will building owners invest in the energy efficiency of

TRANSCRIPT

Chapter 4

Will Building Owners Invest in theEnergy Efficiency of City Buildings?

Contents

Page

introduction . . . . . . . . . . . . . . . . . . . . . . . . . 99

Context for Building OwnerDecisionmaking in 1980-81..........101

W h o O w n s W h a t ? . . . . . . . . . . . . . . . . . . . . 1 0 4

Impact of Ownership on Building Retrofit. .107

Impact of Building Types on the Likelihoodof Retrofit. . . . . . . . . . . . . . . . . . . . . . .. 116

Likelihood of Retrofit in MultifamilyBuildings . . . . . . . . . . . . . . . . . . . . . . . . 117

Likelihood of Retrofit in CommercialBuildings . . . . . . . . . . . . . . . . . . . . . . . . 121

Potential for Retrofit in MarginalN e i g h b o r h o o d s . . . . . . . . . . . . . . . . . . . 1 2 6

Page

Potential for Increasing the Rate of Retrofitby Building Owners. . . . . . . . . . . . . . . .127

Information: Diminishing the Risks ofRetrofit . . . . . . . . . . . . . . . . . . . . .. ....132

Impact of Less Costly Financing on theP a c e of Retrofit . . . . . . . . . . . . . . . . . . . .133

LIST OF TABLES

Table No. Page

27. Likelihood of Retrofit by Building Typeand Owner Type. . , . . . . . . . . . . .- . . . .100

28. Types of Building Owners Interviewed. 10129. Building Types Covered in Building

O w n e r Interviews. . . . . . . . . . . . . . . . . .101

Table NO. Page30.31.

32

334

34.

35.

36.

37.

38.

39.

40.

41.

42.

43<

44.

Energy’s Share of Operating Costs. .. ..162Ownership Types Believed To Be MostCharacteristic of Various Building Types 105Ownership of Office Buildings–Atlanta, 1974, . . . . . . . . . . . . . . . . ., ..105Holders of Residential and CommercialMortgages. . . . . . . . . . . . . . . . . . . . . .. .106Retrofit Payback Criteria, HoldingPeriods, and Access to Financing andAdvice Among Different Types ofOwners . . . . . . . . . .................109Annual Heating Fuel Costs inApartment Buildings. .. .. ... ... ... ..118National Distribution of MeteringTypes of Rental Units . . . . . . . . . . . ....119Landlords’ Ranking of Reasons forDisinvestment. . .. .. .. .. ... ... .,.$.126Thirteen Types of Buildings WithSignificantly Different Retrofit Options. 128Typology of Small MultifamilyBuildings According to the Likelihoodof Major Improvement in EnergyEfficiency . . . . . . . . . . . . . . . . . . . . . . . . 128Typology of Large MultifamilyBuildings According to the Likelihoodof Major improvement in EnergyEfficiency . . . . . . . . . . . . . . . . . . . . . . . . 129Typology of Small Commercialbuildings According to the Likelihoodof Major Improvement in EnergyEfficiency. .. ..... . . . . . . . . . . . . . . 130Typology of Large CommercialBuildings According to the Likelihoodof Major Improvement in EnergyEfficiency ..,.... . . . . . . . . . . . . . . . . . 131Percentage of Apartment BuildingOwners Who Perceived Measures TheyInstalled To Be Effective. . ...........132Impact of uncertainty on ExpectedAnnual Energy Savings From aRetrofit Costing $10,000. . ...........133

Table No.

45. Building Owner Preferences forCredits or Financing Subsidies. .

LIST OF FIGURES

Figure No.

34. Comparison of Prices of Naturaland the Prime Rate, 1970-81 . . .

35

36

PageTax. . . . . . 139

Page

Gas. . . . . . 103

Frequency of Major and Minor EnergyRetrofit Among Building OwnersInterviewed .. .. ... .. ...... . . . . . 108Frequency of Retrofits Among BuildingTypes Covered in Building Owner -

I n t e r v i e w s . . . , . . . . . . . . . . . . . . . . . . , . 1 1 637. Apartment Operating Revenues and

38.

39.

40.

41*

Expenses, 1970-76. . . . . . . . . . ......118Combinations of Loan Terms and lnterestRates Which Allow the Value of EnergySavings to Exceed the Cost of BorrowedMoney the First Year. .. .. ... ... ... ..I34Cash From Operations for an 18-UnitApartment Building With and Withoutan Energy Retrofit. . . . . . . . . . . . . . . . . .136impact of Energy Retrofit Subsidies onPretax and Aftertax Cash Flow for aPrototypical Apartment Building. ..137lmpact of a Retrofit on Pretax andAftertax Cash Flow for Two otherPrototypical Apartment Buildings. ....138

BOXES

PageC. Permanent Financing: Roles of

Mortgage Banks and InsuranceCompanies . . . . . . . . . . .............,106

D. Corporations: Taxes and Accounting....... 106E. A Question of Value: How the Appraiser

Sees It. . . . . . . . . . . . . . . ............113F. Role of the Property Manager. ... ... ...113

Chapter 4

Will Building Owners Invest in theEnergy Efficiency of City Buildings?

INTRODUCTION

Virtually all types of city buildings (as is clearfrom ch. 3) can be retrofit to save a substantialportion of their energy. Some can be retrofiteasily and cheaply. Others can be retrofit onlywith difficulty and at considerable expense butnonetheless in such a way that the expensewould be justified by energy savings over thebuilding’s lifetime.

The question remains, however, will thesebuildings be retrofit? The answer given by thischapter is that city buildings will not be retrofitunless several more conditions are met beyondthe fact that the building is cost effective to ret-rofit.

If a building that can be retrofitted is to be ret-rofitted three additional conditions must bemet:

●

●

●

the building’s energy inefficiency mustcause a noticeable loss i n present or futurereturn from the building,an investment in improved energy efficien-cy is consistent with the building owner’sgoals, andthe building owner has the means—ade-quate information, decisionmaking ability,time, and financial resources—to make theinvest ment.

Furthermore, even if the building owner iswilling and able to make such an investment, itwiII not happen unless there are businessesready to recommend and install the retrofit. Thestate of the energy retrofit business is mentionedbriefly in this chapter but is discussed morecompletely in chapter 7.

For example, it should be easy (given the anal-ysis in ch. 3) to prescribe a set of very cost-effec-tive retrofits for a small frame multifamily build-ing with an old inefficient steam system in a citywith a cold climate. Yet for the identical build-ing with identical retrofit potential the chances

of retrofit range from good if it is an owner-occupied building in an up-and-coming neigh-borhood to very poor if it is owned by an absen-tee landlord, and is located in a declining neigh-borhood.

A curtain wall office building with a decentral-ized heating system of electric baseboard heatand window air conditioners has much poorerprospects for inexpensive easy retrofit than thesmall frame steam-heated building. In mostcases, only expensive retrofits are available forsuch a building, replacing the electric resistanceheaters with heat pumps or installing doubleglazed window panels. Nonetheless, because ofthe potential goals of its owners and their re-sources the chances that such a building wiII ac-tually be retrofit range from good for a corpor-ate headquarters or office building owned by aninsurance company or pension fund to poor if itis owned by a smalI local partnership for taxshelter purposes.

The likelihood that a building will be retrofitdepends both on its type of owner and on theimportance of energy costs for the purpose theowner uses the building for. Table 27 illustratesin a schematic way the general prospects for ret-rofit for different combinations of buildings andowners. In general, the chances that a buildingwill be retrofit are less likely for multifamily thanfor commercial buildings, less likely for build-ings owned for investment than for buildings oc-cupied by their owners, and less likely for build-ings owned by individual owners or local part-nerships than for those owned by institutionalowners such as pension funds and insurancecompanies, or national partnership syndicates.

In fact real estate is not quite so simple astable 27. The rest of the chapter explains someof the complexity of investment for energy effi-ciency in buildings. To date little specific re-search work has been done on the subject of

99

100 ● Energy Efficiency of Buildings in Cities

Table 27.—Likelihood of Retrofit by Building Type and Owner Type

Decreasing likelihood

Multifamily Multifamilymaster- tenant-

Owner-occupants Office Hotel Retail metered metered

Decreasing Corporation . . . . . . . . . L L L x xLikelihood Individual . . . . . . . . . . . M M M M P

Condominium. . . . . . . . X x x M M

investor-owners

Decreasing Institutional (pension,insurance). . . . . . . . . L L L L M

Likelihood Developmentcompany . . . . . . . . . . M M P P u

National partnership . . M M M M PLocal partnership. . . . . P P P P uIndividual . . . . . . . . . . . P P u P u

L = Likely.M = Moderate.P = Possible.U = Unlikely.X = There are none or very few examples of such building types owned by these owners.

SOURCE: Office of Technology Assessment

the motivation to invest in energy efficiency perse although there is voluminous Iiterature on in-vestment i n real estate.1 The chapter relies heav-ily on work done for OTA by the Real Estate Re-search Corp. (RERC) a Chicago-based consult-ing firm specializing in the investment analysisof real estate and in appraisal.

RERC conducted a comprehensive literaturereview, and interviewed buildings owners i n fourcase study cities (Buffalo, N.Y., Des Moines,Iowa, Tampa, Fla., and San Antonio, Tex.) aswell as “national” real estate owners withholdings in all parts of the country. RERC alsoanalyzed prototype multifamily buildings toevaluate the impact of rising energy costs andenergy retrofits financed in several alternativeways. In total, RERC talked to 96 buildingowners representing different types of ownersand different building uses. (The breakdown ofinterviews is shown in tables 28 and 29. ) These

1 Several other useful sources on real estate decisions and energyconservation include: Hittman Associates, PhysIca/ Charac (er-IstIcs, Energy Consumption and /7e/ated /nstI tut/oncJ Facfor$ fn theCornrnercla/ SeC tor, DC)E report, February 1977; Proceedlng~ oithe Mu/tl/am//} and Rental Housing Work$hop, Dec. 4, 5, and 6,1980, Washington, D. C., sponsored by the Federation of Amer-ican Scientists Fund prepared by Deborah L. Blevis; Alice Levine,and Jonathan Raab, So/ar Energ}, Conwrvatlon and Renta/ Hous-ing, Solar Energy Research Institute, March 1981; Mu/t/-Faml/yEnergy Conwrvatlort: A Reader , Coa l i t i on o f Nor theas tMuniclpallties, July 1981.

interviews, supplemented by extensive readingin real estate trade literature, in-house RERC ex-pertise, and OTA staff research form the basisfor this chapter.

This chapter focuses on privately owned, ur-ban commercial, and multifamily buildings–of-fices, retail facilities, hotels, and small, medium,and large apartment houses—partly becausethese form the bulk of the urban building stockand partly because these have been woefullyneglected i n the literature on investment inenergy efficiency. The chapter does not specif-ically address the motivation for investment byowners of single-famiIy houses. This subject wasfully covered in the previous OTA study on Resi-dential Energy Conservation, and other litera-ture, 2 and is addressed to some extent in otherchapters of this report Chapter 5, Retrofit for theHousing Stock of the Urban Poor and Chapter 9,The Public Sector Role in Urban Building EnergyConservation. Under some conditions the moti-vation of single-family home owners parallelsthat of the owner-occupants of small multifam-ily buildings and this will be pointed out in thetext.

2A comprehensive analysls of the potential for energy conserva-tion in single-family houses are the final report and workingpapers of the Res/dentla/ Energ}’ Ef(Ic Ienc} Standards Study sub-mitted to Congress by the Department of Housing and Urban De-velopment In July 1980.

Ch. 4—Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 101

Table 28.—Types of Building Owners Intervieweda

Owner status Buffalo Des Moines Tampa San Antonio National

Individual . . . . . . . . . . . . . . . . 8 4 1 3 6Partnership , . . . . . . . . . . . . . 7 5 4 4 5Corporate . . . . . . . . . . . . . . . . 3 4 1 2 4Institutional . . . . . . . . . . . . . . 0 1 0 0 10Development company . . . . . 3 0 0 1 4Bank . . . . . . . . . . . . . . . . . . . . 4 2 4 3 —Condominium . . . ... , , . . . . 0 0 1 1 1

Total . . . . . . . . . . . . . . . . . . 25 16 11 14 30asom~ owners trrterV@W@ f-rad multiple ownership posltlons (e g., as Individual owners and members of partnerships)

Owners were tabulated on the basis of the!r prlnclpal ownership role

SOURCE Real Estate Research Corp

Table 29.—Building Types Covered in Building Owner Interviews

Building type Buffalo Des Moines Tampa San Antonio

Multifamily . . . . . . . . . . . . 10 9 3 7Retail. . . . . . . . . . . . . . . . . 2 3 3 2

Shopping centersDepartment storesRetail strip

Offices . . . . . . . . . . . . . . . 8 6 4 6Hotels . . . . . . . . . . . . . . . . 1 1 0 2

Total . . . . . . . . . . . . . . . 21 19 17 10

NOTE, The number of bulldlng types WIII not exactly correspond to the number of owner types due to multlple ownershtp andthe fact that banks were not Interviewed as owners In all cases

SOURCE, Real Estate Research Corp

The decision to make energy improvementsin response to rapidly rising energy costs isabove all a real estate investment decision. Likeother real estate decisions it is affected byoverall investment strategy, tax laws, market-ability of the property, lease terms, cost andavailability of financing, perception of risk, andmany other considerations for a particularbuilding. Furthermore, real estate is a complexand diverse industry. Markets vary sharply fromcity to city and even from neighborhood toneighborhood. ownership runs the full rangefrom the giant corporation that owns its own

headquarters building to the retired coupleholding onto their small three-story walkup astheir nest egg. The conditions under which realestate decisions are made can change drastical -Iy from year to year. The rapid increases in infla-tion and interest rates of the last few years havehad profound consequences for decisions madeby all kinds of real estate owners. (More recent-ly, the 1981 tax law has made sweeping changesin the importance of real estate as a tax shelterfor other income.) The chapter treats each ofthese influences on a building’s prospects forretrofit.

CONTEXT FOR BUILDING OWNER DECISIONMAKING IN 1980-81

Although the general goals of investment in work was done, had its particular features,real estate remain the same over years and dec- many of which continued into 1981.ades, the specific concerns of building ownersare significantly influenced by the structure of Energy is Now Important. First of all, aftercosts and opportunities in a particular place and many years of energy price increases, energytime. The year 1980, when most of the survey began to be, for many building owners, a seri-

102 ● Energy Efficiency of Buildings in Cities

ous concern in 1980. It was widely perceived,as reported to RERC, as having crossed athreshold of importance within the overallbalance of income and expense for particularbuildings. In its annual national survey Emerg-ing Trends in Real Estate 1981, RERC describedthis change in consciousness of energy bybuilding owners:3

In 1979, their attitude was that increased costswould simply be passed on to consumers; butthis year’s comments are less cavalier. Lendersare examining the energy efficiency of buildingsbeing purchased or developed; investors areconcerned about absolute operating costs, andnot just those they will pay themselves; and ten-ants are seriously evaluating energy costs whenconsidering space alternatives.

Although some of the building owners inter-viewed for OTA did not share this perception,most did and echoed the concern of the mana-ger of a downtown office tower in Buffalo:“That electric bill is incentive enough, believeme!”

For most categories of building operationsand businesses, the rapid increases in energyprices (described in ch. 2) have been faster thanincreases in other costs of doing business suchas labor or property taxes. For all except hotels(see table 30), the cost of energy was a far

3Real Estate Research Corp., “Emerging Trends in Real Estate:1981 ,“ Chicago, Ill., October 1981.

Table 30.—Energy’s Share of Operating Costs(in percent)

1970 1975 1979

Downtown office(1) . . . . . . . . . . 18.90% 19.1% 23.80/oCenter city hotel (2) . . . . . . . . . . NA 7.9 7.5Neighborhood shopping (3) . . . . 5.9 (1972) 4.2 9.1Elevator multifamily (4):

Heating fuel . . . . . . . . . . . . . . 5.5 NA 13.4Electricity . . . . . . . . . . . . . . . . 6.9 NA 13.8Gas . . . . . . . . . . . . . . . . . . . . 1.3 NA 2.7

Low-rise (12-24 units) (4):Heating fuel . . . . . . . . . . . . . . 13.1 NA 18.9Electricity . . . . . . . . . . . . . . . . 2.8 NA 8.9Gas . . . . . . . . . . . . . . . . . . . . . 1.3 NA 2.7

NA = Not available.

SOURCES: 1980, 1976, 1971, Downtown Office Experience Exchange Report,Building Owners and Managers Association (BOMA), Washington,DC.; Laventhol and Horwath, U.S. Lodging Industry, 1976, 1979,1980 reports; Dollars and Cents of Shopping Centers, 1972, 1975,1978 ULI — The Urban Land Institute, Washington, D. C.; /n-corne/Expense Ana/ysis: Apartments, Institute of Real Esta teManagement (19S0 and 1975 editions). All figures are nationalaverages.

greater share of costs in 1979 than it was in theearly 1970’s. (Vigorous conservation by hotelsappears to be responsible for holding theenergy share down. ) Further rapid increases inenergy prices since 1979, especially in heatingoil, help account for the obvious concern aboutenergy which was evident i n the interviews withbuilding owners in late 1980.

The energy retrofit business scarcely existeda few years ago, and is still in the process of get-ting organized in response to the increasing in-terest in controlling energy costs. A few long-established companies offer specialized energyretrofits such as energy control systems. Manyother companies already expert in the installa-tion and maintenance of heating, ventilating,and air-conditioning systems are acquiring ex-perience and are recommending and installingenergy retrofit measures. There are still only afew general retrofit companies that have bothexperience with mechanical systems and expe-rience with such envelope retrofits as doubleglazing, blockage of air infiltration or insulation.The current embryonic state of the private mar-ket ability to prescribe and install retrofits is de-scribed in more detail in chapters 3 and 7.Nonetheless, observers of this process believethat it will take a few more years for enoughbusinesses to acquire solid reputations in thisfield, so that the building owners’ interest that isnow manifest will be matched by a privatemarket response.

The current state of knowledge about thedemonstrated effects of retrofit on energy use isas embryonic as the energy retrofit business. Al-though proprietary information is now beingdeveloped on retrofit results for such businessesas restaurant chains and department stores,there is still very little published information, ina few years there should be more publicly avail-able information on actual retrofits from sur-veys, from demonstration projects and fromsuch programs as the federally funded programto retrofit schools and hopitals. Improvedknowledge of retrofit results, coupled withlonger track records of the now-forming energyretrofit companies will reduce the element ofuncertainty that still looms large in any decisionto invest in building energy efficiency.

Ch. 4—Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 103

Leasing Trends. Offsetting increasing ownerconcern with energy costs, is an increasingtendency for leases to be written so as to pass allor most energy costs to the tenants. The differ-ent types of leases and their implications forenergy use are described below in sections oneach building type. In multifamily buildingsowners are converting master-metered build-ings to tenant metering if technically feasibleand introducing prorata billing systems forenergy costs when it is not technically feasible.In office buildings new leases are written withpassthrough clauses in a variety of forms. In thelast decade, retail buildings (especially shop-ping centers) have almost entirely convertedfrom gross to net leases in which not onlyenergy costs, but maintenance and cleaningcosts, taxes, and a prorata share of the commonspace are passed on to tenants.

Net leases, and passthrough leases encouragetenant responsibility for sensible use of energyin their rented space. Although little has beendocumented of the impact of these types ofleases on energy use in commercial space, one

estimate of the energy savings from tenant me-tering in multifamily buildings is 5 percent forheating costs (more for electric heat, less for gas)and 20 percent for other energy costs,4 How-ever, for those buildings for which substantialinvestments in energy retrofits such as newlighting systems or more efficient central boilerswould increase their energy efficiency, the prev-alence of net and passthrough leases clearly re-duces the immediate incentive of the owner toinvest.

Over the longer term the owner of a buildingwith net leases may still invest in its energy effi-ciency but will take into account the competi-tive importance of an energy efficient buildingto his tenants in the overall market that theyoperate in. The variations among office, hotel,retail, and multifamily tenants in their concernsabout the energy efficiency of their buildingswill be described below.

4Lou McLelland, “Encouraging Energy Conservation in Multi-Family Housing: RUBS and Other Methods of Allocating EnergyCosts to Residents, ” Executive Summary, 1980, Institute ofBehavioral Science, University of Colorado, p. 8.

4 ~

2 “ .’.

!.I I I I t I I I 1 -

1970 1972 1974 1976 1977 1978 1979 1980 1981(Mar.)

Year

SOURCE : Federal Reserve Board; Department of Energy, Energy Information Administration, Annua/ Repel1980, p 119, Morrthly Energy Review, August 1981, p. 16.

‘t to Congress,

104 ● Energy Efficiency of Buildings in Cities

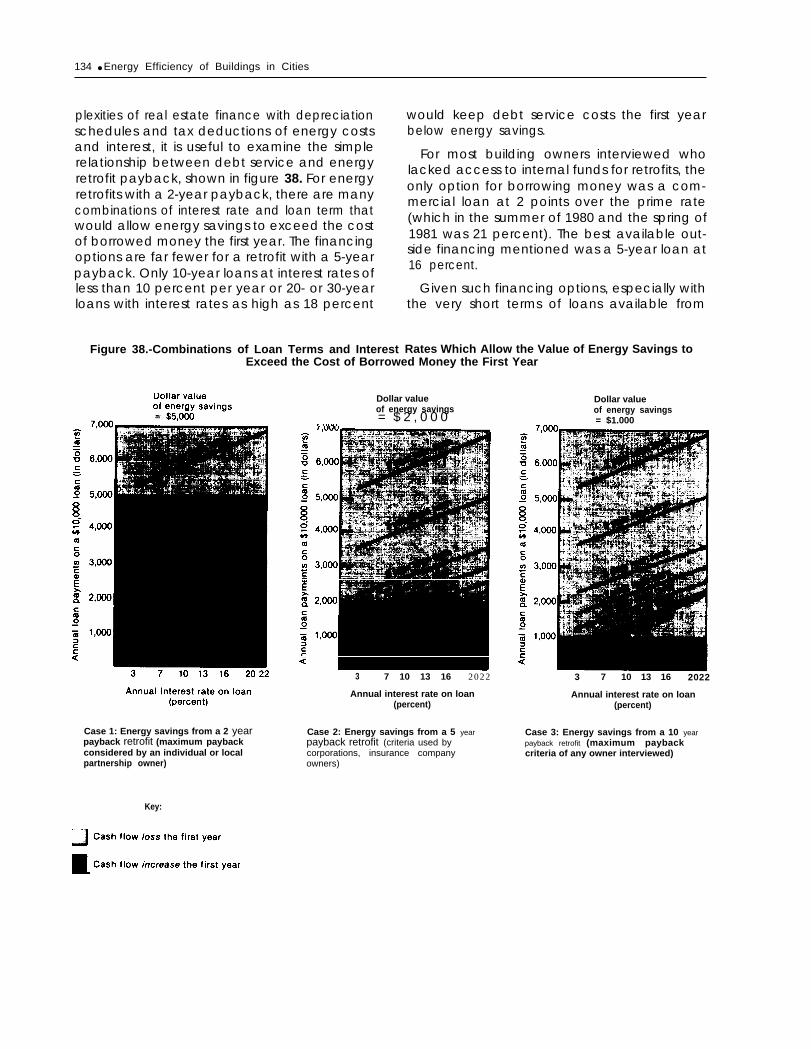

Costs of Financing. Energy isn’t the only costof doing business that has increased in the pastfew years. Since 1977, the cost of financing–forbuildings, equipment, inventories, and energyretrofits—has increased just as fast. Since 1970(as can be seen in fig. 34), the prime rate is seento increase as fast as the price of natural gas.Most energy retrofits substitute capital forenergy. The high cost of financing has been aserious disincentive to retrofits.

Traditionally, major building improvementsincluding energy retrofits were financed by refi-nancing (remortgaging) the entire building, Al-ternatively, second mortgages might be used atpremium, but not prohibitive, rates. In the cur-rent climate neither is practical. Refinancing afixed rate mortgage issued 5 years ago at 9 per-cent with a note of 14 to 17 percent or higher isneither sensible nor affordable. Furthermore, inresponse to persistent high inflation, most finan-cial institutions are moving away from fixedrate, long-term mortgage loans, which in late1980 were virtually unavailable. Instead theyare developing 5-year renegotiable mortgages,variable rate financing methods and equity par-ticipation. As a banker interviewed in Tampaput it: “This last round of madness in moneymarkets has destroyed the conventional meansof financing income property. Now they say‘give me a piece of it’. ”

Some shorter term alternatives to refinancingand second mortgages for buiIding improve-ments—such as commercial bank loans, lines ofcredit, signature loans or borrowing against per-sonal assets—are generalIy avaiIable at the sameinterest rate as construction loans, floating 2points over prime (21 percent in both the sum-mer of 1980 and spring of 1981). To be sure,banks may lend below prime to preferred cus-tomers but these generally must maintain largedeposits in exchange for prefered treatment onloans. At such high financing rates, virtually allbuilding owners will postpone building im-provements including energy retrofits unlessthey can be financed internally (see the later dis-cussion of the availability of internal funds).

Overall Context. To sum up, the year 1980-81finds several contradictory influences on thelikelihood of energy retrofit investment inbuildings. Building owners’ newly recognizedconcerns about energy costs, the gradual im-provement in the organization of the energy ret-rofit business, and the knowledge of the impactof energy retrofit all tend to increase the amountof retrofit that is likely to occur. Strongly offset-ting these influences, however, is the growingtendency toward net and passthrough leasesand the very high cost of financing.

WHO OWNS WHAT?

The prospects for energy retrofit to a parti-cular building depend on both what a buildingis used for and who owns it. Although all kindsof buildings, large and small, commercial andresidential, are owned by individuals or localpartnerships, other organizations active in realestate, such as insurance companies or nationalpartnership syndicates, tend to specialize inonly a few building types, Before proceeding toa discussion of the impact of owner types, orbuilding types on retrofit, it is important toknow who owns what.

ture and the expertise of real estate analysts andoperators. There is virtually no detailed data onownership. In some States such as Il l inois,moreover, ownership is hidden by various de-vices permissible under State law. I n only a fewcities for a few particular markets, office build-ings, multifamily, etc., have there been surveysof types of owners.

The consensus of conventional wisdom inreal estate on who owns what is shown in table31. Small buildings are usually owned by indi-viduals and partnerships, and small business

Most of what is known about ownership of corporations. Large buildings may be owned bybuildings is known from real estate trade litera- individuals and partnerships as well, but may

Ch. 4—Will Building Owners Invest in the Energy Efficiency of City Buildings? Ž 105

Table 31.— Ownership Types Believed To Be Most Characteristic of Various Building Types

Owner-occupants Investor-owners

indivi-dual or National Develop- Local

Corpo- small Condo- lnstitu- partner- ment partner-ration business minium tional ship company ship Individual

Small buildings:Multifamily

(2-9 units). . . . . . . . . . . . . . . x x xOffice buildings . . . . . . . . . . . x x xRetail strip stores . . . . . . . . . x x x

Large buildings:Multifamily (more

than 10 units. . . . . . . . . . . . x x x x xOffice buildings . . . . . . . . . . . X x x x x xShopping centers. . . . . . . . . . x x x xDepartment stores. . . . . . . . . X xHotels . . . . . . . . . . . . . . . . . . . x x x x

SOURCE” Off Ice of Technology Assessment

also be owned by insurance companies, pen-sion funds, major corporations, national part-nership syndicates, or development companies.

Partnerships are believed to be the most com-mon form of real estate ownership, because ofthe real estate tax advantages a partnership hasover a corporation. in a survey of office build-ings in the city of Atlanta (table 32), partnershipsand corporations were not distinguished. If,however, partnerships were the bulk of theowners, as predicted by conventional wisdom,then they accounted for more than half of all of-fice buildings in the city.

Table 32.—Ownership of Office Buildings—Atlanta, 1974

Number ofType of ownership buildings

Corporations and partnerships. . . . . . . . 216Savings and loans . . . . . . . . . . . . . . . . . . 19Banks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17Individuals. . . . . . . . . . . . . . . . . . . . . . . . . 50Labor unions . . . . . . . . . . . . . . . . . . . . . . 3Real estate companies . . . . . . . . . . . . . . 13Insurance . . . . . . . . . . . . . . . . . . . . . . . .... . 26Real estate investment trusts . . . . . . . . . 3Nonprofit organizations . . . . . . . . . . . . . 8Uncertifiable . . . . . . . . . . . . . . . . . . . . . . . 8

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . 363

NOTE Survey Included urban structures of at least 10,000 ft’ and suburbanstructures of at least 30,000 ftz, all wlthl n the vlclnlty I Imlts

S O U R C E Cornrnercia/ Space POIICY Ana/ys/s of Profltablllty of Retrofit ofEnergy Consewat/err, Metro Study Corp , Washington, D C , June1976

Although local partnerships are still the domi-nant form of partnership in real estate, nationalsyndicates of partnerships (such as JMB, RobertMacNeil, and Balcor) have become increasinglyimportant in the last half decade. They are listedwith the Securities and Exchange Commissionand their sales are handled by such brokeragefirms as Merrill Lynch and E. F. Hutton. Nationalsyndicates select their investments with an eyeto future appreciation. A few (such as RobertMacNeil) specialize in multifamily properties;others favor the generally higher returns fromowning and leasing office buildings, shoppingcenters, and hotels.

Development companies, when they own realestate as welI as buiId and develop it, also preferoffice buildings, shopping centers, and hotelsand tend to avoid the smaller returns of smallercommercial buildings and multifamily build-ings. So do the increasingly important institu-tional investors such as insurance companies,and pension funds. These latter have traditional-ly provided the permanent financing for largermultifamily and commercial buildings, general-ly through the brokerage of a mortgage bank(see box C). Increasingly, however, these insti-tutions are becoming more active in the equityownership of buildings themselves. For pensionfunds, recent changes in the Employment Re-tirement and Security Act (ERISA) have per-mitted a more aggressive direct role in real

[, -1, , . —.

106 . Energy Efficiency of Buildings in Cities

estate. As of 1979, the eight biggest life insur-ance companies had about $3.8 billion in realestate purchases, joint ventures and incomeproperty construction, out of total assets of $215b i l l ion inc lud ing about $64 b i l l ion inmortgages. 5 Institutions are a small but increas-ing share of building owners.

Corporations tend to own buildings for theirown use partly because corporate tax laws dis-courage the use of building losses to shelterother income (see box D). They commonly ownoffice buildings, hotels, and department stores,more rarely shopping centers and almost neverapartment buildings.

As a group, the owner s o f m u l t i f a m i l y

buildings are the smallest and least organized ofall owners. About 2.7 million owners occupyone or more apartments of multifamily buildingthey own.6 The Urban Institute found in a 1976— — - —

sCrittenden Financing, Inc., 1980.‘W .S. Bureau of the Census, General Housing Character/st/cs,

U.S. and Regions 1977, 1978.

Ch. 4— Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 107

study of Boston that 60 to 70 percent of themultifamily buildings were owned by individualswho owned less than 30 units. Only 10 to 15percent held buildings with 150 units or more.These findings are consistent with findings fromBaltimore and Newark.7

Condominium ownership of multifamily unitshas not yet made a large dent in the overallrental market but has become significant in afew cities where escalating property values en-courage conversion. According to a 1979 De-partment of Housing and Urban Development(HUD) study, only 1.3 percent of all rental unitshad been converted to condominiums from1970-79. In Washington, D. C., however, 6.8percent had been converted and in Denver andBoulder, Colo., 8.8 percent. In such cities asNew York where cooperative apartments aretraditional, there was a large number of conver-sions to cooperatives, rather than to condomin-iums. 8

— -—-—7La rry oza nrw ancj Ray Struyk, / Iouvng From tlw ExI}tf ng S[CJC k,

The Urban In$tltute, 1976, pp. 107-108. The Information was ob-tained by Struyk from interviews with large property managers InBoston. Results from Newark are reported in George Sternlleb,The Tenement Landlord, Rutgers University Press, 1966, and re-su Its from Baltl more are reported i n Michael Stegman, / I(juv ng /n-~e~tmwrt In the Inner CJ(Y, MIT Press, 1972.

‘Department of H OUSI ng and Urban Development, ThLI (-cm \er-von ()( Rt’n tal I Iou \f ng (() (-ondoml nl urn$ and (’o(~pefa [ I Ie$ A INa -[l~mal Stud} c)t 5( [Jpe, ( auwj and /mpac (, 1980.

Many commercial buildings are small and oc-cupied by their small business owners, who maybe individuals, partners, or small corporations.Based on information in a recently publishedEnergy Information Administration survey ofcommercial buildings, as many as 60 percent ofthe smallest buildings of up to 5,000 ft2 are likelyto be occupied by their owners.9

The structure of ownership is significant forthe prospects for energy retrofit. In general, as isexplained in the next section, the largest, mostfinancially independent and best advised own-ers (corporations, national partnership syndi-cates, development companies, insurance com-panies, and pension funds) tend to own thelarge commercial buildings. The smaller andleast organized owners tend to own multifamilybuildings.

9E nergy I nformat ion Ad ml nl str~tl on, Non -Re\Id(m tJa I BUI ld~ ngjEnerg}’ Con~umptl(m Sunm, 1981, table 23 B. It is harder to beprecise about larger buildings because EIA asked tt hulldlng~ wereoccupied by the owner or his agent. SI nce larger bu I Id I ng~ may beoccu pled by a manager agent of the owner, they are not tru Iyowner-occupied

IMPACT OF OWNERSHIP ON BUILDING RETROFIT

Among the types of owners interviewed, what they said about their motivation and re-there were striking differences in the extent to sources to carry out a retrofit.which they had made major energy investmentsin some or all of their buildings, minor energy The retrofit experience of the owners inter-investments (including significant operational viewed is shown in figure 35. The top levelimprovements), or, no energy investments or shows the “national ” owners with holdingsoperational changes at all. The survey of build- across the country; the bottom level shows theing owners was not constructed to be a statis- owners interviewed i n the four case study cities.tically valid sample of building owners and for The differences among types of owners is strik-this reason only tentative and suggestive conclu- ing. Out of 22 interviewed, only one individualsions can be drawn from the results; nonethe- owner, of any kind, had made a major energyless the pattern of retrofits reported by the differ- investment, although 8 had made minor invest-ent types of building owners is consistent with ments. On the other hand, 10 “national” insti-

108 ● Energy Efficiency of Buildings in Cities

Figure 35.— Frequency of Major and Minor Energy RetrofitAmong Building Owners Interviewed

9

8

7

6

5 E

1---Individualowners

12

11 - —10 —

9 —

8 -

7 -

6 -

5 -

4 -

3 -

2 -

1

NOTE: Minor energvestments, ”

SOURCE: Real Estat

Interviews

kPartner-ships

ith large owners with nationwide

I Buffalo, Des I

h

Institutionalowners

Moines, Tampa,

Condominiums

None

investments cost little enough that they could be handled as “expenses” and not “capital in-

Research lnterwews for OTA

tutional owners interviewed had made major ations interviewed, none had made major ener-energy investments in their buildings. Nationalpartnership syndicates, national corporations,and development companies all had eithermade major or at least minor energy invest-ments.

Significant numbers of the local individualowners and local partnerships had done noth-ing to their buildings in response to increasingenergy prices. Of the four condominium associ-

gy investments.

The results of the interviews cannot be com-pared with any statistically valid survey data be-cause none has been conducted by owner type.The. interviews did make clear, however, thethinking that goes into a building owner’s deci-sion to retrofit or not retrofit and why it is likelyto be different for different types of owners. Therest of this section explains how owners differ i n

Ch. 4— Will Building Owners Invest in the Energy Efficiency of City Buildings? Ž 109

the motivation to make energy investments intheir buildings, and, equally important, in the fi-nancial and managerial resources they can callupon to make an investment.

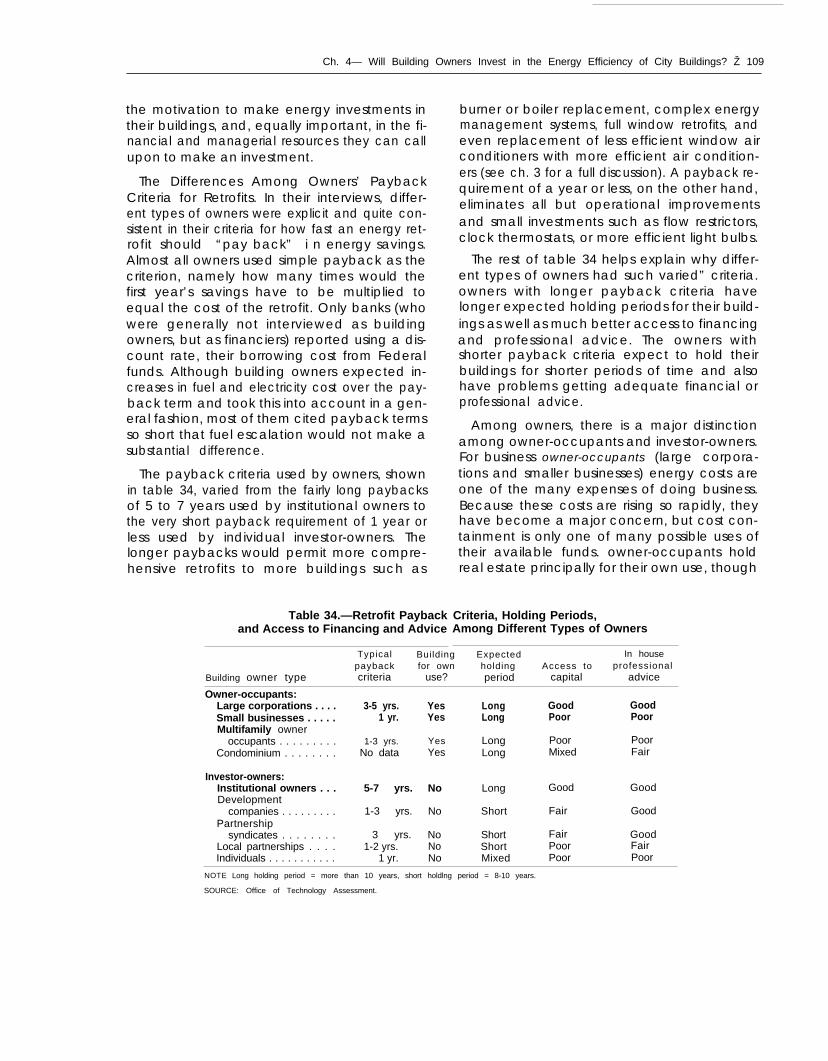

The Differences Among Owners’ PaybackCriteria for Retrofits. In their interviews, differ-ent types of owners were explicit and quite con-sistent in their criteria for how fast an energy ret-rofit should “pay back” i n energy savings.Almost all owners used simple payback as thecriterion, namely how many times would thefirst year’s savings have to be multiplied toequal the cost of the retrofit. Only banks (whowere generally not interviewed as buildingowners, but as financiers) reported using a dis-count rate, their borrowing cost from Federalfunds. Although building owners expected in-creases in fuel and electricity cost over the pay-back term and took this into account in a gen-eral fashion, most of them cited payback termsso short that fuel escalation would not make asubstantial difference.

The payback criteria used by owners, shownin table 34, varied from the fairly long paybacksof 5 to 7 years used by institutional owners tothe very short payback requirement of 1 year orless used by individual investor-owners. Thelonger paybacks would permit more compre-hensive retrofits to more buildings such as

Table 34.—Retrofit Paybackand Access to Financing and Advice

burner or boiler replacement, complex energymanagement systems, full window retrofits, andeven replacement of less efficient window airconditioners with more efficient air condition-ers (see ch. 3 for a full discussion). A payback re-quirement of a year or less, on the other hand,eliminates all but operational improvementsand small investments such as flow restrictors,clock thermostats, or more efficient light bulbs.

The rest of table 34 helps explain why differ-ent types of owners had such varied” criteria.owners with longer payback criteria havelonger expected holding periods for their build-ings as well as much better access to financingand professional advice. The owners withshorter payback criteria expect to hold theirbuildings for shorter periods of time and alsohave problems getting adequate financial orprofessional advice.

Among owners, there is a major distinctionamong owner-occupants and investor-owners.For business owner-occupants (large corpora-tions and smaller businesses) energy costs areone of the many expenses of doing business.Because these costs are rising so rapidly, theyhave become a major concern, but cost con-tainment is only one of many possible uses oftheir available funds. owner-occupants holdreal estate principally for their own use, though

Criteria, Holding Periods,Among Different Types of Owners

Typical Building Expected In housepayback for own holding Access to professional

Building owner type criteria use? period capital advice

Owner-occupants:Large corporations . . . . 3-5 yrs. Yes Long Good GoodSmall businesses . . . . . 1 yr. Yes Long Poor PoorMultifamily owner

occupants . . . . . . . . . 1-3 yrs. Yes Long Poor PoorCondominium . . . . . . . . No data Yes Long Mixed Fair

Investor-owners:Institutional owners . . . 5-7 yrs. No Long Good GoodDevelopment

companies . . . . . . . . . 1-3 yrs. No Short Fair GoodPartnership

syndicates . . . . . . . . 3 yrs. No Short Fair GoodLocal partnerships . . . . 1-2 yrs. No Short Poor FairIndividuals . . . . . . . . . . . 1 yr. No Mixed Poor Poor

NOTE Long holding period = more than 10 years, short holdlng period = 8-10 years.

SOURCE: Office of Technology Assessment.

110 Ž Energy Efficiency of Buildings in Cities

tax benefits may be enjoyed and appreciation inreal estate value hoped for. Residential owner-occupants who live in one unit of a small apart-ment building and condominium owners donot use their real estate to conduct a businessbut share with business owner-occupants thepoint of view that the primary purpose of thebuilding is for their own use and real estatereturn is secondary. Investor-owners, on theother hand, are not interested in buildings fortheir usefulness as buildings but for the manyforms of economic return they may obtain fromholding them. The rest of this section describesthe motivation for energy retrofit of each of theowner-occupants and investor-owners includedin table 34.

Large Corporate Owner Occupants. Largecorporations almost always occupy any build-ings that they own. Corporations are inhibitedfrom owning real estate for investment purposesby aspects of corporate tax status that reducethe return to corporations from real estate be-low what is available to individuals and partner-ships (see box D). Thus, the chief economicbenefit of corporate buildings is their efficiency

as business facilities and, in some cases, theextent to which they enhance the corporateimage.

Corporate owners of their own office facilitiesor downtown retail stores or hotels reported ininterviews that they base energy improvementdecisions on expected business return not onreal estate return. If energy-efficiency results inlower business operating expenses, greater em-ployee productivity, enhanced attractiveness topatrons or better business image, improvementsare likely to be considered in competition withalternative corporate investments in marketing,expansion or inventory control. The dilemma ofchoices among business investments was wellexpressed by the president of a departmentstore in Buffalo: “we make energy improve-ments to help control our operating costs, butthere’s a limit. Remember capital for energy im-provements does not increase sales.” At thesame time, for owner-occupants, there is noway to escape the burden of energy costs whichinvestor-owners can duck with passthroughleases. The president of a national motel chainin San Antonio said he expected to see energy

Photo credit: Steve Friedman

Energy efficient features of this building in Tampa, owned by a corporation,include double glazing, and controls on outside air mixing

Ch. 4—Will Building Owners invest in the Energy Efficiency of City Buildings? Ž 111

costs exceed mortgage costs i n the near future,“1 increase my return by controlling mycosts—now, not later. ”

Large corporations have good access to cap-ital for energy improvements. Most moderate tolarge-sized corporations have formal capitalbudgeting procedures and routinely make cap-ital investments drawing on financing from a va-riety of sources: retained earnings, corporatedebt issues, lines of credit, and commercialloans. Of the five local and three national cor-porate owners interviewed, who had made ma-jor retrofit investments, all had been financedwith internal funds.

Large corporate owners also have good ac-cess to professional advice. They have profes-sional faciIity managers as part of corporateheadquarters staff. They often can afford toemploy internal experts in energy conservationor can retain consultants. The basic corporateplanning cycle encourages explicit considera-tion of energy investments.

The corporate owners interviewed all men-tioned 3- to 5-year paybacks as the criteria theyapply to energy investments. In contrast tomany types of investor-owners this period is notrelated to their holding period for the buildingbut rather to a corporatewide business standardof return for nonmanufacturing facility invest-ments. Unlike smaller owners, corporationshave both financial and professional resourcesto make energy investments based on these cri-teria.

Small Business Owner-Occupants. Smallbusinesses may be individual proprietorships,partnerships, or small corporations. Like largecorporations, they own the buildings to use intheir businesses. Said a San Antonio shoppingcenter owner of the typical small shoestore“they’re in business to sell first and in times likethis, it’s tough to do everything you might likeor should do. ”

Information on the motivation of small busi-nesses is scanty. A few interviews were con-ducted directly with small business owners,mostly individual proprietorships. Further in-sight was provided by several brokers of smallbusiness properties.

Compared to large corporate owners of theirbuildings, small businesses have much less ac-cess to internal funding for energy improve-ments and usually limited access to outside cap-ital at reasonable rates. Such owners are partic-ularly dependent on maintaining reasonablecash flow from their businesses. Energy invest-ments with high initial costs and burdensomedebt service due to high interest rates, shortloan terms, or both (see discussion in the lastsection of this chapter) are serious obstacles toenergy conservation investments.

Small business owners also lack the time andfinancial resources to obtain good professionaladvice about energy investments. Because oftheir dependence on adequate cash flow therisks of a mistake are also much greater than forthe large corporation. For all these reasons,small business, especially individual proprie-tors, appear to limit energy investments to thosethat will pay back in 1 year or less.

Owner-Occupants of Multifamily Buildings.This category of owner is very similar to thesmall business owner, lacking time or profes-sional advice to learn about energy improve-ments and lacking sufficient cash flow to fundenergy investments from internally generatedfunds but with very limited access to outside fi-nancing at reasonable interest rates. However,because these owners also live in their buildingand pay some of its energy costs as part of theirown household expenses, there is a slightlygreater chance that they will consider retrofitswith paybacks of up to 3 years. Of the very smallnumber of multifamily buildings reported as ret-rofitted in the building owner survey, two wereowner-occupied small buildings in Buffalo.

Condominium-Owners. Owners of condo-minium apartments are responsible for energyimprovements to their own units, but the im-provements to the buildingwide systems are theresponsibility of the condominium association.Condominium association fees have been risingat rapid rates and condominium trade associa-tions have recognized the importance of risingenergy costs.

Nonetheless, for a systemwide energy im-provement to be made, the condominium asso-

112 . Energy Efficiency of Buildings in Cities

ciation, in a collective process, must agree onthe improvement’s value and pay for it fromreplacement reserves, debt finance, or a pro-portionate assessment to each owner. The four’condominium associations interviewed re-ported mixed experience with lenders. Collat-eral is a problem for some because the condo-minium association does not hold title to thebuilding. For some associations their authorityto levy special assessments on owners has beensufficient to obtain loans. None of the four asso-ciations interviewed had made a major retrofitinvestment but two had made minor invest-ments. In general, condominium owners ap-pear motivated to consider energy retrofits butare handicapped by the awkwardness of theirform of ownership from making commitmentsto longer payback investments.

Investor-Owners: General. Investor-ownersown buildings only for the economic returnthey bring as real estate. Investor-ownersneither live in their buildings nor do they usethem primarily to house their businesses, al-though for convenience they are likely to havetheir own offices in one of the buildings theyown. For an investor-owner an investment inthe energy efficiency of the building must con-tribute to one or more of the three forms of eco-nomic return in real estate:

●

●

●

Cash flow. Energy retrofits may decreaseexpenses in buildings where the ownerpays all or part of the energy expenses. Forbuildings with net or passthrough leases,energy retrofits only increase cash flow ifthey allow higher rents to be charged or re-duce vacancies.Tax benefits. Many energy retrofits can bedepreciated and used to shelter taxable in-come. Interest on loans to pay for energyretrofits can also be deducted from taxableincome. Tax credits from Federal or Stategovernments may also be available to own-ers for specific energy investments.Resale value. An energy retrofit that in-creases a building’s net income will have adirect effect on its resale value as the net in-come is capitalized by appraisers at somerate typical for that type of building andlocation (see Box E.–As the Appraiser Sees

It). Appraisers usually use 3 years averagenet income to make this determination. Arecent energy retrofit without 3 years’ im-pact on net income may not have much im-pact on resale value.

The main types of investor-owners—insti-tutional, development company, partnership,and individual—emphasize different elementsof the return on real estate and thus havedistinctly different motivation for energy retrofitto their buildings. The building owner types alsodiffer in the financial and professional resourcesthey can bring to bear on energy investments.

Institutional Owners. Insurance companiesand pension funds are the major form of institu-tional owners. Typically they hold buildings forholding periods of 12 years or more, emphasiz-ing the healthy cash flow in the buildings overthe long term. For this reason, energy retrofitwhich promises to increase cash flow over thelong run is viewed as sensible. Such ownershave the longest payback criteria of all owners,5 to 7 years.

Insurance companies and pension funds haveextensive financial capacity to fund building im-provements internally. They also support a pro-fessional management and property investmentstaff to recommend and carry out investmentand management practices to increase incomefrom a property and improve its long-termvalue. Property managers (see Box F: The Roleof the Property Manager) and in-house propertyplanning staff for institutional owners haveclearly defined job performance objectives, in-centives, and capital budgets. Cost conscious-ness is rewarded. operational improvements tosave energy have been a property managementtask since 1975 and annual energy audits andbuilding energy system inventories a regularroutine, All 10 national institutional owners in-terviewed had made major capital investmentsin their buildings including full replacement ofboilers and air conditioning systems and in-stallation of sophisticated computerized energytiming and control systems.

Development Companies. The four nationaland four local development companies inter-viewed varied in their expected holding periods

Ch. 4—Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 113—————. . — .

Box E.-A Question of Value: How the Appraiser Sees it

Do energy improvements enhance a property’s value? To appraisers, the answer is not atall clear. But what is clear is the importance of their response to this question in a go/no-goretrofit investment decision. The appraiser’s consideration of the impact of energy improve-ments on value can be crucial to some lending decisions if loan-to-value ratios are close to ac-cepted limits and can also be important to the return assessment of owners if the improvementis capitalized into the value of the building.

Professional appraisers should, in theory, consider the improvement to value that resultsfrom a reduction in energy costs. In income properties, this would occur through the capital-ization of the resulting higher net income. The appraiser normally does this by examining 3years’ operating results on the building understudy and operating results of comparable build-ings to arrive at stabilized income and expense data. Comparability of energy equipmentamong other things should be considered in selecting buildings for comparison.

At present, several factors make it difficult for appraisers to conform to this procedure.Few buildings exist with 3 years of results of energy improvements, either to use as com-parable, or to appraise. Hence, there is little experience to use in judging indirect or directimpact on market value. As yet, no other standardized methods for incorporating energy con-cerns have been developed. The appraisal division of a commercial bank in San Antonio in-stituted Iifecycle costing as a nonstandard way to approach the issue and to serve as a proxyfor acceptable comparable.

In the face of limited information, many appraisers have responded to rapidly increasingenergy costs by, in effect, incorporating the increased risk in their valuation judgments. Thishas occurred by raising capitalization (which lowers the effective multiplier applied to incometo arrive at value). The higher rate reflects many factors, but the recent rates of inflation in in-terest rates, operating costs and energy prices are considered to be among the major factorsthat result in higher risks.

Efforts have been made by appraiser professional associations to improve their members’skills in evaluating energy conservation in real estate. In addition, many appraisers are activein local building owner and manager associations, which have become very concerned aboutenergy.

Box F.-Role of the Property Manager

Professional property managers play an im-portant role in building operations for manyowners, particularly institutions and partner-ships. Property managers have the discretionto identify and make operational energy im-provements, but only limited authority tomake capital improvements. For example, atone large office building in a case study city,the manager’s authority was limited to im-provements costing $5,000 or less.

Managers can, and often do, identify bothoperations and capital possibilities for reducingenergy costs. In some cases, such as hotels, thecompensation formula is based on net income,which actively encourages managers to seek

ways to cut costs. The presence of professionalmanagers has led to widespread adoption ofoperational improvements in larger officebuildings and to more active consideration ofenergy measures elsewhere. This is true re-gardless of who owns the property. In addi-tion, professional managers interviewed wereby far the most knowledgeable about energycosts and technical options. They felt that therewas a steep dropoff in awareness and knowl-edge among the less professional managersand owners who were not themselves activefull-time managers. There appears to be lessknowledge and less conservation where thereare no professional and/or full-time managers.

114 . Energy Efficiency of Buildings in Cities

for buildings but on the whole their holdingperiods were shorter than those of institutionalowners and their payback criteria for energyretrofits were correspondingly shorter (1 to 3years). Short payback criteria can be explainedpartly by the greater difficulty of developmentcompanies in financing retrofits. Their invest-ments have been traditionally highly leveragedwith a very high ratio of debt to equity (althoughthey are now moving more toward equity fi-nancing). This leaves very little flexibility to addfurther debt. Development companies havealso tended to specialize in owning shoppingcenters with fully indexed net leases, so that theincentive to retrofit is somewhat less than that ofowners of other commercial buildings (see dis-cussion of commercial buildings below). of theeight owners interviewed, four had made majorretrofits, two had made minor retrofits and twohad done nothing.

partnership: General. The popularity of thepartnership, now the most common form of realestate ownership, is in part due to the tax statusof this form of ownership and in part due to thesmall capital requirements for entry. The part-nership is itself not a taxable entity but a taxconduit which passes on the tax advantages ofreal estate ownership fully and directly to thepartner/investor. While partnerships are inter-ested in the cash flow and resale impact of anenergy retrofit, they are very concerned aboutleaving intact or enhancing the tax benefits of aproperty. Since partnerships are formed only forpurposes of owning a particular piece of proper-ty, it is often difficult for the partners to agree onfurther capital investment once the particulardeal has been struck. The tax benefits to a part-nership diminish after 7 to 10 years as interestand depreciation deductions diminish and atthis point, the property is frequently sold.

National partnership Syndicates. These arethe most sophisticated of the partnerships andbear some resemblance to the institutional own-ers. All syndicates have a general partner,responsible for managing the property held bythe syndicate, and many limited partners whobuy into the syndicate either privately or by pur-chasing publicly placed security investments.

National syndicates maintain professionalmanagement staffs in-house and onsite. As partof the syndication, reserves are set aside forbuilding expenses sufficient to fund most im-provements including moderate energy retrofitswithout returning to the investors for extra equi-ty capital. For these partnerships, energy orother building improvements are an aggressiveway to increase building value and create morereturn for investors than passive managementwould create. As the head of a national syn-dicate’s property management department ex-plained: “Any new value we create is a sellingpoint to our customers (investors), old or new.The sophisticated investors we deal with wantquality in their product not just shelter.”

Of the five national partnership syndicates in-terviewed, three had made major energy invest-ments in their buildings and the other two hadmade minor investments. The national syn-dicates agreed on a 3-year payback as a suitablecriteria for retrofit.

Local partnerships. Local partnerships maybe formed with a general partner and limitedpartners or with conventional (equal) partners.They almost always have far more limited finan-cial and managerial resources than the nationalpartnership syndicates. Reserves set aside at thetime of creation of these partnerships are gener-ally insufficient to cover major building im-provements such as energy. It is usually very dif-ficult to raise further equity capital from theoriginal partner investors. Said a San Antoniogeneral partner: “Thirteen can put the newmoney up but two others (partners) don’t havethe cash on hand; so I can’t do it; we are simplytalking group dynamics.”

Of the 20 local partnerships interviewed, onlyfour had made major energy investments, eighthad done nothing. One or two years was thestandard payback criteria for retrofits, cor-responding to the short (7 to 10 year) holdingperiod typical of partnerships. If they are doneat all, energy retrofits are done early in the prop-erty’s holding period. As the San Antonio gener-al partner explained, “After the sixth year, I’mlooking at another building purchase and syndi-cate setup, not the one I’m about to get out of. ”

Ch. 4—Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 115

Individual Investor-Owners. Most individualinvestor-owners, like individual owner-occu-pants, are owners of small amounts of propertyand this constrains their ability to make energyinvestments in their buildings. Because most in-dividual owners lack financial depth, maintain-ing a building's cash flow is usually far more im-portant than sacrificing current cash flow for thesake of future resale value. Many individualowners also lack sophisticated property invest-ment advice that would help them evaluate theresale potential of their property. A large Buffalobroker of small property observed:

Resale value is important but requires somesophistication to be appreciated. Your Momand Pop single investor or owner who thinks hissingle unit or two is going to support his retire-ment or give him financial security is not goingto think in terms of future value, It’s hard to getthem to think of real estate as an investment. . . the way an investor where real estate is his

living would; it is a thing to be kept and kept up,not improved for investment reasons,

With today’s high cost and inaccessibility ofdebt finance, the cash flow of an individual’sproperty is threatened by substantial energy in-vestments. Most of those individual owners in-terviewed set 1 year as their maximum energyretrofit criteria. This extremely short payback re-flected their uncertainty about the risks of anenergy investment and their fears of a mistake asmuch as insistence on a high rate of return. Afew individuals personally concerned aboutenergy efficiency accepted higher. paybacksthan this; one as long as 10 years.

Conclusion. In today’s climate of high cost offinance and continued uncertainty about therisks and benefits of energy retrofit, buildingowner types—institutional owners, corpora-tions, national partnership syndicates, and de-velopment companies—with good access to in-

Photo credit Steve Friedman

The individual who owns this office building in a Northern city has made low capital cost investmentsin calking and boiler efficiency. The owner is currently unable to finance a new boiler

116 ● Energy Efficiency of Buildings in Cities

ternal capital funds and professional informa-tion are far more likely to retrofit their buildingsthan owners—individual and local partnerships—who are constrained by their building’s cashflow from taking on the high debt service cost ofoutside finance and who have poor access to

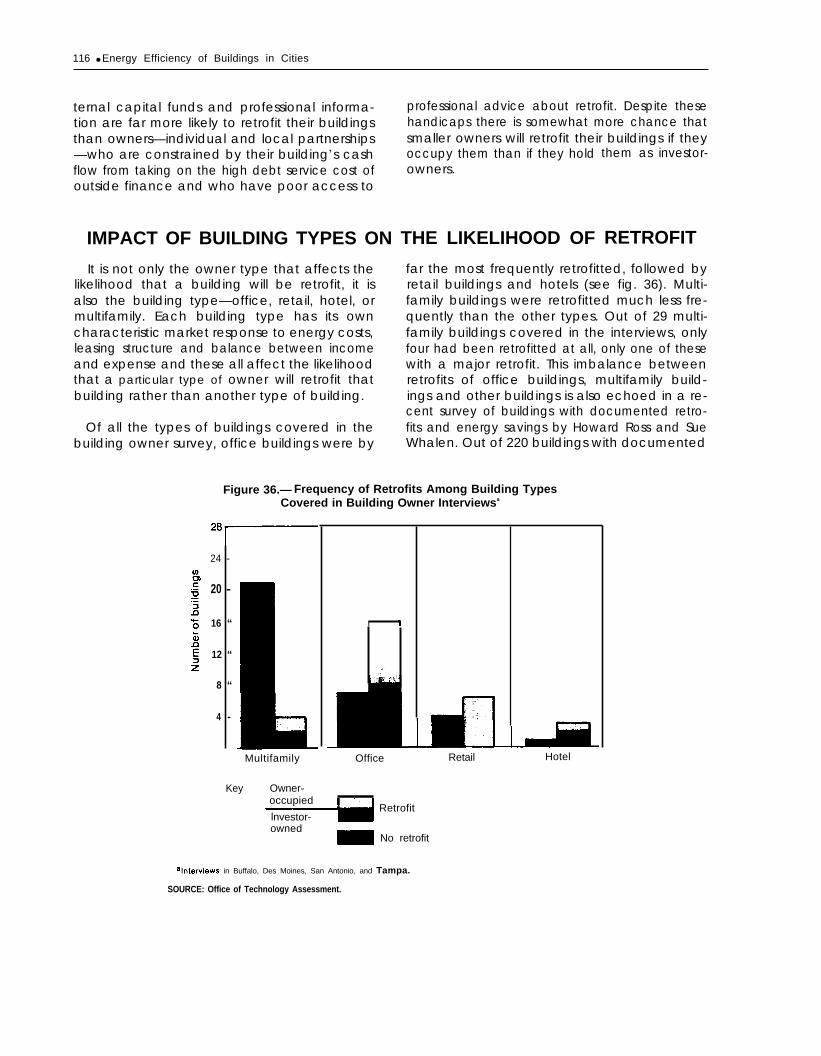

IMPACT OF BUILDING TYPES ON

It is not only the owner type that affects thelikelihood that a building will be retrofit, it isalso the building type—office, retail, hotel, ormultifamily. Each building type has its owncharacteristic market response to energy costs,leasing structure and balance between incomeand expense and these all affect the likelihoodthat a particular type of owner will retrofit thatbuilding rather than another type of building.

Of all the types of buildings covered in thebuilding owner survey, office buildings were by

professional advice about retrofit. Despite thesehandicaps there is somewhat more chance thatsmaller owners will retrofit their buildings if theyoccupy them than if they holdowners.

THE LIKELIHOOD OF

them as investor-

RETROFIT

far the most frequently retrofitted, followed byretail buildings and hotels (see fig. 36). Multi-family buildings were retrofitted much less fre-quently than the other types. Out of 29 multi-family buildings covered in the interviews, onlyfour had been retrofitted at all, only one of thesewith a major retrofit. This imbalance betweenretrofits of office buildings, multifamily build-ings and other buildings is also echoed in a re-cent survey of buildings with documented retro-fits and energy savings by Howard Ross and SueWhalen. Out of 220 buildings with documented

Figure 36.— Frequency of Retrofits Among Building TypesCovered in Building Owner Interviewsa

24 -

20 -

16 “

12 “

8 “

4 -

Multifamily

Key Owner-

r 1

“.

. .

Office Retail Hotel

occupiedRetrofit

lnvestor-owned

m No retrofit

I

alnterviews in Buffalo, Des Moines, San Antonio, and Tampa.

SOURCE: Office of Technology Assessment.

Ch. 4— Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 117

retrofits, 38 were office buildings, four were ers—individuals and local partnerships—whohotels, while there was only one shopping cen- require very short paybacks to make any retrofitter and one multifamily building.10 at all and who frequently do nothing to their

part of the explanation is that multifamily buildings in response to rising energy costs.

buildings tend to be owned by the types of own-However, the problem of retrofits to multifamilybuildings goes beyond ownership. The sections

10Howard ROSS and Sue Whalen, ‘‘Building Energy Use Com- that follow discuss the particular market charac-pilation and Analysis: Part C: Conservation Progress in Commer- teristics of multifamily and commercial build-cial Buildings” (unpublished), May 1981, revised August 1981. Tobe published in Energy and Buildings magazine, Lausanne, ings that affect their prospects for retrofit.Switzerland.

LIKELIHOOD OF RETROFIT IN MULTIFAMILY BUILDINGS

The problems of the owner types who ownthe bulk of multifamily buildings explain muchof their very low rate of retrofit. Individualowners lack access to capital and are con-strained by their dependence on the buildingscash flow from taking on high debt service topay for retrofit. Local partnerships may put capi-tal into retrofit at the time of purchase, but itbecomes increasingly difficult to obtain fundsfrom the partners after that. Both categories ofowners lack information on retrofit oppor-tunities and risk and both have much to losefrom a mistake. Multifamily buildings owned bybetter financed and informed owner types suchas insurance companies, pension funds, and na-tional partnership syndicates are somewhatmore likely to be retrofit than those owned byindividual owners and local partnerships.

The type of owner, however, does not explainall of the low rate of multifamily retrofit.Owners’ problems are exacerbated by overallproblems in the market for multifamily build-ings.

Squeeze on Cash Flow. More than owners ofother building types, multifamily buildingowners have been caught in an income squeezeboth because of rising costs and their inability toraise rents. The latter is attributable to severalfactors, including rent control, consumer re-sistance, and management efforts to minimizeturnover in tenancy. Using operating indexesfrom actual special samples of properties in onearea, a Rand Corp. study of multifamily units un-derlines the expense-revenue gap that emerged

in the 1970’s. “Generally, the evidence suggestsoperating cost increases of 8 to 10 percent an-nually, compounding to between 115 and 160percent for a decade in which rents rose by 74percent and vacancy rates (which also affectrevenue) changed only slightly.’” This trendleads to diminished rates of growth in net oper-ating income, and results both in relatively lessmoney available for debt service and in lowermarket values. In the face of recent increases inmortgage interest rates, this creates a cashsqueeze for any new owner or a relativediminution of value for a potential seller.

Energy cost increases have been a major con-tributor to this cash squeeze. As figure 37shows, increases in fuel and utility costs aloneoutpaced average rental adjustments by morethan 2 to 1 (98 to 39 percent) between 1970 and1976. The trend continued from 1976 to 1979,according to data from the Institute of RealEstate Management (I REM). Heating costs persquare foot increased over 3 years anywherefrom 62 percent for elevator apartments to 120percent for low-rise small buildings (see table35).

Average rental adjustments for multifamilybuildings have not kept pace with increases inenergy costs for reasons that elude the expertsalthough many explanations have been given.One is that traditional renters such as newly-

I I 1 ra s, Lowry, d ra f t rePort I “Rental Housing in the 1970’5:Sea rch ing for the Crlsls, ” the Rand Corp., No\fember 1980;presented at HUD Conference In Rental Housing, No\. 14, 1980.!5ee also Da\id Scott Lindsay and Ira S. Lowry, Rent lnflat~f)n In St.j(lwph Count}, Indiana, 1974-78, the Rand Corp., 1981.

118 ● Energy Efficiency of Buildings in Cities.

Figure 37.—Apartment Operating Revenues andExpenses 1970-76

II

z : “ - , ‘7

120.0

1970 1972 1974 1976

Year

NOTE: Data from 189 properties.

SOURCE: Touche Ross & Co. using data from Booz, Allen & Hamilton (May1 9 7 9 ) . Ach/evmg E n e r g y Corrservdtion In Ex/stlrrg ApartmentBuildings: Append\x D.

Table 35.—Annual Heating Fuel Costsin Apartment Buildings

Heating cost(dollars/ft 2 o f

rentablearea) Percent

Apartment building type 1976 1979 change

Elevator . . . . . . . . . . . . . . . . . . . . $0.21 $0.34 62%Low-rise (24 units +). . . . . . . . . . 0.14 0.23 64Low-rise (12 units). . . . . . . . . . . . 0.15 0.33 120Garden . . . . . . . . . . . . . . . . . . . . . 0.13 0.23 77

NOTE: Only buildings reported for 4 consecutive years,

SOURCE. /ncome Expense Ana/ysis. Apartments 1980 Editton, Institute of RealEstate Management.

weds, single households, and empty-nestors, inresponse to rapid appreciation in property val-ues and the tax-deductible status of mortgageinterest, have been shifting to single-family orcondominium ownership for investment as wellas housing, and are leaving the rental market toa larger proportion of lower income people,who are less able to adjust to increases in rent.There is also some evidence, however, that

lower income renters have increased the qualityof their housing over the decade without in-creasing their average rent. Finally, some of thelag in rents can be explained by a preference ofsome multifamily building owners to reducevacancy ratios and retain long-term tenants byholding back rent increases. Some observerspracticing strict market economics believe thatthe overall explanation for the possibility of alag in rents relative to expenses may be thatthere is an oversupply of multifamily houses.12

Careful studies have shown that this indeed maybe a cause of abandonment of multifamilyhouses in certain areas (see discussion in ch. 5).

The potential for rent adjustment to coverutility costs varies greatly from strong rentalhousing markets to weaker ones. Among thecase study cities, owners in Buffalo and DesMoines perceived the rental market to beweaker and the potential poor for raising rentssufficiently. Several owners expressed a strongsense of crisis in the interviews, foreseeing grimfutures as real estate apartment owners unlessthey “got out soon” at a decent sales price or byconverting to condominiums even when theyacknowledged that the market for condomini-ums was poor in their cities. Apartment ownersin the stronger markets of Tampa and San An-tonio were more optimistic. Even in thesemarkets, however, institutional owners and na-tional syndicates expressed an intention toreduce the amount of investment in multifamilyproperty.

Most important of all, an apartment owner’sability to avoid the squeeze on cash flowdescribed above depends directly on whetherthe owner pays for heat and electricity orwhether tenants do.

Prospects for Retrofit When Tenants PayUtilities. Almost one-half of the multifamilyapartment units in the country are fully tenant-metered (see table 36). If structurally feasible,multifamily owners have converted to tenantmetering as the first and often final response to

lzThis debate is set forth in several papers prepared for the No-vember 1980 HUD Conference on Rental Housing, AnthonyDowns, “The Future of Rental Housing–Overview;” Ira Lowry,“Rental Housing in the 1970’s: Searching for the Crisis. ”

Ch. 4— Will Building Owners Invest in the Energy Efficiency of City Buildings? ● 119

Table 36.—National Distribution of Metering Typesof Rental Unitsa

Type of rental unit Percent of total

Master (full) . . . . . . . . . . . . . . . . . . . . . . . 19 ”/0Tenant (full) . . . . . . . . . . . . . . . . . . . . . . . 46Mixed (tenant pays electric but not

heat or hot water) . . . . . . . . . . . . . . . . 29Miscellany b . . . . . . . . . . . . . . . . . . . . . . . 6

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . 100 ”/0aTwo or more unitsbSy5tems too mixed to Categorize

SOURCE Natlorral Inferfm Energy Consurrrpflon Survey 1978.79, Departmentof Energy, Off Ice of Consumption Data.

escalating energy costs, even though conver-sion costs were clearly capital investments(costing from $125 to $1,600 per apartment unitwith a median of about $1 ,600). ’ 3 Yet paybackis very rapid, depending on how the base rent isadjusted: paybacks of 1 year or less are not un-usual, although the average simple payback is 1to 2½ years. There are several benefits oftenant-metering, in addition to sheltering thelandlord from the full impact of energy in-creases:

● Many buyers, particularly national syn-dicates and institutional investors, are un-willing to consider purchase of multifamilyproperty unless tenants pay the full cost ofutilities. Conversion to tenant metering,therefore, creates resale value in itself.

● Banks are more willing to refinance or lendto tenant-metered building owners.

● professional journals, particularly the wide-ly read Journal of Property Management,have taken an advocacy stance toward ten-ant metering with clearcut articles describ-ing investment return mechanics and own-er benefits, including resale value, fromtenant metering. There is practical adviceon such topics as tenant counseling tech-niques during remetering.

● Many States, particularly in the South andSouthwest, have made tenant electricalmetering in new buildings and sometimesexisting ones a mandate of State conserva-

I ]jeffrey M . Sel sler~ “Escaping the Energy Bite: ConvertingMaster Meters,” journal o(Property Management, May/June 1980.

tion policy law.14 Five out of seven apart-ment owners interviewed in San Antoniohad tenant-metered buildings partly be-cause it is required by law.

Owners interviewed in both the case studyand national interviews described little negativemarket impact as a resuIt of conversion. Tenantshave not reacted against tenant-metered build-ings during sellout or in existing buildings dur-ing remetering. To the contrary, some ownersnoted that tenant metering successfully trans-ferred to the utility companies the “bad guy”image that owners formerly bore for energy in-creases in gross rent.

In the opinion of most landlords interviewedfor the study, tenant metering has createdgreater and more reliable savings in energy con-sumption than any other improvement theycould have made because tenants make behav-ioral adaptations as a result. Savings from tenantmetering have also been documented. A bestestimate is 5 percent for heating and as much as20 percent for other energy.15 At the same time,tenant metering may result in higher per unitenergy costs for tenants i n utility areas wherelarge users pay significantly lower rates thansmall individual users. (See ch. 5 for morediscussion of this point.)

For all its advantages in inducing energy con-servation behavior by tenants, tenant meteringprovides virtually no incentive for apartmentowners to invest in greater efficiency of theirbuildings. There is no incentive to improve in-sulation levels, add storm windows, or improveheating system efficiencies (usually of decen-tralized systems since central heating and cool-ing systems cannot be tenant metered exceptwith great difficulty and expense). None of theowners of tenant metered buildings had madeenergy investments except to make operating

1 dMeterlng: States banning al I master metering include Califor-

nia, Florida, Maryland, Michigan, North Carolina, oklahoma,Rhode Island. States banning master metering for electricity in-clude Louisiana, Massachusetts, Minnesota, New Jersey, NewYork, Oregon, and Texas. Source: Steven Ferrey & Associates,Fo>ter~ng fquj(} jn Urban Conservation. Utf//ty Me[er/ng and UfJ/-

Jty Fjnarrclng, to be published as a working paper to this report.15LOU MC Lelland, op. cit.

120 ● Energy Efficiency of Buildings in Cities

improvements in the heating and cooling andlighting of the building’s common areas.

In theory, energy conservation investmentscan enhance the value of the property by per-mitting the owner to charge a higher rent,allowing for the lower utility cost to the tenant.In theory, if everyone else in the market alsomade energy efficiency investments, or therewere substantial new energy-efficient competi-tion from new buildings, an owner would beforced to improve in order to compete. Also intheory, if no one else improves, the ownercould improve his competitive position if hecould market the necessarily incremental rentadjustment.

To obtain the higher rent, however, requiresboth a sound market and marketing skill. Thetenant must be convinced that the total oc-cupancy cost will still be comparable to thelower rent competition. Given the fragmentednature of multifamily ownership, levels of pro-fessionalism, traditional tenant-landlord rela-tionships and tendency to hold rents down toreduce turnover, it is unlikely that this logic willbe readily adopted by the typical multifamilybuilding owner. Some sophisticated nationalsyndicates and management organizations in-terviewed for the study, however, are makingthe link between conservation and value. It isconceivable that over the long run, the adop-tion of such a strategy by a few large operatorsi n each market or the advocacy of such an eco-nomic rationale by one of the trade informationsources might stimulate such a perspective.

Prospects for Retrofit If the Owner Pays theUtilities. Although multifamily owners are con-verting to tenant metering whenever possible asa reaction to the rising cost of energy, it is notpossible to convert all types of heating systems,(especially central air systems, central steamand hot water systems, ) to tenant metering ex-cept at great expense. As the above table 36showed, more than one-half of all rental unitsare fully master metered or master metered forheat and hot water and tenant metered for elec-tricity.

Multifamily owners whose buildings have notbeen or cannot be fully tenant metered are