why latin america - scg legalscglegal.com/meetings/sao paulo/3 - why latin america 2013.pdfcivets:...

TRANSCRIPT

WHY LATIN AMERICA

Latin America in the world map…

|

… North America seems to be larger,

Source: Worldmapper

© Copyright SASI Group (University of Sheffield) and Mark Newman (University of

Michigan).

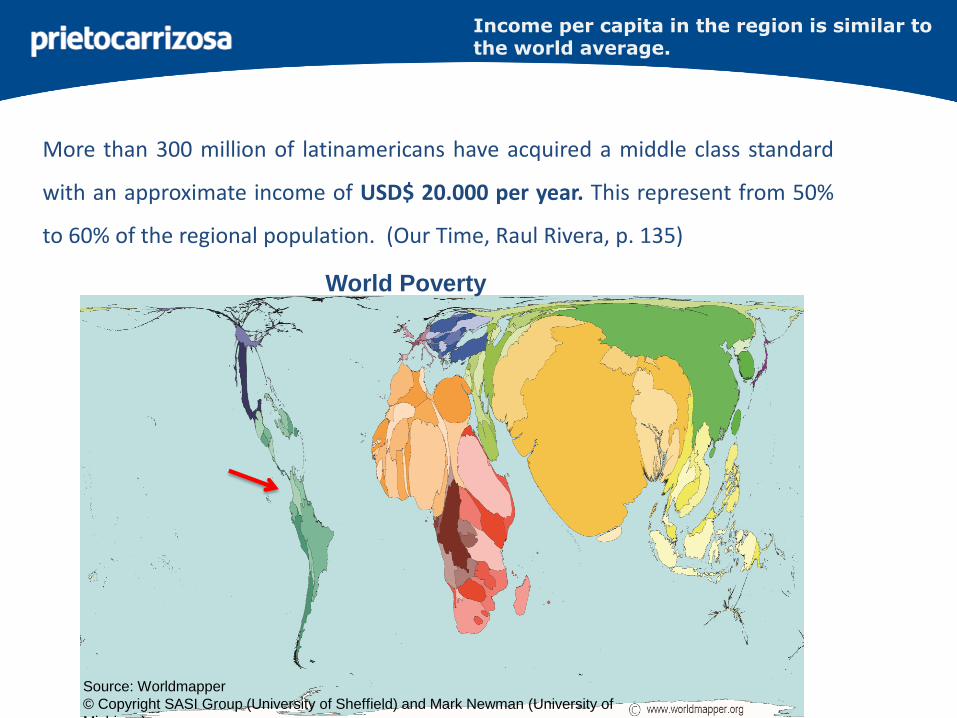

Income per capita in the region is similar to the world average.

More than 300 million of latinamericans have acquired a middle class standard

with an approximate income of USD$ 20.000 per year. This represent from 50%

to 60% of the regional population. (Our Time, Raul Rivera, p. 135)

World Poverty

Source: Worldmapper

© Copyright SASI Group (University of Sheffield) and Mark Newman (University of

Michigan).

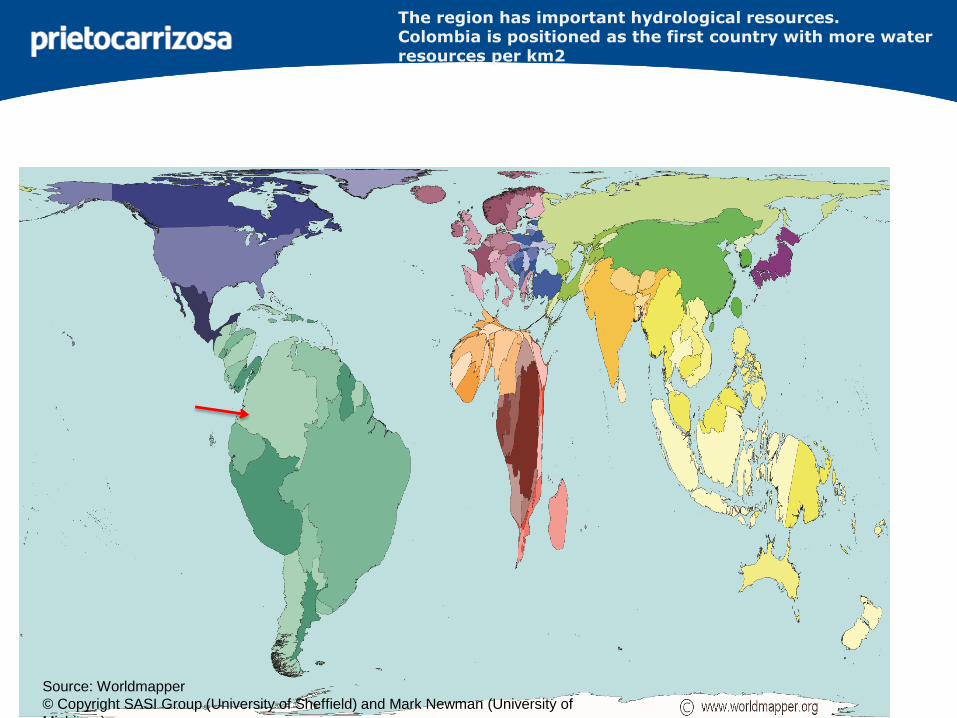

The region has important hydrological resources. Colombia is positioned as the first country with more water resources per km2

Source: Worldmapper

© Copyright SASI Group (University of Sheffield) and Mark Newman (University of

Michigan).

The region has the most important biological production capacity

Bio-Capacity: crops, plain, forest and fishing.

Source: Worldmapper

© Copyright SASI Group (University of Sheffield) and Mark Newman (University of

Michigan).

2,518

1,185

435

321

310

243

168

65

Brazil

Mexico

Argentina

Colombia

Venezuela

Chile

Peru

Ecuador

GDP 2011 (USD Billions)

Colombia´s GPD growth vs the Wolrd´s GPD 2002 - 2011

2.5

3.9

5.3

4.7

6.76.9

3.5

1.7

4

5.9

-4

-2

0

2

4

6

8

GPD growth: Colombia vs. World (%)

2002 2003 2004 2005 2006 2007 2008 2009

2010 2011

**Colombian growth Jan-Jun 2012: 4.9%

CIVETS: an opportunity for diversification

ColombiaIndonesia VietnamEgyptTurkeySouth Africa

CIVETS

Leaders in the wolrd market

CIVETS economies will have

important GPD growth

- Michael Geoghegan,

Global M&A Heat Chart

*US million.

Based on mergermarket companies for sale intelligence:

*Merger Market. M&A Round-up for 2012

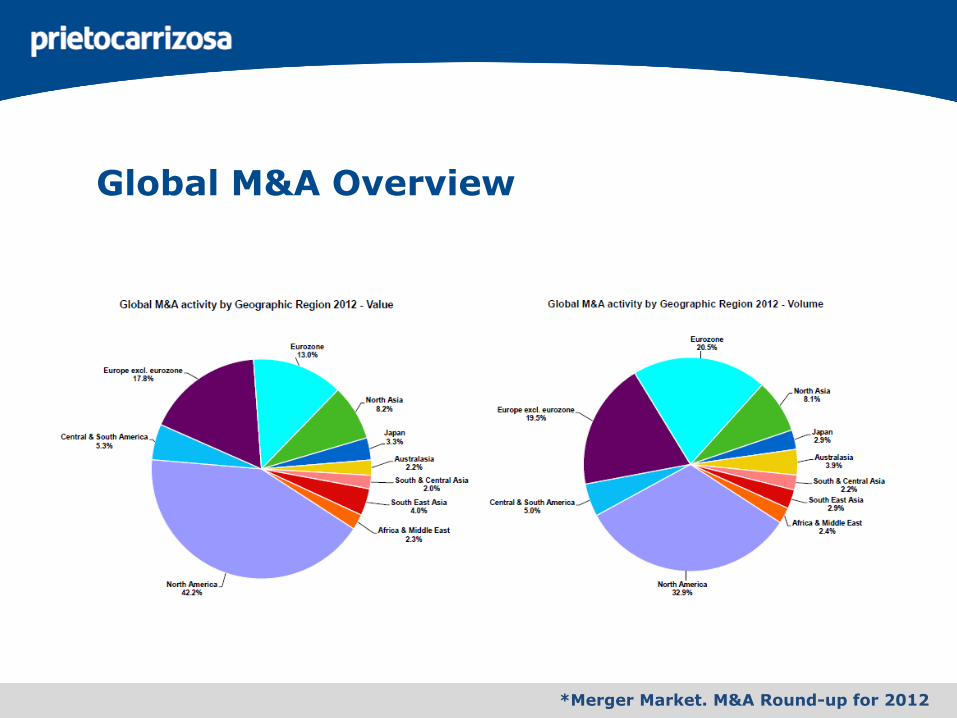

Global M&A Overview

*Merger Market. M&A Round-up for 2012

Global M&A Overview

*Merger Market. M&A Round-up for 2012

Global M&A Overview

*Merger Market. M&A Round-up for 2012

Private Equity Buyouts

Asia-Pacific (excl Japan) saw US$ 27.9bn-worth of buyout deals, sliding 28.9% on 2011 (US$ 39.3bn). 2012 was the second highest year for buyouts in the region since 2007 (US$ 49bn).

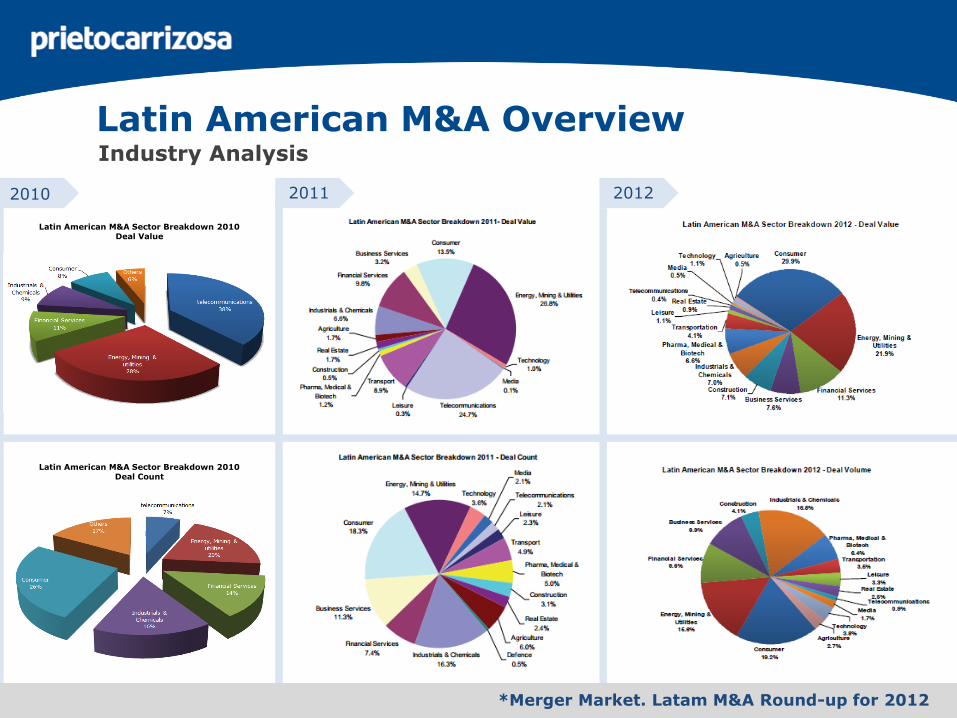

Latin American M&A Overview

*Merger Market. Latam M&A Round-up for 2012

Telefónica SA acquires BrasilcelNV (50% stake). Deal value: US$ 9

billion.

América Móvil(Mexico) acquires

Carso Global Telecom SAB (99.4%). Deal value: US$ 28

billion.

Latin American M&A Overview

*Merger Market. Latam M&A Round-up for 2012

Latin American M&A Overview

*Merger Market. Latam M&A Round-up for 2012

Industry Analysis

2010 2011 2012

Latin American M&A Sector Breakdown 2010 Deal Value

Latin American M&A Sector Breakdown 2010 Deal Count

M&A in the Pacific Alliance

M&A Europe

M&A US

ChileColombia M&A Europe

M&A US

*ISI Emerging Markets

M&A in the Pacific Alliance

PeruMexicoM&A US

M&A Europe

M&A US

M&A Europe

*ISI Emerging Markets

Foreign Investment Pacific Alliance

*www.banrep.com

Mexico

Peru

Mexico

Colombia

Peru

2010:

2011:

2012:

US$ -623 million

US$ 80 million

US$ -1.6 million

Chile

2010:

2011:

2012:

US$ 20 million

US$ 650 million

US$ 3,074 million

2010:

2011:

2012:

US$ 10.7 million

US$ 19 million

US$ 120 million

2010:

2011:

2012:

US$ 57 million

US$ 15 million

US$ 224 million

2010:

2011:

2012:

US$ 279 million

US$ 3,877 million

US$ 0

2010:

2011:

2012:

US$ 478 million

US$ 0

US$ 0

* Foreign Investment Committee.

Colombia

*www.proinversion.gob.pe

Chile

Colombia

Peru

Mexico

2010:

2011:

2012:

US$ 13 million

US$ 205 million

US$ 12 million

2010:

2011:

2012:

US$ 1.7 million

US$ 0.3 million

US$ 3 million

Chile

2010:

2011:

2012:

US$ 73 million

US$ 55 million

US$ 28 million

* www.economia.gob.mx

Mexico

2010:

2011:

2012:

US$ 464 million

US$ 464 million

US$ 476 million

Colombia

2010:

2011:

2012:

US$ 1,048 million

US$ 1,057 million

US$ 1,093 million

2010:

2011:

2012:

US$ 1,347 million

US$ 1,381 million

US$ 1,389 million

Foreign Investment Pacific Alliance

Peru

Multi-Latins in the Pacific Alliance

*ISI Emerging Markets

Banks

*ISI Emerging Markets

Chile

Mexico Colombia

Peru

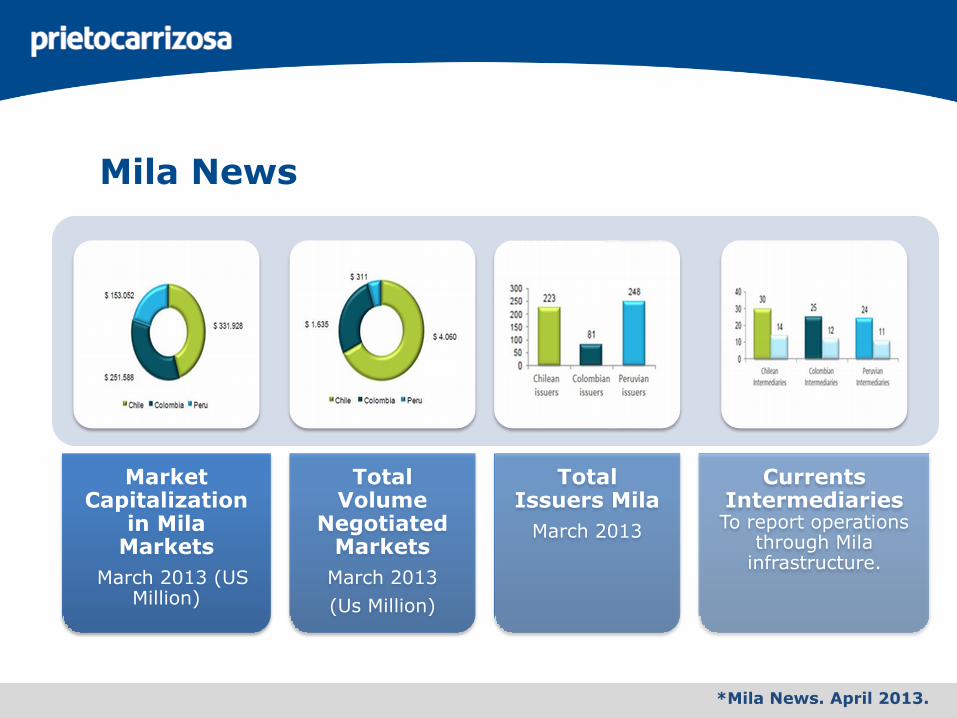

00

Market Capitalization

in Mila Markets

March 2013 (US Million)

Total Volume

Negotiated Markets

March 2013

(Us Million)

Total Issuers Mila

March 2013

Currents Intermediaries To report operations

through Mila infrastructure.

*Mila News. April 2013.

Mila News

Ease on doing business

*Doing Business 2013. IFC.

Rank on the ease of doing business

In the rank that qualifies countryas policy makers, Chile stands at37, Peru at 43, Colombia at 45and Mexico stands at 48.

Starting a new business

Chile

Starting a business

requires 7 procedures, 8 days and costs 4.5% of income

per capita.

ColombiaHas reduced

the time required from 60 days to 14, the cost from

28% of income per capita to

8% and procedures

from 19 to 9

Mexico

Requires 6 procedures, 9 days and costs

10.1% of income per

capita.

Peru

Requires 5 procedures, 26 days and costs

10.6% of income per

capita.

*Doing Business 2013. IFC.

Protecting investors

*Doing Business 2013. IFC.

How strong are investor protections?

Colombia and Peru have ahigh score indicating strongerprotections. Chile stands inthe rank 32 and Mexico inthe rank 49.

*Doing Business 2013. IFC. Page 3.

Business-friendly regulation

Chile, Peru, Colombia andMexico are in the top 5ranking of Latin Americancountries on the ease ofdoing business thatmeasures the economieswith the most business-friendly regulation.

Ease of paying taxes

*Doing Business 2013. IFC.

Globally, Chile stands at 36,Peru at 85, Colombia at 99and Mexico at 107 in theranking of 185 economies onthe ease of paying taxes.

“In 2007 Colombia’s government further institutionalized itscommitment to regulatory reform by establishing the Private Councilfor Competitiveness. The council is made up of business associationsand private sector players working closely with the government topromote sound, business friendly regulatory practices”. Peru andMexico have advanced in regulatory practice as well.

*Doing Business 2013. IFC. Page 27.

Regulatory practices

*Doing Business 2013. IFC. Page 9.

Colombia has achieved considerable success in improving businessregulation since 2005, along countries such as Georgia, Rwanda,China and Poland. Peru stands at 32 and Mexico at 39 in the globalranking

Regulatory practices

Colombia: key principles for foreign investment

Principles

Equal treatment

UniversalityAutomatic

Nature

Stability

*Doing Business 2013.

Chile: key principles for foreign investment

Principles

Political and Economic Stability

An efficient and high level

of connectivity

Important network of free trade

agreements

The legal transparency and stability for foreign investment

*Foreign Investment Committee Chile

Mexico: key principles for foreign investment

Principles

Business friendly

environment

Competitive labor costs

Network of free trade

agreements

Large logistics platform

*www.promexico.com

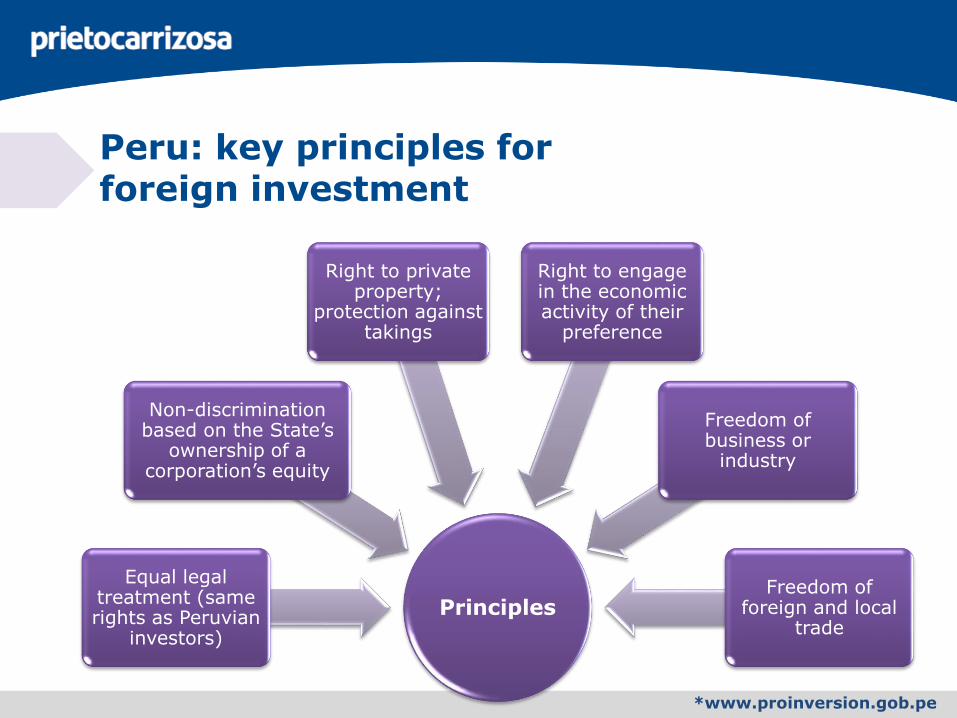

Peru: key principles for foreign investment

Principles

Equal legal treatment (same rights as Peruvian

investors)

Non-discrimination based on the State’s

ownership of a corporation’s equity

Right to private property;

protection against takings

Right to engage in the economic activity of their

preference

Freedom of business or

industry

Freedom of foreign and local

trade

*www.proinversion.gob.pe

Colombia: Free Trade Agreements

Canada

United States

Mexico

Caribbean Community

• Free Trade Agreements

•

•

•

•EFTA

Korea

Japan•

•European Union•

Mercosur

Turkey•• In negotiation,

concluded but not signed.

Colombia has 19 agreements with 59 countries

Cuba •

Venezuela•

•

Guatemala •El Salvador

••Honduras

Peru

•

•

Panama••Costa Rica

Israel •

Pacific Alliance

• Signed and waiting toformalize

Can

*Foreign Trade Ministry

Chile •

Bolivia

•

•

Ecuador

Chile: Free Trade Agreements

Canada

United States

Mexico

Central America

• Free Trade Agreements

•

•

•

•

•EFTA

Korea

Japan

China

•

•

•

•

European Union •

•

• Association Agreements

Colombia

Ecuador

Bolivia

Mercosur

•Venezuela

•

•

• Bilateral Trade Agreements

India •

• Partial Trade Agreement

Malaysia

Turkey•

• In negotiation, concluded but not signed.

Thailand

•

•

Chile has 20 agreements with 56 countries

•

Australia

P4

*Foreign Investment Committee Chile

Pacific Alliance

•Peru

•

•

Panama

Mexico: Free Trade AgreementsMexico has *49 agreements with 44 countries.

* Mexico Economy Secretariat and Promexico

Mercosur•

Canada •

Bolivia•

Costa Rica •

Colombia

Chile(TPP)

Israel •Japan•

Brazil•

Paraguay•

Nicaragua•

Guatemala

El SalvadorHonduras

•• •

Panama•

•EFTA

Cuba•

•Belize

European Union •Canada (APEC) (TPP)

United States (TPP)

Singapore (TPP)

Australia (TPP)

Malaysia (TPP)

Vietnam (TPP)

New Zealand (TPP)

Brunei (TPP)•

•

•

Brunei (TPP) (APEC)•

Korea

China•

•

• Free Trade Agreements

• In negotiation, concluded but not signed.

• Signed and waiting toformalize

Ecuador •

Pacific Alliance

Peru (TPP) •

•

•

*(12 FTAs, 28 promotion agreements <APPRIs>, 9 commercial agreements). Promexico

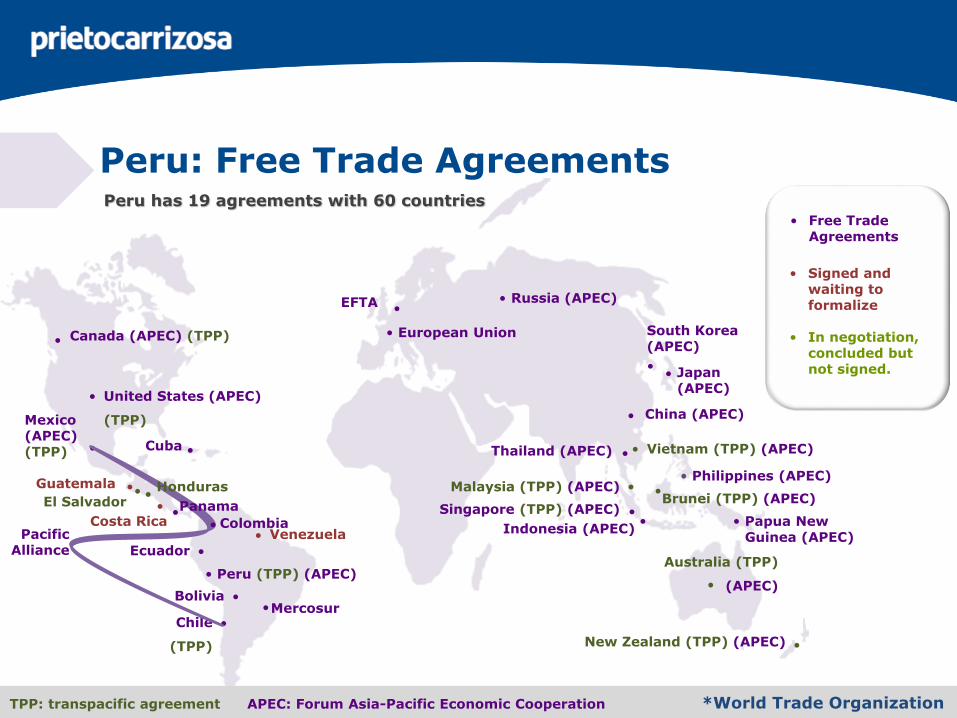

Peru: Free Trade Agreements

Canada (APEC) (TPP)

United States (APEC)

(TPP)Mexico(APEC) (TPP)

•

•

•

•EFTA

Japan (APEC)

European Union

Mercosur

Peru has 19 agreements with 60 countries

Cuba •

Venezuela•

•Chile

(TPP)

•

Peru (TPP) (APEC)•

Bolivia •

Ecuador •

•

•

China (APEC)•

•

••Costa Rica

Guatemala •

Thailand (APEC) •

Singapore (TPP) (APEC) •

South Korea (APEC)

•

•El Salvador

•

Australia (TPP)

(APEC)•

TPP: transpacific agreement

Malaysia (TPP) (APEC) •

Vietnam (TPP) (APEC)•

New Zealand (TPP) (APEC) •

Brunei (TPP) (APEC)•

Russia (APEC)•

*World Trade OrganizationAPEC: Forum Asia-Pacific Economic Cooperation

Indonesia (APEC)• • Papua New

Guinea (APEC)

• Philippines (APEC)

• Free Trade Agreements

• In negotiation, concluded but not signed.

• Signed and waiting toformalize

ColombiaPacific

Alliance

•

Honduras

Panama

Pacific Alliance

*Eltiempo.com

Mexico

Colombia

Peru

Chile

The four countries account more than:

209 million of inhabitants.

They represent:35% of Latin American GDP.

They produce:2.7% of world GDP.

They generate:50% of the Latin American

commerce.

They produce more than:49% of region exports.

•The Pacific Alliance is a union of four countries (Colombia, Mexico, Chile, and Peru) that have coastlines on the Pacific Ocean and which have joined forces to enable them to act as a bloc on issues of trade and investment and to ensure full freedom of movement of goods, services, capital, and people.

What is thePA?

•This new bloc will mean a breakthrough in the economic integration of Latin America, and it will be the opportunity to realize the commercial potential of the Member economies.

Why is it significant?

•This initiative is intended to address the need to expand and diversify the political and economic relations of the region as a whole. It aims to deepen trade relations between the member countries, followed by those with Asia-Pacific, which is a region that shows great commercial, economic, and political dynamics.

What is the purpose?

*Mincomercio.gov.co (Colombian Minister of Trade, Industry, and Tourism Sergio Diaz Granados)

Pacific Alliance

*Mincomercio.gov.co (Colombian Minister of Trade, Industry, and Tourism Sergio Diaz Granados)

•The initiative covers the following topics: the movement ofbusinessmen and workers and the facilitation of immigration,including police cooperation; trade and integration; aspectssuch as trade facilitation and customs cooperation; servicesand capital, which aim to integrate the stock exchanges;cooperation, and the establishment of dispute settlementmechanisms.

What are the topics of

integration?

•One of the issues proposed in this large integration project isthe freedom of capital markets and the integration of stockexchanges. This point has caught the attention of foreigninvestors and has sparked the desire of companies in eachcountry, in respect to accessing a group of homogeneousmarkets in terms of macroeconomic policy.

What are the benefits for investment?

•Colombia will present a draft text covering the disciplines ofinvestment and services. In light of this proposal, the Membercountries will determine the need and desirability ofnegotiating an agreement on these matters. There are alsoplans for the iniciation of sessions of the Joint Committee onServices and Investment so as to identify barriers toinvestment in the countries of the Alliance.

What is the proposed

agenda for services and

capital?

Pacific Alliance

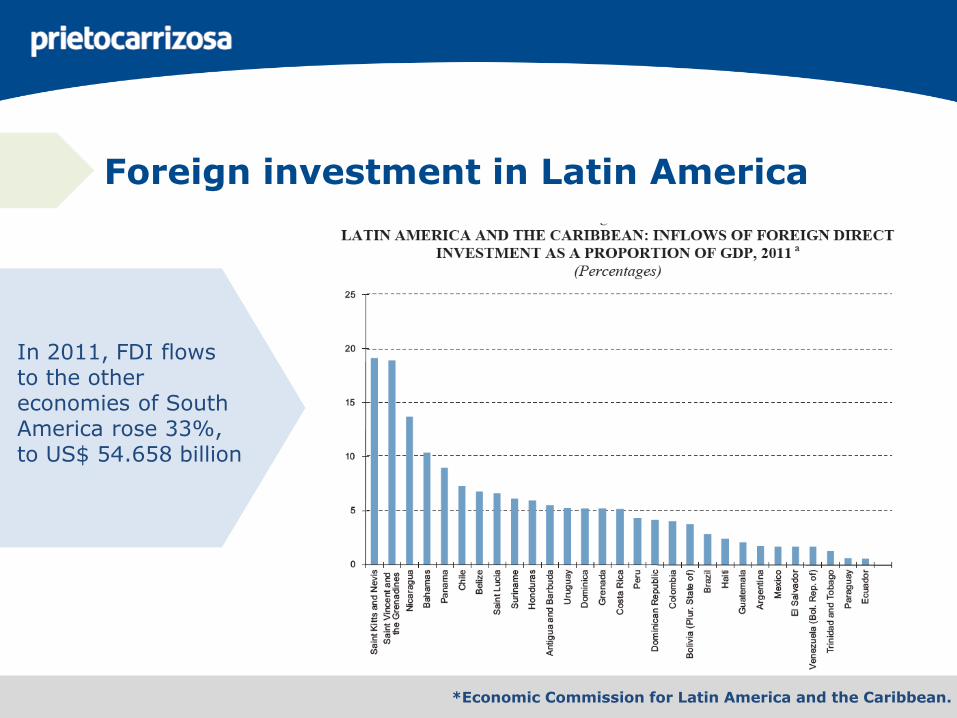

Foreign investment in Latin America

Countries of the Caribbean and Central America received FDI in excess of 5% of GDP. Among the medium-sized and large economies, inward FDI in Chile accounted for as much as 7% of GDP, followed by Uruguay at 5%. For the largest economies in the region, FDI accounted for a far smaller proportion: Mexico and Argentina received flows equivalent to less than 2% of GDP.

*Economic Commission for Latin America and the Caribbean.

Foreign investment in Latin America

In 2011, FDI flows to the other economies of South America rose 33%, to US$ 54.658 billion

*Economic Commission for Latin America and the Caribbean.

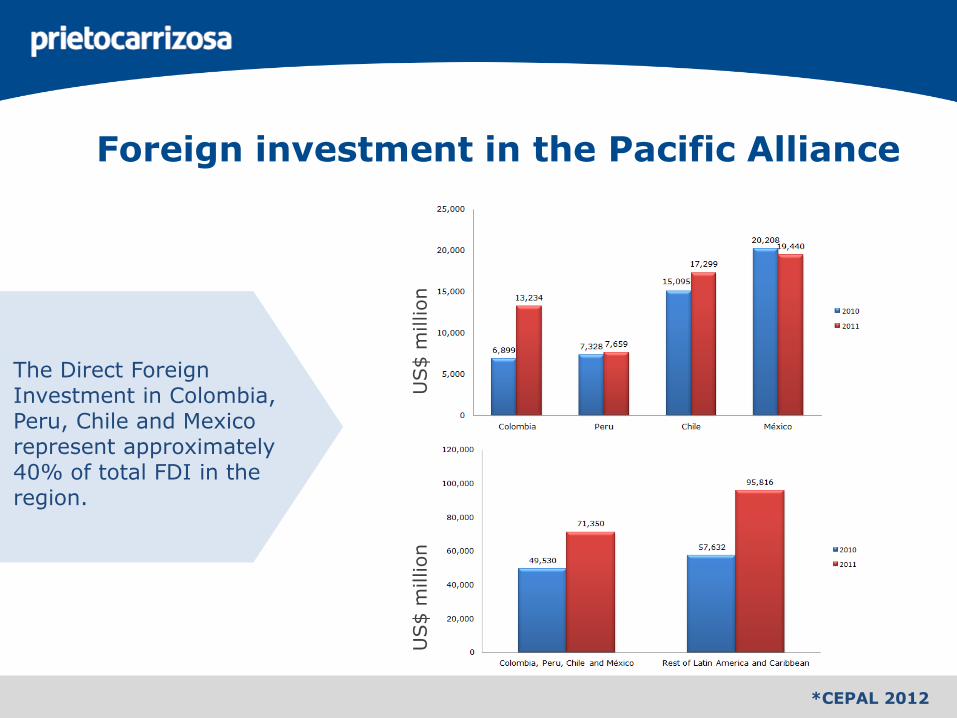

Foreign investment in the Pacific Alliance

*CEPAL 2012

US$

million

The Direct Foreign Investment in Colombia, Peru, Chile and Mexico represent approximately 40% of total FDI in the region.

US$

million

*CEPAL 2012 *¨Proinversion.gob.pe

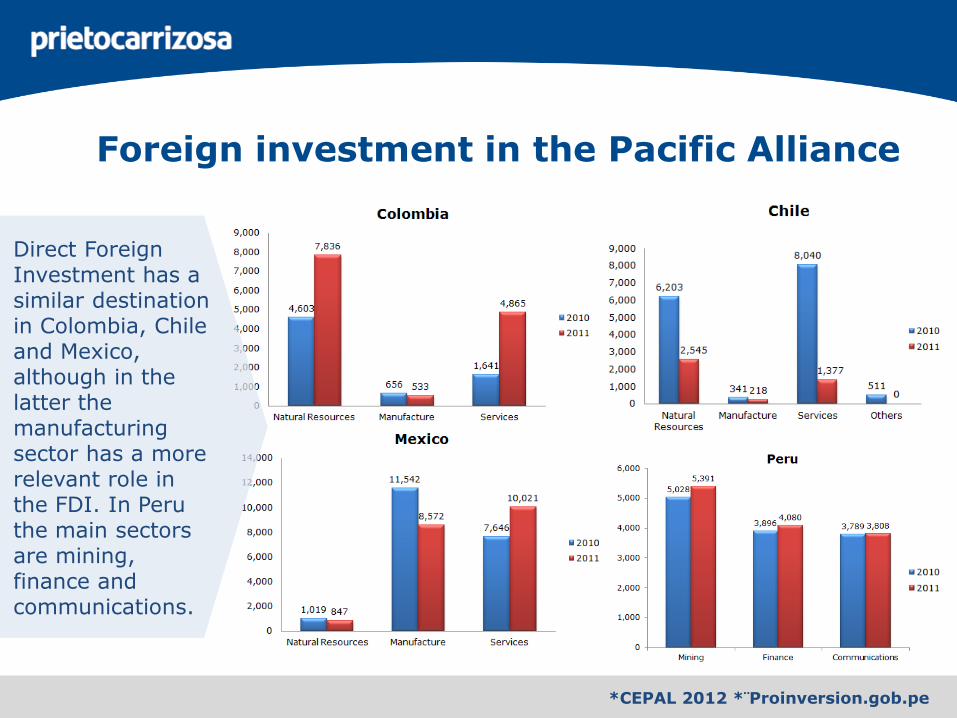

Foreign investment in the Pacific Alliance

Direct Foreign Investment has a similar destination in Colombia, Chile and Mexico, although in the latter the manufacturing sector has a more relevant role in the FDI. In Peru the main sectors are mining, finance and communications.

Inflation rate in the Pacific Alliance

The inflation rate in the Pacific Alliance has decreased progressivelyduring the last 11 years.

*World Economic outlook

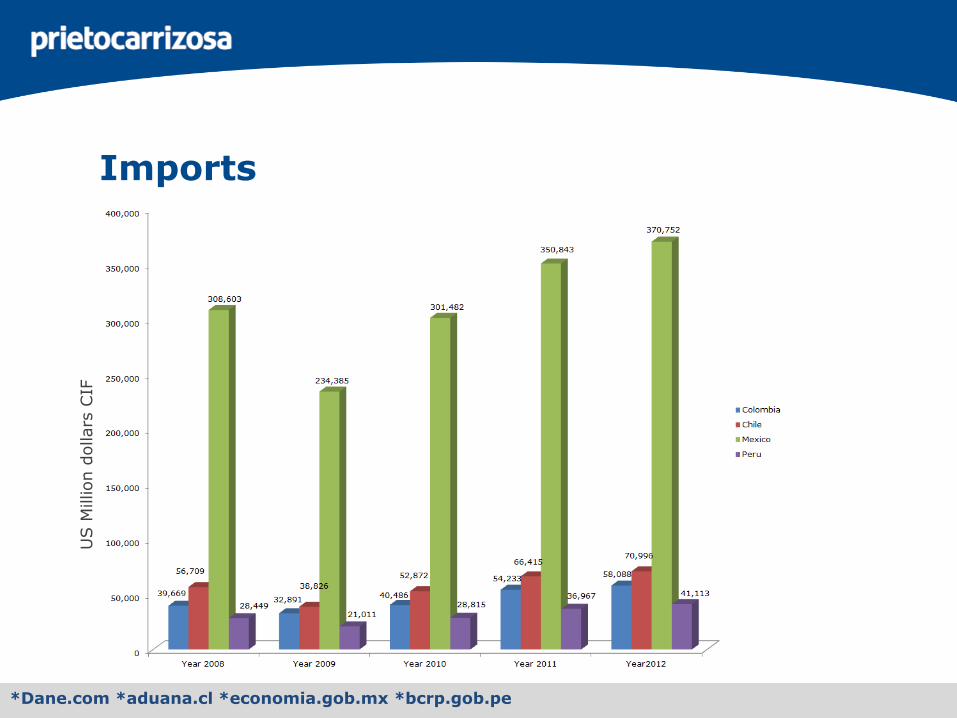

Imports

*Dane.com *aduana.cl *economia.gob.mx *bcrp.gob.pe

US M

illion d

ollars

CIF

Exports

US M

illion d

ollars

CIF

*Dane.com *aduana.cl *economia.gob.mx *bcrp.gob.pe

*DANE REPORT. Second quarter of 2012. - *National Infrastructure Agency (ANI).

Colombia: Investment opportunities

The two industries with the highest growth (related to

the GDP) were mining and quarries (8.5%) and

construction (18.4%)

The National Government started the program The

Fourth Generation (4G) of Road Concessions in

Colombia. The goal is to achieve 3% of GDP in 2014 (US$10

billion).

Law 1508 (Public Private Partnerships), which

introduces a new mechanism for introducing private

investments in infrastructure projects, was approved in

January of 2012.

*National Planning Department (DNP).

The most relevant benefits of Law 1508 (Public PrivatePartnerships).

1

• Private initiatives can propose and structure projects.

2

• This law encourages the participation of institutional and financial investors.

3

• Private equity funds can participate in infrastructure projects through a special regulation (1508 of 2012).

Colombia: investment opportunities

*National Planning Department (DNP).

Currently there is no exact data about all the private publicpartnerships, but the National Planning Department hasreports of some of the projects presented. These are someof the industries with approved projects.

Construction (3)

• Early childhood care.

• Prisons

• Urban Renovation

Roads (23) Railways (7)

Airports (5)

Colombia: investment opportunities

Agribusiness

Energy Infrastructure

Mining

Chile: investment opportunities

*Foreign Investment Committee Chile

Chile: investment opportunities

*Foreign Investment Committee Chile

Agribusiness is one of the country’s most important sectorsaccounting for 12% of Chile’s GDP and 24% of exports in 2010.

Chile is one of only fiveplaces in the world, witha Mediterranean climate.This type of climatefacilitates production offoods such as olive oil,wine, fruit andvegetables that are inline with an internationaltrend towards healthyeating.

Energy

Gold and Metals

IT Services

Infrastructure

Mexico: investment opportunities

*JP Morgan

*Metals Economics Group

Mexico: investment opportunities

Location of significant gold and base metals drill results

Latin America remained the most popular exploration destination, attracting 25% of global spending in 2011, with six countries— Mexico, Chile, Peru, Brazil, Colombia, and Argentina — accounting for the lion’s share of the region’s total, boosted by strong growth in gold exploration in Mexico.

*Promexico

Mexico: investment opportunities

Service Providing Projects

Concessions

Asset Exploitation

Public-private partnerships can take on differentmodalities. In Mexico, the following have been alreadyimplemented through different projects:

Mining

Electricity Industrial

Infrastructure

Peru: investment opportunities

*www.proinversion.gob.pe

Peru: investment opportunities

www.proinversion.gob.pewww.proinversion.gob.pewww.proinversion.gob.pe

*www.proinversion.gob.pe

International Law Firms in the Pacific Alliance

*Latin Lawyer

Top 5 deals of 2012 by value

*Latin Lawyer. Table Leagues 2012.

Deal US$ Firms Deal US$ Firms

Top positions regionwide

*Latin Lawyer. Table Leagues 2012.

By volume By value

*Latin Lawyer. Table Leagues 2012.

Top positions regionwide

Regional deal spread

*Latin Lawyer. Table Leagues 2012.

Top positions regionwide

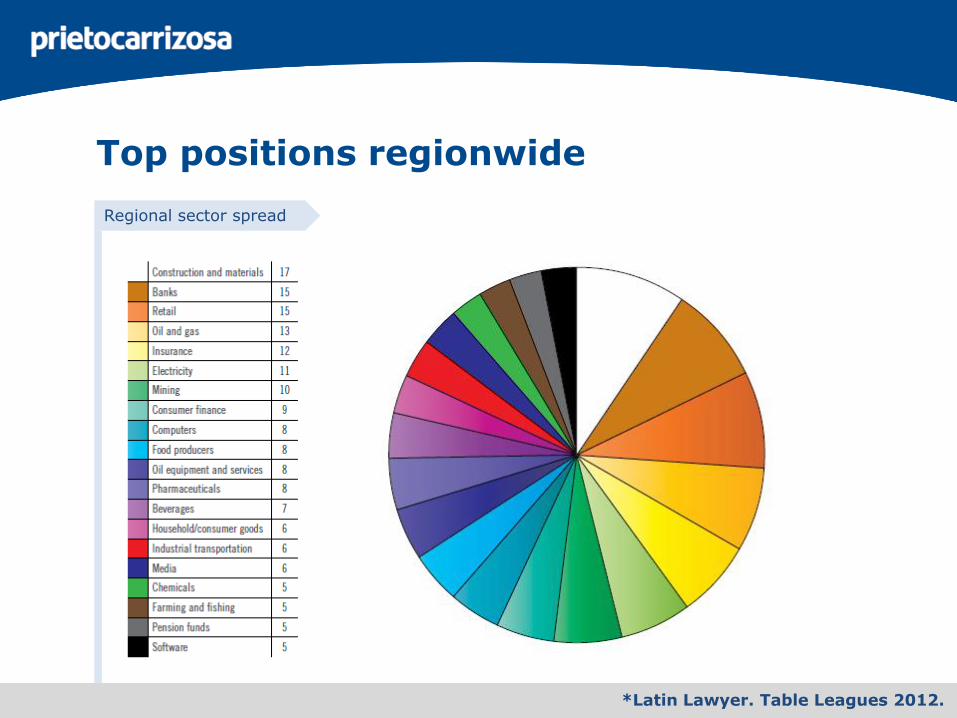

Regional sector spread