2016 iasa carolinas winter meeting - iasa presentation...2016 iasa carolinas winter meeting. pwc |...

TRANSCRIPT

Market Disruptors in Insurance

Scott Topper, PwC Insurance StrategyDecember 5, 2016

2016 IASA Carolinas Winter Meeting

PwC | Future of Insurance

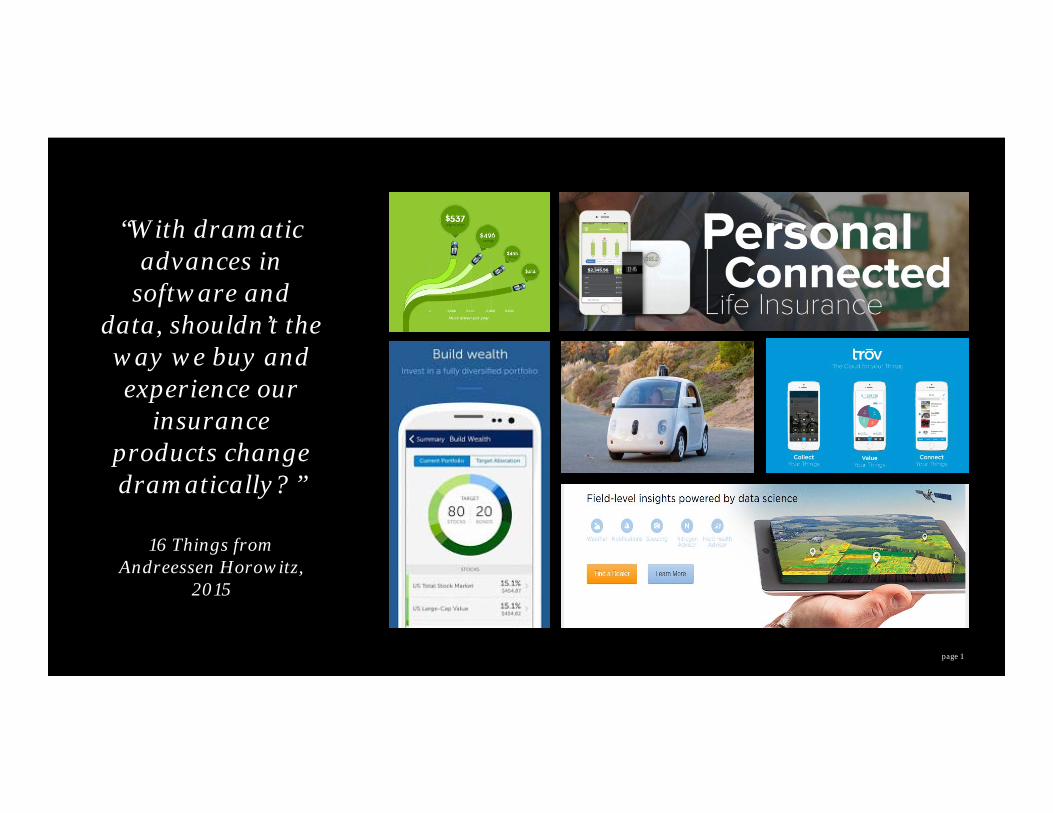

“With dramatic advances in

software and data, shouldn’t the way we buy and experience our

insurance products change dramatically? ”

16 Things from Andreessen Horowitz,

2015

page 1

A new normal in Insurance

page 2

01

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

According to PwC’s Global CEO survey, the insurance industry is undergoing more upheaval than any other industry

page 3

69%Changes in distribution

channels 49%Changes in

availability and use of data

88%Changes in regulation

71%Changes in customer behavior

C a u s e s o f D i s r u p t i o n

Emergence of Innovative

Business Models

Exploding Intelligence and Automation

Consumerization of Decisions

Digitization of Everything

Source: PwC Annual Global CEO Survey

The Insured

Driven by social and technological trends, next generation of insureds will demand solutions to help them and their peers to manage and prevent potential disruptions in individuals and businesses lives.

Contextual

Preventive

Personalized

On-demandRewarded

Shared

Financial impact

ExperienceImpact

Wave 1 Wave 2 Wave 3

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 4

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 5

Customer RevolutionShifts in customer expectations, information access and diversifying needs are creating networks of self-directed, self-organizing and self-aware groups

Power shifting to customers

Growing expectations & sophistication

Rise of sharing economy

Emerging models of advice

Trends• Proliferation of mobile devices• Widespread adoption of social

media networks• Changing behaviors and

demographics

For each customer there is only “one best experience”, and the

attributes of this experience must be in all interactions

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 6

of Smartphone users use the Internet to shop at least once

a month

79%of Adults have Mobile

Devices within Arm’s Reach 24/7

91%Sources of information used

by insurance shoppers

11.7of consumers use at least one

type of social media

95%

Consumerization of decisionsShifts in customer expectations, information access and diversifying needs

are creating self-aware, self-directed, and self-organizing groups

page 6

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

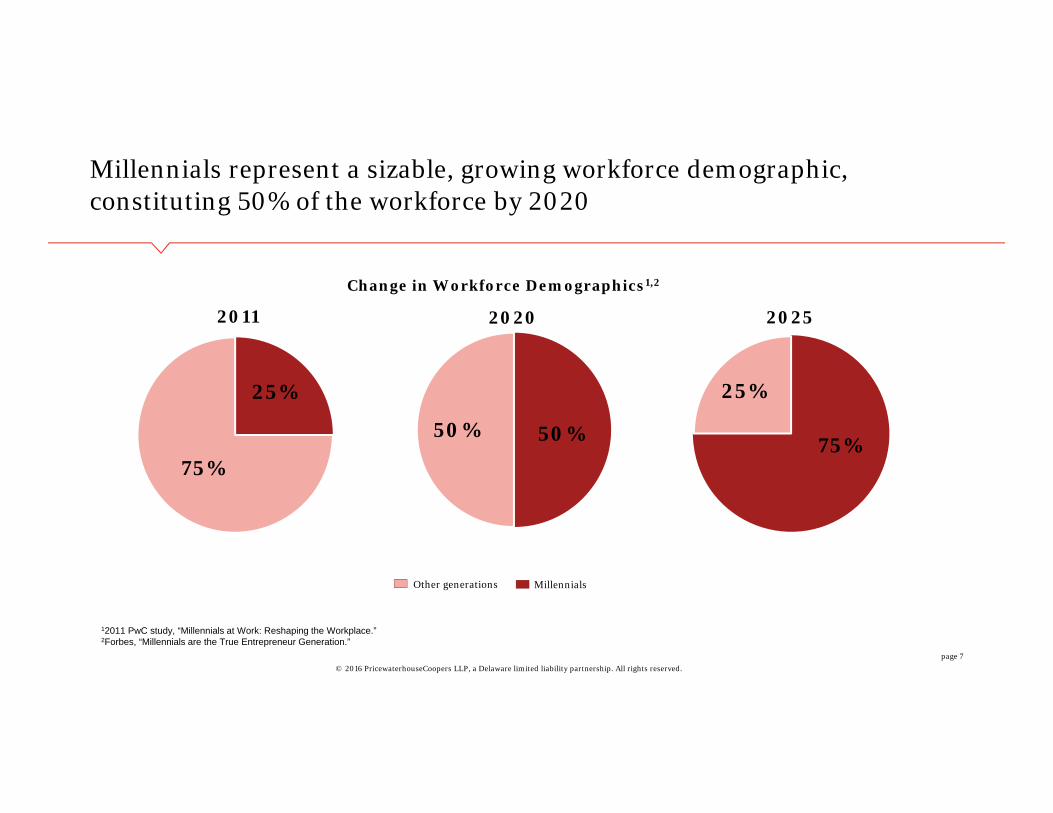

Millennials represent a sizable, growing workforce demographic, constituting 50% of the workforce by 2020

page 7

50%50%

25%

75%

2011 2025

12011 PwC study, “Millennials at Work: Reshaping the Workplace.”2Forbes, “Millennials are the True Entrepreneur Generation.”

75%

25%

2020

Change in Workforce Demographics1,2

Other generations Millennials

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 8

Millennial Small Business Owners67% of Millennials indicate interest in starting their own

business, representing a greater opportunity for small commercial insurers relative to previous generations1

of Millennial entrepreneurs are optimistic the local

economy will improve over the next 12 months2

82%of Millennial entrepreneurs plan to grow their business

in the next 5 years, compared with 73% of Gen X-ers and 57% of Boomers2

87%of Millennial entrepreneurs applied for a business loan within the past two years,

compared with 30% of Gen X-ers and 20% of Boomers2

58%of Millennial entrepreneurs give themselves an “A” or a

“B” on tech-savviness2

85%

1Forbes, “Millennials are the True Entrepreneur Generation.”2Bank of America, Small Business Owner Report, Fall 2014.

page 8

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Millennials are highly-informed consumers and value authenticity, seeking out sources of advice perceived as trustworthy and ignoring advertising

page 9

Of the 80 million millennials living in the U.S. today, about 43% rank authenticity over content when consuming news1

About 33% of all millennials rely on blogs for information when making a purchase, compared to older generations that consumed information via traditional channels2

Only 1% of millennials rely on advertisements to make them trust a brand or company3

12014 PwC study, “Playing for Keeps: How insurers can win customers, one at a time.”2,3Forbes, “10 New Findings about Millennial Shoppers.”42015 PwC study, “Shopping for Growth: Optimizing acquisition to drive growth in insurance.”

AwarenessCustomer is made aware of the company and it’s offerings

Information GatheringCustomer reaches out to the company to gather further information

QuoteCustomer requests a quote to determine premium amount

PurchaseCustomer’s quote is accepted or amended and policy is paid for and bound

Television Social Media

Website/Mobile

Call Center

Online Quote

Online Purchase

Purchase with Agent

Older consumers Millennials

Channels Accessed Over Customer Journey4

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

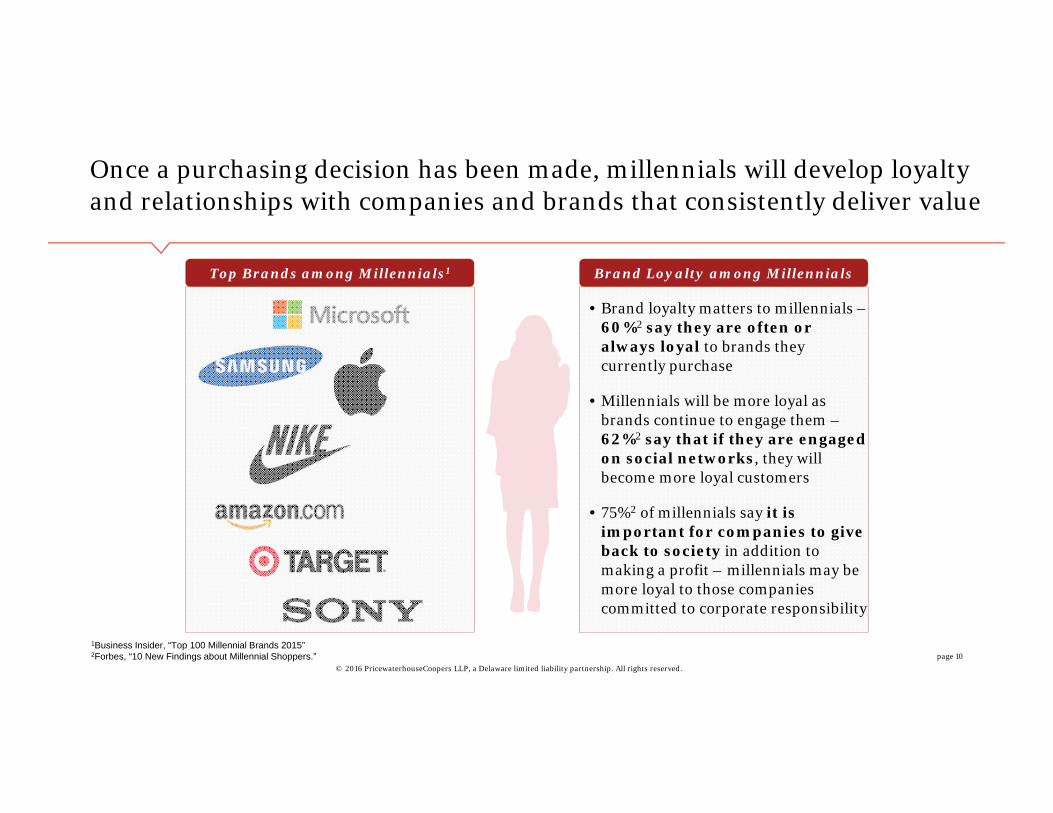

Once a purchasing decision has been made, millennials will develop loyalty and relationships with companies and brands that consistently deliver value

page 10

Brand Loyalty among Millennials

• Brand loyalty matters to millennials –60%2 say they are often or always loyal to brands they currently purchase

• Millennials will be more loyal as brands continue to engage them –62%2 say that if they are engaged on social networks, they will become more loyal customers

• 75%2 of millennials say it is important for companies to give back to society in addition to making a profit – millennials may be more loyal to those companies committed to corporate responsibility

Top Brands among Millennials1

1Business Insider, “Top 100 Millennial Brands 2015” 2Forbes, “10 New Findings about Millennial Shoppers.”

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Social media is increasingly used by commercial carriers to reach a larger segment of the small business market

page 11

Hiscox allows its customers to submit reviews directly on its website and then post those reviews on a variety of social media platforms. It also allows customers to share links to various whitepapers from its website on social media platforms

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

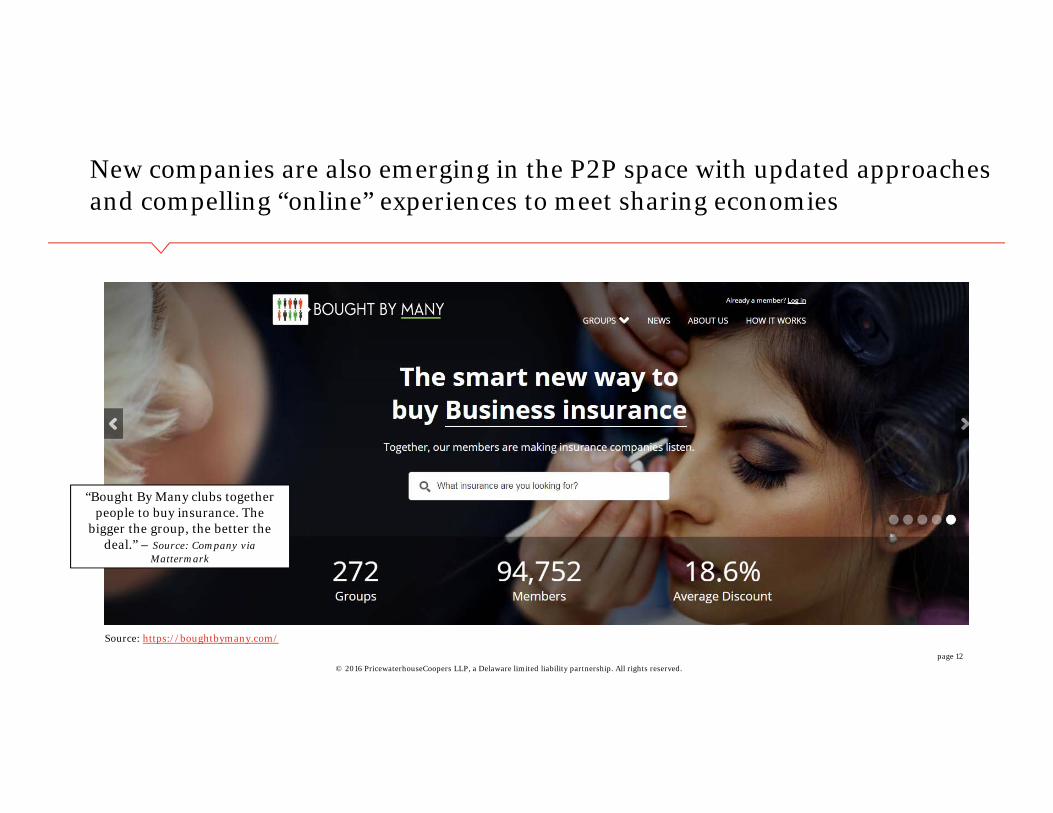

New companies are also emerging in the P2P space with updated approaches and compelling “online” experiences to meet sharing economies

page 12

“Bought By Many clubs together people to buy insurance. The

bigger the group, the better the deal.” – Source: Company via

Mattermark

Source: https://boughtbymany.com/

Health sensors

The Risk

New risks will emerge related to the new technologies, but in general risks will become more predictive and manageable, allowing models to shift from protection to prevention.

Connected Cars and

ADAS

Industrial Sensors

Other sources:

CAT, Weather,

Imaging, etc.

Connected Homes

Behavior influencers

Risk mitigation

Risk factors

detection

Soft Telematics

Lifestyle

Populat-ion

health

Smart cities

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 13

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Companies are increasingly utilizing smart, connected sensor technology, an integral part of the Internet of Things (IoT)

page 14

Sensor Technology Adoption Internet of Things

SensorsSensors measure some characteristic of an object or the environment it is in

Networking PlatformsMeasurements are relayed as structured data on a network

Big Data and ComputingData is gathered in real-time and continuously, driving decisions from analytics

The Internet of Things transforms the data from sensors to become valuable information, so product improvement can occur along with enhanced customer experience

*Top Performers are companies are in the top quartile for revenue growth, profitability, and innovation

Source: PwC 6th Annual Digital IQ survey, 2014 over 1,500 executives

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

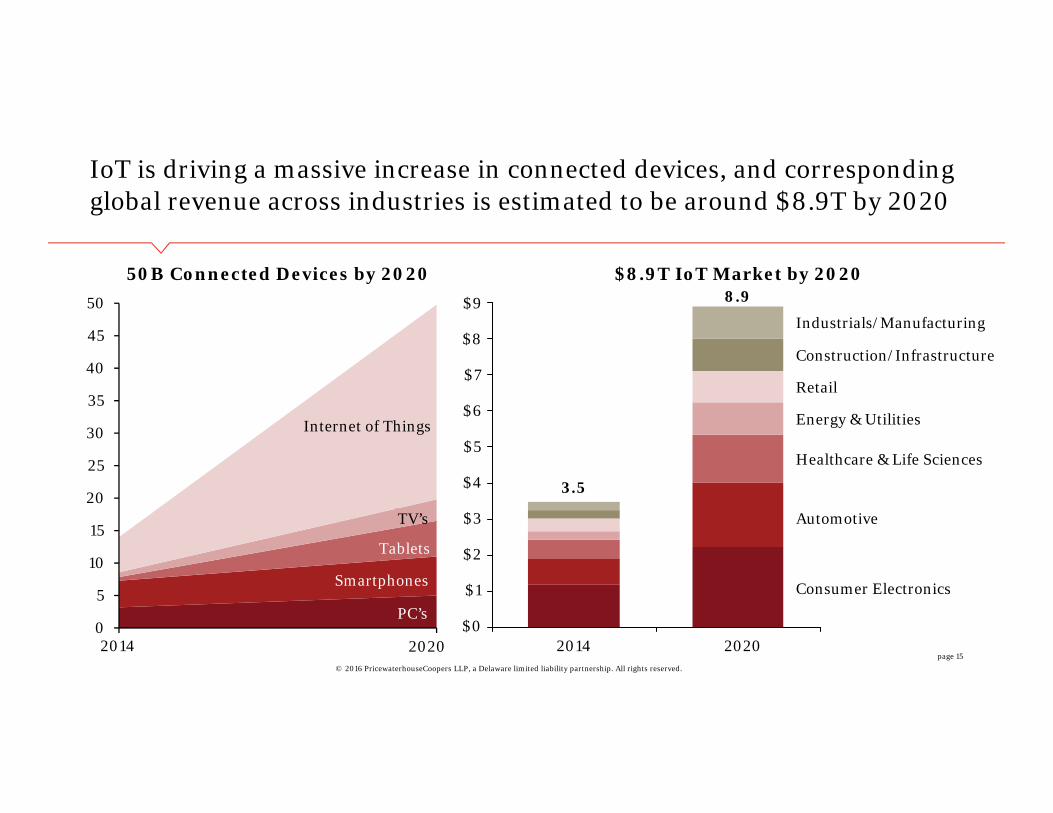

IoT is driving a massive increase in connected devices, and corresponding global revenue across industries is estimated to be around $8.9T by 2020

page 15

$0

$9

$8

$6

$1

$7

$3

$4

$2

$5

Consumer Electronics

Automotive

Healthcare & Life Sciences

Energy & Utilities

Retail

Construction/Infrastructure

Industrials/Manufacturing

2020

8.9

2014

3.5

$8.9T IoT Market by 2020

0

5

10

15

20

25

30

35

40

45

50

TV’s

Internet of Things

2014 2020

Smartphones

Tablets

50B Connected Devices by 2020

PC’s

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

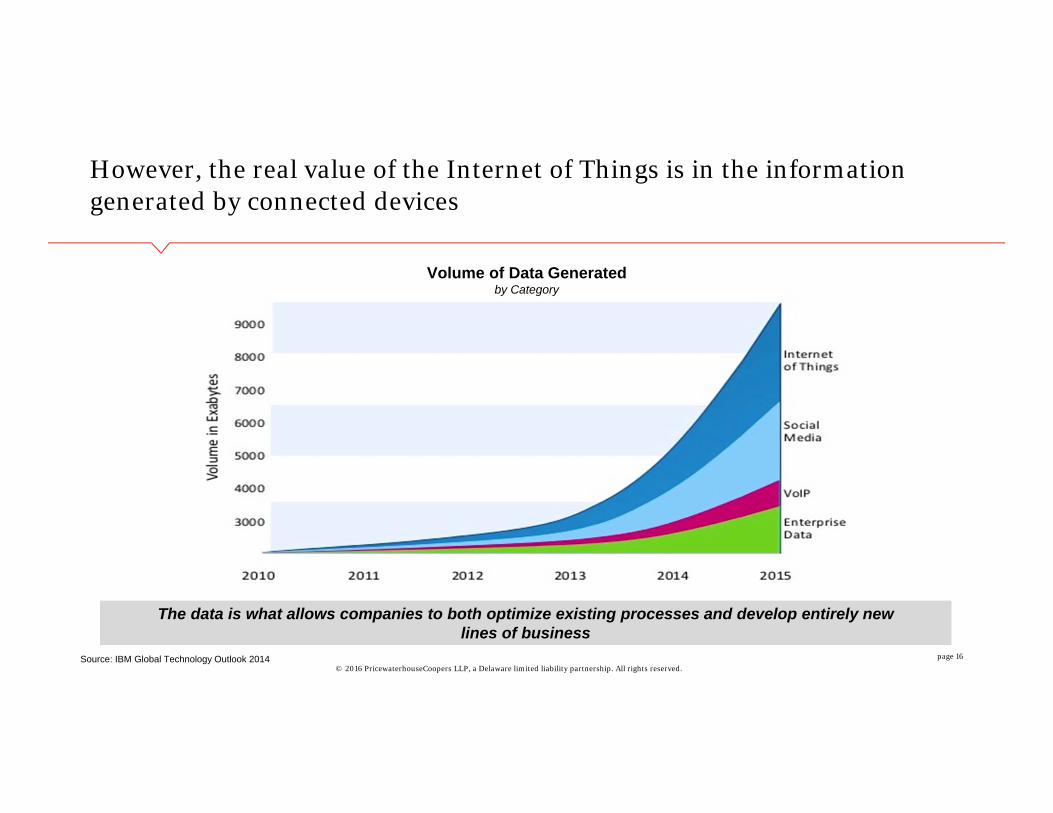

However, the real value of the Internet of Things is in the information generated by connected devices

page 16Source: IBM Global Technology Outlook 2014

Volume of Data Generatedby Category

The data is what allows companies to both optimize existing processes and develop entirely new lines of business

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Across the industry, real-time data from connected devices has traditionally been used in consumer insurance but is now spreading to other sectors

page 17

2014 201920092004

Auto

Sub-

Indu

stry

Ex

ampl

esC

ompa

ny

Exam

ples

• Telematics from car sensors informs UBI

• Behavioral traits derived from consumer driving data enhances underwriting

• 40% decrease in expected premiums in the next ten years

Home Health/Life Workers’ Comp Other Sectors

• Connected Home• Drones reduce

costs and increase efficiency in claims reporting for roof damage

• Armband sensors generate further insights on consumer health trends

• Shoe sensors monitor exercise levels to inform wellness programs

• Body motion sensors provide data on high-risk areas of the workplace

• Hardhat sensors may detect when pressure is applied to the head region

60% of insurance companies

have piloted or considered pilots of IoT

15%of insurance companies

have launched

IoT- based solutions

The Insurance Industry is

investing in IoT

Sources: “Six Primary Use Cases Dominate the Adoption of the Internet of Things Within Insurance.” Gartner, July 2015; “UBI Global Study 2016,” Ptolemus.

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

IoT will likely reduce aggregate loss, driving down premium and creating opportunities for products and services that go beyond compensating for loss

1 2

Total Insurance Industry

Premiums*

Total Insurance Industry

Premiums

20262016

New IoT-enabled Risk Services

New IoT-driven Insurance Products

New IoT-based Products & Services

15%1

40%2

to

1 Represents a drop in the premium basis, mostly across primary perils in the next ten years. ”Can a Fixed Cost Property/Casualty Industry Survive the Internet of Things?”, Celent, March 2016.2 As a comparison, the auto insurance market is projected to decline by as much as 40% due to the expected emergence of autonomous vehicles according to a KPMG study

Impact on reinsurance is expected to be higher as severity decreases

Examples

Guaranteed Performance, Uptime, and other Value-added Services, etc.

New Cyber Liability Coverages for attacks on smart, connected assets

Remote Monitoring and Notification Services, Predictive Maintenance, etc.

Traditional Property Insurance, Liability Insurance, etc.

Explanation

Solution offerings for both insurance and non-insurance companies using the power of IoT

Insurance products and coverage enhancements are developed for risks introduced by IoT tech

New risk-mitigation services are offered by both insurance and non-insurance companies as a

result of adoption of IoT technologies

Existing insurance premium basis declines over time as IoT-enabled risk services help to avoid and mitigate risk, and real-time data from IoT installations makes underwriting more precise

The IoT Opportunity for Insurance

page 18

ILLUSTRATIVE

The Insurer

Carriers will position themselves as risk management platforms, interacting with new partners to bring new value propositions to the market while optimizing their operations.

Insurer as a Platform

Core Claims function

Core Life Insurance function

Sureify HealthIQ Goldbean

Claim DI WeGoLook Tyche

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 19

The Ecosystem

Unlike other industries, innovation opportunities in insurance are driven by advances and changes happening in other areas and industries, and this will expand the ecosystem and the opportunity space for insurers

Intermediaries

Service Providers

Carriers

Reinsurers

Regulators

IoT and Remote Access

Connected Health and P4

Medicine

Connected Cars, ADAS, Autonomous

Artificial Intelligence /

Cognitive Computing

Traditional ecosystem

……

Illustrative, not exhaustive

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. page 20

The opportunity space

page 21

02

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Many believe that Insurance is changing and opportunities exist in a global insurance market of over $5 Trillion

page 22

“I think you’ve got to look at disruptors and see what you can learn

from them, because they often come in with

some very smart innovation and different service propositions.”

John Neal, CEO of QBE Group, PwC 18th Annual CEO Survey

“We have already seen the impact of better

data and new platforms in motor insurance. Insurers

will be Uber-ized unless we find new ways to add value.”

Inga Beale, Lloyd’s CEO

“…there is a significant opportunity to bring a

fresh approach to insurance and

reinsurance, one based not just on world-class

underwriting, but also a strong foundation of large data analytics, research, and fully-

integrated technology.”

“Duperreault to pioneer fresh approach to risk”,

Intelligentinsurer.com, dec.13

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

The industry is gradually transitioning across different dimensions and lines of business

page 23

Purpose Reactive Preventive and pro-active

Product Complicated Simplified / Sophisticated

Distribution Advisor Omni-channel

Advice Siloed Holistic

Decision Maker Employer / State Individual

FROM TO

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Incumbents and investors have realized that new Startups bring answers to many challenges that they face in the current changing environment

page 24

Source: CB Insights

+ 300%

Funding Deals

FinTech Financing TrendFunding in FinTechstartups is booming,

influenced by increasing market

activity.

However, even more relevant is the

increasing deal activity as a proxy to understand how

incumbents are leveraging the

FinTech ecosystem

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Investors have also started to look at a more specific “InsurTech” landscape to seize opportunities in the global insurance market

page 25

900

220

The number of FinTech investors increased by

400% since 2010

Also a new “InsurTech” landscape has

emerged and is attracting more and more interest from investors who are

looking for Insurance-specific solutions

Because of this interest, a group of

290+ investors -almost nonexistent in 2010 - are already in

“InsurTech”

Source: CB Insights

29020

900+

220

FinTechInsurTech

2010 2015

Number of Investors

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Incumbents, but also new players, are bringing solutions that tap into existing opportunities across the insurance value chain

Meet changing customer needs

with new offering

Enhance interactions and

build trusted relationships

Augment existingcapabilities and

reach with strategic

relationships

Business Opportunities – External View

Leverage existing data and analytics to generate deep

risk insights

Utilize new approaches

to underwrite risk and

predict loss

Enable the business with sophisticated

operational capabilities

Business Opportunities – Internal Viewpage 26

• Mainly driven by customer expectations

• Opportunity for fast followers since value propositions can be quickly replicated

• Front runners have the opportunity to gain market relevance and position themselves

• Mainly driven by Technology advances

• A source of competitive advantage but demanding deeper changes

• Sets foundations of how the company wants to understand and manage the risk

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

These solutions are the result of a new mindset that pushes Startups to seek solutions to real problems, enabled by new available technologies

page 27

think as aDisruptor

act as aStartup

Fast Prototyping, starting day 1

Leverage the ecosystem relationships

Continuous evolution

What’s the problem to solve?

Which are potential solutions?

How to be distinctive?

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Incumbents have the opportunity to approach the FinTech ecosystem with different innovation models and take advantage of it

page 28

Sourcing model

• Ideas ‘in-sourced’ from within the company

• Dedicated internal team develops new products & services

• Potential to partner with external companies

• Ideas sourced from both inside and outside the company

• Dedicated internal team constantly monitors trends and markets

• Internal incubator identifies and supports ventures

• Ideas sourced from outside the company

• New ventures division set up to identify, iterate and bring to market new ventures

Fundingmodel

• Streamlined business case or stage-gating to balance procedural burden and risk

• Deploy internal SMEs to incubate and iterate ideas

• Pitch and invest model applied from within the company

• Expert panel provides high level guidance and approval at key milestones

• Pitch and invest model where Company provides cash and support for equity

• Corporate network provides guidance for incubation

Go-to-market model

• Idea / venture adopted under company’s brand

• Venture can go to market under company’s or new brand

• Venture is graduated into company’s R&D funnel

• New venture goes to market under own brand, leveraging corporate channels and relationships

Venture Capitalist

Innovation Hub

Internal Incubator

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Recent activity

shows some examples of

the opportunity space and

how incumbents are reacting

Mass Mutual’s In-house Startup

Offers simplified life insurance for Millennials through a convenient

online experience

John Hancock + Vitality

Partnership allowing personalized life insurance, using wearables and

online channels

“ACE Takes 24% Stake”

ACE backs CoverHound, an online site and Google Insurance search for

comparing and buying auto and property insurance

AXA Strategic Ventures

A €200M venture capital fund. Recent Investments: PolicyGenius (June 2015)

an online platform for comparing & buying insurance and Bee (Nov. 2015)

which provides financial services to low-and middle income neighborhoods

Investments in Digital Currency & Blockchain

New York Life, Transamerica Ventures and others invest in the

Digital Currency Group, a company focused on building and investing in

bitcoin & blockchain companies

Northwestern Mutual Acquires LearnVest

Northwestern Mutual acquires LearnVest, an online personal finance platform initially focused on women

American Family Ventures

Focus investment activity at the intersection of technology & risk management, with a variety of 20

different partners listed online

Allianz Joins Forces to Establish a New Online Player

Allianz joins Chinese internet Giant & an Asian investor to establish a new digital, customer centric insurance company in China with affordable coverage options

Ping An + Bought By Many

Partnership with Bought By Many is using social data to develop niche,

personalized product offerings in the travel insurance market

page 29

Examples of Disruption03

page 30

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Trends in market disruption have varying degrees of impact across personal lines, commercial lines and life insurance businesses

page 31

Personal Lines Commercial Lines Life Insurance

• Reaching the Un(der)insured• Spread of value propositions for

microsegments• Usage & Behavior based personalized

insurance• New models of holistic advice (Robo-Advice)• SoMoLo Omni-channel experience• Online aggregation and comparison• Consolidation of Self directed services• Education & Shared Knowledge• Rise of B2B2C Platforms• Connected Health & P4 Medicine• Sophistication of preventive insurance

models• Granular Risk and/or Loss Quantification• Robotics and Automation in core insurance• As-a-service solutions for core insurance

• Emerging solutions for shared economies• Online aggregation and comparison• Consolidation of Self directed services• Frictionless capital flows across the value

chain • Connected car / automated driving systems• Remote data capture and analysis• Quantification of emerging risks• Sophistication of preventive insurance

models• Shift from probabilistic to deterministic

model• Granular Risk and/or Loss Quantification• Crowdsourcing & Democratization of

information• Robotics and Automation in core insurance• As-a-service solutions for core insurance

• Spread of value propositions for microsegments

• Leveraging peer to peer networks• Emerging solutions for shared economies• Usage & Behavior based personalized

insurance• SoMoLo Omni-channel experience• Online aggregation and comparison• Targeted engagement & Retention models• Consolidation of Self directed services• Ecosystem Partnerships• Connected car / automated driving systems• Sophistication of preventive insurance

models• Granular Risk and/or Loss Quantification• Crowdsourcing & Democratization of

information• As-a-service solutions for core insurance

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Disruptions in Personal Lines Insurance – Usage Based Insurance, Ridesharing, Peer to Peer, Direct-to-consumer, ADAS & Autonomous Cars

page 32

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Disruptions in Commercial Lines Insurance – Direct to Small Business, Drones, Internet-of-things, alternative risk transfer, emerging risks

page 33

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Disruptions in Life Insurance– Robo-advice, Personalized insurance, Medical advances, Automated underwriting, decreasing morbidity and mortality risk

page 34

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

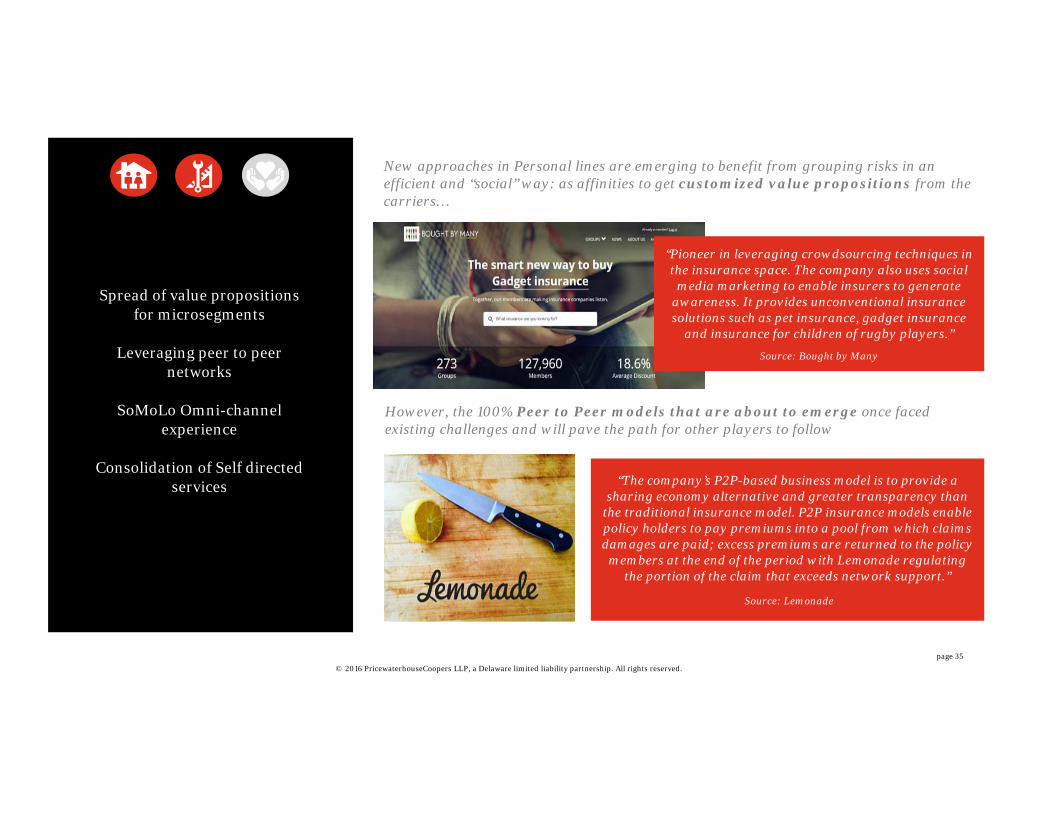

New approaches in Personal lines are emerging to benefit from grouping risks in an efficient and “social” way: as affinities to get customized value propositions from the carriers…

Spread of value propositions for microsegments

Leveraging peer to peer networks

SoMoLo Omni-channel experience

Consolidation of Self directed services

“Pioneer in leveraging crowdsourcing techniques in the insurance space. The company also uses social

media marketing to enable insurers to generate awareness. It provides unconventional insurance solutions such as pet insurance, gadget insurance

and insurance for children of rugby players.”

Source: Bought by Many

page 35

“The company’s P2P-based business model is to provide a sharing economy alternative and greater transparency than

the traditional insurance model. P2P insurance models enable policy holders to pay premiums into a pool from which claims damages are paid; excess premiums are returned to the policy

members at the end of the period with Lemonade regulating the portion of the claim that exceeds network support.”

Source: Lemonade

However, the 100% Peer to Peer models that are about to emerge once faced existing challenges and will pave the path for other players to follow

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Usage based insurance is shifting from an underwriting focus to more consumer focused value propositions: one variable can be enough the meet the needs of a specific segment…

Usage & Behavior based personalized insurance

SoMoLo Omni-channel experience

Connected car and automated driving

Granular Risk and/or Loss Quantification

Ecosystem Partnerships

“One of the pioneers in pay-per-mile insurance in the US, offering an attractive value proposition to low-mileage drivers (…). partnered with Uber to develop a car insurance plan specifically for Uber drivers. This per-mile plan only charges drivers

for miles driven during their personal use, thereby complementing Uber’s insurance plan. ”

Source: Metromile

page 36

“Provide hassle-free and quick insurance to the customer segment that wants to borrow someone else's car and be temporarily insured during

that timeframe. (…). Cuvva claims to provide a superior product compared with other pay-as-you-go companies since it doesn’t have a

fixed monthly fee (…).”

Source: Cuvva

… but also pay as you go service can be an option to provide quick insurance to individual that shared their cars

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Following personal lines trends, online distribution is also impacting the Micro and Small Business space

Spread of value propositions for microsegments

Online aggregation and comparison

Consolidation of Self directed services

“Online insurance broker that helps small- and

medium-scale businesses access commercial

insurance. The company runs insureon.com and

techinsurance.com marketplaces where small business can apply online

and receive insurance quotes for multiple

commercial products.”

Source: Insureon

page 37

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

And data and analytics will provide the opportunity to understand and quantify risks in a more granular way, also by leveraging non-traditional data sources

Remote data capture and analysis

Sophistication of preventive insurance models

Granular Risk and/or Loss Quantification

Crowdsourcing & Democratization of

information

“Imaging analytics solution provider. The company uses

artificial intelligence to process a large

database of satellite imaging and draw

socioeconomic insights. Orbital

insight has developed machine learning algorithms that can be used for self-analysis of data

points.”

Source: Orbital Insight

page 38

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

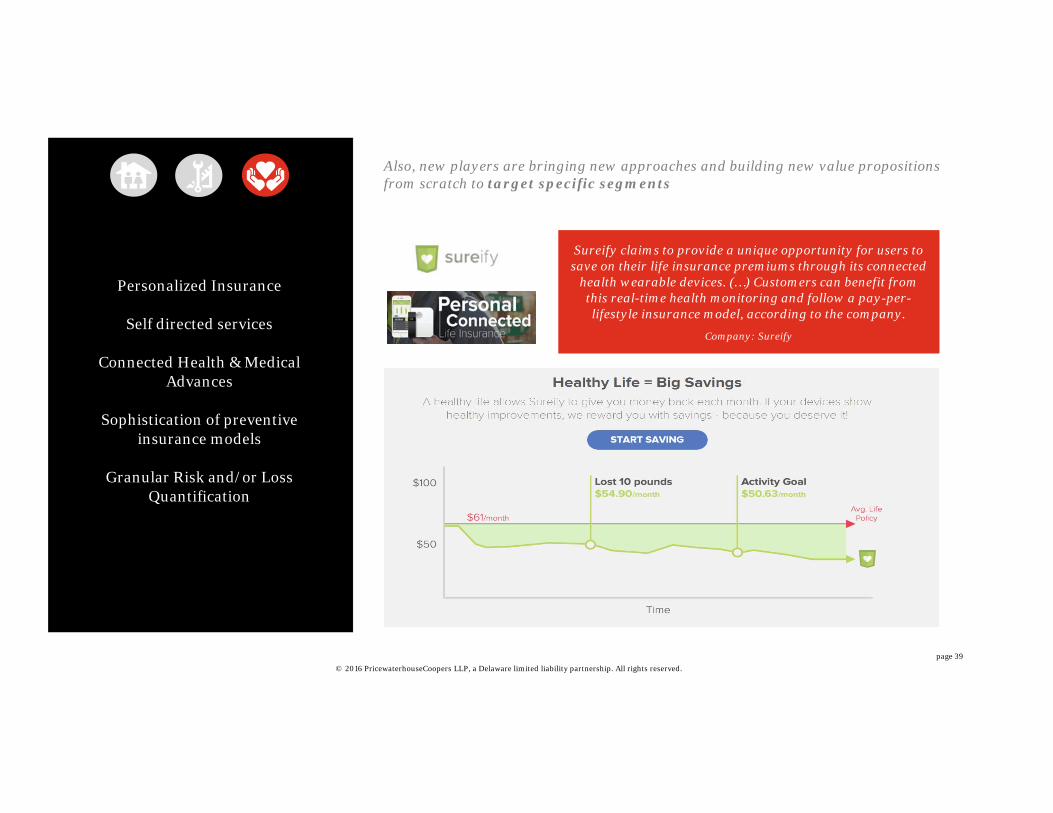

Also, new players are bringing new approaches and building new value propositions from scratch to target specific segments

Personalized Insurance

Self directed services

Connected Health & Medical Advances

Sophistication of preventive insurance models

Granular Risk and/or Loss Quantification

Sureify claims to provide a unique opportunity for users to save on their life insurance premiums through its connected

health wearable devices. (…) Customers can benefit from this real-time health monitoring and follow a pay-per-lifestyle insurance model, according to the company.

Company: Sureify

page 39

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Wearable solutions have already entered the enterprise space, creating new opportunities to engage employees in healthier lifestyles and work habits

Connected Health & Medical Advances (P4 Medicine)

Sophistication of preventive insurance models

Granular Risk and/or Loss Quantification

“WeSavvy claims that with their solution Employees can get rewarded on their

insurance policies by Walking, Running or Cycling. They bring a B2B2C value

proposition targeting policyholders and employers. Also with their BYOW, every

employee can use his own wearable.

Company: WeSavvy

page 40

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

© 2016 PwC. All rights reserved. PwC refers to the PwC network and/or one or more of its member firms, each of which is a separate legal entity. Please see www.pwc.com/structure for further details. This content is general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Thank you

Scott TopperPwC Insurance [email protected]+1 (773) 899-0069

41

Appendix04

page 42

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Aggregators are bringing more and more transparency and independency to buyers, allowing them to easily compare quotes from more and more carriers in a few seconds …

SoMoLo Omni-channel experience

Online aggregation and comparison

Consolidation of Self directed services

“The Zebra says the way it differentiates itself from other insurance comparison engines is

that it takes into consideration the regulation differences across different states in its

quotation calculation. (…) The firm also allows customers to browse premium quotes

anonymously and says it provides protection of customers' personal information.”

Source: Insurance Zebra

page 43

… and a second way to differentiate, they are delivering enhanced experiences as quick quotes without personal data, or detailed quotes launched from ID pics.

MIT Spinout Insurify Raises $2 Million To Replace Human

Insurance Agents With A Robot (TechCrunch)

“claims to be the first shopping platform for car insurance that instantly verifies

customer data and provides an integrated experience. (…). Insurify’s goal is to reduce the time it takes by

providing a quote in just three minutes.”

Source: Insurify

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

New players are bringing new approaches in the small business insurance to pool the risk in an efficient and “social” way

Spread of value propositions for microsegments

Leveraging peer to peer networks

SoMoLo Omni-channel experience

“Gatherins is a crowdfunding platform for business insurance. The company either assigns an

appropriate community to individuals or enables them to start their own community and invite other

entrepreneurs to join-in, using social media.”

Source: Gather

page 44

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

As the ability to generate insights from smart objects and sensors increases, companies are more readily able to collect, analyze and predict risk across multiple contexts

Remote data capture and analysis

Sophistication of preventive insurance models

Granular Risk and/or Loss Quantification

Crowdsourcing & Democratization of

information

“Data analytics and Internet of Things (IoT) solution provider. It offers a Software-as-a-Solution (SaaS) platform to companies from

different sectors including Insurers. The cloud-based platform allows companies to

capture, collect, analyze, and take action on insights. Allows to integrated all kind of

sensors including health, telematics, industrial sensors, etc. to provide deeper

insights.”

Source: Mnubo

page 45

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Advanced analytics such as machine learning bring new opportunities to build more sophisticated prevention models

Remote data capture and analysis

Sophistication of preventive insurance models

Crowdsourcing & Democratization of

information

Robotics and Automation in core insurance

“Offers cost-effective, turnkey API-based machine learning services that help

businesses understand data from monitoring sensors. The technology can be leveraged by

property and casualty (P&C) insurers to analyze data from IoT and connected home

and car devices.”

Source: Glowfish IO

page 46

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Available information can be shared with different players in the ecosystem to maximize go-to-market opportunities

Targeted engagement & Retention models

Crowdsourcing & Democratization of

information

Robotics and Automation in core insurance

“RiskMatch's offering links the various players in the disconnected commercial insurance market. Unlike its competitors in the online insurance sector, which merely provide

insurance quotations, RiskMatch claims to offer software that detects the best products and deals through benchmarking for brokers and insurers.”

Source: RiskMatch

page 47

© 2016 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved.

Sometimes it is just a matter of providing simple products with seamless and convenient end-to-end experiences…

Self directed services

Robotics and Automation in core insurance

“Online life insurance company (…). The company provides a life cover underwritten (…) in roughly ten minutes. (…) distinguishes itself from other online insurance companies

by providing its clients features like an online medical questionnaire (…)”

Company: BeagleStreet

page 48