what airbnb uber and alibaba have in common

DESCRIPTION

ttTRANSCRIPT

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 1 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

STRATEGY

What Airbnb, Uber, andAlibaba Have in Commonby Barry Libert, Yoram (Jerry) Wind, and Megan Beck Fenley

NOVEMBER 20, 2014

When Facebook acquired the messaging service WhatsApp for $19 billion in the spring of

2014, the question on everyone’s mind was, does the service really merit a valuation of

almost 20 times projected revenues?

WhatApp’s valuation may be extreme, but huge gaps between revenues and valuation are

increasingly common. Cloud-based sharing service Dropbox received venture capital

funding at a valuation of $10 billion, or 40 times revenues. Airbnb.com raised funding at a

valuation of $10 billion, which would make it worth nearly 20 times its revenues — and

worth more than Hyatt Hotels or Wyndham Worldwide. Taxi-replacement service Uber is

currently raising funding and is expected to see a valuation of $30 billion, estimated to be

more than 15 times revenues. Most recently, Alibaba’s IPO raised funds at a value

approximately 10 times revenues.

These companies represent a new trend in the types of business that investors prefer.

Leaders of more traditional companies are left wondering why these upstarts merit such

high valuations. Are they more profitable? Do they see faster growth? Do they have higher

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 2 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

return on assets and lower marginal costs?

Our answer is yes — to all of the above.

In collaboration with Deloitte, we examined

40 years of financial data for the S&P 500

companies to see how valuations trends have

evolved along with business models and

emerging technologies. Our research led to

three key findings.

1. There are four business models.

To begin, we searched for a simple way to

characterize the different types of business

that were engaging the hearts and minds, and

pocket books, of investors. Because today’s

highly valued, fast growing businesses can be

found in almost every industry, we quickly

moved past standard industrial classifications

and developed a new framework based on business model, which is the principal way an

organization invests its capital to generate and capture value.

The four models are:

Asset Builders: These companies build, develop, and lease physical assets to make,market, distribute, and sell physical things. Examples include Ford, Wal-Mart, and FedEx.Service Providers: These companies hire employees who provide services to customers or

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 3 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

produce billable hours for which they charge. Examples include United Healthcare,Accenture, and JP Morgan.Technology Creators: These companies develop and sell intellectual property such assoftware, analytics, pharmaceuticals, and biotechnology. Examples include Microsoft,Oracle, and Amgen.Network Orchestrators. These companies create a network of peers in which theparticipants interact and share in the value creation. They may sell products or services,build relationships, share advice, give reviews, collaborate, co-create and more. Examplesinclude eBay, Red Hat, and Visa, Uber, Tripadvisor, and Alibaba.

We applied this business model framework to our dataset, the S&P 500 Index companies

from 1972 to present, in order to see how the four models performed over time. Two

different researchers categorized each company into its dominant business model, giving

consideration to several factors: The company’s description of itself in annual reports; the

revenue generated by different business units; capital allocation patterns such as R&D or

COGS expenditure; and market perceptions including news articles and analyst reports.

Although most companies operate in several business model categories, we assigned to each

company the most advanced business model that it uses for a significant portion of its

business, or that it is making strong efforts to develop. For example, although most of Nike’s

business is manufacturing and selling shoes, which we classify as Asset Building, Nike has

also developed the Nike+ ecosystem, which connects these physical goods to the Internet

where users track activities and share progress with their friends. For this reason, we

classified Nike as a Network Orchestrator.

2. Network Orchestrators create more value.

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 4 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

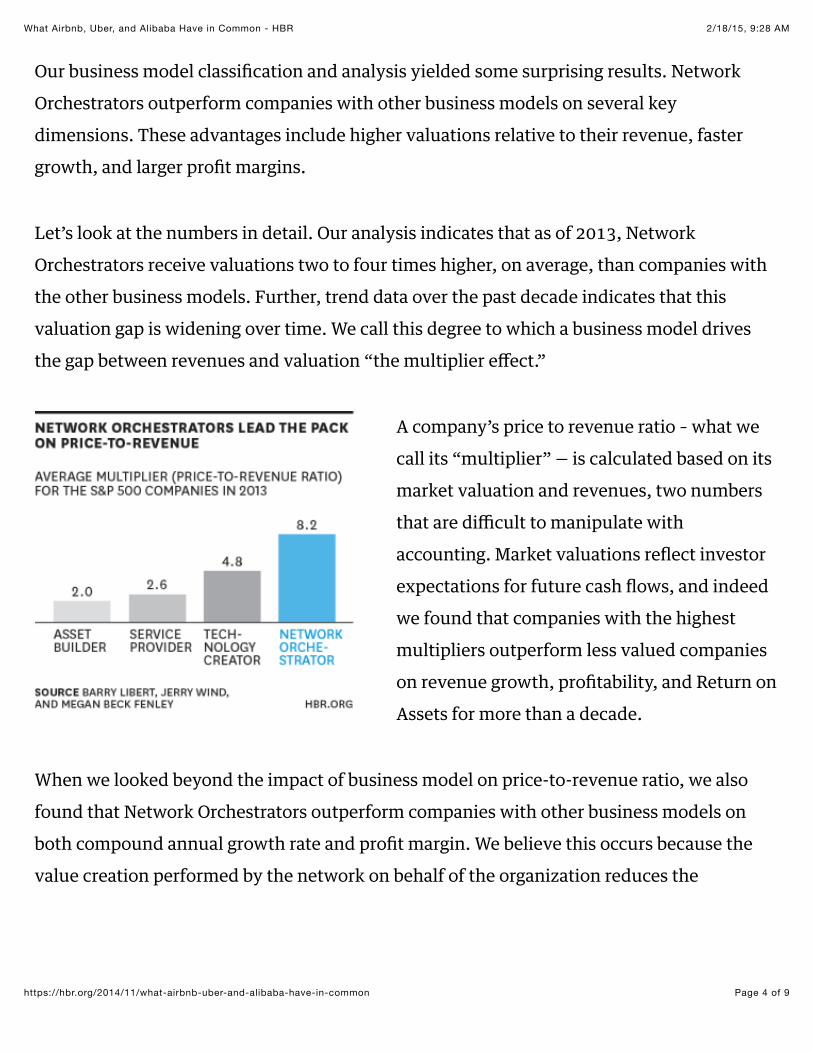

Our business model classification and analysis yielded some surprising results. Network

Orchestrators outperform companies with other business models on several key

dimensions. These advantages include higher valuations relative to their revenue, faster

growth, and larger profit margins.

Let’s look at the numbers in detail. Our analysis indicates that as of 2013, Network

Orchestrators receive valuations two to four times higher, on average, than companies with

the other business models. Further, trend data over the past decade indicates that this

valuation gap is widening over time. We call this degree to which a business model drives

the gap between revenues and valuation “the multiplier effect.”

A company’s price to revenue ratio – what we

call its “multiplier” — is calculated based on its

market valuation and revenues, two numbers

that are difficult to manipulate with

accounting. Market valuations reflect investor

expectations for future cash flows, and indeed

we found that companies with the highest

multipliers outperform less valued companies

on revenue growth, profitability, and Return on

Assets for more than a decade.

When we looked beyond the impact of business model on price-to-revenue ratio, we also

found that Network Orchestrators outperform companies with other business models on

both compound annual growth rate and profit margin. We believe this occurs because the

value creation performed by the network on behalf of the organization reduces the

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 5 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

company’s marginal cost, as described in Jeremy Ri%in’s The Zero Marginal Cost Society. For

example, TripAdvisor.com benefits from its customer’s reviews and AirBnb leverages its

network’s housing assets.

3. Few companies operate as Network Orchestrators.

Fewer than 5% of companies are Network Orchestrators despite the positive impact of this

business model on multiple performance measures. Why? We see several reasons.

First, today’s network-based business models require new technologies and competencies.

Most corporate leaders are skilled at building, owning, and managing their own physical

assets or people. Network Orchestrators, however, rely on intangibles such as knowledge

(Gerson Lehrman Group) or relationships (Facebook), or other people’s assets (Uber) as well

as new “non-management” and “non-ownership” competencies related to facilitating a

network of individuals and their individual assets and relationships.

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 6 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

Second, Generally Accepted Accounting

Principles (GAAP) categorize some assets as

“assets” (plant property and equipment), others

as expenses (people, training, and intellectual

property) and ignores others (customers,

sentiment, and networks) altogether, frequently

resulting in the under-allocation of capital to

intangible assets. This is especially problematic

given that, today, intangible assets make up

approximately 80% of corporate market value.

Third, standard industry designations result in siloed thinking, leaving empty space where

new business models can enter. For example, think back to the early 1990s. Most traditional

retailers were slow to move into the online space because they didn’t consider themselves

“technology companies.” The online market was left open, and in came a slew of new

players such as Amazon, eBay, and Zappos, who gobbled up market share and changed the

retail game. Today, the power of networks is creating a new cross-industry transformation.

Consider what Uber and Lyft are doing to the taxi industry or how Airbnb is affecting the

hotel industry.

Finally, business models are tightly integrated into all parts of a company, and are therefore

daunting to change. Changing business model requires changing capital allocation, but

Research by McKinsey & Company shows that most companies follow the same allocation

patterns year after year, despite dramatic changes in the business environment.

These factors make it difficult for executives and board members to cash in on the value

offered by new business models.

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 7 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

Networks are sources of information, capabilities, and assets that lie in and around every

organization. Most networks, however, lie dormant and untapped. To become a Network

Orchestrator and create more value and better performance, leaders must connect to and

activate their networks, tapping into new sources of value, both tangible (Airbnb’s network

of lodgings) and intangible (the expertise of Apple’s Developer Network). We recommend

that all leaders and boards consider the steps below:

1. Assess your business model. Understand which business models currently exist withinyour organization and also the preferences and biases of the leadership team memberswho have created these models through capital allocation.

2. Inventory your network assets. Take stock of your dormant network assets includingcustomers, employees, partners, suppliers, distributors, and investors, and determinewhich have the greatest potential.

3. Reallocate your capital to networks. Divert at least 5% to 10% of investment capital toactivating your networks. Take an experimental approach to early allocation and expectongoing adaptation. This could be accomplished organically, or through acquisition orpartnership.

4. Add network KPIs. Add to your standard financial metrics new network-orientedindicators such as number of participants, their sentiment, and level of engagement.These KPIs will provide direction for your network adaptation.

The bottom line: begin your evolution today and create the multiplier effect in your own

organization. Activate your dormant networks by reaching out to your customers,

employees, partners, suppliers, employees, and investors and figure out how you can co-

create value with them.

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 8 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

Take this assessement on digitalgrader.com to determine your business model and learn how to

build and leverage your network assets.

Barry Libert is the CEO of OpenMatters, a digital consultancy and angel investor, and

Senior Fellow at the SEI Center at Wharton.

Yoram (Jerry) Wind ([email protected]) is the Lauder Professor and a professor of

marketing at the University of Pennsylvania’s Wharton School in Philadelphia.

Megan Beck Fenley is a digital consultant at OpenMatters and research at the SEI

Center at Wharton.

Related Topics: INNOVATION | BUSINESS MODELS

This article is about STRATEGY

FOLLOW THIS TOPIC

2/18/15, 9:28 AMWhat Airbnb, Uber, and Alibaba Have in Common - HBR

Page 9 of 9https://hbr.org/2014/11/what-airbnb-uber-and-alibaba-have-in-common

Comments

Leave a Comment

P O S T

REPLY 0 0

7 COMMENTS

Niels Trzecieski a month ago

Where would you classify companies that work in businesses comparable to 'Asset Builders' but promost

intangible products - like financial services (banking, insurance)?

POSTING GUIDELINES

We hope the conversations that take place on HBR.org will be energetic, constructive, and thought-provoking. To comment, readers must

sign in or register. And to ensure the quality of the discussion, our moderating team will review all comments and may edit them for clarity,

length, and relevance. Comments that are overly promotional, mean-spirited, or off-topic may be deleted per the moderators' judgment. All

postings become the property of Harvard Business Publishing.

JOIN THE CONVERSATION