2019 beverage alcohol trend analysis · growth in health & wellness (added-value and pet water)...

TRANSCRIPT

2019Beverage Alcohol

Trend Analysis

April 30, 2019

-2-

Unique Beverage Industry Expertise for Providing “Added-Value” to Selected Clients

Beverage Marketing Capabilities

Cutting Edge Insights: New Age Emergence, Multiple Beverage Competition, Specialty Beer Opportunity, Bottled Water Dominance, Hyper-Category

Competition, Micro-Marketing Age

Beverage Marketing Corporation utilizes an integrated model for providing information, analysis and advice to beverage industry clients

-3-

Beverage Marketing Capabilities

All data in this presentation is supplied by:

-4-

2019 Beverage Alcohol Trend Analysis

All data is Beverage Marketing Corporation data

Data is compiled from industry surveys

Data measures all channels so provides a total market perspective

Most importantly… BMC data is

-5-

Ag

en

da

Multiple Beverage Industry Trends

Beer Update

Spirits Update

Wine Update

2019 Beverage Alcohol Trend Analysis

Alternative Beverage Alcohol (ABA)

-6-

Ag

en

da

Multiple Beverage Industry Trends

Beer Update

Spirits Update

Wine Update

2019 Beverage Alcohol Trend Analysis

Alternative Beverage Alcohol (ABA)

-7-

Beverage Headlines

State of the Industry – The Good and the Bad

2019 Multiple Industry Trends

Total U.S. beverage market grew for fifth consecutive year in 2018, and saw slightly accelerated

growth over 2017

Carbonated soft drinks (CSDs) experienced improved performance in 2018 but declined slightly for the 14th consecutive year

Bottled water widened its gap over CSDs as the largest beverage category in the U.S., driven primarily by the single-serve PET segment

Niche categories continue to outperform traditional mass-market categories with exception of bottled water --- continued market fragmentation

Wine and spirits led alcohol growth in 2018, and beer volume continued to decline around 1%

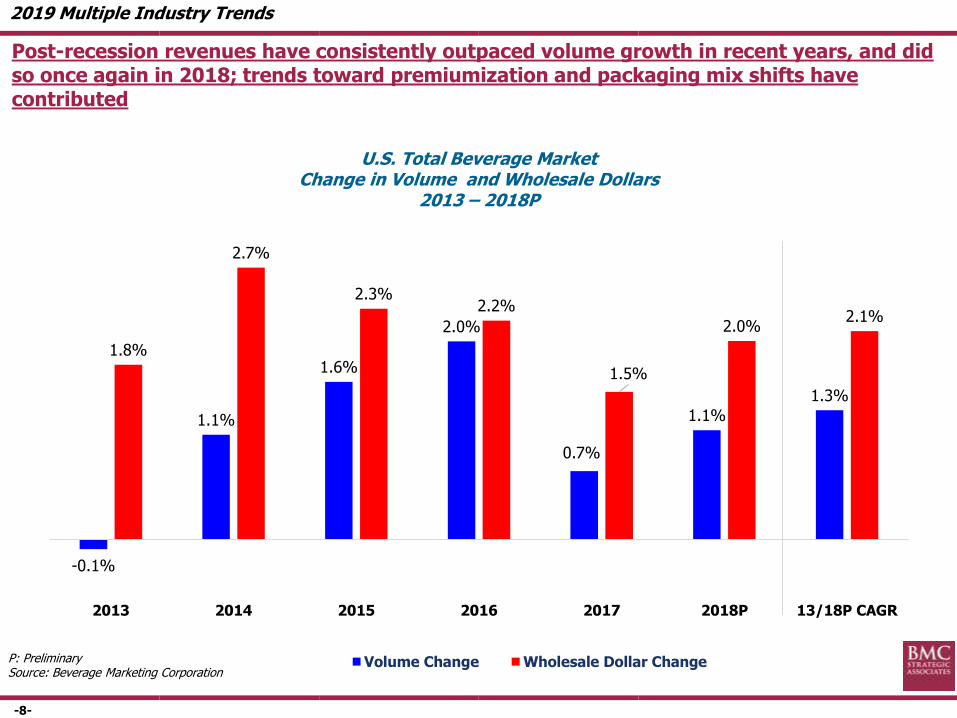

-8-

P: PreliminarySource: Beverage Marketing Corporation

U.S. Total Beverage MarketChange in Volume and Wholesale Dollars

2013 – 2018P

Post-recession revenues have consistently outpaced volume growth in recent years, and did so once again in 2018; trends toward premiumization and packaging mix shifts have contributed

-0.1%

1.1%

1.6%

2.0%

0.7%

1.1%

1.3%

1.8%

2.7%

2.3%2.2%

1.5%

2.0%2.1%

2013 2014 2015 2016 2017 2018P 13/18P CAGR

Volume Change Wholesale Dollar Change

2019 Multiple Industry Trends

-9-

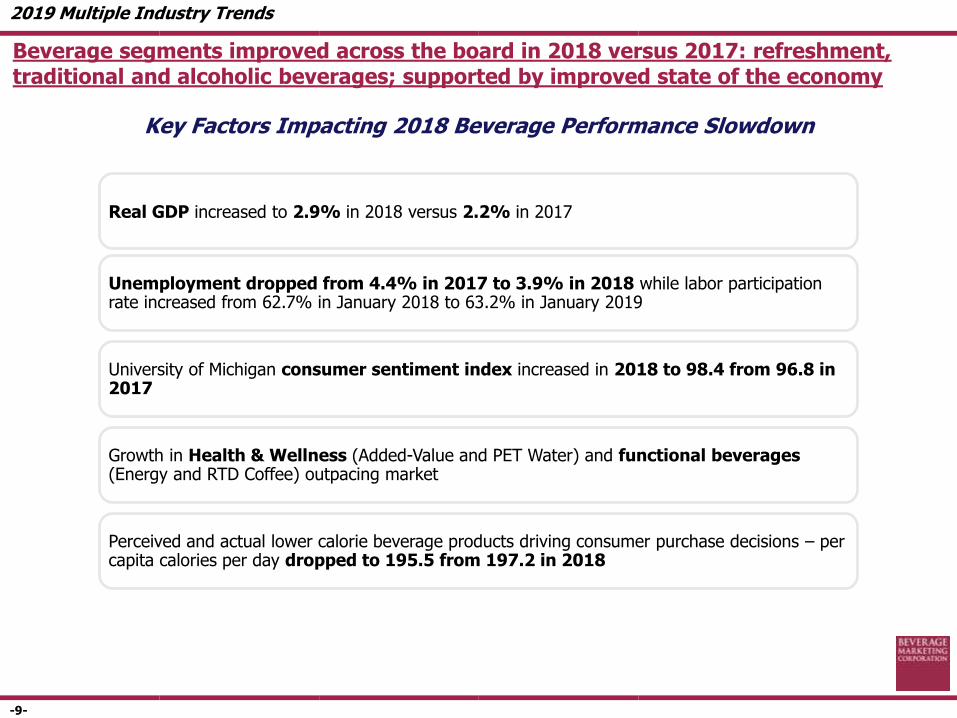

Key Factors Impacting 2018 Beverage Performance Slowdown

Beverage segments improved across the board in 2018 versus 2017: refreshment, traditional and alcoholic beverages; supported by improved state of the economy

Real GDP increased to 2.9% in 2018 versus 2.2% in 2017

Unemployment dropped from 4.4% in 2017 to 3.9% in 2018 while labor participation rate increased from 62.7% in January 2018 to 63.2% in January 2019

University of Michigan consumer sentiment index increased in 2018 to 98.4 from 96.8 in 2017

Growth in Health & Wellness (Added-Value and PET Water) and functional beverages (Energy and RTD Coffee) outpacing market

Perceived and actual lower calorie beverage products driving consumer purchase decisions – per capita calories per day dropped to 195.5 from 197.2 in 2018

2019 Multiple Industry Trends

-10-

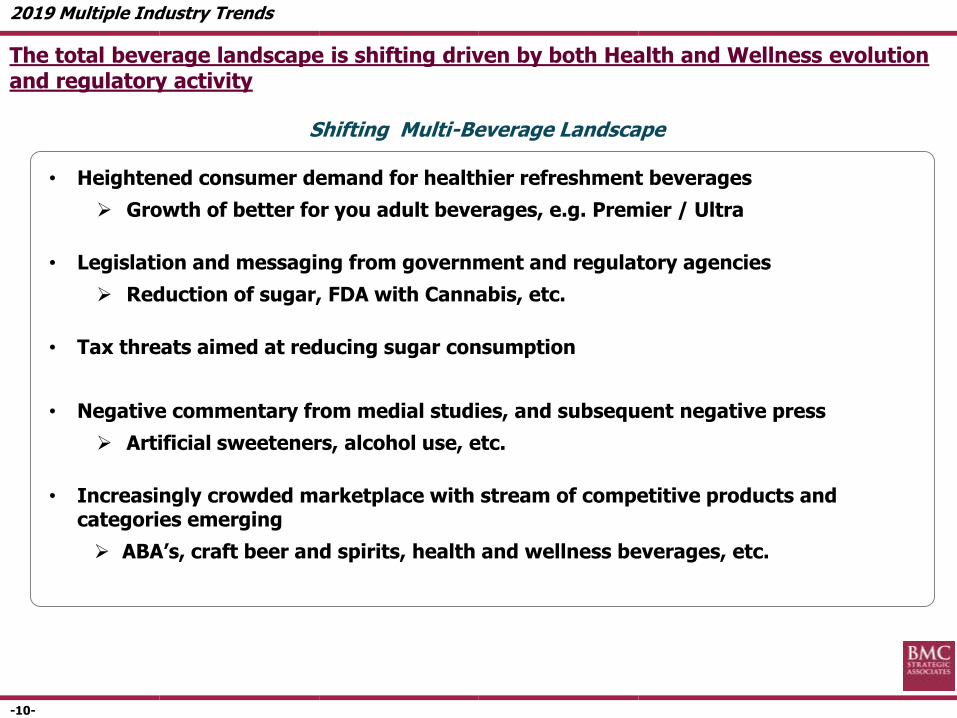

Health and Wellness / Functionality

The total beverage landscape is shifting driven by both Health and Wellness evolution and regulatory activity

Shifting Multi-Beverage Landscape

• Heightened consumer demand for healthier refreshment beverages

Growth of better for you adult beverages, e.g. Premier / Ultra

• Legislation and messaging from government and regulatory agencies

Reduction of sugar, FDA with Cannabis, etc.

• Tax threats aimed at reducing sugar consumption

• Negative commentary from medial studies, and subsequent negative press

Artificial sweeteners, alcohol use, etc.

• Increasingly crowded marketplace with stream of competitive products and categories emerging

ABA’s, craft beer and spirits, health and wellness beverages, etc.

2019 Multiple Industry Trends

-11-

Ag

en

da

Multiple Beverage Industry Trends

Beer Update

Spirits Update

Wine Update

2019 Beverage Alcohol Trend Analysis

Alternative Beverage Alcohol (ABA)

-12-

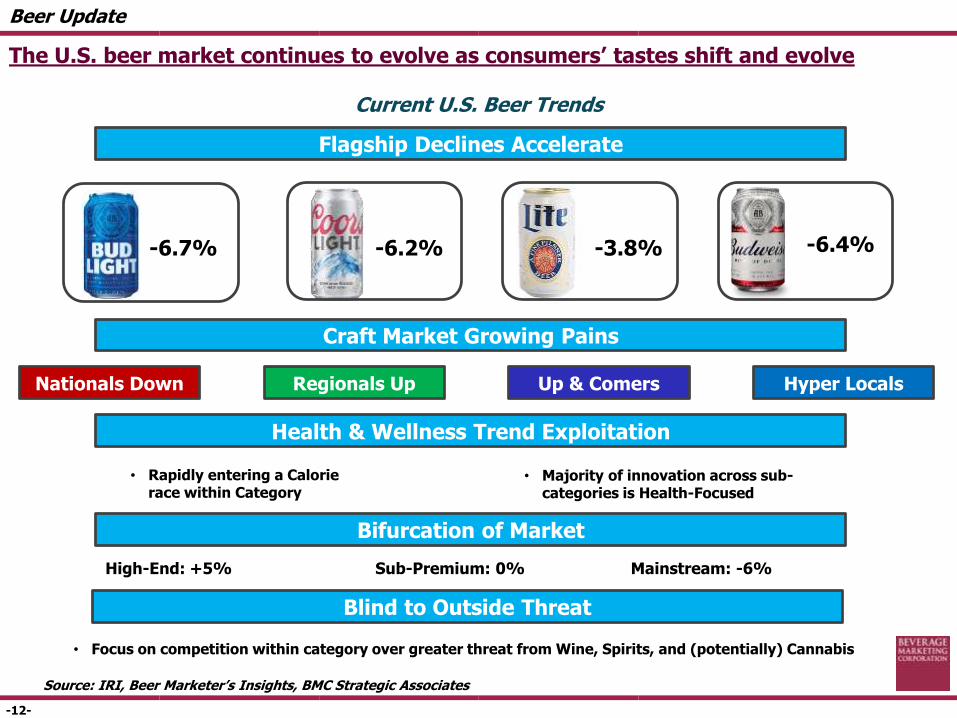

Current U.S. Beer Trends

The U.S. beer market continues to evolve as consumers’ tastes shift and evolve

Beer Update

Flagship Declines Accelerate

-6.7% -6.2% -3.8% -6.4%

Craft Market Growing Pains

Nationals Down Regionals Up Up & Comers

Health & Wellness Trend Exploitation

• Rapidly entering a Calorie race within Category

• Majority of innovation across sub-categories is Health-Focused

Bifurcation of Market

High-End: +5% Sub-Premium: 0% Mainstream: -6%

Source: IRI, Beer Marketer’s Insights, BMC Strategic Associates

Hyper Locals

Blind to Outside Threat

• Focus on competition within category over greater threat from Wine, Spirits, and (potentially) Cannabis

-13-

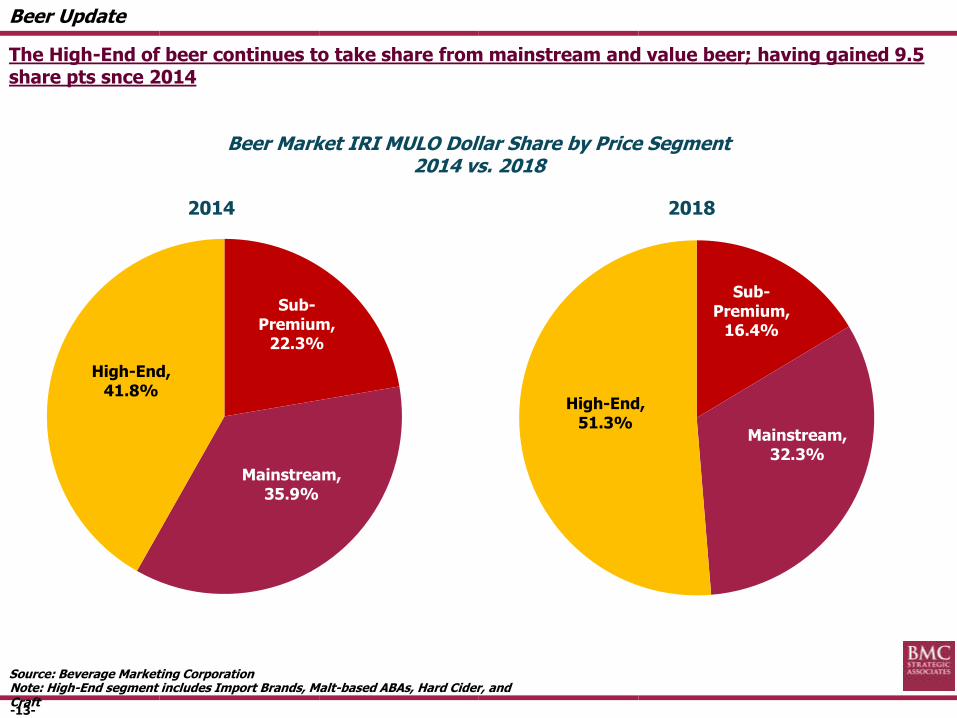

Sub-Premium,

16.4%

Mainstream, 32.3%

High-End, 51.3%

Beer Market IRI MULO Dollar Share by Price Segment2014 vs. 2018

Note: High-End segment includes Import Brands, Malt-based ABAs, Hard Cider, and Craft

The High-End of beer continues to take share from mainstream and value beer; having gained 9.5 share pts snce 2014

Source: Beverage Marketing Corporation

Sub-Premium,

22.3%

Mainstream, 35.9%

High-End, 41.8%

20182014

Beer Update

-14-

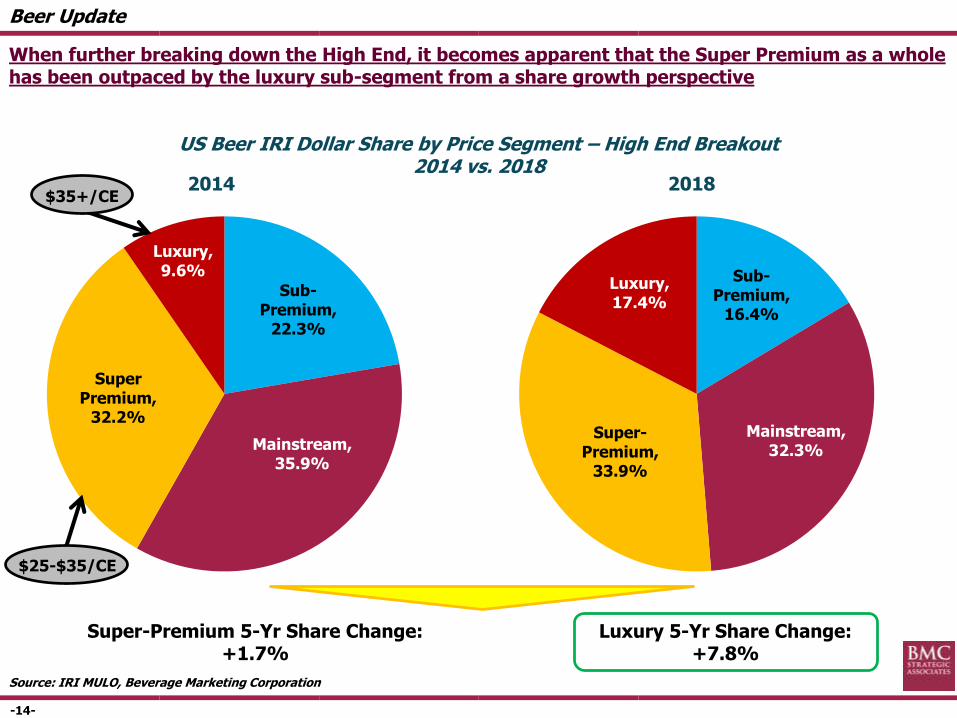

Sub-Premium,

16.4%

Mainstream, 32.3%

Super-Premium,

33.9%

Luxury, 17.4%

US Beer IRI Dollar Share by Price Segment – High End Breakout2014 vs. 2018

2018

When further breaking down the High End, it becomes apparent that the Super Premium as a whole has been outpaced by the luxury sub-segment from a share growth perspective

Source: IRI MULO, Beverage Marketing Corporation

2014

Sub-Premium,

22.3%

Mainstream, 35.9%

Super Premium,

32.2%

Luxury, 9.6%

Super-Premium 5-Yr Share Change: +1.7%

Luxury 5-Yr Share Change: +7.8%

$25-$35/CE

$35+/CE

Beer Update

-15-

Mainstream Beer Losses

The total Beer (malt beverage and cider) shipments declined 0.9% in 2018; but when you eliminate FMB’s and Local Craft Beer, it is closer to 3.0%

Beer Update

*Standard Beer – Beer styles broadly available to consumersSource: BMCSA Analysis, IRI MULO, Beer Business Insights

2017 2018 Growth

Total Beer 2,861.0 2,835.3 -0.9%

Less FMBs 141.7 163.7 +15.5%

Historical Beer 2,719.3 2,671.6 -1.8%

Less Local Craft 173.3 201.1 +16.1%

Standard Beer 2,546.0 2,470.5 -3.0%

-16-

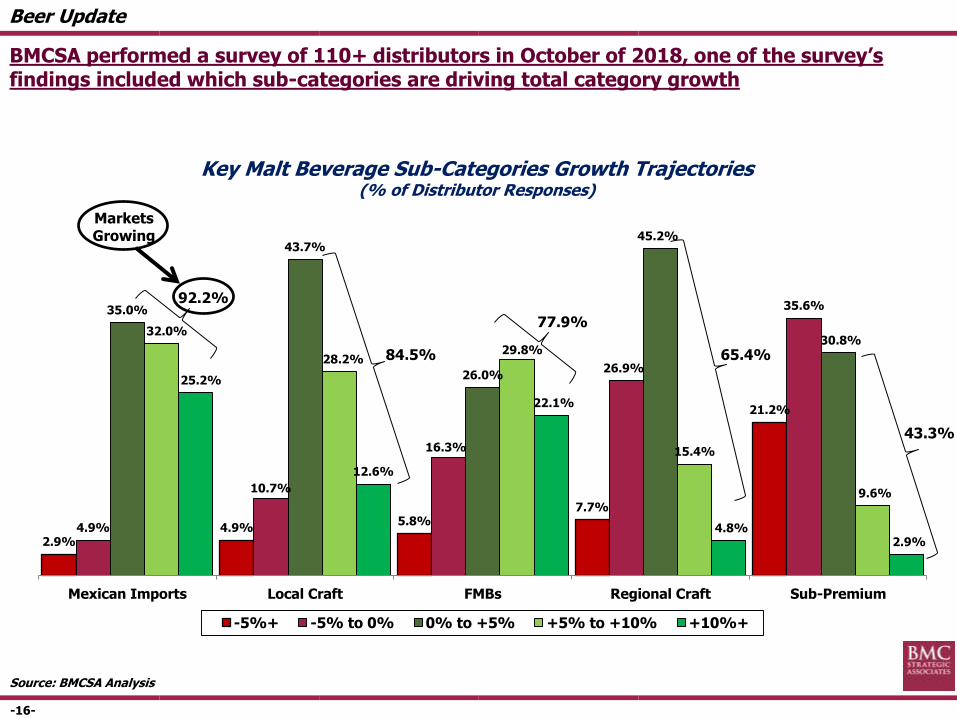

Key Malt Beverage Sub-Categories Growth Trajectories(% of Distributor Responses)

2.9%4.9%

5.8%7.7%

21.2%

4.9%

10.7%

16.3%

26.9%

35.6%35.0%

43.7%

26.0%

45.2%

30.8%32.0%

28.2%29.8%

15.4%

9.6%

25.2%

12.6%

22.1%

4.8%2.9%

Mexican Imports Local Craft FMBs Regional Craft Sub-Premium

-5%+ -5% to 0% 0% to +5% +5% to +10% +10%+

BMCSA performed a survey of 110+ distributors in October of 2018, one of the survey’s findings included which sub-categories are driving total category growth

92.2%

65.4%84.5%

77.9%

43.3%

Source: BMCSA Analysis

Markets Growing

Beer Update

-17-

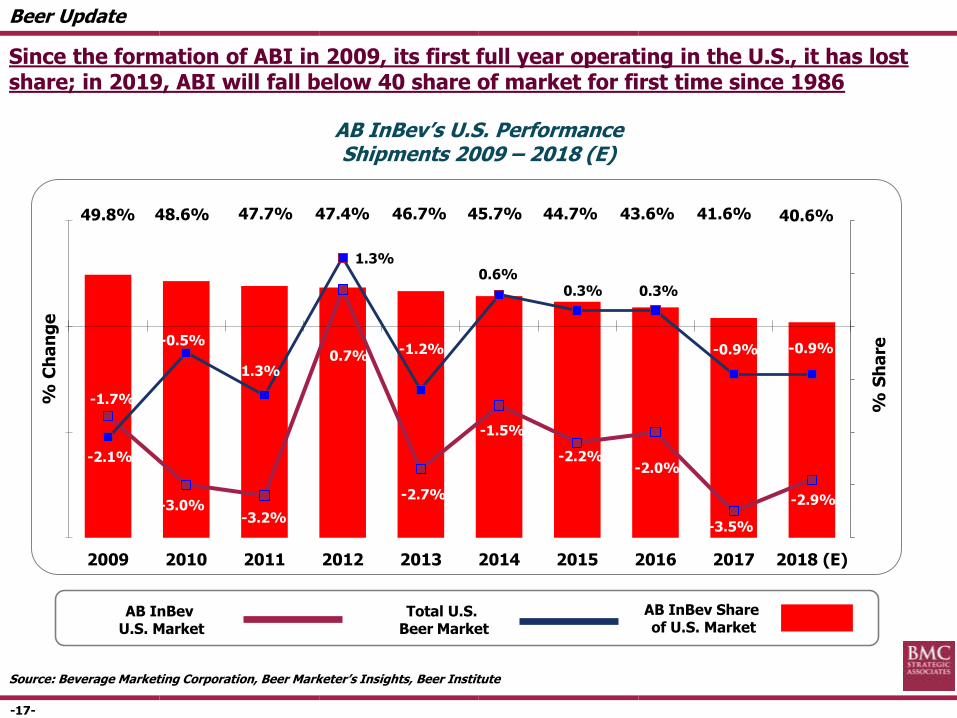

Since the formation of ABI in 2009, its first full year operating in the U.S., it has lost share; in 2019, ABI will fall below 40 share of market for first time since 1986

AB InBev’s U.S. Performance Shipments 2009 – 2018 (E)

Total U.S. Beer Market

AB InBev U.S. Market

49.8% 48.6% 47.7% 47.4% 46.7% 45.7% 44.7% 43.6% 41.6% 40.6%

-1.7%

-3.0%-3.2%

0.7%

-2.7%

-1.5%

-2.2%-2.0%

-3.5%

-2.9%

-2.1%

-0.5%

-1.3%

1.3%

-1.2%

0.6%0.3% 0.3%

-0.9% -0.9%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

-4.0%

-2.0%

0.0%

2.0%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 (E)

% C

ha

ng

e

% S

ha

re

AB InBev Share of U.S. Market

Source: Beverage Marketing Corporation, Beer Marketer’s Insights, Beer Institute

Beer Update

-18-

Since 2012, the top 4 brewers in the US have lost a combined 7.1 share points in aggregate; this would be worse without Constellation’s 4.5 point share gain

• Combined ABI, MC & HUSA have lost 15.8 share points over the same period; the overall share loss in 2018 for the top 4 was at its lowest level since 2013

Top 4 Brewer’s U.S. Share Change Shipments 2012 – 2018

% S

ha

re

Source: Beverage Marketing Corporation, Beer Marketer’s Insights, Beer Institute

47.4% 46.7% 45.7% 44.7% 43.6% 41.5% 40.6%

28.2% 28.2% 27.3% 26.5% 25.5%24.4% 23.5%

6.0% 6.5% 7.1% 7.8% 8.6%9.4% 10.5%

3.9% 3.9% 3.9% 4.0% 3.9%3.8% 3.7%

2012 2013 2014 2015 2016 2017 2018 E

85.5% 85.2% 84.0% 83.0% 81.6% 79.1% 78.4%

Down 6.8%

Down 4.7%

Up 4.5%

Down 0.2%

Down 7.1%

Share vs. ‘12

STZ Share of U.S. Market

HUSA Share of U.S. Market

MC Share of U.S. Market

ABI Share of U.S. Market

Beer Update

-19-

Ag

en

da

Multiple Beverage Industry Trends

Beer Update

Spirits Update

Wine Update

2019 Beverage Alcohol Trend Analysis

Alternative Beverage Alcohol (ABA)

-20-

Source: Beverage Marketing Corporation

U.S. Distilled Spirits Market2010 – 2018 (MM 9-L Cases)

192

199

206209

212

216

221

225

229

170

180

190

200

210

220

230

240

+3.5%

+2.0%

+3.1%

+1.5%

+1.5%

+1.9%

+2.4%

+1.8%

Spirits Update

2010 2011 2012 2013 2014 2015 2016 2017 2018

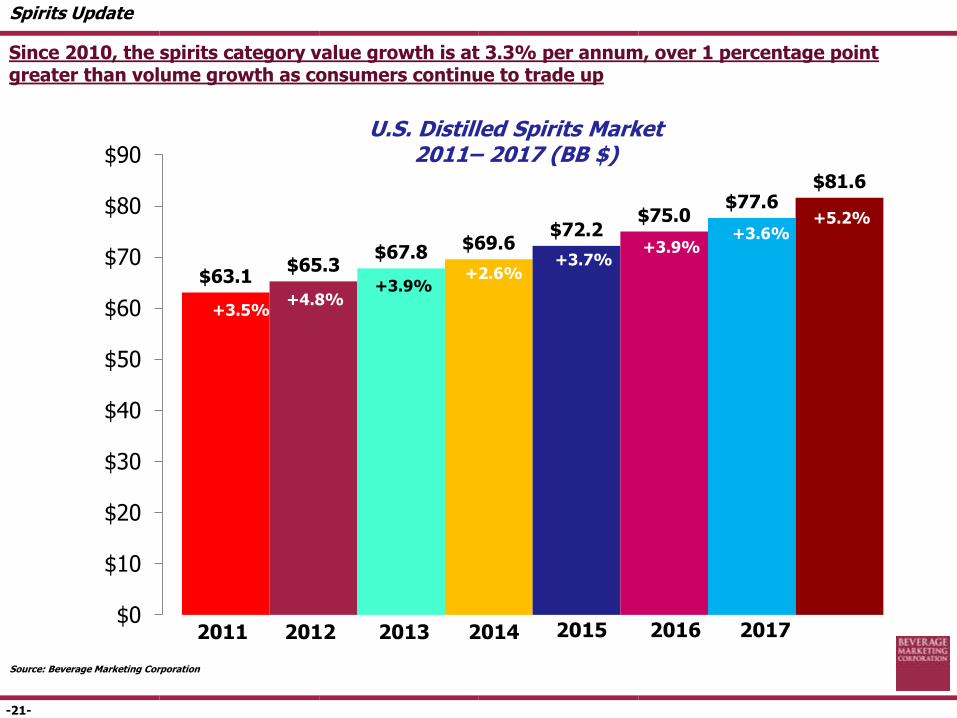

Since 2010, the spirits category has been the best performing of beer, wine and spirits; growing at an annual CAGR of 2.2% since 2010

-21-

Source: Beverage Marketing Corporation

U.S. Distilled Spirits Market2011– 2017 (BB $)

$63.1$65.3

$67.8$69.6

$72.2$75.0

$77.6$81.6

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

+3.5%

+5.2%

Spirits Update

2011 2012 2013 2014 2015 2016 2017

+4.8%

+3.7%+2.6%

+3.6%

+3.9%

+3.9%

Since 2010, the spirits category value growth is at 3.3% per annum, over 1 percentage point greater than volume growth as consumers continue to trade up

-22-

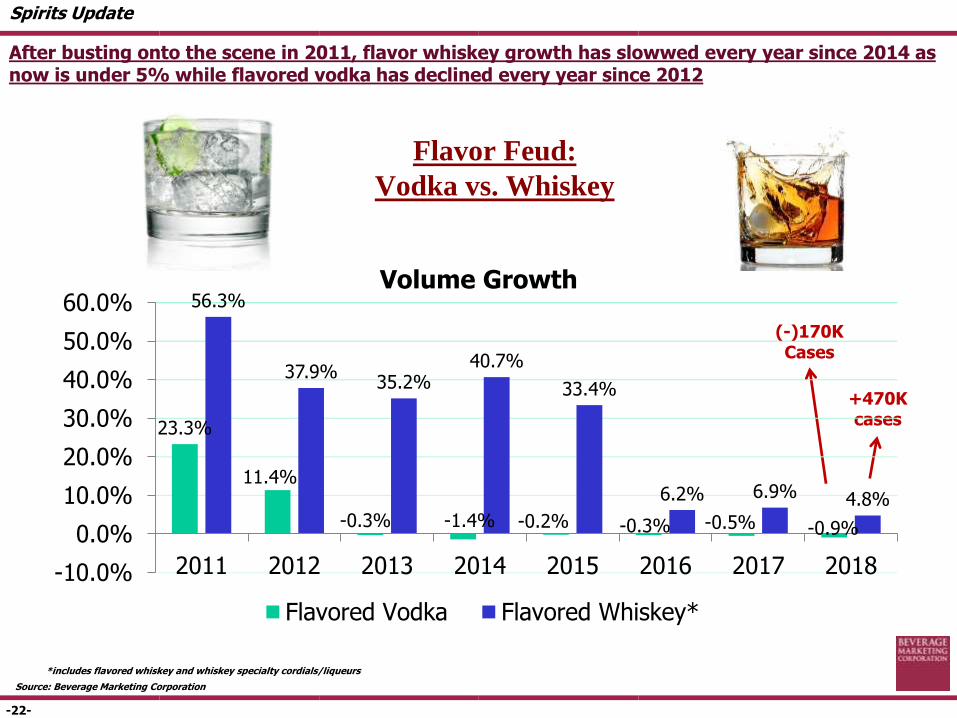

Flavor Feud:

Vodka vs. Whiskey

*includes flavored whiskey and whiskey specialty cordials/liqueurs

Volume Growth

Source: Beverage Marketing Corporation

+470Kcases

(-)170K Cases

Spirits Update

23.3%

11.4%

-0.3% -1.4% -0.2% -0.3% -0.5% -0.9%

56.3%

37.9%35.2%

40.7%

33.4%

6.2% 6.9% 4.8%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

2011 2012 2013 2014 2015 2016 2017 2018

Flavored Vodka Flavored Whiskey*

After busting onto the scene in 2011, flavor whiskey growth has slowwed every year since 2014 as now is under 5% while flavored vodka has declined every year since 2012

-23-

*includes flavored whiskey and whiskey specialty cordials/liqueurs

Source: Beverage Marketing Corporation

Spirits Update

Flavor Feud:

Vodka vs. Whiskey

7178

63

3226

20 1712

312

21 2515 12

7 30

20

40

60

80

100

2011 2012 2013 2014 2015 2016 2017 2018

Flavored Vodka Flavored Whiskey*

Product introductions

As growth of flavored whiskey and vodka has slowed, so has the number of new product introductions

-24-

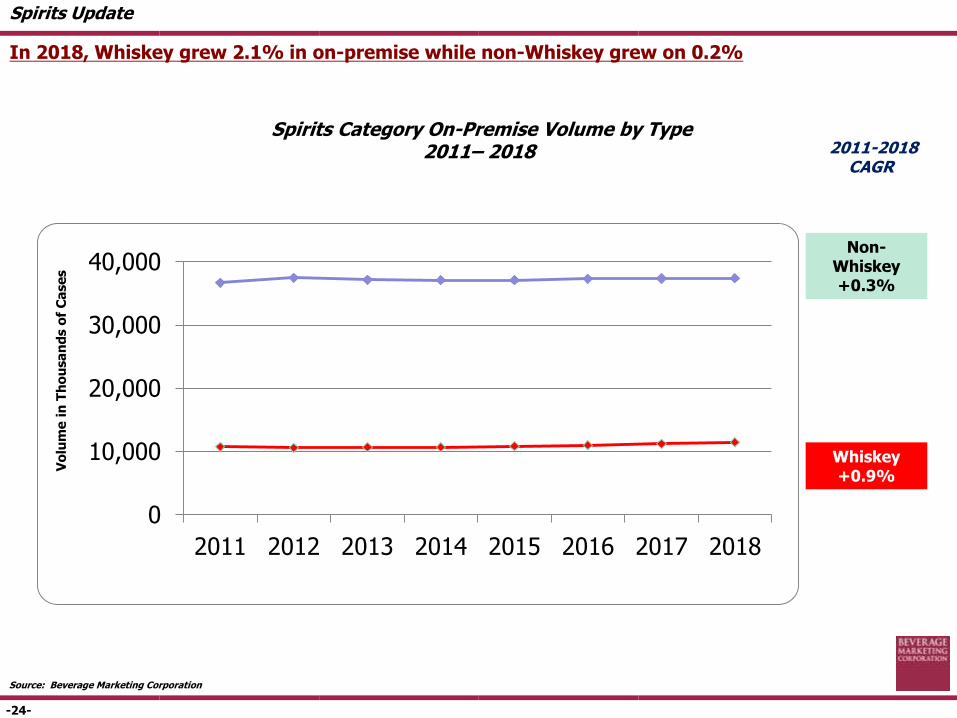

Source: Beverage Marketing Corporation

Spirits Category On-Premise Volume by Type2011– 2018 2011-2018

CAGR

In 2018, Whiskey grew 2.1% in on-premise while non-Whiskey grew on 0.2%

Spirits Update

Vo

lum

e i

n T

ho

usa

nd

s o

f C

ase

s

Non-Whiskey+0.3%

Whiskey+0.9%

0

10,000

20,000

30,000

40,000

2011 2012 2013 2014 2015 2016 2017 2018

-25-

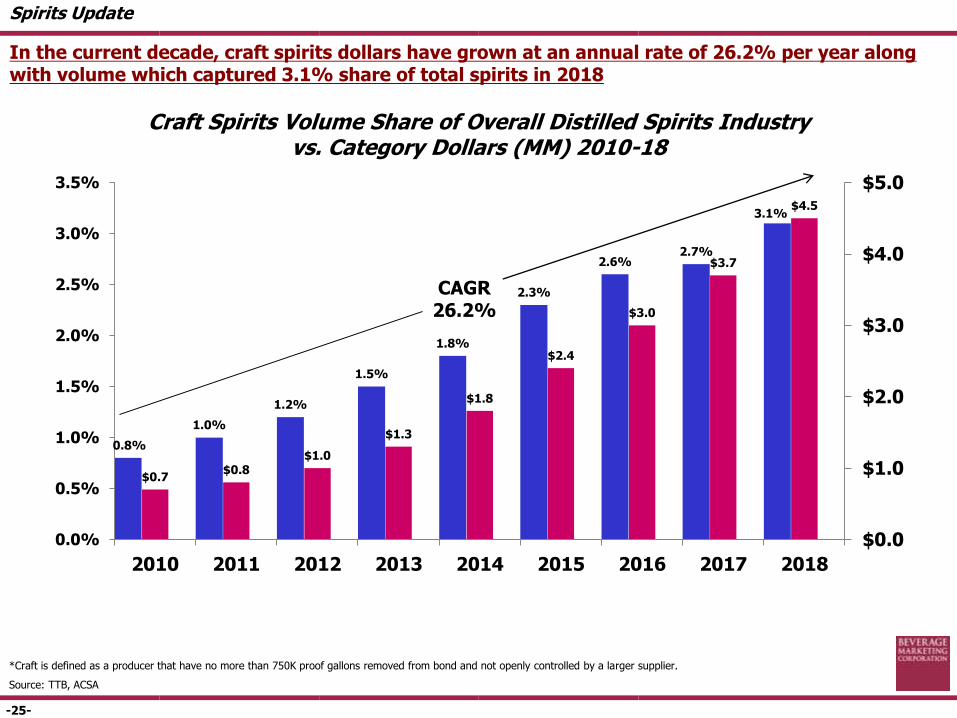

Craft Spirits Volume Share of Overall Distilled Spirits Industryvs. Category Dollars (MM) 2010-18

*Craft is defined as a producer that have no more than 750K proof gallons removed from bond and not openly controlled by a larger supplier.

Source: TTB, ACSA

0.8%

1.0%

1.2%

1.5%

1.8%

2.3%

2.6%2.7%

3.1%

$0.7$0.8

$1.0

$1.3

$1.8

$2.4

$3.0

$3.7

$4.5

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

2010 2011 2012 2013 2014 2015 2016 2017 2018

Spirits Update

CAGR26.2%

In the current decade, craft spirits dollars have grown at an annual rate of 26.2% per year along with volume which captured 3.1% share of total spirits in 2018

-26-

Source: Beverage Marketing Corp., Technomic Inc.

Spirits Update

Bars and full-service restaurants are top locations for adult beverage occasions

• Slowed consumer traffic on premise and stagnancy in occasions involving adult beverages translated to a slight 0.3% increase in total alcohol volume in restaurants and bars in 2018

Shifting on premise account performance

• Market strength is small independent full service restaurants while casual chain restaurants experience challenges. E-commerce sites, e.g. Uber Eats and Grub hub, are aiding at home consumption helping certain restaurants with food sales while hurting on premise alcohol sales

Aged spirits strength continues

• Aged Whiskey and Tequila continue to retain relevance with today’s consumers, especially in restaurants and bars

Vodka On Premise Struggles

• Although vodka remains the best selling spirit category in the on premise, more flavorful spirits such as whiskey continue to grow share in the channel. When vodka was strong, imported and flavor vodka lead the category. Today they are dragging down overall vodka performance.

Adult Beverage Consumer AttitudesOn Premise

In 2018, on premise volume increased 0.3% driven by strength of small independent full service restaurants. Whiskey continues to drive consumption at expense of Vodka

-27-

The industry is using innovation to keep up with changing consumer preferences

• Flavor continues to be a focus area for distillers along with aging which is used to promote uniqueness of offerings

• Using the flexibility of spirits, specialized cocktails are being made using specific types of new spirit styles created by craft distillers

Some examples of these products include new flavor launches such as:

• Sour cherry gin

• Peppermint flavored whiskey

• Hybrid products such as vodka with a blend of rose’ wine

There has also been an influx of different aging methods utilizing wine and beer barrels to produce unique flavor profiles, which include:

• Run finished in Vermouth casks

• Single malt whiskey aged in Ex=Bourbon barrels and finished in Oloroso Sherry casks

• Irish whiskey finished in stout barrels

• Straight whiskey finished in maple syrup barrels

Distiller’s Innovation focused on Aging and Flavors

Spirits Update

Innovation is being used in an attempt by distillers to keep ahead of consumers seeking greater and newer alternatives

-28-

Ag

en

da

Multiple Beverage Industry Trends

Beer

Spirits

Wine

2019 Beverage Alcohol Trend Analysis

Alternative Beverage Alcohol (ABA)

-29-

Wine Market Trends

• Domestic shipments were led by Prosecco as sparkling continued to outpace table wine

• Millennials have become a driving force in wine sales and now are largest consumer (1/3 of total)

These consumers are more adventurous and seek more variety than other wine consumers, looking for wines from outside the U.S. to include Portugal, South Africa, Greece and Austria

Social media and word of mouth recommendations have a big influence on this group

• Direct to Consumer sales hit a new high in 2018, +9% to 6.3 Million cases, but still represents only 1.7% share of total wine shipments

Since 2011, direct shipments to consumers have doubled. Growth is greatest in the $100 per bottle segment versus blow $30 per bottle which grew only 6% in 2018

• Over the past two years, wine volume growth has slowed dramatically while per bottle price increases have accelerated. With shifting demographics to younger consumers, price sensitivity becoming more prevalent

• Varietals that have experienced growth haven’t changed widely over the past couple years; the leading varietals remain Cabernet Sauvignon, Chardonnay and Rose

• Wines that have beverage cues are leading performance in category to include: Sparkling (refreshment), Fortified (alcohol delivery), Rosé (easy to drink) and RTD (convenience)

Wine Update

Wine consumers are becoming younger and looking for wines that perform more like beverages versus traditional wine offerings

-30-

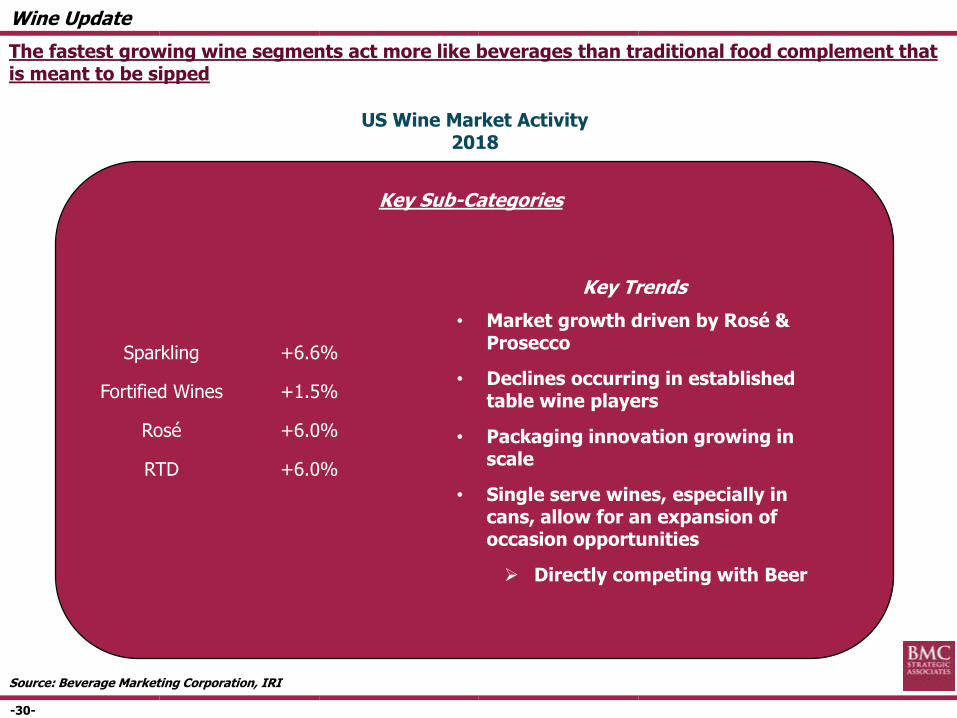

US Wine Market Activity2018

Key Sub-Categories

Sparkling +6.6%

Fortified Wines +1.5%

Rosé +6.0%

RTD +6.0%

Key Trends

• Market growth driven by Rosé & Prosecco

• Declines occurring in established table wine players

• Packaging innovation growing in scale

• Single serve wines, especially in cans, allow for an expansion of occasion opportunities

Directly competing with Beer

The fastest growing wine segments act more like beverages than traditional food complement that is meant to be sipped

Source: Beverage Marketing Corporation, IRI

Wine Update

-31-

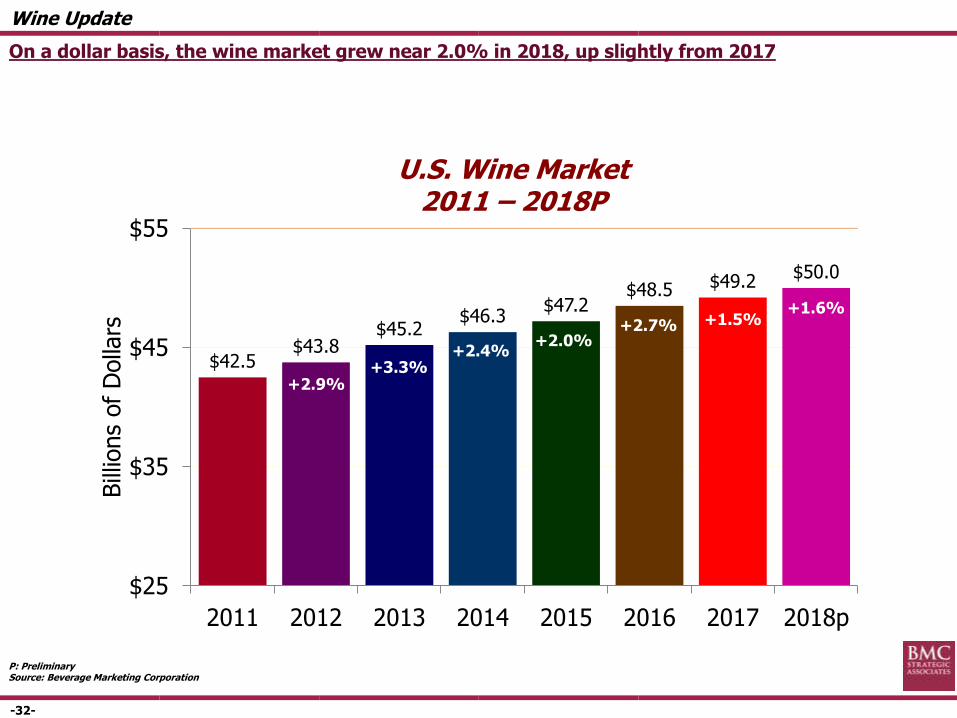

P: PreliminarySource: Beverage Marketing Corporation

U.S. Wine Market2011 – 2018P

338.1

345.6

353.1

357.8360.9

368.3370.0 370.5

320

330

340

350

360

370

380

2011 2012 2013 2014 2015 2016 2017 2018p

+1.4%

+0.9%

+2.0%

+2.2%

+0.5% +0.2%

Mill

ions

of

Nin

e L

iter

Case

s

+2.2%

The wine market volume growth has slowed over the past two years to near flat in 2018

Wine Update

-32-

P: PreliminarySource: Beverage Marketing Corporation

U.S. Wine Market2011 – 2018P

$42.5$43.8

$45.2$46.3

$47.2$48.5 $49.2

$50.0

$25

$35

$45

$55

2011 2012 2013 2014 2015 2016 2017 2018p

Bill

ions

of

Dolla

rs

+2.9%

+2.4%+2.0%

+2.7%

+3.3%

+1.5%+1.6%

On a dollar basis, the wine market grew near 2.0% in 2018, up slightly from 2017

Wine Update

-33-

11.3%

13.6%14.6%

19.1%18.3% 17.8%

15.3%17.7%

18.6%

27.1%

33.9%33.3%

27.2%

16.5% 15.7%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2011 2015 2018p

Super-Premium ($15.00 and above) Premium ($12.00-$14.99) Popular Premium ($9.00-$11.99)

Fighting Varietal ($6.00-$8.99) Value ($5.99 and below)

Table Wine Volume Sales by Price Tier 2011, 2015 & 2018p

Sweet spot for Millennial consumers

The super-premium segment continues to outperform consistent with trading up in other beverage alcohol segments while the popular premium, $9.00 - $11.99 appeals to millennials

Wine Update

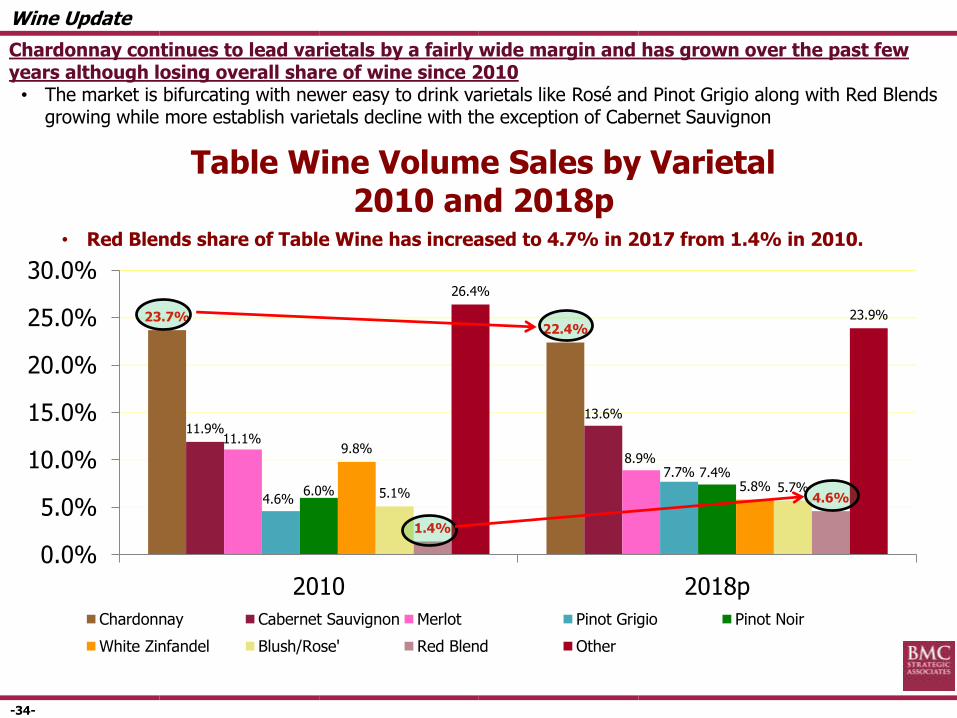

-34-

23.7%22.4%

11.9%13.6%

11.1%

8.9%

4.6%

7.7%

6.0%

7.4%

9.8%

5.8%5.1% 5.7%

1.4%

4.6%

26.4%

23.9%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

2010 2018p

Chardonnay Cabernet Sauvignon Merlot Pinot Grigio Pinot Noir

White Zinfandel Blush/Rose' Red Blend Other

Table Wine Volume Sales by Varietal2010 and 2018p

• Red Blends share of Table Wine has increased to 4.7% in 2017 from 1.4% in 2010.

Chardonnay continues to lead varietals by a fairly wide margin and has grown over the past few years although losing overall share of wine since 2010• The market is bifurcating with newer easy to drink varietals like Rosé and Pinot Grigio along with Red Blends

growing while more establish varietals decline with the exception of Cabernet Sauvignon

Wine Update

-35-

House wine varietals are selling athigh-end craft beer prices. Single serve offerings in can have exploded in the market

Health and Wellness / Functionality

Wine in a Can

ABI purchased a minority stake in Swish, makers of Babe Rosé in March 2018; product is gaining distribution and will compete in the alcohol refreshment space. Although small, the brand poses a potential threat to beer

Wine’s penetration into the ABA space is accelerating with cans and is positioned to source volume from female consumers

• Wine single-serve beverages at 15 million cases and growing mid to high single digits

Wine Update

-36-

Ag

en

da

Multiple Beverage Industry Trends

Beer Update

Spirits Update

Wine Update

2019 Beverage Alcohol Trend Analysis

Alternative Beverage Alcohol (ABA)

-37-

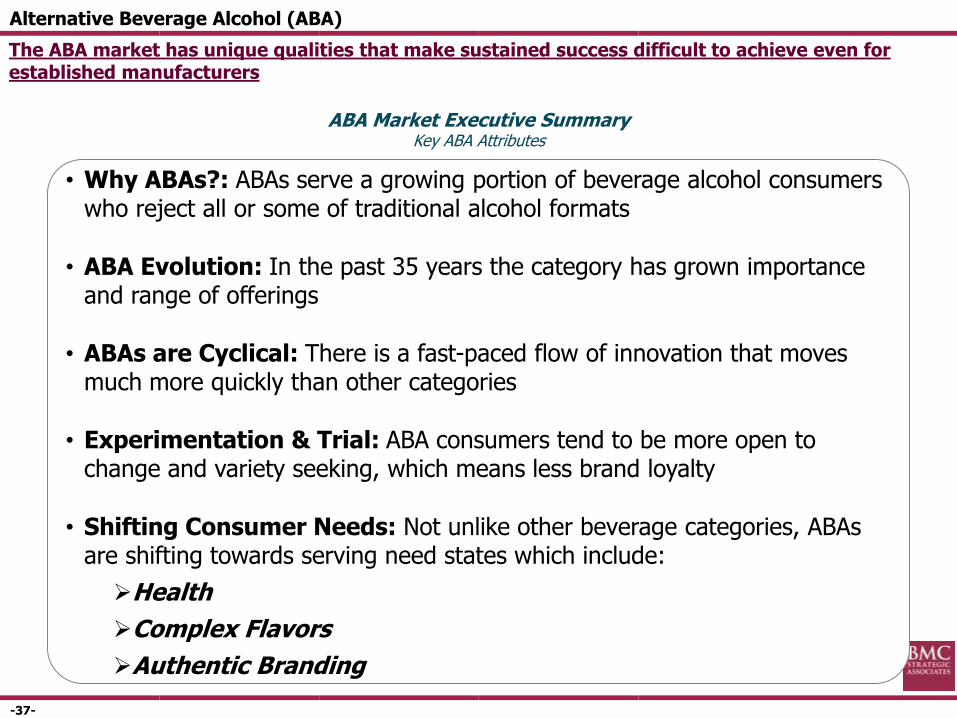

• Why ABAs?: ABAs serve a growing portion of beverage alcohol consumers who reject all or some of traditional alcohol formats

• ABA Evolution: In the past 35 years the category has grown importance and range of offerings

• ABAs are Cyclical: There is a fast-paced flow of innovation that moves much more quickly than other categories

• Experimentation & Trial: ABA consumers tend to be more open to change and variety seeking, which means less brand loyalty

• Shifting Consumer Needs: Not unlike other beverage categories, ABAs are shifting towards serving need states which include:

Health

Complex Flavors

Authentic Branding

The ABA market has unique qualities that make sustained success difficult to achieve even for established manufacturers

ABA Market Executive SummaryKey ABA Attributes

Alternative Beverage Alcohol (ABA)

-38-

275.6 million 288oz cases

9.9% EQ Share of Beer

47%

16%17%

15% 4%

ABA Volume bySub-Segment - 2018

ABA Growth 2014-2018Volume in ‘000 288 Cases

Alternative-Beverage-Alcohol (ABA) sales will reach 275 million cases by end of 2018. Since 2014 classic FMBs, Hard Ciders and Flavored Craft Beers have gained the most volume

Volu

me in 2

88oz

Case

s

+36,000

CAGR %

-1.2% +2.3% +0.3% +2.2% +4.7% +31.0% -4.8% -22.1% +3.7%

Alternative Beverage Alcohol (ABA)

-39-

High Proof FMBs

Classic FMBs

Hard Ciders

Hard Sodas

Neo FMBs & Shandy

RTD Cocktails

Flavored & Sweet Wines

Flavor Fwd. Beers

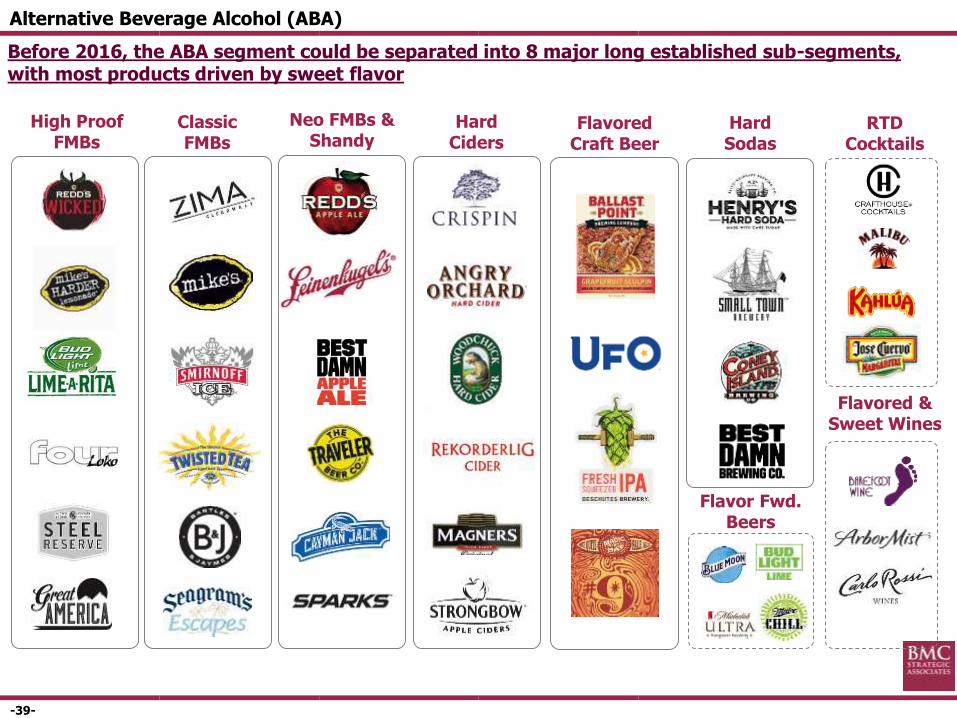

Before 2016, the ABA segment could be separated into 8 major long established sub-segments, with most products driven by sweet flavor

Flavored Craft Beer

Alternative Beverage Alcohol (ABA)

-40-

Agua Fresca Still WaterHard Tonic

Malt Sangria FMB-ACVCider & Wine Ginger Beer

Wine Spritzer

Sangria Wine Cocktail

Fruit Punch

Wine Cocktail

Margarita Coffee Cocktail

Flvd Vodka

Flvd Tequila

Tea Cocktail

Ginger Soda Gin

LI Iced Tea

Gin & Tonic

Vodka Lemonade

FMB - CoffeeFMB - Tea

FM

B -

Wa

ter

FM

B -

Ko

mb

uch

a

Ma

lt &

Cid

er

RT

D W

ine

RT

D S

pir

it

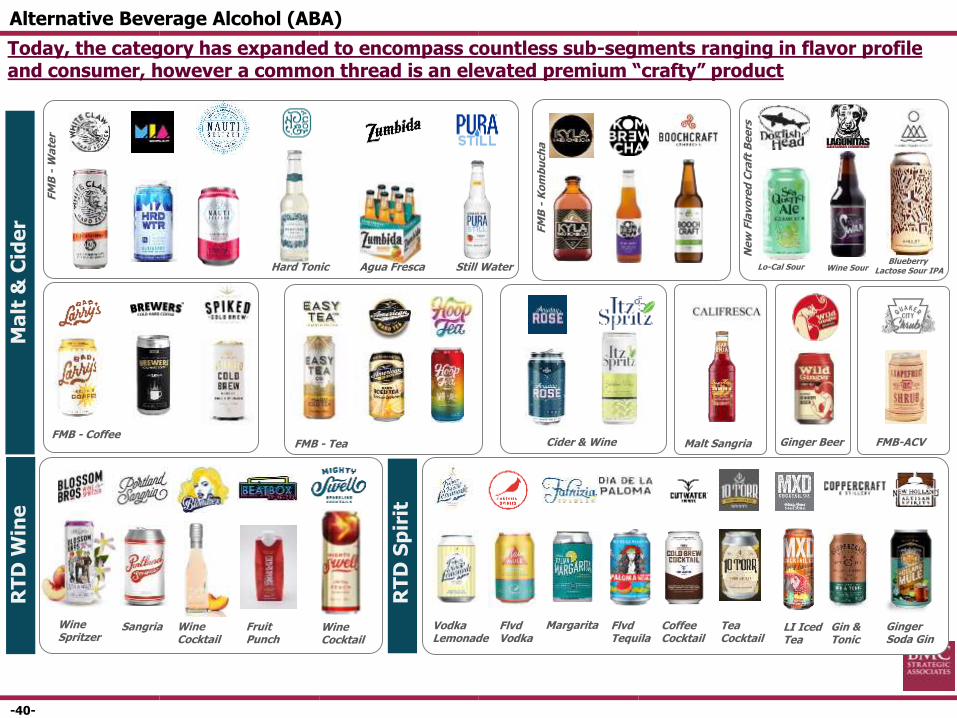

Today, the category has expanded to encompass countless sub-segments ranging in flavor profile and consumer, however a common thread is an elevated premium “crafty” product

Ne

w F

lavo

red

Cra

ft B

ee

rs

Lo-Cal Sour Wine SourBlueberry

Lactose Sour IPA

Alternative Beverage Alcohol (ABA)

-41-

Ben Weiss:Crook & Marker

MillerCoors: Cape Line

Boston Beer:Wild Leaf & Tura

Specialty Water:

CBD

Wild Leaf Hard Tea

Tura Hard Kombucha

CANarchy:Wild Basin

2019 Innovation – ABAs & Specialty Water

• A driving force in Cannabis approaching the mainstream will be CBD (the non-psychoactive element of the flower). Its growing interest is leading to infused beverages which may compete with Beverage Alcohol

Innovation in both the ABA & Specialty Water categories will only accelerate in 2019, as major players look to join established smaller brands in key sub-segments

Alternative Beverage Alcohol (ABA)

-42-

LoNo Sparkling[Low/no carbonation]

Extra Sparkling[medium to heavy carbonation]

More Flavorful

Less Flavorful

Beer

e.g. Wine Sangria e.g. Spirit Cocktail

e.g. Hard Water (Malt) e.g. Hard Seltzer (Malt)

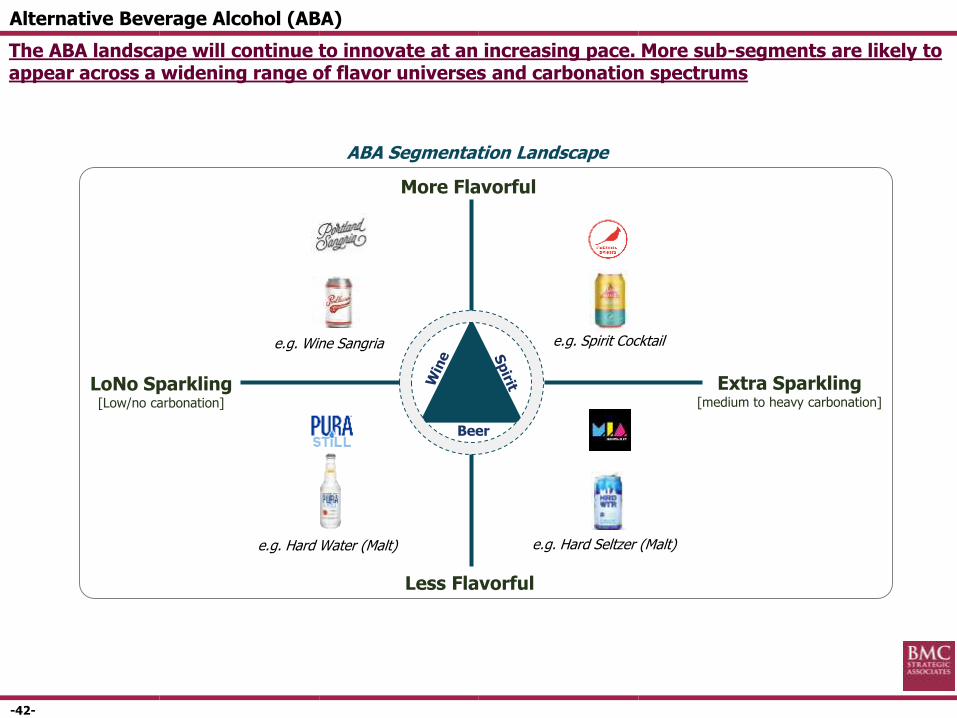

The ABA landscape will continue to innovate at an increasing pace. More sub-segments are likely to appear across a widening range of flavor universes and carbonation spectrums

ABA Segmentation Landscape

Alternative Beverage Alcohol (ABA)

-43-

Alternative Beverage Alcohol (ABA)

What is next?

What are the solutions to future consumer needs?

Welcome Brian Jorgensen: McCormick and Company to discuss

potential solutions to questions above