big call july 2012

TRANSCRIPT

400 W. Wilson Bridge Road, Suite 200, Worthington, OH, 43085 614-846-0146 [email protected]

PAM E L A G O O D F E L L O W

C O N S U M E R I N S I G H T S D I R E C TO R , B I G I N S I G H T ™

G U E S T C O N T R I B U TO R :

E L L E N D AV I S

S E N I O R V I C E P R E S I D E N T, N AT I O N A L R E TA I L F E D E R AT I O N

E X E C U T I V E D I R E C TO R , N R F F O U N D AT I O N

The BIG Call

July 2012

© 2012, Prosper®

July 2012 Consumer Survey

Disclaimer: BIGinsight™ is a trademark of Prosper Business Development Corp. Services are delivered by Prosper and/or a Prosper affiliated company (“Prosper”).

Prosper makes no warranties, either expressed or implied, concerning: data gathered or obtained from any source; the present or future methodology employed in

producing the statistics; or the data and estimates represent only the opinion of Prosper and reliance thereon and use thereof shall be at the user’s own risk.

This report is derived from the following studies:

• BIGinsight™ Monthly Consumer Survey, July 2012 (N = 8509, respondents surveyed 7/2 – 7/9/12)

• BIGinsight™ Monthly Consumer Survey Trends, July 2007 – July 2012

July 2012 Results

• Consumer Confidence

• Employment Outlook

• Practical Purchasing

• 90 Day Outlook: Future Purchase Plans

• Holiday 2012 Spending Preview

Back-to-School Overview with Ellen Davis, NRF SVP

© 2012, Prosper®

Confident/Very Confident in Chances for a Strong Economy Adults 18+

Consumer Confidence

Source: BIGinsight™ Monthly Consumer Survey, JUL 11-12

Highlights:

• Economic sentiment perks up

Up 1+ points from June

Ends two month confidence slide

• Highest confidence reading

headed into the Back-to-School

season since Jul-07 (47.8%)

26.5%

31.3%

32.8%

15%

20%

25%

30%

35%

40%

© 2012, Prosper®

Confident/Very Confident in Chances for a Strong Economy Adults 18+

Consumer Confidence

Source: BIGinsight™ Monthly Consumer Survey, JUL 07-12

26.5%

31.3%

32.8%

15%

20%

25%

30%

35%

40%

47.8

%

18.8

%

27.2

%

27.9

%

26.5

%

31.3

%

32.8

%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jun-12 Jul-12

30%+

decline

from

Jul-07

© 2012, Prosper®

Employment Outlook

Source: BIGinsight™ Monthly Consumer Survey, JUL 10-12

Regarding the U.S. employment environment, over the next 6 months, do you think that there

will be more, the same, or fewer layoffs than at present? Adults 18+

* U.S. Unemployment Rate for the previous month for each corresponding MMM-YY, as reported by the U.S. Bureau of Labor Statistics.

U.S

. U

ne

mp

loym

en

t R

ate

*

La

yo

ff P

red

icti

on

s

Highlights:

• One in four expecting “more”

layoffs over the next six months

Down slightly from June

Thinking bullishly headed into

holiday hiring season?

• Fewer than one in five calling

for “fewer” layoffs

Figure has remained relatively

stagnant over the past three

years

• Employment mantra = more of

the “same.”

Is more of the same “good”

when the unemployment rate

remains in 8-9% territory?

• Personal concerns about

becoming laid off uptick in July

30.8% 29.6% 27.0% 25.9%

55.4%

18.7%

7.6%

7.8%

8.0%

8.2%

8.4%

8.6%

8.8%

9.0%

9.2%

9.4%

9.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jul-10 Jul-11 Jun-12 Jul-12

More Same Fewer U.S. Unemployment Rate*

9.4%*

9.1%

8.2%

8.2%

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, JUL 11-12

Practical Purchasing

In the last 6 months, have you made any of the following changes? Adults 18+

Highlights:

• Practicality off slightly from June

as more consumers cite

confidence in the economy

Nearly half pragmatic in

spending (47.8%)

Down a few points from Jul-

11 (49.9%)

• 56.1% are focused on just the

necessities

Up more than a point from

June, but down two points

from a year ago

• Spending Rebound?

Not so fast: indicators

remain well ABOVE rates

recorded before the “Great

Recession”

40%

42%

44%

46%

48%

50%

52%

54%

56%

58%

60%

Jul-11 Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul-12

I have become more practical and realistic in my purchases

I focus more on what I NEED rather than what I WANT

© 2012, Prosper®

Category: Jun-12 Jul-11 Jul-10 Category: Jun-12 Jul-11 Jul-10

Children’s up up up Toys/Games down up up

Women’s Dress down up up CDs/DVDs/Videos/Books down up up

Women’s Casual down up up Electronics down up up

Men’s Dress down up up Groceries down up up

Men’s Casual down up up Home Improvement down up up

Shoes flat up up Lawn & Garden down up up

HBC up up up Home Furniture flat up up

Dining Out down up up Home Décor down up up

Sporting Goods down up up Linens/Bedding/Draperies down up up

Retail Merchandise Categories - 90 Day Outlook (Jul-12 compared to Jun-12, Jul-11, and Jul-10)

Note: “Up,” Down,” “Flat” refers to the direction of the Diffusion Index compared to the previous month (Jun-12) or years (Jul-11, Jul-10). Diffusion Index = %

Spending More - % Spending Less.

BIG Forward Look: 90 Day Spending

Source: BIGinsight™ Monthly Consumer Survey, JUL 10-12

Over the next 90 days (July, August, and September), do you plan on spending more, the same

or less on the following items than you would normally spend at this time of the year? Adults 18+

© 2012, Prosper® Source: BIGinsight™ Monthly Consumer Survey, JUL 09-12

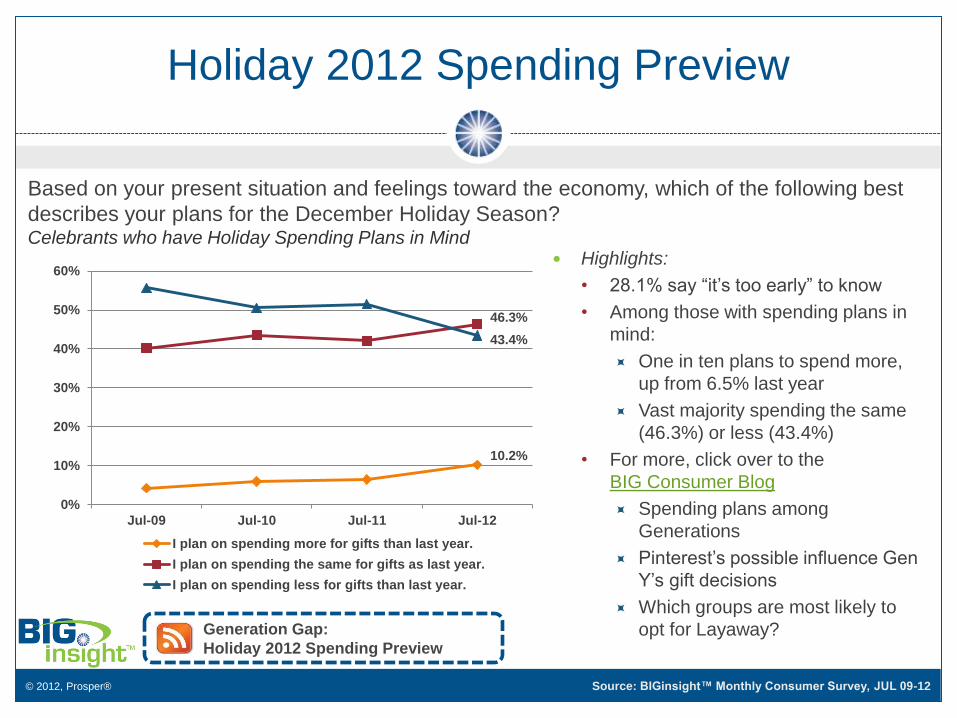

Holiday 2012 Spending Preview

Based on your present situation and feelings toward the economy, which of the following best

describes your plans for the December Holiday Season? Celebrants who have Holiday Spending Plans in Mind

Highlights:

• 28.1% say “it’s too early” to know

• Among those with spending plans in

mind:

One in ten plans to spend more,

up from 6.5% last year

Vast majority spending the same

(46.3%) or less (43.4%)

• For more, click over to the

BIG Consumer Blog

Spending plans among

Generations

Pinterest’s possible influence Gen

Y’s gift decisions

Which groups are most likely to

opt for Layaway?

Generation Gap:

Holiday 2012 Spending Preview

10.2%

46.3%

43.4%

0%

10%

20%

30%

40%

50%

60%

Jul-09 Jul-10 Jul-11 Jul-12

I plan on spending more for gifts than last year.

I plan on spending the same for gifts as last year.

I plan on spending less for gifts than last year.

© 2012, Prosper®

The Economy: Where We’ve Been, Where We’re Going

Retail sales expected to grow 3.4%

this year

• First half 2012 sales grew 4.5%

• Factors behind growth

Warm weather

Inflation

© 2012, Prosper®

Back to School, Back to College 2012

Combined

spending to

total $84 billion

Average parent

of K-12 student

to spend about

$690

Average parent

of college

student to spend

about $900

© 2012, Prosper®

Why the increase?

Replenishment

• Replace what children

had to “make-do” with

last school season

Population growth

• More children entering

elementary and

middle school

© 2012, Prosper®

Economy Remains Top of Mind

More comparison

shopping online

Shopping earlier

• Begin shopping at

least two months

before the start of

school:

2007 = 14.6%

2012 = 22.3%

It’s not all bad news

© 2012, Prosper®

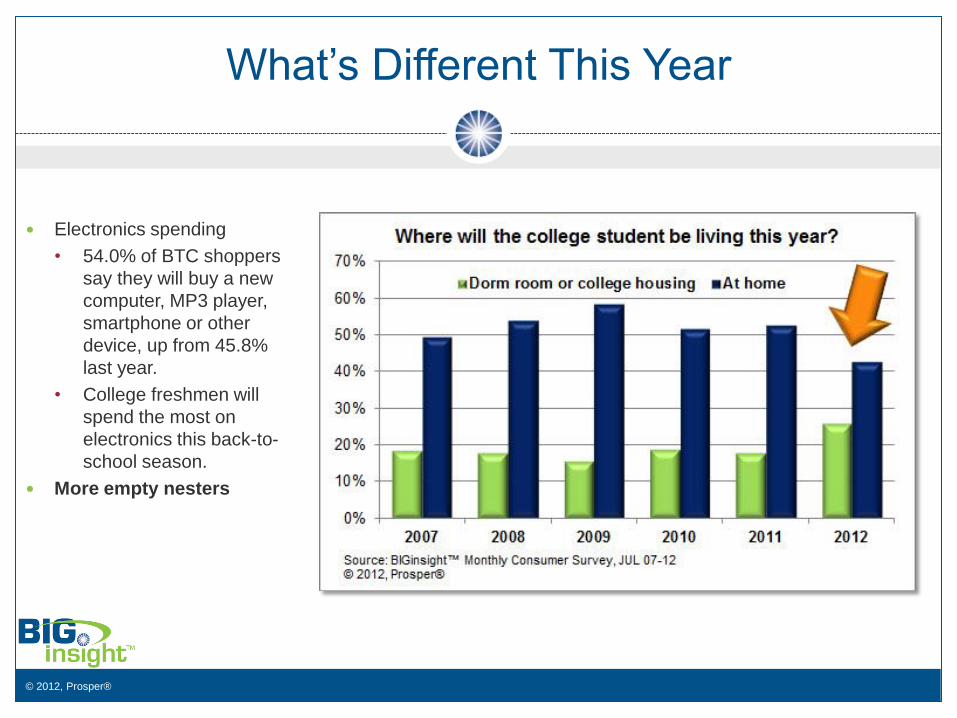

What’s Different This Year

Electronics spending

• 54.0% of BTC shoppers

say they will buy a new

computer, MP3 player,

smartphone or other

device, up from 45.8%

last year.

• College freshmen will

spend the most on

electronics this back-to-

school season.

More empty nesters

© 2012, Prosper®

Retailers’ Recipe for Success

Strong

promotions

Earlier

marketing

Lower

inventory

© 2012, Prosper®

Holiday Implications

What this tells us

What this doesn’t

© 2012, Prosper®

Co

nta

ct

400 W. Wilson Bridge Road

Suite 200

Worthington, OH 43085

Ph: 614-846-0146

for complimentary insights:

www.BIGinsight.com

National Retail Federation

Back-to-School Headquarters

www.nrf.com/backtoschool