working capital management - lakehead...

TRANSCRIPT

Working Capital Management

Gitman and Hennessey, Chapter 14

Spring 2004

14.1 Net Working Capital Fundamentals

In 2002, current assets accounted for 31.7% of non-financial

Canadian corporations’ total assets.

Of this 31.7%, 46.1% were accounts receivable, 37.8% were

inventories and 16.1% was cash.

See Figure 14.1

2

14.1 Net Working Capital Fundamentals

Short-term management–managing current assets and

liabilities–is one of the financial manager’s most important

activities.

Too large an investment in current assets can reduce profitability,

whereas too little investment increases liquidity risk.

Too little current liability financing can reduce profitability

whereas too much increases liquidity risk.

3

14.1 Net Working Capital Fundamentals

Current assets are often referred to as the firm’sworking capital.

Current liabilities represent the firm’s short-term financing.

The conversion of current assets from inventory to receivables to

cash provides the source of cash to pay the current liabilities.

The timing of cash outlays for current liabilities is easily

predictable but the inflows from current assets are not. This is a

source of risk.

4

14.1 Net Working Capital Fundamentals

A tradeoff exists between a firm’s profitability and its risk.

Profitability is the relationship between revenues and costs

generated by using the firm’s assets.

Risk, in the context of short-term financial management, is the

probability that the firm be unable to pay its bill when they come

due.

5

14.1 Net Working Capital Fundamentals

The greater the firm’s net working capital, the lower the risk but

the lower the firm’s profitability.

Current assets, however, includes assets that are not very

productive (cash, for example).

A firm’s productive assets are its long-term assets.

An increase in current liabilities, on the other hand, increases

profitability but also increases risk.

6

14.2 The Cash Conversion Cycle

Cash is not a productive asset but is needed to pay bills.

• What is a reasonable level of cash to keep on hand?

• How much should the firm borrow short-term?

• How much credit should be extended to customers?

• How much inventory should the firm carry?

7

14.2 The Cash Conversion Cycle

From the balance sheet identity

Cash+ non-cash CA+ NFA = CL + LTD + E,

we find

Cash= CL + LTD + E − non-cash CA− NFA.

Hence anincrease in liabilities is a source of cashand an

increase in assets is a use of cash.

8

14.2 The Cash Conversion Cycle

Before selling goods, the firm needs to buy raw materials

(inventory).

Then it has to pay for the raw material (cash out).

Then it sells the goods produced out of the raw material.

Then it receives payment for the goods sold (cash in).

9

14.2 The Cash Conversion Cycle

How long does it take, on average, to recover the cash used to

purchase raw material?

Consider a firm with an average age of inventory (AAI, days’

sales in inventory) of 110 days, an average payment period (APP,

days’ sales in payables) of 30 days and an average collection

period (ACP, days’ sales in receivables) of 45 days.

10

14.2 The Cash Conversion Cycle

The firm’soperating cycleis the average length of time between

the moment raw material isacquiredand the moment customers

pay for the goods they buy:

Operating Cycle (OC)= AAI + ACP = 110+ 45 = 155 days.

11

14.2 The Cash Conversion Cycle

The firm’scash cycleis the average length of time between the

moment raw material ispaid forand the moment customers pay

for the goods they buy:

Cash Conversion Cycle (CCC)= OC−APP

= AAI + ACP − APP

= 110 + 45 − 30

= 125 days.

12

14.2 The Cash Conversion Cycle

The Cash Budget

The cash budget is a primary tool of short-term financial

planning.

It allows managers to identify short-term financing needs.

It helps identify when short-term borrowing will be needed.

The cash budget basically records estimates of cash receipts and

disbursements.

13

The Cash Budget

Thecash budgetdescribes the firm’s planned inflows and

outflows of cash.

This statements aims at determining when the firm will

experience surpluses and shortages of cash.

The cash budget covers a 6- to 12-month period divided into

shorter intervals, usually months.

The more seasonal or uncertain the firm’s cash flows, the shorter

these intervals (weeks or days).

14

The Cash Budget

The Sales Forecast

The starting point of financial planning, whether short- or

long-term, is the firm’s sales forecast.

Sales forecast may come from past sales, economic conditions,

sales expectations about new products, etc. These are usually

provided by the marketing department.

External forecastscome from key external economic indicators.

Internal forecastscome from the firm’s own channels.

15

The Cash Budget

Using sales forecast, the firm can determine the fixed assets

necessary to achieve these sales, variable costs can be evaluated,

and cash inflows and outflows can be estimated.

For example, some of the firm customers will pay immediately

while others will pay after 30, 60 or 90 days. Some customers

may not even pay at all. Cash inflows occur when customers pay,

not when they buy.

Similarly, some of the firm’s cash outflows depend on its credit

arrangements with suppliers.

16

The Cash Budget

Suppose a firm expects to sell for $1,000 in January. Then,

assuming that 20% of its customers pay cash at the time of the

sale, 50% pay one month later, 28% pay two months later and

2% never pay, the cash inflows arising from January sales are

expected to be

$200 in January,

$500 in February and

$280 in March.

Note that the missing $20 could be recovered at some point in

time but it may be more conservative not to count on it.

17

The Cash Budget

Cash Receipts

Cash receipts include all of the firm’s inflows of cash. These are

mainly cash sales and collections of accounts receivable.

Accounts receivable collected in a month come from sales that

took place in preceding months.

18

Example

Coulson Industries is developing its cash budget for October,

November and December. Expected sales for these months are

(in thousands of $) 400, 300 and 200, respectively. Sales in

August and September were 100 and 200, respectively.

Month August September October November December

Sales (forecast) 100 200 400 300 200

19

Example (continued)

Coulton’s sales are expected to convert to cash as follows: 20%

of its customers pay at the time of sales, 50% pay one month

later and 30% pay two months later (assume that every customer

is expected to pay). On top of that, the firm expects to receive

$30,000 from a subsidiary in December. The table below

summarizes the cash inflows.

20

Coulton’s Cash Receipts ($000)

Month Aug. Sept. Oct. Nov. Dec.

Forecast sales 100 200 400 300 200

Cash sales (20%) 20 40 80 60 40

Collections of A/R:

Lagged one month (50%) 50 100 200 150

Lagged two months (30%) 30 60 120

Other cash receipts 30

Total cash receipts 210 320 340

21

The Cash Budget

Cash Disbursements

The most common cash disbursements are

Cash purchases Fixed asset outlays

Payments of accounts payable Interest payments

Rent (and lease) payments Cash dividend payments

Wages and salaries Principal payments (on loans)

Tax payments Repurchases of common shares

22

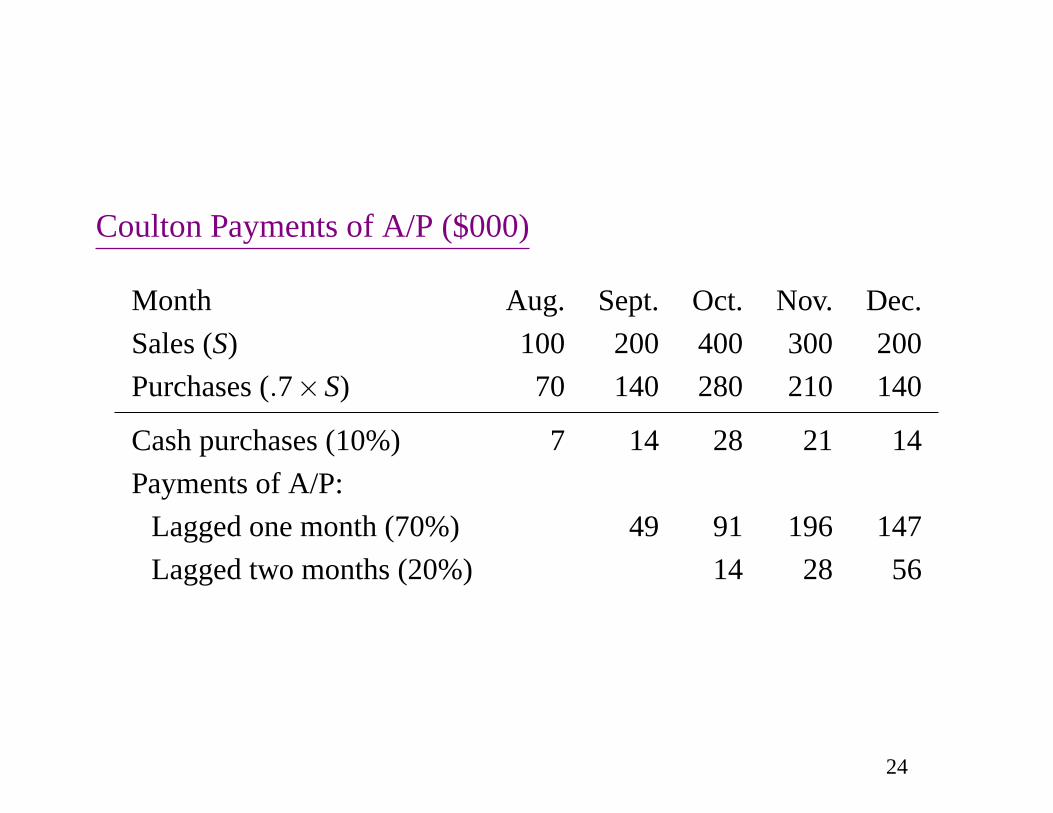

Example (continued)

Purchases: Coulton’s purchases are 70% of sales, 10% of which

are paid in cash, 70% of which are paid one month later and

20% of which are paid two months later. That is, if Coulton

sells for $SJ in January, it will pay

10%×70%×$SJ = .07×SJ in January,

70%×70%×$SJ = .49×SJ in February,

20%×70%×$SJ = .14×SJ in March.

Note: This is not the case in this example, but very often

some of the purchases will occur in months preceding the

sales’ month.

23

Coulton Payments of A/P ($000)

Month Aug. Sept. Oct. Nov. Dec.

Sales (S) 100 200 400 300 200

Purchases (.7×S) 70 140 280 210 140

Cash purchases (10%) 7 14 28 21 14

Payments of A/P:

Lagged one month (70%) 49 91 196 147

Lagged two months (20%) 14 28 56

24

Coulton’s Other Cash Disbursements

Rent payments: $5,000 each month.

Wages and salaries:For Coulton, these are usually 10% of sales plus fixed

salaries of $8,000 per month.

Tax payments: $25,000 in December.

Fixed asset outlays:New machinery costing $130,000 will be purchased in

September and paid for in November.

Interest payments: $10,000 in December.

Cash dividends: $20,000 in October.

Principal payments: $20,000 in December.

Repurchases of shares:$0 for the rest of the year.

25

Coulton’s Cash Disbursements ($000)

Month Aug. Sept. Oct. Nov. Dec.Sales (S) 100 200 400 300 200Purchases (.7×S) 70 140 280 210 140

Cash purchases (10%) 7 14 28 21 14Payments of A/P:

Lagged one month (70%) 49 98 196 147Lagged two months (20%) 14 28 56

Rent payments 5 5 5Wages and salaries 48 38 28Tax payments 25Fixed asset outlays 130Interest payments 10Cash dividends 20Principal payments 20Total disbursements 213 418 305

26

The Cash Budget

Net Cash Flow, Ending Cash and Excess Cash

Net Cash Flow = Cash Receipts− Cash Disbursements

Ending Cash = Beginning Cash+ Net Cash Flow

Required Financing = Minimum Cash Balance− Ending Cash

Excess Cash= Ending Cash− Minimum Cash Balance

Suppose Coulton has $50,000 in cash at the beginning of October

and suppose its minimum cash balance is $25,000.

27

Coulton’s Cash Budget ($000)

Month Oct. Nov. Dec.

Total cash receipts 210 320 340

Less: Total cash disbursements 213418 305

Net cash flow (3) (98) 35

Add: Beginning cash 50 47 (51)

Ending cash 47 (51) (16)

Less: Minimum cash balance 25 25 25

Required financing – 76 41

Excess cash 22 – –

28

The Cash Budget

Evaluating the Cash Budget

Using the information obtained so far, it is possible to determine,

for each period, the balance in cash, in marketable securities and

in notes payable.

Note that a firm should liquidate its marketable securities before

dipping into its line of credit. A firm may have both items at the

same time but this should be temporary.

29

Coulton’s End-of-Month Balances ($000)

October November December

Cash 25 25 25

Marketable securities 22 0 0

Line of credit 0 76 41

Coulton’s management must ensure that a line of credit of at least

$76,000 is secured before November.

30

The Cash Budget

Coping with Uncertainty in the Cash Budget

Many items in the cash budget vary with sales.

The cash budget thus depends on the level of sales expected.

What financing will be needed if sales are 10% less than

expected in each month?

What financing will be needed if sales are 10% more than

expected in each month?

31

The Cash Budget

Coping with Uncertainty in the Cash Budget

Cash flows are also affected by the time customers take to pay

for their purchases.

What would the cash budget look like if only 10% of the sales

were paid cash, 50% paid after one month and 40% paid after

two months?

What if 5% of the sales are never paid?

32

Coping with Uncertainty in the Cash Budget

Suppose, for example, that the time at which accounts are paid isnot expected to change but sales could be

Month Aug. Sept. Oct. Nov. Dec.

Best case (10% higher) 100 200440 330 220

Worst case (10% lower) 100 200360 270 180

33

Scenario Analysis when only Sales Vary

October November December

Cash 25 25 25

Most Likely Scenario

Marketable securities 22 0 0Line of credit 0 76 41

Best-Case Scenario

Marketable securities 23 0 0Line of credit 0 74 31

Worst-Case Scenario

Marketable securities 21 0 0Line of credit 0 78 51

34

Coping with Uncertainty in the Cash Budget

Suppose now that the best-case scenario is such that sales in the

last three months of the year are 10% higher than the initial

figures and, at the same time, 30% of sales are paid cash, 50%

one month later and 20% two months later.

The worst-case scenario, on the other hand, is such that sales are

10% lower than expected and cash sales are 10% of total sales,

50% of sales are paid one month later and 40% of sales are paid

two months later.

We will see that collection of receivables significantly affect the

firm’s cash flows.

35

Scenario Analysis when Sales and Collections of A/R Vary

October November December

Cash 25 25 25

Expected Case

Marketable securities 22 0 0Line of credit 0 76 41

Best-Case Scenario

Marketable securities 57 0 0Line of credit 0 27 6

Worst-Case Scenario

Marketable securities 0 0 0Line of credit 5 112 66

36

14.2 The Cash Conversion Cycle

If a firm’s sales are constant, its investment in operating assets

will also be constant. This firm will only have permanent funding

requirement.

If a firm’s sales vary over time, then its investment in operating

assets will also vary over time. This firm will have seasonal

funding requirements.

37

14.2 The Cash Conversion Cycle

Funding Requirements of the Cash Conversion Cycle

A firm may fund its seasonal needs with short-term debt and its

permanent needs with long-term debt (aggressive funding

strategy).

A firm may fund all its needs, both seasonal and permanent with

long-term debt (conservative funding strategy).

38

14.2 The Cash Conversion Cycle

Funding Requirements: Example 1

Nicholson Company holds, on average, $50 in cash and

marketable securities, $1,250 in inventory and $750 in accounts

receivable. Nicholson’s accounts payable of $425 are stable over

time.

Nicholson has a permanent investment in operating assets (net

operating working capital) of

50 + 1,250 + 750− 425 = $1,625.

.

39

14.2 The Cash Conversion Cycle

Funding Requirements: Example 2

Semper Pump Company, which produces bicycle pumps, has

seasonal funding needs.

It holds, at minimum, $25 in cash and marketable securities,

$100 in inventory and $60 in accounts receivable.

At peak times, inventory increases to $750 and accounts

receivable increase to $400.

Semper’s accounts payable remain $50 throughout the year.

40

14.2 The Cash Conversion Cycle

Funding Requirements: Example 2

Semper permanent funding requirement for its operating assets is

25 + 100 + 60 − 50 = $135,

and its maximum funding requirement is

25 + 750 + 400− 50 = $1,125.

Hence Semper’s seasonal funding requirement is

1,125− 135 = $990.

41

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

Semper’s permanent funding requirement is $135 and its

seasonal needs vary between $0 and $990, for an average of

$101.25.

Semper can borrow short-term funds at 6.25% and long-term

funds at 8%, and it can earn 5% on any surplus balance.

42

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

If Semper follows an aggressive funding strategy, all its seasonal

needs will be funded with short-term debt. There will not be any

surplus to invest throughout the year.

If it follows a conservative strategy, all its needs will be funded

with long-term debt. In this case, there will be surpluses

whenever funding requirements are below $1,125 and these

surpluses will be invested at the rate of 5%.

43

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

Suppose Semper follows an aggressive funding strategy. Then it

uses long-term debt for its permanent funding requirement only,

which costs

8%×135 = $10.8.

Seasonal needs, which average $101.25 will be funded with

short-term debt, the cost being

6.25%×101.25 = $6.33.

44

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

The total cost of the aggressive funding strategy is then

10.8 + 6.33 = $17.13.

45

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

Suppose now that Semper follows a conservative funding

strategy. Then long-term debt is used to finance all operating

assets needed throughout the year, which means that $1,125 is

borrowed at the rate of 8%. This implies a cost of

8%×1,125 = $90.

46

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

The cash raised with long-term debt is not used all the time.

More specifically, the average excess funding during the year is

1,125.00 − 101.25 − 135.00 = $888.75,

which will be invested at the rate of 5%, creating a revenue of

5%×888.75 = $44.44.

47

14.2 The Cash Conversion Cycle

Funding Strategies: Semper

The net cost of the conservative funding strategy is then

90.00 − 44.44 = $45.56.

Note that the aggressive funding strategy is less expensive than

the conservative strategy. The former, however, is more risky

than the latter.

48

14.2 The Cash Conversion Cycle

Strategies for Managing the Cash Conversion Cycle

1. Turn over inventory as quickly as possible without stockouts

resulting in lost sales.

2. Collect account receivable as quickly as possible without

losing sales from high-pressure collection techniques.

3. Pay accounts payable as slowly as possible without

damaging the firm’s credit rating.

49

14.3 Inventory Management

The ABC System

This concept suggests that 20 percent of the firm’s products

account for 80 percent of the firm’s sales and thus 80 percent of

the firm’s inventory. The products within this 20 percent are

classified as A items and are actively managed.

The B group consists of items that account for the next largest

investment in inventory.

The C group consists of a large number of items that require a

relatively small investment.

50

14.3 Inventory Management

The Economic Order Quantity (EOQ) Model

The EOQ is an appropriate model for the management of A and

B items. Let

S = usage in units per period,

O = order cost per order,

C = carrying cost per unit per period,

Q = order quantity in units.

51

14.3 Inventory Management

The Economic Order Quantity (EOQ) Model

The number of orders per period is the number of units used,S, divided

by the size of an order,Q, and thus total order cost per period is

Order cost= O× SQ

.

Inventory is assumed to deplete at a constant rate and thus the carrying

cost of an order per period is

Carrying cost= C× Q2

.

52

14.3 Inventory Management

The Economic Order Quantity (EOQ) Model

The total cost of inventory is then the sum of the order cost and

the carrying cost, which gives

Total cost= O× SQ

+ C× Q2

the quantity minimizing this cost, the economic order quantity

(EOQ), is

EOQ =

√2×S×O

C.

53

14.3 Inventory Management

The Economic Order Quantity (EOQ) Model: Example

MAX Company has an A group of inventory item that is vital for

the production process. This item costs $1,500 and MAX uses

1,100 units of the item per year. The order cost per order of this

item is $150 and the carrying cost per unit per year is $200. The

optimal order strategy for this item is then

EOQ =

√2×1,100×150

200= 41 units.

54