borrowing cost (ias 23) - unisa study...

TRANSCRIPT

Borrowing cost (IAS 23)

Study unit 3

Overview • Definitions

• Accounting treatment - general

• Specific loans

• General loans

• General pool of funds

• Capitalisation period

• Tax

• Disclosure

• Practical examples

Definitions • Borrowing cost

• Interest + other costs

• Incurred by the enterprise

• In connection with the borrowing of funds

• May include

o Interest – effective interest method* (IFRS 9)

o Finance charges – finance leases (IAS 17)

o Exchange differences arising from foreign borrowings to extent

regarded as interest adjustment

• Qualifying asset • Asset

• Substantial time (professional judgement)

• To get ready for intended use/sale

• Exclude assets measured at fair value, e.g. biological assets

Qualifying asset - examples

• Inventory, excluding • Manufactured/produced in large quantities on repetitive basis

• Manufactured/produced over short period of time

• Manufacturing plants

• Power generation facilities

• Intangible assets

• Investment properties (unless measured @ fair

value)

Accounting treatment General

• Directly attributable borrowing cost • Capitalise as part of asset cost

o Still need to meet definition of asset.

o Only capitalise if:

• Future economic benefit is probable

• Cost can be measured reliably

• Borrowing cost not capitalised • Expense in period incurred

• Distinguish between: • Specific loans

• General loans (e.g. bank overdraft)

• General pool of funds

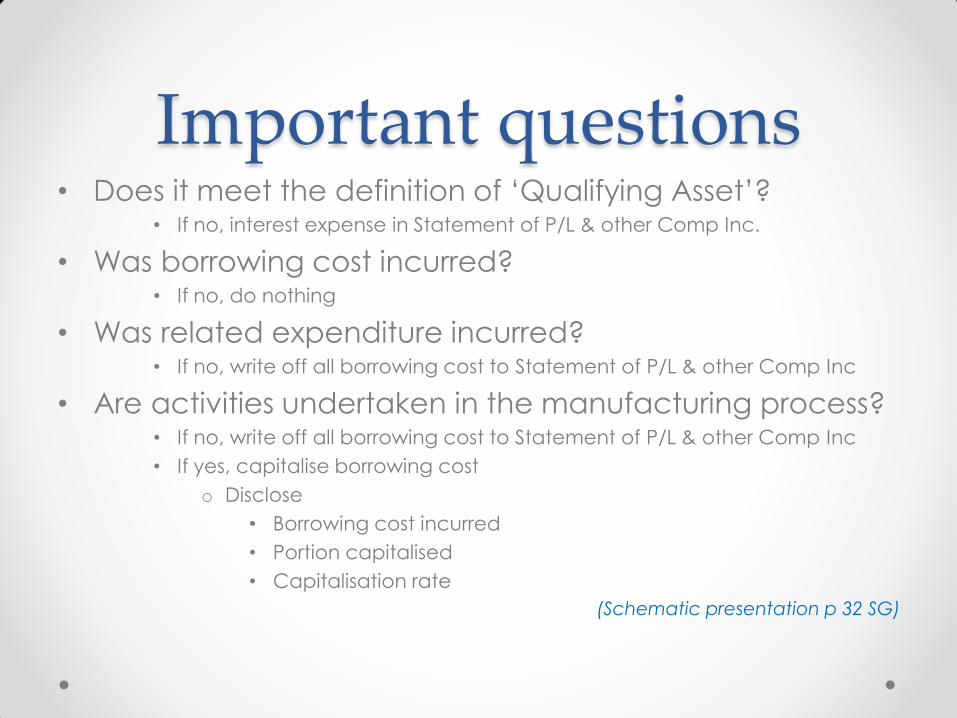

Important questions • Does it meet the definition of ‘Qualifying Asset’?

• If no, interest expense in Statement of P/L & other Comp Inc.

• Was borrowing cost incurred? • If no, do nothing

• Was related expenditure incurred? • If no, write off all borrowing cost to Statement of P/L & other Comp Inc

• Are activities undertaken in the manufacturing process? • If no, write off all borrowing cost to Statement of P/L & other Comp Inc

• If yes, capitalise borrowing cost

o Disclose

• Borrowing cost incurred

• Portion capitalised

• Capitalisation rate

(Schematic presentation p 32 SG)

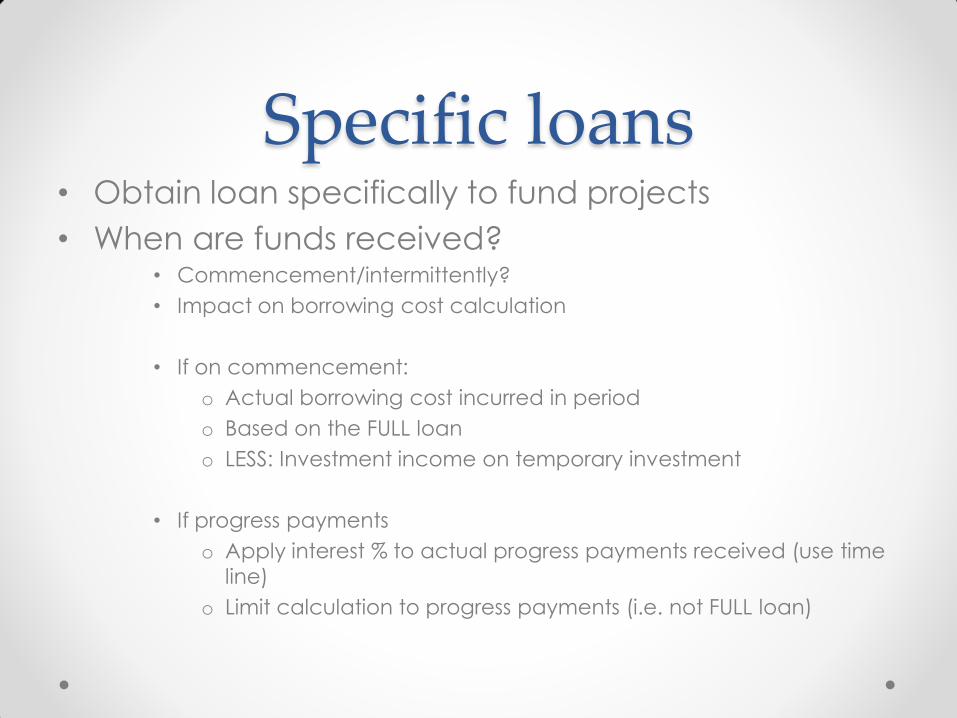

Specific loans • Obtain loan specifically to fund projects

• When are funds received? • Commencement/intermittently?

• Impact on borrowing cost calculation

• If on commencement:

o Actual borrowing cost incurred in period

o Based on the FULL loan

o LESS: Investment income on temporary investment

• If progress payments

o Apply interest % to actual progress payments received (use time

line)

o Limit calculation to progress payments (i.e. not FULL loan)

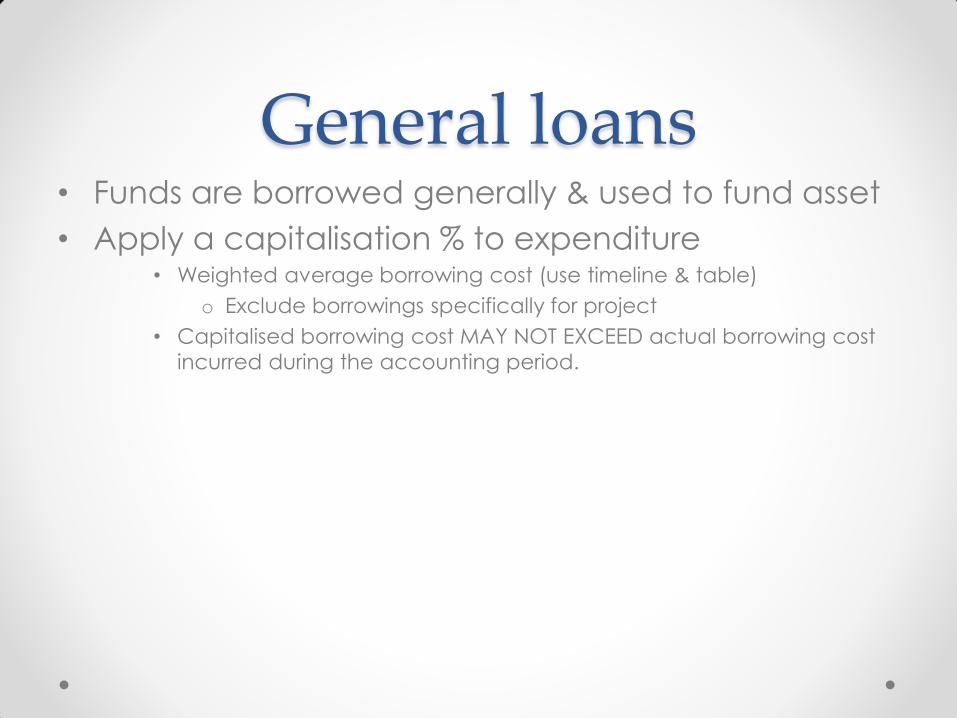

General loans • Funds are borrowed generally & used to fund asset

• Apply a capitalisation % to expenditure • Weighted average borrowing cost (use timeline & table)

o Exclude borrowings specifically for project

• Capitalised borrowing cost MAY NOT EXCEED actual borrowing cost

incurred during the accounting period.

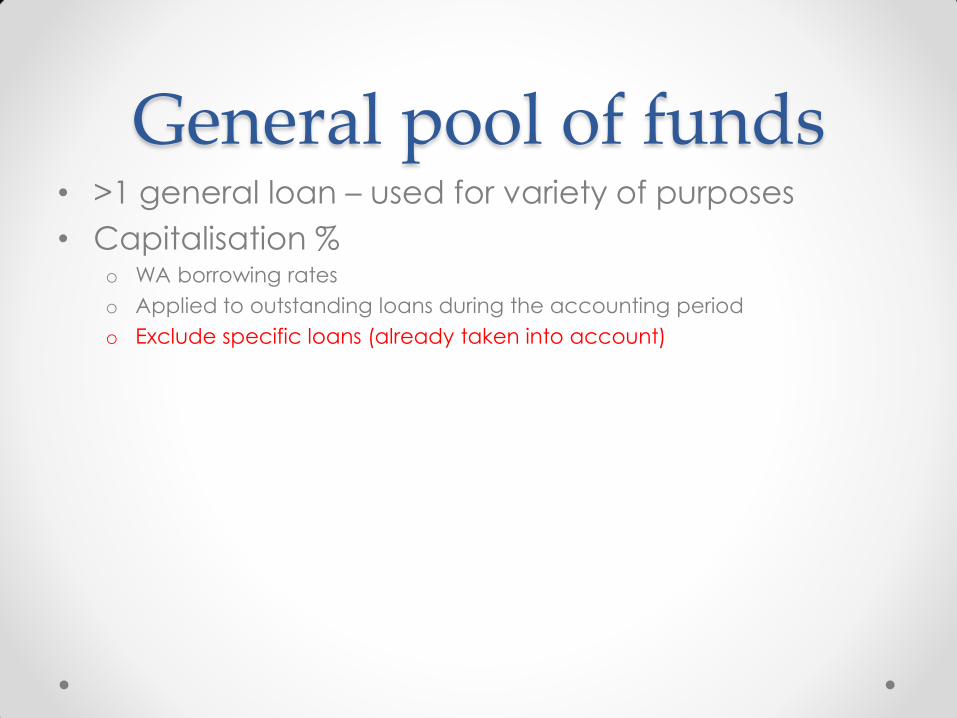

General pool of funds • >1 general loan – used for variety of purposes

• Capitalisation % o WA borrowing rates

o Applied to outstanding loans during the accounting period

o Exclude specific loans (already taken into account)

Capitalisation period • Commencement

• Expenditure for asset is incurred +

• Borrowing costs are incurred +

• Activities necessary to prepare asset for intended use/sale in progress

• Suspension • Extended interruption of active development

• NOT temporary delay - necessary for getting asset ready

• Controlled or beyond control?

• Cessation • Substantially all activities necessary for asset’s preparation completed

• Asset ready for intended use/sale

• Parts

o Each part capable of being used

• Cease when part is completed

o All parts needed to be completed before use/sale

• Cease when WHOLE asset is completed

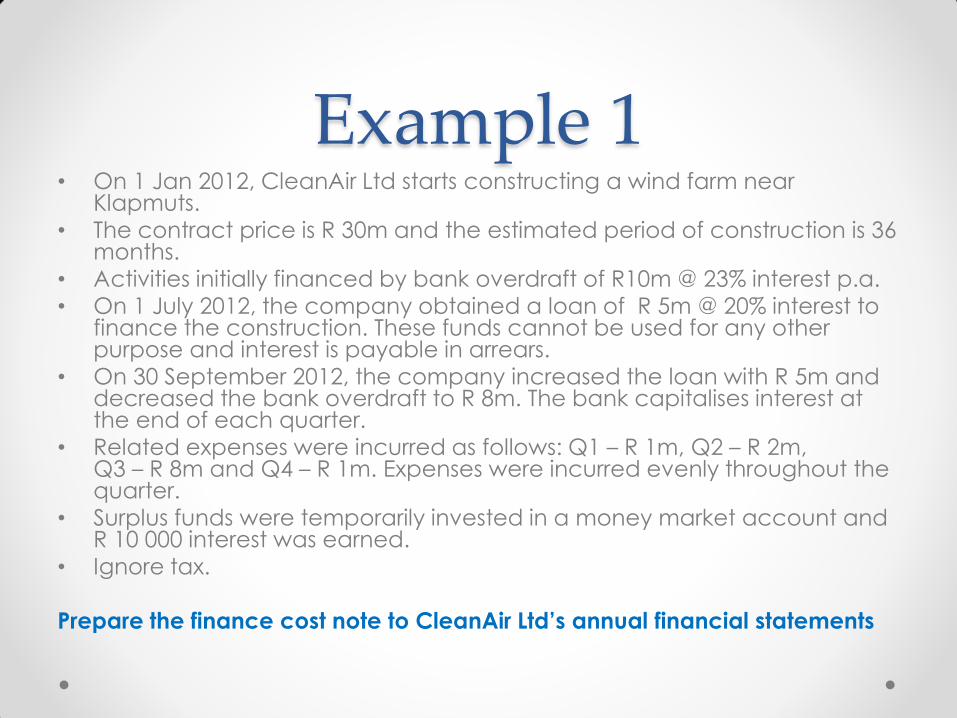

Example 1 • On 1 Jan 2012, CleanAir Ltd starts constructing a wind farm near

Klapmuts. • The contract price is R 30m and the estimated period of construction is 36

months. • Activities initially financed by bank overdraft of R10m @ 23% interest p.a. • On 1 July 2012, the company obtained a loan of R 5m @ 20% interest to

finance the construction. These funds cannot be used for any other purpose and interest is payable in arrears.

• On 30 September 2012, the company increased the loan with R 5m and decreased the bank overdraft to R 8m. The bank capitalises interest at the end of each quarter.

• Related expenses were incurred as follows: Q1 – R 1m, Q2 – R 2m, Q3 – R 8m and Q4 – R 1m. Expenses were incurred evenly throughout the quarter.

• Surplus funds were temporarily invested in a money market account and R 10 000 interest was earned.

• Ignore tax.

Prepare the finance cost note to CleanAir Ltd’s annual financial statements

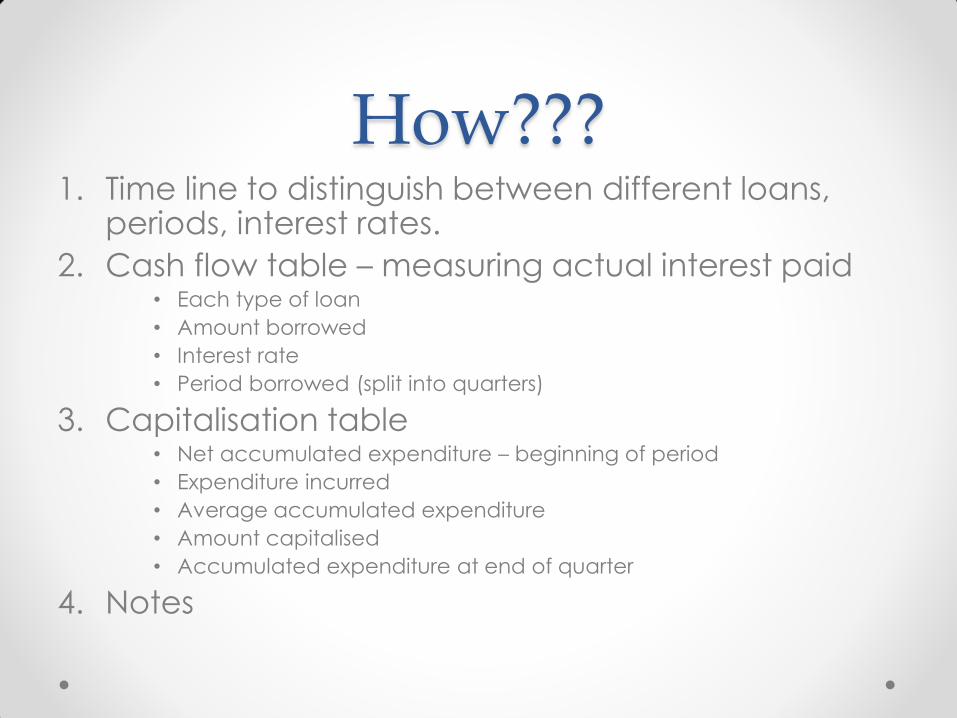

How??? 1. Time line to distinguish between different loans,

periods, interest rates.

2. Cash flow table – measuring actual interest paid • Each type of loan

• Amount borrowed

• Interest rate

• Period borrowed (split into quarters)

3. Capitalisation table • Net accumulated expenditure – beginning of period

• Expenditure incurred

• Average accumulated expenditure

• Amount capitalised

• Accumulated expenditure at end of quarter

4. Notes

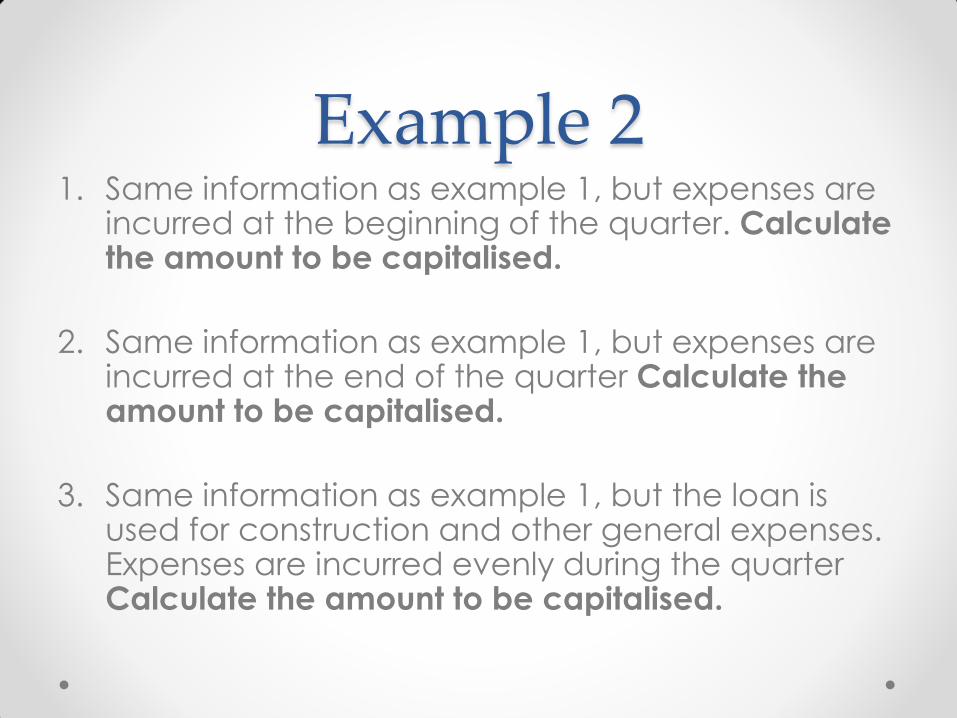

Example 2 1. Same information as example 1, but expenses are

incurred at the beginning of the quarter. Calculate the amount to be capitalised.

2. Same information as example 1, but expenses are incurred at the end of the quarter Calculate the amount to be capitalised.

3. Same information as example 1, but the loan is used for construction and other general expenses. Expenses are incurred evenly during the quarter Calculate the amount to be capitalised.

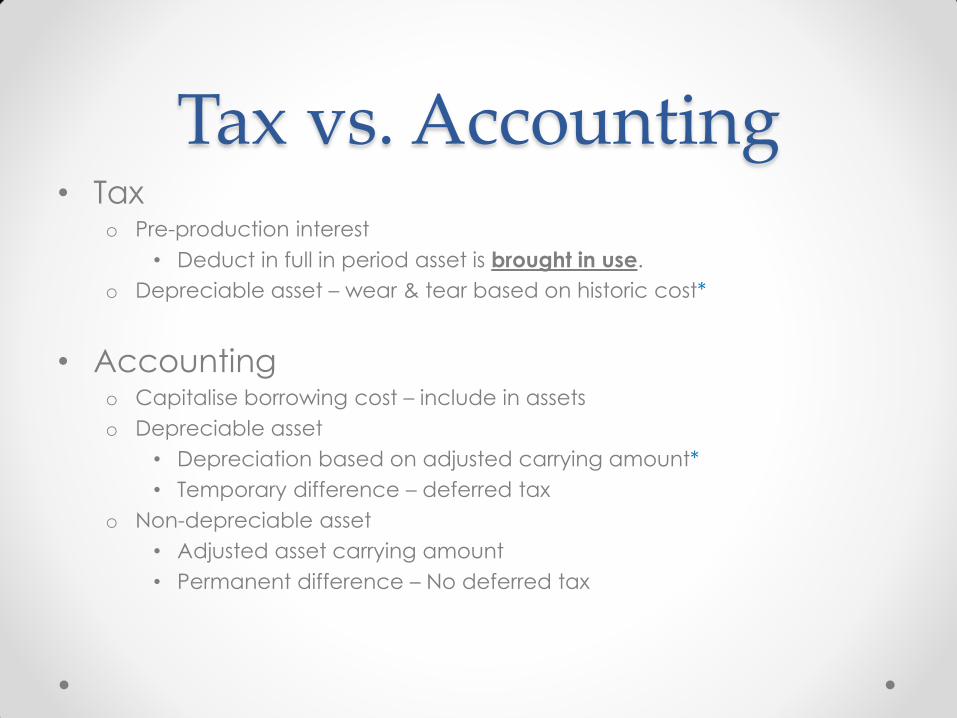

Tax vs. Accounting • Tax

o Pre-production interest

• Deduct in full in period asset is brought in use.

o Depreciable asset – wear & tear based on historic cost*

• Accounting o Capitalise borrowing cost – include in assets

o Depreciable asset

• Depreciation based on adjusted carrying amount*

• Temporary difference – deferred tax

o Non-depreciable asset

• Adjusted asset carrying amount

• Permanent difference – No deferred tax