auto injury claims the what, why and how of it all richard a. derrig opal consulting llc adam...

TRANSCRIPT

AGENDA

WHAT: The characteristics of current day

Auto Injury Coverges,1st and 3rd Party

Why: The Determinants of a Total

Compensation Settlement

How: The Negotiation System to Settle

3rd Party Injury Claims

Bodily Injury Claims per 100 Accidents

0%

10%

20%

30%40%

50%

60%

70%

80%

Fre

q R

atio

CA

MA

MI

NY

CW

Auto Injury Issues

• IRC Studies (1977+, latest 2002 CY)

• AIB Studies (1986+, latest 1996 AY)

• Medicals Dominate

• Injury & Treatment Types

• General Damages (Pain & Suffering)

• Claim Investigation

• Suspicion of Fraud and Build-Up

WHY

• Special (Claimed) and General Damages

• Economic and Non-Economic Damages

• Circumstances of The Claim

• Attorneys

• Fraud and Build-Up

BI Settlement Issues

• Investigation

• Suspicion of Fraud and Build-up

• Settlement Negotiation

• Low Impact Collision

• Passengers

• Bad Faith

• Evolution Over Time

Injury Type Changes

Inj 89 96

Fracture 14% 5%

Inpatient 7% 4%

Serious Visible 14% 2%

Prior Inj. 6% 27%

Source: AIB Final Report (2003)

Total Claimed Medical Charges by Type of Service

1996 BI Claims

Other1%

ER 10%

Inpatient17%

Ambulance2%

Outpatient70%

MO & MI 22%

PT & PO 14%

MD only 11%

CH & CO 23%

General Damages

• Special Damages are Claimant Economic Losses– Medical Bills– Wage Loss– Other Economic

• General Damages are Residual of Negotiated Settlement Less Specials– “Three Times Specials” is a Myth

Figure 8-31996 Settlement/Specials Ratio Distribution

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

0 to 0.5 0.5 to 1 1 to 1.5 1.5 to 2 2 to 2.5 2.5 to 3 3 to 3.5 3.5 to 4 4 to 4.5 4.5 to 5 5 to 5.5 5.5 to 6 6 to 6.5 6.5 to 7 7 to 7.5 7.5 to 8 8 to 8.5 8.5 to 9 9 to 9.5 9.5 to 10 10 to 20 20 to 30

Settlement/Specials Ratio

% o

f C

laim

s

Settlement Modeling

• Major Claim Characteristics

• Tobit Regression for Censored Data

(right censored for policy limits)

• Evaluation Model for Objective “Facts”

• Negotiation Model for all Other “Facts”, including suspicion of fraud or build-up

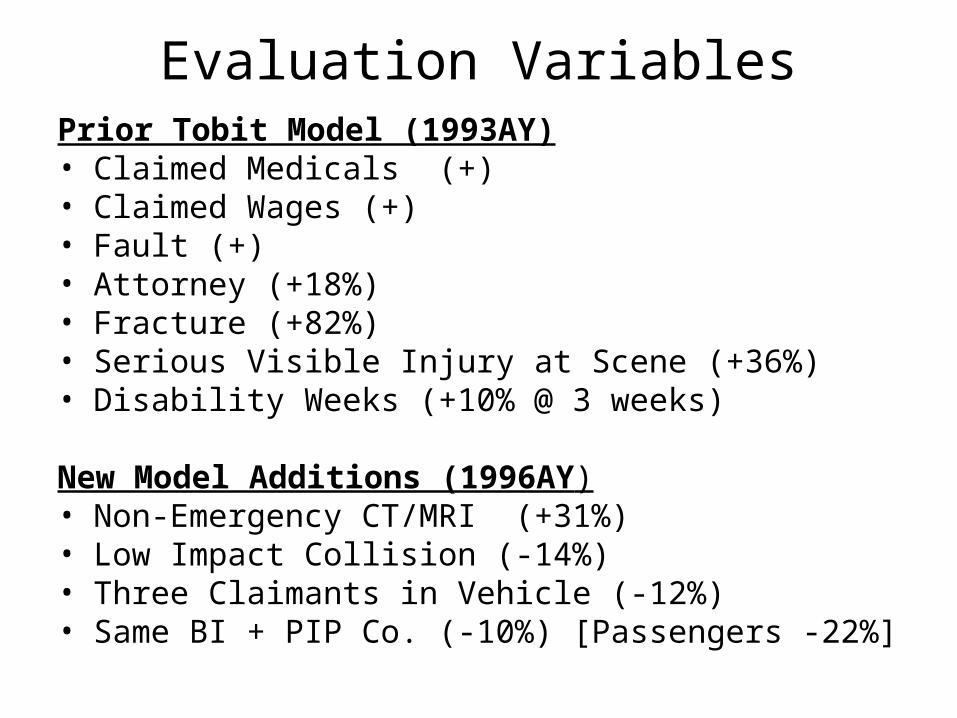

Evaluation VariablesPrior Tobit Model (1993AY)• Claimed Medicals (+)• Claimed Wages (+)• Fault (+)• Attorney (+18%)• Fracture (+82%)• Serious Visible Injury at Scene (+36%)• Disability Weeks (+10% @ 3 weeks)

New Model Additions (1996AY)• Non-Emergency CT/MRI (+31%)• Low Impact Collision (-14%)• Three Claimants in Vehicle (-12%)• Same BI + PIP Co. (-10%) [Passengers -22%]

Negotiation VariablesNew Model Additions (1996AY)

• Atty (1st) Demand Ratio to Specials (+8% @ 6 X Specials)• BI IME No Show (-30%) • BI IME Positive Outcome (-15%)• BI IME Not Requested (-14%)• BI Ten Point Suspicion Score (-12% @ 5.0 Average)• [1993 Build-up Variable (-10%)]• Unknown Disability (+53%)• [93A (Bad Faith) Letter Not Significant]• [In Suit Not Significant]• [SIU Referral (-6%) but Not Significant]• [EUO Not Significant]

Note: PIP IME No Show also significantly reduces BI + PIP by discouraging BI claim altogether (-3%).

Total Value of Negotiation Variables

Total Compensation Variables Avg. Claim/Factor

Evaluation Variables $13,948

Disability Unknown 1.05

1st Demand Ratio 1.09

BI IME No Show 0.99

BI IME Not Requested 0.90

BI IME Performed with Positive Outcome 0.97

Suspicion 0.87

Negotiation Variables 0.87

Total Compensation Model Payment $12,058

Actual Total Compensation $11,863

Actual BI Payment $8,551

HOW

• Negotiation is the Principal Method of Settling Liability Claims

• No Real Studies of How the Process Works

• Bargaining Models (Nash) may be too Complex for Simple Case – One issue $$.

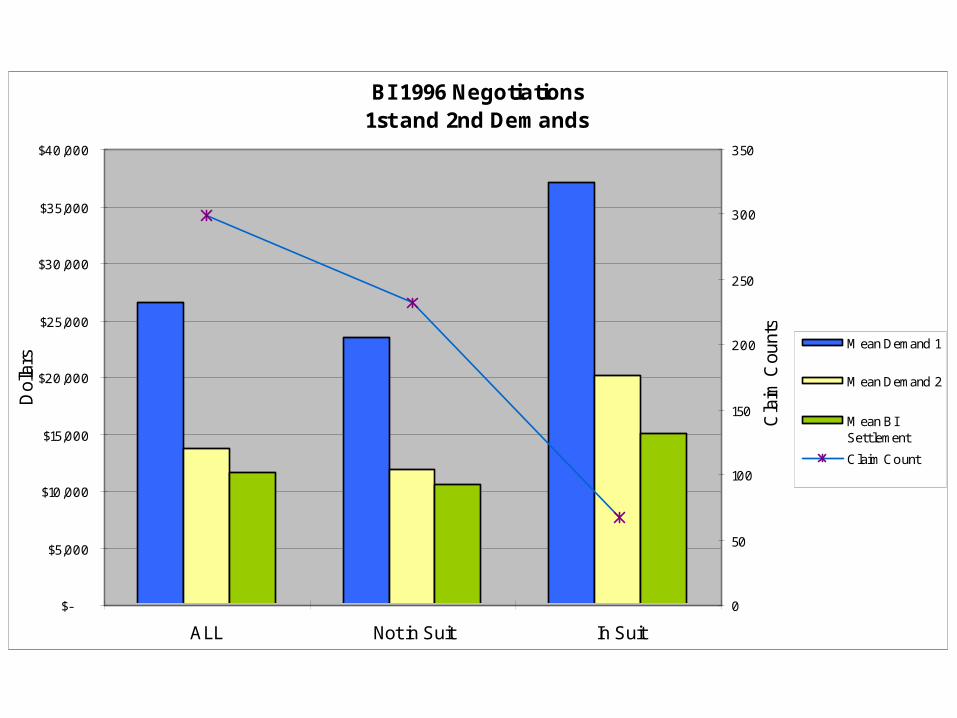

BI 1996 Negotiations1st and 2nd Demands

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

ALL Not in Suit In Suit

Dol

lars

0

50

100

150

200

250

300

350

Cla

im C

ount

s

Mean Demand 1

Mean Demand 2

Mean BISettlement

Claim Count

CSE: First & Second Demand Ratio to BI Settlement Ratio

Limited to 2nd Demand > $0, (315 BI Claims)NO PIP payment in Demand & Settlement, Outlier removed 3860

y = 1.4088x + 0.3452

R2 = 0.5691

y = 2.6414x + 1.4777

R2 = 0.1953

0

2

4

6

8

10

12

14

16

18

20

0 2 4 6 8 10 12 14 16 18 20

BI Settlement Ratio

Fir

st &

Sec

on

d D

eman

d R

atio

First Demand

Second Demand

2nd Demand Ratio

1st Demand Ratio

BI Settlement Ratio 1:1

BI Negotiation Leverage Points

Adjuster Advantages

Adjuster has ability to go to trial

Company has the settlement funds

Attorney, provider, or claimant needs money

Adjuster knows history of prior settlements

Adjuster can delay settlement by investigation

Settlement authorization process in company

Initial Determination of Liability

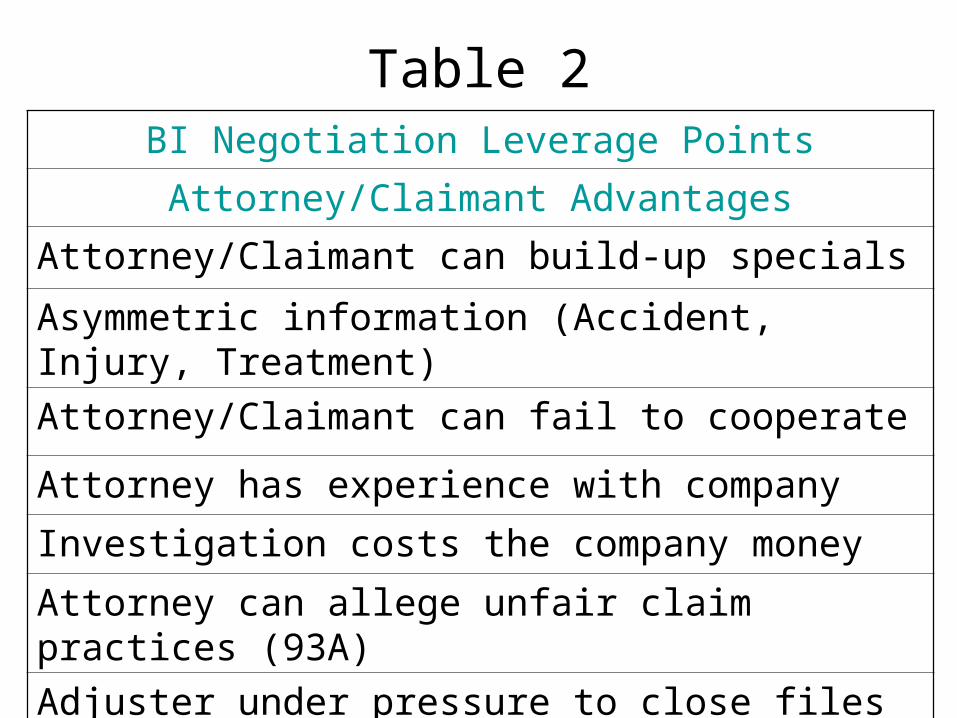

Table 1

BI Negotiation Leverage Points

Attorney/Claimant Advantages

Attorney/Claimant can build-up specials

Asymmetric information (Accident, Injury, Treatment)

Attorney/Claimant can fail to cooperate

Attorney has experience with company

Investigation costs the company money

Attorney can allege unfair claim practices (93A)

Adjuster under pressure to close files

Table 2

Negotiated Settlements

• Specials may be Discounted or Ignored

• Medicals: Real or Built-up?

• Information from Investigation

• Independent Medical Exams (IMEs)

• Special Investigation (SIU)

• Suspicion of Fraud or Build-up

Settlement Ratios by Injury and Suspicion

Variable PIP Suspicion Score = Low (0-3)

PIP Suspicion Score = Mod to High (4-10)

PIP Suspicion Score = All

1996 (N-336) 1996 (N-216) 1996 (N-552)

Str/SP All Other Str/SP All Other Str/SP All Other

Settlement Settlement Settlement

81% 19% 94% 6% 86% 14%

Avg. Settlement/Specials Ratio

3.01 3.81 2.58 3.61 2.82 3.77

Median Settlement/Specials Ratio

2.69 2.89 2.40 2.57 2.55 2.89

HELP

• Anyone willing to study negotiation cooperatively can contribute confidential access to BI claim files.

• Text miners are standing by willing to extract non-identified data relevant to negotiations

• Experts are standing by to analyze the patterns in the data.

References• Derrig, R.A. [2004],The Settlement Negotiation Process for Automobile Bodily

Injury Liability Claims in the Presence of Suspicion of Fraud and Build-Up, Risk Theory Society, NY.

• Derrig, R.A. and H.I. Weisberg, [2004], Determinants of Total Compensation for Auto Bodily Injury Liability Under No-Fault: Investigation, Negotiation and the Suspicion of Fraud, Insurance and Risk Management, v 71 (4), pp.663-662.

• Derrig, R.A., H.I. Weisberg and Xiu Chen, [1994], Behavioral Factors and Lotteries Under No-Fault with a Monetary Threshold: A Study of Massachusetts Automobile Claims, Journal of Risk and Insurance, 61:2, 245-275.

• Ross, Lawrence H. [1980], Settled out of Court, (Chicago, III: Aldine).• Insurance Research Council [2004], Fraud and Build-Up in Auto Injury Claims.

Malvern, PA• Insurance Research Council [ 2003], Auto Injury Insurance Claims. Countrywide

Patterns in Treatment, Cost, and Compensation, Malvern PA• Abrahamse, A. and Stephen J. Carroll [1999], The Frequency of Excess Claims for

Automobile Personal Injuries, Automobile Insurance: Road Safety, New Drivers, Risks, Insurance Fraud and Regulation, Claire Laberge-Nadeau, and Georges Dionne, Eds., Kluwer Academic Publishers, 131-151.