117712_musings 011811

TRANSCRIPT

MUSINGS FROM THE OIL PATCH January 18, 2011

Allen Brooks

Managing Director

Note: Musings from the Oil Patch reflects an eclectic collection of stories and analyses dealing with issues and developments within the energy industry that I feel have potentially significant implications for executives operating and planning for the future. The newsletter is published every two weeks, but periodically events and travel may alter that schedule. As always, I welcome your comments and observations. Allen Brooks Offshore Industry: Waiting For Godot; Will He Ever Come? Godot never does come, which forces the two men to fill their waiting time Director Michael Bromwich delivered a speech about the status of his bureau’s operations, reorganization and new offshore rule promulgation efforts

The offshore oil and gas and oilfield service industries appear to be playing the roles of Vladimir and Estragon, the two lead characters in Samuel Beckett’s Waiting for Godot

. The play deals with two days in the lives of these gentlemen who are awaiting the arrival of an acquaintance who they admit they hardly know and probably might not recognize when he arrives. Godot never does come, which forces the two men to fill their waiting time. While waiting they eat, sleep, talk, argue, sing, play games, exercise, swap hats, and contemplate suicide – anything “to hold the terrible silence at bay.” It sure sounds like the actions of the domestic offshore industry both during and after the offshore deepwater drilling moratorium.

The play was voted "the most significant English language play of the 20th century." It was written during the winter of 1948-1949 and had its initial performance in January 1953. It is often described as an absurdist play and its script has led to much discussion about the hidden meanings behind the storyline. One drama critic wrote about Mr. Beckett and his play that it "has achieved a theoretical impossibility—a play in which nothing happens, that yet keeps audiences glued to their seats. What's more, since the second act is a subtly different reprise of the first, he has written a play in which nothing happens, twice." That description seems an appropriate characterization of the Gulf of Mexico offshore petroleum business for the past six months. Last week, the National Commission on the BP Deepwater Horizon Oil Spill and Offshore Drilling issued its long awaited report and Bureau of Ocean Energy Management, Regulation and Enforcement (BOEMRE) Director Michael Bromwich delivered a speech about the status of his bureau’s operations, reorganization and new offshore rule promulgation efforts. The Commission’s report has a number of

MUSINGS FROM THE OIL PATCH PAGE 2

JANUARY 18, 2011

The government’s solution is to add additional layers of regulation to the industry’s operations After he commented that new offshore drilling permits were coming he said, “I would be stunned if we waited until the third or fourth quarter” We are now well into January with no new deepwater drilling permits having been issued

worthy ideas about offshore regulation and operations that should be explored and discussed. The report also dismisses the positive historical drilling safety record of the offshore industry and characterizes its operations as suffering from a “systemic” problem. The government’s solution is to add additional layers of regulation to the industry’s operations without fully determining the cause of the Deepwater Horizon disaster and the Macondo oil spill. (We have just received a copy of the full report and have not yet had time to read it all.) Dir. Bromwich’s talk focused on the status of the reorganization efforts of the former Minerals Management Service (MMS). The new structure has created three separate organizations – one dealing with revenue collection, another with safety and the third focused on managing the development of the nation’s offshore resources in an environmentally and economically responsible way. The reorganization was designed to reduce and eliminate the conflicting roles the MMS was trying to perform and to increase the professionalism of the department. In reading Dir. Bromwich’s talk, there appeared to be little in the way of new information. Clearly during the question and answer time following the speech, at least according to the story reported by Dow Jones Newswire, Dir. Bromwich did offer some new information. He said that the primary question he is asked when he talks with operators of offshore drilling rigs is when the pace of permit approval will return to what it was before the Macondo oil spill began on April 20, 2010. His response to that question is, “The honest answer is probably never.” Given all the new rules and regulations now required of operators and rig owners, that response is probably quite accurate. That prospect, however, will certainly not boost the spirits of, nor help the planning by, the offshore industry. What may have been a shocker to the industry, however, was after he commented that new offshore drilling permits were coming he said, “I would be stunned if we waited until the third or fourth quarter.” Many industry people held out hope this summer that once the deepwater drilling moratorium was lifted permits would begin to flow. With the early termination of the deepwater drilling moratorium, it was anticipated that permits would be forthcoming quickly and that the industry would be drilling before the end of 2010. We are now well into January with no new deepwater drilling permits having been issued. Dir. Bromwich’s comment about the third and fourth quarters has to be a jolt to the offshore industry. I am sure that had the issuing of new deepwater drilling permits been imminent, Dir. Bromwich would have telegraphed that somehow in his speech or in responses to questions. The increased likelihood that the industry may go for a full year following the Macondo accident without a new deepwater drilling permit will have a negative impact on Gulf of Mexico capital spending, rig and auxiliary offshore equipment employment and the nation’s crude oil and natural gas supply in

MUSINGS FROM THE OIL PATCH PAGE 3

JANUARY 18, 2011

Should we begin passing out lengths of rope to the offshore industry?

2011 and likely 2012, too. Every day of further delay in granting permits increases the prospect of permanent damage to the domestic industry. In each act of Waiting for Godot the two characters contemplate suicide. The first time they decide not to follow through because possibly one of them might not die, leaving him alone, which they considered to be an intolerable situation. Instead, they decide to do nothing – “It’s safer.” At the end of the play, when informed that Godot would not be coming that day but rather the next, they contemplate suicide again, but the rope that is used as a belt by one of them turns out to be too short. They resolve to bring a longer rope the next day and hang themselves if Godot doesn’t show. Should we begin passing out lengths of rope to the offshore industry?

Why Are Electric Vehicles Darlings Of Detroit Auto Show? “But at the opening Monday of the big Detroit auto show, the internal-combustion engine seemed almost passé”

The North American International Auto Show in Detroit that kicks off the year for the global vehicle business featured a 37,000 square foot exposition space called Electric Avenue that featured 12 manufacturers of electric vehicles (EVs) ranging from traditional companies such as Nissan (NSANY.PK) and Mitsubishi Motors (MMTOF.PK) to entrepreneurial companies such as SSI Racing and Saba Motors. In addition, complimenting Electric Avenue was EcoXperience, an exhibit showcasing battery and electric motor technology important to the success of EVs. The show opens for nearly a week exclusively for 6,000 journalists and industry guests from around the world who view the automobile manufacturer exhibits showcasing their newest cars. On January 16th, the show opened to the public and expects about 600,000 visitors to pass through the convention facility. An article on Hybridcars.com captured the role of EVs at this show as its first line stated: “The 2010 North American International Auto Show in Detroit puts to rest once and for all any questions about whether electricity will be integral to the vehicle power-trains of tomorrow.” An article in The New York Times carried the EV theme even further when it said: “But at the opening Monday of the big Detroit auto show, the internal-combustion engine seemed almost passé.” So why all the focus on EVs at this auto show? The simple answer is “the government made me do it.” As Thomas Weber, the head of research and development at Mercedes-Benz, which plans to deliver the first of its B-Class F-cell electric cars to customers in the United States and Europe said, “Green technologies are the master key to the future of the automobile.” This statement comes at a time when consumers are less than enthusiastic about alternatives to internal combustion engines powered by gasoline. But maybe that has something to do with where gasoline prices have been.

MUSINGS FROM THE OIL PATCH PAGE 4

JANUARY 18, 2011

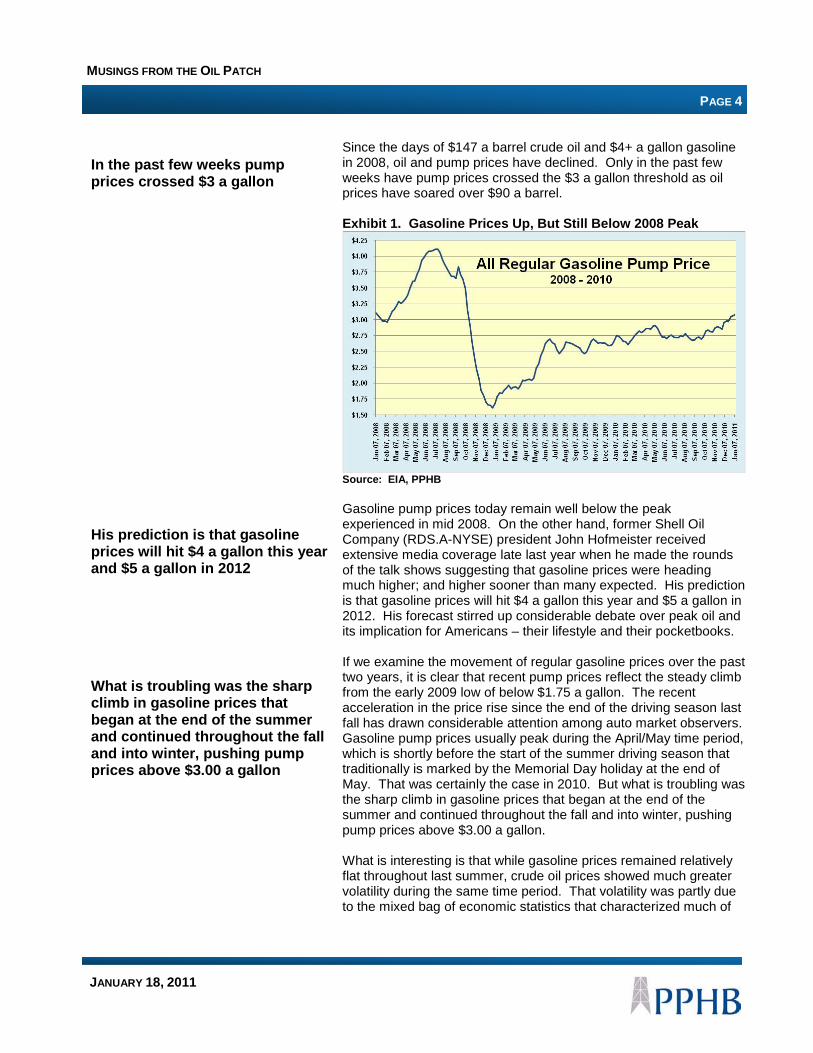

In the past few weeks pump prices crossed $3 a gallon His prediction is that gasoline prices will hit $4 a gallon this year and $5 a gallon in 2012 What is troubling was the sharp climb in gasoline prices that began at the end of the summer and continued throughout the fall and into winter, pushing pump prices above $3.00 a gallon

Since the days of $147 a barrel crude oil and $4+ a gallon gasoline in 2008, oil and pump prices have declined. Only in the past few weeks have pump prices crossed the $3 a gallon threshold as oil prices have soared over $90 a barrel. Exhibit 1. Gasoline Prices Up, But Still Below 2008 Peak

Source: EIA, PPHB Gasoline pump prices today remain well below the peak experienced in mid 2008. On the other hand, former Shell Oil Company (RDS.A-NYSE) president John Hofmeister received extensive media coverage late last year when he made the rounds of the talk shows suggesting that gasoline prices were heading much higher; and higher sooner than many expected. His prediction is that gasoline prices will hit $4 a gallon this year and $5 a gallon in 2012. His forecast stirred up considerable debate over peak oil and its implication for Americans – their lifestyle and their pocketbooks. If we examine the movement of regular gasoline prices over the past two years, it is clear that recent pump prices reflect the steady climb from the early 2009 low of below $1.75 a gallon. The recent acceleration in the price rise since the end of the driving season last fall has drawn considerable attention among auto market observers. Gasoline pump prices usually peak during the April/May time period, which is shortly before the start of the summer driving season that traditionally is marked by the Memorial Day holiday at the end of May. That was certainly the case in 2010. But what is troubling was the sharp climb in gasoline prices that began at the end of the summer and continued throughout the fall and into winter, pushing pump prices above $3.00 a gallon. What is interesting is that while gasoline prices remained relatively flat throughout last summer, crude oil prices showed much greater volatility during the same time period. That volatility was partly due to the mixed bag of economic statistics that characterized much of

MUSINGS FROM THE OIL PATCH PAGE 5

JANUARY 18, 2011

They believe the Fed’s policy creates a high risk of accelerating inflation beginning later in 2011

Exhibit 2. Gasoline Prices Starting To Climb

Source: EIA, PPHB 2010, however the uncertainty about the strength of the economic recovery led many economists to raise the possibility of a double-dip recession that would have undercut crude oil demand. In August, Federal Reserve Chairman Ben Bernanke suggested that the Fed might, and probably would, undertake a quantitative easing program (called QE2) that would involve buying longer term maturity Treasury securities in an attempt to drive down intermediate- and long-term interest rates. At the mere suggestion of the QE2 monetary easing action, bond investors and traders, money managers and various economists raised concerns over whether the Fed was merely creating a new asset bubble stoked by expanding the money supply through buying these bonds. They believe the Fed’s policy creates a high risk of accelerating inflation beginning later in 2011. That prospect sent the value of the U.S. dollar down, which has the near-term impact of pushing up the value of commodities that are traded in dollars and often used as a way to protect against depreciating currencies. Crude oil has become one of the most actively traded commodities just for that reason. This had the impact of driving crude oil prices higher with gasoline prices tracking that move. The interesting result from the rise of crude oil and gasoline prices was the impact on auto sales, but more importantly on the mix of sales. For example, U.S. auto consumers bought more Toyota Motor Company (TM-NYSE) hybrids last December, as gasoline prices reached their zenith and the initial projections of $5 a gallon gasoline appeared, than any other month in 2010. Year over year hybrid sales increased 13.6% while December’s sales increased 37% over the volume sold in November. These sales figures for Toyota’s hybrids compared with the company’s overall December sales performance of an 11.1% year-over-year increase and an 11%

MUSINGS FROM THE OIL PATCH PAGE 6

JANUARY 18, 2011

Prius, sold 15,639 vehicles in December, a 33% year-over-year increase A 2008 survey, when gasoline prices climbed above $4 a gallon, showed 62% of buyers considering a hybrid

month-over-month gain. Exhibit 3. Gasoline Price Tied Closely To Crude Oil Price

Source: EIA, PPHB The U.S. auto industry’s healthy sales increase for all of 2010 was accomplished without help from hybrids as their volume fell by 5%. Passenger car sales overall were only up 1% in 2010, as the industry’s sales increase was driven by a 21% rise in light duty truck sales, primarily pickups, vans and sport utility vehicles. Within Toyota’s hybrid sales figures, the granddaddy of the line, the Prius, sold 15,639 vehicles in December, a 33% year-over-year increase. For all of 2010, Prius sales advanced 0.5%. The Prius represented 8% of Toyota’s total car sales, which fell 5.5% for the year. It would appear from the December data that higher gasoline pump prices coupled with fear of sharply higher prices in the relatively near future helped drive hybrid car sales. An October 2010 telephone survey of perspective automobile buyers by Consumer Reports magazine showed that “driving green” considerations ranked only 11th of 12 possible motivating factors for buying a new car. The survey, however, determined that 39% of respondents were considering either a hybrid or a plug-in electric vehicle for their next car. That percentage, in hindsight, reflects consumers’ recent experiences with gasoline prices as a 2008 survey, when gasoline prices climbed above $4 a gallon, showed 62% of buyers considering a hybrid. It is interesting that the boost in hybrid sales occurred in December after four months of steadily rising gasoline pump prices. The National Automobile Dealers Association (NADA) just published its list of the Top 5 Factors That Will Boost Auto Sales in 2011

. These

MUSINGS FROM THE OIL PATCH PAGE 7

JANUARY 18, 2011

Rising gasoline prices will impact the types of vehicles sold EVs, on the other hand, are new, expensive and untested, besides the fact they create “range anxiety” among buyers The challenge is to make EVs more acceptable to buyers, i.e., address their range-anxiety concerns and reduce the vehicle cost “It’s going to take us three generations of range-extended electric vehicles to get anywhere near reasonable costs”

include: more car and truck choices; increased availability of low-interest credit; tax certainty; an improved stock market; and rising gasoline prices. Others had the same reaction we did: Rising gasoline prices? What they really meant was that higher gasoline pump prices will not necessarily increase the total number of cars sold, but will impact the types of vehicles sold and thus offer hope to the many new vehicle manufacturers entering the market with alternatively-powered vehicles. Clearly among this surge in new alternative-fuel powered vehicles are hybrids and EVs. Because hybrids are better established in the marketplace and have a longer history, even though they sell at a meaningful premium to their conventionally-powered cousins, they should be the primary beneficiary of this fear of peak oil and higher gasoline prices. EVs, on the other hand, are new, expensive and untested, besides the fact they create “range anxiety” among buyers. But EVs are the vehicle of choice in the energy plan being pushed by the Obama administration. A critical part of that plan was enacted last year with the new fuel-efficiency standard for automakers’ fleets that must average 35.5 miles a gallon by 2016, up from 27.5 miles a gallon today. The government is discussing plans to boost the standard to 60 miles a gallon by 2020. The only way auto manufacturers will meet the new standard (and the possible one) is to sell many more small cars, hybrids and EVs with their significantly greater fuel-efficiency performance. The challenge is to make EVs more acceptable to buyers, i.e., address their range-anxiety concerns and reduce the vehicle cost. These are the driving forces behind the push to develop a wide range of EV designs and to push for breakthroughs in the technology for powering EVs. The Detroit auto show highlighted a number of new, sporty EVs designed to attract younger and trend-setting buyers. General Motors (GM-NYSE) has attempted to address the range-anxiety issue with its Chevy Volt that has two small engines – one to recharge the battery and one to help power the vehicle – that allow it to recharge its battery once depleted while enabling the car to be driven longer distances than possible when only powered by the battery. The problem is that the Volt costs in excess of $40,000 without consideration of various tax credits, which is a price point that will prevent it from becoming a popular choice among auto buyers. The economic challenge presented by the Volt was best summed up by Thomas Stephens, G.M.’s vice chairman for product development, when he said, “It’s going to take us three generations of range-extended electric vehicles to get anywhere near reasonable costs. But if we’re going to be ready for the demand in 2020, we have to be out there by 2010 with the first generation.” EV acceptance will depend on the ability of owners to recharge them. At the present time the infrastructure does not exist – it really exists only in utility company plans for new charging stations.

MUSINGS FROM THE OIL PATCH PAGE 8

JANUARY 18, 2011

The key challenge each company faces is estimating the number of EVs that will reside in their territories and the impact they will have on electric power demand The projected fleet size also would be impacted by any technological breakthroughs that reduce the cost of EVs

However, there are other power system upgrades needed before there will be sufficient capacity for charging a large number of EVs. A recent presentation by three electric utility companies actively engaged in preparing for the arrival of EVs in their respective service territories shed light on the challenges they face. One company is NRG Energy (NRG-NYSE) that is developing an EV charging plan for Texas. Another was San Diego Gas & Electric (SDG&E), a part of Sempra Energy (SRE-NYSE) that has the largest utility customer base in the U.S. (until some recently announced utility company mergers are completed). The third presenting company was DTE Energy (DTE-NYSE), a Michigan electric and gas provider. The key challenge each company faces is estimating the number of EVs that will reside in their territories and the impact they will have on electric power demand. As California is leading the nation in embracing alternatively powered vehicles, we thought looking at its assumptions for the number of EVs in their territory would be of interest. The details of the chart in Exhibit 4 are difficult to read, but what SDG&E believes is that at the end of 2010 they had 1,100 plug-in hybrid electric vehicles (PHEVs) and 200 battery electric vehicles (BEVs). In their planning, SDG&E expects U.S. light duty vehicle (LDV) sales to grow by a 6.3% compounded annual growth rate (CAGR) over 2009-2012 and then by a 1% CAGR over 2012-2020. The company assumes that U.S. EV penetration increases to 22% of LDV sales in 2020. They further assume that the early adopter adjustment for SDG&E is 80% greater than the national average in 2010, decreasing to 50% in 2020. Their projection includes 100 Nissan Leaf EV deliveries in 2010 and 1,900 in 2011. The result of these assumptions is the estimate that SDG&E had 1,300 EVs (1,100 PHEVs and 200 BEVs) in 2010 and that this number grows to 62,500 EVs in 2015 (56,900 PHEVs and 5,600 BEVs). By 2020, the company expects the local auto fleet to contain 264,100 EVs (236,600 PHEVs and 27,500 BEVs). Is this a realistic projection? It could be realistic if the federal and state governments continue to provide tax incentives for buying and using EVs and that gasoline prices continue to escalate. In the case of California, other environmental regulations and incentives may further drive EV acceptance. The projected fleet size also would be impacted by any technological breakthroughs that reduce the cost of EVs. Likewise, if there are issues with the EV design or their battery life and/or performance, then the forecast could be at serious risk of over-estimating the size of the EV population. Given the comment made recently by Rebecca Lindland, an analyst in the auto research department of HIS Global Insight that “hybrids are less than 3 percent of the market, and they’ve been less than 3 percent for years, the idea that people are going to immediately accept electric vehicles when hybrids are such a small part of the market is sort of dangerous,” we need to be careful about

MUSINGS FROM THE OIL PATCH PAGE 9

JANUARY 18, 2011

The need to boost fleet fuel-efficiency ratings will force them to build more small cars and EVs, which will become the only choices available to customers Based on the penetration forecasts, its power grid would be at risk during on-peak times for transformer overloads

forecasting the future acceptance of EVs. Ms. Lindland may possibly be missing the power the federal government (Obama administration) has to push auto manufacturers to build EVs and, with the increasing auto fleet fuel-efficiency standard, forcing customers to buy them. Since auto manufacturers will not be able to continue to sell as many large, fuel-inefficient vehicles as in the past, the need to boost fleet fuel-efficiency ratings will force them to build more small cars and EVs, which will become the only choices available to customers when they venture to auto dealer showrooms. Much like the upcoming banning of incandescent light bulbs that leave consumers no option but to buy compact fluorescent light bulbs (CFLs), auto customers will have no option other than to buy small cars or EVs once the limited supply of big cars is exhausted. Exhibit 4. SDG&E Optimistic About EV Market Success

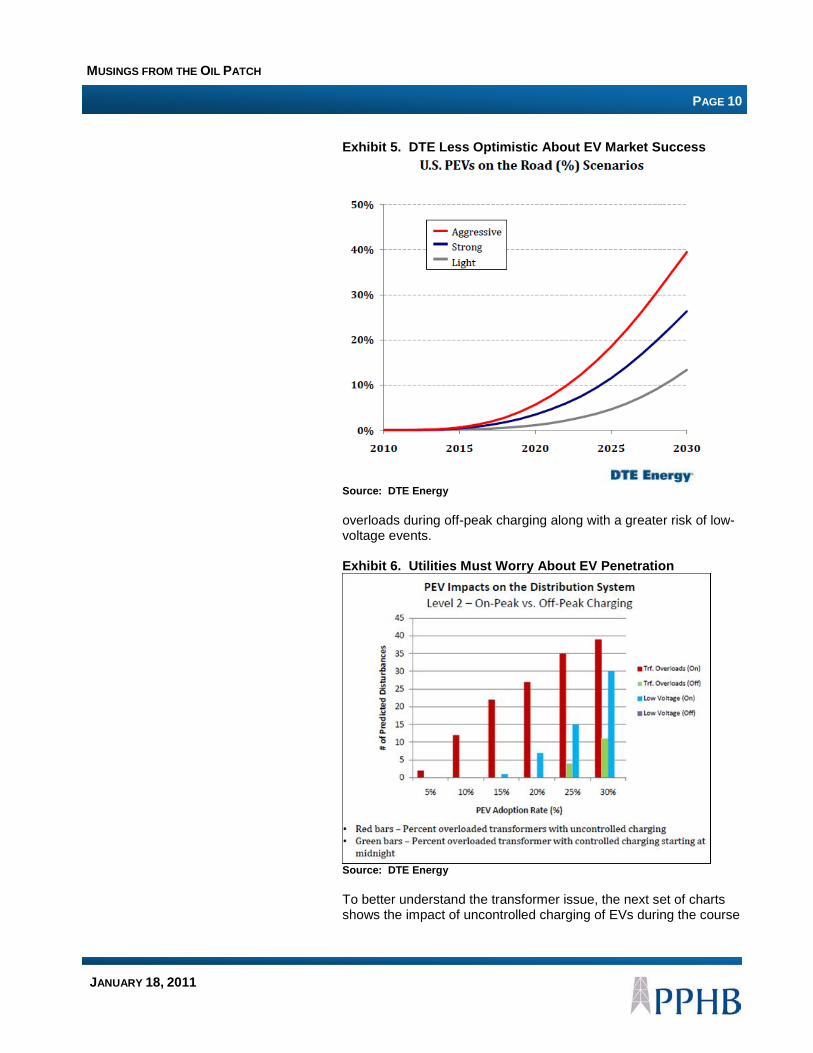

Source: SDG&E DTE Energy also has a planning scenario for the penetration of EVs into the car fleet. The company is considerably less optimistic about the EV penetration rate than other observers with their most aggressive rate representing only about 6% in 2020. The balance of the DTE presentation dealt with its infrastructure challenges and the implication for the company and its customers, which will impact the rate of EV acceptance. In a series of charts, the presenter outlined the challenge for the utility to handle the power needs of increased numbers of EVs. In the first chart, he showed the potential for transformer overloads based on on-peak and off-peak charging times and the amount of charging allowed (uncontrolled or controlled). Based on the penetration forecasts, its power grid would be at risk during on-peak times for transformer overloads. It is not until EV penetration reaches 15%-20% that the grid is at risk of low voltage, which impacts multiple customers beyond just those charging EVs. At higher EV penetration rates, DTE’s grid could experience transformer

MUSINGS FROM THE OIL PATCH PAGE 10

JANUARY 18, 2011

Exhibit 5. DTE Less Optimistic About EV Market Success

Source: DTE Energy overloads during off-peak charging along with a greater risk of low-voltage events. Exhibit 6. Utilities Must Worry About EV Penetration

Source: DTE Energy To better understand the transformer issue, the next set of charts shows the impact of uncontrolled charging of EVs during the course

MUSINGS FROM THE OIL PATCH PAGE 11

JANUARY 18, 2011

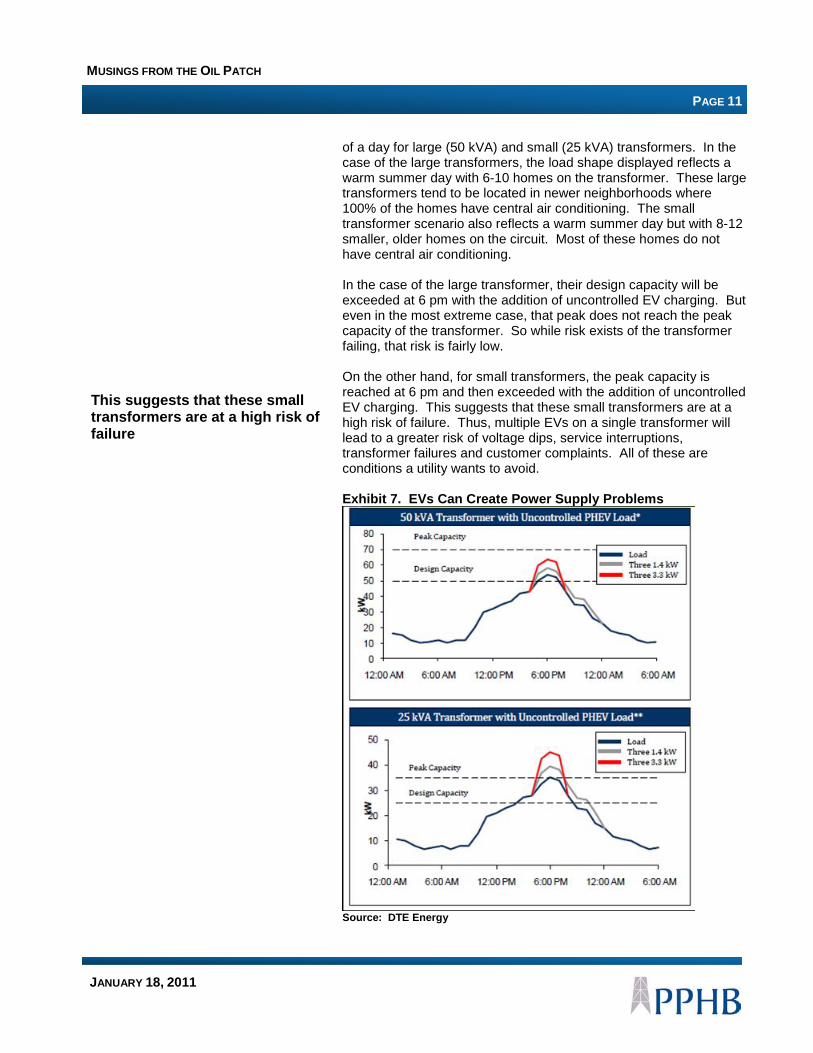

This suggests that these small transformers are at a high risk of failure

of a day for large (50 kVA) and small (25 kVA) transformers. In the case of the large transformers, the load shape displayed reflects a warm summer day with 6-10 homes on the transformer. These large transformers tend to be located in newer neighborhoods where 100% of the homes have central air conditioning. The small transformer scenario also reflects a warm summer day but with 8-12 smaller, older homes on the circuit. Most of these homes do not have central air conditioning. In the case of the large transformer, their design capacity will be exceeded at 6 pm with the addition of uncontrolled EV charging. But even in the most extreme case, that peak does not reach the peak capacity of the transformer. So while risk exists of the transformer failing, that risk is fairly low. On the other hand, for small transformers, the peak capacity is reached at 6 pm and then exceeded with the addition of uncontrolled EV charging. This suggests that these small transformers are at a high risk of failure. Thus, multiple EVs on a single transformer will lead to a greater risk of voltage dips, service interruptions, transformer failures and customer complaints. All of these are conditions a utility wants to avoid. Exhibit 7. EVs Can Create Power Supply Problems

Source: DTE Energy

MUSINGS FROM THE OIL PATCH PAGE 12

JANUARY 18, 2011

Nearly 50% of DTE’s transformers are small, and thus at risk from uncontrolled charging of EVs He sensed that the forecasted ramp up was more conservative than it was in 2010

In the case of DTE, the problem of EVs and small transformers is highlighted by the chart showing the distribution of the utility’s transformer sizes. Nearly 50% of DTE’s transformers are small, and thus at risk from uncontrolled charging of EVs. This means that EV customers must be incentivized to charge their vehicles during off-peak times or they have to be restricted as to when they can charge in order to minimize the risk of too many EVs on the same transformer at one time. Time of day power pricing is one possible solution. Since sales demographic data tends to support the view that early adopters of new technology tend to bunch together, for EVs this could produce serious operational performance challenges for utilities, especially those with older infrastructure. That suggests there will need to be significant investment in utility power grids in order to handle the projected growth in EVs. Or they will need to add many more customer support staff to deal with the complaints. Exhibit 8. DTE Infrastructure Dominated By Small Units

Source: DTE Energy Given the hype over EVs at the auto show, we found an analysis by John Petersen regarding the latest projections for EVs contained in the Energy Information Administration’s (EIA) Annual Energy Outlook for 2011 (AEO2011) quite interesting. Mr. Petersen looked at the assumptions for light duty vehicle sales by technology type in the AEO2011 report and discovered that the EIA has reduced their projections from prior reports. The assumptions underlie a 25-year forecast of sales for cars and trucks. Each category of vehicle has its sales forecast broken down by type of drive-train and fuel. Mr. Petersen said that when he looked at the 2011 projection for EVs he sensed that the forecasted ramp up was more conservative than it was in 2010. To confirm his view, he compared the data from the 2010 report to the 2011 report and found a 30% across the board reduction in the forecasted penetration rate for EVs. Based on the change in the forecast of EV sales between 2010 and 2011, Mr. Petersen went back to the forecasts made by the EIA in the annual energy outlooks since 2007. In each case, the EIA

MUSINGS FROM THE OIL PATCH PAGE 13

JANUARY 18, 2011

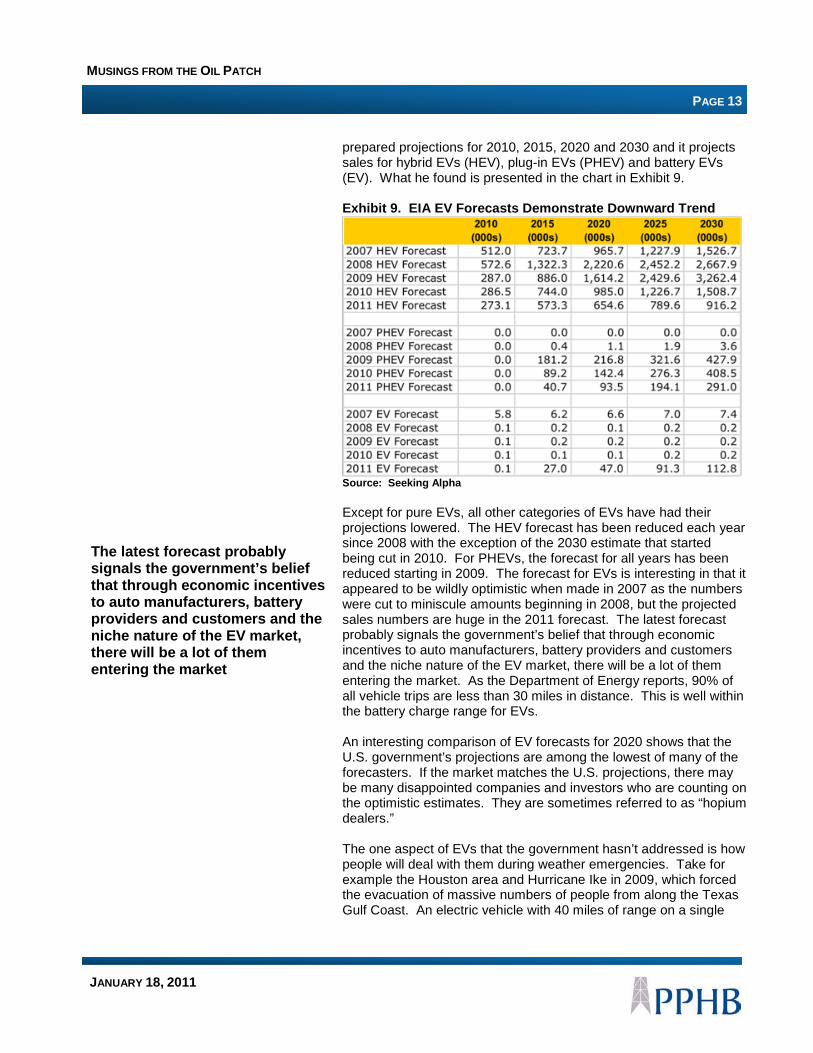

The latest forecast probably signals the government’s belief that through economic incentives to auto manufacturers, battery providers and customers and the niche nature of the EV market, there will be a lot of them entering the market

prepared projections for 2010, 2015, 2020 and 2030 and it projects sales for hybrid EVs (HEV), plug-in EVs (PHEV) and battery EVs (EV). What he found is presented in the chart in Exhibit 9. Exhibit 9. EIA EV Forecasts Demonstrate Downward Trend

Source: Seeking Alpha Except for pure EVs, all other categories of EVs have had their projections lowered. The HEV forecast has been reduced each year since 2008 with the exception of the 2030 estimate that started being cut in 2010. For PHEVs, the forecast for all years has been reduced starting in 2009. The forecast for EVs is interesting in that it appeared to be wildly optimistic when made in 2007 as the numbers were cut to miniscule amounts beginning in 2008, but the projected sales numbers are huge in the 2011 forecast. The latest forecast probably signals the government’s belief that through economic incentives to auto manufacturers, battery providers and customers and the niche nature of the EV market, there will be a lot of them entering the market. As the Department of Energy reports, 90% of all vehicle trips are less than 30 miles in distance. This is well within the battery charge range for EVs. An interesting comparison of EV forecasts for 2020 shows that the U.S. government’s projections are among the lowest of many of the forecasters. If the market matches the U.S. projections, there may be many disappointed companies and investors who are counting on the optimistic estimates. They are sometimes referred to as “hopium dealers.” The one aspect of EVs that the government hasn’t addressed is how people will deal with them during weather emergencies. Take for example the Houston area and Hurricane Ike in 2009, which forced the evacuation of massive numbers of people from along the Texas Gulf Coast. An electric vehicle with 40 miles of range on a single

MUSINGS FROM THE OIL PATCH PAGE 14

JANUARY 18, 2011

It sure would be nice to be able to drive your car more than one day!

Exhibit 10. EIA Least Optimistic On EV Market

Source: Seeking Alpha battery charge won’t even get you from Galveston to Houston. Even those EVs with an estimated 100-mile range still would not have gotten out of Ike’s path. But maybe more challenging would be the experience of people after hurricanes and even ice storms in other parts of the country when they are forced to go days without electricity. It sure would be nice to be able to drive your car more than one day! Has any government official thought about this problem?

Seismic Replaced By Fracturing, But E&P Cycle Building At the turn of the century, 3-D/4-D seismic technology was considered the most important technology by 58% of the respondents

We noted in the oil and gas industry capital spending survey conducted late last year by Barclays Capital (BCS-NYSE) that seismic was no longer considered the E&P industry’s top technology as it had been for many years. That mantle has been shifted to hydraulic fracturing technology, which, when married with improvements in the ability to drill horizontal wells, has contributed to the success in exploiting shale gas resources. For a number of years the Barclays survey (and its predecessor survey) has asked respondents to rank the most important technologies in the exploration and development business. In the latest survey, Barclays presented a table showing the ranking of the various technologies over the last decade. At the turn of the century, 3-D/4-D seismic technology was considered the most important technology by 58% of the respondents. For the 2011 survey, seismic technology was down to only a 19% ranking, which is the low end of the range of 19%-22% that has existed since 2007. Exhibit 11. Seismic Loses Most Important Technology Title

Source: Barclays Capital

MUSINGS FROM THE OIL PATCH PAGE 15

JANUARY 18, 2011

Seismic technology’s rise to prominence did not start in 2000 but rather was a function of the increased focus by oil and gas companies on growing their reserves and production organically through the drill bit during the 1990s Seismic crews onshore grow and shrink to match the size of the project being performed so there is no standard definition of a “crew”

Readers may wonder why seismic technology has experienced such erosion given its historical importance for E&P success. The decline is probably best explained by the shale gas phenomenon that has come to drive virtually the entire industry’s E&P efforts in the United States, and now even overseas areas. Seismic technology’s rise to prominence did not start in 2000 but rather was a function of the increased focus by oil and gas companies on growing their reserves and production organically through the drill bit during the 1990s. That desire became a reality with the introduction of new seismic equipment that helped revolutionized the business. Better data collection at a lower cost coupled with improved software for analyzing the geology sparked a surge in E&P activity. A facilitating factor in this seismic revolution was the dramatic increase in computing power that significantly reduced the cost and the time needed to process seismic data. What caught our eye recently was a press release issued by OYO Geospace (OYOG-Nasdaq) about the sale of a 7,000 single-channel GSR wireless seismic data acquisition system to BGP Inc., a subsidiary of China National Petroleum Corporation, and one of the world’s largest seismic data acquisition companies. OYO’s new GSR system represents the leading edge of the new technology in the seismic data acquisition industry. There were two reasons this announcement struck us. First, BGP’s role in the global seismic industry and especially within China is significant. Couple the company’s market presence with China’s growing thirst for oil and gas resources around the globe and one can see the potential for a whole new growth cycle for the seismic equipment business. Secondly, BGP has formed a joint venture with ION Geophysical Corporation (IO-NYSE) to design, develop, manufacture and sell land-based seismic data acquisition equipment. Included in this joint venture are ION’s cabled seismic data acquisition systems and its wireless system, FireFly®. Also included are ION’s sensors and its vibrator equipment. The size of the global seismic sector of the oilfield service industry is one of the most difficult to measure. Seismic crews onshore grow and shrink to match the size of the project being performed so there is no standard definition of a “crew.” In the offshore segment of the industry, seismic data is collected in all types of water – deepwater with vessels pulling multiple streamers containing seismic sensors and in shallow water where fewer streamers can be pulled due to structural impediments. Seismic data is also collected in the extremely shallow waters off the coast and often involve surveys spanning the coastal land and shallow waters, referred to as the transition zone. The one characteristic of all these markets is the logistical challenge of hauling the equipment around to perform the shoot.

MUSINGS FROM THE OIL PATCH PAGE 16

JANUARY 18, 2011

The trend throughout the history of the seismic industry is that as equipment becomes easier to handle and cheaper, the E&P industry desires more data to improve its analytical capabilities These systems are easier to deploy, more flexible in their layout, easily expandable, easier to maintain and deliver similar or better data translates into wireless systems being cheaper to operate

Another complicating factor about estimating the size of the seismic data acquisition market is the large number of local competitors. The chart below shows an estimate of the number of active seismic data acquisition crews both onshore and offshore for the month of June in 2009 and 2010. The global estimate shows essentially a flat crew count year over year. What is not known from the crew count is how much data, reflected in the number of channels recording data in a survey, is being collected. The trend throughout the history of the seismic industry is that as equipment becomes easier to handle and cheaper, the E&P industry desires more data to improve its analytical capabilities. As a result there has been a steadily increasing trend in the number of channels being deployed in surveys. Exhibit 12. Seismic Activity Flat; Market Growing Slowly

Source: Geokinetics (GOK-NYSE) What do the OYO and ION wireless systems offer the petroleum companies and the seismic contractors? Exhibit 13 contains a listing of the perceived advantages of a wireless seismic data acquisition system compared to the traditional cabled system. Due to the fact that these systems are easier to deploy, more flexible in their layout, easily expandable, easier to maintain and deliver similar or better data translates into wireless systems being cheaper to operate.

MUSINGS FROM THE OIL PATCH PAGE 17

JANUARY 18, 2011

The critical consideration a wireless system has been for customers to verify through use the performance claims It is possible that the petroleum industry could be on the cusp of another wave of significant seismic technology improvements The emerging success of wireless systems is also being tied to the growth of gas shale development The potential seismic industry environment is similar to one the industry experienced in the early to mid 1990s

On the other side of the ledger, there are certain perceived disadvantages of wireless systems with a major one being the limited battery life. Issues about the system’s inability to deliver data in near-real time and having to determine the location of the acquisition point from a satellite are relatively minor points given the huge cost and logistical advantage of wireless systems. However, the critical consideration a wireless system has been for customers to verify through use the performance claims. That appears to be happening. Exhibit 13. Challenges For Wireless Seismic Systems

Source: OYO Geospace The decision by BGP to not only become a partner and 16% shareholder in ION with its new wireless system but to also purchase an OYO system suggests that wireless systems may become the new standard for the industry. These developments are also coming at a time when petroleum industry capital spending is rising as operators are growing more confident about the sustainability of high crude oil prices and the likelihood of higher natural gas prices in the future, too. It is possible that the petroleum industry could be on the cusp of another wave of significant seismic technology improvements that help producers improve their investment returns by boosting exploration success rates and reducing finding and development costs. The emerging success of wireless systems is also being tied to the growth of gas shale development. While at one time it was thought that the blanket nature of gas shale formations in a basin obviated the need for seismic, the industry is now learning that shales also have “sweet spots” that can be identified with seismic. Seismic data is also contributing to improved knowledge of the natural fractures in shale formations that can improve recoverability by better planning of horizontal wells and their hydraulic fracturing applications. This technology can improve producer returns, which gains increased importance in a period of low natural gas prices. The potential seismic industry environment we are describing, marked by a wave of new seismic data acquisition equipment, is similar to one the industry experienced in the early to mid 1990s. At that time the industry was introducing a number of new, larger land data acquisition systems that produced more and better information enabling analysts to do more in-depth geological modeling. That capability spurred both a capital spending surge by seismic contractors along with increased interest in the newly collected data

MUSINGS FROM THE OIL PATCH PAGE 18

JANUARY 18, 2011

It may be another year before we know for sure whether or not these new wireless seismic data acquisition systems will spur an industry-wide revolution the new systems did during the 1990s

by producers. At that time, the company with the highest visibility and earnings leverage was Input Output (IO), which has been transformed into ION. The success of IO and seismic data acquirer Dawson Geophysical (DWSN-Nasdaq) during the early 1990s can be seen by looking at charts of their stock price performance during that period. Exhibit 14. IO Was Major Beneficiary Of 1990s New Equipment

Source: Yahoo Finance IO showed a dramatic price rise following its spin-off to the public in 1991 as the company’s size enabled its earnings to explode as the new series of data acquisition systems hit the market. During this period, IO had little real competition for its new systems. Dawson, on the other hand, is a seismic contractor that uses the hardware to collect data for oil and gas companies. (Exhibit 15 below.) As a result, it does not have as much earnings leverage from new systems, but rather sees its business grow as a result of increased customer demand for seismic data and data acquired by the new seismic hardware sold by companies such as IO. It may be another year before we know for sure whether or not these new wireless seismic data acquisition systems will spur an industry-wide revolution the new systems did during the 1990s. Our sense is that it will be confirmed as oil and gas companies are slowly getting back to work following the recession and financial turmoil of 2008-2009. The gas shale revolution underway, even with its poor economics, will also provide a strong underpinning to the seismic industry’s business. For many in the seismic industry, the next few years may become the fulfillment of that old bumper sticker: “Please Lord just give me one more boom. I promise not to screw it up!”

MUSINGS FROM THE OIL PATCH PAGE 19

JANUARY 18, 2011

Exhibit 15. Dawson Benefited From 1990s Equipment Phase

Source: Yahoo Finance

Dutch Opt For New Strategy On Energy And Renewables During the subsequent election campaign, then-candidate and now Prime Minister Mark Rutte remarked that “Windmills turn on subsidies” The old subsidy scheme had the effect of rewarding expensive renewable energy sources

Last year a new government was elected to lead the Netherlands. That government was formed by a coalition of right-wing political parties. One of the election issues was the policies of the previous government with respect to subsidizing the development of “green energy” projects. Their approach was in step with the policies of most of the Netherlands’ neighbors in Europe – heavily subsidize the development of expensive renewable energy sources through grants directly from the government. In May 2010, the government authorized the maximum subsidy possible of €4.5 billion ($6.0 billion) to support construction of two 300-megawatt (MW) offshore wind farms located off the country’s northern coast. During the subsequent election campaign, then-candidate and now Prime Minister Mark Rutte remarked that “Windmills turn on subsidies.” Late last year the new Dutch government announced a radically different renewable power subsidy scheme. Under the old scheme, subsidies were awarded based solely on the difference in cost between the technology in question and the cost of fossil-fuel generated electricity. The cost “deficit” was calculated by the Energy Research Center of the Netherlands (ECN), and still is under the new scheme. Last year, the deficit resulted in a subsidy to offshore wind power of 9.7 eurocents ($0.13) per kilowatt-hour; onshore wind 4.0 eurocents ($0.05), solar PV 43.0 eurocents ($0.58) and so forth. Under the old scheme, all power technologies were subsidized up to the amount they needed to be competitive with gas-fired and coal-fired power. The old subsidy scheme had the effect of rewarding expensive renewable energy sources. Under the new renewable power subsidy scheme, which takes effect at mid-year 2011, the subsidies will be allocated in stages, all based on the first-come, first-served principle. The subsidy in the first

MUSINGS FROM THE OIL PATCH PAGE 20

JANUARY 18, 2011

The challenge is that if any of these applicants are granted a subsidy, they will have to live with the level of subsidy granted and will be below the amount of subsidy determined by the ECN that they would have gotten had they filed under their appropriate stage They have been determined to be too expensive are solar power, large-scale biomass and offshore wind power For the government, the scheme will be much more cost-effective since it will be paid for by the energy users

stage will be 9.0 eurocents ($0.12) and only available to producers that have cost deficits of less than 9.0 eurocents. Based on figures from the ECN, the eligible renewable sources would include biogas, hydropower, power from waste processing installations, and gas from fermentation processes. Assuming subsidy money remains available then in the second stage, a subsidy of 11.0 eurocents ($0.15) would be available to producers of onshore wind power and fertilizer-based gas. Again, if money still remains, then in stage three the subsidy will be 13.0 eurocents ($0.17) and open to producers of hydropower and small-scale biomass. Finally, the fourth stage with a 15.0 eurocent ($0.20) subsidy would be available for electricity produced from all-purpose fermentation processes. There is also a “free category” of applicants for subsidies under the scheme. These include all the power providers listed as eligible under the four stages. They can apply during any of the stages. Additionally, producers with renewable energy forms with cost deficits of over 15.0 eurocents ($0.20) are also eligible to apply under this free option. The challenge is that if any of these applicants are granted a subsidy, they will have to live with the level of subsidy granted and will be below the amount of subsidy determined by the ECN that they would have gotten had they filed under their appropriate stage. However, with the prospect of a smaller subsidy pool, as the government has reduced the amount of subsidies it will grant from about €4.0 billion ($5.4 billion) to €1.5 billion ($2.0 billion) a year, renewable power project developers may want to grab for money, even if it is less, because the risk of no money being available is higher than in the past. Not included in any of the four subsidy stages because they have been determined to be too expensive are solar power, large-scale biomass and offshore wind power. Large-scale biomass and offshore wind power also do not qualify under the “free category.” For offshore wind power, other than the two large projects subsidized last year and a small, 100-MW project still to be financed out of the old subsidy program, there will likely not be any additional projects in Dutch waters for the foreseeable future. The new Dutch subsidy scheme stands in stark contrast to the policies of many of its neighbors such as Germany, the UK, Denmark and Ireland that continue to push to expand offshore wind power in their territorial waters. The rationale behind the government’s new subsidy scheme is “for the Netherlands to achieve the European renewable energy target in the most cost-effective way.” For the government, the scheme will be much more cost-effective since it will be paid for by the energy users in the form of a surcharge on their electricity and gas bills rather than from the government’s general funds. It is estimated that

MUSINGS FROM THE OIL PATCH PAGE 21

JANUARY 18, 2011

Long-term the government plans to step up investments in innovation and R&D in offshore wind power and other “expensive” forms of renewable energy By taking this approach, the government hopes to minimize the cost to the economy

the cost of the subsidies will be split about evenly between homeowners and businesses. The subsidy scheme does not translate into a total abandonment of offshore wind power according to government ministers. They stress that the Dutch government is working a two-prong plan – short-term and long-term. The new subsidy scheme is the short-term approach. Long-term the government plans to step up investments in innovation and R&D in offshore wind power and other “expensive” forms of renewable energy. While a radical change to subsidizing renewable energy projects, the Dutch plan strikes us as both sensible and effective. Rather than turn the traditional cost structure for power upside down in the country, by rewarding the least-costly providers, the government wants to attack high-cost power technologies. They hope to reduce the cost by investing in efforts to create technological breakthroughs that would significantly lower the cost of these expensive renewable energy forms. By taking this approach, the government hopes to minimize the cost to the economy. The R&D effort could lead to major breakthroughs that might spur the growth of these industries in the Netherlands and provide long-term economic benefits for the economy. We wonder if our Nobel prize-winning secretary of energy has ever considered this plan rather than to just push for tens of thousands of offshore wind turbines along the East Coast?

What Vintage Is Your Barrel Of Crude Oil? Two economists at the IMF recently examined the performance of crude oil and fine wines and concluded that their price behavior “has shown remarkable similarity”

In the world of investing, there have been many studies over the years showing how portfolios diversified across multiple asset classes are the secret to solid long-term investment returns – possibly producing less upside during stock market booms but offering greater downside protection in periods of market busts. It has been this research and the investment success demonstrated by leading college endowment funds practicing this strategy, including the use of commodities, which was largely responsible for the explosion in commodity investing by individuals. Two economists at the International Monetary Fund (IMF) recently examined the performance of crude oil and fine wines and concluded that their price behavior “has shown remarkable similarity.” The two economists presented their findings in a working paper published by the IMF. According to the economists, “Our results suggest that although fine wine can be considered as an investable asset, its behavior is not significantly different than other commodities and therefore may fail to enhance portfolio diversification.” The research study found that the statistical behavior of crude oil and fine wine prices demonstrated a correlation of over 90% during

MUSINGS FROM THE OIL PATCH PAGE 22

JANUARY 18, 2011

But overall in 2010, fine wine outperformed all other asset classes for the second consecutive year The two economists’ research led them to conclude that global macroeconomic variables also account for the bulk of the variation in fine wind prices, which is similar to the explanation for the movement in crude oil prices

Exhibit 16. Wine And Oil Prices Tend To Move Together

Source: IMF the time period studied. This is interesting in light of fine wine’s recent price performance. According to statistics quoted in a news article in the Financial Times, in December the price rise for fine wine was only 1% compared to equities that rose 6.7%, gold being up 2% and crude oil’s climb of 8.7%. But overall in 2010, fine wine outperformed all other asset classes for the second consecutive year, up 32% compared to gold, for example, rising only 22%. Research shows that over the past 15 years the average return on fine wine has been 15%. The study’s authors made the point that “Notwithstanding the continuing debate over the nature of price volatility, a plethora of recent studies has emphasized macroeconomic factors as the main determinants of crude oil prices over the last decade. On the other hand, most empirical research tends to explain the formation of wine prices with supply-side factors such as climatic conditions, grape quality, age effects, and external quality ratings.” The two economists’ research led them to conclude that global macroeconomic variables also account for the bulk of the variation in fine wind prices, which is similar to the explanation for the movement in crude oil prices. Exhibit 17. Dynamics Of The Crude Oil Market

Source: IMF

MUSINGS FROM THE OIL PATCH PAGE 23

JANUARY 18, 2011

Emerging market consumption accounted for the bulk of growth in global demand for high quality, investment grade wine Demand is the dominant factor in determining the behavior of crude oil and fine wine prices

We found some of the data cited in the study about the wine market quite fascinating. The economists found that per capita wine consumption has been declining in mature markets such as France and Italy while in emerging markets it has grown, albeit from a low base. As a result of that growth, emerging market consumption accounted for the bulk of growth in global demand for high quality, investment grade wine. That demand may also have been helped by income growth and wealth accumulation in these emerging markets relative to the trends in more mature economies. Exhibit 18. Dynamics Behind Fine Wine Market

Source: IMF The two most important conclusions from the empirical results of the study are that demand is the dominant factor in determining the behavior of crude oil and fine wine prices. As would be expected, production constraints have the expected effect on fine wine and crude oil prices. The second conclusion was that aggregate demand growth, especially in emerging markets, is the most decisive factor in determining crude oil and fine wine prices. These are interesting conclusions because within the past week in a letter to the editors of the Financial Times from two Washington, D.C. analysts claims that speculators are primarily responsible for the rise in crude oil prices because they supposedly control $50 billion of institutional money that is projected to flow into commodity indexes this year on top of the roughly $350 billion or more presently invested. I wonder what vintages these investors are buying today.

Contact PPHB: 1900 St. James Place, Suite 125 Houston, Texas 77056 Main Tel: (713) 621-8100 Main Fax: (713) 621-8166 www.pphb.com PPHB is an independent investment banking firm providing financial advisory services, including merger and acquisition and capital raising assistance, exclusively to clients in the energy service industry.