based on research by roger ibbotson, james xiong, robert p. kreitler, charles f. kreitler, and peng...

Post on 19-Dec-2015

217 views

TRANSCRIPT

BASED ON RESEARCH BY ROGER IBBOTSON, JAMES XIONG,

ROBERT P. K R E I T L E R , CHARLES F. KREITLER, AND PENG CHEN

National Savings Rate Guidelines for Individuals

Financial Planning for Women

October 14, 2009Presented by Jean Lown, Ph.D.

PPT Design by Diana Burk

2

Upcoming FPW

FPW survey via e-mailNovember 11: All about Individual Retirement

Accounts & Why switch from a traditional to a

Roth IRA

3

How will these guidelines help me?

“Provides guidelines that

individuals of different ages, incomes, and accumulated wealth

can easily apply in determining

how much to save for an adequate retirement.”

4

Definitions

pre-retirement gross income: yearly income before subtracting any deductions

pre-retirement net income: gross income minus the amount saved for retirement each year during pre-retirement

savings: stocks, mutual funds, bonds, CDs, IRAs, savings accounts

% of pre-retirement income: post-retirement replacement income (calculated at 80% and 60%)

5

The Approach

The amount needed for retirement savings is calculated based on pre-retirement net income rather than gross income

Basing savings rate on pre-retirement net income significantly reduces the amount of money needed

6

Three Easy Steps

1. Determine the annual cash flow needed in retirement

2. Determine the capital (total $) needed to generate this lifetime retirement cash flow

3. Determine the annual savings needed to build the capital to provide retirement cash flow

7

Determine annual cash flow needed

Calculation of Assets Needed at Age 65 to Provide Retirement Cash Flow

Income Pre-retirement $20,000 $40,000 $60,000 $80,000 $100,000 $120,000

Less Annual Contributions to Savings $1,720 $ 4,880 $8,760 $13,120 $17,600 $23,040

Net Income (Gross Less Savings) $18,280 $35,120 $51,240 $66,880 $82,400 $96,960

Income Post-Retirement

(80% Replacement of Net Income) $14,624 $28,096 $40,992 $53,504 $65,920 $77,568

Sources of Retirement Income

Estimate Social Security $11,242 $17,795 $22,177 $25,252 $27,343 $27,343

Pension of Other Income -- -- -- -- -- --

Annual Cash Flow from Portfolio $3,382 $10,298 $18,815 $28,252 $38,577 $50,225

Total Annual Income in Retirement $14,624 $28,096 $40,992 $53,504 $65,920 $77,568

Portfolio Assets Needed to Provide Annual Cash Flow $64,946 $190,647 $434,847 $512,821 $697,144 $904,063

8

Determine Capital needed to generate lifetime retirement cash flow

Savings Rate for Different Income Levels with 80% or 60%

Replacement of Gross Income and No Past Savings

Age Income

SavingsRate for

80% Income

Replacement

SavingsRate for

60% IncomeReplacement

25 $20,000 6.8% 1.4%25 $40,000 10.0% 4.6%25 $60,000 12.0% 6.4%25 $80,000 13.8% 8.0%30 $20,000 8.8% 2.0%30 $40,000 12.8% 5.8%30 $60,000 15.6% 8.4%30 $80,000 17.2% 10.4%35 $20,000 11.4% 2.4%35 $40,000 16.4% 7.4%35 $60,000 19.6% 10.6%35 $80,000 22.0% 13.2%35 $100,000 23.8% 14.8%

Savings Rate for Different Income Levels with 80% or 60%

Replacement of Gross Income and No Past Savings

Age Income

SavingsRate for

80% IncomeReplacemen

t

SavingsRate for

60% IncomeReplacement

40 $20,000 14.8% 3.2%40 $40,000 21.6% 9.8%40 $60,000 25.8% 14.2%40 $80,000 29.0% 17.4%40 $100,000 31.0% 19.8%45 $20,000 20.0% 4.2%45 $40,000 29.4% 13.4%45 $60,000 35.0% 19.4%45 $80,000 39.4% 23.6%45 $100,000 42.8% 26.8%45 $120,000 46.2% 30.2%

Savings Rate for Different Income Levels with 80% or 60%

Replacement of Gross Income and No Past Savings

Age Income

SavingsRate for

80% IncomeReplacement

SavingsRate for

60% IncomeReplacement

50 $20,000 28.8% 6.0%50 $40,000 42.4% 19.0%50 $60,000 50.0% 27.2%50 $80,000 56.8% 33.4%50 $100,000 61.0% 39.0%50 $120,000 66.6% 43.8%55 $20,000 45.6% 9.6%55 $40,000 66.6% 30.2%55 $60,000 79.8% 43.8%55 $80,000 89.6% 53.2%55 $100,000 97.0% 62.0%55 $120,000 105.6% 70.0%60 $20,000 94.6% 19.6%60 $40,000 137.2% 62.4%60 $60,000 >150% 89.8%60 $80,000 >150% 111.2%60 $100,000 >150% 130.2%60 $120,000 >150% 146.0%

9

Example of how to use the table

Age Gross Income

Savings Rate

Deduction Each $10,000 of Portfolio

35 $20,000 8.60% 1.75%

35 $40,000 12.20% 0.86%

35 $60,000 14.60% 0.55%

35 $80,000 16.40% 0.43%

35 $100,000 17.60% 0.34%

A 35 year old with gross income of $80,000 needs to save 16.4% or $13,120, leaving net income of $66,880.

However, if already saved $100,000, then deduct 10 x 0.43% = 4.3% so that should save 16.4% - 4.3% = 12.1%, each year until retirement.

10

Determine Capital needed to generate lifetime retirement cash flow 80%

Savings Rate for Different Gross Income Levels with 80% Replacement of Net Income

Age IncomeSavings

Rate

Deduction Each

$10,000 of Portfolio

25 $20,000 5.8% 1.60%25 $40,000 8.2% 0.78%25 $60,000 10.0% 0.55%25 $80,000 11.2% 0.40%30 $20,000 7.0% 1.65%30 $40,000 10.0% 0.79%30 $60,000 11.8% 0.54%30 $80,000 13.6% 0.42%35 $20,000 8.6% 1.75%35 $40,000 12.2% 0.86%35 $60,000 14.6% 0.55%35 $80,000 16.4% 0.43%35 $100,000 17.6% 0.34%

Savings Rate for Different Gross Income Levels with 80%

Replacement of Net Income

Age IncomeSavings

Rate

Deduction Each

$10,000 of Portfolio

40 $20,000 10.2% 1.67%40 $40,000 14.8% 0.86%40 $60,000 17.6% 0.57%40 $80,000 19.8% 0.42%40 $100,000 21.4% 0.35%45 $20,000 12.4% 1.76%45 $40,000 18.0% 0.90%45 $60,000 21.4% 0.59%45 $80,000 24.0% 0.45%45 $100,000 26.2% 0.37%45 $120,000 28.2% 0.31%

Savings Rate for Different Gross Income Levels with 80%

Replacement of Net Income

Age IncomeSavings

Rate

Deduction Each

$10,000 of Portfolio

50 $20,000 15.0% 1.87%50 $40,000 22.0% 0.97%50 $60,000 26.2% 0.64%50 $80,000 29.8% 0.48%50 $100,000 32.2% 0.39%50 $120,000 35.0% 0.33%55 $20,000 18.6% 2.11%55 $40,000 27.2% 1.04%55 $60,000 32.6% 0.71%55 $80,000 36.6% 0.53%55 $100,000 40.2% 0.43%55 $120,000 43.6% 0.36%60 $20,000 23.8% 2.39%60 $40,000 34.4% 1.23%60 $60,000 41.2% 0.81%60 $80,000 46.8% 0.61%60 $100,000 51.4% 0.50%60 $120,000 55.4% 0.41%

11

Projected Accumulated Wealth by Current Age forVarious Income Levels at 80% Net Income Replacement

Panel A: 50% Probability

AgeIncome$20,000

Income$40,000

Income$60,000

Income$80,000

Income$100,000

Income$120,000

35 $0 $0 $0 $0 $0 $0

40 $9,811 $27,836 $49,969 $74,839 $100,394 $131,425

45 $22,290 $63,243 $113,526 $170,029 $228,088 $298,588

50 $39,117 $110,984 $199,226 $289,384 $400,271 $523,991

55 $59,408 $168,553 $302,567 $453,160 $607,898 $795,793

60 $85,394 $242,282 $434,916 $651,381 $873,804 $1,143,889

65 $118,414 $335,965 $603,084 $903,249 $1,211,675 $1,586,193

Panel B: 90% Probability

AgeIncome$20,000

Income$40,000

Income$60,000

Income$80,000

Income$100,000

Income$120,000

35 $0 $0 $0 $0 $0 $0

40 $6,702 $21,824 $39,176 $58,674 $78,710 $103,038

45 $16,005 $45,408 $81,512 $122,082 $163,768 $214,387

50 $26,023 $73,831 $132,533 $198,497 $266,277 $348,581

55 $37,434 $106,207 $190,650 $285,540 $383,042 $501,436

60 $51,562 $146,292 $262,607 $393,310 $527,612 $690,691

65 $68,650 $194,775 $349,637 $523,658 $702,467 $919,594

Income is gross income. Savings start at age 35.

12

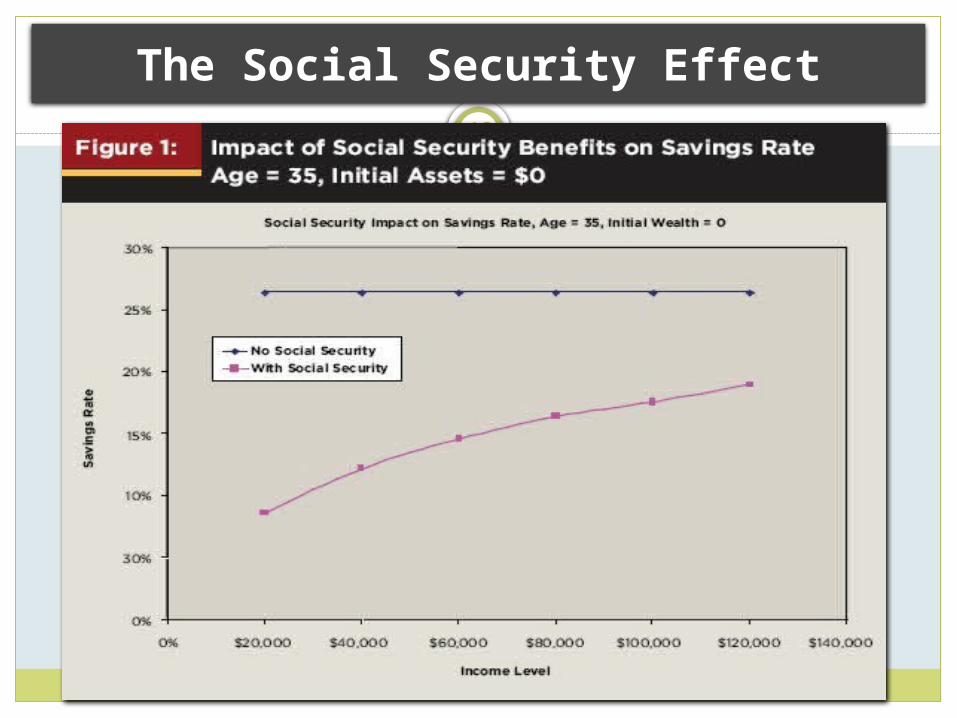

The Social Security Effect

13

Stocks and Bonds Allocations Across Target Maturity Funds

ProviderYears

to Retire

35 30 25 20 15 10 5 0

Provider A

Stock 90% 86% 82% 76% 70% 55% 45% 45%

Bond 10% 14% 18% 24% 30% 45% 55% 55%Provider

BStock 100% 93% 93% 88% 80% 75% 68% 60%

Bond 0% 7% 7% 12% 20% 25% 33% 50%Provider

CStock 84% 78% 69% 59% 54% 49% 40% 33%

Bond 17% 22% 32% 41% 46% 52% 60% 68%

Average Stock 86% 86% 81% 74% 68% 60% 51% 46%

Bond 14% 14% 19% 26% 32% 41% 49% 54%

Allocations obtained from the prospectus of each fund in Aug 2005.

14

15

Summary Checklist 1

Saving for retirement is possible with reasonable savings rates

Starting early is important so you can save without a significant drop in lifestyle

Critical inflection point at age 35 to 40

Creates benchmarks for amount needed for retirement based on income and age

Shows targets for how much an individual should have accumulated at age 65 prior to retiring (SS FRA > 65)

16

Summary Checklist 2

Calculated on retirement income as a percent of net pre-retirement income

Calculates cash flow using an 80 percent replacement ratio of pre-tax pre-retirement net income for a single person

Shows the difference in savings required for 60 and 80 percent replacement ratios with out the pre-retirement net income approach

Takes into account Social Security benefits

17

Summary Checklist 3

Shows how higher-income individuals need to save at a substantially higher rate as Social Security benefits are skewed to lower-income individuals

Starting your savings after 35 to 40 increases the challenge of an increasingly higher savings rate needed to accumulate sufficient capital

Those whose income increases faster than inflation will have to save an increasing amount to “catch up” so as to be able to provide for the higher assumed standard of living in retirement

18

Additional Variables

How long will you live? Longer = more $ Planning for a Secure Retirement http://www.ces.purdue.edu/retirement/ Module 1B- links to longevity estimators

Does not “cover” Long term care expensesHealth care expenses will likely be MUCH

higher than during working yearsMedicare funding is in trouble

19

Health Care Costs in Retirement2009 Retirement Confidence Survey

Retirees report health care costs at least as much, if not more, than expected

40% of retirees have spent more on health care than they expected

20

Health Care $ needed in Retirement

EBRI research $ needed to cover health insurance to

supplement Medicare & out-of-pocket health care expenses

a women retiring at age 65 in 2009 will need $98,000–$242,000 for a 50% of having enough

money $164,000–$450,000 for a 90% chance

21

NATIONAL SAVINGS RATE GUIDELINES FOR INDIVIDUALS

What questions do you have?

http://spwfe.fpanet.org:10005/public/Unclassified%20Records/FPA%20Journal%20April%202007%20-%20National%20Savings%20Rate%20Guidelines%20for%20Individuals.pdf

22

FPW Survey & Nov. 11 Program

Email survey of FPW participants coming soon

Nov. 11: All about IRAs and why switch to a Roth

December: No programReminder: check the FPW website

www.usu.edu/fpwPPTs posted on the web