your global macro playbook - port phillip · pdf fileyour global macro playbook jason...

TRANSCRIPT

YOUR GLOBAL MACRO

PLAYBOOK

2

Your Global Macro Playbook

Jason Stevenson, Resources Analyst

[Date of updated content: Wednesday, 2 August 2017]

Due to the large volume of similar reader questions, I’ve updated and assembled content from previous Resource Speculator updates below. The compilation shows my outlook for stocks, bonds and commodities over the short and long term.

My previous target for the next financial crisis was late 2018. However, that’s now changed. The entire sovereign debt crisis I’m predicting might, in fact, blow out into 2020. Perhaps Cycles, Trends and Forecasts Editor Phil Anderson’s 2026 target for the stock and property market high could be on the money.

In the meantime, I’ll keep recommending the best resource stocks in the hottest sectors.

Your Global Macro Playbook covers the following:

• The big-picture story for resources

• Why the best days are ahead for resources

• Are government bonds really safe?

• Why history is a great roadmap

• Where are we at today?

• How to survive the initial panic

• What to do after the panic

• Will gold survive heading into the government debt defaults?

• The truth behind gold

• The latest technical analysis on gold

3

Your Global Macro Playbook

The big-picture story for resourcesFrom 2008 to 2011, China and commodity-driven emerging markets grew quickly.

China announced a RMB¥4 trillion (US$586 billion) stimulus package at the height of the US sub-prime mortgage crisis in 2008. The country’s capital was spent quickly across a few years, mostly on infrastructure projects. That demanded lots of natural resources. And it’s why commodity-driven emerging markets and Australia — itself a major supplier of commodities — benefitted greatly.

When the stimulus spending stopped, however, emerging-market economies and Australia began to slow down. Emerging markets now face major crises. During the good times, these countries spent big, but now they can’t afford to pay back the debt.

Chinese growth has also slowed — it’s moving towards a consumption-driven economy, which, historically, has seen a slowdown in GDP growth. Its economy also faces major debt issues.

Given this economic slowdown around the world, it’s little surprise that commodities haven’t done well since 2011. The sector’s performance is shown on the chart below in blue:

Source: Interactive Investor

Commodities are down 39.91% since 2008.

In comparison, reflecting large and mid-capitalisation stocks across 23 developed market countries, the global stock market is up about 170.81%

4

Your Global Macro Playbook

since 2008. You can see that by looking at the red line, which represents the MSCI World Index.

The green line shows the global aggregate total return index, which focuses on investment grade debt from 24 local currency markets. That index is up 96.02% from 2008, which isn’t surprising given the amount of central bank money-printing around the world.

Resource stocks are the most unloved and challenged in the stock market today. And while some see that as reason enough to stay away, I believe it creates a major opportunity for you.

In fact, the way I see it, the next commodities bull market is set to be explosive.

Why the best days are ahead for resourcesWhen the bull market begins, it should see strong demand from electric vehicles (EV) and hydrogen-fuel-cell vehicles. But both industries aren’t ready to take off yet. Just look at Tesla, Inc.’s [NASDAQ:TSLA] development as an indicator. The company still hasn’t become a mass-producing EV company. But, when that happens, we should start to see a positive knock-on effect across resource stocks underpinning the industry’s growth.

Quartz reported on 11 July (my emphasis added):

‘ Can Tesla sell mass-market EVs without the credits? Maybe not, argues Michelle Krebs of Autotrader. “There isn’t enough consumer demand on their own to drive sales, even with the tax credit,” she argued in an interview, pointing to dealer discounting and an inventory buildup as signs of a soft market for EVs. GM’s Chevy Bolt, its first all-electric, 236-mile range car which has sold about 7,600 cars this year, hasn’t exactly taken the US market by storm.

‘ Only 1% of new vehicles sold in the US are all-electric.

‘ Tesla, which rolled out its first mass-market Model 3 on July 8, plans to produce 500,000 a year by 2018. “I think it boils down to we have to figure out what it’s going to take consumers to buy these kinds of vehicles,” said Krebs.’

Clearly, while not all resources will react the same way, EVs need a tremendous growth burst to trigger a commodities bull market. I believe there are sufficient resources out there to support current and near-term demand for EVs. And hydrogen-fuel-cell cars are still probably a few years away as well.

5

Your Global Macro Playbook

In addition, supercomputers, robots and self-driving cars should also demand significant natural resources in the future. However, despite their astonishing advancements, demand probably won’t take off for a few more years. The world is still mostly in the development — not production — phase for these futuristic technologies.

There’s plenty of promise for commodities in the medium-to-long term. To match the demand prospects, there are major supply threats brewing across most commodities (copper, nickel, lithium, tin, vanadium, uranium, platinum, and so forth) dependent for the next phase of the technology revolution.

The combination of demand triggers and major supply deficits should trigger an almighty commodities bull market. Unlike the 2008–11 commodities bull market, which was fuelled by demand growth, the next bull market will probably be triggered by supply shortfalls.

These types of bull markets are generally bigger and longer lasting than demand-driven ones. That’s because supply attempts to catch up with demand, which struggles due to the lack of projects in development.

But that doesn’t necessarily mean we’ll be waiting years for a bull market to develop.

In the short term, geopolitical conflicts could trigger a surge in demand for commodities as well. There’s ongoing political drama rising across the Middle East, North Korea, on the Indian border with Pakistan and China, and the South China Sea. Even if there isn’t a major war, and we hope there won’t be, these issues could still pose supply crises for many commodities.

If North Korea does something foolish, such as launching a missile that goes off track, global tensions could rise tremendously overnight. And governments might start spending even more money on military armaments, which would likely boost commodity demand.

On another note, if there’s a major war in the Middle East — home to much of the world’s oil reserves — I believe crude oil could hit $200 per barrel. A dispute between Iran and Saudi Arabia could trigger such an outcome. Tensions between Saudi Arabia and Qatar — the richest nation per capita on Earth — are also worth keeping an eye on.

But, despite ongoing tensions, there’s no reason to turn bullish on crude oil yet. That’s just one part of the resource story we’ll be keeping an eye on.

Other than that, the coming sovereign debt crisis I see coming should be very good news for gold and silver stocks. However, I believe precious

6

Your Global Macro Playbook

metals will break out after the sovereign debt crisis meltdown plays out.

Of course, I could be wrong.

And I’d love to see commodities and precious metals take off now. I’m carefully studying the fundamentals and technicals of all commodities. When natural resources start to turn around, that’s when the big money will be made. Commodities could easily become the best-performing sector on the market. It’s worthwhile monitoring the resources market for that reason, even if you don’t want to buy any resource stocks today.

Ultimately, whether the commodities bull market ends up arising from shorter- or longer-term factors, the outlook for the sector is positive. And the outlook for certain stocks within the sector looks even better. That’s why I’m looking for the hottest stocks in the best sectors, while we wait for the next commodities bull market. That lucrative proposition is certainly worth your time and money today.

Now, if you’re worried about the wider economic environment, the true events of the Great Depression should help you understand the future. That’s because history tends to repeat.

Let’s wind back the clock…

Are government bonds really safe?The stock market crash of 1929 is the most talked about financial disaster in history. Yet it’s also the most misunderstood financial crash of all time.

Initially, the panic was due to an overbought, and overvalued, market. The Roaring Twenties led to excessive risk-taking. I won’t go into the full story here. But economic conditions weren’t supporting the stock market’s advance at the time.

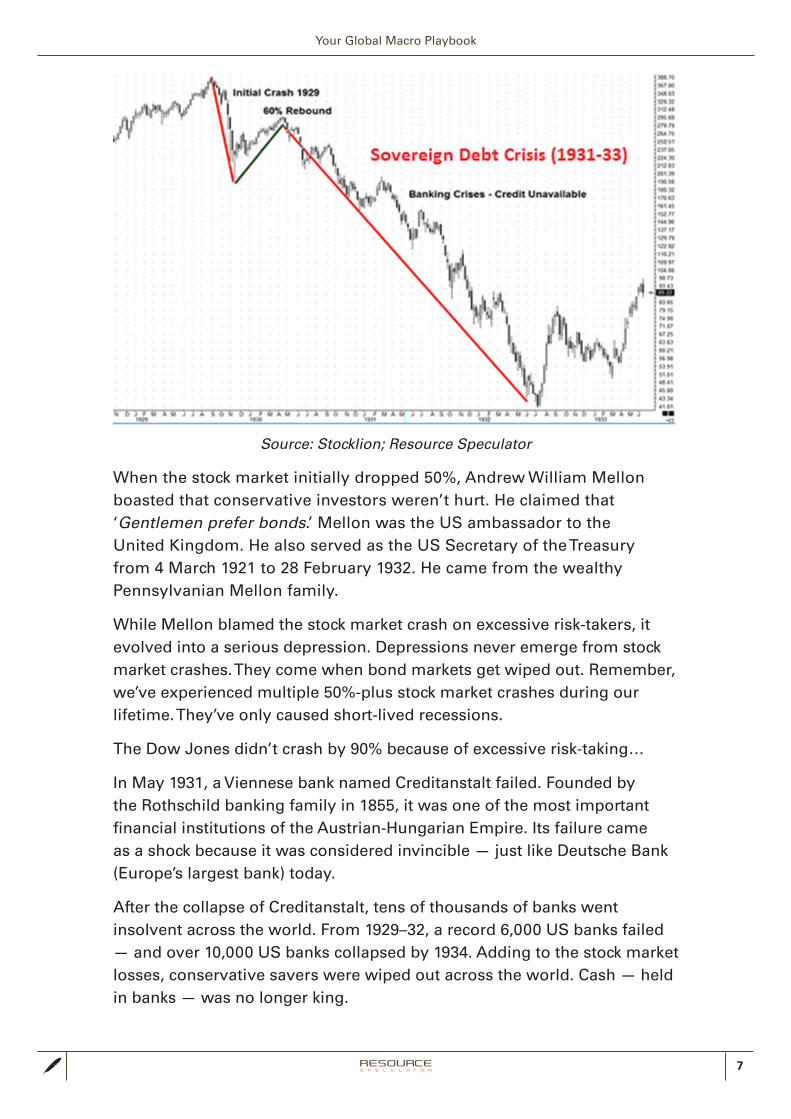

The crash began on 24 October, when the market opened 11% lower. Prior to this crash, the stock market peaked on 3 September, with the Dow Jones Industrial Average at 381.17 points. After an initial 50% drop in 1929, it saw a 60% rebound going into 1930. But it was short-lived.

The Dow reached its ultimate bottom on 8 July 1932, at 41.22 points. From peak to trough, this amounted to a loss of 89%. You can see this in the chart on the next page.

7

Your Global Macro Playbook

Source: Stocklion; Resource Speculator

When the stock market initially dropped 50%, Andrew William Mellon boasted that conservative investors weren’t hurt. He claimed that ‘Gentlemen prefer bonds.’ Mellon was the US ambassador to the United Kingdom. He also served as the US Secretary of the Treasury from 4 March 1921 to 28 February 1932. He came from the wealthy Pennsylvanian Mellon family.

While Mellon blamed the stock market crash on excessive risk-takers, it evolved into a serious depression. Depressions never emerge from stock market crashes. They come when bond markets get wiped out. Remember, we’ve experienced multiple 50%-plus stock market crashes during our lifetime. They’ve only caused short-lived recessions.

The Dow Jones didn’t crash by 90% because of excessive risk-taking…

In May 1931, a Viennese bank named Creditanstalt failed. Founded by the Rothschild banking family in 1855, it was one of the most important financial institutions of the Austrian-Hungarian Empire. Its failure came as a shock because it was considered invincible — just like Deutsche Bank (Europe’s largest bank) today.

After the collapse of Creditanstalt, tens of thousands of banks went insolvent across the world. From 1929–32, a record 6,000 US banks failed — and over 10,000 US banks collapsed by 1934. Adding to the stock market losses, conservative savers were wiped out across the world. Cash — held in banks — was no longer king.

8

Your Global Macro Playbook

Moreover, commodities, property and agriculture all collapsed to cents on the dollar.

And this is only half the story.

Most European, South American and Asian governments defaulted entirely on their bonds. After confiscating gold, Franklin Delano Roosevelt (FDR) devalued the dollar by 41%. He increased the gold price by 69%, from US$20.67 to US$35 an ounce. It was a partial default on US government bonds held by international parties.

Indeed, absolutely nothing survived the financial crisis of 1929–33 unscathed — stocks, property, commodities, bonds, agriculture…everyone took a hit, including the Rothschild family.

Why history is a great roadmap Vern Gowdie, Editor of The Gowdie Letter and Gowdie Family Wealth advisory services, believes we’re in for a historic stock market crash similar to 1929–32. Vern believes that — as with the 2008–09 financial meltdown — the stock market will crash by 80–90%. He’s recommended retreating to the safety of cash for many months.

I don’t believe that we will see a major stock market crash.

There’s a bubble in bonds — not stocks.

The sovereign debt crisis could wipe out much of the world’s capital.

People talk about something being ‘too big to fail’. The ‘too big to fail’ theory argues that certain corporations, particularly the banking and financial institutions, are so big and interconnected that they can’t fail. Failure would be disastrous to the greater economic system. The theory suggests that government must support these institutions when they face potential failure. Well, unfortunately, the theory ignores that government has grown too big and can’t continue to support the world.

The sovereign debt crisis — major defaults on government bonds — should mark the end of socialism. A lot of benefits are likely to be rolled back, which we’re starting to see taking place now around the world.

It’s likely that a lot of people will start protesting on the streets in greater numbers — especially when governments default on their pension and socialist promises. When that plays out, I believe global stock markets could sell off in panic.

The US Dow Jones Industrial Average index could fall by 30% within a few

9

Your Global Macro Playbook

months. That could be the extent of the stock market collapse.

When fund managers, pension funds and sovereign wealth funds realise the crisis exists in the bond market, they will start buying stocks, commodities, and property. That’s why, if anything, we’re probably looking at a short and sharp selloff in stocks during the initial panic.

I don’t expect a major correction of this magnitude to start until something happens, mind you. There must be a major macroeconomic issue to scare the herd…like a major bank failure. In the meantime, until something major happens that spooks the public, the stock market is likely to keep making new highs.

There’s nothing to worry about…yet.

Remember, before the GFC hit in 2008, there were credit defaults throughout 2007. During 2007, lenders began foreclosure proceedings on nearly 1.3 million properties, a 79% increase over 2006. Northern Rock, formerly the Northern Rock Building Society, was a British bank drowning in mortgage debt. It asked the Bank of England for liquidity support on 14 September 2007.

With hindsight, that should have been a major red flag…

We need to see some bigger, more glaring signs of the next financial crisis. In my view, that hasn’t happened yet.

I believe another country probably needs to leave the European Union to get the sovereign debt crisis rolling.

There has been no major political upset in Europe since Brexit. The French and Dutch elected politicians that didn’t truly stand for change. German Chancellor Angela Merkel will also probably win the election this year.

The next political upset might not come for months…or years.

The European Commission is considering triggering Article 7 on Poland for refusing to accept refugees. That denies the member to vote. Poland might be the second country to leave the EU.

It might not happen for some time, though.

The entire sovereign debt crisis might, in fact, blow out into 2020. As mentioned previously, Phil Anderson’s 2026 target for the stock and property market high could well be on the money.

Politicians could very easily kick the can down the road as well. That would build the next financial crisis into something of an Armageddon event.

10

Your Global Macro Playbook

Where are we at today?There’s a lot to consider with this story. The Fed is looking towards raising interest rates. As interest rates move higher, bond prices will move lower. Remember that bond prices and interest rates have an inverse relationship. That’s likely to attract more capital into the US stock market in the short term, as bonds become less attractive.

Inflation has also skyrocketed across the UK. That’s put pressure on the Bank of England to lift interest rates.

The Bank of Japan, on the other hand, remains dovish. That’s seen as good news for the Japanese yen. Recently, the BOJ pushed back its inflation timing target into 2020–21. The central bank probably won’t end its money-printing program soon. In other words, punters gets to borrow yen at near-zero interest rates for longer.

Meanwhile, the European Central Bank (ECB) is nearing the end of its money-printing program. ECB President Mario Draghi said he would discuss potential changes to the program before year’s end.

If Draghi reverses course later this year, it may trigger minor 10–15% stock market correction. It would be a big change in policy, which could make markets nervous. That said, I wouldn’t worry about the correction. Corrections are a healthy part of bull markets, and there hasn’t been a 10% correction since January 2016. So, assuming another correction plays out in the second half of this year, it would be a good time to buy your favourite stocks in my view.

The Chinese debt issue story could also cause a 10–15% correction. In any case, we’re well overdue for another minor 10–15% correction.

The risk of a major stock market correction doesn’t look likely anytime soon. There’s no near-term risk of a major collapse.

Remember, similar to 2007 and early 2008, something major needs to happen to panic markets. That hasn’t happened. For that reason, don’t anticipate a ‘black swan’ event that you can’t control. Let the market reveal itself. I’ve started going more with the flow these days. And so should you.

I truly believe history will repeat itself. Just like the sovereign debt crisis of 1929–32, almost every debt class should temporarily sell off during the sovereign debt crisis. That includes gold and silver, which I’ll get to below. Ironically, the US dollar — the world reserve currency — should continue to rally.

As the US dollar shoots higher, global economic growth should slow.

11

Your Global Macro Playbook

Emerging and developed nation government bond defaults should storm across the world.

Emerging markets are more likely to default on their national debts. Developed governments could either default entirely, significantly extend bond maturity dates, or cut interest payments.

I’m recommending either shorting government bonds or avoiding them entirely. I also recommend shorting government bonds on any rally.

You can see how there’s a very serious crisis on the horizon. We could see all asset classes — commodities, stocks, and bonds — collapse due to outright fear. But it might not happen for some time. The US dollar index might need to burst past US$1.10 to trigger the defaults, especially across emerging markets and China, which own trillions of dollar-denominated debt.

How to survive the initial panicPunters and institutions won’t know what to do when the defaults play out. Punters are likely to move their money into cash (US dollars) for safety. Keep in mind that I’m only referring to the initial panic here.

US Treasuries may receive the majority of capital flows. That’s starting to happen now, in fact.

Blue-chip corporate bonds could see a lot of capital inflows.

Remember, large capital needs to park its money somewhere. These are a few options on where that money could flow.

What comes after this point should be the complete opposite.

What to do after the panicThe bottom is likely to happen following a major policy decision. Take history as an example…

During the sovereign debt crisis of 1929–32, FDR devalued the dollar against gold. He confiscated all the gold, which was money at the time. That stopped the hoarding. He then proposed the ‘New Deal’ in 1933 — a major infrastructure package aimed to increase employment. That’s when stocks started to take off into 1937.

During the global financial crisis, the US dollar gold price started to reverse in November 2008. Interestingly, that’s when then US Fed

12

Your Global Macro Playbook

Chairman Ben Bernanke announced the Troubled Asset Relief Program (TARP). TARP purchased toxic assets and equity from financial institutions to strengthen its financial sector. Stocks started to reverse in March 2009, when the Fed said it would print an extra US$1 trillion to save the financial system.

Indeed, history suggests that a major policy change is required to save the day. When it comes, whatever the policy idea may be, the stock market should take off to new highs.

Commodities — especially precious metals and agriculture — could see their biggest bull market in history.

Unfortunately, the majority will probably miss out on the action.

A major correction could scare off the investment herd. Rather than buying stocks, many are likely to stay in cash or, worse, lose all their money in government bonds. Most punters and institutions will think another global financial crisis — and another major stock market crash — is around the corner.

But they’re overlooking something important…

In contrast to the financial meltdown of 1931–33, both sovereign wealth funds (SWFs) and pension funds exist today.

Bloomberg statistics show Japan’s Government Pension Investment Fund — the world’s largest — manages roughly US$1.2 trillion in funds. Realising there are risks in the bond market — and that trillions of dollars’ worth of bonds still boast negative yields — the Japanese want to diversify into quality stocks. The Australian Government Future Fund manages roughly AU$120 billion by comparison.

Historically, SWFs and pension funds have invested around 70% of their funds in ‘safe’ government bonds. They also own a lot of high-yielding assets, like bank and insurance bonds, and stocks and other corporate debt.

According to the Bank for International Settlements, the global government bond market is worth roughly US$40 trillion. I should note that ING Research shows the global debt market is worth US$223.3 trillion. This includes banking, insurance, emerging market, household and corporate debt. In comparison, based on statistics from 58 members of the World Federation of Exchanges, along with stock indices around the world, the global stock market is worth roughly US$56 trillion.

There’s a massive debt to equity shift coming…but after the initial stages of the panic.

13

Your Global Macro Playbook

I expect SWFs and pension funds to start buying stocks. Their bids should prevent a major stock market crash.

Eventually, as capital switches from bonds to stocks, the stock market should make new highs — not lows. The stock market could become the best place to create wealth within the next 10–15 years.

Remember, gold is likely to get destroyed during the initial stages of the sovereign debt crisis. Gold’s likely to fall with stocks during the start of the crisis, until punters wake up and realise that government is the problem. That’s when everything should start to flip.

A lot of gold bugs would call me crazy. They will tell you to buy gold — and never sell — because the world is loaded with unsustainable debt. Frankly, they have been saying that for over three decades.

The gold promoters just don’t get it. To understand how gold works, let’s wind back the clock…

Will gold survive heading into the government debt defaults?

Gold increased slightly heading into the sovereign debt crisis of 1931–33. But at the time, the world was on a gold standard — money was gold. If you didn’t like holding cash, you could exchange it for gold.

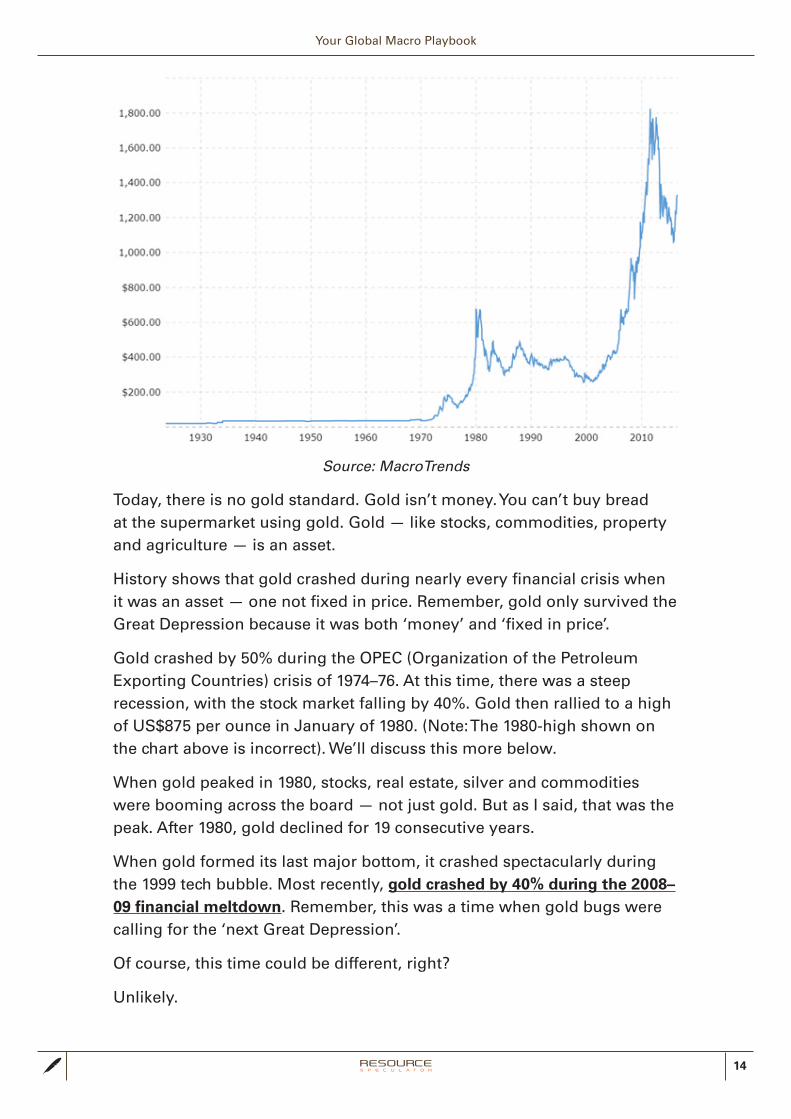

Currencies across the world were pegged to bullion. Plus, until 1971, the gold price remained at a fixed price — it didn’t fluctuate like it does today. You can see this in the chart on the next page.

14

Your Global Macro Playbook

Source: MacroTrends

Today, there is no gold standard. Gold isn’t money. You can’t buy bread at the supermarket using gold. Gold — like stocks, commodities, property and agriculture — is an asset.

History shows that gold crashed during nearly every financial crisis when it was an asset — one not fixed in price. Remember, gold only survived the Great Depression because it was both ‘money’ and ‘fixed in price’.

Gold crashed by 50% during the OPEC (Organization of the Petroleum Exporting Countries) crisis of 1974–76. At this time, there was a steep recession, with the stock market falling by 40%. Gold then rallied to a high of US$875 per ounce in January of 1980. (Note: The 1980-high shown on the chart above is incorrect). We’ll discuss this more below.

When gold peaked in 1980, stocks, real estate, silver and commodities were booming across the board — not just gold. But as I said, that was the peak. After 1980, gold declined for 19 consecutive years.

When gold formed its last major bottom, it crashed spectacularly during the 1999 tech bubble. Most recently, gold crashed by 40% during the 2008–09 financial meltdown. Remember, this was a time when gold bugs were calling for the ‘next Great Depression’.

Of course, this time could be different, right?

Unlikely.

15

Your Global Macro Playbook

A financial crisis is a financial crisis.

Plus, gold promoters never question why gold hasn’t rallied yet. To get the answer, one needs to look at history.

The truth behind gold

‘History doesn’t repeat itself but it often rhymes.’

Mark Twain

Mark Twain spent his life observing and reporting on his surroundings. There’s no better person to learn from with regard to history.

During his life‚ Twain watched a youthful United States evolve into an international powerhouse. It was no cruisy ride. The nation was torn apart by massive civil unrest (including the American Civil War), multiple recessions and depressions, a state sovereign debt crisis, and international wars…all during his lifetime.

Twain observed and experienced this vast growth and change. And along the way‚ he often had something to say about the changes happening in his country. In 1873, for example, he co-wrote The Gilded Age, a novel that attacked political corruption‚ big business, and the American obsession with getting rich, which seemed to dominate the era.

Times certainly haven’t changed.

Unfortunately, these days, most investors no longer observe or think for themselves. And gold promoters have capitalised on this wilful ignorance for decades.

When gold rallies, without fail, the gold bugs argue that this time is different. When the precious metal falls, they argue gold is ‘correcting’ but remains in a bull market. Despite history often rhyming, gold’s promoters refuse to observe the pattern…let alone report on it.

Few people bother to ask why gold follows a fairly predictable pattern. To get the answer, it’s useful taking a step back in time…

Following the Second World War, the world economy experienced a rapid expansion. The US contributed significantly to the rise. It replaced the United Kingdom as the world’s largest economy in 1914, rising into 1999.

Despite the rise of China and other developing nations over the past 17 years, the US remains the world’s largest economy. And it continues to grow (albeit slowly and painfully) thanks to its size and influence.

Gold, like all other commodities, is priced in US dollars. That’s because the

16

Your Global Macro Playbook

US dollar is the world reserve currency. The Australian dollar gold price is merely a currency adjustment of the US gold price. In that case, as modern history shows, the US dollar gold price is the key to driving another gold bull market. Every other gold currency will react to its move.

A lot of analysts have been bullish on gold since the 1980 high of US$875 per ounce. You can see the price spike on the chart below:

Source: goldcoin.org

I wasn’t alive back then. But I do know my history. History is the key to understanding financial markets — it’s a roadmap for the future.

As you can see, gold broke out during mid-1979…

US citizens were suffering a collapse in the confidence in government. The nation was recovering from its defeat in the Vietnam War, the Watergate scandal and Nixon’s subsequent impeachment, and the assassinations of John F Kennedy, Robert F Kennedy and Martin Luther King Jr.

On 15 July 1979, US President Jimmy Carter addressed the nation on TV. He said there was a ‘crisis of confidence’ among the American people. At the time, as shown on the chart above, gold was breaking out. Like today, gold remains a hedge against a collapse in confidence in the government.

The yellow metal surged into January 1980. The confidence in government collapsed for a number of reasons.

First, 52 US citizens were captured during the Iran hostage crisis, when Iranian students overtook the US embassy on 4 November 1979.

Second, Russia invaded Afghanistan on 27 December 1979. Carter’s

17

Your Global Macro Playbook

approval rating had already crashed with his seemingly relaxed attitude towards the hostage crisis. Russia’s aggression only saw this worsen.

And then there was inflation. US inflation figures went through the roof and hit an all-time high of 13% in December 1979.

That inflation was in direct correlation with the collapse in the confidence in government — and all assets (gold, property, commodities and stocks) went up. The majority feared hyperinflation and the collapse of the American empire, with the Cold War heating up.

The gold price went parabolic…

Carter finally addressed the Soviet-Afghan situation in January 1980 — the month that gold peaked. His approval rating surged towards 60% that month. But by late March, Carter’s approval rating dropped back to 39%.

US President Ronald Reagan (an outsider candidate at the time; you may have heard the comparisons to current US President Donald Trump) promised to solve the nation’s economic problems. He called Carter an ‘inept’ leader. The gold promoters argued that Reagan’s policies would cause the next Great Depression, meaning gold was sure to keep going up. (We’re hearing the same thing with Trump today.)

Reagan brought his ‘magic pen’ to the White House and signed every cheque. Making matters worse, US Federal Reserve Chairman Paul Volcker increased interest rates from about 13% to 18% from January to March 1980. Interest rates peaked at about 20% in 1981.

Aggressive fiscal and monetary policy tripled the US national debt during the 1980s. Despite the ‘end of the world’ forecasts by gold bugs, the yellow metal crashed during that decade. As stated earlier, gold ended up falling for 19 consecutive years into 1999.

I bet you can guess the reason why gold fell. That’s right — ‘confidence in government’ returned.

Remember, as it did heading into 1980, the confidence in major world governments must collapse in order for gold to rally. We’re nearing that point, but we’re not there yet.

Gold is likely to remain the hedge against any confidence in government and the banking system…until it falls apart. When the system falls apart, gold — an asset, not money — is likely to collapse. That’s exactly what happened during the global financial crisis of 2008–09.

US$931 per ounce remains my primary target for now. Silver could retest the US$11-per-ounce level.

While there will always be opportunities to trade gold (up and down), I

18

Your Global Macro Playbook

wouldn’t buy gold producers from an investment perspective. It’s not yet time. That said, you might think that I’m wrong — especially if you’re a fan of charts.

The latest technical analysis on gold

Take a look at the monthly chart dating back to 2009 (chart drawn on 28 July):

Source: Tradingview.com; Gold Stock Trader

First, look at the thin black downtrend lines, dating back to the 2011 high of US$1,920 per ounce. That shows gold’s six-year downtrend channel. In other words, gold remains in a major bear market. On a positive note, it has traded along the upper thin black line (major resistance) since July 2016.

Gold did close above the major resistance level of US$1,260 per ounce in July. It was the first time gold closed above technical resistance since mid-2011. That’s promising. But we can’t assume that the gold bull market is back. There’s a lot more work for gold to do yet.

Take a look at this image:

Source: Meta Binary Options

The left-hand image shows an uptrend, with higher highs (HH) and higher lows (HL). The right-hand picture shows a downtrend, with lower highs (LH) and lower lows (LL). Now take a look at the dark black lines painted on the monthly gold chart again. The monthly chart is important to look at for

19

Your Global Macro Playbook

either pattern.

The 2009–11 bull market was defined by higher highs and higher lows. And, while we can’t be sure yet, gold may have entered a new bull market in December 2015.

The major low might be US$1,046 per ounce in the future. That would mean that we’re more than 18 months into the bull market at the time of writing. Gold moved to US$1,374 in July 2016, creating a possible higher high. It pulled back to US$1,122 per ounce in December — a possible higher low.

Hopefully we now see a new higher high.

Look at the horizontal pink lines on the monthly gold chart:

Source: Tradingview.com; Gold Stock Trader

The lower pink line shows US$1,122 per ounce. I showed that number above — it’s potentially the most recent higher low in December. If gold closes below that on a monthly basis, you should ‘look out below’.

The upper pink line at US$1,374 — the previous higher high — shows major resistance. If gold closes above that on a monthly basis, it would define a new higher high. Hopefully the next higher high comes around US$1,500 per ounce.

That’s the key to this story.

A close above US$1,374 would signal that gold has entered a new bull market. Once it makes a new higher high, it can pull back and make a new higher low. That’s the technical formation needed for a bull market. If that doesn’t happen, gold might have made a false technical breakout in July.

I’m letting the numbers do the talking — not my opinion.

I’d love to see gold shoot up soon.

20

Your Global Macro Playbook

That said, your analyst remains a medium-to-long-term gold bull. I believe the yellow metal should hit US$4,000 per ounce within the next 10 years. But, fundamentally, until the numbers prove otherwise, gold probably won’t skyrocket until after the next sovereign debt crisis.

I’ll recommend the best gold producers when the bull market starts inside Resource Speculator. That will be either below US$931 or higher than US$1,374 per ounce. I’m waiting for the right time.

So, while I can only hope I’m wrong, don’t expect gold to break out just yet. In my mind, it will happen for certain eventually. That’s why it’s worth focusing on the junior gold sector. There are plenty of quality ‘penny gold’ stocks trading at dirt-cheap prices. When gold does break out, we’re likely to see a tremendous multi-year bull market. Remember, the best junior gold stocks could make you 10–100 times your money during the good days.

Of course, if you’re dealing with the speculative end of the market, tiny gold stocks could reward you much sooner. Your ‘penny gold’ miners need to hit the golden mother lode…or unveil a major resource upgrade that exceeds expectations…or get taken over by a bigger rival…or announce an exciting acquisition. Any of these things could play out on any day.

It’s a very exciting market that we’re investing into.

Remember, previous gold bull markets show how much money can be made if you can back the right stocks. The idea is to hold the best portfolio of junior gold stocks for the next gold bull market. If you’re interested, I’m focused on finding the best juniors for Gold Stock Trader readers here.

At the end of the day, while there’s likely a major financial crisis on the horizon, it probably won’t happen for some time. There should be plenty of moneymaking opportunities in the resources sector heading into the crisis. You just need to think smart and back the right stocks. I’ll do the hard work for you by finding those stocks.

Your job is to buy your favourite stocks below the buy-up-to prices and stick to the stop-losses.

I hope this contrarian outlook proves useful to your trading.

Cheers,

Jason Stevenson, Resources Analyst

21

Your Global Macro Playbook

All content is © 2005–2017 Port Phillip Publishing Pty Ltd All Rights Reserved

Port Phillip Publishing Pty Ltd holds an Australian Financial Services License: 323 988. | ACN: 117 765 009 ABN: 33 117 765 009

All advice is general advice and has not taken into account your personal circumstances. Please seek independent financial advice regarding your own situation, or if in doubt about the suitability of an investment.

Calculating Your Future Returns: The value of any investment and the income derived from it can go down as well as up. Never invest more than you can afford to lose and keep in mind the ultimate risk is that you can lose whatever you’ve invested. While useful for detecting patterns, the past is not a guide to future performance. Some figures contained in this report are forecasts and may not be a reliable indicator of future results. Any potential gains in this letter do not include taxes, brokerage commissions, or associated fees. Please seek independent financial advice regarding your particular situation. Investments in foreign companies involve risk and may not be suitable for all investors. Specifically,

changes in the rates of exchange between currencies may cause a divergence between your nominal gain and your currency-converted gain, making it possible to lose money once your total return is adjusted for currency. The Reader acknowledges that the contents of this newsletter and all associated intellectual property rights of Port Phillip Publishing Pty Ltd (PPP) including copyright, design rights, property rights, rights to data and databases, trademarks, service marks and any other rights created or developed in the course of the provision of the newsletter shall be and remain the sole and exclusive property of PPP. No person is permitted to copy, forward or reproduce the newsletter and/or its contents

without express consent of PPP. Subscribers to the newsletter are permitted to use this material for their own personal and investment use.

If you would like to contact us about your subscription please call us on 1300 667 481 or email us at [email protected]

Port Phillip Publishing Attn: Resource Speculator PO Box 713 South Melbourne VIC 3205 | Tel: 1300 667 481 | Fax: (03) 9558 2219