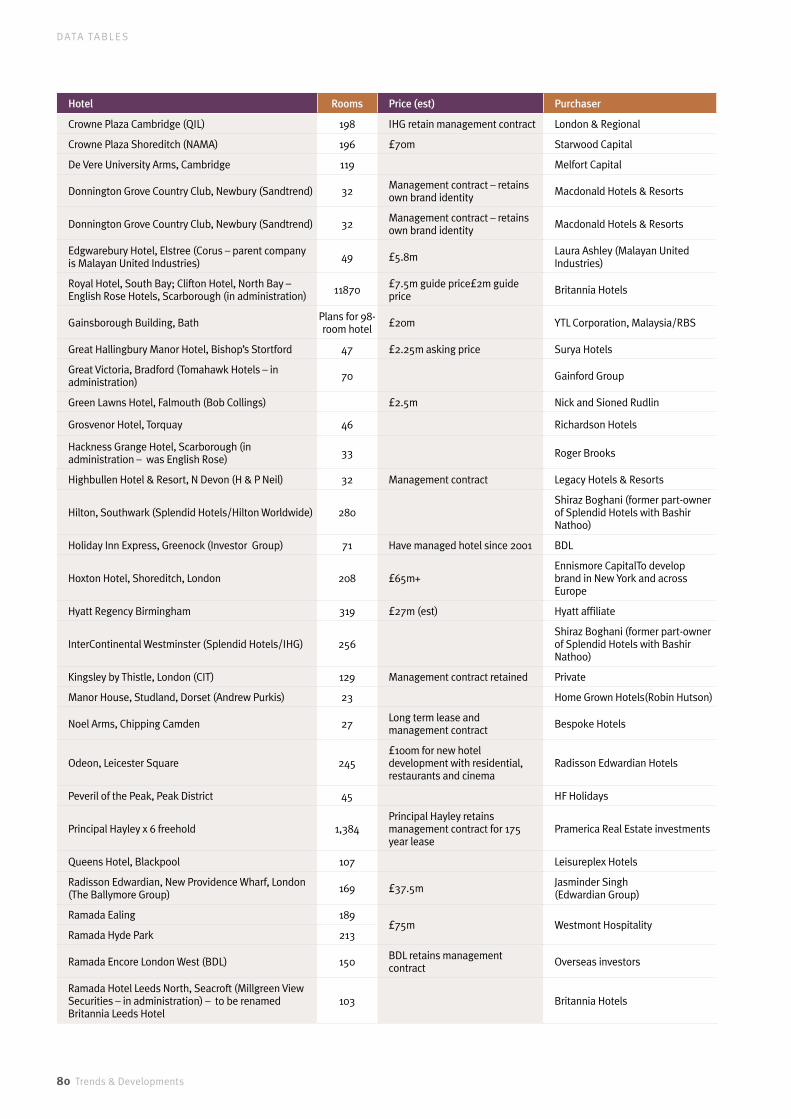

Property transactions during 2012, apart from the continuing disposal of the von Essen portfolio (Table 28, page 79) did not feature any major insolvency, though Travelodge’s CVA represented a setback for one of the UK’s most aggressive hotel companies.

One prominent name to disappear from the UK hotel scene was that of the Spanish-based Barcelo hotel group which had signed a 45-year lease to run 21 hotels, including the Lygon Arms in Broadway, Imperial in Torquay and Majestic in Harrogate owned by Puma Hotels. Barcelo paid a £20m penalty to terminate its leases after asking for a reduction in the rent it paid for the properties, in view of a fall in business during the recession.

Prior to the grant of the leases in 2007, Puma Hotels itself operated the hotels through its head office in Hinckley and now resumes direct management. The company, in which the AIM-listed Hotel Corporation has a 49.9 per cent stake, revived the old Paramount Hotels brand and has appointed Chardon Management to assist in the management of the hotels. Subsequently, doubts have been expressed about Puma’s £300m debt to Allied Irish Banks which is now in the hands of the Irish Bank Resolution Corporation.

In a £200m deal, Principal Hayley, bought back six hotels for £200m from property fund AAIM. The group then immediately sold the freehold of the properties to Pramerica, the real-estate arm of America’s Prudential, but will continue to operate them on a 175-year lease. Principal Hayley originally sold the properties – which include Hotel Russell in London, Selsdon Park in Surrey, Leeds Metropole, Royal York, Palace Manchester and George in Edinburgh – to AAIM in 2006, at the height of the property market, for circa £275m.

Another hotel name likely to disappear is the Cavendish in London. Originally built by Trust Houses in 1964 for £2m, the

252-room hotel, owned by the Barclay Brothers (owners of the Ritz) was sold to Ascott, the serviced accommodation company, for £168m, who will convert much of the hotel into serviced apartments.

One notable property to change hands during the year was the Belfry in the West Midlands, with its championship golf course, which had been owned and operated since 2007 by the Irish-based Quinn Group after it bought the hotel from De Vere for £165m. The hotel was sold to KSL Capital Partners, a leading US private equity firm, in 2012 for £70m, who installed De Vere as operators.

The Britannia Hotel group continues its expansion with the acquisition of the Royal Bath in Bournemouth – one of the most traditional of all resort hotels – the Village, Daresbury Park from De Vere and two hotels in Scarborough – The Royal and Clifton which were part of the English Rose collection which was in administration. During the year, Britannia also acquired the Ramada in Leeds.

Other well known hotels to change hands include The Hoxton at a guide price of £67.5m purchased by US based Ennismore Capital, which was established in 2010. The aim is to develop the Hoxton brand by opening further hotels in London, US and Europe in the next five years.

A major new development in London’s Leicester Square will see the Odeon Cinema site turned into a hotel, residential complex and restaurants by Jasminder Singh, whose Radisson Edwardian group also acquired the freehold of two of the group’s hotels – in Birmingham and Canary Wharf. This move is contrary to

the trend for hotel companies to dispose of their freehold interests.

Meanwhile, the sale of the freehold of individual hotel properties, with the current operators retaining the management contract, continues apace.

200 £millionPrincipal Hayley bought back six hotels

wHO sOLd wHAT in 2012?

Barcelo paid a £20m penalty to terminate its leases after asking for a reduction in the rent it paid for the properties.

22 Trends & Developments

H OT E L I N DUS T RY

Hotel Rooms Price (est) Purchaser

AAIM Principal Hayley Hotels x 6: Hotel Russell, London; Palace, Manchester; George, Edinburgh; Royal York, York; Selsdon Park, Surrey; Metropole, Leeds

1,384 £200m Re-acquired by Principal Hayley & Conference Venues

Principal Hayley x 6 freehold 1,384

Principal Hayley retains management contract for 175 year lease

Pramerica Real Estate investments

The Belfry, West Midlands (Quinn Group affiliate) 324 (550 acre resort)

£70m asking price – management contract to DeVere

KSL Capital Partners

Barcelo 20 hotels

Pulls out of 45 year lease with £20.25m penalty fee – management contract to Chardon Management

Puma Hotels resume ownership

Cavendish Hotel , London (Barclay Brothers) 230 £158.8m Ascott serviced apartments

The Scotsman Edinburgh; The Calls, Leeds; Hotel de la Tremoille, Paris(Scotsman Hotel Group – in administration)

203 £40m Sheikh Mohamed Bin Issa al-Jaber through JJW Group

Royal Hotel, South Bay; Clifton Hotel, North Bay – English Rose Hotels, Scarborough (in administration)

118/70 £7.5m guide price; £2m guide price Britannia Hotels

Hoxton Hotel, Shoreditch, London 208 £65m+ Ennismore Capital (to develop brand in New York and across Europe)

InterContinental Westminster (Splendid Hotels/IHG) 256 Shiraz Boghani (former part-owner of Splendid

Hotels with Bashir Nathoo)

Radisson Edwardian, New Providence Wharf, London (The Ballymore Group) 169 £37.5m Jasminder Singh (Edwardian Group)

Odeon, Leicester Square 245

£100m for new hotel development with residential, restaurants and cinema

Radisson Edwardian Hotels

Von Essen Hotels – (company in administration) 28

Ramada Hotel Leeds North, Seacroft (Millgreen View Securities – in administration) – to be renamed Britannia Leeds Hotel

103 Britannia Hotels

De Vere Royal Bath, Bournemouth; Village, Daresbury Park, Warrington 140, 125 £20m Britannia Hotels

Peveril of the Peak, Peak District 45 HF Holidays

Great Victoria, Bradford (Tomahawk Hotels – in administration) 70 Gainford Group

Manor House, Studland, Dorset (Andrew Purkis) 23 Home Grown Hotels(Robin Hutson)

Queens Hotel, Blackpool 107 Leisureplex Hotels

Bailbrook House Hotel, Bath 78 £6.95m guide price Hand Picked Hotels

Hyatt Regency Birmingham (in administration) 319 £27m (est) Hyatt affiliate

Source: Wordsmith and Company

Major property transactions and management contracts, November 2011 – November 2012 (for full list see Table 28, page 79)

I N T RO DU C T I O N

Trends & Developments 23

H OT E L I N DUS T RY

Hotel construction – 2002-2012/15

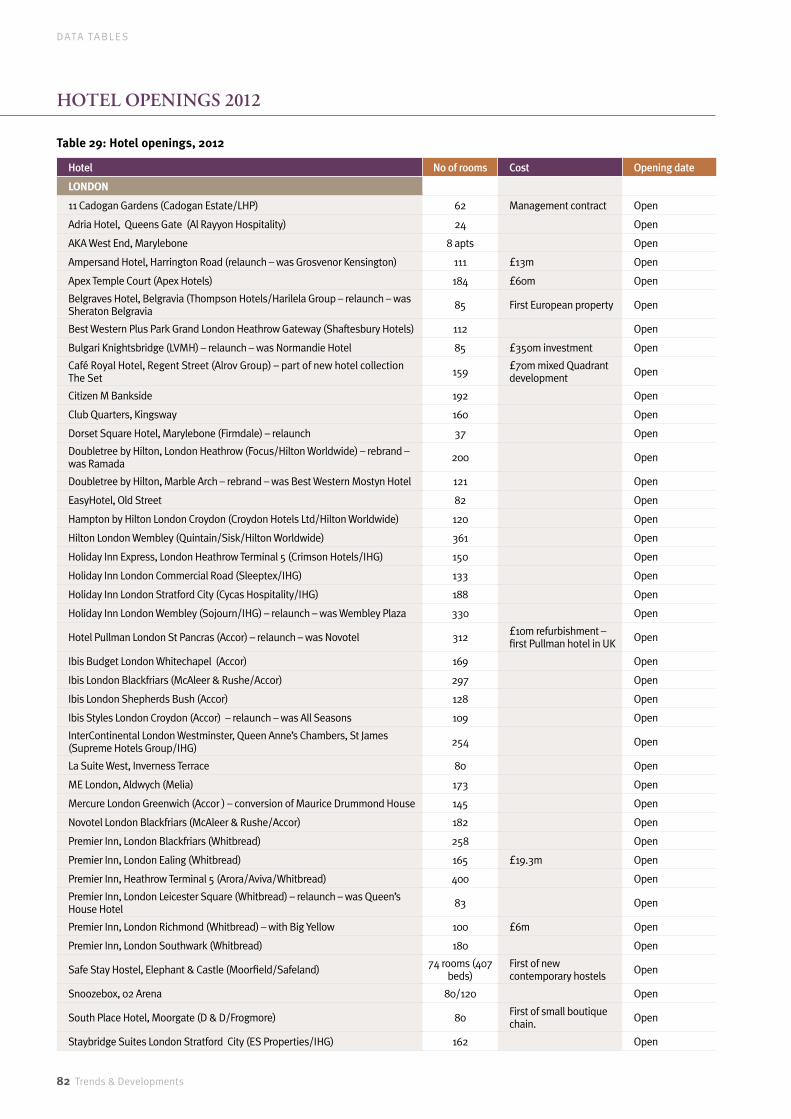

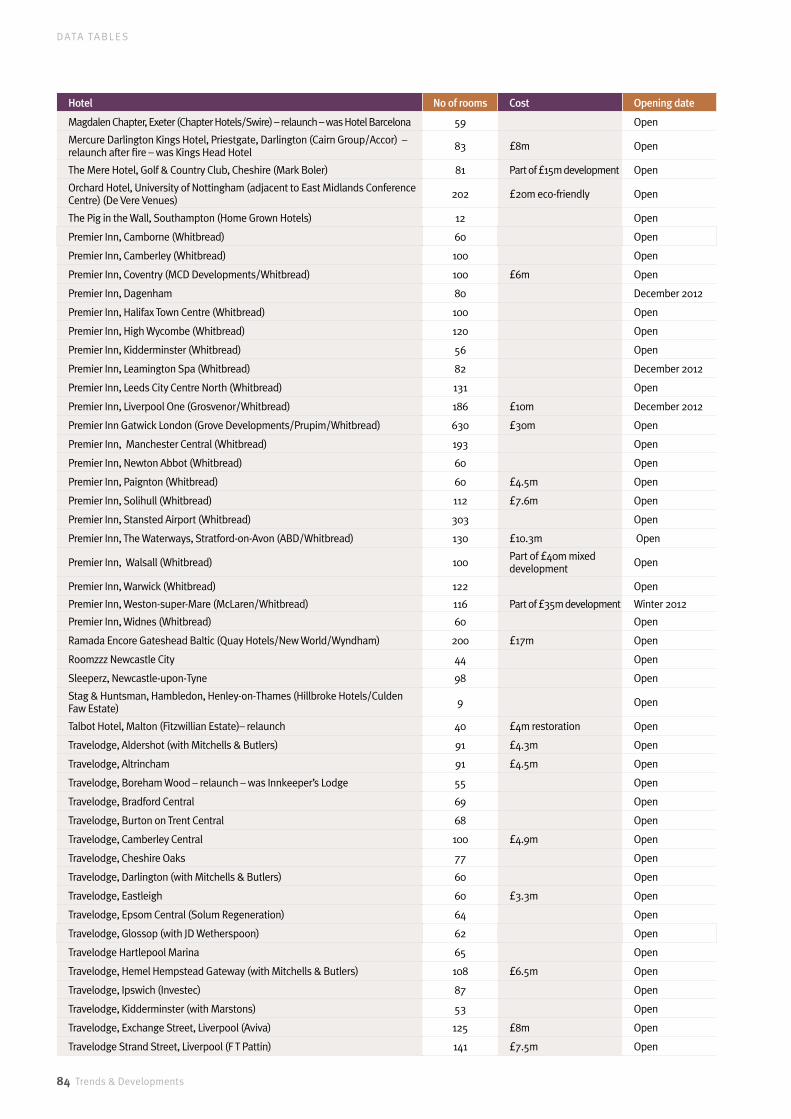

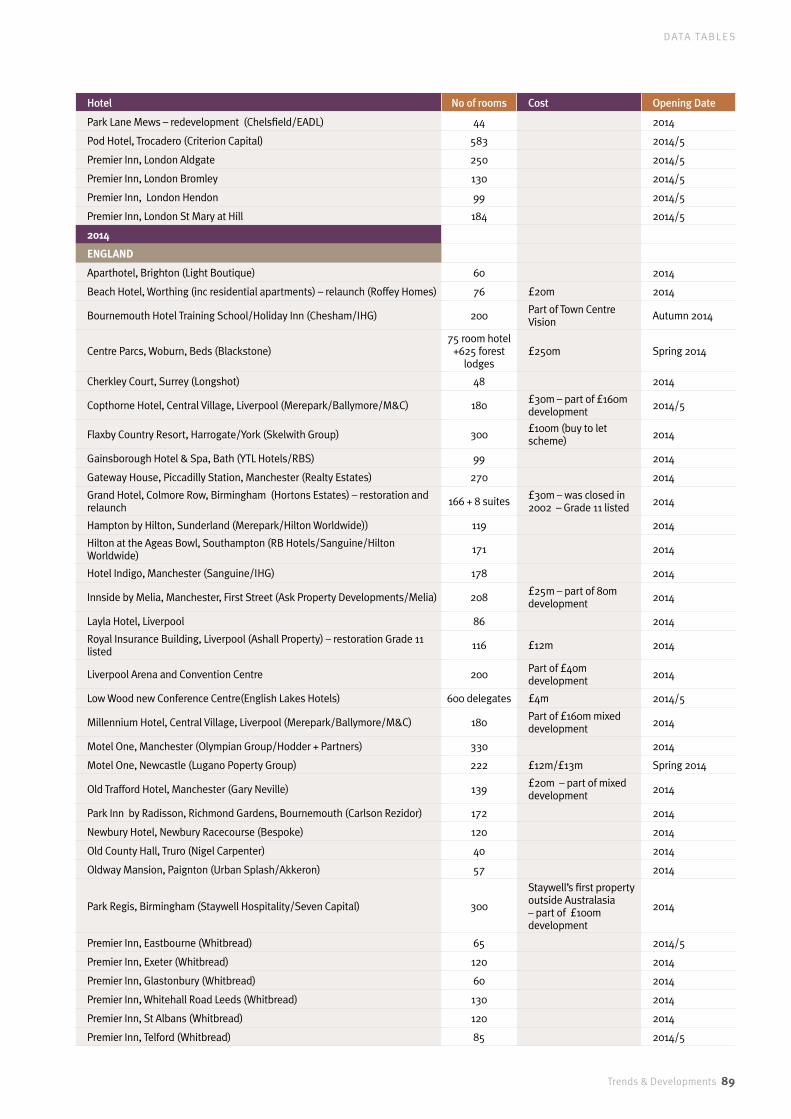

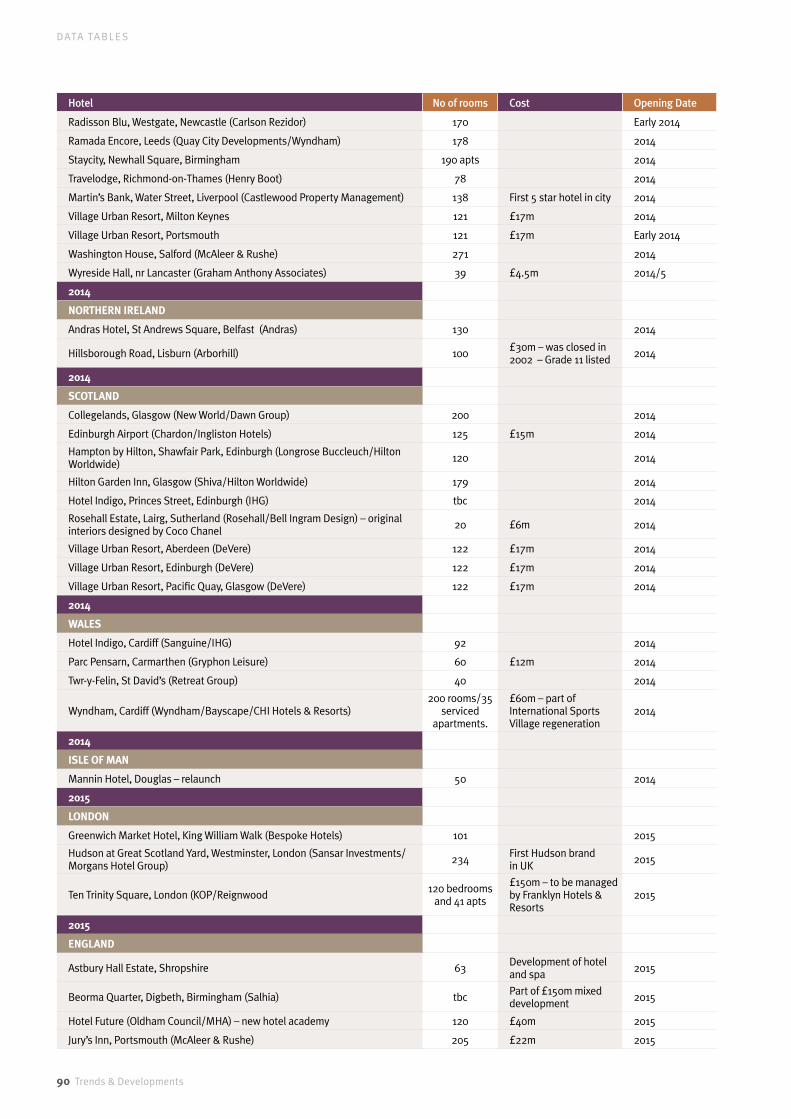

There is no let-up in the rate of hotel expansion which continues throughout the UK. Over 17,000 rooms opened in 2012 – the largest number since 2007 – with a further 13,000+ planned to open in 2013 and a similar number in 2014. For the full list, see pages 82-92. Expansion in the budget sector is leading the way with budget rooms representing 72 per cent of all new openings in 2012 and 66 per cent of those planned for 2013. We have not attempted to separate out budget and other hotels in 2014 and beyond.

By the end of 2012, the industry will have gained 123,911 additional rooms since 2002, 58 per cent being in the budget category.

HOTEL OPEninGs

17,000 rooms opened in 2012

53 new hotels in London 2012

Expansion in the budget sector is leading the way.

Number of new hotels 2012

England 74

Scotland

London

15

53

Wales 4

Northern Ireland 1 72%

of all new openings are in the budget sector

Number of new hotel rooms(foracompletelistofhotelopeningsseeTable29,page82)

2011

11,9

39

2012

17,0

29

2013

13,0

54

2014

12,8

68

2015

7,27

2

Trends & Developments 23

24 Trends & Developments

H OT E L I N DUS T RY

HOTEL OPENINGS – 2012

InterContinental continued its strong expansion with a new InterContinental Hotel in St James (254 rooms), three new Holiday Inns, a new Holiday Inn Express and a new Staybridge Suites in London, together with a further three Holiday Inns in England – Southend (129 rooms), Walsall (156 rooms) and London Gatwick (118 rooms) and five new Holiday Inn Express properties – all operated by franchisees. Two new Hotel Indigos also opened in Newcastle (148 rooms) and Edinburgh (60 rooms), which was a re-launch of the former Osbourne Hotel, with one opening in Kensington, London (51 rooms) in January 2013.

Hilton also increased its portfolio with a new Hilton at Wembley (361 rooms) and at the new FA complex at St George’s Park, Burton on Trent (146 rooms), which also has a new Hampton by Hilton (86 rooms). Three other Hampton by Hiltons also opened – at Birmingham (284 rooms), Luton (250 rooms) and York (120 rooms).

Three Doubletree by Hilton have opened this year – all rebrands – including the seventh in London. Premier Inn and Travelodge continued their strong expansion both in London and in the provinces with Premier Inn adding 3,939 rooms and Travelodge 4,000 rooms.

Meanwhile some new names have appeared on the London hotel scene. London has its first Pullman Hotel (Accor’s re-launch of the Novotel in Euston Road). The Bulgari in Knightsbridge opened on the site of the old Normandie Hotel and the nearby 36-room Wellesley in Knightsbridge, in a 1920s building which was the site of a

former Pizza Express restaurant, opened in December. Also opening in December is one of London’s most famous banqueting houses – the former Café Royal in Regent Street has been turned into a 159-room hotel. The first US-based Thompson hotel – Belgraves (a re-working of the former Sheraton Belgravia) – has opened and Melia’s 173-room ME hotel opened in the Aldwych after a long building delay. South Place Hotel in Moorgate (80 rooms) is the first hotel in a proposed chain of boutique properties by the restaurant group, D&D. In the budget sector, the Malaysian-owned Tune Hotel group continued its rapid expansion in London with three new properties (Liverpool Street (183 rooms), Paddington (137 rooms) and Kings Cross (217 rooms); Apex and Accor both added to their London portfolios.Plans for The Edge Hotel School, based at Wivenhoe House on the University of Essex campus at Colchester at last materialised. The Edge, the first hotel school based entirely in a fully operational hotel, is the result of the partnership between the independent education foundation Edge, the University of Essex and its academic partner Kaplan Open Learning.

On the south coast, plans have been revived for the Bournemouth Hotel School. With similar aims to the Edge, the project, based on the construction of a 200-room Holiday Inn, has the support of InterContinental Hotels group, Holiday Inn and Bournemouth University, with an opening date scheduled for 2013.

Another hotel school – Hotel Future – based in Oldham is planned for 2015.

InterContinental, Hilton, Accor, Premier Inn and Travelodge continued their strong expansion in 2012.

24 Trends & Developments

Trends & Developments 25

H OT E L I N DUS T RY

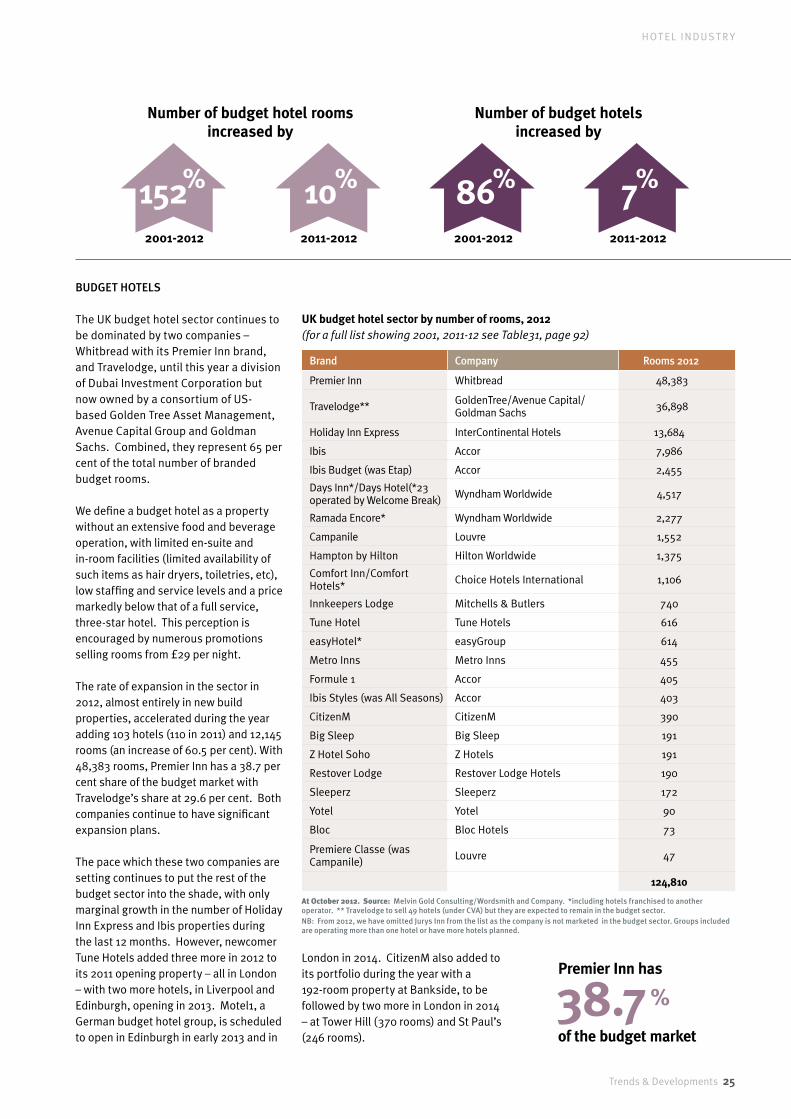

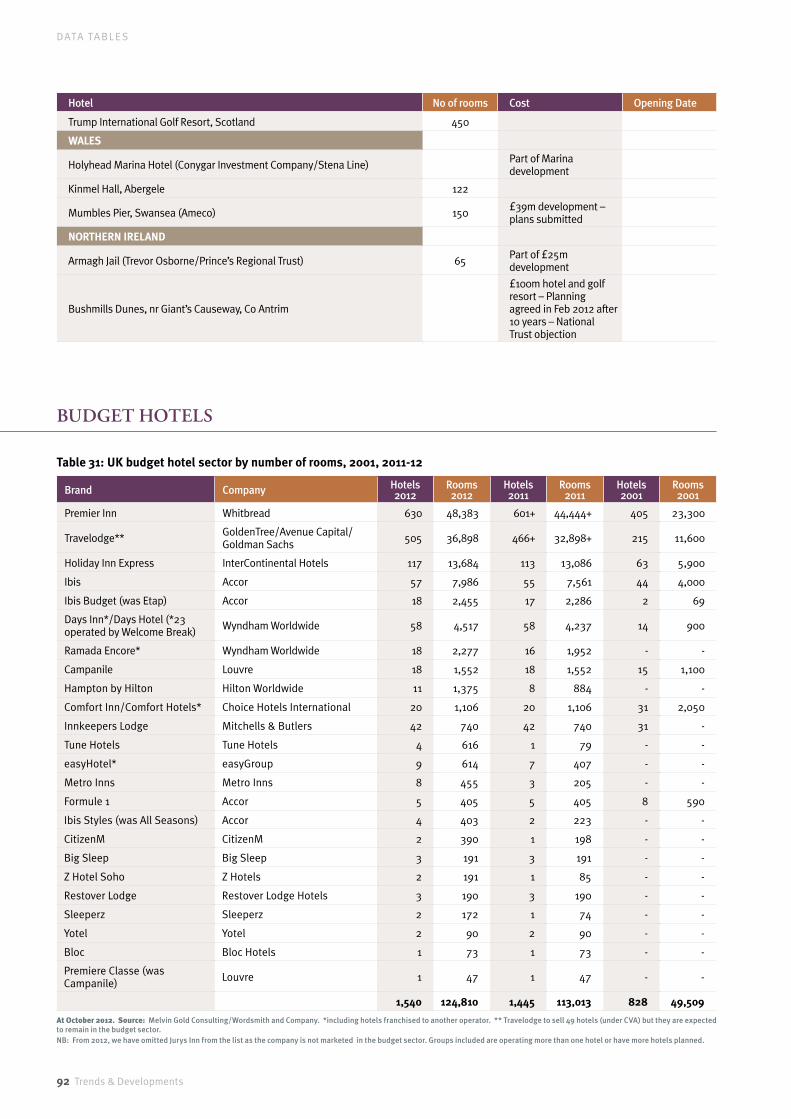

BUDGET HOTELS

The UK budget hotel sector continues to be dominated by two companies – Whitbread with its Premier Inn brand, and Travelodge, until this year a division of Dubai Investment Corporation but now owned by a consortium of US-based Golden Tree Asset Management, Avenue Capital Group and Goldman Sachs. Combined, they represent 65 per cent of the total number of branded budget rooms.

We define a budget hotel as a property without an extensive food and beverage operation, with limited en-suite and in-room facilities (limited availability of such items as hair dryers, toiletries, etc), low staffing and service levels and a price markedly below that of a full service, three-star hotel. This perception is encouraged by numerous promotions selling rooms from £29 per night.

The rate of expansion in the sector in 2012, almost entirely in new build properties, accelerated during the year adding 103 hotels (110 in 2011) and 12,145 rooms (an increase of 60.5 per cent). With 48,383 rooms, Premier Inn has a 38.7 per cent share of the budget market with Travelodge’s share at 29.6 per cent. Both companies continue to have significant expansion plans.

The pace which these two companies are setting continues to put the rest of the budget sector into the shade, with only marginal growth in the number of Holiday Inn Express and Ibis properties during the last 12 months. However, newcomer Tune Hotels added three more in 2012 to its 2011 opening property – all in London – with two more hotels, in Liverpool and Edinburgh, opening in 2013. Motel1, a German budget hotel group, is scheduled to open in Edinburgh in early 2013 and in

Number of budget hotel rooms increased by

Number of budget hotels increased by

2011-2012 2011-20122001-2012 2001-2012

38.7 %Premier Inn has

of the budget market

152% 86%10% 7%

UK budget hotel sector by number of rooms, 2012(forafulllistshowing2001,2011-12seeTable31,page92)

Brand Company Rooms 2012

Premier Inn Whitbread 48,383

Travelodge** GoldenTree/Avenue Capital/Goldman Sachs 36,898

Holiday Inn Express InterContinental Hotels 13,684

Ibis Accor 7,986

Ibis Budget (was Etap) Accor 2,455

Days Inn*/Days Hotel(*23 operated by Welcome Break) Wyndham Worldwide 4,517

Ramada Encore* Wyndham Worldwide 2,277

Campanile Louvre 1,552

Hampton by Hilton Hilton Worldwide 1,375

Comfort Inn/Comfort Hotels* Choice Hotels International 1,106

Innkeepers Lodge Mitchells & Butlers 740

Tune Hotel Tune Hotels 616

easyHotel* easyGroup 614

Metro Inns Metro Inns 455

Formule 1 Accor 405

Ibis Styles (was All Seasons) Accor 403

CitizenM CitizenM 390

Big Sleep Big Sleep 191

Z Hotel Soho Z Hotels 191

Restover Lodge Restover Lodge Hotels 190

Sleeperz Sleeperz 172

Yotel Yotel 90

Bloc Bloc Hotels 73

Premiere Classe (was Campanile) Louvre 47

124,810

At October 2012. Source: Melvin Gold Consulting/Wordsmith and Company. *including hotels franchised to another operator. ** Travelodge to sell 49 hotels (under CVA) but they are expected to remain in the budget sector.NB: From 2012, we have omitted Jurys Inn from the list as the company is not marketed in the budget sector. Groups included are operating more than one hotel or have more hotels planned.

London in 2014. CitizenM also added to its portfolio during the year with a 192-room property at Bankside, to be followed by two more in London in 2014 – at Tower Hill (370 rooms) and St Paul’s (246 rooms).

26 Trends & Developments

H OT E L I N DUS T RY

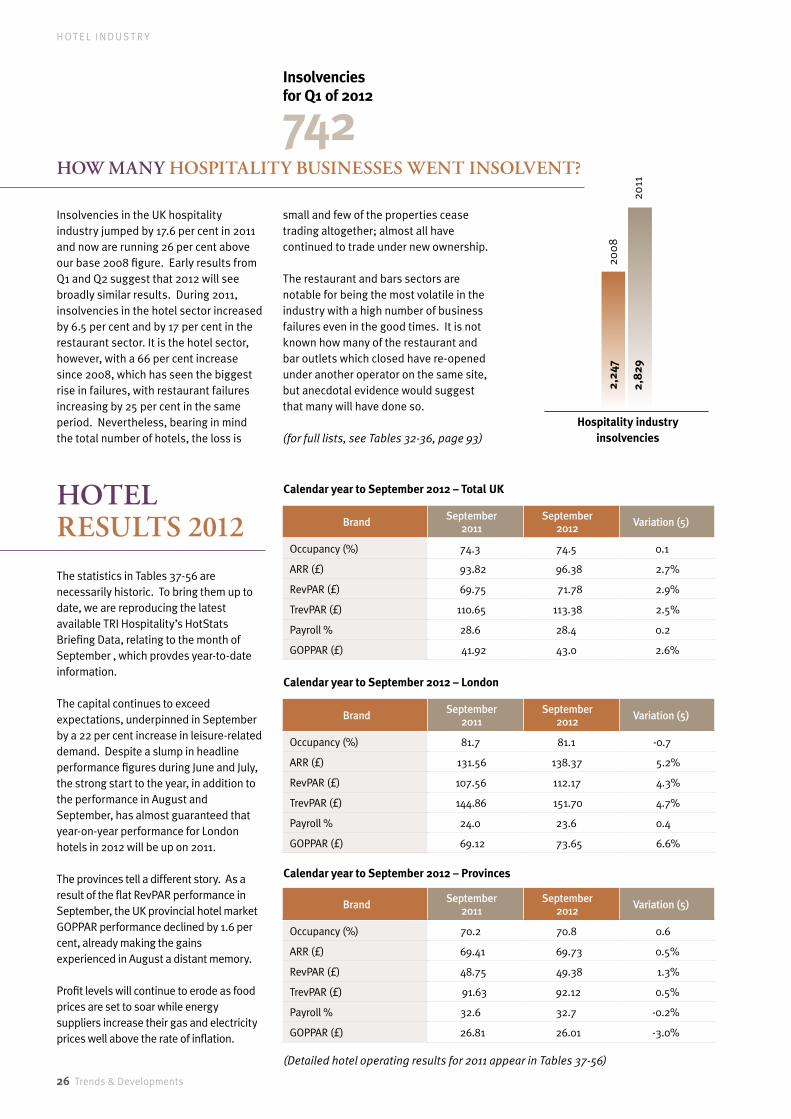

HOw mAnY HOsPiTALiTY BUsinEssEs wEnT insOLvEnT?

HOTEL REsULTs 2012

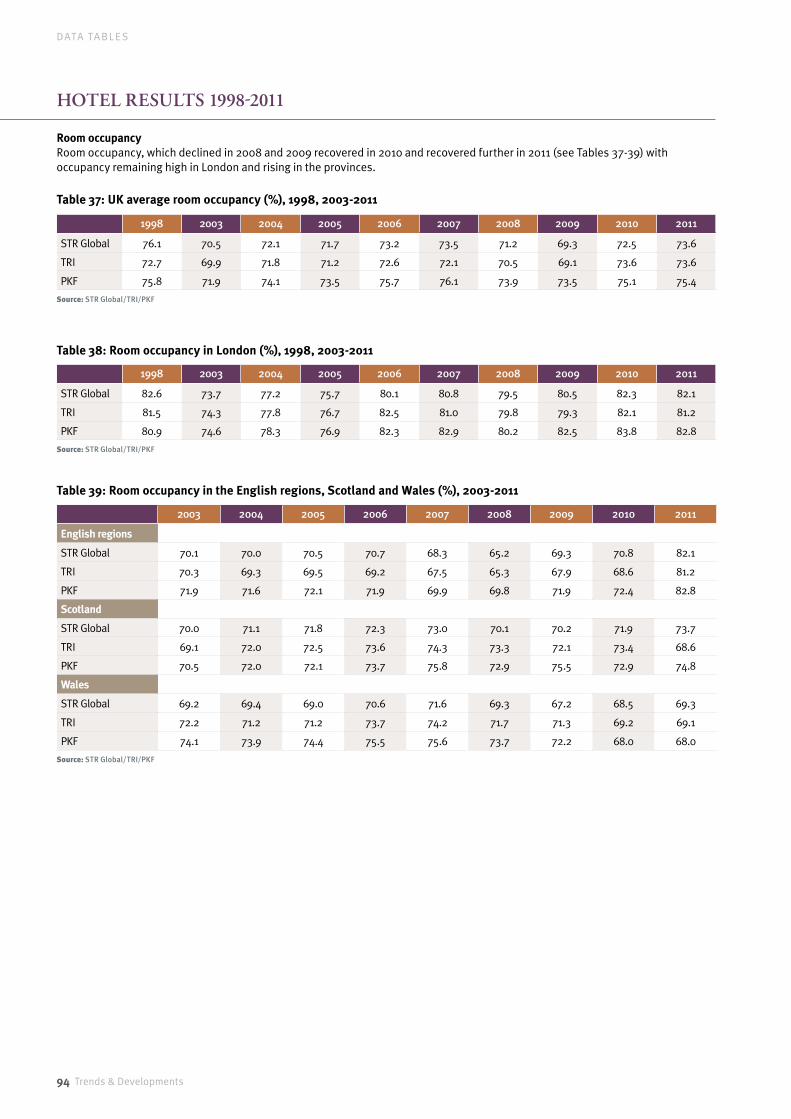

Insolvencies in the UK hospitality industry jumped by 17.6 per cent in 2011 and now are running 26 per cent above our base 2008 figure. Early results from Q1 and Q2 suggest that 2012 will see broadly similar results. During 2011, insolvencies in the hotel sector increased by 6.5 per cent and by 17 per cent in the restaurant sector. It is the hotel sector, however, with a 66 per cent increase since 2008, which has seen the biggest rise in failures, with restaurant failures increasing by 25 per cent in the same period. Nevertheless, bearing in mind the total number of hotels, the loss is

small and few of the properties cease trading altogether; almost all have continued to trade under new ownership.

The restaurant and bars sectors are notable for being the most volatile in the industry with a high number of business failures even in the good times. It is not known how many of the restaurant and bar outlets which closed have re-opened under another operator on the same site, but anecdotal evidence would suggest that many will have done so.

(forfulllists,seeTables32-36,page93)

The statistics in Tables 37-56 are necessarily historic. To bring them up to date, we are reproducing the latest available TRI Hospitality’s HotStats Briefing Data, relating to the month of September , which provdes year-to-date information. The capital continues to exceed expectations, underpinned in September by a 22 per cent increase in leisure-related demand. Despite a slump in headline performance figures during June and July, the strong start to the year, in addition to the performance in August and September, has almost guaranteed that year-on-year performance for London hotels in 2012 will be up on 2011.

The provinces tell a different story. As a result of the flat RevPAR performance in September, the UK provincial hotel market GOPPAR performance declined by 1.6 per cent, already making the gains experienced in August a distant memory.

Profit levels will continue to erode as food prices are set to soar while energy suppliers increase their gas and electricity prices well above the rate of inflation.

Hospitality industryinsolvencies

2008

2011

2,24

7

2,8

29

742Insolvencies for Q1 of 2012

Brand September 2011

September 2012 Variation (5)

Occupancy (%) 74.3 74.5 0.1

ARR (£) 93.82 96.38 2.7%

RevPAR (£) 69.75 71.78 2.9%

TrevPAR (£) 110.65 113.38 2.5%

Payroll % 28.6 28.4 0.2

GOPPAR (£) 41.92 43.0 2.6%

Brand September 2011

September 2012 Variation (5)

Occupancy (%) 81.7 81.1 -0.7

ARR (£) 131.56 138.37 5.2%

RevPAR (£) 107.56 112.17 4.3%

TrevPAR (£) 144.86 151.70 4.7%

Payroll % 24.0 23.6 0.4

GOPPAR (£) 69.12 73.65 6.6%

Brand September 2011

September 2012 Variation (5)

Occupancy (%) 70.2 70.8 0.6

ARR (£) 69.41 69.73 0.5%

RevPAR (£) 48.75 49.38 1.3%

TrevPAR (£) 91.63 92.12 0.5%

Payroll % 32.6 32.7 -0.2%

GOPPAR (£) 26.81 26.01 -3.0%

Calendar year to September 2012 – Total UK

Calendar year to September 2012 – London

Calendar year to September 2012 – Provinces

(Detailedhoteloperatingresultsfor2011appearinTables37-56)

I N T RO DU C T I O N

Trends & Developments 27

H OT E L I N DUS T RY

HOTEL vALUEs

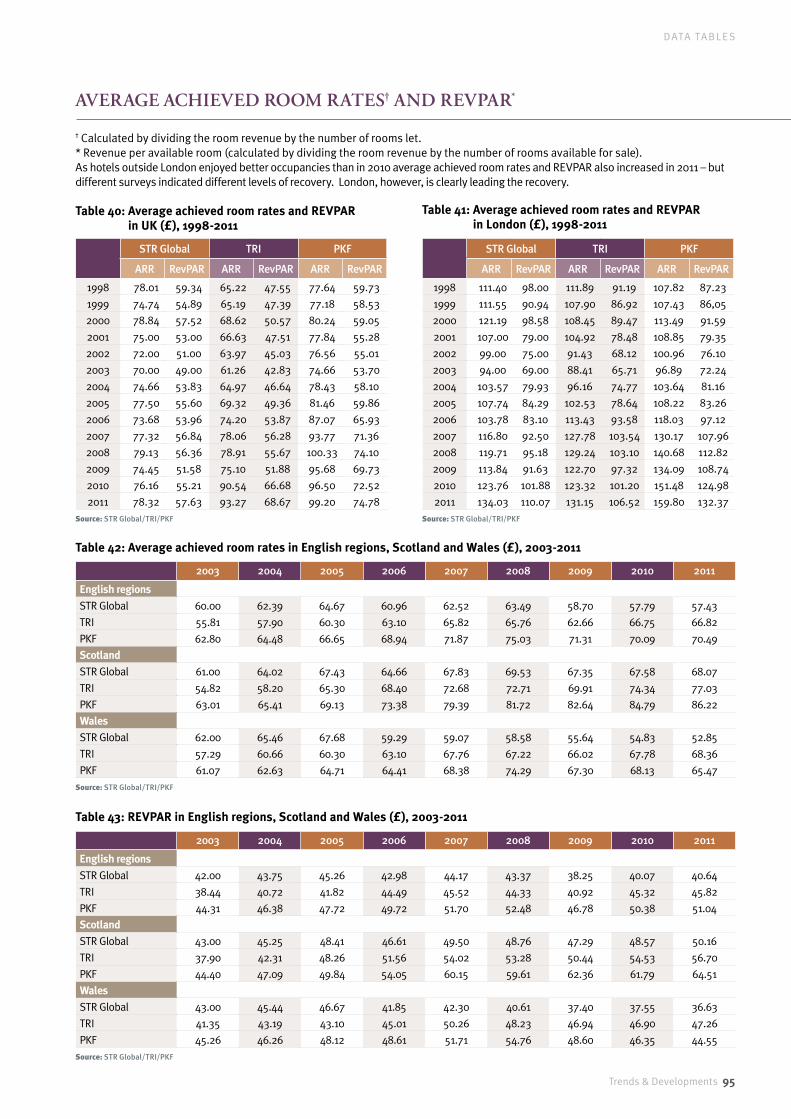

According to consultancy HVS, hotel values are climbing back to their 2006 peak, increasing in London in 2011 by 12.0 per cent, in Edinburgh by 1.7 per cent, in Manchester by 0.2 per cent but falling in Birmingham by 6.7 per cent. These changes, which brought the capital back to its peak values of 2006/2007, reflected London’s continuing emergence from the recession as it benefits from stronger corporate and leisure demand as well as its position as a global financial centre. Edinburgh, which is the UK’s second most popular business destination, also made progress. Manchester, however, saw little growth while Birmingham, with over 600 rooms added in 2011 – and with more planned – saw hoteliers chasing occupancy rather than rates, and hotel values fell by 6.7 per cent. London remains one of the

leaders of recovery in Europe, with room values second only to Paris (€630,928) and considerably above third placed Zurich (€518,496). HVS Index monitors changes in the values of mainly four- and five-star hotels in key European cities. We give only UK cities here. The methodology employed is based on operating data from a representative sample of hotels, which is then aggregated. In arriving at each valuation, HVS takes into account its own valuation experience, as well as current trends in the market place. (Tables60-62,page101)

Hotel ownership has now become an international investment, which is clearly demonstrated by the continuing purchase of trophy assets across Paris and London by private individuals and funds. Growth becomes more prominent from 2013 onwards for most cities with London and Paris again leading the way, followed by Zurich and Geneva. These cities already have high occupancies but further rate increases are expected to push up values.

Lond

on

Edin

burg

h

Man

ches

ter

Bir

min

gham

11%

23%

20%

27%

Lond

on

Edin

burg

h

Man

ches

ter

Bir

min

gham

4%

-1%

-22%

-38

%

Hotel valuation per room since 2000

Forecast increase hotel valuation 2012-2016

Increase/decrease in hotel valuation since 2000

Edinburgh

-1%

Manchester

-2%

Birmingham

-38%

London

4%

Trends & Developments 27

28 Trends & Developments

H OT E L I N DUS T RY

The term “lost decade” was first applied to the Japanese economy during the 1990s and, following a five-year period of inactivity which is in danger of continuing, it might also provide a fitting description for the UK.