bayesian estimation - · pdf fileintroduction bayesian estimation: the basics priors...

TRANSCRIPT

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Dynamic Macro

Bayesian Estimation

Petr Sedlacek

Bonn University

Summer 2015

1 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

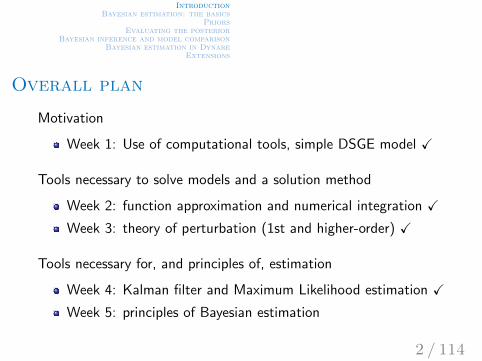

Overall plan

Motivation

Week 1: Use of computational tools, simple DSGE model X

Tools necessary to solve models and a solution method

Week 2: function approximation and numerical integration X

Week 3: theory of perturbation (1st and higher-order) X

Tools necessary for, and principles of, estimation

Week 4: Kalman filter and Maximum Likelihood estimation X

Week 5: principles of Bayesian estimation

2 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Plan for today

Bayesian estimation: the basic ideas

extra information over ML: priors

main challenge: evaluating the posterior

Markov Chain Monte Carlo (MCMC)

practical issues: acceptance rate, diagnostics

implementation in Dynare

3 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

Bayesian estimation: basic concepts

4 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

Frequentist vs. Bayesian views

Frequentist view:

parameters are fixed, but unknown

likelihood is a sampling distribution for the data

realizations of observables YT

just one of many possible realizations from L(YT |Ψ)

inferences about Ψ

based on probabilities of particular YT for given Ψ

5 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

Frequentist vs. Bayesian views

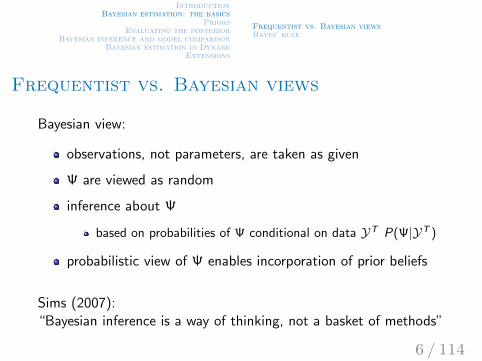

Bayesian view:

observations, not parameters, are taken as given

Ψ are viewed as random

inference about Ψ

based on probabilities of Ψ conditional on data YT P(Ψ|YT )

probabilistic view of Ψ enables incorporation of prior beliefs

Sims (2007):“Bayesian inference is a way of thinking, not a basket of methods”

6 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

Bayes’ rule

1701-1761

7 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

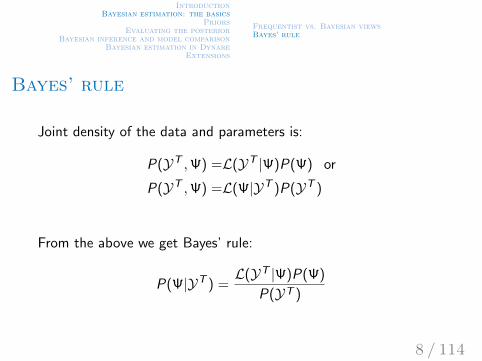

Bayes’ rule

Joint density of the data and parameters is:

P(YT ,Ψ) =L(YT |Ψ)P(Ψ) or

P(YT ,Ψ) =L(Ψ|YT )P(YT )

From the above we get Bayes’ rule:

P(Ψ|YT ) =L(YT |Ψ)P(Ψ)

P(YT )

8 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

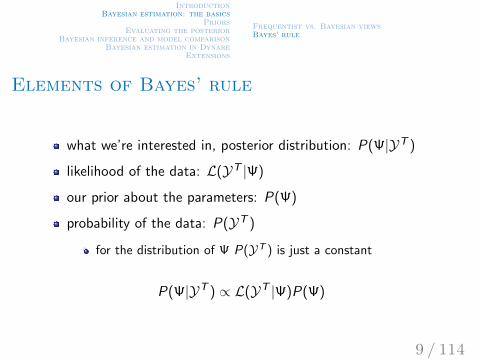

Elements of Bayes’ rule

what we’re interested in, posterior distribution: P(Ψ|YT )

likelihood of the data: L(YT |Ψ)

our prior about the parameters: P(Ψ)

probability of the data: P(YT )

for the distribution of Ψ P(YT ) is just a constant

P(Ψ|YT ) ∝ L(YT |Ψ)P(Ψ)

9 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

What is the challenge?

getting the posterior is typically not such a big deal

problem is that we often want to know more:

conditional expected values of a function of the posterior

like mean, variance, model etc.

10 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

What is the challenge?

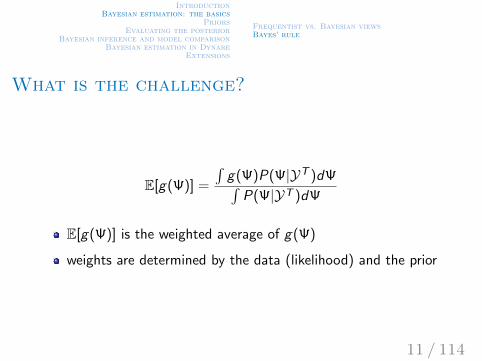

E[g(Ψ)] =

∫g(Ψ)P(Ψ|YT )dΨ∫

P(Ψ|YT )dΨ

E[g(Ψ)] is the weighted average of g(Ψ)

weights are determined by the data (likelihood) and the prior

11 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

What is the challenge?

we need to be able to evaluate the integral!

Special/Simple case:

we are able to draw Ψ from P(Ψ|YT )

can evaluate integral via Monte Carlo integration

you won’t be lucky enough to experience this case

12 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Frequentist vs. Bayesian viewsBayes’ rule

Evaluating the posterior

Our situation:

we can calculate P(Ψ|YT ), but we cannot draw from it

Solutions:

numerical integration

Markov Chain Monte Carlo (MCMC) integration

What is the standard?

although numerical integration is fast and accurate

computational burden rises exponentially with dimension

suited for low-dimension problems

→ use MCMC methods

13 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Priors

14 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Idea of priors

summarize prior information

previous studies

data not used in estimation

pre-sample data

other countries etc.

don’t be too restrictive

more on prior selection in “extensions”

15 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Priors

Most commonly used distributions:

normal

beta, support ∈ [0, 1]

persistence parameters

(inverted-) gamma, support ∈ (0,∞)

volatility parameters

uniform

16 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Prior predictive analysis

check whether priors “make sense”

use the prior as the posterior

steady state?

impulse response functions?

17 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Some terminology

Jeffreys prior

non-informative prior

improper vs. proper priors

improper prior is non-integrable (integral is ∞)

important to have proper distributions for model comparison

18 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Some terminology

(natural) conjugate priors

family of prior distributions

after multiplication with the likelihood

produce a posterior of the same family

Minnesota (Litterman) prior

used in VARs for distribution of lags

19 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Evaluating the posterior

20 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Starting point

Aim is to be able to calculate something like

E[g(Ψ)] =

∫g(Ψ)P(Ψ|YT )dΨ∫

P(Ψ|YT )dΨ

we know how to calculate P(Ψ|YT )

but we cannot draw from it

the system is too large for numerical integration

21 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Principle of posterior evaluation

We cannot draw from the “target” distribution, but

1. can draw from a different, “stand-in”, distribution

2. can evaluate both stand-in and target distributions

3. comparing the two, we can re-weigh the draw “cleverly”

22 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Principle of posterior evaluation

the above procedure is the idea of “importance sampling”

MCMC methods effectively a version of importance sampling

traveling through the parameter space is more sophisticated

and or acceptance probability more sophisticated

23 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

A few simple examples

Problem:

we want to simulate x

x comes from truncated normal with

mean µ and variance σ2

and a < x < b

Solution:

1. draw y from N(µ, σ2)

2a. if y ∈ (a, b) then keep draw (accept) and go back to 1

2b. otherwise discard draw (reject) and go back to 1

24 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

A few simple examples

Problem:

want to draw x from F (x), but we cannot

we can sample from G (x) and f (x) ≤ cg(x) ∀xSolution:

1. sample y from G (y)

2. accept draw with probability f (y)cg(y) and go back to 1

Note:

acceptance rate higher for lower c

optimal c is c = supxf (x)g(x)

Metropolis-Hastings sampler (MCMC) is a generalization

25 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

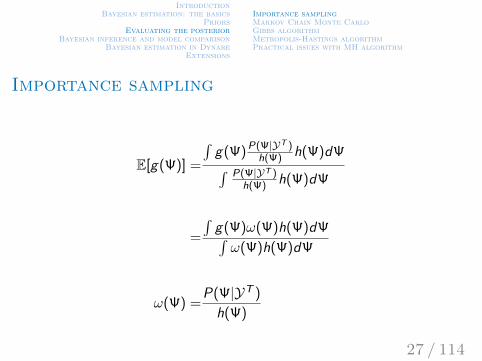

Importance sampling

Main idea very similar to the previous example:

cannot draw from P(Ψ|YT )

but can draw from H(Ψ)

be smart in reweighing (accepting) the draws

26 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Importance sampling

E[g(Ψ)] =

∫g(Ψ) P(Ψ|YT )

h(Ψ) h(Ψ)dΨ∫ P(Ψ|YT )h(Ψ) h(Ψ)dΨ

=

∫g(Ψ)ω(Ψ)h(Ψ)dΨ∫ω(Ψ)h(Ψ)dΨ

ω(Ψ) =P(Ψ|YT )

h(Ψ)

27 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Importance sampling

Approximate the integral using MC integration:

E[g(Ψ)] ≈∑M

m=1 ω(Ψ(m))g(Ψ(m))∑Mm=1 ω(Ψ(m))

M is the number of draws from importance function h(Ψ)

28 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

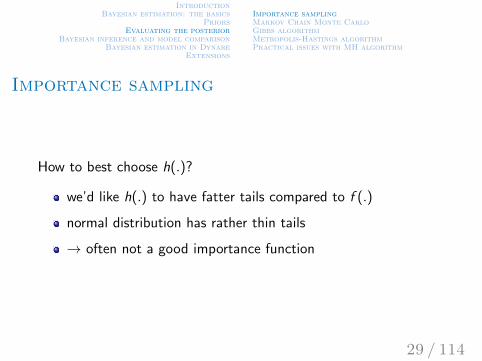

Importance sampling

How to best choose h(.)?

we’d like h(.) to have fatter tails compared to f (.)

normal distribution has rather thin tails

→ often not a good importance function

29 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Before we move on

3 doors, behind one of them is a car

pick one

I will open one of the remaining two without the car

you can choose to stick with your choice or switch

who stays and who switches?

30 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Some preliminaries for MCMC

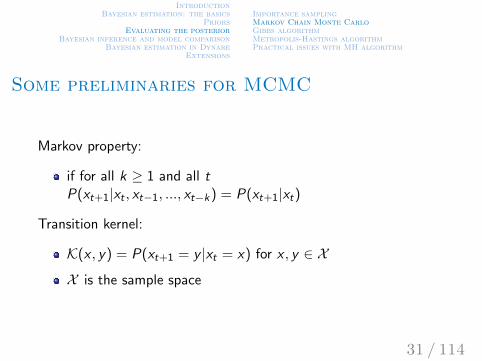

Markov property:

if for all k ≥ 1 and all tP(xt+1|xt , xt−1, ..., xt−k ) = P(xt+1|xt)

Transition kernel:

K(x , y) = P(xt+1 = y |xt = x) for x , y ∈ X

X is the sample space

31 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Main idea behind MCMC methods

as before, we’d like to sample from P(Ψ|YT ), but we cannot

MCMC methods provide a way to

create a Markov chain transition kernel (K) for Ψ

that has an invariant density P(Ψ|YT )

given K simulate the Markov chain P ′ = KP

starting with some initial values P(Ψ0)

(eventually) distribution of Markov chain → P(Ψ|YT )

32 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Main idea behind MCMC methods

a principle of constructing such kernels

→ Metropolis (-Hastings) algorithm (MH)

the Gibbs sampler is a special case

33 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Gibbs algorithm

special case of the MH algorithm

applies when can sample from each conditional distribution

again, this will rarely be applicable in our case

34 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Gibbs algorithm

instead of draws of Ψ from P(Ψ|YT )

portion Ψ into k blocks

sample each from P(Ψj |YT ,Ψ−j ) for j = 1, ..., k

iterate until convergence

35 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Gibbs sampling

Iterations (k = 2):

initiate sample with Ψ0

then iterate according to:

Ψ1i+1 ∼ P(Ψ1|YT ,Ψ2

i )

Ψ2i+1 ∼ P(Ψ2|YT ,Ψ1

i )

can prove that the above converges to P(Ψ|YT )

discard first B number of draws to eliminate influence of Ψ0

36 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

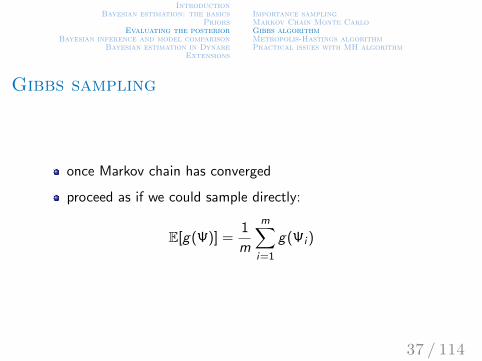

Gibbs sampling

once Markov chain has converged

proceed as if we could sample directly:

E[g(Ψ)] =1

m

m∑i=1

g(Ψi )

37 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

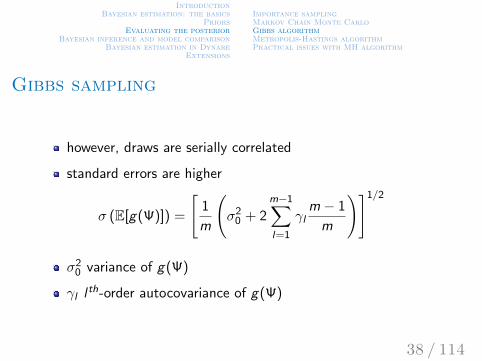

Gibbs sampling

however, draws are serially correlated

standard errors are higher

σ (E[g(Ψ)]) =

[1

m

(σ2

0 + 2m−1∑l=1

γlm − 1

m

)]1/2

σ20 variance of g(Ψ)

γl lth-order autocovariance of g(Ψ)

38 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Metropolis-Hastings algorithm

Main idea same as with importance sampling:

1. draw from a stand-in distribution h(Ψ; θ)

θ explicitly shows parameters of stand-in distribution

e.g. mean (µh ) and variance (σ2h)

2. accept/reject based on probability q(Ψi+1|Ψi )

3. go back to 1

3a. stand-in density does not change (indpendent MH)

3b. mean of stand-in adjusts (random walk MH)

can show convergence to target distribution

39 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

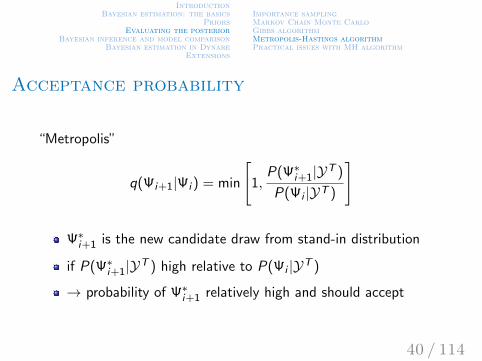

Acceptance probability

“Metropolis”

q(Ψi+1|Ψi ) = min

[1,

P(Ψ∗i+1|YT )

P(Ψi |YT )

]

Ψ∗i+1 is the new candidate draw from stand-in distribution

if P(Ψ∗i+1|YT ) high relative to P(Ψi |YT )

→ probability of Ψ∗i+1 relatively high and should accept

40 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

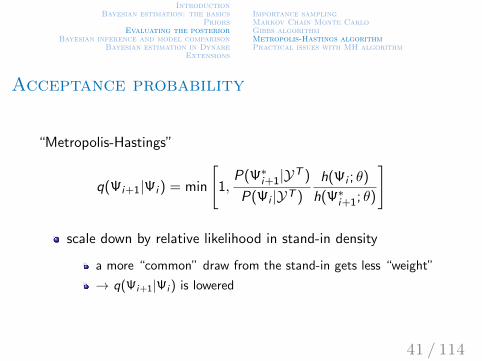

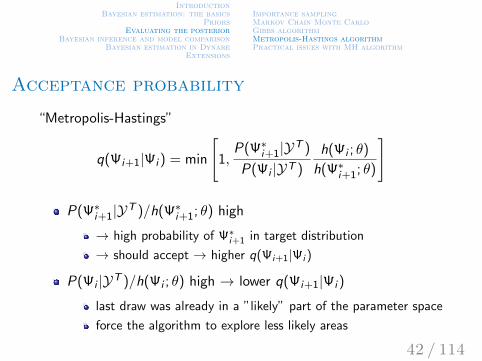

Acceptance probability

“Metropolis-Hastings”

q(Ψi+1|Ψi ) = min

[1,

P(Ψ∗i+1|YT )

P(Ψi |YT )

h(Ψi ; θ)

h(Ψ∗i+1; θ)

]

scale down by relative likelihood in stand-in density

a more “common” draw from the stand-in gets less “weight”

→ q(Ψi+1|Ψi ) is lowered

41 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Acceptance probability

“Metropolis-Hastings”

q(Ψi+1|Ψi ) = min

[1,

P(Ψ∗i+1|YT )

P(Ψi |YT )

h(Ψi ; θ)

h(Ψ∗i+1; θ)

]

P(Ψ∗i+1|YT )/h(Ψ∗i+1; θ) high

→ high probability of Ψ∗i+1 in target distribution

→ should accept → higher q(Ψi+1|Ψi )

P(Ψi |YT )/h(Ψi ; θ) high → lower q(Ψi+1|Ψi )

last draw was already in a ”likely” part of the parameter space

force the algorithm to explore less likely areas

42 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Updating the stand-in density

“Independence chain variant”

stand-in distribution does not change

it is independent across Monte Carlo replications

this is also the case in importance-sampling

43 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

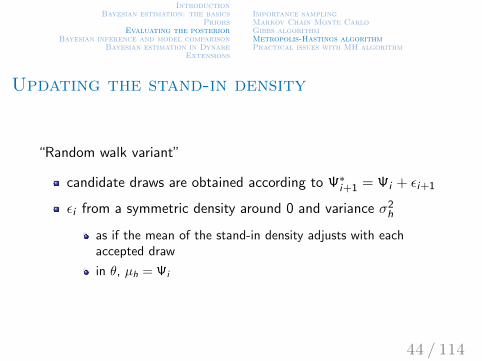

Updating the stand-in density

“Random walk variant”

candidate draws are obtained according to Ψ∗i+1 = Ψi + εi+1

εi from a symmetric density around 0 and variance σ2h

as if the mean of the stand-in density adjusts with eachaccepted draw

in θ, µh = Ψi

44 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Summary of MCMC with MH algorithm

1. maximize log-posterior logP(YT |Ψ) + logP(Ψ)

this yields the posterior mode Ψ

2. draw from a stand-in distribution h(Ψ; θ)

should have fatter tails than posterior

3. accept/reject based on probability q(Ψi+1|Ψi )

Metropolis vs. Metropolis-Hastings specification

4. go back to 2

adjust (random walk variant) stand-in distribution

do not adjust (independence variant) stand-in distribution

45 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Summary of MCMC with MH algorithm

evaluation of the likelihood (step 1 and 3) requires

computation of the steady state

solution of the model

constructing the likelihood function (via the Kalman filter)

46 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

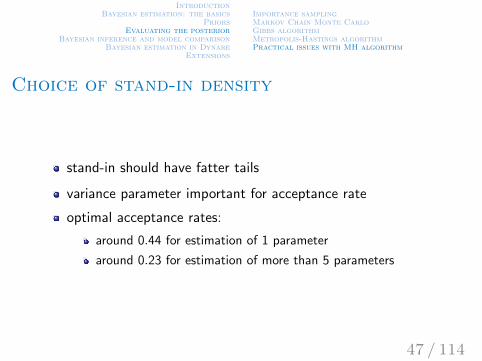

Choice of stand-in density

stand-in should have fatter tails

variance parameter important for acceptance rate

optimal acceptance rates:

around 0.44 for estimation of 1 parameter

around 0.23 for estimation of more than 5 parameters

47 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Choice of stand-in density

often, stand-in is N(Ψ, c2ΣΨ)

Ψ is the posterior mode

ΣΨ is the inverse (negative) Hessian at the mode

tip: start with c = 2.4/√d

d is number of estimated parameters

increase (decrease) c if acceptance rate is too high (low)

48 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

Convergence statistics

theory says that distribution will converge to target

when does this happen?

→ diagnostic tests

sequence of draws should be from the invariant distribution

moments should not change within/between sequences

49 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

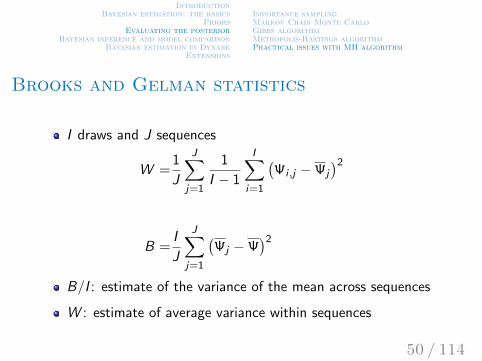

Brooks and Gelman statistics

I draws and J sequences

W =1

J

J∑j=1

1

I − 1

I∑i=1

(Ψi ,j −Ψj

)2

B =I

J

J∑j=1

(Ψj −Ψ

)2

B/I : estimate of the variance of the mean across sequences

W : estimate of average variance within sequences

50 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

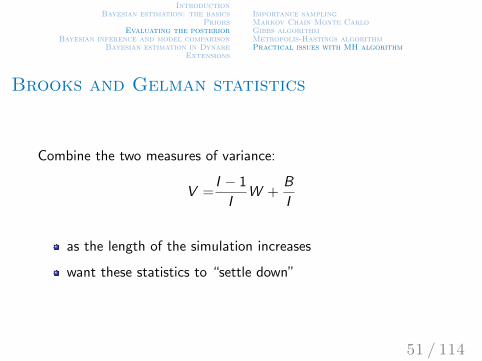

Brooks and Gelman statistics

Combine the two measures of variance:

V =I − 1

IW +

B

I

as the length of the simulation increases

want these statistics to “settle down”

51 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Importance samplingMarkov Chain Monte CarloGibbs algorithmMetropolis-Hastings algorithmPractical issues with MH algorithm

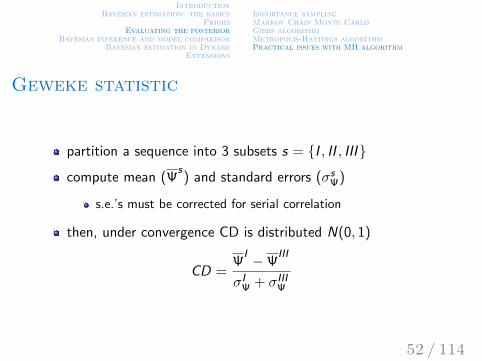

Geweke statistic

partition a sequence into 3 subsets s = I , II , III

compute mean (Ψs) and standard errors (σs

Ψ)

s.e.’s must be corrected for serial correlation

then, under convergence CD is distributed N(0, 1)

CD =Ψ

I −ΨIII

σIΨ + σIII

Ψ

52 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

Bayesian inference and model comparison

53 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

Bayesian vs. frequentist inference

Bayesian inference cannot use frequentist principles

t-test, F-test, LR-test etc.

they have a frequentist justification of repeated sampling

instead, there are two common Bayesian principles:

Highest Posterior Density (HPD) interval

Bayes factors (posterior odds)

54 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

Highest posterior density intervals

A 100(1− α)% posterior interval for Ψ is given by

P(b < Ψ < b) =

∫ b

bP(Ψ|YT )dΨ = 1− α

there exists many such intervals

the HPD interval is the smallest one of them

55 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

HPD “tests”

the HPD test amounts to checking whether Ψi ∈ HPD1−α

this is an informal way of comparing nested models

i.e. different parameter values

Bayesians can also compare non-nested models

56 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

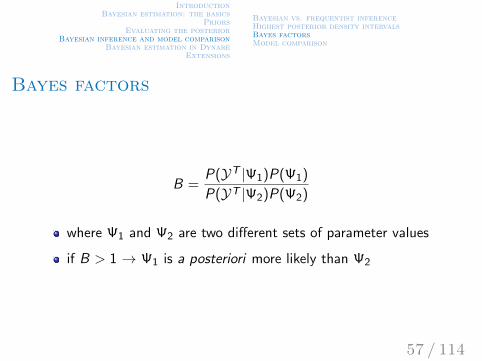

Bayes factors

B =P(YT |Ψ1)P(Ψ1)

P(YT |Ψ2)P(Ψ2)

where Ψ1 and Ψ2 are two different sets of parameter values

if B > 1 → Ψ1 is a posteriori more likely than Ψ2

57 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

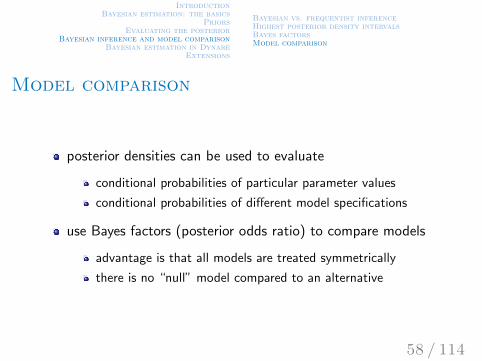

Model comparison

posterior densities can be used to evaluate

conditional probabilities of particular parameter values

conditional probabilities of different model specifications

use Bayes factors (posterior odds ratio) to compare models

advantage is that all models are treated symmetrically

there is no “null” model compared to an alternative

58 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

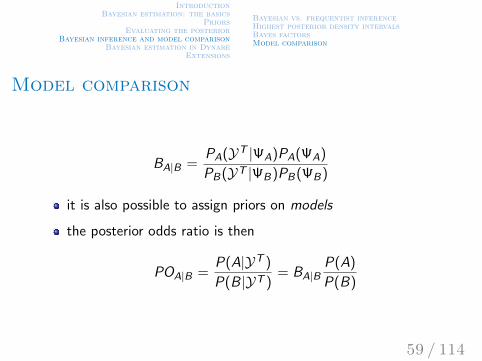

Model comparison

BA|B =PA(YT |ΨA)PA(ΨA)

PB(YT |ΨB)PB(ΨB)

it is also possible to assign priors on models

the posterior odds ratio is then

POA|B =P(A|YT )

P(B|YT )= BA|B

P(A)

P(B)

59 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

Model comparison

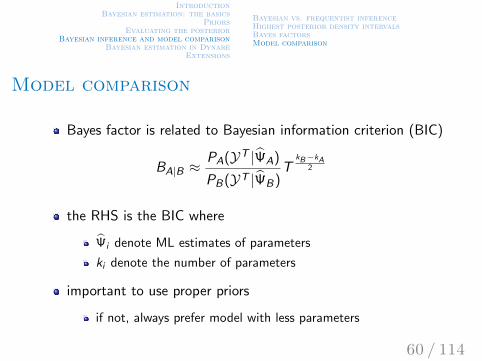

Bayes factor is related to Bayesian information criterion (BIC)

BA|B ≈PA(YT |ΨA)

PB(YT |ΨB)T

kB−kA2

the RHS is the BIC where

Ψi denote ML estimates of parameters

ki denote the number of parameters

important to use proper priors

if not, always prefer model with less parameters

60 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

Bayesian vs. frequentist inferenceHighest posterior density intervalsBayes factorsModel comparison

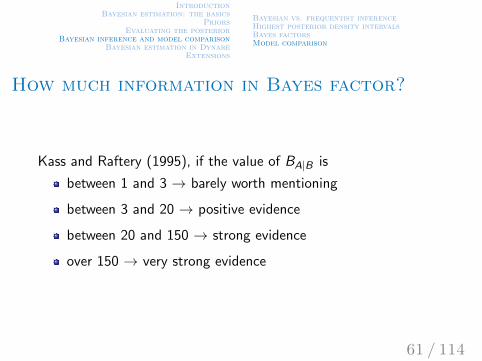

How much information in Bayes factor?

Kass and Raftery (1995), if the value of BA|B is

between 1 and 3 → barely worth mentioning

between 3 and 20 → positive evidence

between 20 and 150 → strong evidence

over 150 → very strong evidence

61 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare

62 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Preliminaries

setup is the same as with ML estimation

always a good idea to solve model first

some parameter values are likely to remain calibrated

63 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

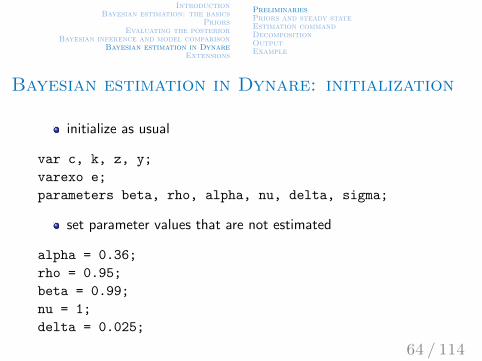

Bayesian estimation in Dynare: initialization

initialize as usual

var c, k, z, y;

varexo e;

parameters beta, rho, alpha, nu, delta, sigma;

set parameter values that are not estimated

alpha = 0.36;

rho = 0.95;

beta = 0.99;

nu = 1;

delta = 0.025;

64 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare: setting it up

after model part, and specification of steady state

tell Dynare which parameters he should estimate

estimated params;

stderr e, inv gamma pdf, 0.01, inf;

end;

the above tells Dynare to

estimate σ, the st. error of the productivity disturbance

the prior distribution is an inverted gamma

the prior mean is 0.01 and the prior st. error is ∞

65 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare: steady state

steady state calculated for many different values of Ψ!

solve for the steady state yourself (linearizing makes it easier)

give the exact steady state to Dynare for the initial values

option to provide own function that calculates steady state!

modfilename steadystate.m or

steady state model; block

66 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare: estimation

then also tell Dynare which are the observable variables

varobs y;

estimation(options);

options include

specify data file for estimation: datafile=data

number of MH sequences: mh nblocks

number of MH replications: mh replic

parameter of stand-in distribution variance (c): mh jscale

variance of initial draw: mh init scale

first observation (default first): first obs

sample size (default all): nobs

many more!67 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare: decomposition

decompose endogenous variables into contribution of shocks

possible also after stoch simul

shock decomposition(options) variables;

options include e.g. parameter set

use calibrated values: =calibration

use prior/posterior mode: =prior mode/=posterior mode

variables specifies for which variables to run the decomposition

68 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare: output

RESULTS FROM POSTERIOR MAXIMIZATION:

most important is the mode

other stuff based on normality assumptions (typically violated)

when Dynare gets to MCMC part it shows:

in which MCMC sequence you are

which fraction has been completed

acceptance rate: adjust mh jscale appropriately

remember that low acceptance rate

→ algorithm travels through a larger part of Ψ domain

69 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Bayesian estimation in Dynare: plots

priors

MCMC diagnostics

prior and posterior densities

shocks implied at the mode

observables and corresponding implied values

70 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Estimating the neoclassical growth model

use neoclassical growth model as data generating process

265 observations of output

use Bayesian estimation to estimate

σ

σ, ρ, δ, α

71 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Estimating the neoclassical growth model

Easy case:

estimated params;

stderr e, inv gamma pdf, 0.01, inf;

end;

varobs y;

estimation(datafile=y,mh nblocks=1,mh replic=10000,

mh jscale=3,mh init scale=12) c, k, y;

72 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

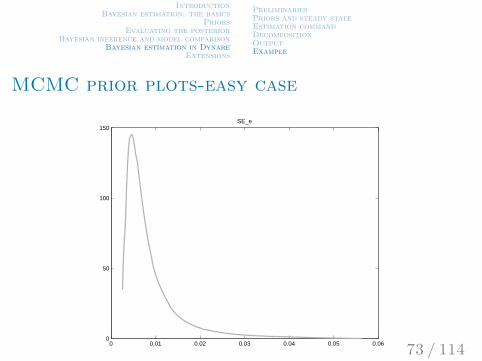

MCMC prior plots-easy case

0 0.01 0.02 0.03 0.04 0.05 0.060

50

100

150SE_e

73 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

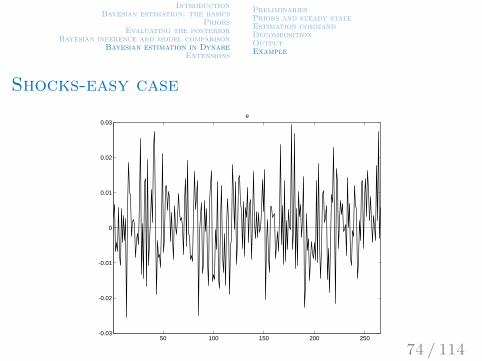

Shocks-easy case

50 100 150 200 250-0.03

-0.02

-0.01

0

0.01

0.02

0.03e

74 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

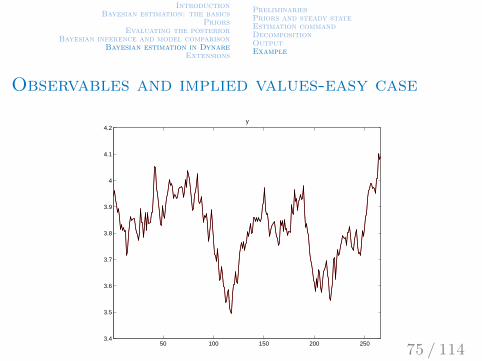

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Observables and implied values-easy case

50 100 150 200 2503.4

3.5

3.6

3.7

3.8

3.9

4

4.1

4.2y

75 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

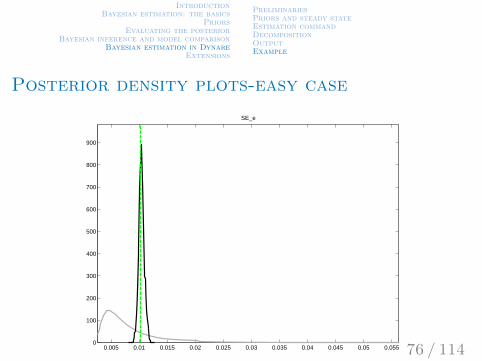

Posterior density plots-easy case

0.005 0.01 0.015 0.02 0.025 0.03 0.035 0.04 0.045 0.05 0.0550

100

200

300

400

500

600

700

800

900

SE_e

76 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Printed results - easy case

Posterior mode:

0.0103 (0.0004)

Average acceptance rate:

37.7%

Diagnostic statistics (Geweke):p-values on equality of means in sub-samples

0.037 (no taper) 0.33 (4% taper) 0.38 (8% taper) etc.

Posterior mean and HPD interval:

0.0104 (0.0096 - 0.0111)

77 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

What we did today

Basic concept of Bayesian estimation

priors

evaluating the posterior

Markov Chain Monte Carlo (MCMC)

practical issues

acceptance rate, diagnostics

implementation in Dynare

78 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

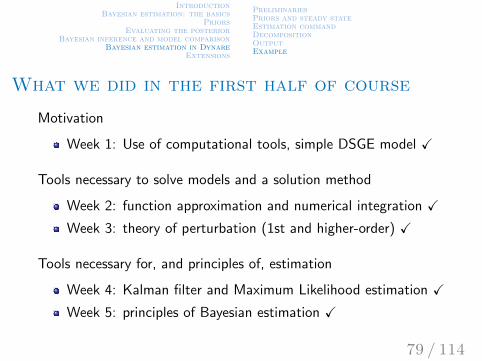

What we did in the first half of course

Motivation

Week 1: Use of computational tools, simple DSGE model X

Tools necessary to solve models and a solution method

Week 2: function approximation and numerical integration X

Week 3: theory of perturbation (1st and higher-order) X

Tools necessary for, and principles of, estimation

Week 4: Kalman filter and Maximum Likelihood estimation X

Week 5: principles of Bayesian estimation X

79 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

PreliminariesPriors and steady stateEstimation commandDecompositionOutputExample

Extensions

80 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Trends

Problem:

methodology works for stationary environments

data has trends

not clear which trend the model represents?

81 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Trends

1940 1950 1960 1970 1980 1990 2000 2010 2020-15

-10

-5

0

5

10

devi

atio

ns fr

om tr

end

(%)

HP (1600)

HP(105)

linear

quadratic

BP(6,32)

82 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Trends

we could build in a trend within the model

e.g. productivity is trending

“stationarize” non-stationary variables within the model

i.e. inspect variables relative to productivity

however, not clear that data satisfies balanced growth

83 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Trends

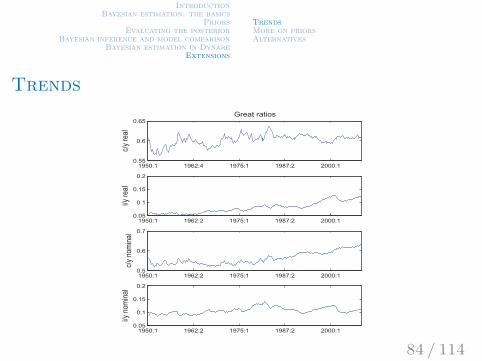

b) Build-in a trend into the model. Detrend the data with model-based-trend. Problem: data does not seem to satisfy balanced growth.

1950:1 1962:4 1975:1 1987:2 2000:10.55

0.6

0.65Great ratios

c/y re

al

1950:1 1962:2 1975:1 1987:2 2000:10.05

0.1

0.15

0.2

i/y re

al

1950:1 1962:2 1975:1 1987:2 2000:10.5

0.6

0.7

c/y n

omina

l

1950:1 1962:2 1975:1 1987:2 2000:10.05

0.1

0.15

0.2

i/y n

omina

l

0 0.2 0.4 0.6 0.8 1−20

−10

0Log spectra

0 0.2 0.4 0.6 0.8 1−20

−10

0

0 0.2 0.4 0.6 0.8 1−20

−10

0

0 0.2 0.4 0.6 0.8 1−20

−10

0

Real and nominal Great ratios in US, 1950-2008.

84 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Trends

Solutions:

use differenced data

highlights high-frequency movements (measurement error)

detrend prior to estimation

85 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Estimation on detrended data

use e.g. quadratic trend:

yt = a0 + a1t + a2t2 + ut

each variable can have its own trend

using HP or Band Pass filter:

yobs−filteredt = B(L)yobs

t

B(L) is a 2-sided filter!

→ creates artificial serial correlation in the filtered data

→ apply filter also to model data

86 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Estimation on detrended data

the above implies that the model is fitted to low(er)frequencies only

Canova (2010) points out that the above can lead to:

underestimated volatility of shocks

persistence of shocks is overestimated

less perceived noise → decisions rules imply higherpredictability

substitution and income effects may be distorted due to theabove

proposes to estimate flexible trend specifications within model

87 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

More on selecting priors

what we’ve described is based on selecting (independent)priors about deep parameters

however, often we have priors about observables

moreover, reasonable independent priors may form ratherunreasonable properties of the model

solutions proposed in the literature:

Del Negro, Schorfheide (2008)

Andrle, Benes (2013)

Jarocinsky, Marcet (2013)

88 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Del Negro, Schorfheide (2008)

more guidance for eliciting priors

three main issues with (independent) priors about deepparameters:

may lead to probability mass on unrealistic properties of themodel

most exogenous shock processes are latent, i.e. difficult toform priors about

priors are often transfered to different models

89 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Del Negro, Schorfheide (2008)

they group parameters into three categories:

those determining the steady state

those determining exogenous shocks

those determining the endogenous propagation mechanism

90 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Del Negro, Schorfheide (2008)

Parameters related to steady state relationships

discount rate, depreciation, returns to scale, inflation targetetc.

let SD(Ψss) be a vector of steady state relationshipsdepending on a set of parameters Ψss

then S = SD(Ψss) + η are measurements of thoserelationships with measurement error η

S has a probabilistic interpretation and therefore

using Bayes’ rule, one can write P(Ψss |S) ∝ L(S |Ψss)P(Ψss)

allows for overidentification

91 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Del Negro, Schorfheide (2008)

Exogenous processes

volatility and persistence parameters

use implied moments of endogenous variables to “back out”priors

the above is given values for Ψss and Ψendo

→ valid for a particular model and should not be directlytransfered across models

92 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Del Negro, Schorfheide (2008)

Endogenous propagation mechanisms

price rigidity, labor supply elasticity etc.

one could use similar principle as above

authors suggest independent priors because researchers oftenhave a relatively good idea

note that the joint prior induces non-trivial non-linearrelationships between parameters

joint prior becomes

P(Ψ|S) ∝ L(S |Ψss)P(Ψss)P(Ψendo)

requires an additional step in MCMC algorithm

93 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Andrle, Benes (2013)

Andrle and Benes do not distinguish between groups ofparameters

their “system priors” are priors about concepts such as

impulse response functions

conditional correlations etc.

94 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Andrle, Benes (2013)

even sensible individual-parameter priors can lead tounintended properties of the aggregate model

independence of priors can lead to substantial mass on suchparameter regions

call for careful prior-predictive analysis:

IRFs, second moments ...

compare with posterior results

is it the data or the model driving the results?

95 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Andrle, Benes (2013)

Candidates for system priors:

steady states

sensible values in levels or growth rates

(un-)conditional moments

cross-correlations (conditional on shocks)

impulse response properties

peak impacts, duration, horizon of monetary policyeffectiveness etc.

96 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Andrle, Benes (2013)

Implementation:

use Bayes’ rule again

specify model properties you care about Z = h(Ψ)

these can be characterized by a probabilistic modelZ ∼ D(Z s)

D(Z s) is a distribution function

Z s are parameters of that function (hyper-parameters)

its likelihood function (the system prior): P(Z s |Ψ, h)

composite joint prior: P(Ψ|Z s , h) ∝ P(Z s |Ψ, h)P(Ψ)

97 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Andrle, Benes (2013)

The posterior becomes

P(Ψ|YT ,Z s) ∝ L(YT |Ψ)P(Z s |Ψ, h)P(Ψ)

evaluation is in principle the same as before

use of MCMC methods

additional step in evaluating the system prior

slows things down - have to run MCMC on prior (withlikelihood “switched off”) and then posterior

98 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Jarocinsky, Marcet (2013)

similar ideas as above, but in the context of Bayesian VARs

their point is that widely used priors about parameters

can lead to behavior of observables that is counterfactual

→ always a good to do prior-predictive analysis of you model!

99 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Alternatives to Bayesian estimation

Maximum likelihood

calibration

GMM

SMM & indirect inference

100 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Maximum likelihood

we’ve seen it yesterday

conceptually different from Bayesian estimation

tools required part of Bayesian estimation

101 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Calibration

wide-spread methodology at least since Kydland and Prescott(1982)

prior to this, state-of-the-art were systems of simultaneousequations

those were viewed as “true statistical” models to be estimated

102 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Calibration

although calibration is also an empirical exercise

it lacks the probabilistic interpretation

the constraint is that the model mimics (a priori identified)features in the data

Kydland and Prescott (1996):It is important to emphasize that the parameter values selected arenot the ones that provide the best fit in some statistical sense.

103 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Calibration

Parameters are pinned down by a selection of real-world features

long-run averages (labor share, hours worked)

micro studies (preference parameters)

certain business cycle properties of the data (shockparameters) etc.

104 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Calibration

compare different features of the data to model predictions

closely related to moment-matching (estimating models)

however, calibration lacks the statistical formality

the above is a strong source of criticism of calibration

no formal rules on selecting dimension to which model is fit

no formal rules of comparing alternatives - models arenecessarily misspecified

not that the last point does not hold for Bayesian modelcomparison

105 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Matching moments (GMM, SMM, II)

idea similar to calibration:

a set of moments (features) of the data used to parameterizemodel

a different set of moments used to judge the performance ofmodel

matching moments adds statistical rigor

estimation

hypothesis testing

106 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Matching moments (GMM, SMM, II)

as with calibration, moment matching is based on a selectionof moments

often referred to as limited-information procedures

a full range of statistical implications contained in model’slikelihood function

disadvantages of limited-information procedures

potential loss of efficiency

inference potentially sensitive to selected moments

advantages of limited-information procedures

no need to make distributional assumptions

107 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Generalized method of moments

attributed to Hansen (1982), generalization, asymptoticproperties

the main idea is to use “orthogonality conditions” (e.g.first-order-conditions)

E[f (xt ,Ψ)] = 0

xt is a vector of variables

Ψ are model parameters

108 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Generalized method of moments

pick Ψ s.t. the sample analogs of orthogonality conditionsg(X ,Ψ) = 1/T

∑t f (xt ,Ψ)

hold exactly, exactly identified case

number of parameters = number of moment conditions

are as close to zero as possible, overidentified case

are number of parameters < number of moment conditions

109 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Generalized method of moments

in the over-identified case

minΨ

g(X ,Ψ)′Ωg(X ,Ψ)

Ω is a weighting matrix

the optimal weighting matrix is the inverse of the var-covarmatrix of g(X ,Ψ)

110 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Simulated method of moments

in some cases the orthogonality conditions cannot be assessedanalytically

moment-matching estimation based on simulations retainsasymptotic properties of GMM

111 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Simulated method of moments

let zt be model variables corresponding to data xt

let empirical targets be summarized by h(xt)

SMM estimation is based on

E[h(xt)] = E[h(zt ,Ψ)]

→ f (xt ,Ψ) = h(xt)− h(zt ,Ψ)

112 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Indirect inference

based on reduced-form models

main idea is to use structural model to interpret reduced-formresults

can simulated data from a structural model replicate areduced-form estimate using real-world data?

i.e. it is a moment-matching exercise

moments are clearly defined by prior reduced-form analysis

113 / 114

IntroductionBayesian estimation: the basics

PriorsEvaluating the posterior

Bayesian inference and model comparisonBayesian estimation in Dynare

Extensions

TrendsMore on priorsAlternatives

Indirect inference

let δ be a vector of reduced-form estimates

δ(xt) are those in the data and δ(zt ,Ψ) are those from themodel

pick Ψ s.t.δ(xt) = δ(zt ,Ψ)

114 / 114