audit of key financial processes at the western quebec ... · pdf fileaudit of key financial...

TRANSCRIPT

AUDIT OF KEY FINANCIAL PROCESSES AT THE WESTERN QUEBEC FIELD UNIT

FINAL REPORT

Prepared By: Spearhead Management Canada Ltd.

January 2007

Report tabled and approved by the A&E Committee

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

©Her Majesty the Queen in Right of Canada, represented by

the Chief Executive Officer of Parks Canada, 2007

Cagalogue No. : R60-3/2-17-2007

ISBN : 978-0-662-69895-1

PARG 2 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

TABLE OF CONTENTS

SUMMARY ...............................................................................................................................4 1 OVERVIEW.......................................................................................................................8

BACKGROUND ..............................................................................................................................8

OBJECTIVES AND SCOPE............................................................................................................8

METHODOLOGY ...........................................................................................................................9

ASSURANCE STATEMENT........................................................................................................10

CONCLUSION...............................................................................................................................10

2 OBSERVATIONS AND RECOMMENDATIONS ......................................................10 2.1 MANAGEMENT CONTROL FRAMEWORK ..................................................................10

2.2 PAYMENTS TO SUPPLIERS ............................................................................................13

2.3 ACQUISITION CARDS......................................................................................................16

2.4 TRAVEL EXPENSES .........................................................................................................17

2.5 CONTRACTING ................................................................................................................20

2.6 REVENUES.........................................................................................................................22

2.7 FINANCIAL CODING........................................................................................................28

2.8 INVENTORIES ...................................................................................................................29

Report tabled and approved at the A&E Committee meeting on May 28, 2007

PARG 3 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

SUMMARY

BACKGROUND The Parks Canada Agency (PCA) is currently conducting a series of cyclical audits of the key financial, administrative and management practices in the field units, service centres and the National office. The audits are based on compliance with the policies and practices of the Treasury Board Secretariat (TBS) and the PCA. The audit of the Western Quebec Field Unit (WQFU) was conducted as part of this cyclical audit program.

OBJECTIVES AND SCOPE The objectives of this audit were to ensure that due diligence is being exercised in the key administrative processes at the Western Quebec Field Unit and that the control processes in place are satisfactory and comply with TBS and PCA policies and practices. The exercise included a review of the management control framework (MCF) for financial management as well as the following main financial areas: revenues, contracting, the use of acquisition cards, payments to suppliers, travel expenses, financial coding, inventories and attractive low-dollar items. The audit covered the period from April 1 to September 30, 2006, with visits to the Carillon Canal and Fort Chambly.

METHOD The audit method consisted of a review of relevant vouchers, interviews with WQFU staff members and transaction controls in the main financial areas. Visits were made to the WQFU sites from October 16 to 27, 2006.

ASSURANCE STATEMENT In our view, the audit work carried out and the evidence collected were sufficient to support the conclusions formulated in this report.

CONCLUSION We determined that the WQFU had demonstrated due diligence in applying the management policies for acquisition cards, contracting, payments to suppliers, financial coding, control over its vehicles and in collecting revenue generated by the historic canals and sites. On the other hand, the WQFU needs to strengthen or introduce management processes and procedures to ensure that reliable budget reports are prepared and monitored, to carry out its strategy to maximize, control and collect revenue generated by leases and permits, to follow rules governing travel expenses, to control attractive items and items valued between $1,000 and $10,000, and to ensure the reliability and consistency of information contained in the SAP1 and AMS inventory systems for goods valued $10,000 and over. 1 The names SAP and STAR are used equally in this report to designate the financial system.

PARG 4 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

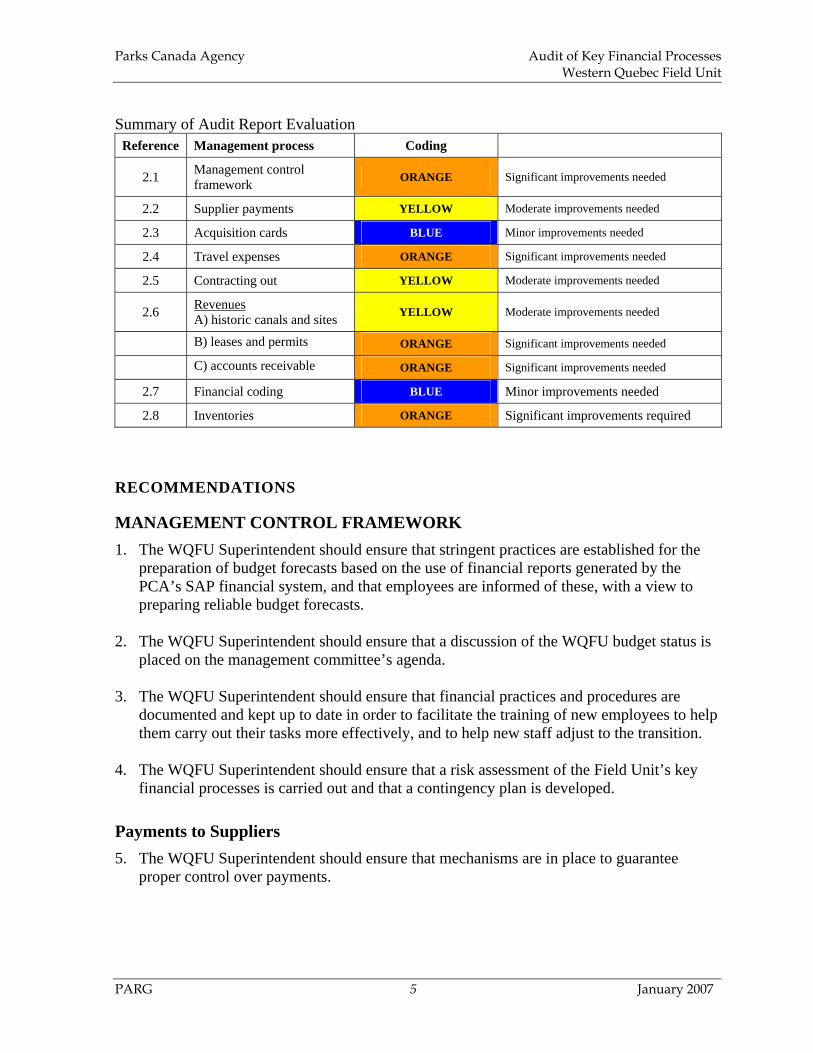

Summary of Audit Report Evaluation Reference Management process Coding

2.1 Management control framework ORANGE Significant improvements needed

2.2 Supplier payments YELLOW Moderate improvements needed

2.3 Acquisition cards BLUE Minor improvements needed

2.4 Travel expenses ORANGE Significant improvements needed

2.5 Contracting out YELLOW Moderate improvements needed

2.6 Revenues A) historic canals and sites YELLOW Moderate improvements needed

B) leases and permits ORANGE Significant improvements needed C) accounts receivable ORANGE Significant improvements needed

2.7 Financial coding BLUE Minor improvements needed

2.8 Inventories ORANGE Significant improvements required

RECOMMENDATIONS

MANAGEMENT CONTROL FRAMEWORK 1. The WQFU Superintendent should ensure that stringent practices are established for the

preparation of budget forecasts based on the use of financial reports generated by the PCA’s SAP financial system, and that employees are informed of these, with a view to preparing reliable budget forecasts.

2. The WQFU Superintendent should ensure that a discussion of the WQFU budget status is

placed on the management committee’s agenda. 3. The WQFU Superintendent should ensure that financial practices and procedures are

documented and kept up to date in order to facilitate the training of new employees to help them carry out their tasks more effectively, and to help new staff adjust to the transition.

4. The WQFU Superintendent should ensure that a risk assessment of the Field Unit’s key

financial processes is carried out and that a contingency plan is developed.

Payments to Suppliers 5. The WQFU Superintendent should ensure that mechanisms are in place to guarantee

proper control over payments.

PARG 5 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

6. The WQFU Superintendent should ensure that the person who certifies payment requisitions under section 33 of the FAA signs the report of authorized payments or initials the section 33 seal stamped on every invoice paid.

7. The WQFU Superintendent should ensure that signing authorities for administration and

finance are updated to reflect the new organizational structure of the WQFU and the delegated authorities.

8. The WQFU Superintendent should ensure that the segregation of financial and

administrative duties is clearly defined and is consistent with PCA practices and policies. 9. The WQFU Superintendent should ensure that expenditures for hospitality are supported

by an authorization form and a list of participants as required by the PCA Hospitality Policy.

Acquisition Cards 10. The WQFU Superintendent should ensure that steps are taken to check that no accounts

are paid twice. 11. The WQFU Superintendent should review the need for petty cash and the amounts

involved because many of the petty cash holders also have an acquisition card.

Travel Expenses

12. The WQFU Superintendent should ensure that an internal procedure for processing travel expenses is updated.

13. The WQFU Superintendent should implement measures to ensure that: • travel is authorized in advance by the appropriate authority, as stated in section 34

of the FAA

• the place of work is defined in order to provide better control over expenses

• travel claims include all required supporting documents. (for example, receipts for all lunches claimed at the workplace and boarding passes)

14. The WQFU Superintendent should try to evaluate and incorporate certain costs related to

travel expenses into the strategic planning so that they can be identified ahead of time to optimize expenditure control.

15. The WQFU Superintendent should ensure that appropriate verifications are made before

payment is authorized.

PARG 6 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Contracting 16. The WQFU Superintendent should arrange for training on contracting and purchase

orders for all WQFU managers and appropriate administrative staff, in order to improve compliance with the regulations governing these processes.

17. The WQFU Superintendent should ensure that all supporting documentation required for

contracting are obtained and kept in the central file by the officer responsible for contracting and asset management.

18. The WQFU Superintendent should ensure that contracts with “Friends of” the WQFU

comply with the management guidelines for cooperating associations.

Revenues 19. The WQFU Superintendent should look into the possibility of a separate cash drawer for

each employee. 20. The WQFU Superintendent should finalize the strategy for maximizing revenue

generated by leases and permits, and establish a reasonable schedule for its implementation.

21. The WQFU Superintendent should work with those in charge of the SAP system in order

to be able to issue and control accounts receivable through the system. 22. The WQFU Superintendent should determine whether manual invoices in the accounts

receivable binder and invoices not paid in the SAP system still represent valid accounts receivable, and make the accounting adjustments required to update the accounts receivable in this system.

Inventories 23. The WQFU Superintendent should establish a strategy for maintaining and updating

inventories of items worth over $10,000 in the SAP system. 24. The WQFU Superintendent should ensure that the AMS accurately represents the assets

under her responsibility. 25. As a best practice, the WQFU Superintendent should consider updating the inventory of

high-risk valuable small items in order to include this information in the database when the new system becomes operational.

PARG 7 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

OVERVIEW

CONTEXT The Parks Canada Agency (PCA) is conducting a series of cyclical audits of key financial, administrative and management practices for all field units, service centres and the national office. The Agency has 32 field units and four service centres. Field units are groupings of national parks, national historic sites and national marine conservation areas that are usually in proximity to one another. This proximity allows them to share management and administrative resources. The field units provide the PCA with support in various professional and technical areas. The service centre directors and field unit superintendents must ensure that TBS and PCA policies and guidelines are observed.

On behalf of the Performance, Evaluation and Audit Group, Spearhead Management Canada Ltd., as part of this program of cyclical audits, conducted an audit at the offices of the Western Quebec Field Unit (WQFU) in Chambly. The WQFU is responsible for 17 historic sites, including five national historic canals in Quebec. It manages assets whose replacement cost is valued at $823 million. The WQFU also has some responsibilities with respect to management of the national historic sites commemoration program, which has over 181 designations, including 82 sites, thus representing 10% of all designations in Canada. The 17 sites are spread over an area of 110,000 km² and attract over 1.4 million visitors each year. The WQFU has an A-Base budget of $9.3 million for operations and expenditures. Its revenue objectives are $739,000 per year. The WQFU staff in terms of full-time equivalents represents 140 positions. The 240 employees of the WQFU are either indeterminate (20%), seasonal (20%), term (20%) or students (31%).

OBJECTIVES AND SCOPE The audit objectives were to ensure that due diligence is being carried out in the key administrative processes of the Western Quebec Field Unit and that the processes and controls in place are satisfactory and consistent with TBS and PCA policies and practices. The exercise therefore included a review of the management control framework (MCF) and of the following key financial areas:

♦ revenues

♦ contracting

♦ use of acquisition cards

♦ payments to suppliers

♦ travel expenses

PARG 8 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

♦ financial coding

♦ inventories The audit of transactions covered the period from April 1 to September 30, 2006.

METHODOLOGY The methodology consisted of a visit to the WQFU, a visit to the Fort Chambly National Historic Site, a visit to the Carillon Canal and the following procedures:

♦ a review of relevant documents: the 2003-08 WQFU business plan, the organization chart, PCA financial resources management principles, the list of delegated PCA signing authorities, TBS and PCA policies on the key financial areas mentioned above and the financial reports prepared by the WQFU finance and administration manager

♦ interviews with members of management and staff responsible for key financial processes at the WQFU

♦ an analysis of the processes and procedures used for financial management of activities related to the financial areas covered by the audit

♦ a review of the sample of transactions in each financial area (this was not a scientific sampling)

Once the audit work was completed, a meeting was held to present and discuss any deficiencies observed in the course of the audit and the expected recommendations. The Field Unit Superintendent and the finance and administration officer attended this meeting.

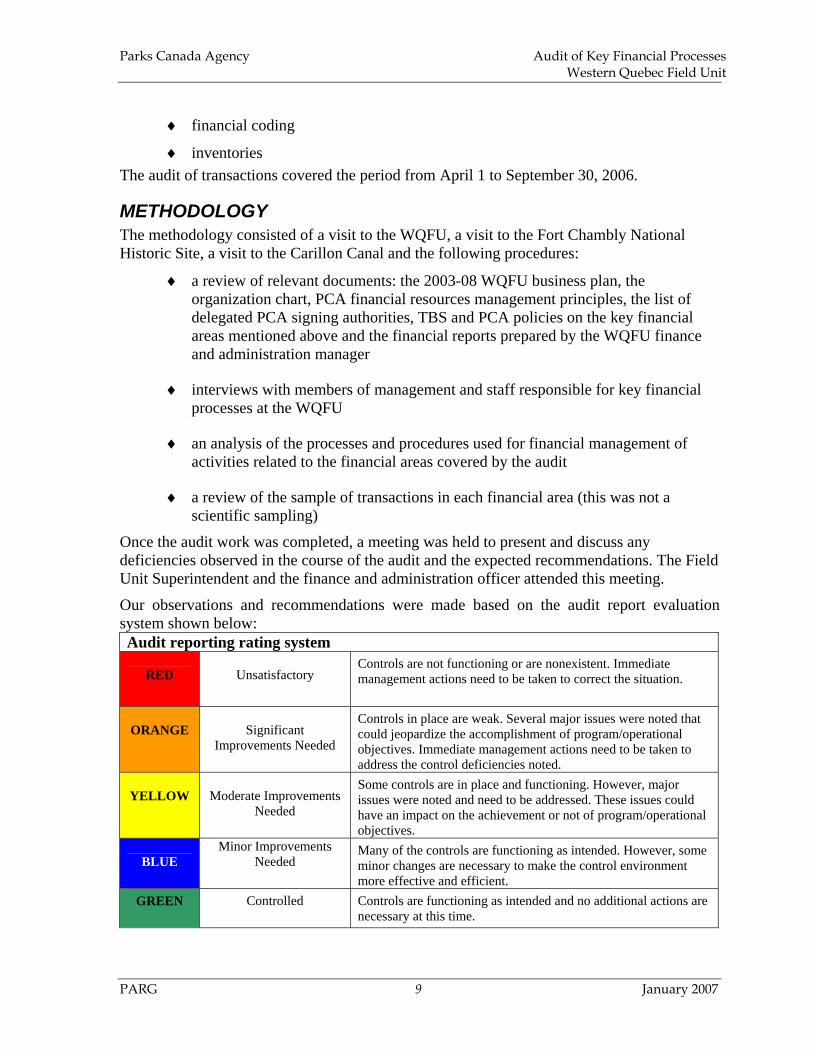

Our observations and recommendations were made based on the audit report evaluation system shown below: Audit reporting rating system

RED

Unsatisfactory

Controls are not functioning or are nonexistent. Immediate management actions need to be taken to correct the situation.

ORANGE

Significant

Improvements Needed

Controls in place are weak. Several major issues were noted that could jeopardize the accomplishment of program/operational objectives. Immediate management actions need to be taken to address the control deficiencies noted.

YELLOW

Moderate Improvements

Needed

Some controls are in place and functioning. However, major issues were noted and need to be addressed. These issues could have an impact on the achievement or not of program/operational objectives.

BLUE

Minor Improvements Needed

Many of the controls are functioning as intended. However, some minor changes are necessary to make the control environment more effective and efficient.

GREEN Controlled

Controls are functioning as intended and no additional actions are necessary at this time.

PARG 9 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

ASSURANCE STATEMENT In our opinion, sufficient audit work has been performed and the necessary evidence has been gathered to support the conclusions contained in this report.

CONCLUSION We found that due diligence is being exercised by the WQFU with respect to the management processes for acquisition cards, contracting, payments to suppliers, financial coding, control over its vehicles and in the collection of revenue generated by the historic canals and sites. However, the WQFU needs to strengthen or implement management processes and procedures to properly monitor and control the preparation of reliable budget reports, to properly implement its strategy to maximize, control and collect revenue generated by leases and permits, to observe the rules governing travel expenses, to control attractive items and those valued between $1,000 and $10,000, and to ensure the reliability and consistency of information contained in the SAP and AMS inventory systems for assets worth $10,000 or more. We will present our observations and recommendations in the next section, where applicable, concerning the MCF that governs financial management and the main financial areas reviewed.

OBSERVATIONS AND RECOMMENDATIONS

2.1 MANAGEMENT CONTROL FRAMEWORK

ORANGE

Significant Improvements Needed

Controls in place are weak. Several major issues were noted that could jeopardize the accomplishment of program/operational objectives. Immediate management actions need to be taken to address the control deficiencies noted.

Current Practices and Observations

Planning and Budgeting

There is a process for preparing and updating the 5-year sustainable business plan (2003-08). All of the managers and the finance and administration officer (FAO) contribute to the development of the WQFU objectives and ensure that they are consistent with the national PCA objectives. The management committee, which consists of the director and main managers, meets regularly, and the minutes are made available to employees on the Intranet. On the other hand, the fact that the 17 historic sites and canals are scattered over such an immense area rarely enables all the managers to meet. The work sessions are therefore generally held at the WQFU office and the minutes for the topics discussed are prepared and kept by the director’s administrative assistant. The planning also requires preparing 17 corporate plans, which represent more than one quarter of the 50 corporate plans prepared

PARG 10 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

for the whole of the PCA. Each corporate plan identifies the issues, priority management measures and the implementation costs for each of these measures. All of this planning can be found in the business plan, and it is used in preparing the budget forecasts. The WQFU budget for 2006-07 consists of the following, broken down into 84 cost centres: Goods and services $6,410,070

Salaries and wages $6,549,950 Advertising $5,000 Park contributions $8,150

Total $12,973,170

Observations Managers received a budget report from the SAP financial system in August, but not all of them submitted the budget forecasts requested. Another budget report was prepared in October and the FU Superintendent and the FAO had begun to hold meetings with the managers to prepare reliable budget forecasts. Currently, the managers rely more on a parallel system (i.e. Excel files) and not the reports from the SAP financial system, to monitor their budgets. There is a lack of confidence in the usefulness and reliability of the reports generated by the SAP system and the earlier budget forecasts. For 2005-06, the WQFU projected a deficit of approximately $300,000, but at the end of the year it had a surplus of over $300,000. The fact that the national review had not yet been completed on time explains much of this discrepancy. For this reason, the managers did not consider it useful to analyze any discrepancies so early in the year. The use of two separate systems creates information gaps and reduces the ability of the WQFU to forecast future expenditures properly. It also reduces the ability of management at the PCA to rely on information in the SAP system, because it does not accurately represent the financial position of the WQFU. The WQFU’s financial position appears to be shaky, because a negative discrepancy is expected by the FAO for 2006-07. This deficit would be largely attributable to the cost of reclassifying employees, to increases in the cost of materials and services to maintain the WQFU assets. Efforts are needed to train and convince managers to work with the SAP financial system reports. Without this coordination, the ability of the WQFU to generate reliable budget reports that are useful to PCA national management is reduced.

Training The WQFU did not have a plan to provide financial management training to its managers. While they did take the F&A 101 course, they are not using the SAP system to track their budgets. As mentioned previously, they prefer to use a parallel system that they maintain independently of the SAP system. The managers would benefit from training to make them more familiar with contracting rules (see section 2.5). There is no training plan for finance employees. The longest-serving employees have not taken the course for many years and no courses were scheduled for the new employee hired in June 2006. Furthermore, there are few or no written procedures to facilitate the work of new employees. Each employee, working together with the supervisor, should identify his or her training requirements.

PARG 11 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Control and MonitoringFinance employees make sure that the payment requisition matches the amount on the invoice and check the validity of the financial coding. There is also some control over financial commitments for contracting and for purchase order purchases. Management committee meetings, work sessions and the preparation of management plans are also instruments that can monitor the objectives and budgets. On the other hand, the weaknesses identified in this report, such as the lack of control over inventories of high-risk small items worth between $1,000 and $10,000, over billing and collection of accounts receivable and /or the preparation of reliable budget forecasts reduce the ability of the WQFU to provide effective control and monitoring. Risk Management While the WQFU management plans identify risks in terms of program delivery and methods to mitigate them, there is no succession plan for key finance personnel. From June to September 2006, this section had a serious shortage of staff. The situation delayed the entry of revenues into the SAP financial system until September. In addition, assistance from the Cornwall Service Centre was necessary to pay invoices until the end of October 2006. Some employees have acquired a great deal of knowledge over the years, but there is little documentation to help in transmitting this knowledge to new employees. Nor has the WQFU assessed the risk involved in key financial processes, or developed a contingency plan. The latter would cover factors such as the temporary reorganization of offices, the identification of essential services to be maintained, damaged equipment replacement and the temporary relocation of employees under circumstances beyond the organization’s control.

Recommendations 1. The WQFU Superintendent should ensure that rigorous practices are established for

the preparation of budget forecasts based on the use of financial reports generated by the PCA’s SAP financial system, and that employees are informed of these, with a view to preparing reliable budget forecasts.

Management Response: Agree: The WQFU acknowledges the need to introduce such systems to

improve monitoring and controls. Over the past few years, Finance has undergone many staff changes that reduced its ability to develop systems and properly inform personnel. In addition, the volume of activity in the Field Unit places a great deal of pressure on current resources. Many changes that have also occurred on the management team has led to a greater emphasis on human resources at the expense of finance. A special effort will be made to develop and introduce systems over the next 18 months in order to have procedures and processes that are operational and up to date by early April 2009.

PARG 12 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

2. The WQFU Superintendent should ensure that a discussion of the WQFU budget status is placed on the management committee’s agenda.

Management Response:

Agree with reservation: We recognize that it is important to keep finances on the agenda at meetings. This item will be added for future meetings. However, a number of meetings, for example for work sessions, are to cover specific topics and do not necessarily need financial discussions.

3. The WQFU Superintendent should ensure that financial practices and procedures are documented and kept up to date in order to facilitate the training of new employees to help them carry out their tasks more effectively, and to help new staff adjust to the transition.

Management Response: Agree: Steps to do the above have already been taken. As indicated in the

response to recommendation #1, these practices and procedures will be developed within the next 18 months.

4. The WQFU Superintendent should ensure that a risk assessment of the Field Unit’s key financial processes is carried out and that a contingency plan is developed.

Management Response Agree: The Parks Canada national office will develop a policy and guidelines

for the identification of risks and prepare an activity resumption plan by June 2007. Once this national directive is released, over the following year the Field Unit will identify the major risks and a contingency plan for its financial and administrative systems.

2.2 PAYMENTS TO SUPPLIERS YELLOW

Moderate Improvements Needed

Some controls are in place and functioning. However, major issues were noted and need to be addressed. These issues could have an impact on the achievement or not of program/operational objectives.

Current Practices Owing to a shortage of personnel in finance at the WQFU, payments to suppliers were made by the Ontario Service Centre in Cornwall (CSC) from August 2006 to November 2006. The WQFU sent invoices to CSC for verification and payment authorization under section 33 of the Financial Administration Act (FAA). The invoices were then returned to the WQFU for filing. The staff shortage created delays in the payment of invoices, and the WQFU had to pay a total of $845.19 in interest during the period audited.

PARG 13 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

OBSERVATIONS We interviewed finance personnel and tested a sample of 19 supplier payment files totalling $237,181. Generally speaking, the files were readily acceptable, properly documented and the amounts correctly reported in the SAP financial system. However, we nevertheless found that:

• Payment of $25,435 for licence plates for WQFU vehicles was made based on a photocopy of the overall invoice. The list of licensed vehicles and the cost of the licence for each one, along with the original invoice, was found in the section responsible for vehicles.

• A payment of $162 was made to rent a photocopier, for which the accuracy of the amount could not be checked. Normally, a purchase order should be available, as well as a specific commitment for this purchase order in the SAP financial system. At the WQFU, however, specific commitments for photocopiers were replaced by blanket commitments to avoid the need to prepare goods receipt slips in the invoice payment system. This method weakens control over expenditures, particularly as the overall commitment is an approximation of the actual expenditure. Proceeding in this way involves a risk of overpayments or inaccurate payments.

• The staff responsible for checking and entering invoices into the SAP system sign under section 34 of the FAA for invoices related to fixed costs (hydro, telephone, mail, courier, etc.). This practice does not follow the segregation of duties principle, which makes it possible to control transactions properly.

• The person authorizing section 33 payment requisitions can also create and change supplier codes in the SAP system. This concentration of powers increases the risk of inappropriate transactions going unnoticed.

• Signing authorities are not up to date and the signature cards do not always clearly show the responsibility centre or centres for which the manager is authorized to sign. This makes it difficult to check the appropriate authorizations. In one instance, the manager signed under section 33 even though that person did not have the authority to do so.

Recommendations 5. The WQFU Superintendent should ensure that mechanisms are in place to guarantee

proper control over payments. Management Response Agree: We consider that the current controls are sufficient. The shifting of

payments to the Ontario Service Centre enabled the WQFU to continue operating. However, some irregularities affected the data processing during this period. The situation has returned to normal with the resumption of operations by the WQFU.

PARG 14 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

6. The WQFU Superintendent should ensure that the person who certifies payment requisitions under section 33 of the FAA signs the report of authorized payments or initials the section 33 seal stamped on every invoice paid.

Management Response Agree: The audit procedures are now carried out before payment from the

beginning of the new fiscal year. The originals of invoices will now be sent to Finance.

7. The WQFU Superintendent should ensure that signing authorities for administration

and finance are updated to reflect the new organizational structure of the WQFU and the delegated authorities.

Management Response Agree: All signature cards will be updated by June 2007. This takes into

account the fact that a management change at the Field Unit is expected.

8. The WQFU Superintendent should ensure that the segregation of financial and

administration tasks is clearly defined and is consistent with PCA practices and policies.

Management Response Agree: The situation has been corrected. From now on, managers must

authorize expenditures related to their cost centre.

Hospitality Charges YELLOW

Moderate Improvements Needed

Some controls are in place and functioning. However, major issues were noted and need to be addressed. These issues could have an impact on the achievement or not of program/operational objectives.

Current Practices At the start of the year, the Field Unit establishes a plan for the various hospitality activities planned for the current year. This plan is subdivided by cost centre and provides a description of the planned activities such as meetings with various stakeholders; acknowledgement of volunteers; 26th edition of the Village Festival; and meetings with participants at public consultations. In all, the WQFU expected to spend $5,825 in hospitality charges for 2006-07.

OBSERVATIONS While auditing travel expenses, we found that the hospitality charges were not supported by an authorization form or a list of participants, as prescribed by the PCA Hospitality Policy. This makes it impossible to audit the approvals. Recommendation

9. The WQFU Superintendent should ensure that expenditures for hospitality are supported by an authorization form and a list of participants, as required by the PCA Hospitality Policy.

PARG 15 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Management Response Agree: All managers will be reminded so that the practice is strengthened.

Information will be disseminated at the management meeting scheduled for April 2007.

2.3 ACQUISITION CARDS BLUE

Minor Improvements Needed

Many of the controls are functioning as intended. However, some minor changes are necessary to make the control environment more effective and efficient.

Current Practices The F&A Officer is responsible for issuing, cancelling and controlling acquisition cards (AC). All cardholders must sign a statement promising to comply with the responsibilities and obligations involved in using the cards. On the audit date, 66 WQFU employees had an acquisition card. During the audit period, the value of purchases made using the cards totalled $148,459.

Observations We carefully examined $4,093 in purchases made by 9 randomly selected cardholders. We also checked 10 cancelled accounts to ensure that they were indeed inactive. Generally speaking, the use of acquisition cards followed the policies and guidelines. However, we found one account that had been paid once by the WQFU and a second time by the Cornwall Service Centre. There is the possibility that other expenditures were paid twice. It would be appropriate to examine more specifically the initial payment requisitions sent to the Cornwall Service Centre. Lastly, we compared the list of acquisition cardholders with the list of people who had petty cash for purchases and found that most of these people appeared on both lists. At least 12 people have petty cash of $300 or more, even when they have an acquisition card.

Recommendations 10. The WQFU Superintendent should ensure that steps are taken to check that no

accounts are paid twice. Management Response Agree: The verifications were carried out and no other duplications were made.

11. The WQFU Superintendent should review the need for petty cash and the amounts involved because many of the petty cash holders also have an acquisition card.

Management Response Agree: This will be analyzed over the next few weeks and action will be taken to

correct the situation where applicable.

PARG 16 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

2.4 Travel expenses ORANGE

Significant Improvements Needed

Controls in place are weak. Several major issues were noted that could jeopardize the accomplishment of program/operational objectives. Immediate management actions need to be taken to address the control deficiencies noted.

Current Practices

Travel expenses account for approximately 0.6% ($158,000) of the WQFU operating budget for the period covered. The internal procedures written for Finance and the work instructions describing the procedure to be followed by staff in processing travel expenses are not up to date. Such documents enhance understanding of Agency and Treasury Board rules and directives and ensure consistent processing of these expenses as well as facilitating the transition when there are personnel changes.

Each traveller is responsible for consulting the policies applicable to their situation, which are available on the Agency Intranet. However, the F&A Officer provides information to all staff by e-mail when there have been changes in the allowances. In terms of planning, travel expenses are not identified in the Field Unit operational plan. As the WQFU has 17 sites over a very large area, the amount allocated annually to travel expenses is high. Establishing strategic planning for recurring trips would give managers an overview of the upcoming travel expenses and, through prior commitment of these funds, would make it possible to better control the budgets. At the time of the audit, there was no list of travel cardholders available from the Field Unit. Prior to August 2006, the Quebec Service Centre was responsible for managing travel cards. Since the beginning of August, responsibility for managing travel cards has rested with the Field Unit. A coordinator should be identified and assigned the role as an advisor on the use of travel cards. This person should also be able to request additional cards. Travel advances are not used by the Field Unit except for employees who have a standing advance. Most employees who are required to travel frequently during working hours have been assigned continuing travel authority. This practice lightens the administrative burden by not requiring that a signature be obtained prior to the trip. However, restrictions apply and should be identified on this authority. These include:

- The region in which the employee is authorized to travel needs to be clearly entered on the form.

- These authorities need to be renewed every fiscal year. Complying with these travel authority obligations increases control and ensures that employees travelling are covered by insurance.

PARG 17 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

The place of work for WQFU employees was not clearly identified in writing as required in Appendix E of the Agency’s policy on travel expenses. Geographical location of the Field Unit is problematic in some instances, because many sites are grouped within a radius of less than 100 km. Designating the place of work would reduce the risk of claims that are too high and would allow for better control over costs. A designation of this kind would also have an impact on the application of the WQFU travel policy because section 3.1.9 of the policy clearly establishes the criteria that need to be followed in order to be able to claim meals within the headquarters area. Furthermore, travellers are required to provide vouchers when making a meal claim. The WQFU must of course reimburse the amount of the invoice up to the total amount authorized by Appendix C of the policy.

Observations To check the completeness of the documentation and compliance with the Parks Canada Agency policy on travel expenses, we based our sample on the transactions entered in the SAP financial system. In order to obtain a sample that was as representative as possible of Western Quebec Field Unit operations, we selected transactions from several cost centres. A total of 22 transactions entered between April 1, 2006 and September 30, 2006 and worth $10,547.31 were examined. We found that:

- 38% of transactions did not have a valid travel authority in accordance with the Agency’s policy. Furthermore, 8 cases had a blanket travel authorization but these authorizations did not clearly indicate the nature of the travel authorized.

- 41% of transactions did not have a valid section 34 authorization under the FAA.

Either the person who certified under section 34 did not have a signature card (6 cases) or the person had signed for a cost centre that was not under that person’s responsibility (3 cases).

- 22% of transactions were for meal claims for which there were no vouchers.

- There was nothing to show that the travel claims had been checked. The only sign of

this was a “STAR” stamp indicating that the information had been entered into the SAP system.

- Section 33 payment authority is given without checking the vouchers. The WQFU

uses statistical sampling to check the accuracy of the transactions. However, the January 2002 audit and sampling plan clearly stipulates that in addition to statistical sampling, the Field Unit is required to do a basic level of verification for low-risk expenses.

PARG 18 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

- Four transactions were coded under travel expenses but should have been under hospitality. There was no authorization form or list of participants for these expenses, which were placed under travel in the general ledger.

- One travel account included expenses for two separate fiscal years. - One transaction covered travel expenses for a person who is not an employee of the

Agency. The file did not contain a description or an explanation of the expenses, or a contract or invoice.

Recommendations 12. The WQFU Superintendent should ensure that an internal procedure for processing

travel costs is updated. Management Response Agree: This will be done by September 2007. 13. The WQFU Superintendent should introduce measures to ensure that:

• travel is authorized in advance by the appropriate authority, as required in section 34 of the FAA

• the place of work is defined in order to provide better control over expenditures

• travel claims include all required supporting documents. For example, receipts for

all lunches claimed at the workplace and boarding passes. Management Response Agree: An exercise will be carried out over the next few weeks to evaluate the

need for the annual travel authorities that are used. In addition, all managers will be reminded about signing procedures and supporting documentation. However, the definition of place of work needs to be clearly established and the size of the Field Unit makes this difficult. The place of work will be established, but advice will first be taken from the national office and other field units or service centres to ensure that the place of work or work area is established fairly and equitably.

14. The WQFU Superintendent should try to evaluate and incorporate certain costs

related to travel expenses into the strategic planning so that they can be identified ahead of time to optimize expenditure control.

PARG 19 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Management Response Disagree: Each manager prepares a travel plan in which travel expenses are

considered. These plans are integrated into the strategic planning to ensure control over recurring travel expenses for the Field Unit. Only activities with respect to all the national level training are not factored in, and would require a schedule in order to be able to incorporate them into the planning.

15. The WQFU Superintendent should ensure that appropriate verifications are made

before payment is authorized. Management Response Agree: A clarification of the roles and responsibilities of the various parties

will be completed by September 2007. Furthermore, a random check will be performed from now on prior to giving payment authorization.

2.5 CONTRACTING YELLOW

Moderate Improvements Needed

Some controls are in place and functioning. However, major issues were noted and need to be addressed. These issues could have an impact on the achievement or not of program/operational objectives.

Current Practices The WQFU awards contracts for goods and services using a variety of mechanisms, including service contracts, local purchase orders and acquisition cards (see section 2.3 of this report). During the audit period, from April 1 to September 30, 2006, the WQFU awarded 37 contracts worth a total of $1,167,368.68, and at the time of the audit, there were still 65 active contracts valued at $2,469,348.03. We selected 12 contracts representing 49% of the total value of active contracts for audit purposes. We also reviewed all of the procedures for contracting and the use of purchase orders with the officer in charge of contracting and asset management.

OBSERVATIONS We determined that managers had not received training on contracting, or documentation that would familiarize them with the rules and procedures governing contracting and the use of purchase orders. On the other hand, the officer who handles contracting is in regular contact with managers and informs them of the regulations and procedures to follow. The audit identified the following discrepancies:

The documents required for a ferry contract, such as evidence of insurance, ship compliance and captain credentials were not on file, but were obtained prior to the end of the audit.

PARG 20 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

The contracts for the “Friends” of the WQFU did not always follow the management guidelines of the Cooperating Associations Program, for the following reasons:

o A lack of evidence on file that the contracted association is a non-profit organization (NPO)

o One Friends group provides a variety of services, including $8,000 worth of

cleaning services. This amount is included in a $32,000 sole source contract. This maintenance service is not consistent with the spirit of the policy, which is rather to organize all kinds of activities, generally in connection with the PCA mandate, such as re-enactments in period costumes, making and selling products and the acquisition of materials for exhibits.

o The contracts with Friends do not require them to report on their financial

activities to receive a portion of the revenues they generate in contributing to the Parks Canada mandate, as mentioned in the management guidelines Management Guidelines for Cooperating Associations.

A contract for one group of Friends was not signed, even though the group had already provided services during the summer. Another Friends contract was signed by a manager who did not have the required authority to do so.

Purchases were made by means of purchase orders over the $5,000 limit.

There were purchases of $2,500 and over that had not obtained 3 estimates in order to get the lowest possible price.

Recommendations 16. The WQFU Superintendent should arrange for training on contracting and purchase

orders for all WQFU managers and appropriate administrative staff, in order to improve compliance with the regulations governing these processes.

Management Response Agree: Training will be provided during 2007-08 with a view to ensuring that

all personnel involved in these areas receive appropriate training. 17. The WQFU Superintendent should ensure that all supporting documentation required

for contracting is obtained and kept in the central file by the officer responsible for contracting and asset management.

Management Response Agree with reservation: The Field Unit has to deal with factors beyond its control to

obtain supporting documentation that goes through third parties. Monthly follow-ups will be introduced to improve the situation.

PARG 21 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

18. The WQFU Superintendent should ensure that contracts with WQFU “Friends” comply with the Management Guidelines for Cooperating Associations

Management Response Agree: Whenever the agreement is renewed, special attention will be paid to

the factors raised in the course of the audit.

2.6 REVENUES

A) Historic Sites and Canals YELLOW

Moderate Improvements Needed

Some controls are in place and functioning. However, major issues were noted and need to be addressed. These issues could have an impact on the achievement or not of program/operational objectives.

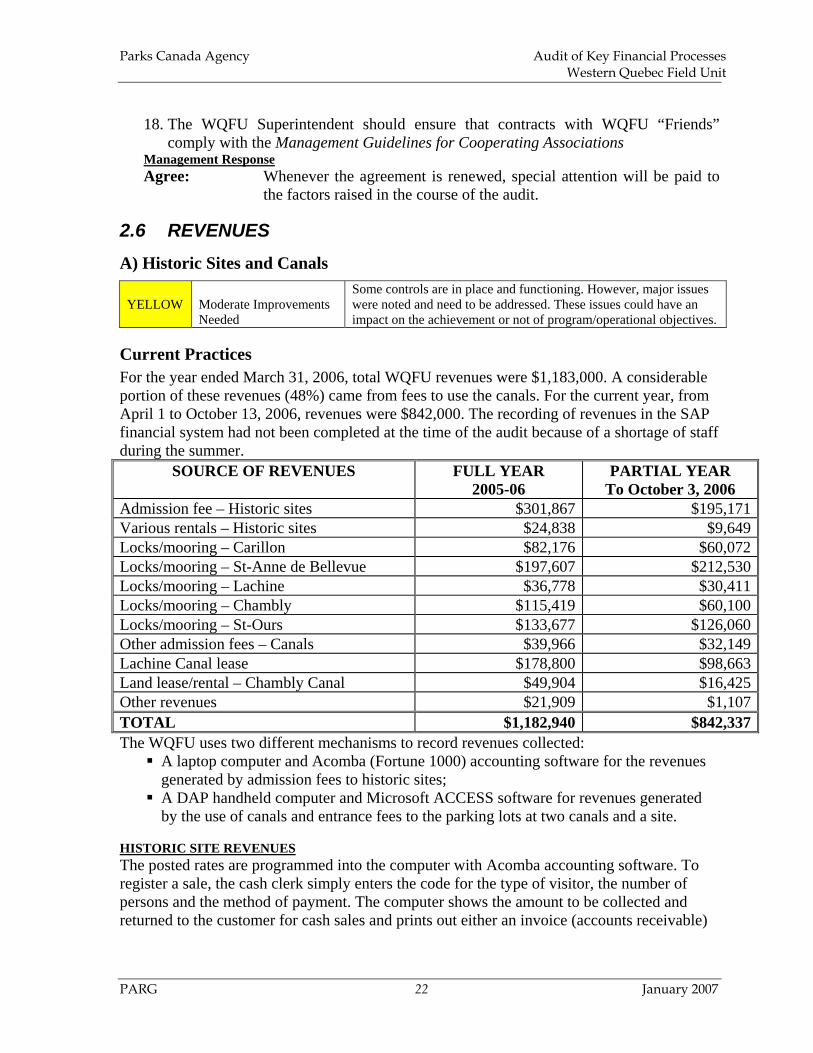

Current Practices For the year ended March 31, 2006, total WQFU revenues were $1,183,000. A considerable portion of these revenues (48%) came from fees to use the canals. For the current year, from April 1 to October 13, 2006, revenues were $842,000. The recording of revenues in the SAP financial system had not been completed at the time of the audit because of a shortage of staff during the summer.

SOURCE OF REVENUES FULL YEAR 2005-06

PARTIAL YEAR To October 3, 2006

Admission fee – Historic sites $301,867 $195,171Various rentals – Historic sites $24,838 $9,649Locks/mooring – Carillon $82,176 $60,072Locks/mooring – St-Anne de Bellevue $197,607 $212,530Locks/mooring – Lachine $36,778 $30,411Locks/mooring – Chambly $115,419 $60,100Locks/mooring – St-Ours $133,677 $126,060Other admission fees – Canals $39,966 $32,149Lachine Canal lease $178,800 $98,663Land lease/rental – Chambly Canal $49,904 $16,425Other revenues $21,909 $1,107TOTAL $1,182,940 $842,337The WQFU uses two different mechanisms to record revenues collected:

A laptop computer and Acomba (Fortune 1000) accounting software for the revenues generated by admission fees to historic sites;

A DAP handheld computer and Microsoft ACCESS software for revenues generated by the use of canals and entrance fees to the parking lots at two canals and a site.

HISTORIC SITE REVENUES The posted rates are programmed into the computer with Acomba accounting software. To register a sale, the cash clerk simply enters the code for the type of visitor, the number of persons and the method of payment. The computer shows the amount to be collected and returned to the customer for cash sales and prints out either an invoice (accounts receivable)

PARG 22 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

or the cash receipt. Receipts are kept in a file that is separate from the Acomba software. At the end of the day, the clerk prints out the daily report showing the details of the day’s transactions and the subtotal for each payment method. This report is then used to complete the “Cash statement” (using EXCEL) which makes it possible to balance the cash with the day’s receipts. Once it has been balanced, the reports, the money and the credit card and debit card statements are given to the responsible person identified for control purposes. The customer service assistant is the person responsible for preparing bank deposits. Accounts receivable – Most groups do not pay an admission fee when they visit. An invoice, which is generated by the Acomba system, is sent to the WQFU administrative office along with the cash journal to be sent to clients. The issuing of invoices and the collection of accounts receivable are the responsibility of financial services (see section C for more details about Current Practices). When payments are received, the site manager is advised so that the account receivable can be entered as received in the Acomba accounting system. At the end of the year, each site sends a list of unpaid accounts to finance so that they can be reconciled with the information entered in the Field Unit account receivable registers. CANAL REVENUES At each service point, 2 to 3 DAP handheld computers are used, depending on the level of traffic, each of which has an infrared link to a small printer. Each operator has his/her own user number and password to be entered in the DAP before operations can be performed. The journal can be closed at midday and the DAP can be loaned to another operator without losing the details of the first person’s transactions. Each operator begins the day with $100 in cash. For each boat entering the locks, the operator enters the boat’s name or registration number in the DAP. If the boat has already gone through during the season, the DAP indicates whether a season pass or a 60-day pass had been sold previously, and if not, it generates the length of the boat and the amount to be charged. If the trip through the locks is a new one and if a seasonal or 6-day pass is being purchased, additional information is entered in the system to generate the amount to be collected. For credit or debit card payments, the owner must go to the office/counter to complete the transaction. At the end of the day, the cash report generated by the DAP is reconciled in the presence of the lockmaster or the lockmaster’s assistant. Credit and debit card reports and cash are placed in an envelope, and the name of the operator and the date are written on the envelope. The envelope is given to the lockmaster and placed in the safe. If any discrepancies or gaps are identified (e.g. wrong card coding or payment method) a note needs to be written to explain the discrepancies and placed in the envelope. Training mode – Since 2006, the main menu on the DAP lists “Training mode” as an option. This option can be accessed by the site manager only and is used for training new employees. When it is used, a “TRAINING MODE” line is printed out at the top and bottom of all documents printed using the DAP. In addition, an alarm signal sounds every 3minutes to remind users that the computer is in training mode.

PARG 23 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Friends of the canals – The WQFU uses the services of community associations for reception, collection and interpretation services for two of its canals. A cooperation agreement and a service contract are signed each year with each of the organizations. The PCA provides the associations with DAP computers to facilitate receipt collection/ accounting for access to the sites. The receipts are then given to the lockmaster together with the receipts from the locks. Under the cooperation agreement, the organization’s financial statements need to be submitted to the PCA. Permit inventory and control – Annual permits for the use of the locks and for mooring are pre-numbered. When they are given to the lockmaster, an acknowledgement of receipt is returned to finance. Unused permits are returned to finance at the end of the season and entered into a spreadsheet in order to be able to control the use made of them at each of the sites. Segregation of duties – The audit focused in particular on the segregation of duties and on the controls in place to ensure that there is an audit trail for the collection of receipts. The DAP and Acomba systems ensure that there are consistent charges at all points of service, in addition to facilitating the registration of receipts, the collection of amounts received and the issuing of a cash receipt. The cash journal compiled by the DAP system provides a complete audit trail for activities (time, boat, amount collected, reason for free passage, etc.) at each lock and for each operator. For both types of receipts, there is a clear audit trail that cannot be deleted once it has been entered, and that makes it possible to track an operation from start to finish, from the accounting records back to the original operation. The people operating the systems and collecting receipts at the various points of service almost always have a supervisor or an assistant. The reconciliation of receipts at the end of the day with the transactions journal is to be given directly to the supervisor. Deposits are always made by a person other than the one who collected the receipts. The supporting documentation for the cash journal and the receipt accounting are always checked by different persons than the one responsible for reconciling the deposits with the Field Unit’s revenues. We were given detailed descriptions of the processes used for receipts and the verification procedures used at each step in the process. An audit of a sample of transactions showed that generally speaking, the processes and controls for the collection and deposit of receipts were satisfactory and that they had been applied during the audit period, and that personnel had done their work with due diligence. All of the recommendations made in a report dated March 2006 following a review of the procedures used to record and deposit canal receipts during the 2005 season were implemented during the 2006 season.

Observations Each user of the Acomba software does not have a different password for registering admission receipts to historic sites. When traffic is heavy, while responsibility for cash is

PARG 24 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

assigned to a single person, more than one employee could make entries in the Acomba software and have access to the cash drawer. If there were a cash discrepancy, it would be impossible to identify the person responsible for it.

Recommendation 19. The WQFU Superintendent should look into the possibility of a separate cash drawer

for each employee. Management Response Agree with reservation: The Field Unit decided to introduce the new VECTRON

system in 2008-09. The DAP system currently in use will be replaced next year. This change should solve the cash drawer problem.

B) Leases and permits ORANGE

Significant Improvements Needed

Controls in place are weak. Several major issues were noted that could jeopardize the accomplishment of program/operational objectives. Immediate management actions need to be taken to address the control deficiencies noted.

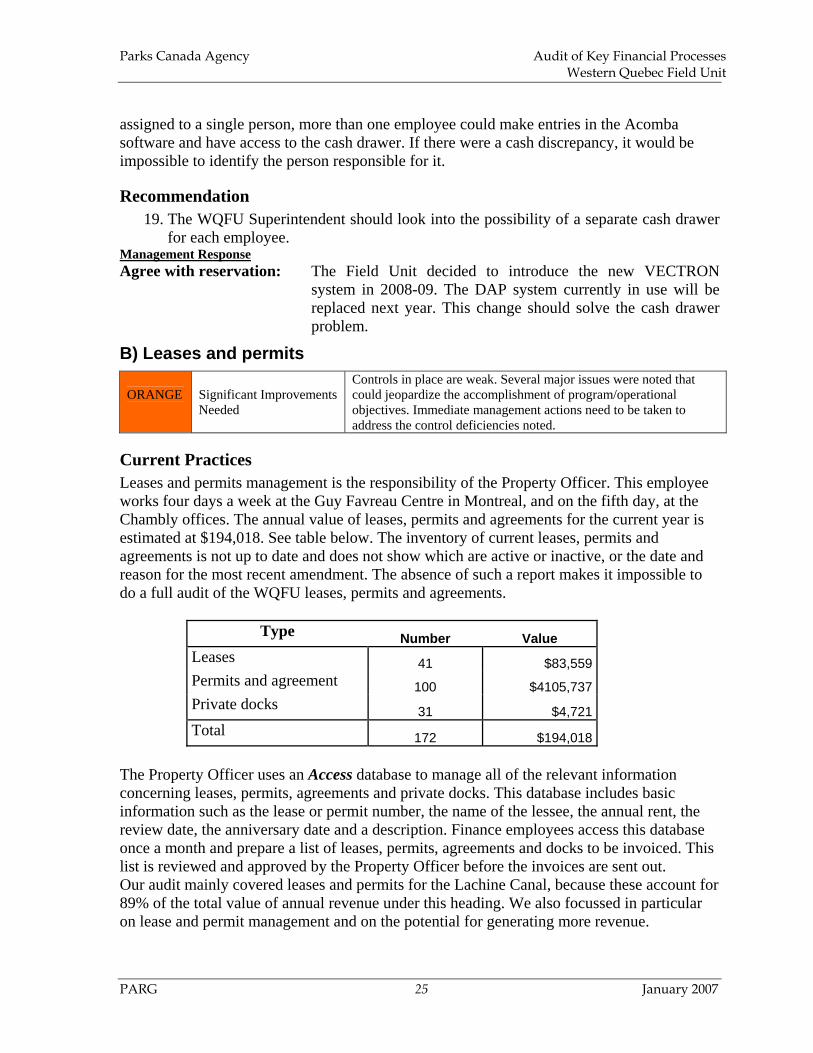

Current Practices Leases and permits management is the responsibility of the Property Officer. This employee works four days a week at the Guy Favreau Centre in Montreal, and on the fifth day, at the Chambly offices. The annual value of leases, permits and agreements for the current year is estimated at $194,018. See table below. The inventory of current leases, permits and agreements is not up to date and does not show which are active or inactive, or the date and reason for the most recent amendment. The absence of such a report makes it impossible to do a full audit of the WQFU leases, permits and agreements.

Type Number Value Leases 41 $83,559 Permits and agreement 100 $4105,737 Private docks 31 $4,721 Total 172 $194,018

The Property Officer uses an Access database to manage all of the relevant information concerning leases, permits, agreements and private docks. This database includes basic information such as the lease or permit number, the name of the lessee, the annual rent, the review date, the anniversary date and a description. Finance employees access this database once a month and prepare a list of leases, permits, agreements and docks to be invoiced. This list is reviewed and approved by the Property Officer before the invoices are sent out. Our audit mainly covered leases and permits for the Lachine Canal, because these account for 89% of the total value of annual revenue under this heading. We also focussed in particular on lease and permit management and on the potential for generating more revenue.

PARG 25 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

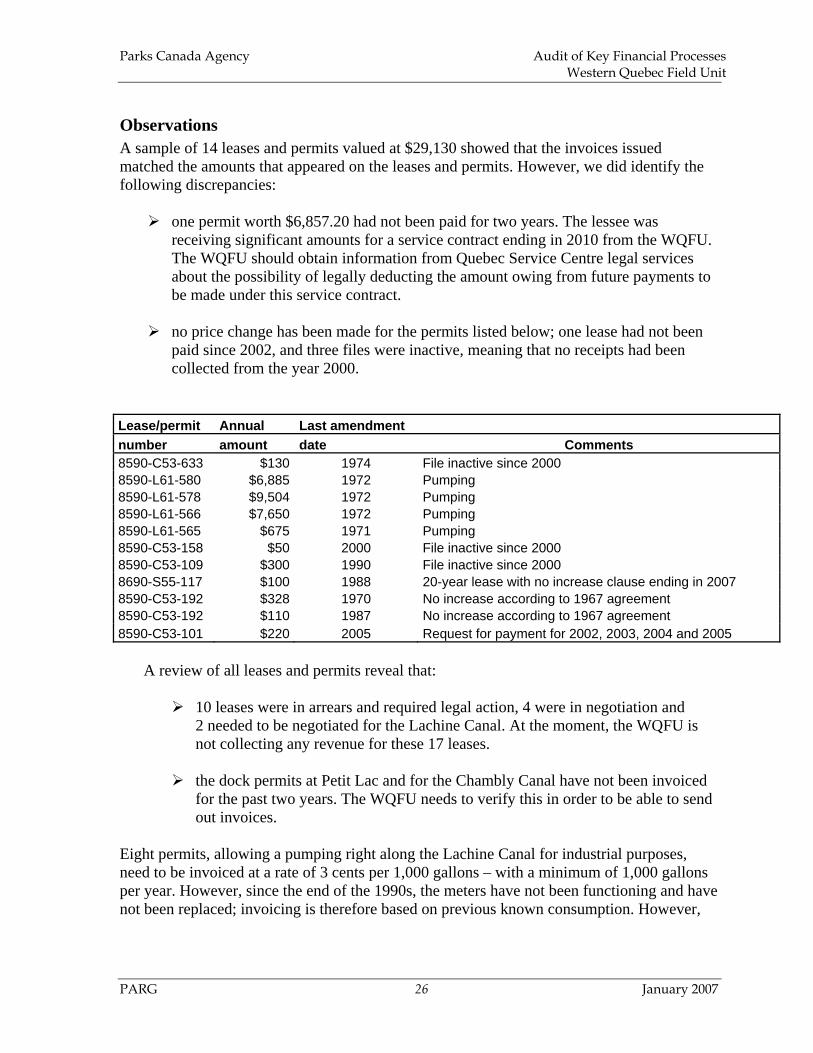

Observations A sample of 14 leases and permits valued at $29,130 showed that the invoices issued matched the amounts that appeared on the leases and permits. However, we did identify the following discrepancies:

one permit worth $6,857.20 had not been paid for two years. The lessee was receiving significant amounts for a service contract ending in 2010 from the WQFU. The WQFU should obtain information from Quebec Service Centre legal services about the possibility of legally deducting the amount owing from future payments to be made under this service contract.

no price change has been made for the permits listed below; one lease had not been

paid since 2002, and three files were inactive, meaning that no receipts had been collected from the year 2000.

Lease/permit Annual Last amendment number amount date Comments 8590-C53-633 $130 1974 File inactive since 2000 8590-L61-580 $6,885 1972 Pumping 8590-L61-578 $9,504 1972 Pumping 8590-L61-566 $7,650 1972 Pumping 8590-L61-565 $675 1971 Pumping 8590-C53-158 $50 2000 File inactive since 2000 8590-C53-109 $300 1990 File inactive since 2000 8690-S55-117 $100 1988 20-year lease with no increase clause ending in 2007 8590-C53-192 $328 1970 No increase according to 1967 agreement 8590-C53-192 $110 1987 No increase according to 1967 agreement 8590-C53-101 $220 2005 Request for payment for 2002, 2003, 2004 and 2005

A review of all leases and permits reveal that:

10 leases were in arrears and required legal action, 4 were in negotiation and 2 needed to be negotiated for the Lachine Canal. At the moment, the WQFU is not collecting any revenue for these 17 leases.

the dock permits at Petit Lac and for the Chambly Canal have not been invoiced

for the past two years. The WQFU needs to verify this in order to be able to send out invoices.

Eight permits, allowing a pumping right along the Lachine Canal for industrial purposes, need to be invoiced at a rate of 3 cents per 1,000 gallons – with a minimum of 1,000 gallons per year. However, since the end of the 1990s, the meters have not been functioning and have not been replaced; invoicing is therefore based on previous known consumption. However,

PARG 26 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

the agreement allows for the recovery of the cost of replacing the meters. These permits generate annual revenue of $57,879.

the same rate of 3 cents has been used since the issuing of the permits in the early 1970s, even though some of the agreements allow for annual increases based on the value of the service provided.

There is also potential to issue approximately 30 leases for land along the Chambly Canal. However, the WQFU does not have the resources needed to go forward with this project. The WQFU is aware of the fact that there is potential to generate more revenue for leases and permits and is currently working with legal services at the Quebec Service Centre and at the national office to do something about it. In its sustainable plan, the WQFU had agreed to submit to the finance committee a strategy for revenue generation from leases and permits by September 2006. This whole area involves important legal and environmental issues and has been slowly progressing for a number of years. Recommendations

20. The WQFU Superintendent should finalize the strategy for maximizing revenue generated by leases and permits and establish a reasonable schedule for its implementation.

Management Response Agree: The revenue generation strategy was submitted to the finance

committee in November 2006. Implementation of the strategy requires an increase in the Field Unit’s capacity. Thus far, a monitoring system has been put in place to monitor the various leases at every stage in the process. We are continuing to work on the overall implementation of the strategy.

C) Accounts receivable ORANGE

Significant Improvements Needed

Controls in place are weak. Several major issues were noted that could jeopardize the accomplishment of program/operational objectives. Immediate management actions need to be taken to address the control deficiencies noted.

Current Practices and Observations Accounts receivable are calculated manually rather than through the SAP financial system. Recent changes to the SAP system make it difficult to use for invoicing the various WQFU clients. The new system uses unique line items, and requires a new item for each invoice and the involvement of Headquarters to prepare it. The manual invoices are placed together in a binder and divided into current accounts, accounts unpaid for 30 to 60 days and accounts

PARG 27 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

unpaid for more than 90 days. This practice weakens control and monitoring over accounts receivable because the SAP system no longer reflects all of the accounts to be collected. In addition, we determined that the balance of accounts receivable in the SAP system included at least two entries, worth a total of $20,474.46, that had already been paid. We also found that paid invoices were still in the unpaid invoices binder. Rectification is required to establish the actual amounts of accounts receivable.

Recommendations

21. The WQFU Superintendent should work with those in charge of the SAP system in order to able to issue and control accounts receivable through the SAP system.

Management Response Agree: Discussions will be set in motion with the national office. 22. The WQFU Superintendent should determine whether manual invoices in the

accounts receivable binder and unpaid invoices in the SAP system still represent valid accounts receivable, and make the accounting adjustments required to update the accounts receivable in this system.

Management Response Agree: Completed.

2.7 FINANCIAL CODING BLUE

Minor Improvements Needed Many of the controls are functioning as intended. However, some

minor changes are necessary to make the control environment more effective and efficient.

Current Practices Managers are responsible for entering the financial code on each payment requisition sent to finance. Finance staff are responsible for checking the financial code and making corrections when needed. Finance staff are also responsible for assigning the financial code for payment requisitions related to fixed costs, such as telephone, electricity, mail, courier and photocopy accounts.

Observations While there is no checklist to facilitate the entry of financial codes, we observed that they were generally accurate, except for some hospitality expenses that were incorrectly coded (see section 2.4 - Travel expenses). Interviews with finance staff and audit of payments to suppliers and acquisition cards, as well as 10 payment files, identified only one GL account coding error.

PARG 28 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Recommendations No recommendation.

2.8 INVENTORIES ORANGE

Significant Improvements Needed

Controls in place are weak. Several major issues were noted that could jeopardize the accomplishment of program/operational objectives. Immediate management actions need to be taken to address the control deficiencies noted.

Current Practices Western Quebec Field Unit inventories are entered on five inventory lists:

1) An inventory of bridges, canals, buildings, parking lots, vehicle, truck and tractor fleets, etc., as entered in the asset management system (AMS)

2) An inventory of assets worth over $10,000 in the SAP system 3) An inventory of assets worth between $1,000 and $10,000, including attractive items

such as digital cameras and binoculars worth less than $1,000, managed by the asset manager

4) An inventory of computers and peripherals, managed by the computer manager 5) An inventory of collections, managed by the Quebec Service Centre.

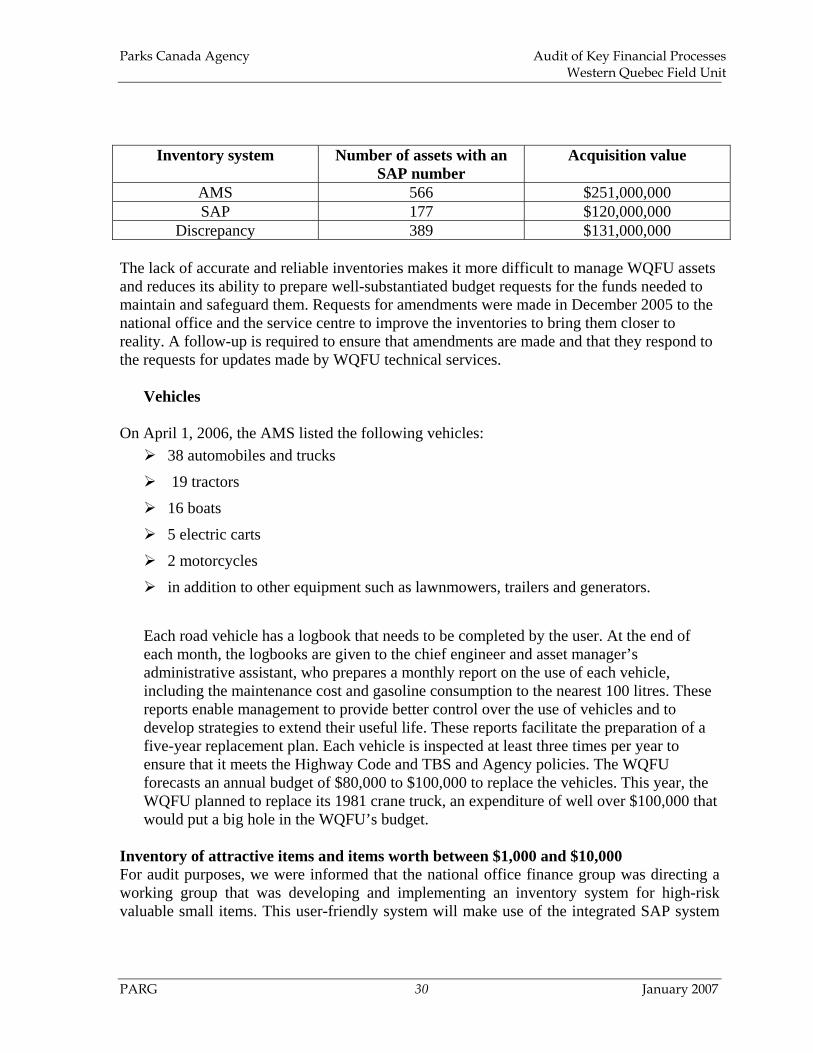

Observations AMS and SAP Inventories The asset management system (AMS) shows that the WQFU has assets valued at over $823,000,000, in terms of replacement costs, and at more than $251,000,000 based on original cost. The vast majority of these assets consist of properties such as bridges, canals, buildings, parking lots and rolling stock such as vehicles, tractors and boats. Local AMS management is under the responsibility of the chief engineer and asset manager. Normally, assets worth more than $10,000 should also be entered into the SAP financial system, which is the responsibility of the finance and administration manager. We determined that the AMS includes items for which the replacement cost and/or original cost are not shown, either because the amendments requested have not been made or because of the nature of the assets (e.g. archaeological artefacts). It may also be that the original cost is not available. Most of these items do not have the SAP number because the value shown in the AMS is zero. There is also a considerable difference between assets that have an SAP number in the AMS and assets entered in the SAP financial system inventory, as demonstrated in the table below. This discrepancy may result from a number of factors, including the fact that assets worth less than $10,000 sometimes appear only in the AMS (e.g. plaques, monuments); assets related to archaeology and exhibition programs have been entered into the AMS.

It is important to note that the development of the AMS under the responsibility of the national office was interrupted, and that the decision was made to acquire a commercially available system.

PARG 29 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

Inventory system Number of assets with an SAP number

Acquisition value

AMS 566 $251,000,000 SAP 177 $120,000,000

Discrepancy 389 $131,000,000 The lack of accurate and reliable inventories makes it more difficult to manage WQFU assets and reduces its ability to prepare well-substantiated budget requests for the funds needed to maintain and safeguard them. Requests for amendments were made in December 2005 to the national office and the service centre to improve the inventories to bring them closer to reality. A follow-up is required to ensure that amendments are made and that they respond to the requests for updates made by WQFU technical services.

Vehicles

On April 1, 2006, the AMS listed the following vehicles: 38 automobiles and trucks

19 tractors

16 boats

5 electric carts

2 motorcycles

in addition to other equipment such as lawnmowers, trailers and generators.

Each road vehicle has a logbook that needs to be completed by the user. At the end of each month, the logbooks are given to the chief engineer and asset manager’s administrative assistant, who prepares a monthly report on the use of each vehicle, including the maintenance cost and gasoline consumption to the nearest 100 litres. These reports enable management to provide better control over the use of vehicles and to develop strategies to extend their useful life. These reports facilitate the preparation of a five-year replacement plan. Each vehicle is inspected at least three times per year to ensure that it meets the Highway Code and TBS and Agency policies. The WQFU forecasts an annual budget of $80,000 to $100,000 to replace the vehicles. This year, the WQFU planned to replace its 1981 crane truck, an expenditure of well over $100,000 that would put a big hole in the WQFU’s budget.

Inventory of attractive items and items worth between $1,000 and $10,000 For audit purposes, we were informed that the national office finance group was directing a working group that was developing and implementing an inventory system for high-risk valuable small items. This user-friendly system will make use of the integrated SAP system

PARG 30 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

and will be operational by April 1, 2007. From that point on, field units will be required to enter all new acquisitions into the database. For the time being, retroactive entry into the system is not compulsory. Inventory of computer equipment The computer specialist maintains an inventory of computer equipment in a Microsoft ACCESS database. For each inventoried item, the following information is entered: type of equipment, manufacturer, model, serial number, purchase date, cost, location of use and replacement date. The software in question can generate reports and statistics about the equipment in various formats. A detailed report of the whole inventory was prepared during the audit. The summary equipment report by location shows that the WQFU has 139 desktop computers, 44 laptops and 21 handheld DAP computers for collecting receipts at canals, as well as 71 printers. The total cost of the equipment in the inventory was approximately $560,000. The computer specialist responsible for the inventory acknowledged that a physical count will be required to update the information that was entered at the time of purchase, but that the information is not updated afterwards. Inventory of collection assets The inventory of all collection assets is the responsibility of the Quebec Service Centre. For each location where there are collection assets, the manager is responsible for a physical count of all assets when the location is closed and for sending the results to the service centre inventory manager, and is also responsible for advising the manager of any theft, breakage or other changes to collection objects.

Recommendations 23. The WQFU Superintendent should establish a strategy for maintaining and updating

inventories of items worth over $10,000 in the SAP system. Management Response Agree: The requisition process will be enhanced by April 2007 to ensure that

there is more accurate information in the SAP.

24. The WQFU Superintendent should ensure that the AMS accurately represents the assets under her responsibility.

Management Response Agree: An internal system will be used from now on by Finance at the WQFU

to improve the quality of information in the financial and asset management systems. Follow-up action will also be taken with respect to requisitions made in December 2005.

PARG 31 January 2007

Parks Canada Agency Audit of Key Financial Processes Western Quebec Field Unit

25. As a best practice, the WQFU Superintendent should consider updating the inventory of high-risk valuable small items in order to include this information in the database when the new system becomes operational.

Management ResponseAgree: We will attempt to obtain a list of low-dollar items at each of the sites

and include this information in the system; staff will also be informed of the procedures required to enter the information.

PARG 32 January 2007