world bank document official use only abbreviations and acronyms badc - bangladesh agricultural...

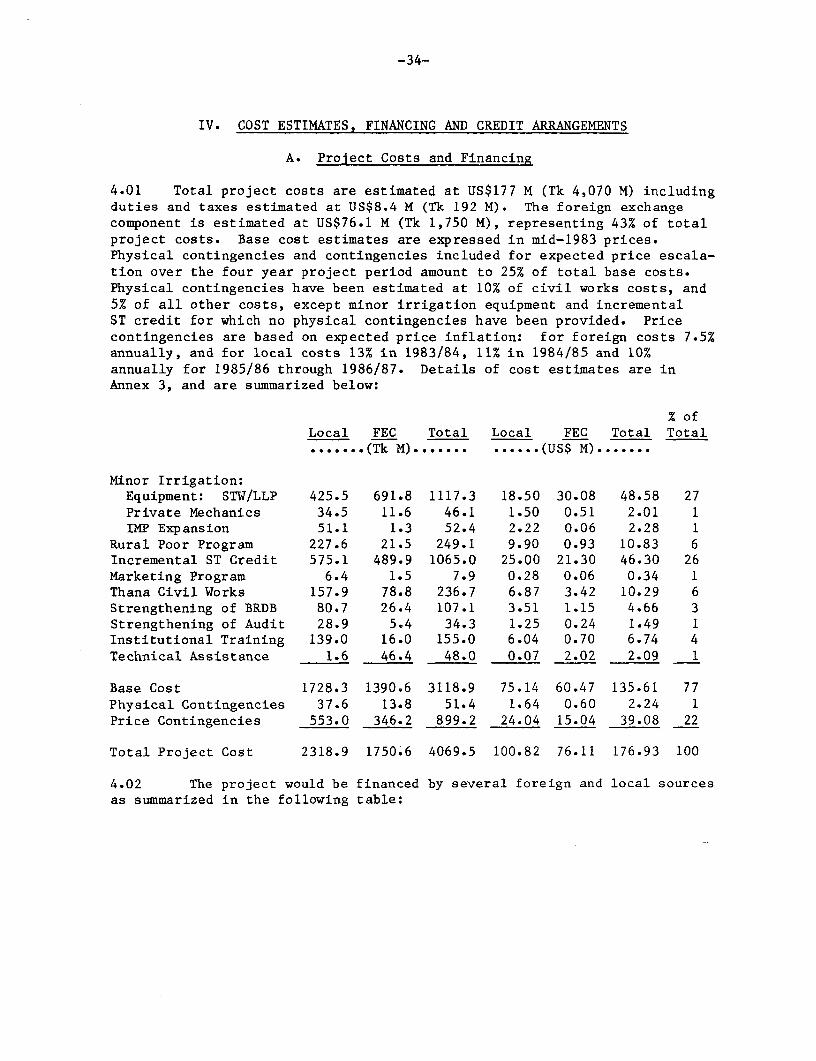

TRANSCRIPT

Document of

The World Bank

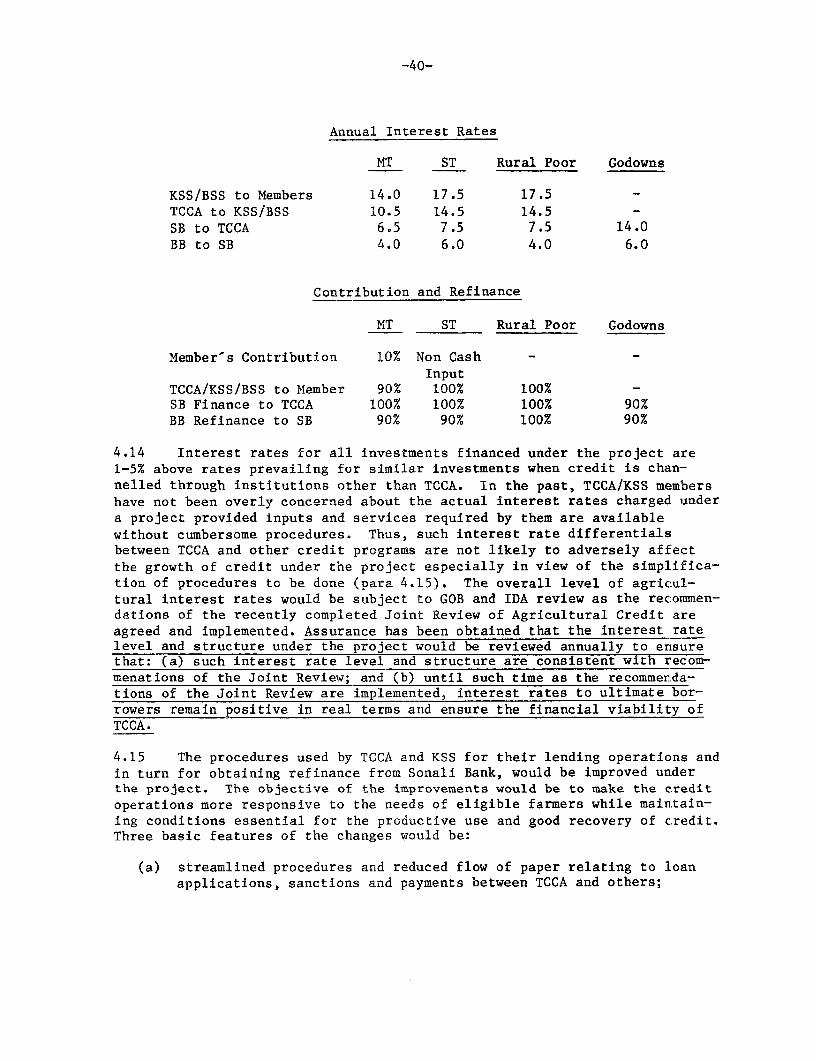

FOR OFFICIAL USE ONLY

Report No. 4348-BD

STAFF APPRAISAL REPORT

BANGLADESH

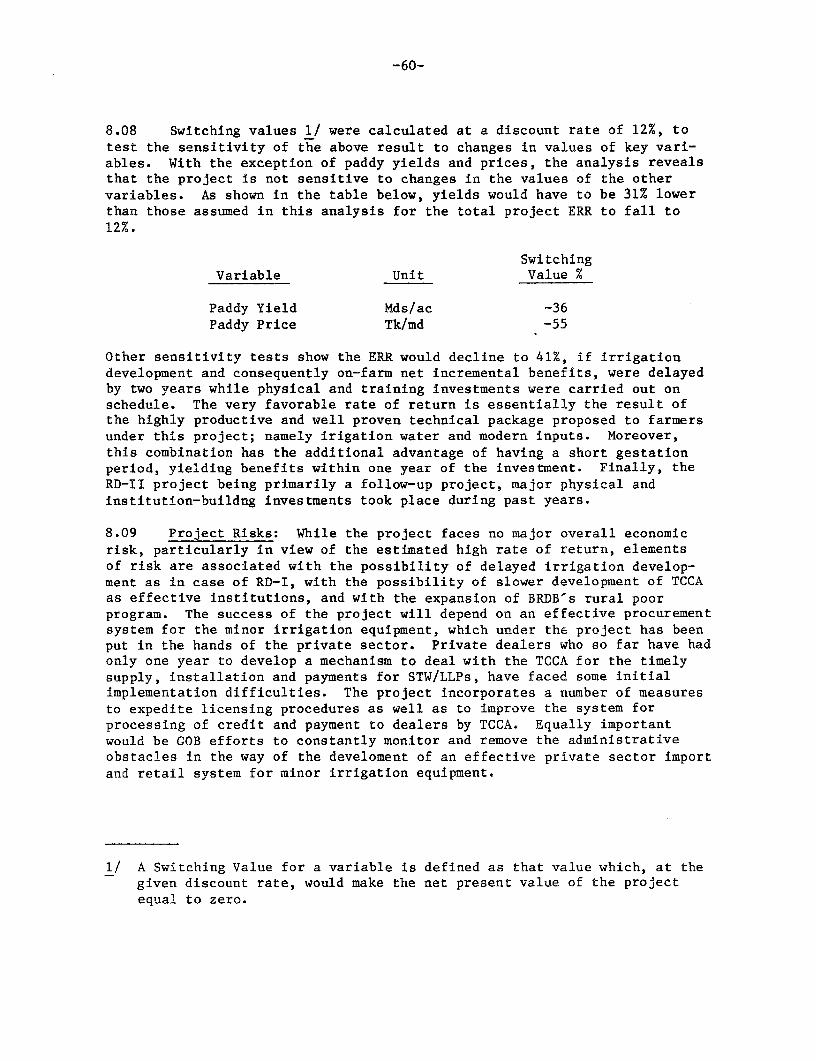

RURAL DEVELOPMENT II PROJECT

May 17, 1983

South Asia Projects DepartmentGeneral Agriculture

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

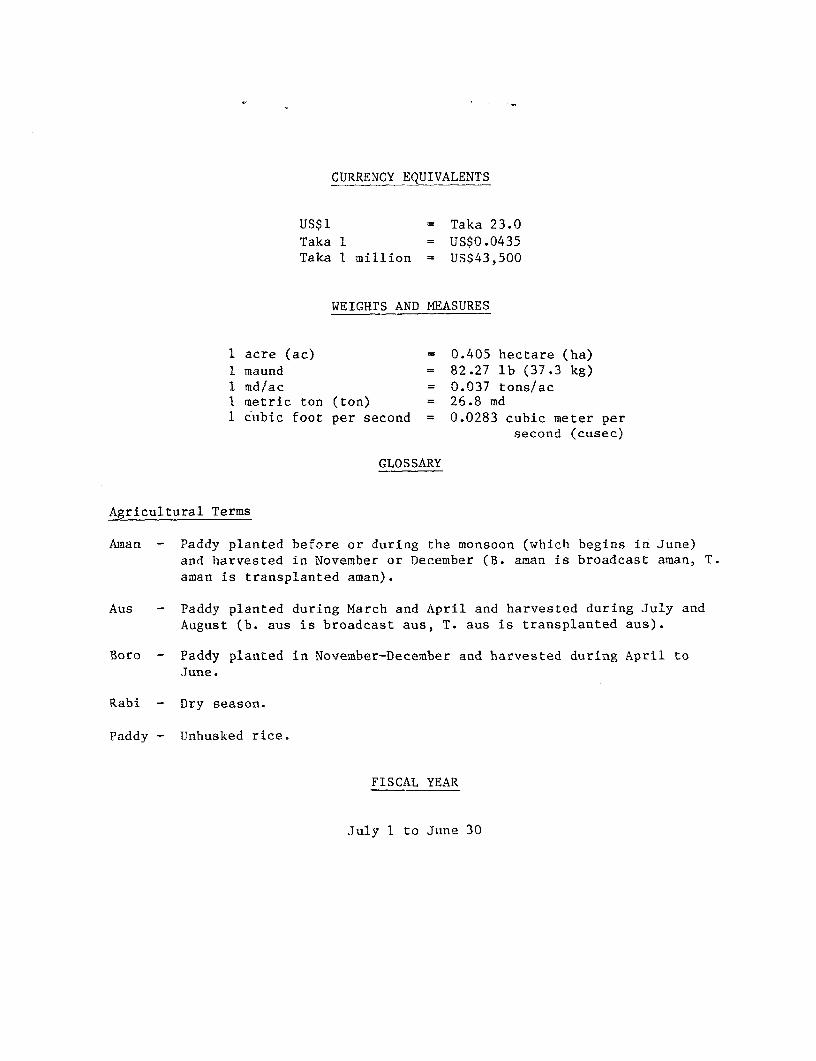

CURRENCY EQUIVALENTS

US$1 = Taka 23.0

Taka 1 = US$0.0435

Taka 1 million = US$43,500

WEIGHTS AND MEASURES

1 acre (ac) = 0.405 hectare (ha)1 maund = 82.27 lb (37.3 kg)1 md/ac = 0.037 tons/acI metric ton (ton) = 26.8 md1 cubic foot per second = 0.0283 cubic meter per

second (cusec)

GLOSSARY

Agricultural Terms

Aman - Paddy planted before or during the monsoon (which begins in June)and harvested in November or December (B. aman is broadcast aman, T.aman is transplanted aman).

Aus - Paddy planted during March and April and harvested during July andAugust (b. aus is broadcast aus, T. aus is transplanted aus).

Boro - Paddy planted in November-December and harvested during April toJune.

Rabi - Dry season.

Paddy - Unhusked rice.

FISCAL YEAR

July 1 to June 30

FOR OFFICIAL USE ONLY

ABBREVIATIONS AND ACRONYMS

BADC - Bangladesh Agricultural Development CorporationBB - Bangladesh BankBHB - Bangladesh Handloom BoardBKB - Bangladesh Krishi BankBRDB - Bangladesh Rural Development BoardBSCIC - Bangladesh Small & Cottage Industries CorporationBSS - Bittyaheen Samabaya SamityCCC - Cooperative College in ComillaCIDA - Canadian International Development AgencyDTIW - Deep TubewellGOB - Government of BangladeshHTW - Hand TubewellIDA - International Development AssociationIMP - Irrigation Management ProgramIRDP - Integrated Rural Development ProgranKSS - Krishi Samabaya SamityLLP - Low Lift PumpMTFPP - Medium Term Food Production PlanNCB - Nationalized Commercial BanksNCIIRD - National Committee for Multi-Sectoral Rural DevelopmentNGO - Non-Governmental OrganizationODA - Overseas Development AdministrationPECU - Project Engineering & Construction UnitPWD - Public Works DepartmentRCS - Registrar of Cooperative SocietiesRDA - Rural Development Academy, BograRDTI - Rural Development Training Institute, SylhetSTW - Shallow TubewellTCCA - Thana Central Cooperative AssociationTPO - Thana Project OfficerTTDC - Thana Training & Development CenterTTU - Thana Training UnitsUNDP - United Nations Development Program

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

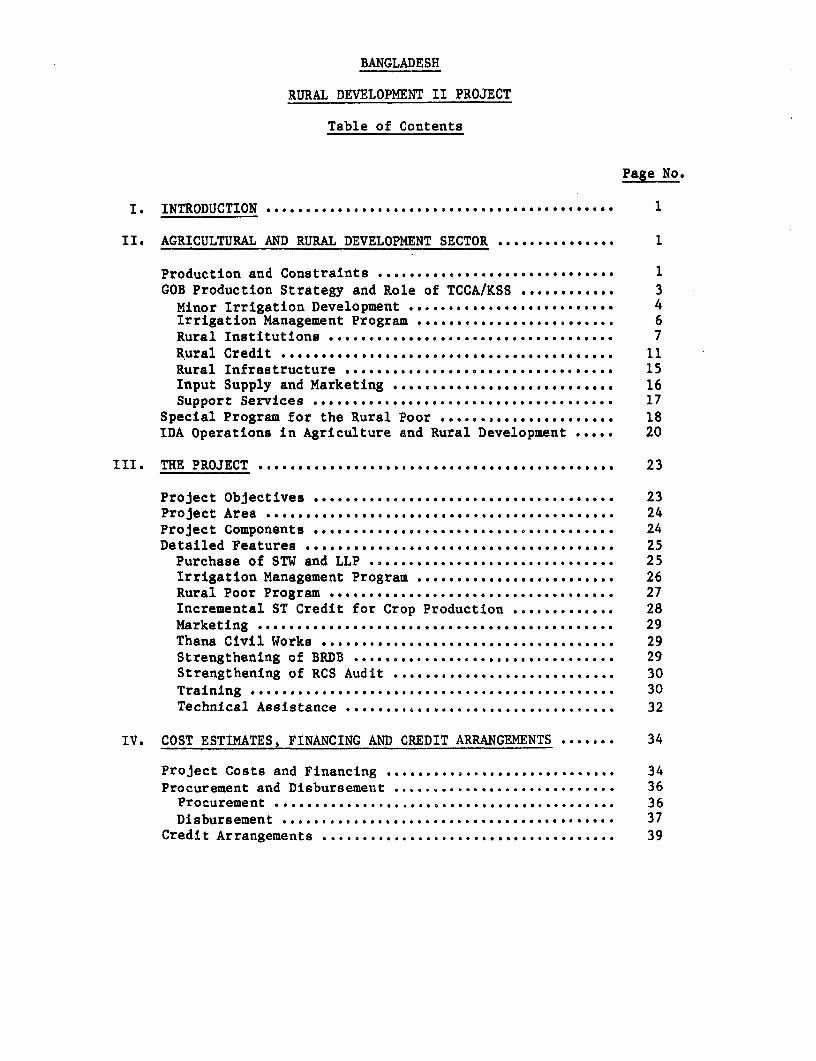

BANGLADESH

RURAL DEVELOPMENT II PROJECT

Table of Contents

Page No.

I. INTRODUCTION ........................................ 1

II. AGRICULTURAL AND RURAL DEVELOPMENT SECTOR ............... 1

Production and Constraints .............................. lGOB Production Strategy and Role of TCCA/KSS ............ 3

Minor Irrigation Development .......................... 4Irrigation Management Program ....................... 6Rural Institutions ...... .................................. 7

Rural Infrastructure .................... ................ 15Input Supply and Marketing ............... ............. 16Support Services ........... . ........ .............. . ....... . 17

Special Program for the Rural Poor ..... ................. 18IDA Operations in Agriculture and Rural Development ..... 20

III. THE PROJECT *............................................ 23

Project Objectives ......... ... .. .... ............... .... 23Project Area .......................................... . 24Project Components ............................ ....... . 24Detailed Features .. *...*.*.*...*.*.*..*.***.*.*.*.*. .... ... 25Purchase of STW and LLP ...................... * ***.*.... 25Irrigation Management Program ......................... 26Rural Poor Program ....... .. . .................... .. . .. . . . 27Incremental ST Credit for Crop Production ............. 28Marketing ................ 0......... 00...............* ......... 29Thana Civil Works ..* ***. ***** *******........................ ......... . 29Strengthening of BRDB .....,... .......... 29Strengthening of RCS Audit ....... o .. .............. 30Training ........................................ 0............. 30Technical Assistance .................... .............. 32

IV. COST ESTIMATES, FINANCING AND CREDIT ARRANGEMENTS ....... 34

Project Costs and Financing ............ ........... 34Procurement and Disbursement ..... ....................... 36Procurement ...................................... 36Disbursement .. . .. . .............................. ..... . 37

Credit Arrangements ................. . 39

-ii-

Page No.

V. ORGANIZATION AND MANAGEMENT ..... ........................ 41

Policy and Management ...... ............................ 41

Policy Guidance ....... ................................ 41Project Management ... ................................... 41

Participating Agencies . ....................... .. 43

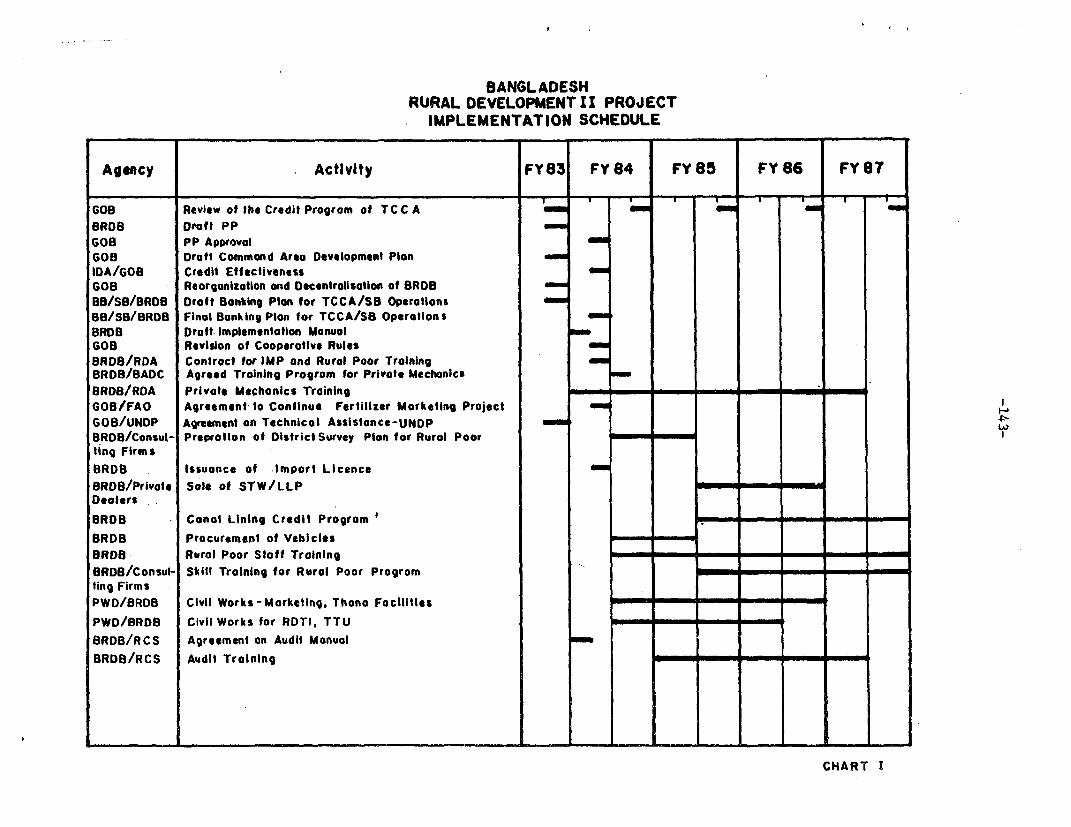

Inter-agency Coordination ..... 44Project Implementation ...... ............................ 45Implementation Schedule ............................... 45

Monitoring and Evaluation ..... .......................... 46Accounts and Audit ...... ................................ 47

VI. PRODUCTION, MARKETS AND PRICES ..... ..................... 48

Cropping Patterns ...... ............................... 48

Yields and Production ... ................................ 48Marketing ............................................. 49Prices ................................................ 49

VII. FINANCIAL ANALYSIS AND COST RECOVERY ................... 50

Farm Incomes ...................... ...................... 50Income from Activities under the Rural Poor Components .. 51Financial Performance of Participating TCCA ............. 52

TCCA Grants ..................... ...................... 53Produce and Fertilizer Marketing ......... .. ........... 54

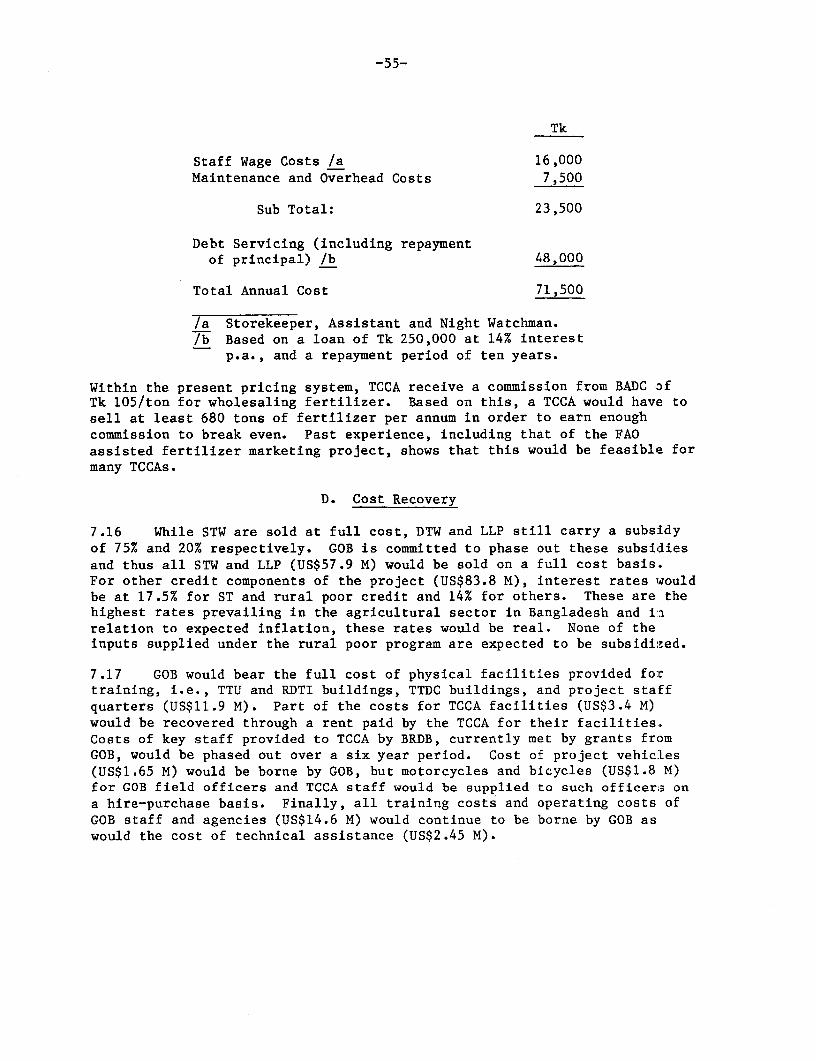

Cost Recovery ........................................... 55

VIII. BENEFITS AND JUSTIFICATION .............................. 56

IX. RECOMMENDATIONS ....... .................................. 61

SCHEDULE A - Lending Terms and Conditions ...................... 64

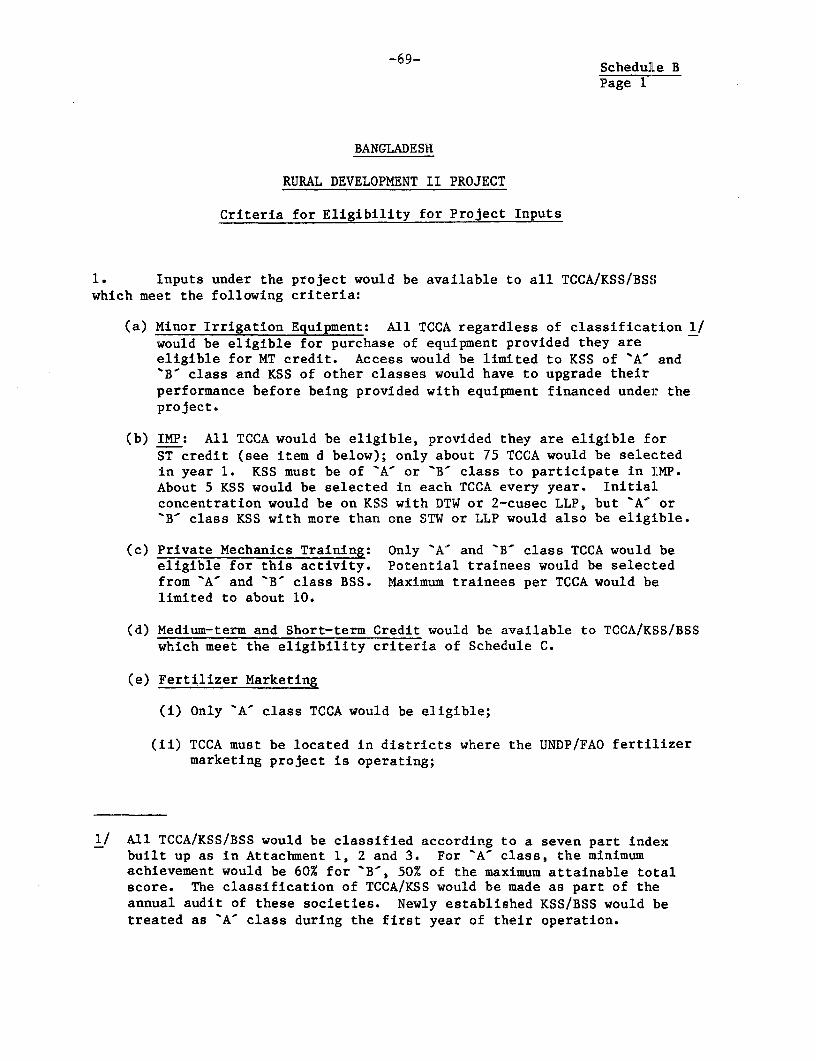

SCHEDULE B - Eligibility Criteria for Project Inputs .... ....... 69

SCHEDULE C - Lending Procedures for TCCA Credit Operations .... 74

ANNEX 1 - Background Data

Table 1 - TCCA/KSS System - Coverage ., 78Table 2 - Credit Operations of TCCA/K',S .79Table 3 - National Agriculture Credit Program ............... 80Table 4 - Minor Irrigation Experience . .81

Table 5 - Input Marketing Performance .82Table 6 - MTFPP - Requirement and Commitments for

Minor Irrigation Equipment .83

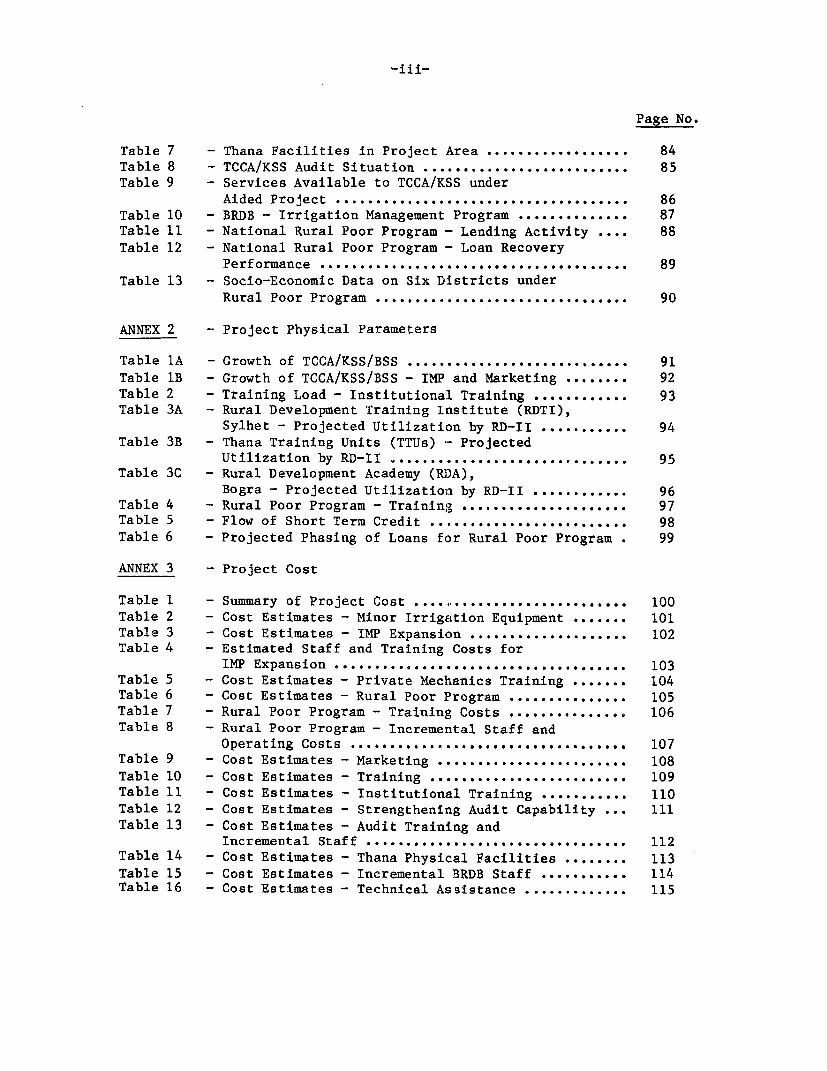

-iii-

Page No.

Table 7 - Thana Facilities in Project Area ............... ... 84Table 8 - TCCA/KSS Audit Situation ..... ..................... 85Table 9 - Services Available to TCCA/KSS under

Aided Project ............... ................ ....... 86

Table 10 - BRDB - Irrigation Management Program . .. 87Table 11 - National Rural Poor Program - Lending Activity 88

Table 12 - National Rural Poor Program - Loan RecoveryPerformance ........ 89

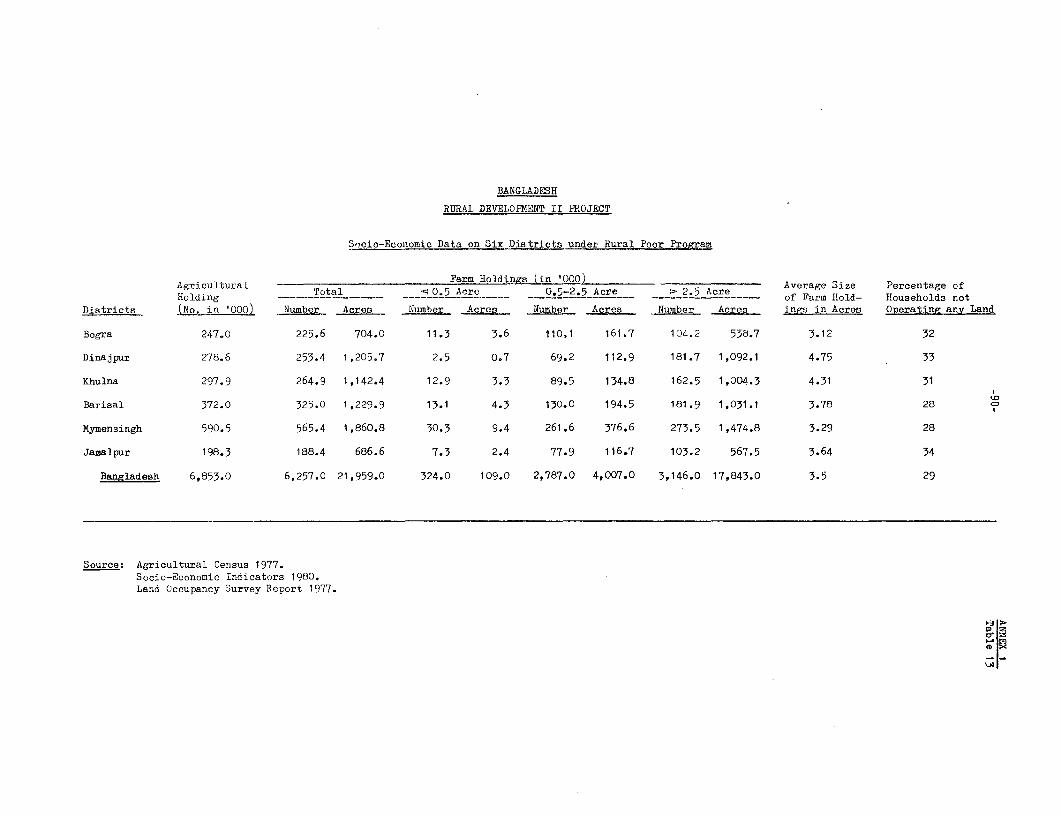

Table 13 - Socio-Economic Data on Six Districts underRural Poor Program ........ .. 90

ANNEX 2 - Project Physical Parameters

Table 1A - Growth of TCCA/KSS/BSS .91Table 1B - Growth of TCCA/KSS/BSS - IMP and Marketing .92Table 2 - Training Load - Institutional Training 93Table 3A - Rural Development Training Institute (RDTI),

Sylhet - Projected Utilization by RD-II .94Table 3B - Thana Training Units (TTUs) - Projected

Utilization by RD-II .. 95Table 3C - Rural Development Academy (R)A),

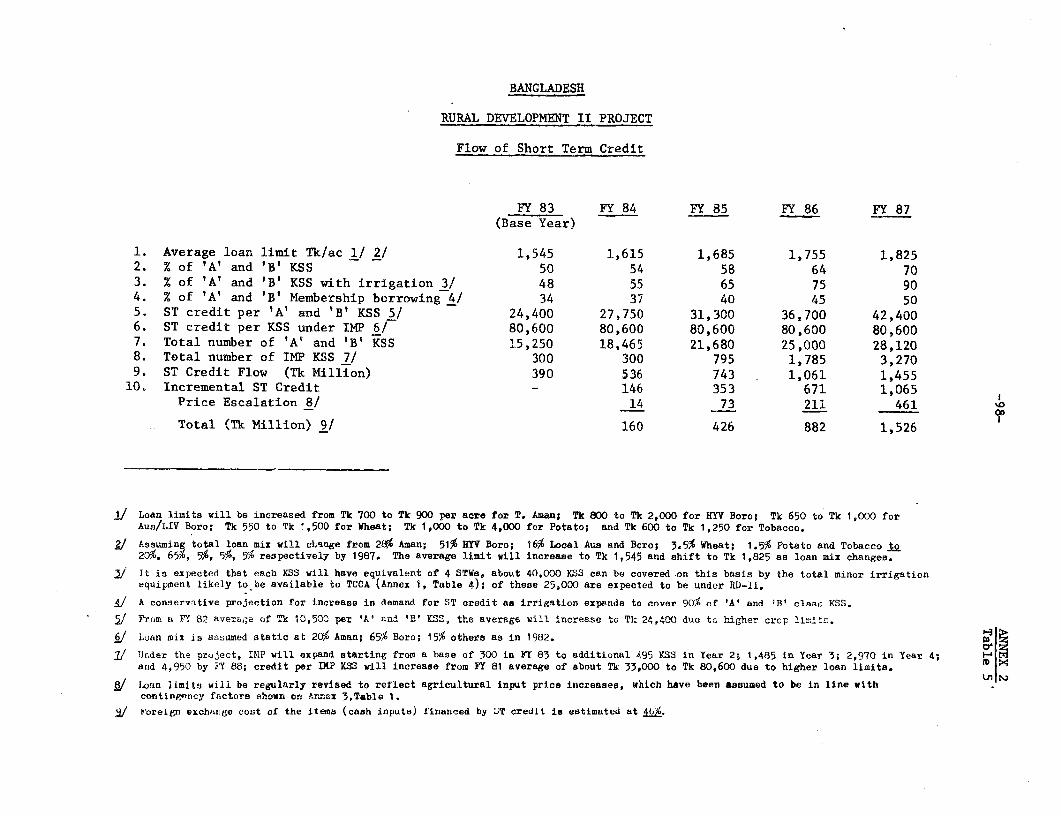

Bogra - Projected Utilization by RD-II .96Table 4 - Rural Poor Program - Training ..... ................ 97Table 5 - Flow of Short Term Credit ..... .................... 98

Table 6 - Projected Phasing of Loans for Rural Poor Program 99

ANNEX 3 - Project Cost

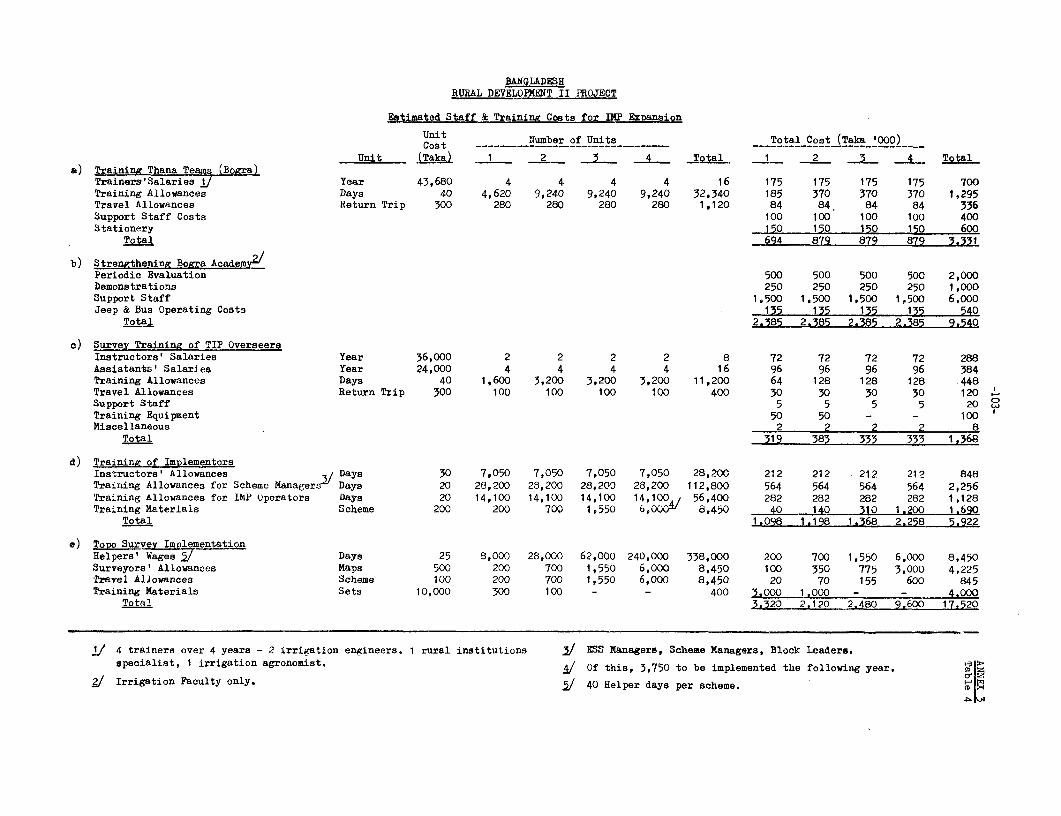

Table 1 - Summary of Project Cost . ............ .. 100Table 2 - Cost Estimates - Minor Irrigation Equipment . 101Table 3 - Cost Estimates - IMP Expansicon . 102Table 4 - Estimated Staff and Training Costs for

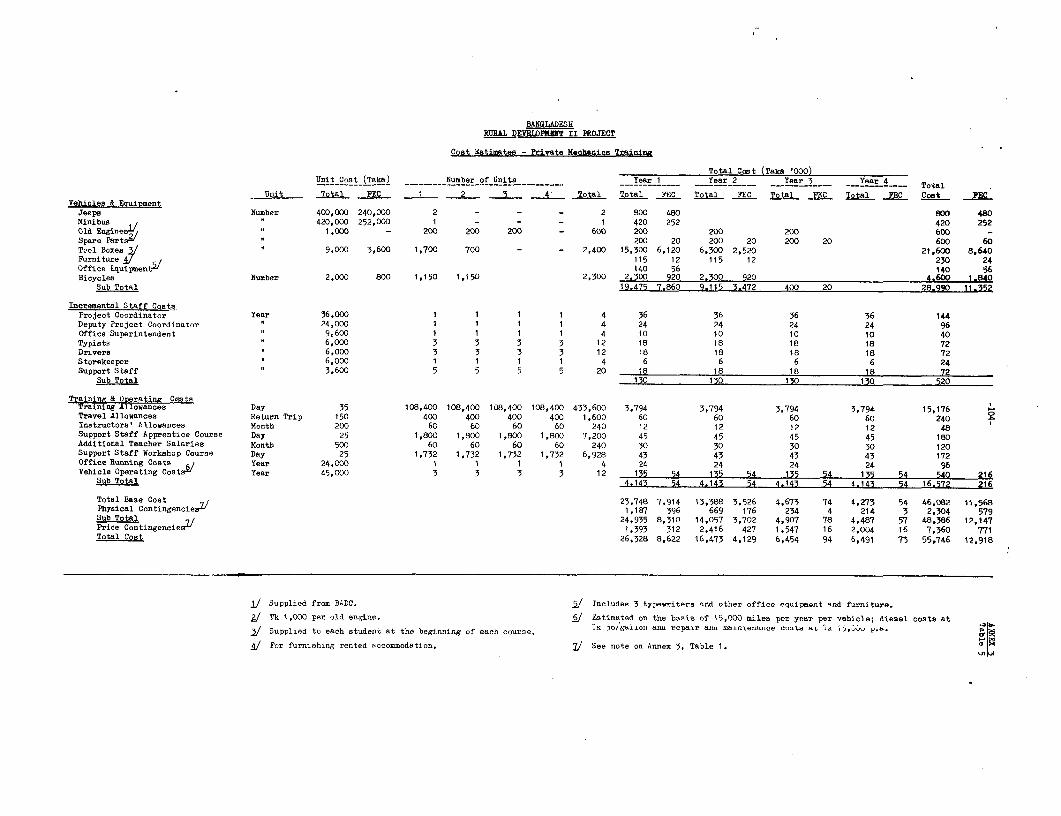

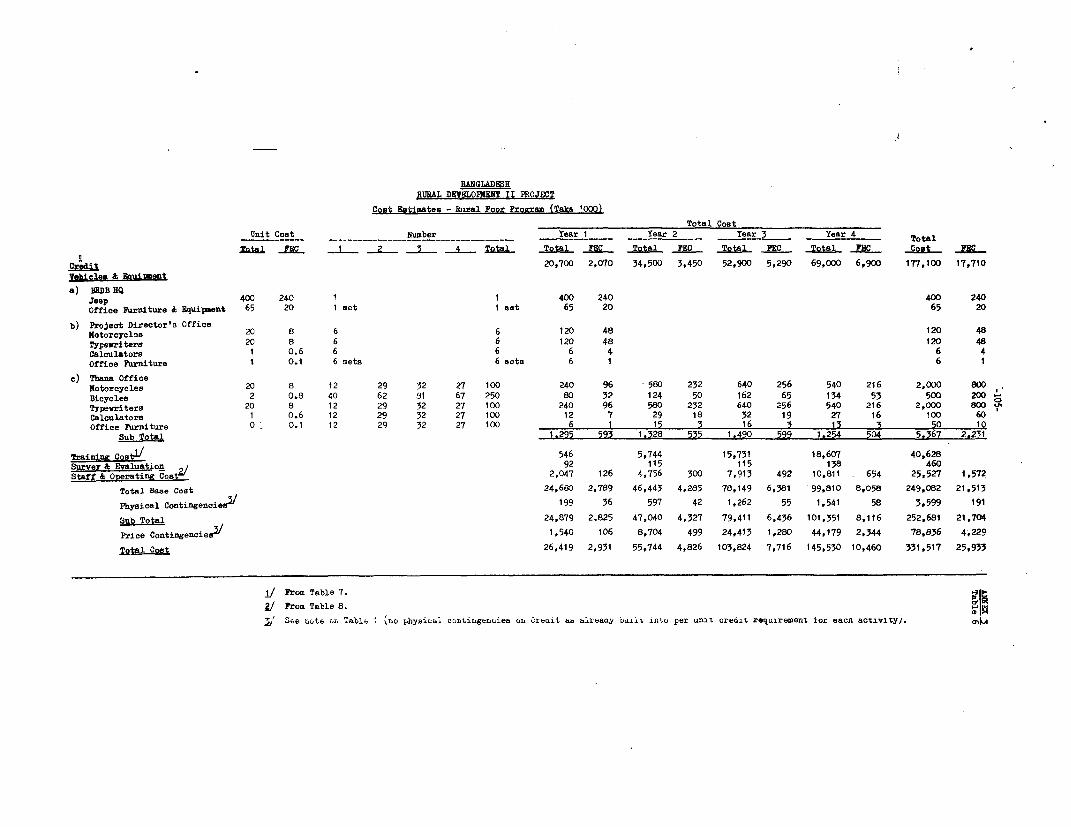

IMP Expansion .. . ...... ... . 103Table 5 - Cost Estimates - Private Mechanics Training . 104Table 6 - Cost Estimates - Rural Poor Program . 105

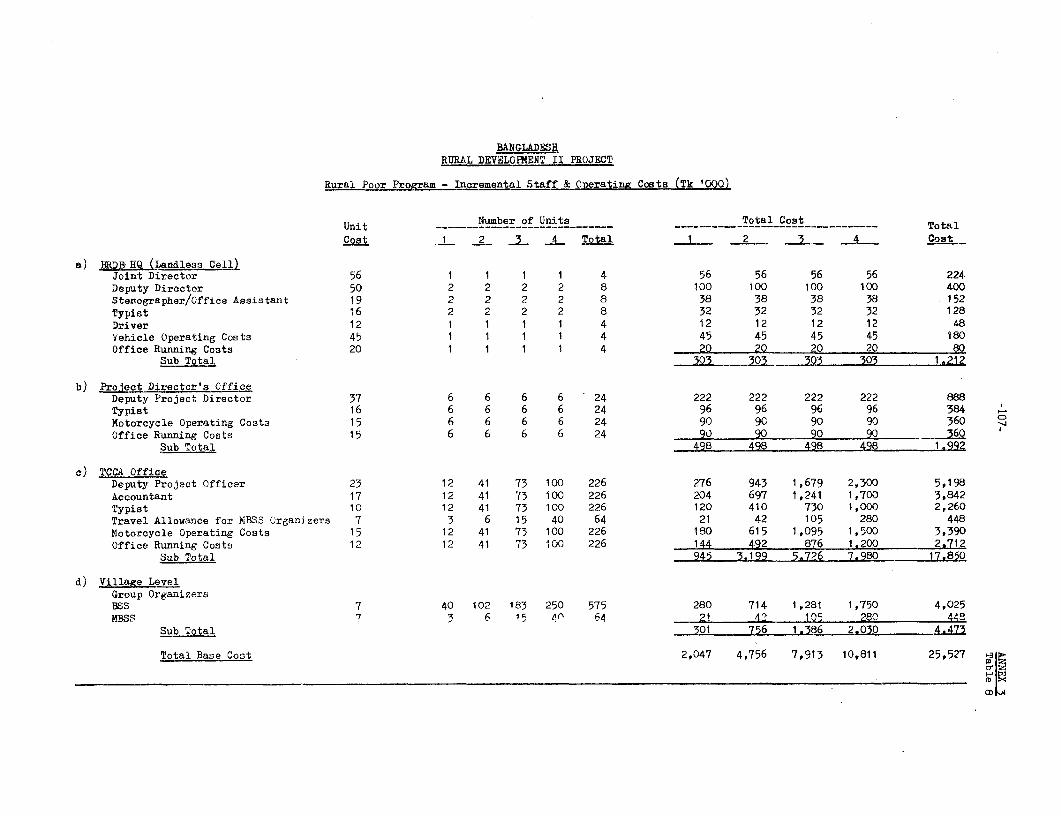

Table 7 - Rural Poor Program - Training Costs ... 106Table 8 - Rural Poor Program - Incremental Staff and

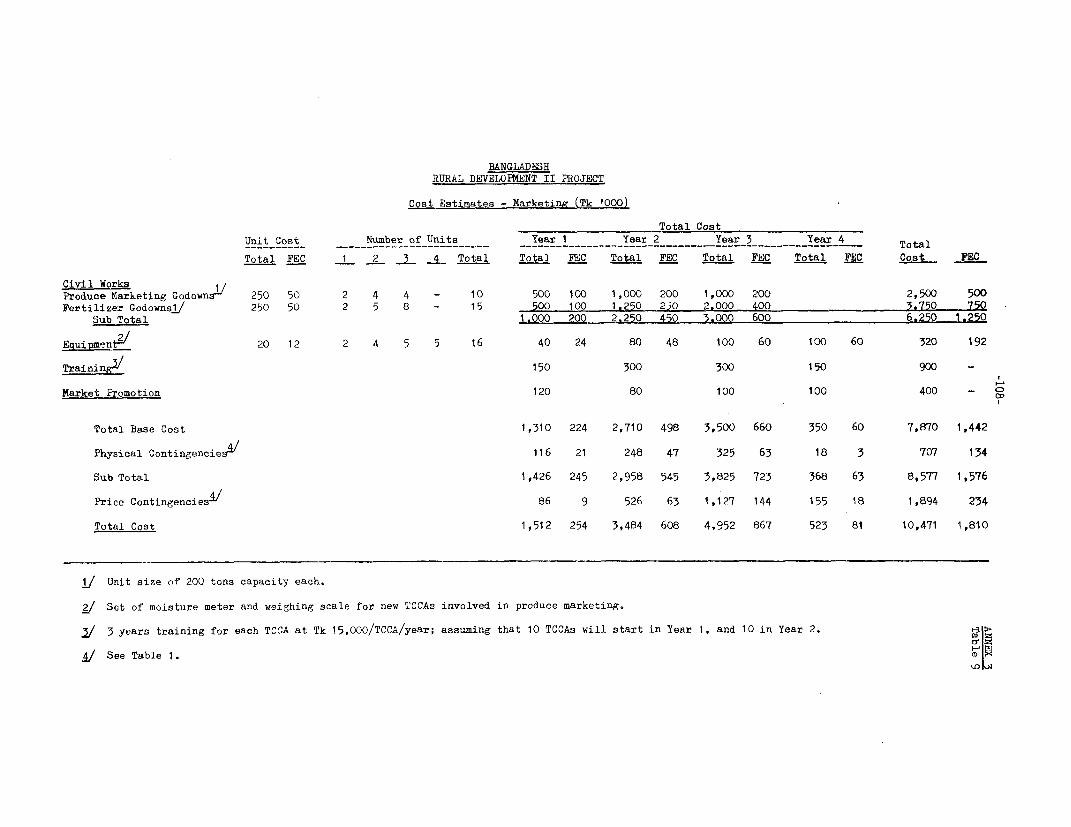

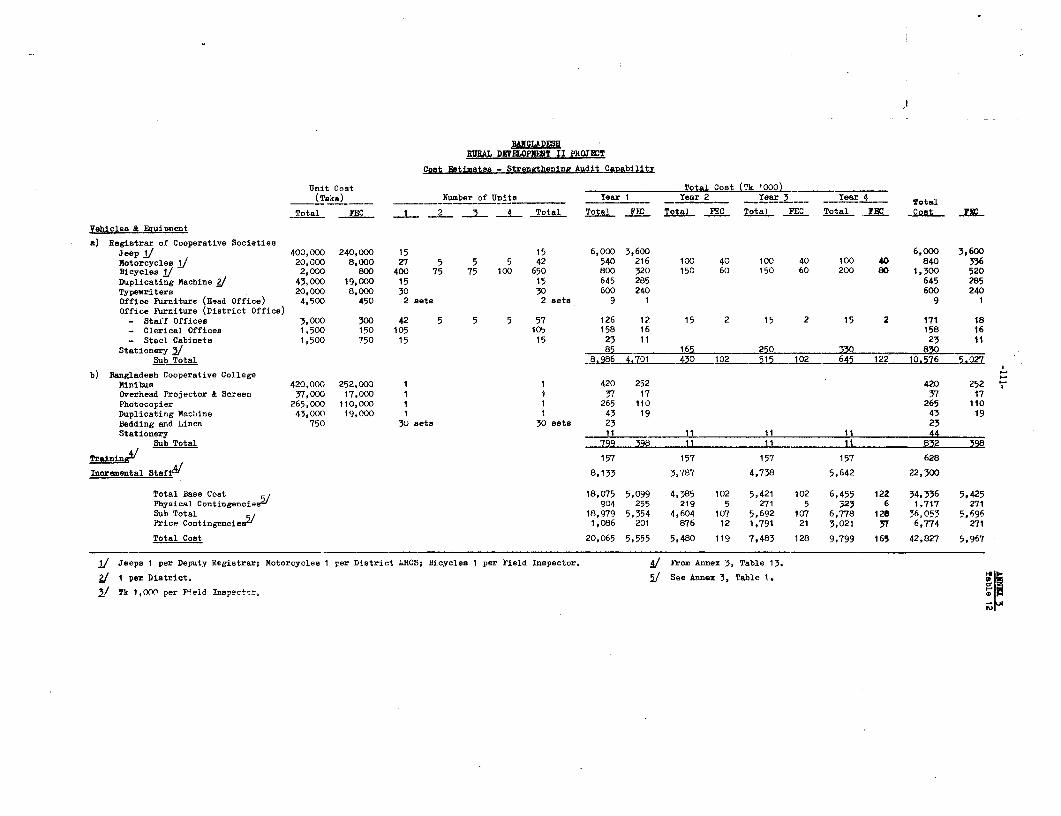

Operating Costs .............. . ..... . ........... 107Table 9 - Cost Estimates - Marketing . 108

Table 10 - Cost Estimates - Training ............ . 109Table 11 - Cost Estimates - Institutional Training .... 110

Table 12 - Cost Estimates - Strengthening Audit Capability ... 111Table 13 - Cost Estimates - Audit Training and

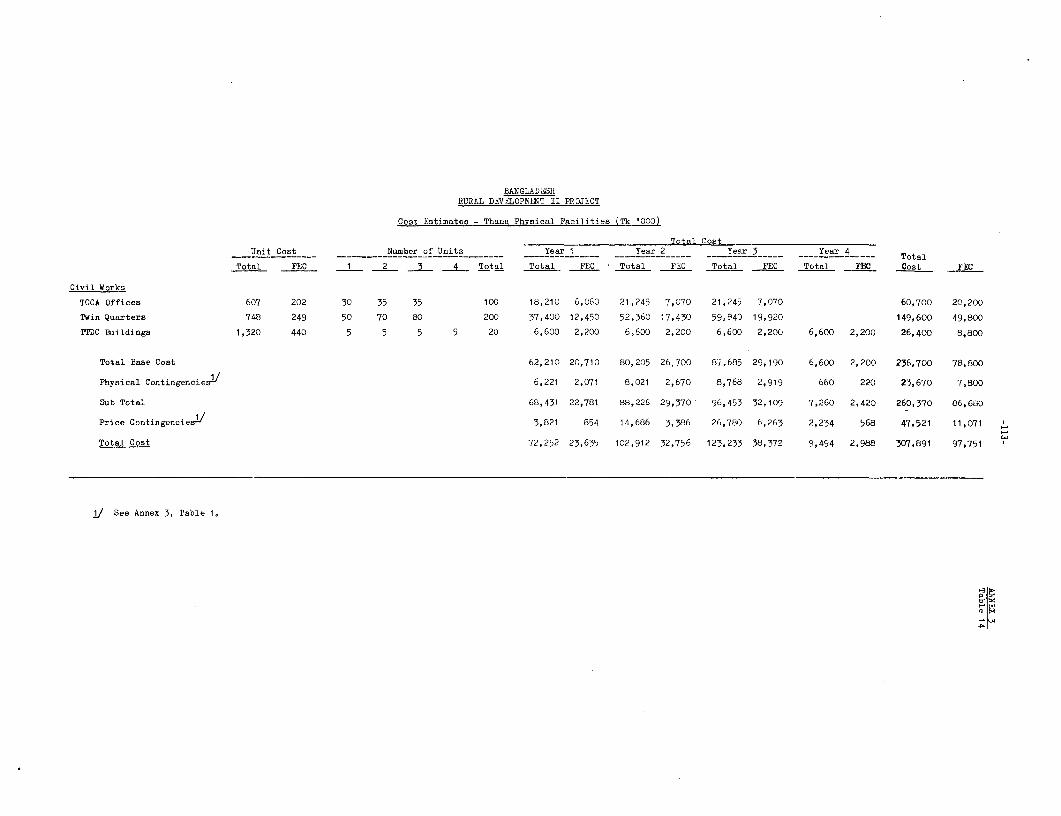

Incremental Staff .... 112Table 14 - Cost Estimates - Thana Physic.al Facilities ... 113

Table 15 - Cost Estimates - Incremental BRDB Staff ... 114Table 16 - Cost Estimates - Technical Assistance ... 115

- iv-

Page No.

Appendix I - Rural Poor Program - A Profile ofIncome Generating Activities ............ 116

ANNEX 4 - Project Financing and Disbursement

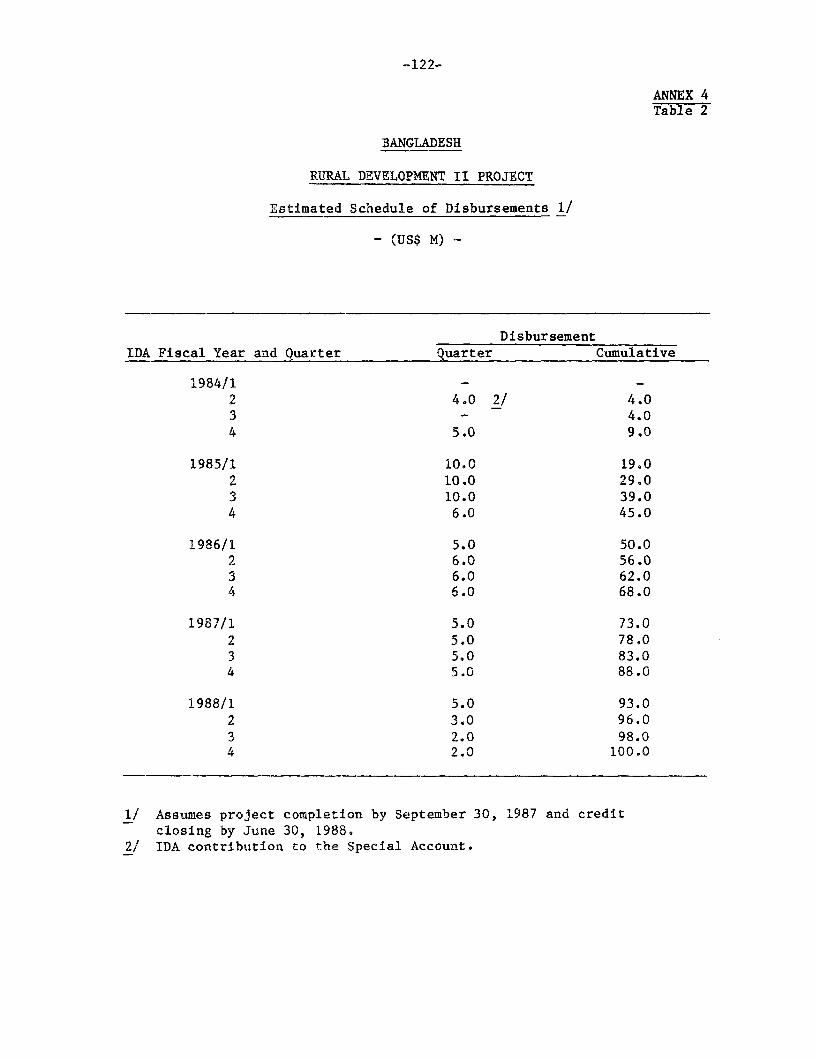

Table 1 - Project Financing Plan ............................ 121Table 2 - Disbursement Schedule ...... 122

ANNEX 5 - Financial Analysis

Table 1 - Cropping Patterns and Phasing, of Irrigated Area 123Table 2 - Summary of Crop Yields, and Input Requirements .... 124Table 3 - Estimated Operating Cost for Irrigation Equipment . 125Table 4 - Financial Analysis for STW Irrigation Group ....... 126Table 4A - Footnotes for Tables 4 and 5 .... . 127Table 5 - Financial Analysis for LLP Irrigation Group ....... 128Table 6 - Summarized Indicators of Return from

Rural Poor Activities ....... ...................... 129Table 7 - TCCA - Financial Analysis - Income Projection

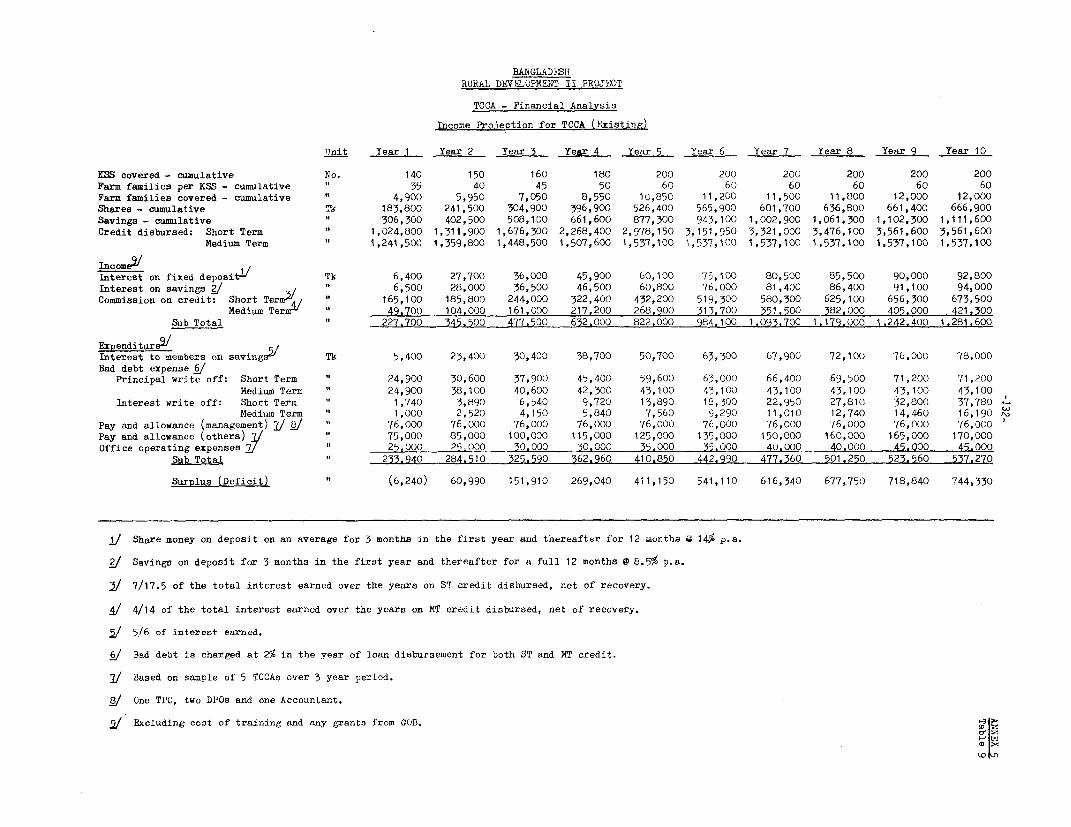

for New TCCA ...................................... 130Table 8 - Assumptions for TCCA Model (New) .... .............. 131Table 9 - TCCA - Financial Analysis - Income Projection

for Existing TCCA ... .......... ......... ........... 132

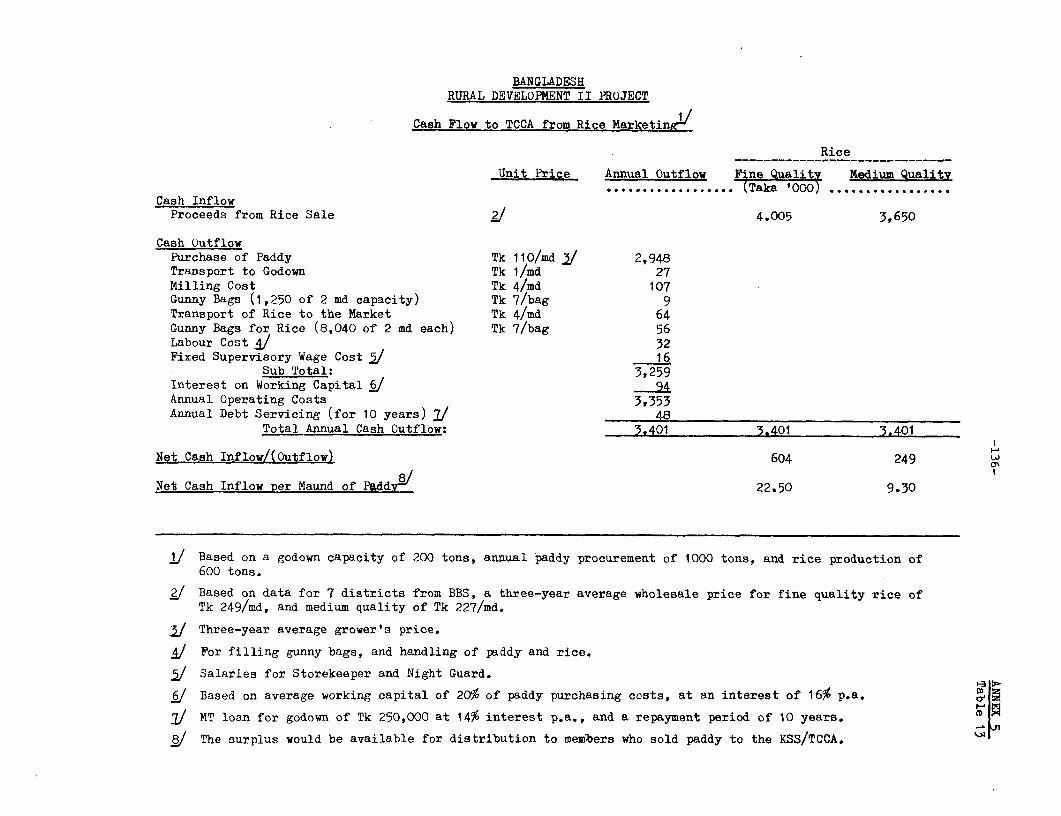

Table 10 - Assumptions for TCCA Model (Existing) . 133Table 11 - BRDB - TCCA/KSS System - Key Indicators . 134Table 12 - TCCA - Financial Analysis - Sensitivity Analysis . 135Table 13 - Cash Flow to TCCA from Rice Miarketing ... 136

ANNEX 6 - Economic Analysis

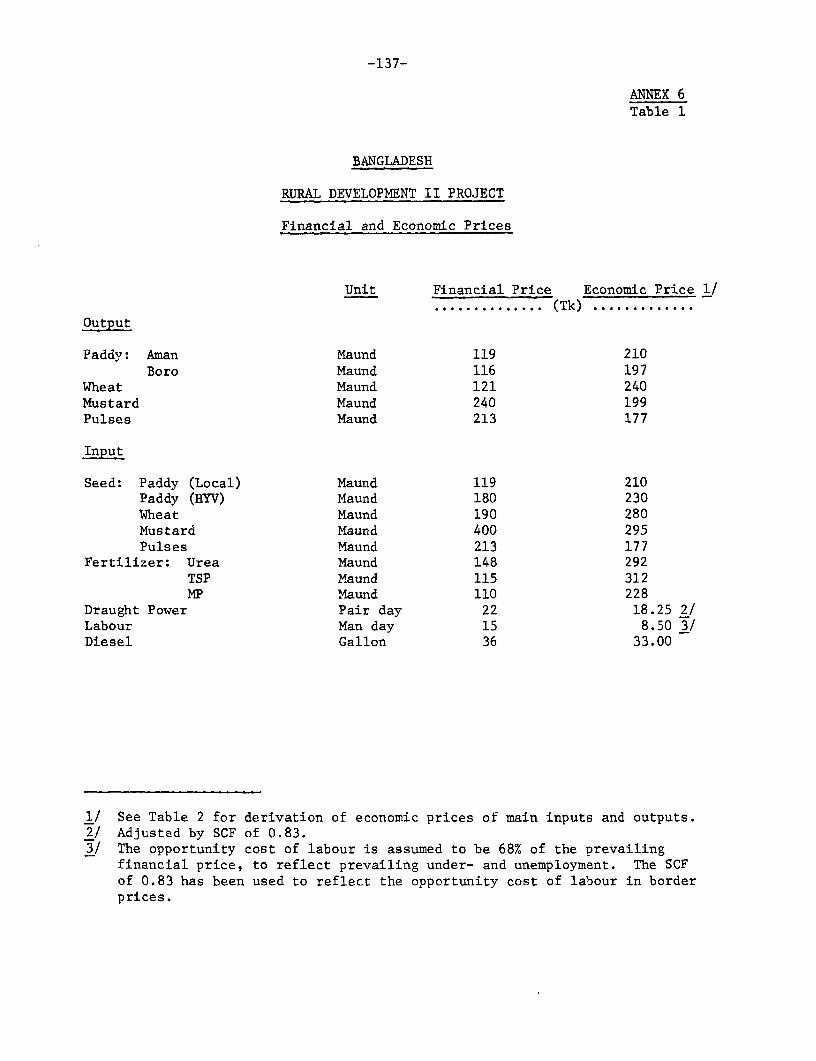

Table 1 - Financial and Economic Prices ..................... 137Table 2 - Derivation of Farmgate Economic Prices ............ 138Table 3 - Economic Analysis . ................................ 139

ANNEX 7 - List of Documents on Project File ................ 140

CHARTS

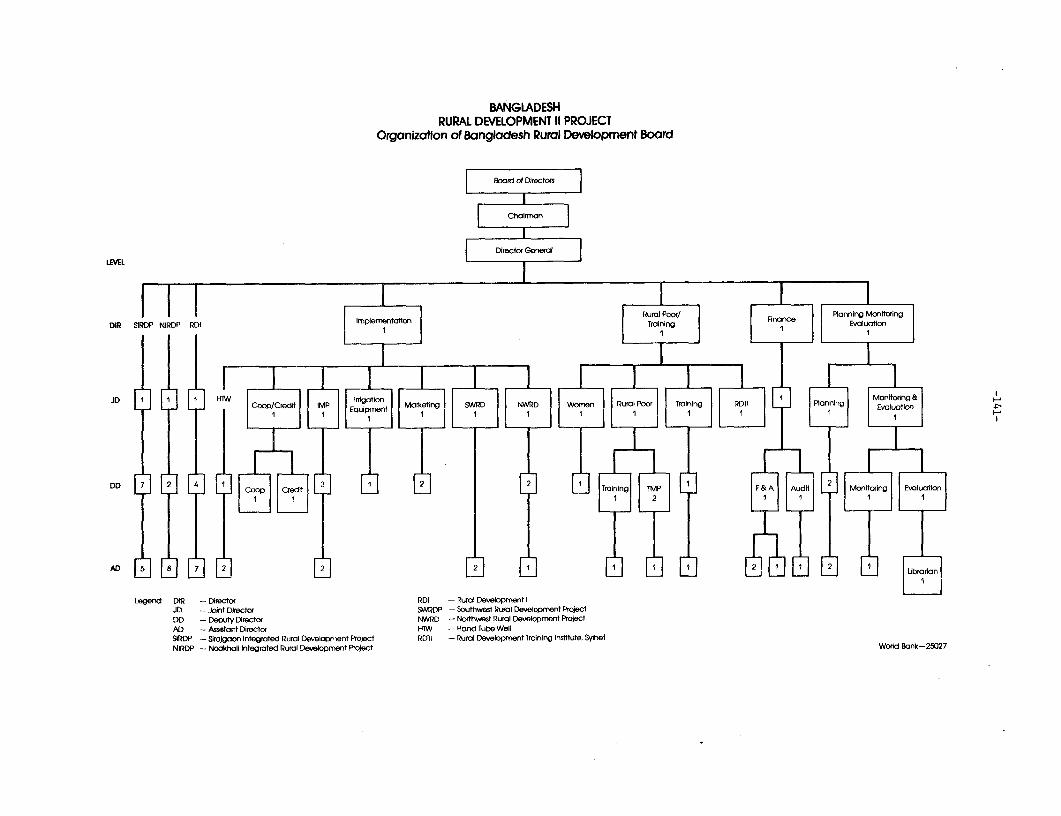

Chart No. 25027 - Organization of BRDB .................... .... 141

Chart No. 24717 - Coordination of the Rural Development Effort . 142Chart No. I - Implementation Schedule ...... ....... 143

MAPS

IBRD Map No. 17064IBRD Map No. 17066

BANGLADESH

RURAL DEVELOPMENT II PROJECT

I. INTRODUCTION

1.01 The Government of Bangladesh (GOB) has requested the InternationalDevelopment Association (IDA) for assistance in financing a Second RuralDevelopment Project. The project is based on the experience gained under anumber of IDA supported agricultural and rural development projects whichhave involved the GOB's Integrated Rural Development Program (IRDP), inparticular the first Rural Development Project, Cr. 631-BD (RD-I) and theShallow Tubewells Project, Cr. 724-BD. The policy framework of the proposedsecond project has emerged from a Joint Review of IRDP, conducted by GOB andIDA in 1980-81 and similar joint reviews of minor irrigation and agricul-tural credit sectors. 1/

1.02 A team set up by GOB prepared the project with some assistance fromFAO/CP. Further preparation was required and this was merged with appraisalof the project which started in September 1982, and was managed by theResident Mission in Bangladesh (RMB). Appraisal was completed in October1982. The preparation and appraisal team comprised Messrs. A. K. Seth,I. Ahmed, W. Kock, K. Loganathan, H. Sanger and Ms. W. Huq (IDA) and Messrs.R. Lesire, R. Raturi and K. Selvavinayagam (FAO/CP).

II. AGRICULTURAL AND RURAL DEVELOPMENT SECTOR

A. Production and Constraints

2.01 Bangladesh's economy is predominantly agricultural and agricultureaccounts for 57% of GDP, 75% of all direct or indirect employment and over80% of the country's exports. Out of a total land area of 35 million acres,about 22.5 million acres are under cultivation at a cropping intensityaveraging about 150%. Rice is by far the most important crop and accountsfor over 80% of the cultivated area; jute is the principal export andindustrial raw material crop and accounts for 6%; and a variety of othercrops, such as wheat, pulses, tobacco, oilseeds, sugarcane, and vegetablesmake up the balance.

1/ "Bangladesh Integrated Rural Development Program. A Joint Review byGOB and World Bank", October 1981.

"Minor Irrigation Sector Review. A Joint Study by GOB/IDA", draftreport, April 1981.

"Agricultural Credit Sector Review. A Joint Study by GOB/IDA", draftreport, April 1983.

-2-

2.02 Bangladesh still suffers from a chronic shortage of foodgrains,though growth in foodgrain production has accelerated in recent years andwas 2.6% over the period 1970-1981 compared to aL population growth rate of2.7%. However, annual production varies considerably, and in years of badproduction annual imports have reached 1.5 M tons. To achieve self suf-ficiency, which is a major target of GOB's development programs, wouldrequire a growth rate of 7% if it is to be achieved by 1985, the end ofGOB's Second Five Year Plan (SFYP). This would be difficult to achieve eventhough the technology for achieving this growth in production exists and hasbeen in use in Bangladesh since the mid sixties. Full exploitation of thisnew technology depends on the prompt elimination of many constraints.

2.03 Production is held back by physical, socio-economic, institutional,and resource constraints. Practically all of the 22.5 M ac cultivable landis fully utilized and increases in production must therefore come fromintensification. However, nearly two-thirds of the cultivable area isaffected by flood and drainage problems of varying intensities, and only4 M ac are protected by physical works such as embankments and drains. Dryseason irrigation, which avoids the flood problem, is now available for only4 M ac. About 70% of farms are below 2 ac in size and are often fragmentedinto as many as 10 parcels. About 25% of farm families own less than oneacre, and about 40% of all land is sharecropped. The rural power structureis well entrenched. In this situation small and marginal farmers pay dearlyfor tenure and credit, and have poor access to GOB supported services andinputs. Generally, rural areas are physically isolated due to poor roadcommunications, and they lack the basic physical infrastructure needed forthe development of rural industry or for effective administration of GOB'sdevelopment efforts.

2.04 Farmers, who are hard working and responsive to innovation, dependon a number of GOB agencies for essential inputs, credit, technical advice,and price incentives required for the widespread adoption of the HYV basedtechnology. Given the small scale of the average farmer-s needs for water,fertilizer, and credit, and the small size of his marketable surplus, GOBagencies have difficulties in effectively interacting with farmers. Inaddition, poor coordination between GOB agencies providing complementaryservices slows down the spread of the new technology. While actions areunderway to improve the performance of GOB agencies serving the farmer,fiscal constraints prohibit any significant expansion. Consequently GOB isplacing greater reliance on the private sector in providing those serviceswhich are commercial in nature and marketing of fertilizers and pesticides,import and retailing of minor irrigation equipment and their repair andmaintenance, are being increasingly privatized.

2.05 Overshadowing the problem of small and marginal farmers is that ofthe landless. Reliable data is available from the Land Occupancy Survey of1977; a new survey is to be done in 1983. Available evidence shows that the

-3-

problem has become more acute. Even in 1977, about a third of the ruralhouseholds had no land under cultivation and a large proportion ofhouseholds (20%) were seeking employment and incomne opportunities outsidethe farm sector. The rural scene is characterized by widespread poverty.Using a daily calorie intake of 2,100 as indicating the poverty line, thepercentage of rural population below the poverty 'Line has increased from 65%in 1964 to 87% in 1977 and this trend has continued. Such widespread ruralpoverty and real low wages for agricultural labor, are limiting the purchas-ing power of rural people and thus the effective demand for foodgrains.GOB-s intervention to purchase foodgrains at guaranteed prices offers only apartial and so far ineffective solution to the problem of lack of effectivedemand.

B. GOB Production Strategy and Role of TCCA/KSS

2.06 The SFYP and the Medium Term Food Production Plan (MTFPP) developedwith IDA's assistance 1/ give top priority to the achievement of foodgrainself sufficiency by increasing production from 13.5 M tons in 1978 to 20.0 Mtons by 1985. This is to be achieved by a basic strategy to make use of theinitiative of the nation's 7 million private farmers by providing them withthe resources and services that they have shown themselves to be able to useeffectively. Thus, 85% of physical investment under the SFYP/MTFPP isconcentrated on provision of water control and dry season irrigationfacilities, supply of complementary inputs and access to markets. Suppor-tive rural institutions, credit and input supply mechanisms and extensionand research are to be strengthened. Finally, greater reliance is to beplaced on the private sector, on reduction of subsidies, and on increasingefforts for domestic resource mobilization. The MTFPP started off well witha 10% increase in foodgrain production in FY81 but then ran into twounusually dry years. However, expansion of irrigation under MTFPP isproceeding close to plans (para 2.08).

2.07 Bangladesh-s own rural development model - the so called ComillaModel - originated in response to constraints similar to those describedabove (para 2.03). An integral element of the model was the establishmentof Thana Central Cooperative Associations (TCCA) located at the headquartersof the 450 thanas into which Bangladesh is divided administratively; andagricultural cooperative societies - Krishi Shamabay Samities (KSS) -located in the 68,000 villages of Bangladesh. Other components of theComilla Model were: (a) Rural Works Program, planned and implementedthrough local councils for building local infrastructure; (b) Thana Trainingand Development Center to bring together physically the various governmentagencies, local councils and TCCA; and (c) Thana I;rrigation Program to

1/ Bangladesh: Medium Term Foodgrain Production I'lan, February 1981.

-4-

utilize irrigation equipment, and maintain them. After a decade of success-ful experimentation in 20 thanas, the Comilla concept of TCCA/KSS wasexpanded nationwide under the aegis of the Integrated Rural DevelopmentProgram (IRDP), an agency of GOB's Ministry of Rural Development andCooperatives; while other components were expanded nationwide under separateprograms managed by other GOB agencies. The Joint Review by GOB and IDAreviewed the nationwide performance of IRDP. The Review, the report ofwhich was approved by the Cabinet in August 1982, found that the TCCA/KSSsystem had been playing a useful - through far below potential - role infurthering GOB's agricultural and rural development plans and that it was avaluable resource to be used for achieving objectives of GOB's developmentplans. As recommended in the Joint Review, IRDP has recently been estab-lished as an autonomous Bangladesh Rural Development Board (para 2.17).

Minor Irrigation Development

2.08 In the Bangladesh context, with substantial surface water flows butwith a topography that almost excludes any large scale gravity irrigation,farmers have traditionally depended upon small scale lift irrigation fromsurface water bodies using Low Lift Pumps (LLPs) of 1-2 cusec capacity.Since the early seventies, however, Bangladesh's large ground water resour-ces have been increasingly exploited for irrigation in the dry season bydiesel engine operated Shallow Tubewells (STWs) of 0.5-0.75 cusec capacityand Deep Tubewells (DTWs) of 2 cusec capacity as well as by simple manuallyoperated Hand Tubewells (HTWs) capable of irrigating half to one acre ofland. LLPs, DTWs, STWs and HTWs are collectively referred to as minorirrigation equipment. Minor irrigation development is a key component ofthe MTFPP, and its expansion up to end of FY82 was generally encouraging,except for HTW and DTW programs which were constrained by poor supply ofequipment to meet farmer demand.

MTFPP Target Actual % Above/For July 1, 1982 Achievement Below Target

STW in Operation 58,000 63,300 + 9DTW in Operation 13,000 11,490 - 11.5LLP in Operation: 1 cusec 10,500 12,200 + 16

2 cusec 33,500 30,400 - 9HTW Sales 175,000 135,800 - 22

2.09 Groundwater resources, which are expected to provide 45% of theirrigation water used for agricultural production by 1985, are very ade-quate. Bangladesh is part of a geological basin which contains a majoraquifer complex saturated with groundwater. Three major inter-connectedwater bearing zones, the composite aquifer, the main aquifer and the deepaquifer have been identified. The composite aquifer, at a depth varyingfrom a few meters in the north to as much as 60 meters in the south, con-sists of silty to fine sand overlaying the main aquifer. Extraction from

-5-

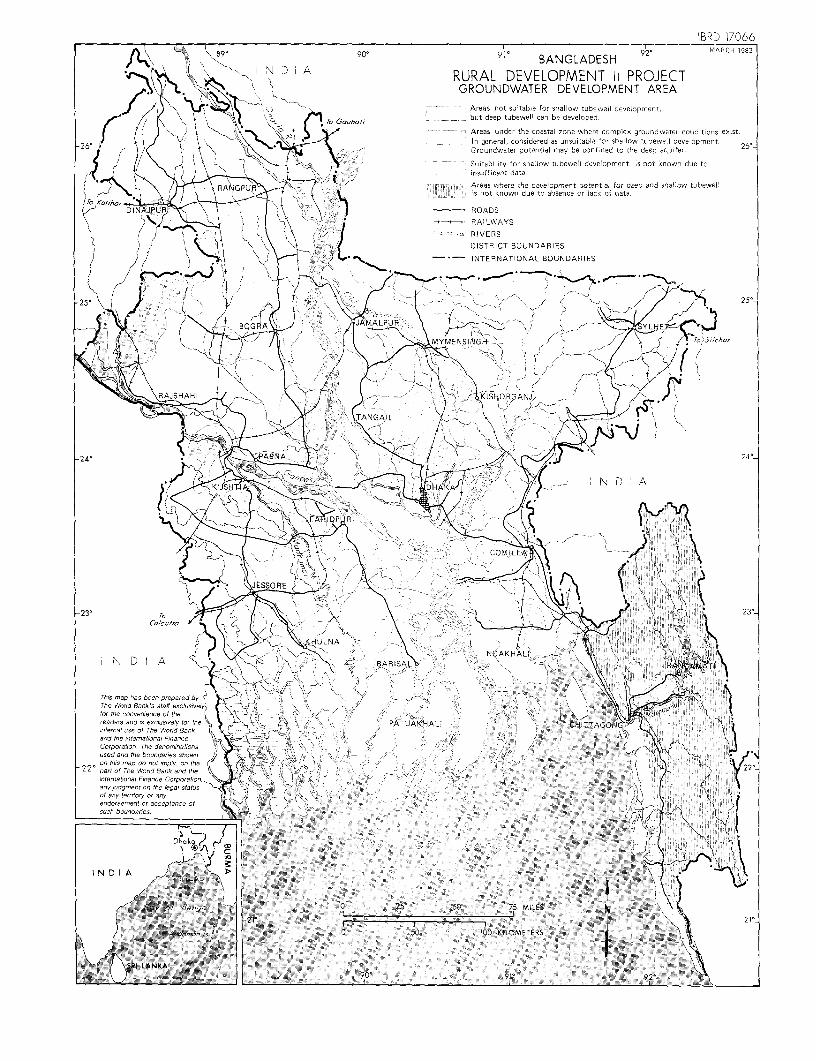

this aquifer is possible by shallow tubewells for irrigation as well as forrural water supplies. The main aquifer consists of medium and coarse-groundsandy sediments, occasionally inter-bedded with gravel, which extends todepths averaging 140 meters. Extraction is by deep tubewells primarily forirrigation (see Map). The deep aquifer, ranging from 150 meters to 450meters in depth, has been mainly exploited for urban and industrial watersupplies in Dhaka and in the coastal areas. Present groundwater resourcesare utilized as follows:

Million Ac/Ft %

Groundwater resources in main andcomposite aquifer 24.4 100

Present extraction from main andcomposite aquifer 2.8 11

Planned extraction by 1985 forirrigation (MTFPP target) 13.0 53

Source: UNDP - "Groundwater in Bangladesh", draft, April 1982.

2.10 The policy framework for the development of the minor irrigationsector is based on the experience gained under a number of GOB and IDAfinanced projects, and was drawn up in the course of the Joint GOB/IDAReview of the minor irrigation sector. It is now basic GOB policy toencourage private ownership of irrigation equipment rather than their rentalfrom GOB as in the past, and to encourage the private sector in the import,retailing, and subsequent servicing of these equipment, rather than operatea GOB monopoly for these activities. IDA financed Agricultural CreditProject (1147-BD) has assisted GOB in its first major effort to supportprivate sector import and retailing of STWs. STWs have for long been soldto farmers at full cost, but sales of new LLPs and DTWs are presently sub-sidized by 20% and 75Z respectively. LLPs and DTWs previously owned by GOBhave now been put on sale, supported by credit. GOB is gradually reducingsubsidies with the aim of progressively eliminating them. Since 1980,rental rates charged for LLPs and DTWs which still remain with GOB have beentrebled and subsidy on sale of new LLPs has been halved, while the sellingprice of DTWs has been increased by 40%.

2.11 A critical factor in the effective development of irrigated agricul-ture is the relatively large areas (DTW 100 ac, LLP 40 ac, STW 15 ac) whichneed to be irrigated for the economic operation of the existing minorirrigation equipment, which are almost all operated by diesel engines. Asrural electrification expands, small horsepower units would become economi-cally feasible. Given the small size and fragmentation of holdings and thevast number of farmers to be reached, farmers have to work in groups to

-6-

optimize the use of such equipment. The Joint Review has supported theencouragement given by GOB to TCCA/KSS for expanding their role in minorirrigation development.

2.12 TCCA/KSS participation in the national minor :Lrrigation program hasbeen important and has been regularly supported by IDA under its project andprogram credits. For example, in 1980, as part of IDA's Imports X ProgramCredit (Cr. 1194-BD), GOB launched a nationwide program of term credit toTCCA/KSS for purchase of minor irrigation equipment and such purchases havebeen significant in recent years as shown below:

National Sales of Minor Irrigation Equipment

FY81 FY82% Purchased % Purchased

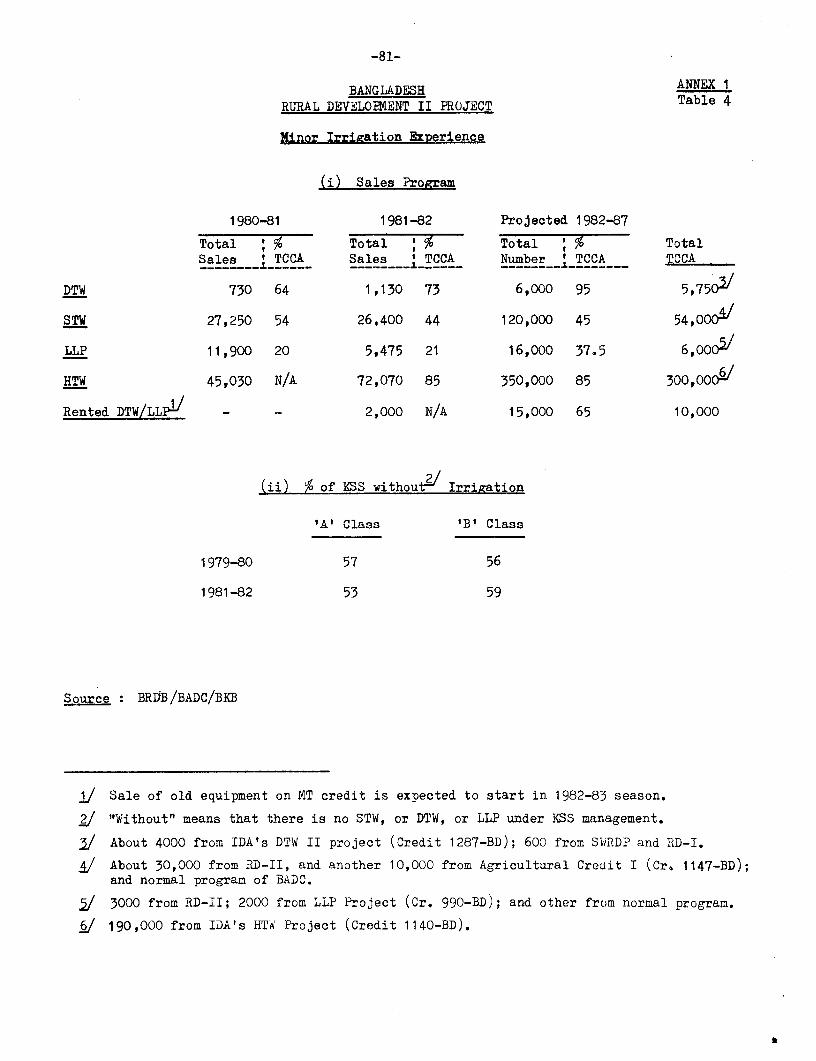

Total Sales by TCCA Total Sales by TCCA

DTW 730 64 1,110 73STW 27,250 54 26,400 44LLP 11,900 20 5,475 21HTW 45,000 N/A 72,000 85

However, less than 45% of existing A- and B class KSS 1/ have irrigationfacilities.

Irrigation Management Program (IMP)

2.13 Minor irrigation equipment is currently irrigating an average of20-25 acres for one cusec installed capacity while the potential would be atleast 50% greater. Primary reasons for the under-utilization of equipmentis the poor organization and management of user groups. To remedy thisproblem, Irrigation Management Program (IMP) was introduced in the RD-IProject in 1979-80. Under IMP, BRDB, BADC and Department of AgriculturalExtension (DAE) officers at the district and thana levels jointly supportthe TCCA to increase the command area per irrigation equipment and thusreduce the cost of irrigation. Essential features of the program are:(a) preparation of action plans; (b) organizing KSS meetings to explainutility of water management; (c) training of managers, and chairmen of KSS,TCCA inspectors, village accountants, block leaders, fieldmen, and tubewelloperators; (d) preparation of land maps and land registers; (e) laying ofirrigation channels; (f) preparation of irrigation budgets; and (g) obtain-ing credit for production costs. The program has been. very successful

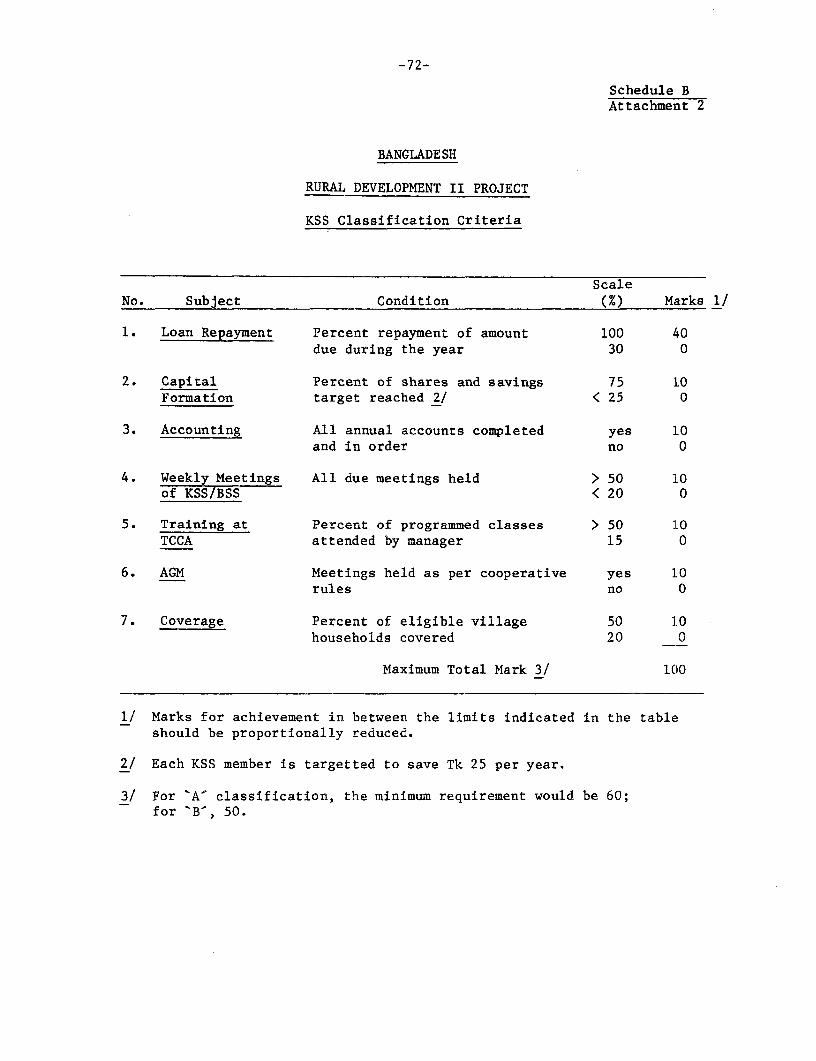

1/ Since 1980, IRDP has a system of classifying KSS according to perfor-mance on membership, loan recovery, savings, and related factors(Schedule B); 'A and -B class KSS are judged to be active and viable.

-7-

(Annex 1, Table 10). During 1981-82, IMP covered 43 T(CA and 430 irrigationunits and on average increased command areas by 53%, farmer participation by35% and yields by 15%. Because of such promising results, GOB has decidedto replicate IMP on a nationwide basis and has published a comprehensivemanual in Bengali for implementing IMP. BRDB has been given the respon-sibility for monitoring IMP activities and Rural Development Academy, Bograthe responsibility for training GOB staff with the assistance of an UNDP/FAOproject. IDA is supporting the implementation of IMP in three districtsunder the DTW II Project (Cr. 1287-BD).

Rural Institutions

2.14 The TCCA/KSS system is the basic system of farmer cooperatives andbetween 1978 and 1982, the system has grown as follows:

FY78 FY82

Number of TCCA 250 350Number of KSS 27,500 48,800% of 'A' and 'B' Class KSS N/A 48Paid Membership ('000) 844 1,690Total Savings and Shares (Tk M) 54 163

2.15 This growth has been achieved despite a difficult environment inwhich the system has been unable to guarantee the flow of services most indemand by its members. Thus apart from 74 TCCAs, which are thebeneficiaries of projects financed by IDA and other donors, the services ingreatest demand by members - minor irrigation equipment, medium term credit,fertilizer, and seed - have been rarely available to the TCCA, because ofthe failure of the public sector agencies controlling their supply to meetTCCA demands. These problems have not been totally absent in the case ofTCCA assisted by IDA, though the position has been much better; as has beenthe performance of these TCCA compared to others. This is evident by comi-parison between the 7 TCCAs of RD-I Project and the nationwide TCCA program:

Bangladesh RD-I

Number of TCCA 350 7Number of KSS per TCCA 139 200% of 'A' and 'B' Class KSS /a 48 49Number of Members per KSS 35 54% Farm Families covered in adopted thanas 20 41% Membership of -A- and 'B' Class KSS borrowing 32 77LLP and STW purchased per TCCA per year in FY80-82 47 250

/a RD-I average figure is low because for the 1,070 KSS in theDistrict of Mymensingh, where only DTWs are feasible, no irrigationfacilities have yet been provided.

-8-

2.16 While the TCCA/KSS system has expanded rapidly in recent years, itsqualitative performance is far less impressive. For example, abouttwo-thirds of the membership of A' and B' class KSS does not participatein the system's credit program, partly because of cumbersome procedures andpartly because 55% of these KSS do not yet have irrigation facilities whichtend to drive the demand for credit. At least half of the KSS which havebeen organized are not active, partly because of the problem of providingreal services to their members. Problems of equity and maladministrationare pervasive even among the active KSS; for example, while the membershipof the small and medium size farmers reflects the general situation, themanaging committees tend to be dominated by larger farmers. 1/ In partthese problems arise because of the ineffectiveness of the Department ofCooperatives in ensuring the holding of Annual General Mleetings, conductingof timely audit, weaknesses that in part are due to ambiguities in coopera-tive laws (para 2.22).

2.17 The Bangladesh Rural Development Board (BRDB) which promotes thegrowth of the TCCA/KSS system, was established by GOB in December 1982. Itsestablishment eliminated the uncertainty that in recent years has shroudedthe status of IRDP and its staff; an uncertainty which had led to con-siderable demoralization of the staff responsible for promoting the TCCA/KSSsystem. BRDB is managed by a Governing Council, of which the Minister ofRural Development and Cooperatives is the Chairman, and Secretary RuralDevelopment, the Vice Chairman, and whose other members are:

- Secretaries of Agriculture and Forests, Fisheries and Livestock,Irrigation, Water Development and Flood Control, Local Government,Finance, and Energy divisions (6);

- Chairman of BADC (1);

- Registrar of Cooperatives (1);

- Member (Agricultural and Rural Institutions), Planning Commission (1);

- Director, Rural Development Academy, Comilla (or Bogra, alterna-tively) (1);

- Representative of a major financial institution (1);

- Chairman, Bangladesh Small and Cottage Industries Corporation (1);

1/ In a sample of 25 TCCAs, 44% of the members of the managing committeeswere from among farmers who had more than 5 ac of land, while only 23%of the membership was from this group.

-9-

- five elected Representatives from the National Federation of TCCAs (5);

- one Nominee of the National Cooperative Union (1);

- Director General, BRDB, as Member Secretary (1).

2.18 Under its charter, the role of BRDB is to:

(a) promote village based cooperatives and TCCA so that they become, inthe shortest possible time, autonomous, self- managed and viablevehicles for increasing production, employment and rural develop-ment;

(b) encourage functional cooperatives for sponsoring income generatingactivities for the rural poor;

(c) promote intensive irrigated agriculture as a means of cooperativedevelopment as well as for efficient use of irrigation facilities;

(d) channel and ensure productive utilization of institutional creditthrough village cooperatives and TCCA system and promote membersaccumulation of deposits and savings;

(e) encourage financially viable TCCA to diversify activities, espe-cially in marketing of agricultural inputs and produce;

(f) arrange for effective training of members;

(g) promote the growth of federations of TCCAs at the district andnational levels with a view to progressively hand over to them thepromotional, motivational and educational functions relating torural development;

(h) liaise with concerned agencies for mobilizing supplies, services andsupport for the cooperative system; and

(i) engage competent evaluation teams and research institutions to studyand evaluate the progress made and effectiveness of the projects andprograms of the Board.

2.19 A Director General, a GOB official of the rank of AdditionalSecretary, is the Chief Executive of BRDB. He is presently supported bythree Directors, responsible for Implementation, Monitoring and Evaluation,and, Finance and Administration. At Dhaka, BRDB currently has about 40officers and in the field its strength will increase to 1,500 from 1,000 asTCCA are established in all 450 thanas. The BRDB-s 22 district offices arestaffed by a Project Director (PD), and two Deputy Project Directors (DPDs)with a small accounts cell. PDs monitor the implementation of BRDB's

-10-

projects, assist in promotional activities and most importantly ensure theavailability of inputs to TCCA from GOB and private sector agencies at thedistrict level. To facilitate the development of TCCA, BRDB recruits,trains and seconds to each TCCA, three key staff: a Thana Project Officer(TPO), a Deputy Project Officer, and an Accountant whose salaries BRDB pays.The TPO works as the Secretary to the Managing Committee of the TCCA. Thecommittee is elected for a one year term. All other staff of the TCCA(approximately 25 inspectors and village accountants) are paid out of TCCAs'own earnings.

2.20 BRDB operates a Rural Development Training Institute (RDTI) atSylhet. The RDTI is used for staff training, but because facilities arestill incomplete, in-service and pre-service training of BRDB staff arelagging behind requirements. Facilities of the Rural Development Academy(RDA) at Comilla and the recently completed Bogra RDA 1/ also are used tothe extent available by BRDB for staff training. The two RDAs undertakeaction research in rural development strategies and also organize specialtraining for innovative programs to be executed by TCCA/KSS. The RDA, Bograhas gradually become the focal point for the training for IMP (para 2.13),and is presently engaged in useful action research in the field of specialprograms to create income generating activities for the rural poor (para2.41).

2.21 The Registrar of Cooperative Societies (RCS) is responsible for theregistration, audit and inspection of all cooperatives under the CooperativeSocieties Act, 1940. RCS staff, which number 2,250 have not increased asthe cooperative network has grown. RCS staff also promote and supervise theoperation of the non-Comilla type (or traditional) cooperatives, only 6-10%of which are active. This has overburdened the RCS. As a result, as ofOctober 1982, audits of 12,000 KSS and 83 TCCA were overdue for more thanone year. To train the auditors responsible for KSS audit, RCS operates aCooperative College in Comilla (CCC), whose facilities are underutilized dueto financial constraints. Thus quality of audit has deteriorated steadily.In recognition of this weakness, audit of TCCAs under IDA assisted projectsis currently assigned to locally recruited firms of auditors.

2.22 Following the completion of the Joint IRDP Review, GOB has decidedto merge the two cooperative systems, TCCA/KSS and traditional, startingfrom the village level and also to reallocate the role of the RCS, BRDB,TCCA and the bank which finances the TCCA so as to maintain a system ofchecks and balances. The reallocated functions are:

1/ Completed under IDA assisted Agricultural and Rural Training Project,Cr. 621-BD, for improving the quality of rural training programs andresearch related to rural development.

-ll-

Financing

Function RCS BRDB TCCA Bank

Audit / - - -

Inspection (Act and Rules) _ - - -

Registration / - -

Promotion - / _

Credit: Sanction - - - _/

Disbursement - - I -

Collection - - /

Internal Audit - / -

Supervision: Overall Performance - _/

Credit - J - I

Cooperative laws which the Registrar administers, have not been reviewed

since 1940. These laws have been found in practice to be ineffective indealing with credit defaulters and in regulating mis-managed cooperatives.

Current rules, because of their ambiguity, allow chairmen of defaulting KSSto be represented on the managing committee of a TCCA. Other necessaryimprovements relate to the one year term of elected member which is shortfor good management, secret ballotting, reservation of one position on themanaging committee for a BSS member and creation of a bad debt fund. GOB isundertaking an amendment of the Cooperative Act to overcome these deficien-cies.

Rural Credit

2.23 Since 1976, when the Special Agricultural Credit Program (SACP) waslaunched, Bangladesh has operated a multi-agency approach to provideinstitutional credit to farmers. All six Nationalized Commercial Banks(NCBs), Bangladesh Krishi Bank (BKB) and Bangladesh Shamabaya Bank Ltd.(BSBL) which is the apex bank for the traditional cooperatives, have par-ticipated in it. Bangladesh Bank (BB) has supported SACP by liberalrefinance, on average refinancing 40% of total agricultural lending.However, the TCCA/KSS system was excluded from SACP and received its financefrom Sonali Bank, a nationalized commercial bank, without access torefinance from BB. Total lending for agriculture has increased fromTk 470 M in FY76 to Tk 4,395 M in FY 82. The relative lending operations ofcredit agencies are as follows:

-12-

Lending by Credit Agencies(FY82)

Total (Tk M) % % Refinancecl by BB

BKB /a 2,710 62 47NCBs 1,226 28 26BSBL 186 4 94TCCA/KSS 273 6 0

4,395 100 40

/a Including BKB's diversified lending for agro industry andtea which amounts to nearly 45% of its total lending.

2.24 GOB has placed considerable emphasis on rural credit and as aresult, the number of rural branches of NCBs and BKB has now reached 2,850.Compared to only a third in 1972, these branches now comprise nearlytwo-thirds of all NCB/BKB branches. In addition, credit is available at27,000 'A' and 'B' class KSS. This has contributed to the expansion ofrural credit and deposits. Rural deposits account for 16% of total depositswith the above institutions and rural advances now account for 95% of ruraldeposits compared to only 34% in 1975. All TCCA deposits are kept withSonali Bank. In 1982, these amounted to Tk 245 M or 89% of TCCA/KSS annuallending. About two-thirds of these deposits were thrift savings and sharedeposits; the remaining were accumulated profits and surpluses.

2.25 TCCA/KSS as a group tend to reach smaller farmers and thus to sup-port a much larger number of farming households than indicated by the sys-tem's share of total lending volume:

Loan Size and Borrowers(FY81)

Average Loan Size No. of Borrowers /a (%)(Tk)

BKB 5,360 390,000 (28)NCBs 1,380 680,000 (48)TCCA/KSS 915 330,000 (24)

National 1,910 1,400,000 /a (100)

/a BSBL data is excluded because of its unreliability.

-13-

2.26 Despite the uncertainty and serious morale problem that hasafflicted BRDB staff since 1976, the relative loan recovery performance ofthe TCCA/KSS system is satisfactory. Loan recovery can be measured in twoways; as a loan recovery profile, or as an annual recovery index. Theprofile shows the percentage of recovery at a point in time against loansgiven in each fiscal year. As loans given in a particular year are col-lected over the following years, the profile shows an increasing trendapproaching 100% performance for good recovery and stopping at much below100% for poor performance. Loan recovery profiles for various institutionsare shown below:

Loan Recovery Profile

% Recovery of Principal and InterestLoans as of June 30, 1982 Total

Disbursed in BKB Sonali BSBL TCCA Average LendingS7 (S) (N) (Tk M)

FY77 94 90 98 81 97 88 986FY78 82 83 94 82 95 82 1,570FY79 66 74 93 80 90 79 1,850FY80 50 57 74 73 75 64 2,906FY81 31 36 42 58 49 43 3,622

N: Bank's own "normal" program not refinanced by BB.

S: 100-Crore Agricultural Credit Program. For BKB, 'N' data isbiased by lending to tea plantations and agro industry whichis nearly 45% of total; but data excluding these is not available.

2.27 Annual recovery index measures the actual recovery in a 12 monthperiod of a fiscal year, against total including previous overdues, due forrecovery during the fiscal year. This index has tended to deteriorate forall credit agencies, and GOB is taking action, which would be supportedunder the project, to arrest this trend.

-14-

Annual Recovery Index for Farm Credit

FY80 FY81 FY82

BKB (S) /a 36 32 30NCBs /b 47 38 38BSBL 27 22 22TCCA 58 47 40

/a BKB normal program, because of its bias dueto tea plantation and agro business credit,is not comparable.

/b Excluding TCCA/KSS lending.

2.28 BSBL, the national apex bank of the traditional cooperatives hasoften been suggested as the logical agency for refinancing the TCCA/KSS.However, the Agricultural Credit Review has indicated that major reform ofBSBL will be required to allow it to become so. This is now under con-sideration of GOB but the nature of the changes is such that their implemen-tation will require a gradual approach starting in a limited geographicalarea, possibly a district or subdivision. Hence, the possibility of BSBLbeing used as a channel for TCCA lending under the proposed project isremote.

2.29 Sonali Bank (SB) is the largest commercial bank in Bangladesh withthe most experience in agricultural lending. Its total agricultural lendingwas Tk 740 M in FY82, about 35% through TCCA. SB's total assets increasedfrom Tk 9,000 M to Tk 24,000 M between FY77 and FY81, while deposits grewfrom Tk 4,500 M to Tk 9,500 M over the same period. In 1980-81 it made anet profit of Tk 232 M. While profitable overall, 55% of its newly estab-lished rural branches showed losses. Its accounting system is satisfactoryand bad debt reserves for agriculture (Tk 70 M) fully cover agriculturaloverdues more than 3 years old. SB operates through 1,026 branches (705rural) and has established a rural credit department with 50 professionalstaff at head office, headed by a deputy general manager. Field staffconsist of about 1,000 special agricultural workers supervised by 37agricultural graduates and farm technologists. SB has excellent trainingfacilities, and training in agricultural lending is being added to itstraining programs.

2.30 SB is participating in all IDA and donor assisted projects providingcredit to TCCA. Current TCCA/KSS lending terms and conditions allow someflexibility for delayed recoveries at the TCCA level, but are essentiallystrict at the KSS and member level where 100% repayment of past loans is acondition for further loans. In Bangladesh, with its complex croppingsystems, the inputs of a crop are often required before a farmer can sell

-15-

off and repay the loans for a preceeding crop. Such requirements and cum-bersome loan sanction procedures have tended to restrict the growth inlending volume. In addition, Sonali Bank has little incentive to lend toTCCA since it has been denied the normal refinance available at 6% fromBangladesh Bank under SACP. Furthermore, given that the Sonali Bank branchmanager receives his funds for lending to a TCCA at an internal transferprice of 11% and lends it to the TCCA at 7.5%, the branch manager has noreal incentive to increase lending to TCCA. These and other factors con-straining the credit program of the TCCA have been studied in the GOB/IDAJoint Reviews of IRDP and of Agricultural Credit. The fact that many suchobvious anomalies have been permitted to exist for so long is one of themost important reasons why progress in agricultural development inBangladesh has been less than what it would have been. The changes neededto reform the TCCA/KSS credit system, which would be implemented under thisproject, are discussed in Chapter IV.

2.31 Apart from financial procedures and interest rates, per acre ceil-ings on loans are prescribed by BB for various crops on the basis of recom-mendation of the Ministry of Agriculture. They have left much to be desiredand were stagnant for almost three years. These have recently been revisedto satisfactory levels based on the recommendation of the AgriculturalCredit Review:

Crop Credit Ceilings (Tk/Ac)

Old New

Wheat 550 1,500Boro 800 2,000T. Aman 700 900Aus 650 1,000Potato 1,000 4,000Tobacco 600 1,250

Rural Infrastructure

2.32 GOB's effort to achieve rural uplift is now reflected in thedecentralization of administration to the thana level and a concurrentemphasis on rural roads, rural electrification, development of physicalfacilities at the thana headquarters, and the establishment of rural inputsupply and marketing facilities. Excluding the national and district high-ways there are 60,000 miles of village to market roads, 13,000 miles ofroads connecting union and thana headquarters, and 5,000 miles of ruralfeeder roads, which connect thana HQ and important market places. Over 85%of these roads are in need of major repair and construction. GCIB is nowstrengthening its Rural Works Program (RWP) to improve these roa,ds. A ruralroads project is being prepared for IDA financing. GOB attaches; highpriority to rural electrification and many donor assisted projects including

-16-

one financed by IDA (Cr. 1262-BD), are now under construction in 100 thanas.The Rural Electrification Board (REB) includes a representative of BRDB.REB presently operates some 120,000 rural connections, more than 85% ofwhich are domestic.

2.33 Thana Training and Development Centers (TTDC) are built by GOB forthe use of its officials posted to the thana. A TTDC complex is owned bythe Thana Council and typically consists of a two-storey building with12,000 sft. office space and a training hall, plus 15-25 ac of land toaccommodate housing, demonstration plots, TCCA buildings, workshops, dieselfuel tanks, fertilizer godowns and other similar facilities. All but 40thanas in the country have a TTDC. About 16 key GOB officials are eligibleto be provided with housing in the TTDC when available. Allowing for 260donor financed units now under construction, about 820 additional housingunits are needed to provide essential housing facilities in all thanas asshown below:

Availability of Staff Housing at TTDC

--- % of Thanas with

4 Units 918 Units 7812 Units 3816 Units 6

About 276 TCCA do no yet have an office building but about 135 are to bebuilt under ongoing projects.

Input Supply and Marketing

2.34 Input Supply: Until 1978, the supply of farm inputs to farmers hadbeen the monopoly of BADC which owns, rents and operates 1,124 godownstotalling 360,000 tons capacity and currently markets 850,000 tons of fer-tilizers annually. Under a New Marketing System (NMS) introduced in 1978,BADC has withdrawn from its Thana Sales Centers (TSC) to about 110 primarydistribution points, except in about 120 'remote thanas where for variousreasons, the response from private sector dealers has been poor. NMS nowcovers the entire country. It has been judged to have been successful 1/ inintroducing the private retailing of fertilizers. Prior to the introductionof NMS, BADC had given wholesale distribution rights in their thanas toabout 65 TCCA which either owned or rented godowns. For these TCCA the NMS

1/ A formal joint evaluation by GOB/USAID is presently underway and areport is expected by March 1983.

-17-

has led to the loss of their market share from 55% to 17%. A greater con-cern to GOB is that in these thanas, along with the reduction in TCCA marketshare, total sales of fertilizers have declined by 35% between 1980, whenNMS was extended nationwide in 1982 (Annex 1, Table 5). GOB has now takenaction to remedy this situation by:

(a) asking BADC to continue to provide fertilizer to TCCAs on credit;

(b) renting BADC godowns to TCCAs at those TSC which have been closeddown;

(c) offering fertilizer wholesalership to TCCAs in -remote- thanas; and

(d) encouraging TCCA to extend fertilizer marketing to the KSS levelusing the experience of an FAO assisted fertilizer marketing pilotprogram, which has demonstrated that fertilizer sales increasesignificantly when supported by credit and made available at theKSS.

2.35 Most farm produce is marketed immediately after harvest. Because ofthe need for cash, problems of on-farm storage and need to repay cropproduction loans, most farmers are unable to hold stocks over an extendedperiod. The private sector handles roughly 75-80% of the marketed grainthrough 8,500 primary markets. Farmers have the option to sell t:heir grainto the Ministry of Food (MOF) which operates a price support program pur-chasing foodgrain at about 850 locations. It is estimated that only 20%of MOF procurement of grains comes directly from farmers because farmersfind the MOF purchase centers inaccessible and purchase and payment proce-dures complicated for the typically small amounts (2-10 mds) they have forsale. Since 1979 GOB has been developing a new TCCA/KSS based paddy andrice marketing system. The so called 'Mukta' marketing project is now intrial operation in four TCCAs, under the IDA financed Second FoocdgrainStorage project (Cr. 787-BD). Under the pilot project farmers retceivepayment for their sales at the KSS at the going market price within 24 hoursand later receive two bonuses, one from KSS and the other from TCCA afterfinal sales. Over the last nine marketing seasons, the final price receivedby farmers from TCCA after covering all operating costs has been 26% higherthan MOF official purchase prices.

Support Services

2.36 GOB provides agricultural extension services through the Departmentof Agriculture. An IDA supported Extension and Research Project (Cr.729-BD) has helped establish in five districts of the country a singletraining and visit (T&V) type extension system that replaced six separateservices that operated on a separate crop basis. A follow-up Second Exten-sion and Research Project (Cr. 1215-BD) is helping to extend the system andunification on a nationwide basis. A farmer to extension worker ratio of

-18-

1,000:1 is expected to be achieved by 1987. Training of the extension staffis at 14 Agricultural Extension and Training Institutes (AETIs), four ofwhich were built under IDA financed Agricultural and Rural Training Project(Cr. 621-BD).

C. Special Programs for the Rural Poor

2.37 It has been estimated that if production targets of MTFPP arereached, agriculture can at best absorb only about 20% 1/ of the expectedaddition to the rural labor force expected by 1987. In an attempt toalleviate the problem a number of programs to reach the rural poor and toincrease their incomes have been initiated by GOB. These include Food forWork (FFW) and Rural Works Programs (RWP); programs of Bangladesh Small andCottage Industries Corporation (BSCIC) and Bangladesh Handloom Board (BHB),the work of many Non-Governmental Organizations (NGOs); and special programsunder BRDB.

2.38 Rural Works and Food for Work programs involve an expenditure ofabout US$100 M annually and generate about 90 M person days of employmentand undertake the construction of productive physical infrastructure such asflood control embankments, rural roads and drainage channels. The qualityof works is generally not good, especially under FFW which is often treatedas a welfare program. RWP operates through the Thana Plan Book, whichcontains a phased 10 year plan for high priority infrastructure developmentand include detailed maps showing location of existing structures, floodinglevels, drainage flows and proposed developments. Virtually all thanas havea Plan Book but many have not been updated since they were first dlrawn up inthe sixties.

2.39 The Bangladesh Small and Cottage Industries Corporation (]3SCIC)helps develop entrepreneurship in rural industries such as carpet weaving,cottage industries and workshops. For this purpose BSCIC has established 20industrial estates, limited thana level extension services, and a trainingcenter in Dhaka. It has completed special rural industry surveys in threedistricts. A BSCIC-s subsidiary, the Bangladesh Handicraft Marketing Cor-poration (BHMC) undertakes domestic as well as export sales of handicrafts.The Bangladesh Handloom Board (BHB) promotes the local handloom industry byproviding training to a member of a loom owning family, and operat:ing a yarndistribution system. At 17 special weavers' centers, it now provides inputand marketing support to about 100,000 weavers.

1/ This compares with the SFYP target to absorb 39% of the incrementallabor force in crop production, 23% in non-crop agriculture, 12% insmall scale rural industries, and the remaining 26% in other sectors.

-19-

2.40 Non-Governmental Organization (NGO) have been assisting the ruralpoor of Bangladesh since independence. Small but successful programs havebeen carried out by Bangladesh Rural Advancement Committee (BRAC),Proshikha, Grameen Bank, and Small Farmers Development Project (SEDP) ofFAO. Their activities are detailed in Annex 1, Tables 12 and 13, andsalient facts are shown below:

Pilot Programs for Rural Poor

BRAC Proshikha SFDP GBP BRDB

Estimated number ofbeneficiaries 16,000 10,000 1,700 25,000 15,000

Credit volume up toJune 1982 (Tk M) 10.5 2.3 16.4 68 20.8

Loan recovery againsttotal due (%) /a 94 80 81 99 /b 84

Village covered N/A 950 46 440 3,500

/a Since inception of each program; thus figure is biased towards older ones/b GBP policy allows loans to remain current provided some repayments,

even if partial, are being made and thus its recovery is overstated.

The NGOs have focussed their credit program on landless laborers, marginalfarmers and disadvantaged women with simple activities such as beef fatten-ing (20%); rickshaw pulling (11%); paddy husking (22%); oil milling (4%);weaving (6%); pond fisheries (2%), irrigation assets (2%); and others (33%).About 37% of the beneficiaries are women. NGO's programs have notencouraged formal grouping of beneficiaries but informal groups of peopleinvolved in similar activities are established and members are encouraged tosave systematically at weekly meetings. NGOs get no financial support fromGOB, except in the case of GBP for which Bangladesh Bank and NCBs bear thecost of promotion, motivation and loan supervision. In FY82 these amountedto roughly Tk 4 M or 20% of loans outstanding.

2.41 BRDB activities to assist the rural poor are also of recent origineven though in the sixties a Special Cooperative Federation (SCF) was set upin Comilla TCCA to cater to the landless and other occupational groups. TheSCF supported 24 agro-based as well as non-farm activities for these groupsand about 100 primary societies with a total membership of about 6,345 arestill operating under the SCF. BRDB started its programs to assist therural poor only in 1977. By 1982, it had established about 2,500 specialcooperatives for the landless with a total membership of 69,000. BRDB alsostarted in 1979 a special program for promoting rural women's cooperativesunder IDA supported Population Planning and Health Project (Cr. 921-BD). So

-20-

far about 100 such cooperatives have been financed and a recent survey hasshown that 15% of their members depend upon wage employment as the primarysource of income. Activities supported under BRDB programs are similar tothose discussed earlier. Major problems faced in the implementation ofthese programs of BRDB have been delays in the registration of newsocieties, delays in the flow of credit, training and extension support anda lack of management focus in BRDB to implement a more extensive program.

2.42 For the design of successful programs for the rural poor some usefullessons have been learnt from the pilot projects undertaken so far. Theseare that:

(a) a group approach which brings together the rural poor with similarsocio-economic background into separately organized productive unitsis necessary for dealing with the established rural power structureand for ensuring adequate supply of inputs and services;

(b) there exist a number of traditional rural occupations which canprovide income earning opportunities for which the necessary skillsare already available with potential beneficiaries;

(c) availability of institutional credit at unsubsidized rates is essen-tial for the rural poor to undertake productive activities and highrepayment rates can be achieved for credit given to landless groups,under adequate technical guidance;

(d) training for the catalysts as well as group leaders is essentialto give them the necessary skills to deal with the rural poor, andbuild up their confidence;

(e) design of such a program needs to be light on planning and strong onevaluation to allow innovation and adjustments based on experienceof implementation; and that the beneficiaries need to have con-siderable say in the choice of activities to be undertaken; and

(f) such a program can make effective contribution to help landlesswomen, who have generally been left out of the development process.

D. IDA Operations in Agriculture and Rural Development

2.43 Since independence in 1971 until March 1983, the Bank has assistedagricultural development in Bangladesh with 20 credits for projects in theagricultural sector and two fertilizer import credits. Total lending foragriculture over this period amounts to about US$450 M, or 20% of total IDAlending to Bangladesh.

2.44 The main thrust of GOB's SFYP, and in particular of the MTFPP, isstrongly endorsed by IDA. This is reflected in the composition of IDA's

-21-

lending program which provides strong support for achieving the objectivesof MTFPP, particularly in the areas of irrigation and drainage and floodcontrol. These projects are:

(a) Low Lift Pump Project (Cr. 990-BD);(b) Hand Tubewells Project (Cr. 1140-BD);(c) Agricultural Credit Project (Cr. 1147-BD);(d) Deep Tubewells II Project (Cr. 1287-BD);(e) Drainage and Flood Control I Project (Cr. 864-BD);(f) Small Scale Drainage and Flood Control Project (Cr.955-BD); and(g) Drainage and Flood Control II Project (Cr. 1194-BD).

Preparation is underway on a Drainage and Flood Control III Project and aWDB Sector Credit.

2.45 As recognized in GOB's overall strategy, rural institutions must bedeveloped to enable Bangladesh's predominantly small farmers and landlesspeasants to be provided with inputs, credit and income generating oppor-tunities and to be organized into groups for the effective utilization ofirrigation equipment. The nearly complete RD-I Project 1/ and this proposedsecond project are designed to support this institutional developmenteffort.

2.46 The First Rural Development Project, Cr. 631-BD (RD-I) was financedin 1976 to test the replicability of the Comilla's TCCA/KSS approach inseven selected thanas in two districts in northern Bangladesh. After anencouraging start'on the training of field staff, and reorganization ofexisting KSS into the Comilla type TCCA/KSS by rescheduling of old debts ofthese KSS and other preparatory work, the supply of inputs like irrigationequipment, fertilizers and technical advice to the project's TCCA ran intoserious problems. For example, procurement of minor irrigation equipmentwas delayed for three years due to BADC's inability to follow the Bank'sprocurement guidelines. Other inputs, which were not financed directlyunder the project, were also in short supply and priority was not given byBADC to the project area. As a result, the only service available tofarmers for the first three years under RD-I was short term (ST) creditwhich was of use basically only to larger farmers who already had irrigationfacilities. Thus, KSS membership did not expand in the project area.Morale of field staff declined rapidly, along with their creditability withthe newly established KSS. Resentment built up further since farmers in theproject area, while getting no services from the project, had to pay inter-est at 17.5% for ST credit, while GOB's SACP, operation of which wasexcluded from the project area, charged interest at only 12%. Thus, exceptfor the project's rural works program, there was little physical evidence of

1/ The project is expected to be complete by June 1983.

-22-

the usefulness of the project and the TCCA/KSS concept came to be ques-tioned. Project implementation began to pick up, however, in 1980 when GOBand IDA took a number of steps:

(a) a core program of minor irrigation, TCCA/KSS management, credit,completion of rural works and fisheries was agreed for concentratedattention;

(b) an Executive Director was appointed after a gap of 18 months andRD-I finances were delinked from other BRDB activities;

(c) monthly thana action plans for the core program were prepared andmonitored during intensive field supervision by the Bank's ResidentMission to Bangladesh (RMB);

(d) a financial incentive system for TCCA staff, based on a quarterlyevaluation of TCCA/KSS, was introduced;

(e) a system for classifying KSS according to performance criteria, andsupplying the limited minor irrigation equipment and other servicesto the best KSS, was introduced; and

(f) procurement of STWs and LLPs, following a farmer choice system, wasintroduced.

2.47 By early 1981, the project's performance had improved noticeably.Disbursements of credit to eligible KSS and farmers increased to Tk 13 Mfrom Tk 2 M in FY79, while the number of borrowers owning less than twoacres increased to 76% from 57% in 1978. Credit recovery of 85% againstdemand was achieved. Two of the seven TCCAs achieved a level of accumulatedsavings that exceeded their annual ST loans; 110 landless fishery coopera-tives were organized and made operational; and a pilot project for improvingutilization of DTWs was successfully undertaken. Sale of 5,000 HTWs, allavailable STWs (730), and DTWs (90) was completed. Training programs forKSS managers and TCCA staff were revitalized and the backlogs of audits andelections for the managing committee for all A and B' class KSS werecleared. By the original closing date (June 1982), the US$16 M project wasbasically complete at a cost saving of US$5 M, a part of which has sincebeen allocated to finance 250 DTWs for the 1,000 KSS located in MymensinghDistrict, where it was found during implementation, that the plan to use STWwas not feasible. The current status of RD-I activities is summarized inTable 1, Annex 1. Problems of audit backlogs and delays in registration oflandless BSS have surfaced. In addition, in Mymensingh, where irrigationdevelopment has been slow due to delays in procurement of DTW, performanceof KSS has not been as good as in Bogra.

2.48 Important lessons have been learnt from RD-I. The first orLe is thatif the principal objective is to create an institution to provide farmers,

-23-

and in particular small farmers, with the means to adopt new technology andundertake efficient irrigation development, it is counter productive topackage investments which are not directly relevant to the basic program, inthis case, establishing viable TCCA/KSS. Attempts to implement a wide rangeof activities divert the attention of project staff from the priority taskof institutional development. The second unsatisfactory aspect of RD-Idesign, which appears common to similar projects financed by other donors isthe concentration on a relatively few thanas. This is unsatisfactory fortwo reasons, because operation of two programs -- project and nonproject --is confusing to district officials because of the administrative problemsinvolved; and further confining an intensive development program to a fewfavored thanas creates local tensions which in turn adversely affectimplementation. Not least, other GOB departments expected to provide serv-ices to projects, in these cases directed by BRDB, seem to have found itdifficult to equate the priority they had been expected to provide suchareas with their responsibilities to provide such services nationwide.Finally, it is evident from the experience of RD-I that institutionaldevelopment cannot take place in the absence of an assured supply of inputsand services to farmers. The strong initial farmer response to RD-I turnedinto antagonism as BADC failed to complete the procurement of STWs underICB. Only when the farmer choice system (para 4.04) was introduced couldthe procurement be completed and the institutional development effortsrevived. Even now, the poor performance of TCCA/KSS in the District ofMymensingh is directly attributable to the failure of BADC to complete theprocurement of DTWs, which alone are feasible for the TCCA located in thesethanas. The proposed Second Rural Development Project appraised in thisreport takes into account these experiences.

III. THE PROJECT

A. Project Objectives

3.01 The primary objective of the Second Rural Development Project(RD-II) would be to strengthen and expand the TCCA/KSS cooperative systemand improve the capability and performance of its promotional agency BRDB.The project would streamline procedures for (a) the purchase by TCCA ofirrigation equipment, and (b) for the distribution of credit by Sornali Bankto the TCCA. Efforts would also be made to diversify the activities of alimited number of selected TCCA into crop and input marketing. Finally, theproject would assist BRDB in providing a special package of inputs throughTCCA for members, including women, of the special cooperatives (BittaheenSamabaya Samity - BSS) of the rural poor. About 90 new TCCA, 8,000 new KSSand 3,000 new BSS 1/ are expected to be formed during the project's four

1/ The term BSS' includes the separate cooperatives for women - or MSS.

-24-

year implementation period. The 210 existing TCCA would focus their atten-tion on the 15,000 A' and B' class KSS, but attempt also to upgrade the7,000 KSS which have yet to reach these standards.

B. Project Area

3.02 With the exceptions set out below, all TCCA would be eligible toparticipate in the project. Due to ongoing and proposed projects which areassisting TCCA in the districts of Kushtia, Pabna and Raishahi (the ADBfinanced Northwest Development Project); Jessore and Faridpur (the IFADfinanced Southwest Rural Development Project); Noakhali (the Danish Govern-ment financed Noakhali Integrated Rural Development Project); and the Chit-tagong Hill Tracts (the ADB financed Chittagong Hill Tracts DevelopmentProject), it is anticipated that TCCA in the seven districts covered bythese projects would not draw on the inputs and services made availableunder RD-II. However, it is expected that the institutional arrangementsemployed in the seven districts would be similar to those used under RD-IIwhich themselves are consistent with the recommendations of the JoiLnt Reviewof IRDP. Because of BRDB-s currently limited implementation capacity theproposed rural poor and marketing components would be initially concentratedin six districts. Eligibility criteria for the participation of individualTCCA in project activities would take account of their needs, managementcapacity and availability of complementary infrastructure and otherfacilities. Assurances have been obtained that these criteria (Schedule B)would be followed. Other BRDB programs should not be affected adversely byRD-II; on the contrary, the strengthening of BRDB and the TCCA under theproject should facilitate the implementation of a number of project:s inwhich BRDB is involved, including some financed by IDA.

C. Project Components

3.03 The principal components of the project would be:

(a) provision of medium term (MT) credit to TCCA/KSS members for thepurchase of about 30,000 STW, 2,000 LLP, 2,300 tool kits, a,nd 2,300bicycles;

(b) expansion of an ongoing Irrigation Management Program (IMP) to coverabout 4,400 DTW and 1,100 LLP/STW clusters; 1/

(c) provision of medium term (MT) credit to about 3,000 TCCA/BSS, undera Rural Poor Program, for productive activities such as beef fatten-ing, weaving, handicrafts, and pond fisheries;

1/ Where STW or LLP are employed in batteries and thus command a substan-tial potentially irrigable area.

-25-

(d) provision of short term (ST) credit to TCCA/KSS members for cropproduction;

(e) implementation of a TCCA Crop and Input Marketing Program in alimited number of TCCA;

(f) construction of basic thana facilities, the Thana Training andDevelopment Center (TTDC), at 20 thanas where these have yet to beprovided by GOB;

(g) construction of essential TCCA office facilities, at 100 thanas andthe residential accommodation required for the staff of GOB agencieswho would be essential for project activities in these thanas;

(h) strengthening BRDB and the audit capacity of the Registrar ofCooperatives by the appointment of additional staff and the provi-sion of vehicles and office equipment;

Mi) training of BRDB staff, Cooperative Department auditors,TCCA/KSS/BSS staff and members, and thana irrigation teams in thewide range of activities essential to the success of the project.This component would include the construction of five new ThanaTraining Units and additional classrooms and staff accommodation atthe Rural Development Training Institute (RDTI) at Sylhet; and

(j) technical assistance required for the Rural Poor Program, marketing,training, audit and accounts, and monitoring and evaluation - atotal of 240 man months.

D. Detailed Features

3.04 Purchase of STW and LLP (Annex 3, Table 2): National demand of theTCCA/KSS system for STW is estimated conservatively at 15,000 per annum andthat for LLPs at 1,500. The project would finance the purchase by eligibleKSS on MT credit provided by TCCA, of 30,000 STW and 3,000 one-cusec LLPS.Installed units which would be mostly diesel engine driven would cost aboutTk 33,000 for a STW and Tk 27,000 for a LLP. The balance of the TCCA demandfor STW would be met from sources such as the IDA financed AgriculturalCredit Project (Cr. 1147-BD) and projects financed by other sources. TheTCCA will also require HTW and DTW, but this demand should be met fully byongoing IDA and other donor financed operations. By 1987, 90% of A and'B class KSS are expected to have some irrigation facilities compared toonly 45% now. Project STW and LLP together with spare parts equivalent toat least 5% of the value of the engines would be imported, retailed,installed and serviced by private dealers. TCCA would however have theoption to purchase STWs in bulk from dealers and install these using privatedrilling contractors. Credit would also be made available to private

-26-

mechanics sponsored by TCCA, for purchase of simple toolboxes and bicycles.Based on irrigation equipment likely to be in operation, it is estimatedthat 2,300 such private mechanics would be required. These mechanics wouldoperate as mobile private repairmen and would be suitably trained (para3.23). Lending terms and conditions are specified in Schedule A. For thisMT credit component to function smoothly, a number of improvements would berequired in the credit mechanism used by BB, Sonali BAnk and TCCA. Theseare discussed in detail in Schedule C.

Irrigation Management Program (IMP) (Annex 3, Tables 3 and 4)

3.05 The project would meet the cost of the expansion of IMP from itspresent coverage of 430 DTW/LLP units (para 2.13) to about 5,500 DTW andSTW/LLP clusters. The expansion would require (a) strengthening of theirrigation faculty at the Rural Development Academy, Bogra; (b) training ofthana level teams; and (c) training of irrigation group leaders.

3.06 About 300 thana irrigation teams, each consisting of a BADC SectionOfficer, TCCA Deputy Project Officer, Thana Extension Officer and ThanaOverseer would be trained under the project at RDA, Bogra. Funds would beprovided under this component to complete the furnishing of RDA traineehostel. The FAO/UNDP's command area development team at Bogra would con-tinue as now to assist RDA's irrigation management faculty in this work.It is expected that all positions already approved for the irrigationfaculty at RDA would be filled by December 1983. Details of the trainingprogram are discussed in para 3.22.

3.07 DTW schemes into which IMP has already been introduced have beenstudies in detail by the Bangladesh Agricultural University. These studieshave shown that further improvements in the efficiency of irrigation can beachieved on all existing IMP units. Generally, improved compaction ofearthen irrigation channels can result in decline of heavy seepage losses,but special canal lining may also be justified on lighter soils or where thecommand area has a topography which allows only poor embankment stability.An allocation of US$0.5 M would be provided (as MT credit) under the projectfor KSS who wish to undertake improved canal construction or lining.

3.08 Although under IMP the specific responsibilities of the thana staffof DEM, BADC and BRDB have now been clearly defined, GOB is yet to act onthe recommendation of the Minor Irrigation Review, to formally establishthese responsibilities for the overall development of DTW/LLP command areas.GOB has constituted a National Committee to consider proposals covering theroles of key agencies and would formally establish their responsibilities byOctober 31, 1983.

-27-

Rural Poor Program (Annex 3, Tables 6, 7, and 8)

3.09 The project would provide MT credit for productive economic.activities to rural poor organized as BSS. Because of BRDB-s experience inrural poor programs is limited, this project component would be small inscale and flexible in design to allow modification as experience dictates.

3.10 The rural poor component would be implemented to start with in thesix districts of Bogra, Mymensingh, Jamalpur, Khulna, Dinajpur and Barisalin which there are no similar activities ongoing or planned. Socio-economicdata of these six districts are in Annex 1, Table 13. Four of the districtshave a landless population above the national average while in the other twothis is equal to the national average. Only about 3% of the 25,000 villagesin these six districts have BSS, mostly in Bogra and Mymensingh where RD-Iis located. Their membership is about 21,000. Of the 2,900 new BittaheenSamabaya Samities (BSSs) to be formed under the project, about 400 would beexclusively for women. Membership of the BSS would be limited as now tothose owning less than 0.5 ac of land and earning their basic livelihoodfrom casual labor. By year 4, BSS membership is expected to reach about120,000 men and 9,000 women.

3.11 The major activities to be supported under the Rural Poor Programare discussed in detail in Annex 3, Appendix 1. Pond fisheries wouldinvolve the formation of BSS around ponds leased from GOB, excavation of thederelict pond using funds in the form of MT credit from the project, pur-chase of fish fries from GOB operated hatcheries or private sources andmarketing of the catch in local markets. Beef fattening would involvepurchase under credit of young calves, grazing and some supplement feeding,and sale of mature cattle. Credit would also be available for purchase ofcows for milk production. A cattle insurance program has been introduced byBRDB with the national insurance company and this would operate for allproject financed animals. Credit for weaving would be for purchase of semiautomatic looms and for working capital. BSS would link up with BHB's yarndistribution centers for input supply and marketing support. Rickshawswould be financed for members of BSS and a self insurance scheme within eachTCCA would cover the financial risk in case the rickshaw gets seriouslydamaged. Cane and bamboo work would be promoted by financing credit forworking capital which is the major constraint. Pottery, a traditionalactivity, would be supported under the project by funds for the purchase ofimproved kilns and for working capital. BSCIC would provide extension andtraining support to the BSS undertaking pottery activity. Other activities

-28-

like carpentry, oil milling or setting up biogas units 1/ would be includedshould there be a demand for these.

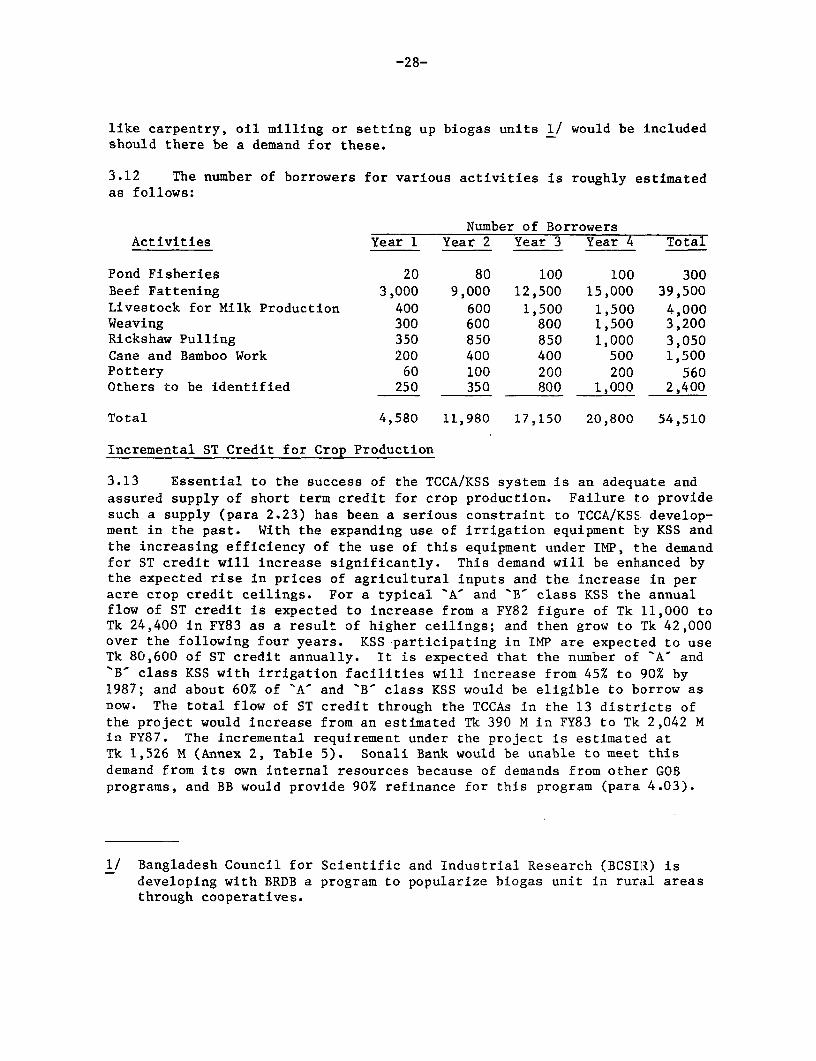

3.12 The number of borrowers for various activities is roughly estimatedas follows:

Number of BorrowersActivities Year 1 Year 2 Year 3 Year 4 Total

Pond Fisheries 20 80 100 100 300Beef Fattening 3,000 9,000 12,500 15,000 39,500Livestock for Milk Production 400 600 1,500 1,500 4,000Weaving 300 600 800 1,500 3,200Rickshaw Pulling 350 850 850 1,000 3,050Cane and Bamboo Work 200 400 400 500 1,500Pottery 60 100 200 200 560Others to be identified 250 350 800 1,000 2,400

Total 4,580 11,980 17,150 20,800 54,510

Incremental ST Credit for Crop Production