welcome to intertanko’s member seminar shanghai 3 rd december 2009 国际油轮船东协会

TRANSCRIPT

Welcome to INTERTANKO’s Member Seminar

Shanghai

3rd December 2009

国际油轮船东协会

INTERTANKO Overview

Members’ Seminar, Shanghai3 December 2009

Peter M. Swift

INTERTANKO Overview

• INTERTANKO & Organisation Review• Tanker Market Overview• Greenhouse Gas Emissions• Piracy• Criminalisation and fair treatment of seafarers• Fuel issues, EU, CARB, Annex VI ECA

INTERTANKO Report from Council

• New Chairman – Graham Westgarth, President of Teekay Marine Services

• 4 new Executive Committee members

• Membership and Finances strong• Committees, Panels active and effective• Secretariat busy

• Membership Fees for 2010 reduced by 10%

Organisation Review

Organisation Review

Executive Committee proposed to Council in May 2009 to conduct an Organisation Review to ensure the continuing effectiveness of the Association.

Conscious of:• potential overlaps with other organisations• need to ensure cost efficiency• desire to provide optimal service to Members• maintaining a strong tanker voice

Organisation Review - Process

• Working group established

• Council members consulted with a review questionnaire on the organisational structure of the association

• Additional inputs provided by members and secretariat

• Findings reviewed by Executive Committee

• Further consultations / discussions on preliminary findings via Panel and other meetings

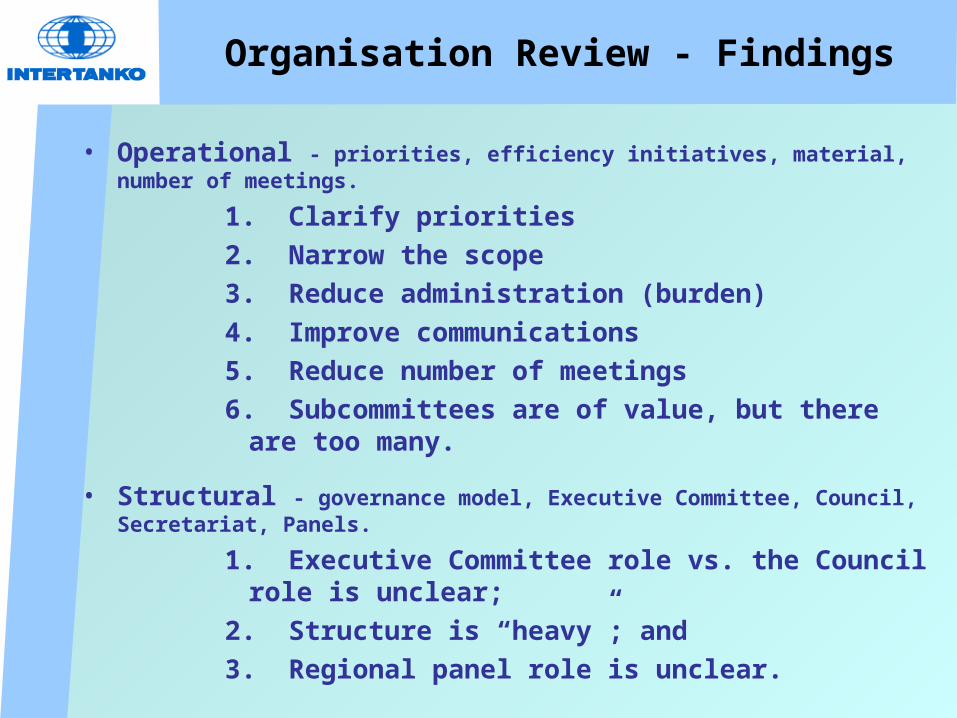

Organisation Review - Findings

• Operational - priorities, efficiency initiatives, material, number of meetings.

1. Clarify priorities

2. Narrow the scope

3. Reduce administration (burden)

4. Improve communications

5. Reduce number of meetings

6. Subcommittees are of value, but there are too many.

• Structural - governance model, Executive Committee, Council, Secretariat, Panels.

1. Executive Committee role vs. the Council role is unclear;

2. Structure is “heavy”; and

3. Regional panel role is unclear.

Organisation Review- Articles of Association

“The Policy of the Association shall be decided upon and determined by the Council. The Executive Committee shall, while keeping the Council generally informed, conduct the business and affairs of INTERTANKO and supervise the management of INTERTANKO’s office”.

Council: sets policy, direction and prioritiesExecutive Committee: implements the policies and priorities as directed by Council

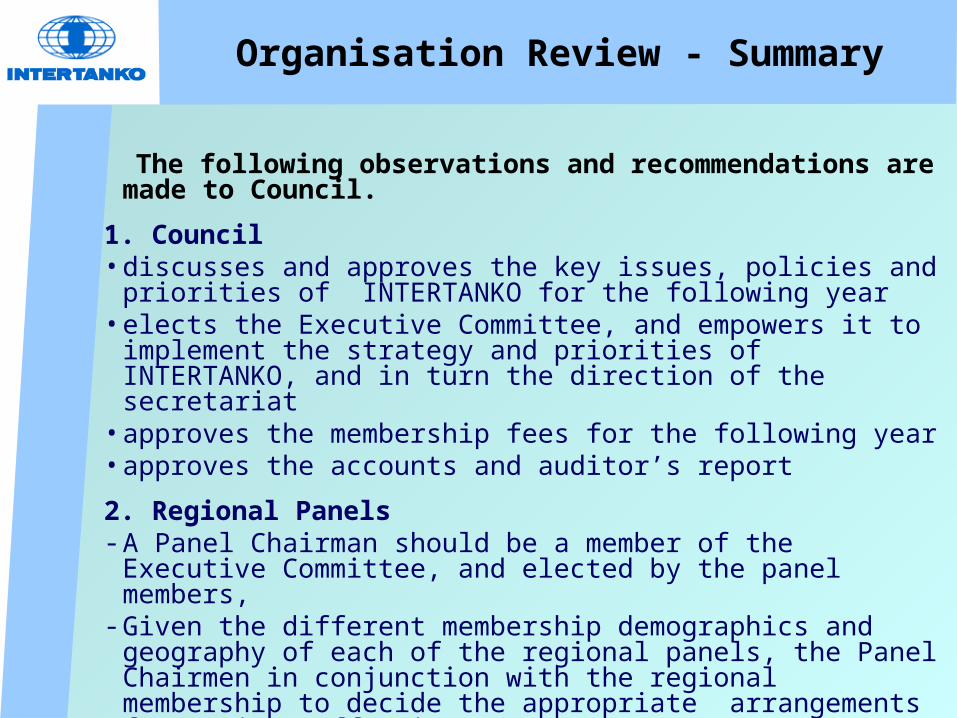

Organisation Review - Summary

The following observations and recommendations are made to Council.

1. Council• discusses and approves the key issues, policies and priorities of

INTERTANKO for the following year• elects the Executive Committee, and empowers it to implement the

strategy and priorities of INTERTANKO, and in turn the direction of the secretariat

• approves the membership fees for the following year• approves the accounts and auditor’s report

2. Regional Panels- A Panel Chairman should be a member of the Executive Committee,

and elected by the panel members,- Given the different membership demographics and geography of

each of the regional panels, the Panel Chairmen in conjunction with the regional membership to decide the appropriate arrangements for maximum effectiveness

Organisation Review Key Objectives and Key issues

Key objectives:• Developing best practices • Promoting the industry• Influencing stakeholders• Providing advice and information for members

Key issues:• Environment• Safety• Technical• Human element• Vetting• Chemicals• Other ?

Tanker Market Overview

Global Financial Crisis

Tanker Market Overview

INTERTANKO’s Anti-Trust/Competition law Compliance Statement

INTERTANKO’s policy is to be firmly committed to maintaining a fair and competitive environment in the world tanker trade, and to adhering to all applicable laws which regulate INTERTANKO’s and its members’ activities in these markets. These laws include the anti-trust/competition laws which the United States, the European Union and many nations of the world have adopted to preserve the free enterprise system, promote competition and protect the public from monopolistic and other restrictive trade practices. INTERTANKO’s activities will be conducted in compliance with its Anti-trust/Competition Law Guidelines.

MarketsMarkets

Credit crunch – liquidity; financing; exposures; covenants & more….

• Oil prices ?• Steel prices ?• Newbuild / scrap prices ?• Economic slowdown (or meltdown !) ?• Green agenda slowdown ?• Markets ?• Other ?

Global Financial Crisis (end 2008)

Global Financial Crisis (end 2009)

• Demand : World trade & by sector

• Supply : Ships on Order & Fleet development

• Tanker market

• Shipbuilding capacity

World GDP, Trade and Oil Demand

-16

-12

-8

-4

0

4

8

12

16

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

Wo

rld

Imp

ort

s% y

-y

-1.5

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

GD

P %

y-y

OECD WorldImports of Goods

IMF GDP

-4-3-2-10123456

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

% c

ha

ng

e (

ye

ar

on

ye

ar)

IMF GDPOil Demand

Source: Clarksons (September 2009)

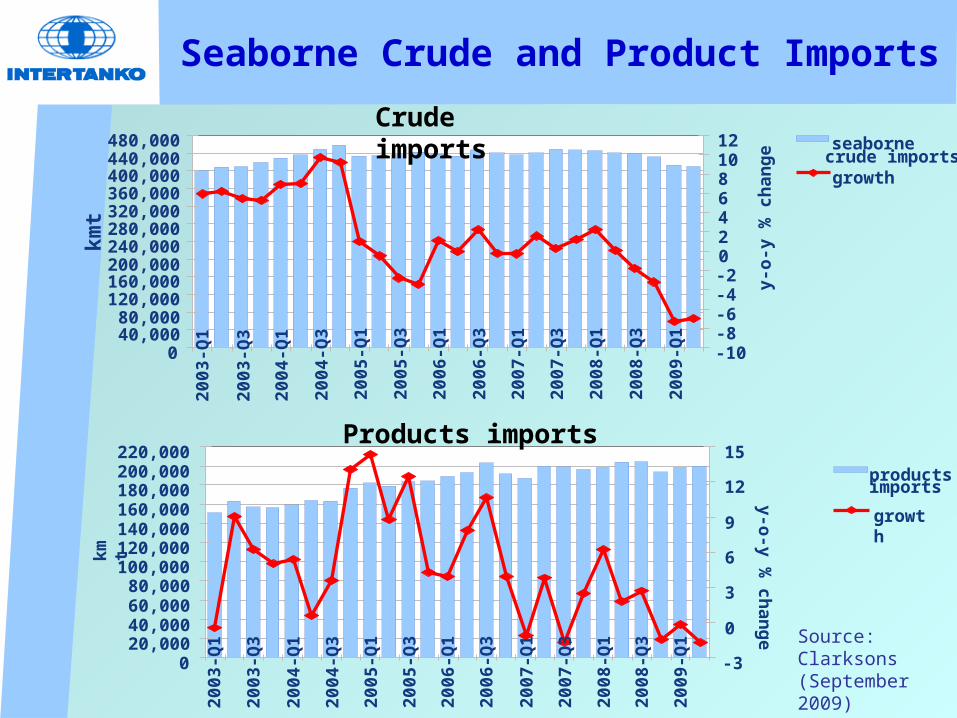

Seaborne Crude and Product Imports

040,00080,000

120,000160,000200,000240,000280,000320,000360,000400,000440,000480,000

2003

-Q1

2003

-Q3

2004

-Q1

2004

-Q3

2005

-Q1

2005

-Q3

2006

-Q1

2006

-Q3

2007

-Q1

2007

-Q3

2008

-Q1

2008

-Q3

2009

-Q1

kmt

-10-8-6-4-2024681012

y-o

-y %

ch

ang

e

seabornecrude importsgrowth

020,00040,00060,00080,000

100,000120,000140,000160,000180,000200,000220,000

2003

-Q1

2003

-Q3

2004

-Q1

2004

-Q3

2005

-Q1

2005

-Q3

2006

-Q1

2006

-Q3

2007

-Q1

2007

-Q3

2008

-Q1

2008

-Q3

2009

-Q1

kmt

-3

0

3

6

9

12

15

y-o-y %

chan

ge

productsimports

growth

Source: Clarksons (September 2009)

Crude imports

Products imports

Green Shoots of Recovery ?

Demand increases ?More long-haul crude; more refinery imbalances (and emerging opportunities ?)

CRUDE Production (mbd) 2008 2009 2010

OPEC 31.27 29.02 29.19

NON-OPEC (Selected)

Brazil 2.40 2.60 2.83

Canada 3.35 3.38 3.43

The United States 8.51 8.92 9.00

Azerbaijan 0.88 1.04 1.18

Kazakhstan 1.43 1.51 1.66

Russia 9.79 9.78 9.78Mexico 3.19 2.93 2.69

North Sea 5.20 4.90 4.54

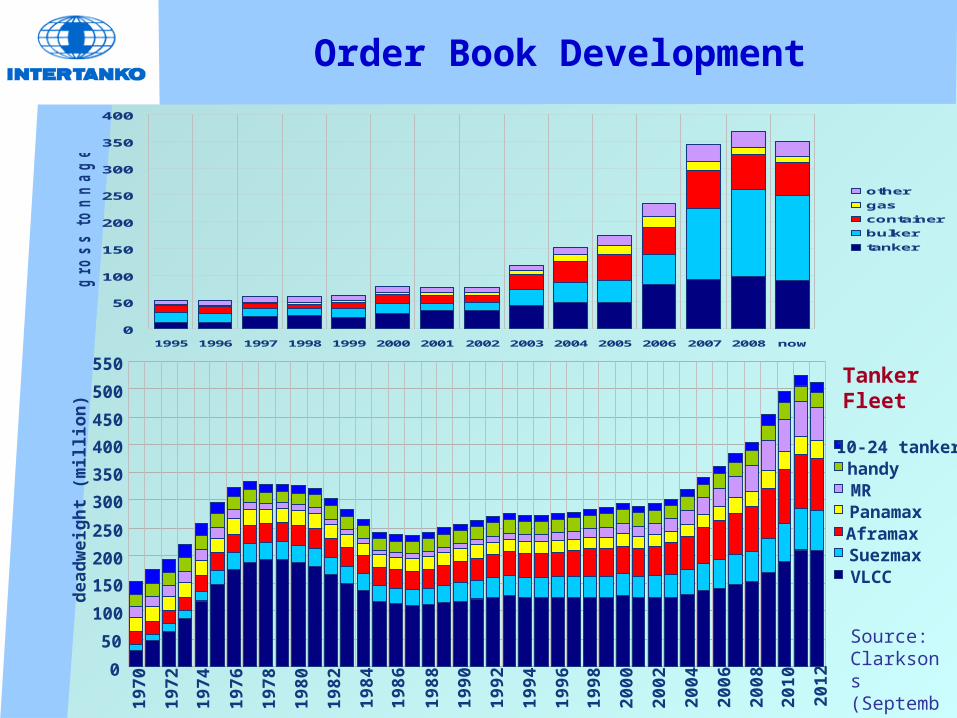

Order Book Development

0

50

100

150

200

250

300

350

400

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 now

gro

ss

to

nn

ag

e (

millio

ns

)

other

gas

container

bulker

tanker

0

50

100

150

200

250

300

350

400

450

500

550

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

dea

dw

eig

ht

(mill

ion

)

10-24 tankerhandyMRPanamaxAframaxSuezmaxVLCC

Tanker Fleet

Source: Clarksons (September 2009)

Orderbook by ship type(as % existing fleet)

Source: Clarksons (September 2009)

33

64

41

15

33

0

10

20

30

40

50

60

70

Tanker Chemical Bulk carrier Container ship LPG carrier

per

cen

tag

e o

f cap

acity

Some are advocating

Some are advocating

Compulsory Scrapping Schemes

Compulsory Scrapping Schemes

Tanker sales for demolitionand VLCC freight rate

Source: INTERTANKO

m dwt USD / day

* Until week ending 4 September** Sales for demolition until 4 September*** Clarkson Freight rate AG-Japan week ending 4 September

0

6

12

18

24

30

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09*0

20,000

40,000

60,000

80,000

100,000VLCCs sales for demolition

<200,000 dwt sales for demolition**

VLCC freight rate***

SH trading beyond 2010?http://www.intertanko.com/templates/intertanko/issue.aspx?id=18805

– Australia No– China No (?)– EU No– Mexico No– Romania No– S Korea No– Philippines No– UAE No

no official note to IMO

– Bahamas Yes– Barbados Yes– Liberia Yes– Marshall Isl. Yes– Panama Flag Yes– Japan Yes– Singapore Yes– India Yes– Hong Kong * Yes

*20 years

Flag/Port States positions MARPOL 20 Trading until the age of 25 years

– United States N/A OPA90

Source: Baltic Exchange/INTERTANKO

USD/dayUSD/day

Average tanker freight rates (based on Baltic Exchange rates)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

2001 2002 2003 2004 2005 2006 2007 2008 8m09

VLCC AG-Japan, 250,000 ts

Suezmax Wafr-US 130,000 ts

Aframax N Sea-UKCont, 80,000 ts

Product Caribs-US, 38,000 ts

Lower Freight Rates & Fleet surpluses (in ALL sectors – not just tankers)

Implications ?

• Challenge to maintain quality and standards

• Challenge to meet the issues of the day

• and government interventions ?

Shipbuilding output and forecast

Source: Worldyards/INTERTANKO Aug 09

m cgtm cgt

2631 33

38

26

26

55

42

15

3 0

914% 26

38%

4876% 62

95%67

99%

0

10

20

30

40

50

60

70

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Available capacity

Orderbook

Historical deliveries

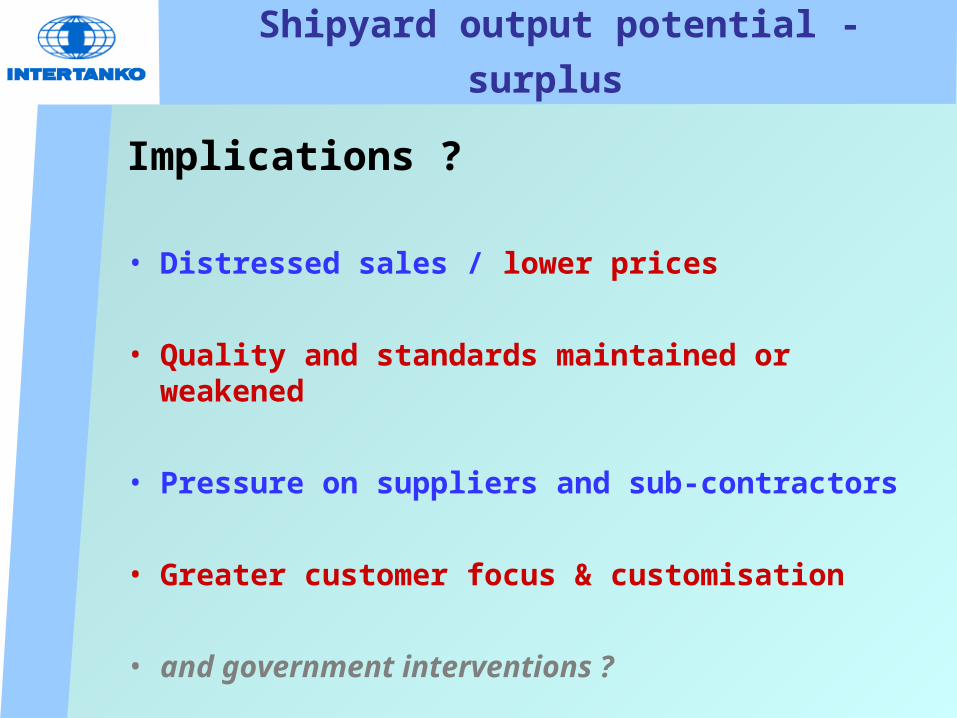

Shipyard output potential - surplus

Implications ?

• Distressed sales / lower prices

• Quality and standards maintained or weakened

• Pressure on suppliers and sub-contractors

• Greater customer focus & customisation

• and government interventions ?

Green House Gas Emissions

Greenhouse Gas Emissions

• Key Dates• Kyoto Protocol• Means of reducing GHG emissions• IMO (MEPC) Programme• UNFCCC COP 15 Meeting• INTERTANKO Position• “Virtual Arrival”

Shipping’s GHG Emissions

Selected Key Dates

• 1997 Kyoto Protocol• 1998 IMO initiates work on Greenhouse Gas

emissions • 2000 IMO Greenhouse Gas Study• 2003 IMO Assembly Resolution A.963(23)• 2007-2009 IMO updates 2000 Greenhouse Gas Study• 2009 IMO MEPC 59

• 11/2009 INTERTANKO Council• 12/2009 UNFCCC COP15 Meeting, Copenhagen• 3/2010 IMO MEPC 60• 5/2010 INTERTANKO Council• 10/2010 IMO MEPC 61• 9-10/2010 INTERTANKO Council• Spring 2011 INTERTANKO Council• 7/2011 IMO MEPC 62• 12/2011 EU Deadline for IMO/International Agreement

Kyoto Protocol

• Established under UN Framework Convention on Climate Change (UNFCCC) and adopted in 1997

• Ratified by 181 countries – not the USA• Categorises Annex 1 (Developed) Countries and Non-

Annex 1 (Developing) Countries • Annex 1 Countries are committed to make GHG

reductions with set targets, but also flexible mechanisms

• Runs through to 2012, with Conference of Parties (COP15) to meet in Copenhagen in Dec 2009 to develop successor

• Kyoto recognises “common but differentiated responsibilities”, i.e. developed countries produce more GHGs and should be “responsible” for reductions

• Kyoto looks to IMO to address Shipping and ICAO to address Aviation, and as such these emissions are currently excluded from Kyoto targets

Means of Reducing GHG Emissions

• Technical• Operational• Economic / Market

Reductions expected from both new & existing ships

While not restricting growth in shipping trades, especially since this is the most carbon-efficient transportation mode

One particular challenge for the shipping industry- i.e. seaborne trade will continue to grow strongly

Source: Fearnleys/INTERTANKO

IndexIndex

80

100

120

140

160

180

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

Population

Energy use

Seaborne trade

CO2 emission

There has been strong growth in shipping

Trends – Population, Energy Use, Seaborne trade & CO2 emissions

IMO MEPC 59 (July 2009)

• Agreed:– Interim Guidelines on the method of calculation of

the EEDI for new ships and – Interim Guidelines on voluntary verification of the

EEDI

• Adopted:

Ship Energy Efficiency Managment Plan (SEEMP)

• Adopted:

Guidelines for voluntary use of the ship EEOI

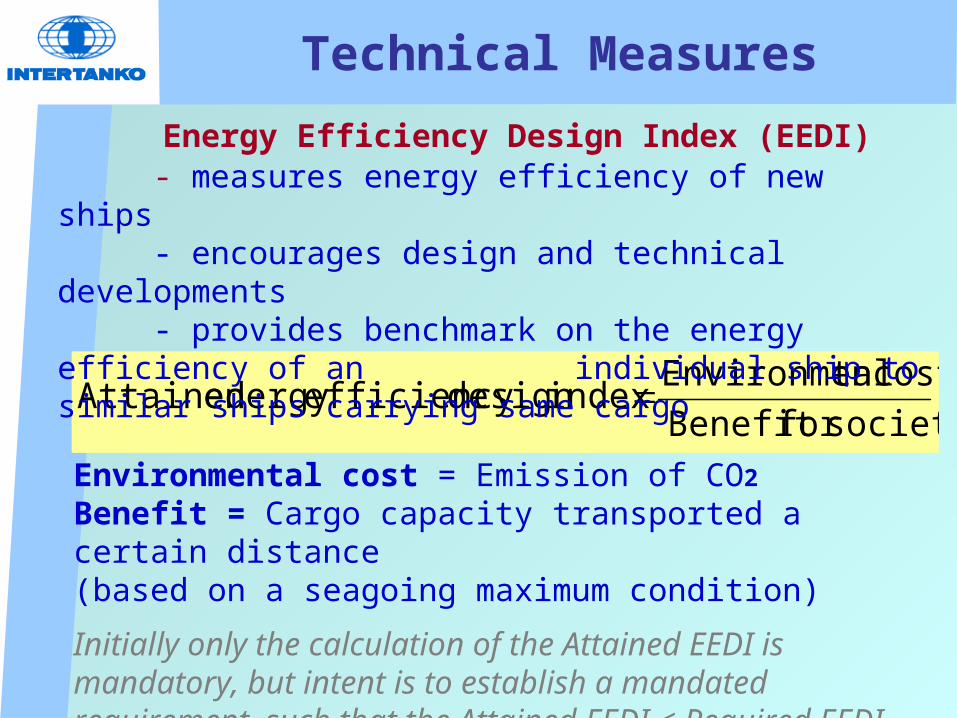

Technical Measures

societyforBenefit

costtalEnvironmenindexdesign efficiencyenergy Attained

Energy Efficiency Design Index (EEDI)- measures energy efficiency of new ships- encourages design and technical developments - provides benchmark on the energy efficiency of an individual ship to similar ships carrying same cargo

Environmental cost = Emission of CO2

Benefit = Cargo capacity transported a certain distance(based on a seagoing maximum condition)

Initially only the calculation of the Attained EEDI is mandatory, but intent is to establish a mandated requirement, such that the Attained EEDI < Required EEDI

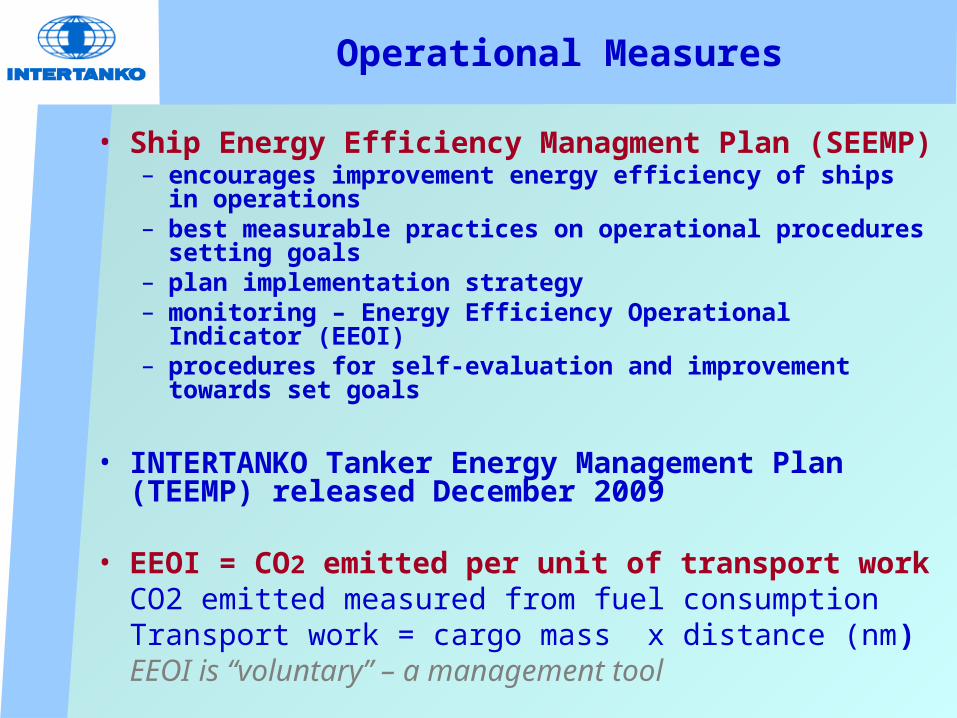

Operational Measures

• Ship Energy Efficiency Managment Plan (SEEMP)– encourages improvement energy efficiency of ships in

operations– best measurable practices on operational procedures

setting goals– plan implementation strategy– monitoring – Energy Efficiency Operational Indicator (EEOI)– procedures for self-evaluation and improvement towards

set goals

• INTERTANKO Tanker Energy Management Plan (TEEMP) released December 2009

• EEOI = CO2 emitted per unit of transport workCO2 emitted measured from fuel consumptionTransport work = cargo mass x distance (nm)EEOI is “voluntary” – a management tool

Market Measures

• MEPC 59 developed outline roadmap for MBIsReasons given to include MBIs :– Long life of ships– Growth of international shipping– EEDI (new ships) = longer term impact– SEEMP/EEOI (existing ships) = not sufficient to meet

likely/possible target reductions (e.g. 20% or more in the shorter term, say up to 2020)

• MEPC 60 to resume discussion

• Which MBI?– GHG Compensation Fund– Emission Trading Scheme (ETS)– US alternative – a simplified Cap & Trade Scheme– Alternatives to or combinations of these

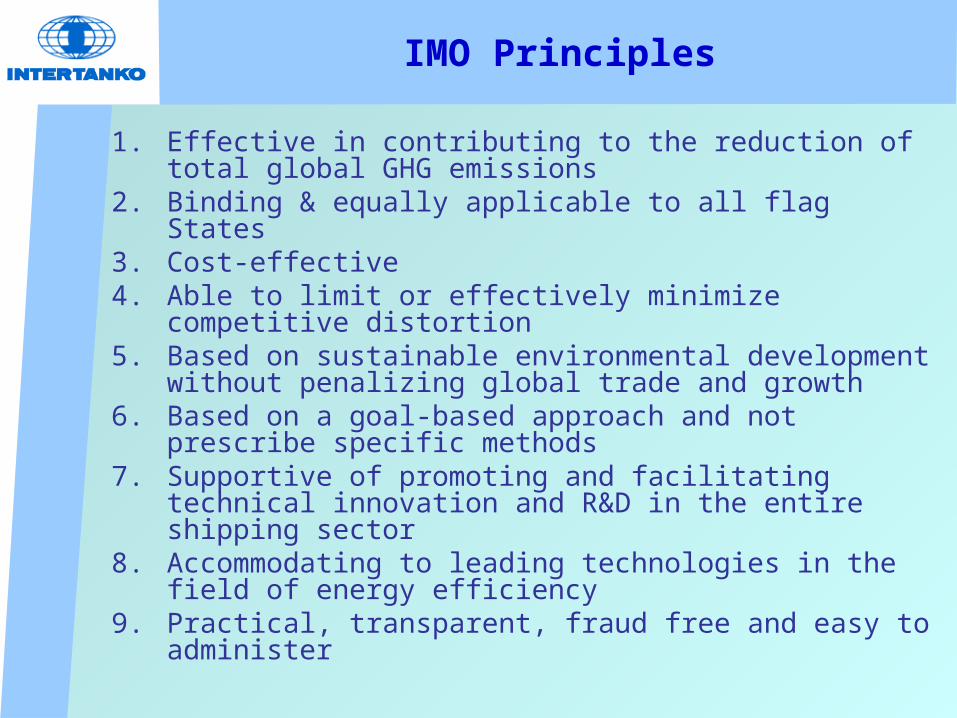

IMO Principles

1. Effective in contributing to the reduction of total global GHG emissions

2. Binding & equally applicable to all flag States3. Cost-effective4. Able to limit or effectively minimize competitive

distortion5. Based on sustainable environmental development

without penalizing global trade and growth6. Based on a goal-based approach and not prescribe

specific methods7. Supportive of promoting and facilitating technical

innovation and R&D in the entire shipping sector8. Accommodating to leading technologies in the field of

energy efficiency 9. Practical, transparent, fraud free and easy to

administer

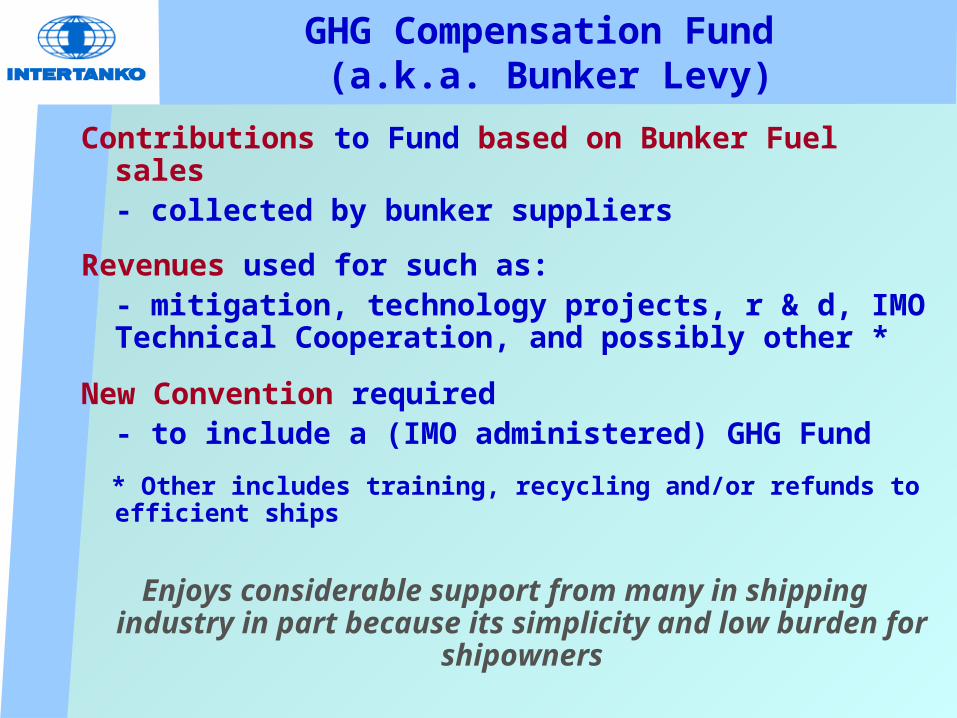

GHG Compensation Fund (a.k.a. Bunker Levy)

Contributions to Fund based on Bunker Fuel sales- collected by bunker suppliers

Revenues used for such as:- mitigation, technology projects, r & d, IMO Technical Cooperation, and possibly other *

New Convention required- to include a (IMO administered) GHG Fund

* Other includes training, recycling and/or refunds to efficient ships

Enjoys considerable support from many in shipping industry in part because its simplicity and low

burden for shipowners

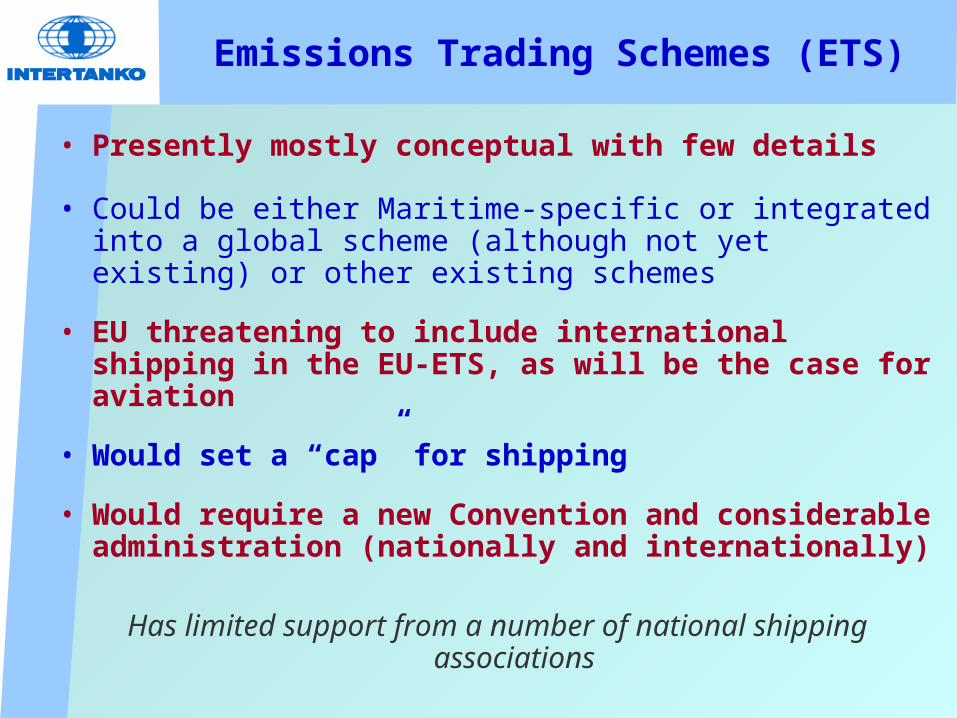

Emissions Trading Schemes (ETS)

• Presently mostly conceptual with few details

• Could be either Maritime-specific or integrated into a global scheme (although not yet existing) or other existing schemes

• EU threatening to include international shipping in the EU-ETS, as will be the case for aviation

• Would set a “cap” for shipping

• Would require a new Convention and considerable administration (nationally and internationally)

Has limited support from a number of national shipping associations

USA’s MBI Hybrid/Alternative

• Mandatory efficiency standards for both new and for existing ships, using the EEDI as a model

• The concept is based on the following principles:– regulations set up efficiency baseline for each ship, new and

existing– the efficiency base line would be gradually improved (i.e. the

energy index value will be lowered)– ships which would not be able to improve their energy

efficiency, as required, would be expected to buy credits– IMO has to establish an “efficiency credit generation and

trading” amongst the shipping community only

• US argue that this approach would provide an equitable, cost effective and timely market-based solution that would complement the developments of the EEDI, EEOI, and SEEMP.

MBI – The unanswered questions (1)

? Market Based Instrument, Mechanism or Solution

? Objective:To generate funds orTo incentivise / penalise the party/partiesorBoth

andTo set a cap ?

? Use of funds:As offset in other industriesand/orTo support marine “activities, such as research, technology developments, training, recycling, other

? To incentivise owners, charterers/shippers, terminals, others

MBI – The unanswered questions (2)

? Mechanism:- Based on individual ship or company-wide- Based on total fuel usage (all CO2) or on marginal fuel usage (incremental CO2)

? Administration via:- International (UNFCCC/IMO),- Regional (e.g. EU), or - National, or- Combination

? Involvement/influence of shipowners- Initially, later; and how ?

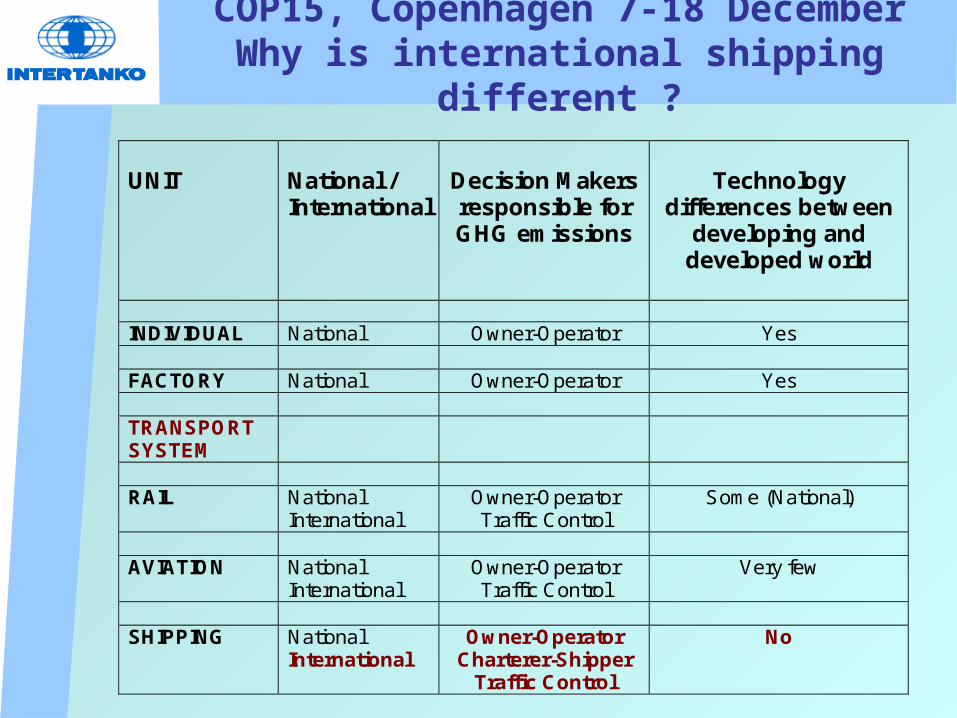

COP15, Copenhagen 7-18 DecemberWhy is international shipping different ?

• Global industry

• Regulated internationally

• Regulation principally of ships and their operation (owners and operators)

COP15, Copenhagen 7-18 DecemberWhy is international shipping different ?

UNIT

National / International

Decision Makers responsible for GHG emissions

Technology

differences between developing and

developed world

INDIVIDUAL National Owner-Operator Yes FACTORY National Owner-Operator Yes TRANSPORT SYSTEM

RAIL

National International

Owner-Operator Traffic Control

Some (National)

AVIATION National

International Owner-Operator Traffic Control

Very few

SHIPPING National

International Owner-Operator

Charterer-Shipper Traffic Control

No

INTERTANKO Policy Position

INTERTANKO Council agrees:

• that shipping should strive to deliver a significant reduction in its GHG emissions, particularly CO2 emissions

• to support measures that would result in CO2 and other GHG emissions reductions from tankers and to involve other stakeholders

• to support the IMO process to develop real and sustainable GHG emission reductions regulations from ships; such reductions should not hinder trade

• that GHG regulations should be “ship neutral”

INTERTANKO Policy Position

INTERTANKO Council agrees:

• to support the adoption of the EEDI as soon as possible, and encourages early usage of the EEDI formulae to establish target levels for CO2 emission reductions for new ships

• to support the adoption of SEEMP by IMO

• in respect of MBIs, to report the result of its evaluations and a comparison between various concrete alternative proposals as soon as sufficiently details are available

• that it is essential that stakeholders and regulators discuss and assess (practical) targeting levels for GHG emission reductions from shipping, on both a short and long term basis

Further, INTERTANKO believes it is important to initiate the process of CO2 emission reduction from shipping as soon as possible and accepts that the initially agreed target levels might be adjusted as experience is gained

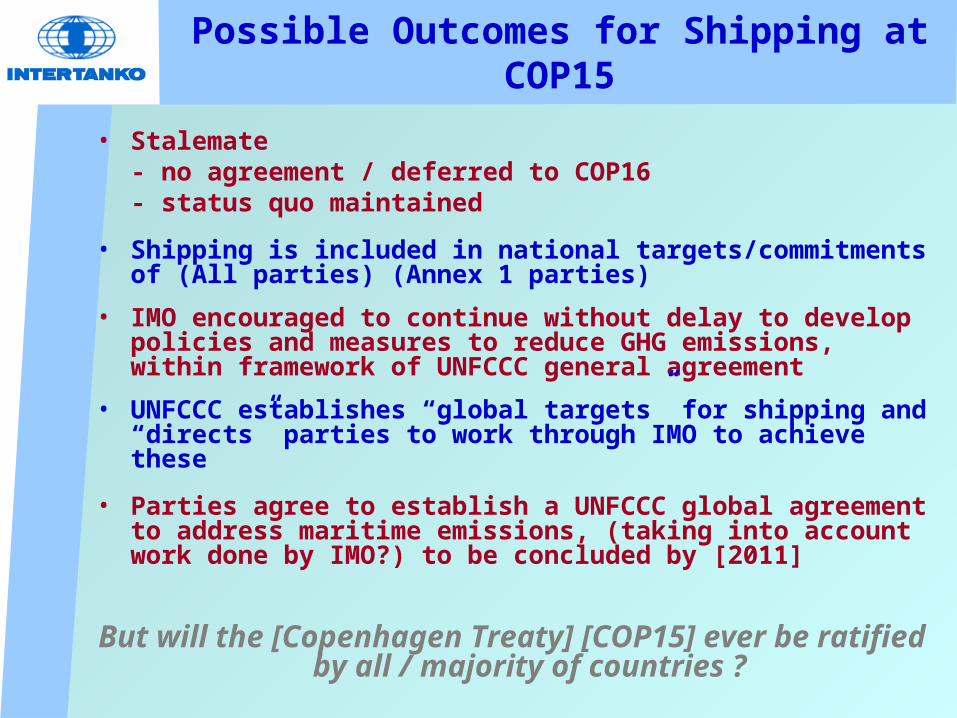

Possible Outcomes for Shipping at COP15

• Stalemate- no agreement / deferred to COP16- status quo maintained

• Shipping is included in national targets/commitments of (All parties) (Annex 1 parties)

• IMO encouraged to continue without delay to develop policies and measures to reduce GHG emissions, within framework of UNFCCC general agreement

• UNFCCC establishes “global targets” for shipping and “directs” parties to work through IMO to achieve these

• Parties agree to establish a UNFCCC global agreement to address maritime emissions, (taking into account work done by IMO?) to be concluded by [2011]

But will the [Copenhagen Treaty] [COP15] ever be ratified by all / majority of countries ?

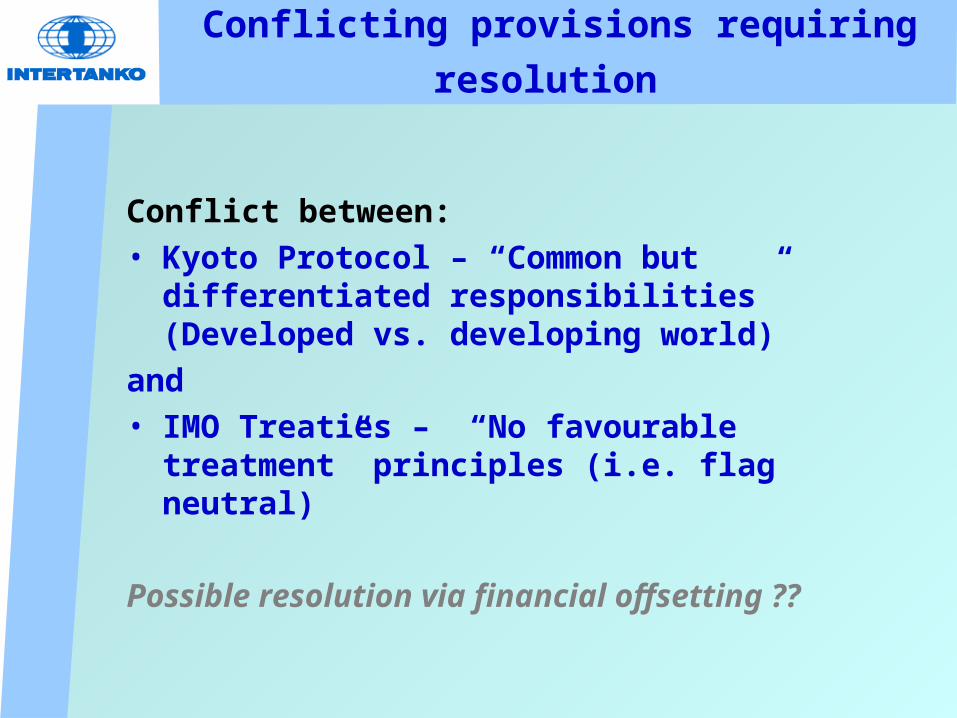

Conflicting provisions requiring resolution

Conflict between:• Kyoto Protocol – “Common but differentiated

responsibilities” (Developed vs. developing world)

and• IMO Treaties – “No favourable treatment”

principles (i.e. flag neutral)

Possible resolution via financial offsetting ??

Virtual Arrival

• Cooperation between Charterer (Terminal Operator) and Owner

• Speed is “optimised” when ship’s estimated arrival is before the terminal is ready

• Owners and Charterers agree a speed adjustment

• Uses independent 3rd party to calculate / audit adjustment

• Owners retain demurrage, while fuel savings and any carbon credits are split between parties

Next Steps:• OCIMF-INTERTANKO running joint workshops• Charter Parties being reviewed – indemnity and liability issues,

including bills of lading• Individual oil majors and owners “trialling” system• Bulk carrier sector examining feasibility

Piracy

Piracy / Armed Robbery

• Malacca Straits / South China sea

• Nigeria / Gulf of Guinea

• South America

• Somalia – Gulf of Aden /

W Indian Ocean

PIRACY - Gulf of Aden/Somali CoastINTERTANKO Activities

Providing members with topical information on events and best practice guidance and as part of industry’s liaison with the naval authorities, administrations and other organisations.

Activities include:

• Testimony to US Congress on International Piracy• Delegate with UN Contact Group and Working Groups

on Piracy• Industry spokesperson at Djibouti meeting finalising

regional code• Member IMO Correspondence Group revising MSC

Guidance Circulars• Providing MNLO Secondee to MSCHOA• Development of Industry Best Management Practices • Participation in Naval Shared Awareness and De-

Confliction (SHADE) Meetings

PIRACY - Gulf of Aden/Somali CoastINTERTANKO Activities

Activities include: (continued)

• Contributed to production of Anti--Piracy Charts• Developing Merchant Shipping Communication

Plan• Developed Piracy Model Clauses• Providing regular Security Bulletins to Members• Providing Routing Guidance• Developing Industry Positions on Arming of

Ships• Participating at Industry Seminars• Frequent contacts with national governments

Best Mangement Practices

Best Management Practices to Deter Piracy in the Gulf of Aden

and off the Coast of Somalia

(Version 2 - August 2009)

I n an effort to counter piracy in the Gulf of Aden and off the Coast of Somalia, these best management practices are

supported by the following international industry representatives:-

1. I nternational Association of I ndependent Tanker Owners (INTERTANKO)

2. I nternational Chamber of Shipping (ICS) 3. Oil Companies I nternational Marine Forum (OCIMF) 4. Baltic and International Maritime Council (BIMCO) 5. Society of I nternational Gas Tanker and Terminal Operators (SIGTTO) 6. I nternational Association of Dry Cargo Ship Owners (I NTERCARGO) 7. I nternational Group of Protection and Indemnity Clubs (I GP&I ) 8. Cruise Lines I nternational Association (CLI A) 9. I nternational Union of Marine I nsurers (I UMI ) 10. J oint War Committee (J WC) & J oint Hull Committee (J HC) 11. I nternational Maritime Bureau (IMB) 12 I nternational Transport Workers Federation (I TF) These best management practices are also supported by:- 1) Maritime Security Centre Horn of Africa (MSCHOA) 2) UK Maritime Trade Organisation (UKMTO Dubai) 3) Maritime Liaison Office (MARLO)

Practical Measures to Avoid, Deter or Delay

Piracy Attacks

“Our paramount concern is the safety of our seafarers”

PIRACY – Guidance for the Gulf of Aden / Somali Basin

Guidance for Gulf of Aden / Somalia

• Pre-transit:Assess RiskPlan self-protection/defensive measuresRegister Company and Ship with MSCHOAIF appropriate, join Group Transit

• During transit: Stay alertReport regularly to UKMTO, Dubai (or to MARLO)Follow “best management practices”

Criminalisation / Fair Treatment

Criminalisation- and unfair treatment

• Criminalisation

- “Find the guilty” culture rather than a thorough investigation of the cause

• Failure to adhere to IMO/ILO guidelines on “Fair Treatment of Seafarers” – in particular after a marine accident

Criminalisation- and unfair treatment

Examples include:

– Prestige (Spain) [Captain Mangouras: European Court of Human Rights]

– Tasman Spirit (Pakistan)

– Hebei Spirit (Korea)

– Tosa (Taiwan)

– Full City (Norway)

BUT also many more

Criminalisation- and unfair treatment

Actions by industry:

• Actively lobbying governments to adopt and implement the IMO/ILO Guidelines

• Challenging legislation that is not consistent with international treaty obligations (such as MARPOL, UNCLOS) and/or introduces criminalisation for accidents and simple negligence

• Speaking out in cases of unjustified detentions and criminal proceedings

Fuel Issues

Fuel Issues - EU

EU Directive 2005/33/EC requiring use of 0.1% Sulphur Marine Fuel at Berth

1 January 2010 Deadline - (Not aligned to MARPOL Annex VI)

Issues arising:Safety & technical ; 3 grades of fuel ; Supply (logistics)

INTERTANKO-OCIMF Position:• Delay in implementation (6 or 12 months) but subject

to verifying that compliance measures have been initiated

• Port State Control officials to be properly primedPosition is supported by class societies and insurers

Fuel Issues - US

CARB Fuel Requirements for Ocean-going Vessel Main (Propulsion) Diesel Engines, Auxiliary Diesel Engines, and Auxiliary Boilers

• Phase I effective 1 July 2009:

Marine gas oil (DMA) at or below 1.5% sulfur; or Marine diesel oil (DMB) at or below 0.5% sulfur

• Phase II effective 1 January 2012:

Marine gas oil (DMA) or Marine diesel oil (DMB) at or below 0.1% sulfur

ECA Proposed for North America

200 nm200 nm

200 nm200 nm

Thank you

For more information, please visit:www.intertanko.com

www.poseidonchallenge.comwww.shippingfacts.com

www.maritimefoundation.com

London, Oslo. Washington, Singapore and Brussels

United Nations Contact Group (CGPCS)

• Contact Group steers the overall programme • WG 1 : measures to improve the coordination of, and information

sharing between, the various naval forces present in the region and their interfacing with civilian shipping

• WG 2 : programmes to facilitate the prosecution of those caught and suspected of piracy

• WG 3: facilitates development of industry “Best Management Practices” to counter piracy and their application within the international shipping community

• WG 4 : communications and outreach strategies for use within

Somalia and to the wider international community as part of capacity building programmes - this latter to be in conjunction with other UN programmes already on the ground within the region

Piracy – Industry positions

Eliminating piracy is a SHARED RESPONSIBILITY between the maritime industry and governments,

BUT

Establishment of LAW AND ORDER on the high seas is the responsibility of governments

Our first concern is for the safety and welfare of our seafarers, both at sea and in port,

while also concerned for the security of our ships and their cargoes !

Role of Governments

• Provide and maintain sufficient assets in the region (EUNAVFOR, NATO, CTF, National Navies)

• Establish and ensure a coordinated approach (via SHaDE and Mercury)

• Establish and ensure a single, or at least compatible, rules of engagement (CGPCS)

• Develop necessary legal authorities to prosecute pirates (e.g. nationally or in third country such as Kenya)

• Develop a long term solution to the Somalia problem on land (CGPCS)

IMO Action

IMO Maritime Safety Committee (MSC) updated guidance to governments and industry

• MSC.1/Circ.1333 - PIRACY AND ARMED ROBBERY AGAINST SHIPS, “Recommendations to Governments for preventing and suppressing piracy and armed robbery against ships”

• MSC.1/Circ.1334 - PIRACY AND ARMED ROBBERY AGAINST SHIPS “Guidance to shipowners and ship operators, shipmasters and crews on preventing and suppressing acts of piracy and armed robbery against ships”

and issued• MSC Circulars endorsing the BMPs from the GCPCS

Arming Ships – Industry position

Armed guards or arming ships’ crews is NOT an INTERTANKO advocated approach

• Legal issues for flag states and port states• Serious potential safety concerns• Major liability and insurance issues in the event of

death or injury• Risk of collateral damage• Potential to provoke an escalation of fire power by

the pirates

Arming Ships

“ INTERTANKO believes that the use of armed guards, security forces or mercenaries onboard merchant ships has to be a matter for each individual owner or manager to assess as part of their own risk assessment, and as a consequence is unable to endorse any of those companies or individuals offering such services. “

Summary and Challenges

• Both industry and governments recognize that eliminating piracy is a shared responsibility and each is doing their part

• Significant progress has been made by both

• BUT, more must be done to eradicate piracy and we must work together to do it

• Maintaining assets and resources will be a challenge for both governments and industry associations over the medium/longer term

• Adherence to Best Management Practices is still incomplete

• Any escalation of activity/levels of violence will create new challenges

• The “solution” to the Somali problem stills seems very distant

• There is a risk that the “Somali” model is copied elsewhere