before the haryana electricity regulatory commission · pdf filebefore the haryana electricity...

TRANSCRIPT

1 | P a g e

BEFORE THE HARYANA ELECTRICITY REGULATORY COMMISSION AT PANCHKULA

Case No. HERC/PRO-12 of 2016

Date of Hearing : 14.07.2016

Date of Order : 03.10.2016

In the Matter of Application seeking clarification on the order issued by Hon’ble Commission in Suo-

Moto Case No. PRO-15 of 2013 dated 20.11.2013 for determination of Generic Tariff

for Renewable Energy Projects to be commissioned during FY 2013-14 under the

Haryana Electricity Regulatory Commission (Terms and Conditions for Determination

of Tariff for Renewable Energy, Renewable Purchase Obligations and Renewable

Energy Certificates) Regulations, 2010 read with amendments issued from time to

time.

Petitioner

M/s. Star Wire (India) Vidyut Pvt. Ltd., New Delhi

Respondent

Haryana Power Purchase Centre, Panchkula

Present

On behalf of the Petitioner

1. Shri R.K. Jain, Advocate.

On behalf of the Respondents

1. Shri Randhir Singh, AE, HPPC.

2. Shri Vinod S. Bhardwaj, Advocate

Quorum

Shri Jagjeet Singh, Chairman

Shri M.S Puri, Member

ORDER

Brief Background of the Case

1. The Commission, vide order dated 15.5.2007, issued its first tariff order

determining generic tariff for energy generated using renewable sources including

Biomass. The said order was challenged by the petitioner and other stakeholders and

2 | P a g e

the tariff was re-determined by the Commission, as per orders of the Hon’ble Appellate

Tribunal for Electricity, based on the CERC regulations, in the absence of any such

regulations framed by the State Commission. The petitioner participated in the

determination of the first generic tariff and also challenged the said order in the court of

the Hon’ble Appellate Tribunal for Electricity. Subsequently, the Commission notified

the Haryana Electricity Regulatory Commission (Terms and Conditions for

determination of Tariff from Renewable Energy Sources, Renewable Purchase

Obligation and Renewable Energy Certificate) Regulations, 2010, Regulation No.

HERC/23/2010 (hereinafter referred to as “RE regulations, 2010, vide notification

dated 03.02.2011. In accordance with these regulations, the Commission, vide orders

dated 27.05.2011, 25.01.2012 and 03.09.2012 determined generic tariff for generating

stations using renewable sources set up in the State of Haryana upto the FY 2012-13.

Certain stakeholders including the petitioner have participated in each such exercise of

tariff determination raising objections on various components of tariff. Subsequently,

the Commission, vide order dated 20.11.2013, issued the impugned Order determining

a generic levelised tariff of Rs. 6.97/- per kwh for Biomass power projects set up in the

State of Haryana during FY 2013-14. The Bio-mass project of the petitioner is based in

Mohindergarh District of Haryana State with an aggregate installed capacity of 9.9

MW. and was synchronized with the grid on 03.05.2013.

2. The generic tariff for plants commissioned in the FY 2014-15 was published

vide order dated 13.08.2014. Subsequently, a suo moto corrigendum dated

29.05.2015 was issued regarding correction of calculation error in the tariff published

vide order dated 13.08.2014.

3. The petitioner submitted that the order dated 20.11.2013 did not have the

detailed calculation sheet annexed to the order as in the case of order dated

13.08.2014 & subsequent corrigendum dated 29.05.2015.

4. The petitioner observed certain inadvertent calculation errors in the Suo Motu

order issued on 20.11.2013 relating to the following norms/method of calculation after

the suo motu corrigendum of 29.05.2015:-

4.1 Adoption of PLF/CUF:-

3 | P a g e

Commission in its order dated 20.11.2013 considered various

parameters/norms for determination of generic tariff and for Bio-mass based projects

observed as follows:-

10.0 Biomass / Bagasse based power projects :

10.1 The Commission has considered the objections and suggestions of M/s

Star Wire and Saraswati Sugar Mills on the issue of cost of biomass / baggase

as well as project cost, PLF, GCV of biomass / bagasse based generation

projects and observe as under:-

The Commission observes that the fact that in the area, consciously decided by

the intervener, the fuel availability i.e. mustard stalk, reportedly is for 3 months

only. This may not be true for other areas and other fuels in Haryana; hence

the location specific issue cannot form the benchmark for deciding a generic

tariff for the entire state. Further, the terms and conditions for payments are

mutually agreed upon by the parties in line with HERC RE Regulations while

signing the Power Purchase Agreement which also has delayed payment

penalty as well as rebate for timely payment to mitigate financial risks. Hence

granting any relaxation in estimating working capital requirement is not

appropriate. As far as interest rate on Working Capital is considered the same

shall be considered in line with HERC RE Regulations after appropriate

adjustments if the market conditions so require.

While determining generic tariff it is appropriate to adopt the normative project

cost as per RE Regulations, 2010 notified by the Commission. On a case to

case basis the direct as well as incidental costs may vary from project to project

depending upon the location and other project specific requirements. Any extra

or incidental cost arising out of action of any authority i.e. Irrigation Department

cannot be factored in to modify the normative project cost. As far as

connectivity is concerned the HERC (Terms and Conditions for Grant of

Connectivity and Open Access for Intra – State Transmission and Distribution

System) Regulations, 2012 provides that for less than 10 MW capacity the

connectivity shall be at 33 kV and below. Consequently, any project to be

commissioned in FY 2013-14 i.e. after coming into force of the RE Regulations

4 | P a g e

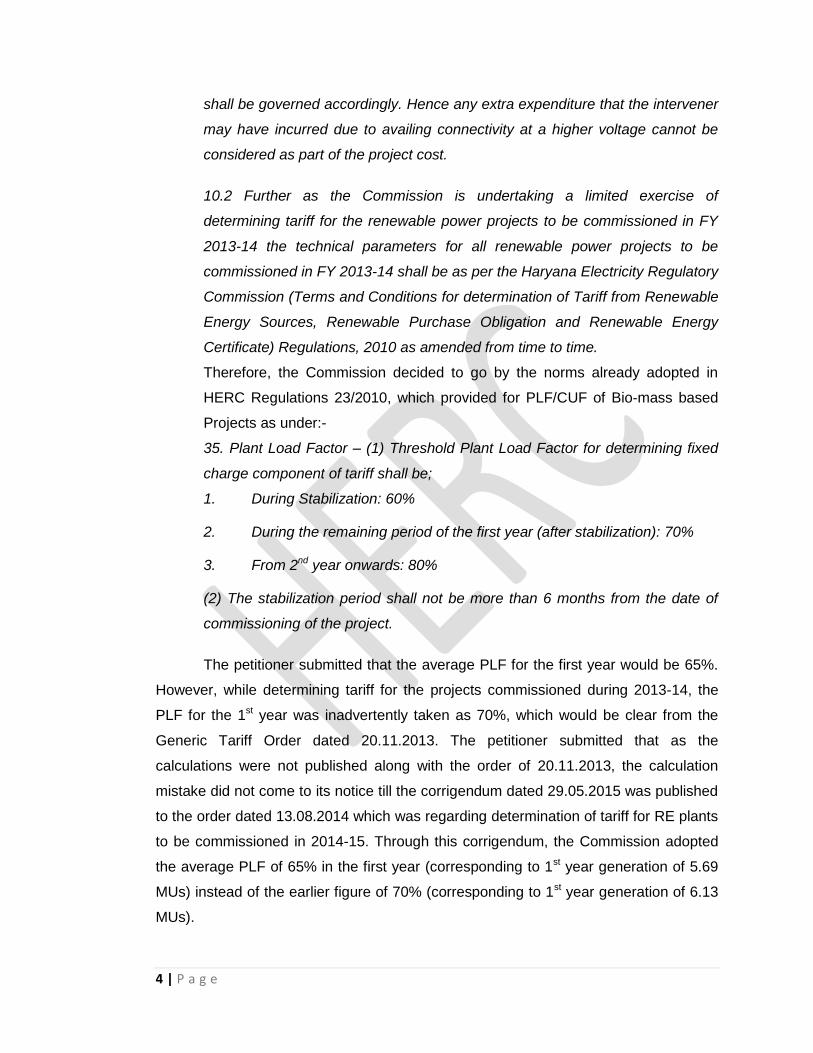

shall be governed accordingly. Hence any extra expenditure that the intervener

may have incurred due to availing connectivity at a higher voltage cannot be

considered as part of the project cost.

10.2 Further as the Commission is undertaking a limited exercise of

determining tariff for the renewable power projects to be commissioned in FY

2013-14 the technical parameters for all renewable power projects to be

commissioned in FY 2013-14 shall be as per the Haryana Electricity Regulatory

Commission (Terms and Conditions for determination of Tariff from Renewable

Energy Sources, Renewable Purchase Obligation and Renewable Energy

Certificate) Regulations, 2010 as amended from time to time.

Therefore, the Commission decided to go by the norms already adopted in

HERC Regulations 23/2010, which provided for PLF/CUF of Bio-mass based

Projects as under:-

35. Plant Load Factor – (1) Threshold Plant Load Factor for determining fixed

charge component of tariff shall be;

1. During Stabilization: 60%

2. During the remaining period of the first year (after stabilization): 70%

3. From 2nd year onwards: 80%

(2) The stabilization period shall not be more than 6 months from the date of

commissioning of the project.

The petitioner submitted that the average PLF for the first year would be 65%.

However, while determining tariff for the projects commissioned during 2013-14, the

PLF for the 1st year was inadvertently taken as 70%, which would be clear from the

Generic Tariff Order dated 20.11.2013. The petitioner submitted that as the

calculations were not published along with the order of 20.11.2013, the calculation

mistake did not come to its notice till the corrigendum dated 29.05.2015 was published

to the order dated 13.08.2014 which was regarding determination of tariff for RE plants

to be commissioned in 2014-15. Through this corrigendum, the Commission adopted

the average PLF of 65% in the first year (corresponding to 1st year generation of 5.69

MUs) instead of the earlier figure of 70% (corresponding to 1st year generation of 6.13

MUs).

5 | P a g e

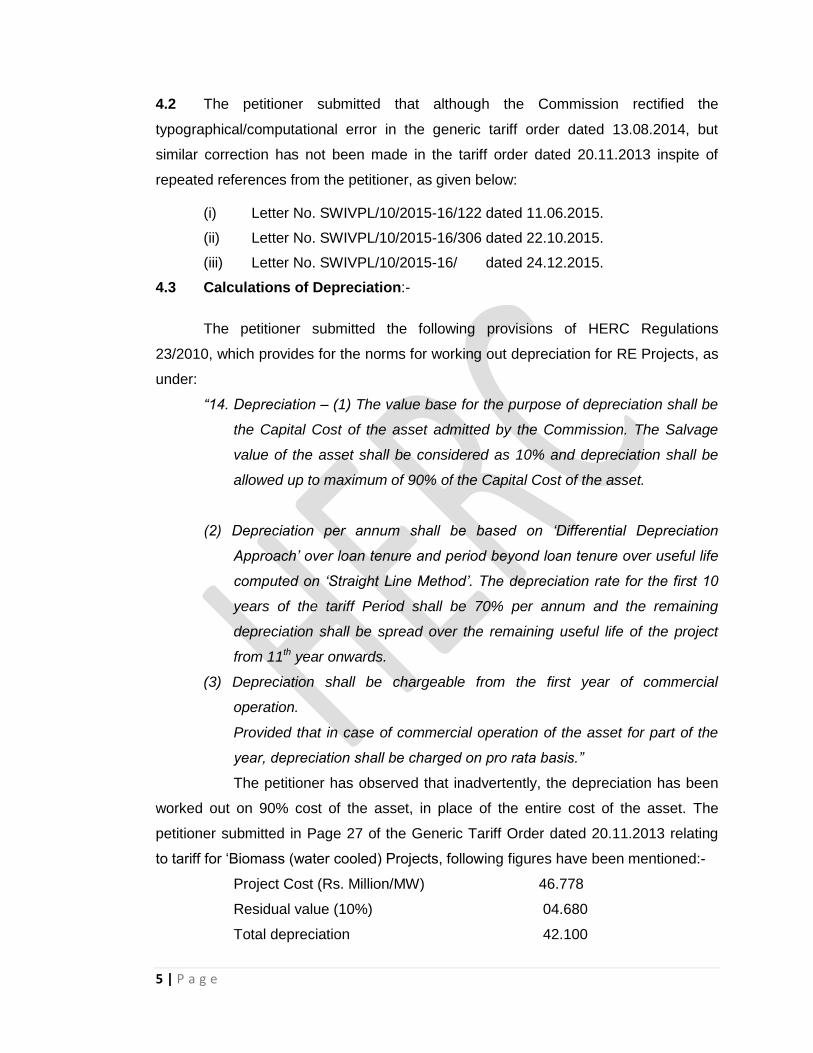

4.2 The petitioner submitted that although the Commission rectified the

typographical/computational error in the generic tariff order dated 13.08.2014, but

similar correction has not been made in the tariff order dated 20.11.2013 inspite of

repeated references from the petitioner, as given below:

(i) Letter No. SWIVPL/10/2015-16/122 dated 11.06.2015.

(ii) Letter No. SWIVPL/10/2015-16/306 dated 22.10.2015.

(iii) Letter No. SWIVPL/10/2015-16/ dated 24.12.2015.

4.3 Calculations of Depreciation:-

The petitioner submitted the following provisions of HERC Regulations

23/2010, which provides for the norms for working out depreciation for RE Projects, as

under:

“14. Depreciation – (1) The value base for the purpose of depreciation shall be

the Capital Cost of the asset admitted by the Commission. The Salvage

value of the asset shall be considered as 10% and depreciation shall be

allowed up to maximum of 90% of the Capital Cost of the asset.

(2) Depreciation per annum shall be based on ‘Differential Depreciation

Approach’ over loan tenure and period beyond loan tenure over useful life

computed on ‘Straight Line Method’. The depreciation rate for the first 10

years of the tariff Period shall be 70% per annum and the remaining

depreciation shall be spread over the remaining useful life of the project

from 11th year onwards.

(3) Depreciation shall be chargeable from the first year of commercial

operation.

Provided that in case of commercial operation of the asset for part of the

year, depreciation shall be charged on pro rata basis.”

The petitioner has observed that inadvertently, the depreciation has been

worked out on 90% cost of the asset, in place of the entire cost of the asset. The

petitioner submitted in Page 27 of the Generic Tariff Order dated 20.11.2013 relating

to tariff for ‘Biomass (water cooled) Projects, following figures have been mentioned:-

Project Cost (Rs. Million/MW) 46.778

Residual value (10%) 04.680

Total depreciation 42.100

6 | P a g e

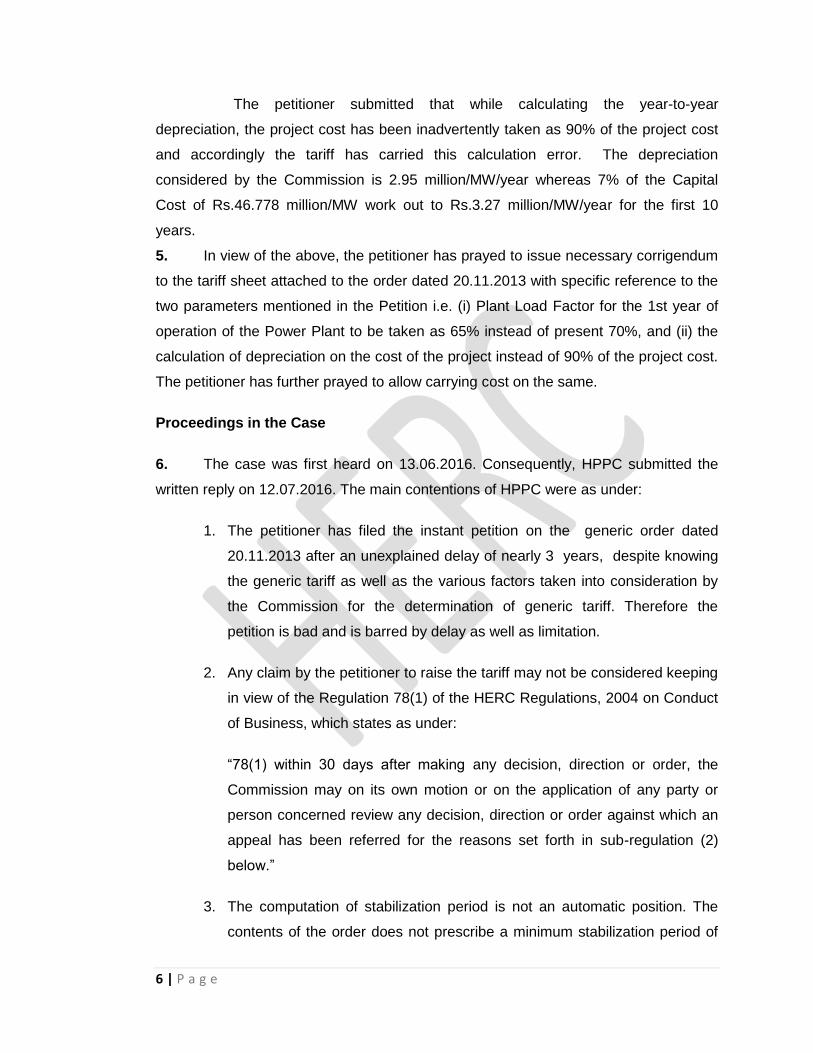

The petitioner submitted that while calculating the year-to-year

depreciation, the project cost has been inadvertently taken as 90% of the project cost

and accordingly the tariff has carried this calculation error. The depreciation

considered by the Commission is 2.95 million/MW/year whereas 7% of the Capital

Cost of Rs.46.778 million/MW work out to Rs.3.27 million/MW/year for the first 10

years.

5. In view of the above, the petitioner has prayed to issue necessary corrigendum

to the tariff sheet attached to the order dated 20.11.2013 with specific reference to the

two parameters mentioned in the Petition i.e. (i) Plant Load Factor for the 1st year of

operation of the Power Plant to be taken as 65% instead of present 70%, and (ii) the

calculation of depreciation on the cost of the project instead of 90% of the project cost.

The petitioner has further prayed to allow carrying cost on the same.

Proceedings in the Case

6. The case was first heard on 13.06.2016. Consequently, HPPC submitted the

written reply on 12.07.2016. The main contentions of HPPC were as under:

1. The petitioner has filed the instant petition on the generic order dated

20.11.2013 after an unexplained delay of nearly 3 years, despite knowing

the generic tariff as well as the various factors taken into consideration by

the Commission for the determination of generic tariff. Therefore the

petition is bad and is barred by delay as well as limitation.

2. Any claim by the petitioner to raise the tariff may not be considered keeping

in view of the Regulation 78(1) of the HERC Regulations, 2004 on Conduct

of Business, which states as under:

“78(1) within 30 days after making any decision, direction or order, the

Commission may on its own motion or on the application of any party or

person concerned review any decision, direction or order against which an

appeal has been referred for the reasons set forth in sub-regulation (2)

below.”

3. The computation of stabilization period is not an automatic position. The

contents of the order does not prescribe a minimum stabilization period of

7 | P a g e

six months, rather, the same is the maximum period. Hence, the person

claiming the benefit has to necessarily submit proof to the Commission as

regards the stabilization period. In absence of the any such evidence, there

is no automatic determination of stabilization period to be a minimum period

of six months. There is no such content in the order passed by the

Commission as regards determination of average PLF @ 65%. The

petitioner cannot be permitted to misconstrue the order passed by the

Commission and try to seek a review under the grab of rectification of

clerical error.

4. The benefit of depreciation has to be granted on the value so determined

as the factor beyond 90% of the capital cost investment could not have

been taken towards the project value for the purpose of determination of

generic tariff.

5. The HPPC has to purchase power from Biomass based power projects to

meet its non-solar RPO targets as per the HERC Regulations, 2010. HPPC

further submitted that the tariff for biomass based power projects is the

highest among all the other sources of energy to meet non-solar RPO

targets. HPPC submitted that as per latest HERC Order dated 09.10.2015,

the existing levelised tariff being paid to the petitioner is Rs. 8.43/Kwh and

the current year (3rd year) tariff is Rs. 7.43/KwH. Thus, the cost of per unit

power purchase in case of Biomass project is much higher than hydro

power which is purchased by HPPC @ Rs. 4.7/-Kwh. HPPC further

submitted that any further increase in the tariff will further make this project

unviable for it.

7. The case was finally heard on 14.07.2016. The Commission allowed the

parties to the petition to submit their written arguments, if desired, within next

one week.

8. Accordingly, M/s. Star Wire (India) Vidyut Pvt. Ltd. filed the written submission

on 27.07.2016, reiterating the arguments as per its initial petition.

Commission’s Order:

8 | P a g e

9. The Commission has heard the arguments of the petitioner and the

respondents as well as their replies/written submissions including rejoinders provided

in the matter and observes that the petitioner has sought a review of the HERC order

dated 20.11.2013 on the following two issues:

a) PLF

b) Depreciation

The petitioner has sought the review on the ground that the impugned order of the

Commission contained certain errors that came to the notice of the petitioner only

when the corrigendum dated 29.05.2015 to the order dated 13.08.2014 was published

with reference to the correction in PLF.

10. The Commission observed that the filing of the petitioner was incomplete as

the fee submitted with the filing was less than the fee prescribed for the matter under

the HERC Fee Regulations. Additional fee was demanded vide HERC memo dated

30.06.2016 and 26.08.2016. The same was submitted by the petitioner only on

05.09.2016, vide memo no. SWIVPL/2015-16/154 dated 02.09.2016. Accordingly, the

Commission examined the petition and proceeded to pass the Order.

11. The respondent in the first instance has raised the issue of maintainability of

the petition on account of inordinate delay in filing the review petition. The petitioner

has sought to justify the delay citing that the erroneous calculation of PLF came to its

notice only on 29.05.2015 and of depreciation on 09.10.2015. The said petition has

been filed by the petitioner on 14.03.2016.

12. Further, Regulation 78 of HERC (Conduct of Business Regulations), 2004,

specifies that “Within 30 days after making any decision, direction or order, the

Commission may on its own motion or on the application of any party or person

concerned review any decision, direction or order against which an appeal has been

referred”. Thus, the present petition has crossed the time limit specified in the ibid

Regulations. Also, the petitioner has already availed of the appellate remedy

against the ibid order dated 20.11.2013 which has been decided by the Hon’ble

Appellate Tribunal for Electricity vide order dated 02.09.2014 in appeal no. 31 of

2014.

13. The Commission has examined the procedure undertaken by it for

determination of generic tariff for power generated using renewable sources vide order

9 | P a g e

dated 20.11.2013. The Commission observes that the petitioner had actively

participated in not only the proceedings relating to the impugned Order but has been

an active participant in all the proceedings right since 2007 when the first order on

generic Tariff from Renewable sources was determined by the Commission vide order

dated 15.07.2007. It must be noted that there are various components for

determination of tariff including but not limited to PLF, capital cost, depreciation,

interest on loan both long term and short term, return on equity, income tax, cost of

fuel etc. The final tariff is worked out by allocating the total cost over the estimated

units to be generated in a year and is therefore only a final product of these

components. The petitioner, in its various interventions, petitions and appeals has

sought review on many of these components. Therefore it can safely be concluded

that the petitioner was well aware of the final impact of each of these cost components

on the tariff which is not possible to be worked out unless there is a denominator in

form of energy generated using a predetermined PLF. Therefore the Commission is

not inclined to agree with the contention of the petitioner that it was unaware of the

units generated during the first year of tariff till the corrigendum dated 29.5.2015.

14. The Petitioner was well aware of the fact that while determining the generic

tariff the Commission has kept the PLF norm as 70% for 1st year and 80% thereafter.

The Petitioner has even prayed that it should be reduced to 60% and 70%

respectively. This fact is recorded in the Commission’s Order dated 20.11.2013 at para

3.5.1 of the ibid order. Thus it is evident that the Commission has already considered

the issue of PLF for the 1st year and after due consideration kept the same at 70%.

The Petitioner was already well aware of the same, before entering into PPA with

HPPC. Therefore, the issue of clerical/arithmetical mistake does not arise at all.

15. The PLF specified in the HERC (Terms and Conditions for Determination of

Tariff for Renewable Energy, Renewable Purchase Obligations and Renewable

Energy Certificates) Regulations, 2010 is threshold PLF and is not an absolute term,

which mandatorily has to be applied, while determining the tariff. The relevant extract

of the HERC Regulations 23/2010, that determined the PLF for the first year is as

given below:

Plant Load Factor – (1) Threshold Plant Load Factor for determining fixed

charge component of tariff shall be;

10 | P a g e

4. During Stabilization: 60%

5. During the remaining period of the first year (after stabilization): 70%

6. From 2nd year onwards: 80%

(2) The stabilization period shall not be more than 6 months from the date of

commissioning of the project.

As is apparent from a reading of the above regulation the benefit of low PLF

during stabilization can be provided to a generator for a maximum period of six months

and that is not a prescribed period ( it may be less but never more than six months).

Hence, the person claiming the benefit has to necessarily submit proof to the

Commission as regards the stabilization period. The petitioner has, at no place,

alleged that the above regulation was not in its knowledge. As construed, the PLF for

the first year was based on the stabilization period which could vary. In case the

petitioner was discriminated against, or was positioned at a disadvantageous position

by the above clause, it was open for him to approach the Commission within the time

frame available to him in compliance with the statute. At least, the appropriate time

would have been on completion of the stabilization period or completion of the first

year. The Petitioner has nowhere, at any stage in this case, demonstrated the

stabilization period taken by its project or that it has suffered any loss on this account.

The Commission, therefore, is not inclined to interfere with its order on this ground

Furthermore, the arguments on the same at this stage i.e. after 3 years (approx.) of the

date of Order, regarding the computational error does not hold good.

16. On the issue of depreciation, the Commission observes that the total

depreciation of Rs. 4.21 crore/MW (i.e. 90% of the capital cost of Rs. 4.67/MW) has

been allowed over the period of 20 years for arriving at levelised tariff. It is further

observed that neither the capital cost nor the total depreciation has been disputed by

the petitioner. It is only the year to year allocation that is now being disputed. The

petitioner may note that the HERC (Terms and Conditions for Determination of Tariff

for Renewable Energy, Renewable Purchase Obligations and Renewable Energy

Certificates) Regulations, 2010 has only specified the broad terms for deriving the tariff

and subsequently, and it is not disputed that while arriving at the levelized tariff, the

Commission has applied those terms in way that total depreciation allowed to the

generator over the life of the project is 90% of the capital cost.

11 | P a g e

It is pertinent to note that the Hon’ble APTEL has in Appeal no. 106/2008 vide

order dated 26.02.2009 and in appeal no. 77/2014, vide order dated 13.05.2015

observed that the structuring of tariff is a prerogative of the Commission and the

Appropriate Commission has power to design the tariff as per its wisdom.

17. It is also a matter of fact that the petitioner, M/s. Star Wire (India) Vidyut Pvt.

Ltd. is a commercial business entity and it entered into PPA with the distribution

licensee to supply power subsequent to the determination of tariff by the Commission

with open eyes. As a commercial entity, it also has a duty to its shareholders to have

analyzed the profitability of its generating plant at the pre-determined generic tariff

being offered by the respondent. It is further assumed that as a responsible business

entity, it analysed its ability to generate adequate profits to enable it to service its debts

and generate sufficient profits to cover the cost of equity and only then submitted its

offer to supply power to the respondent at the tariff determined by the Commission.

There was no compulsion imposed either by the Commission or the HPPC on the

petitioner to enter into PPA. Further, the Petitioner has not demonstrated any hardship

caused to it due to the manner in which levelized tariff has been fixed by the

Commission.

18. The Commission, vide its Order dated 20.11.2013 determined the generic tariff

which was the upper limit for a Biomass Generator. Subsequent to such determination

of tariff, the petitioner offered to supply power to the respondent which was accepted

and thus a contract was entered into between the two parties. Once the tariff

determined by the Commission has been adopted and agreed by two parties, the

same cannot be altered except through mutual consent of both parties.

19. The generic tariff determined by the Commission vide its order dated

20.11.2013 was applicable to biomass power projects set up during FY 2013-14. The

said order has now been superseded by the HERC Order on determination of Generic

Tariff for the biomass projects to be set up during FY 2014-15 and so on. In a similar

case, the Hon’ble APTEL in its order dated 22nd August, 2014, while deciding Appeal

No. 279 of 2013 gave due consideration to the argument that Section 64(6) of the

Electricity Act permits amendment or alteration to the tariff order only during the time of

its operation. The relevant extract contained in Para 129 of the Hon’ble APTEL is

reproduced below:

12 | P a g e

“It has been pointed out by the Respondents that the relief sought for by the

Appellant in the Petition filed before the State Commission in the year 2013 only after

the operation of the first control period of two years from 29.1.2010 has come to an

end. Therefore, these reliefs cannot be granted since the Order which was sought to

be re-visited was no longer in operation by virtue of Section 64 (6) of the Electricity

Act, 2003. Section 64(6) of the Electricity Act permits amendment or alteration to the

tariff order only during the time of its operation. Such tariff order having lived its life and

having been replaced by a fresh tariff order passed in the year 2012 is incapable of

revision and revisit in 2013 i.e. after two years is over. This argument of the

Respondent, in our view also deserves consideration.”

Similarly, in the present case the tariff order dated 20.11.2013 has lived its life

and having been replaced by a fresh tariff order passed in the year 2014 is incapable

of revision and revisit in 2016 i.e. after three years are over.

20. The petitioner has been in contract to supply power to the respondent since

22.06.2012. It has been supplying power, raising bills and getting paid for the same.

The operation of a commercial contract between two parties like in case of the

petitioner and the respondents which is in operation for a successful period of three

years gives rise to legitimate expectation and is also subject to Promissory Estoppel.

The Hon’ble APTEL in its order dated 22nd August, 2014 while decided Appeal No. 279

of 2013, gave due consideration to the Doctrines of Legitimate Expectation and

Promissory Estoppel as under:

a) Doctrine of Legitimate Expectation:

In Para 147 of the ibid Order, the question was discussed regarding

applicability of doctrine of Legitimate Expectation. The relevant extract has

been reproduced below:

“The question whether the parties having agreed upon to the terms and conditions and having acted upon the same, could go back violating the legitimate expectations of the developers to have the legitimate right to seek enforcement of the said representation of the PPAs.”

The question so raised, has been answered in Para 152 of the ibid Order

and the relevant extract has been reproduced below:

“Once a tariff and process of computation has been represented by the State, then based on the Doctrine of the Legitimate Representations, the Respondents have got the right to seek enforcement of the said representation.”

13 | P a g e

From the above, it has been construed that once the parties to the contract

have agreed to certain terms & conditions and have acted upon the same,

could not go back violating the legitimate expectation of its enforcement.

b) Doctrine of Promissory Estoppel:

While deciding the doctrine of Promissory Estoppel in the ibid Order,

Hon’ble APTEL considered the judgement reported in the case of Union of

India v Wing Commander R R Hingorani (1987) 1 SCC 551. In this decision

the Hon’ble Supreme Court has held as follows:

“8.....Before an estoppels can arise, there must be first a representation of

an existing fact distinct from a mere promise made by one party to the

other; secondly that the other party believing it must have been induced to

act on the faith of it; and thirdly, that he must have so acted to his

detriment.”

So, as per this decision, the ingredients for satisfying the estoppels would be: (a) a representation of an existing fact distinct from a mere promise made by one party to the other; (b) the other party believing it must have been induced to act on the faith of it; (c) The other party must have so acted to his detriment;

Thus, the ingredients for satisfying the estoppels are squarely present in this

case. The parties to the contract i.e. the petitioner and the respondent, were well

aware of the generic tariff determined by the Commission and have acted accordingly.

The merit order of dispatch and procurement of power have been undertaken by

HPPC on the faith of a price determined in the generic tariff order. Therefore, the

contention of Petitioner to seek its review is in violation of Doctrine of Promissory

Estoppel.

21. The Petitioner has agreed to pay the levelized tariff determined by the

Commission on 20.11.2013 in the PPA dated 22nd June, 2012 entered into with the

Respondent. The Petitioner cannot now seek to evade its obligations under the PPA.

Hon’ble Supreme Court in Gujarat Urja Vikas Nigam Ltd. Vs. Emco Ltd. & Anr

(Judgement dated 02/02/2016 in Civil Appeal No. 1120 of 2015) has held that it is not

open to the Appellant to wriggle out of the terms of the contract entered into and that

too in accordance with the Regulations.

22. The Petitioner and the Respondent have entered into PPA at a particular price

and exposed themselves to financial commitments. The settled law on such issue is

14 | P a g e

quite clear and contracting parties would squarely fall under the ambit of the doctrine

of promissory estoppels as the HPPC, in the present case, has been exposed to

financial commitments. The courts, in numerous cases, have held that once a contract

comes into existence, it can be amended or modified only with mutual consent.

The Hon’ble Supreme Court in Gopal Chand Sharma vs State (U I T ) And

Ors on 11 October, 2012 has held as below:

In the instant case the letter dated 5-3-2008 issued by the UIT on the face of it

constituted a proposal. As against the proposal the petitioners deposited the required

amount. Under Section 8of the Contract Act this tantamounted to acceptance of the

proposal of the promisee. Therefore a concluded contract came into existence. In my

considered view a concluded contract having thus come into force, it was binding on

the UIT unless there were allegations of fraud or misrepresentation as against the

petitioner, based whereupon requisite declaration from a competent court of law

could have been sought. No such fraud or misrepresentation has been alleged against

the petitioners. No suit for cancellation of a duly formed contract has been filed. The

Hon'ble Division Bench of the Delhi High Court in Govt. of NCT of Delhi Vs. Bhushan

Kumar [LPA No.141 and 168/2006 and WP (C) No.2040/2007 decided on 18-3-

2008], held that allotment having been made specifically mentioning the area and

property number allotted to the applicant and consideration having been paid by the

applicant a concluded contract came into existence between the parties. It was held

that the terms and conditions of the allotment following a concluded contract can

only be modified (novation under Section 60 of the Contract Act) with mutual consent

and not unilaterally unless there exists a provision in the law or in the contract itself.

Similarly no policy decision could obstruct the operation of a concluded contract. A

party to a contract can not unilaterally alter the terms and conditions of the contract.

Consequently no escape from the inexorable effect of a contract was available to any

of the party to the contract. It was further held that even in cases of unilateral

mistake, which was not occasioned by the successful allottees who had acted upon

proposal and accepted it a duly concluded contract could not be cancelled. Reference

was also made to Section 22 of the Contract Act, which provides a contract is not

voidable merely because it was caused under a mistake as to a matter of fact, and

where allottes were not guilty of fraud, misrepresentation or unfair dealing, their

rights could not be stalled by arbitrary action. In the aforesaid case where the

15 | P a g e

allottees parted with money and deposited the sale consideration with the authority,

which was accepted and retained by the authority, (as also in the present case where

considerable amounts have been deposited for over last four years) the sanctity of

the contract had to be maintained as contrarily the allottees would apart from

arbitrary action of the authority also suffer loss and damages in circumstances not of

their making.

23. The Commission further observes that the exercise of determining the tariff by

the Commission is an ongoing process that is tempered by change in circumstances

and procedures. In case we examine the various orders issued by the Commission on

determination of generic tariff for the renewable projects in sequence, we observe that

there are certain deviations in each subsequent order and such deviations, certainly,

do not render the earlier order defective. Similarly, the change in PLF in subsequent

order does not make the earlier order defective. The process of review and appeal is

so made time bound so that any development, that is subsequent to the period of

limitation cannot impinge upon the legality of the order that is now deemed to have

attained finality. In case it was not so, no order can ever attain finality and that would

lead to endless litigation.

Accordingly, the present petition is dismissed.

This Order is signed, dated and issued by the Haryana Electricity Regulatory

Commission on 03rd October, 2016.

Date: 03.10.2016

(Jagjeet Singh)

Place: Panchkula Chairman

The Order dated 03.10.2016 in case no. HERC/PRO-12 of 2016 has been

signed by Shri Jagjeet Singh, Hon’ble Chairman, HERC (hereinafter referred to as

“the Order”. I express my difference of opinion as per my Dissenting Note attached.

Date: 18th October, 2016 (M. S. Puri) Place: Panchkula Member

16 | P a g e

ORDER

In terms of Section 92(3) of the Electricity Act, 2003, I exercise the second / casting

vote vested in me, accordingly the Order of the Chairman shall be the Order of the

Commission.

This order is signed, dated and issued by the Haryana Electricity Regulatory

Commission on 18.10.2016

Date : 18.10.2016 (M. S. Puri) (Jagjeet Singh)

Place: Panchkula Member Chairman

1 | P a g e

Dissenting Order in Case No: HERC/PRO-12 of 2016 in the matter of Application

seeking clarification on the order issued by the Commission in Suo-Moto Case

No. PRO-15 of 2013 dated 20.11.2013 for determination of Generic Tariff for

Renewable Energy Projects to be commissioned during FY 2013-14 under the

Haryana Electricity Regulatory Commission (Terms and Conditions for

Determination of Tariff for Renewable Energy, Renewable Purchase Obligations

and Renewable Energy Certificates) Regulations, 2010 read with amendments

issued from time to time.

The Order dated 03.10.2016 in case no. HERC/PRO-12 of 2016 has been signed

by Shri Jagjeet Singh, Hon’ble Chairman, HERC (hereinafter referred to as “the Order”,

I express my difference of opinion on certain paragraphs, including conclusion part, of

the said Order as under:-

1. Para 1 to 5 of the Order

The aforesaid paragraphs provide the background of the case and the

submissions made by the parties. A few aberrations in the said paragraphs are as

under:-

At paragraph 1 of the Order it has been stated that this Commission had

determined RE Generic Tariff vide Order dated 15.05.2007 based on CERC

Regulations. I have perused the Order supra and observe as under:-

i) The Commission had passed the Order dated 15.05.2007 for determination of

RE Generic Tariff based on the feedback received from the Stakeholders on the

discussion / consultation paper circulated in September, 2006. The relevant extract

from the ibid Order is reproduced below:-

“In compliance with the statutory provision in the Act and the policy guidelines

given in the Tariff Policy of the Govt. of India, the Commission tentatively

indicated the following parameters and vide order dated 31.1.2007 decided to

invite suggestions/objections from all the stakeholders”.

ii) CERC had notified its RE Regulations only on 16th September, 2009.

2 | P a g e

In view of the above, it is difficult to phantom that this Commission’s Order dated

7.05.2007 was based on CERC Regulations which was notified at a much later date.

Even the approach for determination of RE Tariff by this Commission was entirely

different e.g. this Commission had determined tariff based on specific fuel consumption

(Kg/kWh) as against CERC’s Regulations wherein fuel consumption is determined on

the basis of Heat Rate and Calorific Value of biomass fuel mix.

iii) The statement that the petitioner participated in the determination of the first

generic tariff, though irrelevant, is also not factually correct. It is evident from the

Annexure to this Commission’s RE Tariff Order dated 7.05.2016 that the M/s Starwire

(India) Ltd. had participated in the proceedings leading to the ibid Order and not the

Petitioner herein i.e. M/s Star Wire (India) Vidyut Pvt. Ltd. Even otherwise, in response

to the public notice any party / Stakeholder can participate in the proceedings and

present their views / comments / objections on the draft / discussion paper wherein

tentative norms are indicated with the sole purpose of eliciting public/Stakeholders view

before finalizing the same.

Iv) The fact, as evident from the Order dated 7.05.2007 and the Order dated

20.11.2013, that they did not contain the detailed calculation of tariff, is not disputed.

2. Para 13 to 23 of the Order

As already observed by me, reference to this Commission’s Order dated

15.07.2007 and the Petitioner’s participation thereto is irrelevant. Further, the two

Orders i.e. dated 20.11.2013 (without detailed tariff calculation sheet) for the biomass

based power projects to be commissioned in the FY 2013-14 and the Order dated

13.08.2014 for the biomass based power projects to be commissioned in the FY 2014-

15 (with detailed tariff calculation sheet) including the corrigendum, were based on the

HERC RE Regulations, 2010. Therefore, I am not able to figure out any reasons as to

why the norms, as specified in the RE Regulations, should be applied differently for the

projects commissioned in the FY 2013-14 and the FY 2014-15 as neither the said

Regulations nor the two Orders referred to above provide for treating PLF and

3 | P a g e

depreciation differently. Moreover, the computational error in the case of projects

commissioned in the FY 2014-15 was rectified by the Commission. Hence, in my

considered view, there ought not to be any discrimination between the two. Additionally,

the Order assumes that the Petitioner was well aware of the final impact of each of the

tariff components also lacks merit. This assumption is farfetched as the Petitioner’s

contention that the computational error came to his notice from the detailed calculation

sheet attached with the Order dated 13.08.2014 and the subsequent corrigendum dated

29.05.2015 has to be given due weightage. Hence, any Order based on assumptions /

premises is liable to be held bad in the eyes of law.

Additionally, I have examined regulation 79 of the HERC (Conduct of Business)

Regulations, 2004. The relevant regulation is reproduced below:-

“The Commission may on its own motion or on the application of any party

correct any clerical or arithmetical errors in any order passed by the

Commission”

In view of the above background, I have framed the two following issues for

discussions and my Order:-

Issue No. 1: Whether the Petitioner is entitled for relief on account of PLF and depreciation. The generic tariff for the biomass based projects commissioned in the FY 2013-

14 and the FY 2014-15 was decided on the basis of parameters / norms set out by the

Commission in the HERC Tariff Regulations, 2010 including its subsequent

amendments. Regarding calculation of PLF and Depreciation the principal Regulations

provides as under:-

“The first Control Period or Review Period under these Regulations shall be of three years, of which the first year shall be the period from the date of notification of these regulations to 31st march, 2011.

4 | P a g e

Tariff Period. - (1) The Tariff Period for Renewable Energy power projects shall generally correspond to their respective project life or reckoned with the period provided in the PPA as the case may be.

14. Depreciation. -(1) The value base for the purpose of depreciation shall be the

Capital Cost of the asset admitted by the Commission. The Salvage value of the asset

shall be considered as 10% and depreciation shall be allowed up to maximum of 90% of

the Capital Cost of the asset.

35. Plant Load Factor. -(1) Threshold Plant Load Factor for determining fixed charge component of Tariff shall be:

1. During Stabilisation: 60%

2. During the remaining period of the first year (after stabilization) : 70%

3. From 2nd Year onwards: 80 %

(2) The stabilisation period shall not be more than 6 months from the date of

commissioning of the project.

The Commission vide its 4th Amendment dated 12th August, 2015 made the

following provisions:-

1. Short Title and Commencement. –

(1) These Regulations shall be called the Haryana Electricity Regulatory Commission (Terms and Conditions for determination of Tariff from Renewable Energy Sources, Renewable Purchase Obligation and Renewable Energy Certificate) (4th Amendment) Regulations, 2015.

(2) These Regulations shall extend to all the RE Projects commissioned / to be commissioned in FY 2013-14, 2014-15, 2015-16 and 2016-17 in the State of Haryana.

(3) For the existing projects commissioned during FY 2013-14 onwards, the revised norms shall be applicable prospectively from the date of notification of these Regulations unless provided otherwise in these Regulations. For the period prior to the date of notification, existing norms as per Principal Regulations shall be applicable for such projects.

(4) These regulations shall come into force from the date of their notification in the Official Gazette. 2. Amendment of Regulation 4 of the Principal Regulations: - The existing Regulation 4 of the Principal Regulations shall be substituted as under:-

5 | P a g e

“4. Control Period or Review Period – The second Control Period or Review Period

under these Regulations shall be of four years, of which the first year shall be the

FY 2013-14.

It is evident from the above that all the projects commissioned / to be

commissioned from the FY 2013-14 to the FY 2016-17 were brought under the same

Regulations. Further, the principal regulation governing PLF and Depreciation was

continued without any amendment as such.

Tested on the above anvil, it is apparent that while calculating normative gross

generation the PLF originally considered by the Commission in its Order dated

7.05.2007 was pegged at 80%. While in its Order dated 25.01.2012 the PLF, for the 1st

Year was pegged at 60% (stabilization, up to six months) 70% (1st year) and 80% from

the 2nd year onwards. The same dispensation was continued with in the Commission’s

Order dated 3.09.2012 as well as Annexure “A” appended with the Order dated

20.11.2013. It needs to be noted that this Commission, under HERC RE Regulations,

2010 including its subsequent amendment determines generic levellised tariff which is

applicable to all RE Projects to be commissioned in Haryana in that particular year.

Hence, the stabilization period may vary from one project to the other. Therefore, to

provide a level playing field the stabilization period has been capped at six months.

Accordingly, the gross generation, for the first year, is calculated considering average

PLF of 65% i.e. 5.694 MUs considering six months generation @ 60% and the

subsequent six months @ 70% and not 5.256 MUs @ 60% PLF or 6.132 MUs @ 70%

PLF. In case the intention was to relate the PLF with the actual stabilization period it

would tantamount to case specific tariff determination and the same would also not be

possible until CoD of the project. Such an exercise would defeat the very purpose of

HERC RE Regulations notified by this Commission.

The Corrigendum to Commission’s Order dated 13.08.2014 in the matter of

determination of levellised generic tariff for renewable energy projects to be

commissioned during FY 2014-15 under regulation 7 of the Haryana Electricity

Regulatory Commission (Terms and Conditions for determination of Tariff from

6 | P a g e

Renewable Energy Sources, Renewable Purchase Obligation and Renewable Energy

Certificate) Regulations, 2010 as amended from time to time clearly stated as under:-

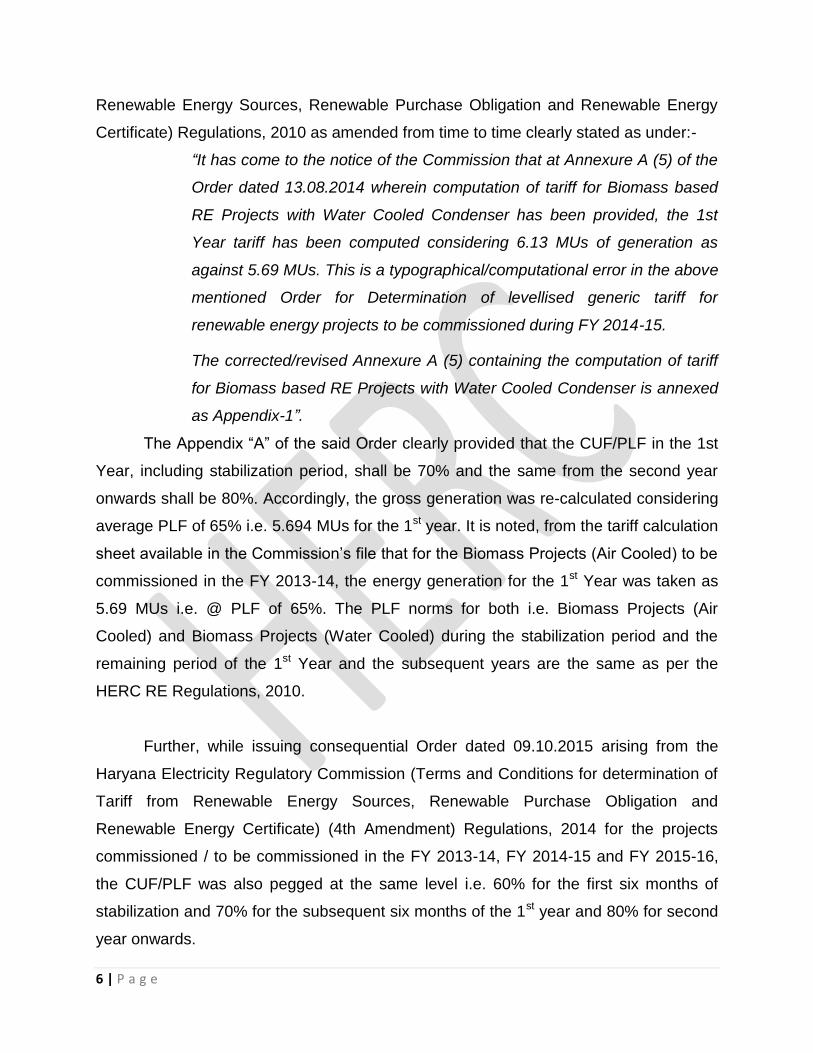

“It has come to the notice of the Commission that at Annexure A (5) of the

Order dated 13.08.2014 wherein computation of tariff for Biomass based

RE Projects with Water Cooled Condenser has been provided, the 1st

Year tariff has been computed considering 6.13 MUs of generation as

against 5.69 MUs. This is a typographical/computational error in the above

mentioned Order for Determination of levellised generic tariff for

renewable energy projects to be commissioned during FY 2014-15.

The corrected/revised Annexure A (5) containing the computation of tariff

for Biomass based RE Projects with Water Cooled Condenser is annexed

as Appendix-1”.

The Appendix “A” of the said Order clearly provided that the CUF/PLF in the 1st

Year, including stabilization period, shall be 70% and the same from the second year

onwards shall be 80%. Accordingly, the gross generation was re-calculated considering

average PLF of 65% i.e. 5.694 MUs for the 1st year. It is noted, from the tariff calculation

sheet available in the Commission’s file that for the Biomass Projects (Air Cooled) to be

commissioned in the FY 2013-14, the energy generation for the 1st Year was taken as

5.69 MUs i.e. @ PLF of 65%. The PLF norms for both i.e. Biomass Projects (Air

Cooled) and Biomass Projects (Water Cooled) during the stabilization period and the

remaining period of the 1st Year and the subsequent years are the same as per the

HERC RE Regulations, 2010.

Further, while issuing consequential Order dated 09.10.2015 arising from the

Haryana Electricity Regulatory Commission (Terms and Conditions for determination of

Tariff from Renewable Energy Sources, Renewable Purchase Obligation and

Renewable Energy Certificate) (4th Amendment) Regulations, 2014 for the projects

commissioned / to be commissioned in the FY 2013-14, FY 2014-15 and FY 2015-16,

the CUF/PLF was also pegged at the same level i.e. 60% for the first six months of

stabilization and 70% for the subsequent six months of the 1st year and 80% for second

year onwards.

7 | P a g e

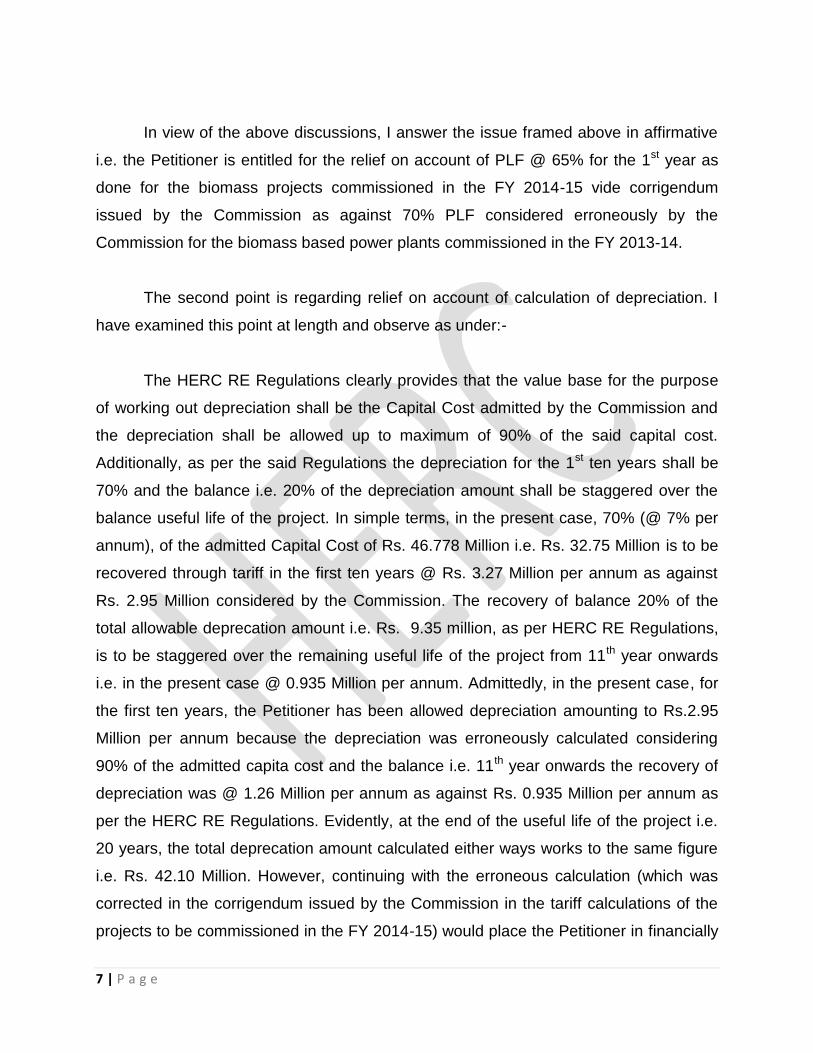

In view of the above discussions, I answer the issue framed above in affirmative

i.e. the Petitioner is entitled for the relief on account of PLF @ 65% for the 1st year as

done for the biomass projects commissioned in the FY 2014-15 vide corrigendum

issued by the Commission as against 70% PLF considered erroneously by the

Commission for the biomass based power plants commissioned in the FY 2013-14.

The second point is regarding relief on account of calculation of depreciation. I

have examined this point at length and observe as under:-

The HERC RE Regulations clearly provides that the value base for the purpose

of working out depreciation shall be the Capital Cost admitted by the Commission and

the depreciation shall be allowed up to maximum of 90% of the said capital cost.

Additionally, as per the said Regulations the depreciation for the 1st ten years shall be

70% and the balance i.e. 20% of the depreciation amount shall be staggered over the

balance useful life of the project. In simple terms, in the present case, 70% (@ 7% per

annum), of the admitted Capital Cost of Rs. 46.778 Million i.e. Rs. 32.75 Million is to be

recovered through tariff in the first ten years @ Rs. 3.27 Million per annum as against

Rs. 2.95 Million considered by the Commission. The recovery of balance 20% of the

total allowable deprecation amount i.e. Rs. 9.35 million, as per HERC RE Regulations,

is to be staggered over the remaining useful life of the project from 11th year onwards

i.e. in the present case @ 0.935 Million per annum. Admittedly, in the present case, for

the first ten years, the Petitioner has been allowed depreciation amounting to Rs.2.95

Million per annum because the depreciation was erroneously calculated considering

90% of the admitted capita cost and the balance i.e. 11th year onwards the recovery of

depreciation was @ 1.26 Million per annum as against Rs. 0.935 Million per annum as

per the HERC RE Regulations. Evidently, at the end of the useful life of the project i.e.

20 years, the total deprecation amount calculated either ways works to the same figure

i.e. Rs. 42.10 Million. However, continuing with the erroneous calculation (which was

corrected in the corrigendum issued by the Commission in the tariff calculations of the

projects to be commissioned in the FY 2014-15) would place the Petitioner in financially

8 | P a g e

adverse position which is also against the HERC RE Regulations, 2010. It is noted that

repayment of term loan amounting to Rs. 32.74 Million, has been considered by the

Commission is 10 years. In case the erroneous deprecation is continued with then

during the FY 2013-14, the FY 2014-15 and up to 12.08.2015 there will be some

mismatch between the depreciation amount and the loan repayment amount which will

invariably reduce the RoE of the project during the said period. Whereas, correcting the

inadvertently error shall restore the parity. Thus, taking a holistic view in the matter and

time value of money, I answer this issue in affirmative i.e. the Petitioner is entitled for

relief prayed for on account of inadvertent error in the calculation of depreciation up to

12.08.2015 i.e. till the time the Commission corrected the calculation of depreciation

vide its consequential Order arising from the 4th Amendment dated 12.08.2015 to the

HERC RE Regulations, 2010. The operating part of the consequential Order of the

Commission dated 09.10.2015 is reproduced below:-

“For the Biomass projects commissioned in FY 2013-14, the yearly tariff

as already determined shall be applicable for FY 2013-14 and FY 2014-

15. For FY 2015-16, the tariff as already notified shall be applicable up to

the date of notification of the 4th amendment dated 12.08.2015 and for the

remaining part of FY 2015-16 the revised tariff as now determined shall be

applicable. For FY 2016-17 and thereafter revised tariff as now

determined shall be applicable”.

Issue No. 2: Whether the doctrine of Promissory Estoppel gets triggered in the present case. This issue has been discussed at length in the present Order on the plea

that the tariff Order dated 20.11.2013 i.e. the Order for which correction of error has

been sought by the Petitioner, has lived its life and the parties are bound by the contract

(Power Purchase Agreement) dated 22nd June, 2012, has been examined by me.

Firstly, it is a well established principle of law that the Regulations notified by the

SERCs have the overriding power over any contract or Order. Hence, the PPA, in the

present case, shall get modified to that extent. Secondly, the remaining tariff period, in

the present case is also about 17 years. The levellised tariff for the biomass based

9 | P a g e

power projects was arrived at by discounting the year to year tariff arrived at for twenty

years by applying an appropriate discounting factor. Hence, it is evident that the term of

PPA is still a long way to go and cannot be said to have lived its life. Additionally, the

tariff Order issued for the biomass projects to be commissioned in the subsequent year

i.e. FY 2014-15 and the FY 2015-16 does not supersede the tariff Order(s) issued for

the projects commissioned in the FY 2013-14, as the tariff so determined shall continue

to be effective for twenty years thereafter i.e. for the entire term of the PPA. In the

present case the PPA is dated 22.06.2012 while the tariff in question was determined by

the Commission vide its Order dated 20.11.2013. Hence, the PPA will certainly not

contain the tariff which was determined at a much later stage. At the most it mentions

that the tariff applicable shall be as determined by the Commission for the relevant year

in this case for the projects to be commissioned in the FY 2013-14. Therefore,

correcting apparent computational errors does in no way tantamount to re-writing the

terms of contract.

In view of the above, I answer the above issue in negative i.e. the doctrine of

promissory estoppels does not get triggered in the present case.

Conclusion

1. PLF for the first year shall be pegged at 65% instead of 70%. Hence, the first year

tariff for the biomass based power projects commissioned in the FY 2013-14 shall be

accordingly corrected.

2. The deprecation shall be aligned with the HERC RE Regulations, 2010. However, in

view of the Commission’s Order dated 9.10.2015 wherein the yearly tariff for the

projects commissioned in the FY 2013-14 has already been revised in regard to

calculation of deprecation from the date of notification of the 4th Amendment i.e.

12.08.2015, hence the same shall now be corrected for the period up to 12.08.2015

only.

Date: 18th October, 2016 (M. S. Puri) Place: Panchkula Member