what investors need to know about technology and … · source: dnv gl, ourworldindata.org, vaclav...

TRANSCRIPT

Proprietary information – not for distribution beyond intended recipient.

What Investors Need to Know About Technology and Climate Change: The Race of Our Lives April 11, 2018

1 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Presenter

Jeremy Grantham

Mr. Grantham co-founded GMO in 1977 and is a member of GMO’s Asset Allocation team, serving as the firm’s chief investment strategist. He is a member of the GMO Board of Directors and has also served on the investment boards of several non-profit organizations. Prior to GMO’s founding, Mr. Grantham was co-founder of Batterymarch Financial Management in 1969 where he recommended commercial indexing in 1971, one of several claims to being first. He began his investment career as an economist with Royal Dutch Shell. Mr. Grantham earned his undergraduate degree from the University of Sheffield (U.K.) and an M.B.A. from Harvard Business School. He is a member of the Academy of Arts and Sciences, holds a CBE from the UK and is a recipient of the Carnegie Medal for Philanthropy.

The Race of Our Lives:

Climate Change Accelerates

3 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Global Greenhouse Gas Oscillates… Until… Historical CO2 Levels

Proxy (Indirect) Measurements

Source: Reconstruction from ice cores Credit: NOAA

4 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Surface Temperatures: Not Just Rising but Accelerating

-1

-0.5

0

0.5

1

1.5

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010

Tem

pera

ture

Ano

mal

y (°

C)

1958

+.007°C per year

+.025°C per year from peak to peak

+.015 °C per year

As of 8/31/16 Source: NASA Goddard Institute for Space Studies

5 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Ocean Temperatures Also Accelerating

Source: “Improved Estimates of Ocean Heat Content from 1960 to 2015”, Cheng et al, Science Advances

Ocean Heat Content (in Joules)

0 – 2000 M 1950 – 1990 = 37 units/year 1990 – 2016 = 99 units/year

6 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

With Consequences!

7 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

0

100

200

300

400

500

600

1950-1983 1984-2017

Num

ber o

f Dro

ught

s

0

100

200

300

400

1950-1983 1984-2017

Num

ber o

f Wild

fires

0

500

1,000

1,500

2,000

2,500

3,000

1950-1966 1967-1983 1984-2000 2001-2017

Num

ber o

f Flo

ods

Serious, Widespread Consequences Global extreme weather events have been on the rise

Floods Droughts

Wildfires Extreme Temperature Events

Source: HSBC 0

100

200

300

400

500

1950-1972 1973-1995 1996-2017

Num

ber o

f Eve

nts

Climate Change:

But Greener Technologies Also Accelerate

Resulting in De-Carbonizing the Economy

9 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

From the Horse’s Mouth

“Without incentives, wind is going to be a $0.02 or $0.03 product early in the next decade. Battery storage will be $0.01 on top of that. And when you look at (...) coal and nuclear, today, operating costs are around $0.03. New wind and new solar, without incentives and combined with storage, are going to be cheaper than the operating cost of coal and nuclear in the next decade. That is going to totally transform this industry.

— James Robo, 06/22/2017

CEO of NextEra Energy

Alternative energy will crush fossil fuels – on cost!

10 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Hot Off the Press: Renewable Energy Proposals for Excel Corporation Colorado

■ 350 Proposals for wind and solar, both with battery storage for 2023

■ Median price $21/MWH for wind plus storage $36 for solar plus storage

■ Storage bids $3 – $7 down from $15/MWH for Arizona Utility in May 2017

11 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

As Costs Continue to Drop for Wind and Solar, We Have Reached an Inflection Point When this exhibit was first done, the title said “Will Reach”

As of 12/31/16 Source: Lazard, SNL 2017, as cited by Carbon Tracker Initiative, No Country for Coal Gen (2017)

$/M

Wh

(Log

Sca

le)

$400

$100

$50

Unsubsidized Levelized Cost of Energy over Time

Onshore Wind

Utility Scale Solar

Coal

12 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

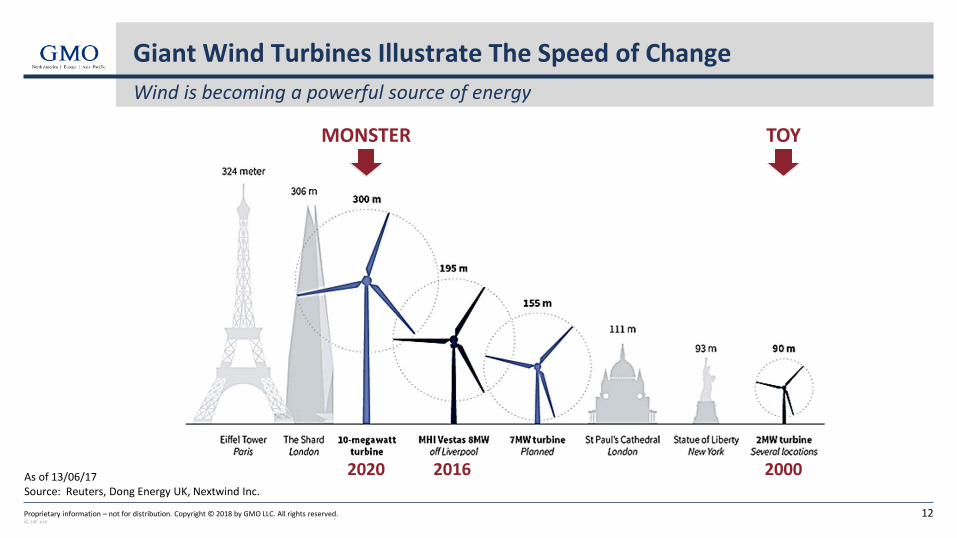

Giant Wind Turbines Illustrate The Speed of Change Wind is becoming a powerful source of energy

As of 13/06/17 Source: Reuters, Dong Energy UK, Nextwind Inc.

2020 2016 2000

TOY MONSTER

13 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

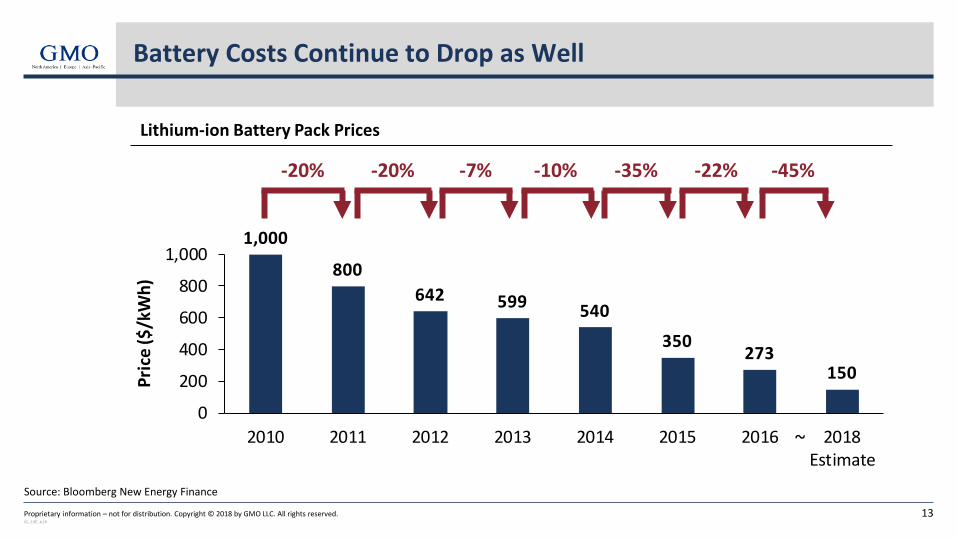

Battery Costs Continue to Drop as Well

Source: Bloomberg New Energy Finance

Lithium-ion Battery Pack Prices

-20% -20% -7% -10% -35% -22%

1,000

800642 599 540

350273

150

0

200

400

600

800

1,000

2010 2011 2012 2013 2014 2015 2016 2018Estimate

Pric

e ($

/kW

h)-45%

~

14 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Energy to Peak, Renewables to Grow... But fossil fuels still 50% by 2050

As of 09/30/17 Data from 2010-2050 is estimated or forecast Source: DNV GL, OurWorldInData.org, Vaclav Smil

World Annual Primary Energy Consumption by Source (1800-2010)

Coal

15 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

But Climate Change Will Not Have Been Stopped

As of 09/30/17 Data from 2015-2050 is estimated or forecast Source: DNV GL, OurWorldInData.org, Vaclav Smil, Carbon Dioxide Information Analysis Centre

Annual Energy Supplied by Fossil Fuels, and Cumulative Total Human CO2 Emissions

16 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Prepare Yourselves: 2°C, Here We Come!

As of 09/30/17 Data from 2016-2050 is estimated or forecast Source: DNV GL, National Oceanic and Atmospheric Administration

Atmospheric CO2 Concentration and Temperature Increase since Pre-Industrial Era

1.9°C

17 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

0

500

1000

1500

2000

2500

2015 2020 2025 2030 2035 2040 2045 2050

Billi

ons o

f 201

5 U

SD

Portfolios Must Prepare For Change Too (The biggest transformation since the introduction of oil)

As of 09/30/17 Data from 2015-2050 is estimated or forecast Source: DNV GL

Annual Global Renewable Energy Capex (billions of 2015 USD)

2.1 Trillion

300 Billion

Climate Change: But Now the Terrible News, Feeding the 12 Billion

The impact on food sufficiency of: – population growth (plus increasing wealth) – climate change – soil erosion (and many related factors)

19 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

World Population Projections: 2000-2100

0

2,000,000,000

4,000,000,000

6,000,000,000

8,000,000,000

10,000,000,000

12,000,000,000

14,000,000,000

16,000,000,000

18,000,000,000

1500 1575 1650 1725 1800 1875 1950 2025 2100

Actual Low Projection Mid Projection High Projection

1798: Malthus publishes Essay on the Principle of Population

1938: I was born

X Y

1500 As of 1/25/18 Source: UN World Population Prospects

20 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

As of 12/31/12 Source: World Bank, Centers for Disease Control and Prevention

Our Last Best Hope: Fertility Rates Drop Beyond the wildest dreams of Malthus

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1961 1971 1981 1991 2001 2011

Ferti

lity

Rat

e, C

hild

ren

/ Wom

an

Low Birthrates in the "Western World"

United StatesFrance

GermanyItaly

United KingdomCanada

21 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Fertility Rates Also Drop for Many Poorer Countries

As of 12/31/12 Source: World Bank

Declines in Emerging Countries

Iran Bangladesh

Egypt

India Morocco

Malaysia

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1961 1971 1981 1991 2001 2011

Fert

ility

Rat

e, C

hild

ren

/ W

oman

22 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

African Population: The Real Population Problem (in the higher UN estimate for 2100)

As of 09/30/17 Source: United Nations World Population Prospects

World Population

Africa Nigeria The Rest of the World

2015 Population: 7.4 Billion 2050 Population: 9.8 Billion 2100 Population: 11.2 Billion

Total increase in population: 3.8 Bn

0.5 Bn 0.6 Bn 3.3 Bn Of which:

23 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

0

5

10

15

20

25

1961 1970 1979 1988 1997 2006 2015

Trill

ion

kcal

/ d

ay

Total World Food Demand Trillions of kilocalories daily

As of Dec 2016 Source: FAOSTAT

24 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

(projection*)

10-Year Average Annual Growth In Crop Yields

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1971 1976 1981 1986 1991 1996 2001 2006 2011

3.5%

1.0%

1971 2006

10-Year Average Growth in Crop Yields

10-Year Average Growth in Population

As of 9/17/12 Source: Food and Agriculture Organization of the United Nations, GMO * 2011 crop yields is a projection; population data is actual.

25 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Growth in Very Best Yielding Crops Slow Towards Zero Crop Yields (5-Year Moving Average)

As of 12/31/13 Source: UN Food and Agriculture Organization

40,000

45,000

50,000

55,000

60,000

65,000

70,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006

Rice Yields, Hg/Ha

Whe

at Y

ield

s, Hg

/Ha

France (Wheat - Left Axis)

Germany (Wheat - left axis)

United Kingdom (Wheat - left axis)

Japan (Rice - right axis)

26 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

-

2

4

6

8

10

12

1961 1966 1971 1976 1981 1986 1991 1996 2001 2006 2011

Fertilizer Use Starts to Max Out Tons of fertilizer used annually

As of 12/31/12 Source: Food and Agriculture Organization of the United Nations

10

1961

5X

27 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1930-1950 1950-1970 1970-1990 1990-2010 2010-2030 (GMOprojection)

Aver

age

Annu

al Y

ield

Gro

wth

Grain Productivity Shows Diminishing Returns

-1.7%

-0.5% -0.25%

Green Revolution

Average Annual Agricultural Productivity Growth in the United States, by 20-year block Average of yield growth for corn, wheat and rice

As of Jan 2018 Source: USDA NASS

28 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Effect of Erosion on Grain Production

U.S. Grain Yields, Historical and Projected Index averaging corn, wheat, soy and rice yields, 2017 = 1

-10%

As of Jan 2018 Source: USDA NASS; “Soil Erosion, Climate Change and Global Food Security: Challenges and Strategies”, Rhodes, Science Progress, 2014; GMO

0.0

0.5

1.0

1.5

1970 1980 1990 2000 2010 2020 2030 2040

Historic Data

Projection only of historic productivity advances

Projection including effect of soil erosion (Rhodes 2014)

Projection including effect of increased flooding on soil erosion*

29 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Image Source: Iowa Public Radio “The Greatest Story Never Told”, installation in Adair County, Iowa, by David B. Dahlquist and RDG Planning & Design.

Soil Depth in Iowa Has Halved Since Intensive Cultivation Began in 1850

14”

11.5”

9.5” 7”

5.5”

1850 1900 1950 1975 2000

30 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Effect of Climate Change on Grain Production

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1970 1980 1990 2000 2010 2020 2030 2040

Historic Data

Projection only of historic productivity advances

Projection including effect of climate change (Liang et al 2017)

U.S. Grain Yields, Historical and Projected Index averaging corn, wheat, soy and rice yields, 2017 = 1

-47%

As of Jan 2018 Source: USDA NASS; “Determining Climate Effects on US Total Agricultural Productivity”, Liang et al, Proceedings of the National Academy of Sciences; GMO

31 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Combined Effect Climate Change & Soil Erosion

As of Jan 2018 Source: USDA NASS, Rhodes 2014, Liang et al 2017, GMO

U.S. Grain Yields, Historical and Projected Index averaging corn, wheat, soy and rice yields, 2017 = 1

-56%

0.0

0.5

1.0

1.5

1970 1980 1990 2000 2010 2020 2030 2040

Historic DataProjection only of historic productivity advancesProjection including diminishing productivity advancesProjection including impact of soil erosionProjection including erosion / flooding interactionProjection including erosion accelerated by climate changeProjection including effect of climate changeProjection including adaptation to climate change

-38%

32 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Other Problems Facing “Big Ag”

■ Water availability

■ Urban expansion

■ Bug and pathogen immunity

■ Toxic environment

−75% loss of flying insects

■ Global distribution of phosphate reserves

33 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Phosphate Distribution: A Nearly Certain Crisis There are no substitutes for phosphorous in agriculture

As of 12/31/10 Source: USGS

Production (2010) ReservesMorocco and Western Sahara 26.0 50,000

World 176.0 65,000

Annual Production and Reserves (millions of metric tons)

Climate Change: Problems with Capitalism

The Sixth Great Extinction

Toxicity affecting humans also: over 50% loss of sperm count in developed world

Complete inability of capitalism to deal with externalities, tragedies of the commons, and the very long-term

The Devil and the Farmer

35 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

The Devil’s Deal: Your Soil & Your Soul! Three times more profit now in exchange for 1% per year soil erosion over 100 years (i.e. complete)

Profits per year under deal and no deal

As of Jan 2018 Source: GMO

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

0 10 20 30 40 50 60 70 80 90 100

Annu

al P

rofit

s

Year

"No deal" present value (5% discount rate): $2,000,000

"Deal" present value (5% discount rate): $5,583,000!

36 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Illustrative Climate Change Portfolio (Global Equities)

Segment Exposure

Clean Energy 34.58%Solar 9.92%Wind 5.61%Other Clean Energy 0.95%Clean Power Generation 10.45%Batteries & Storage 7.66%

Smart Grid 5.44%Copper 9.30%Energy Efficiency 20.31%

Transportation 6.25%Buildings 0.32%Diversified Efficiency 7.81%Technology 2.88%Lighting 1.68%Recycling 1.36%

Agriculture 23.18%Farming 5.33%Farm Machinery 2.51%Timber 1.20%Eco-Chemicals/Seeds 2.42%Fertil izer 8.34%Fish Farming 3.38%

Water 4.93%Cash 2.25%

And Finally the Peril of Divestment!

38 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Sep-90 Mar-95 Sep-99 Mar-04 Sep-08 Mar-13 Sep-17

9.44% 9.54% 9.56% 9.66% 9.71% 9.74% 9.75% 9.77% 9.84% 9.90% 9.94%

0%

4%

8%

12%

Ex Health Care Ex ConsumerStaples

Ex IT Ex Industrials S&P 500 Ex Energy Ex ConsumerDiscretionary

Ex Utilities Ex Materials Ex Telecom Ex Financials

Yes, You Can Divest From Oil – or Anything Else – Without Much Consequence

Annualized Absolute Returns (Nominal Terms): 1989-2017 – Range: 50 bps

Ex Cons. Discr. Ex Cons. Staples Ex Energy Ex Financials Ex Health Ex Industrials Ex IT Ex Materials Ex Telecom Ex Utilities S&P 500 Ab

solu

te R

etur

ns

(Nom

inal

Ter

ms,

Log

arith

mic

Sca

le)

As of 9/30/17 Source: S&P, GMO

39 JG_LSE_4-18

Proprietary information – not for distribution. Copyright © 2018 by GMO LLC. All rights reserved.

Yes, You Can Divest From Oil – or Anything Else – Without Much Consequence

As of 9/30/17 Source: S&P, GMO Note: Prior to March 1957 the S&P 500 is represented by the S&P 90 Index

10.04% 10.12% 10.18% 10.25% 10.28% 10.28% 10.34% 10.34% 10.34% 10.39% 10.65%

0%

4%

8%

12%

Ex ConsumerStaples

Ex HealthCare

Ex Energy S&P 500 Ex ConsumerDiscretionary

Ex IT Ex Industrials Ex Telecom Ex Utilities Ex Financials Ex Materials

1957-2017 Range: 61bps

11.37% 11.39% 11.44% 11.48% 11.51% 11.51% 11.51% 11.53% 11.54% 11.57% 11.91%

0%

4%

8%

12%

Ex ConsumerStaples

Ex HealthCare

Ex ConsumerDiscretionary

Ex Energy Ex IT Ex Telecom Ex Utilities S&P Index Ex Financials Ex Materials Ex Industrials

1925-2017 Range: 54bps