financial planning and forecasting - lakehead...

TRANSCRIPT

Financial Planning and Forecasting

Long-Term Planning

Spring 2004

4.3 Fundamentals of Preparing Pro Forma Statements

A cash budget is not the only statement that must be forecasted.

Future profits and financial needs must also be projected.

The three main outputs of financial forecasting are

1. Pro forma income statement

2. Pro forma balance sheet

3. A statement of external financing required (EFR)

2

4.3 Fundamentals of Preparing Pro Forma Statements

Preparing pro forma statements requires a set of assumptions

about

• the increase in sales,

• the increase in costs,

• the increase in assets,

• the increase in debt,

• etc...

3

4.3 Fundamentals of Preparing Pro Forma Statements

Preparing the pro forma statements requires the use ofplug

variables.

A plug variable varies to ensure that the balance sheet balances

and to ensure that the pro forma balance sheet figures are

consistent with the pro forma income statement figures.

That is, the growth assumptions cannot concern all items on the

statements. How plug variables vary will determine the firm’s

external financing required.

4

A Simple Financial Planning Model

Computerfield CorporationCurrent Financial Statements

Income Statement

Sales 1,000Costs (800)Net income 200

Balance Sheet

Assets 500 Debt 250Equity 250

Total 500 Total 500

Dividends 100Earnings retained 100

5

A Simple Financial Planning Model

Example 1Assumptions: Sales, costs, assets, debt and equity are all

expected to increase by 20% in the coming year. “Dividends” is

the plug variable:

Computerfield CorporationPro Forma Financial Statements

Income Statement

Sales 1,200Costs (960)Net income 240

Balance Sheet

Assets 600 Debt 300Equity 300

Total 600 Total 600

Dividends ?Earnings retained 50

6

A Simple Financial Planning Model

Example 1 (continued)

Equity is expected to increase by 50 while net income is

expected to be 240.

For the pro forma income statement to be consistent with the pro

forma balance sheet, dividends must be

240− 50 = 190.

“Dividends” is used at the plug variable in the present example.

The next example uses a different plug variable.

7

A Simple Financial Planning Model

Example 2Assumptions: Sales, costs, assets, are all expected to increase by

20% in the coming year. The dividend payout ratio will remain

50% of net income, so debt is the plug variable.

Computerfield CorporationPro Forma Financial Statements

Income Statement

Sales 1,200Costs (960)Net income 240

Balance Sheet

Assets 600 Debt ?Equity 370

Total 600 Total 600

Dividend 120Earnings retained 120

8

A Simple Financial Planning Model

Example 2 (continued)

Total liabilities and equity are expected to increase to 600 while

equity is expected to be 370.

For the pro forma balance sheet to balance, future debt has to be

600− 370 = 230,

i.e. debt has to be reduced by 20.

9

A Simple Financial Planning Model

In the last example, EFR is -20, i.e. the firm will be able to repay

$20 of long-term debt if the projections are correct.

There are many ways to construct pro forma statements. Two of

these are:

• The percent-of-sales approach.

• The judgemental approach.

10

The Percent-of-Sales Approach

The percent-of-sales approach assumes that some items on theincome statement and balance sheet always vary in proportionswith sales.

For example, it may be reasonable to assume that current assetsincrease by 20% whenever sales increase by 20%.

There are some items, however, that do not have to vary in thesame proportions as sales. These are debt, common stock,retained earnings, short-term debt and interest payments, amongothers. Other balance sheet items, such as accounts receivable,can also be relatively independent of sales, as we will see in thejudgemental approach.

11

The Percent-of-Sales Approach: An Illustration

Consider the following statements:

Rosengarten Corporation

Current Financial Statements (in millions of $)

Income Statement

Sales 1,000Costs (800)Taxable income 200Taxes (34%) (68)Net income 132

Dividend (33.33%) 44Earnings retained 88

Balance Sheet

Cash 160 A/P 300A/R 440 N/P 100Inventory 600 C.L. 400C.A. 1,200

LTD 800NFA 1,800 C/S 800

R/E 1,000Total 3,000 Total 3,000

12

The Percent-of-Sales Approach: An Illustration

Main assumption: Sales are expected to increase by 25%.

Assumptions concerning the income statement:

• Costs are a constant fraction of sales (800/1,000= 80%).

• The tax rate is not expected to change (34%).

• Dividend payout ratio will remain constant (33.33%).

13

The Percent-of-Sales Approach: An Illustration

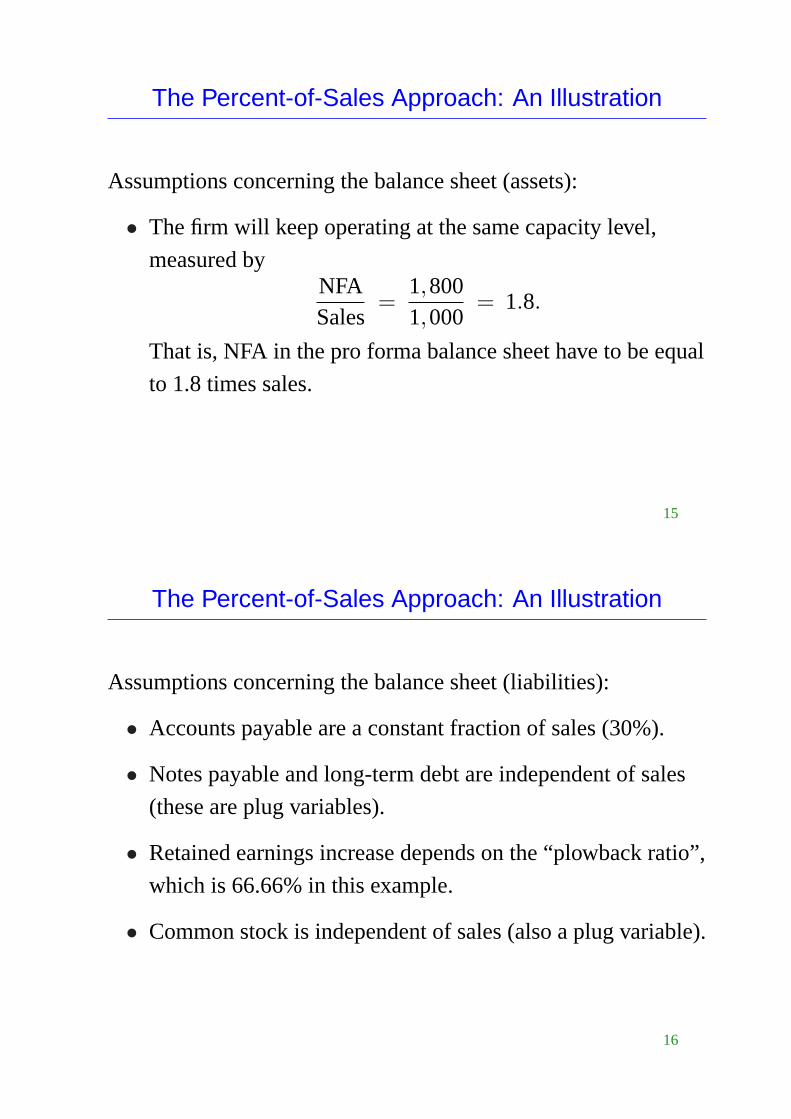

Assumptions concerning the balance sheet (assets):

• Each current asset is a constant fraction of sales:

1601,000

= 16% for Cash,

4401,000

= 44% for A/R,

6001,000

= 60% for inventory.

14

The Percent-of-Sales Approach: An Illustration

Assumptions concerning the balance sheet (assets):

• The firm will keep operating at the same capacity level,

measured byNFASales

=1,8001,000

= 1.8.

That is, NFA in the pro forma balance sheet have to be equal

to 1.8 times sales.

15

The Percent-of-Sales Approach: An Illustration

Assumptions concerning the balance sheet (liabilities):

• Accounts payable are a constant fraction of sales (30%).

• Notes payable and long-term debt are independent of sales

(these are plug variables).

• Retained earnings increase depends on the “plowback ratio”,

which is 66.66% in this example.

• Common stock is independent of sales (also a plug variable).

16

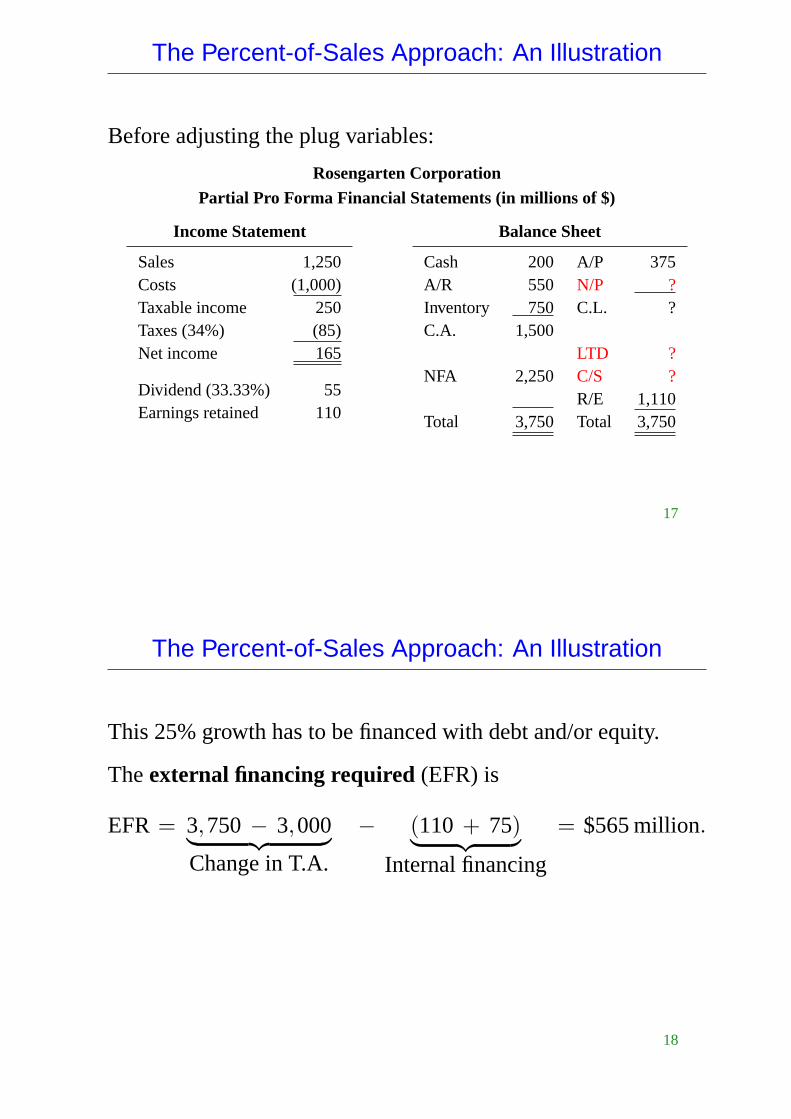

The Percent-of-Sales Approach: An Illustration

Before adjusting the plug variables:

Rosengarten Corporation

Partial Pro Forma Financial Statements (in millions of $)

Income Statement

Sales 1,250Costs (1,000)Taxable income 250Taxes (34%) (85)Net income 165

Dividend (33.33%) 55Earnings retained 110

Balance Sheet

Cash 200 A/P 375A/R 550 N/P ?Inventory 750 C.L. ?C.A. 1,500

LTD ?NFA 2,250 C/S ?

R/E 1,110Total 3,750 Total 3,750

17

The Percent-of-Sales Approach: An Illustration

This 25% growth has to be financed with debt and/or equity.

Theexternal financing required (EFR) is

EFR = 3,750− 3,000︸ ︷︷ ︸Change in T.A.

− (110 + 75)︸ ︷︷ ︸Internal financing

= $565million.

18

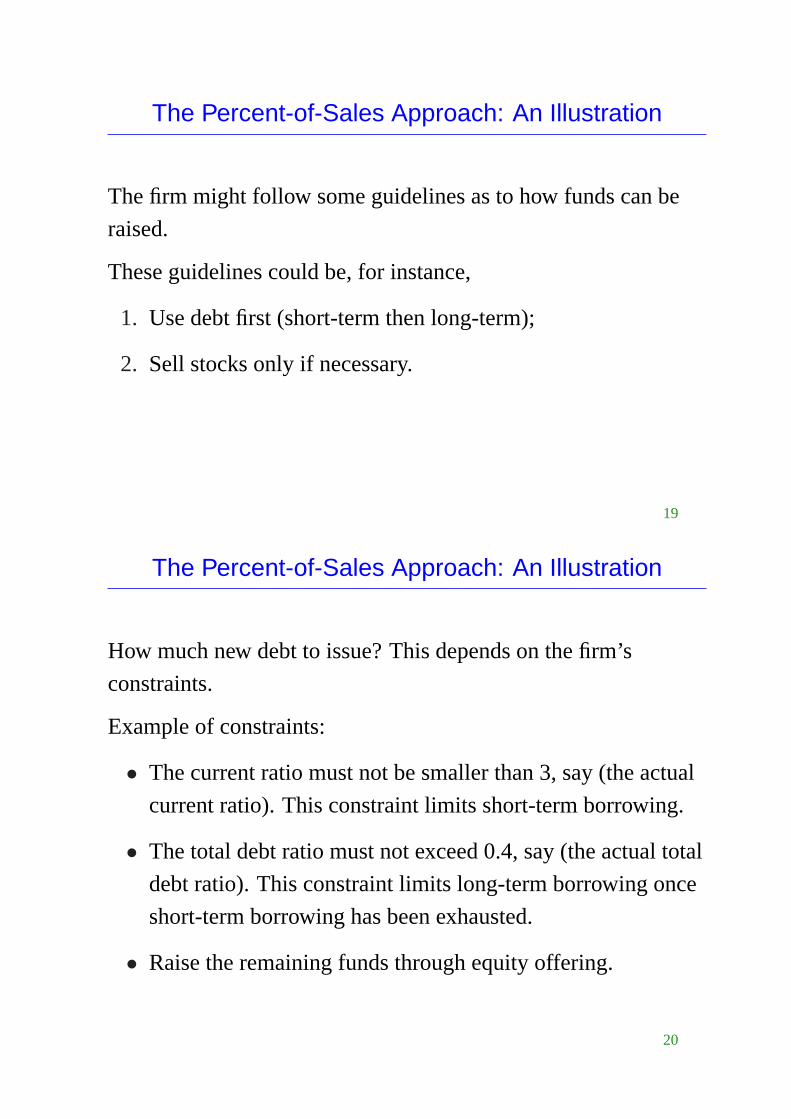

The Percent-of-Sales Approach: An Illustration

The firm might follow some guidelines as to how funds can be

raised.

These guidelines could be, for instance,

1. Use debt first (short-term then long-term);

2. Sell stocks only if necessary.

19

The Percent-of-Sales Approach: An Illustration

How much new debt to issue? This depends on the firm’s

constraints.

Example of constraints:

• The current ratio must not be smaller than 3, say (the actual

current ratio). This constraint limits short-term borrowing.

• The total debt ratio must not exceed 0.4, say (the actual total

debt ratio). This constraint limits long-term borrowing once

short-term borrowing has been exhausted.

• Raise the remaining funds through equity offering.

20

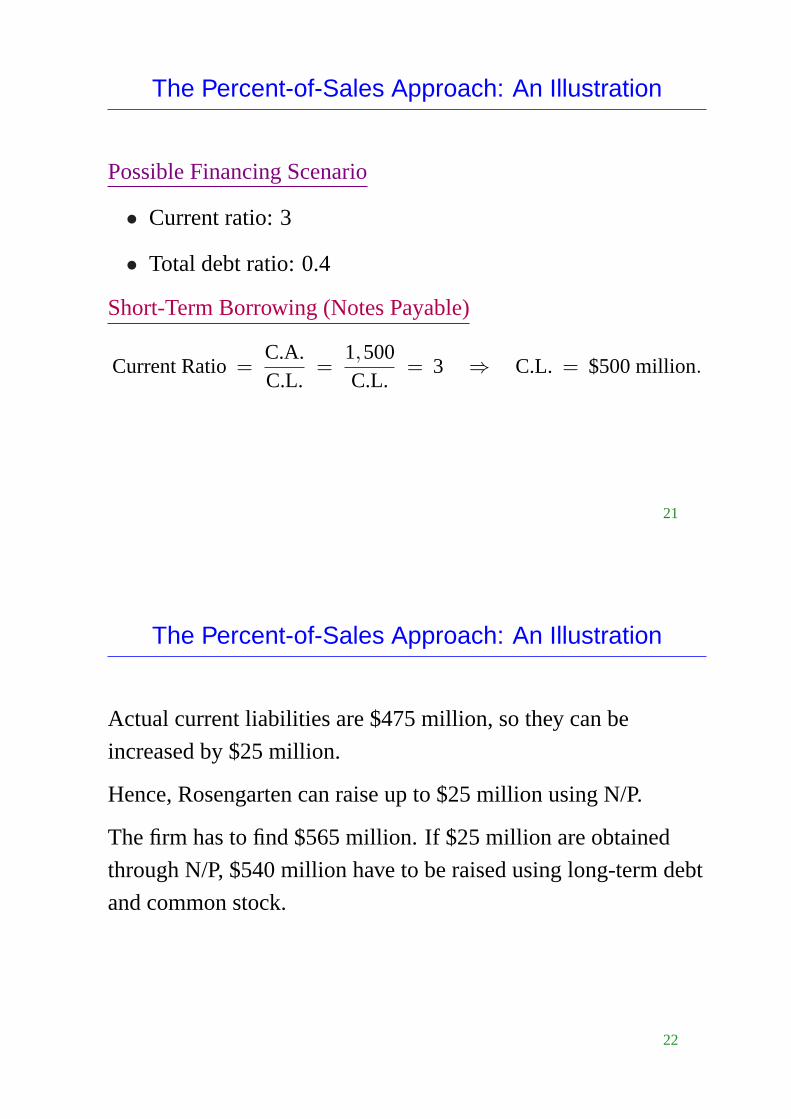

The Percent-of-Sales Approach: An Illustration

Possible Financing Scenario

• Current ratio: 3

• Total debt ratio: 0.4

Short-Term Borrowing (Notes Payable)

Current Ratio=C.A.C.L.

=1,500C.L.

= 3 ⇒ C.L. = $500million.

21

The Percent-of-Sales Approach: An Illustration

Actual current liabilities are $475 million, so they can be

increased by $25 million.

Hence, Rosengarten can raise up to $25 million using N/P.

The firm has to find $565 million. If $25 million are obtained

through N/P, $540 million have to be raised using long-term debt

and common stock.

22

The Percent-of-Sales Approach: An Illustration

Long-Term Debt

Total Debt Ratio=Total debt

Total assets=

Total debt3,750

= 0.4,

which gives

Total debt= $1,500million.

Thus the firm can raise up to

1,500− 500− 800 = $200million

in long-term debt, which leaves us with540−200= $340

million to find.

23

The Percent-of-Sales Approach: An Illustration

The remaining $340 million will be raised through a common

stock issue, which gives the following pro forma statements:

Rosengarten Corporation

Pro Forma Financial Statements (in millions of $)

Income Statement

Sales 1,250Costs (1,000)Taxable income 250Taxes (34%) (85)Net income 165

Dividend (33.33%) 55Earnings retained 110

Balance Sheet

Cash 200 A/P 375A/R 550 N/P 125Inventory 750 C.L. 500C.A. 1,500

LTD 1,000NFA 2,250 C/S 1,140

R/E 1,110Total 3,750 Total 3,750

24

Weaknesses of the Percent-of-Sales Approach

The percent-of-sales approach has three weaknesses:

1. It is unrealistic to assume that all expenses will remain

exactly the same percent of sales from one fiscal year to the

next.

2. With the percent-of-sales method, a company is essentially

locked into a given profit margin.

3. The percent-of-sales approach assumes that all of the firm’s

costs are variable. Fixed costs create “leverage”.

25

Example

Vectra ManufacturingActual and Pro Forma Income Statements (POS Approach)

2002 Percent 2003 Percent(Actual) of sales (Pro Forma) of sales

Sales 100,000 140,000Less: COGS 80,000 80% 112,000 80%Gross Margin 20,000 20% 28,000 20%Less: Operating expenses 10,000 10% 14,000 10%Operating earnings 10,000 14,000Less: Interest expenses 1,000 1% 1,400 1%Earnings before taxes 9,000 12,600Less: Taxes (15%) 1,350 1,890Net income after tax 7,650 7.7% 10,710 7.7%

Common share dividends 4,000 5,600Earnings retained 3,650 5,110

26

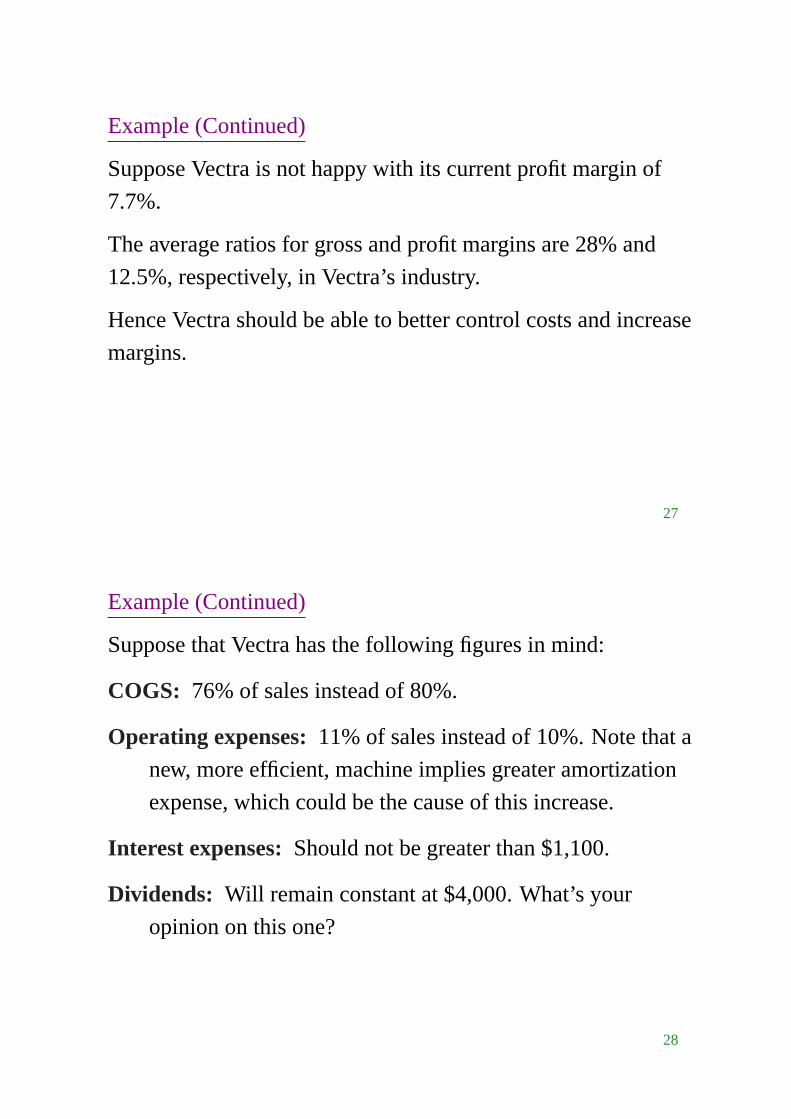

Example (Continued)

Suppose Vectra is not happy with its current profit margin of

7.7%.

The average ratios for gross and profit margins are 28% and

12.5%, respectively, in Vectra’s industry.

Hence Vectra should be able to better control costs and increase

margins.

27

Example (Continued)

Suppose that Vectra has the following figures in mind:

COGS: 76% of sales instead of 80%.

Operating expenses:11% of sales instead of 10%. Note that a

new, more efficient, machine implies greater amortization

expense, which could be the cause of this increase.

Interest expenses:Should not be greater than $1,100.

Dividends: Will remain constant at $4,000. What’s your

opinion on this one?

28

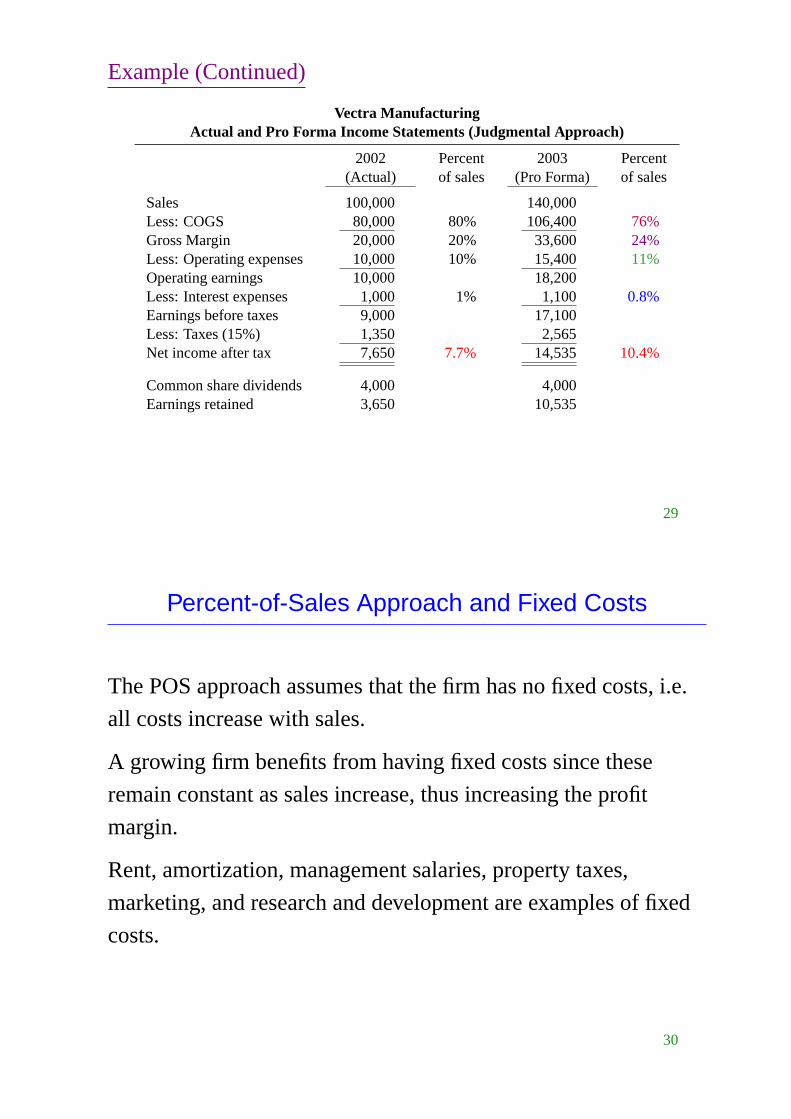

Example (Continued)

Vectra ManufacturingActual and Pro Forma Income Statements (Judgmental Approach)

2002 Percent 2003 Percent(Actual) of sales (Pro Forma) of sales

Sales 100,000 140,000Less: COGS 80,000 80% 106,400 76%Gross Margin 20,000 20% 33,600 24%Less: Operating expenses 10,000 10% 15,400 11%Operating earnings 10,000 18,200Less: Interest expenses 1,000 1% 1,100 0.8%Earnings before taxes 9,000 17,100Less: Taxes (15%) 1,350 2,565Net income after tax 7,650 7.7% 14,535 10.4%

Common share dividends 4,000 4,000Earnings retained 3,650 10,535

29

Percent-of-Sales Approach and Fixed Costs

The POS approach assumes that the firm has no fixed costs, i.e.

all costs increase with sales.

A growing firm benefits from having fixed costs since these

remain constant as sales increase, thus increasing the profit

margin.

Rent, amortization, management salaries, property taxes,

marketing, and research and development are examples of fixed

costs.

30

Variable and Semi-Variable Costs

Variable costs, on the other hand, always vary with sales.

Examples of these are raw material, labour, factory overhead and

sales commissions.

Note that there also are semi-variable costs, which vary with

sales only once they have reached a certain level. That is,

semi-variable costs will not vary for low sales levels.

Take equipment maintenance, for example. A minimum amount

of maintenance must always be performed regardless of the sales

level but more maintenance must be performed as sales increase

beyond a certain point.

31

Profit Margin and Fixed Costs

Let

S ≡ Sales (in $), v ≡ Variable costs per $ sold,

F ≡ Fixed Costs, t ≡ Corporate Tax Rate.

EBT = S− vS− F

NIAT = (1− t)((1−v)S− F),

where NIAT is net income after taxes.

32

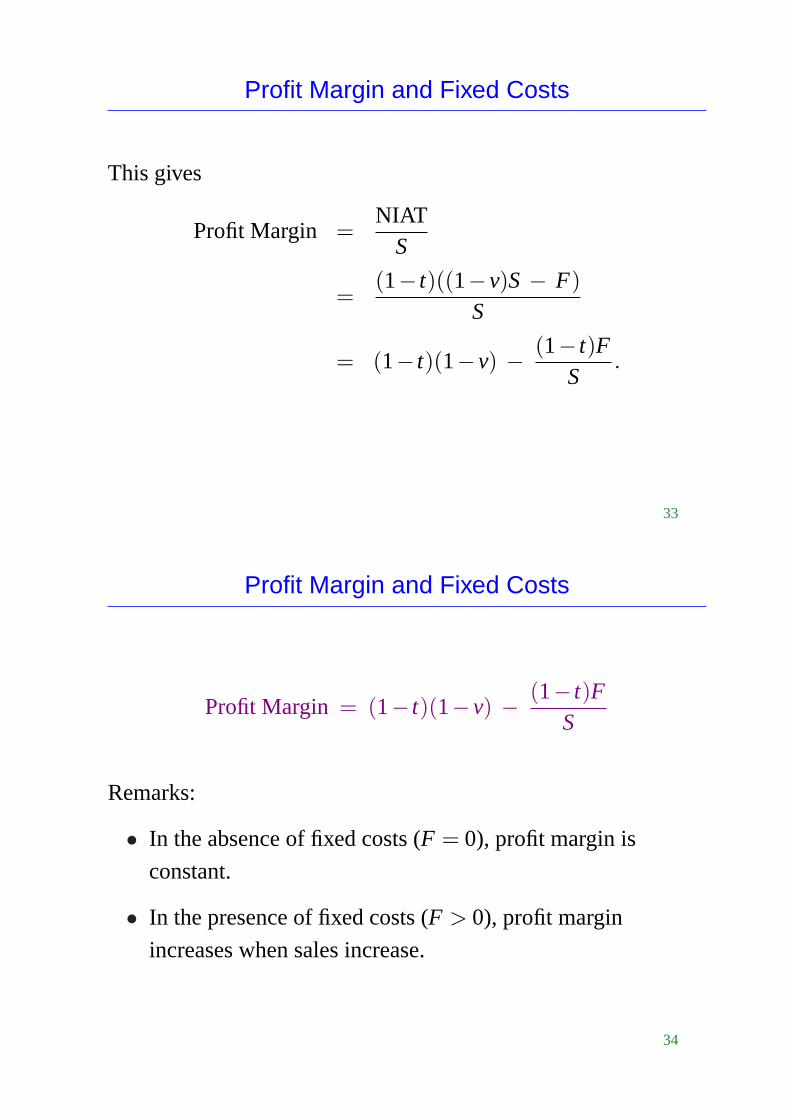

Profit Margin and Fixed Costs

This gives

Profit Margin =NIAT

S

=(1− t)((1−v)S− F)

S

= (1− t)(1−v) − (1− t)FS

.

33

Profit Margin and Fixed Costs

Profit Margin = (1− t)(1−v) − (1− t)FS

Remarks:

• In the absence of fixed costs (F = 0), profit margin is

constant.

• In the presence of fixed costs (F > 0), profit margin

increases when sales increase.

34

Profit Margin and Fixed Costs

In the Vectra example, suppose that, in 2002, fixed costs were$21,000: $12,000 in COGS, $8,000 in operating expenses (OE)and $1,000 in interest expenses. As a fraction of sales, variablecosts were then

Variable CostsSales

=Variable COGS+ Variable OE

S

=(80,000−12,000) + (10,000−8,000)

100,000

=68,000+2,000

100,000= 70%.

35

Profit Margin and Fixed Costs

If variable costs remain 70% of sales and if fixed costs remain

$21,000, net income after taxes (NIAT) in 2003 is expected to be

NIAT = (1− t)((1−v)S− F)

= 0.85× (0.30×140,000− 21,000)

= 17,850

and the profit margin is expected to be

NIATS

=17,850140,000

= 12.75%.

36

Same thing, but using the income statements.

Vectra ManufacturingActual and Pro Forma Income Statements (Judgmental Approach)

2002 Percent 2003 Percent(Actual) of sales (Pro Forma) of sales

Sales 100,000 140,000Less: COGS

Fixed 12,000 12,000Variable 68,000 68% 95,200 68%

Gross Margin 20,000 32,800Less: Operating expenses

Fixed 8,000 8,000Variable 2,000 2% 2,800 2%

Operating earnings 10,000 22,000Less: Interest expenses 1,000 1,000Earnings before taxes 9,000 21,000Less: Taxes (15%) 1,350 3,150Net income after tax 7,650 7.65% 17,850 12.75%

37

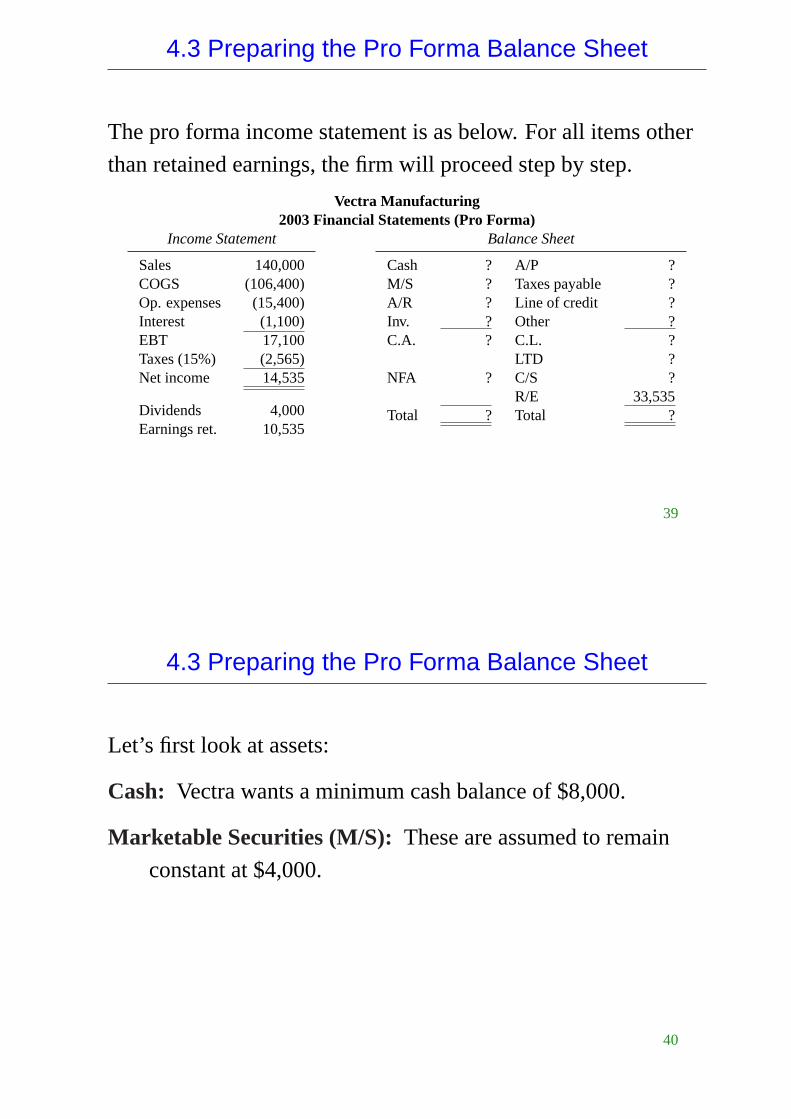

4.3 Preparing the Pro Forma Balance Sheet

In what follows, the pro forma balance sheet for Vectra

Manufacturing will be prepared using thejudgmental approach.

Vectra Manufacturing2002 Financial Statements (Actual)

Income Statement

Sales 100,000COGS (80,000)Op. expenses (10,000)Interest (1,000)EBT 9,000Taxes (15%) (1,350)Net income 7,650

Dividends 4,000Earnings ret. 3,650

Balance Sheet

Cash 6,000 A/P 7,000M/S 4,000 Taxes payable 300A/R 13,000 Line of credit 8,300Inv. 16,000 Other 3,400C.A. 39,000 C.L. 19,000

LTD 18,000NFA 51,000 C/S 30,000

R/E 23,000Total 90,000 Total 90,000

38

4.3 Preparing the Pro Forma Balance Sheet

The pro forma income statement is as below. For all items other

than retained earnings, the firm will proceed step by step.

Vectra Manufacturing2003 Financial Statements (Pro Forma)

Income Statement

Sales 140,000COGS (106,400)Op. expenses (15,400)Interest (1,100)EBT 17,100Taxes (15%) (2,565)Net income 14,535

Dividends 4,000Earnings ret. 10,535

Balance Sheet

Cash ? A/P ?M/S ? Taxes payable ?A/R ? Line of credit ?Inv. ? Other ?C.A. ? C.L. ?

LTD ?NFA ? C/S ?

R/E 33,535Total ? Total ?

39

4.3 Preparing the Pro Forma Balance Sheet

Let’s first look at assets:

Cash: Vectra wants a minimum cash balance of $8,000.

Marketable Securities (M/S): These are assumed to remain

constant at $4,000.

40

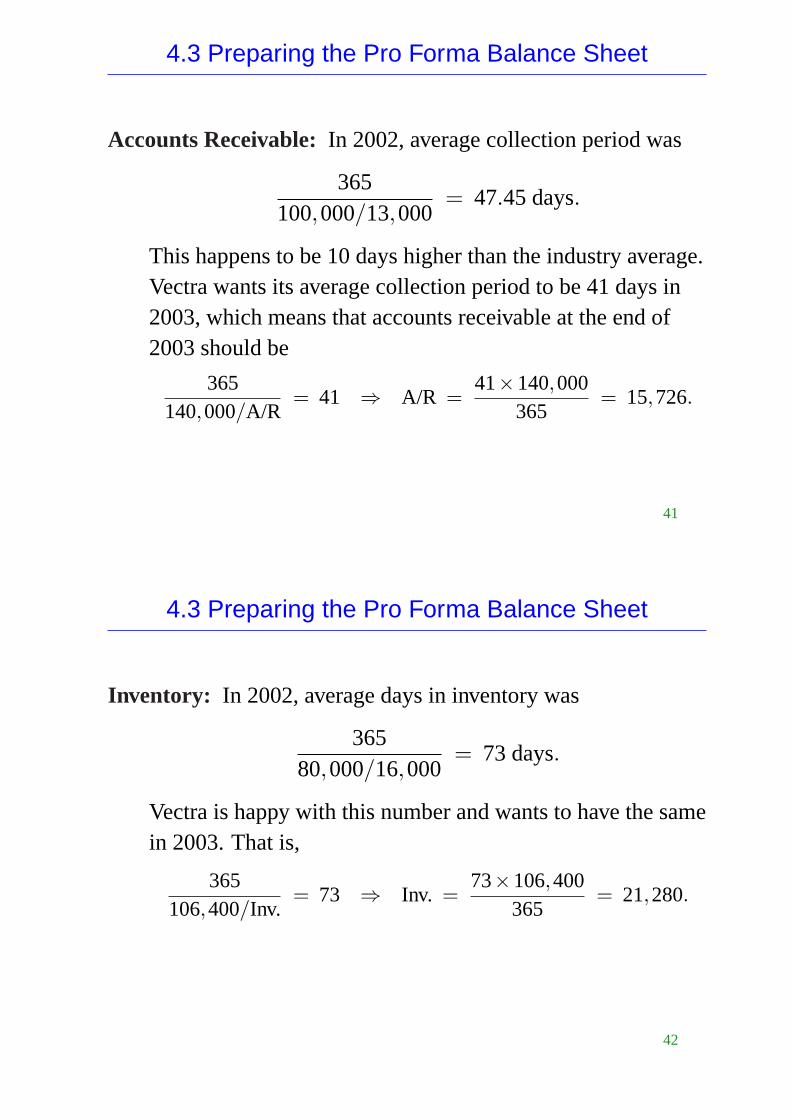

4.3 Preparing the Pro Forma Balance Sheet

Accounts Receivable:In 2002, average collection period was

365100,000/13,000

= 47.45days.

This happens to be 10 days higher than the industry average.Vectra wants its average collection period to be 41 days in2003, which means that accounts receivable at the end of2003 should be

365140,000/A/R

= 41 ⇒ A/R =41×140,000

365= 15,726.

41

4.3 Preparing the Pro Forma Balance Sheet

Inventory: In 2002, average days in inventory was

36580,000/16,000

= 73days.

Vectra is happy with this number and wants to have the samein 2003. That is,

365106,400/Inv.

= 73 ⇒ Inv. =73×106,400

365= 21,280.

42

4.3 Preparing the Pro Forma Balance Sheet

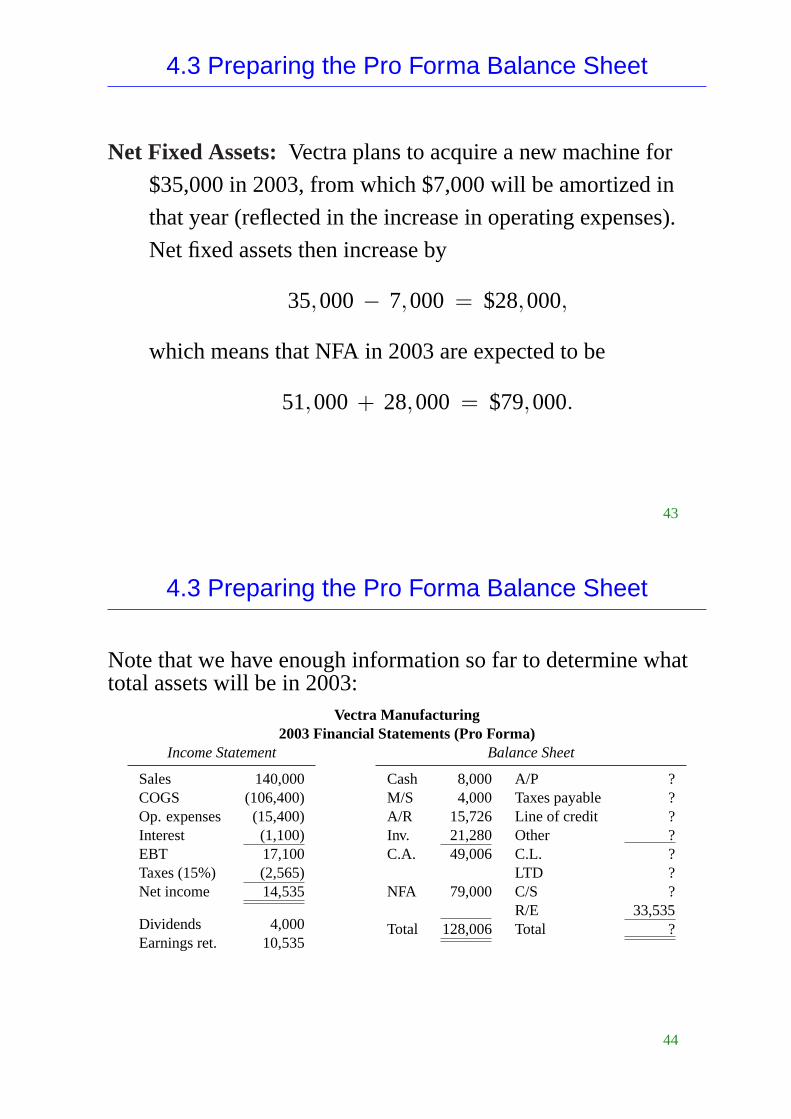

Net Fixed Assets:Vectra plans to acquire a new machine for

$35,000 in 2003, from which $7,000 will be amortized in

that year (reflected in the increase in operating expenses).

Net fixed assets then increase by

35,000− 7,000 = $28,000,

which means that NFA in 2003 are expected to be

51,000 + 28,000 = $79,000.

43

4.3 Preparing the Pro Forma Balance Sheet

Note that we have enough information so far to determine whattotal assets will be in 2003:

Vectra Manufacturing2003 Financial Statements (Pro Forma)

Income Statement

Sales 140,000COGS (106,400)Op. expenses (15,400)Interest (1,100)EBT 17,100Taxes (15%) (2,565)Net income 14,535

Dividends 4,000Earnings ret. 10,535

Balance Sheet

Cash 8,000 A/P ?M/S 4,000 Taxes payable ?A/R 15,726 Line of credit ?Inv. 21,280 Other ?C.A. 49,006 C.L. ?

LTD ?NFA 79,000 C/S ?

R/E 33,535Total 128,006 Total ?

44

4.3 Preparing the Pro Forma Balance Sheet

Let’s now consider liabilities and equity:

Accounts Payable: Purchases are 45% of COGS and Vectra’s

average payment period in 2002 was

365(0.45×80,000)/7,000

= 71days.

Suppliers want this average to be reduced to 62 days in2003, which translates into

365(0.45×106,400)/A/P

= 62days ⇒ A/P =62×0.45×106,400

365= 8,133.

45

4.3 Preparing the Pro Forma Balance Sheet

Taxes Payable:These are assumed to be 25% of the tax amount

that appears on the income statement, which is, for 2003,

25%×2,565 = 641.

Other Current Liabilities: Remain unchanged.

Line of Credit: Depends on the financing plan.

Long-Term Debt: Depends on the financing plan.

Common Stock: Depends on the financing plan.

46

4.3 Preparing the Pro Forma Balance Sheet

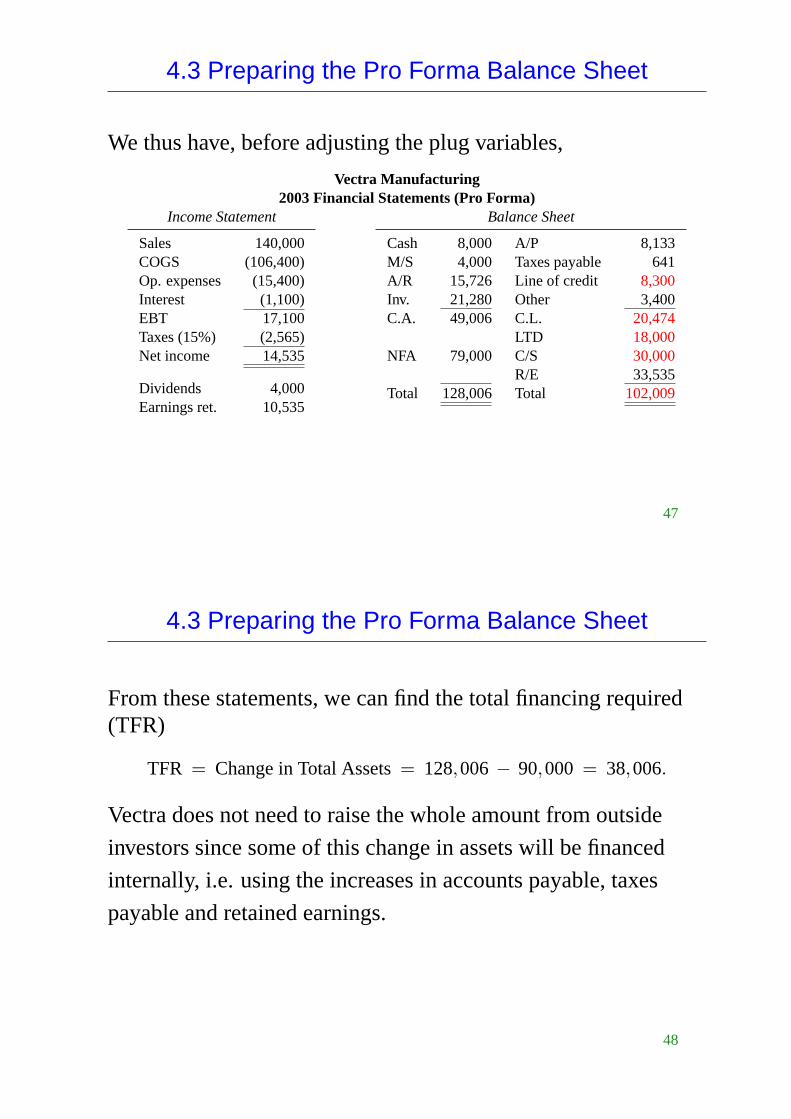

We thus have, before adjusting the plug variables,

Vectra Manufacturing2003 Financial Statements (Pro Forma)

Income Statement

Sales 140,000COGS (106,400)Op. expenses (15,400)Interest (1,100)EBT 17,100Taxes (15%) (2,565)Net income 14,535

Dividends 4,000Earnings ret. 10,535

Balance Sheet

Cash 8,000 A/P 8,133M/S 4,000 Taxes payable 641A/R 15,726 Line of credit 8,300Inv. 21,280 Other 3,400C.A. 49,006 C.L. 20,474

LTD 18,000NFA 79,000 C/S 30,000

R/E 33,535Total 128,006 Total 102,009

47

4.3 Preparing the Pro Forma Balance Sheet

From these statements, we can find the total financing required(TFR)

TFR = Change in Total Assets= 128,006− 90,000 = 38,006.

Vectra does not need to raise the whole amount from outside

investors since some of this change in assets will be financed

internally, i.e. using the increases in accounts payable, taxes

payable and retained earnings.

48

4.3 Preparing the Pro Forma Balance Sheet

The funds raised from outside investors, theexternal financing

required, is found as follows:

Total financing required 38,006

Less: Internal sources

Increase in accounts payable 1,133

Increase in taxes payable 341

Reinvested profits 10,535

Total internal sources 15,009

External financing required 25,997

49

4.3 Preparing the Pro Forma Balance Sheet

Note that my example differs from the one in the book as I

assumed the dividend payment to remain $4,000.

Now that you know Vectra’s external financing required, what

are your suggestions regarding a possible financing plan?

50