wk47. this week's news a snapshot on the economic and...

TRANSCRIPT

This Week’s News Snapshot- ending November 28th

(Week 47/14)

Global Economy:

Stronger policy response needed to avoid risks to growth, especially in the euro area, says OECD in latest

Economic Outlook

The Economic Outlook draws attention to a global economy stuck in low gear, with growth in trade and investment

under-performing historic averages and diverging demand patterns across countries and regions, both in advanced

and emerging economies.

“We are far from being on the road to a healthy recovery. There is a growing risk of stagnation in the euro zone that

could have impacts worldwide, while Japan has fallen into a technical recession,” OECD Secretary-General Angel

Gurria said. “Furthermore, diverging monetary policies could lead to greater financial volatility for emerging

economies, many of which have accumulated high levels of debt.”

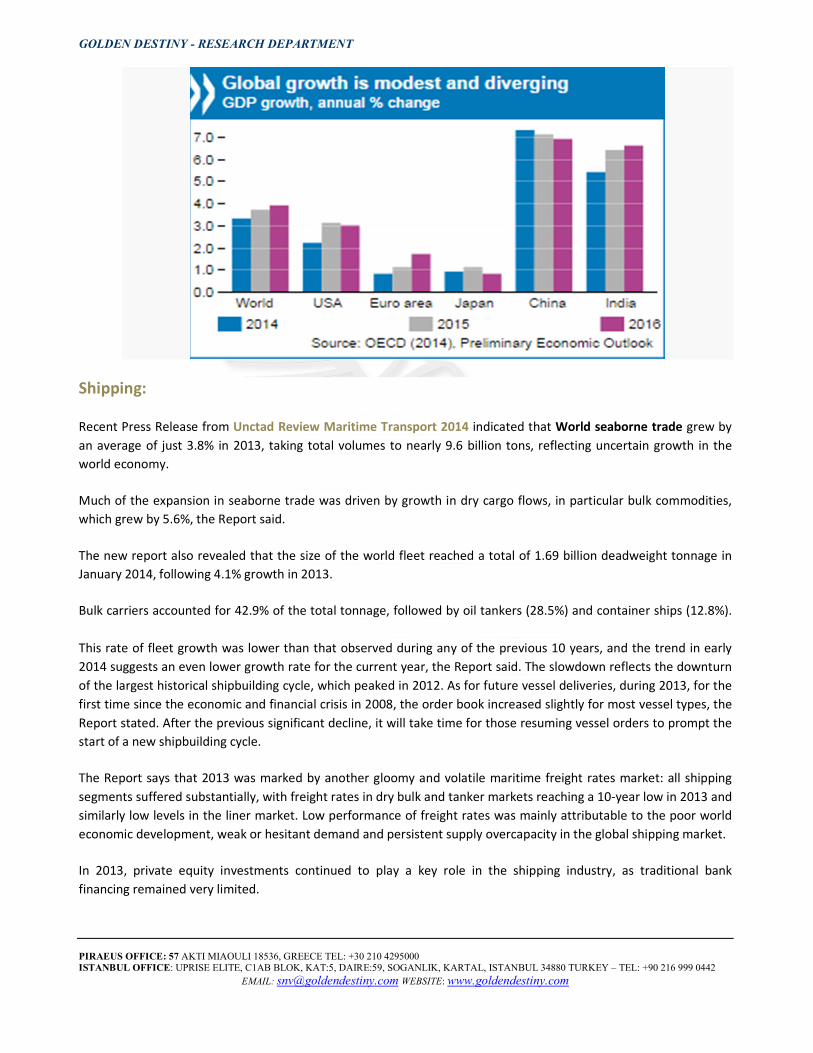

Global GDP growth is projected to reach a 3.3% rate in 2014 before accelerating to 3.7% in 2015 and 3.9% in 2016,

according to the Outlook. This pace is modest compared with the pre-crisis period and somewhat below the long-

term average.

• The euro area is projected to grow by 0.8% in 2014, before slight acceleration to a 1.1% rate in 2015 and a

1.7% rate in 2016. With the euro zone outlook weak and vulnerable to further bad news, a stronger policy

response is needed, particularly to boost demand,” said OECD Chief Economist Catherine L Mann. “That will

mean more action by the European Central Bank and more supportive fiscal policy, so that there is space for

deeper structural reforms to take hold. A Europe that is doing poorly is bad news for everyone.”

• Among the major advanced economies activity is gaining strength in the United States, which is projected to

grow by 2.2% in 2014 and around 3% in 2015 and 2016. In Japan, growth was impacted by consumption tax

hikes in 2014, with expected growth of only 0.4% in 2014, and rises modestly to 0.8% in 2015 and 1% in

2016.

• Large emerging economies are projected to show diverging performance over the coming years. A

slowdown in China, towards more sustainable growth rates, will see GDP growth drop from a 7.3% growth

rate in 2014 to a 7.1% rate in 2015 and a 6.9% rate in 2016. However, the rapid increase in credit, rising

share of non-bank credit as well as housing market and local government activity are raising concerns about

financial stability. A scenario in the Outlook shows that a 2-percentage point decline in the growth of

Chinese domestic demand would lower global GDP by 0.3 percent per year.

• “The Chinese authorities will need to use all of their policy instruments to keep the economy on an even

keel,” Ms Mann said.

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

Shipping:

Recent Press Release from Unctad Review Maritime Transport 2014 indicated that World seaborne trade grew by

an average of just 3.8% in 2013, taking total volumes to nearly 9.6 billion tons, reflecting uncertain growth in the

world economy.

Much of the expansion in seaborne trade was driven by growth in dry cargo flows, in particular bulk commodities,

which grew by 5.6%, the Report said.

The new report also revealed that the size of the world fleet reached a total of 1.69 billion deadweight tonnage in

January 2014, following 4.1% growth in 2013.

Bulk carriers accounted for 42.9% of the total tonnage, followed by oil tankers (28.5%) and container ships (12.8%).

This rate of fleet growth was lower than that observed during any of the previous 10 years, and the trend in early

2014 suggests an even lower growth rate for the current year, the Report said. The slowdown reflects the downturn

of the largest historical shipbuilding cycle, which peaked in 2012. As for future vessel deliveries, during 2013, for the

first time since the economic and financial crisis in 2008, the order book increased slightly for most vessel types, the

Report stated. After the previous significant decline, it will take time for those resuming vessel orders to prompt the

start of a new shipbuilding cycle.

The Report says that 2013 was marked by another gloomy and volatile maritime freight rates market: all shipping

segments suffered substantially, with freight rates in dry bulk and tanker markets reaching a 10-year low in 2013 and

similarly low levels in the liner market. Low performance of freight rates was mainly attributable to the poor world

economic development, weak or hesitant demand and persistent supply overcapacity in the global shipping market.

In 2013, private equity investments continued to play a key role in the shipping industry, as traditional bank

financing remained very limited.

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

Dry Segment: Seaborne iron ore price tumbled to record lows for the first time since 2009 favoring Chinese buyers

who are holding back their plans on purchasing spot cargoes. In addition, cold weather in China is causing fall in the

country’s steel consumption as productivity in the construction industry, a major driver of steel demand wanes.

Seaborne iron ore prices tumbled below the $70/dry mt CFR North China mark for the first time since June 2009,

with the benchmark Platts 62% Fe Iron Ore Index being assessed at $69.75/dmt CFR North China Friday, November

21.

The last time the 62% Fe IODEX was lower was on June 3, 2009, when it was assessed at $69.50/dmt CFR North

China, making the current price the lowest point in nearly five-and-a-half years, Platts data showed.

The last week ended with small decrease in spot chartering activity. According to figures from Commodore Research,

113 vessels were chartered to haul dry bulk commodities in the spot market last week, 4 less than the previous

week. In addition, 4 vessels were chartered for period deals, 6 less than the previous week. 1 was for a period of a

year or more. There was also a decrease in iron ore fixture volumes as 31 iron ore fixtures came to the market last

week, 11 less than the previous week and 5 less than the trailing four week average. 30 of last week’s iron ore

fixtures were for capesize vessels, 10 less than the previous week and 4 less than the trailing four week average.

28 vessels were chartered to haul spot iron ore cargoes to Chinese buyers last week, 10 less than the previous week

but just 3 less than the trailing four week average. Overall, Chinese demand for imported iron ore cargoes is poised

to stay strong s as China’s steel mills continue to consume a greater amount of imported iron ore over domestic iron

ore. In the thermal coal market, 6 vessels were chartered to haul spot thermal coal cargoes to Chinese buyers last

week. This is 1 less than was chartered during the previous week but the same as the trailing four week average.

While Chinese thermal coal fixture volume has increased from October’s very low level, volumes are still historically

low.

On Friday November 28th, BDI closed at 1153 points, down by 13% from last week’s closing and down by 37% from a

similar week closing in 2013, when it was 1821 points. All dry indices closed in green, while the largest weekly

increase is recorded in the cape segment. BCI is up by 7% week-on-week, BPI is up by 6% week-on-week, BSI is up

5% week-on-week, BHSI is up by 6% week-on-week.

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

Capesizes are currently earning $14,564/day, down by $8,426/day from last week’s closing and panamaxes are

earning $8,943/day, up by $500/day from last week’s closing. At similar week in 2013, capesizes were earning

$24,611/day, while panamaxes were earning $13,293/day. Supramaxes are trading at $10,310/day, up by $462/day

from last week’s closing, about 29% lower than capesize and 15% higher than panamax earnings. At similar week in

2013, supramaxes were getting $15,424/day, hovering at 37% lower levels than capesizes versus 29% today’s lower

levels. Handysizes are trading at $7,124/day, up by $418/day from last week’s closing; when at similar week in 2013

were earning $10,870/day.

Wet Segment: A firm upward trend is evidenced in the crude tanker segment, with remarkable highs in the

aframax and suezmax vessel category.

In the VLLC segment, rates in AG-USG stayed at WS29 for three straight weeks, up by 9 points from the beginning of

October. In AG-SPORE and AG-JPN routes, rates gained 3 points from previous week and moved up to WS 55, 14.5

points above from the beginning of October. In WAFR-USG, rates increased by 10 points to WS75 (up by 30 points

from the beginning of October) and in WAFR-China route, rates stayed at WS55 for three straight weeks (up by 10

points from the beginning of October).

In the suezmax segment, rates in WAFR-USAC showed an unexpected weekly increase of 57.5 points and concluded

at WS137.5 (up by 62.5 points from the beginning of October), while in B.SEA-Med route, rates moved up by 42.5

points to WS 135 (up by 60 points from the beginning of October). In the aframax segment, rates in the Caribbean

market recorded a weekly decrease of 15 points and concluded at WS145 (up by 40 points from the beginning of

October), while in the Med-Med route, rates increased by 70points to WS220 (up by 142 points from the beginning

of October).

28/11/2014 21/11/2014 2013 % %

week 47 week 46 w-o-w week 47 w-o-w y-o-y

Dry BDI 1153 1324 -171 1821 -13% -37%

Capesize BCI 2151 2014 137 3089 7% -30%

Panamax BPI 1120 1055 65 1665 6% -33%

Supramax BSI 986 942 44 1475 5% -33%

Handy BHSI 491 462 29 764 6% -36%

28/11/2014 21/11/2014 2013 % %

week 47 week 46 w-o-w week 47 w-o-w y-o-y

Capesize Average T/C routes 14564 22990 -8426 24611 -37% -41%

Panamax Average T/C routes 8943 8443 500 13293 6% -33%

Supramax Average T/C routes 10310 9848 462 15424 5% -33%

Handy Average T/C routes 7124 6706 418 10870 6% -34%

Summary of Baltic Dry Indices & Average Time Charter Earnings

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

Route Vessel Size

VLCC: AG-USG 280,000t WS 29 (last week WS 29) Steady

AG-JPN 265,000t WS 55 (last week WS 52) Upward Trend

AG-SPORE 270,000t WS 55 (last week WS 52) Upward Trend

WAFR-USG 260,000t WS 75 (last week WS 65) Upward Trend

WAFR-China 260,000t WS 55 (last week WS 55) Steady

Route Vessel Size

Suez: WAFR-USAC 130,000t WS 137.5 (last week WS 80) Upward Trend

B.SEA-Med 130,000t WS 135 (last week WS92.5) Upward Trend

Route Vessel Size

Afram: CBS-USG 70,000t WS 145 (last week WS 160) Downward Trend

Med-Med 80,000t WS 220 (last week WS 155) Upward Trend

Route Vessel Size

Clean: AG-JPN 75,000t WS 112 (last week WS 115) Downward Trend

AG-JPN 55,000t WS 119 (last week WS 127.5) Downward Trend

In terms of oil demand, 2015 indicates lower figures according to OPEC sub-committee. An OPEC sub-committee

affirmed the group’s forecast that demand for its crude will be lower next year, according to three officials who

attended the meeting in Vienna. The Organization of Petroleum Exporting Countries forecast on Nov. 12 that

demand for its crude will fall to 29.2 million barrels a day in 2015, from 29.5 million this year. Demand for OPEC’s

crude is shrinking as growth in global consumption slows and booming shale output pushes U.S. production to the

highest level in three decades. Twenty analysts surveyed this week by Bloomberg News were evenly split on

whether the group will agree a production cut at its meeting on Nov. 27, or maintain its existing target of 30 million

barrels a day.

Meanwhile, Chinese crude oil imports from its major suppliers, including Iran, rose significantly during October

versus a year ago. According to last figures from the General Administration of Customs, crude imports from Iran last

month surged to 1.44 million mt, or an average 340,027 barrels/day, up by 35.5% from a year earlier. China

imported less crude from Saudi Arabia and Angola in October despite its total crude imports rising 18% from a year

earlier to 5.7 million barrels/day. In addition, Chinese crude imports from Iraq in October increased by 45.1% year-

on-year to 1.96 million mt, although the volumes decreased 20.5% from September. Overall for the first 10 months

of the year from January to October, China’s total imports of crude oil rose 9.2% to 6.09 million barrels/day, which is

the fastest pace of growth since 2010.

LNG Segment: Global LNG prices are on decrease as Australia and Nigeria offer fresh supply and LNG demand for

December and January show a flat trend. On Friday, Asian spot LNG prices for January delivery fell 70 cents week-on-

week to around $10.10 per million British thermal units (mmBtu), while prices for December delivery dropped to

$9.85 per mmBtu. More supply is due from Australia’s North West Shelf export project, which on Monday will close

a tender to sell at least four cargoes for December and January loading.

The tender is likely to draw limited demand from Asian buyers, which are facing lower winter import costs for the

first time since the Fukushima nuclear disaster in 2011, thanks to high inventories left over from a mild summer and

winter. “Buyers are careful to indicate any demand. They’ve been saying for months in a much disciplined manner

that they don’t need any cargoes whatsoever,” a trader from oil major said.

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

According to 2014 Gas Market Report released by the Bureau of Resources and Energy Economies, global LNG trade

is booming and Australia will play a growing role in the Asian market despite increasing competition and cost

pressures. Australia is well on its way to become the world’s largest LNG exporter, with seven new LNG projects

currently under construction. This scale of development has put pressure on labor and capital costs, which were

often already high as a result of the scope and remoteness of a number of projects.

Additional supply is also emerging from North America and other sources. This is expected to put downwards

pressure on LNG prices globally, including in Asia where the LNG price has been relatively high in recent years.

However, Australia is projected to remain a long term supplier to Asia trading partners. This will continue because of

growing production from conventional basins off Western Australia and the Northern Territory, as well as growing

unconventional production and world-first exports of coal seam gas.

Container Segment:

The Shanghai Container Freight Index has stayed above of 1,000 points for four straight weeks, with sharp weekly

decrease in Asia –Europe route for two straight weeks. Asia-Europe and Asia-Med rates show a negative trend from

mid November, while transpacific rates record gains. The index ended at 1013 points last week, 38 points down from

previous closing and down by 183 points from the levels of beginning August.

In Asia-Europe route, rates decreased to $809/TEU, down by $125/TEU (13% w-o-w) and in Asia-Med, rates moved

down by $114/TEU (10% w-o-w) and concluded at $1013/TEU. The levels in Asia-Europe route are now down by

$646/TEU from the beginning of August and down by $595/TEU in Asia-Med route.

In transpacific routes, rates moved up by $68/FEU (3% w-o-w) in Asia-USWC and up by $39/FEU (1% w-o-w) in Asia-

USEC route. Rates in Asia-USWC route concluded at $2,158/FEU and $4,229/FEU in Asia-USEC route. Compared with

the beginning of August, rates in Asia-USWC route are now down by $40/FEU and up by $42/FEU in Asia-USEC route.

Rates in Asia-USWC are now above the barrier of $2000/FEU and in Asia-USEC route above the barrier of $4000/FEU

for two consecutive weeks.

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

Shipbuilding:

South Korean shipbuilders have surpassed their Chinese rivals in terms of delivery record for the first time in five

years since 2009. This is because shipowners have preferred to choose shipyards with higher productivity and more

advanced technology, said analysts in a research note. Hana Daetoo Securities analysts Moohyun Park and Jaeseon

Yoo said, “For the first 10 months of the year, [South] Korea delivered vessels of a combined 10,027cgt compared to

China’s 9,784cgt.” They continued, “Delivery record is the clearest criterion for a shipyard’s capacity. Although

Korean shipyards have recently experienced lower profits due to delay of the delivery, they have concentrated on

selective order intended to secure profitability since the [end] of last year.” “On the other hand, Chinese shipyards

still have increased their orders through low vessel price and emphasized on their unproven fuel efficiency effect. As

a result, China’s volume of the delivery has not increased.” Park and Yoo said. The analysts highlighted that delivery

record is more important than new orders, and it is the clearest criterion for a shipyard’s capability. “Shipowners put

a premium on delivery record as well as price and time limit when they select [a] shipyard. Top-tier shipowners have

a tendency to deal with yards with excellent productivity. Vessel technology evolution is speeding up amid keen

competition on fuel efficiency.” They concluded, “Chinese shipyards’ delivery record will be more reduced due to

lack of technology to cater for shipowners’ requirement for evolved ship[s].”

Shipping Finance:

Ship financing deals: Oldendorff Carriers sealed export credit financing for the construction of two eco ultramax

bulkers of 60,500dwt at Japan Marine United. The 12 year term loans have been arranged by the Japan Bank for

International Cooperation (JBIC) and will be co-financed with Deutsche Bank covered by buyer’s credit insurance

from Nippon Export and Investment Insurance (NEXI).

Capital Market:

Scorpio Bulkers Inc. previously announced that it has entered into a Securities Purchase Agreement with certain

institutional investors for the private placement of its shares of common stock, par value $0.01 per share . An

aggregate of 40,000,000 Common Shares will be sold at a price of $3.75 per share, resulting in gross proceeds to the

Company of $150 million. The Company intends to use the net proceeds of this offering to fund installment

payments due under its newbuilding program, and the remaining amount, if any, for general corporate purposes and

working capital. The Company expects to issue the Common Shares on or about November 20, 2014. RS Platou

Markets, Inc. and RS Platou Markets AS acted as Placement Agents for the private placement.

GOLDEN DESTINY Research & Valuations Department

Maria Bertzeletou, Shipping Analyst

For more Research Services, please contact us: Email: [email protected]

GOLDEN DESTINY - RESEARCH DEPARTMENT

PIRAEUS OFFICE: 57 AKTI MIAOULI 18536, GREECE TEL: +30 210 4295000 ISTANBUL OFFICE: UPRISE ELITE, C1AB BLOK, KAT:5, DAIRE:59, SOGANLIK, KARTAL, ISTANBUL 34880 TURKEY – TEL: +90 216 999 0442

EMAIL: [email protected] WEBSITE: www.goldendestiny.com

Disclaimer: All the information contained in this report is given in good faith, but without any guarantee from our part, and is based on our

S&P Market Reports and Insight Market Information provided and/or collected from various sources. This report is presented for

the sole and exclusive information of its recipients and whilst every care has been taken in the preparation of this report, no

representation or warranty, express or implied, is made by Golden Destiny S.A. in respect of the accuracy, completeness or

correctness of the information contained herein. Neither our company nor its directors or employees assumes or accepts any

liability whatsoever for any loss or damage incurred by any person whatsoever in relation to and/or as a result of the use of

and/or due to any person’s reliance on the information contained in this report. Furthermore, no responsibility is accepted in

respect of any errors or inaccuracies which may be contained in this report.