wpg resources limited whatsoever on the part of this firm or any member or employee thereof. ......

TRANSCRIPT

Research Note

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 1

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

WPG RESOURCES LIMITED

EMERGING GOLD PRODUCER: UP FOR THE CHALLENGE

Investment Highlights

WPG Resources Ltd (WPG) has been rapidly transformed into an emerging gold producer through its recent acquisition of the Challenger Gold mine. The Company is targeting at least 50kozpa of gold production from the mine and a further 20kozpa of supplemental ore from its satellite Tarcoola deposit. Based on the existing Challenger Mineral Resource estimate of 277koz of gold, we see the potential for an initial 3.5 year mine life with a number of growth opportunities close, and lateral, to existing development. Our modelling suggests the potential for WPG to generate $14.6m in free cash in FY17, $37.3m in FY18 and $42.7m in FY19. The Company will likely use some of this cash to explore new opportunities as well as look to develop its large Tunkillia gold project. WPG has a solid team of mining professionals with a broad range of mining experience who have a proven track record of success. We are initiating coverage of WPG with a Speculative Buy rating and target price of $0.15/sh.

Building an Emerging Gold Producer: WPG recently acquired 100% of

the Challenger gold mine through purchasing the remaining 50% from PYBAR for $9m. WPG has re-published an updated Mineral Resource of 945kt at 9.11g/t Au for 277koz gold and has provided FY17 guidance of 50koz of production from Challenger. In addition, the Company recently published an updated feasibility study for the development of the Tarcoola gold project, which has the potential to add output of 20kozpa. Mining is expected to commence towards the end of 2016 with the ore from Tarcoola to be processed over 3 years at Challenger which is located some 165km away by road.

Backing the Team: The WPG team has a successful track record of

delivering for shareholders. The Company is led by Martin Jacobsen as Managing Director/CEO who has extensive gold experience. Bob Duffin is Executive Chairman and has 40 years’ experience in mining. The most significant return for the Company was in 2011 when the Company sold its South Australian iron ore assets for $320m. The majority of the sale value was returned to shareholders.

Valuation $0.15/sh: We have determined a Net Asset Value (NAV) for

WPG of $0.15/sh. We have assumed that WPG produces c.54koz of gold in FY17. All-In-Sustaining Costs are estimated at $1,360/oz for FY17 falling to c.$1,100/oz by FY19 which is partially due to accessing higher grade areas. There is potential to extend mine life through accessing Challenger Deeps to which WPG has secured 100% of the rights.

14 October 2016

12mth Rating SPECULATIVE BUY

Price A$ 0.080

Target Price A$ 0.15

12mth Total Return % 82.5

RIC: WPG.AX BBG: WPG AU

Shares o/s m 686.3

Free Float % 81.8

Market Cap. A$m 54.9

Net Debt (Cash) A$m -4.0

Net Debt/Equity % na

3mth Av. D. T’over A$m 0.14

52wk High/Low A$ 0.11/0.02

2yr adj. beta 0.27

Valuation:

Methodology DCF

Value per share A$ 0.15

Analyst: Simon Tonkin

Phone: (08) 9225 2816

Email: [email protected]

12 Month Share Price Performance

Performance % 1mth 3mth 12mth

Absolute 0.0

17.1

165.4 Rel. S&P/ASX 300 -4.9 7.0

126.5

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 2

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

INVESTMENT SUMMARY

We are initiating coverage of WPG Resources Ltd (WPG) with a Speculative Buy rating and target price of $0.15/sh. The Company has been rapidly transformed into an emerging gold producer through its recent

acquisition of the Challenger gold mine. WPG aims to produce at least 50kozpa of gold from Challenger and is targeting a further 20kozpa from its satellite Tarcoola deposit. Based on the existing Challenger Mineral Resource estimate of 277koz, we see the potential for an initial 3.5 year mine life with a number of growth opportunities close, and lateral, to existing development. We calculate, based on the expected mining costs of $1,300/oz, the potential for a c.$400-500/oz margin which equates to c.$15m in free cash flow in FY17. WPG has a solid team of mining professionals with a broad range of mining experience with a proven track record of success.

Building an Emerging Gold Producer: WPG recently acquired 100% of the Challenger gold mine by

acquiring the remaining 50% from PYBAR for $9m. Previously, in March 2016, WPG and PYBAR formed a 50/50 JV to acquire the Challenger gold mine from Kingsgate Consolidated (KCN) for $1m, which included $2.7m in environmental bonds. Overall, the opportunistic acquisition provides a significant opportunity for WPG to emerge as a mid-tier gold producer. In May 2016, the Company re-hired many of the previous Challenger employees and re-negotiated key mine services contacts with the aim of re-commissioning the mine. The new team achieved its first gold pour under the JV at the end of May and produced 3.4koz in the June 2016 Q. We anticipate that WPG will produce c.12-13koz in the September 2016 Q. The mine has produced in excess of 1Moz since commencing production in 2002. Our recent site visit revealed that there is remaining ore on the Run of Mine (ROM) pad and production stopes are established. There is also a significant amount of light vehicles, spares and equipment on-site.

Good Potential for a 3 year Mine Life: In May 2016, WPG republished an updated Mineral Resource

estimate for Challenger of 945kt at 9.11g/t Au for 277koz gold. The Company has provided FY17 production guidance of c.50koz and aims to develop its 100% owned Tarcoola deposit which could add a further 20kozpa. Therefore, we see the potential for WPG to achieve 60-80kozpa of gold production over the next 2-3 years at an estimated All-In-Sustaining Costs (AISC) of c.$1,360/oz.

Exploration Upside: There appears to be significant potential to extend the mine life at Challenger. Laterally

there are a number of opportunities close to existing development with further drilling required. At Challenger south-southwest (SSW) an intercept of 0.2m at 368g/t Au has been reported, with previous drilling identifying additional intercepts on multiple levels which could suggest an additional structure. WPG plans to do sufficient drilling to systematically define new mining areas in advance of expected mining. Challenger Deeps also represents a significant opportunity with the extension of the rich M1/M2 ore shoots; however, this will depend on the prevailing gold price as the decline is at a depth of more than 1km below surface. WPG recently resolved a dispute with Tyranna Resources Limited (TYX) which allowed the Company to secure 100% of the rights for the Challenger Deeps area.

Tarcoola Satellite Operation to Add c.20kozpa: WPG plans to establish a satellite open pit operation at

Tarcoola, which is located some 100km to the southeast of Challenger. The Company recently updated its feasibility study on Tarcoola with capital costs falling to $4m (from $16.7m) by utilising its Challenger processing plant. The Company plans to mine the 710kt at 3.1g/t Au for 71koz via open pit over two years and then process the ore at Challenger over three and a half years. The Company plans to commence mining at Tarcoola by the end of 2016.

Other Opportunities: Once WPG has generated sufficient cash from Challenger/Tarcoola it could look to

use the capital to develop the Tunkillia project, which has a significant Mineral Resource estimate of 12.32Mt at 1.41g/t Au for 558koz. Furthermore, WPG has a joint venture with Tyranna Resources (TYX) whereby the Company has returned some interesting gold results. Any discovery could potentially be processed through the Challenger plant.

Backing the Team: The WPG team has a broad range of mining experience and has a proven track record

of success. The Company is led by Martin Jacobsen as Managing Director/CEO who has extensive gold experience and has previously worked for Golden China Resources and Emperor Mines. Bob Duffin (Executive Chairman) has 40 years’ experience in mining and has held senior positions within the exploration divisions of Peko Wallsend Ltd and MIM Holdings. Cornel Parshotam was recently appointed Chief Operating Officer and is a mining professional with over 36 years of leadership and operational experience in the minerals industry, including as Head of Operations at BHP Billiton’s Olympic Dam mine in South Australia. He was also Acting Operations Manager at Emperor Mines in Fiji and General Manager Operations at Metallon Gold in Zimbabwe, which at the time was the largest gold producer in Zimbabwe. Gary Jones (Technical Director) is a geologist with over 45 years professional experience in mineral exploration and resource and reserve estimation for various types of mineral deposits including porphyry copper-gold and epithermal gold. Wayne Rossiter (Chief Financial Officer) is both a mining engineer and a chartered accountant he has held senior finance and management roles in resource and energy companies including Clean Global Energy, Core Mining, Sino Gold Mining, Cockatoo Coal, Roc Oil and Novus Petroleum.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 3

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

VALUATION

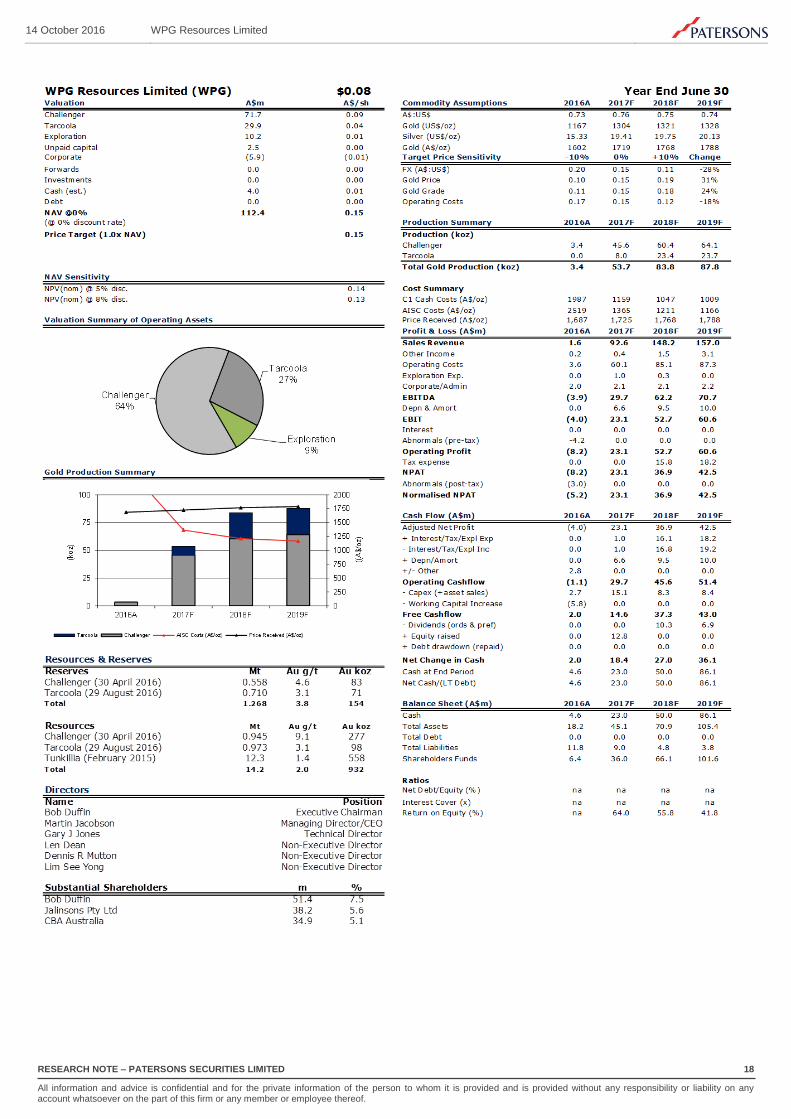

We have determined a Net Asset Value (NAV) for WPG of $0.15/sh. Our valuation is based on a discounted cashflow model for the Challenger gold mine and Tarcoola satellite open pit. For Challenger, we have assumed a three year mine life processing 1.5Mt at 4.7g/t Au for 229koz, which is based on an 80% conversion of contained gold from Mineral Resources (945kt at 9.11g/t Au for 277koz gold) to Ore Reserves. The grade used equates to the achieved average over the past 5 years. Following our recent site visit, we believe this is feasible given that there are a number of lateral development opportunities within the mine. We expect lower grades in FY17, as WPG is processing some stockpiled ore from the ROM pad (c.1.3g/t Au) and previous owner KCN has already exploited some of the higher grade areas within the immediate stopes. As WPG continues to mine, it will look to develop into higher grade ore, which, in turn, will increase production and lower the overall cost per ounce. We estimate production of 45.6koz of gold from Challenger in FY17, which increases to 60.4koz in FY18 and 64.1koz in FY19. All-In-Sustaining costs are expected to drop from $1,360/oz in FY17 to $1,100/oz in FY19.

At Tarcoola, which is expected to average 20kozpa, we have based our model on the information provided in the updated feasibility study which was released on the 1 September 2016. The Tarcoola project has an Ore Reserve estimate of 710kt at 3.1g/t Au for 71koz. WPG plans to truck ore mined from the Tarcoola open pit to the Challenger processing plant, which is located some 165km away by road. Mining will be conducted over a two year period with processing at Challenger over a three and a half year period. Significantly, due to WPG’s opportunistic purchase of the Challenger gold mine, the capital cost for Tarcoola reduces from $16.5m to $4m. The estimated average All-In-Sustaining cost is $916/oz. Project development is expected to occur in the December Q 2016 and we have assumed that 8koz of gold will be produced from Tarcoola in FY17.

We have assumed the value of exploration assets at $10.2m, which is based on 10% of our value for Challenger and Tarcoola. We believe this is reasonable given that WPG has been able to secure 100% of Challenger Deeps and there are further mine opportunities identified.

Figure 1: WPG Net Asset Valuation (NAV)

Source: Patersons Securities Ltd

Valuat io n A $ m A $ / sh

Challenger 71.7 0.09

Tarcoola 29.9 0.04

Exploration 10.2 0.01

Unpaid capital 2.5 0.00

Corporate (5.9) (0.01)

Forwards 0.0 0.00

Investments 0.0 0.00

Cash (est.) 4.0 0.01

Debt 0.0 0.00

N A V @0% 112.4 0.15

(@ 0% discount rate)

P rice T arget (1.0x N A V) 0.15

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 4

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

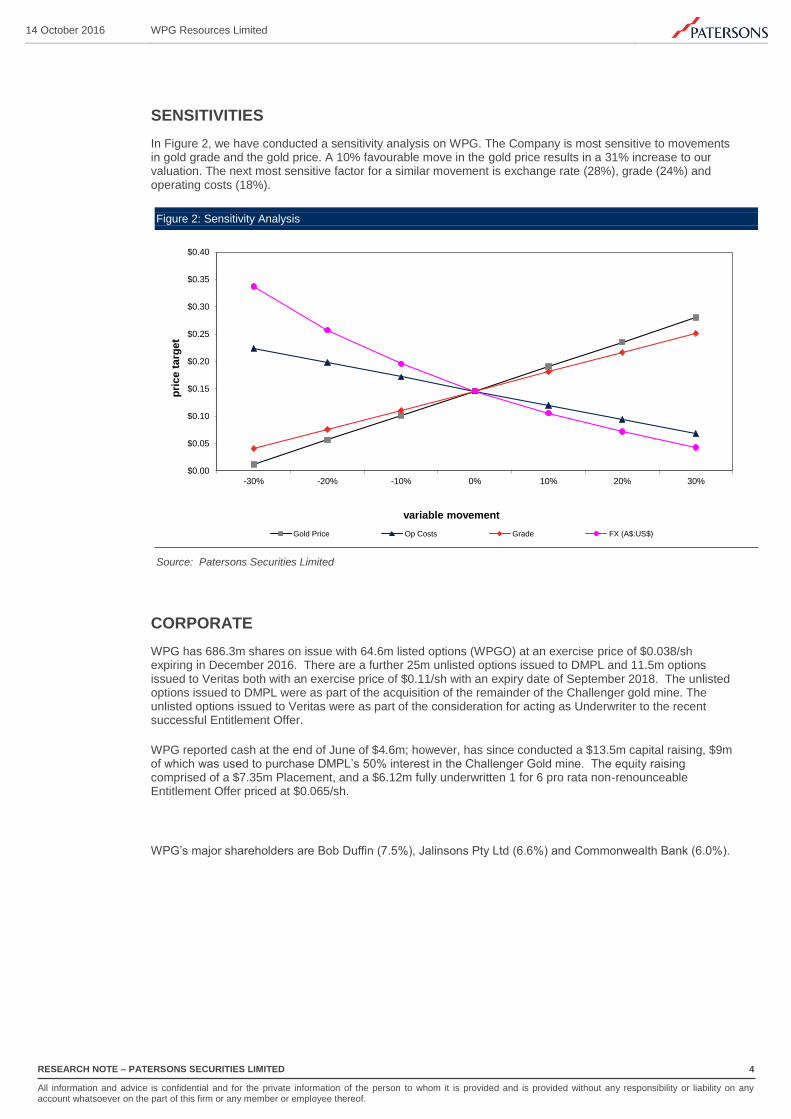

SENSITIVITIES

In Figure 2, we have conducted a sensitivity analysis on WPG. The Company is most sensitive to movements in gold grade and the gold price. A 10% favourable move in the gold price results in a 31% increase to our valuation. The next most sensitive factor for a similar movement is exchange rate (28%), grade (24%) and operating costs (18%).

Figure 2: Sensitivity Analysis

Source: Patersons Securities Limited

CORPORATE

WPG has 686.3m shares on issue with 64.6m listed options (WPGO) at an exercise price of $0.038/sh expiring in December 2016. There are a further 25m unlisted options issued to DMPL and 11.5m options issued to Veritas both with an exercise price of $0.11/sh with an expiry date of September 2018. The unlisted options issued to DMPL were as part of the acquisition of the remainder of the Challenger gold mine. The unlisted options issued to Veritas were as part of the consideration for acting as Underwriter to the recent successful Entitlement Offer.

WPG reported cash at the end of June of $4.6m; however, has since conducted a $13.5m capital raising, $9m of which was used to purchase DMPL’s 50% interest in the Challenger Gold mine. The equity raising comprised of a $7.35m Placement, and a $6.12m fully underwritten 1 for 6 pro rata non-renounceable Entitlement Offer priced at $0.065/sh.

WPG’s major shareholders are Bob Duffin (7.5%), Jalinsons Pty Ltd (6.6%) and Commonwealth Bank (6.0%).

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

-30% -20% -10% 0% 10% 20% 30%

pri

ce t

arg

et

variable movement

Gold Price Op Costs Grade FX (A$:US$)

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 5

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

ASSET SUMMARY

WPG is focused on gold assets in South Australia (Figure 3). The acquisition of the Challenger gold mine has transformed the Company into a gold producer targeting at least 50kozpa. In addition, the acquisition has provided some synergies with significant cost savings for the development of the Tarcoola deposit. This was outlined in the recent feasibility study which showed upfront capital cost savings of c$13m by utilising the Challenger mill for processing. This provides the opportunity for WPG to produce c.60-80kozpa of gold, which would place the Company into the ranks of the mid-tier gold miners. At Tunkillia, WPG has defined a significant lower grade resource of 12.32Mt at 1.41g/t Au for 558koz. The Company could use some of the cash flow generated from Challenger/Tarcoola to look at developing Tunkillia.

Figure 3: WPG Assets

Source: WPG Resources Ltd

Challenger Gold Mine (WPG 100%)

The Challenger gold mine has been in operation under various owners since April 2002 and has produced 1.1Moz of gold to date. It is located 730km northwest of Adelaide, 150km southwest of Coober Pedy and 130km northwest of WPG’s Tarcoola gold project. Site infrastructure, covering approximately 3km

2 of a

Mineral Lease area of 13.2km2, is located on the Mobella Pastoral Station, within the Woomera Prohibited

Area and consists of underground development and services, a crushing and processing Carbon-in-Pulp (CIP) plant and accommodation village. Employees and contractors fly in and out of site from Adelaide utilising the established airstrip.

Background

Challenger was a virgin gold discovery made by a Joint Venture between Resolute Resources and Dominion Gold Operations Pty Ltd in 1995. Dominion carried out a Bankable Feasibility Study, and proceeded with construction in September 2001. The Challenger open pit commenced in mid-2002 and plant and infrastructure was completed during the September 2002 Q, with the first shipment of gold bullion completed on 24 October 2002. Underground development commenced in February 2004 and full-scale underground production began mid-2005. The pouring of the one millionth ounce of gold at Challenger was celebrated in November 2014.

In 2013, a revised mine plan was developed, with a focus on the Challenger West underground orebody. The Challenger West orebody remains the focus of near-term mining operations.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 6

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

In Figure 4, we show production results from the Challenger gold mine from 2011-2015. We note that production has averaged over 80kozpa at an average grade of 4.6g/t Au. WPG plans to reduce the production rate to 50-60kozpa and lower the mining dilution through using smaller mining equipment.

Figure 4: Challenger Production 2011-2015 (Under Kingsgate Consolidated)

Source: WPG Resources Ltd

Geology

The Challenger deposit is located within portions of Christie gneiss, a member of the Mulgathing Complex that forms part of the Gawler Craton, a large crystalline basement province consisting of late Archaean to Mesoproterozic rocks. The deposit occurs within quartz-feldspar-biotite ± garnet-cordierite gneiss, a variation of Christie gneiss.

The host to gold mineralisation is a silica and feldspar rich greisenised pegmatite. These veins are typically ptygmatically folded. The deposit is typically shear hosted with the morphology of the mineralised envelope being lensoid in three dimensions and anastomosing in character.

Coarse visible gold of variable size, and in association with sulphide mineralisation, is a common feature of the higher grade ore zones. Gold grains contain inclusions of arsenopyrite, pyritised pyrrhotite and native bismuth.

All lodes remain open at depth and historical drilling of the M1 lode has demonstrated the continuity of the orebody to at least 2.8km down-plunge. Both primary host rock and the quartz, feldspar, garnet veins associated with gold mineralisation are generally competent, necessitating minimal ground support. Underground conditions are effectively dry, with little groundwater inflow into the mine.

0

1

2

3

4

5

6

0

20

40

60

80

100

120

2011 2012 2013 2014 2015

Gra

de

(g/

t)

Go

ld P

rod

uct

ion

(ko

z)

Gold (koz) Head Grade (g/t)

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 7

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Mineral Resources

In May 2016, WPG completed an updated Mineral Resource estimate (Figure 5). The update was based on the interpretation of the geology and gold bearing lode structures that have been developed as a continually evolving model by hands-on experienced site geologists before and since the commencement of mining in 2002. The current interpretation is based on a combination of drill results, face sampling and geological mapping of development headings. Historically, Resources at Challenger have continued to expand through further drilling and resource optimisation.

Figure 5: Challenger Mineral Resource

Source: WPG Resources Ltd

Due to the complex nature of the lode zones, the resource has been estimated using a combination of geological grade calculations, generic modelling and block modelling. There is a high nugget effect in the Challenger deposit and significant visible gold and therefore various top cuts are applied to the grade calculations. The cut-off grade used in the estimate is 5.0g/t Au for all of the lodes and is based on what is considered an economic cut-off for underground mining in relation to the prevailing gold price and projected operating costs.

Mining factors taken into consideration for the resource estimate are that the mineralisation will continue to be mined using a combination of up-hole retreat stoping utilising rib pillars and a minor number of downhole long hole bench stopes. Metallurgical factors taken into consideration for the resource estimate are that the mined ore will continue to be processed through the Challenger CIP plant.

Challenger Deeps also represents a significant opportunity, with the extension of the rich M1/M2 ore shoots, However, this will depend on the prevailing gold price as they are at a depth of more than 1km below surface (Figure 6). WPG recently resolved a dispute with TYX, which allowed the Company to secure 100% of the rights for the Challenger Deeps area.

Figure 6: Challenger Long Section

Source: WPG Resources Ltd

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 8

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

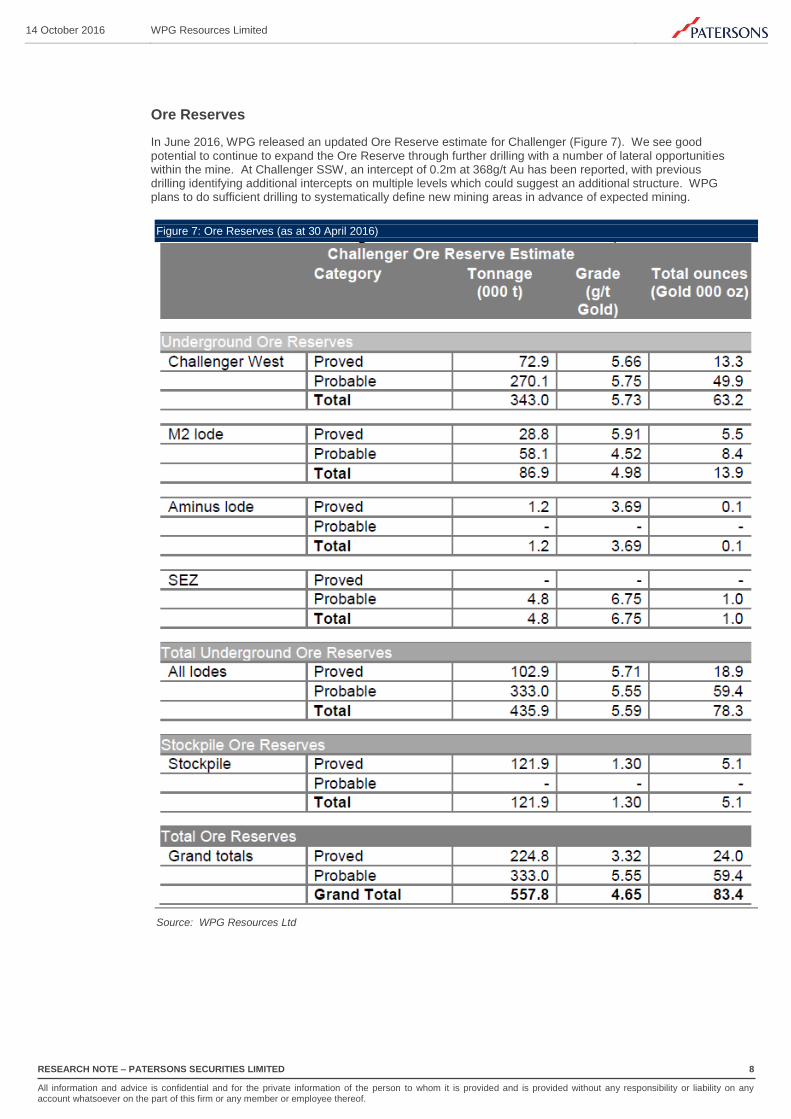

Ore Reserves

In June 2016, WPG released an updated Ore Reserve estimate for Challenger (Figure 7). We see good potential to continue to expand the Ore Reserve through further drilling with a number of lateral opportunities within the mine. At Challenger SSW, an intercept of 0.2m at 368g/t Au has been reported, with previous drilling identifying additional intercepts on multiple levels which could suggest an additional structure. WPG plans to do sufficient drilling to systematically define new mining areas in advance of expected mining.

Figure 7: Ore Reserves (as at 30 April 2016)

Source: WPG Resources Ltd

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 9

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Operation/Infrastructure

The existing infrastructure at the Challenger mine includes the Challenger Open Pit, Challenger West Open Pit, SEZ Open Pit, underground mine, crusher circuit, processing plant, process water pond, airstrip, production borefield, Integrated Waste Landform (IWL) Tailings Storage Facility, RO plant, underground and open pit mining contractor workshops, hazardous goods storage facility, magazine, Power Station 1 & 2, vent rise, fuel farm, bioremediation facility, evaporation ponds, exploration and main camps, site laboratory, administrative buildings, airstrip, Emergency Response Team (ERT) training area and laydown areas.

The Challenger Open Pit was developed to a depth of 125m below surface level and the SEZ Open Pit was excavated to a depth of 60m. Development of underground mining operations commenced in February 2004. A portal near the base of the existing Challenger Open Pit is used as an access point for the underground operations. The ‘Jumbuck’ decline has been developed down to 1,064m below surface. A ventilation shaft was sunk (4.5m diameter, 730m depth) in February 2010.

The processing plant comprises a jaw crusher supplemented by a cone crusher, two ball mills, a gravity circuit to recover coarse gold, cyanidation leaching and adsorption circuit and conventional elution and electrowinning to produce gold bullion. In January 2010, the plant was upgraded with a secondary ball mill and thickener installed to increase throughput from 430ktpa to 650ktpa. It is located approximately 1km southeast of the Challenger Open Pit and utilises a CIP process for the extraction of gold.

The underground mining method used at Challenger is up-hole retreat, mined from sub-levels 20m apart. All stopes are accessed through drives (varying in size from 4.5 x 4.0m to 5m x orebody width) developed from the main 5.0 x 5.0m Jumbuck decline (which increases in size at depth to 5.3 x 5.8m to facilitate appropriate ventilation airflow).

Figure 8: Aerial View of the Challenger Operations

Source: WPG Resources Ltd

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 10

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Western Gawler Craton Joint Venture (WGCJV – WPG 34%; TYX 66%)

The Western Gawler Craton Joint Venture (WGCJV) holds exploration tenements in the region of WPG’s Challenger gold mine in South Australia. The current interests in the Joint Venture are TYX owns approximately 66% and WPG 34%. WPG holds its interest through its 100% owned subsidiary Challenger Gold Operations Pty Ltd (CGO). TYX is manager of the WGCJV.

In October 2016, WPG and TYX resolved a dispute over the ownership of the tenements. Under the binding term sheet, which has been signed by the parties, TYX has agreed to drop its claim that the northern part of EL 5661 that surrounds the Challenger mine and the recently granted ML 6457 form part of the WGCJV. The Challenger mine lies on ML 6103 which abuts ML 6457. In return, WPG has agreed that ownership of the tenements subject to the WGCJV will be transferred to TYX and its subsidiary Half Moon Pty Ltd (HMP) and that a new gold exploration joint venture will be formed between WPG and TYX and their subsidiaries. The interests of the two parties in the new joint venture will be exactly the same as under the old joint venture, and there will be no change to the dilution provisions. As with the old joint venture, TYX will be manager of the new joint venture.

WPG and TYX each hold mining or exploration tenements near Challenger in their own right, as well as the tenements that are part of the WGCJV. In addition, a third party holds a carried interest in a small area of the WGCJV tenement package. A number of the tenements are also subject to rights to specific minerals held by other parties. TYX has made several early stage discoveries within the region including Greenwood, Mainwood, Campfire Bore and Golf Bore. Given that the Challenger plant is located in close proximity, there is potential for WPG to toll treat the ore.

Figure 9 shows the tenements that will be included in the new joint venture in blue and green (WGCJV tenure), and the tenements held by CGO and not included in the joint venture in pink (the CGO tenure).

Figure 9: WGCJV Tenements in Relation to the Challenger Mineral Leases

Source: WPG Resources Ltd

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 11

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Tarcoola Gold Project (WPG 100%)

WPG aims to commence the development of the Tarcoola gold project before the end of the year. It is expected to supply c.20kozpa of gold to the Challenger plant. The project is 165km by road to the Challenger mine and approximately 190km south of Coober Pedy and 600km northwest of Adelaide. It is approximately 3km west of the largely abandoned Tarcoola township, adjacent to the Trans-Australian and Central Australian railway lines, and has excellent existing infrastructure and communications facilities.

The first alluvial gold was discovered in the Tarcoola area in 1893. The area has reportedly produced c.77koz of gold at an average grade of ~37.5g/t Au, most of which was mined prior to the 1940’s. The goldfield has been dormant for many years and has historically suffered from fragmented ownership. There are many old but shallow workings within the Mineral Lease (ML) area and the greater exploration tenement (EL 5355). There is excellent potential to identify additional open-pittable deposits to add to the mine life.

Figure 10: Tarcoola gold project Location

Source: WPG Resources Ltd

The project is located on Crown Reserve land and Native Title is held by the Antakirinja Matu-Yankunytjatjara people represented by the Antakirinja Matu-Yankunytjatjara Aboriginal Corporation (AMYAC). A Native Title Mining Agreement is in place with AMYAC. Given the Tarcoola goldfield’s importance to the evolution of South Australia’s history, there are a number of areas within the ML which have been confirmed as a State Heritage Place in the SA Heritage Register. Proposed mining activities are not expected to impact on any heritage areas, whose ongoing preservation will be ensured by the State Heritage Unit.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 12

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Ore Reserves

The total Ore Reserve estimate of 710kt at an average grade of 3.1g/t Au containing 71koz, is a revision to the September 2015 estimate. The main difference is that ore will be trucked to Challenger for processing by carbon in pulp (CIP) rather than processing on site by heap leaching. The reserves are defined at the point where the ore is delivered to the processing plant. Compared to the September 2015 Ore Reserves estimate the CIP processing method;

• Marginally reduced the ore tonnes and increased the cut-off grade due to the increased trucking and ore processing costs,

• Marginally decreased estimated contained gold, but • Increased estimated recovered gold as the CIP gold recovery is expected to be significantly higher than

the heap leach recovery and this will more than compensate for the reduction in ore tonnes and contained gold.

The project remains a small to medium sized open pit gold mine with ore trucked 165km to the Challenger mine for processing.

Updated Feasibility Study

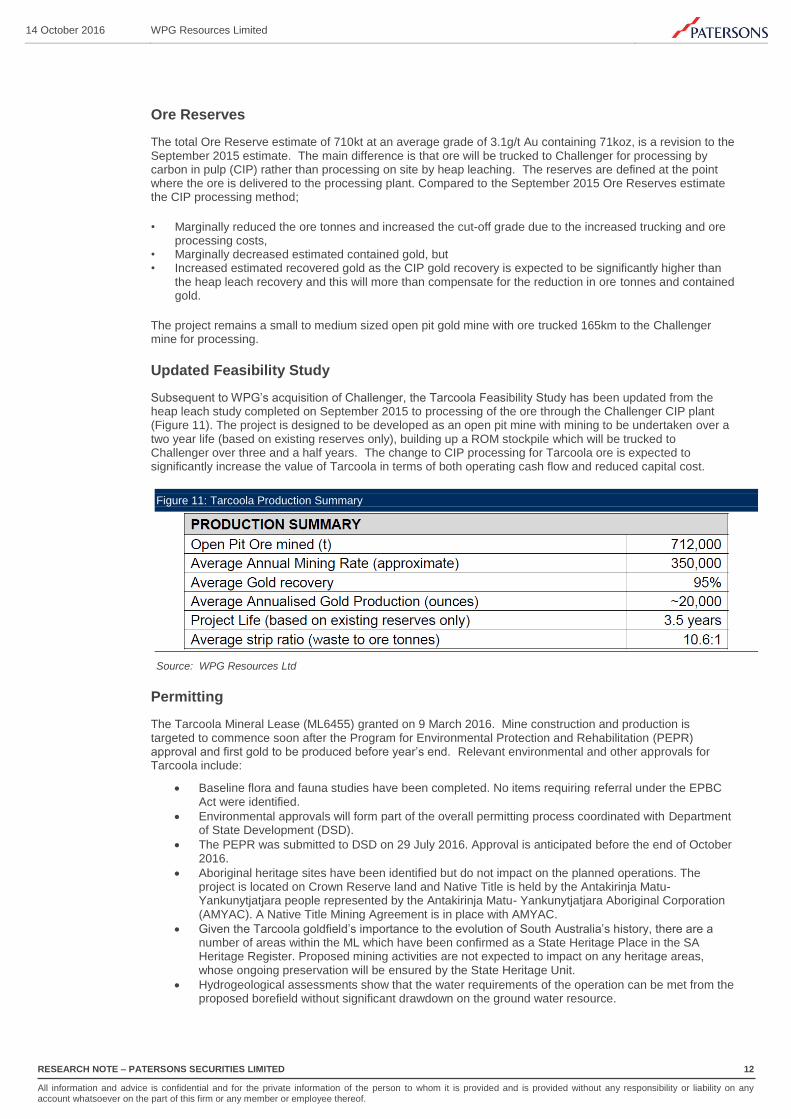

Subsequent to WPG’s acquisition of Challenger, the Tarcoola Feasibility Study has been updated from the heap leach study completed on September 2015 to processing of the ore through the Challenger CIP plant (Figure 11). The project is designed to be developed as an open pit mine with mining to be undertaken over a two year life (based on existing reserves only), building up a ROM stockpile which will be trucked to Challenger over three and a half years. The change to CIP processing for Tarcoola ore is expected to significantly increase the value of Tarcoola in terms of both operating cash flow and reduced capital cost.

Figure 11: Tarcoola Production Summary

Source: WPG Resources Ltd

Permitting

The Tarcoola Mineral Lease (ML6455) granted on 9 March 2016. Mine construction and production is targeted to commence soon after the Program for Environmental Protection and Rehabilitation (PEPR) approval and first gold to be produced before year’s end. Relevant environmental and other approvals for Tarcoola include:

Baseline flora and fauna studies have been completed. No items requiring referral under the EPBC Act were identified.

Environmental approvals will form part of the overall permitting process coordinated with Department of State Development (DSD).

The PEPR was submitted to DSD on 29 July 2016. Approval is anticipated before the end of October 2016.

Aboriginal heritage sites have been identified but do not impact on the planned operations. The project is located on Crown Reserve land and Native Title is held by the Antakirinja Matu-Yankunytjatjara people represented by the Antakirinja Matu- Yankunytjatjara Aboriginal Corporation (AMYAC). A Native Title Mining Agreement is in place with AMYAC.

Given the Tarcoola goldfield’s importance to the evolution of South Australia’s history, there are a number of areas within the ML which have been confirmed as a State Heritage Place in the SA Heritage Register. Proposed mining activities are not expected to impact on any heritage areas, whose ongoing preservation will be ensured by the State Heritage Unit.

Hydrogeological assessments show that the water requirements of the operation can be met from the proposed borefield without significant drawdown on the ground water resource.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 13

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Tunkillia

In May 2014, WPG acquired the Tunkillia Gold Project and has 100% of all minerals in the area which covers 1,604km

2. Tunkillia is located some 550km northwest of Adelaide and 70km southwest of Tarcoola in the

Gawler Craton and was first discovered in 1996.

The project comprises three exploration licences:

EL 4812 Lake Everard 1,088 km2

EL 5670 Lake Everard West 149 km2

EL 5790 Cooritta Hill 367 km2

An in depth review of the potential development scenarios for Tunkillia including optimisation studies has been carried out enabling the Company to set a platform to redefine the project parameters and advance an accelerated exploration and development strategy.

Figure 12: Tunkillia Project Prospect Location Map

Source: WPG Resources Ltd

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 14

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Mineral Resource

A detailed review of the Tunkillia gold project data confirmed that the resource estimate for the main 223 deposit can be enhanced at higher cut-off grades allowing a wide degree of flexibility for strategic development options. In February 2015, the Mineral Resource estimate was updated using a 0.5g/t cut-off grade in the oxide zone, and a 1.0g/t cut-off grade in the primary zone. Using these parameters, the current resource estimate is 12.3Mt at 1.41 g/t Au (84% Measured & Indicated) for 558koz Au and 1.5Moz Ag.

Figure 13: Tunkillia Resource Estimate

Source: WPG Resources Ltd

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 15

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

RISKS

We have identified a number of risks which may impact WPG. These are by no means a complete list of risks and there may be others beyond those identified:

Resource Conversion: At Challenger, WPG will need to conduct further drilling to convert Mineral

Resources into Ore Reserves. There is a risk that the outcomes of this drilling may not meet our expectations of an 80% conversion from Mineral Resources to Ore Reserves. However, there does appear to be a number of opportunities to convert laterally within the mine.

Technical: At Challenger, WPG’s approach is to reduce the production rate of the mine and focus on lower

cost ounces. The use of smaller equipment is expected to reduce the amount of dilution. If the dilution is higher than expected then there is a risk that processed grades could be lower and subsequently force costs higher.

Permitting: Approvals for mining to commence at Tarcoola are expected in the December 2016 Q. Delays

could impact our production estimates and our valuation.

Commodity Price: The project is most sensitive to gold price with a 10% move resulting in a 31% change to

our valuation.

Exchange Rate: Movements in the AUDUSD exchange rate have an impact on our valuation. A 10% move

in exchange rate has a 28% impact to our valuation.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 16

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

DIRECTORS AND MANAGEMENT

Robert (Bob) H Duffin – Executive Chairman

BSc (Hons), MSc (Hons), Grad Dip Mgt, FAusIMM

Bob Duffin is a company director with over 45 years’ experience in resource exploration, project assessment, mining investment analysis, and company management.

Bob has held senior positions in the exploration divisions of Peko Wallsend and MIM Holdings, then two of Australia’s largest mining companies, and is a former Managing Director of Austirex International, an international resource exploration consulting and contracting firm. He has lived and worked in mining communities, including periods in Kalgoorlie in Western Australia and Mount Isa in Queensland, where he worked on exploration programs for a number of commodities, including gold, copper, uranium, base metals and iron ore. He has also worked with three stockbroking firms and was head of research at one of Australia’s leading resource sector brokers in the 1980s.

Bob is a former Non-Executive Director of a number of companies, including Centennial Coal, Midwest Corporation, Ferrowest, Burmine, Austmin Gold, Mt Lyell, the UK resources investment company Europa Minerals Group, and Mancala, a mining contractor. Bob has been a Director of WPG since 2004.

Martin Jacobsen – Managing Director and CEO

MSCC, MDP (Unisa)

Martin Jacobsen joined WPG from his previous position as Vice President, Operations, with Golden China Resource Corporation Limited, a gold mining and exploration company with project assets in China. Prior to that he was Technical Director with Emperor Mines Limited and had earlier held senior management positions in gold, chrome and platinum mining operations in South Africa. He has been project manager for a number of projects in a wide range of commodities and mine types. Martin manages all phases of WPG’s mining and exploration projects. He was appointed Managing Director in October 2013.

Gary Jones – Technical Director

BSc, FAusIMM, MSEG

Gary Jones is a geologist with over 45 years professional experience in mineral exploration and resource and reserve estimation for various type of mineral deposits including porphyry copper-gold and epithermal gold. He is Managing Director of Geonz Associates Ltd, a leading New Zealand firm of consulting geologists, and has been an independent consultant to the mining industry for the past 29 years during which time assignments have been completed in many parts of the world including Australia, Indonesia, North and South America, Canada and New Zealand.

Prior to setting up his own consultancy Gary worked as an exploration geologist for Geopeko for 15 years in various parts of Australia including 12 years in central New South Wales where he established and managed a new exploration operation for Geopeko. During this time he supervised numerous base and precious metal projects throughout the Lachlan Fold Belt and parts of the New England region and is credited with the discovery of the Northparkes porphyry copper-gold deposits.

Following the initial discoveries at Goonumbla, Gary also had a major input into the pegging of a large block of exploration licences in the Lake Cowal region. He planned and supervised the initial regional exploration programs that ultimately led to the discovery of the 4.4 million ounce Cowal porphyry gold deposit. Early in his career Gary worked on iron ore exploration and mining activities in the Northern Territory. Gary has been a Director of WPG since 2004.

Len Dean – Non-Executive Director

BSc (Met)

Len Dean has had a 40 year career in the resources sector, with particular emphasis in the global iron ore industry. He spent 36 years with BHP, finishing in 2000 as Vice President, Coal and Iron Ore Marketing. During his period with BHP he was General Manager, Marketing for BHP Iron Ore in Perth for 8 years, he managed iron ore mining operations at BHP’s Yampi Sound mine, and he lived and worked at BHP’s (now OneSteel’s) Whyalla works for 3 years. He was Managing Director of Sesa Goa Limited, India’s largest private sector exporter of iron ore, from 2003 to 2006. More recently, he has been an iron ore consultant with a wide client base including Orinoco Iron (Venezuela), Mitsui Iron Ore Development, CVRD (Brazil) and Mineral Enterprises Limited (India). Len has been a Director of WPG since 2007.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 17

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Dennis Mutton – Non-Executive Director

BSc (Hons), Grad Dip Mgt, JP, FAIM, FAICD

Dennis Mutton is a management consultant specialising in natural resource management, primary industries and resources, regional growth initiatives and business-government relations. From 1997 to 2002 he was Chief Executive of the South Australian Department of Primary Industries and Resources. He has a portfolio of directorships including Chair of Bio Innovation SA and Chair of CRC Pork Ltd. He is a former Director of Mines, former Chair of the Natural Resources Management Council, and a former Director of the Australian Rural Leadership Foundation. Dennis lives in Adelaide. He was a Director of WPG from 2007 – 2008, and re-joined the Board in 2010.

Lim See Yong – Non-Executive Director

BBA (Singapore)

Lim See Yong is General Manager and Director of Xin Sheng International Private Limited, a trading company related to Tangshan Xingye Industrial and Trade Group Corporation, an investor in raw materials for the steel industry. He spent 11 years with NatSteel Trade International, a Singapore mill that produces bars and wire rods from scrap. He was NatSteel’s chief representative in China for 7 years from 1995. From 2002 to 2006 he was in charge of selling iron ore and steel products to China, and exporting semi and finished steel products to South East Asian markets. See Yong lives in Singapore. He has been a Director of WPG since 2007.

Wayne Rossiter – Chief Financial Officer

BE (Mining), ACA, MAppFin, MAusIMM, GMAICD

Wayne Rossiter is both a mining engineer and a chartered accountant. Wayne has held senior finance and management roles in resource and energy companies. Wayne has knowledge and experience in transitioning companies from the exploration stage through to development and into production. His range of experience includes underground coal gasification, coal seam gas, coal, conventional oil and gas, precious metals, gold and iron ore with global experience covering Australia, Africa, China, Indonesia, the USA, the UK, the former Soviet Republic of Georgia and the Middle East.

Larissa Brown – Company Secretary

BA, Dip Ed, Grad Dip ACG, AGIA

Larissa Brown is a chartered secretary with particular experience in the administration of resource and resource technology companies. Larissa manages corporate and regulatory compliance, share registry and shareholder liaison & communications and annual reporting, as well as work health safety, safety governance and policy development. Larissa was appointed Group Company Secretary on 6 August 2009.

Cornel Parshotam – Chief Operating Officer

Dip Mining, GCC

Cornel Parshotam is a mining professional with over 37 years of operational mining experience.

Cornel has held senior mining management positions in Africa and Australasia including General Manager Operations at Metallon Gold Zimbabwe, Acting Operations Manager at Emperor Gold Mines in Fiji and more recently General Manager Mine and then Head of Operations and BHP Billiton’s Olympic Dam Mine in South Australia. His range of experience encompasses the management and operation of both surface and underground operations in base metal and precious metal mining.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 18

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 19

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.

Recommendation History

Stock recommendations: Investment ratings are a function of Patersons expectation of total return (forecast price appreciation plus dividend yield) within the next 12 months. The investment ratings are Buy (expected total return of 10% or more), Hold (-10% to +10% total return) and Sell (> 10% negative total return). In addition we have a Speculative Buy rating covering higher risk stocks that may not be of investment grade due to low market capitalisation, high debt levels, or significant risks in the business model. Investment ratings are determined at the time of initiation of coverage, or a change in target price. At other times the expected total return may fall outside of these ranges because of price movements and/or volatility. Such interim deviations from specified ranges will be permitted but will become subject to review by Research Management. This Document is not to be passed on to any third party without our prior written consent.

14 October 2016 WPG Resources Limited

RESEARCH NOTE – PATERSONS SECURITIES LIMITED 20

All information and advice is confidential and for the private information of the person to whom it is provided and is provided without any responsibility or liability on any account whatsoever on the part of this firm or any member or employee thereof.