whither goest calpers? - csmfo · whither goest calpers? csmfo annual conference . richard...

TRANSCRIPT

Whither Goest CalPERS? CSMFO Annual Conference

Richard Costigan, Board Member

Marcie Frost, CEO Scott Terando, Chief Actuary

February 8, 2017

2

WELCOME

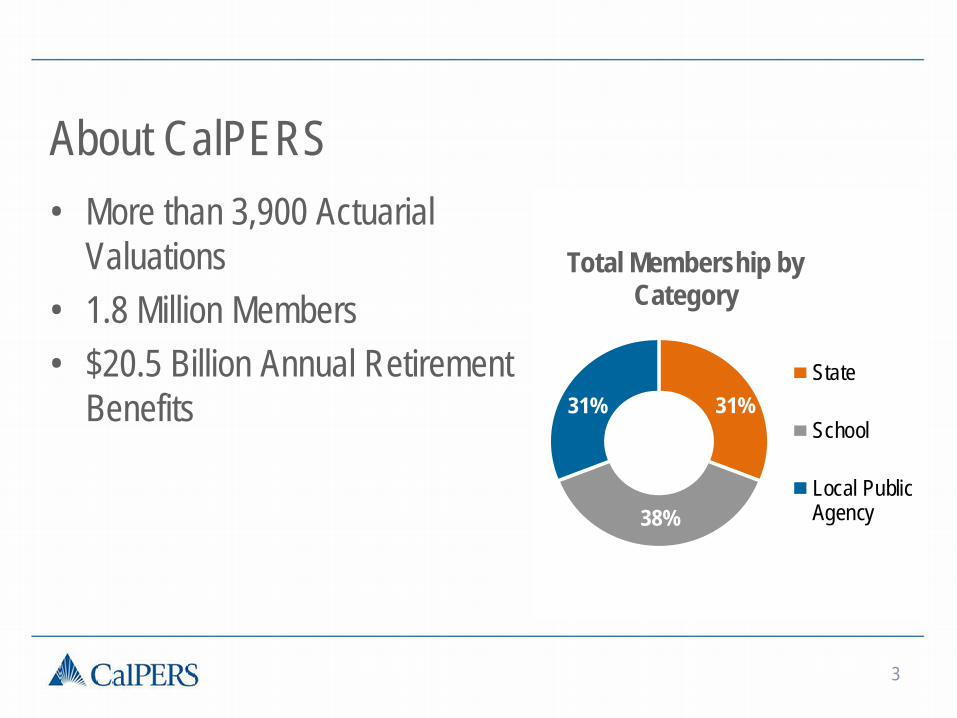

About CalPERS • More than 3,900 Actuarial

Valuations • 1.8 Million Members • $20.5 Billion Annual Retirement

Benefits

3

Total Membership by Category

State

School

Local PublicAgency

31%

38%

31%

Financial Highlights

4

$300 B

.61% 5.1%

ASSETS UNDER MANAGEMENT

7.03% 2015/16 PORTFOLIO

RETURN 10 – YR ANNUALIZED

RETURN 20 – YR ANNUALIZED

RETURN

5

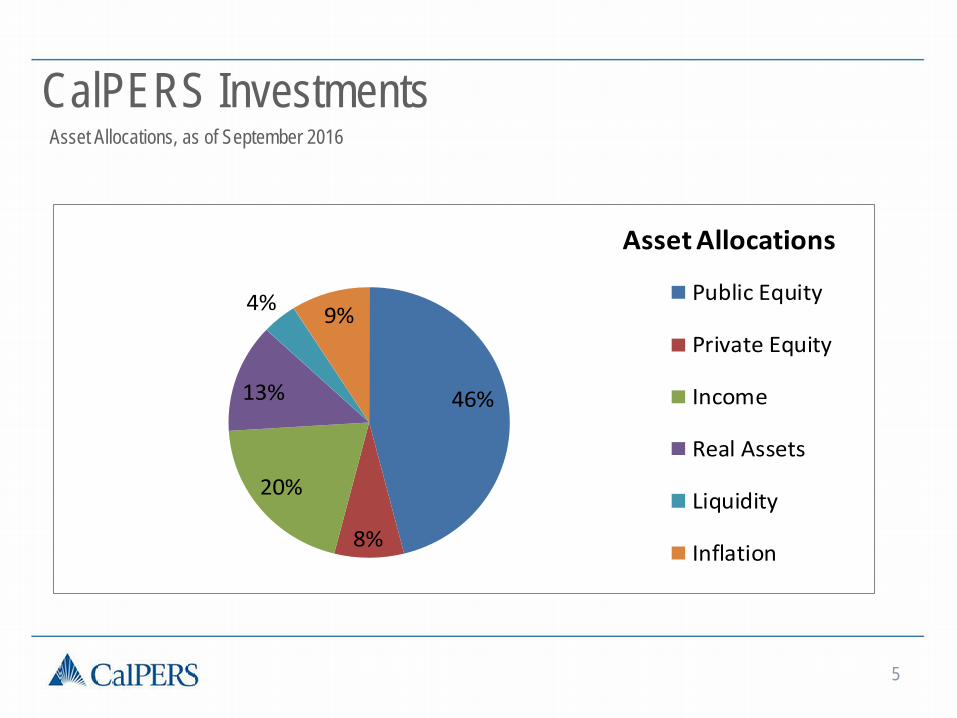

46%

8%

20%

13%

4% 9%

Asset Allocations

Public Equity

Private Equity

Income

Real Assets

Liquidity

Inflation

Asset Allocations, as of September 2016

CalPERS Investments

6

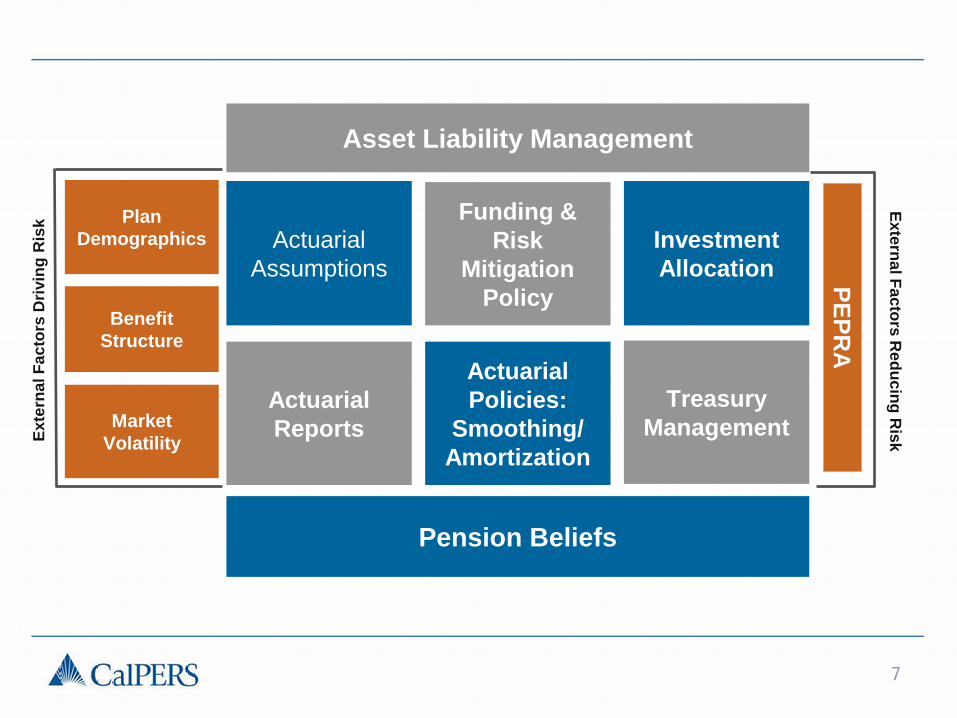

ASSET LIABILITY MANAGEMENT

7

Actuarial Reports

Actuarial Policies:

Smoothing/ Amortization

Asset Liability Management

Pension Beliefs

Funding & Risk

Mitigation Policy

Treasury Management

Actuarial Assumptions

Investment Allocation

Plan Demographics

Benefit Structure

Market Volatility Ex

tern

al F

acto

rs D

rivin

g R

isk

External Factors Reducing R

isk

PEPRA

8

WHAT IS DRIVING RISK?

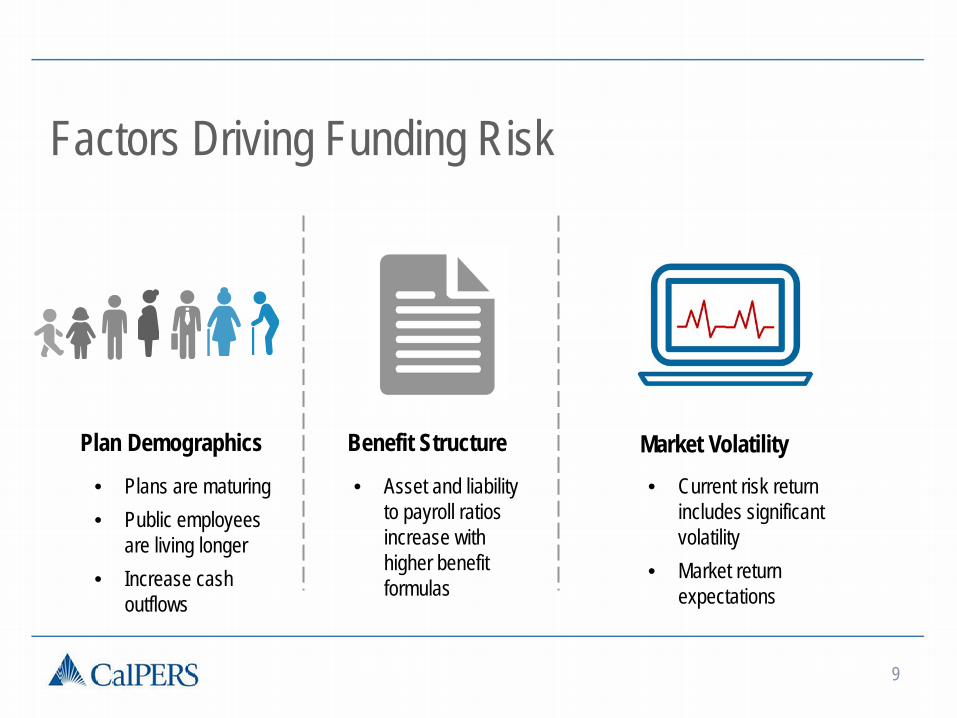

Factors Driving Funding Risk

9

Plan Demographics Benefit Structure Market Volatility • Current risk return

includes significant volatility

• Market return expectations

• Asset and liability to payroll ratios increase with higher benefit formulas

• Plans are maturing • Public employees

are living longer • Increase cash

outflows

10

PLAN DEMOGRAPHICS

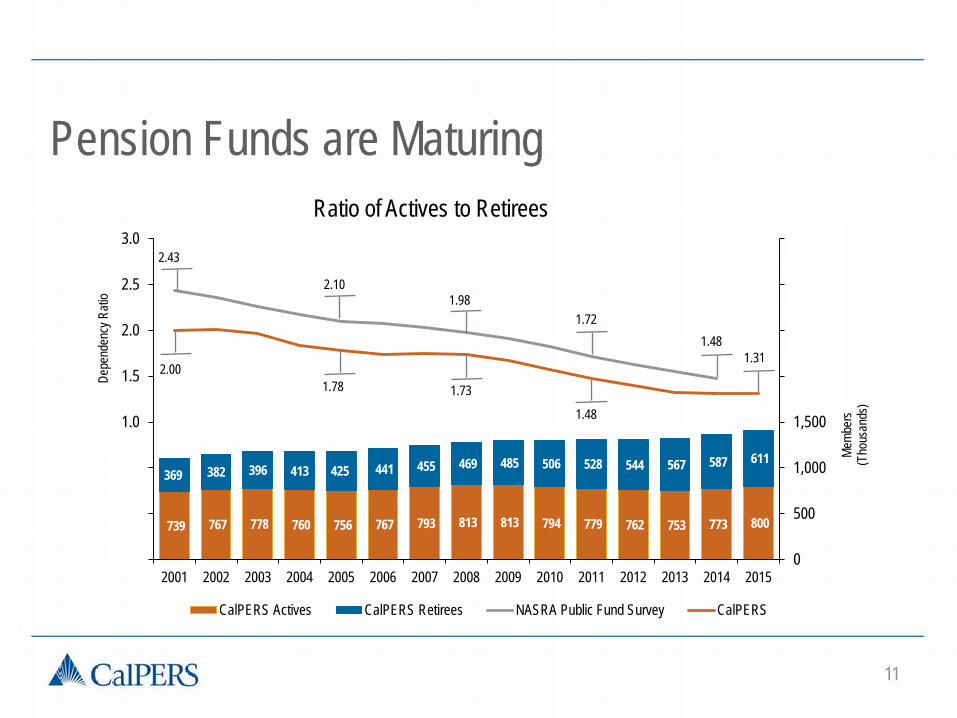

Pension Funds are Maturing

11

739 767 778 760 756 767 793 813 813 794 779 762 753 773 800

369 382 396 413 425 441 455 469 485 506 528 544 567 587 611

2.43

2.10 1.98

1.72 1.48

2.00 1.78 1.73

1.48

1.31

0

500

1,000

1,500

2,000

2,500

3,000

3,500

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Memb

ers

(Tho

usan

ds)

Depe

nden

cy R

atio

Ratio of Actives to Retirees

CalPERS Actives CalPERS Retirees NASRA Public Fund Survey CalPERS

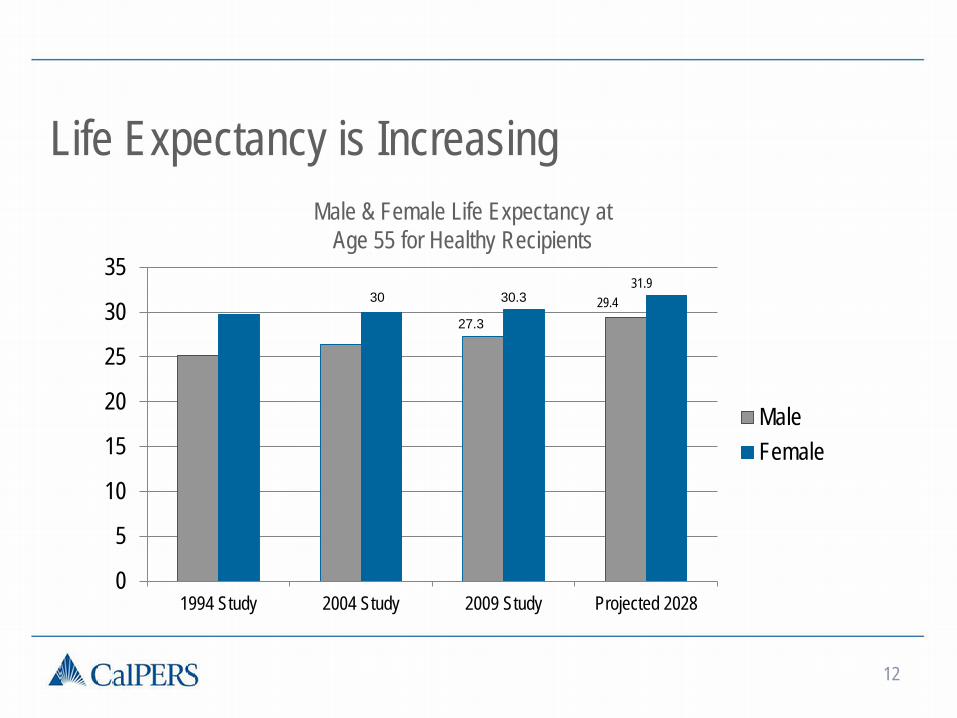

Life Expectancy is Increasing

12

0

5

10

15

20

25

30

35

1994 Study 2004 Study 2009 Study Projected 2028

MaleFemale

30

27.3

30.3 29.4 31.9

Male & Female Life Expectancy at Age 55 for Healthy Recipients

Plan Demographics Mitigation • Actuarial Experience Study • Change in Actuarial Assumptions • Funding Level & Risk Report

13

14

BENEFIT STRUCTURE

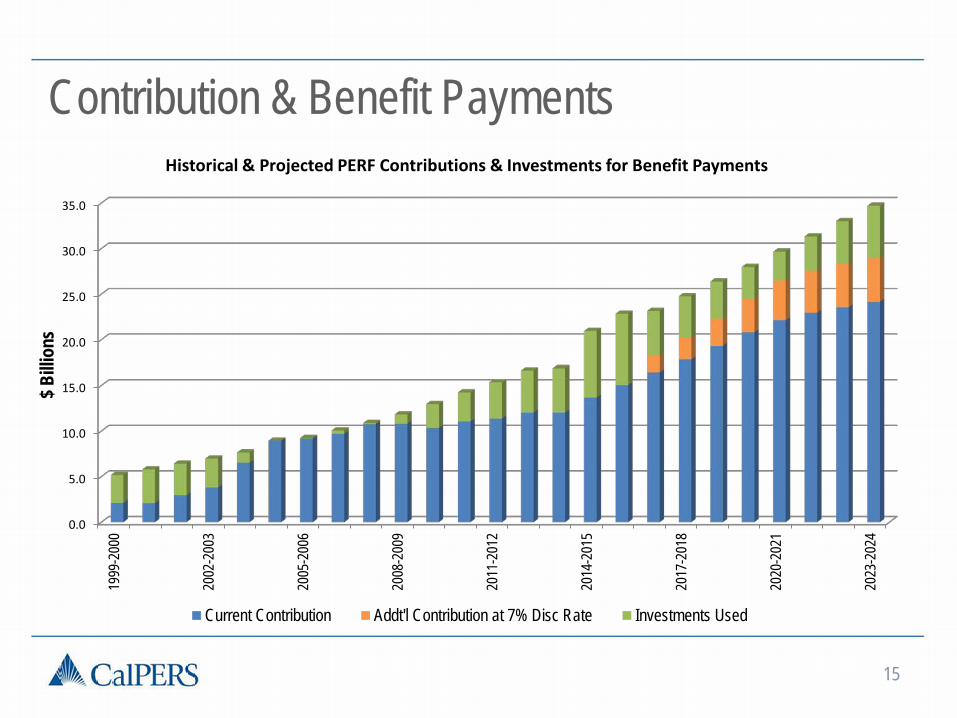

Contribution & Benefit Payments

15

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

1999

-200

0

2002

-200

3

2005

-200

6

2008

-200

9

2011

-201

2

2014

-201

5

2017

-201

8

2020

-202

1

2023

-202

4

$ Billi

ons

Historical & Projected PERF Contributions & Investments for Benefit Payments

Current Contribution Addt'l Contribution at 7% Disc Rate Investments Used

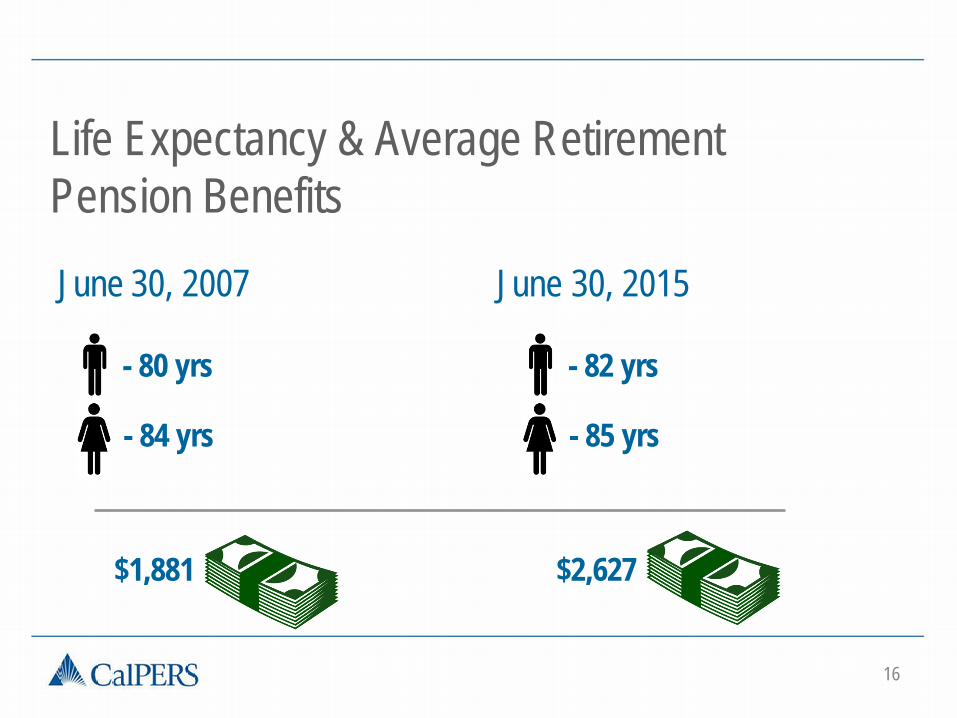

Life Expectancy & Average Retirement Pension Benefits

June 30, 2007 June 30, 2015

16

- 80 yrs

- 84 yrs

- 82 yrs

- 85 yrs

$1,881

$2,627

Benefit Structure Mitigation • Funding Level & Risk Report • New actuarial policies • Smoothing • Amortization • Treasury Management

17

18

MARKET VOLATILITY

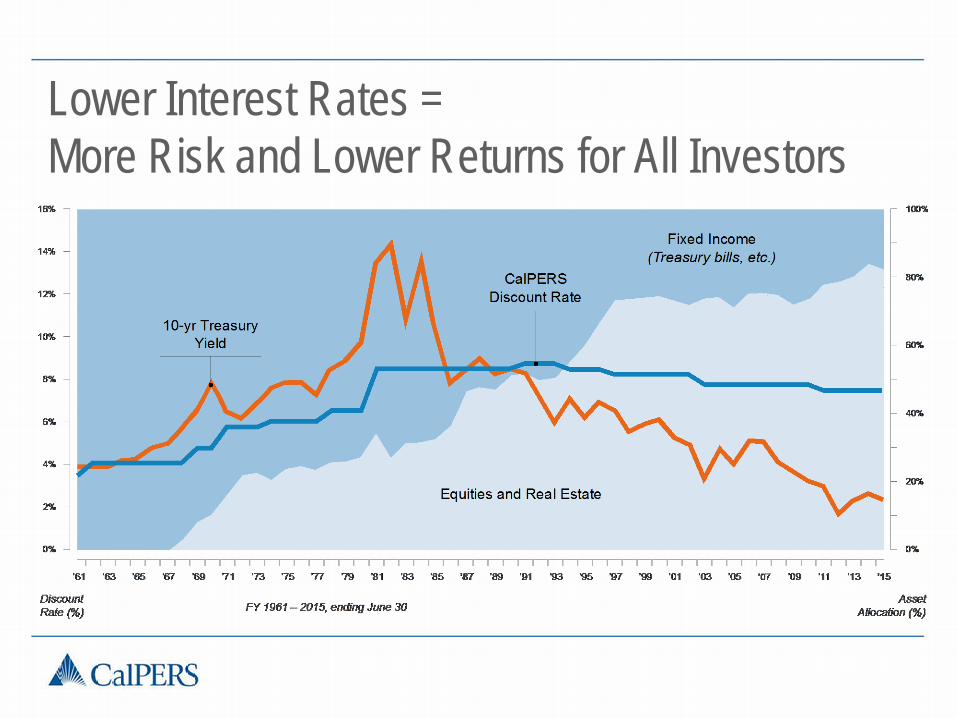

Lower Interest Rates = More Risk and Lower Returns for All Investors

Funded Status & Investment Returns

20

-25

-20

-15

-10

-5

0

5

10

15

20

25

0

20

40

60

80

100

120

05 06 07 08 09 10 11 12 13 14 15 16

Investment Returns Funded Status

Fiscal Year Ending June 30

Investment R

eturns by %

Fund

ed S

tatu

s by

%

Market Volatility Mitigation

• Actuarial Valuation Report • Investment Allocation • New Actuarial Policies: Smoothing/ Amortization • Funding Risk Mitigation Policy

21

22

WHY A DISCOUNT RATE CHANGE NOW?

Why a Discount Rate Change Now? • ALM cycle requires us to recognize changing conditions • Market conditions have changed • Seeing more uncertainty in the forecast • Next 10 years are consequential • To close the cash flow funding gap • Risks in system continue to grow

24

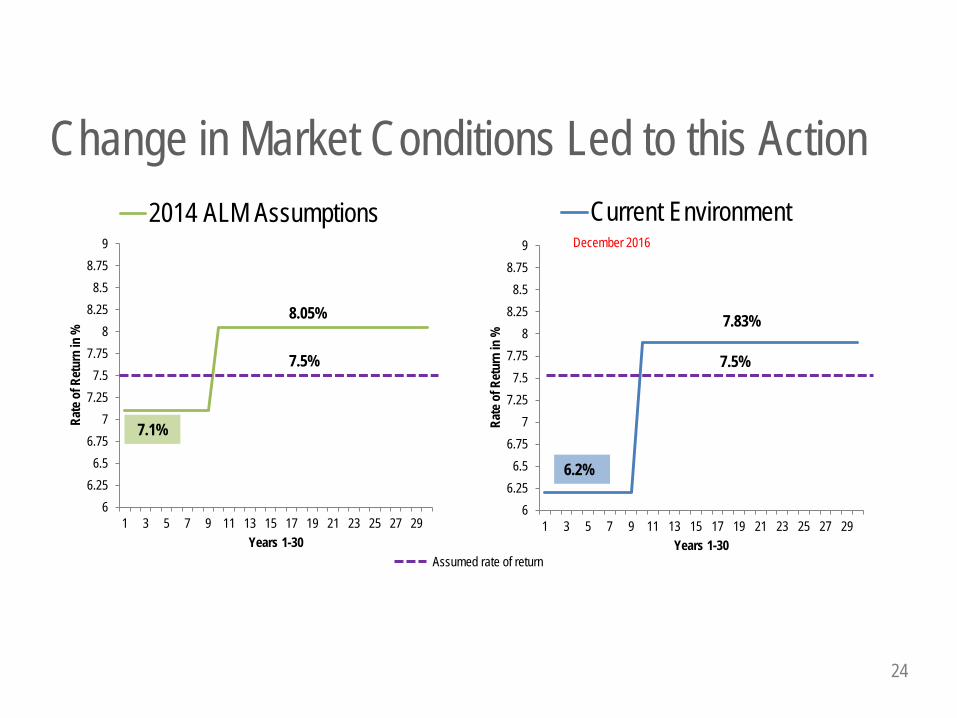

Change in Market Conditions Led to this Action

66.25

6.56.75

77.25

7.57.75

88.25

8.58.75

9

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Rate

of R

etur

n in

%

Years 1-30

2014 ALM Assumptions

8.05%

7.5%

66.25

6.56.75

77.25

7.57.75

88.25

8.58.75

9

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Rate

of R

etur

n in

%

Years 1-30

Current Environment

7.83%

7.5%

Assumed rate of return

6.2%

7.1%

December 2016

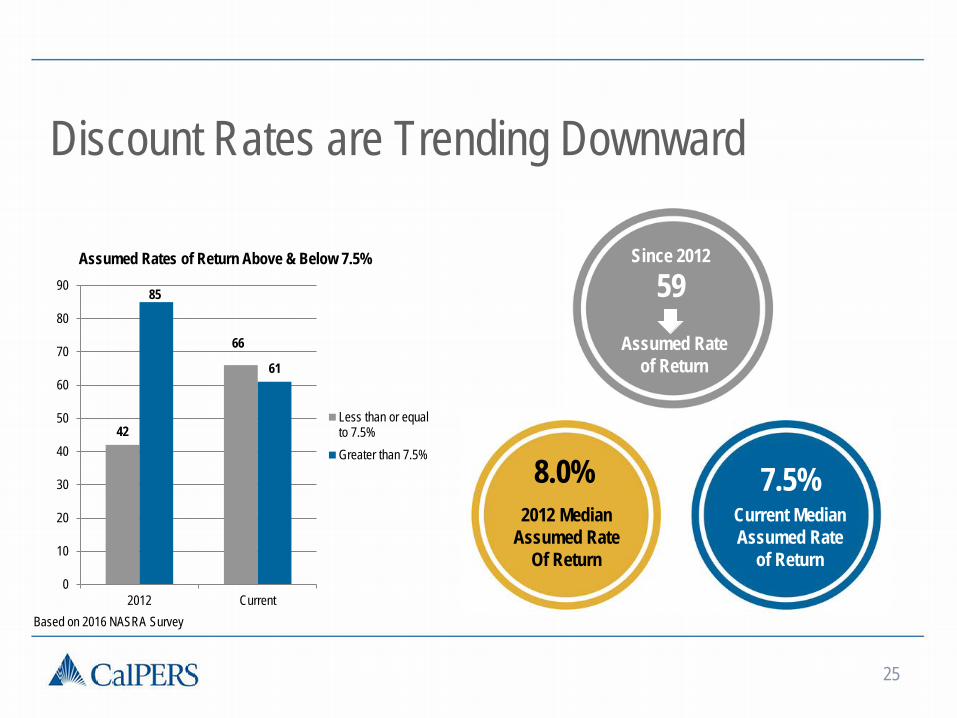

Discount Rates are Trending Downward

42

66

85

61

0

10

20

30

40

50

60

70

80

90

2012 Current

Less than or equalto 7.5%Greater than 7.5%

25

Assumed Rates of Return Above & Below 7.5%

7.5% Median

Discount Rate

Based on 2016 NASRA Survey

59 Assumed Rate

of Return

Since 2012

8.0% 2012 Median

Assumed Rate Of Return

7.5% Current Median Assumed Rate

of Return

• Market conditions have changed • Seeing more uncertainty in the forecast • Next 10 years are consequential • To close the cash flow funding gap • Risks in system continue to grow

26

Other Driving Factors

27

WHAT DID THE BOARD ADOPT AND HOW WILL IT BE

IMPLEMENTED?

28

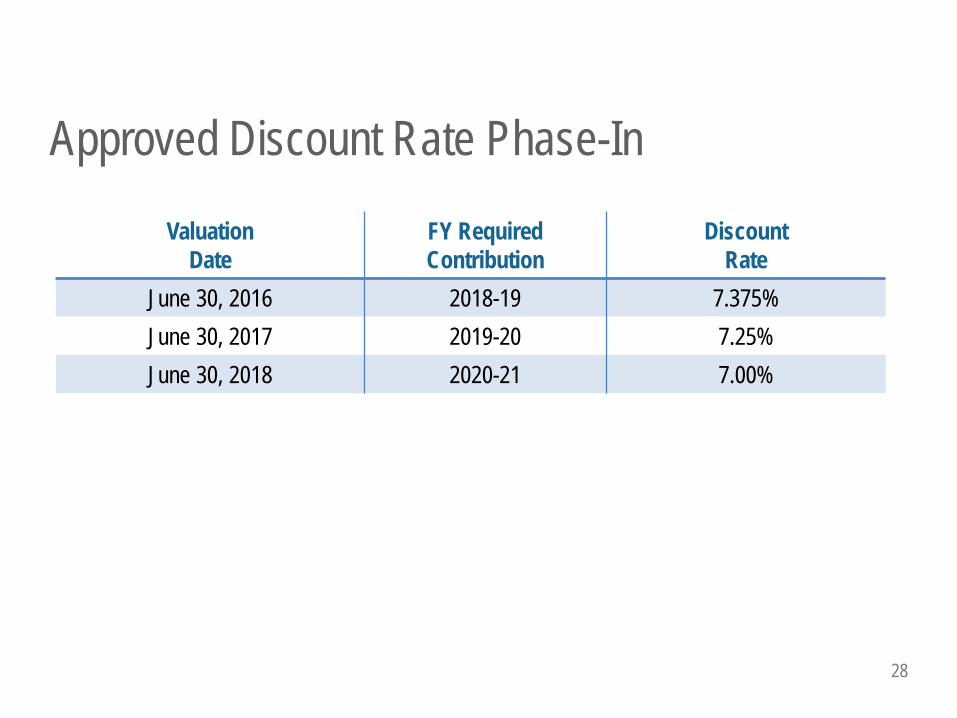

Approved Discount Rate Phase-In

Valuation Date

FY Required Contribution

Discount Rate

June 30, 2016 2018-19 7.375% June 30, 2017 2019-20 7.25% June 30, 2018 2020-21 7.00%

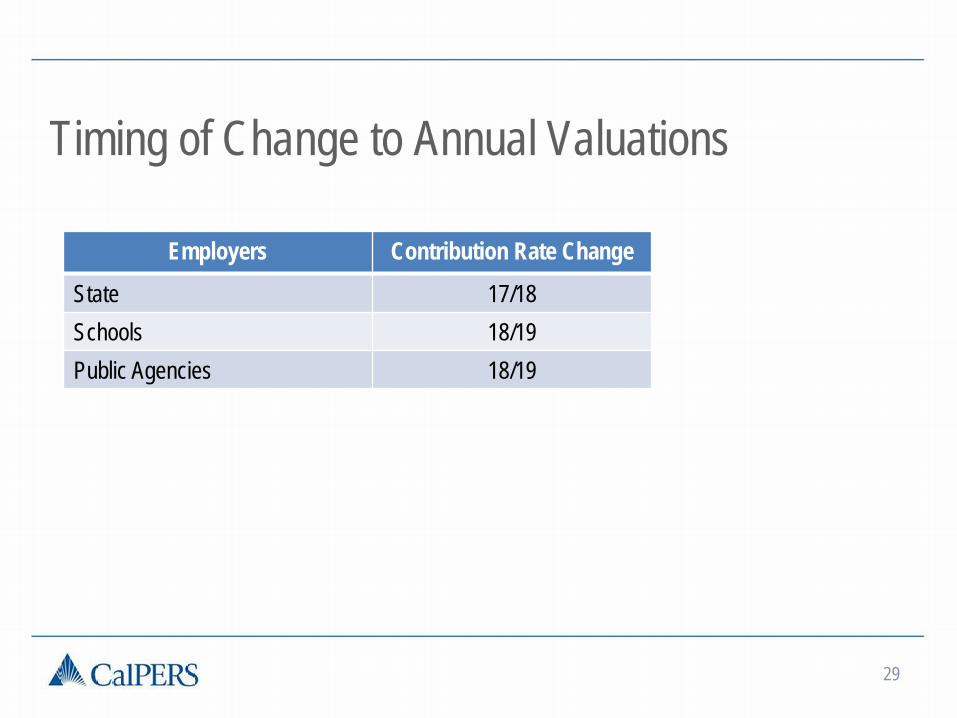

Timing of Change to Annual Valuations

29

Employers Contribution Rate Change

State 17/18 Schools 18/19 Public Agencies 18/19

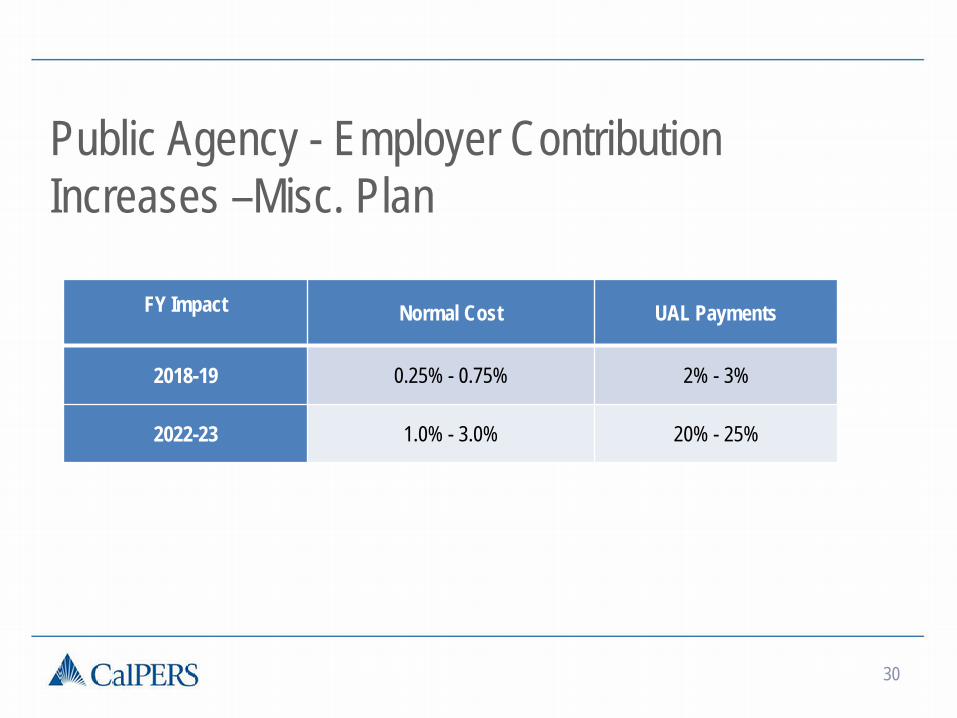

Public Agency - Employer Contribution Increases –Misc. Plan

FY Impact Normal Cost UAL Payments

2018-19 0.25% - 0.75% 2% - 3%

2022-23 1.0% - 3.0% 20% - 25%

30

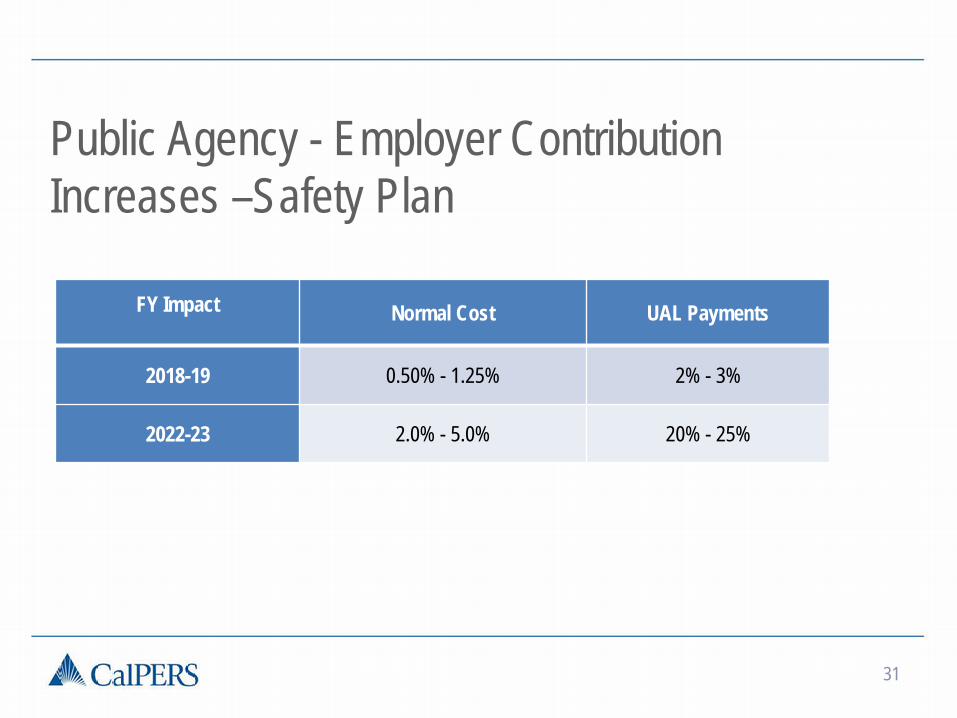

Public Agency - Employer Contribution Increases –Safety Plan

31

FY Impact Normal Cost UAL Payments

2018-19 0.50% - 1.25% 2% - 3%

2022-23 2.0% - 5.0% 20% - 25%

Benefits of Reducing the Discount Rate • Strengthens long-term sustainability of the fund to pay

promised benefits • Reduces negative cash flow; additional contributions will

help to offset growing pension payments • Reduces the long-term chances of falling below a 50%

or 60% funded status that would weaken the sustainability of the fund

• Reduces the risk of contribution increases in the future from volatile investment markets

33

LOOKING AHEAD

Next Steps • Public Agency valuations distributed in July 2017 • Begin Asset Liability Management cycle of reviews

- Asset allocation - Capital market assumptions - Experience study

• Reconsider discount rate in February 2018