applying islamic finance principles to microfinance abyan ahmed, muslim aid uk

TRANSCRIPT

Applying Islamic Finance Principles to Microfinance

ABYAN AHMED, MUSLIM AID UK

WHAT IS ISLAMIC FINANCE?

Refers to a system of banking that is consistent with Islamic Law(Sharia) principles

This system reflects Islam's teachings on wealth distribution, social and economic Justice.

The basic practices and principles of Islamic Finance date back to the early part of the seventh century. (Islamic Finance: A Euromoney Publication, 1997)

Islamic finance is currently estimated at $1 trillion with an expected growth rate of 15 percent per year ( Forbes)

PRINCIPLES OF ISLAMIC FINANCEPRINCIPLES OF ISLAMIC FINANCE

Prohibition of Interest

Risk sharing

Social Mission

Prohibition of speculative behaviour

Sanctity of contracts

Shariah-approved activities.

PROHIBITION OF INTEREST

The prohibition is strict, absolute and unambigous.

The Holy Qur'an in verse 278 of Surah Al-Baqarah states:

"O ye who believe! fear Allah and give up what remains of your demand for riba, if ye are indeed believers."

Riba means any fixed or guaranteed interest payment on cash advances or on deposits.

Islam encourages the earning of profits but forbids the charging of interest

To replace interest, the ideal mode of financing under the Islamic banking system is "Financing on Profit & Loss Sharing" (PLS) basis

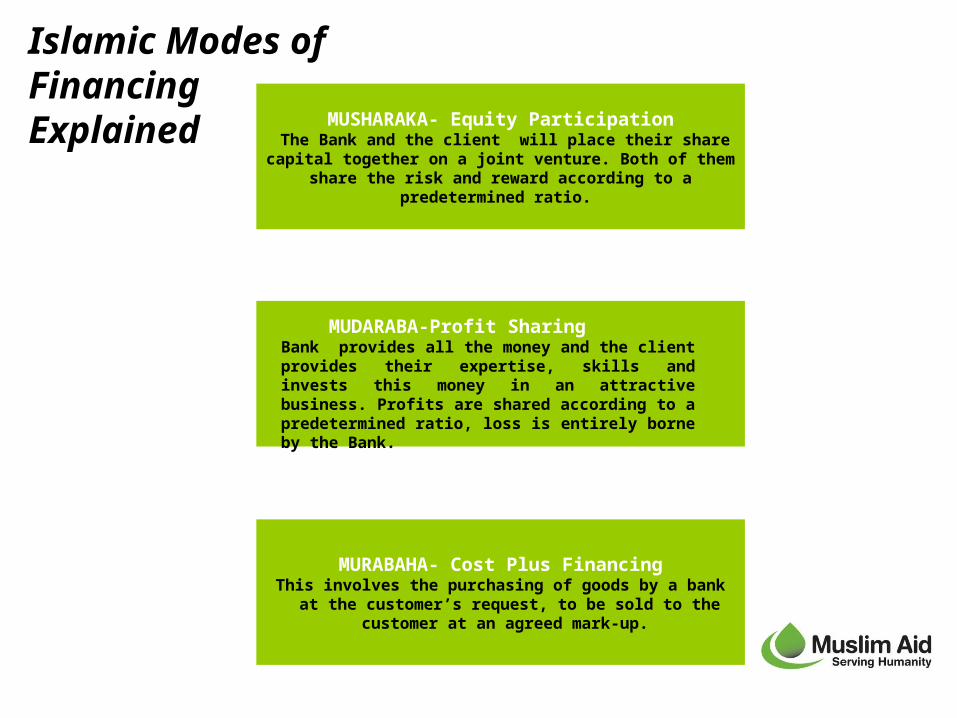

Islamic Modes of Financing Explained MUSHARAKA- Equity Participation

The Bank and the client will place their share capital together on a joint venture. Both of them share the risk and

reward according to a predetermined ratio.

MURABAHA- Cost Plus FinancingThis involves the purchasing of goods by a bank at the

customer’s request, to be sold to the customer at an agreed mark-up.

MUDARABA-Profit Sharing

Bank provides all the money and the client provides their expertise, skills and invests this money in an attractive business. Profits are shared according to a predetermined ratio, loss is entirely borne by the Bank.

MURABAHA

Can achieve the goals of microenterprise lending

Eliminates the need for written records (especially useful for when dealing with illeterate client)

Well-defined contract exists

There is no opportunity for abuse on the part of the client through inaccurate or false record-keeping

Asset-based – can prevent diversion of funds for consumption

A fixed contract creates simple and straight forward procedures

lower adminstrative costs and monitoring cost for the institution

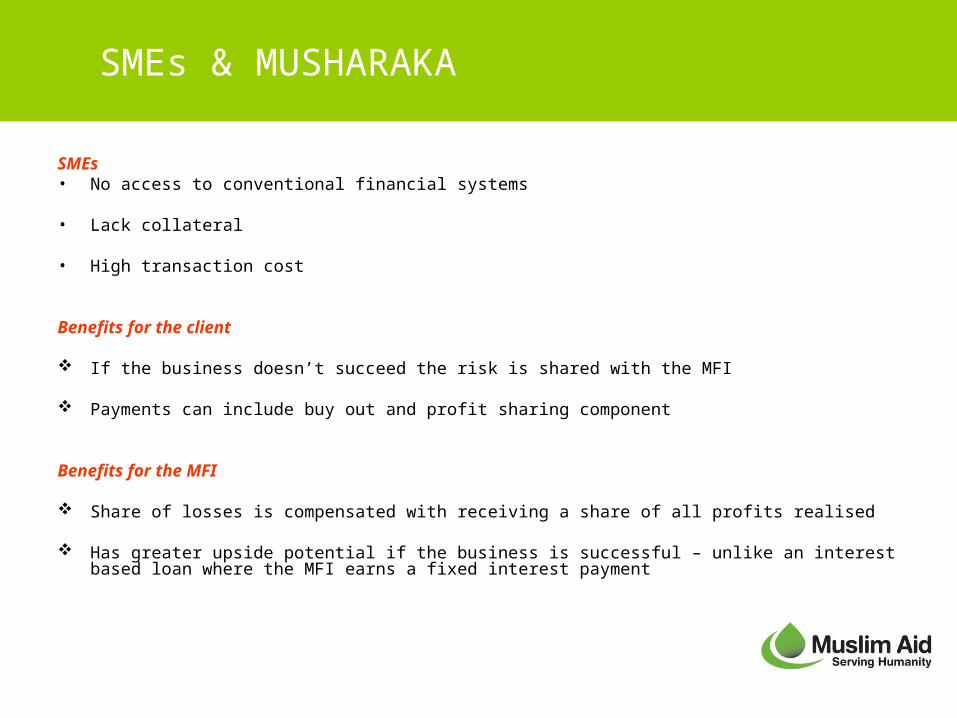

SMEs & MUSHARAKA

SMEs• No access to conventional financial systems

• Lack collateral

• High transaction cost

Benefits for the client

If the business doesn’t succeed the risk is shared with the MFI

Payments can include buy out and profit sharing component

Benefits for the MFI

Share of losses is compensated with receiving a share of all profits realised

Has greater upside potential if the business is successful – unlike an interest based loan where the MFI earns a fixed interest payment

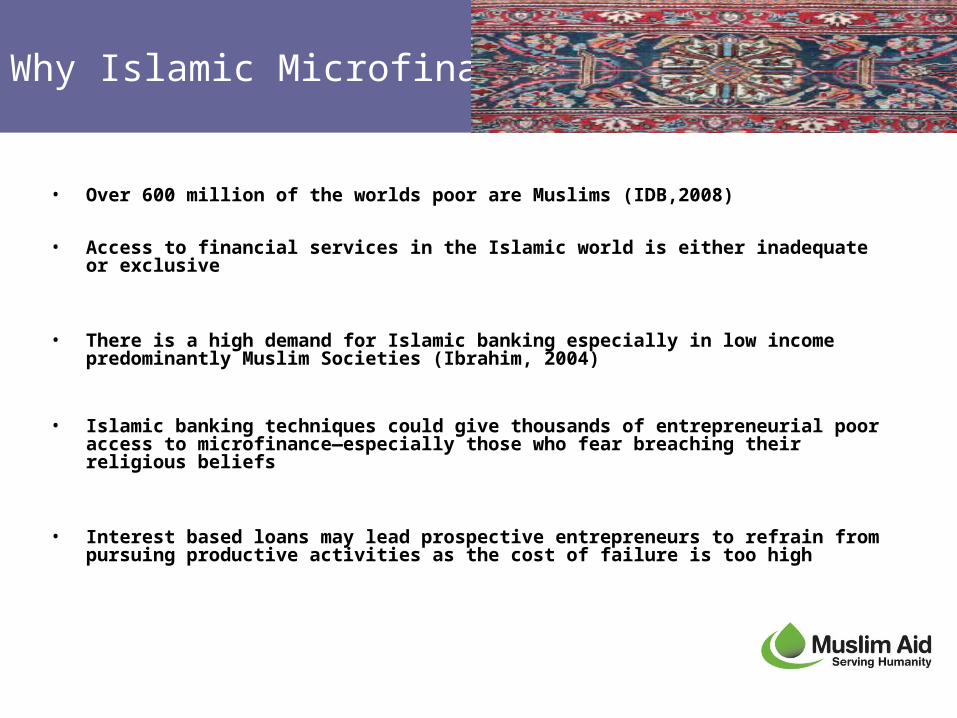

Why Islamic Microfinance?

• Over 600 million of the worlds poor are Muslims (IDB,2008)

• Access to financial services in the Islamic world is either inadequate or exclusive

• There is a high demand for Islamic banking especially in low income predominantly Muslim Societies (Ibrahim, 2004)

• Islamic banking techniques could give thousands of entrepreneurial poor access to microfinance—especially those who fear breaching their religious beliefs

• Interest based loans may lead prospective entrepreneurs to refrain from pursuing productive activities as the cost of failure is too high

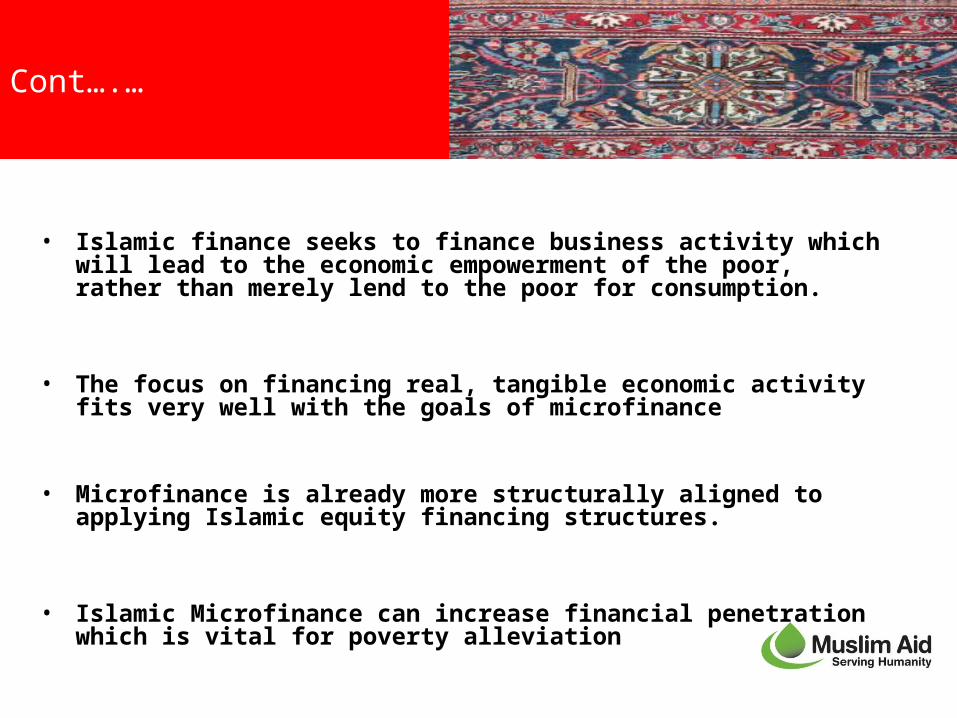

• Islamic finance seeks to finance business activity which will lead to the economic empowerment of the poor, rather than merely lend to the poor for consumption.

• The focus on financing real, tangible economic activity fits very well with the goals of microfinance

• Microfinance is already more structurally aligned to applying Islamic equity financing structures.

• Islamic Microfinance can increase financial penetration which is vital for poverty alleviation

Cont….…

SIMILIARITIES

Both systems

Advocate entrepreneurship

Risk sharing

Strongly believe the poor should take active part in their own development.

Financial Inclusion

Represent unconventional solutions to financial needs

They start from egalitarian approaches

ISLAMIC MICROFINANCE

& SUSTAINABILITY

One of the guiding principles of Microfinance is that the programme must ensure financial sustainability

Apart from financing on a profit & loss basis Islamic Microfinance can also use service charge to cover their costs

Service charge is a legitimate mechanism for pursuing sustainability

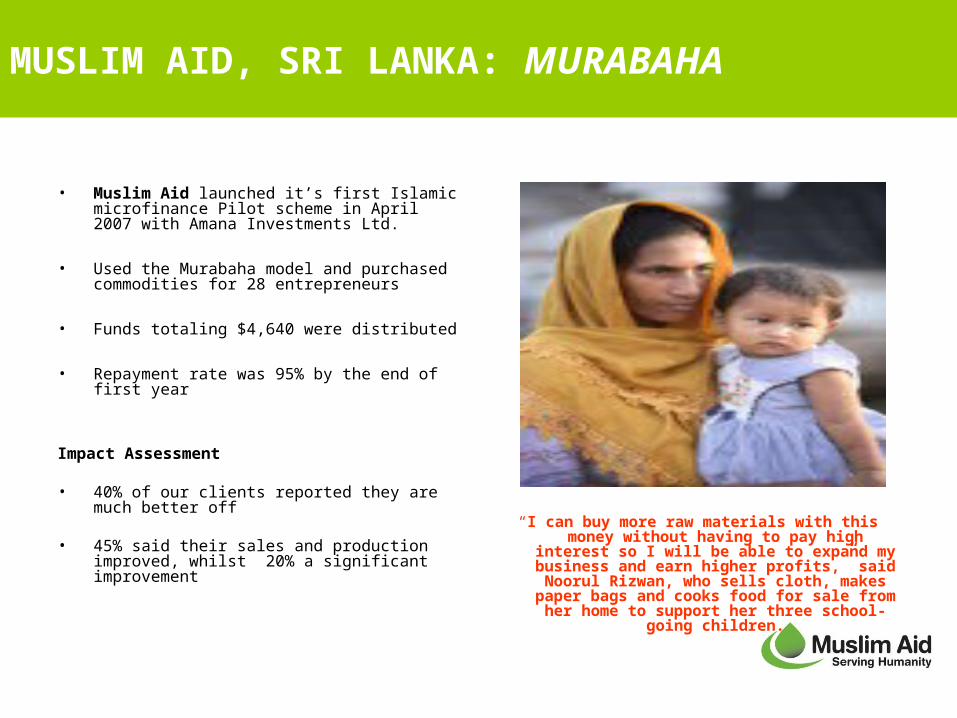

MUSLIM AID, SRI LANKA: MURABAHA

• Muslim Aid launched it’s first Islamic microfinance Pilot scheme in April 2007 with Amana Investments Ltd.

• Used the Murabaha model and purchased commodities for 28 entrepreneurs

• Funds totaling $4,640 were distributed

• Repayment rate was 95% by the end of first year

Impact Assessment

• 40% of our clients reported they are much better off

• 45% said their sales and production improved, whilst 20% a significant improvement

“I can buy more raw materials with this money without having to pay high interest so I will be able to expand my business and earn higher profits,” said Noorul Rizwan, who sells cloth,

makes paper bags and cooks food for sale from her home to support her three school-going

children.

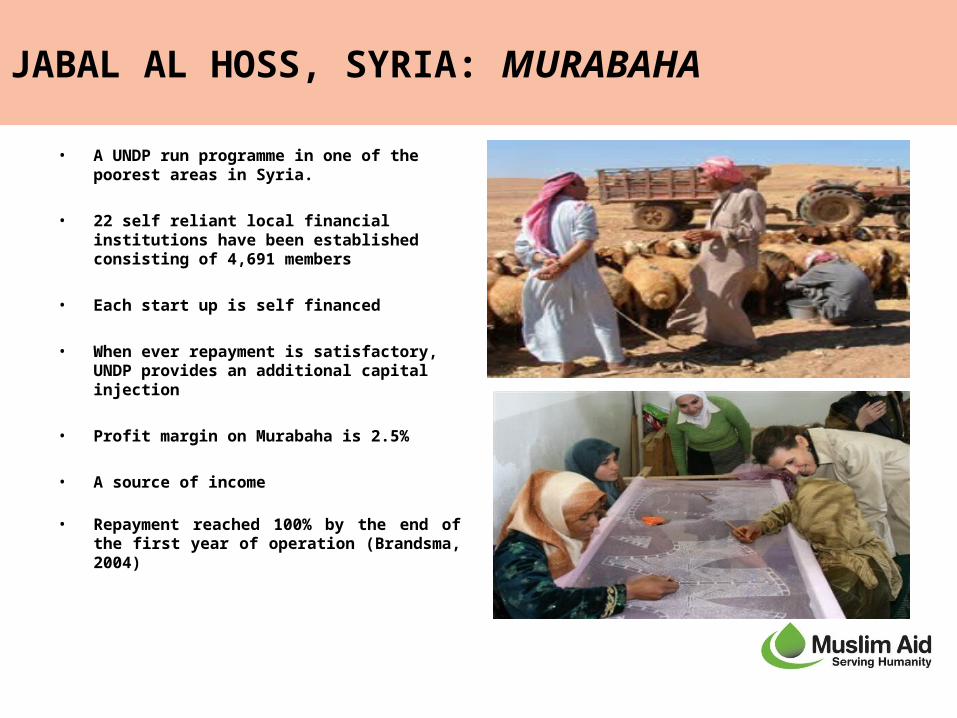

JABAL AL HOSS, SYRIA: MURABAHA

• A UNDP run programme in one of the poorest areas in Syria.

• 22 self reliant local financial institutions have been established consisting of 4,691 members

• Each start up is self financed

• When ever repayment is satisfactory, UNDP provides an additional capital injection

• Profit margin on Murabaha is 2.5%

• A source of income

• Repayment reached 100% by the end of the first year of operation (Brandsma, 2004)

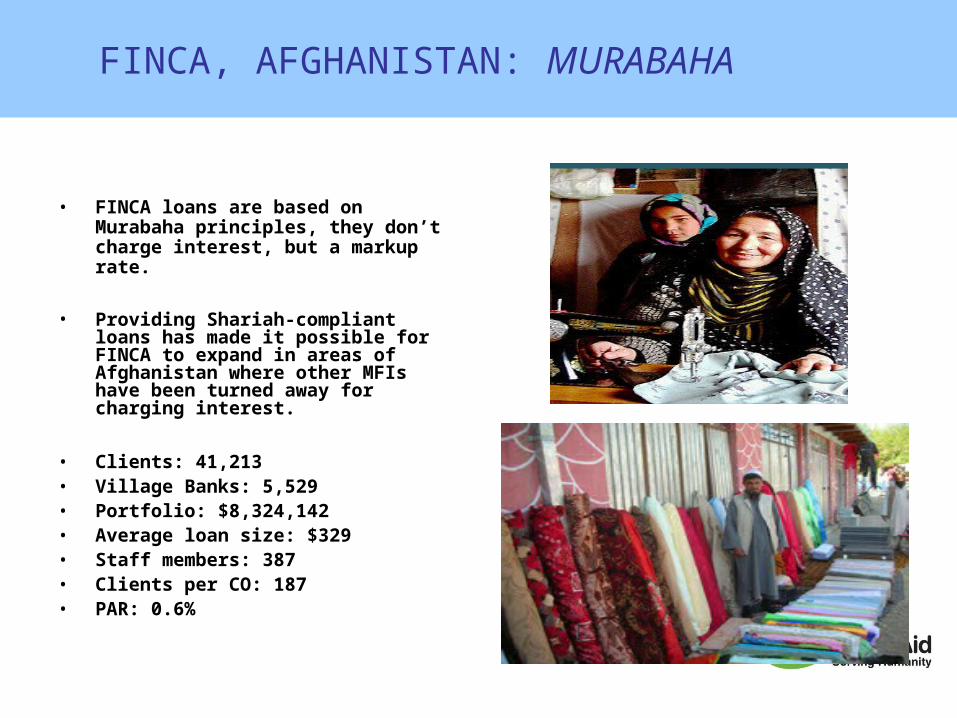

FINCA, AFGHANISTAN: MURABAHA

• FINCA loans are based on Murabaha principles, they don’t charge interest, but a markup rate.

• Providing Shariah-compliant loans has made it possible for FINCA to expand in areas of Afghanistan where other MFIs have been turned away for charging interest.

• Clients: 41,213• Village Banks: 5,529• Portfolio: $8,324,142• Average loan size: $329• Staff members: 387• Clients per CO: 187• PAR: 0.6%

Islamic Microfinance

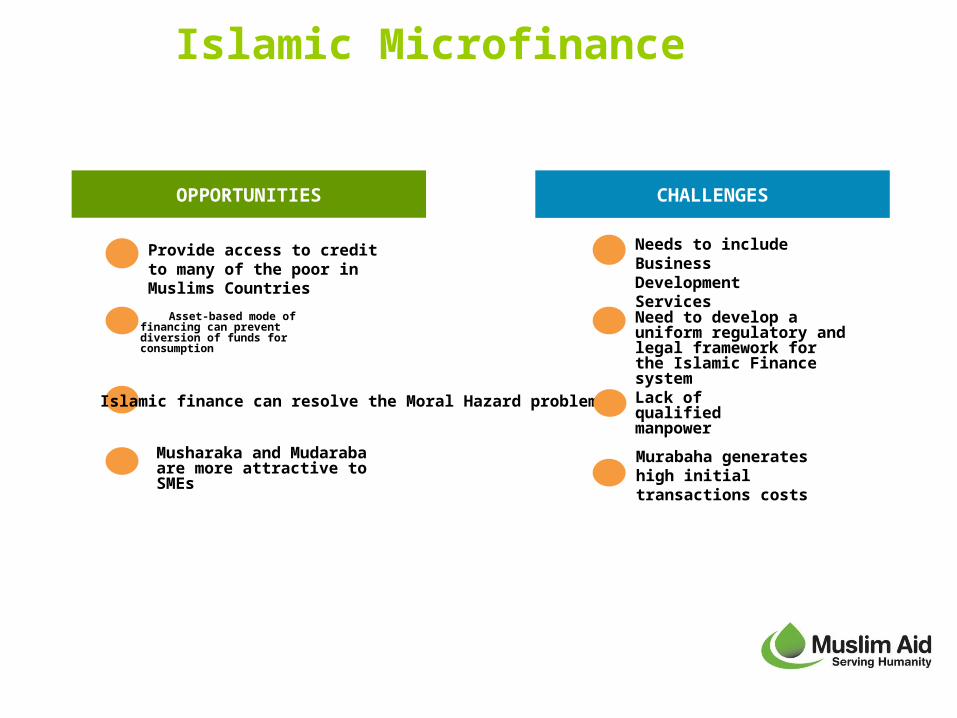

Asset-based mode of financing can prevent diversion of funds for consumption

CHALLENGESOPPORTUNITIES

Needs to include Business Development Services

Provide access to credit to many of the poor in Muslims Countries

Musharaka and Mudaraba are more attractive to SMEs

Islamic finance can resolve the Moral Hazard problem Lack of qualified manpower

Need to develop a uniform regulatory and legal framework for the Islamic Finance system

Murabaha generates high initial transactions costs

Conclusion

Diverse approaches are needed- making this a reality entails breaking down the walls real and imaginary that currently separate microfinance from the much broader world of financial systems

In the context of poor people in Muslim societies, building inclusive financial systems would most certainly require integration of microfinance with Islamic finance.

Cultural and religious sensitivities of the Islamic world are somewhat unique and these must be given due emphasis in any attempt to build inclusive financial systems and bring the over one-billion Muslims into the fold of formal financial systems.

MUSLIM AID: Towards Economic Empowerment

THANK YOU!

Muslim Aid PO Box 3London E1 1WP

Contact:[email protected]@muslimaid.org