brands and innovation final2 - unilever global … / project / country 7x projectsin 10+ countries...

TRANSCRIPT

Unilever 2010 Investor Seminar

Singapore

Winning with Brands and Innovation

Michael Polk / Geneviève Berger

Agenda

• Progress

• Sharpening the choices

• Bigger, better, faster innovation

• R&D

Strongest volume in 25 years

categories

11/11

MCO’s

19/22

top brands

12/13

6% volume growth year-to-date

Tremendous leverage in our brands

17>€0.5bn

34>€250mn

11>€1bn

Fit to compete in battlegrounds

fabric cleaningIndia

>100bps

18%

fabric cleaningTurkey

5%

>100bps

fabric cleaningThailand

7%

>100bps

Ability to price where necessary

spreadsUK

170bps

5%

dressingsUS

40bps

2%

deodorantsIndonesia

700bps

4%

Bigger Faster

roll-out +30 marketsin 6 months

+€50m innovationturnover year 1

Growth: bigger, faster innovation

Growth: better products

€100m investment inproduct quality

40% reduction inconsumer complaints

Design Delivered

-50%

-40%

quality incidents complaints

Growth: more sustainable products

RAW MATERIALS MANUFACTURE CONSUMER USE DISPOSALTRANSPORT

three big targets across the total value chain

HELP

1 BILLIONPEOPLE IMPROVE

THEIR HEALTH& WELLBEING

HALVEENVIRONMENTAL

FOOTPRINT OFOUR PRODUCTS

SOURCE

100%OF AGRICULTURAL

RAW MATERIALSSUSTAINABLY

Growth: brand deployment

Latin AmericaChina Indonesia

Japan/Bangladesh Indonesia Equador

France Indonesia Nigeria

Growth: repeatable models

Oral Care Market Development Model

Growth: effective marketing

>100mm views46mm unique visitors

4,617,493heart ages tested

Growth: effective advertising

% of ads falling into Green/ Amber/ Red boxes onthe Communication Effective Matrix

Ice Cream Greece Hair Global Tomatoes BrazilDisposal

Growth: strengthening portfolio

Ice Cream Denmark Frozen ItalyDisposal

Hair Global

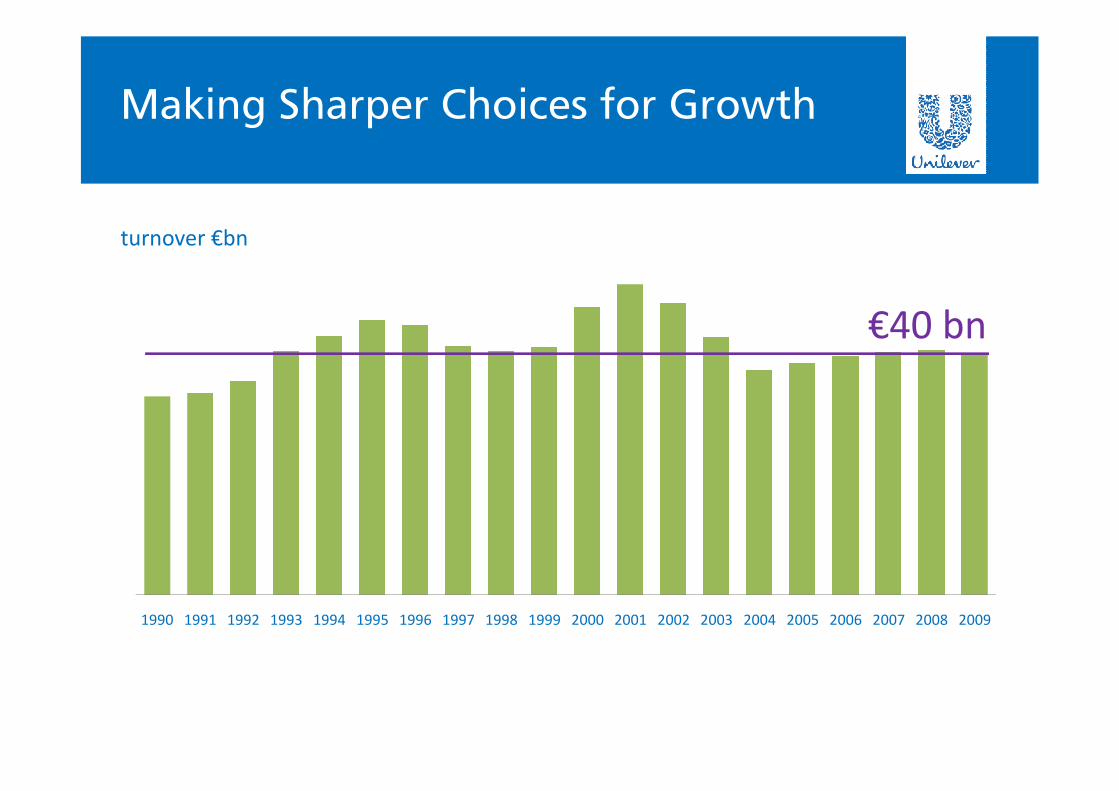

Making Sharper Choices for Growth

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

turnover €bn

€40 bn

Categories report against 4 platforms

Fabrics &Surface

Care

PersonalCare

FoodsIce Cream &Beverages

Fabric Cleaning

Fabric Conditioning

Household Care

Deos

Skin

Hair

Oral Care

Ice Cream

Tea

Soy Beverage

Spreads

Dressings

Savoury

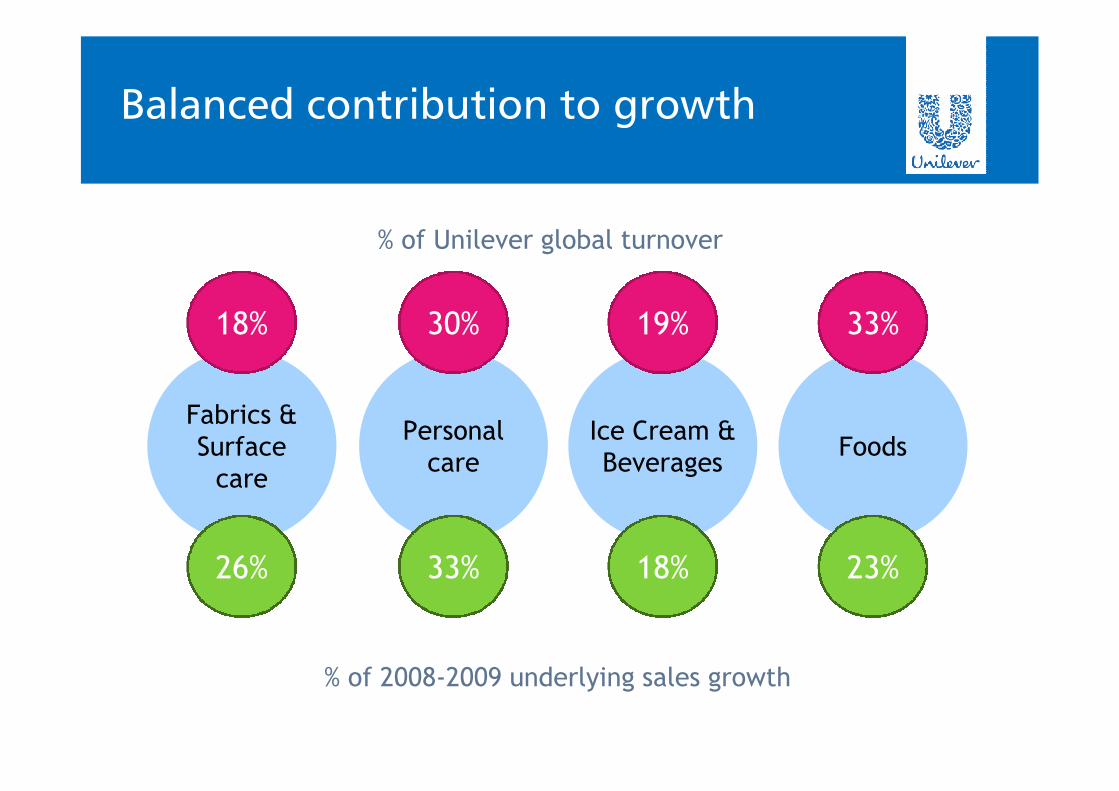

Different contribution to turnover

Fabrics &Surface

care

Personalcare

FoodsIce Cream &Beverages

% of Unilever global turnover

18% 30% 19% 33%

Balanced contribution to growth

Fabrics &Surface

care

Personalcare

FoodsIce Cream &Beverages

% of Unilever global turnover

18% 30% 19% 33%

26% 33% 18% 23%

% of 2008-2009 underlying sales growth

With different business dynamics

big global markets

markets start early in income spectrum

more common ‘global’ habits

disruptive innovation creates advantage

toughest competition

strong D&E Unilever market share

Fabrics &Surface

care

Personalcare

FoodsIce Cream &Beverages

Fabrics &Surface

care

Personalcare

FoodsIce Cream &Beverages

big global markets

at home and out-of-home

impulse purchase

technology can create advantage

unique business system (frozen, RTD)

strong global market shares

With different business dynamics

Fabrics &Surface

care

Personalcare

FoodsIce Cream &Beverages

mature, smaller categories

developed world dominated

products not as transferable

technology less disruptive

market development key

strong brands matter

With different business dynamics

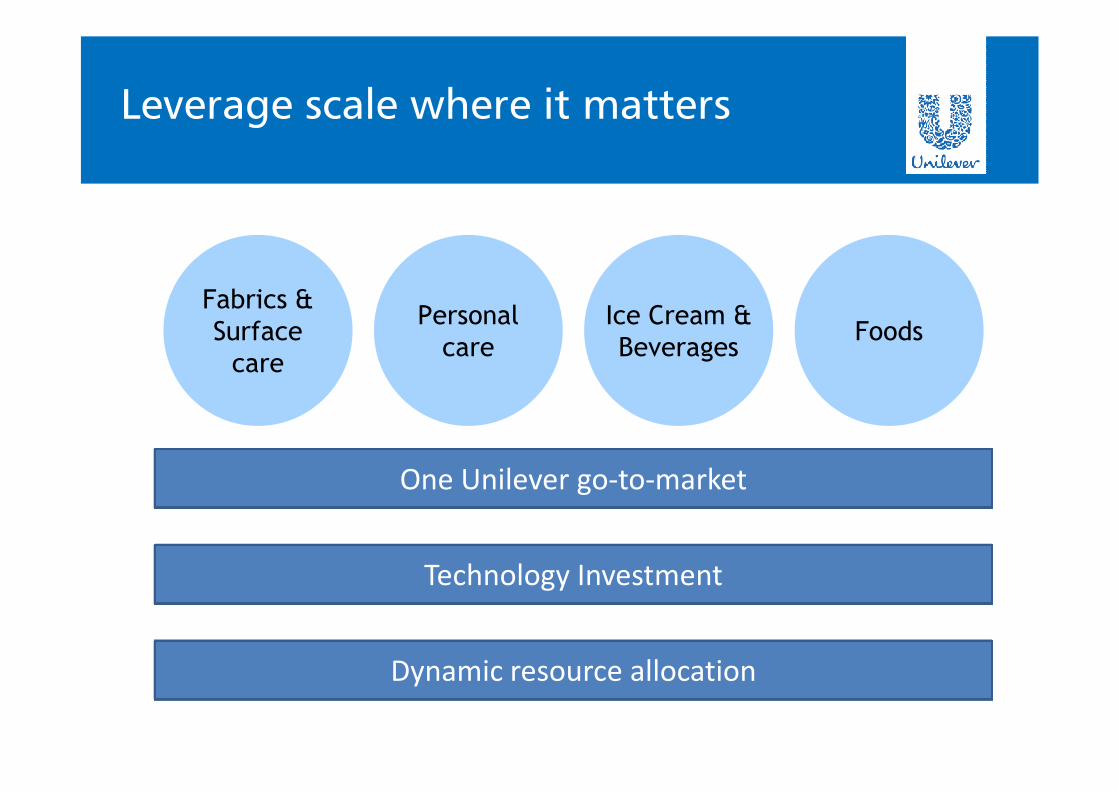

Leverage scale where it matters

One Unilever go-to-market

Technology Investment

Dynamic resource allocation

Fabrics &Surface

care

Personalcare

FoodsIce Cream &Beverages

Leverage the differences as well

59%

41%

24%

76% 69%

31%42%

58%

PersonalCare

Ice Cream &Beverages

FoodsFabrics &

Surface care

D&E Developed

Foods is developed world led

14 key cells > 40% of businessGeographic footprint

Sauces & others

Soups

Meals & sides

Frozen meals

US, Germany

Germany,France, NL

N America, Germany

USA

Spreads

Dressings

N America, Germany, UK

N America, France, Brazil

Developed

D&E31%

69%

Habits govern expansion potential

0

5000

10000

15000

20000

0 1000 2000 3000

Spreads market size €m

Bre

adm

arke

tsi

ze€

m

Spreads & Breads Markets Correlate Win Where We Are

D&E vs D % of Sales

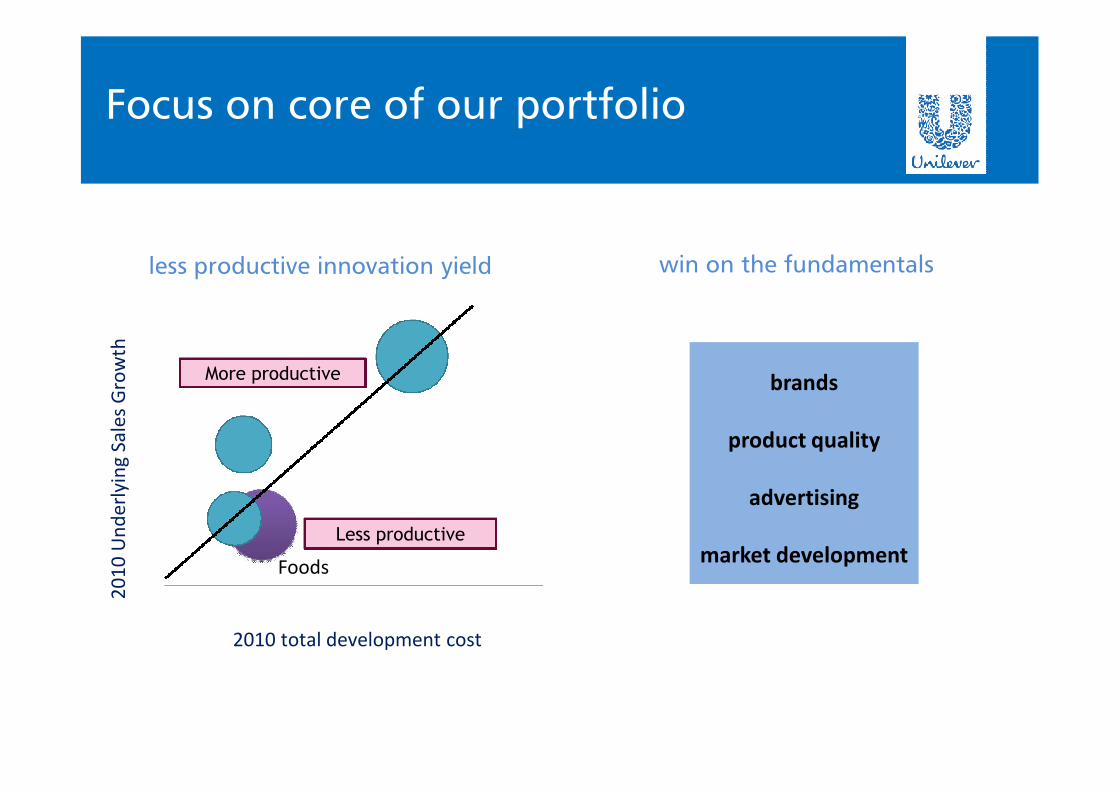

Focus on core of our portfolio

2010 total development cost

20

10

Un

der

lyin

gSa

les

Gro

wth

Less productive

More productive

Foods

less productive innovation yield win on the fundamentals

brands

product quality

advertising

market development

Balance scale and local opportunity

scale global platforms leverage local opportunities

Fabrics and surface care is D&E led

Developed

D&E76%

24%

insidetoilets

+100%

fridgefreezers

+190%

microwaveovens

+130%

washingmachines

+230%

in BRIC alone, by 2020

kitchensinks

+115%

Source: CMI

geographic footprint major market development opportunity

Foundation for emerging markets

0%

25%

50%

75%

100%

Cote D'Ivoire Morocco Vietnam Romania Sri Lanka Bangladesh

Fabrics & Surface Care Rest of portfolio

portfolio composition (% total turnover)

Opportunity to reach more than we do

Super premium Ice Cream

Machine dishwash

Deodorants

Personal wash liquid

Ice Cream OOH

Fabric solution wash

Shampoo

Toothpaste & Toothbrushes

Bar soap

Small surface cleaners powder

Population Reach

6 bn

3.9bn

1.8bn

0.9bn

2.4bn

0 5000 10000 15000 20000 25000

GDP / capita $

$350

penetration opportunity portfolio deployment opportunity

Country DIG Skip Surf FabCon

Romania

UK

Finland

Norway

Austria

Sweden

Belgium

Pakistan

South Africa

ANZ

Malaysia

Algeria

Morocco

Tunisia

Turkey

French R. Africai

Ghana

Gulf ii

China

Philippines

Brazil

Ice Cream & Beverages global & big

massive, global markets

38 billion liters market of tea

Ice Cream €50bn+ market

leading positions

Brand leaders and innovators

leaders in innovationpower brands

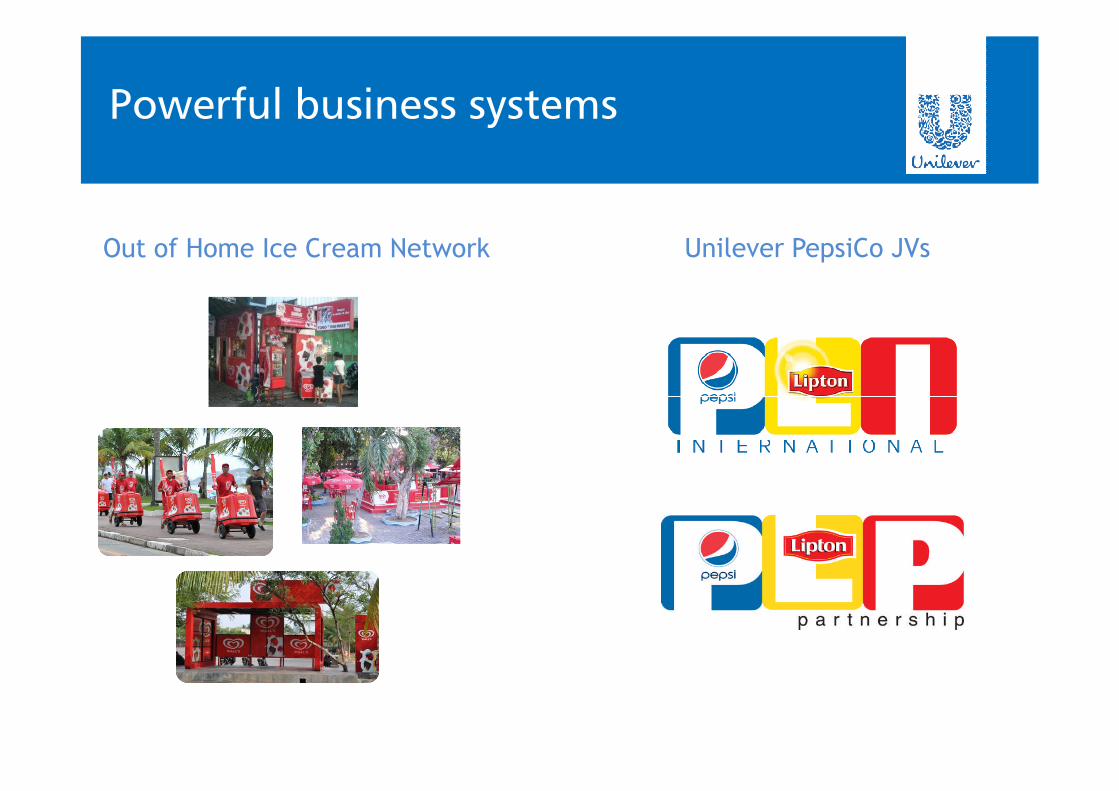

Powerful business systems

Out of Home Ice Cream Network Unilever PepsiCo JVs

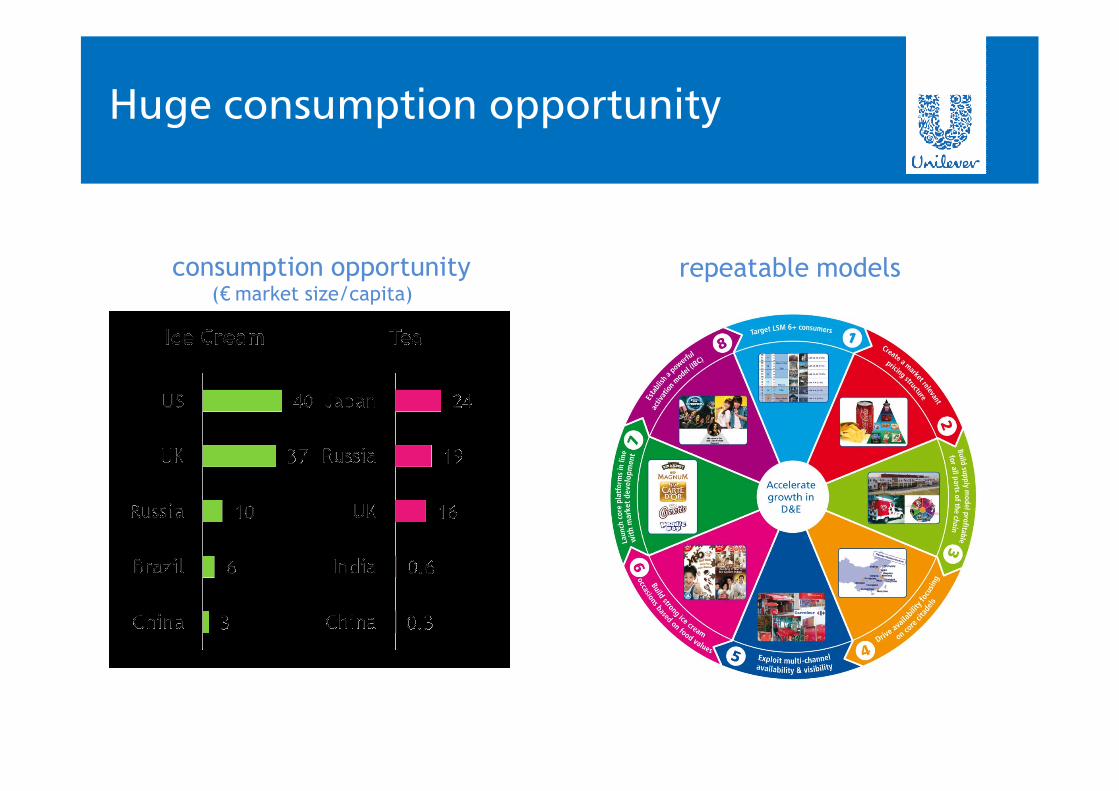

Huge consumption opportunity

repeatable modelsconsumption opportunity(€ market size/capita)

Strengthen agenda with M&A

Partnership

Russia USA Denmark Greece

Personal Care most global business

Developed

D&E58%

42% Developed

D&E53%

47%

Pre-acquisitions Post-acquisitions

Famous and powerful brands

Top 10 brands >€10bn turnover

Innovation and marketing driven

Pond’s Gold Radiance Clear Relaunch

Dove Hair Relaunch Dove Men+Care

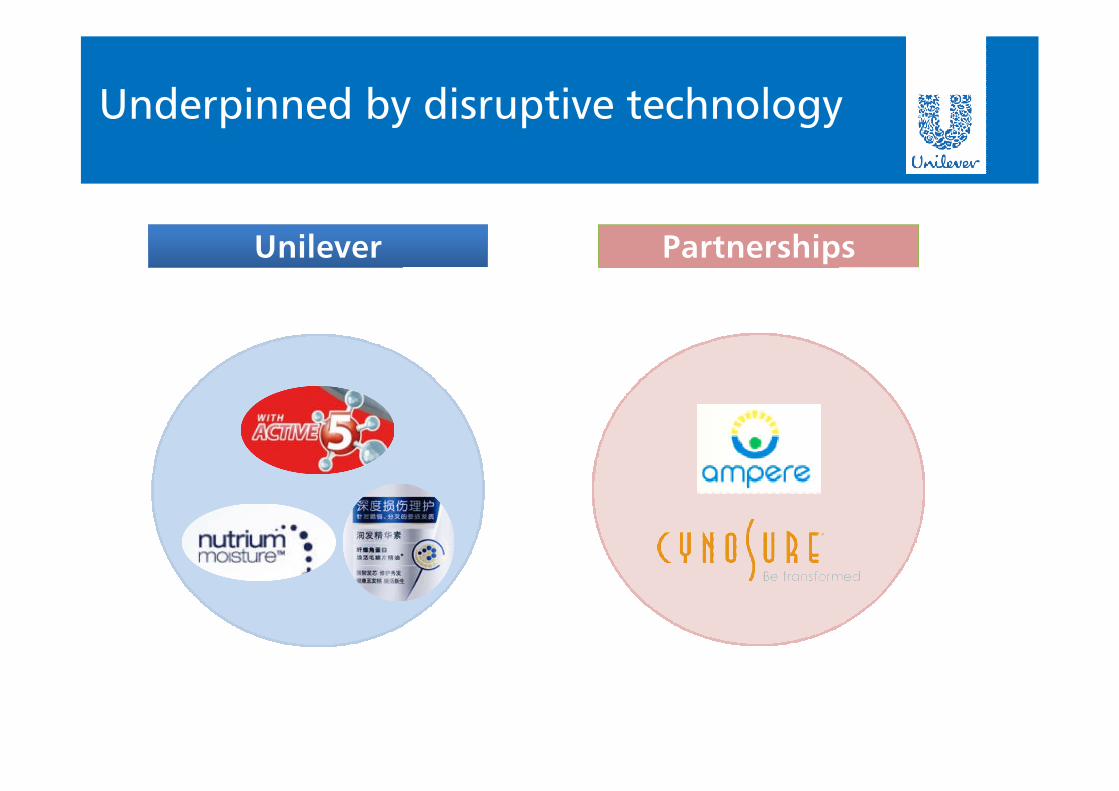

Underpinned by disruptive technology

Unilever Partnerships

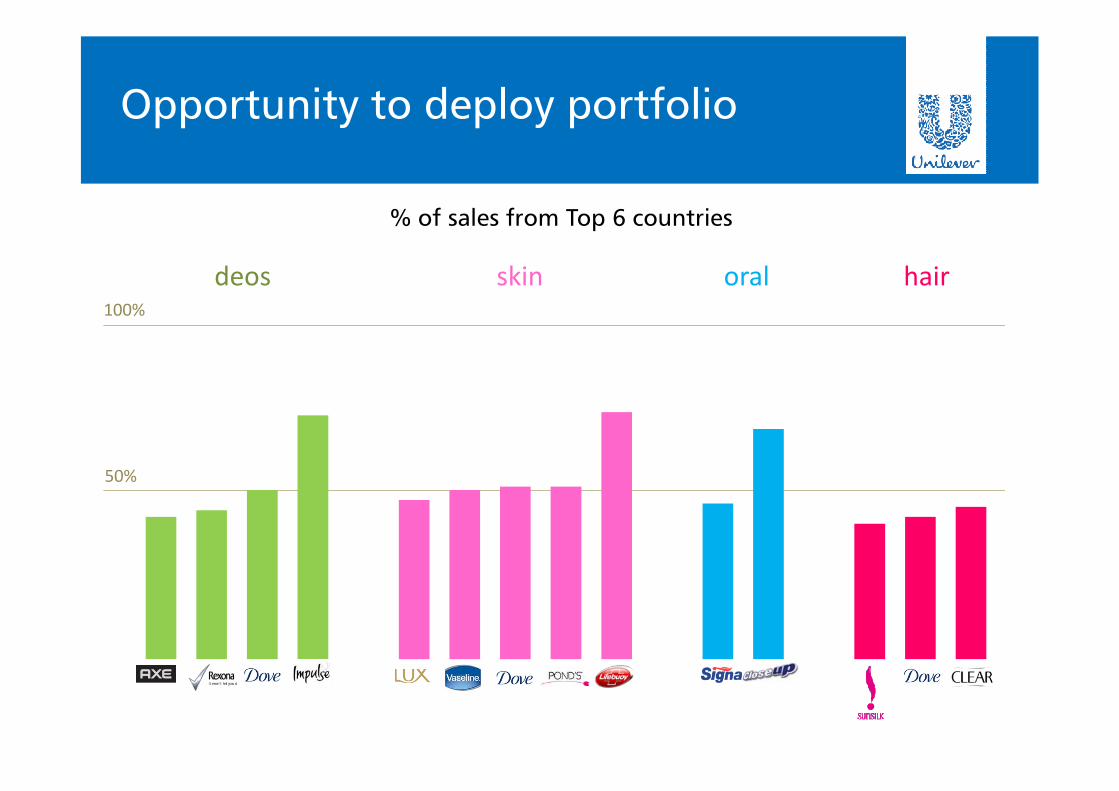

Opportunity to deploy portfolio

oraldeos hairskin100%

50%

% of sales from Top 6 countries

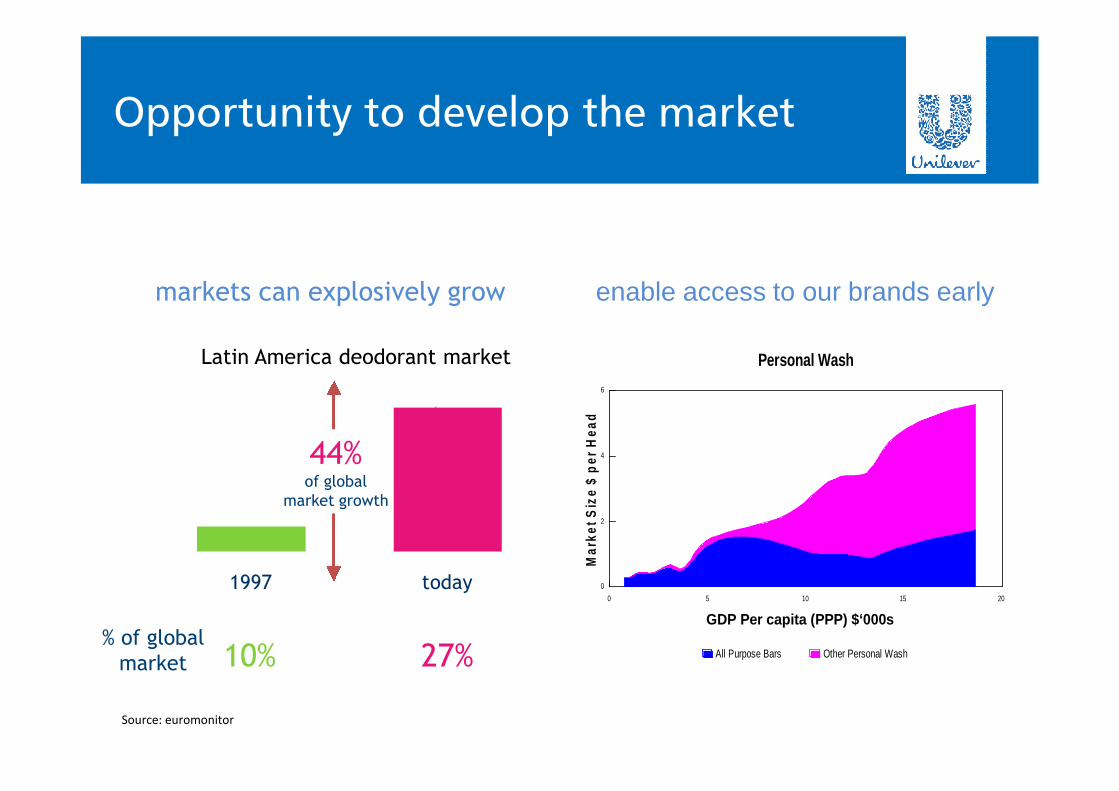

Opportunity to develop the market

538

3,100

1997 today

Latin America deodorant market

27%% of global

market 10%

44%of global

market growth

Source: euromonitor

markets can explosively grow

0 5 10 15 20

0

2

4

6

Thousands

Spending per Head $ (PPP) '000's

Ma

rke

tS

ize

$p

er

He

ad

All Purpose Bars Other Personal Wash

Personal Wash

GDP Per capita (PPP) $‘000s

enable access to our brands early

Strengthen agenda with M&A

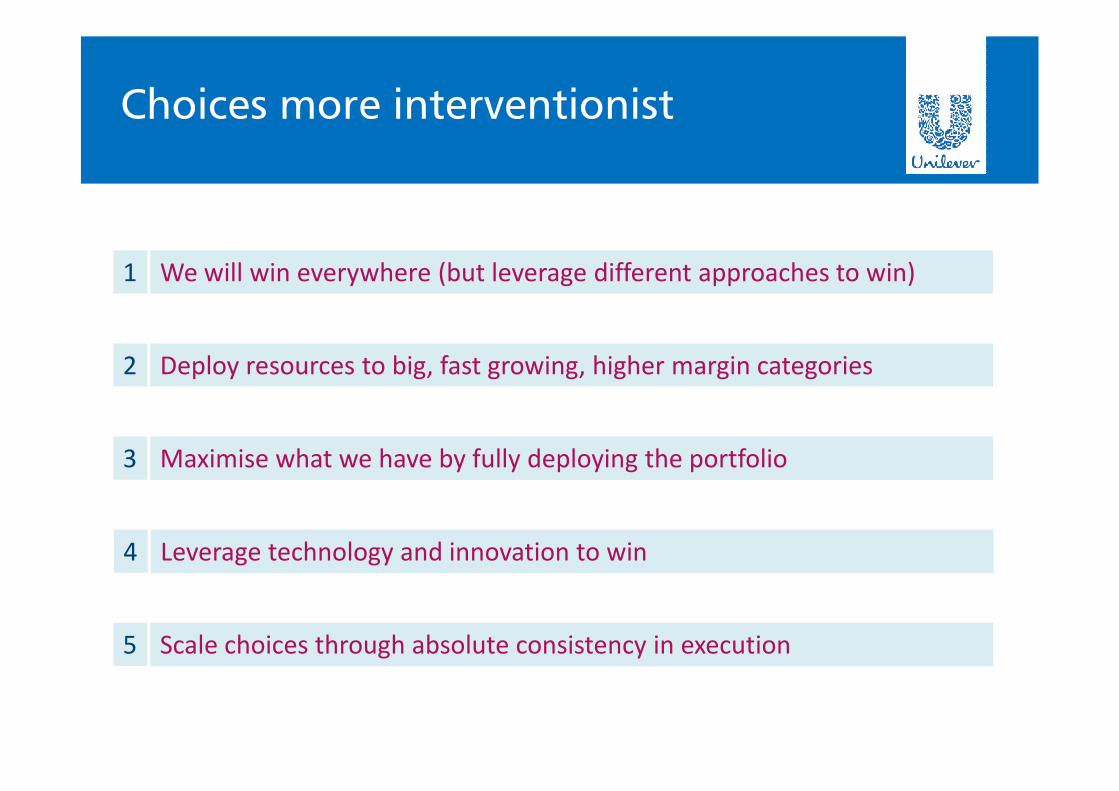

Choices more interventionist

Deploy resources to big, fast growing, higher margin categories2

We will win everywhere (but leverage different approaches to win)1

Scale choices through absolute consistency in execution5

Maximise what we have by fully deploying the portfolio3

Leverage technology and innovation to win4

Enabled by new ways of working

StrengthenedCapabilities

New businessmodels

Categoryintervention

Disciplined useof resources

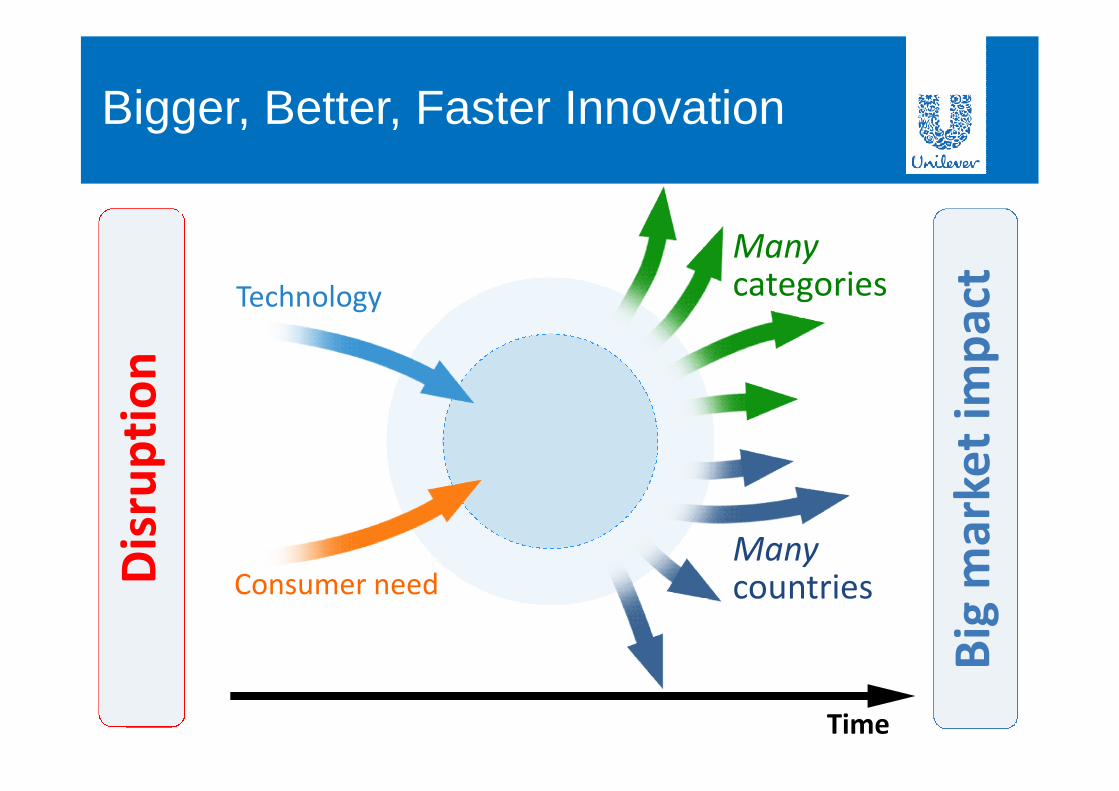

Disruptive innovation key to success

Bigger

Platform based

Cross-category

Technology led

Global roll-out

Better

New claimable benefits

Superior products

Proprietary technology

World-Class Design

Faster

Speed in development

Fast to market

Marketed aggressively

Intelligent risk taking

Working together seamlessly

Consumer needsMarketing

Customer needsCustomer Development

TechnologyR&D

Brand conceptsCategory

Progress across the metrics

bigger+75%

iTO / project /country

7xprojects in

10+ countries

better

€100minvestmentin quality

faster

35markets

50markets

30+6x

€50miT/o AxeHair US

Yr 1

Unilever 2010 Investor Seminar

Singapore

Winning with Brands and Innovation

Michael Polk / Geneviève Berger

Dis

rup

tio

n

Big

mar

ket

imp

act

Bigger, Better, Faster Innovation

Manycategories

ManycountriesConsumer need

Technology

Time

What does “leveragingacross categories” look like?

Blue whiteningtechnology

In market

Filtration Emulsion scienceSurface

modification

What does “disruptive technology”look like?

Materialsscience

2010

Processscience

2010

Visualisation andmodellingtechniques

2010

Plant/nutritionscience

2010

Structuringscience

2009

How we are building a robustinnovation pipeline

Genesis New waysof innovating

Underpinning supportCriticalfunctional capabilities

Underpinning supportCriticalfunctional capabilities

New waysof innovating

Genesis

How we are building a robustinnovation pipeline

Genesis as it looks at end 2010

Foods

Each fieldwith multipledeliverablesacrosscategories

Fabrics &Surface Care

Personal Care Ice Cream &Beverages

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesis

Genesishas become the way we work

We arelengthening and

strengthening ourinnovation pipelineand are increasing

the value

Dynamic process

On track to deliver

Genesis

Underpinning supportCriticalfunctional capabilities

New waysof innovating

How we are building a robustinnovation pipeline

Open innovationSupplier partnerships

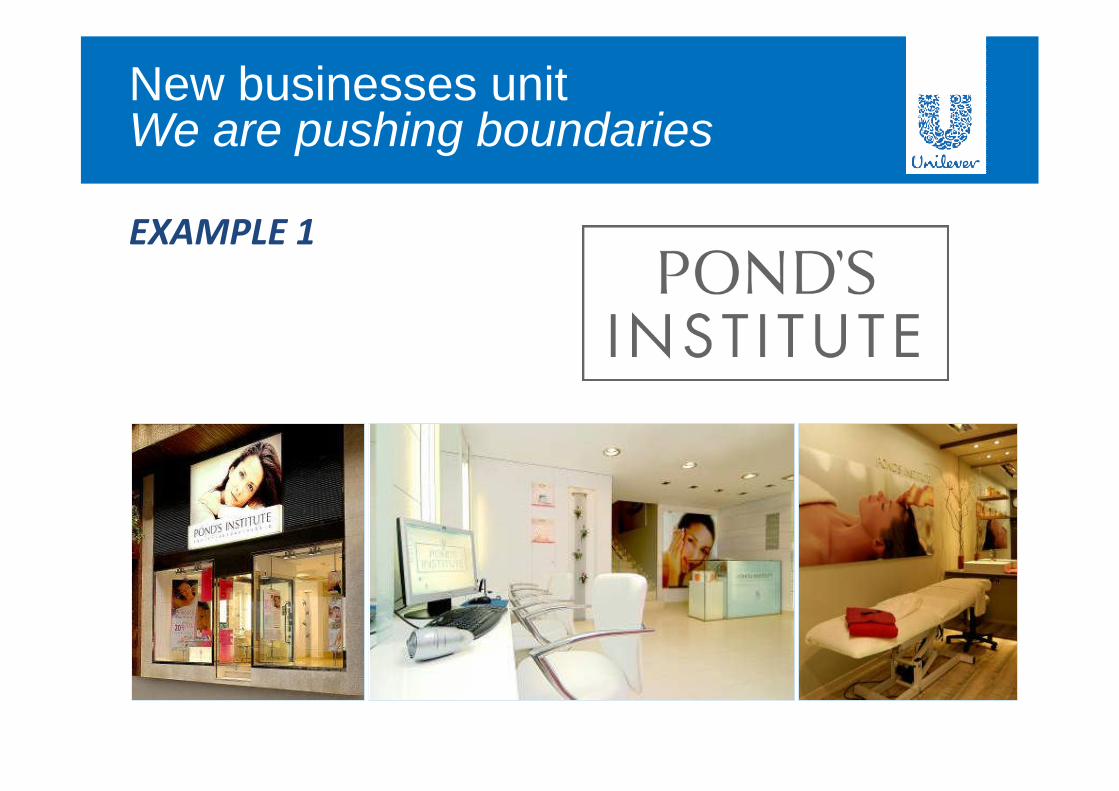

New businesses unit

We are innovating in new ways

48% of Unilever pipelineleverages Open innovation

31% of new products inconsumer staples containexternal technology in 2010*

* Corporate Executive Board -The Research and Technology Executive Council 2010 Budget, Spend, and Performance Survey

New businesses unitWe are pushing boundaries

EXAMPLE 1

New businesses unitWe are pushing boundaries

EXAMPLE 2

AfterCourtesy Robert Weiss, M.D., Hunt Valley, Maryland

Before

An experimentallight-basedsystem to addressfacialrejuvenation

New businesses unitWe are pushing boundaries

EXAMPLE 3

Partnership with Ampere –Spin-off fromEdison Pharmaceuticals

EXAMPLE 4

New businesses unitWe are pushing boundaries

Genesis New waysof innovating

Underpinning supportCriticalfunctional capabilities

How we are building a robustinnovation pipeline

Low High

Accessing global talent

Inventor countries 2006-09

Unilever Company 1

Company 2

Critical functional capabilitiesBuilding strong patent portfolios

EFSA state of play

Critical functional capabilitiesClinical trials to support our claims

Proportion of claims withpositive opinionUnilever

relevant

100%

Industryaverage

~20%

Conclusion

Strong R&D capability• working differently• strong science base

Clear strategy in place• focus, prioritisation, disruption, cross-category

leverage

Strong innovation pipeline• Genesis on track• innovating in new ways

Summary

Confidence to sharpen choices2

Strengthening fundamentals and good performance in tough times1

Scale choices through absolute consistency in execution5

Leverage technology and innovation to win4

3 We will win everywhere (but leverage different approaches to win)