your guide to business + legal success in latin america

TRANSCRIPT

z

Regional Impact Global Leadership

Council of Great Lakes Governors Co-Chairs:

Illinois Governor Pat Quinn and

Michigan Governor Rick Snyder

Zoë Munro, Program Manager

Conference of Great Lakes and

St. Lawrence Governors and Premiers

SOUTH AMERICA TRADE MISSION

Conference of Great Lakes and

St. Lawrence Governors and Premiers

Conference formed in June, 2015

Chief executives of Illinois, Indiana,

Michigan, Minnesota, New York,

Ohio, Ontario, Pennsylvania, Québec

and Wisconsin are working as equal

partners to grow the region’s $5 trillion

economy and protect the world’s

greatest freshwater system.

The Council of Great Lakes Governors

serves as secretariat.

Council of Great Lakes Governors Co-Chairs:

Illinois Governor Pat Quinn and

Michigan Governor Rick Snyder

Economic Development

International Trade and

Investment

Maritime

Tourism

Environmental Protection

Priorities

Water Management

Aquatic Invasive Species

Conference of Great Lakes and

St. Lawrence Governors and Premiers

Regional Leadership Global Impact

Region’s economy is 3rd largest

“country” GDP in the world

One of the country’s

emerging mega regions

Centralized location with

outstanding market access

Extensive air, rail, road and

maritime transportation systemwww.bmo.com

Regional Leadership Global Impact

Santiago, Chile

Toronto, Canada

São Paulo, Brazil

Johannesburg, South Africa

Shanghai, China

Sydney, Australia

United Kingdom

Germany

Trade Office

Tourism Office

New Delhi, IndiaMexico City, Mexico

CHICAGO, ILLINOIS

Headquarters

Trade Office

LONDON, UNITED KINGDOM

BERLIN, GERMANY

Export Missions

Québec – 2015

Mexico – 2015

Czech Republic, Poland and Turkey – 2014

India – 2014

Colombia, Chile and Brazil – 2012 & 2013

Australia – 2006, 2009 & 2013

South Africa – 2007, 2011 & 2013

Dubai, Abu Dhabi and Qatar – 2012

Indonesia, Vietnam and Thailand – 2012

Brazil, Chile, Peru - 2010

Australia & New Zealand – 2009

Argentina, Brazil & Chile – 2004 & 2008

CGLSLGP Trade Missions have assisted over 300 Great Lakes

companies to export their products and services to 20 international

markets

South America Trade Mission 2015

• Multi-sector trade mission to Brazil, Chile and

Colombia October 17-27, 2015

• São Paulo, Santiago and Bogotá

• Customized one-on-one business appointments

with interested distributors, agents and other

prospective business partners set up by the

CGLSLGP Trade Office (average 2 – 4

appointments per day)

• Brief market overview including industry sector

information and target company profiles

South America Trade Mission 2015

• In-country market business briefings

• In-country staff support of CGLSLGP Brazil and Chile

Trade Offices. Chile Trade Office covering Colombia.

• Group airport-hotel-airport ground transportation in all

three cities

• Assistance with hotel bookings, drivers and interpreters

South America Trade Mission 2015

Itinerary

Saturday, October 17

Sunday, October 18

Depart U.S. for São Paulo, Brazil

AM: Arrive São Paulo

PM: Country Business Briefing and Networking

Dinner

Monday, October 19 Individual Business Appointments in São Paulo

Tuesday, October 20 Individual Business Appointments in São Paulo

Wednesday, October 21 AM: Fly to Santiago, Chile

PM: Country Business Briefing and Networking

Dinner

Thursday, October 22 Individual Business Appointments in Santiago

Friday, October 23 Individual Business Appointments in Santiago

Saturday, October 24 Free day in Santiago

Itinerary Continued

Sunday, October 25 AM: Depart for Bogotá, Colombia

Monday, October 26 Individual Business Appointments in Bogotá

Tuesday, October 27 Individual Business Appointments in Bogotá

Late PM: Fly back to US (pending flight schedules)

Wednesday, October 28 AM: Fly back to US

South America Trade Mission 2015

Mission Logistics

• Drivers/Interpreters

• Hotel Block Bookings

• Group Inter-Country Flights

• Group Ground Transport

• Visa Invitation Letters

• Travel/Medical Insurance

CGLG Trade Mission Website

Website: http://www.cglg.org/projects/international-trade/trade-

missions/south-america-mission-2015/

South America Trade Mission 2015

Mission registration deadline: August 19, 2015

Mission Participation Fee US$ 995

per person

Brief Market Research and Appointment Setting

Brazil US $ 3,852

Chile US $ 2,500

Colombia US$ 2,600

Grant funding available in many states

Main goal: To assist SMEs from the Great Lakes

region or Canada looking to export products and

services to Brazil, Chile and Colombia

*varies by state

Website: http://www.cglg.org/projects/international-trade/trade-

missions/south-america-mission-2015/mission-costs/

October 17-27, 2015

Other Mission CostsCosts Paid Directly by Participants

(All costs below are estimated and will depend on exchange rate at the time of the

mission)

International Airline Ticket $1,800 USD Approx.

US-Sao Paulo, Santiago & Bogotá

Each participant will make their own flight arrangements to travel both to/from

and within the South America. Recommended group flight times will be provided.

Hotels

Sao Paulo, Santiago, & Bogotá (10 nights) $2,3000 USD Approx.

The Council will reserve a block of discounted rooms at hotels in Sao Paulo,

Santiago and Bogotá.

Material translation – website, business cards, materials (Portuguese and

Spanish)

Other Mission CostsAll fees are approximate

Transportation to Meetings

Brazil: $600 USD per day

Combines driver and interpreter fee

Santiago: $20 USD per hour

Bogotá: $320 USD for 9 hours

Interpreters

Brazil see above

Santiago: $260 USD for 9 hours

Bogotá : $380 USD for 8 hours

Material translation – website, business cards, materials to Portuguese and

Spanish

Brazil Business Visa Fee $160 USD

CGLSLGP FY15-16 TRADE MISSIONS

Brazil, Chile and Colombia: October 17-27, 2015

São Paulo, Santiago and Bogotá

Germany and the United Kingdom: March 1-9, 2016

Frankfurt (base) and London (base)

China: May 7-14, 2016

Shanghai, Guangzhou and Beijing

Kazakhstan and Azerbaijan: June, 2016

Website: http://www.cglg.org/projects/international-trade/trade-

missions/

Trade Mission Feedback“The South America trip that was organized by the Council of

Great Lakes Governors was simply outstanding. All three

countries we visited were very productive from a business

standpoint. The potential customers that CGLG prequalified

and set up for us to meet were exactly the type of customers

we want to do business with. As we visited these potential

customers, the interpreters were very professional and smart.

In the short time we were with them, they picked up our

industry lingo and knew our product very well.

The entire experience was nothing short of great! We look

forward to going on another trade mission trip in the future!”

Jeremy Sizer and Jodi Boldenow

Industrial Door Co. Inc, Minnesota

"As an international business developer, I have worked with

other US agencies for similar trade services. I do have to admit

that this is by far the best experience I’ve had. I was very

impressed by the thoroughness and enthusiasm in not leaving

any stone unturned in peruse of any potential opportunities for

my company. In all honesty, I was concerned about meetings

schedule crossing the country. However, the planned logistics

were impeccable making my time in Australia both effective and

efficient.

I would with all confidence recommend both the Council of

Great Lakes Governors and the CGLG Trade Office in

Australia.”

Nalex Cordova

Blair Rubber, Ohio

Trade Mission Feedback

Questions?

Zoë Munro

Program Manager

20 N. Wacker Dr., Suite 2700

Chicago, Illinois 60606

Email: [email protected]

Phone: +1 312 407-0177

Website: www.cglslgp.org

“Your Guide to Business + Legal Success in

Latin America”June 28th, 2015

Let the U.S. Commercial Service

connect you to a world of opportunity.

Presented by

Amy Freedman

US Commercial Service, Cleveland

US Commercial ServiceThe U.S. Commercial Service is the export arm of the U.S. Department of

Commerce’s International Trade Administration. With offices throughout

the United States and in U.S. Embassies and consulates in nearly 80

countries, the U.S. Commercial Service utilizes its global network of trade

professionals to connect U.S. companies with international buyers

worldwide.

Export.gov/LookSouth Amy Freedman

What is Look South?

• LOOK SOUTH is a coordinated Federal Government effort led

by the U.S. Department of Commerce to help more American

companies “Look South” to do business with FTA countries

• Export promotion

• Trade Winds

• Trade Missions

• IBP

• Financing

• SBA

• OPIC

• Training and Education

• US Trade & Development Agency

• Procurement Initiative

• Strategic Partnerships

• Chambers

• Private companies

Mexico is our second-largest

trading partner (Canada is the

largest), with record U.S.

merchandise exports of $216.3

billion in 2012. This “LOOK

SOUTH” campaign encourages

more than 54,000 U.S.

companies already exporting

to Mexico to expand exports to

other Latin American markets.

Look South Target Markets

7/28/2015 International Trade Administration 26

U.S. FTA partner markets in

Latin America:

• Mexico

• CAFTA-DR

• Panama

• Colombia

• Peru

• Chile

FUN FACT: Latin American

countries are developing their own

SBDC-like networks, with the

support of the U.S. State

Department. These SBDC-like

networks will become part of the

Small Business Network of the

Americas (SBNA).

7/28/2015 27International Trade Administration

Look South target markets show great opportunity

Stable, growing economies

• Target market GDP growth averages 4.7%

Untapped markets

• Growing middle class seeks new products

Favorable trade policies

• Free trade agreements, regional integration, reduced trade barriers

7/28/2015 28International Trade Administration

U.S. products ideal for meeting latent demand

Automotive Parts and Supplies

• A growing middle class has led to more car ownership, including U.S. brands, raising the demand for U.S. auto parts.

Construction Equipment

• Growth in infrastructure projects, housing, and mining development all demand construction equipment.

Medical/Healthcare Equipment

• Growing incomes and increased social safety nets in these markets lead to growing sales.

Markets have favorable policies for doing business

7/28/2015 International Trade Administration 29

Free Trade Agreements

• Provide U.S. goods with favorable tariff treatment, government procurement opportunities, legal and intellectual property rights protections, among others.

Regional integration

• Integration of regional trade blocks such as Central America and the newly formed Pacific Alliance, builds common markets, regulatory regimes, and product standards, and allows for accumulation of origin.

Active U.S. engagement

• USG agencies are actively engaged in the removal of policy barriers in target markets through programs such as the Customs and Border Management Program and the Standards Alliance.

Look South Resources

• Commercial Service in each target market.

• Full trade event and webinar schedule.

• Export.gov/LookSouth.

• Coordinated support from other government agencies, partner networks.

7/28/2015 International Trade Administration 30

• Export.gov/LookSouth.• Newsletter registration.

• Market and sector reports.

• Promo and Fact Sheets.

• Spotlights: missions, shows, conferences, webinars.

• Social Media: regular blogs and tweets.

• Financing.

• Policy support.

• Direct Line calls.7/28/2015 31International Trade Administration

Look South Toolkits

• August 2015

• Brazil Health IT Trade Mission

Mon, 8/17/2015 – Thu, 8/20/2015

Sao Paulo, Brazil

• September 2015

• Inter-American Dialogue: Latin America Clean Transport

Forum

Wed, 9/02/2015

Mexico City, Mexico

*This event will be held in Spanish

• Franchise Trade Mission to Central America

Sun, 9/20/2015 – Sat, 9/26/2015

San Jose, Costa Rica

• 32nd Perumin Mining Convention

Mon, 9/21/2015 – Fri, 9/25/2015

Lima, Peru

• International Buyer Program (IBP): Pack Expo

Mon, 9/28/2015 – Wed, 9/30/2015

Las Vegas, NV

• October 2015

• CONEXPO Latin America

Wed, 10/21/2015 – Sat, 10/24/2015

Santiago, Chile

• Discover Global Markets: Pacific Rim Consumers

Thu, 10/29/2015 – Fri, 10/30/2015

Orange County, CA

• November 2015

• American Water Works Association Trade Mission to South

America

Sun, 11/15/2015 – Sat, 11/21/2015

Santiago, Chile and Bogotá, Colombia

• SelectUSA Canada 2015

Tue, 11/17/2015

Toronto, Canada

• International Buyer Program (IBP): Greater New York Dental

Meeting

Fri, 11/27/2015 – Wed, 12/2/2015

New York, NY

• December 2015

• Enterprise Florida Export Sales Mission to Honduras

Tue, 12/1/2015 – Thu, 12/3/2015

Tegucigalpa, Honduras

• SelectUSA Brazil Road Show

Tue, 12/1/2015 – Fri, 12/4/2015

Rio de Janeiro, São Paulo, Belo Horizonte, Brazil

• Houston: Gateway to the Americas

Mon, 12/2/2015 – Wed, 12/4/2015

Houston, TX

Upcoming Trade Events

z

in Latin America

Sr. Director & GM, Latin America Consumer Business Group 20+ years experience in the international business sector, specifically LATAM

Global Lawn & Garden Industry

Latin America L&G industry

Why venture into LATAM? Mexico?

Challenges Regulatory

Business Practices

Logistics

Opportunities Business Expansion

M&A

‘Testing the Waters’

z

My Background

Before joining Kegler Brown in 2011, lived in São Paulo Brazil and worked in a Brazilian law firm

2012 Council of Great Lakes Governors Trade Mission to Brazil, Chile and Colombia participant

2014 Greater Columbus Sister Cities International, Inc. Curitiba, Brazil delegation member

MBA course instructor at The Ohio State University

z

Designed, developed and lead multinational global business MBA course at The Ohio State University,

Fisher College of Business

MBA Course Instructor

z

z

Course Accomplishments

z

Course Accomplishments

Managed three MBA consulting teams and related

projects for U.S. multinational business.

z

Course Accomplishments

Analyzed Brazil macro political, economic, social,

and technological considerations.

z

Course Accomplishments

Analyzed Brazil’s outlook for growth with leading

global economist.

z

Course Accomplishments

Analyzed regulatory and policy trends, with experts

from U.S. DoS.

z

Course Accomplishments

Analyzed structured trade and export finance

solutions, with representatives of HNB.

z

Course Accomplishments

Analyzed Brazil market entry and organizational

structure considerations.

z

Course Accomplishments

Analyzed employment and other relationships in

Brazil – including Brazil specific labor, agent, and

distributor considerations.

z

Sample LatAmExperience

z

Sample LatAmExperience

Managed acquisition of Dow Chemical Company

polyolefin films facility by Brazilian manufacturer.

Transaction included not only physical real estate

assets, but also certain intellectual property,

strategic corporate tax planning, environmental

implications and tax incentives.

z

Sample LatAmExperience

Managed acquisition and post acquisition

integration of Brazilian software company by Santa

Monica based U.S. technology company.

z

Sample LatAmExperience

Assisted U.S. publically traded company with

development of Brazilian market entry strategy.

z

Sample LatAmExperience

Negotiated and drafted definitive agreements

related to acquisition of assets, including robotic

equipment and tooling, in Mexico, by U.S.

publically traded company.

z

Sample LatAmExperience

Negotiated and drafted supply agreements for use

by U.S. publically traded company in Mexico.

z

Sample LatAmExperience

Managed drafting and negotiation of Uruguayan

distribution agreement related to farm and

compact construction equipment.

z

Sample LatAmExperience

Managed drafting and negotiation of Brazilian

distribution agreements in software and

manufacturing industries.

z

Sample LatAmExperience

Developed and provided anti-corruption training to

publically traded U.S. company employees in Brazil.

z

z

z

Import Export Process

z

State

DepartmentDirectorate of Defense

Trade Controls (DDTC)

Arms Export Control Act

International Traffic in Arms

Regulations ITAR

22 C.F.R. Parts 120-130

UML - U.S. Munitions List

Commerce

DepartmentBureau of Industry and

Security (BIS)

Export Administration Act

Export Administration

Regulations (EAR)

15 C.F.R. Parts 700-799

CCL - Commerce Control

List

Treasury

DepartmentOffice of Foreign Assets

Control (OFAC)

Trading with the Enemy Act,

Int’l Emergency Economic

Powers Act

Iraq Sanctions, Terrorism

Regulations, and Others

31 C.F.R. Parts 500-599

List of Specially

Designated

Nationals +

Blocked Persons

Cuba

z

z

Import Export Process

Tax/DutyRadar

Obtain

importing

license

(if required)

Register with the

governmental

registration

system

(if required)

z

General Import Taxes + Duties

II-Import Dutyvaries based on product

& Country of origin

(NCM, HS)

0-35% Import Duty0-5% raw materials, 20%

finished consumer

goods, 35% autos and

luxury items

0-35%

12%

avg

Import Duty 6%

IPI-Industrial

Product TaxVaries based on product

(CNM) up to 300%

tobacco

20% avg VAT 16% VAT 19%

PIS-Social

Integration Program

Contribution

1.65%

COFINS-Social

Security Financing

Contribution

7.6%

ICMS-State Tax 7-25%*

SP 18%

*Current legislation and recent Supreme Court

decisions may impact the applicable ICMS rate.

Decree 8,426/15 – effective this month (July 2015)

z

Additional Tax Considerations

On average, firms make 9 tax

payments per year and spend

2600 hours per year filing,

preparing and paying taxes

Brazil: 2,600

LatAm: 366

OECD: 175

Corporate TaxPlus 10% on taxable

income over R$240,000

-may choose deemed

profit system if under

threshold

15% Corporate Tax 34% Corporate Tax 20%

Transfer Price

ConsiderationsYes Transfer Price

ConsiderationsYes Transfer Price

ConsiderationsYes

Source: World Bank, Doing Business 2012

On average, firms make 9 tax

payments per year and

spend 239 hours per year

filing, preparing and paying

taxes

On average, firms make 9 tax

payments per year and

spend 291 hours per year

filing, preparing and paying

taxes

Baseline:+ medium size business

+ taxes and mandatory

contributions are

measured at all levels of

government

+ a range of standard

deductions and

exemptions is also

factored

z

Brazil Ex-Tarifário Program

Tariff reductions generally reduce the applicable tariff from to 0-2% and may also reduce IPI (Resolução CAMEX 35/2006)

Importer must file for the Ex-tarifário

Certificate or statement from appropriate body, technical reports, public consultation among other things may be considered to determine the existence of a similar domestic good

If no similar good is

produced domestically,

an importer may

qualify for reduced or

eliminated tariffs

z

Importer May Qualify If:

Higher quality product or service

Higher productivity of equipment

Increased efficiency

Reduced delivery time

Other specific performance factors may be considered depending on product

z

ICMS credit to

importer

PIS/COFINS reducedII/IPI 0%

or 88% reduction

IRPJ reduced 75%

Free TradeManaus Free Trade Zone – ZFM

Western Amazon – AO

Free Trade Areas - ALC

General Process

Cert of importer eligibility on the SISCOMEX

Classification of imported goods HS / NCM

Submit Invoice

Register Transaction on SISCOMEX

Import Licenses

z

MERCOSUL Southern Common Market

Free from import duty with certificate of origin

Exceptions to Common External Tariff (CET)

Brazil is permitted 93 exceptions to the CET

June 2009 trade minister raised several import duty rates

Mexico/Brazil revised auto tariff structure

Decision No. 39/11 of the Mercosul Common Market Council permits and outlines procedures for the countries to negotiate these topics

Member Countries

+ Brazil

+ Argentina

+ Uruguay

+ Paraguay

+ Venezuela

Applied

+ Guyana

+ Suriname

Associate Members

+ Bolivia

+ Chile

+ Colombia

+ Ecuador

+ Peru

Observer of

Agreement

+ Mexico

+ New Zealand

z

Pacific Alliance

Latin America (NO BRAZIL) trade bloc

Members:

Chile

Colombia

Mexico

Peru

Observers 30+ Countries:

+ Costa Rica

(currently applying for membership)

+ Panama

+ Finland

+ India

+ Israel

+ Singapore

+ Canada

+ U.S.

z

Level of corruptionTransparency International, 2014 CPI index

The abuse of entrusted power for private gainPerception of corruption in public sector

2014USA: 17th of 175Brazil: 69th of 175

1995 (year 1 of CPI)USA: 15 of 41Brazil: 36 of 41

P E S TPolitical Risk

+ The ability of government to respond to political risk

+ The ability of government to NOT cause political risk The unit of

measurement

for political risk

is STABILITY

Denmark

1st

USA

17th

Chile

21st

Brazil

69th

India

85th

Colombia

94th

China

100th

Russia

136th

North

Korea,

Somalia

174th

z

FCPA

z

About the FCPA

Applies to U.S. companies, citizens, foreign subsidiary, officer, director, employee, or agent of a U.S. company or its foreign subsidiary, any stockholder acting on behalf of the company, foreign companies with U.S. registered securities

Scope and operation of FCPA not restricted to USA territorial boundaries

z

Facts about the FCPA

U.S. has pursued 3.5 formal foreign bribery enforcement actions for every one action pursued by all other countries

Companies settle, pay fines and forfeit profits

U.S. Justice Dept. continues to focus on individuals

Guilty employees go to jail, pay fines and must make restitution

z

Best Practices

Contract

Review

Compliance

Program +

Culture

Financial

Controls

z

Agents + Distributors

z

Questions to Ask

What is the relationship?

Is a written agreement required?

Rights and duties?

Termination?

Permanent establishment?

z

Agent DistributorActivities subject to some control by supplier Activities subject to only minimal control by

supplier

Does NOT take title to goods Takes title to goods, buys and sells for own

account

May handle products of other suppliers; but, is

less likely to do so than distributor

May handle products of other suppliers

Generally compensated on a commission basis Earnings based on resale profit margin

Usually does not warehouse goods Usually warehouses and physically delivers goods

Usually does not use own capital Uses own capital

Bears no risk of failure of payment Bears economic risk of failure of payment by

customer

May have power to contract on behalf of the

supplier

Has no power to bind the supplier contractually

z

Agent Distributor

Creation Statutory requirements Contract law

Compensation CommissionSells on own account

Termination Enumerated “just cause” reasons Contract law

z

Best Practices

If properly structured commercial representative and distributorship agreements may require less up-front investment than a more direct presence in the market.

Tradeoff for this can be less control over how product is promoted, sold and serviced in the market.

Using commercial representatives or distributors may make sense as a means to first enter the market or even as a permanent business model.

If proper safeguards are not in place, mismanagement of product by commercial representative or distributor can permanently damage a brand.

z

Best Practices

Foreign companies should structure commercial representative and distribution agreements with a long-term strategy that preserves maximum flexibility and may include a future more direct presence in the market. For this strategy to work, well-crafted written agreement is imperative.

Care must be exercised to not blur the distinctions between a commercial representative and a distributor.

Long term exclusive contracts should generally be avoided. In some countries, short term contracts once renewed may be considered contracts for "indefinite terms" after the first renewal, by some courts.

z

Best Practices

Minimum sales requirements should generally be established in the agreement.

Standards for product service and maintenance should generally be set out in the agreement.

Generally, regular and adequate reporting should be required.

Other key points to address often include termination and causes for termination, distribution points and control over distribution in case of termination.

z

VisasTemporary

Visas

Technical Visas

Permanent

Visas

z

Data Protection

z

Legal Advice

The content of this presentation is for educational purposes only. Each legal issue is fact dependent, this presentation should not be used or viewed as legal advice; your legal counsel should be consulted on the application of your particular factual situation to the current law.

BrazilTAX

Corporate Tax RateTop marginal corporate tax rate stands at 34 % in Brazil

Break down of 34%

◦ 15 % Basic rate

◦ 10% Surtax on income above BRL 240,000 per year (approximately $ 800,000)

◦ 9% Social contribution on pre-tax profits

◦ Losses can be carried forward indefinitely

◦ Dividends are not subjected to withholding taxes on profits generated on or after Jan 1, 1996

Importation of Royalties and Services

◦ 15% withholding tax for Royalties from patents knowhow and services

◦ PIS, CONFIS, and CIDE total 19.25%

Historically the tax rates have been consistent

Repatriation

Generally there are no restrictions on repatriation of earnings. The investors must register the original investment and any capital increases/ earnings with BACEN (Banco Central do Brasil)

Repatriations of originally invested capital are subject to withholding tax t 15%

Over the past few years all levels of government have increased incentives to attract foreign investments

Assuming the dividend paid was after Jan 1, 1996The example considers Federal Taxes only

Example

Rate Dividend Services Royalties

Pre tax income 1,000,000 1,000,000 1,000,000

Basic rate 15% (150,000.) (150,00) (150,000)

Surtax 10% (100,000) (100,000) (100,000)

(PIS & COFINS) Social Contribution 9% (90,000) (90,000) (90,000)

Withholding 15% - (99,000) (99,000)

PIS/COFINS/CIDE 19.25

Effective Tax RateAll earnings paid out asdividends

All earnings used to import services

All earnings used to import know how

withholding tax creditable/(not creditable) in US 34% 56.6%/47% 56.6%/47%

660,000 433,950/531,300 433,950/531,300

ChileTAX

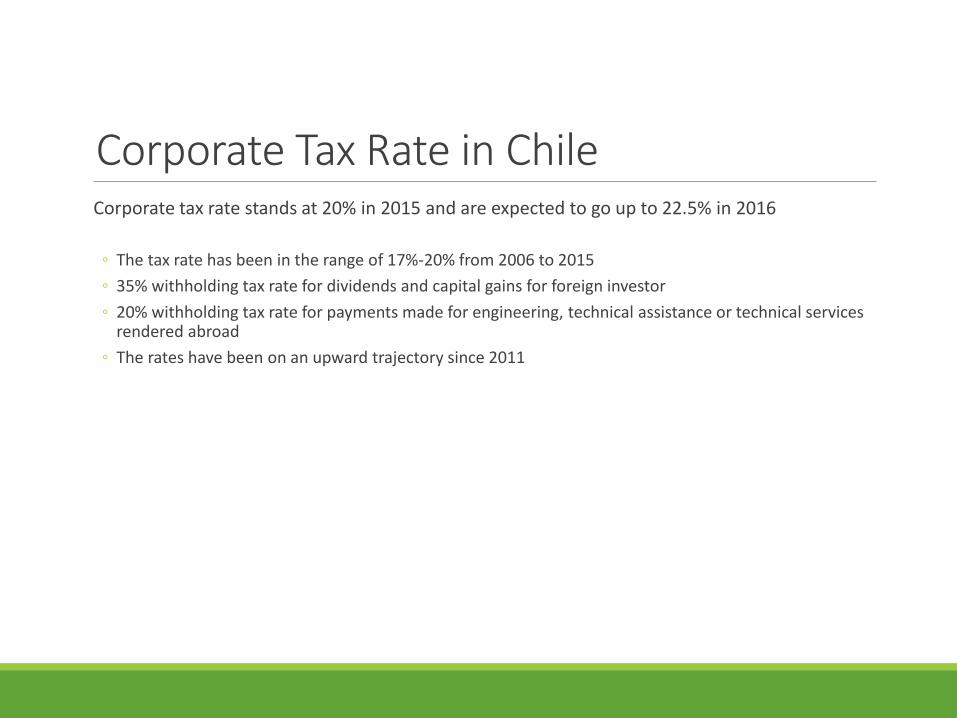

Corporate Tax Rate in ChileCorporate tax rate stands at 20% in 2015 and are expected to go up to 22.5% in 2016

◦ The tax rate has been in the range of 17%-20% from 2006 to 2015

◦ 35% withholding tax rate for dividends and capital gains for foreign investor

◦ 20% withholding tax rate for payments made for engineering, technical assistance or technical services rendered abroad

◦ The rates have been on an upward trajectory since 2011

Repatriation

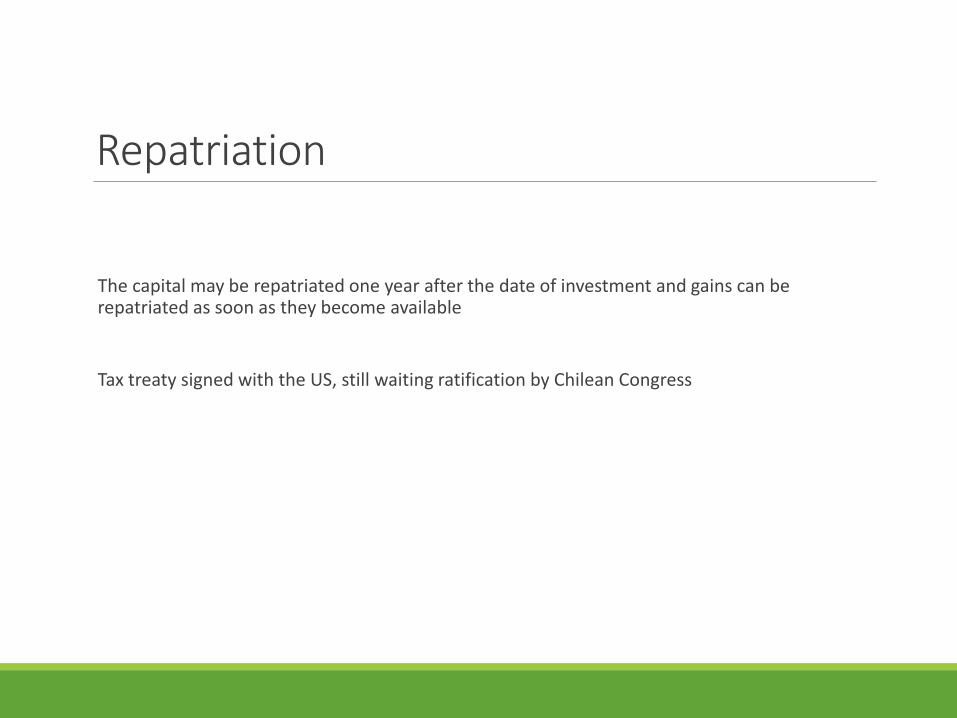

The capital may be repatriated one year after the date of investment and gains can be repatriated as soon as they become available

Tax treaty signed with the US, still waiting ratification by Chilean Congress

The taxes considered are at the Federal level only

Example

Rate Dividend Services Royalties

Pre tax income 1,000,000.00 1,000,000.00 1,000,000.00

Corporate Tax Rate 20% (200,000.00) (200,000.00) (200,000.00)

Withholding 20% - (200,000.00) (200,000.00)

Tax rate for dividend 35% (280,000.00) - -

Return 520,000.00 600,000.00 600,000.00

ColombiaTAX

Corporate Tax Rate in ColombiaCorporate tax rate stands at 25% in 2015 and 2016

◦ The tax rate have been consistent at 25%

◦ Corporate income tax for equality rate- 9% (applies to corporate tax payers required to file return)

◦ Capital Gains are taxed at 10%

◦ Dividends paid to nonresidents without a branch or PE in Colombia are not subject to tax if the dividend are paid out of profit taxed at corporate level. If the dividends paid are paid out of profit not taxed at corporate level are subject to 33% withholding tax

◦ Withholding tax of 26.4% for software royalties and 10% withholding tax for technical service, technical assistance or consulting services

◦ Municipal and state taxes may apply

Repatriation

Foreign investment needs to be registered with the central bank

The government has the authority to restrict remittance if the international reserve fall below 3 months worth of imports (The reserve have been above this level for decades)

No tax treaty in place yet with the US

The taxes considered are at the Federal level only

Example

Rate Dividend Services Royalties

Pre tax income 1,000,000.00 1,000,000.00 1,000,000.00

Corporate Tax Rate 25% (250,000.00) (250,000.00) (250,000.00)

Corporate Tax Rate for equality 9% (90,000.00) (90,000.00) (90,000.00)

Withholding for Services 10% - (66,000.00) -

Withholding for Royalties 26.4% - - (174,240.00)

Return 660,000.00 594,000.00 485,760.00