© horváth & partner gmbh atlanta barcelona berlin bucharest budapest dubai düsseldorf...

TRANSCRIPT

© Horváth & Partner GmbH

Atlanta • Barcelona • Berlin • Bucharest • Budapest • Dubai • Düsseldorf • Frankfurt • Munich • Stuttgart • Vienna • Zurich

www.horvath-partners.com

Martin Hammerschmid

09.23.2009

Adjusting Retail BankingStrategy to New Conditions

Head of Central and Eastern Europe Business

Horváth & Partner GmbH Biberstraße 15A-1010 Vienna

Phone: +43 1 5127508-0

E-Mail: [email protected]

2

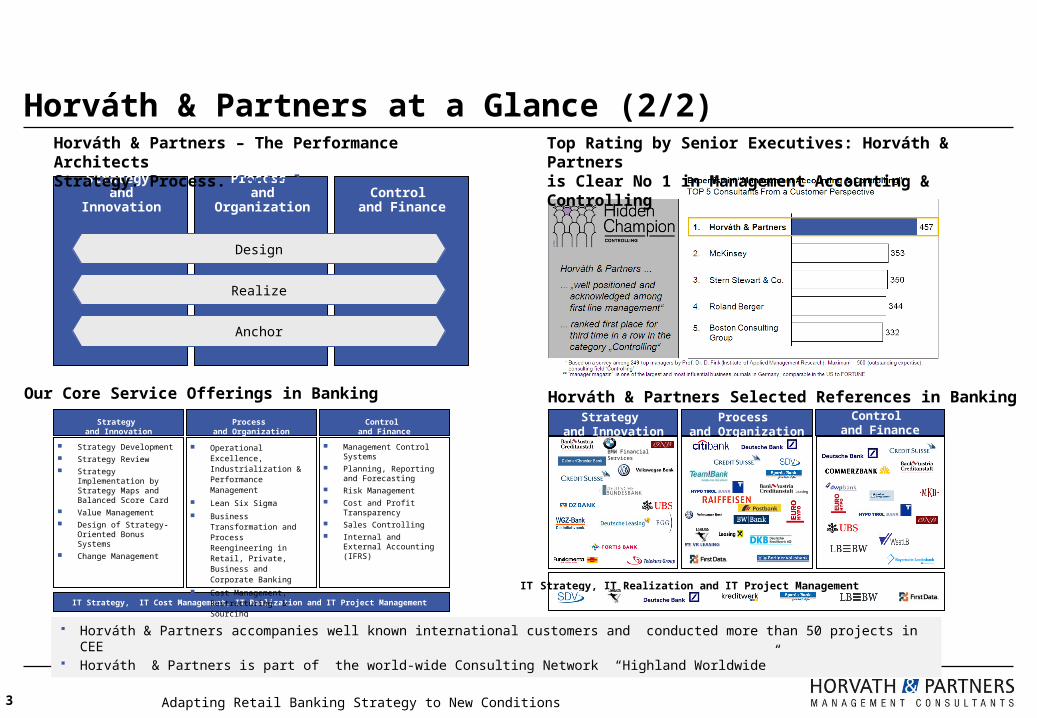

Horváth & Partners at a Glance (1/2)

Employees More than 450

Customers Global corporations, national corpora-tions and medium-sized companies from the industrial, service and retail sectors, as well as public organizations

Industry Global management consulting Offices Atlanta, Barcelona, Berlin, Bucharest, Budapest, Dubai, Düsseldorf, Frank-furt, Munich, Stuttgart, Vienna, Zurich

Additional partner offices in Asia, Europe, and North America through the "Highland Worldwide" consulting network

Adapting Retail Banking Strategy to New Conditions

Horváth & Partners at a Glance (2/2)

Adapting Retail Banking Strategy to New Conditions3

Design

Realize

Anchor

Process and Organization

Control and Finance

Strategy and Innovation

IT Strategy, IT Cost Management, IT Realization and IT Project Management

Strategy Development Strategy Review Strategy Implementation

by Strategy Maps and Balanced Score Card

Value Management Design of Strategy-

Oriented Bonus Systems Change Management

Management Control Systems

Planning, Reporting and Forecasting

Risk Management Cost and Profit

Transparency Sales Controlling Internal and External

Accounting (IFRS)

Operational Excellence, Industrialization & Performance Management

Lean Six Sigma

Business Transformation and Process Reengineering in Retail, Private, Business and Corporate Banking

Cost Management, Restructuring & Sourcing

Sales Performance Management

Strategy and Innovation

Process and Organization

Control and Finance

IT Strategy, IT Realization and IT Project Management

BMW Financial Services

Control and Finance

Strategy and Innovation

Process and Organization

Horváth & Partners – The Performance ArchitectsStrategy. Process. Control.

Top Rating by Senior Executives: Horváth & Partners is Clear No 1 in Management Accounting & Controlling

Our Core Service Offerings in Banking

Horváth & Partners accompanies well known international customers and conducted more than 50 projects in CEE Horváth & Partners is part of the world-wide Consulting Network “Highland Worldwide”

Horváth & Partners Selected References in Banking

Slowed growth and lack of business confidence in market

Exchange and interest rate volatility High unemployment Depleted credit availability Low savings rates Margin pressures

CEE markets exhibit volatile economic conditions that jeopardize the profitability of residing financial institutions

Sources: a) Unemployment from Raiffeisen Research, b) DE unemployment from Bundesministerium für Wirtschaft und Technologie, c) Savings from Global Market Information Database, d) Currency from Yahoo! Finance e) all currency against Euro

Adapting Retail Banking Strategy to New Conditions4

Challenges

Opportunities

Many under-banked customers

Backlog demand for financial products

Need for secure products

Strong request for risk-protection

Emerging M&A Opportunities

90,5

Eurozone

Savings Rate vs. Currency Value Lost against EUR (in %)

† The 2 Year Period covers from September 3, 2007 – September 3, 2009

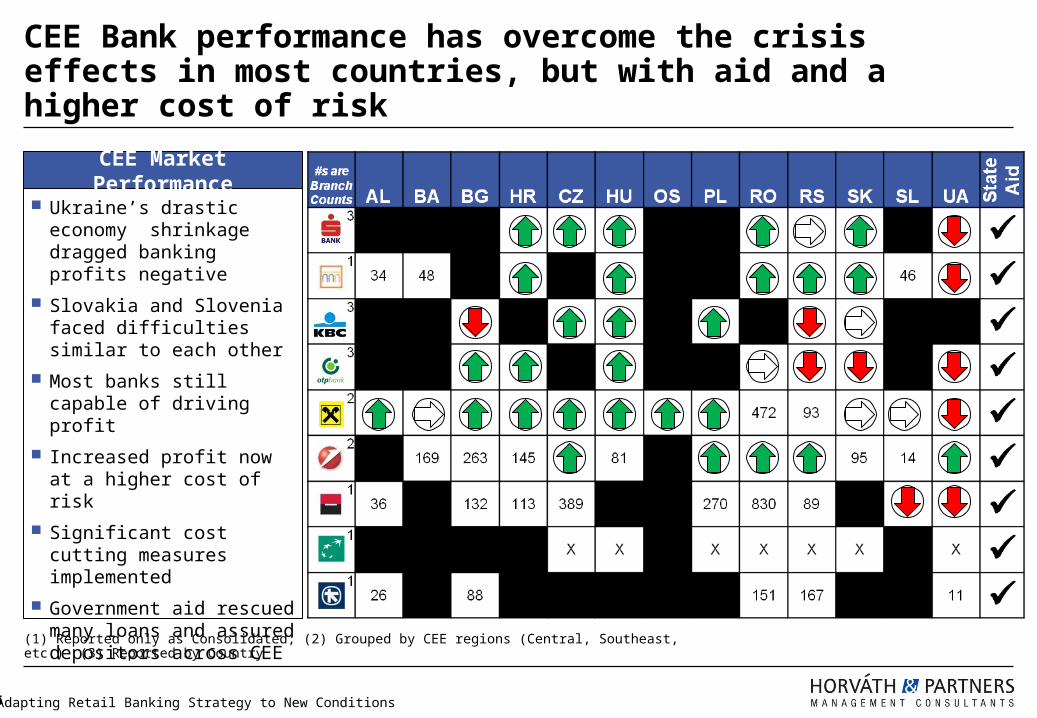

CEE Bank performance has overcome the crisis effects in most countries, but with aid and a higher cost of risk

(1) Reported only as Consolidated; (2) Grouped by CEE regions (Central, Southeast, etc.) (3) Reported by Country

Adapting Retail Banking Strategy to New Conditions5

Ukraine’s drastic economy shrinkage dragged banking profits negative

Slovakia and Slovenia faced difficulties similar to each other

Most banks still capable of driving profit

Increased profit now at a higher cost of risk

Significant cost cutting measures implemented

Government aid rescued many loans and assured depositors across CEE

CEE Market Performance

Strategic Confusion

What growth can we expect and when will it even come?

How will customer behavior and customers’ bankability change?

Are we striving for the right goals, or have we poorly speculated in the East?

How can we prepare for the recovery in times of crisis?

Retail Banking in CEE countries faces challenges mandating a renewed strategic model for competing in the new market

Adapting Retail Banking Strategy to New Conditions6

Opportunities and hot issues

Strategy Review

Restructuring the business model

M&A Management

Strategically-oriented incentive and compensation systems

Controlling efficiency & management

New rules in a post-Lehman world

(Straits Times, 09/07/2009)

Recoveries in Eastern Europe slow

(Reuters 09/04/2009)

Adjustment after a period of vibrant growth will be painful

(Economist 10/10/2008)

Fitch drops ratings for banks due to Eastern Europe

(04/16/09 Reuters)

Expect sustained change in customer behavior

(PresseEcho.de 26/08/2009)

A strategic readjustment in retail banking strategy will aid CEE banks in emerge from the crisis prepared for the new market

Adapting Retail Banking Strategy to New Conditions7

From: Reliance on simple asset

products Build initial belief in banking

systemTo: Increase Customer Touch Points Trust again in Sector and Brand

From: In-house productions & capacity Internal capabilities determine

productsTo: Vendor Management Source complex products and

services

From: Top line growth focus Easy financing in foreign currencyTo: Adjusted Cost and Risk Base Increased Hedging Product Use Allocated Resources Across BUs

From: Lending and interest-driven focus Web presence and distanced

bankingTo: Customer Segments & Channel

Focus Cross-Selling Products &

Services

From: Processes grew alongside

demand External Growth from acquisitionTo: Industrialize the value chain Find synergies across all group

levels

From: Labor grew directly with sales

growth Compensation followed lending

volumeTo: Performance-based Incentive

System Staff Management & Expert

TrainingFrom: Growth projections and volume

drivers Mass market entry and general

focusTo: Scenario-based Decision Making Niche and innovation

management

Human Capital Customer Interface

Value ChainConcepts for the Future

Strategic Core

Customer Perception

Cooperation

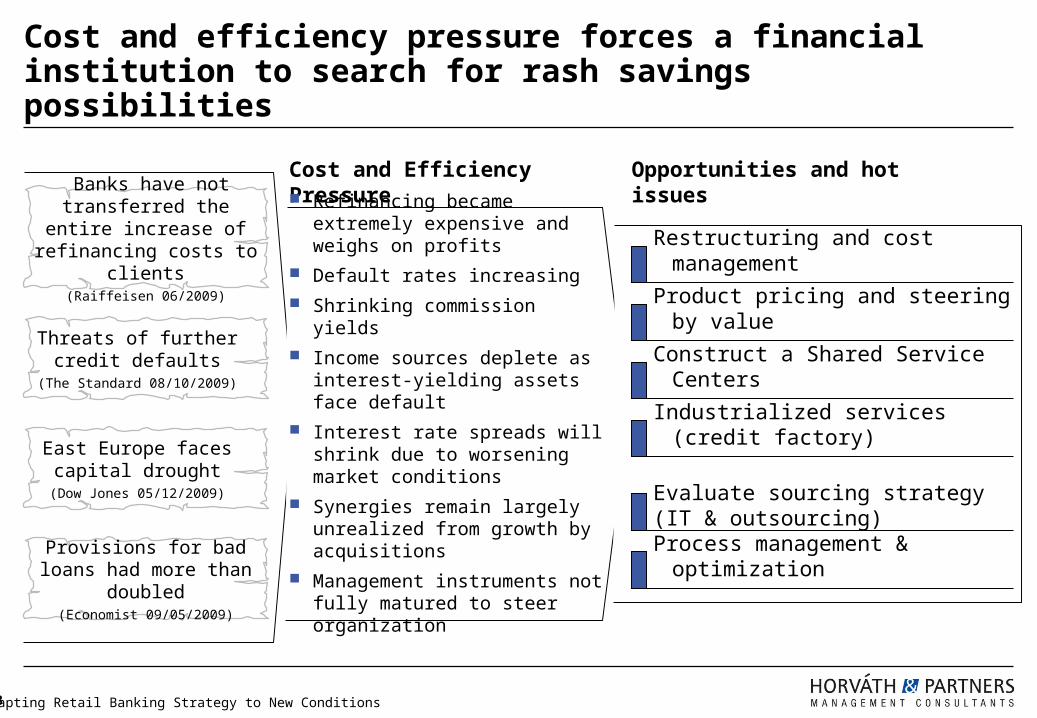

Cost and Efficiency Pressure

Refinancing became extremely expensive and weighs on profits

Default rates increasing

Shrinking commission yields

Income sources deplete as interest-yielding assets face default

Interest rate spreads will shrink due to worsening market conditions

Synergies remain largely unrealized from growth by acquisitions

Management instruments not fully matured to steer organization

Cost and efficiency pressure forces a financial institution to search for rash savings possibilities

Adapting Retail Banking Strategy to New Conditions8

Opportunities and hot issues

Restructuring and cost management

Process management & optimization

Evaluate sourcing strategy (IT & outsourcing)

Construct a Shared Service Centers

Industrialized services (credit factory)

Product pricing and steering by value

East Europe faces capital drought

(Dow Jones 05/12/2009)

Provisions for bad loans had more than doubled

(Economist 09/05/2009)

Threats of further credit defaults

(The Standard 08/10/2009)

Banks have not transferred the entire increase of

refinancing costs to clients(Raiffeisen 06/2009)

Financial Institutions must evolve from short-term cost cutting to Operational Excellence and Sustainable Cost Management

Adapting Retail Banking Strategy to New Conditions9

Reorganizing and Industrializing Processes

ClusteringAllocation

Management

Distribution chain

Products

“Assembly line”

Process Modules

Optimizing Processes Recognizing Benefits from Changes

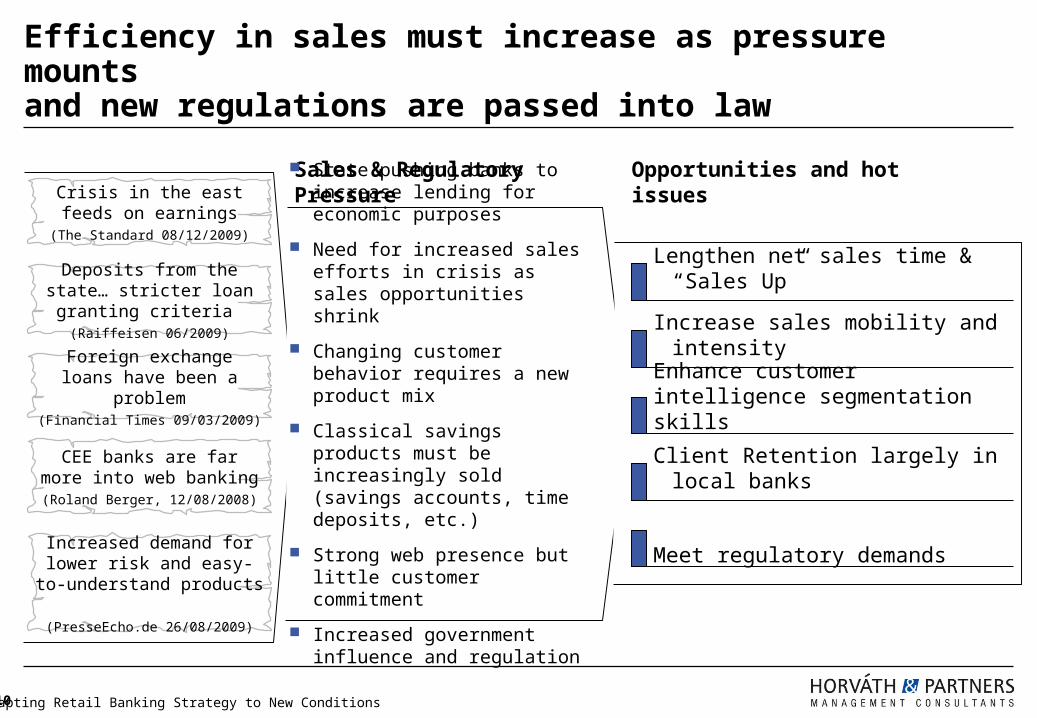

Sales & Regulatory Pressure

State pushing banks to increase lending for economic purposes

Need for increased sales efforts in crisis as sales opportunities shrink

Changing customer behavior requires a new product mix

Classical savings products must be increasingly sold (savings accounts, time deposits, etc.)

Strong web presence but little customer commitment

Increased government influence and regulation

Efficiency in sales must increase as pressure mounts and new regulations are passed into law

Adapting Retail Banking Strategy to New Conditions10

Opportunities and hot issues

Lengthen net sales time & “Sales Up”

Increase sales mobility and intensity

Enhance customer intelligence segmentation skills

Client Retention largely in local banks

Meet regulatory demands

Crisis in the east feeds on earnings

(The Standard 08/12/2009)

Foreign exchange loans have been a problem

(Financial Times 09/03/2009)

Deposits from the state… stricter loan granting criteria

(Raiffeisen 06/2009)

CEE banks are far more into web banking

(Roland Berger, 12/08/2008)

Increased demand for lower risk and easy-to-understand

products (PresseEcho.de 26/08/2009)

Professional Customer Management and innovative ways to manage your sales force can make the necessary difference

Adapting Retail Banking Strategy to New Conditions11

Your sales force must be appropriately energized and managed

Profit-oriented segmentation must become the basis for Customer Management

Relative improvement in the past year(Year 1 vs. Year 0)

Best Practice Sharing

Potential-Oriented Top-Down Goal

Bottom Line Leaders“ = 100%

Own Position in Year 1

Your Contact at Horváth & PartnersWe look forward to hearing from you

12 Adapting Retail Banking Strategy to New Conditions

Martin HammerschmidPrincipalCompetence Center Financial ServicesHead of Financial Services Austria and CEE

Horváth & Partner GmbH Biberstraße 15A-1010 ViennaPhone +43 1 5127508-0Mobile +43 664 3107250

E-Mail [email protected]

13 Adapting Retail Banking Strategy to New Conditions