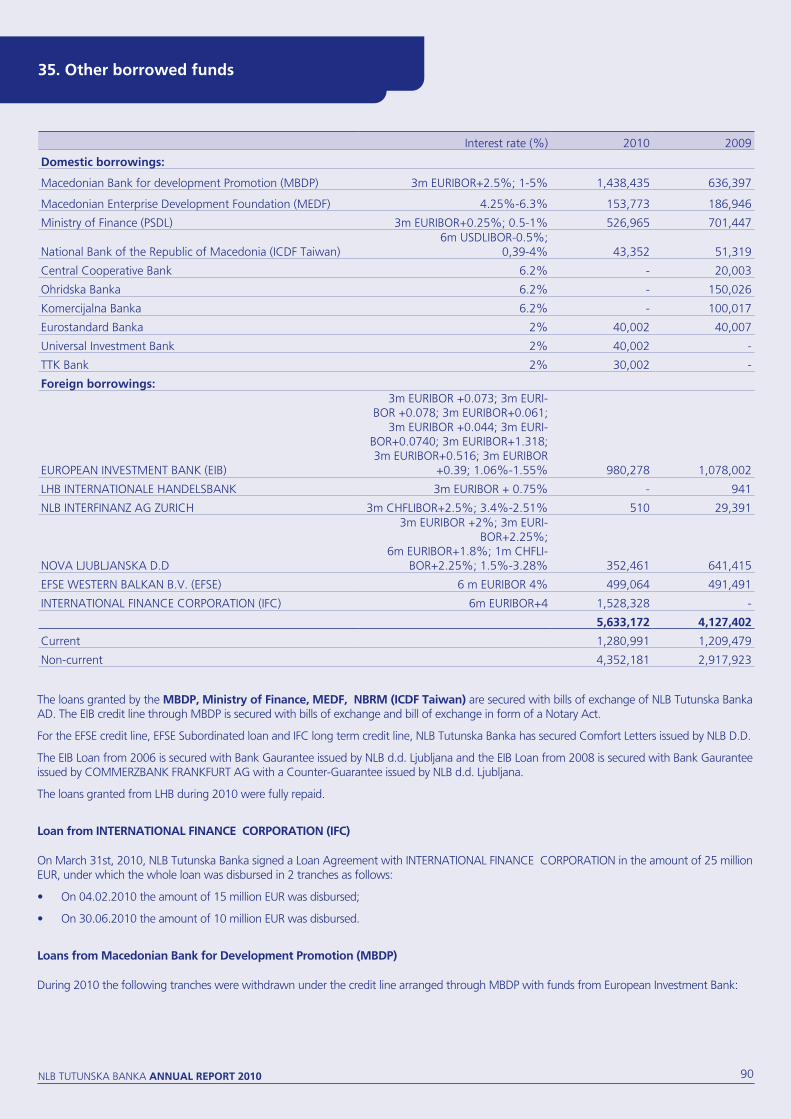

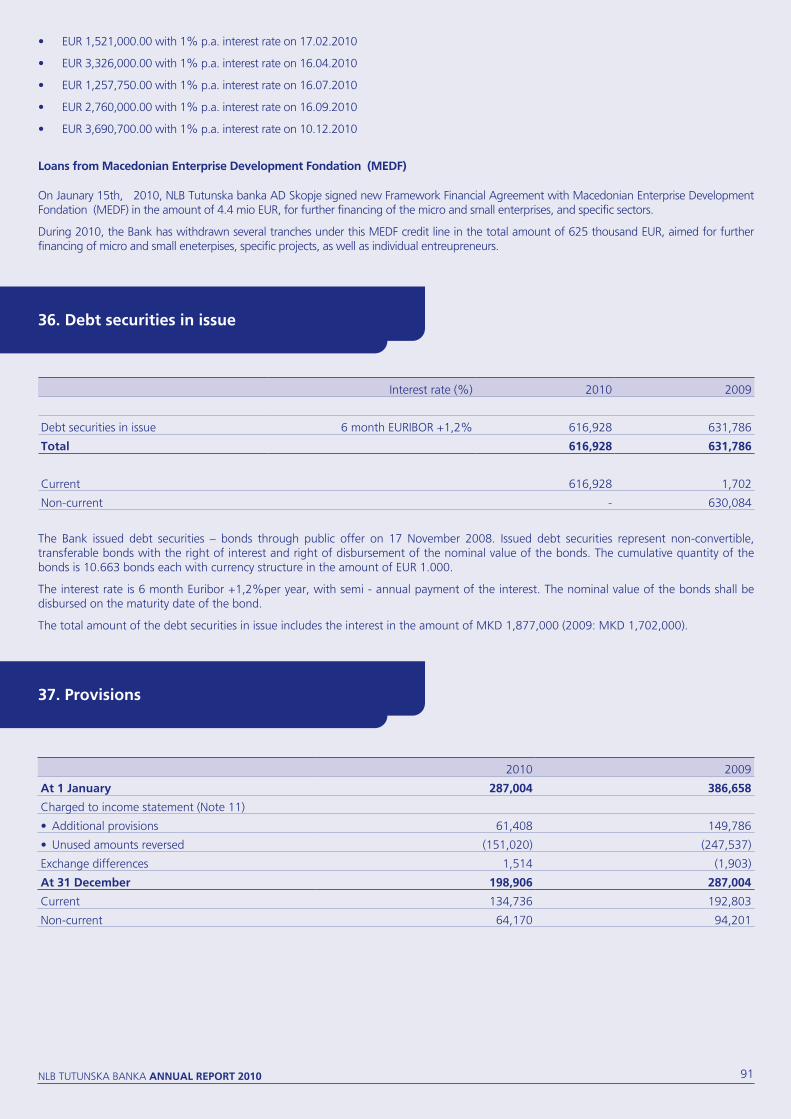

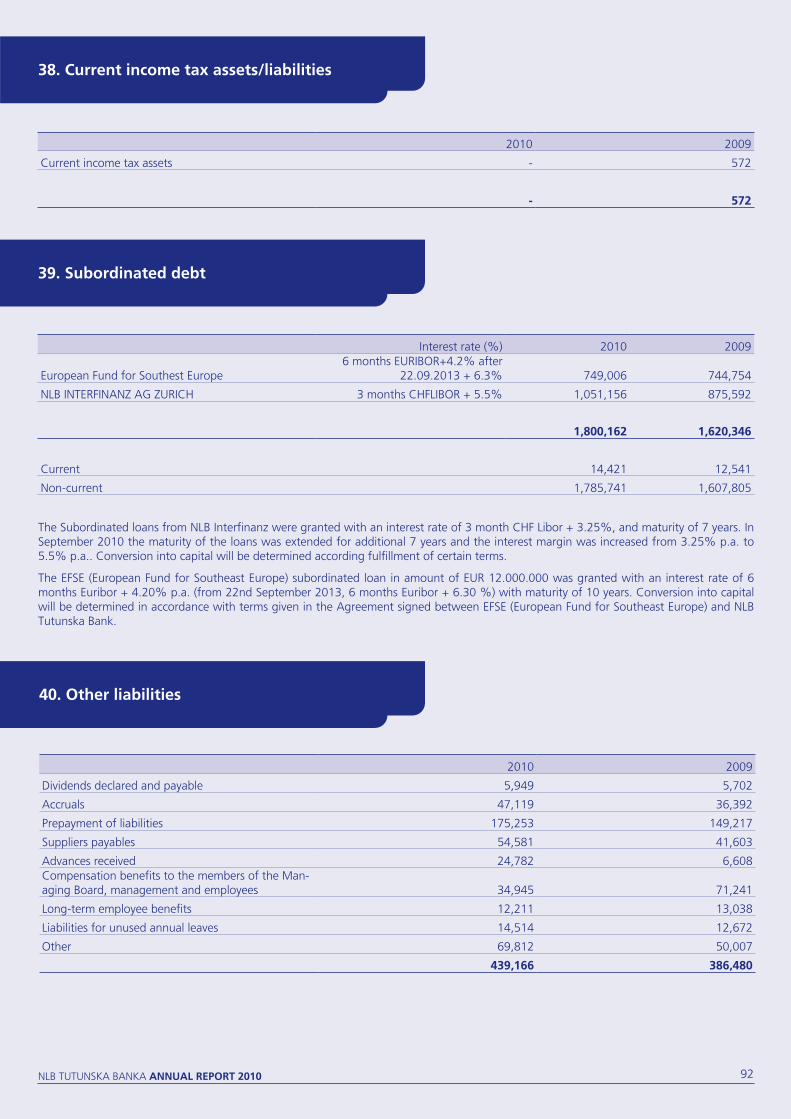

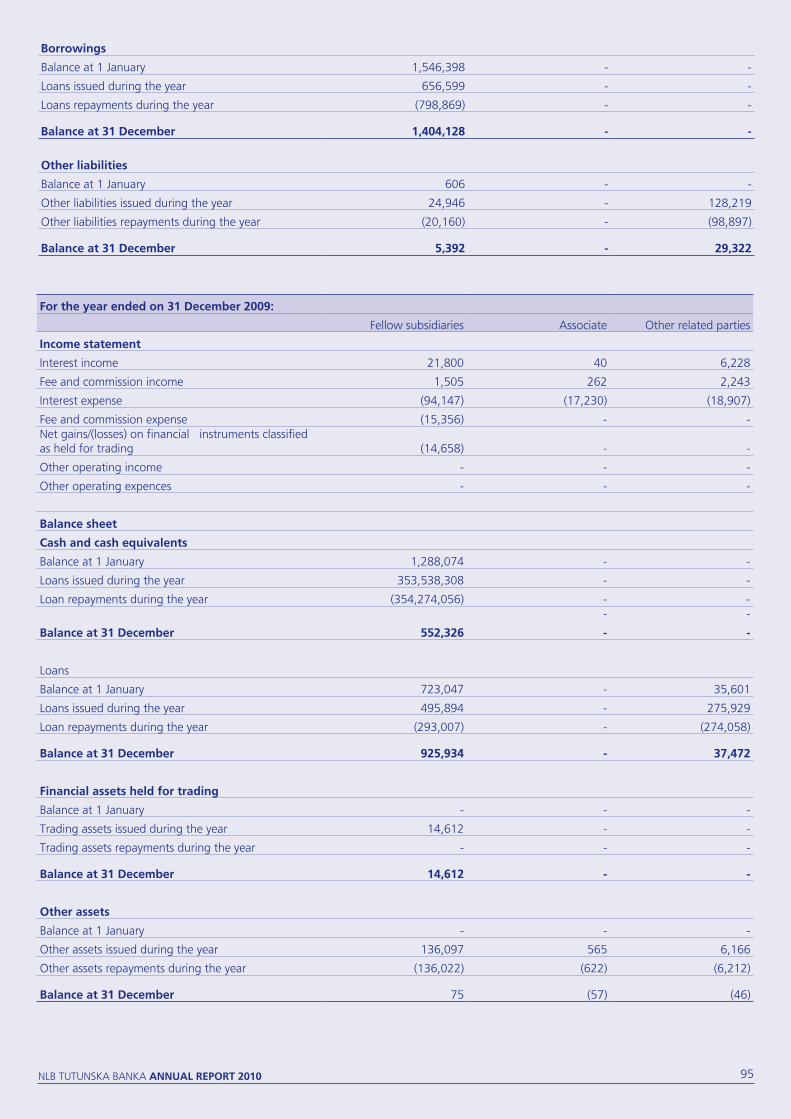

annual report 2010 - Македонски - Почетна › wbstorage › files ›...

TRANSCRIPT

Annual Report 2010

NLB tutuNska BaNka annual report 2010 2

Contents page

Bank’s profile ...................................................................................................................................................3

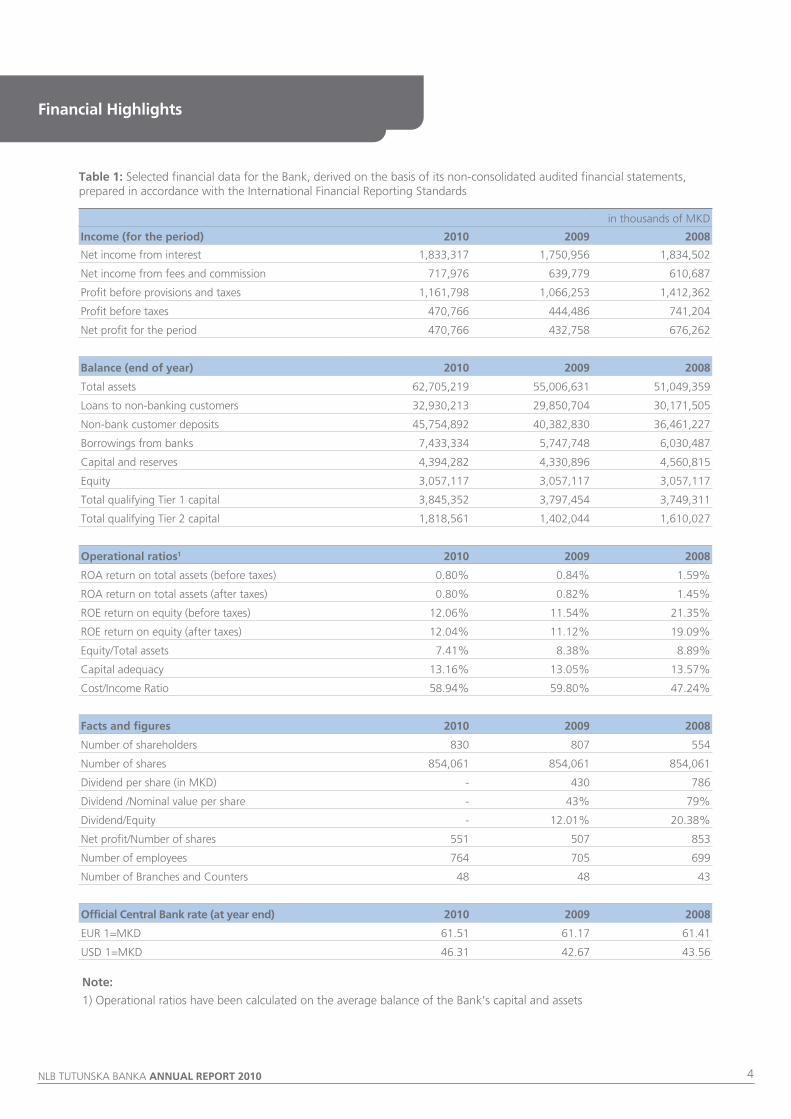

Financial Highlightstable 1: selected financial data for the Bank, derived on the basis of its non-consolidated audited financial statements, prepared in accordance with the International Financial Reporting standards ...............................4

Financial Highlights table 2: selected financial data for the Bank, derived on the basis of its non-consolidated audited financial statements, prepared in accordance with the International Financial Reporting standards.................................5

address of the President of the Management Board ........................................................................................7

Menagement structure ....................................................................................................................................9

Corporate management, share capital and ownership structure .................................................................11-13

Business Ethics ...............................................................................................................................................14

Bank’s business environment ..........................................................................................................................15

Overview of the financial results of the Bank for 2010 ............................................................................... 17-19

Retail banking ...........................................................................................................................................20-21

Net of affiliates of NLB tutunska banka aD skopje ....................................................................................22-23

Corporate banking and activities considering small and medium enterprises (sME) ....................................24-26

Financial markets ...........................................................................................................................................27

Risk management .....................................................................................................................................29-30

Information technology ..................................................................................................................................31

Human resources management ......................................................................................................................33

Work organisation .........................................................................................................................................34

Financial statements .................................................................................................36-98

NLB tutuNska BaNka annual report 2010 3

NLB tutunska banka aD skopje is one of the leading banking institutions in the Republic of Macedonia with a constant growing trend and positive results since it’s foundation until today. It is founded in 1985, and since 1993 it operates as a commercial bank that provides all financial and banking services for domestic and international customers. the bank ranks among the big banks and represents the third biggest bank in the Republic of Macedonia according to the net assets.

the Bank is a member of the NLB Group. strategic shareholders are Nova Ljubljanska Banka d.d. Ljubljana and NLB InterFinanz aG Zurich that posess 86.97% of the Bank’s total capital. the membership in the Group and the corporate brand of NLB imply a special quality of the Bank’s operation that connotes transfer of knowledge, experience and technology among the Group’s members, as well as easy access to forein markets.

NLB tutunska banka is one of the most successful banks within NLB Group. the success is a result of the Bank’s established corporate culture and tradition combined with modern information technology, professional personnel and successful market strategy, supported by the NLB brand. the Bank sees the whole public society as partly responsible for it’s success, so it pays special attention to it’s corporate social responsibility.

One of the basic strategic commitments of the Bank is to support and finance the development of small and medium enterprises as carrier of the economic development in the Republic of Macedonia, and the Bank itself is significantly involved in all financial events and promotes the Macedonian business on international markets.

the Bank pays special attention to the enrichment and adjustment of the offer of products and services according to the needs of the different market segments, as well as facilitation of the access to them by investing in the modern business network that is consisted of 48 modern affiliates organized as small banks, as well as by investments in modern access channels to the Bank and its products and services.

NLB tutunska banka together with Nova Ljubljanska Banka d.d. Ljubljana is the owner and founder of the Company for pension funds management - NLB Nov Penziski Fond aD skopje.

awards and tributes

Numerous international and national awards referring to business results, positive image and recognition value, as well as to highly developed corporate social responsibility certify the successful work of NLB tutnska banka. among them:

• the tribute for Bank of the year 2003, 2006, 2007, 2008 and 2009 in the republic of Macedonia awarded by the financial magazine „the Banker”,

• the tributes from „Finance Central Europe“ for Bank with the highest realized profit in Macedonia for 2002, 2003, 2004 and 2006 and Best bank according the return of equity (roe) for the year 2005,

• the tribute for Best investment bank in Macedonia for the year 2008 from the financial magazine „Euromoney“,

• Certificate for good corporate management from transparentnost nulta korupcija for 2007 and 2008,

• tributes from Deutsche Bank London for outstanding quality of Euro sWIFt payments to Deutsche Bank for 2006, 2007, 2008 and 2009,

• tribute for superbrand of Macedonia for 2009,

• award for Development of the philantrophy in the Republic of Macedonia for 2008, and

• award from the Financial Markets association of the Republic of Macedonia - aCI Macedonia for the most active participant in the inter-bank trade in the country.

Bank’s mission

Our goal is to become one of the leading financial institutions in the country.

to provide a higher level of service quality, a modern offer of new products and to develop the Bank’s tradition.

to draw profit through efficiency and cost-effectiveness of our activities.

Bank’s profile

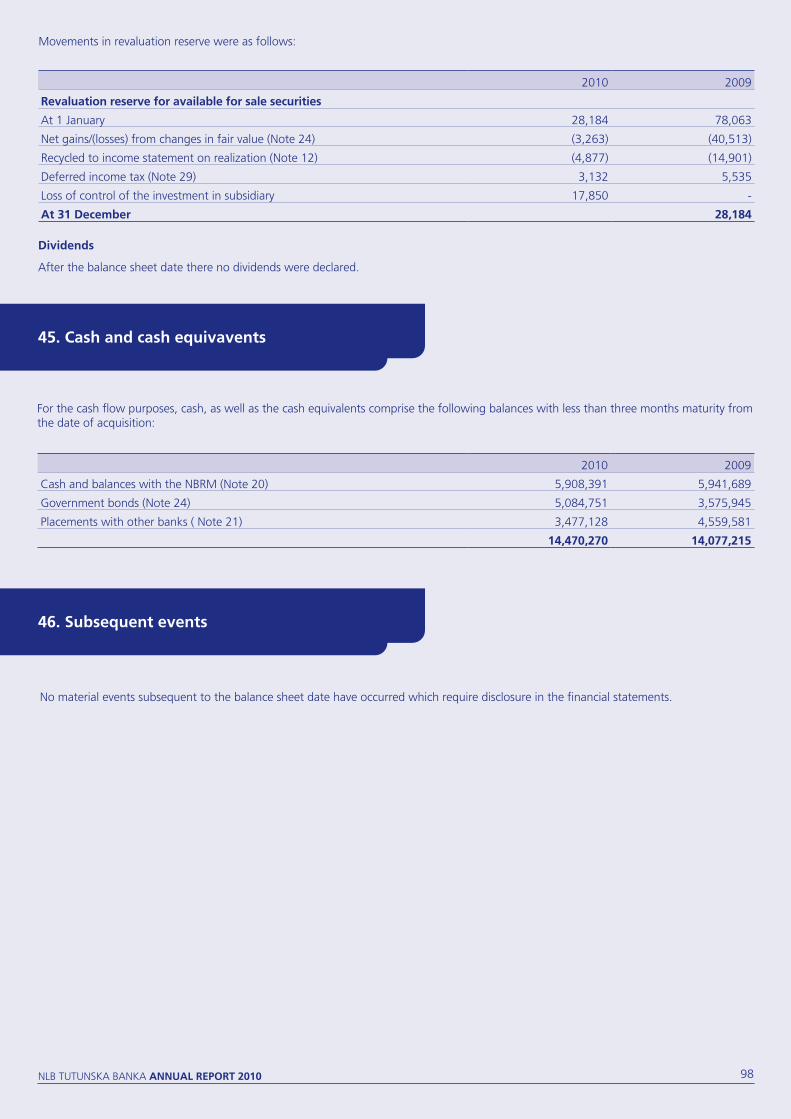

NLB tutuNska BaNka annual report 2010 4

in thousands of MkD

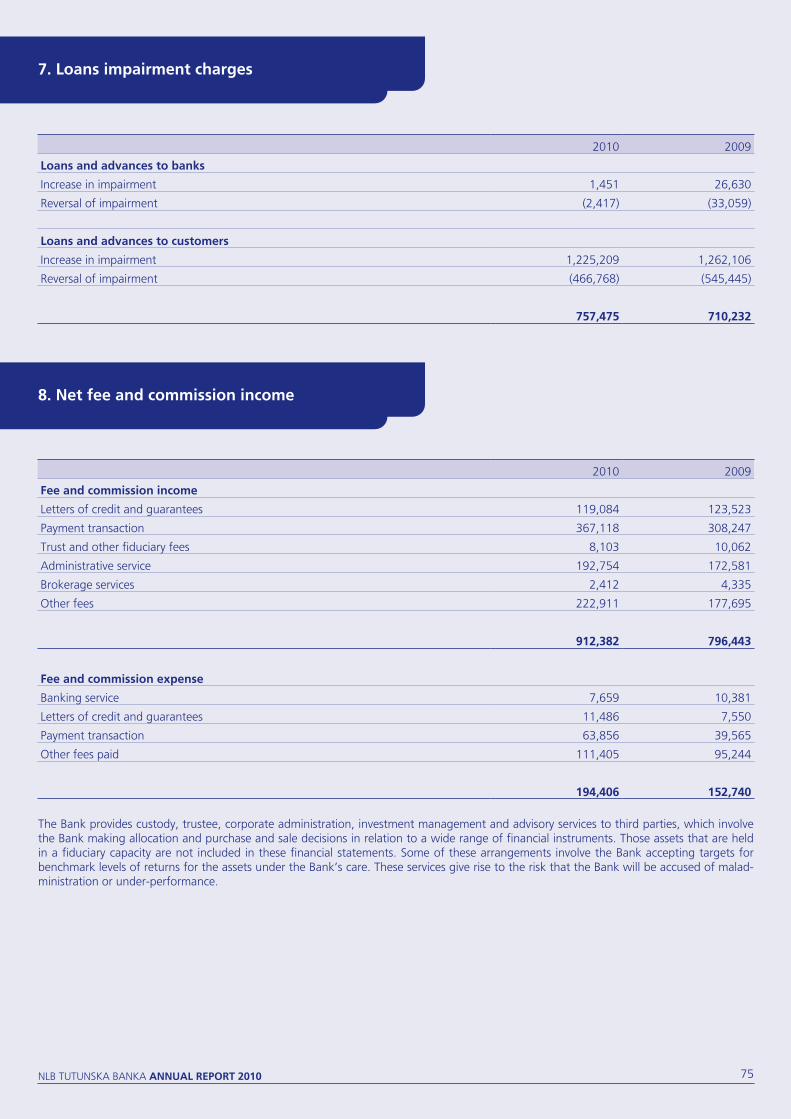

Income (for the period) 2010 2009 2008

Net income from interest 1,833,317 1,750,956 1,834,502

Net income from fees and commission 717,976 639,779 610,687

Profit before provisions and taxes 1,161,798 1,066,253 1,412,362

Profit before taxes 470,766 444,486 741,204

Net profit for the period 470,766 432,758 676,262

Balance (end of year) 2010 2009 2008

total assets 62,705,219 55,006,631 51,049,359

Loans to non-banking customers 32,930,213 29,850,704 30,171,505

Non-bank customer deposits 45,754,892 40,382,830 36,461,227

Borrowings from banks 7,433,334 5,747,748 6,030,487

Capital and reserves 4,394,282 4,330,896 4,560,815

Equity 3,057,117 3,057,117 3,057,117

total qualifying tier 1 capital 3,845,352 3,797,454 3,749,311

total qualifying tier 2 capital 1,818,561 1,402,044 1,610,027

operational ratios1 2010 2009 2008

ROa return on total assets (before taxes) 0.80% 0.84% 1.59%

ROa return on total assets (after taxes) 0.80% 0.82% 1.45%

ROE return on equity (before taxes) 12.06% 11.54% 21.35%

ROE return on equity (after taxes) 12.04% 11.12% 19.09%

Equity/total assets 7.41% 8.38% 8.89%

Capital adequacy 13.16% 13.05% 13.57%

Cost/Income Ratio 58.94% 59.80% 47.24%

Facts and figures 2010 2009 2008

Number of shareholders 830 807 554

Number of shares 854,061 854,061 854,061

Dividend per share (in MkD) - 430 786

Dividend /Nominal value per share - 43% 79%

Dividend/Equity - 12.01% 20.38%

Net profit/Number of shares 551 507 853

Number of employees 764 705 699

Number of Branches and Counters 48 48 43

official Central Bank rate (at year end) 2010 2009 2008

EuR 1=MkD 61.51 61.17 61.41

usD 1=MkD 46.31 42.67 43.56

Financial Highlights

table 1: selected financial data for the Bank, derived on the basis of its non-consolidated audited financial statements, prepared in accordance with the International Financial Reporting standards

note:

1) Operational ratios have been calculated on the average balance of the Bank’s capital and assets

NLB tutuNska BaNka annual report 2010 5

in thousands of MkD

Income (for the period) 2010 2009 20081

Net income from interest - 1,757,634 1,840,665

Net income from fees and commission - 643,703 622,005

Profit before provisions and taxes - 1,098,444 1,463,232

Profit before taxes - 468,380 792,074

Net profit for the period - 456,466 725,525

Balance (end of year) 2009 20081

total assets - 55,128,083 51,182,889

Loans to non-banking customers - 29,850,704 30,171,505

Non-bank customer deposits - 40,388,538 36,469,855

Borrowings from banks - 5,747,748 6,030,487

Capital and reserves - 4,504,722 4,721,245

operational ratios2 2009 20081

ROa return on total assets (before taxes) - 0.88% 1.69%

ROa return on total assets (after taxes) - 0.86% 1.55%

ROE return on equity (before taxes) - 11.76% 21.88%

ROE return on equity (after taxes) - 11.35% 19.65%

Facts and figures 2010 2009 20081

Number of employees 764 712 707

Number of Branches and counters 48 48 43

official Central Bank rate (at year end) 2010 2009 20081

EuR 1=MkD 61.51 61.17 61.41

usD 1=MkD 46.31 42.67 43.56

Financial Highlights

table 2: selected financial data for the Bank, derived on the basis of its non-consolidated audited financial statements, prepared in accordance with the International Financial Reporting standards

note:

1) according to the application of IFRs in Macedonia, certain items of the income statement were reconciled

2) Operational ratios have been calculated on the average balance of the Bank’s capital and assets

Vision

NLB tutuNska BaNka annual report 2010 7

Dear shareholders,

the recovery of the European economies in the last year had a positive impact on the real sector in the Republic of Macedonia. the increased activities of the most significant trade partners initiated an upward increase of the Macedonian export, and an additional export stimulus was also the rise of the metal prices, which in total reflected positively on the payment balance, the foreign exchange reserves and the whole macroeconomic stability. the realized increase of the GDP by 0.7% in 2010 raises hope for finalization of the last recession stages, but the risks of illiquidity are still present in the real sector. the equilibration of the monetary and fiscal policies enabled partial relaxation of the monetary policy through descent of the bills interest rate from 8.5% to 4.0%. the banking sector was stable all the year round and had a high liquidity. the money supply rose by 12.2%, while the rise of the total deposits amounts 13.7% (2009: 7.1%). the credit growth amounts 7.1%, so it is double as high as in 2009 (3.5%). Despite the decrease of the macroeconomic risks, the NBRM kept the rate of the obligatory reserve in Denar at 10%, in Denar with currency clause at 20% and in foreign currency at 13%. the total assets rose by 14%, while the net profit rose by 37% compared to the previous year, which shows that the Bank had successfully softened the economic crisis blow. the capital adequacy amounts 16%.

Last year was successful for the Bank. as in the previous year, the primary commitments were strengthening of the deposit basis, maintenance of the structural liquidity and keeping the credit portfolio quality. Reservations in a total amount of 11.2 million EuR were sorted out, which enabled coverage of the reserves portfolio of 10.1%. the net profit amounts 7.4 million EuR with a return on capital rate of 11.3%. the guarantee capital of the Bank reached 90.5 million EuR while the capital adequacy amounts 13.16%.

the balance sheet total was increased by 14%, and the number of customers rose by 12%. the total deposit basis rose by 12.3%. On the other hand, because of the improvement of the economic conditions in the second half of the year, the credit activity of the Bank rose by 10.1%, while the time structure of the loans changed in direction of increase of the long-term loans portion.

On the field of Corporate Banking, in direction of stimulation of the new investment cycle at the enterprises, the Bank lowered the interest rates for loans to legal entities. In addition to the current credit lines, new credit lines from the International Finance Corporation (IFC) and new credit products from the Macedonian Enterprice Development Foundation (MEDF) were ensured, namely: loans for financing of information and communication technologies, loans for financing of tourism, loans for organic production and loans to business-beginners, as well as new funds from the program of the European Investment Bank (EIB) via the Macedonian Bank for Development Promotion. additionally hereto, were issued new guarantees worth 141.5 million EuR for export arrangements and participation of domestic enterprises in tendering procedures for domestic and international projects. the deposits from legal entities decreased by 6.8% as a reflection of the prolonged liquidity problems the economy and the public society had to deal with.

On the field of Retail Banking, it was recorded an increase of the civil crediting by 13.2%, in line with which new credit products were promoted, and relaxation of the credit approval conditions and decrease of the interest rates of credits

address of the president of the Management Board

NLB tutuNska BaNka annual report 2010 8

and deposits were realized, with the goal to decrease the general level of the interest rates and intensify the crediting. Including the successful realization of the promotional campaigns for the NLB super deposit, the total civil deposits at the Bank rose by 27.1%.Regarding the electronic services of the Bank, new functionalities for bank cards and e-banking for individuals were introduced, and also more significant investments for increase of their security were realized.

Furthermore, under conditions of interest margine reduction and limited possibilities for a bigger market expansion, the Bank realized activities for rationalization of the operational costs and increase of the cost-effectiveness as a part of the adopted NLB Group strategy, that in line with the improvement of the operational efficiency will lead to continuous profitability increase.

the successful operations of the Bank in 2010 are supported by a strengthened market position through a bigger market share in several segments: we realized a market share of 18.9% on the field of civil crediting, a market share of 20.1% on the field of savings, on the field of bank cards operations of 25.8% and a record-breaking share of the foreign exchange market of 26.7%.

Dear shareholders,

Finally, I would conclude that last year was a year of challenges, but also a successful year, in which we exceed the figure of 1 billion EuR balance sheet total, although the negative effects of the economic recession were still present. Our priorities in the future time period are to ensure stable long-term financing sources, to keep the high liquidity of the Bank, to maintain the credit portfolio quality, to offer customer services with higher quality than the competition does, to improve the operative efficiency and to harmonize with the NLB Group.

Yours truly,

Gjorgji Janchevski President of the Management Board

NLB tutuNska BaNka annual report 2010 9

Menagement structure

Menagement board

Gjorgji Janchevski - President of the Management Board

ljube rajevski - Member of the Management Board

tome perinski - Member of the Management Board

Councelors of the management board

Dushan Spikovski, Counselor of the Management Board on the field cash operations and depot radovan trpkoski, Counselor of the Management Board on the field of investments, purchasing and general activities trajko Mateski, Counselor of the Management Board for Bank’s security systems management Dragi tasevski, Counselor of the Management Board for human resources management and cost management of the Bank

Internal revision division

liljana nastoska, Manager

Coordination centre for cooperation with members of the nlB group and their customers

Damir Kuder, Manager

legal, compliance and problematic loans division

nadica Ceneva, Manager

risk management division

Bogoja Kitanchev, Manager

logistics division

Jordanka Grujoska, Manager

Financial markets and means management business division

Stojna Stojkoska, Manager

Corporate banking business division

Strasho pupulkovski, Manager

Business network - business division

antonio argir, Manager

Sales logistics division

Slagjana Beleva, Manager

Cash operations and depot division

Dragan panovski, Manager

Information technology division

aleksandar Misovski, Manager

payment systems division

Igor Davchevski, Manager

Corporate management

NLB tutuNska BaNka annual report 2010 11

Corporate management

the corporate management in a bank as a sum of mutual relations between the Management Board, the supervisory Board, other individuals with special rights and responsibilities, who have a managerial position in the Bank, the Bank’s shareholders and other interested subjects, is based on the principles of responsibility, transparency and control at decision making, in the daily business and at reporting about the situations in the Bank.

the Bank has a clear organisational structure, which precisely defines the rights and responisibilities of the members of the supervisory and management bodies and the Bank’s employees, as well as the control and check structure during the daily realization of the tasks.

the corporate management of the Bank is represented by the bodies with a key role in the Bank’s efficient operating:

• Shareholders assembly. In 2010 was held one session.

the annual shareholders assembly was held on 22.4.2010 and besides the regular items about the assembly’s work, was adopted a Decision for amendment and supplement of the Rules on Working Procedures of the shareholders assembly of NLB tutunska banka aD skopje with the goal of adjustment to the statute of NLB tutunska banka aD skopje.

• Supervisory Board of the Bank. the supervisory Board held 12 sessions in 2010. In 2010 the supervisory Board was active in a structure of six members, in particular:

1. Matej narat - President of the supervisory Board and assistant of the Management of NLB d.d. Ljubljana, Master of Economics;

2. alojz Jamnik - Deputy President of the supervisory Board and assistant of the Management of NLB d.d. Ljubljana, Bachelor of Economics;

3. Janko Gedirh - Member of the supervisory Board, Bachelor of Law;

4. andrej Hazabent - Member of the supervisory Board, Master of Economics;

5. abdulmenaf Bedjeti - Independent Member of the supervisory Board and Prorector of the south East European university, tetovo, Doctor of Economics;

6. Borislav atanasovski - Independent Member of the supervisory Board and Manager of Revision, evaluation and financial consulting - B I LJ BORO I LJuPCHO DOO skopje, Bachelor of Economics.

• Management Board. the Management Board held 43 regular sessions in 2010. until 2.6.2010 the Management Board was active in a structure of three members, in particular:

1. Gjorgji Janchevski, President of the Management Board;

2. ljube rajevski, Member of the Management Board;

3. tome perinski, Member of the Management Board.

Over the year the number of members was downsized to two members representing the legal minimum.

• auditing Board. the auditing Board held six sessions in 2010. the Board is consisted of five members, in particular:

1. alojz Jamnik - President of the auditing Board and assistant of the Management of NLB d.d. Ljubljana

Corporate management, share capital and ownership structure

NLB tutuNska BaNka annual report 2010 12

(Member of the supervisory Board);

2. Matej narat - Member of the auditing Board and assistant of the Management of NLB d.d. Ljubljana (Member of the supervisory Board);

3. Janko Gedrih - Member of the auditing Board (Member of the supervisory Board);

4. abdulmenaf Bedjeti - Member of the auditing Board and Prorector of the south East European university, tetovo (Member of the supervisory Board) and

5. Stojan Jordanov - Member of the auditing Board, Manager of the Company for auditing Censum DOOEL skopje, Bachelor of Economics and authorized auditer.

• Information System Supervisory Board. Founded based on the regulations of the NBRM, the Basel Principles and the international standards for information system safety. the members of the Information system supervisory Board are chosen from the individuals with special rights and responsibilities including the person responsible for information system safety. President of the Information system supervisory Board is the President of the Management Board, Mr. Gjorgji Janchevski.

Because of the higher efficiency of the daily management, the Management Board of the Bank operated through following Boards, by which individual fields of the Bank’s operations are monitored more closely, in particular:

• Development Board - members of the Development Board are the members of the Management Board, the Manager of the Coordination Center for Cooperation with Members of the NLB Group and their Customers and the Manager of the Logistics Division of the Bank. the President of the Development Board is the President of the Management Board, Mr. Gjorgji Janchevski.

• risk Management Board - the members of the Risk Manangement Board are chosen from the individuals with special rights and responsibilities employed in the Bank. the President of the Risk Management Board is the President of the Management Board, Mr. Gjorgji Janchevski.

• Management Board for assets and liabilities - the members of the Management Board for assets and Liabilities are chosen from the individuals with special rights and responsibilities employed in the Bank. Member of the Board is also a representative of NLB d.d. - Ljubljana. the President of the Management Board for assets and Liabilities is the President of the Management Board, Mr. Gjorgji Janchevski.

Corporate Management Code

the Corporate Management Code in the Bank defines the management and leading standards of the Bank’s bodies. Respecting the standards, the Bank has determined a transparent and understandable manangement system that increases the trust level of domestic and international investors, employees and public.

the Principles of good corporate management are completely incorporated in the Corporate Management Code, meaning:

• the members of the supervisory Board have appropriate qualifications, understand their role in the corporate management of the Bank and are capable of realistic evaluation of the Bank’s work;

• the management and supervision bodies of the Bank determine and monitor the fulfillment of the strategic goals and corporate values of the Bank and inform all their employees about them;

• the supervisory and management bodies determine appropriately defined responsibilities and the reporting strucute among all employees in the Bank;

• the supervisory Board of the Bank has to be sure that the Management Board and other individuals with special rights and responsibilities realise appropriate supervision and monitoring of the Bank’s work;

• the supervisory Board, the Management Board and other individuals with special rights and responsibilities that hold a managerial position in the Bank, shall efficiently make use of the Bank’s Internal audit Division, as well as the audit association;

• the supervisory Board and the Management Board should be sure that the awarding policy and the appropriate procedures are in accordance with the corporate culture, the long-term goals and the strategy, as wall as with the Bank’s monitoring environment;

• Provision of transparency of the coprorative management.

NLB tutuNska BaNka annual report 2010 13

the Corporate Management Code is evaluated once a year on the Bank’s shareholders assembly.

Internal audit

the internal audit of NLB tutunska banka aD skopje is organized as a separate organizational part, functionally and organizationally separated from the other parts of the Bank, directly responsible to the supervisory Board. In 2010, the Department for internal audit realized 15 functional checks, as well as 13 unannounced checks of affiliates. Besides regular checks, in 2010 were also realized two irregular audits.

Corporate social responsibility

the care for the public good represents one of the highest ranking priorities of the Bank’s value system and an integral part of the strategy, because of which the Bank pays special attention to the social responsibility and interest protection of all interested parties. By supporting projects of humanitarian character and on the field of culture, sport, science, education and ecology, kids and youngsters, the Bank makes efforts to contribute for improvement and modernization of the whole life quality of infividuals, families, institutions and organizations of the environment it is active in.

Sponsorships and donations

In 2010, the Bank sponsored following projects: We travel to Europe - organized by the civil organization MOst; shar Planina ski Cup - Popova shapka - tetovo; Macedonian Opera and Ballet; Festival Ohrid summer - Ohrid 2010; Band “synthesis“; NLB League (Basketball); Project for construction of bus stations in the Municipality of kichevo; Municipal project for beautification of the City of Prilep; ZOO - skopje. Following donations were made: computer equipment for the P.H.I. Clinical Centre tetovo; „First donator auction of chocolate“ - for the Children’s Clinic for pulmonary diseases - kozle.

NLB tutuNska BaNka annual report 2010 14

the Bank supports organizations and initicatives that campaign for equal treatment, business ethics and humanism, that adds value to the society and contributes to strengthening of the public tissue and social cohesion.

the Bank accepts completely and applies in its work the International Declaration on Human Rights, the Declaration of Ecology and the International treaties regarding social care and ecology.

prevention of money laundering

the Bank has adopted and applies consistently the Programm for Prevention of Money Laundering and internal acts that regulate this field. Furthermore, it cooperates with responsible institutions and correspondent banks. the Bank implemented completely all instruments that arise from the legal regulations referring to efficient detection and pre-vention of money laundering.

Share capital and ownership structure

the share capital of the Bank on 31.12.2010 is consisted from 854,061 ordinary shares with nominal value of 1,000 MkD per share or 854,061,000 MkD in total. the shares are registered and recorded at the Central securities Deposi-tary of the Republic of Macedonia.

the ordinary shares give the owners the right on payout of dividend and voting right on the shareholders assembly session. One vote in the Bank’s assembly is an equivalent to one ordinary share.

the Bank hasn’t realized an acquisition of own shares in 2010.

Inclusive 31.12.2010, the number of shareholders of the Bank is 830 (2009: 807) that represents an increase by 3% compared to the previous year. 688 of them are individuals (2009: 667) and 142 are legal entities (2009: 140).

Based on the agreement on transfer of the Voting Rights upon shares and annex 1, 2, 3, 4 and 5 to the agreement concluded between NLB InterFinanz aG Zurich and Nova Ljubljanska Banka d.d. Ljubljana, the voting rights of the shareholder NLB InterFinanz aG Zurich (26.71%) based on the shares of NLB tutunska banka, are transfered to Nova Ljubljanska Banka d.d. Ljubljana. according hereto, the participation of Nova Ljubljanska Banka d.d. Ljubljana in the total voting rights amounts 86.97% on 31.12.2010.

In May 2010, a dividend from the profit for 2009 in a total amount of 367,246,230 MkD was paid to the shareholders, which represents 92% of the realized net profit for 2009. the dividend per share amounted 430 MkD or 43% of the shares nominal value.

the Bank is registered with special reporting responsibilities in the Registry of Joint stock Companies, which is a part of the security and Exchange Commission of the Republic of Macedonia. Pursuant to the Law on securities and the bylaws, the Bank regulary submits to the Commission information about its activities, the members of the manage-ment bodies, the management and the legal relations with third parties and events of interest for the Bank’s operation.

Business ethics

Shareholders with over 5% participation on 31.12.2010% participation according

the amount of ordinary shares

Nova Ljubljanska Banka d.d. Ljubljana 60.26

NLB InterFinanz aG Zurich 26.71

NLB tutuNska BaNka annual report 2010 15

In 2010 the economic condition in Macedonia improved. although the healing process was not as fast as expected, the improved external conditions, the positive trend in the construction industry and the credit support of the banking sector enabled a GDP rise of 0.7% compared to the previous year. But, besides the high export rise by 32.4% and the final consumption rise by 0.3%, the industrial production recorded a descent of 4.3% p.a. (2009: -7.7%). the current account deficite was significantely decreased under the impact of the stable transfers from abroad and the positive flows of the external trade exchange, while the lack of capital inflows is still representing one of the main problems for more significant growth of the Macedonian economy.

the average inflation rate in 2010 amounts 1.6%. In this year the pricing level was stable, in a frame from 0.7% to 1.6%, and the biggest growth was recorded at the regulatory feedstock energy prices. Regarding the internal turnover, the wholesale increased in the fourth quarter by 10.4%, while the retail trade increased by 5.8% in comparison with the same time period in 2009. the unemployment, although still high, declined to 30.9%. the real net salaries were 1.4% higher, which had an impact on saving the net available civil income.

In the beginning of 2010, the budget of the central government was not balanced, as a result of the lower income from Vat and contributions (Pension and Disability Insurance Fund of Macedonia), because of what the state ran up depts on the domestic market by issuing of state bonds. On the end of the year the deficite amounts 171.4 million Euros (2009: 178.1 million EuR or 2.8% of GDP). at the end of the year the Government signed an agreement on Precaution Credit Line Facility with the IMF with an amount of 480 million Euros, intended for dealing with potential risks of the budgetary and payment-balance illiquidity.

the total external trade exchange in 2010 increased by 22.2%, in line with a higher rise of the export (32.4%) as of the import (16.7%). the rate of the coverage of the import by export is 60.6% (2009: 53.4%). this resulted with a descent of the external trade deficite on annual basis by 1.3% (calculated at market prices in Euro) and it equals 1,618.1 million Euros (2009: 1,640.1 million Euros) while the payment balance deficite on the end of the year amounts 191.1 million Euros.

the exchange rate of the Denar was stable over the year, without significant oscillations, which enabled keeping the inflation level low. the initiation of the new calculation model for the foreign exchange rate of the Denar via quotation of exchange rates of domestic banks (market makers), resulted with a small depreciation (0.5%) of the Macedonian Denar (MkD) compared to the Euro, by which the exchange rate displayed the real market price of the domestic currency. Over the year, NBRM appeared on the foreign currency market as a net buyer of foreign currencies that enabled an increase of the foreign exchange reserves level to 1,14.51 million Euros (+117 million Euros or + 7.3%).

the liquidity of the banking sector in the Republic of Macedonia remained strong, mainly supported by the stabile private saving. On the end of 2010, the money mass rose by 12.2% compared to the previous year, while the increase of the total deposits equals 13.7% (2009: 7.1%). the credit rise amounts 7.1% what’s double as high as in 2009 (3.5%). Besides the decrease of the macroeconomic risks, the NBRM kept the rate of obligatory reserve in Denar at 10%, in Denar with clause at 20% and in foreign currencies at 13%. In the same time, in direction of monetary policy relaxation and stimulation of crediting activities, NBRM decreased the interest rate of the central bank bills several times, which rate was lowered from 8.5% in 2009 at 4.0% at the end of 2010. In the same time, the referent interest rate for Denar decreased at 5% (2009: 9%).

the total net external debt of the Republic of Macedonia on 31.12.2010 amounted 1,417.79 million Euros (2009: 1,281.86 million Euros). In the following period the main risks of the economic growth of the Republic of Macedonia arise from the incertainity of the economies in the countries, which are trade partners and of the international financial markets, and the dealing with possible effects from them will very much depend on the coordination of the economic, fiscal and monetary measures of the Government and the NBRM and their on-time adjustment. this coordinated economic policy will have to stimulate the external stability and in the same time to stimulate the domestic investments via tax, legal, regulatory and political relaxation measures.

Bank’s business environment

Financial results

NLB tutuNska BaNka annual report 2010 17

overwiev of the financial results of the Bank for 2010

In 2010 the Bank realized the planned goals defined in the Business Policy for 2010, the strategic Directions for Development and Operation of the Bank for 2010-2012 and the Directions for 2010 defined by the NLB Group. Over the year, because of the change of the economic conditions under which the Bank was operating and based on the realized projections, it accordingly adjusted the current activities and the financial policy. under the conditions of prolonged recession in the first half of the year and relatively healing in the second half, accompanied by the relaxed monetary policy, the Bank kept and improved its market position in different segmets, securing at the same time a high structural liquidity, stable financing sources, high portfolio quality and high profitability.

record of success

the net profit for 2010 amounts 470.8 million MkD and is 8.8 % higher than last year. Over the year 689.0 million MkD were sorted out for reservation for risky loans, which is 10.8% more than in 2009 and 37.8% more than the planned amount, according to the assets quality and the directions of the NLB Group regarding the risk management strategy. the coverage of the portfolio by reservations amounts 10.1% (2009: 9.4%).

the Return of Equity (ROE) amounts 12.0% (2009: 11.12%).

the net profit per share amounts 551 MkD (2009: 507).

net profit (000) MKD return of equity roe and per share profit

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

432,758432,758 470,766470,766

2008 2009 2010

676,262676,262

0

100

200

300

400

500

600

700

800

900

0%

5%

10%

15%

20%

25%

11.1%11.1% 12.0%12.0%

2008 2009 2010

19.1%19.1%

Profit per share (in denars)

tne net interest earnings amount 1,833.3 million MkD or 4.7% more than in 2009. the earnings from interest are higher as a result of investments in securities and the credit portfolio rise of legal entities. at the end of 2010, the average net interest margine was 3.11% (2009: 3.30%). the average net interest assets were increased by 12.8% in comparison to 2009.

NLB tutuNska BaNka annual report 2010 18

Interest assets and liabilities

net balance sum (000) MKDDeposits of the non-financial sector

(000) MKD

the net non-interest earnings amount 885.9 million MkD or 1.7% less than last year, wherefrom 81.0% represent net earning from commission.

the net earnings from commission amount 718.00 million MkD, which is 12.2 % more than in 2009. the earnings from dividend upon capital investments in financial and non-financial legal entities, amount 2.6 million MkD, which is 33.0 % less than in 2009. the Bank realized net positive exchange differences of 105.6 million MkD or 34.9% less than in 2009, while the net earnings from securities amount 81.4 million MkD.

the expenditures in the general bussiness in 2010 amount 1,647.9 million MkD, in doing so the spending was done extraordinary racional. the participation of the costs in the business earnings in 2010 amounts 58.94%, while the participation of the operative costs in the total assets of the Bank amounts 2.80% (2009: 2.99%).

Balance sheet

the Bank realized a net balance sum of 62,705 million MkD that shows an annual rise of 14.0% and a market share of 20.5%. the rise was mostly supported by the increase of the civil deposits. the total deposits from the non-financial sector rose by 13.3% and amounted 45,754.90 million MkD on 31.12.2010.

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

55,006,63155,006,63162,705,21962,705,219

2008 2009 2010

51,049,35951,049,359

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

40,382,83040,382,83045,754,89245,754,892

2008 2009 2010

36,461,22736,461,227

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2008 2009 2010

-

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

average net interest-bearing assets (in 000 denars)

average net interest-bearing liabilities (in 000 denars)

average net interest margin in %

NLB tutuNska BaNka annual report 2010 19

the liabilities upon loans increased by 36.5% compared to 2009 as a result of the use of funds from new and present credit lines.

the total Bank’s capital amounts 4,394.3 million MkD and represents 7% of the Bank’s total sources.

In 2010 the Bank increased the dynamics of crediting of the non-banking sector which resulted with increase of the credit portfolio of the non-financial sector by 10.3%, while the credit time structure changed in advantage of the long-term credits which participated in the total credit sum with 67.3% in 2010 (2009: 61.2%).

a part of the sources of funds was invested in short-term securities and short-term deposits in banks, by which the participation of these highly liquid instruments in the Bank’s assets amounts 26.8% (2009: 24.5%)

Regarding the currency structure, 63.7% of the financial sources and 59.33% of the financial investments are in foreign currency and in Denars with currency clause.

NLB tutuNska BaNka annual report 2010 20

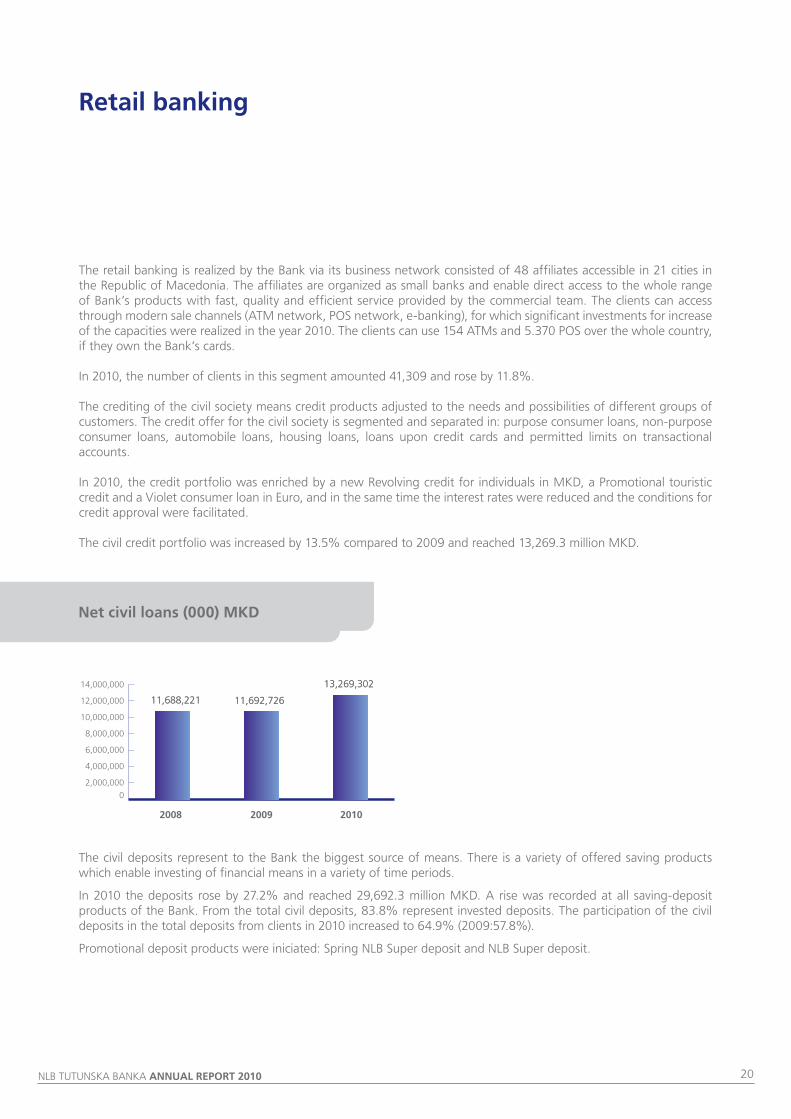

the retail banking is realized by the Bank via its business network consisted of 48 affiliates accessible in 21 cities in the Republic of Macedonia. the affiliates are organized as small banks and enable direct access to the whole range of Bank’s products with fast, quality and efficient service provided by the commercial team. the clients can access through modern sale channels (atM network, POs network, e-banking), for which significant investments for increase of the capacities were realized in the year 2010. the clients can use 154 atMs and 5.370 POs over the whole country, if they own the Bank’s cards.

In 2010, the number of clients in this segment amounted 41,309 and rose by 11.8%.

the crediting of the civil society means credit products adjusted to the needs and possibilities of different groups of customers. the credit offer for the civil society is segmented and separated in: purpose consumer loans, non-purpose consumer loans, automobile loans, housing loans, loans upon credit cards and permitted limits on transactional accounts.

In 2010, the credit portfolio was enriched by a new Revolving credit for individuals in MkD, a Promotional touristic credit and a Violet consumer loan in Euro, and in the same time the interest rates were reduced and the conditions for credit approval were facilitated.

the civil credit portfolio was increased by 13.5% compared to 2009 and reached 13,269.3 million MkD.

retail banking

net civil loans (000) MKD

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

11,692,72611,692,726

13,269,30213,269,302

2008 2009 2010

11,688,22111,688,221

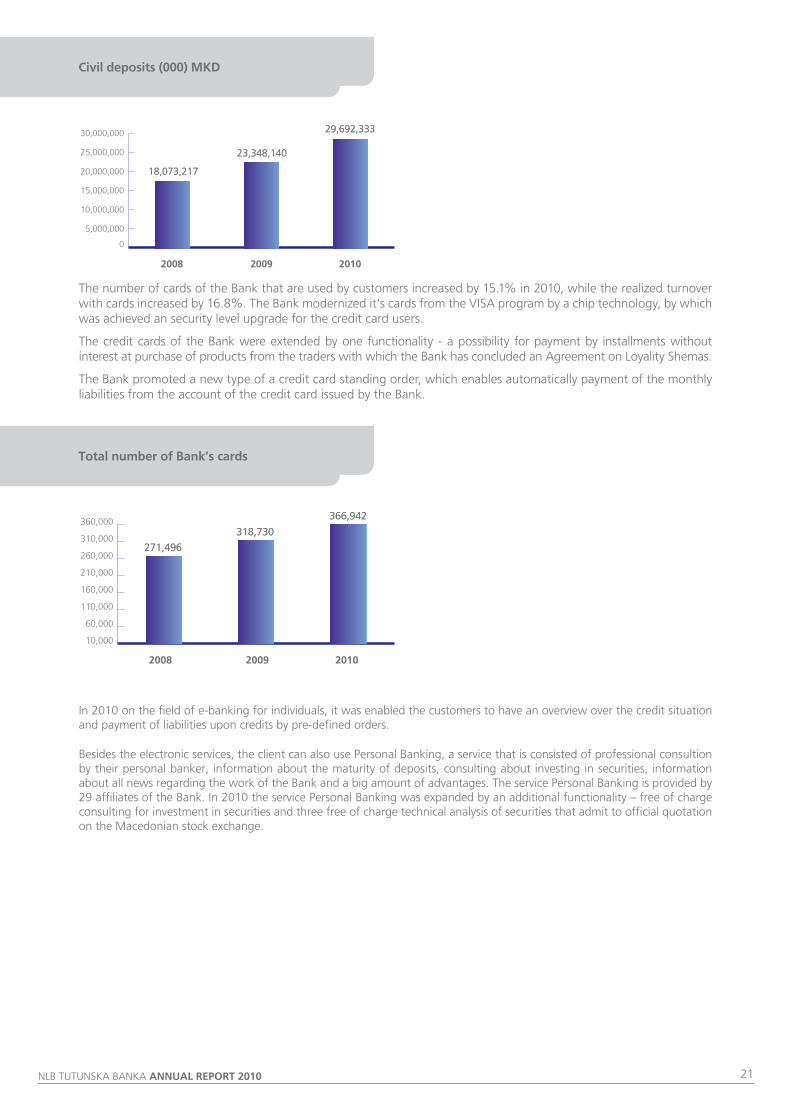

the civil deposits represent to the Bank the biggest source of means. there is a variety of offered saving products which enable investing of financial means in a variety of time periods.

In 2010 the deposits rose by 27.2% and reached 29,692.3 million MkD. a rise was recorded at all saving-deposit products of the Bank. From the total civil deposits, 83.8% represent invested deposits. the participation of the civil deposits in the total deposits from clients in 2010 increased to 64.9% (2009:57.8%).

Promotional deposit products were iniciated: spring NLB super deposit and NLB super deposit.

NLB tutuNska BaNka annual report 2010 21

Civil deposits (000) MKD

total number of Bank’s cards

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

23,348,14023,348,140

29,692,33329,692,333

2008 2009 2010

18,073,21718,073,217

10,000

60,000

110,000

160,000

210,000

260,000

310,000

360,000318,730318,730

366,942366,942

2008 2009 2010

271,496271,496

the number of cards of the Bank that are used by customers increased by 15.1% in 2010, while the realized turnover with cards increased by 16.8%. the Bank modernized it’s cards from the VIsa program by a chip technology, by which was achieved an security level upgrade for the credit card users.

the credit cards of the Bank were extended by one functionality - a possibility for payment by installments without interest at purchase of products from the traders with which the Bank has concluded an agreement on Loyality shemas.

the Bank promoted a new type of a credit card standing order, which enables automatically payment of the monthly liabilities from the account of the credit card issued by the Bank.

In 2010 on the field of e-banking for individuals, it was enabled the customers to have an overview over the credit situation and payment of liabilities upon credits by pre-defined orders.

Besides the electronic services, the client can also use Personal Banking, a service that is consisted of professional consultion by their personal banker, information about the maturity of deposits, consulting about investing in securities, information about all news regarding the work of the Bank and a big amount of advantages. the service Personal Banking is provided by 29 affiliates of the Bank. In 2010 the service Personal Banking was expanded by an additional functionality – free of charge consulting for investment in securities and three free of charge technical analysis of securities that admit to official quotation on the Macedonian stock exchange.

NLB tutuNska BaNka annual report 2010 22

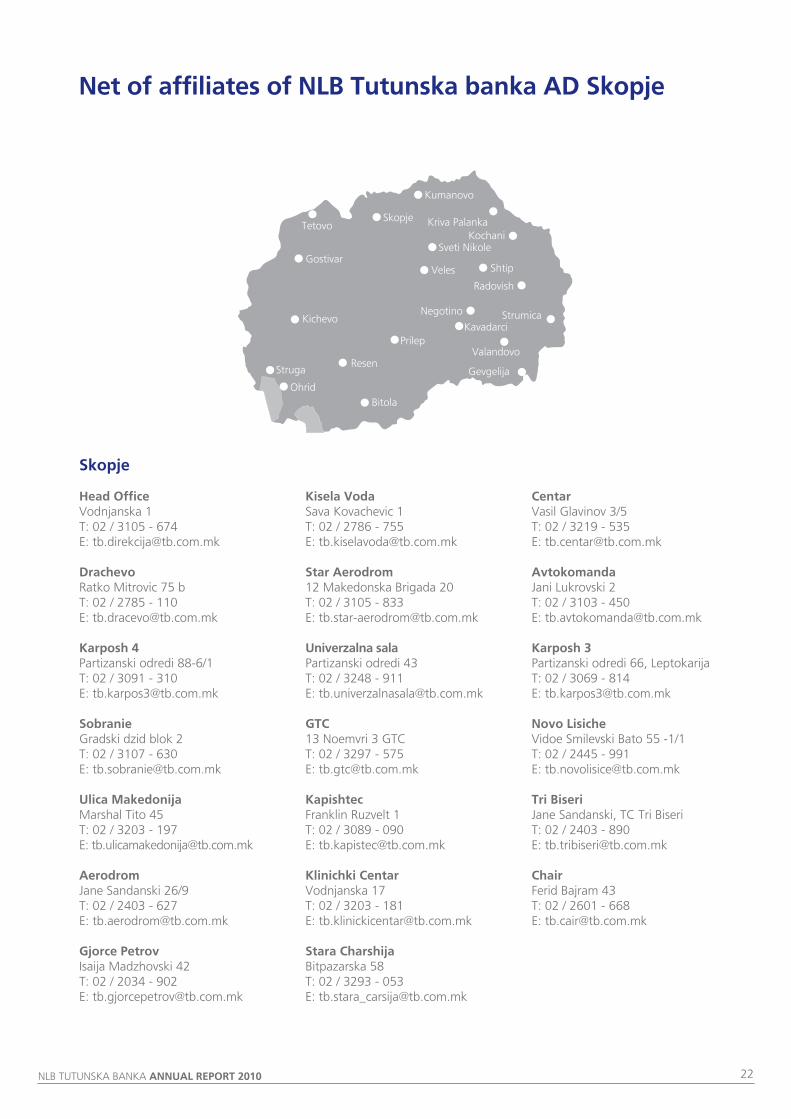

net of affiliates of nlB tutunska banka aD Skopje

Head officeVodnjanska 1Т: 02 / 3105 - 674Е: [email protected]

DrachevoRatko Mitrovic 75 bТ: 02 / 2785 - 110Е: [email protected]

Karposh 4Partizanski odredi 88-6/1Т: 02 / 3091 - 310 Е: [email protected]

SobranieGradski dzid blok 2Т: 02 / 3107 - 630Е: [email protected]

ulica MakedonijaMarshal tito 45Т: 02 / 3203 - 197Е: [email protected]

aerodromJane sandanski 26/9Т: 02 / 2403 - 627Е: [email protected]

Gjorce petrovIsaija Madzhovski 42Т: 02 / 2034 - 902Е: [email protected]

Kisela Vodasava kovachevic 1Т: 02 / 2786 - 755Е: [email protected]

Star aerodrom12 Makedonska Brigada 20Т: 02 / 3105 - 833Е: [email protected]

univerzalna salaPartizanski odredi 43Т: 02 / 3248 - 911Е: [email protected]

GtC13 Noemvri 3 GtCТ: 02 / 3297 - 575E: [email protected]

KapishtecFranklin Ruzvelt 1Т: 02 / 3089 - 090Е: [email protected]

Klinichki CentarVodnjanska 17Т: 02 / 3203 - 181Е: [email protected]

Stara CharshijaBitpazarska 58Т: 02 / 3293 - 053Е: [email protected]

CentarVasil Glavinov 3/5Т: 02 / 3219 - 535Е: [email protected]

avtokomandaJani Lukrovski 2Т: 02 / 3103 - 450Е: [email protected]

Karposh 3Partizanski odredi 66, LeptokarijaТ: 02 / 3069 - 814Е: [email protected]

novo lisicheVidoe smilevski Bato 55 -1/1Т: 02 / 2445 - 991Е: [email protected]

tri BiseriJane sandanski, tC tri BiseriТ: 02 / 2403 - 890Е: [email protected]

ChairFerid Bajram 43Т: 02 / 2601 - 668Е: [email protected]

Skopje

sveti Nikole

Resen

tetovo

Gostivar

kichevo

struga

Ohrid

Bitola

skopje

kumanovo

kriva Palankakochani

shtipVeles

Radovish

strumicaNegotino

kavadarci

Valandovo

Gevgelija

Prilep

NLB tutuNska BaNka annual report 2010 23

Bitola Josif Hristovski bbТ: 047 / 202 - 756Е: [email protected]

Bitola - Shirok SokakMarshal tito 45 , shirok sokakТ: 047 / 208 - 647Е: [email protected]

ValandovoMosha Pijade 2Т: 034 / 383 - 355Е: [email protected]

Veles Marshal tito 80Т: 043 / 221 - 282Е: [email protected]

Veles 2Goce Delchev 26Т: 043 / 214 - 450Е: [email protected]

Gevgelija Marshal tito bbТ: 034 / 215 - 441Е: [email protected]

Gevgelija 2Marshal tito zgrada 1Т: 034 / 210 – 404Е: [email protected]

GostivarBorche Jovanovski bbТ: 042 / 221 - 330Е: [email protected]

Gostivar 2Goce Delchev 104/1Т: 042 / 219 - 060Е: [email protected]

Kavadarci Ilindenska 81Т: 043 / 400 - 436Е: [email protected]

Kichevo Bul. Osloboduvanje bbТ: 045 / 224 - 460Е: [email protected]

Kochanitrgovski centar blok 17 Т: 033 / 276 - 910Е: [email protected]

Kriva palankaMarshal tito 172Т: 031 / 475 - 280Е: [email protected]

Kumanovo Ploshtad Marshal tito bbТ: 031 / 475 - 240Е: [email protected]

Kumanovo 2 Oktomvriska Revolucija 24Т: 031 / 475 - 274Е: [email protected]

negotinoMarshal tito bbТ: 043 / 364 - 010Е: [email protected]

ohridPartizanska bbТ: 046 / 251 - 360, 251 – 350Е: [email protected]

prilepGoce Delchev bbТ: 048 / 419 - 758Е: [email protected]

prilep 2Marksova 44Т: 048 / 400 - 570Е: [email protected]

radovish22 Oktomvri bbТ: 032 / 633 - 771Е: [email protected]

resen11 Oktomvri bbТ: 047 / 455 - 071Е: [email protected]

Sveti nikoleVera Ciriviri 1Т: 032 / 226 - 770Е: [email protected]

Struga Proleterski brigadi bbТ: 046 / 788 - 640Е: [email protected]

StrumicaMarshal tito bbТ: 034 / 326 - 780Е: [email protected]

Strumica 2 Blagoj Mucheto 4Т: 034 / 334 - 463Е: [email protected]

tetovo tC Merdzhan, vlez 1, kat 1Т: 044 / 356 - 705Е: [email protected]

ShtipVancho Prke bbТ: 032 / 391 - 663Е: [email protected]

NLB tutuNska BaNka annual report 2010 24

Corporate banking and activities considering small and medium enterprises (SMe)

the offer for legal entities for the big corporate customers is prepared centralized, according the model of intergrated management of customer relations, and for the small and medium enterprises (sME) - detached via the Business network.

activities related to legal entities represent the biggest part of the Bank’s activities and are the main carrier of the business growth. they include short-term crediting for current needs, short-term loans in domestic and foreign currencies for support of export arrangements, revolving loans, long-term loans in domestic and foreign currencies for financing of investment projects, loans for purchase of business premises, loans for motor vehicles for business purpose, micro-crediting, purpose loans for construction of residental and business space, commissional loans, issuance of letters of credit and guarantees, depositary activities, domestic and international payment operations and activities for transfer and keeping of funds. For financing of big projects of strategic clients, the Bank enables also a joint crediting with Nova Ljubljanska banka d.d. Ljubljana through the agreement for Risk Participation.

In 2010, the offer for the legal entities was expanded by short-term and long-term loans from the credit line of the International Financial Corporation (IFC) and new credit products from the MEDF, in particular: loans for financing of information-communication technologies, loans for tourism financing, loans for organic production and loans for business-beginners.

the crediting of micro, small and medium enterprises was executed through crediting of development projects for micro and small businesses from the credit lines aCDF, MEDF, EFsE, agricultural loans, automobile business loans and short-term loans from own sources.

On the field of depositing activities, the activities were directed to stimulation of the deposit work of the corporate clients by offering of deposit products in Denar and foreign currencies including different possibilities regarding the time frame, the interest rates and the purpose.

Investment credit activities

In 2010 were provided two new credit lines for financing of projects of micro, small and medium enterprises, in particular:

• a credit line of the International Finance Corporation in an amount of 25 million Euros;

• a credit line of the Macedonian Enterprice Development Foundation in an amount of 4.4 million Euros.

In 2010 in comparison to 2009, the investments upon loans were increased by 8.3% on the field of non-financial legal entities and amount 19,660.9 million MkD. the biggest part of the means was approved for current needs of the companies.

net loans to companies (000) MKD

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

20,000,000

18,158,97818,158,97819,660,91119,660,911

2008 2009 2010

18,483,28418,483,284

NLB tutuNska BaNka annual report 2010 25

net loans to companies according the customer’s size (000 MKD)

Regarding the activities, the loans were invested in quality projects of present and new clients in the sectors production (18.9%), trade (36.9%), real estate (11.7%), social sector (0.01%) and other activities (32.5%).

Regarding loans of legal entities, 23.2% (2009: 22.5%) represent loans to big enterprises (classified pursuant to the Company Law). the loans given to small and medium enterprises represent 76.8% (2009: 77.5%) of the total loans to legal entities.

Deposit operations

the total deposits of non-financial legal entities deposited in the Bank in 2010 amount 16,062.6 million MkD.

real estate 11,7%real estate 11,7%

social sector 0,0%social sector 0,0%

production 18,9%production 18,9%

other activities 32,5%other activities 32,5%

trade 36,9%trade 36,9%

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

4,089,4304,089,430

2009 2010

14,068,54714,068,547

4,555,2214,555,221

15,105,68915,105,689

net credits of enterprises per spheres of activities

Deposits from non-financial legal entities (000) MKD

0

5,000,000

10,000,000

15,000,000

20,000,000

17,034,69017,034,69016,062,55916,062,559

2008 2009 2010

18,388,01018,388,010

NLB tutuNska BaNka annual report 2010 26

operations regarding documents and guarantees

additional to the funds that the Bank provides for direct financing, the legal entities had access to bank guarantees and letters of credit for export arrangements, as well as assistance at participation in tendering procedures in international and domestic projects.

In 2010 were issued new quarantees in an amount of 6,206.4 million MkD and letters of credit in an amount of 2,533.5 million MkD.

Domestic and international payment operations and cash payments

On the field of the domestic payment operations, the Bank significantly raised its market share in 2010 by 20.1%, while the number of accounts in the total turnover was increased by 8.2%.

the international payment operations via the Bank decreased compared to 2009, because of the lower economic activity of the legal entities with foreign countries.

the Bank offers its clients also a service for purchase and sale, transport and provision of cash in the home country and from/to abroad for other banks and legal entities via the only cash center in Macedonia.

e-banking

On the field of e-banking, the total turnover (Denar and foreign currencies) realized in 2010 through е-banking for legal entities increased by 18.9%, and the number of clients using this service increased by 31.4% p.a.

the orders realized via e-banking participate in the total orders realized in the domestic payment operations of the Bank with 14.9% (2009: 13.0%) based on the number of orders and 21.0% (2009: 21.3%) based on the turnover.

Commissional services

the Bank manages funds on behalf and for account of legal entities and individuals, which funds are invested as loans to enterprises with no specific purpose, as loans for self-employment of individuals – a project of the Employment agency and as securities for clients. these means are operated separately of the Bank’s means.

the total commissial activities at the end of 2010 amounted 1,945.4 million MkD, that represents a descent of 28.8% compared to 2009.

NLB tutuNska BaNka annual report 2010 27

liquidity management

Over 2010 the bank managed the liquidity respecting the legal prescriptions and limitations pursuant to the Decision for Obligatory Reserve and the Decision for Bank Liguidity Risk Management prescribed by the National Bank of the Republic of Macedonia and the internal limitations and directions of the Bank and the NLB Group.

the surplus of funds was invested in central bank bonds, in state bonds and on the inter-bank deposit market. the mode, type and the instruments used for investment of the funds surplus depended on the current and planned time structure of the funds and short-term and logn-term liabilities, the general economic situation in the environment and the flows on the money and securities markets.

the interest rate of the central bank bonds in 2010 amounted 5.7% (2009: 8.5%).

In 2010 the Bank realized a total turnover on the foreign exchange market of 2,021.6 million us Dollars, via 67,761 transactions, whereby the Bank’s turnover was increased by 4.3% (2009: 1,938.0 million us Dollars). Herewith was reached a record market share of 26.68% (2009: 26.04%).

On the international foreign currency market was traded with 537.4 million Euros, via 10,909 transactions, which represents an increase of 17.3% compared to the previous year. the turnover upon the concluded forward agreements for the clients amounts 2.6 million Euros.

Broker services

In 2010 the Bank received a permit for realization of securities services by the securities and Exchange Commission of Republic of Macedonia. In total were concluded 776 brokerage agreements with domestic and foreign legal entities.

In October 2010 we received the consent by the NBRM for starting the realization of financial activities: investment consulstation, acting as patron at admitting to official quotation, realizing of transactions and activities on account of third parties needed for overtaking of joint stock companies according the Law on the takeover of Joint stock Companies.

Custody services and services of the Bank - property Guardian (Depositary bank)

since 2010, besides for non-residents, the Bank started to realize custody services for residents as well, pursuant to the Law on Foreign Currencies Operations

Over 2010, the Bank realized the services – the Bank – Property Guardian for:

• Open investment funds;

• Private investment funds;

• Open obligatory pension fund;

• Open voluntary pension fund.

Financial markets

Risk management

NLB tutuNska BaNka annual report 2010 29

the Bank applies a highly conservative policy of anticipation of operative risks, by maintenance of an efficient system of integrated risk management. this enables realization of high collection of investments, a satisfactory level of capital adequacy, protection from unpredictable events and possible non-realisation of the planned policy.

Credit risk management

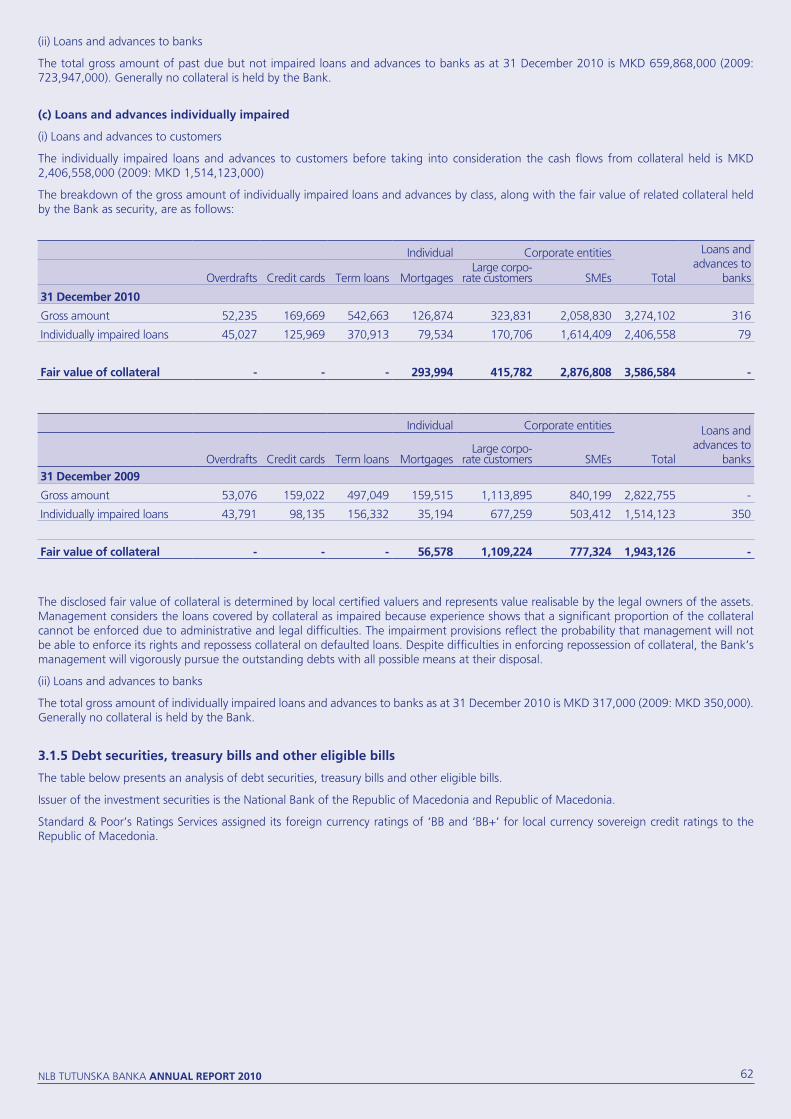

the credit risk management includes a permanent analysis of the credit portfolio of the Bank, with regards to the sectoral diversification and concentration on the portfolio, analysis and evaluation of the financial performances of the customers, monitoring of the regularity at attention of the liabilities and separation of a satisfactory level of reservations for investments.

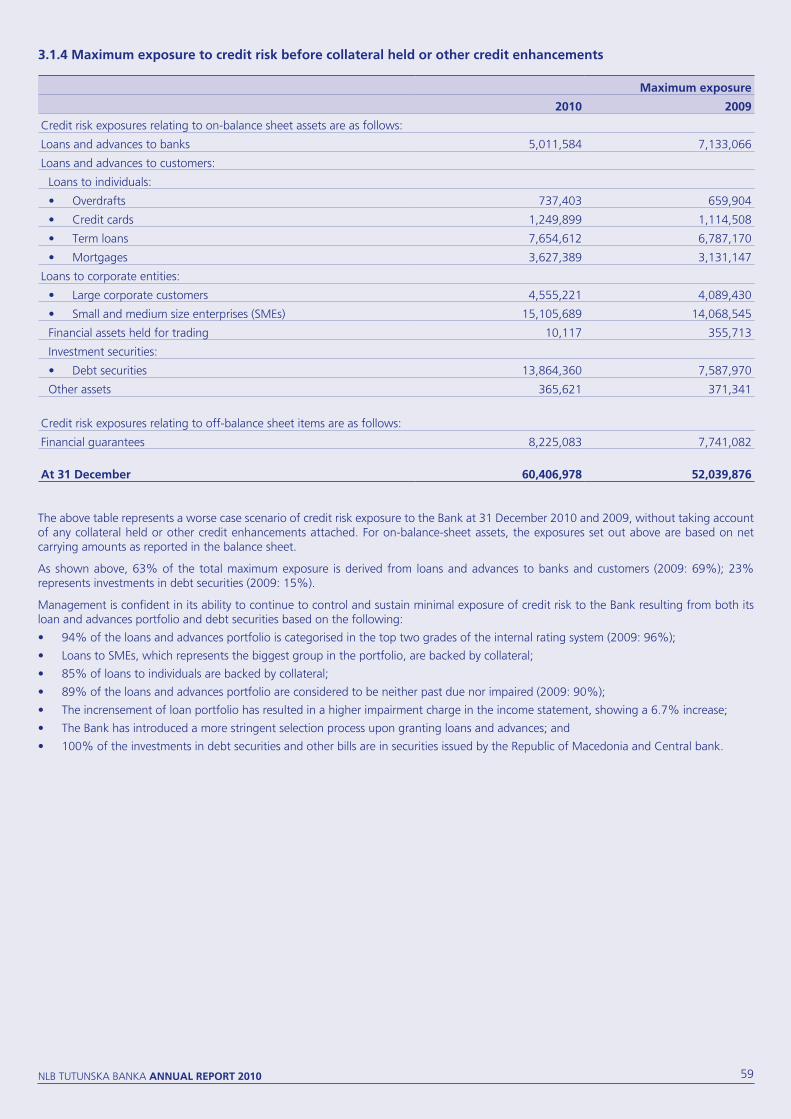

the total exposure of the Bank in 2010 increased by 4,299.0 million MkD (10.6%) and amounts 44,999.0 million MkD. the total reservation fund on 31.12.2010 amounts 4,537.9 million MkD, wherewith the possibility of portfolio coverage is realized with 10.1% (2009: 9.4%).

Credit portfolio quality

the participation of the a and B investments in the total portfolio on the end of 2010 amounts 92.4% (2009: 92.9%). the coverage of the investments classified in the C, D and E risk categories with total separated reservations amounts 132.6% (2009: 132.7%).

risk management

Credit portfolio on which reservations are calculated (000 MKD)

0,000,000

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

40,700,00040,700,00044,999,03344,999,033

2008 2009 2010

40,838,76140,838,761

Structure of the credit portfolio

per categories of risk

A 65,7%A 65,7%

B 26,7%B 26,7%

C 2,4%C 2,4%

D 0,8%D 0,8%

E 4,4%E 4,4%

NLB tutuNska BaNka annual report 2010 30

non-credit risk management

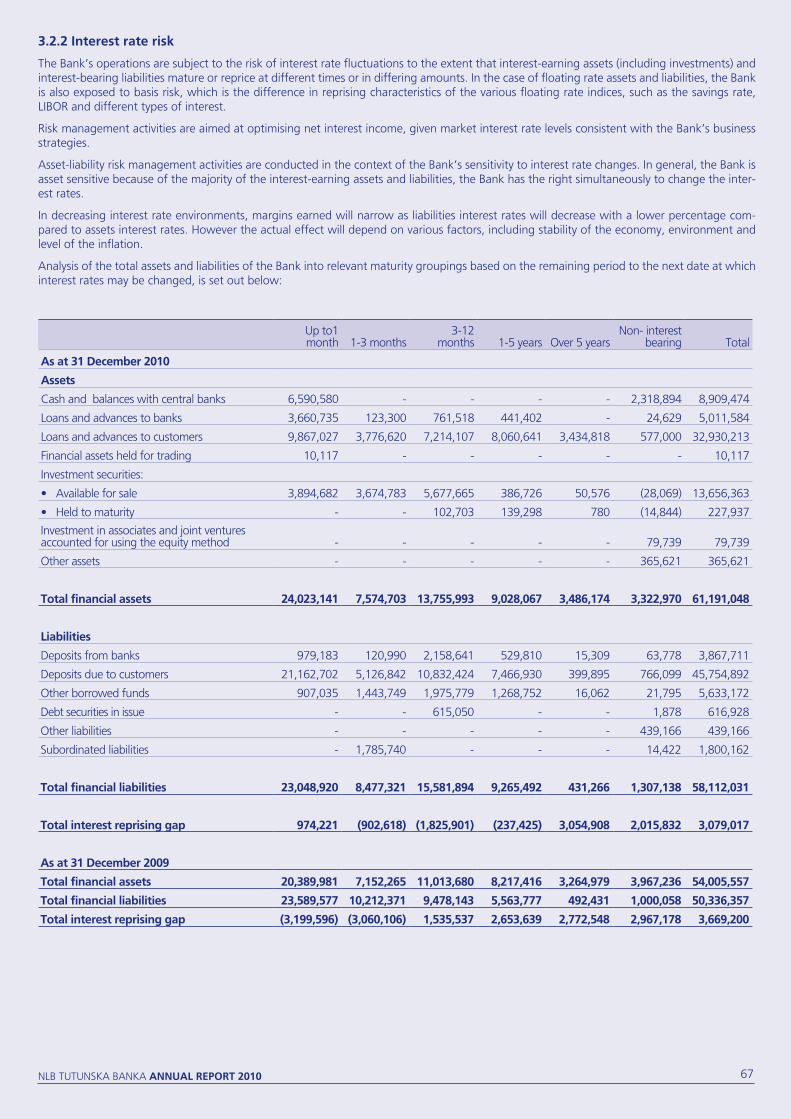

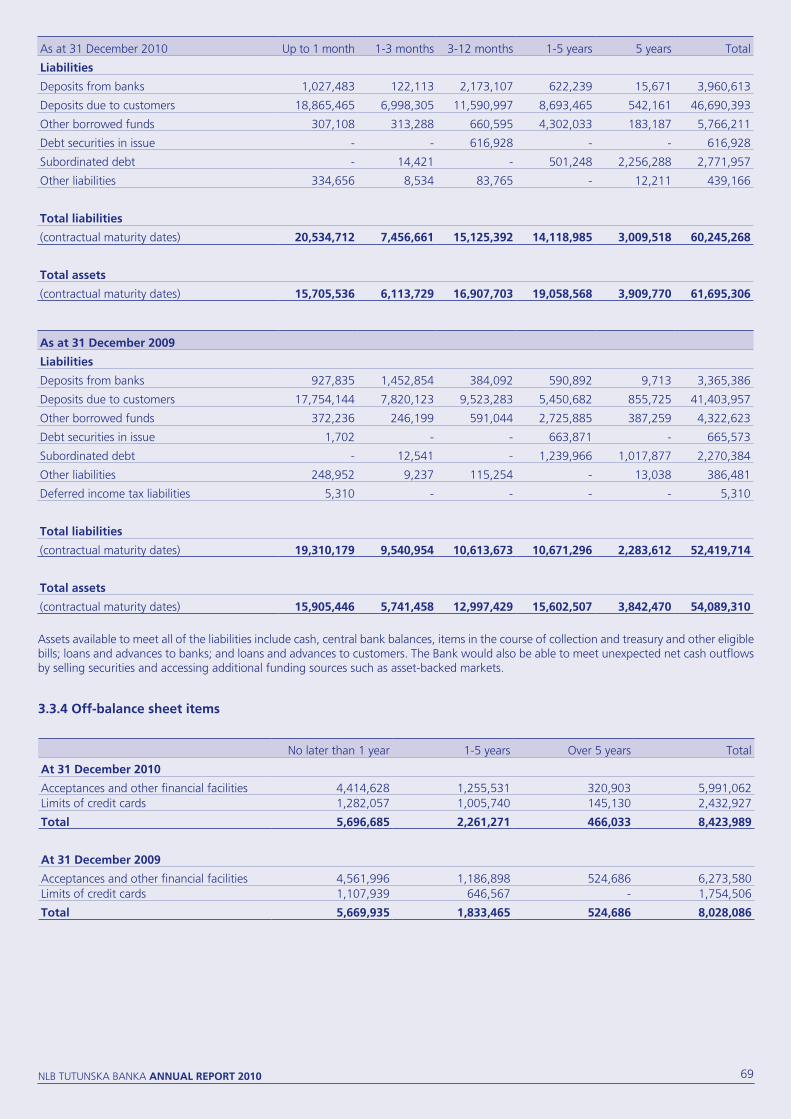

the Bank has defined policies for monitoring of the non-credit risks. In the Bank are monitored and managed the liquidity, foreign currency, interest, operative, legal, strategic and reputational risk and in the same time is monitored and managed the information system safety.

In 2010 were concluded stress-tests on a half-year basis, which show how exposed the bank is to a liquidity risk, foreign currency risk and interest risk, which show the stable position of the Bank.

operative risk management

the operative risk management understands implementation of a system for recording, monitoring, control and finding solutions for possible and real events causing damage, which result from the daily business of the Bank and external factors, and have a negative impact on the financial result.

In 2010 was realized a repeated identification and analysis of the operative risks for the most processes in the Bank. the analysis of the operative risks and the status of the realized measures were submitted to the Committee for operative risks.

Capital management and adequacy of capital

Over 2010 the adequacy of the Bank’s funds was kept on a level above 12.0%. In september, the present subordinary loans from NLB InterFinanz aG Zurich were prolonged, by which the guarantee capital of the Bank was increased to 5,567.9 million MkD (2009: 5,103.5 million MkD), which leaded to increase of the capital adequacy coefficient to 13.16% (2009: 13.05%).

Capital adequacy in %

10

12

14

16

18

20

13.013.0

2009 20102008

13.613.613.213.2

NLB tutuNska BaNka annual report 2010 31

In 2010 were realized several activities from the aspect of expansion and maintenance of the information infrastructure, system adjustments and implementation of new software solutions, which enables development and maintenance of an effective and efficient information system. Herewith, the Bank has the possibility to easily monitor the increase of the work load, the organizational changes, the changes of the regulations, the introduction of new innovative products and services and can easily adapt to them, supporting at the same time unhindered and not decreased realization of the profitability.

Information system safety

the information safety of NLB tutunska banka aD is realized pursuant to the Circular No. 9 of the National Bank of the Republic of Macedonia, the Decision on Information system safety of the bank and is corresponding with the international standards IsO 27001 and IsO 17799-2005 (IsO 27002). Pursuant to these standards an information safety system was established in the Bank, that is consisted of following chapters:

• risk management - the Bank has established a continuous process of identification of the weaknesses and dangers to its information systems;

• policy on information systems safety;

• Implementation of safety controls - By following of the events and operative controls, the Bank realizes administrative, physical and technical controls, by which a protection of the information and systems safety is realised on several levels;

• Monitoring and upgrade - the Bank has established a process of continuous collection and analysis of information regarding the occurrence of new dangers and weaknesses of the information system

Information technology

Human resources

NLB tutuNska BaNka annual report 2010 33

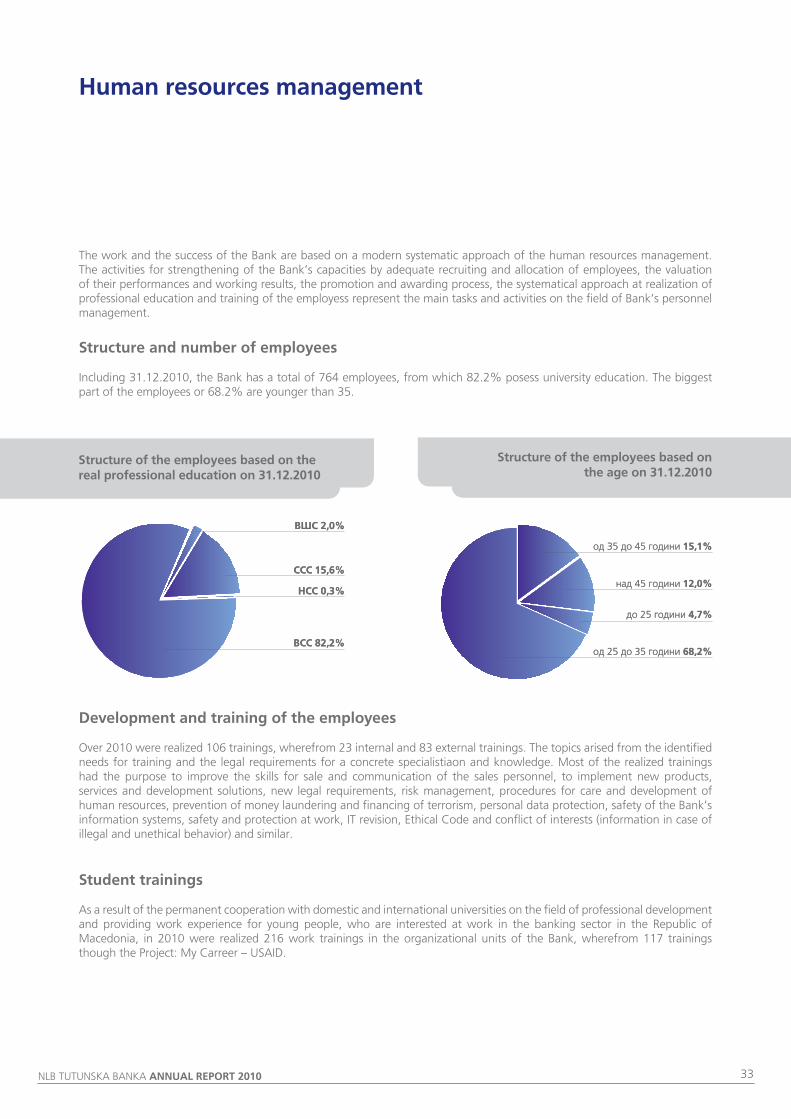

the work and the success of the Bank are based on a modern systematic approach of the human resources management. the activities for strengthening of the Bank’s capacities by adequate recruiting and allocation of employees, the valuation of their performances and working results, the promotion and awarding process, the systematical approach at realization of professional education and training of the employess represent the main tasks and activities on the field of Bank’s personnel management.

Structure and number of employees

Including 31.12.2010, the Bank has a total of 764 employees, from which 82.2% posess university education. the biggest part of the employees or 68.2% are younger than 35.

Human resources management

Structure of the employees based on the real professional education on 31.12.2010

Structure of the employees based on the age on 31.12.2010

Development and training of the employees

Over 2010 were realized 106 trainings, wherefrom 23 internal and 83 external trainings. the topics arised from the identified needs for training and the legal requirements for a concrete specialistiaon and knowledge. Most of the realized trainings had the purpose to improve the skills for sale and communication of the sales personnel, to implement new products, services and development solutions, new legal requirements, risk management, procedures for care and development of human resources, prevention of money laundering and financing of terrorism, personal data protection, safety of the Bank’s information systems, safety and protection at work, It revision, Ethical Code and conflict of interests (information in case of illegal and unethical behavior) and similar.

Student trainings

as a result of the permanent cooperation with domestic and international universities on the field of professional development and providing work experience for young people, who are interested at work in the banking sector in the Republic of Macedonia, in 2010 were realized 216 work trainings in the organizational units of the Bank, wherefrom 117 trainings though the Project: My Carreer – usaID.

до 25 години 4,7%до 25 години 4,7%

од 25 до 35 години 68,2%од 25 до 35 години 68,2%

од 35 до 45 години 15,1%од 35 до 45 години 15,1%

над 45 години 12,0%над 45 години 12,0%

ВСС 82,2%ВСС 82,2%

ССС 15,6%ССС 15,6%

НСС 0,3%НСС 0,3%

ВШС 2,0%ВШС 2,0%

NLB tutuNska BaNka annual report 2010 34

Work organisation

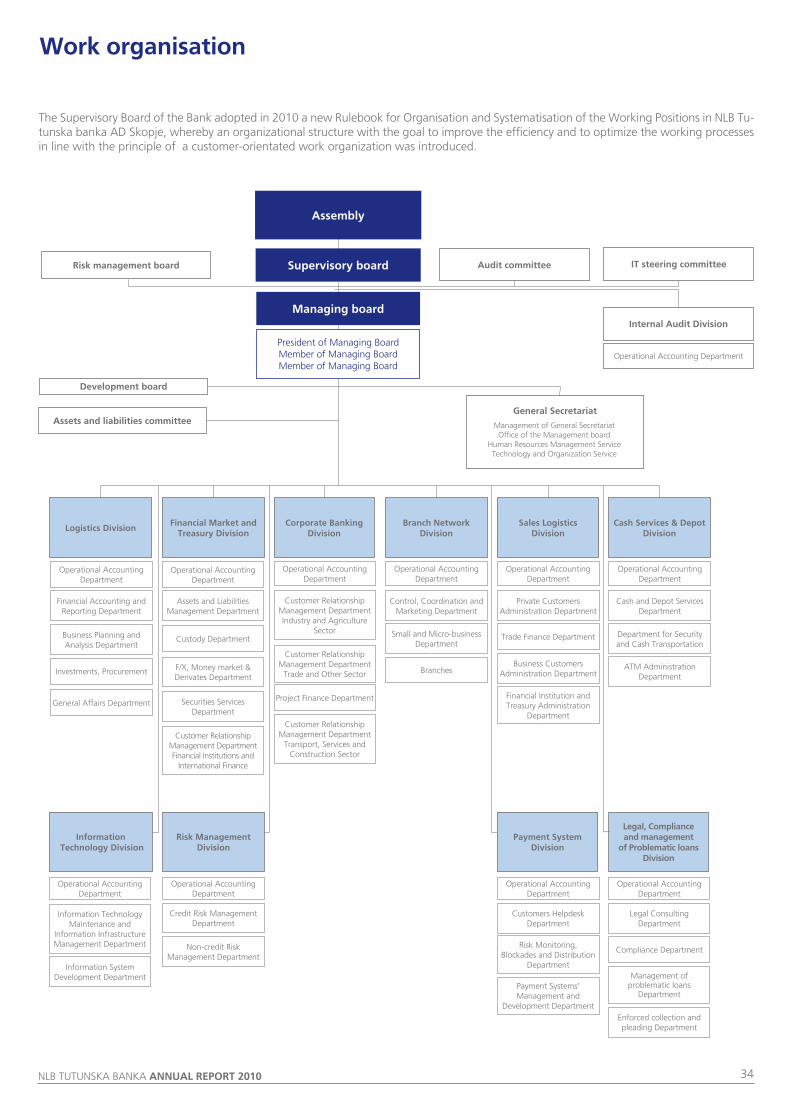

the supervisory Board of the Bank adopted in 2010 a new Rulebook for Organisation and systematisation of the Working Positions in NLB tu-tunska banka aD skopje, whereby an organizational structure with the goal to improve the efficiency and to optimize the working processes in line with the principle of a customer-orientated work organization was introduced.

risk management board

Development board

assets and liabilities committee

audit committee

General Secretariat

logistics DivisionFinancial Market and

treasury DivisionCorporate Banking

DivisionBranch network

DivisionSales logistics

DivisionCash Services & Depot

Division

Operational accounting Department

Operational accounting Department

Operational accounting Department

Operational accounting Department

Operational accounting Department

Management of General secretariatOffice of the Management board

Human Resources Management servicetechnology and Organization service

Operational accounting Department

Operational accounting Department

Operational accounting Department

Operational accounting Department

Operational accounting Department

Customer Relationship Management Department Industry and agriculture

sector

Control, Coordination and Marketing Department

Private Customers administration Department

Cash and Depot services Department

Project Finance Department

Customer Relationship Management Department

transport, services and Construction sector

Customer Relationship Management Department

trade and Other sector

small and Micro-business Department

trade Finance Department Department for security and Cash transportation

BranchesBusiness Customers

administration DepartmentАТМ administration

Department

legal, Compliance and management

of problematic loans Division

risk Management Division

Information technology Division

payment System Division

Financial Institution and treasury administration

Department

Legal Consulting Department

Credit Risk Management Department

Compliance DepartmentNon-credit Risk Management Department

Management of problematic loans

Department

Information technology Maintenance and

Information Infrastructure Management Department

Customers Helpdesk Department

Enforced collection and pleading Department

Information system Development Department

Risk Monitoring, Blockades and Distribution

Department

Payment systems’ Management and

Development Department

Financial accounting and Reporting Department

assets and Liabilities Management Department

Business Planning and analysis Department

Custody Department

Investments, Procurement F/X, Money market & Derivates Department

General affairs Department securities services Department

Customer Relationship Management Department Financial Institutions and

International Finance

It steering committee

Internal audit Division

Operational accounting Department

assembly

Supervisory board

Managing board

President of Managing BoardMember of Managing BoardMember of Managing Board

Financial results

NLB tutuNska BaNka annual report 2010 36

nlB tutunska Banka aD Skopje

Financial statements prepared in accordancewith International Financial reporting Standards

For the year ended 31 December 2010

NLB tutuNska BaNka annual report 2010 37

page Content

Independent auditor’s report ................................................................................................................... 38-39

Income statement ..........................................................................................................................................40

statement of comprehensive income ..............................................................................................................41

statement of financial position (balance sheet) ...............................................................................................42

statement of changes in equity ......................................................................................................................43

Cash flow statement ................................................................................................................................ 44-45

Notes to the financial statements ............................................................................................................. 46-98

NLB tutuNska BaNka annual report 2010 38

to the Shareholders of nlB tutunska Banka aD - Skopje

We have audited the accompanying financial statements of NLB tutunska Banka aD - skopje, which comprise the statement of financial position as of 31 December 2010 and the income statement and the statement of comprehensive income, statement of changes in equity and cash flows for the year then ended and a summary of significant accounting policies and other explanatory notes.

Management’s responsibility for the financial statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting standards. this responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of the financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

auditor’s responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International standards on auditing. those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

an audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. the procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. an audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

Independent auditor’s report

NLB tutuNska BaNka annual report 2010 39

We believe that the audit evidence we have obtained is sufficient and appropriate to provide basis for our audit opinion.

opinion

In our opinion, the accompanying financial statements give a true and fair view of the financial position of NLB tutunska Banka aD skopje as of 31 December 2010 and of its financial performance and its cash flows for the year than ended in accordance with International Financial Reporting standards.

.

pricewaterhouseCoopers reVIZIJa doo

Skopje,

XX February 2011

NLB tutuNska BaNka annual report 2010 40

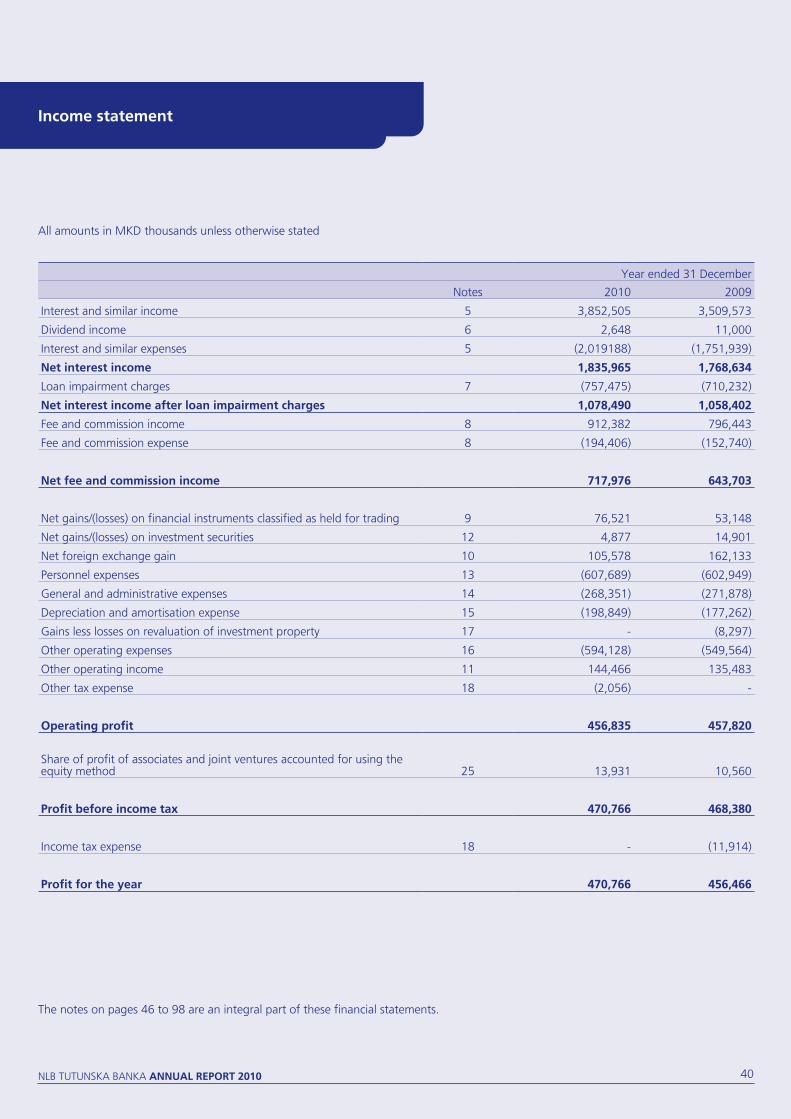

Year ended 31 December

Notes 2010 2009

Interest and similar income 5 3,852,505 3,509,573

Dividend income 6 2,648 11,000

Interest and similar expenses 5 (2,019188) (1,751,939)

net interest income 1,835,965 1,768,634

Loan impairment charges 7 (757,475) (710,232)

net interest income after loan impairment charges 1,078,490 1,058,402

Fee and commission income 8 912,382 796,443

Fee and commission expense 8 (194,406) (152,740)

net fee and commission income 717,976 643,703

Net gains/(losses) on financial instruments classified as held for trading 9 76,521 53,148

Net gains/(losses) on investment securities 12 4,877 14,901

Net foreign exchange gain 10 105,578 162,133

Personnel expenses 13 (607,689) (602,949)

General and administrative expenses 14 (268,351) (271,878)

Depreciation and amortisation expense 15 (198,849) (177,262)

Gains less losses on revaluation of investment property 17 - (8,297)

Other operating expenses 16 (594,128) (549,564)

Other operating income 11 144,466 135,483

Other tax expense 18 (2,056) -

operating profit 456,835 457,820

share of profit of associates and joint ventures accounted for using the equity method 25 13,931 10,560

profit before income tax 470,766 468,380

Income tax expense 18 - (11,914)

profit for the year 470,766 456,466

all amounts in MkD thousands unless otherwise stated

Income statement

the notes on pages 46 to 98 are an integral part of these financial statements.

NLB tutuNska BaNka annual report 2010 41

Year ended 31 December

Notes 2010 2009

profit for the year 470,766 456,466

net gains on available-for-sale financial assets

• unrealised net gains arising during the period, before tax (3,263) (40,513

• Net reclassification adjustments for realised net losses, before tax (4,877) (14,901)

Income tax relating to components of other comprehensive income 3,132 5,535

other comprehensive income for the year, net of tax 19 (5,008) (49,879)

total comprehensive income for the year 465,758 406,587

Statement of comprehensive income

all amounts in MkD thousands unless otherwise stated

the notes on pages 46 to 98 are an integral part of these financial statements.

NLB tutuNska BaNka annual report 2010 42

as at 31 December

Notes 2010 2009

assets

Cash and balances with central banks 20 8,909,474 8,553,400

Loans and advances to banks 21 5,011,584 7,133,066

Loans and advances to customers 23 32,930,213 29,850,704

Financial assets held for trading 22 10,117 370,325

Investment securities:

• available for sale 24 13,656,363 7,341,741

• Held to maturity 24 227,937 317,030

Investments in associates for using the equity method 25 79,739 65,200

Investment properties 26 70,471 70,471

Property, plant and equipment 27 804,543 874,351

Intangible assets 28 115,288 93,951

Current income tax assets 38 - 572

Deferred income tax assets 29 - 2,178

Foreclosed collateral 30 493,005 83,753

Other assets 31 365,621 371,341

assets classified as held for sale 32 30,864 -

total assets 62,705,219 55,128,083

liabilities

Deposits from banks 33 3,867,711 3,176,495

Deposits from customers 34 45,754,892 40,388,538

Other borrowed funds 35 5,633,172 4,127,402

Debt securities in issue 36 616,928 631,786

Provisions 37 198,906 287,004

Deferred income tax liabilities 30 - 5,310

subordinated debt 39 1,800,162 1,620,346

Other liabilities 40 439,166 386,480

total liabilities 58,310,937 50,623,361

equity

Capital and reserves attributable to equity of parent entity

share capital 44 854,061 854,061

share premium 44 2,203,056 2,203,056

Revaluation reserve 44 41,026 28,184

Retained earnings 685,110 786,533

Other reserves 611,029 632,888

total equity 4,394,282 4,504,722

total equity and liabilities 62,705,219 55,128,083

Statement of financial position (balance sheet)

all amounts in MkD thousands unless otherwise stated

the notes on pages 46 to 98 are an integral part of these financial statements.

NLB tutuNska BaNka annual report 2010 43

Statement of changes in equity

attributable to owners of the parent entityshare

capitalshare

premium Revaluation

reserveRetained earning

Otherreserves

total equity

Balance at 1 January 2009 854,061 2,203,056 78,063 1,006,602 579,463 4,721,245

Profit - - - 456,466 - 456,466Fair value gains on available for sale financial assets, net of tax - - (49,879) - - (49,879)

total comprehensive income - - (49,879) 456,466 - 406,587

Dividends income to 2008 - - - (623,110) - (623,110)

transfer to statutory reserve - - - (53,425) 53,425 -

Balance at 31 December 2009 854,061 2,203,056 28,184 786,533 632,888 4,504,722

Balance at 1 January 2010 854,061 2,203,056 28,184 786,533 632,888 4,504,722

Profit - - - 470,766 - 470,766Fair value gains on available for sale financial assets, net of tax - - (5,008) - - (5,008)

total comprehensive income - - (5,008) 470,766 - 465,758Dividends income to 2009 - - - (408,051) - (408,051)