wealth management

TRANSCRIPT

Partner Wealth Management

Mark O’Reilly

Using History as a Guide

If you have a client logo or other co-branding to include, this should go here. It should never be larger than the Deloitte logo.

Wealth Management

Using History as Our Guide

Mark O’Reilly, FIA

2©2014. For information, contact Deloitte China.

Asset Classes Property (real estate)

Equities (domestic, international)

Bonds

Annuities

Cash or “near cash”

Decisions How to allocate

What vehicles to use

How frequently to review

Wealth ManagementWhat We Can Invest In

3©2014. For information, contact Deloitte China.

EquitiesWhat Can We Reasonably Expect?

1

10

100

1,000

10,000

100,000

1,000,000

10,000,000

1871

1875

1879

1883

1887

1891

1895

1899

1903

1907

1911

1915

1919

1923

1927

1931

1935

1939

1943

1947

1951

1955

1959

1963

1967

1971

1975

1979

1983

1987

1991

1995

1999

2003

2007

2011

S&P500 Adjusted for Inflation, 1871-2015

Over 200 years, stockmarkets have show great volatility from year to year, but have proved much more consistent for periods of twenty+ years.

If history is any guide, they offer the best foundation for long-term (30 years+) years of investing

We use the S&P500 as an example because:

It represents 75% of the stock value in the USA;

The US market is one of the oldest and has been least affected by wars, civil unrest, etc.

It remains 38% of global exchanges and 50% of global indexes

4©2014. For information, contact Deloitte China.

EquitiesS&P500: Periods of the Best and Worst Returns

Period(Inclusive) Years Real Nominal Real Nominal1871-2014 144 7% 9% 1,501,528$ 28,159,836$ 1948-1965 18 14% 16% 1,060$ 1,422$ 1982-1999 18 15% 19% 1,216$ 2,176$ 2009-2014 6 15% 17% 235$ 260$ 2000-2008 9 -6% -4% 57$ 71$ 1966-1974 9 -5% 0% 61$ 99$ 1966-1981 16 -1% 6% 84$ 250$ 1929-1932 4 -16% -22% 49$ 37$ 1929-1947 19 1% 1% 121$ 121$

Annualized Return $100 Becomes

There is no pattern to bull or bear markets, and the effects of inflation upon “real” returns can vary greatly (real return = nominal return adjusted for consumer prices)

Return = appreciation + dividends. Does not reflect trading costs which were very substantial until the 1980s and remained substantial until the 2000s

"Stock prices have reached what looks like a permanently high plateau." Irving Fisher, October 21, 1929

5©2014. For information, contact [Legal name and branch name]. (Go Header & Footer to edit this text)

Equities

11.6%The annual return on the S&P500 over the

last 30 years

3.8%The annual return

earned by stock mutual-fund investors over the

last 30 years*

2.7%The annual rate of price inflation over the last 30

years

1.8%The annual return earned

by asset-allocation mutual-fund investors over the last

30 years*

“The overwhelming driver is bad timing by investors.”

“It would also help to design products that give an incentive not to bail out at the wrong moment.”

John Authers, The Financial Times

* Quantitative Analysis of Investor Behavior published by the US market research group Dalbar

The Dangers of Following the Market’s Momentum

6©2014. For information, contact Deloitte China.

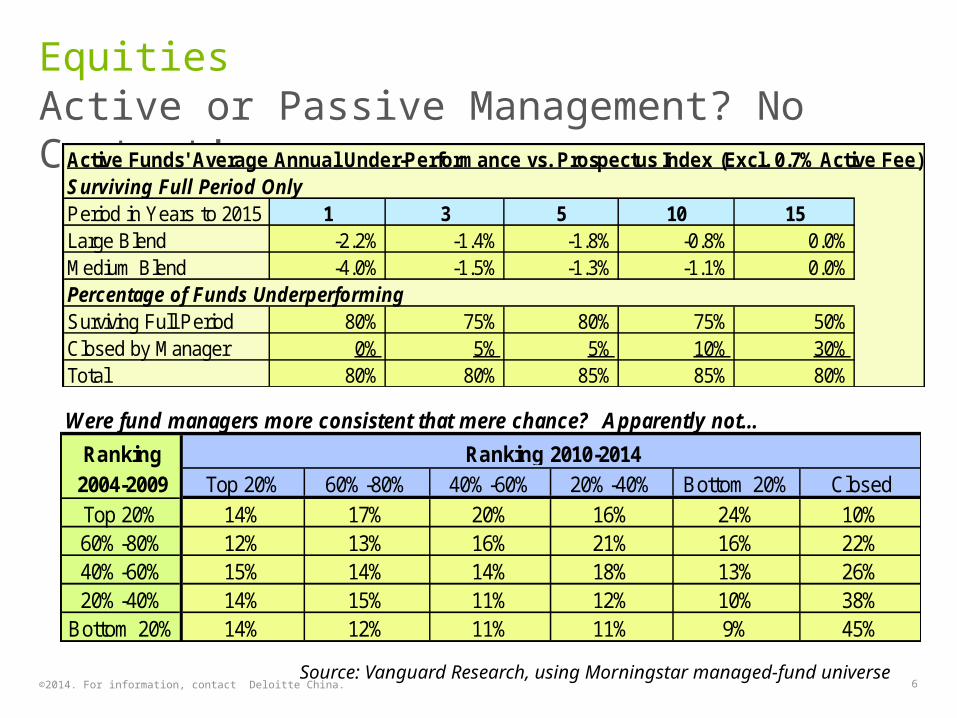

EquitiesActive or Passive Management? No Contest!

Active Funds' Average Annual Under-Performance vs. Prospectus Index (Excl. 0.7% Active Fee)Surviving Full Period OnlyPeriod in Years to 2015 1 3 5 10 15Large Blend -2.2% -1.4% -1.8% -0.8% 0.0%Medium Blend -4.0% -1.5% -1.3% -1.1% 0.0%Percentage of Funds UnderperformingSurviving Full Period 80% 75% 80% 75% 50%Closed by Manager 0% 5% 5% 10% 30%Total 80% 80% 85% 85% 80%

Source: Vanguard Research, using Morningstar managed-fund universe

Were fund managers more consistent that mere chance? Apparently not…Ranking

2004-2009 Top 20% 60%-80% 40%-60% 20%-40% Bottom 20% ClosedTop 20% 14% 17% 20% 16% 24% 10%60%-80% 12% 13% 16% 21% 16% 22%40%-60% 15% 14% 14% 18% 13% 26%20%-40% 14% 15% 11% 12% 10% 38%

Bottom 20% 14% 12% 11% 11% 9% 45%

Ranking 2010-2014

©2014. For information, contact Deloitte China. 7

How Expensive is the Current Market?Equities

The Shiller S&P500 PE Ratio*

Current Value: 24.6 Mean:16.6 Median: 16.0 Min: 4.8 Max: 44.2

Source: Robert Shiller, Yale University

* Uses average inflation-adjusted earnings from prior ten years

0

5

10

15

20

25

30

35

40

45

50

01-J

an-0

201

-Jan

-05

01-J

an-0

801

-Jan

-11

01-J

an-1

401

-Jan

-17

01-J

an-2

001

-Jan

-23

01-J

an-2

601

-Jan

-29

01-J

an-3

201

-Jan

-35

01-J

an-3

801

-Jan

-41

01-J

an-4

401

-Jan

-47

01-J

an-5

001

-Jan

-53

01-J

an-5

601

-Jan

-59

01-J

an-6

201

-Jan

-65

01-J

an-6

801

-Jan

-71

01-J

an-7

401

-Jan

-77

01-J

an-8

001

-Jan

-83

01-J

an-8

601

-Jan

-89

01-J

an-9

201

-Jan

-95

01-J

an-9

801

-Jan

-01

01-J

an-0

401

-Jan

-07

01-J

an-1

001

-Jan

-13

01-J

an-1

6

©2016. For information, contact Deloitte China 8

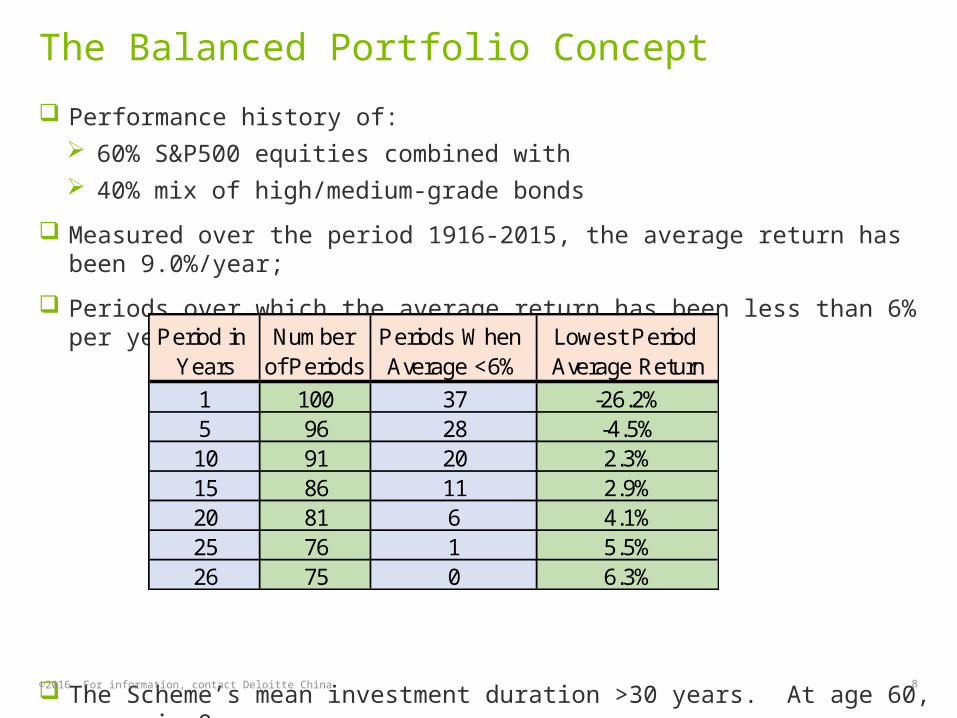

The Balanced Portfolio Concept

Performance history of: 60% S&P500 equities combined with 40% mix of high/medium-grade bonds

Measured over the period 1916-2015, the average return has been 9.0%/year;

Periods over which the average return has been less than 6% per year:

The Scheme’s mean investment duration >30 years. At age 60, yours is 8 years

.

* Source: NYU Stern School of Business, US Federal Reserve

Period in Years

Number of Periods

Periods When Average <6%

Lowest Period Average Return

1 100 37 -26.2%5 96 28 -4.5%10 91 20 2.3%15 86 11 2.9%20 81 6 4.1%25 76 1 5.5%26 75 0 6.3%

©2014. For information, contact Deloitte China. 9

How to Choose the Equities?Bonds with Equities

Like the S&P500 tracks 75% of the US stockmarket, there are indexed funds which track the global equity market, in proportion to its freely tradable market capitalization. For example, the FTSE* Global All Cap Index (GACI) differs from the market cap of global exchanges as follows:

Country/Exchange Index ExchangesUnited States 51% 38%United Kingdom 7% 9%Japan 8% 7%China (incl HK) 4% 14%Other Europe 14% 13%Australia/Canada 6% 4%Other 10% 15%Total 100% 100%

An advantage of choosing the global market is avoiding making “bets” on which local market performs best. For freely traded stocks, current prices represent the consensus of global investors, so any apparent advantage is already “priced in” at this consensus.

* FTSE Group, subsidiary of the London Stock Exchange (FTSE30 and FTSE100 are the LSE’s primary benchmarks)

A low-cost tracker fund for the GACI is Vanguard Total World Stock Fund (VT)

©2014. For information, contact Deloitte China. 10

How to Choose the Bonds?Bonds with Equities

An important first step is to understand the nature of the bond market

Term/ DefaultBond Types Risk Level Source 10/06/2015 17/04/2015 Rate /Year "BND"

Treasuries "Risk free" 10y 2.5% 1.7% NilTreasuries "Risk free" 20y 3.0% 2.3% NilTIPS "Risk free"/Inflation-linked 20y 1.0% 0.4% NilAAA Very high quality Fed. 4.3% 3.4% Negligible 6%AA High quality est. 4.6% <0.1% 4%A Upper medium quality est. 4.9% 0.10% 13%BBB (Baa) Medium quality Fed. 5.2% 4.4% 0.40% 14%"Junk" Below medium quality Fund 6%+ >2%? Nil

Yield

63%

A deeper look into US bonds…

US Bond MarketBond Type 2007 2015Treasuries 14% 32%Other Government 20% 15%Corporate 17% 20%Mortgage/Asst-backed 36% 26%Money Market 14% 7%Total US$ trillions $31.7 $39.2

Global Financial AssetsAsset Type 2007 2008 2014Equities 27% 15% 23%Government bonds 14% 17% 20%Corporate bonds 33% 37% 31%Other loans 26% 31% 26%Total US$ trillions $242 $222 $294

©2014. For information, contact Deloitte China. 11

Mutual Funds vs. Exchange-Traded Funds (ETFs)Bonds with Equities

Mutual Fund

Since 1920s1970s: 400 funds, $50BN2015: >15,000 US funds, $17TN $30TN worldwide 22% US household wealth

Open-ended fund invested according to prospectus (active or indexed)

Price valuation, purchase and sales can occur only at market closeLowest management fee: 0.05%

ETF

Since 1990s201%: >1,500 US funds, $2TN

Open-ended fund invested according to prospectus. Will seek to match a given index of equities or bonds (includes international, commodity and industry sectors.)

Funds are listed in exchange, starting at portfolio value but thereafter according to trades of market-makers, i.e rely upon market efficiency.Lowest management fee: 0.05%

©2014. For information, contact Deloitte China. 12

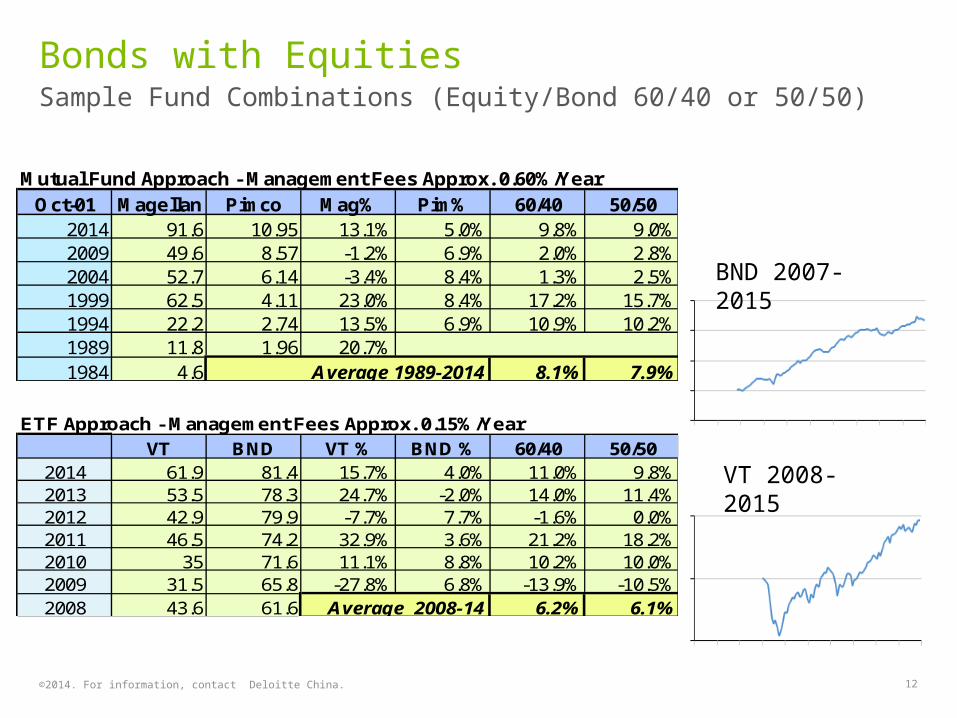

Sample Fund Combinations (Equity/Bond 60/40 or 50/50)Bonds with Equities

ETF Approach - Management Fees Approx. 0.15%/YearVT BND VT % BND % 60/40 50/50

2014 61.9 81.4 15.7% 4.0% 11.0% 9.8%2013 53.5 78.3 24.7% -2.0% 14.0% 11.4%2012 42.9 79.9 -7.7% 7.7% -1.6% 0.0%2011 46.5 74.2 32.9% 3.6% 21.2% 18.2%2010 35 71.6 11.1% 8.8% 10.2% 10.0%2009 31.5 65.8 -27.8% 6.8% -13.9% -10.5%2008 43.6 61.6 Average 2008-14 6.2% 6.1%

Mutual Fund Approach - Management Fees Approx. 0.60%/YearOct-01 Magellan Pimco Mag% Pim% 60/40 50/50

2014 91.6 10.95 13.1% 5.0% 9.8% 9.0%2009 49.6 8.57 -1.2% 6.9% 2.0% 2.8%2004 52.7 6.14 -3.4% 8.4% 1.3% 2.5%1999 62.5 4.11 23.0% 8.4% 17.2% 15.7%1994 22.2 2.74 13.5% 6.9% 10.9% 10.2%1989 11.8 1.96 20.7%1984 4.6 Average 1989-2014 8.1% 7.9%

VT 2008-2015

BND 2007-2015

13©2014. For information, contact Deloitte China.

PropertyGlobal ValuationsFirst Half 2014, Financial Times Survey

CityPrice To Income Ratio

Gross Rental

Yield City Centre %

Gross Rental Yield

Outside of Centre %

Price To Rent Ratio

City Centre

Price To Rent Ratio Outside Of

City Centre

Mortgage as Percentage Of Income

%

Beijing, China 33.6 2.7 2.7 36.6 37.8 290Hong Kong, Hong Kong 29.0 3.0 2.9 33.2 34.6 189Guangzhou, China 27.6 2.8 2.5 36.2 39.4 224Shenzhen, China 27.4 2.9 3.5 34.8 28.8 265Shanghai, China 27.4 3.2 3.5 31.2 28.4 242Singapore, Singapore 21.6 3.9 4.2 25.7 23.7 136Paris, France 16.6 2.7 2.9 37.1 34.6 116London, United Kingdom 16.2 3.9 4.2 25.9 23.9 120Barcelona, Spain 13.2 3.4 4.0 29.1 25.3 88Munich, Germany 11.6 3.0 3.6 33.7 28.0 81Amsterdam, Netherlands 9.4 4.8 4.9 21.0 20.6 70San Francisco, CA, United States 9.4 6.2 5.5 16.1 18.3 69Sydney, Australia 8.6 5.3 5.5 18.9 18.3 72Tokyo, Japan 8.2 5.8 4.1 17.3 24.5 50New York, NY, United States 8.1 6.2 7.9 16.1 12.7 59Brussels, Belgium 6.0 5.9 6.7 16.8 15.0 43Frankfurt, Germany 4.9 4.0 4.5 24.8 22.4 32Boston, MA, United States 3.5 12.7 11.6 7.9 8.7 25Chicago, IL, United States 3.3 11.3 12.9 8.8 7.8 25Philadelphia, PA, United States 2.7 12.0 12.7 8.3 7.9 20

14©2014. For information, contact Deloitte China.

PropertyDemographic Headwinds (Source: United Nations)

Japan

Females 20-29 60-74 75+1975 100% 100% 100%1980 85% 114% 129%1985 80% 117% 136%1990 84% 121% 144%1995 93% 124% 151%2000 91% 128% 159%2005 80% 132% 168%

Selected Age Groups

-

5,000

10,000

15,000

20,000

25,000

30,000

JAPAN - Females, Selected Age Groups

20-29 60-74 75+

Females 20-29 60-74 75+1995 100% 100% 100%2000 88% 110% 112%2005 82% 112% 116%2010 97% 113% 120%2015 96% 115% 124%2020 75% 118% 128%2025 62% 120% 132%

Selected Age Groups

China

-

50,000

100,000

150,000

200,000

250,000

CHINA - Females, Selected Age Groups

20-29 60-74 75+

40% drop for ages 25-29

15©2014. For information, contact Deloitte China.

PropertyREITs are a Means to Invest in Property through Tradable Equity

To qualify as a US REIT: >=75% assets in real estate >=75% gross income from

rents, mortgages, financing & sales of real property

>=90% of taxable income paid as dividends

Be managed by a board of directors or trustees

<=50% shares held by five individuals Industry Type US Index

Retail 25%Residential 17%Office 16%Healthcare 14%Hotel 7%Factory 4%Other 17%

Global Ex-USA

USA

Comparing Returns at 31/3/15Period US REITs S&P500

1 year 24.2% 12.7%3 years 14.2% 16.1%5 years 15.9% 14.5%10 years 9.8% 8.0%

S&P Global ex-U.S. Property IndexCompany %

Mitsubishi Estate Co Ltd 3.4MITSUI FUDOSAN CO LT 3.0CKH Food & Health Limited 2.9Sun Hung Kai Properties Ltd 2.8Unibail-Rodamco SE 2.8SUMITOMO REALTY & DE 1.9CHINA OVERSEAS LAND& 1.7Scentre Group 1.6Land Securities Group PLC 1.6Daiwa House Industry Co Ltd 1.5

Region AllocationPacific 51%Europe 23%Emerging 20%Other 6%

Unlike direct property ownership, REIT prices respond immediately to

investors’ views on future earnings, often leveraged by the REITs’ borrowing