6 facets and the nature of a life insurance contract

TRANSCRIPT

(300)

6 FACETS AND THE NATURE OF A LIFE INSURANCE CONTRACT

INTRODUCTION - The Contract of Insurance

The principal law, which governs the life insurance business in

India, is the Insurance Act, 1938 (in its amended form under the Industry

Regulatory and Development Authority Act, 1999). The Act does not

contain a definition of life insurance contracts as such. It, however, defines

(section 2(11)) life insurance business as:

“Business of affecting contracts of insurance upon human life,

including any contract whereby the payment of money is assured on

death (except death by accident only) or the happening of any

contingency dependent on human life, and any contract which is

subject to payment of premiums for a term dependent on human

life…..”1

The definition may be taken to include a whole set of life contingent

contracts including death, disability, capital redemption and annuities.

Though accident and health insurance has been traditionally covered by the

general insurance industry, the scope of life insurance contracts has also

been expanded to include areas like critical illness or dread diseases. A

point of significance is that many of the provisions and practices

1 . Shashidharan K. Kutty, “Managing Life Insurance”, PHI Learning Pvt. Ltd., New Delhi,

2008, 53.

(301)

underlying the life insurance contract are not entirely mandated by the

Insurance Act or other legislation. Rather, they have their origins in

common law.

BASIC FEATURES OF A LIFE INSURANCE CONTRACT

The provisions of the Indian Contract Act, 1872 govern all contracts

in India, including life insurance contracts. Sections 2 and 10 of the above

act set out some of the important elements that go to make a valid contract.

These are offer and its acceptance, lawful consideration, capacity or parties

to contract, consensus ad idem and legality of object. Let us consider each

of these in some details, in the context of life insurance.

A contract is an agreement between parties, which are enforceable

at law.2 To be enforceable by law, an agreement must possess the essential

elements of a valid contract as contained in Sections 10.

Essential of a valid contract: The contract of insurance, like any other

contract must fulfill the following essential requirements of a valid

contract as laid down in the Indian contracts act. A contract is an

agreement made between two or more parties, which the law will enforce.

The essential requirements of a valid contract as laid down in the Indian

contract act are:

1. Agreement: This involves, one party making the offer and the other

party accepting it. The acceptance of the offer must be in writing or given 2 . Section 10, Indian Contract Act, 1872, quoted by Padhi, P.K., “Legal Aspects of

Business”, PHI Learning Private Limited, New Delhi, 2002, 35.

(302)

verbally and must be absolute and unconditional and must be

communicated to the proposer.

It is often believed that the individual who signs a proposal for

insurance is the one who makes the offer and the insurer is the one who

accepts it. In reality when an individual completes the proposal form and

submits it to the insurer, he or she only invites the latter to make an offer.

When the insurance underwriter ‘accepts’ a proposal on certain terms and

determines the premium payable, he is in effect making a counter offer.

The insurer has the right to refuse to make such an offer if the

circumstances warrant that that no insurance cover is granted to a

particular individual. In general, once the counter officer is intimated to the

proposer, it is deemed that the payment of the premium by the latter is

equal to its acceptance. No other formal written communication is

necessary for the purpose.

In India and other markets, the premium has to be paid upfront at the

time of making the proposal. In the large majority of cases, we have a

situation where the first premium has been sent with the proposal and the

insurer without any modification accepts the proposal. In all such cases, it

is deemed that the insurer normally assumes risk from the date of

acceptance, assumption of risk being indicated by a separate receipt issued

for first premium (the first premium receipt). A question, however, would

arise when the underwriter imposes a premium extra or certain other

(303)

conditions-like an aviation clause for pilots, which excludes death while on

duty as a pilot from the cover. In such instances the contract comes into

existence only when the person to whom the underwriting decision is

communicated accepts the extra premium or the new conditions imposed.

Again, in a number of markets the regulatory authorities have provided for

a ‘cooling off’ period of say 15 days after the date of underwriter’s

acceptance, during which the proposer has the right to decide to reject the

offer made by the insurer.

Another fact to note is that an acceptance (by the underwriter) is

always subject to the condition that if any adverse event connected with

the risk has occurred between the date of proposal and the date of

acceptance, the assurance will be invalidated unless intimation of such an

even is given to the insurer and the acceptance is re-approved. The

proposer, thus, has a duty to disclose to the insurer all relevant facts and

information coming to his knowledge until the date of the contract.

Insurance is an intangible product which is a contract of promise

wherein one party, the insured, fulfills its promise in advance by paying

the premium while the other part of promise is to be activated only at the

time of the event insured.3

2. Consideration in Life Insurance Contract: In a life insurance

contract the payment of premium by the life assured and the assurance

3 . Sudhir Kumar Jain, “Consumer Orientation – Insurance Product”, IRDA Journal, April, 2012, 27.

(304)

given by the insurer to secure him a sum of money, apparently constitute a

lawful consideration recognized by law to be a lawful contract. To be a

valid contract, the objective also should be lawful.4

Under every insurance policy, a small sum is paid as premium and

on death of the life assured, nominees or beneficiaries collect the assured

sum. Thus it looks like gambling on that life. Only the survivors pay the

full quantum of premium and they possibly happen to contribute more to

make a few people to have gains. This scenario seems to mock the

institution of life insurance as a lawful contract.

Insurance Contract is not a ‘Wagering Contract’

In a contract of wager all the parties does not have any interest in

happening of the event other than the sum or stake him will win or lose.

This is what marks the difference between a wagering agreement and a

contract of insurance because every contract of insurance requires for its

validity the insurable interest.

Wagering is illegal in India and against to the norms of society or

in short wagering is against public policy and distinction between an

insurance and a wager is this a insurance is properly speaking a contract to

indemnify the insured in respect of some interest which he has against

perils which he contemplates it will be liable to.

4 . Shashidharan K. Kutty, “Managing Life Insurance”, PHI Learning Pvt. Ltd., New Delhi,

2008, p.-260.

(305)

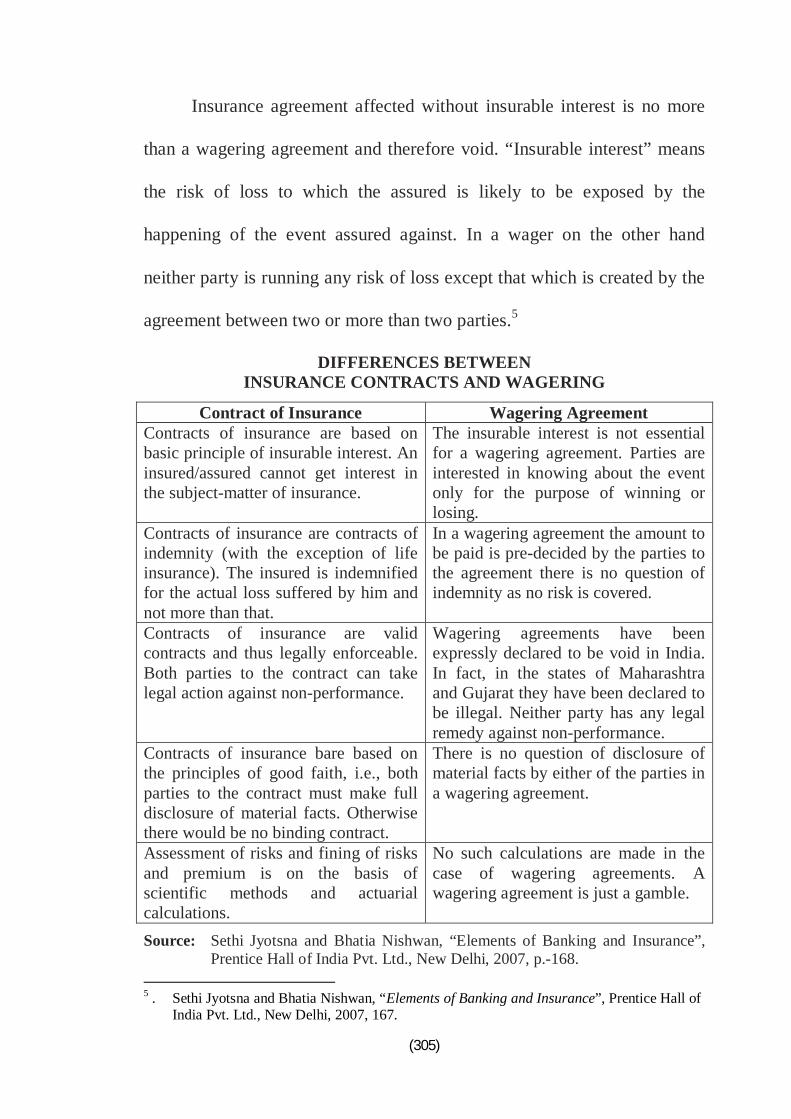

Insurance agreement affected without insurable interest is no more

than a wagering agreement and therefore void. “Insurable interest” means

the risk of loss to which the assured is likely to be exposed by the

happening of the event assured against. In a wager on the other hand

neither party is running any risk of loss except that which is created by the

agreement between two or more than two parties.5

DIFFERENCES BETWEEN INSURANCE CONTRACTS AND WAGERING

Contract of Insurance Wagering Agreement Contracts of insurance are based on basic principle of insurable interest. An insured/assured cannot get interest in the subject-matter of insurance.

The insurable interest is not essential for a wagering agreement. Parties are interested in knowing about the event only for the purpose of winning or losing.

Contracts of insurance are contracts of indemnity (with the exception of life insurance). The insured is indemnified for the actual loss suffered by him and not more than that.

In a wagering agreement the amount to be paid is pre-decided by the parties to the agreement there is no question of indemnity as no risk is covered.

Contracts of insurance are valid contracts and thus legally enforceable. Both parties to the contract can take legal action against non-performance.

Wagering agreements have been expressly declared to be void in India. In fact, in the states of Maharashtra and Gujarat they have been declared to be illegal. Neither party has any legal remedy against non-performance.

Contracts of insurance bare based on the principles of good faith, i.e., both parties to the contract must make full disclosure of material facts. Otherwise there would be no binding contract.

There is no question of disclosure of material facts by either of the parties in a wagering agreement.

Assessment of risks and fining of risks and premium is on the basis of scientific methods and actuarial calculations.

No such calculations are made in the case of wagering agreements. A wagering agreement is just a gamble.

Source: Sethi Jyotsna and Bhatia Nishwan, “Elements of Banking and Insurance”, Prentice Hall of India Pvt. Ltd., New Delhi, 2007, p.-168.

5 . Sethi Jyotsna and Bhatia Nishwan, “Elements of Banking and Insurance”, Prentice Hall of

India Pvt. Ltd., New Delhi, 2007, 167.

(306)

In case of Alamani v. Positive Govt. Security Life Insurance Co.6

the plaintiffs husband took a policy of insurance on the life of Mehbub Bi,

the wife of a clerk working under him and about a week later got the

policy assigned in the favour of the plaintiff, Mehbub Bi died a month later

and the plaintiff as assignee claimed the sum assured and in this case court

find that there was no insurable interest present in this case and hence their

lordships of Bombay High Court held the view that in India, insurance for

a term of years on the life of a person in which the person effecting the

insurance has no interest is void as a wagering contract under Sec.30 of

Indian Contract Act. Any Life Insurance Contract devoid of insurable

interest will be a gamble.

In case of Brahm Dutt Sharma Vs Life Insurance Corporation of

India, (1965)7 the Allahabad High Court has held a similar view and made

Sec.30 of the Contract Act applicable to all life insurance contracts

wherever it is found that the person effecting a life policy on another's life

without having insurable interest, is void as a wagering contract.

A person effecting a policy on his own life is presumed to have

insurable interest on his life to an unlimited extent. That is why people go

in for policies for huge sums. Here again, the limiting factor is the element

of Moral hazard and the capacity to pay the premium.

6 . Alamani vs. Positive Govt. Security Life Insurance Co (1899) ILR 23 Bom.191, 206. 7 . Re. Brahm Dutt Sharma Vs Life Insurance Corporation of India, (1965) AIR 1966 All,

474.

(307)

2. Legal Relationship: when the two parties enter into an agreement

their intention must be create legal relationship between them. With many

informal and social agreements, such as, an agreement to give a friend a

lift in one's car, there is never any intention of legal consequences so the

agreement for same reason should not be carried out

3. Lawful Consideration: The, agreement is legally enforceable, only

when the contract is supported by consideration, i.e., when both the parties

give something in return. In insurance both parties provide consideration.

Consideration from the insured to the insurer is the premium while from

the insurer to the insured is a promise to compensate the insured or to

make certain payment in the event of certain happenings taking place.

4. Capacity of Parties: The parties and their capacity to enter into

enforceable agreement give the third element in the contract. Section 11 of

the Indian Contract Act indicates who are the persons competent to

contract. Every person who is of the age of majority (according to the law

to which one is subject) and who is of sound mind and not disqualified

from contracting by any law to which he is subject is, thus, competent to

enter into a contract. The rationale for the above is that parties to a contract

should be in a legal and personal position to understand the intricacies (the

pros and cons) of the contract they formulate and to discharge their

obligations and enjoy their rights under the contract.

(308)

The above qualifications apply in the case of life insurance contracts

as well. An important question that can arise here is about contracts, which

are written on the lives of minors, as under children’s plans. As a minor

cannot contract, any such legal agreement with a minor would be null.

Such contracts are, thus, made with the parent or guardian of the minor.

The contract, thus, vests in the minor on attainment of the age of majority,

unless he or she chooses to disaffirm it.

Consensus Ad Idem

A critical requirement of any valid contract is that the parties to it

are ad idem, i.e. of the same mind. If the agreement is induced by coercion,

undue influence, fraud misrepresentation etc., there is absence of free

consent. The principle of consensus ad idem is critical to insurance. The

parties to a contract cannot be said to be in ad idem if the proposer

withholds material information form the insurer. The latter is then

accepting the risk without being able to make a proper assessment of the

same. The ‘Basis Clause’ in every insurance contract implies that the

statements made by the insured in the proposal and other submissions form

the basis of the contract. If they are not true, the contract can be held to be

void. By the same token, the insurance company also has the obligation to

fully explain the implications of the basis clause to the insured. Thus:

If the insurer wants to repudiate a policy on the grounds of

misstatement by the insured, he must establish to the satisfaction of the

(309)

court that he acted fairly and honourably to the insured by explaining

properly the implications of declaration to be signed by the insured and the

range or amplitude of the questions required to be answered. This is very

important because very often an inaccurate and, therefore, ‘strictly’ false

answer is in another sense a true answer if considered ‘fairly’.

Clauses are introduced into policies of insurance which ‘unless they

are fully explained to the parties will lead a vast number of persons to

suppose that they have made a provision for their families by an insurance

on their lives and by payment of perhaps a very considerable proportion of

their income, when a point of fact, from the very commencement, they

policy was not worth the paper upon which it was written……” Fletcher

Moulton.8

5. Free and Genuine Consent: There must also be a free and genuine

consent of the parties to the agreement.

“A contract of Insurance will be concluded only when the party to

whom an offer has been made accepts it unconditionally and

communicates his acceptance to the person making the offer. Though in

certain human relationships silence to a proposal might convey acceptance

but in the case of insurance proposal, silence does not denote consent and

no binding contract arises until the person to whom an offer is made says

or does something to signify his acceptance. Mere delay in giving an

8 . Quoted by A.P. High Court in LIC Vs Shakuntala Bai, 1975 AIR (AP) 68.

(310)

answer cannot be construed as an acceptance, as, prima facie, acceptance

must be communicated to the offeror. Similarly, the mere receipt and

retention of premium until after the death of the applicant or the mere

preparation of the policy document is not acceptance.”9

6. Lawful Object: The object of the contract must be lawful. Thus, the

object of the agreement must not be illegal, immoral, or opposed to public

policy. If an agreement suffers from any legal flaw, it would not be

enforceable by law. For example a landlord knowingly lets a house to

terrorist to carry out his activities, and he cannot recover the rent through

the court of law.

7. Agreement Not Declared Void: The agreement, though it might

possess all the essential elements, must not have been expressly declared

void by any law in force in country. Any contract which is contrary to the

law of this country is void, such as insurance on goods being traded with

an enemy national in times of war.

8. Certainty and Possibility or Performance: It is essential the

creation of every contract that the terms of agreement must be certain and

not vague, indefinite, or ambiguous. An agreement to do an act impossible

in itself cannot be enforced. For example Q agrees with P, to increase his

height by magic. This agreement is not enforceable by law.

9 . Life Insurance Corporation Vs. Raja Vasireddy Kamalavalli Kamba, AIR 1984 SC

1014. quoted by Padhi, P.K., “Legal Aspects of Business”, PHI Learning Private Limited, New Delhi, 2002, 34.

(311)

9. Legal Formalities: The agreement maybe either oral or in writing.

But if it is in writing, it must comply with the necessary legal formalities

as to writing, registration, attestation, and stamp and must be issued under

seal.

Contracts Which Are Defective

Void Agreement: An agreement not enforceable by law is said to

be void [Sec 2(g)]. A void agreement does not create any legal rights or

obligations. It is void ab-initio, i.e. from very beginning, for example an

agreement with minor.

Void Contracts: A contracts which legally does not exist is known

as void contract. In other words, a contract, which ceases to be

enforceable, is void when it ceases to be enforceable. It is valid when it is

entered into, but something, which happens subsequently to the formation

of the contract makes it void. Example: a contract to import goods from

foreign country. It may subsequently become void.

Voidable Contract: An agreement which is enforceable by law at

the option of one or more of the parties thereto, but not at the option of the

other or others, is voidable contract. In other words when either party is in

breach of the essential terms of the contract, the other party has a right to

consider the contract void. If the aggrieved party may decide to overlook

the breach or to waive the breach, the contract on this case is unaffected

and remains in full force.

(312)

Example: Anu promises to sell his watch for Rs. 500. Her consent is

obtained by use of force. The contract is voidable at the option of Anu. She

may accept it or reject it.

Unenforceable Contracts: Unenforceable contracts are those which

are neither void nor voidable but which cannot be enforced through the

courts. For example, an insurance policy without proper stamp duty cannot

be produced as evidence of a contract in court. Unenforceable contracts are

fully valid contracts but the parties cannot enforce them through the courts.

ESSENTIAL FEATURE OF INSURANCE CONTRACTS

Though insurance has been differentiated into marine, fire, life etc.,

there are certain general principles applicable to all forms of insurance.

These general principles have a two-fold purpose. They serve as a guide to

the sound interpretation of the purport of the insurance contracts in their

diversified forms. For example, the principles of indemnity, insurable

interest, uberrima fides and the existence of risk are some of the principles

having common application.

(a) Existence of risk:

It is indispensable to every contract of insurance that the subject

matter should be exposed to the contingency of loss or risk. Risk involves

the happening of an uncertain event adverse to the interest of the assured.

In marine insurance the ship or cargo is exposed to the loss by perils of the

sea.

(313)

In fire insurance the risk is destruction of property by fire. In life

insurance the risk in the death of the assured is, though a certainty,

uncertain as to the time of its happening. In an abstract sense risk may be

defined as the chance of loss. It can either be an uncertainty as to the

outcome of some event or events, or loss as the result of at least one

possible outcome. In any case, the promise of the insurer is to save the

assured against the uncertain consequences.

(b) Indemnity, the key principle:

Insurance is essentially a contract of indemnity. All the claims of the

assured will be adjusted only with reference to the actual loss sustained by

him. Thus it is implicit in every contract of insurance that the assured in

case of a loss against which the policy has been made, shall be fully

indemnified but shall never be more than fully indemnified. The effect of

the principle of indemnity, in laying down that the satisfaction ought not to

exceed the actual loss, is to prevent fraud on the part of the assured. It

checks the temptation to gain by unfair means and wilful causing of loss.

However, the real basis for the application of the principle of indemnity is

not the prevention of crime or consideration of public policy but it derives

from the intrinsic nature of the bargain.

In assessing the amount payable on a contract of insurance, the

principle of indemnity though a guiding principle, is not an unqualified

one. It is common that insurers limit their liability to a particular amount of

(314)

money known as the ‘sum assured.’ In case of loss, the ‘sum assured’ is all

that the assured is entitled to even if the value of the thing is far in excess

of it. But in all other cases, excepting the valued policies (in Marine

Insurance) the insurer is liable to indemnify only to the tune of the actual

loss, even though the ‘sum assured’ is a higher amount. In ‘valued

policies,’ the parties agree that the value of the subject-matter shall be

agreed. The object of the valued policies is to avoid dispute after the loss

occurs as to the quantum of the assured’s interest.

In contracts of life insurance, personal accident and sickness

insurances and in some forms of contingency insurance, the loss is seldom

measured in monetary terms. They are to be distinguished from contracts

of indemnity like marine and fire insurance. It is now well established that

life insurance in no way resembles a contract of indemnity.

Not infrequently the contract of life insurance is considered as an

arrangement for profitable investment. It is because the assured by paying

the premiums is effecting a saving, the cumulative sum which he can

recover after the expiry of the fixed period. Life insurance may properly be

considered as an investment of money because it enables to secure an

ultimate fund to those persons who have no greater opportunity of making

savings or which left to themselves they would have found it beyond their

means. Yet, the objective of a contract of life insurance is mainly to

provide for the risk of death happening at an uncertain time. Though to

(315)

consider it as a sort of investment holds good in some cases, it is departing

from the essential feature of insurance security against risk. It is, therefore

observed that a life policy is not a contract of indemnity. Generally a

contract of indemnity is entered into for the sole purpose of making good a

loss incurred. The value of a life, however, is incapable of estimation and

except, in a limited sense, cannot be “made good” by insurance. An

important distinction which thus arises between life insurance and other

forms of insurance is that the principle of “subrogation,” under which the

insurer (i.e., the company) takes the right of recovery against the third

party causing the loss, has no application to life insurance.

(c) Insurance and wager not identical:

The fundamental principle of indemnity on which the greater part of

the law of insurance is based, prima facie, negatives any treatment of

insurance on par with wagering contracts. Wagering contracts are those,

wherein “two persons, professing to hold opposite views touching the issue

of a future uncertain event, mutually agree that, dependent upon the

determination of that event, one shall win from the other, and that other

shall pay and hand over to him, a sum of money or stake.” Again, “the

distinction between a wagering contract and one which is not a wager,

depends upon whether the person making it has or has not an interest in the

subject matter of the contract.” That means, “if the event happens the party

will gain an advantage, if it is frustrated he will suffer a loss.” Probably,

(316)

the common feature of the two types of agreement – the element of

uncertainty, gave rise to the misconception of insurance in terms of a

gamble.

At one time according to Sir William Anson10, the father of the

“Law of Contract” insurance was placed on a different ground from a pure

wager merely because it is permitted by law. Insurance was regarded as no

better than a wagering contract despite the presence of insurable interest.

But this view has been modified by himself later on and now he affirms

insurance is described as having only a ‘superficial resemblance’ to a

wager.

Though the distinction is subtle, it is the intention of the parties

rather than the form of the contract that distinguishes insurance from

wager. A wagering contract is made generally with a view to secure profit.

The probability of the happening of an event is completely extraneous to

the interests of the parties except for the chance of gain. A wager is

concerned with the happening of an event per se and the consequential

determination of the conflicting interests. The purpose is to win or lose in

lieu of the mere probability of an event. In insurance the interest of the

assured in the subject matter of risk known as insurable interest, is of the

utmost importance.

10 . Sir William Reynell Anson, Ernest Wilson Huffcut, “Principles of the English Law

of Contract and of Agency in Its Relation to Contract”, Banks Law Publishing Company, 1899.

(317)

A contract of insurance is described as aleatory. It is speculative to

such an extent that the parties may not know whether the event insured

against will occur or not, thus involving a case of mutual risk. The insurer

in turn for a comparatively small sum in the shape of a premium

undertakes to compensate against a heavy loss. But such undertakings will

normally be with reference to actuarial practice and therefore insurance

always stands apart from a mere speculative venture. Insurance can be only

with reference to a previously existing risk and unlike a wager it does not

create risk with its inception. The interests of the parties in a pure wager

are centered round the fact that they have contracted to pay each other

certain sums on the happening or otherwise of a certain event thereby

bringing into being risk not of previous existence.

In the case of insurance, the individual subjected to the risk before

negotiations, obtains security and to that extent there will be a shifting of

risk rather than a creation of it. Therefore, to say that insurance

accomplishes the reverse of a wagering contract seems to be correct

proposition. At one time life insurance was considered to be immoral, as

“gambling in human life.” This idea arose because policies were taken

where no insurable interest existed and where the insurance was effected

solely for speculative purposes. Life insurance, however, is now chiefly

used and properly regarded as an economic and social necessity and when

properly understood cannot be considered as a “wager” even though a

(318)

large financial gain may result from the early death of the insured. On the

other hand, a wagering contract is one where profit is sought to be made

through chance, while the true object of life insurance is rather the

opposite, the avoidance of loss arising through chance. A life insurance

policy, therefore, is not a wagering contract, which would be

unenforceable on grounds of public policy.

Life insurance was regarded as a contract of indemnity similar to

other contracts of insurance even so late as 1854. It will, therefore, be not

out of place to note here the contrast that now exists between life insurance

and other forms of insurance.

1. Most contracts of insurance are usually annual contracts and the

insurers have option to refuse renewal at the end of each and any period of

insurance. In some cases the insurer reserves to him the right to terminate

the insurance any time on a proportionate return of premium in respect of

the unexpired period of the risk. Life assurance contracts are, in the main,

long-term contracts, and in the absence of any fault or any flaw the insurer

has no option to cancel the insurance.

2. The risk insured against under a fire, accident or marine insurance

contract may or may not occur but the event insured against under life

assurance contract is bound to happen.

3. From the above we see that the general contract of insurance

continues to be a contract of indemnity, but life insurance is considered as

(319)

an assurance contract. Regarding the life insurance contract, McGillivray

says, “the contract of insurance may be to pay on the happening of the

event insured against, a certain or ascertainable sum of money irrespective

of whether or not the assured has suffered loss or of the amount of such

loss if he has suffered any.”

(d) Insurable Interest:

The next test for a valid insurance contract is the existence of

insurability interest. The ‘insurable interest’ may be defined thus: “Where

the assured is so situated that the happening of the event on which the

insurance money is to become payable would, as a proximate result

involve the insured in the loss or the diminution of any right recognized by

law or in any legal liability, there is an insurable interest to the extent of

the possible loss or liability.”

Here again we see that such interest should exist at the time of

happening of the event in the general insurance contracts, but is not

necessarily so in the case of the life insurance contracts. This is because

the former is a contract of indemnity and the latter is a contract of

assurance. Taking an example of fire insurance, it is clear that an insured

person suffers no loss under a policy if at the time of loss or damage to the

property he has no interest in it either as full or partial owner. McGillivray

says, “if the assured has no interest at the time the event happens it is clear

that he cannot recover anything, because he suffers no loss, and therefore

(320)

has no claim to an indemnity. Similarly, if he has an interest which is

limited to something less than the full value of the subject-matter, he

suffers no greater loss than the value of his interest at the time of the loss,

and therefore, his claim to an indemnity cannot exceed the value of his

interest.” He further continues: “An interest is required by the terms of the

contract itself if the promise of the insurer is merely to indemnify the

assured against pecuniary loss arising from the event insured against.” If

the above was not so, insurance would prove to be a good inducement to

the deliberate destruction of insured property with a view to making a

profit out of the loss.

In this connection life insurance stands on different ground. No

value can be assigned to human life in the same way as is done in respect

of tangible property. But all the same it is possible to measure the extent of

loss that would be caused by the failure of a given life. Insurable interest of

some kind is necessary to every contract of insurance of whatever kind and

any insurance made without such interest is illegal and void.

It is clear from the above discussion that an insurable interest as

defined above is an indispensable feature of contracts of indemnity. Life

insurance, however, stands on a different footing and it is now established

that provided a bona fide interest exists at the date of the contract no

interest need be shown at the date of loss. Similarly the amount

recoverable under a life policy refers to the interest at the time of making

(321)

of a contract. These conclusions are based on judicial interpretation and are

now universally recognized.

The guiding factor is that an insurable interest is a reasonable

expectation of financial benefit from the continued life of the subject or an

expectation of loss if the subject dies. For instance, a parent has a clear

insurable interest in the life of a minor child, since he is entitled to the

services and earnings of that child.

The concept of insurable interest primarily appears to be an

invention of the courts. It may be necessary for the assured to show interest

but common law contains no general prohibition of contracts in which no

insurable interest exists. It was perhaps introduced to curb insurances by

way of wager, and obtained statutory recognition. The presence of

insurable interest is insisted for two reasons: (1) the assured cannot be

taken to have suffered any damage if he has no interest in the property

insured at the time of loss. (2) Secondly, if the interest of the assured is

limited to something less than the full value of the subject-matter, no

greater damage than his interest in the subject matter will result. In both

cases the interest in the subject-matter is required by the terms of the

contract itself since the promise of the insurer will be only to compensate

the actual loss.

To have insurable interest, it is essential that there should be some

contractual or proprietary right, whether legal or equitable so long as it is

(322)

enforceable in the courts. Accordingly the main principles determining the

existence of insurable interest are (a) the interest must be enforceable at

law; (b) the continued existence of the interest will be beneficial to the

assured. Strict legal or pecuniary interest is not necessary. Equitable

interest is sufficient to give rise to insurable interest.

Under the contract of life insurance, the assured has insurable

interest in his own life to an unlimited extent. But where a person takes an

insurance on the life of another, the criteria applied in assessing the

insurable interest are of great importance. It is not the legal or beneficial

interest as in the case of marine and fire insurance, but the person insuring

the life of the other must stand in such relationship as will justify a

reasonable expectation of advantage or benefit from the continuance of the

life of the person on whom the insurance is effected. The test applicable is

whether there was actual dependence of the person effecting the insurance

on the person whose life is insured, or he had an expectancy of some

advantage from the continued existence of the person insured.

The effect of the requirement of insurable interest in all contracts of

insurance seems to be two-fold. Its absence makes a contract of insurance

equivalent to a wager. Also the principle of indemnity cannot be applied

unless there be some interest in the subject-matter, because, the actual loss

alone will be indemnified. Thus it became a preventive of wagering

(323)

policies and also limited the amount recoverable to the loss sustained by

the assured.

Time for Insurable Interest11: Life insurance contract is not a

contract of indemnity, so the courts have viewed that the insured must

have insurable interest at the time when the policy is effected. It is

immaterial whether or not he latter ceases to have such interest. So

insurable interest need not to be exist at the time of claim.

(e) Principle of Utmost Good Faith :

In the case of ordinary commercial transaction the legal maxim

“caveat emptor” (meaning “let the purchaser beware”) prevails. In the

absence of an enquiry the other party to the contract is under no obligation

voluntarily to furnish detailed information regarding the subject matter of

the contract. It is, however, understood that one party to the contract

should not be misled by the other by any false declaration. All the same it

is open to both the parties to the contract to satisfy themselves and each

party is entitled to make the best bargain that he can make.

As a contrast to such commercial contracts the insurance contract is

dominated by the legal maxim “the utmost good faith”. The observance of

utmost good faith by the parties is vital to a contract of insurance.

Insurance is called an UBERRIMAE FIDEI contract because the parties

11 . Dalby Vs India and London Life Assurance and Co. 1854. Quoted by Arjunajatesan J. and

Vishwanathan T.R., in their book “Risk Management and Insurance – Concepts and Practices of Life and General Insurance”, Macmillan Publishers India Ltd., 2009, 39.

(324)

are required to conform to a higher degree of good faith than in the general

law of contract. Good faith and honesty though principles of equity and

justice are equally applicable to every agreement; yet, in contracts other

than insurance, the parties are free to settle their own terms. In a contract

of sale of goods CAVEAT EMPTOR is the principle and the seller has no

obligation to make known to the purchaser all facts that might affect his

decision. But in insurance there is something more than an obligation to

treat the insurer honestly and frankly.

Insurance being a device of risk transference stands on a separate

basis. The non-disclosure of a material fact by the assured whether

fraudulent or innocent, has the same effect of avoiding the contract. A

stringent duty is imposed on the assured to provide all the material facts

that might influence the decision of the insurer. The fact that the assured

believed as a reasonable man certain information as immaterial to the

purpose does not provide a defence. The materiality of a particular fact

will be considered independently of the belief of the assured. This

fundamental principle applies to all branches of insurance. It may be

summarized from one of the several judgments pronounced: “It is the duty

of the assured to disclose all material facts within their knowledge. In

cases of life insurance, certain specific questions are proposed as the points

affecting in general all mankind. But there may be circumstances also

affecting particular individuals, which are not likely to be known to the

(325)

insurer, and which had they been known, would no doubt, have been made

subject to specific enquiries.”

The onus of good faith lies equally on both the parties to the

contract, but in the nature of things the assured has to pay more particular

attention to the observance of the principles. The selection of a life for

insurance by the company depends to a large extent on the information

supplied by the proposer. As the company solicits proposals from the

general public whose members are total strangers to the company there is

an urgent need for disclosing all material facts within the knowledge of the

proposer to enable the company to come to a decision. The proposer has

within his knowledge all the facts, which are material to the risk. He is

morally and legally bound to disclose all matters, which in point of fact are

material to the contract.

The question as to which information is material to the contract is a

wide one. In case of dispute a court or a committee of arbitrators may

decide it. But this cannot certainly be left to the opinion of the proposer.

“Every circumstance is material which would influence the judgment of a

prudent insurer in fixing the premium or determining whether he will take

the risk”. This definition has been embodied in the Marine Insurance Act

of 1906 and is equally applicable to life insurance. Nevertheless, the

proposer is excused from explicitly disclosing certain facts. These are:

(1) What the insurer already knows,

(326)

(2) What the insurer ought to know,

(3) What the insurer waives being informed of,

(4) Features, which lessen the risk.

In an insurance contract each party acts on the good faith of the

other. If the proposer conceals or misrepresents material facts, the contract

is vitiated. Deliberate concealment or misrepresentation amounts to fraud,

and the policy is legally void. Innocent misstatement or misrepresentation

renders the policy voidable at the option of the insurer up to two years. In

practice, however, policies are usually allowed to continue, subject to

adjustment, if the company is satisfied that there was no intention on the

part of the assured to defraud it.

Incidental to our discussion of the subject is the consideration of

representations and warranties which we may now examine. As stated

before, full disclosure of material information having a bearing on the risk

is necessary on the part of the proposer. This is due to the principle of

uberrima fides that governs the insurance business. The statements made

by the proposer in the proposal form and his statement before a medical

examiner are in legal language, either representations or warranties.

A warranty in insurance is a statement or condition incorporated in

the contract relating to the risk, which the applicant presents as true and

upon which it is presumed that the insurer relied in issuing the contract.

Marine insurance, the first branch of insurance to develop commercially,

(327)

evolved the doctrine of warranty. The Marine Insurance Act, 1906

(England), gives the following definition of a warranty:

“A warranty is a statement by which the assured undertakes that

some particular thing shall or shall not be done, or that some condition

shall be fulfilled, or whereby he affirms or negatives the existence of a

particular state of fact.” This Act states further that “A warranty as above

defined is a condition which must be exactly complied with, whether it be

material to the risk or not.”

The other replies given by the proposer, which are not intended to

have the force of warranty, are known as representations. In life insurance

there is a recital clause by which the answers given in the proposal and the

replies made to the medical examiner are made the basis of the contract

and thereby given the effect of warranty. The present tendency of the

offices is to treat the replies as representation. Any misstatements are,

therefore, judged from this approach and if the company thinks that the

misstatement is material, that is, the knowledge of the correct statement

would have influenced the decision of the company adversely, the insurer

can seek to avoid the policy on the ground of non-disclosure or

misstatement and must also offer to return the premiums. The law courts

also do not favour any unfair rigidity in the interpretation of answers to the

questions in the proposal form. Even then it is always desirable on the part

(328)

of the proposer to warrant the answers to the best of his knowledge and

belief.

This materially safeguards his interests. A contract is vitiated when

it contains some flaw, which renders it legally of no effect. In life

insurance the breach of warranty voids a contract absolutely. The other

cases in which it becomes void are, mistake, illegality, fraud. In these cases

they vitiate the contract and is voidable at the option of the insurer. The

contract becomes voidable also on account of innocent misrepresentation

or non-disclosure. As stated above, if the insurer seeks to void the policy

he must show that the non-disclosure or misrepresentation was material to

the assessment of the risk and was of such a nature as would influence the

judgment of a prudent insurer.

We have just seen that a policy may be void on the ground of

mistake, fraud or illegality. It is also voidable at the option of the injured

party under certain circumstances. In such cases, the insurer may not pay

the whole sum assured, but may be bound to return the premiums already

paid. It is because if a policy is void ab initio the risk has never been

covered and, therefore, no premiums have been earned. On the other hand,

if the risk has once commenced under a valid policy, the entire premium is

deemed to have been earned by the insurer and the assured can claim no

return if under changed circumstances the contract is rendered void in

future. In cases where the insurer seeks to avoid a policy on grounds of

(329)

non-disclosure or misrepresentation, he is in equity bound to offer the

return of premiums, but in practice, life offices provide for the forfeiture of

all premiums paid.

To obviate the difficulties of the assured, the offices generally have

an indisputability clause in their policies and all answers given in the

proposal and the medical report become indisputable after a period of two

or three years. After this period the policy cannot be called into question

except on grounds of fraud and illegality. The above indisputability clause

has been made a part of the Insurance Act of 1938.

In contracts of utmost good faith, contracting parties are placed

under a special duty towards each other, not merely to refrain from active

misrepresentation but make full disclosure of all material facts within their

knowledge and the principle of caveat emptor has no place.

In saying that the utmost good faith be observed by both the parties

the salient feature to be noted is that ‘FIDES UBERRIMAE’ is not one

sided requirement. The duty lay not only upon the assured, but also upon

the underwriter.

The question of interest that sometimes arises in insurance cases is

whether a person can claim the insured amount by pleading ignorance to

the contents of a proposal to which he previously gave his signature. The

insured person must be held responsible for the untrue averment in the

application form which he signed, as the duty of making himself

(330)

acquainted with the contents of what he was signing lay upon the insured

person himself. It is a general proposition of law binding on every insured

person who merely puts his signature to forms in a language quite

unknown to him when these forms are filled in by an agent. Insurance

contracts are a special class of contracts, one of the distinctive features of

which is that they are based on the rocky foundation of utmost good faith.

Such good faith is not a matter of art, but has to be really and sincerely

appreciated by the insured...’ Insurance is a form of contract where an

onerous duty of disclosure surpassing the boundaries of the general law of

contract, is placed on the assured.

The obligation of utmost good faith operates generally in cases

where the assured has to answer the questions in the declaration form, the

contents of which he has understood clearly. It is submitted that the same

principle of good faith, should be applied even where the assured gives

answers without properly understanding the questions. In such cases the

insurance policy would stand to be avoided because (i) the insurance

company cannot be said to have consented to insure the life of the person

on the basis of the wrong information, although unwittingly given; (ii) the

obligation to provide the correct information should be the same whether it

is a case of non-disclosure by reason of the assured believing the facts are

immaterial or due to the reason of not knowing the proposal. Therefore, a

positive duty to know the contents of the insurance policy may be

(331)

imposed. A person cannot be in a better position with regard to the

requirement of good faith, merely because he is a stranger to the language

contained in a proposal form.

Under section 45 of the Insurance Act, 1938 in the case of life

insurance a two years’ time limit is imposed in bringing the validity of the

policy into question by the insurer on the ground of misstatements in

answers to questions in the proposal form or in any report or document

leading to the issue of the policy. Section 45 says that after the expiry of

two years from the date on which it was effected no policy of life

insurance be called in question by an insurer on the ground that a statement

made in the proposal for insurance or in any report of a medical officer, or

referee, or friend of the insured, or in any other document leading to the

issue of the policy, was inaccurate or false.

The insurer cannot avoid the consequences of the insurance contract

by simply showing inaccuracy or falsity of the statement made in the

proposal form but has to prove under section 45 that the life insurance

policy has been obtained by means of fraudulent misrepresentation. For

avoiding the policy on the ground of fraudulent concealment under the

provisions of section 45, “it must be convincingly shown that the matter in

question was knowingly concealed.” The insurer has also to show ‘(1) that

such statement was on a material matter or suppressed facts which it was

material to disclose’ and ‘(2) that it was fraudulently made by the

(332)

policyholder’ and ‘(3) that the policyholder knew at the time of making it

that the statement was false or that it suppressed facts which it was

material to disclose.’

The courts generally do not uphold the plea of the insurer that the

information given by the assured is fraudulent. In life insurance, the

liability of the insurers is dependent on human life, or on the happening of

some other contingency which is itself dependent on human life. The cover

afforded by the policy of life insurance is not restricted to loss by accident

as in other insurances but provides also against the death of the assured

from disease or other natural causes. The prime factor of risk lies not so

much in the happening of the death of the assured but relates to the

uncertainty of human life. The death of the assured though ‘most natural

event’ is uncertain as to the point of time at which it will happen.

Under an endowment policy the insurer promises to pay a fixed sum

on the death of the assured, or on the arrival of a specific date during the

life of the assured. This differs from strict life insurance because the event

insured may not be the death but the duration of life up to a specified date.

So to be inclusive of this type of insurance, namely, endowment policy,

life insurance may be broadly considered as a contract in any way relating

to human life.

In a wider sense, Life Insurance comprises any contract in which

one party agrees to pay a given sum upon the happening of a particular

(333)

event contingent upon the duration of human life, in consideration of the

immediate payment of a smaller sum or certain equivalent periodical

payments by another party. Life insurance is a special form of insurance

contract. It is a financial arrangement by which a man protects himself

and/or the members of his family against the contingencies of life. In a

contract of life insurance the agreement made by the insurer is to pay a

certain sum of money on the death of a person or on maturity and when

once fixed, it is constant and invariable.

Thus, the life insurance contract is a special contract with many

legal dimensions. In spite of its legal character, life insurance contract has

some ‘social value’ in the sense, it has to consider social realities and

economic limitation when offered to the general public. The life insurance

which has theoretical basis of providing security measure to the risk of

death considers the welfare of the family of the insured. Above all, it has

legal rigidity while such contracts are construed by the courts.

The principal legislation regulating the insurance business in India is

the Insurance Act, 1938 (hereinafter referred to as the Act), and the

recently enacted Insurance Regulatory and Development Authority

(hereinafter referred to as IRDA) Act, 1999. Apart from these, the

provisions of the Companies Act, 1956 are applicable to companies

carrying on insurance business. Further, insurance being a contract, the

provisions of the Indian Contract Act, 1872 are applicable to such

(334)

contracts. The subordinate regulations that need to be referred to are the

Insurance Rules, 1939, the Redressal of Public Grievances Rules, 1998 and

around 27 regulations framed by IRDA on various subjects ranging from

the Actuarial Report and Abstract Regulations to the Protection of the

Policyholders’ Interest Regulations, 2002.

The IRDA made a reference to the Law Commission of India 3, 4

years ago to make recommendations for the revision of the Insurance Act,

1938 and for consequential amendments thereto. The present exercise of

the Law Commission is confined to the restructuring of the Insurance Act,

1938 in the light of the changes in the insurance sector and the merging of

the sections of the IRDA Act, 1999 with the Act. One of the purposes of

this exercise is to bring a consistency among the various provisions placed

in different sections of the Act by putting them into a core provision

relating to a particular subject/topic. Another aspect is that with the

enactment of the IRDA Act, 1999 some provisions have been inserted in

the principal Act, the effect of which is to nullify some of the existing

provisions.

In fact merging of the provisions of the IRDA Act, 1999 would also

make it a comprehensive statute and would avoid multiplicity of

legislations for an industry. As such it would make it easier for the

insurers, insured, intermediaries and the public at large and the functioning

of the IRDA, and would also be of assistance in locating all the provisions

(335)

at one place. Moreover, some of the provisions of the Act are now dealt

with by the Regulations framed by the Authority and hence the same need

to be deleted from the principal Act to avoid duplication. The revised

legislation is intended to present a simplified and streamlined legal

framework to strengthen the IRDA, to promote insurance in liberalized era

and to protect interests of the policyholders. The report of the Law

Commission on the Revision of the Insurance Act, 1938 and the IRDA

Act, 1999 needs to be finalized and released at the earliest for the smooth

functioning of the Insurance Industry in the light of the present day

scenario.

LIFE INSURANCE POLICY DOCUMENT

The life insurance policy is there in this world from very beginning.

The mentality of people to have some protection against risk can be traced

back some 5000 years ago.12 There were not any documents to support the

insurance policies but still there were ways to promote it and also help the

people get protection against the risks in their lives. The definition of

insurance is to have coverage against a risk and if someone wants to

protect one’s life, he/she can purchase the life insurance policy.

Life insurance policy is a document which expresses the contract

between the insurer and the insured. Most of the insurance companies have

standard forms of policies with standardized policy conditions in respect of 12 . Desai G.R., “Life Insurance” Life insurance in India: its history and dimensions of growth,”

Macmillan India, 1973, 2.

(336)

various plans of assurance offered by them. The policy document, to be

enforceable by law, is to be signed by the competent authority and duly

stamped according to the Indian Stamp Act.13

One of the essential elements to make a valid contract is that the

objective has to be lawful. According to Section 10 of the Indian Contract

Act, all agreements are contracts, if they are made by free consent of

parties, competent to contract for a lawful consideration and with a lawful

object, and are not expressly declared by the Act to be void. The

expressions given below are equally applicable for a life insurance

contract.

CONTENTS OF A POLICY DOCUMENT

The proposal and declaration signed by the party form the basis of

contract of insurance. The form contains a schedule which gives all

essential particulars of the policy like name, address, plan of insurance,

premium, amount of insurance, etc. On the back of the policy, the

standardized terms and conditions applicable to all persons insuring under

a particular plan are printed. Any special conditions imposed are indicated

by endorsement.

Some of the most common and important conditions and privileges

which form a part of the policy document, and their significance, are

narrated below:

13 . Prabhakara G., “Life Insurance Contract”, The IRDA Journal, Volume-V, No.4, March 2007, 23.

(337)

Days of Grace14

Days of grace or grace period is the ‘extra time’ given to the

policyholder for payment of instalment premium after the due date, during

which the policy remains in force. It is normally provided for a period of a

fortnight to a month. Grace period is meant to be a convenience to the

policyholders, some of whom may not be able to pay the premiums on

time due to certain preoccupations etc.

Revival of Policies15

A lapsed policy can be brought back to life through revival, as if it is

a fresh contract, subject to certain restrictions with regard to the period of

lapse etc. The policyholder may however be required to submit a fresh set

of medical and other requirements/declarations at the time of revival. For

the purpose of a claim too, the policy may be treated as new and Sec.45 of

the Insurance Act, 1938 be applied.

Surrender and Paid-up-value16

Sec.113 of the Insurance Act provides for accrual of certain

benefits to policyholders even if they are unable to keep their policies in

full force by payment of further premiums. If premiums for at least three

consecutive years have been paid, there shall be a guaranteed surrender

14 . Gulati Neelam C., “Principles of Insurance Management: A Special Focus on Indian Insurance

Sector-Pre and Post Liberalisation”, Excel Books, New Delhi, 2007, 120. 15 . Krishnaswamy G., “A Textbook on Principles and Practice of Life Insurance”, Excel Books, New

Delhi, 2009, 170. 16 . Kenneth Black, Jr. and Harold D.Skipper, Jr., “Life and Health Insurance”, Dorling Kindersley

(India) Pvt. Ltd., Noida, Thirteenth Edition, 2008, 238.

(338)

value. If the policy is not surrendered, it shall subsist as a paid up policy

for reduced sum. The policy conditions usually provide for a more liberal

surrender value and paid up value than those secured by the statutory

provisions.

Policy Loans17

Policy loan is a ready source of borrowing to a policyholder, in a

financial contingency. It is paid by insurers against the surrender value

accrued to a policy. Policy loans lend liquidity to contracts which are

otherwise ‘frozen’ during the term of the policy. From the insurers’ point

of view, they add to the marketability of the insurance products while also

being an avenue for secure investments.

Non-Forfeiture Regulations18

While grace period is meant to be a convenience, non-forfeiture

regulations provide succour to policyholders who are unable to pay

premiums due to temporary financial difficulties. Non-forfeiture

regulations allow additional time of, say, six months or a year for payment

of premiums on a policy, even as the risk under the policy continues to be

covered. Insurers offer this privilege after the policy has been in force for a

few years and is not offered on term assurance and some of the ‘high risk

cover’ policies.

17 . Rejda George E., “Principles of Risk Management and Insurance”, Tenth Edition, Dorling

Kindersley (India) Pvt. Ltd., Noida, 2011, 118. 18 . Tyagi C.L. and Tyagi Madhu, “Insurance Law and Practice”, Atlantic Publishers and Distributers

(P) Ltd., New Delhi, 2007, 58.

(339)

Riders: It is possible to tag-along coverage of additional risks to the

basic life product on payment of additional premiums, subject to certain

conditions and restrictions. Such add-ons like accident riders, critical

illness riders, premium waiver riders in case of minor life policies etc. are

quite popular and more such riders are coming into vogue. Riders are

complex by nature and are often not properly/fully understood by the

parties concerned. This causes complaints and legal disputes at the time of

claims and calls for defining and interpreting the coverages and exclusions

sharply. The most popular and perhaps the most ancient of all the riders is

the accident benefit rider which provides for payment of additional sum

assured in the event of death or permanent disability by accident.

Suicide Clause19

As per Indian law suicide is not a crime, but attempt to suicide is a

crime unlike in English law where suicide is a crime. Hence, contracts of

insurance that agree to pay the sum assured even in the event of the death

of life assured due to suicide are not against public policy. But, to avoid a

possible moral hazard and adverse selection, insurance companies do place

a restrictive clause by not covering death as a result of suicide up to one

year from the date of commencement of policy or date of issuing of policy

whichever is later.

19 . Rejda George E., “Principles of Risk Management and Insurance”, Tenth Edition, Dorling

Kindersley (India) Pvt. Ltd., Noida, 2011, 246.

(340)

However, provided a due notice is received, life insurers protect the

bonafide interests of the third parties who are having an interest in the life

of the life assured. While the former dissuades the life assured to be not

magnetic of the benefits of life assurance by committing suicide, the later

protects the financial interests of third parties as life insurance policies are

also used as tools of collateral security.

Pregnancy Clauses20

On life insurance policies issued during the pregnancy of a female

proponent, life insurers apply this clause to exclude coverage of

pregnancy/child birth related deaths. However, with the advancement of

medical technology, the relevance of these clauses is gradually reducing.

But, life insurers may apply these clauses to those female lives who reside

away from medical facilities that are potentially prone to risks of

pregnancy/child birth related deaths. If data pertaining to pregnancy risk in

a particular region is not available, insurers may apply these clauses to the

female lives of the region.

Specific clauses on female lives21

Certain classes on female lives such as females in the age group of

20-35 who have no earned income are susceptible to moral hazard. To

20 . Kenneth Black, Jr. and Harold D. Skipper, Jr., “Life and Health Insurance”, Dorling Kindersley

(India) Pvt. Ltd., Noida, Thirteenth Edition, 2008, 242. 21 . Sashidharan K. Kutty, “Managing Life Insurance”, Prentice Hall of India Pvt. Ltd., New Delhi,

2008, 282.

(341)

avoid this risk, insurance companies do impose these clauses excluding

coverage of accidental death in other than public places.

Occupation related clauses22

To exclude the risks that are closely related to the occupation (like

that of a pilot whose occupation is prone to aviation risks) of the life

assured, insurance companies do levy these clauses excluding the risk

coverage owing to the death of the life assured during the course of

employment. Ex: Aviation clause, divers' clause.

Lien Clause23

In respect of certain types of high risk life insurance policies where

insurers have a lower level of comfort due to the adverse disclosures made

in application for life insurance and where insurance coverage cannot be

denied based on such disclosures, life insurance companies do impose lien

clause which could either limit the liability of the insurer during a specified

period (like 50% of sum assured during first year, 75% in the second year

and 100% from the third year onwards); or defer the coverage for a

specified period (like no life cover during first year of the policy). Life

insurers also reserve the right to impose a clause during the term of the

policy through a clause based on the future occupation that a minor life

may engage in. Under the current clause, insurers require the minor life to

notify them in the event of minor life engaging in hazardous occupations. 22 . Ibid, 282. 23 . Ibid, 519.

(342)

On receipt of information from the life assured on his reaching the

majority or on his joining the services of hazardous occupations, life

insurers may apply such occupational clauses as deemed necessary. Hence,

policies issued to minor lives will be subject to these clauses.

Reg.6 of the IRDA (PPI), 200224 exclusively deals with matters to

be stated in a life insurance policy and includes important items such as:

• Name of the plan and whether it is participating in profits or not.

• Benefits payable and contingencies upon which these are payable

• Details of the riders attaching to the main policy

• The premiums payable, periodicity, grace period, implication of

discontinuing the payment of an instalment of premium and

provisions of a guaranteed surrender value.

• Age at entry and admission status, policy requirements for

surrender, non-forfeiture and revival of lapsed policies.

• Exclusions, both in respect of main policy and riders

• Provisions for nomination, assignment and policy loans and

statement about rate of interest on policy loans.

• Special clauses such as suicide clause, first pregnancy clause etc.

• Address of the insurer.

• Documents normally required to be submitted by a claimant in

support of a claim.

24 . IRDA (Protection of Policyholders’ Interests) Regulations, 2002, IRDA.

(343)

• Reg. 6(2) refers to the 15 days period available to the policyholder

to review the terms and conditions and where he disagrees to the

same, to return the policy.

Unit Linked Insurance Policies25

The advent of unit linked insurance policies has created new issues

with regard to policy conditions and privileges of the policyholder apart

from issues on disclosures. To overcome these issues, IRDA came out with

its guidelines in Dec 2005 which mandate, among others, that the

following be mentioned prominently on a policy bond:

• The minimum and maximum percentage of the investments in

different types (like equities, debt etc.)

• The definition of all applicable charges, method of appropriation of

these charges and the quantum of charges that are levied

• The maximum limit up to which the insurer reserves the right to

increase the charges subject to prior clearance of the Authority

• On top of the policy document, wherever applicable, the statement

'In this policy, the investment risk in investment portfolio is borne

by the policyholder'.

At present as many as twenty four life insurance companies are

operating in India and each one is issuing policy formats with different

25 . IRDA, “Life Insurance Products: Guidelines for Unit Linked Life Insurance

Products”, Circular No. 032/IRDA/Actl/Dec-2005, Dated: 21/12/05.

(344)

variations. 26 As there is no uniformity, it is difficult for the market as well

as policyholders to comprehend and make reasonable comparisons of

terms and conditions, privileges and benefits offered by different insurers.

Hence, it is worthwhile that a serious attempt is made at the earliest to

reduce the complexities of the policy bond with a judicial standardisation

which provides much needed solution without compromising the

competitive spirit of the market.

Conclusion:

Life insurance is a contract between the insured and the insurer,

imposing rights and obligations on both. The contract cover death,

disability, granting of annuities and capital redemption. The provisions and

practices underlying the contract are not entirely mandated by the

Insurance Act or other legislation but rather have their origins in common

law. Contract features like offer and acceptance, parties to the contract,

lawful consideration, consensus ad idem and legality of object are

common. But life insurance also has some special contract features like

that of adhesion and the principle of utmost good faith. The law indeed

subjects insurance contracts to a higher obligation – good faith contracts

become utmost good faith contracts when it comes to insurance the insured

is duty bound to disclose all material facts. A material fact has been

26 . U. Jahawaharlal, “Simple and Sweet – Success Mantra in Product Wording”, IRDA

Journal, April, 2012, IRDA, Mumbai, 14.

(345)

defined as a fact that would affect the judgement of a prudent underwriter

in deciding whether to accept the risk and if so, at what rate of premium

and subject to what terms and conditions. Breaches of utmost good faith

may occur via non-disclosure or misrepresentation. Section 45 of the

Insurance Act provides that a contract can be repudiated by the insurer for

breach of utmost good faith only on proving that the insured had

knowingly and with mall-intention sought to deceive the insurer.

The proposal for life insurance includes a number of documents

such as the proposal form, the confidential report of the agent and moral

hazard reports by other branch officials, medical examination reports,

motor vehicle records, and other inspection reports age proof. The life

insurance policy has three parts – the policy schedule, which gives specific

details of the contract between insured and insurer; the standard provisions

that define the rights, privileges and other conditions, which are applicable

under the contract; and the specific provisions that are generally linked to

the particular contract between the insurer and the insured.

Some of the standard provisions contained in life insurance contracts

are grace period, provision in the event of misstatement of age, lapse and

reinstatement, on-forfeiture provisions, surrender value and loan option,

suicide clause, double accident and permanent disability benefits. The

policy also provides certain rights to policy holders such as nomination

(346)

and assignment, alteration, issue of duplicate policy and creation of trust

under MWP Act. The contracts are subject to exchange control regulations.

A low level of awareness further supplemented by a huge

complexity in contractual wording only adds to the initial hesitancy from

the applicant. It is one thing to mean steadfastness in one's dealing, but

altogether a different case in being explicitly so. Simple and plain contracts

would not only put the average buyer in a great deal of comfort and ease

but would certainly add to a check on frauds.