wholesale trid procedures - merrimack mortgage tpo · wholesale trid procedures name ......

TRANSCRIPT

Wholesale TRID Procedures

Wholesale TRID Procedures rev. 12/30/15

1

Wholesale TRID Procedures

Table of Contents Definition of an

application..............................................................................................................................3 Submitting a Disclosure

File.............................................................................................................................3 How to complete the Service

Providers........................................................................................................4 Adding a new

contact..........................................................................................................................................9 How to complete the Fees

Worksheet.........................................................................................................11 Submission

Checklists......................................................................................................................................20 Submitting the Underwriting

File................................................................................................................21 Broker Required

Disclosures........................................................................................................................21 TBDs.......................................................................................................................................................................

22 Loan

Tracking.....................................................................................................................................................22

Notifications.........................................................................................................................................................22

Rate Locks.............................................................................................................................................................23

LE/CD Revision Request..................................................................................................................................23

Fees not required by the Lender...................................................................................................................24

Who provides the LE?.......................................................................................................................................24

Disclosure Issuance...........................................................................................................................................24

Tolerances (Variances)....................................................................................................................................25

Business Day Definitions.................................................................................................................................26

When must my loan be CTC?..........................................................................................................................27

Closing Disclosure..............................................................................................................................................27

Closing Threads..................................................................................................................................................28

AUS Run

2

Wholesale TRID Procedures

Requests..............................................................................................................................................30 Disclosures no longer

required.....................................................................................................................31 When can I order my

appraisal?...................................................................................................................31 FHA Case Number

Requests...........................................................................................................................31 Miscellaneous

Information.............................................................................................................................32 Exhibits

A - Disclosure File Submission Checklist..............................................................................................33

B - Underwriting File Submission Checklist........................................................................................35

C - Pre-Approval File Submission Checklist.........................................................................................38

D - TBD Flip File Submission Checklist..................................................................................................40

E - 2015 Lender X Appraisal Fee List.....................................................................................................42

F - LE/CD Revision Request Form...........................................................................................................43

Definition of an application

Once the following are obtained, you now have an “application”. Remember the acronym ALIENS!:

● Address of Property ● Loan Amount ● Income ● Estimated Value ● Name of the Consumer(s) ● Social Security Number

3

Wholesale TRID Procedures

Once the 6 pieces of application information are received, MMC must disclose the file within 72 hours.

Submitting a Disclosure File

Once the 6 pieces of application are obtained, the loan must be registered on our system and submitted within 24 hours of the application date.

When the loan is registered in OpenClose, you will select the ‘TPO- TRID” Closing Cost Scenario.

You will also complete the Fee Worksheet screen in OpenClose and the following must be submitted within 24 hours of application:

• 1003 signed by the Loan Officer (Consumer signatures are not required)

• Completed Submission Form

• Acceptable AUS Findings per product guidelines

• Purchase Agreement (if applicable or obtained)

You will upload these items to “Disclosure File Submission” and complete the “Submit Loan to Lender” function.

o Enter a valid email address for all Consumers so we may e-deliver the disclosures

o Please only submit required documents listed above

How to complete the Service Providers

Before you can complete the Fees Worksheet, you must set up your Service Providers. TRID requires the disclosure of at least one service provider for each type of provider listed in Section C. Procedures for adding these companies are shown on the following pages. From the ‘Loan Actions” menu, select ‘Loan Contacts’:

4

Wholesale TRID Procedures

This screen allows you to attach specific Vendors to your loan.

In the ‘Select View’ drop down, choose one of the following options based on your needs. ● Company Contacts = Existing vendors in Merrimack Mortgage’s database you can choose ● My Contacts = Vendors the TPO client has added to their own database within OpenClose

to choose (if needed, refer to ‘Adding a new contact’) To attach an existing MMC contact: In the ‘Select View’, choose ‘Company Contacts’.

5

Wholesale TRID Procedures

Name - Specific contact person’s name at the Vendor (Do not use) Company - Specific company name of the vendor (Best Option) Type - Choose the type of vendor from the dropdown (i.e. Title Company)

6

Wholesale TRID Procedures

When you receive the above message, click “OK” to proceed.

7

Wholesale TRID Procedures

8

Wholesale TRID Procedures

Adding a new contact

If your Service Provider is not currently in ‘My Contacts’, input the New Contact information and save at the bottom of the screen. You must input the contact’s name, company, address, phone # and email address at a minimum.. Click ‘Save’ at the bottom of the screen. The Closing Agent cannot be added here. To select the Closing Agent, you must select it from ‘Company Contacts’ as shown on next page.

Once all the information is completed click save.

9

Wholesale TRID Procedures

You can now attach your vendor from selected view of ‘My Contacts”.

10

Wholesale TRID Procedures

How to complete the Fee Worksheet

After your loan is registered, go to the Loan Snapshot screen. From this screen, click on the 'Loan Actions' menu and select 'Edit Fees Worksheet'.

Next, we will go through the highlighted sections shown below:

11

Wholesale TRID Procedures

You will select who a fee is being paid by. For example, if the fee is being paid by the seller, you would select “Seller” from the drop down here:

Within the Fee Worksheet screen, you will want to make sure to select who a fee is being paid to. The field will appear as follows:

On the far right of the screen, you will see multiple check boxes. Please make sure you do not check or uncheck any of these boxes. The boxes appear as follows:

There are multiple calculator icons within the Fee Worksheet Screen. Please do not use the calculators. The calculator icons appear as follows:

12

Wholesale TRID Procedures

What to enter

● 1st Payment Date - This will calculate the prepaid interest properly ● Estimated Closing Date

● When entering the dates, be sure to use the Calendar icon. Do not input manually

Credit or Discount:

● Nothing is entered here. These fields carry over from the price/lock information. If the loan is floating, the numbers will change when the loan is locked

● Be sure not to change anything in these fields

13

Wholesale TRID Procedures

Section A - Origination:

● Admin Fee if the fee has not been deducted as an LLPA based on the product code (ie 30C-AF vs. 30C). If an Admin Fee is required, you must add it here as it will not auto populate based on product code

● If this is a Consumer Paid transaction, you will enter the mortgage broker fee. If there is a credit or discount, this is auto populated

● Supplement Origination Fee (on 203KS program)

Section B - Services You Can’t Shop For:

● Appraisal Fee - Use Appraisal Fee Matrix (Exhibit E) ● Credit Report Fee ● Any additional fees required for the mortgage transaction that the Consumer cannot shop

for

14

Wholesale TRID Procedures

Section C - Service you can shop for:

● Closing/Escrow Fee

● Title Exam Fee

● Doc Prep Fee

● Attorney fee

● Title Insurance

● Abstracting Charges

● Plat Drawing

● Any additional services required by the program (ie. VA pest inspection, FHA Water Test)

● Title insurance must be itemized

● If the Closing Agent fees are lumped on the LE, they cannot be broken out when the CD is issued. You must obtain the exact name of the fees the Closing Agent is charging

15

Wholesale TRID Procedures

Section E - Taxes and other government fees:

● Recording Fees (10% tolerance) ● City/County/State Tax Stamps (0% tolerance)

16

Wholesale TRID Procedures

Section F - Prepaids:

● Interest will auto populate based on the 1st payment date you entered

● Hazard insurance

● Flood Insurance

Section G - Initial Escrows:

● Hazard reserves - # of months and monthly payment

● City taxes - # of months and monthly payment

● Flood reserves - # of months and monthly payment (Please note, as of January 1, 2016, flood reserves are required)

● If they are or are not escrowing, make sure the correct boxes are checked

17

Wholesale TRID Procedures

Section H - Other:

● Fees incurred not required by the Lender

● Water Test if not required by Lender

● Home Inspection

● Broker Agent Fees

● Personal representation fees

*For all fees listed, a Service Provider must be associated. You may manually type the Service Provider name under ‘Provider/Payee’. The Service Provider will not show on the LE, but will show on the CD.

● This section is a breakdown of the Details of Transaction. If you have subordinate financing, you should see it here. It would have auto populated from the Price/Lock screen

18

Wholesale TRID Procedures

● This section details the credits associated with the transaction. This is where you

confirm the seller credits per the P&S and the earnest money deposit

● Here you will see the total estimated monthly payments. This will include, principal, interest, taxes, insurance and any HOA dues. If flood insurance is applicable, this will be combined with the hazard insurance payment within this section

19

Wholesale TRID Procedures

Submission Checklists

We have developed new checklists that have been included in the presentation and are available to you on our website.

The checklists show which disclosures you are responsible for.

The bottom of the checklists will remind you where to upload your file.

These new submission checklists are:

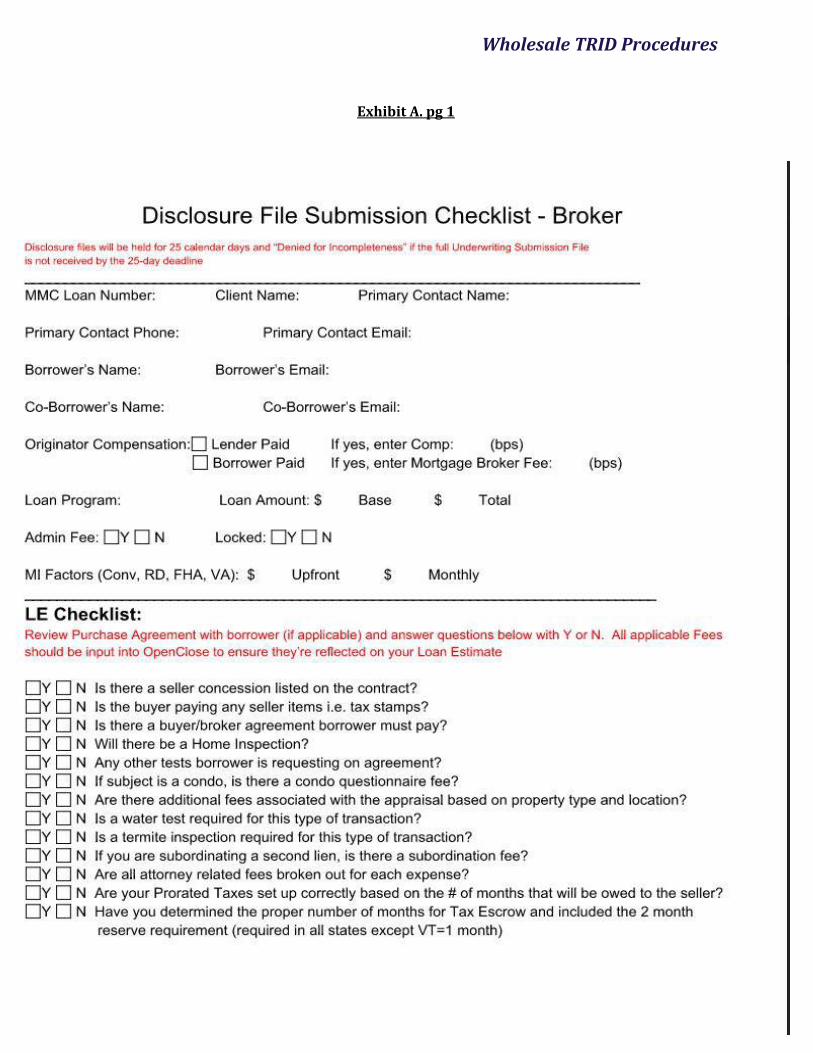

❍ Disclosure File Submission Checklist (Exh. A) - Use to submit limited documentation so MMC may disclose on the loan

❍ Underwriting File Submission Checklist (Exh. B) - Use after MMC has disclosed on the loan and you are submitting a full Underwriting file

❍ Pre-approval Submission Checklist (Exh. C) - Use when submitting a loan with no property address for Underwriting (TBD)

❍ TBD Flip Submission Checklist (Exh. D) - Use when a loan with no property has already been underwritten and a property has been found

20

Wholesale TRID Procedures

Submitting the Underwriting File

Once MMC’s initial disclosure package has been signed and the submission checklist documents have been received , the full Underwriting file may be submitted.

Please upload your submission file as one document.

Make sure to upload the Underwriting file to “Underwriting Submission File” and complete the ‘Update Lender’ function.

The "Intent to Proceed" must be signed within 10 days of receiving the application information.

The full Underwriting file must be received within 25 days of receiving the application information.

Broker Required Disclosures

☐ Consumer(s) Certification and Authorization ☐ Risk Based Pricing Disclosure ☐ Business 4506T for Consumer(s), if applicable ☐ 4506T for Consumer(s) ☐ Affiliated Business Agreement, if applicable ☐ Massachusetts Loan Origination and Compensation Agreement ☐ Maine Mortgage Broker Agreement ☐ ME Disclosure to Consumer/Material Consumer Protection ☐ NJ - Mortgage Broker Service Agreement Disclosure ☐ VT Broker Prospective Consumer Agreement (aka VT Mortgage Broker Fee Agreement and Disclosure)

● These are the disclosures that Merrimack requires. Please check with your internal Compliance Department on what your company requires

21

Wholesale TRID Procedures

TBDs

If your submission is truly a TBD, please make sure to enter the address as TBD in the street line.

Without the property address, the 6 pieces of information have not been obtained and disclosure is not required.

If you are providing the consumer with an Early Estimate you must include the following verbiage in 12 point font or larger and it must be shown at the top of the page:

“Your actual rate, payments, and costs could be higher. Get an official Loan Estimate before choosing a loan.”

Loan Tracking

In order to make sure your loans are in compliance with TRID, we will be monitoring reports multiple times throughout the course of the day each day looking for registered loans.

Considering you must have 6 pieces of information to register a loan (except for TBDs), we will be contacting you to submit your disclosure file within 24 hours of registration so we can disclose within 72 hours from the application date.

Notifications

We have expanded on the Loan Comments you receive via email. We will notify you when the loan has been disclosed. We will note the Loan Comments, but we will also send an email to the LO and Processor. The comments will read as follows:

“ File has been disclosed electronically to Consumer. A copy of the Disclosures can be found in the E-Doc Manager under Findings, Doc Magic Disclosure PDF. Appraisal can be ordered once you're in receipt of MMC's fully executed Intent to Proceed. Thank you.”

22

Wholesale TRID Procedures

Rate Locks

Due to the timing requirements involved in TRID, all loans must be locked at least 15 calendar days prior to closing.

MMC will issue a revised LE upon receipt of a LE/CD Revision Request (Change Circumstance) when the loan is locked.

TPO clients are responsible for uploading the LE/CD Revision Request at the time of rate lock. Upload LE/CD Revision Request to “Change of Circumstance” only.

LE/CD Revision Requests (Change of Circumstance Requests)

As a reminder, LE/CD revision requests are accepted in the following cases:

• An extraordinary event beyond the control of any interested party or other unexpected event specific to the consumer or transaction;

• Information specific to the consumer or transaction that the creditor relied upon when providing the Loan Estimate and that was inaccurate or changed after the disclosures were provided; or

• New information specific to the consumer or transaction that the creditor did not rely on when providing the Loan Estimate

Please be sure to fully complete the LE/CD Revision Request Form (Exh. F).

Information the creditor knew or had in its possession at the time the initial LE was issued cannot be considered a changed circumstance, even if it was not reviewed until after the LE was issued.

When you upload a LE/CD Revision Request, please make sure to upload it to “Change of Circumstance” only. If the form is uploaded to the wrong area, redisclosure may be delayed which may cause a compliance violation.

23

Wholesale TRID Procedures

Fees not required by the Lender

If there are fees associated with the purchase or refinance of a home that are not required by the Lender, these items must be listed on the LE and CD in Section H (ie, home inspection, radon test, buyer/broker fee, etc). Items handled outside of closing that are known to the Closing Agent or Creditor must be disclosed in this section.

The seller may pay for these fees. If the seller is paying items in Section H, these amounts will be included in the maximum seller contributions allowed per the program limits. Invoices and proof of payment must be provided.

Who provides the LE?

MMC will provide the Loan Estimate.

MMC does not allow a Broker to issue a LE. The LE must be provided by MMC.

If a LE is issued by a Broker, MMC will be unable to accept the loan. The loan can be resubmitted but not before the LE has expired which is 10 days from the date of issuance on a floating loan or after the rate lock expiration on a locked loan.

Disclosure Issuance

MMC will deliver via e-disclosure. Your clients will have disclosures emailed to them for signature and the documents will be loaded into the E-Doc Manager under ‘Findings’. If you want to print the docs and deliver them you may do so from the E-Doc Manager.

24

Wholesale TRID Procedures

Tolerances (Variances)

The existing tolerance categories of 0%, 10% aggregate, and “no tolerance” will continue to be used. However, there are some changes to the charges included in these categories: 0% Tolerance: Fees in this category may not increase from the LE to the CD.

• Fees paid to the creditor, broker, or an affiliate of either • Fees paid to a third party if the Consumer was not allowed to shop for the third party

service • Transfer taxes

10% Aggregate Tolerance: The total of all charges in this category cannot increase by more than 10% from charges listed on the last LE issued to the charges listed on the CD. Please note only charges for services actually obtained will be used in the comparison.

• Government recording fees • Fee for service Consumer may shop for when a Consumer chooses provider from

creditor’s provider list Note: Providers that are affiliates of creditor or broker are subject to 0% tolerance “No Tolerance”: Charges in the “no tolerance” category may increase in any amount, but still must be disclosed on the LE in good faith*

• Prepaid Interest • Property Insurance Premiums • Amount paid into escrow • Fee for service Consumer may shop for when Consumer selects a provider not on

creditor’s provider list • Charges paid for third-party services not required by the creditor, even if paid to affiliate

**Note: If these fees are listed on the LE, there is no tolerance for changes when the CD is issued. If they are omitted from the LE, they cannot be charged without a valid Change Circumstance or cure.

25

Wholesale TRID Procedures

Business Day Definition

There are two different definitions of a “business day” under TRID.

● Standard Business Day (SBD): Any day on which Merrimack’s offices are open to the public for substantially all of its business functions. This definition is generally used for timing requirements related to the LE and other early disclosures, except for the required time between a LE being issued and loan consummation.

● Precise Business Day (PBD): All calendar days except Sundays and federally recognized holidays. This definition is generally used for timing requirements related to the CD.

○ Exceptions: The Precise Business Day rule is used to calculate: ■ The minimum 7 business day period between sending the LE and loan

closing ■ The minimum business day period between issuance of a revised LE and

loan closing While SBD and PBD are not regulatory terms, they will be used in this document to to clarify which definition of “business day” applies to a requirement.

26

Wholesale TRID Procedures

When must my loan be CTC?

Please make sure to check our website and our daily rate sheet to determine condition review turn times.

All loans must have all "Prior to Docs" conditions cleared 10 calendar days prior to closing and all "Funding" conditions cleared 3 business days prior to closing.

Non-credit conditions on the loan may be moved to "Funding" conditions in order to prepare the CD.

All required information from the Closing Agent is needed before a CTC may be issued.

All "Funding" conditions must be cleared 3 SBD prior to closing.

Closing Disclosure

The CD must be sent out and acknowledged at least 3 PBD days prior to closing. Please note in order to prepare the CD, we must have all of the required information from the Closing Agent at least 72 hours prior to issuance.

This means that not only does the closing package have to be prepared, but the CD must be issued, approved, mailed or e-delivered to the Consumer and the Consumer must consent to the CD 3 PBD prior to closing.

We will e-deliver a copy of the CD to the Consumer and include it in the Closing Thread.

The Broker contact and Closing Agent will be included on the Closing Thread.

The Broker should follow up with the Consumer to make sure they have acknowledged the CD at least 3 PBD days before closing.

All rescindable transactions (most refinances) require any non-borrowing title holder(s) to acknowledge receipt of the CD 3 PBD prior to closing.

The Seller’s CD will be completed by the Closing Agent.

A CD may be prepared prior to a CTC as long as all credit conditions are satisfied.

27

Wholesale TRID Procedures

Closing Threads

The Loan Officer is now included in our Closing Threads. You will need to set up an account once you receive the first Closing Thread. Then you will have a User ID and Password going forward. Below are examples of Closing Threads:

28

Wholesale TRID Procedures

29

Wholesale TRID Procedures

AUS Run Requests

When requesting an AUS run (DU, LP or GUS) you must:

● Register the loan ● Upload the 1003, credit and Consumer's authorization to “_AUS Run Requests”

● Then email [email protected] and let us know the docs are there to be reviewed and AUS to be run. DO NOT Submit Loan to Lender

If the loan is truly a TBD, please make sure the street address is listed as TBD. If an address, mock or otherwise, is in our system, that will trigger MMC to contact you so we can disclose.

30

Wholesale TRID Procedures

Disclosures no longer required

The Servicing Transfer Disclosure and the ECOA Appraisal Disclosure are no longer required. They are now combined within the LE.

When can I order my appraisal?

The Consumer may pay for the appraisal as soon as the MMC Intent to Proceed is signed. If the Loan Officer would like to pay for the appraisal and be reimbursed by the Consumer at closing, the appraisal may be ordered at any time.

FHA Case Number Requests

FHA Case numbers can be requested only after the application has been signed by the LO and the Consumer.

31

Wholesale TRID Procedures

Miscellaneous Information

● Keep turn times in mind when reviewing time frames. Conditions are reviewed in 48

hours so all conditions to clear the loan should be in 10 business days prior to closing

● Conditions received after 4:00 pm go in the next business day

● Flood insurance is combined with Homeowner's Insurance on the LE in Section G

● Make sure to follow our 2015 Lender X Appraisal Fee guide when disclosing

Conventional, FHA and RD (Exh. E). When disclosing VA appraisal fees, refer to the

Cleveland VA Appraisal Fee List

● Any non-borrowing title holders must consent to the CD (not required on the LE)

● For loans that require a Power of Attorney and meet our POA Policy, the POA must be

approved at least 7 SBD prior to closing

● The POA cannot acknowledge receipt of the CD, but may sign the CD at closing

● All Closing Agents must be approved with MMC prior to selecting the Service Provider.

Closing Agent firms are approved based on location

● Check our website at www.mmcitpo.com under “TRID Central”

32

Wholesale TRID Procedures

Exhibit A. pg 1

33

Wholesale TRID Procedures

Exhibit A. pg 2

34

Wholesale TRID Procedures

Exhibit B. pg 1

35

Wholesale TRID Procedures

Exhibit B pg 2

36

Wholesale TRID Procedures

Exhibit C pg 3

37

Wholesale TRID Procedures

Exhibit C pg 1

38

Wholesale TRID Procedures

Exhibit C pg 2

39

Wholesale TRID Procedures

Exhibit D pg 1

40

Wholesale TRID Procedures

Exhibit D pg 2

41

Wholesale TRID Procedures

Exhibit E

42

Wholesale TRID Procedures

Exhibit F

43