webinar slides: creative ways to structure bonus plans and ensure current tax deductions

TRANSCRIPT

#cbizmhmwebinar 1

CBIZ & MHM Executive Education Series™

Creative Ways to Structure Bonus Plans and Ensure Current Tax Deductions Priya Kapila and Phil Zaman August 19 and September 17, 2015

#cbizmhmwebinar 2

About Us

• Together, CBIZ & MHM are a Top Ten accounting provider • Offices in most major markets • Tax, audit and attest* and advisory services • Over 2,900 professionals nationwide

A member of Kreston International A global network of independent accounting firms

#cbizmhmwebinar 3

Before We Get Started…

• To view this webinar in full screen mode, click on view options in the upper right hand corner.

• Click the Support tab for technical assistance.

• If you have a question during the presentation, please use the Q&A feature at the bottom of your screen.

#cbizmhmwebinar 4

CPE Credit

This webinar is eligible for CPE credit. To receive credit, you will need to answer periodic participation markers throughout the webinar. External participants will receive their CPE certificate via email immediately following the webinar.

#cbizmhmwebinar 5

Disclaimer

The information in this Executive Education Series course is a brief summary and may not include all

the details relevant to your situation.

Please contact your service provider to further discuss the impact on your business.

CBIZ & MHM 6

Presenters

Priya Kapila is Senior Manager in the compensation consulting division

at CBIZ Human Capital Services. Ms. Kapila has participated in the

development of compensation plans for multiple organizations. During

her time with CBIZ, she has gained experience in market pricing,

developing and reviewing job analysis questionnaires, designing salary

structures, drafting compensation plan policies and procedures, and

structuring performance-based incentive programs for a variety of

positions within many industries. Recently, she has led the development

of analyses to test for compensation discrimination within public and

private organizations.

314.995.5558• [email protected]

Priya Kapila, CCP, SPHR Senior Manager, Compensation

Consulting Services

CBIZ & MHM 7

Presenters

Phil Zaman has over 18 years of experience in public accounting. As a

director in the CBIZ National Tax Office, he contributes as an author and

editor to the firm's tax thought leadership publications, oversees the

development and implementation of national tax policies and

procedures, and co-directs the firm's standardized tax technology

platforms. Phil also directs the learning programs for the tax practice

within CBIZ MHM, including the tax curriculum of the CBIZ MHM

National Level Training Program as well as the practice's webcast and

self-study programs.

816.945.5645 • [email protected] Phil Zaman, CPA Director

CBIZ & MHM 8

Agenda

Best Practices and Creative Approaches for Bonus Plan Design

02

01

03

Ensuring Current Tax Deductions for Accrued Bonuses

Questions

CBIZ & MHM 9

BEST PRACTICES AND CREATIVE APPROACHES FOR BONUS PLAN DESIGN

#cbizmhmwebinar 10

Variable Pay Overview

• Variable Pay is compensation that is contingent on discretion, performance, or results achieved

• More than 80% of U.S. organizations provide some form of short-term variable compensation, while over 50% have at least one long-term incentive plan

• Incentive prevalence and amounts have grown in recent years • Driven by cost control and retention efforts • Nearly two-thirds of business executives indicate talent

acquisition and retention is the top HR goal

Sources: WorldatWork Salary Budget Survey 2015-2016; Harvard Business Review

#cbizmhmwebinar 11

Types of Incentive Plans

Bonuses

• Discretionary or Project-based

• Goal: Recognition

Annual Incentives

• Performance- and Time-based

• Goal: Motivation

Long-term Incentives

• Performance- and Time-based

• Goal: Retention

#cbizmhmwebinar 12

Incentive Eligibility

• Considerations: • Compensation Philosophy • Plan Purpose and Objectives • Ability to Influence Results • Job Function and Level • Market-competitiveness of Incentive Awards • Incentive Type and Value

#cbizmhmwebinar 13

Pay Mix

• Base salary: The annual fixed rate that an individual is paid for performing a job.

• Short-term/Annual incentives: At-risk cash compensation awarded to employees on an annual or more frequent basis. The sum of base salary and short-term incentives is typically defined as total cash compensation.

• Benefits: Non-cash compensation provided to an employee. Some benefits are required by law (e.g., payroll taxes, unemployment compensation and workers compensation) while others may be provided at the discretion of an employer (e.g., medical care, life insurance, paid time off, retirement plans, etc.).

• Perquisites: Any benefit that is offered to only a subset of the broader employee population. Prevalent perquisites include a company car, supplemental life and/or medical insurance and country club dues.

• Long term incentives: Compensation (cash, stock, phantom stock, etc.) typically earned as a bonus for performance which is measured over a multi-year period (typically 3-5 years).

#cbizmhmwebinar 14

Pay Mix

Non-Executive

Base Salary

AnnualIncentivesBenefits &PerquisitesLong-termIncentives

Executive

#cbizmhmwebinar 15

• Corporate vs. Individual • Qualitative vs. Quantitative

• Corporate and individual performance measures should be weighted by the relative ability to impact performance

Recommended Target Bonus Payout

Job Level (% of Base Salary) Corporate IndividualC-Suite 40.0% 100% 0%Vice Presidents 25.0% 80% 20%Middle Management 18.0% 60% 40%Supervisors 12.0% 40% 60%Professional Staff 10.0% 20% 80%Hourly Staff 5.0% 0% 100%

% Based On Goals

Performance Measures

#cbizmhmwebinar 16

Performance Measures

• Corporate Measures • Financial

• Examples: Sales growth, Profitability, Stock Price • Customer Satisfaction

• Examples: Product Development and Promotion, Customer Feedback

• Process Improvement • Examples: Quality Enhancement and Controls,

Productivity

• Corporate measures are generally limited to 2-5

#cbizmhmwebinar 17

Performance Measures

• Financial

-Revenue Growth

-Raising Capital

-Revenue Growth

-Profitability

-Cash Flow

-Return Measures

-Profitability

-ROC

-Cash Flow

-Cost Control

-Cash Flow

-ROC

-Cost Control

#cbizmhmwebinar 18

Performance Measures

• Customer Satisfaction

-Brand Awareness

-Market Penetration

-Customer Satisfaction

-Market Share Growth

-Production Ramp-up

-Maintain Market Share

-Customer Perceptions

-Customer Retention

-Product Revitalization

#cbizmhmwebinar 19

Performance Measures

• Process Improvement

-Production Milestones

-Process Efficiency

-Production Capability

-Quality Control

-Process Improvements

-Quality Control and Enhancement

-Process Improvements

-R&D/Innovation

#cbizmhmwebinar 20

Performance Measures

• Individual Measures • Production • Quality • Customer Service • Competencies • Job Performance

• Team or Department Measures

#cbizmhmwebinar 21

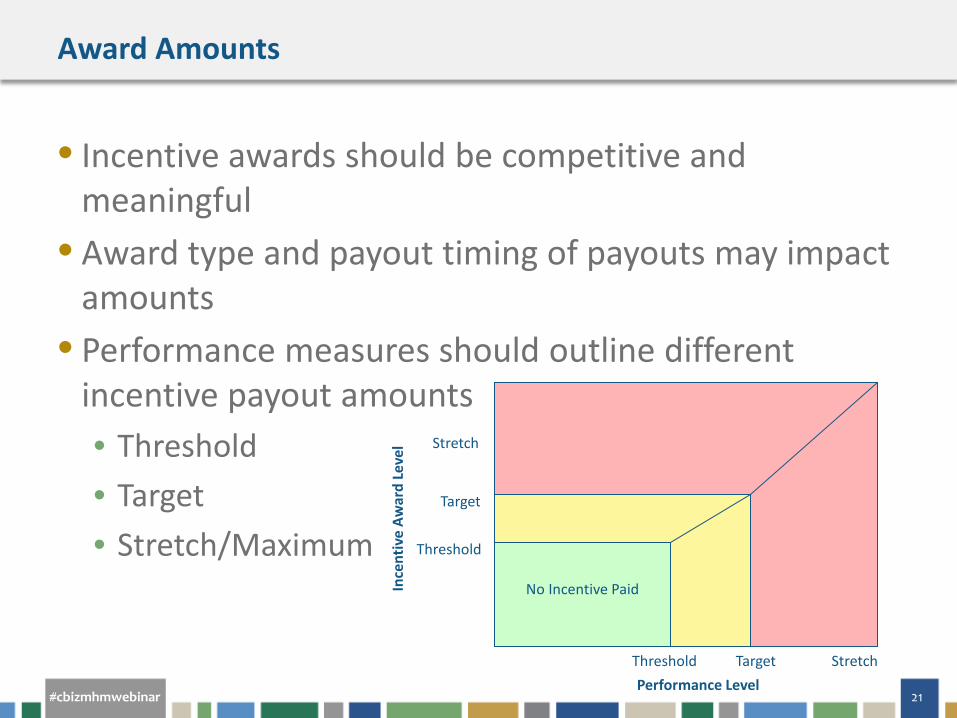

Award Amounts

• Incentive awards should be competitive and meaningful

• Award type and payout timing of payouts may impact amounts

• Performance measures should outline different incentive payout amounts • Threshold • Target • Stretch/Maximum

Threshold

Target

Stretch

Stretch Threshold

Target

No Incentive Paid

Performance Level

Ince

ntiv

e Aw

ard

Leve

l

#cbizmhmwebinar 22

Award Amounts

• Incentive award amounts should reflect the total compensation philosophy • Who does the organization attract employees from and

lose employees to? (i.e., “the market”) • How should the organization compare to the market?

• Various resources may be used to determine amounts • Compensation surveys • Competitive peer data • Historical incentive awards

#cbizmhmwebinar 23

Award Amounts

• Incentive Plan Funding • Budgeted • Self-funded

• Funding Considerations: • Hurdles • Payout Scenarios (Worst Case and Windfalls)

#cbizmhmwebinar 24

Award Amounts

• Example

• Performance Measures and Benchmark Levels

• Incentive Award Payout Levels

Threshold Target Stretch

Threshold 10% 15% 20%

Target 15% 18% 24%

Stretch 20% 24% 30%

Return on Assets Performance

Tota

l Ass

et

Grow

th

Perfo

rman

ce

Weight Threshold Target StretchReturn on Assets 50.0% 1.0% 2.5% 4.0%Total Asset Growth 50.0% 5.0% 10.0% 20.0%

#cbizmhmwebinar 25

Incentive Plan Communication

Communication is critical! • Performance measures should be established prior to

or at the beginning of the period • Distribute plan document to employees • Share progress frequently • Provide periodic feedback on individual performance • Announce results in advance of awards

#cbizmhmwebinar 26

Incentive Plan Effectiveness

• Evaluating the incentive plan’s effectiveness should begin several months before the next performance period

• Consider all stakeholder perspectives • Possible Results of Evaluation:

• Continuance • Refinement • Termination

#cbizmhmwebinar 27

ENSURING CURRENT TAX DEDUCTIONS FOR ACCRUED BONUSES

#cbizmhmwebinar 28

What’s the Issue?

• Taxpayer & tax practitioner assumption – If bonuses are paid within 2 ½ months after year-end, the bonuses are deductible in year services rendered

• IRS has issued several rulings in the past few years indicating that is not necessarily the case

• Rulings detail hurdles that will be difficult for many taxpayers to clear without modifications to bonus programs

• Accounting method changes may be necessary

#cbizmhmwebinar 29

When are Bonuses Deductible?

• Bonuses are deductible in the tax year in which: 1. All events have occurred that establish the fact of

the liability 2. The amount must be determined with reasonable

accuracy 3. Economic performance has occurred (i.e., the

services were rendered)

#cbizmhmwebinar 30

When are Bonuses Deductible?

• Other restrictions: • Compensation to related party taxpayers deductible in

year paid • Compensation paid more than 2 ½ months after year-

end deductible in year paid

#cbizmhmwebinar 31

When are Bonuses Deductible?

• Bonuses are deductible in the tax year in which: 1. All events have occurred that establish the fact of

the liability 2. The amount must be determined with reasonable

accuracy 3. Economic performance has occurred (i.e., the

services were rendered)

#cbizmhmwebinar 32

Situations Where Fact of Liability NOT Established by Year End

• Employee must still be employed on day bonus is paid to receive his or her bonus and unpaid bonuses revert back to employer

• Company reserves right to modify or cancel bonuses at any time prior to payment

• Bonuses must be approved by e.g., Board of Directors and approval doesn’t take place until after year end

• Bonus formula based in part on employee performance reviews which do not take place until after year end

#cbizmhmwebinar 33

Example 1 – Forfeited Bonus Reverts to Employer

• Facts: • Bonus accrued at year end pursuant to formula based

on performance metrics • Employee must be employed on date bonus paid to

receive compensation • Amounts not paid to employees due to termination

revert back to employer • Conclusion:

• Fact of liability isn’t established until bonus paid

#cbizmhmwebinar 34

Example 2 – Forfeited Bonus Allocated to Other Employees

• Facts: • Bonus accrued at year end pursuant to formula based

on performance metrics • Employee must be employed on date bonus paid to

receive compensation • Amounts not paid to employees due to termination

were reallocated to other employees in bonus pool • Conclusion:

• Fact of liability is established at year end • Fact that identity of a bonus recipient is not known at

year end does not prevent the fact of the liability from being established

#cbizmhmwebinar 35

Example 3 – Forfeited Bonus after Certain Date Revert to Employer

• Similar Facts as Example 2, except: • In February, section manager allocates bonus pool

among employees • Any employees terminated since year end forfeit bonus

and amount is reallocated to other employees • If employee terminates after the allocations are

determined, unpaid bonus reverts back to employer • Conclusion:

• Fact of liability isn’t established until bonus paid

#cbizmhmwebinar 36

Public Companies Face Additional Challenges

• Performance-based compensation must meet certain conditions to avoid the §162(m) $1 million deduction limitation

• The plan may not allow for discretion to increase bonuses (i.e., forfeited bonuses cannot be reallocated to other covered employees)

• Compensation committee would need to certify by year end that performance goals have been met

#cbizmhmwebinar 37

Ways to Establish Fact of Bonus Liability by Year End

• Do not require that employee be employed at time bonus is paid • Otherwise, reallocate forfeited bonuses to other

employees • Ensure any actions impacting the bonus formula take

place by year end (e.g., performance reviews) • Allow only until year end the ability to reduce or

eliminate bonuses • Ensure any bonus approvals take place by year end • Use minimum bonus strategy to protect portion of

deduction while providing some flexibility

#cbizmhmwebinar 38

What if We Choose Not to Restructure Bonus Plan?

• Deducting bonuses in a year prior to when the fact of the liability is established is an improper accounting method

• Change accounting method to begin deducting bonus in year paid

• Automatic accounting method change # 133 • Form 3115 • Due by the extended due date of tax return • No user fee • Audit protection • Four year spread of deduction recapture

#cbizmhmwebinar 39

Automatic Accounting Method Change # 133

• Taxpayer must qualify under automatic change procedures: • Must be compliant with §263A with respect to bonuses • Must not have requested change with respect to

bonuses within prior five years • Additional restrictions apply if under IRS audit

• Benefits of automatic change provisions: • Form 3115 due by the extended due date of tax return • No user fee • Audit protection • Four year spread of deduction recapture

#cbizmhmwebinar 40

? QUESTIONS

#cbizmhmwebinar 41

If You Enjoyed This Webcast…

Upcoming courses: • 8/20 & 9/1: How to Make the Most Out of Derivatives and Hedging

• 8/27 & 9/11: PPA Plan Restatement - Emerging Opportunities for Pre-Approved Plans

• 9/8 & 11/11: Revenue Recognition Updates for Manufacturers

• 9/17: Controlling and Managing Healthcare Costs - Practical Guidance to Maximize Value

• 9/17: Creative Ways to Structure Bonus Plans and Ensure Current Tax Deduction

Recent Thought Leadership: • Enhance Your Organization's Cybersecurity Strategy

• Proposed Changes to Family Valuation Discounts

• Six Ways the AICPA Plans to Improve Audit Quality

• Modifications Coming to Inventory Measurement

#cbizmhmwebinar 42

Connect with Us

linkedin.com/company/ mayer-hoffman-mccann-p.c.

@mhm_pc

youtube.com/ mayerhoffmanmccann

slideshare.net/mhmpc

linkedin.com/company/ cbiz-mhm-llc

@cbizmhm

youtube.com/ BizTipsVideos

slideshare.net/CBIZInc

MHM CBIZ