welcome welcome sacramento regional economic vitality conversation august 4, 2004 made possible...

TRANSCRIPT

WelcomeWelcomeSacramento Regional

Economic Vitality Conversation

August 4, 2004

Made possible through generous support from Pacific Gas and Electric Company

A Joint Venture of

California State University, Sacramento

And the

Sacramento Area Commerce & Trade Organization

Dr. Robert Fountain, California State University, Sacramento

A Decade of Excellence

8,7

00

-11

,00

0

60

0

15

,00

0

17

,70

0

18

,30

0

19

,90

0 26

,90

0 33

,80

0

23

,80

0

21

,50

0

12

,30

0

8,9

00

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Growth in Non-Farm EmploymentSacramento MSA

Data for the Sacramento MSA 1990-2003. Source: EDDSACTO-CSUS Sacramento Regional Research Institute, May 2004.

Employment Growth Rate ComparisonSacramento, California and US

1.6%

0%

1%

2%

3%

4%

5%

6%

JU

L 9

9

OC

T 9

9

JAN

00

AP

R 0

0

JUL

00

OC

T 0

0

JAN

01

AP

R 0

1

JUL

01

Non-agricultural wage & salary employment. Growth compared to same month previous year. Source: Employment Development Department, US Bureau of Labor Statistics.

Sacramento Sacramento

USUS

California

California2.5%

3.0%

5.5%

4.8%

4.1%

3.2%

2.8%

0.4%

-0.5%

0.0%

-0.4%

0.4%

0.6%0.7%

-0.4%

-0.4%

0.0%

0.9%1.0%

-3.3%

-3.4%-3.2%

-2.1%

-1.2%

-0.9%

1.0%1.5%

1.1%

0.8%

1.1%

0.5%0.4%

-4%

-3%

-2%

-1%

0%

1%

2%

Jun-03 Jul-03 Aug-03 Sep-03 Oct-03 Nov-03 Dec-03 Jan-04 Feb-04 Mar-04 Apr-04 May-04 Jun-04

Sacramento Region

California

U.S.

-0.9%

1.3%

1.8%

2.0%

2.4%

2.6%

2.8%

2.9%

-1% 0% 1% 2% 3%

San Jose PMSA

Los Angeles - Long Beach PMSA

San Francisco PMSA

Oakland PMSA

San Diego PMSA

Orange PMSA

Sacramento PMSA

Riverside - San Bernardino PMSA

Employment Growth RatesMajor California PMSA'S

12 months ending July 2001

Non-agricultural wage & salary employment, change from same month previous year.Source: Employment Development Department.

Winners and Losers

Employment Increase

Percent of Increase

Total Nonfarm 187,842 100.0%

Local Government 35,675 19.0% Health Care and Social Assistance 19,775 10.5%

Construction 19,083 10.2% State Government 16,650 8.9%

Retail Trade 15,642 8.3% Financial Activities 15,633 8.3%

Information 5,358 2.9% Manufacturing 3,467 1.8%

(Computer and Electronic Product Manufacturing) 2,983 1.6% Federal Government (18,983) -10.1%

Data for Sacramento PMSA, 1990-2003. Source: EDD

SACTO-CSUS Sacramento Regional Research Institute Feb, 2004

Business Cycle Employment Growth in the Sacramento Region

-1.0%

-0.8%

-0.7%

-0.4%

-0.2%

-0.2%

-0.2%

-0.2%

-0.1%

0.2%

0.3%

0.5%

0.5%

0.6%

3.7%

-1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

Federal Government

Finance, Insurance & Real Estate

Retail Trade

Wholesale Trade

Primary & Fabricated Metal

Food & Kindred Products

Hotels & Other Lodging Places

Industrial Machinery

Computer & Office Equipment

Transportation & Public Utilities

Health Services

Construction

Local Education

Amusement, Including Movies

Business Services

California Shift in Economic Composition

1990-2000

Very high High Low Very Low

LOS ANGELES-LB Transportation & Utilities Manufacturing, Services Construction

ORANGE Manufacturing, Trade, Finance Services Transportation & Utilities Government

OAKLANDConstruction, Transportation &

Utilities

MODESTO Manufacturing Trade, Construction Transportation & Utilities Finance, Services

SACRAMENTO Construction, Government FinanceTransportation & Utilities, Trade,

Manufacturing

SAN DIEGO Services, Government

SAN JOSE Manufacturing, ServicesTransportation & Utilities, Trade, Finance,

Government

RIVERSIDE-SB Construction, TradeTransportation & Utilities,

Government Services Finance

SAN FRANCISCOTransportation & Utilities, Finance,

Services Construction Manufacturing, Trade, Government

SANTA BARBARA Government Transportation & Utilities

SAN LUIS OBISPO Trade, Services, Government Construction Manufacturing, Trade, Government

Method: Location Quotient method

Dr. Robert Fountain, January 2003.

Sectors of Concentration for California Regions

Data Source: California Economic Development Department

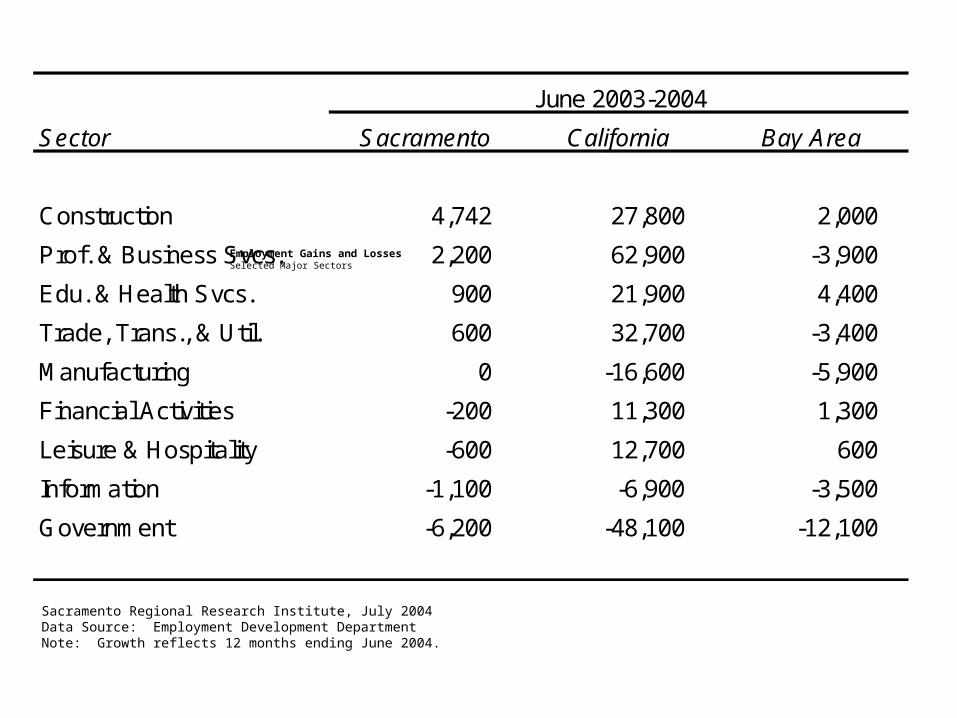

Employment Gains and LossesSelected Major Sectors

Sector Sacramento California Bay Area

Construction 4,742 27,800 2,000

Prof. & Business Svcs. 2,200 62,900 -3,900

Edu. & Health Svcs. 900 21,900 4,400

Trade, Trans., & Util. 600 32,700 -3,400

Manufacturing 0 -16,600 -5,900

Financial Activities -200 11,300 1,300

Leisure & Hospitality -600 12,700 600

Information -1,100 -6,900 -3,500

Government -6,200 -48,100 -12,100

June 2003-2004

Sacramento Regional Research Institute, July 2004Data Source: Employment Development DepartmentNote: Growth reflects 12 months ending June 2004.

2.7

3.3

4.2

5.6

6.3

8.7

9.2

9.9

12.4

14.0

0 2 4 6 8 10 12 14 16

Sacramento Regional Research Institute, December 2002.Data Source: US Census Bureau.Note: 2000 Census used for population figures.

San Francisco, CA

Los Angeles,CA

San Diego, CA

Seattle, WA

Portland, OR

Austin, TX

Denver, CO

Sacramento, CA

Phoenix, AZ

Atlanta, GA

New Houses per 1000 PeopleSelected PMSAs Nationwide

October, Year to Date

Median Home Sale Prices Major California Regions and the State, February 2004

$256,810

$275,000

$279,470

$390,010

$394,300

$479,540

$481,583

$566,200

$569,760

$0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000

Riverside-San Bernardino

Stockton-Lodi

Sacramento

Los Angeles-Long Beach

California

San Diego

San Francisco

San Jose

Orange

Sacramento Regional Research Institute, April 2004 Data Source: California Association of Realtors

Sector Total Revenues Employment

Wholesale trade $243,430,576 1,993Architectural and engineering services $139,570,448 1,581Real estate $111,605,424 801Motor vehicle and parts dealers $87,307,768 999Monetary authorities and depository credit interme $80,458,056 424Building material and garden supply stores $78,118,816 1,188Truck transportation $75,664,232 614Miscellaneous store retailers $58,471,784 1,193Insurance carriers $56,892,040 331Legal services $49,933,832 557Sawmills $46,829,332 248Wood kitchen cabinet and countertop manufacturing $42,081,804 551Management of companies and enterprises $39,648,680 416Employment services $32,190,026 1,154State and local government electric utilities $30,494,804 59Accounting and bookkeeping services $28,879,588 511Gasoline stations $28,057,856 375Wood windows and door manufacturing $27,418,326 186Machinery and equipment rental and leasing $25,808,798 77Management consulting services $23,485,660 287Reconstituted wood product manufacturing $22,208,544 85Engineered wood member and truss manufacturing $21,004,544 171Other millwork- including flooring $15,068,131 212Commercial machinery repair and maintenance $14,807,888 151Custom architectural woodwork and millwork $14,495,547 78Plastics plumbing fixtures and all other plastics $13,546,847 72Postal service $11,869,142 155Logging $11,201,065 76Business support services $11,191,621 220Waste management and remediation services $10,351,798 79Asphalt paving mixture and block manufacturing $10,134,549 25Plastics pipe- fittings- and profile shapes $8,280,466 59Environmental and other technical consulting servi $7,805,066 63Specialized design services $4,858,457 48Foam product manufacturing $3,214,956 16Ready-mix concrete manufacturing $2,382,965 12

Data from IMPLAN model for the Sacramento CMSA using year 2003 housing construction data.

Selected sectors with highest indirect impacts.

Dr. Robert Fountain, March 2004.

Total Revenues and Employment in Support Sectors Created by New Housing Construction

Three Scenarios of Long Term Economic Development

1. Absorption into the Bay Area Economy 2. Central City of the Central Valley 3. Unique Technology Cluster

Three Scenarios for the Region

Convergences

1. The inter-dependence between transportation, land use, housing, and economic elements which determine our regional quality of life.

2. Economic changes underway will require active intervention to maintain our regional quality.

3. Workforce quality is the economic variable over which we have the most control.

4. Education is emerging as the consensus mechanism for achieving the desired economic outcomes.

%California 26.6

Marin County 51.3San Francisco County 45.0San Mateo County 39.0Contra Costa County 35.0Alameda County 34.9Yolo County 34.1Orange County 30.8Placer County 30.3San Diego County 29.5El Dorado County 26.5Los Angeles County 24.9Sacramento County 24.8Solano County 21.4Riverside County 16.6Sutter County 15.3Merced County 11.0Yuba County 10.3

Source: Year 2000 census data

Dr. Robert Fountain, February 2003

Percent of Population with Bachelor's Degree or

Higher25 years or Over

Comparisons

of Educational Attainment

Sacramento Region California

Enrollment Per 1,000 Residents 95.8 57.0Graduates per 1,000 Residents 11.6 6.0

Higher Education Participation

What We Now Have:

1. An Integrated Picture of Transportation, Land Use, Environment, Housing, and Economic Vitality

2. A willingness to work on multi-jurisdictional

approaches, as long as they are seen as providing increased opportunities without loss of local political power.

3. Multi-faceted leadership with a regional

perspective:

SACOG SACTO Valley Vison Metro Chamber Education Leadership

What We Need Next

To Assemble and Enable this emerging integrated leadership with a focus on enhancing Economic Vitality

Susan FrazierCEO/Director

Valley Vision

Three sections:• Our Economic Engine • People and Community • Place

Breakdowns by geography and ethnicity

Valley Vision Quality of Life Report

Industry Clusters of Opportunity—Selection Criteria

Size Current Economic Impact

# employees. Determines if an industry is a significant component of the cluster’s activity in the region

Average Annual Growth Rate

Job Creation

Growth in # employees. Shows how various components of the cluster have weathered market forces and their subsequent employment generation

Concentration Regional Specialization

Concentration of industries/sub-industries within region. Specialization generally reflects industry competitiveness.

Average Payroll per Employee

Job Quality

High average payroll per employee relative to the regional average indicates a sector with relatively high productivity and value-added.

Economic Portfolio

x axis

Employment Concentration

y axis

Average annual employment growth rate

Size (# employees)

1994-2000

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-2.0% 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

Computer, Semi, Electronics

(32,191)

Innovation Services(56,922)

Construction(63,453)

Health and Biomedical

(74,776)

Miscellaneous Mfg

(43,974)

FIRE(54,420)

Transportation-Logistics-Warehsng

(18,634)Information & Telecom Services(16,170)

Ag and Processing

(34,323)

Visitor Services(77,941)

Sacramento regional economic portfolio by employment concentration, 2000 (vertical axis), Average Annual Growth Rate 1994-2000 (horizontal axis) and employment, 2000 (size of bubble).

Clu

ste

r e

mp

loym

en

t co

nce

ntr

atio

n r

ela

tive

to C

alif

orn

ia, 2

00

0 >

1.0

= m

ore

co

nce

ntr

ate

d th

an

CA

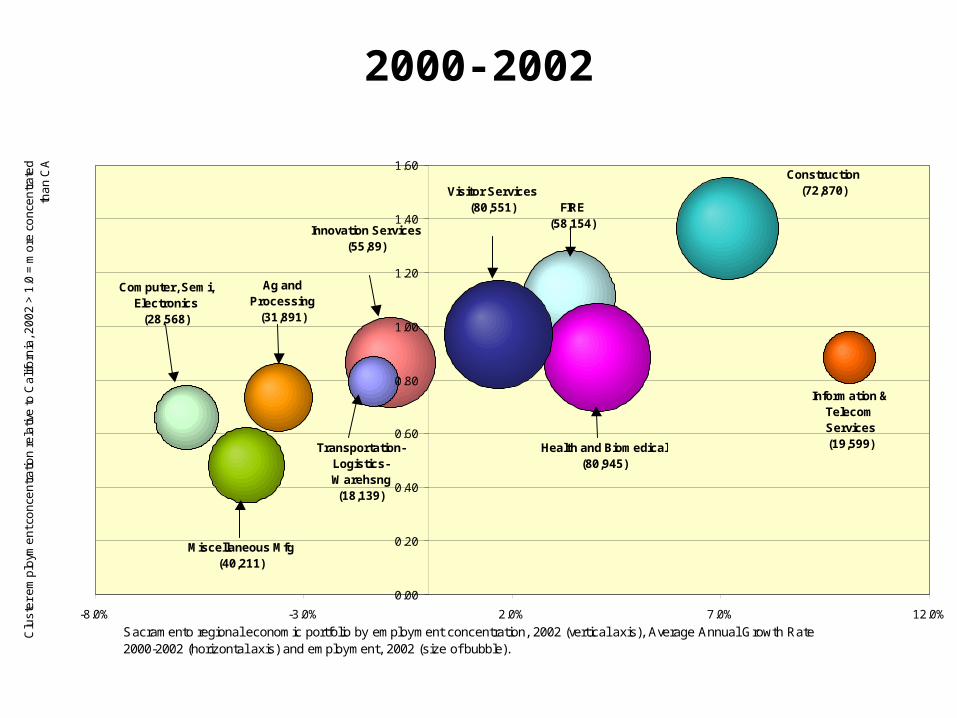

2000-2002

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

-8.0% -3.0% 2.0% 7.0% 12.0%

Computer, Semi, Electronics

(28,568)

Innovation Services(55,89)

Construction(72,870)

Health and Biomedical(80,945)

Miscellaneous Mfg(40,211)

FIRE(58,154)

Transportation-Logistics-Warehsng(18,139)

Information & Telecom Services(19,599)

Ag and Processing

(31,891)

Visitor Services(80,551)

Clu

ste

r e

mp

loym

en

t co

nce

ntr

atio

n r

ela

tive

to C

alif

orn

ia, 2

00

2 >

1.0

= m

ore

co

nce

ntr

ate

d

tha

n C

A

Sacramento regional economic portfolio by employment concentration, 2002 (vertical axis), Average Annual Growth Rate 2000-2002 (horizontal axis) and employment, 2002 (size of bubble).

Assessing Clusters of Opportunity2000-2002

83110729465Growth(Ranked Highest to Lowest)

75981062134Conc.(Ranked Highest to Lowest)

10987654321Size(Ranked Highest to Lowest)

Trans, Logis & Whsng

Info & Telecom

Ag & Proces

sing

Innovation Service

FIRECons-

tructionVisitor Svcs.

Health & Bio Misc. Mfg

Com-Semi-Elec.

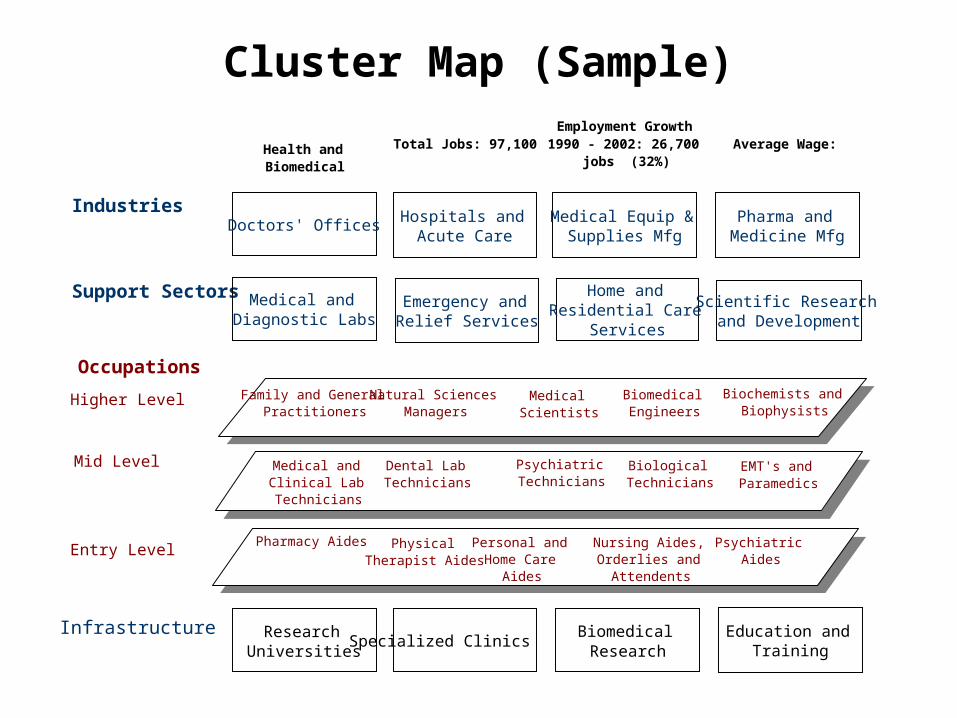

Cluster Map (Sample)

Industries

Support Sectors

Occupations

Higher Level

Mid Level

Entry Level

Infrastructure

Employment Growth 1990 - 2002: 26,700

jobs (32%)Total Jobs: 97,100 Average Wage: Health and

Biomedical

Doctors' Offices

Emergency and Relief Services

Home and Residential Care

Services

Research Universities

Specialized Clinics Biomedical Research

Hospitals and Acute Care

Medical Equip & Supplies Mfg

Education and Training

Scientific Research and Development

Medical and Diagnostic Labs

Pharma and Medicine Mfg

Family and General Practitioners

Natural Sciences Managers

Medical Scientists

Biochemists and Biophysists

Medical and Clinical Lab Technicians

Psychiatric Technicians

Dental Lab Technicians

Biological Technicians

EMT's and Paramedics

Nursing Aides, Orderlies and

Attendents

Personal and Home Care

Aides

Physical Therapist Aides

Psychiatric Aides

Pharmacy Aides

Biomedical Engineers

Economic Vitality ConversationToday’s Focus

1. What state actions will have the most immediate positive impact on California’s economic recovery?

2. What state actions will result in the most significant long-term improvement to California’s economic competitiveness and comparative advantage?

3. How do we best structure an effective partnership between the regions and the state around economic strategy?