1 pedestrian traffic study pittsburgh downtown partnership fall 2006 prepared by: strategic metrics...

TRANSCRIPT

1

Pedestrian Traffic Study

Pittsburgh Downtown PartnershipFall 2006

Prepared by: STRATEGIC METRICS GROUP

www.strategicmetricsgroup.com 412.480.4332

2

SUMMARY OF KEY FINDINGSSUMMARY OF KEY FINDINGS

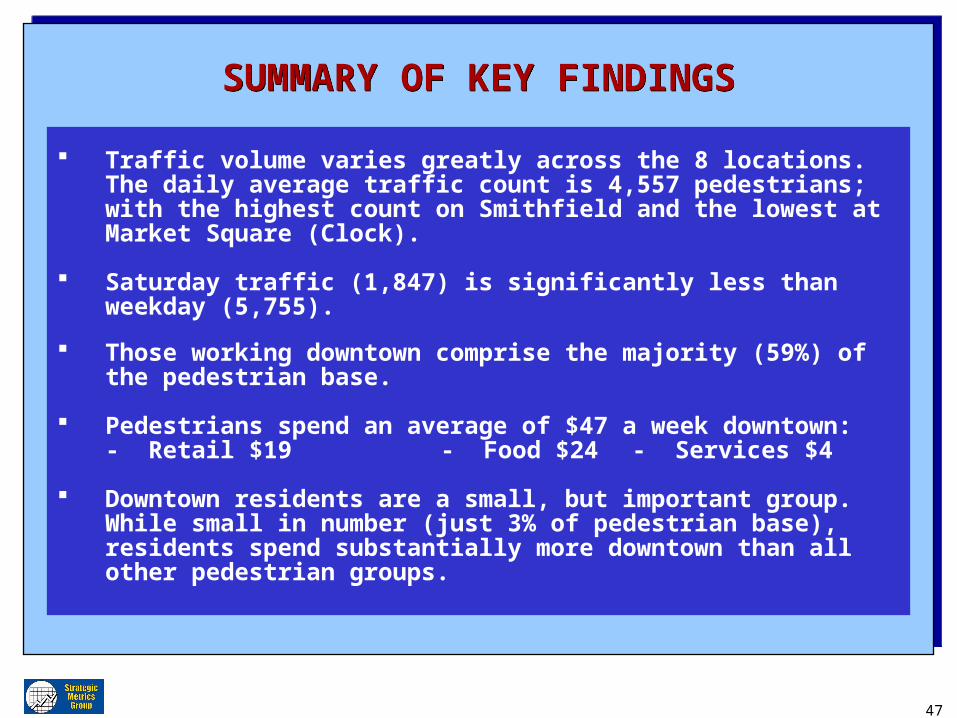

Traffic volume varies greatly across the 8 locations. The daily average traffic count is 4,557 pedestrians; with the highest count on Smithfield and the lowest at Market Square (Clock).

Saturday traffic (1,847) is significantly less than weekday (5,755).

Those working downtown comprise the majority (59%) of the pedestrian base.

Pedestrians spend an average of $47 a week downtown:- Retail $19 - Food $24 - Services $4

Downtown residents are a small, but important group. While small in number (just 3% of pedestrian base), residents spend substantially more downtown than all other pedestrian groups.

3

SUMMARY OF KEY FINDINGSSUMMARY OF KEY FINDINGS

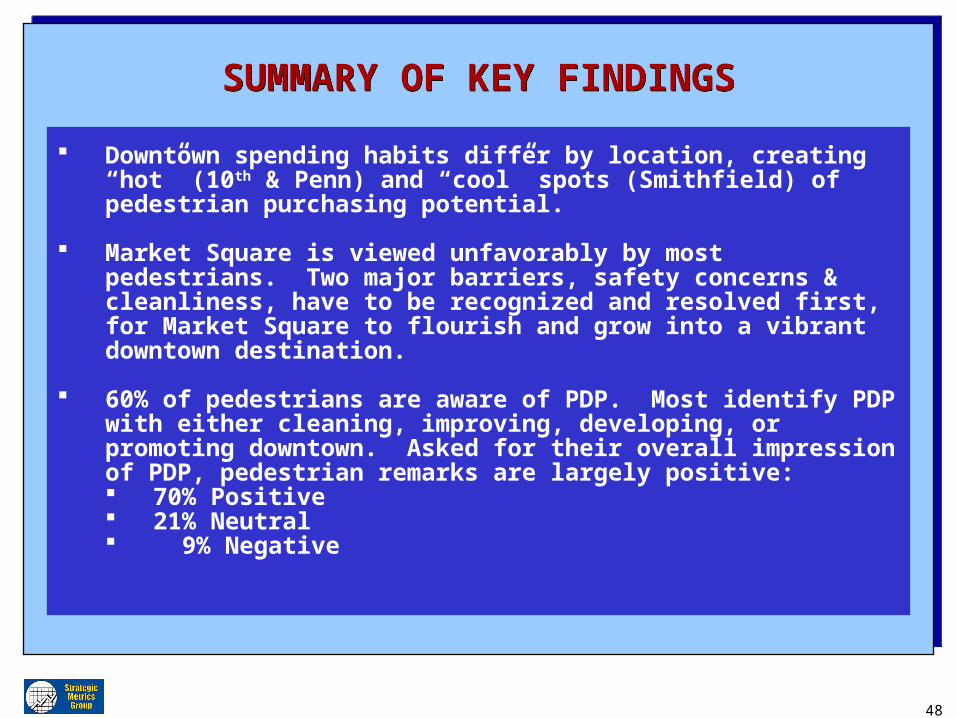

Downtown spending habits differ by location, creating “hot” (10th & Penn) and “cool” spots (Smithfield) of pedestrian purchasing potential.

Market Square is viewed unfavorably by most pedestrians. Two major barriers, safety concerns & cleanliness, have to be recognized and resolved first, for Market Square to flourish and grow into a vibrant downtown destination.

60% of pedestrians are aware of PDP. Most identify PDP with either cleaning, improving, developing, or promoting downtown. Asked for their overall impression of PDP, pedestrian remarks are largely positive: 70% Positive 21% Neutral 9% Negative

4

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

5

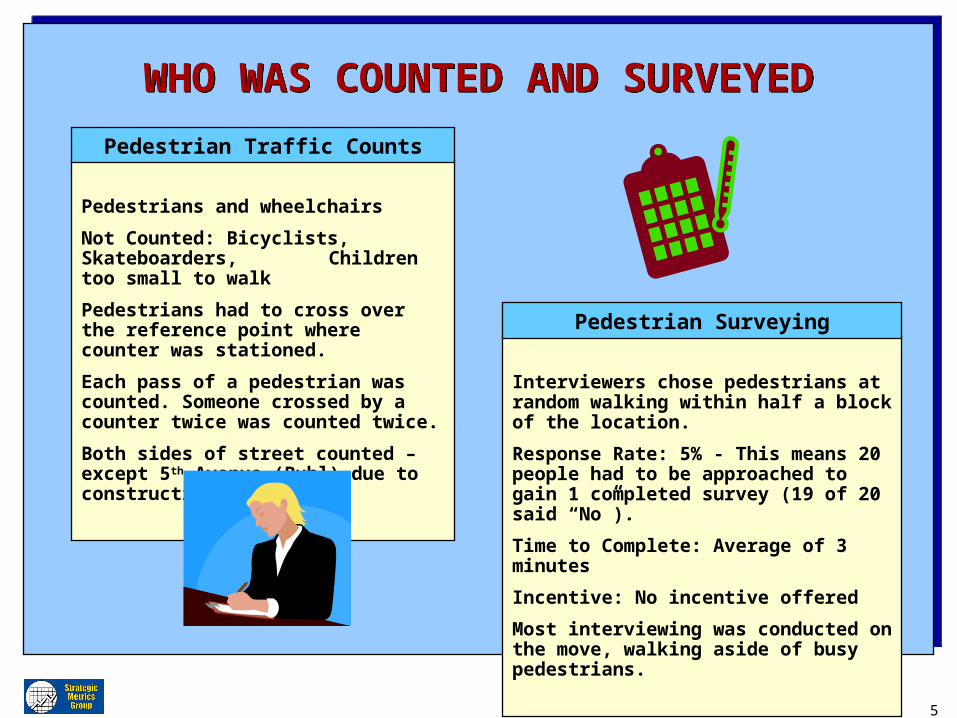

WHO WAS COUNTED AND SURVEYEDWHO WAS COUNTED AND SURVEYED

Pedestrians and wheelchairs

Not Counted: Bicyclists, Skateboarders, Children too small to walk

Pedestrians had to cross over the reference point where counter was stationed.

Each pass of a pedestrian was counted. Someone crossed by a counter twice was counted twice.

Both sides of street counted – except 5th Avenue (Buhl) due to construction.

Pedestrian Traffic Counts

Interviewers chose pedestrians at random walking within half a block of the location.

Response Rate: 5% - This means 20 people had to be approached to gain 1 completed survey (19 of 20 said “No”).

Time to Complete: Average of 3 minutes

Incentive: No incentive offered

Most interviewing was conducted on the move, walking aside of busy pedestrians.

Pedestrian Surveying

6

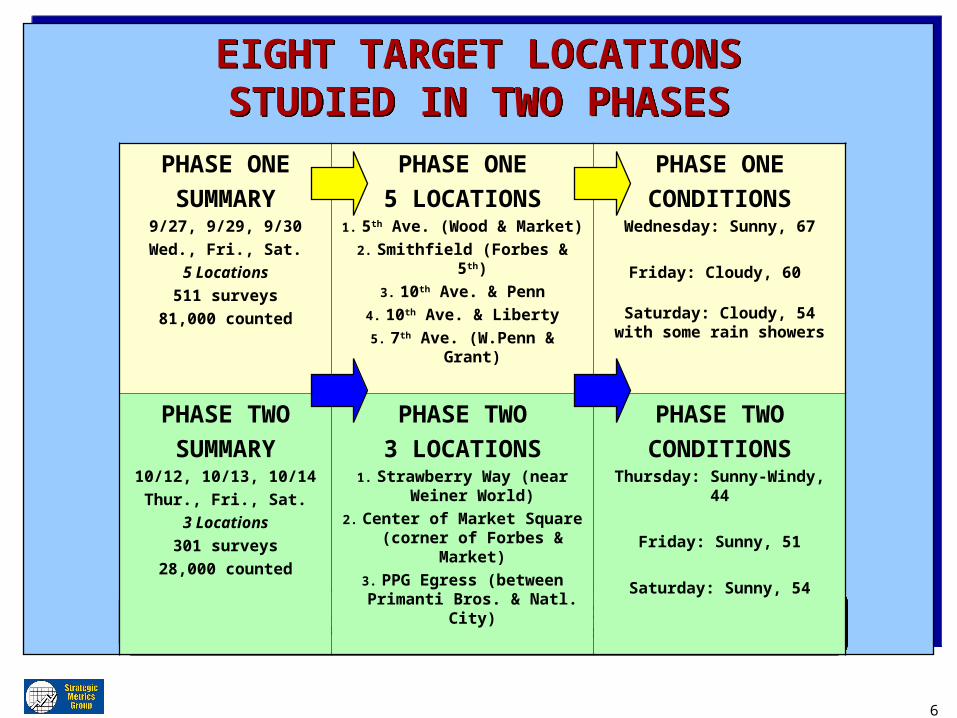

EIGHT TARGET LOCATIONSSTUDIED IN TWO PHASES

EIGHT TARGET LOCATIONSSTUDIED IN TWO PHASES

Surveying and counting were both conducted throughout entire 12 hour day (7:00 AM to 7:00 PM).

Surveying and counting were both conducted throughout entire 12 hour day (7:00 AM to 7:00 PM).

PHASE ONE

SUMMARY9/27, 9/29, 9/30

Wed., Fri., Sat.

5 Locations

511 surveys

81,000 counted

PHASE ONE

5 LOCATIONS1. 5th Ave. (Wood & Market)

2. Smithfield (Forbes & 5th)

3. 10th Ave. & Penn

4. 10th Ave. & Liberty

5. 7th Ave. (W.Penn & Grant)

PHASE ONE

CONDITIONSWednesday: Sunny, 67

Friday: Cloudy, 60

Saturday: Cloudy, 54 with some rain showers

PHASE TWO

SUMMARY10/12, 10/13, 10/14

Thur., Fri., Sat.

3 Locations

301 surveys

28,000 counted

PHASE TWO

3 LOCATIONS1. Strawberry Way (near Weiner

World)

2. Center of Market Square (corner of Forbes & Market)

3. PPG Egress (between Primanti Bros. & Natl. City)

PHASE TWO

CONDITIONSThursday: Sunny-Windy, 44

Friday: Sunny, 51

Saturday: Sunny, 54

7

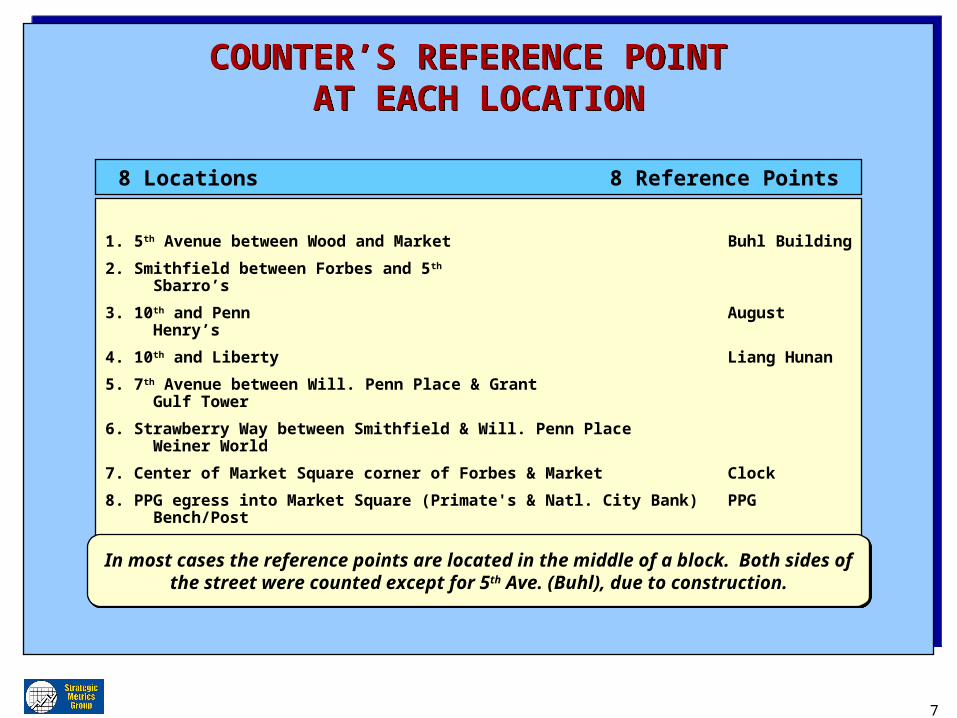

COUNTER’S REFERENCE POINT AT EACH LOCATION

COUNTER’S REFERENCE POINT AT EACH LOCATION

1. 5th Avenue between Wood and Market Buhl Building

2. Smithfield between Forbes and 5th Sbarro’s

3. 10th and Penn August Henry’s

4. 10th and Liberty Liang Hunan

5. 7th Avenue between Will. Penn Place & Grant Gulf Tower

6. Strawberry Way between Smithfield & Will. Penn Place Weiner World

7. Center of Market Square corner of Forbes & Market Clock

8. PPG egress into Market Square (Primate's & Natl. City Bank) PPG Bench/Post

8 Locations 8 Reference Points

In most cases the reference points are located in the middle of a block. Both sides of the street were counted except for 5th Ave. (Buhl), due to construction.

In most cases the reference points are located in the middle of a block. Both sides of the street were counted except for 5th Ave. (Buhl), due to construction.

8

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

9

TOTAL PEDESTRIAN TRAFFIC COUNT8 Locations

TOTAL PEDESTRIAN TRAFFIC COUNT8 Locations

0

2,000

4,000

6,000

8,000

10,000

0

2,000

4,000

6,000

8,000

10,000

n =109,356

A total of 109,356 pedestrians were counted over the entire project. Peak volume times include 8 AM, 5 PM, and the lunch or mid-day hour.

Time of Day

# of Pedestrians

10

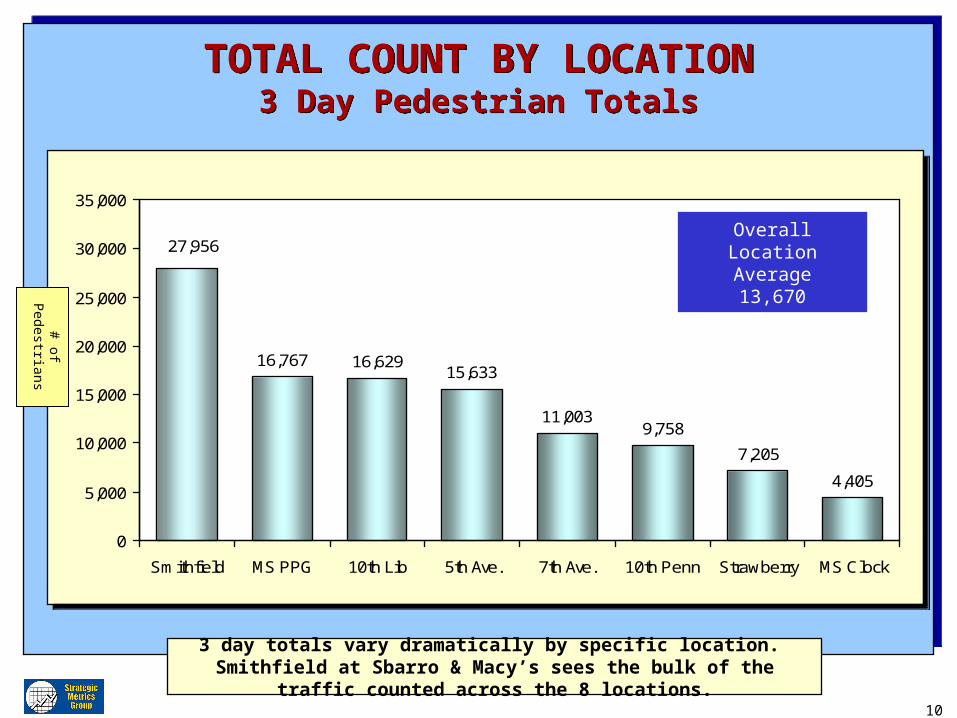

TOTAL COUNT BY LOCATION3 Day Pedestrian Totals

TOTAL COUNT BY LOCATION3 Day Pedestrian Totals

16,767 16,62915,633

11,0039,758

7,205

4,405

27,956

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Smithfield MS PPG 10th Lib 5th Ave. 7th Ave. 10th Penn Strawberry MS Clock

16,767 16,62915,633

11,0039,758

7,205

4,405

27,956

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Smithfield MS PPG 10th Lib 5th Ave. 7th Ave. 10th Penn Strawberry MS Clock

OverallLocation Average

13,670

3 day totals vary dramatically by specific location. Smithfield at Sbarro & Macy’s sees the bulk of the traffic counted across the 8 locations.

# of Pedestrians

11

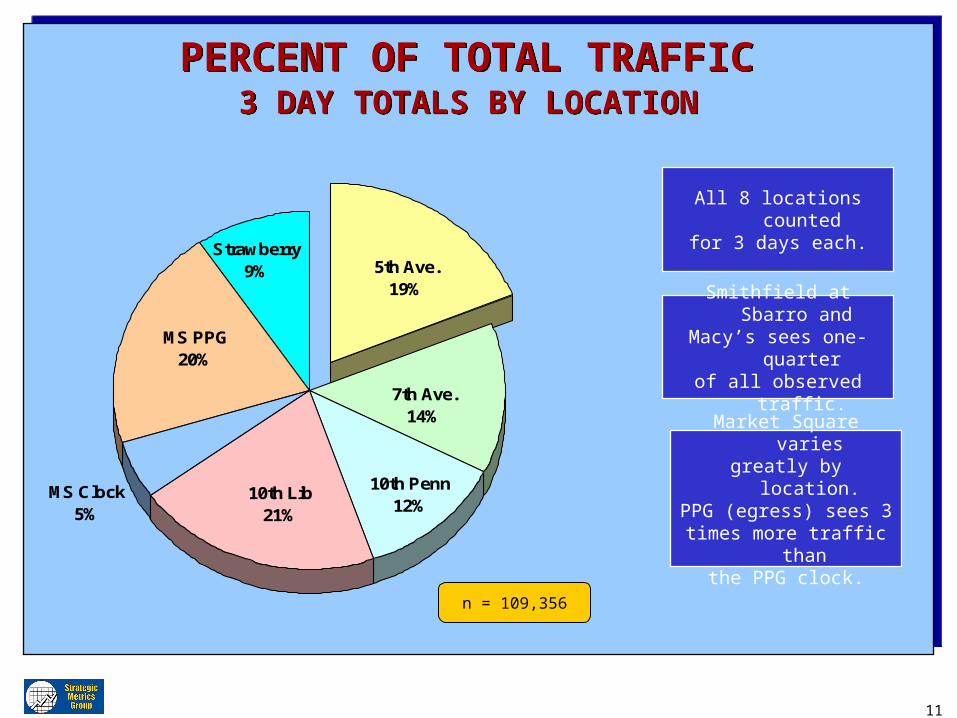

PERCENT OF TOTAL TRAFFIC 3 DAY TOTALS BY LOCATION

PERCENT OF TOTAL TRAFFIC 3 DAY TOTALS BY LOCATION

n = 109,356

All 8 locations countedfor 3 days each.

10th Penn12%

7th Ave.14%

5th Ave.19%

MS PPG20%

Strawberry9%

MS Clock5%

10th Lib21%

Smithfield at Sbarro and Macy’s sees one-quarter

of all observed traffic.

Market Square variesgreatly by location.

PPG (egress) sees 3times more traffic than

the PPG clock.

12

AVERAGE DAILY COUNT BY LOCATIONMean Number of Pedestrians

AVERAGE DAILY COUNT BY LOCATIONMean Number of Pedestrians

5,589 5,5435,211

3,6683,253

2,402

1,468

9,319

0

2,000

4,000

6,000

8,000

10,000

12,000

Smithfield MS PPG 10th Lib 5th Ave. 7th Ave. 10th Penn Strawberry MS Clock

5,589 5,5435,211

3,6683,253

2,402

1,468

9,319

0

2,000

4,000

6,000

8,000

10,000

12,000

Smithfield MS PPG 10th Lib 5th Ave. 7th Ave. 10th Penn Strawberry MS Clock

Overall DailyLocation Average

4,557

Each location average is based on a 3 day average – 2 weekdays and a Saturday.

# of Pedestrians

13

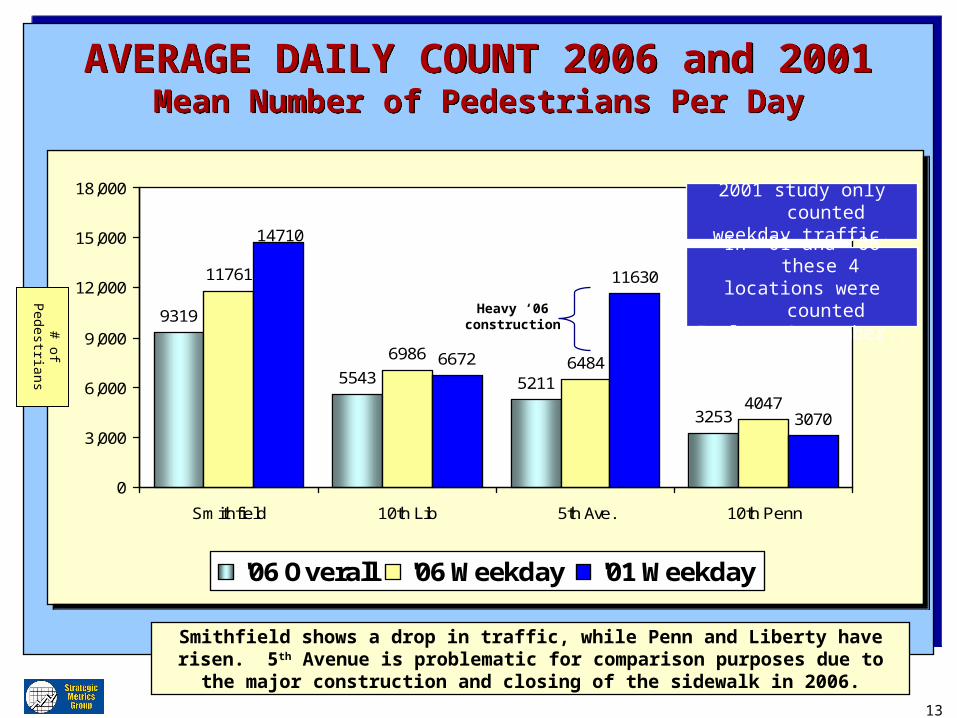

AVERAGE DAILY COUNT 2006 and 2001Mean Number of Pedestrians Per Day

AVERAGE DAILY COUNT 2006 and 2001Mean Number of Pedestrians Per Day

9319

5543 5211

3253

11761

69866484

4047

6672

11630

3070

14710

0

3,000

6,000

9,000

12,000

15,000

18,000

Smithfield 10th Lib 5th Ave. 10th Penn

'06 Overall '06 Weekday '01 Weekday

9319

5543 5211

3253

11761

69866484

4047

6672

11630

3070

14710

0

3,000

6,000

9,000

12,000

15,000

18,000

Smithfield 10th Lib 5th Ave. 10th Penn

'06 Overall '06 Weekday '01 Weekday

Smithfield shows a drop in traffic, while Penn and Liberty have risen. 5 th Avenue is problematic for comparison purposes due to the major construction and closing of

the sidewalk in 2006.

# of Pedestrians

Heavy ‘06construction

2001 study only countedweekday traffic.

In ’01 and ’06 these 4 locations were counted

In late September..

14

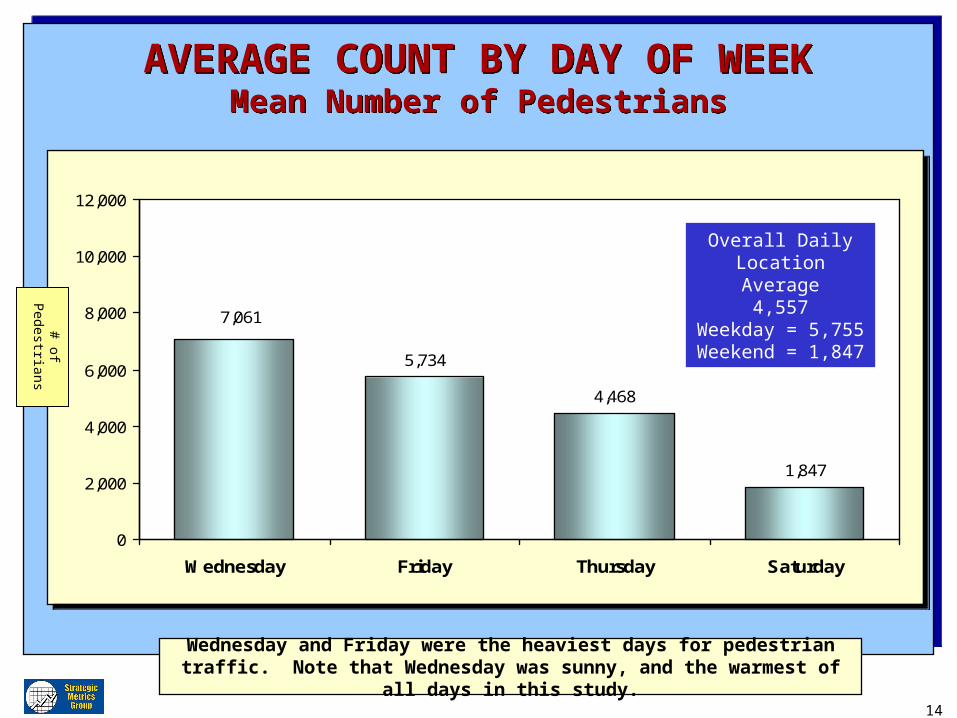

AVERAGE COUNT BY DAY OF WEEKMean Number of Pedestrians

AVERAGE COUNT BY DAY OF WEEKMean Number of Pedestrians

5,734

4,468

1,847

7,061

0

2,000

4,000

6,000

8,000

10,000

12,000

Wednesday Friday Thursday Saturday

5,734

4,468

1,847

7,061

0

2,000

4,000

6,000

8,000

10,000

12,000

Wednesday Friday Thursday Saturday

Wednesday and Friday were the heaviest days for pedestrian traffic. Note that Wednesday was sunny, and the warmest of all days in this study.

Overall DailyLocation Average

4,557Weekday = 5,755Weekend = 1,847

# of Pedestrians

15

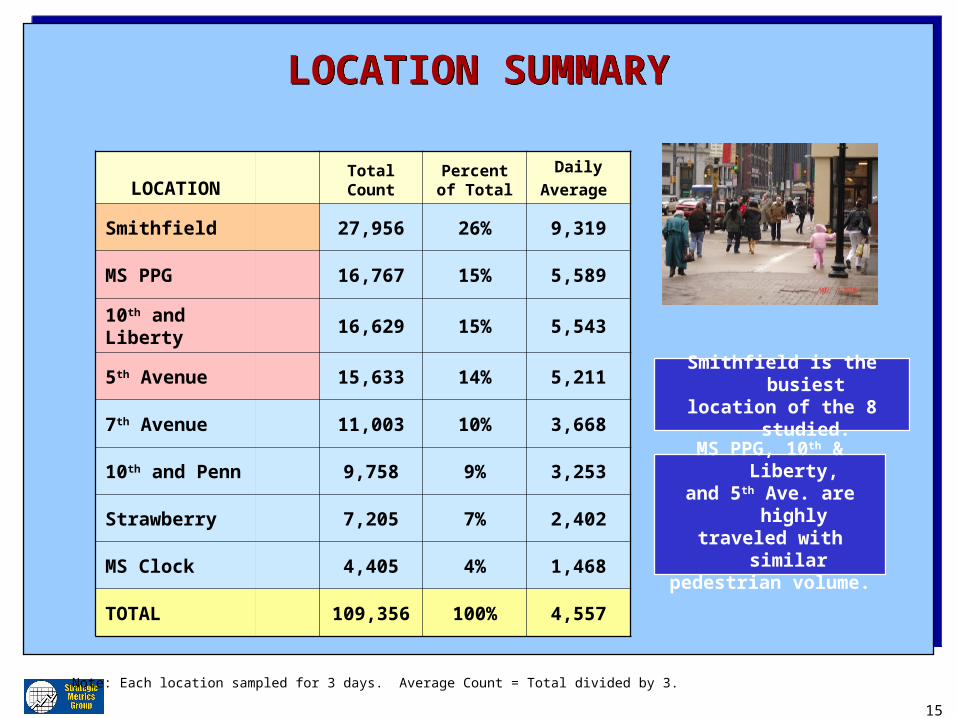

LOCATION SUMMARYLOCATION SUMMARY

LOCATIONTotal Count

Percent of Total

Daily

Average

Smithfield 27,956 26% 9,319

MS PPG 16,767 15% 5,589

10th and Liberty 16,629 15% 5,543

5th Avenue 15,633 14% 5,211

7th Avenue 11,003 10% 3,668

10th and Penn 9,758 9% 3,253

Strawberry 7,205 7% 2,402

MS Clock 4,405 4% 1,468

TOTAL 109,356 100% 4,557

Note: Each location sampled for 3 days. Average Count = Total divided by 3.

Smithfield is the busiestlocation of the 8 studied.

MS PPG, 10th & Liberty,and 5th Ave. are highlytraveled with similar pedestrian volume.

16

Wed Smith

Fri Smith

Thu MS PPG

Fri 5th Ave

Wed 10/Lib

Fri 10/Lib

Fri MS PPG

Wed 5th Ave

Wed 7th Ave

Fri 7th Ave

Sat Smith

Wed 10/Penn

Fri 10/Penn

Fri Straw

Thu Straw

Sat 5th Ave

Sat 10/Lib

Thu MS Clock

Fri MS Clock

Sat MS PPG

Sat 10/Penn

Sat 7th Ave

Sat MS Clock

Sat Straw

Wed Smith

Fri Smith

Thu MS PPG

Fri 5th Ave

Wed 10/Lib

Fri 10/Lib

Fri MS PPG

Wed 5th Ave

Wed 7th Ave

Fri 7th Ave

Sat Smith

Wed 10/Penn

Fri 10/Penn

Fri Straw

Thu Straw

Sat 5th Ave

Sat 10/Lib

Thu MS Clock

Fri MS Clock

Sat MS PPG

Sat 10/Penn

Sat 7th Ave

Sat MS Clock

Sat Strawn = 109,356

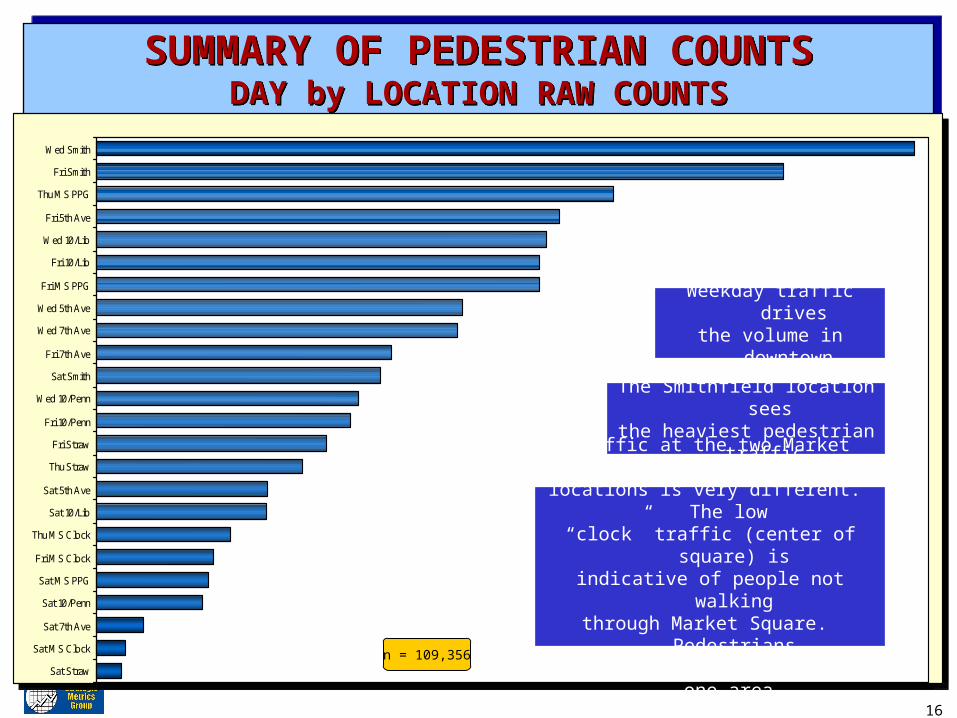

SUMMARY OF PEDESTRIAN COUNTSDAY by LOCATION RAW COUNTS

SUMMARY OF PEDESTRIAN COUNTSDAY by LOCATION RAW COUNTS

Weekday traffic drivesthe volume in downtown.

The Smithfield location seesthe heaviest pedestrian traffic.

Traffic at the two Market Square locations is very different. The low “clock” traffic (center of square) isindicative of people not walking

through Market Square. Pedestrianswalk the perimeter or stay in one area.

17

COUNT OF ALL TRAFFICCOUNT OF ALL TRAFFIC

WED THURFRI SAT TOTAL

Smithfield 12,785 NC 10,736 4,435 27,956

5th Avenue 5,731 NC 7,237 2,665 15,633

7th Avenue 5,648 NC 4,615 740 11,003

10th and Penn 4,110 NC 3,984 1,664 9,758

10th and Liberty 7,032 NC 6,939 2,658 16,629

Market Square Clock

NC 2,099 1,843 463 4,405

Market Square PPG

NC 8,079 6,935 1,753 16,767

Strawberry Way NC 3,227 3,583 395 7,205

TOTAL 35,306 13,405 45,872 14,773 109,356

n = 109,356Note: NC = “not counted”. Phase 1 counted on Wed., Phase 2 on Thur..

18

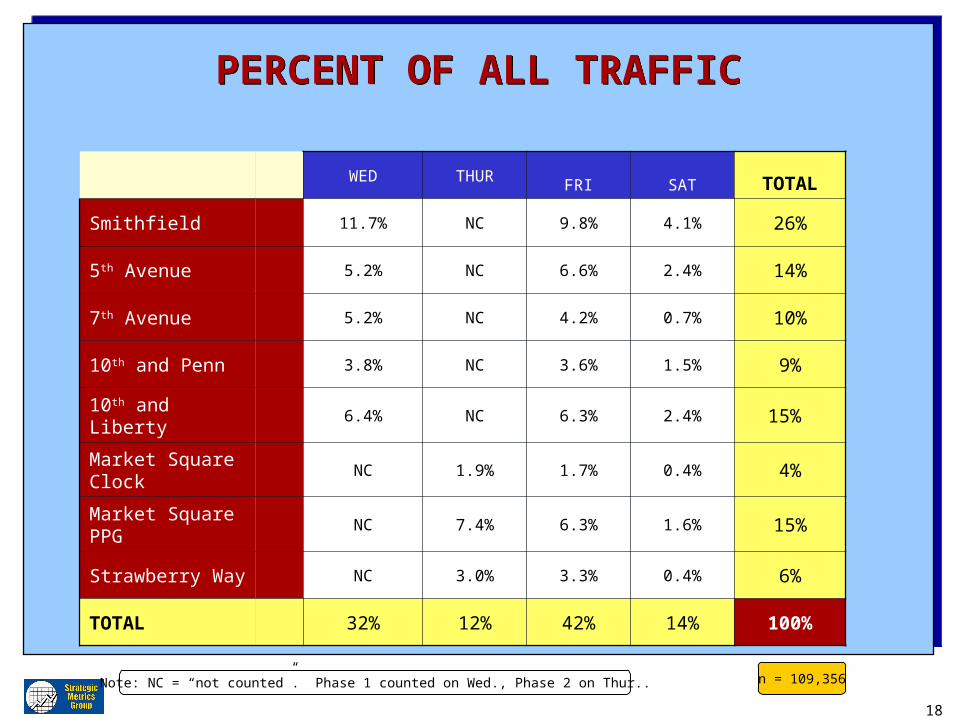

PERCENT OF ALL TRAFFICPERCENT OF ALL TRAFFIC

WED THURFRI SAT TOTAL

Smithfield 11.7% NC 9.8% 4.1% 26%

5th Avenue 5.2% NC 6.6% 2.4% 14%

7th Avenue 5.2% NC 4.2% 0.7% 10%

10th and Penn 3.8% NC 3.6% 1.5% 9%

10th and Liberty 6.4% NC 6.3% 2.4% 15%

Market Square Clock

NC 1.9% 1.7% 0.4% 4%

Market Square PPG

NC 7.4% 6.3% 1.6% 15%

Strawberry Way NC 3.0% 3.3% 0.4% 6%

TOTAL 32% 12% 42% 14% 100%

n = 109,356Note: NC = “not counted”. Phase 1 counted on Wed., Phase 2 on Thur..

19

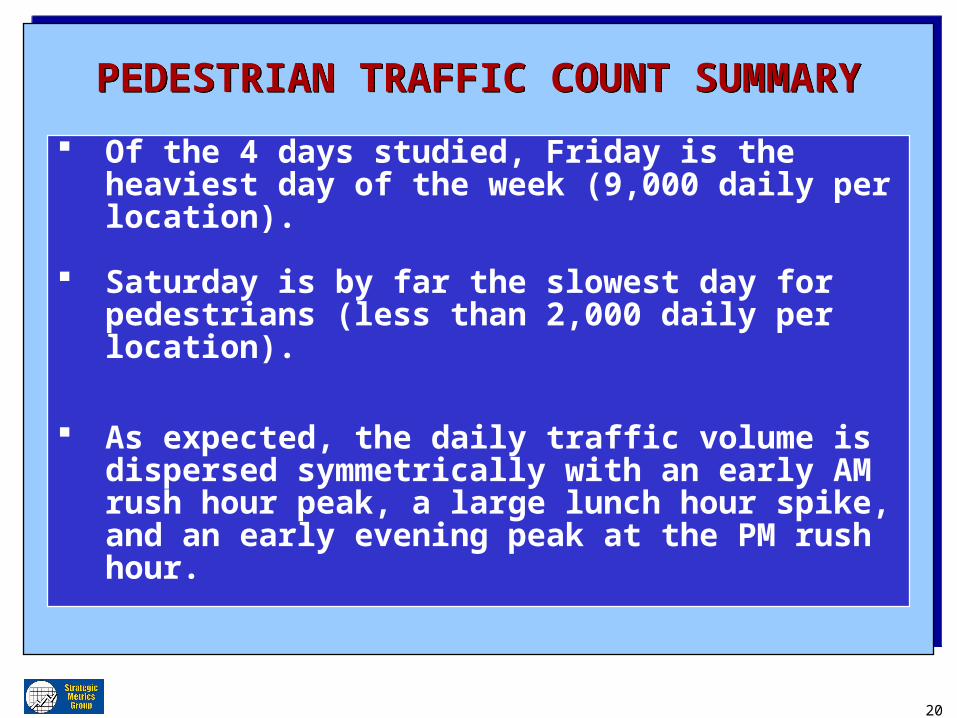

PEDESTRIAN TRAFFIC COUNT SUMMARYPEDESTRIAN TRAFFIC COUNT SUMMARY

8 downtown locations are each studied across a 3 day period.

The study period includes 2 weekdays and a Saturday.

Counting is conducted from 7:00 AM to 7:00 PM.

109,356 pedestrians are counted in the study.

An average of 4,557 pedestrians cross a given location in the 12 hour period. Average daily counts by location range from a high of 9,300 (Smithfield) to a low of 1,500 at the Market Square Clock.

8 downtown locations are each studied across a 3 day period.

The study period includes 2 weekdays and a Saturday.

Counting is conducted from 7:00 AM to 7:00 PM.

109,356 pedestrians are counted in the study.

An average of 4,557 pedestrians cross a given location in the 12 hour period. Average daily counts by location range from a high of 9,300 (Smithfield) to a low of 1,500 at the Market Square Clock.

20

PEDESTRIAN TRAFFIC COUNT SUMMARYPEDESTRIAN TRAFFIC COUNT SUMMARY

Of the 4 days studied, Friday is the heaviest day of the week (9,000 daily per location).

Saturday is by far the slowest day for pedestrians (less than 2,000 daily per location).

As expected, the daily traffic volume is dispersed symmetrically with an early AM rush hour peak, a large lunch hour spike, and an early evening peak at the PM rush hour.

21

PRESENTATION OVERVIEW PRESENTATION OVERVIEW

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

22

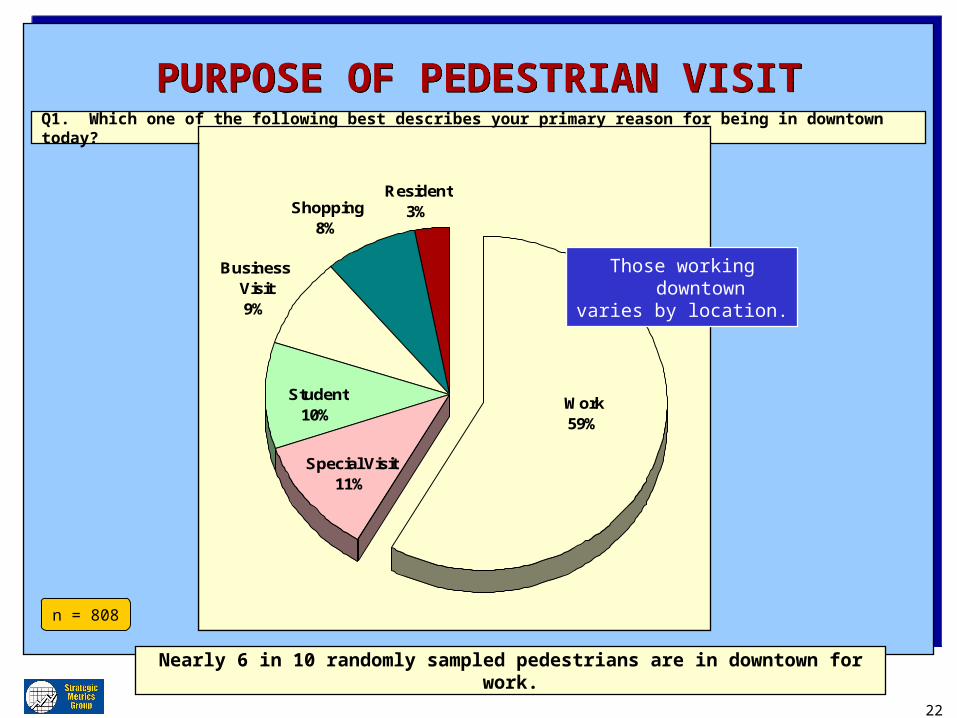

PURPOSE OF PEDESTRIAN VISITPURPOSE OF PEDESTRIAN VISITQ1. Which one of the following best describes your primary reason for being in downtown today?

n = 808

Shopping8%

Resident3%

Business Visit9%

Work59%

Special Visit11%

Student10%

Nearly 6 in 10 randomly sampled pedestrians are in downtown for work.

Those working downtown varies by location.

23

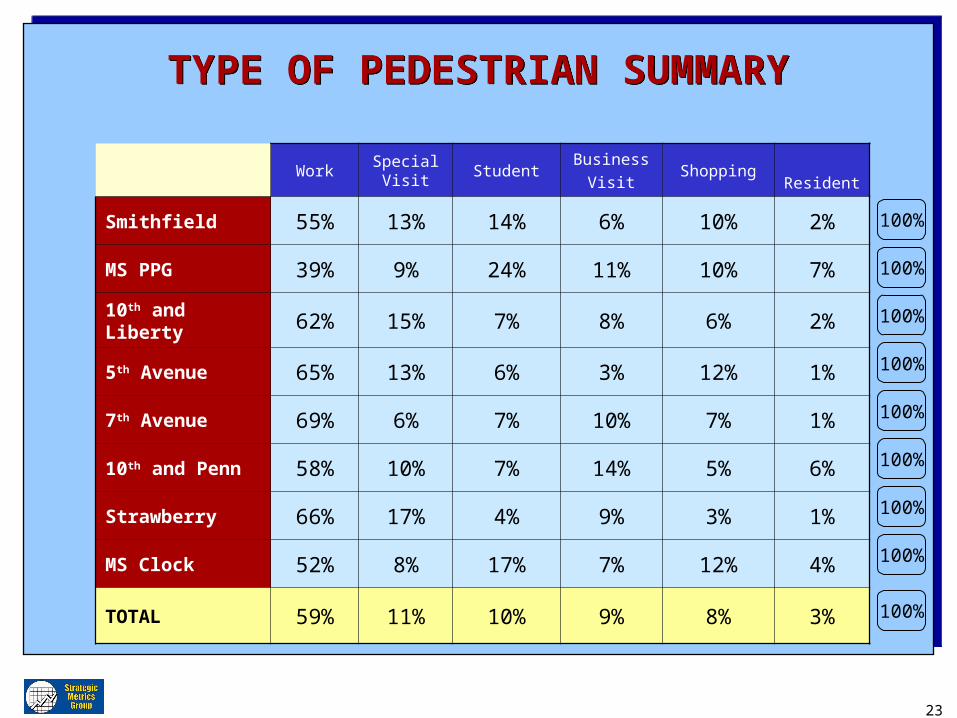

TYPE OF PEDESTRIAN SUMMARYTYPE OF PEDESTRIAN SUMMARY

WorkSpecial

VisitStudent

Business

VisitShopping

Resident

Smithfield 55% 13% 14% 6% 10% 2%

MS PPG 39% 9% 24% 11% 10% 7%

10th and Liberty 62% 15% 7% 8% 6% 2%

5th Avenue 65% 13% 6% 3% 12% 1%

7th Avenue 69% 6% 7% 10% 7% 1%

10th and Penn 58% 10% 7% 14% 5% 6%

Strawberry 66% 17% 4% 9% 3% 1%

MS Clock 52% 8% 17% 7% 12% 4%

TOTAL 59% 11% 10% 9% 8% 3% 100%

100%

100%

100%

100%

100%

100%

100%

100%

24

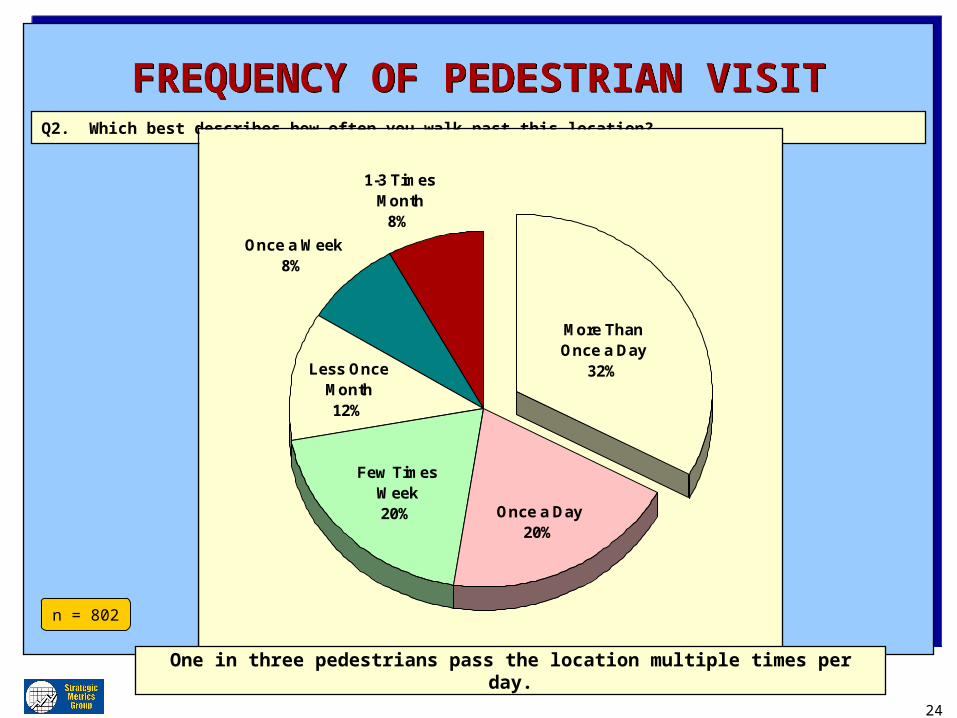

FREQUENCY OF PEDESTRIAN VISITFREQUENCY OF PEDESTRIAN VISITQ2. Which best describes how often you walk past this location?

n = 802

Once a Week8%

1-3 Times Month

8%

Less Once Month12%

More Than Once a Day

32%

Once a Day20%

Few Times Week20%

One in three pedestrians pass the location multiple times per day.

25

VISIT PURPOSE SUMMARYVISIT PURPOSE SUMMARY

The largest block of pedestrians surveyed (59%) are downtown because they work downtown. Special Visitors (11%) and Students (10%) comprise the second largest block of downtown pedestrians.

Business visitors (9%), Shoppers (8%), and Residents (3%) comprise the third, and smallest group of pedestrians.

7th Avenue (Gulf) and Strawberry Way (Weiner World) see more work force pedestrians than the other 6 locations. Market Square Clock and Market Square PPG (National City) see the lowest percentage of downtown work force pedestrians.

26

VISIT FREQUENCY SUMMARYVISIT FREQUENCY SUMMARY

Half of those surveyed walk by the location once a day or more. One-third pass by the location multiple times per day.

The number of repeated passes pedestrians make past a location is linked to the purpose of the downtown visit.

Downtown workers and residents make more frequent and repeated passes by locations than all other groups.

Shoppers and Special Visitors (Dining, Theatre, Sporting Event) make the lowest number of passes by a location.

27

DOLLARS SPENT - DOWNTOWN RETAILAmount Spent in a Typical Week

DOLLARS SPENT - DOWNTOWN RETAILAmount Spent in a Typical Week

4%

18% 17%

6%2%

53%

0%

20%

40%

60%

80%

$0 $1 - 5 $6 - 20 $21 - 50 $51 - 100 $101 +

% o

f R

espo

nden

ts

4%

18% 17%

6%2%

53%

0%

20%

40%

60%

80%

$0 $1 - 5 $6 - 20 $21 - 50 $51 - 100 $101 +

% o

f R

espo

nden

ts

n = 812

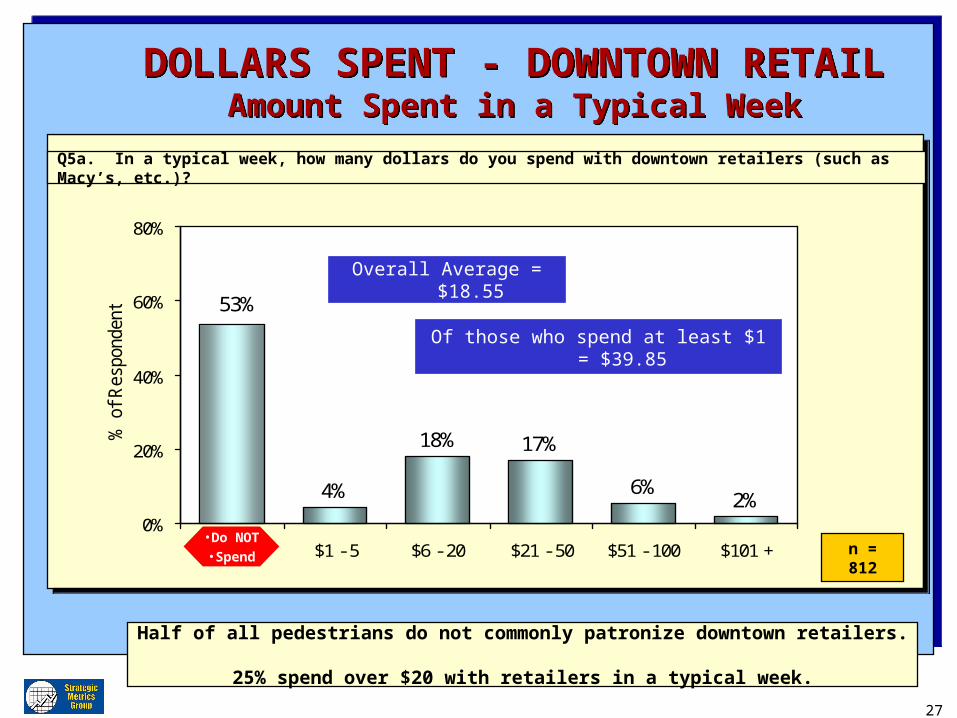

Half of all pedestrians do not commonly patronize downtown retailers. 25% spend over $20 with retailers in a typical week.

Q5a. In a typical week, how many dollars do you spend with downtown retailers (such as Macy’s, etc.)?

Overall Average = $18.55

Of those who spend at least $1 = $39.85

•Do NOT•Spend

28

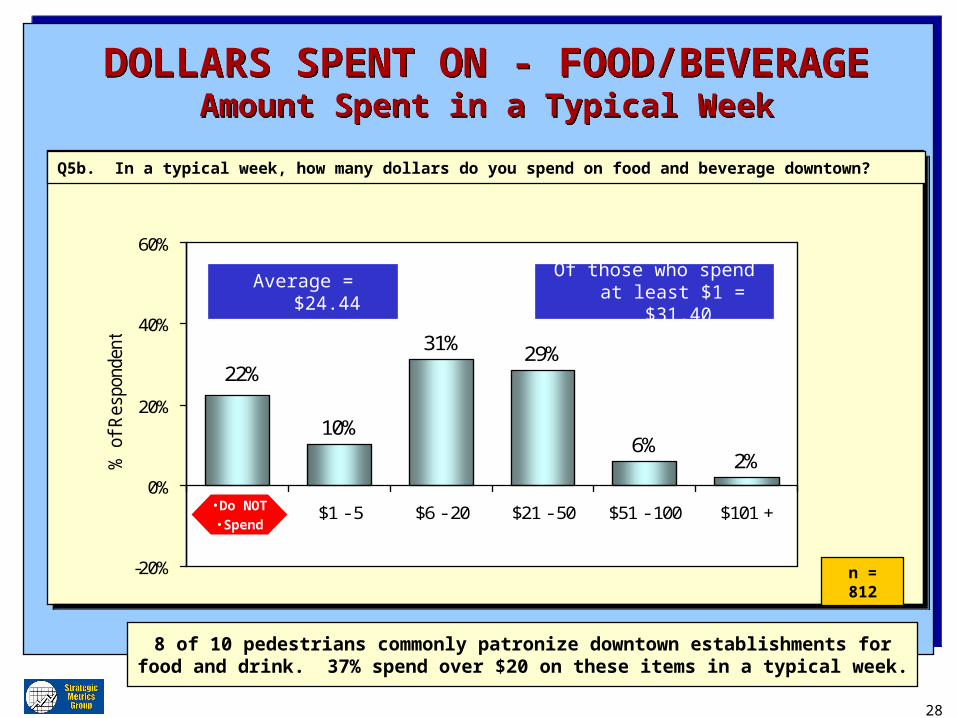

DOLLARS SPENT ON - FOOD/BEVERAGEAmount Spent in a Typical Week

DOLLARS SPENT ON - FOOD/BEVERAGEAmount Spent in a Typical Week

10%

31% 29%

6%2%

22%

-20%

0%

20%

40%

60%

$0 $1 - 5 $6 - 20 $21 - 50 $51 - 100 $101 +

% o

f R

espo

nden

ts

10%

31% 29%

6%2%

22%

-20%

0%

20%

40%

60%

$0 $1 - 5 $6 - 20 $21 - 50 $51 - 100 $101 +

% o

f R

espo

nden

ts

n = 812

8 of 10 pedestrians commonly patronize downtown establishments for food and drink. 37% spend over $20 on these items in a typical week.

Q5b. In a typical week, how many dollars do you spend on food and beverage downtown?

Average = $24.44Of those who spend at

least $1 = $31.40

•Do NOT•Spend

29

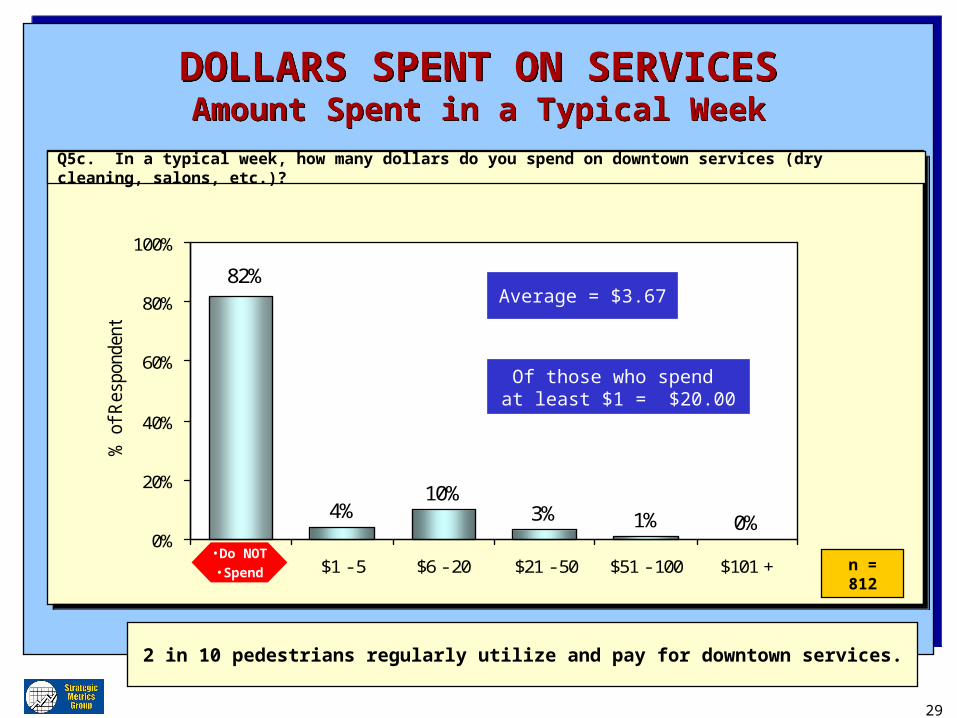

DOLLARS SPENT ON SERVICESAmount Spent in a Typical Week

DOLLARS SPENT ON SERVICESAmount Spent in a Typical Week

4%10%

3% 1% 0%

82%

0%

20%

40%

60%

80%

100%

$0 $1 - 5 $6 - 20 $21 - 50 $51 - 100 $101 +

% o

f R

espo

nden

ts

4%10%

3% 1% 0%

82%

0%

20%

40%

60%

80%

100%

$0 $1 - 5 $6 - 20 $21 - 50 $51 - 100 $101 +

% o

f R

espo

nden

ts

n = 812

2 in 10 pedestrians regularly utilize and pay for downtown services.

Q5c. In a typical week, how many dollars do you spend on downtown services (dry cleaning, salons, etc.)?

Average = $3.67

Of those who spend at least $1 = $20.00

•Do NOT•Spend

30

$21 $21 $19 $17 $19 $12 $16

$37$30 $25 $26

$22 $21$18 $17

$3 $4 $4$6 $3

$4 $1

$21

$4

$0

$15

$30

$45

$60

$75

$90

Retail Food & Bev Services

$21 $21 $19 $17 $19 $12 $16

$37$30 $25 $26

$22 $21$18 $17

$3 $4 $4$6 $3

$4 $1

$21

$4

$0

$15

$30

$45

$60

$75

$90

Retail Food & Bev Services

n = 812

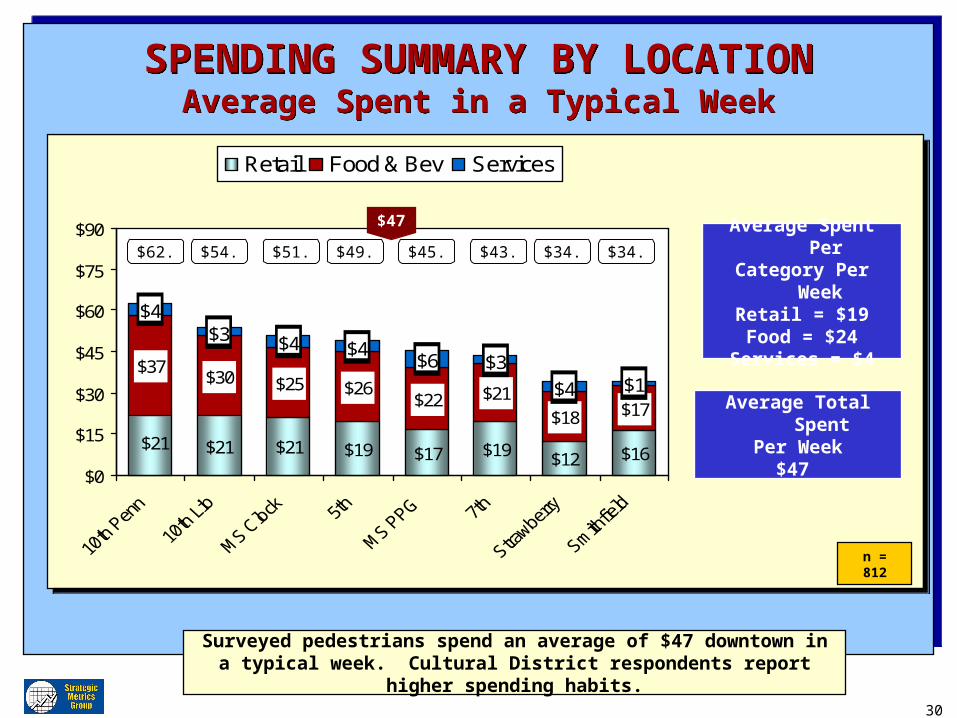

Surveyed pedestrians spend an average of $47 downtown in a typical week. Cultural District respondents report higher spending habits.

Average Spent PerCategory Per Week

Retail = $19Food = $24

Services = $4

SPENDING SUMMARY BY LOCATIONAverage Spent in a Typical Week

SPENDING SUMMARY BY LOCATIONAverage Spent in a Typical Week

$62. $54. $51. $49. $43.$45. $34. $34.

Average Total SpentPer Week

$47

$47

31

$39$20 $16 $14 $12

$60

$17

$25 $26$17 $22$42

$2$5$4$1

$3

$4

$0

$20

$40

$60

$80

$100

$120

$140

Retail Food & Bev Services

$39$20 $16 $14 $12

$60

$17

$25 $26$17 $22$42

$2$5$4$1

$3

$4

$0

$20

$40

$60

$80

$100

$120

$140

Retail Food & Bev Services

n = 808

Residents spend significantly more in downtown than the other groups.

Average Spent PerCategory Per Week

Retail = $19 Food = $24Services = $4

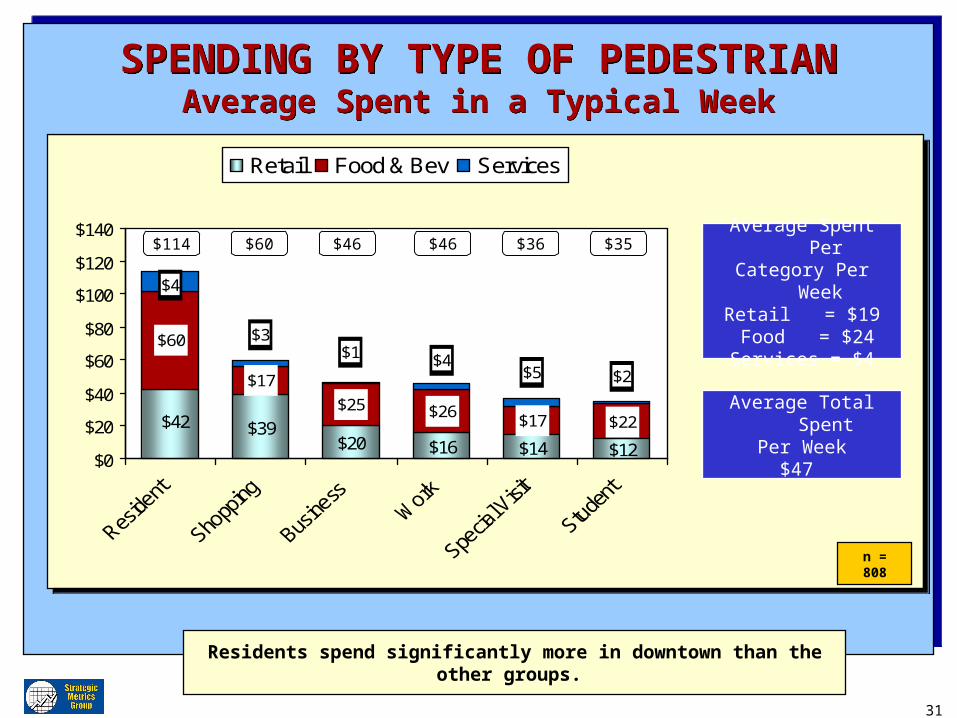

SPENDING BY TYPE OF PEDESTRIANAverage Spent in a Typical Week

SPENDING BY TYPE OF PEDESTRIANAverage Spent in a Typical Week

$114 $60 $46$46 $36 $35

Average Total SpentPer Week

$47

32

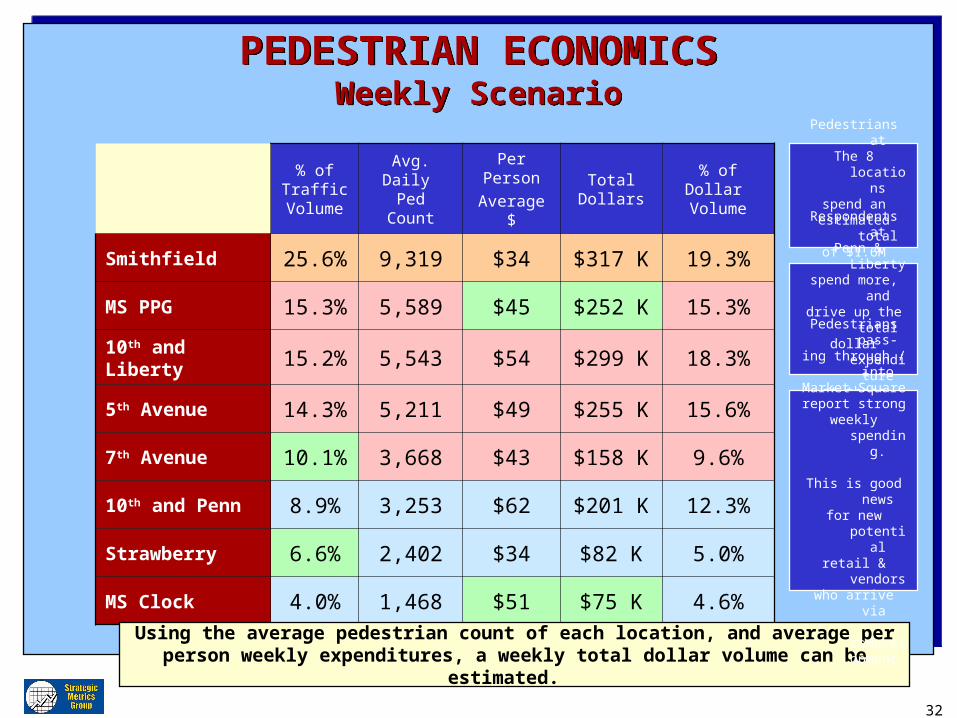

PEDESTRIAN ECONOMICSWeekly Scenario

PEDESTRIAN ECONOMICSWeekly Scenario

% of Traffic

Volume

Avg. Daily Ped Count

Per Person

Average $

Total Dollars

% of Dollar Volume

Smithfield 25.6% 9,319 $34 $317 K 19.3%

MS PPG 15.3% 5,589 $45 $252 K 15.3%

10th and Liberty 15.2% 5,543 $54 $299 K 18.3%

5th Avenue 14.3% 5,211 $49 $255 K 15.6%

7th Avenue 10.1% 3,668 $43 $158 K 9.6%

10th and Penn 8.9% 3,253 $62 $201 K 12.3%

Strawberry 6.6% 2,402 $34 $82 K 5.0%

MS Clock 4.0% 1,468 $51 $75 K 4.6%

Using the average pedestrian count of each location, and average per person weekly expenditures, a weekly total dollar volume can be estimated.

Pedestrians atThe 8 locations

spend anestimated total

of $1.6M weekly.

Respondents at Penn & Liberty

spend more, anddrive up the totaldollar expenditureat these locations.

Pedestrians pass-ing through / intoMarket Squarereport strong

weekly spending.

This is good newsfor new potentialretail & vendorswho arrive via

redevelopment.

33

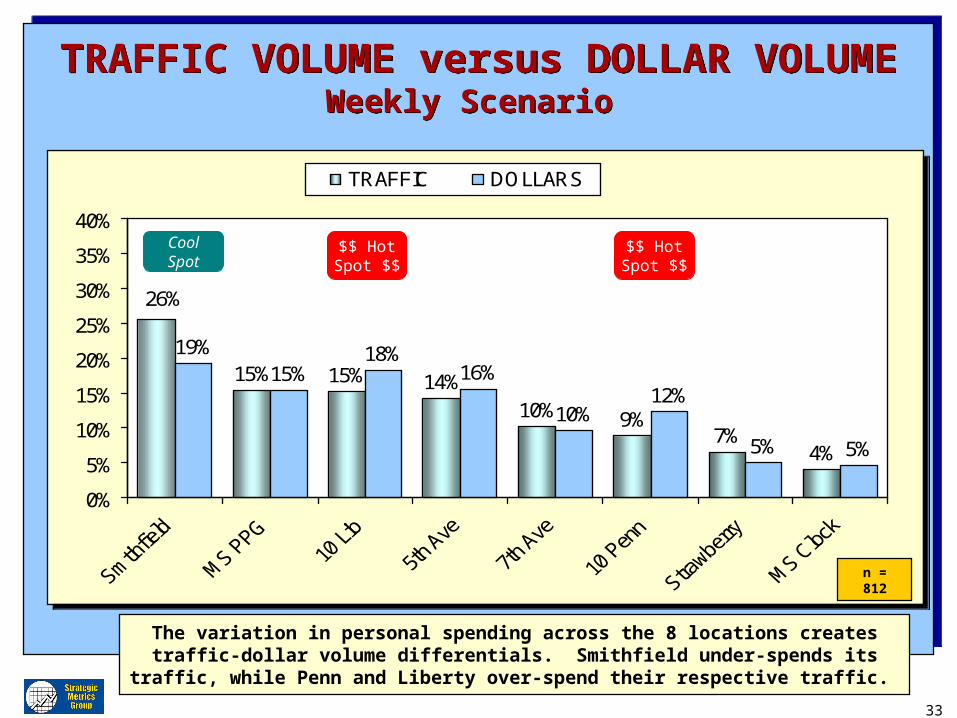

TRAFFIC VOLUME versus DOLLAR VOLUMEWeekly Scenario

TRAFFIC VOLUME versus DOLLAR VOLUMEWeekly Scenario

15% 15% 14%

10% 9%7%

4%

19%15%

18%16%

10%12%

5% 5%

26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

TRAFFIC DOLLARS

15% 15% 14%

10% 9%7%

4%

19%15%

18%16%

10%12%

5% 5%

26%

0%

5%

10%

15%

20%

25%

30%

35%

40%

TRAFFIC DOLLARS

n = 812

The variation in personal spending across the 8 locations creates traffic-dollar volume differentials. Smithfield under-spends its traffic, while Penn and Liberty over-spend

their respective traffic.

CoolSpot

$$ HotSpot $$

$$ HotSpot $$

34

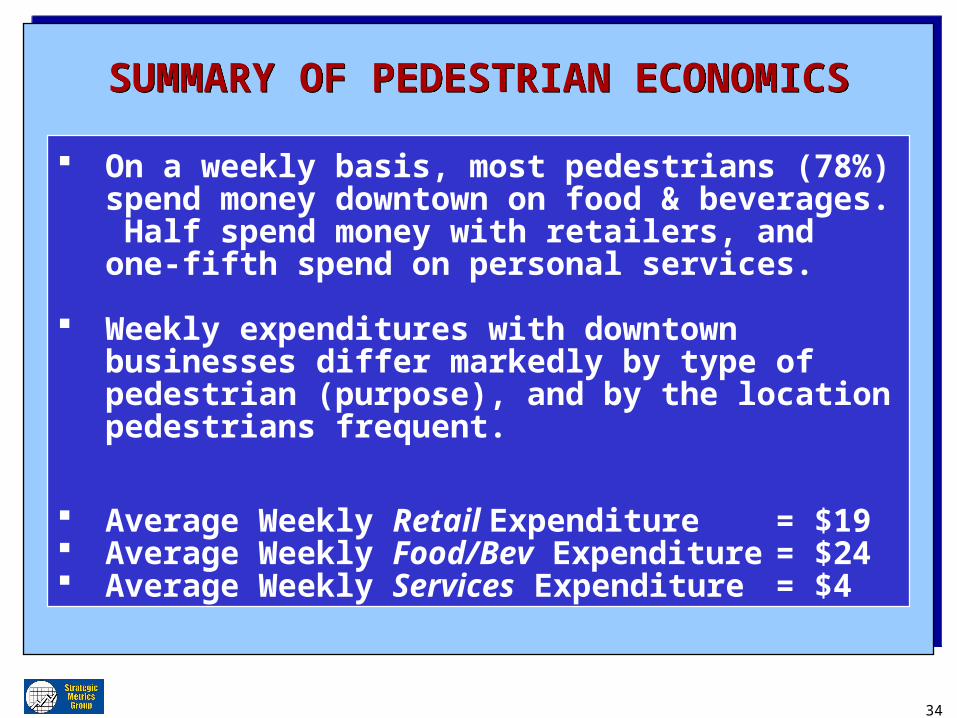

SUMMARY OF PEDESTRIAN ECONOMICSSUMMARY OF PEDESTRIAN ECONOMICS

On a weekly basis, most pedestrians (78%) spend money downtown on food & beverages. Half spend money with retailers, and one-fifth spend on personal services.

Weekly expenditures with downtown businesses differ markedly by type of pedestrian (purpose), and by the location pedestrians frequent.

Average Weekly Retail Expenditure = $19 Average Weekly Food/Bev Expenditure = $24 Average Weekly Services Expenditure = $4

35

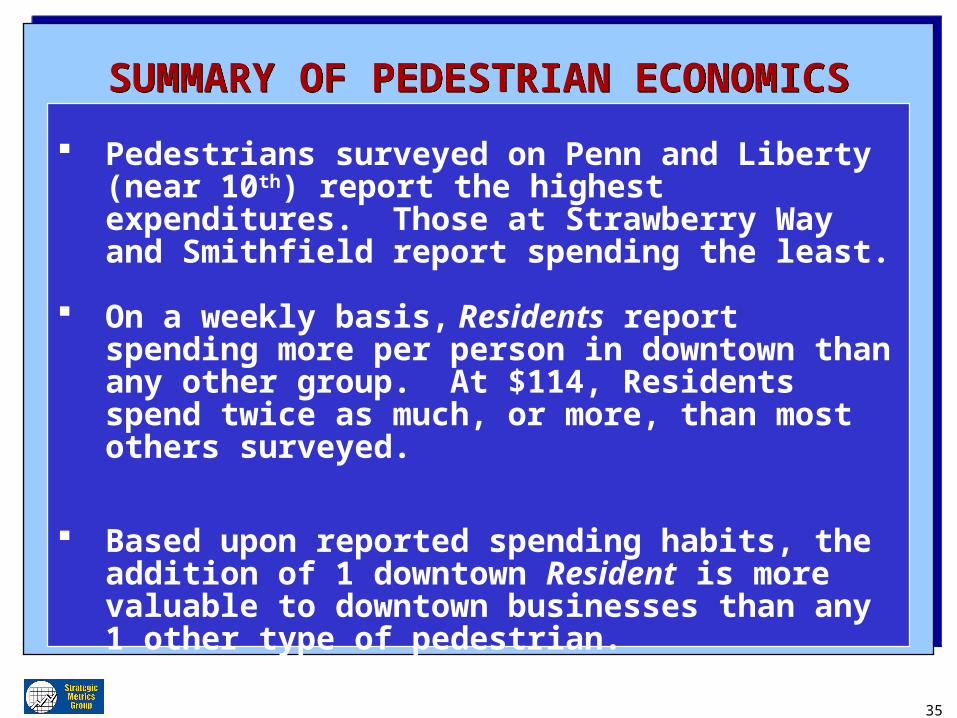

SUMMARY OF PEDESTRIAN ECONOMICSSUMMARY OF PEDESTRIAN ECONOMICS

Pedestrians surveyed on Penn and Liberty (near 10th) report the highest expenditures. Those at Strawberry Way and Smithfield report spending the least.

On a weekly basis, Residents report spending more per person in downtown than any other group. At $114, Residents spend twice as much, or more, than most others surveyed.

Based upon reported spending habits, the addition of 1 downtown Resident is more valuable to downtown businesses than any 1 other type of pedestrian.

36

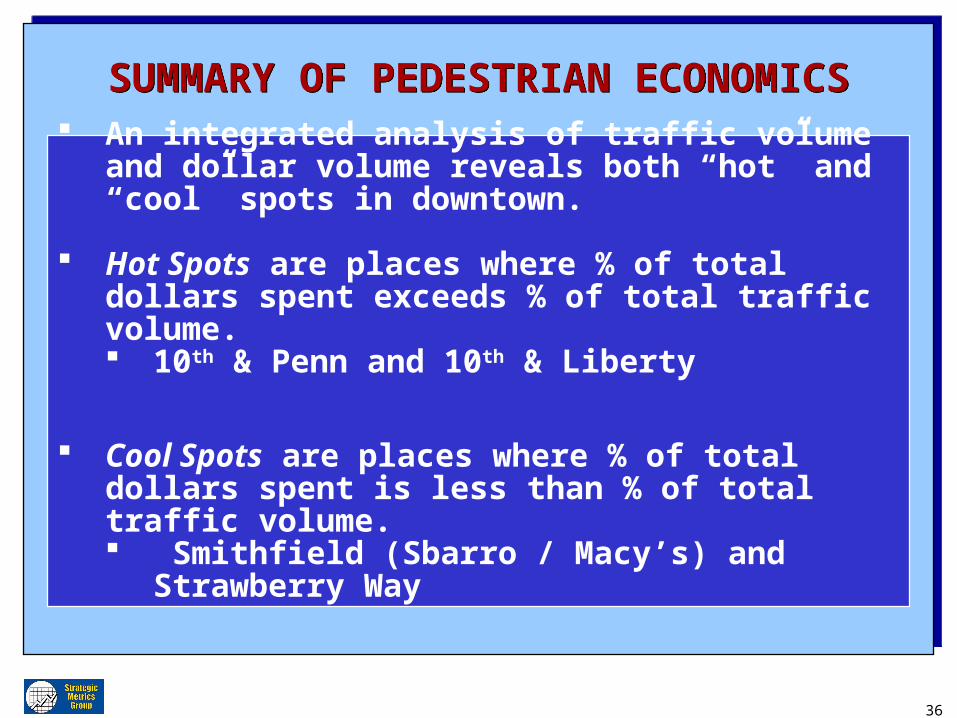

SUMMARY OF PEDESTRIAN ECONOMICSSUMMARY OF PEDESTRIAN ECONOMICS

An integrated analysis of traffic volume and dollar volume reveals both “hot” and “cool” spots in downtown.

Hot Spots are places where % of total dollars spent exceeds % of total traffic volume. 10th & Penn and 10th & Liberty

Cool Spots are places where % of total dollars spent is less than % of total traffic volume. Smithfield (Sbarro / Macy’s) and Strawberry Way

37

SUMMARY OF PDP IDENTITY & PERCEPTIONSSUMMARY OF PDP IDENTITY & PERCEPTIONS

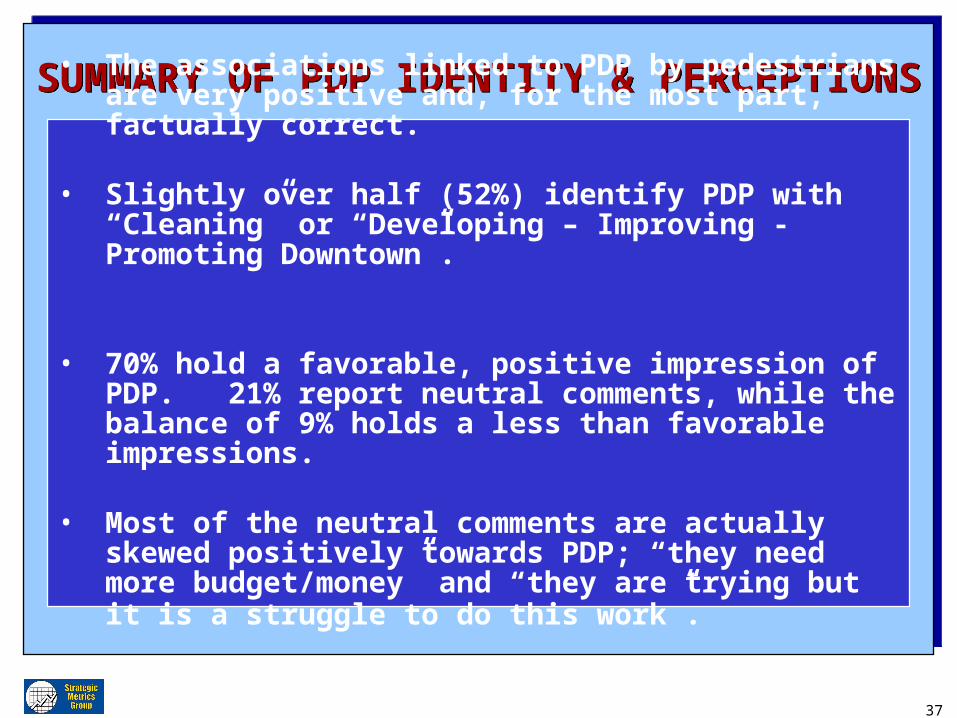

• The associations linked to PDP by pedestrians are very positive and, for the most part, factually correct.

• Slightly over half (52%) identify PDP with “Cleaning” or “Developing – Improving - Promoting Downtown”.

• 70% hold a favorable, positive impression of PDP. 21% report neutral comments, while the balance of 9% holds a less than favorable impressions.

• Most of the neutral comments are actually skewed positively towards PDP; “they need more budget/money” and “they are trying but it is a struggle to do this work”.

38

PERCEPTIONS

of

MARKET SQUARE

PERCEPTIONS

of

MARKET SQUARE

.

39

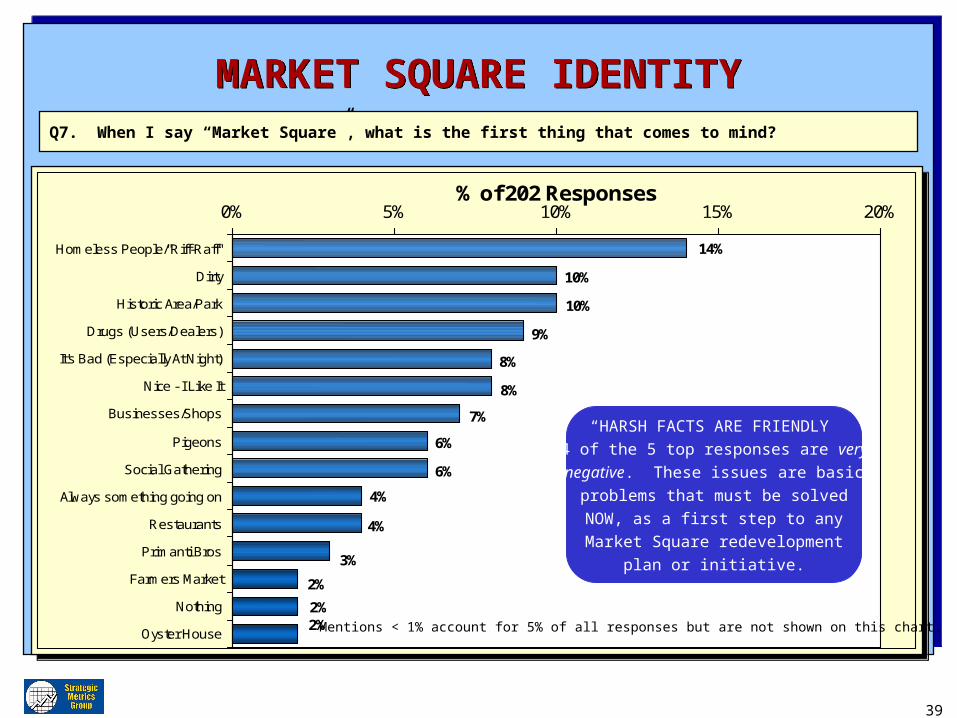

MARKET SQUARE IDENTITYMARKET SQUARE IDENTITYQ7. When I say “Market Square”, what is the first thing that comes to mind?

6%

6%

4%

4%

3%

2%

2% 2%

7%

8%

8%

9%

10%

14%

10%

0% 5% 10% 15% 20%

Homeless People/"Riff-Raff"

Dirty

Historic Area/Park

Drugs (Users/Dealers)

It's Bad (Especially At Night)

Nice - I Like It

Businesses/Shops

Pigeons

Social Gathering

Always something going on

Restaurants

Primanti Bros

Farmers Market

Nothing

Oyster House

% of 202 Responses

6%

6%

4%

4%

3%

2%

2% 2%

7%

8%

8%

9%

10%

14%

10%

0% 5% 10% 15% 20%

Homeless People/"Riff-Raff"

Dirty

Historic Area/Park

Drugs (Users/Dealers)

It's Bad (Especially At Night)

Nice - I Like It

Businesses/Shops

Pigeons

Social Gathering

Always something going on

Restaurants

Primanti Bros

Farmers Market

Nothing

Oyster House

% of 202 Responses

“HARSH FACTS ARE FRIENDLY”4 of the 5 top responses are very

negative. These issues are basic

problems that must be solved

NOW, as a first step to any

Market Square redevelopment

plan or initiative.

Mentions < 1% account for 5% of all responses but are not shown on this chart.

40

IMPROVING MARKET SQUAREIMPROVING MARKET SQUARE

4%

4%

4%

2%

2%

2%

1%

4%

4%

10%

10%

18%

19%

13%

0% 5% 10% 15% 20% 25%

More events

Keep Out Homeless/"Riff Raff"/Solicitors

Clean it up

More shops/restaurants

More Police

Get Rid of Drugs (Users/Dealers)

Get Rid of Pigeons

Grocery/Food Store/Market

Nothing

Make More Park Like

Eliminate/Lower Parking Fees

Repair Pavement

Get Rid of Road

Allow buskers/busking

% of 217 Responses

4%

4%

4%

2%

2%

2%

1%

4%

4%

10%

10%

18%

19%

13%

0% 5% 10% 15% 20% 25%

More events

Keep Out Homeless/"Riff Raff"/Solicitors

Clean it up

More shops/restaurants

More Police

Get Rid of Drugs (Users/Dealers)

Get Rid of Pigeons

Grocery/Food Store/Market

Nothing

Make More Park Like

Eliminate/Lower Parking Fees

Repair Pavement

Get Rid of Road

Allow buskers/busking

% of 217 Responses

Mentions < 1% account for 3% of all responses but are not shown on this chart.

Q8. What would help make Market Square a more interesting and appealing place for you to visit?

Core ImprovementsHalf of the suggested

improvements refer directly to

safety, cleanliness, and

the drug/criminal element.

Other ImprovementsMore events, shops,

restaurants, grocery / markets.

41

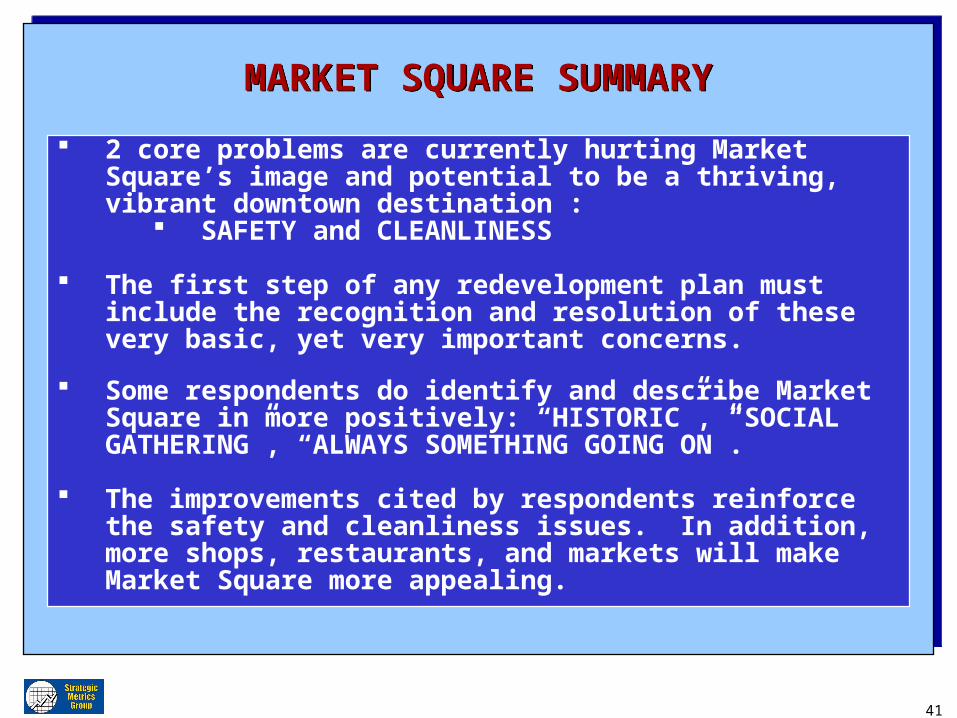

MARKET SQUARE SUMMARYMARKET SQUARE SUMMARY

2 core problems are currently hurting Market Square’s image and potential to be a thriving, vibrant downtown destination :

SAFETY and CLEANLINESS

The first step of any redevelopment plan must include the recognition and resolution of these very basic, yet very important concerns.

Some respondents do identify and describe Market Square in more positively: “HISTORIC”, “SOCIAL GATHERING”, “ALWAYS SOMETHING GOING ON”.

The improvements cited by respondents reinforce the safety and cleanliness issues. In addition, more shops, restaurants, and markets will make Market Square more appealing.

42

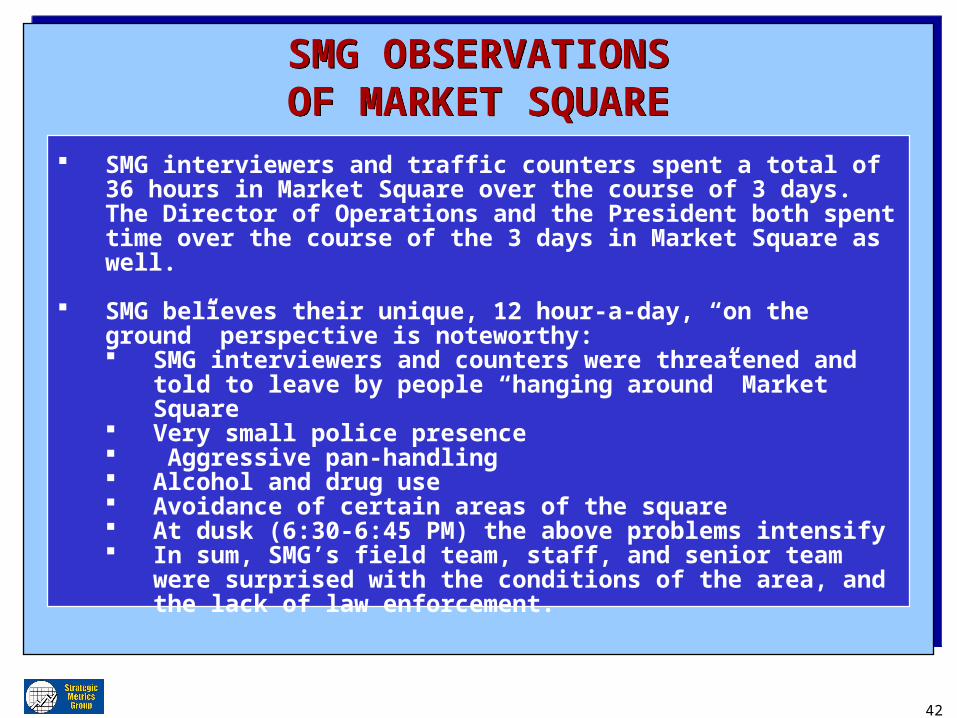

SMG OBSERVATIONSOF MARKET SQUARESMG OBSERVATIONSOF MARKET SQUARE

SMG interviewers and traffic counters spent a total of 36 hours in Market Square over the course of 3 days. The Director of Operations and the President both spent time over the course of the 3 days in Market Square as well.

SMG believes their unique, 12 hour-a-day, “on the ground” perspective is noteworthy: SMG interviewers and counters were threatened and told to leave

by people “hanging around” Market Square Very small police presence Aggressive pan-handling Alcohol and drug use Avoidance of certain areas of the square At dusk (6:30-6:45 PM) the above problems intensify In sum, SMG’s field team, staff, and senior team were surprised

with the conditions of the area, and the lack of law enforcement.

43

PRESENTATION OVERVIEW PRESENTATION OVERVIEW

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

44

DEMOGRAPHICS – ALL RESPONDENTS DEMOGRAPHICS – ALL RESPONDENTS

21%18%

22%15%

5%1%

18%

0%

20%

40%

60%

<24 25-34 35-44 45-54 55-64 65-74 75+

% o

f Res

pond

ents

21%18%

22%15%

5%1%

18%

0%

20%

40%

60%

<24 25-34 35-44 45-54 55-64 65-74 75+

% o

f Res

pond

ents

32%

19%

9% 10%

30%

0%

20%

40%

60%

<25K 25-49K 50-74K 75-99K 100K +

% o

f Res

pond

ents

32%

19%

9% 10%

30%

0%

20%

40%

60%

<25K 25-49K 50-74K 75-99K 100K +

% o

f Res

pond

ents

47%53%

0%

20%

40%

60%

80%

100%

Male Female

% o

f Res

pond

ents

47%53%

0%

20%

40%

60%

80%

100%

Male Female

% o

f Res

pond

ents

AGE GROUPAGE GROUP INCOMEINCOME

GENDERGENDER

19%

3%

78%

0%

20%

40%

60%

80%

100%

Solo 2 3+

% o

f Res

pond

ents

19%

3%

78%

0%

20%

40%

60%

80%

100%

Solo 2 3+

% o

f Res

pond

ents

PARTY SIZEPARTY SIZE

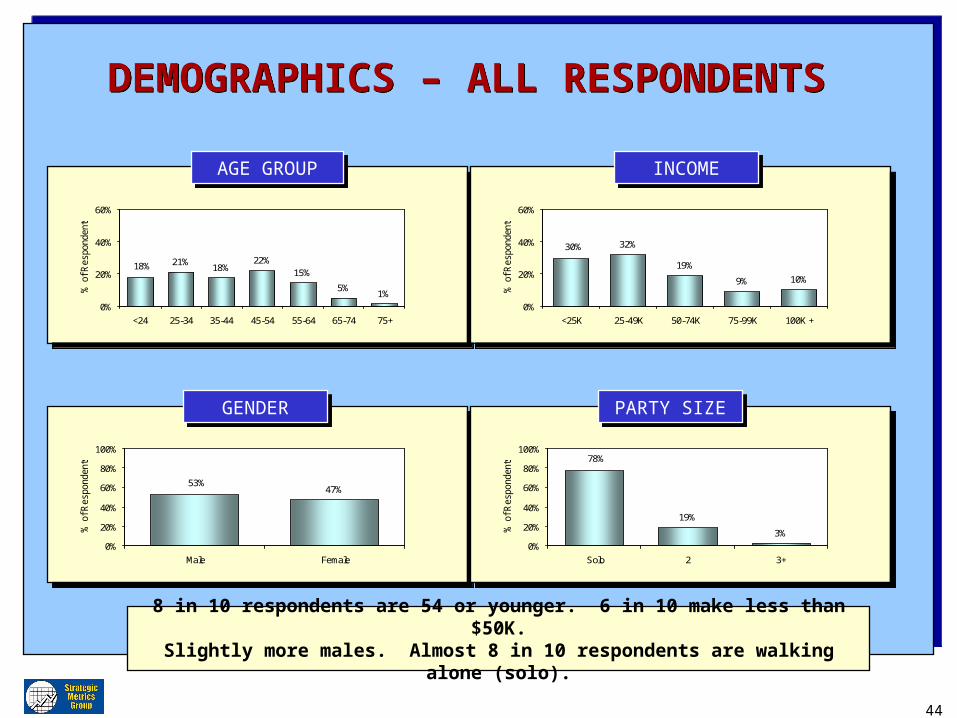

8 in 10 respondents are 54 or younger. 6 in 10 make less than $50K.Slightly more males. Almost 8 in 10 respondents are walking alone (solo).

45

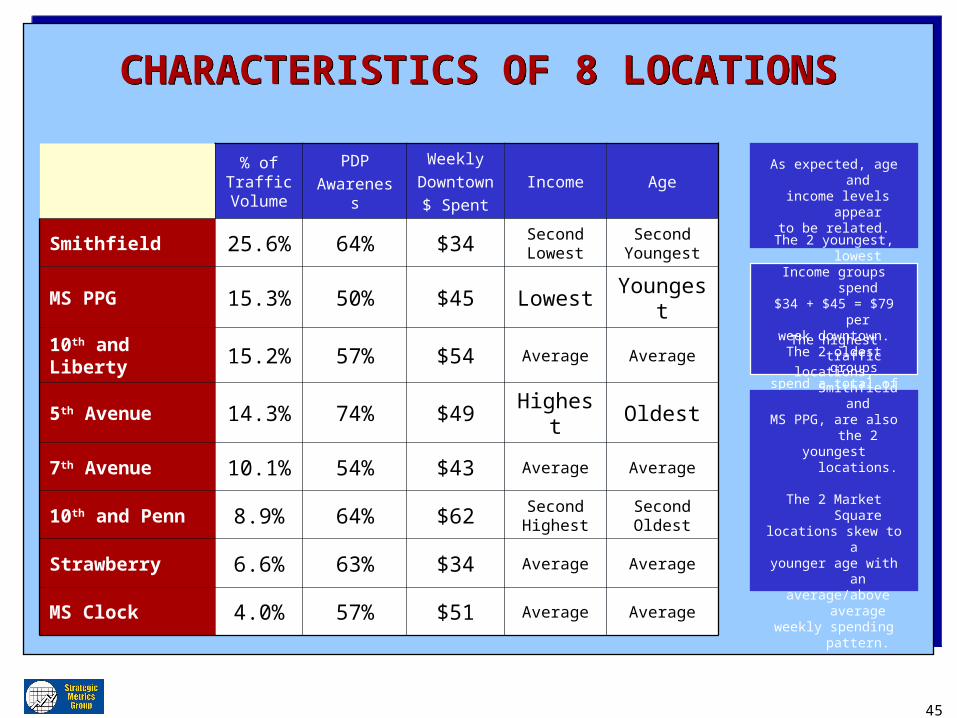

CHARACTERISTICS OF 8 LOCATIONSCHARACTERISTICS OF 8 LOCATIONS

% of Traffic

Volume

PDP

Awareness

Weekly

Downtown

$ Spent

Income Age

Smithfield 25.6% 64% $34 Second Lowest

Second Youngest

MS PPG 15.3% 50% $45 Lowest Youngest

10th and Liberty 15.2% 57% $54 Average Average

5th Avenue 14.3% 74% $49 Highest Oldest

7th Avenue 10.1% 54% $43 Average Average

10th and Penn 8.9% 64% $62 Second Highest

Second Oldest

Strawberry 6.6% 63% $34 Average Average

MS Clock 4.0% 57% $51 Average Average

As expected, age and income levels appear

to be related.

The 2 youngest, lowestIncome groups spend$34 + $45 = $79 per

week downtown.The 2 oldest groups

spend a total of $111.

The highest traffic locations, Smithfield andMS PPG, are also the 2

youngest locations.

The 2 Market Squarelocations skew to a younger age with an

average/above averageweekly spending pattern.

46

PRESENTATION OVERVIEW PRESENTATION OVERVIEW

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

1. Methodology and Sampling

2. Pedestrian Traffic Data

3. Pedestrian Survey Findings

4. Location & Pedestrian Profiles

5. Key Findings & Summary

47

SUMMARY OF KEY FINDINGSSUMMARY OF KEY FINDINGS

Traffic volume varies greatly across the 8 locations. The daily average traffic count is 4,557 pedestrians; with the highest count on Smithfield and the lowest at Market Square (Clock).

Saturday traffic (1,847) is significantly less than weekday (5,755).

Those working downtown comprise the majority (59%) of the pedestrian base.

Pedestrians spend an average of $47 a week downtown:- Retail $19 - Food $24 - Services $4

Downtown residents are a small, but important group. While small in number (just 3% of pedestrian base), residents spend substantially more downtown than all other pedestrian groups.

48

SUMMARY OF KEY FINDINGSSUMMARY OF KEY FINDINGS

Downtown spending habits differ by location, creating “hot” (10th & Penn) and “cool” spots (Smithfield) of pedestrian purchasing potential.

Market Square is viewed unfavorably by most pedestrians. Two major barriers, safety concerns & cleanliness, have to be recognized and resolved first, for Market Square to flourish and grow into a vibrant downtown destination.

60% of pedestrians are aware of PDP. Most identify PDP with either cleaning, improving, developing, or promoting downtown. Asked for their overall impression of PDP, pedestrian remarks are largely positive: 70% Positive 21% Neutral 9% Negative