welcomes all the participants to the seminar on tds …

TRANSCRIPT

WELCOMES

ALL THE PARTICIPANTS TO

THE SEMINAR ON TDS (TAX DEDUCTED AT SOURCE)

WHAT IS TDS OR TAX DEDUCTED AT SOURCE?

Tax deducted at source (TDS), as the very name implies aims at collection of revenue at the very source of income. It is essentially an indirect method of collecting tax which combines the concepts of “pay as you earn” and “collect as it is being earned.”

•SIGNIFICANCE TO THE GOVERNMENT • it advances the collection of tax, •ensures a regular source of revenue, • provides for a greater reach and wider base for tax.

•AT THE SAME TIME, TO THE TAX PAYER: • provides for a simple and convenient mode of payment.

SIGNIFICANCE OF TDS

TDS CHAIN

DEDUCTION AND REMITTANCE

• Responsibility • It is the responsibility of the deductor to deduct income tax at the time of

payment as per the prevailing rates, remit the same to Govt. account and also to ensure correctness of the details of PAN submitted by the deductee/payee

• Who is the Deductor? • Deductor is the Drawing and Disbursing Officer

Time Limit to deposit the tax deducted at source:

• If the tax is to be paid by challan – 7th of the following month in which deduction was made

/TRANSFER CREDIT

BOOK ADJUSTMENT BANK DEPOSIT

GAR 7 CHALLAN * ITNS 281 CHALLAN

ACCOUNT OFFICE (TREASURY) BANK

CENTRAL BOARD OF DIRECT TAX

INCOME TAX (TDS)

✓Only for Govt. Deductor (Offices) ✓Both Govt. and Non-Govt. office

* Government Account Receipt & Payment Challan -7

TDS Process – Book Adjustment (only for Govt. Deductors)

ENTITY TYPE IDENTIFICATION RETURN TYPE PERIODICITY COMPLAINCE PROOF

ACCOUNTS

OFFICE AIN 24G Monthly BIN Details

TAX PAYEE

DEDUCTORS

PAN

TAN

ITR

24Q / 26Q

Annually

Quarterly

ITR-V

Token &

Receipt Nos.

TDS PAYMENTS – POINTS TO REMEMBER

• Tax is to be deducted at appropriate rates

• PAN of the deductee is to be quoted mandatorily

• TAN is to be quoted all matters relating to TDS such as filing of TDS quarterly returns, challans while making payment of TDS, etc.

TAN (Tax Deduction Account Number)

• Composition of TAN – Example CHEB90468K

• 1st three alphabets denotes place of the TAN holder

• 4th alphabet represents the alphabet with which the name of

the deductor begins

• The five digits represent running serial number

• Every tax deductor to obtain TAN

• Application to obtain TAN no. – FORM 49B

POINTS TO NOTE

• Tax is to be deducted at appropriate rates

• PAN of the deductee is to be quoted mandatorily

• TAN is to be quoted all matters relating to TDS such as filing of TDS quarterly returns, challans while making payment of TDS, etc.

PAYMENTS LIABLE FOR TDS

• SECTION 192 – PAYMENT OF SALARY

• SECTION194C • Payment of car hire charges • Payment of courier charges • Payment of AMC charges for maintenance of

generator/a.c./lift etc.-194C • Payment of charges for security services-194C • Payment of charges for supply of manpower

• SECTION 194H • Payment of Commission / brokerage

PAYMENTS LIABLE FOR TDS

• SECTION 194 I • Payment of rent

• Payment for hiring of equipment such as generator etc.,

• SECTION 194J • Payment of fees to advocates/chartered accountants

• Payment of AMC charges for maintenance of computer/networking hardware/software • Payment towards cash management service

PAYMENTS THAT ARE EXEMPT FROM TDS

GENERAL EXEMPTIONS

• Payments to the following persons are exempt from TDS under Section 196 of the Income Tax Act – ➢Government

➢ RBI ➢Mutual funds ➢ Corporations established under central Law whose income is

exempt

➢In case of those funds or authorities or Boards or bodies, by whatever name called, whose income is unconditionally exempt under section 10 of the Income-tax Act and who are statutorily not required to file return of income as per section 139 of the Income-tax Act, there would be no requirement for tax deduction at source since their income is anyway exempt under the Income-tax Act. ➢Interest paid to banks, cooperative banks, financial institutions

established under the law, LIC, UTI, Insurance companies

FILING OF TDS RETURNS

• TDS Returns can be filed only in electronic form

• Return Preparer Utility (RPU) is made available by NSDL

• Based on RPU softwares are also available in the market for filing e-TDS return. Eg.Compu-TDS, TDS MAN, etc

• File Validation Utility (FVU) file generated from the software / utility is to be submitted to TIN-FC alongwith Verification Form (Form 27A).

FORMS USED FOR FILING TDS RETURNS

– FOR TDS ON SALARY PAYMENTS

– FOR TDS ON NON - SALARY PAYMENTS

– FOR TDS ON IMMOVABLE PROPERTY TRANSACTION

- FOR TDS ON ALL PAYMENTS MADE TO A NON-RESIDENT OTHER THAN SALARY PAYMENT

DUE DATES FOR FILING TDS RETURNS WITH EFFECT FROM 1ST JUNE 2016

S NO QUARTER ENDING ON DUE DATE FOR FILING TDS RETURN

1 30TH JUNEOF THE FINANCIAL YEAR 31ST JULY OF THE FINANCIAL YEAR

2 30TH SEPTEMBER OF THE FINANCIAL YEAR 31ST OCTOBER OF THE FINANCIAL YEAR

3 31ST DECEMBER OF THE FINANCIAL YEAR 31ST JANUARY OF THE FINANCIAL YEAR

31ST MAY OF THE FINANCIAL YEAR IMMEDIATELY FOLLOWING 31ST MARCH OF THE FINANCIAL YEAR

THE FINANCIAL YEAR IN WHICH THE DEDUCTION IS MADE. 4

ISSUE OF CERTIFICATE FOR TDS IN FORM 16 / 16A

• TDS Certificate in Form 16 as well as Form 16A has to be

generated ONLY from the TRACES website of income tax

department (www.tdscpc.gov.in) after filing of e-tds quarterly

statement / return (26Q), and issued to the deductee within

the stipulated time.

• Computerised or typed form 16 / form 16A should not be

issued.

www.tdscpc.gov.in

DUE DATES FOR ISSUING TDS CERTIFICATES.

Form No 16

ANNUALLY ON OR BEFORE 15th JUNE

Form No 16A

Quarterly Within 15 days from the last date of filing quarterly TDSs

Statement/Return

TO BE DOWNLOADED FROM Income Tax Website/..www.tdscpc.gov.in

DEFAULT NOTICES UNDER SECTION 200A OF IT ACT

❖Notice under section 200A of the Income tax Act is similar to Intimation issued under section 143 (1) of the Income tax Act -issued in the case of Income-tax returns

❖Intimation under section 200A is to be treated as a notice of demand as per the deeming provision under section 156 of the IT Act.

❖Currently these statements are computer generated and are received from TRACES website.

❖Intimation can be in respect of arithmetical errors and incorrect claim apparent from information furnished in the statement / return

DO’S !ND DON’T’S

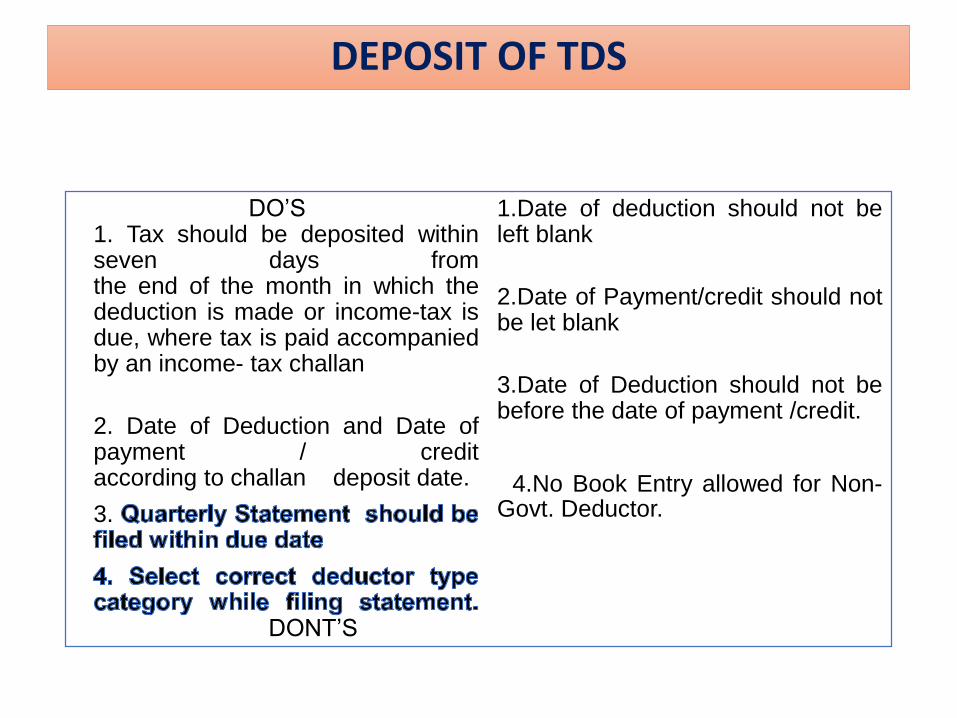

DEPOSIT OF TDS

DO’S 1. Tax should be deposited within seven days from the end of the month in which the deduction is made or income-tax is due, where tax is paid accompanied by an income- tax challan

2. Date of Deduction and Date of payment / credit according to challan deposit date.

3.

1.Date of deduction should not be left blank

2.Date of Payment/credit should not be let blank

3.Date of Deduction should not be before the date of payment /credit.

4.No Book Entry allowed for Non-Govt. Deductor.

DONT’S

• DO’S

1. Deduct TDS according to the prescribed rates.

2. Quote valid PAN while filing statement.

3. Appropriate flag should be raised as given below:

A - Lower/No Deduction for Certificate

B - No deduction for Form 15G/H cases.

C - Higher Deduction where PAN is not available

T - No Deduction for Transporters having PAN

Y - No deduction due to payment below threshold limit.

4. Certificate No. issued by the Income tax Department should be quoted

for relevant TAN – PAN Combination, F.Y, Quarter and periodicity.

5. Certificate no. should be of 10 digits with alpha numeric structure

SHORT PAYMENT

• DO’S

• 1. Deducted/Collected amount should be equal to deposited

amount.

• 2. Balance available in OLTAS should be equal or more than the

deducted / collected amount.

• 3. Oltas challan should be matched with statement Challan.

• DONT’S

• 1. There should’nt be any a difference in tax deducted and

deposited.

• 2. Balance available in OLTAS should not be less than the amount

deducted / collected

PAN VERIFICATION

• 206(6) says “Where the Permanent Account

• Number provided to the deductor is invalid or does not belong to the deductee, it shall be deemed that the deductee has not furnished his PAN NO to the deductor and the provisions of sub-section(1) shall apply accordingly

• Hence deductor would be liable for short deduction in case of invalid PAN. Online verification of PAN facility is available)

• Rectification of more than 4 characters in the PAN not permissible (2 digits & 2 letters) (whether valid to valid or invalid to valid)

• Penalty u/s. 272B may be levied for not quoting correct PAN

REVISION OF TDS STATEMENTS / RETURNS

• TDS Statements can be revised suo moto or in response to notice u/s 200A

• Unlike Return of Income , there is no time limit for revision of a TDS Statement

DECLARATION FOR NON-FILING OF A STATEMENT HAS BEEN ENABLED ON TRACES

A new facility(option) has been introduced in the TRACES

website of TDS, whereby the Deductor has the facility to

declare/update the record regarding NIL TDS return in a

particular quarter, in respect of the quarter where there are

not payments / deduction of TDS.

On account of the above facility the deductor would be free

from the notices which are otherwise being sent to those

deductors for non filing of TDS return for the particular quarter.

CERTIFICATES UNDER SECTION 197 OF THE INCOME TAX ACT, 1961 FOR NON-DEDUCTION / LOWER

DEDUCTION

• Certification under section 197 of the Income tax Act is issued by the TDS Assessing Officer.

• Certificate is valid prospectively from the date of its issue and is valid till the end of the financial year only

• Valid only to the extent of the amount specified therein

CONSEQUENCES OF FAILURE TO DEDUCT TAX AT SOURCE

Particulars Description

Failure to deduct or to pay TDS Interest u/s 220(2) upto amount not [order u/s 201(1) ] deducted or pay

1% per month from the date on which tax was deductible to actual date of deduction

Late deduction or late payment of TDS [Interest u/s 201(1A) ]

1.5% per month from the date of deduction to date of payment

PENALTIES FOR DEFAULTS Default/Failure Consequences

Failure to apply for TAN Penalty of Rs. 10,000

Failure to deduct tax at source Tax + Interest @ 1% p.m. of tax deductible +

Penalty equal to the amount of tax deductible

Failure to deposit tax at source Tax + Interest @ 1.5% p.m. of tax + Imprisonment for 3 months - 7 years with fine

Failure to furnish prescribed -Fees of Rs. 200/day during which the default statements u/s 200(3) continues subject to maximum of TDS amount

Failure to issue TDS certificates Penalty of Rs. 100/day during which the default continues (subject to maximum of TDS amount)

Failure to mention PAN of the Penalty of Rs. 10,000 deductee in the TDS statements (CIT vs. DHTC Logistics Ltd (Delhi HC)) and certificates

Furnishing of incorrect Penalty ranging between Rs. 10,000 - Rs. 100,000 information

PENALTIES

SECTION CONTENT AMOUNT

271C Non deduction of tax Equal to the tax not deducted

271CA Non collection of tax Equal to the tax not collected

271H Delay in submission of TDS returns / wrong information in statement

Minimum : Rs.10,000 Maximum : Rs. 1,00,000

272A(2)(g) Failure to issue TDS certificates

Rs.100 per day of default subject to maximum of the tax deducted

272B(2) Non quoting of PAN of payee

Rs.10,000

272BB TAN not obtained Rs.10,000

272BB(1A) Quoting of false TAN Rs.10,000

221(1) Assessee in default Not to exceed the amount of tax in arrears

Section DEFAULT PUNISHMENT

Imprisonment – Failure to credit the TDS to the Central

276B 3 months to 7 years Government

and with fine

Failure to credit the TCS to the Central Imprisonment – 276BB

Government 3 months to 7 years and with fine

If the tax exceeds Rs.25,000 – 6 months to 7 yrs.

276C Willful attempt to evade tax

In any other case - 3 months to 2 yrs.