yale school of management – edhec-risk institute...

TRANSCRIPT

Institute

Yale School of Management – EDHEC-Risk Institute Certificate in Risk and Investment Management

2

Reshaping the Future of the Investment Management Industry

Having learned through the recent crises about the limitation of existing investment paradigms, investment

managers and institutional investors are showing unprecedented interest in innovative forms of investment

solutions. At the same time, recent advances in academic research have paved the way for the development

of a new generation of financial engineering techniques aimed at improving investor welfare. In this changing

and challenging market environment, it has become crucial for senior investment professionals to keep abreast

of the latest research advances and state-of-the-art investment practices.

It is against this backdrop that EDHEC-Risk Institute and the Yale School of Management are now jointly

offering top-quality executive education courses based on the exceptional strength and relevance of academic

research conducted by both Yale SOM and EDHEC-Risk finance faculty. November 2013 saw the beginning

of a series of joint executive education seminars around the unifying theme, “Advanced Risk and Investment

Management”, throughout the U.S. and Europe. The second edition of the seminar series will start again from

January 2016.

The focus of these seminars is on utilising the latest academic insights to help investment professionals

better understand and implement advanced investment approaches and methodologies. The seminars provide

relevant academic insights with respect to some of the most important dimensions of the investment process,

including implementing disciplined risk and asset allocation decisions, efficiently harvesting factor risk premia

across and within traditional and alternative asset classes, and designing truly meaningful forms of liability-

driven or goal-based investment solutions.

3

4

Yale SOM-EDHEC-Risk

Institute

5

Yale SOM–EDHEC-Risk Certificate in Risk and Investment Management

Validate and Expand your Expertise with this State-of-the-Art Executive Seminar Series in the US and Europe

Participants in these seminar series can acquire the joint Yale School of Management – EDHEC-Risk Certificate in Risk and Investment Management which is a formal recognition of your commitment.

Requirements to obtain the certificate:• Attend four seminars. The Certificate can be completed over a 1 to 2-year period in London and/or New Haven.• Successfully submit one dedicated assignment for each attended seminar. The assignment will take the form of a four-page overview of how the themes covered in the seminar may be used in the design of innovative investment solutions.

6

The programme has been designed along four seminars that are intended to reflect the major steps in a modern investment process. The starting point from an institutional or individual asset owner’s perspective should always be a broad asset allocation decision, with an emphasis on long-term strategic asset allocation decisions that are designed to achieve an optimal risk-return trade-off with respect to the investor’s liabilities or goals.

An in-depth discussion of advanced methods for performing asset allocation decisions is precisely the focus of the first seminar, with a particular emphasis on the design of investment solutions that should help investors achieve their long-term objectives, such as retirement financing goals for example. Once the broad asset allocation decision has been taken and a relevant policy portfolio has been designed, the next step consists in an effective implementation of asset allocation decisions through an efficient harvesting of risk premia across the various segments of financial markets. In this context, the second seminar in the series has a focus on efficient risk premia harvesting in traditional asset classes, namely in equity and bond markets, while the third seminar in the series has a focus on risk premia harvesting in alternative asset classes and investment strategies such as hedge funds, commodities, private equity, infrastructure, real estate or fine arts.

Finally, the fourth and last seminar in the seminar series has a focus on how such global investment strategies can be best implemented in a multi-asset multi-manager context.

Seminar 1: Asset Allocation and Investment SolutionsDay 1 - Risk and asset allocation decisionsDay 2 - Liability-driven and goal-based investing solutions

Seminar 2: Harvesting Risk Premia in Equity and Bond MarketsDay 1 - Foundations and recent research advances in equity portfolio managementDay 2 - Equity factor investing in practice: Applications to portfolio managementDay 3 - Efficient harvesting of interest rate and credit risk premia

Seminar 3: Harvesting Risk Premia in Alternative Asset Classes and Investment StrategiesDay 1 - Foundations and recent research advances in private equity, hedge funds, real estate and fine artDay 2 - Commodities: Investment narrative and fundamentals of commodity investingDay 3 - Infrastructure: Investment narrative, asset pricing and performance measurement

Seminar 4: Multi-Asset Multi-Manager Products and SolutionsDay 1 - Evidence of predictability in asset, factor and manager returns Day 2 - Global tactical asset allocation strategies

Yale SOM–EDHEC-Risk Synthetic Overview of the Programme Structure

7

Asset Allocation and Investment SolutionsTwo days 26-27 January 2016 in London3-4 February 2016 in New HavenThe aim of this 2-day seminar is to equip participants with practical tools to improve asset allocation and risk management decision processes, and to implement novel investment management approaches.

The first day of the course, led by Professors Justin Murfin and Frank Zhang, is designed to familiarise investors with efficient strategic asset allocation decisions for both institutional and individual portfolios. In the first section of Day 1, participants will explore the fundamentals of asset allocation covering classical mean-variance geometry, risk and return relationships, valuation, diversification, multiple betas, optimisation, as well as risk parity portfolio construction techniques.

During the second section of Day 1, participants will use the tools and insights from the morning session to develop a framework whereby active and passive portfolio strategies can be efficiently combined so as to supplement investors’ exposure to broad market factors. We explore the optimal active portfolio, as well as the trade-offs facing managers choosing active versus passive exposures. Over the course, participants will investigate practical issues in the implementation of portfolio choice.

Day 2 of the seminar, led by Professor Lionel Martellini, has a focus on the efficient use of the three forms of risk management (hedging, diversification and insurance) for the production and distribution of improved investment solutions for asset owners. The seminar will present disciplined approaches to liability-driven investing strategies and goal-based investing strategies, and explain how asset managers may help investors maximise the probability of reaching their objectives subject to dollar and risk budget constraints, with applications in institutional or individual money management.

Seminar Key Learning Objectives:• Learn how to perform factor investing and risk allocation• Develop an understanding of strategic asset allocation in the presence of liability constraints• Assess how to overcome effect of estimation error by imposing better constraints• Understand how to implement liability-driven investment solutions with cash and derivatives instruments• Learn about goal-based investing strategies in institutional and private wealth management• Identify affordability conditions for essential and aspirational goals• Discuss implementation and mass customisation challenges for individual investment solutions• Explore novel welfare-improving forms of investment solutions• Discuss an application to the design of efficient retirement solutions

Harvesting Risk Premia in Equity and Bonds Markets Three days9-11 May 2016 in London18-20 May 2016 in New HavenInvestment portfolios are based on the idea that risk must be taken in order to increase expected returns. However, there are intelligent ways to take risk. Participants will learn about how to use current models and empirical evidence about global capital markets to construct asset portfolios based on the principles of factor investing, with a particular focus on equity and bond markets. The seminar introduces the historical evidence for the existence of “smart beta” portfolios based on equity and fixed-income factors in global markets. The economic rationale behind factor portfolios is explored: Why have they provided higher returns historically? What are the risks the factor portfolios are exposed to and

Yale SOM-EDHEC-Risk Executive Seminar Series

when do they manifest themselves? Will factor risk premia continue in the future? How do factors behave during financial crises? How costly are they to implement? How are factor exposures combined into a portfolio? The behavioural foundations of factor risk premia and portfolio choice are also essential for modern risk managers and portfolio managers to understand, and they will be discussed.

In a first section of the seminar, the focus will be on equity markets. In the face of recent crises, the question of the value added by both active and passive equity managers has been raised with heightened intensity. Academic and industry research has offered convincing empirical evidence that market-cap weighted indices exhibit poor risk-adjusted performance, while other studies have questioned the persistence of positive abnormal performance generated by active managers. The combination of these empirical and theoretical developments has significantly weakened the case for the current equity investment paradigm based on a combination of a passively managed core portfolio and one of several actively managed satellite portfolios. While a new paradigm known as smart beta equity investing has been proposed, the emergence of which blurs the traditional clear-cut split between active and passive equity portfolio management, a host of questions remain regarding the implications with respect to how the equity investment process should be executed by institutional investors and/or asset managers. In this context, this 3-day seminar equips participants with both the technical and conceptual tools that will allow them to better understand the limits and benefits of traditional and alternative equity investing strategies.

A second section of the seminar will give participants the skills necessary to understand how to efficiently harvest risk premia in fixed-income markets, and most notably the interest rate and credit risk factors. More precisely, the seminar will review advanced techniques for interest rates and risk management in bond markets. It will develop insights into different bond portfolio strategies and illustrate how various types of cash and derivative securities can be used to shift the risks associated with investing passively or actively in fixed-income securities. Bond portfolio

optimisation techniques will receive specific attention, as well as their applications in asset-only and asset-liability management contexts.

Seminar Key Learning Objectives:• Appreciate the post-crisis passive-active equity management controversy• Understand the drawbacks of the popular equity strategy that combines a passively managed core portfolio with one of several actively managed satellite portfolios• Find out about the dangers of naively optimised equity portfolios and the benefits of robust optimisation• Discover how to address the challenges in implementing optimised portfolios, in particular, how to manage portfolio liquidity and turnover• Study the limits of traditional equity indices; find out about the minimum-variance benchmark, equally-weighted benchmark, and other forms of benchmarks; evaluate the objectives and assumptions underlying alternative indices and learn about model selection and hidden risks entailed in the choice of a particular benchmark• Develop an understanding of the concepts and tools for evaluating and implementing the new paradigm of equity strategies such as smart beta• Measuring and managing systematic and specific risk of smart beta benchmarks• Discover the many dimensions of putting factor investing into practice through the case-study approach (The Norway Model)• Explore the rational and behavioural foundations of factor risk premia and portfolio choice• Evaluate methods for efficiently harvesting risk premia in equity markets / fixed income markets• Identify and control the various risks associated with a bond portfolio using factor models• Learn how to control portfolio risk using interest rate and credit derivatives• Understand the shortcomings of existing bond benchmarks and learn how a smart bond benchmark can be used as an alternative

8

Harvesting Risk Premia in Alternative Asset Classes and Investment StrategiesThree days27-29 June 2016 in London11-13 July 2016 in New HavenInvestors are increasingly turning to alternative investments to find new ways of increasing the performance and decreasing the risk of their portfolio, in a context where the benefits of diversification within traditional equity and bond portfolios have decreased. Broadly speaking, this seminar shows how to deal with non-Gaussian returns, illiquid assets, and flawed data. It also presents qualitative and quantitative techniques to control asset-class exposures, and manages liquidity, valuation and counterparty risks for portfolio-wide decisions involving alternatives.

The first day of the seminar presents a broad introduction to current academic research into alternative asset classes by one of the world’s leading researchers in the field, and analyses the risks, return drivers and the conditional performance of the various alternative asset classes and strategies. It also includes a discussion of the celebrated Yale model, which suggests that large investors (such as endowments and public pension funds) can achieve superior returns by shifting a significant portion of investments away from traditional stocks and bonds and into carefully selected alternatives In one of the two remaining days, the seminar gives participants a deeper understanding of long-term investment in infrastructure assets, which have become a prominent part of the allocation for a number of large, well-diversified institutional investors. It proposes a bottom-up approach to understand the asset class starting from the financial economics of infrastructure projects and the different instruments used to finance them, to asset pricing and risk models adapted to illiquid, thinly traded assets, and portfolio construction and benchmarking of asset allocations to infrastructure. In another one of the remaining two days, the seminar will examine, in addition to the theoretical foundations, the empirical evidence on risk and return in commodity markets. This will include the perspective of a variety of market participants including investors, hedgers, and asset managers such as CTAs.

Throughout the class the speaker will illustrate how the insights from research have been implemented in the design of commodity benchmarks and the products offered on the market.

Seminar Key Learning Objectives:• Explore the efficacy of an alternatives-based portfolio• Analyse various alternative investment vehicles including real estate, private equity, hedge funds, infrastructure and commodities• Discuss the celebrated Yale model• Understand underlying infrastructure assets and learn about the existing track record of listed and unlisted infrastructure investments solutions• Learn about applicable pricing and risk models for infrastructure project debt and equity investments• Explore the major global trends in commodities trading, production, and demand around the world• Understand the fundamental interconnection between spot and futures markets• Investigate investable commodity indices, the effects of the financialisation of commodity markets, and the influence of speculative capital in the markets

Multi-Asset Multi-Manager Products and SolutionsTwo days 5-6 December 2016 in New Haven12-13 December 2016 in LondonThis seminar has a focus on multi-asset and multi-manager investment products and solutions.

The seminar will begin with a discussion about the predictability of broad asset class returns, particularly equity and fixed income market returns. It will include a discussion about predictability of returns of sectors and styles within the equity market. Finally, the first day of the seminar will also present the methodologies used for identifying the managers who

9

10

are most likely to outperform in the future for situations when the asset allocation strategy is implemented via active mutual fund managers.

The second day of the seminar will discuss the models, techniques and applications of tactical asset allocation strategies as well as factor rotation strategies. It will start with a review of the different types of dynamic asset allocation techniques, the modelling issues involved in building successful asset return prediction models, the risk forecasting techniques used in practice and the portfolio construction issues involved when running an active allocation strategy. It will also review developments in equity factor rotation, volatility, commodity and volatility strategies and use case studies to illustrate the challenges and issues involved in designing, building and implementing tactical asset strategies. The broad focus of this day will be on the application of modern portfolio management principles to bridge the gap between the theory and practice of tactical asset allocation. Seminar Key Learning Objectives:• Learn the evidence on return predictability• Discuss the models, techniques and applications of active multi-asset allocation strategies• Review the methodologies used for identifying mutual fund managers who are most likely to outperform• Learn how to incorporate active views on tactical asset allocation models• Discover recent techniques for factor rotation strategies within and across asset classes• Provide practical application through real-world examples of the techniques introduced during the seminar

11

Faculty

Lionel Martellini, Professor of Finance, EDHEC Business SchoolDirector, EDHEC Risk InstituteSenior Scientific Advisor, ERI Scientific BetaPhD U.C. Berkeley

> Lionel Martellini is a specialist in fixed income modelling, derivatives, asset allocation and retirement solutions. He was previously on the faculty of the Marshall School of Business at the University of Southern California and has also held a visiting position at Princeton University. He has served as a consultant to various institutional investors, investment banks, and asset management firms on questions related to risk management, asset allocation decisions and investment solutions. His research on asset management, portfolio theory, derivatives valuation, fixed income products, and alternative investment has appeared in leading academic and practitioners’ journals. He was awarded the Inquire Europe First Prize in 2009/2010 for his work on dynamic liability-driven investing strategies. He sits on the editorial boards of various journals including the Journal of Alternative Investments and the Journal of Portfolio Management.

James Choi, Professor of Finance, Yale School of ManagementPhD Harvard University

> James Choi is an expert in behavioural finance and household financial decision making. His research includes investigations of the pricing impact of investor sentiment and information asymmetry in the Chinese stock market, household selection of mutual funds, retirement savings choices, the effect of personal experience and peer influence on savings rates, and the effect of the Internet on trading behaviour. He has published in all of the leading academic finance journals and has had his research covered by the New York Times, Wall Street Journal, Financial Times, BusinessWeek, The Economist, Barron’s, Money, MarketWatch, and many other outlets. Professor Choi is a recipient of the TIAA-CREF Paul A. Samuelson Award for outstanding scholarly writing on lifelong financial security. He is a member of the FINRA Investor Issues Committee and a TIAA-CREF Institute Fellow.

Frédéric Blanc-Brude, Director, EDHEC Risk Institute—AsiaPhD King’s College London

> Frédéric Blanc-Brude is in charge of the infrastructure investment research programme at EDHEC-Risk Institute. He is the author of numerous scientific publications on infrastructure economics and investment. His latest book on infrastructure asset valuation was published in March 2015. He also represents EDHEC-Risk Institute on the Advisory Council of the World Bank’s Global Infrastructure Facility (GIF). He is leading a new effort to aggregate cash flow and investment information about private infrastructure investments that will allow better calibration of risk and prudential models and the design of investment benchmarks for investors in infrastructure equity and debt. Prior to joining EDHEC, he worked for ten years in the infrastructure finance sector, and was actively involved in transactions representing a cumulative value of more than USD6bn in Europe, Asia and the Middle East. He holds a PhD in Finance from King’s College London, an MSc in Political Theory from the London School of Economics, a Master in Economics from the Sorbonne University, and is a graduate of the Paris Institute of Political Studies (Sciences Po).

Will Goetzmann, Edwin J. Beinecke Professor of Finance and Management Studies, Director of the International Center for Finance, Yale School of ManagementPhD Yale University

> William N. Goetzmann is an expert on a diverse range of investments, including stocks, mutual funds, real estate, and paintings. His research topics include forecasting stock markets, selecting mutual fund managers, housing as investment, and the risk and return of art. Professor Goetzmann’s work has been featured in The Wall Street Journal, The New York Times, Business Week, The Economist, Forbes, and Art and Auction. Professor Goetzmann has a background in arts and media management. As a documentary filmmaker, he has written and coproduced programmes for Nova and the American Masters series, including a profile of artist Thomas Eakins. A former director of Denver’s Museum of Western Art, Professor Goetzmann co-authored The Origins of Value: The Financial Innovations that Created Modern Capital Markets.

Justin Murfin, Associate Professor of Finance, Yale School of ManagementPhD Duke University

> Professor’s Murfin research interests include banking, financial intermediation and financial contracting. His current work is focused on how the allocation of control rights in loan contracts varies based on lenders’ recent experience. Prior to Yale SOM, he worked for Barclays Capital in New York, Miami and Bogotá, Colombia, as well as the Federal Reserve Bank of Dallas.

12

13

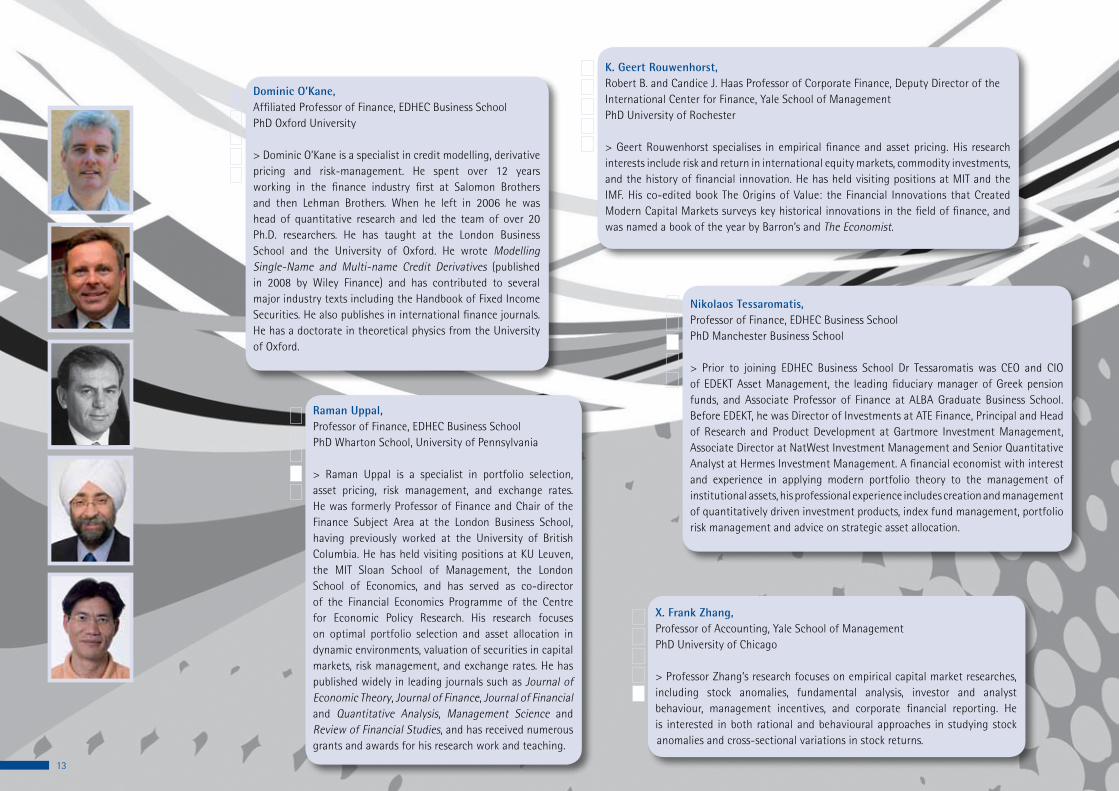

Raman Uppal, Professor of Finance, EDHEC Business SchoolPhD Wharton School, University of Pennsylvania

> Raman Uppal is a specialist in portfolio selection, asset pricing, risk management, and exchange rates. He was formerly Professor of Finance and Chair of the Finance Subject Area at the London Business School, having previously worked at the University of British Columbia. He has held visiting positions at KU Leuven, the MIT Sloan School of Management, the London School of Economics, and has served as co-director of the Financial Economics Programme of the Centre for Economic Policy Research. His research focuses on optimal portfolio selection and asset allocation in dynamic environments, valuation of securities in capital markets, risk management, and exchange rates. He has published widely in leading journals such as Journal of Economic Theory, Journal of Finance, Journal of Financial and Quantitative Analysis, Management Science and Review of Financial Studies, and has received numerous grants and awards for his research work and teaching.

Dominic O’Kane, Affiliated Professor of Finance, EDHEC Business SchoolPhD Oxford University

> Dominic O’Kane is a specialist in credit modelling, derivative pricing and risk-management. He spent over 12 years working in the finance industry first at Salomon Brothers and then Lehman Brothers. When he left in 2006 he was head of quantitative research and led the team of over 20 Ph.D. researchers. He has taught at the London Business School and the University of Oxford. He wrote Modelling Single-Name and Multi-name Credit Derivatives (published in 2008 by Wiley Finance) and has contributed to several major industry texts including the Handbook of Fixed Income Securities. He also publishes in international finance journals. He has a doctorate in theoretical physics from the University of Oxford.

K. Geert Rouwenhorst, Robert B. and Candice J. Haas Professor of Corporate Finance, Deputy Director of the International Center for Finance, Yale School of ManagementPhD University of Rochester

> Geert Rouwenhorst specialises in empirical finance and asset pricing. His research interests include risk and return in international equity markets, commodity investments, and the history of financial innovation. He has held visiting positions at MIT and the IMF. His co-edited book The Origins of Value: the Financial Innovations that Created Modern Capital Markets surveys key historical innovations in the field of finance, and was named a book of the year by Barron’s and The Economist.

Nikolaos Tessaromatis, Professor of Finance, EDHEC Business SchoolPhD Manchester Business School

> Prior to joining EDHEC Business School Dr Tessaromatis was CEO and CIO of EDEKT Asset Management, the leading fiduciary manager of Greek pension funds, and Associate Professor of Finance at ALBA Graduate Business School. Before EDEKT, he was Director of Investments at ATE Finance, Principal and Head of Research and Product Development at Gartmore Investment Management, Associate Director at NatWest Investment Management and Senior Quantitative Analyst at Hermes Investment Management. A financial economist with interest and experience in applying modern portfolio theory to the management of institutional assets, his professional experience includes creation and management of quantitatively driven investment products, index fund management, portfolio risk management and advice on strategic asset allocation.

X. Frank Zhang, Professor of Accounting, Yale School of ManagementPhD University of Chicago

> Professor Zhang’s research focuses on empirical capital market researches, including stock anomalies, fundamental analysis, investor and analyst behaviour, management incentives, and corporate financial reporting. He is interested in both rational and behavioural approaches in studying stock anomalies and cross-sectional variations in stock returns.

14

Who Should AttendThe seminar series are intended for senior officers, investment specialists and administrators working for buy- and sell-side institutions, and for consultants and key account representatives advising high net worth individuals and institutional investors.

ScheduleA typical programme day lasts from 9:00 am to 5:00 pm and is usually divided into lectures andapplication cases. The two class sessions in each half-day period are separated by 30 minuterefreshment breaks. Lunch is included.

Fees, Further Information & RegistrationLocationLondon and/or New Haven

FeesFor a 2-day seminarStandard rate: USD 4,000/EUR 3,500

Group discounts available.For London seminars: VAT at a rate of 20% will be applied.

Fees for the Certificate Seminar SeriesRegistrants for the Certificate Seminar Series will benefit from a 15% discount on the total cost of the programme. Fees include instruction, documentation, refreshments at breaks, and lunch.Accommodation is not included.

Further information and registrationPlease contact: Caroline Prévost, EDHEC-Risk Institute at: [email protected] or on: +33 493 183 496David Pramer, Yale School of Management at: [email protected] or on: +1 203 432 6268

Continuing Professional Education Credits

15

EDHEC-Risk Institute is registered with CFA Institute as an Approved Provider of continuing education programs

EDHEC-Risk Institute is registered with GARP as an Approved Provider of continuing professional education credits for FRMs and ERPs.

For a 3-day seminarStandard rate: USD 6,000/EUR 5,200

16

Institute

Founded in 1906, EDHEC Business School offers management education at undergraduate, graduate, post-graduate and executive levels. Holding the AACSB, AMBA and EQUIS accreditations and regularly ranked among Europe’s leading institutions, EDHEC Business School delivers degree courses to over 6,500 students from the world over and trains 10,000 professionals yearly through executive courses and research events. The School’s ‘Research for Business’ policy focuses on issues that correspond to genuine industry and community expectations.

Part of EDHEC Business School and established in 2001, EDHEC-Risk Institute has become the premier academic centre for industry-relevant financial research. In partnership with large financial institutions, its team of close to 50 permanent professors, engineers, and support staff, and 36 research associates and affiliate professors, implements six research programmes and 10 research chairs focusing on asset allocation and risk management and has developed an ambitious portfolio of research and educational initiatives in the domain of investment solutions for institutional and individual investors. EDHEC-Risk Institute also has highly significant executive education activities for professionals. In partnership with CFA Institute, it has developed advanced seminars based on its research which are available to CFA charterholders and have been taking place since 2008 in New York, Singapore and London.

In 2012, EDHEC-Risk Institute signed two strategic partnership agreements, with the Operations Research and Financial Engineering department of Princeton University to set up a joint research programme in the area of asset-liability management for institutions and individuals, and with Yale School of Management to set up joint certified executive training courses in North America and Europe in the area of risk and investment management.

Yale University, founded in 1701, is one of the world’s great universities, attracting students from 108 countries. The mission of the Yale School of Management is to educate leaders for business and society. We are committed to understanding the complex forces transforming global markets and using that understanding to build organisations—in the for-profit, nonprofit, entrepreneurial, and government sectors—that contribute lasting value to society.

We aspire to be the most global among U.S. business schools, reaching the fast-growing frontiers of the global economy. Yale SOM led the effort to convene the Global Network for Advanced Management, which includes 22 top business schools throughout the world in 2012.

In the area of finance, with a world-renown faculty of scholars and practitioners, our International Center for Finance is a research nexus in financial economics. The Center’s fellowship is comprised of leading researchers both inside and outside of the Yale School of Management who work on key empirical and theoretical problems in financial economics, including asset pricing, corporate finance, investment management, market microstructure, behavioural finance, fixed income and derivatives, international financial markets, law and finance, and the history of financial markets.

Yale’s Executive Education initiatives focus on creating customised, transformational experiences for managers and executives from around the world. Yale takes special pride in crafting and delivering unique educational opportunities that feature access to the top minds in business—whether leading academic experts or practitioners who lead thriving organisations. We are delighted to join forces with EDHEC-Risk Institute to offer an extraordinary opportunity for executive education in specialty areas of finance and risk management.

About the Organisers

Institute

EDHEC-Risk Institute393 promenade des AnglaisBP 3116 - 06202 Nice Cedex 3FranceTel: +33 (0)4 93 18 78 24

EDHEC Risk Institute—Europe 10 Fleet Place, LudgateLondon EC4M 7RBUnited KingdomTel: +44 207 871 6740

EDHEC Risk Institute—Asia1 George Street#07-02Singapore 049145Tel: +65 6438 0030

EDHEC Risk Institute—North AmericaOne Boston Place, 201 Washington StreetSuite 2608/2640, Boston, MA 02108United States of AmericaTel: +1 857 239 8891

EDHEC Risk Institute—France 16-18 rue du 4 septembre75002 Paris FranceTel: +33 (0)1 53 32 76 30

www.edhec-risk.com

Yale School of Management165 Whitney AvenueNew Haven, CT 06511-3729Tel.: +1 203.432.5932