volatility and directional information-based trading in ... · volatility and directional...

TRANSCRIPT

Volatility and Directional Information-Based Trading in

Options

Yong Jin Mahendrarajah Nimalendran Sugata Ray1

JEL Classifications: D53, G12, G28

Keywords: Option market microstructure, Probability of informed volatility

trading (VolPIN), Probability of informed direcitonal trading (DirPIN), PIN

December 10, 2013

1Yong (Jimmy) Jin, Mahendrarajah Nimalendran, and Sugata Ray, Warrington College of BusinessAdministration, University of Florida, P.O. Box 117168, University of Florida, Gainesville FL 32611-7168. Jin: [email protected]; Nimalendran: [email protected]; Ray: [email protected];.

Volatility and Directional Information-Based Trading in

Options

Abstract

We develop a sequential trade model and estimate the probability of volatility information

trading (V olPIN) and the probability of directional information trading (DirPIN) in the

options market using high frequency individual stock options data. We find that informed

trading in options has a significant impact on price discovery of the underlying asset and

market microstructure of the options market. In particular, DirPIN has a positive effect on

stock returns and a stock with a 10 % higher DirPIN relative to the average DirPIN leads

to a 1.8% per year increase in expected returns; V olPIN predicts future unpriced volatility.

Both PIN measures are significant determinants of option spreads, explaining up to 30% of

the bid-ask spread.

1 Introduction

The process by which information is revealed through trading has been studied extensively.2

Most of this research focuses on directional information, with much less attention given to

the question of how and where information concerning volatility is revealed.3 Compelling

evidence from the time-series and option-pricing literatures indicates that volatility is time-

varying and stochastic. Also, there is a large literature on the relation between future

volatility and option implied volatility. Yet we know little about the extent to which new

information about future volatility is revealed through the trading process. Presumably,

investors with private information about volatility will trade in instruments whose price is

sensitive to volatility, an obvious choice being the options market.4

In this paper, we investigate information based trading on the options market. We

propose a structural model in the spirit of Easley, Kiefer, O’Hara, and Paperman (1996)

and Easley, Hvidkjaer, and O’Hara (2002) to measure the probability of both volatility and

directional information based trading on the options market.5 The model assumes that each

period, there is some probability of an information event. Conditional on the informational

event, the information can be either about volatility or direction with a certain probability,

further we condition the volatility and directional information based on whether it is bullish

or bearish. This results in traders placing orders in accordance with the newly created

information structure, resulting in a rich sequential trade model. Using high frequency

transaction level data and trade direction (buyer initiated and seller initiated) for calls

and puts on individual stock options we estimate the model using maximum likelihood

techniques and obtain separate estimates for the the probabilities of volatility and directional

information-based trading in individual stock options.

Informed directional traders will buy calls and/or sell puts if they are bullish on the price

and sell calls and buy puts when bearish. In contrast, informed volatility traders will buy

calls and buy puts (a straddle) if they are bullish on volatility and sell straddles if they are

2Theoretical underpinnings of this literature include Glosten and Milgrom (1985), Kyle (1985), and Easley,Kiefer, O’Hara, and Paperman (1996) Empirical work in this area is described in Hasbrouck (1995).

3In our study, directional information refers to information about whether a stock price is going up ordown. Volatility information refers to information regarding the future volatility of a stock either increasingor decreasing.

4Recently there have been ETFs on VIX as well as futures on VIX that can be traded. However, we arenot aware of securities on individual stock volatility.

5 Ni, Pan, and Poteshman (2008) [NPP] also investigate informed trading on volatility in the optionsmarket using daily net non-market maker trading volume on calls and puts to construct a measure fortrading on volatility information. We discuss the differences in our studies and findings in the followingsection.

1

bearish. In addition there will be noise or uninformed traders who will be buying and selling

calls and puts. These trading choices provide identification to estimate separate probabilities

of informed trading for directional and volatility trading, which we term DirPIN , and

V olPIN , respectively.

We validate our estimated V olPIN and DirPIN measures by confirming that they

are correlated with intuitively linked observable variables. For example, periods with high

V olPIN are followed by periods with high absolute unpriced volatility (|realized volatility

minus option price implied volatility|). Similarly, we find DirPIN is positively correlated

with the Easley, Kiefer, O’Hara, and Paperman (1996) stock PIN measure, with a correla-

tion of 0.22, while V olPIN has a weaker correlation of .09. We also find that V olPIN and

DirPIN are higher prior to earnings announcements.

We use the estimatedDirPIN and V olPIN together with stock PIN to estimate relative

contributions to asset returns, and bid-ask spreads. We find that the V olPIN and DirPIN

are both significantly related to option market bid-ask spreads. A one standard deviation

(.066) increase in the V olPIN increases relative bid ask spreads by 0.34% and a one standard

deviation (.066) increase in DirPIN increases relative bid ask spreads by 0.73%. Based on

an average spread of 5.8% in the options market, the effect of one standard deviation increase

in volatility and directional information risks in options lead to a 18% increase in spreads.

We also find that the DirPIN is positively linked to future abnormal returns for the

stock. Following the model outlined in Easley, Hvidkjaer, and O’Hara (2002), investors

holding stocks with higher amount of informed trading expect a higher return for the in-

formational risks they face. We find that a stock with a 10% higher DirPIN is associated

with a 1.8% increase in expected returns. The V olPIN does not significantly affect stock

returns. Easley, Hvidkjaer, and O’Hara (2002) find a similar link with the stock PIN as

our findings regarding the DirPIN , documenting a 2.5% higher return for stock with a 10%

larger stock PIN . Interestingly, in our study, the stock PIN is not a significant determinant

of expected returns returns based on Fama-MacBeth regression model. This may be due to

our using only the largest stocks, where more informed trading may be carried out in the

option markets, or a difference in time periods used for the sample.

Our findings are consistent with informed trading in option markets affecting both the

market microstructure of the options market and also future asset returns. Our main contri-

butions are: (1) The construction and estimation of a information risk measure for options

markets, (2) a decomposition of option market bid/ask spreads to include the effects of

asymmetric information about both direction and volatility, as well as the hedging and re-

balancing costs associated delta hedging, (3) linking the directional DirPIN measure from

2

option markets to asset returns, and (4) documenting information-based trading prior to

earnings announcements.

2 Literature review

There is a rich literature covering directional informed trading and its link to market mi-

crostructure 6. The literature examining directional informed trading in both stock and

option markets is narrower, with theoretical roots in Easley, O’hara, and Srinivas (1998)

which proposes a theoretical model, with directionally informed traders choosing between

stock and option markets based on the transaction costs in the markets and the “bang-for-

buck” in the form of leverage, afforded by the options market. The authors conclude there

may be a separating equilibrium, where informed traders trade only in the stock market,

or a pooling equilibrium, where informed traders trade in both, depending on the relative

transaction costs differences in these markets.

Subsequent empirical work focused on directional informed trading in these two venues

has largely supported the theoretical predictions in the model (e.g. Cao, Chen, and Griffin

(2005) which studies option trading prior to takeovers) or extended the framework to include

other interactions between the two markets (e.g. Huh, Lin, and Mello (2012) which allows

the market makers in the option markets to hedge in the stock market).7

The literature examining informed volatility trading is more recent. Johnson and So

(2013), which estimates a multi-market information asymmetry measure, similar to the PIN ,

for option markets using aggregate unsigned volume. While simple to compute as it does

not rely on estimation of a structural model, it includes both information on volatility and

direction in one measure.

Ni, Pan, and Poteshman (2008) (NPP) use trades by non-market makers in the option

markets to estimate demand for volatility and show that this demand is “informative about

the future realized volatility of underlying stocks.” In contrast to our study, which uses

intraday quote and transaction data to sign trades, NPP use non-market maker volume

(NMMV ), obtained from the Chicago Board of Options Exchange (CBOE) at the daily level

for their analysis. Additionally, rather than estimating PIN measures, the study separates

6Bagehot (1971), Glosten and Milgrom (1985), Kyle (1985), Easley and O’hara (1987)7More generally, numerous authors have examined informed trading in option markets, for example,

Chakravarty, Gulen, and Mayhew (2004), and Kaul, Nimalendran, and Zhang (2004) but these authorsfocus on directional information about the underlying stock price, not information about the volatility.Simaan and Wu (2007) examine price discovery across option exchanges, but they make no attempt todifferentiate between option price changes resulting from underlying stock price changes and those resultingfrom volatility changes.

3

option volume into trades that could have been used for constructing straddles and those that

were not. Their findings relating informed volatility trading, estimated using NMMV , to

future changes in volatility closely mirror our own findings regarding the V olPIN and future

volatility. In our study, we separately estimate measures for directional and volatility based

information trading in the options market. While NPP largely disregard “non-straddle”

trading, exclusively focusing on straddle trades, we holistically characterize trades as noise,

directional, or volatility information driven, and separately estimate measures for volatility

and directions information-based trades.

The advantages of our analysis over NPP include: (1) Using intraday data that allow us

to sign trades individually, rather than relying on aggregate daily volume.(2) Examining the

contribution of both volatility and directional information-based risk measures to explain

simultaneously using the PIN framework allows us to assess asset pricing implications of the

two measures separately and to decompose their effect on the option market bid ask spread.

3 Model

In this section we outline our information-based trading model that captures both directional

information and volatility information. Our sequential trade model is a generalization of

Easley, Kiefer, O’Hara, and Paperman (1996) and Easley, Hvidkjaer, and O’Hara (2002)’s

probability of information-based trade (PIN) model.

Our model extends their model to the options market where agents can trade on direc-

tional information as well as volatility information on the underlying stock. Traders having

information about the future increase in stock price can use a long call/short put strategy

and long put/short call strategy for information on future decrease in stock price. If the

information is about volatility, then they can employ a long straddle (long call and long put)

when the information is about an increase in volatility and short straddle for a decrease in

future volatility.

In our model, new information arrives every 30 minutes with probability α and, con-

ditional on a information event, it is either volatility information with probability θ or

directional information with probability 1 − θ. Volatility information can be high (prob δ)

or low (prob 1− δ). Directional information is either good news (prob γ) or bad news (prob

1− γ).

Orders from informed and uninformed traders to buy/sell, call/put options follow in-

dependent Poisson processes. Uninformed buyers (seller) arrive according to independent

4

Poisson processes at rate ε ∈ {εBC , εSC , εBP , εSP}, where the subscripts C and P denote calls

and puts, and superscripts B and S denote buys and sells by the traders. Orders from

traders possessing volatility information arrive at rates µ ∈ {µBC , µBP } for high volatility,

and {µSC , µSP} for low volatility. Finally, orders from informed directional traders arrive at

rate ν ∈ {νBC , νSP} for high direction, and {νSC , νBP } for low direction. Figure 1 shows the

information and the decision tree for the traders’ strategies.

When there is no information in the market (1 − α), the orders are purely uninformed,

with arrival rates εBC , εSC , ε

BP , ε

SP for long call, short call, long put, short put respectively. When

information event occurs in the market (α), and the information is about volatility (θ), and

if the volatility is high (δ), the joint probability of high volatility information event is αθδ.

Under this situation, the market orders arrive rates µBC + εBC , εSC , µ

BP + εBP , ε

SP for long call,

short call, long put, short put respectively. Similarly, we have the probabilities and arrival

rates for each of the five end nodes in the tree. Based on these assumptions we can derive

the likelihood function conditional on number of buys(B), sells (S) for call (C) and put (P )

options.

3.1 Likelihood Function and Estimation

The likelihood function given the model is based on the following assumptions. 1) There is

only one information event in the defined unit period (in our estimation we use 30 minutes

in a day); (2) There is no possibility of volatility information and direction information

occurring simultaneously. Then the marginal likelihood function one period is given by

equation 1, where we have suppressed the subscript t.

l(Θ|Orders) =(1− α)e−εBC

(εBC)CB

CB!e−ε

SC

(εSC)CS

CS!e−ε

BP

(εBP )PB

PB!e−ε

SP

(εSP )PS

PS!

+ αθδe−(µSC+εBC ) (µ

SC + εBC)CB

CB!e−ε

SC

(εSC)CS

CS!e−(µ

BP+εBP ) (µ

BP + εBP )PB

PB!e−ε

SP

(εSP )PS

PS!

+ αθ(1− δ)e−εBC (εBC)CB

CB!e−(µ

SC+εSC) (µ

SC + εSC)CS

CS!e−ε

BP

(εBP )PB

PB!e−(µ

SP+εSP ) (µ

SP + εSP )PS

PS!

+ α(1− θ)γe−(νSC+εBC ) (νSC + εBC)CB

CB!e−ε

SC

(εSC)CS

CS!e−ε

BP

(εBP )PB

PB!e−(ν

SP+εSP ) (ν

SP + εSP )PS

PS!

+ α(1− θ)(1− γ)e−εBC

(εBC)CB

CB!e−(ν

SC+εSC) (ν

SC + εSC)CS

CS!e−(ν

BP+εBP ) (ν

BP + εBP )PB

PB!e−ε

SP

(εSP )PS

PS!(1)

5

3.1.1 Simplified Model

The model give by equation 1 has 16 parameters, and estimating all the parameters using

MLE is challenging. To make the model tractable we impose several restrictions. First, we

set all the uninformed arrival rates to be the same ε = εBC = εSC = εBP = εSP . This is not a very

restrictive assumption as these are non-strategic traders. Second, we set the informed arrival

rates for high and low volatility traders to be the same, µ = µBC = µSC = µBP = µSP . This is

more restrictive as one might expect arrival rates for high volatility to be different from low

volatility. Finally, we assume that the arrival rates for the high and low directional trader to

be the same, ν = νBC = νSC = νBP = νSP . We do not expect directional traders to prefer high

or low directional trades and hence this assumption is not restrictive. These assumptions

reduce the number of parameters to be estimated to 7 from 16 and the likelihood function

is given by equation 2:

l(Θ|Orders) =1

CB!CS!PB!PS!{(1− α)e−εεCBe−εεCSe−εεPBe−εεPS

+ αθδe−(µ+ε)(µ+ ε)CBe−εεCSe−(µ+ε)(µ+ ε)PBe−ε(ε)PS

+ αθ(1− δ)e−εε)CBe−(µ+ε)(µ+ ε)CSe−εεPBe−(µ+ε)(µ+ ε)PS

+ α(1− θ)γe−(ν+ε)(ν + εBC)CBe−εεCSe−εεPBe−(ν+ε)(ν + ε)PS

+ α(1− θ)(1− γ)e−εεCBe−(ν+ε)(ν + ε)CSe−(ν+ε)(ν + ε)PBe−εεPS}

=1

CB!CS!PB!PS!e−4ε{(1− α)εCB+CS+PB+PS + αθδe−2µεCS+PS(µ+ ε)CB+PB

+ αθ(1− δ)e−2µε)CB+PB(µ+ ε)CS+PS + α(1− θ)γe−2νεCS+PB(ν + ε)CB+PS

+ α(1− θ)(1− γ)e−2µεCB+PS(ν + ε)CS+PB}(2)

The log likelihood function is given by,

L(Θ|Orders) = Log(T∏t=1

lt). (3)

We use a maximum likelihood method (MLE) to estimate the parameters of the model,

Θ = {α, δ, θ, γ, ε, µ, ν}, using signed orders Orders ∈ {CB,CS, PB, PS} for individual

stock options. From these estimates we construct estimates for the probability of volatility

informed trading (V olPIN) and directional informed trading (DirPIN).

6

3.2 Information-Based Measures; V olPIN and DirPIN

3.2.1 Simplified Model

The probability of volatility information is αθ, and conditional on this the expected informed

arrival rate is 2(δµ + (1− δ)µ) = 2µ. Hence the expected rate of volatility informed arrival

is 2αθµ. Similarly, the expected directional informed arrival rate is 2α(1 − θ)ν. The total

expected uninformed arrival rate is 4ε. Based on this the information measures V olPIN

and DirPIN are give by the following equations.

V olPIN =αθµ

αθµ+ α(1− θ)ν + 2ε(4)

DirPIN =α(1− θ)ν

αθµ+ α(1− θ)ν + 2ε(5)

We use a 30 minute interval during a day as the time period, and use two weeks of

observations for t. Since each day has 6.5 hours of trading, we get 13 observations per day

and over two weeks, we obtain 130 (T ) observations for the estimation. In the following

section, we use Monte Carlo simulation techniques to ascertain the finite sample properties

of the estimators and ensure parameter recovery using 130 periods is possible and accurate.8

4 Monte Carlo Simulation

We follow the approach used by Nimalendran (1994) to carry our Monte Carlo simulation

for estimating and analyzing the finite sampe properties of the sample parameter estimators.

In this study we use R-Project software to generate simulated samples and obtain the

finite sample behavior using the following procedure.

1. We first set the values for the parameters (α, θ, δ, γ, ε, µ, ν).

8Note that the term CB!CS!PB!PS! can be factored out for the marginal likelihood function. Thisterm does not involve any of the parameters. Hence, in the MLE procedure we eliminate the term from loglikelihood function.

7

2. Generate four independent and identical uniformly (0, 1) random variables to decide the

“No information, High Vol information, Low Vol information, High Dir information,

Low Dir information” state. For example if α = .5, and the generated Uniform variable

is less than .5 then we will be in the no information state. Similarly for the other states

of the tree.

3. Once the terminal node of the tree is determined, we use the given parameters to

simulate the number (volume) of orders of long call, short call, long put, short put for

a certain fixed observations of periods (T = 100 or T = 300), thus a sample including

T observation of Orders ∈ {CB,CS, PB, PS} is generated.

4. Use non-linear optimization tools to estimate the parameters by maximizing the log-

likelihood function, and then record the estimated parameters as (α̂1, δ̂1, θ̂1, γ̂1, ε̂1, µ̂1, ν̂1).

5. Repeat steps 2-4 for 200 replications and record the estimated parameters as,

(α̂i, δ̂i, θ̂i, γ̂i, ε̂i, µ̂i, ν̂i), where i = 1 : 200.

6. After obtaining the set of all the estimated parameters, we calculate the number

of replications for which the optimization converged to feasible estimates (NC), the

mean estimates MEAN = 1NC

∑NCi=1 η̂i and the standard errors of the means SEM =

1√NC

[ 1(NC−1)

∑NCi=1(η̂i −MEAN)2]1/2, where η ∈ {α, δ, θ, γ, ε, µ, ν}.

The results of our simulation is presented in Table 1. We present six set of parameter

choices and two sets of number of observations (100, and 300). The parameters (α, θ, δ, γ)

are chosen to be between 0.3 and 0.7. While the arrival rates for traders is chosen to be (50,

100, or 150) in different combinations. We find that the number of convergences were close

to 100%. The estimators also have very good finite sample properties. The bias for all the

estimators are very small, and the standard error of the estimates are also very small. For

example, the percentage of estimation error of α varies from 0 to 1.2% and the absolute value

of t-test which is the bias/SEM varies from 0 to 0.125, which cannot reject the null that

the estimates are different from the parameters. The efficiency of the estimators improves

when more observations enter the simulated sample, which is the same as our expectation.

Different combinations of parameters also provide information of sensitivity but overall, our

simulation shows that the procedure is efficient and accurate to get the estimates for the

parameters for our Option PIN model using 130 observations.

8

5 Data and summary statistics

5.1 Data

In this paper, all the option transaction level data are obtained from OPRA Option Database.

This data was provided by the OptionData warehouse, Baruch College, CUNY.9 The stock

transaction level data are extracted from the Trade and Quote (TAQ) Database. Other

option data such as option Greeks, implied volatility, and realized volatility are obtained

from Optionmetrics Database. Finally, the stock data such as end of day price, ask price, bid

price, shares outstanding, traded volume are obtained from Center for Research in Security

Prices (CRSP).

5.2 V olPIN and DirPIN Estimation Details

We construct our sample using the following procedure: 1) Compile a list of all the stocks in

TAQ and merge this list with OPRA database; 2) Sort the merged list by the option volume

in 2010 obtained from OptionMetrics, and keep the top 500 stocks. We do this to ensure

sufficient option volume to estimate our PIN measures.

For our study, we consider options within 10% of the strike price, or the nearest in-

and out- of-the-money strikes, whichever results in broader coverage. In terms of option

maturity, we keep all options expiring within 7 to 183 days. OPRA data has second level

quote data for the options markets, as well as transaction data. We use the Lee and Ready

(1991) algorithm to sign trades in both stock and option markets. Finally, we use signed

trades aggregated at 30 minute intervals (CB,CS, PB, PS) to estimate our model.

The time period of our sample (2011 calendar year) is split into 2 week estimation periods.

For each 2 week estimation period, we use 30 minute intervals to measure order flow to

compute V olPIN and DirPIN measures. For each day we have 13 30 minute observations

and over two weeks, we have 130 such observations. These 130 observations are used for our

estimates.

To estimate the PIN measure for stocks, we merge NBBO and Trades data from TAQ

and use Lee and Ready (1991) to define the stock trade direction. Similar to the process

for options, for every 30 minute interval, we calculate the volume of Trades-up (buys) and

9Option Price Reporting Authority (OPRA) was established as a securities information processor for mar-ket information, for collecting, consolidating and disseminating the option market data from its participantsincluding AMEX, ARCA, BATS, BX, BSE, C2, CBOE, ISE, MIAX, NASDAQ, and PHLX. OPRA OptionDatabase contains all the transaction level data (Trades and Quotes) for stock options which is traded inthe participants’ exchange.

9

Trades-down (sells) for each stock. We use two weeks or 10 trading days to obtain 130

observations to estimate PIN using the technique outlined in Easley, Kiefer, O’Hara, and

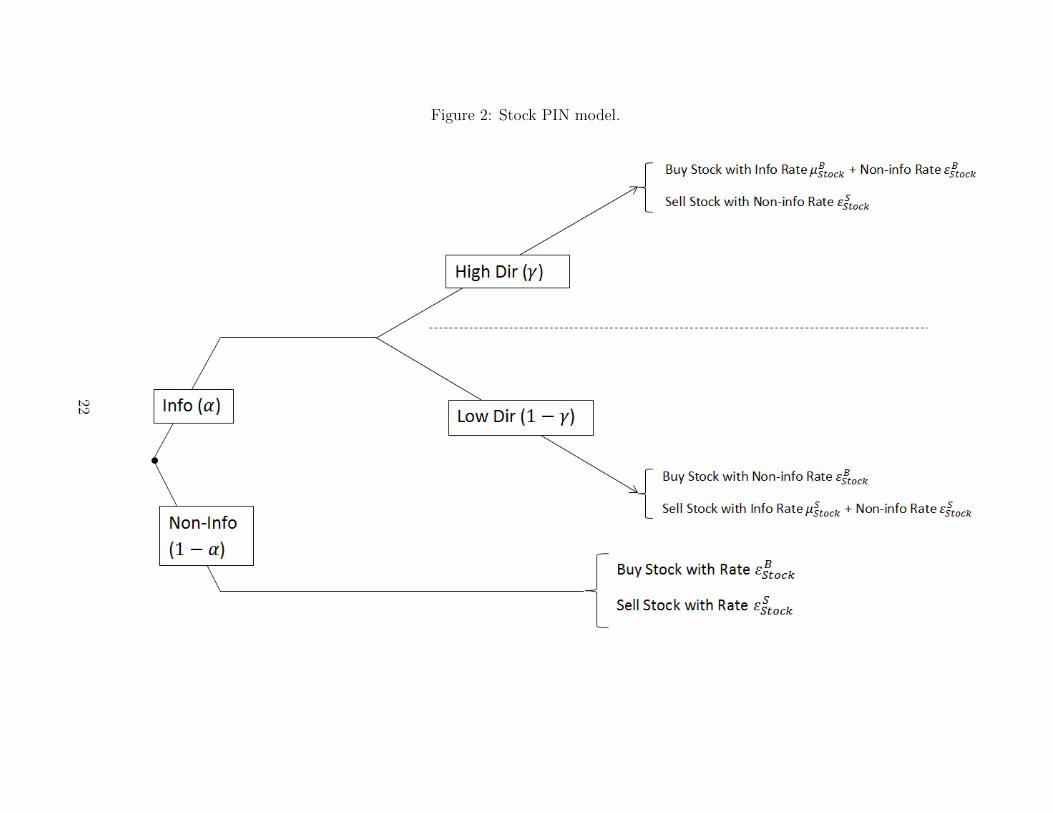

Paperman (1996). The stock PIN model is given in Figure 2.

5.3 Summary statistics

Table 5 presents summary statistics for option related variables in our sample. The sample

consists of 500 stocks over the 26 2-week periods in 2011. Lack of option volume, or other

variables leads to the overall sample size being around 8000 observations (rather than 500

* 26 = 13000). The average bid ask spread for options in our sample is 10.5 cents, which

translates to a relative bid ask spread of 5.8%. The average log daily volume for options

is 8.2 (or 3640 options traded). The log volume over each two week period is 10.5 (36315),

reflecting approximately 10 trading days per two week window. The Greeks for the options

are also presented. The average ∆ is 0.53, reflecting the fact that only options at or around

the money are used in the analysis.

The average option price implied volatility is 39.0% (annualized). This is slightly higher

than realized volatility (37.7%), in line with the option volatility premium documented

in previous literature. The average unpriced volatility (realized volatility minus implied

volatility) is the difference (-1.3%) and the average absolute unpriced volatility is 10.3%.

Note that informed volatility trading would be reflected in higher absolute unpriced volatility,

rather than simply unpriced volatility, as informed volatility traders may go long or short

volatility.

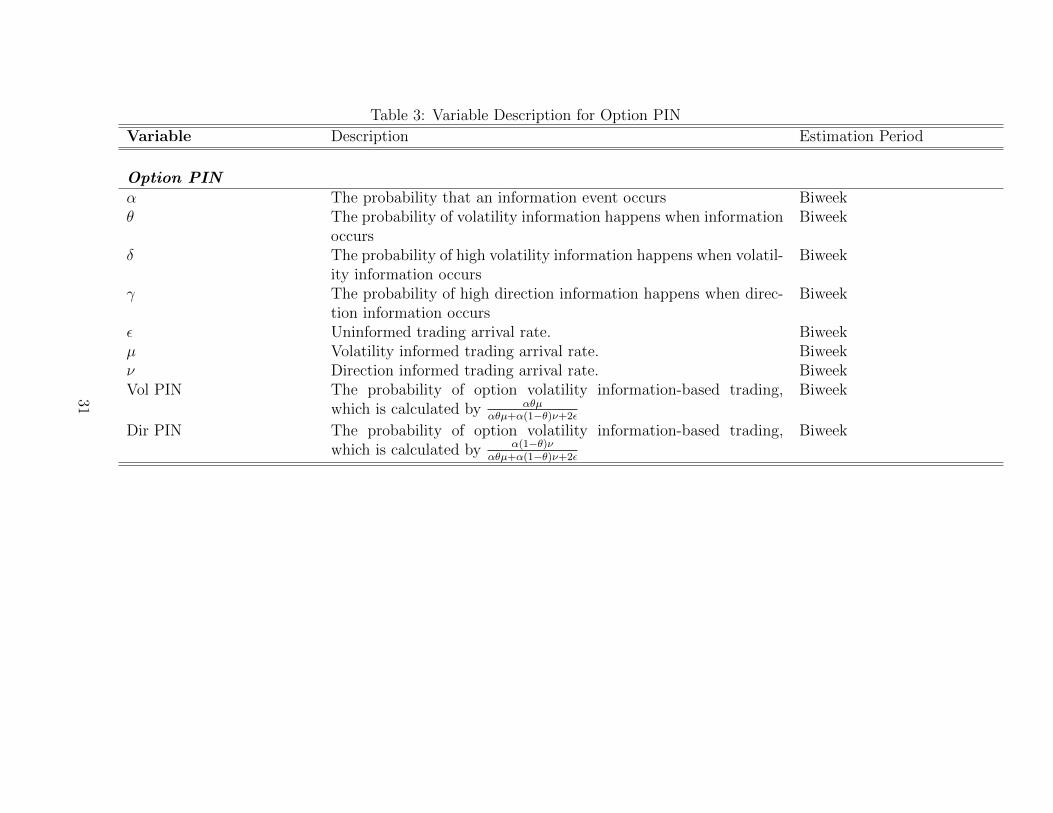

The variables used to construct V olPIN and DirPIN are given in Section 3. As a recap,

α is the probability that there is information in each 30 minute interval. θ is the probability

that the information is regarding direction, rather than volatility, conditional on there being

information. γ is the probability that directional information is good news rather than bad

news. δ is the probability information is regarding an increase in volatility rather than a

decrease.

V olPIN and DirPIN are estimated over 2 week horizons, by examining order flow in

each 30 minute interval in the 2 week horizon separately. We can see that the probability

of informed trading in each 30 minute horizon is 0.46, with roughly an even probability

that the information is regarding direction and volatility. Information regarding volatility is

more likely to be regarding an increase in volatility (δ = 0.613) but information regarding

direction is equally likely to reflect either good or bad news (γ = 48.5%). The overall

V olPIN and DirPIN are estimated at 0.225 and 0.202 respectively, suggesting roughly an

equal probability of informed volatility and directional trading.

10

Table 6 presents corresponding summary statistics for the underlying stocks in our sam-

ple. The average bid ask spread is 1.64 cents, corresponding to a relative bid ask spread of

4.5bps. The log volume is 15.547 (5.6 million shares) and the log market cap is 16.3 ($12BN).

The stock PIN is computed as per the technique outline in Easley, Kiefer, O’Hara, and Pa-

perman (1996). The probability of informed trading in each 30 minute windows is 0.339, and

informed traders are equally likely to trade on good news and bad news. The overall stock

PIN is estimated as 0.169, which is similar to the numbers reported by Easley, Hvidkjaer,

and O’Hara (2002).

Figure 3 presents distributions of V olPIN and DirPIN parameters in our sample. Fig-

ure 4 presents distributions of stock PIN parameters in our sample.

Table 7 presents the correlations across the various variable in the study. In line with

intuition, PIN measures (V olPIN and DirPIN and Stock PIN) are negatively correlation

with stock and option volume, as well as market cap. They are positively correlated with

bid ask spreads. Also in line with expectations, DirPIN is more positively correlated with

Stock PIN than V olPIN .

Table 8 presents selected summary statistics sorted by market capitalization quintiles.

Consistent with expectations, the probability of all types of informed trading decreases

with market capitalization, reflecting the greater transparency of larger companies. The

differences in the PINs of companies in the largest fifth are significantly different from the

PINs of companies in the smallest quartile.

6 Results and Analysis

6.1 Unpriced volatility and the V olPIN

In this section we study the relation between our option PIN measures and unpriced volatility,

UV = (|RV − IV |) using the following empirical model.

UV = β0 + β1(V olPIN) + β2(DirPIN) + γX + ε (6)

γX refers to control variables and additional interaction terms. Table 9 presents re-

gressions estimating the above equation and analysing the explanatory power of our PIN

measures on the absolute unpriced volatility (realized volatility over the next 2 weeks minus

the implied volatility in the option prices at the end of the current 2 week period). We find

V olPIN has a uniform positive relationship with unpriced volatility, with a one standard

deviation increase (0.066) in V olPIN associated with a 0.8% increase in absolute unpriced

11

volatility (based on model 3 estimate of 0.120 reported in 9). This change translates to a

7.8% increase based on the average unpriced volatility of 10.2%.

The positive relationship is strongest when the realized volatility is higher than the im-

plied volatility. The coefficient estimate increases to 0.227 after including a dummy variable

for the instances when the realized volatility is lower than the implied volatility. This leads

to nearly doubles (1.5% increase and a 15% change from the average) the impact of V olPIN

on future unpriced volatility. Our findings suggest that informed volatility trading, as esti-

mated using our V olPIN measure, is indeed linked to significantly large differences between

implied and realized volatility. Furthermore, the informed trading captured by our measure

is more likely to be trading on increasing volatility, rather than decreasing volatility.

In addition to V olPIN we find thatDirPIN too is positively related to absolute unpriced

volatility. Though, the sensitivity of 0.0541 is about half of the V olPIN effect. However,

when we interact DirPIN with the I(IV−RV ), the estimate increases to 0.0871. This is

consistent with an increase in volatility being positively related to a decrease in stock price.

Our results suggest that there is more directional informed traders in the options market

when the future volatility is higher than the implied volatility.

6.2 Asset Pricing and the DirPIN

In this section we study the relation between our option PIN measures and excess asset

returns (ER). The model is based on the study by Easley, Hvidkjaer, and O’Hara (2002).

ER = β0 + β1(Portfolioβ) + β2(StockPIN) + β3(V olPIN)+

β4(DirPIN) + β5(Log(MktCap)) + β6(StockRelSpread)+

β7(ImpliedV ol) + β8(TurnOver) + ε

(7)

Table 10 and 11 presents results of a Fama-Macbeth and fixed-effects regression model

estimates analysing the effect of our PIN measures on stock returns for the following 2

weeks. Following the model outlined in Easley, Hvidkjaer, and O’Hara (2002), we regress

daily stock returns on estimated market β, market cap, and our PIN measures. We do not

include BM variable as our data spans only one year and Easley, Hvidkjaer, and O’Hara

(2002) do not find a significant effect of this variable on returns. We find that in all the

different specifications the DirPIN to have a positive, significant relationship with future

daily stock returns. More over the coefficient estimate of 0.00362 (Model 7, Table 10) leads

to an increase in expected returns of 1.8% (based on 252 trading days) per year, for a stock

12

that has a 10% higher DirPIN relative to a stock that has average DirPIN of 0.202. Easley,

Hvidkjaer, and O’Hara (2002) using stock PIN find a 2.5% higher expected returns using a

longer time horizon and a larger cross-section of stocks.

Interestingly, the stock PIN in our analysis using Fama-MacBeth model is not a signif-

icant explanatory variable of future returns. These findings are reassuring as the intuition

outlined in Easley, Hvidkjaer, and O’Hara (2002) holds in our sample: investors in stocks

with informed trading have to be compensated for the information risk they face when trad-

ing these stocks. The fact that the Stock PIN is not significant in our analysis suggests

that for such large stocks, more of the directionally informed trading may be done in the

options markets where the transactions costs are relatively low compared to options on small

cap stocks. It also reassuring that the V olPIN is insignificant in this regression analysis

as informational risk regarding the second moment of a stock’s returns should not result in

positive returns for the stock.

The fixed effects regression estimates are shown in Table 11. In these model both Stock

PIN and DirPIN have very significant and positive coefficients. Since the fixed effect esti-

mator is based on removing the time-invariant characteristics of the assets, it is appropriate

to consider the effects as more short term in nature and less due to long term cross sectional

differences in asset returns.

Our results based on overall correlations, results regarding unpriced volatility, and asset

pricing tests are consistent with DirPIN and V olPIN being good measures of directional

and volatility based information trading in the options market.

6.3 Determinants of Option Bid-Ask Spreads

6.3.1 Adverse Selection Cost

Adverse selection costs play an important role in determining stock spreads. On the options

market, the extant evidence is mixed. If informed agents can trade strategically on the

stock and the options markets to maximize their returns from private information, and if

option market makers cannot instantaneously hedge the option exposure to adverse selection,

then the option market makers will face the same information disadvantage as stock market

makers do, and the option spread must compensate for this cost.10

Black (1975) argues that informed agents might prefer the options market for its high

leverage. On the other hand, Easley, O’hara, and Srinivas (1998) find that informed agents

10The bid-ask spreads on stocks compensate market makers for order processing, inventory (Ho and Stoll(1981)), and adverse selection costs (Bagehot (1971), Glosten and Milgrom (1985), Kyle (1985), Easley andO’hara (1987)).

13

may trade in both the option and the stock markets simultaneously. This has implications

for where price discovery occurs. The empirical evidence on this issue is mixed. For example,

Vijh (1990) and Cho and Engle (1999) find that option market makers do not face significant

adverse selection costs, while Easley, O’hara, and Srinivas (1998) and Cao, Chen, and Griffin

(2005) find evidence consistent with informed trading on the options market.

To proxy for adverse selection costs we will use DirPIN , V olPIN and Stock PIN. These

are measures of information based trading in the options market and the stock market.

6.3.2 Hedging Costs

Black and Scholes (1973) show that in a “perfect” market the payoff to an option can be

replicated by continuously unbalancing a portfolio of stocks and bonds. If the conditions

necessary for a perfect market hold, then option spreads should only compensate option mar-

ket makers for order processing costs, and perhaps for informed volatility trading. However,

when there are market frictions such as transaction costs, it is no longer possible to replicate

the option payoff using a dynamic strategy involving continuous unbalancing. Therefore,

option market makers must be compensated for the costs associated with unbalancing at

discrete time intervals, as well as costs due to market frictions such as bid-ask spread on the

underlying stock, price discreteness, information asymmetry, and model misidentification.

The costs consist of the cost of setting up and liquidating the initial delta neutral position,

and the cost to continuously rebalance the portfolio to maintain a delta neutral position.

Several papers, including Leland (1985), Merton and Samuelson (1990), and Boyle and Vorst

(1992), have theoretically examined the impact of stock bid-ask spreads on the hedging costs

imposed on option dealers due to discrete rebalancing. They show that the option spread

(the difference between the prices of long and short calls) due to the discrete rebalancing

is positively related to the proportional spread on the underlying asset, inversely related to

the revision interval, and positively related to the sensitivity of the option to changes in

volatility (vega).

Initial Hedging Cost

An option market maker would set up a delta neutral position by purchasing ∆ shares of

the stock at the ask price and close the position by selling at the bid price. This would lead

to a cost,

IC = kS∆ (8)

14

where, IC represents the initial hedging cost, k is the proportional stock spread, S is the

stock price, and ∆ is the option delta.

Rebalancing Cost

The initial hedging cost does not include the cost of rebalancing the portfolio to maintain

a delta-neutral position. Following Leland (1985) and Boyle and Vorst (1992), we define the

rebalancing cost as follows:

RC =2νk√2π(δt)

(9)

where ν is the option Vega, k is the proportional stock spread and δt is the rebalancing

interval.

The rebalancing cost is proportional to the option’s Vega and the spread on the underlying

stock, and is inversely related to the rebalancing interval. Since Vega is highest when the

stock price is equal to the present value of the exercise price, ceterisparibus, we would

expect at-the-money options to have the highest rebalancing costs. The expression for the

rebalancing costs also has an intuitive explanation the bid-ask spread on the stock gives rise

to an extra volatility when the option is replicated. For example, if you replicate a long call

option, then when the stock price increases, rebalancing would require you to purchase more

stock. But this has to be done at the ask price. Similarly, when the stock price falls, the

stock has to be sold at the bid price to maintain a delta neutral position. This effectively

increases the volatility of the asset, and this increase in volatility would be proportional to

the bid-ask spread (Roll (1984)).

In constructing the above measure of rebalancing cost we do not observe the rebalancing

frequency. Therefore, we assume that this frequency is the same across all option contracts

and drop the term√

2π(δt) in our construction of the rebalancing cost. Hence, we obtain

the following expression for rebalancing costs:

RC = νk (10)

Order Processing Costs

Since order-processing costs are likely to be fixed for any particular transaction, the order

processing costs should decrease as the expected trading volume increases. Copeland and

Galai (1983) suggest a negative relation between bid-ask spreads and trading volume in the

15

long run, and . Easley and OHara (1992) develop a model that implies spreads decrease

with an increase in expected trading volume. We use trading volume of the option contract

(number of contracts traded), denoted as OptV ol, to proxy for order processing costs. Since

we control for adverse selection, we expect the trading volume to be negatively related to

spreads.

6.3.3 A Model of Option Bid-Ask Spread

We propose the following empirical model for the determinants of option spreads.11

OptSprd = β0 + +β1(V olPIN) + β2(DirPIN) + β3(IC) + β4(RC) + β5(OptV ol) + ε (11)

Table 12 provides OLS and fixed effect regression model estimates for the above model.

We find that in all the specification, the option PIN measures and the stock PIN measure

has significant positive impact on option spreads. In OLS models, they explain nearly 31 % of

the option spreads. The economic significant of the information measures are also significant.

A one standard deviation higher probabilities of the option information measures of V olPIN

and DirPIN increase option spread by 18% from its mean value of 5.8%. Interestingly, the

stock PIN too has a significant economic impact and increases option spread by 15 %. The

findings are consistent with information traders splitting their trades between the option and

the stock markets.

6.3.4 Information Based Trading Around Earnings Announcements

In a spirit similar to NPP, we examine the effect of earnings announcement on our PIN

measures. We denote each set of PIN estimates over the 2 weeks covering an earnings

announcement as “earnings periods. The 2 weeks immediately preceding and following the

“earnings periods are denoted as “pre-earnings and “post-earnings. The remainder of the

weeks is baseline weeks.

We analyse the effects of earnings announcement by regressing V olPIN , DirPIN and

the relative bid ask spread for options on dummy variables for each of these periods. The

results are presented in Table 13. These findings are also presented graphically in Figure 5.

11We do not include the inventory costs as a determinant for two reasons. First, the literature on stockspreads suggests that its magnitude is trivial (Stoll (1989) and Madhavan and Smidt (1991)). Second, optionmarket makers rarely take directional risks. Even if they carry inventory, it is likely to be hedged.

16

We find that, in general, informed trading in option markets occurs away from earnings

periods. Both V olPIN and DirPIN measures are significantly lower during the 2 weeks

encompassing earnings announcements. The V olPIN is lower by 3% and the DirPIN is

lower by 8%. Correspondingly, the relative bid ask spreads in option markets are also the

lowest during this period (5% lower). In contrast, informed trading in the stock market is

higher during earnings periods. These results suggest that, in contrast to stock markets,

informed traders on option markets do not trade as much around earnings.

We do note that given our 2 week estimation horizon, this analysis is quite coarse, as

earnings announcements may occur towards the beginning or end of the 2 week horizon.

However, as our analysis of the preceding and subsequent 2 weeks is generally consistent with

findings for earnings weeks, this concern is not major. Additionally, this lack of precision is

likely to add noise to our analysis, and to the extent we find significant results even with

this added noise, the true results are only likely to be statistically stronger.

7 Conclusion

We estimate separate measures for the probability of informed trading in directional and

volatility information in option markets. Our option PIN measures predict future unpriced

volatility and asset prices, in line with expectations. Additionally, our option PIN measures

suggest both directionally informed and volatility informed traders contribute to the high

bid ask spreads in option markets, even after controlling for the underlying Stock PIN .

Asset pricing tests suggest the DirPIN for option markets is actually a better measure

for directional informed trading in the underlying stocks in our sample, rather than the

PIN from the stock markets. In our sample DirPIN is significantly and positively linked

to future returns, while the stock PIN only has relation in fixed effect tests. This may be

due to the shorter horizons, or the nature of large stocks used in our sample. It may also

reflect a growing trend of using option markets to trade on information. Option market

volumes have increased over the last decade, even as stock volumes have stayed largely flat.

As this volume continues to increase, and more information about both the future direction

and volatility of stocks is revealed on the option markets, analyzing the effect of informed

trading on option markets will be paramount. We hope the V olPIN and DirPIN measures,

as proposed in this study, will help with this analysis.

17

References

Bagehot, Walter, 1971, The only game in town, Financial Analysts Journal 27, 12–14.

Black, Fischer, 1975, Fact and fantasy in the use of options, Financial Analysts Journal pp.

36–72.

Black, Fischer, and Myron Scholes, 1973, The pricing of options and corporate liabilities,

The journal of political economy pp. 637–654.

Boyle, Phelim P, and Ton Vorst, 1992, Option replication in discrete time with transaction

costs, The Journal of Finance 47, 271–293.

Cao, Charles, Zhiwu Chen, and John M. Griffin, 2005, Informational Content of Option

Volume Prior to Takeovers, The Journal of Business 78, 1073–1109.

Chakravarty, Sugato, Huseyin Gulen, and Stewart Mayhew, 2004, Informed trading in stock

and option markets, The Journal of Finance 59, 1235–1258.

Cho, Young-Hye, and Robert F Engle, 1999, Modeling the impacts of market activity on bid-

ask spreads in the option market, Working paper, National Bureau of Economic Research.

Copeland, Thomas E, and Dan Galai, 1983, Information effects on the bid-ask spread, the

Journal of Finance 38, 1457–1469.

Easley, David, Soeren Hvidkjaer, and Maureen O’Hara, 2002, Is Information Risk a Deter-

minant of Asset Returns?, The Journal of Finance 57, pp. 2185–2221.

Easley, David, Nicholas M. Kiefer, Maureen O’Hara, and Joseph B. Paperman, 1996, Liq-

uidity, Information, and Infrequently Traded Stocks, The Journal of Finance 51, pp.

1405–1436.

Easley, David, and Maureen O’hara, 1987, Price, trade size, and information in securities

markets, Journal of Financial economics 19, 69–90.

Easley, David, and Maureen OHara, 1992, Adverse selection and large trade volume: The

implications for market efficiency, Journal of Financial and Quantitative Analysis 27,

185–208.

Easley, David, Maureen O’hara, and Pulle Subrahmanya Srinivas, 1998, Option volume

and stock prices: Evidence on where informed traders trade, The Journal of Finance 53,

431–465.

18

Glosten, Lawrence R., and Paul R. Milgrom, 1985, Bid, ask and transaction prices in a

specialist market with heterogeneously informed traders, Journal of Financial Economics

14, 71–100.

Hasbrouck, Joel, 1995, One Security, Many Markets: Determining the Contributions to Price

Discovery, The Journal of Finance 50.

Ho, Thomas, and Hans R Stoll, 1981, Optimal dealer pricing under transactions and return

uncertainty, Journal of Financial economics 9, 47–73.

Huh, Sahn-Wook, Hao Lin, and Antonio Mello, 2012, Hedging by Options Market Makers:

Theory and Evidence, Available at SSRN 2123965.

Johnson, Travis, and Eric So, 2013, A Simple Multimarket Measure of PIN, Available at

SSRN 2181038.

Kaul, Gautam, Mahendrarajah Nimalendran, and Donghang Zhang, 2004, Informed trading

and option spreads, Available at SSRN 547462.

Kyle, Albert S, 1985, Continuous Auctions and Insider Trading, Econometrica 53, 1315–35.

Lee, Charles M. C., and Mark J. Ready, 1991, Inferring Trade Direction from Intraday Data,

The Journal of Finance 46, pp. 733–746.

Leland, Hayne E, 1985, Option pricing and replication with transactions costs, The journal

of finance 40, 1283–1301.

Madhavan, Ananth, and Seymour Smidt, 1991, A Bayesian model of intraday specialist

pricing, Journal of Financial Economics 30, 99–134.

Merton, Robert C, and Paul Anthony Samuelson, 1990, Continuous-time finance, .

Ni, Sophie X, Jun Pan, and Allen M Poteshman, 2008, Volatility information trading in the

option market, The Journal of Finance 63, 1059–1091.

Nimalendran, Mahendrarajah, 1994, Estimating the effects of information surprises and

trading on stock returns using a mixed jump-diffusion model, Review of Financial Studies

7, 451–473.

Roll, Richard, 1984, A simple implicit measure of the effective bid-ask spread in an efficient

market, Journal of Financial Economics 39.

19

Simaan, Yusif E, and Liuren Wu, 2007, Price discovery in the US stock options market, The

Journal of Derivatives 15, 20–38.

Stoll, Hans R, 1989, Inferring the Components of the Bid-Ask Spread: Theory and Empirical

Tests, The Journal of Finance 44, 115–134.

Vijh, Anand M, 1990, Liquidity of the CBOE equity options, The Journal of Finance 45,

1157–1179.

20

Figure 1: Option PIN model.

21

Figure 2: Stock PIN model.

22

Figure 3: Parameter distribution with pooled data in Option PIN model.

This figure provides the empirical distribution of the estimated Option PINmodel parameters with 26 bi-weeks and all the options in our sample. PanelA shows the empirical distribution of Option α, the probability that aninformation event occurs. Panel B shows the empirical distribution of Optionθ, the probability of volatility information happens when information occurs.Panel C shows the empirical distribution of Option δ, the probability of highvolatility information happens when volatility information occurs. Panel Dshows the empirical distribution of Option γ, the probability of high directioninformation happens when direction information occurs. Panel E shows theempirical distribution of Volatility PIN. Panel F shows the empirical distributionof Direction PIN.

Panel A: Empirical distribution of Option α, the probability that an information eventoccurs.

Panel B: Empirical distribution of Option θ, the probability of volatility informationhappens when information occurs.

23

Panel C: Empirical distribution of Option δ, the probability of high volatility informationhappens when volatility information occurs.

Panel D: Empirical distribution of Option γ, the probability of high direction informationhappens when direction information occurs.

24

Panel E: Empirical distribution of Volatility PIN.

Panel F: Empirical distribution of Direction PIN.

25

Figure 4: Parameter distribution with pooled data in Stock PIN model.

This figure provides the empirical distribution of the estimated Stock PIN modelparameters with 26 bi-weeks and all the options in our sample. Panel A showsthe empirical distribution of Stock α, the probability that an information eventoccurs. Panel B shows the empirical distribution of Stock γ, the probabilityof good news happens when information occurs. Panel C shows the empiricaldistribution of Stock PIN.

Panel A: Empirical distribution of Stock α, the probability that an information event occurs.

Panel B: Empirical distribution of Stock γ, the probability of good news happens wheninformation occurs.

26

Panel C: Empirical distribution of Stock PIN.

27

Figure 5: Percentage Changes in Information Measures Around Earning Announcement.

28

Table 1: Finite sample properties of the MLE estimators of the Option PIN model based onMonte Carlo Simulations

The finite sample properties are based on 200 replications of either 100 or 300observation days, that is, 100 or 300 sets of number of long call, short call, longput and short put orders. NC is the number of replications for which the opti-mization converged to feasible estimates, MEAN is the mean estimates, whichis calculated by MEAN = 1

NC

∑NCi=1 η̂i, and SEM is the standard error of the

MEANs, which is calculated by SEM = 1√NC

[ 1(NC−1)

∑NCi=1(η̂i −MEAN)2]1/2,

where η ∈ {α, δ, θ, γ, ε, µ, ν}.T = 100 T = 300

Set Parameter Sim Val NC Mean SEM NC Mean SEM1 α 0.50 200 0.494 0.048 200 0.501 0.031

θ 0.50 200 0.491 0.074 200 0.500 0.043δ 0.50 200 0.503 0.103 200 0.502 0.062γ 0.50 200 0.496 0.100 200 0.500 0.057ε 100.00 200 100.063 0.612 200 100.012 0.340µ 100.00 200 100.291 2.162 200 100.035 1.157ν 100.00 200 99.877 2.127 200 100.004 1.183

2 α 0.50 200 0.506 0.051 200 0.501 0.030θ 0.50 200 0.497 0.070 200 0.495 0.038δ 0.50 200 0.509 0.105 200 0.504 0.056γ 0.50 200 0.498 0.092 200 0.495 0.063ε 100.00 200 99.911 0.559 200 99.971 0.353µ 50.00 200 50.108 1.808 200 50.046 1.169ν 50.00 200 50.200 1.827 200 49.990 1.131

3 α 0.30 200 0.299 0.046 200 0.298 0.025θ 0.70 200 0.704 0.088 200 0.702 0.049δ 0.50 200 0.493 0.114 200 0.497 0.065γ 0.50 200 0.498 0.173 200 0.500 0.093ε 100.00 200 99.960 0.567 200 99.996 0.310µ 100.00 200 100.174 2.261 200 99.914 1.296ν 100.00 200 100.148 3.687 200 99.991 2.019

4 α 0.30 200 0.295 0.049 200 0.298 0.026θ 0.70 200 0.696 0.085 200 0.699 0.046δ 0.40 200 0.388 0.103 200 0.402 0.061γ 0.40 200 0.405 0.177 200 0.397 0.098ε 100.00 200 99.969 0.547 200 100.005 0.324µ 100.00 200 99.870 2.287 200 100.025 1.339ν 100.00 200 100.104 3.508 200 100.201 2.079

5 α 0.30 200 0.301 0.051 200 0.300 0.025θ 0.70 200 0.702 0.086 200 0.702 0.047δ 0.40 200 0.403 0.108 200 0.401 0.060γ 0.40 200 0.393 0.178 200 0.395 0.100ε 50.00 200 49.726 3.484 200 49.989 0.216µ 100.00 200 100.252 1.902 200 99.893 1.066ν 100.00 200 99.796 4.385 200 99.897 1.738

6 α 0.30 200 0.299 0.086 200 0.301 0.029θ 0.70 200 0.681 0.143 200 0.704 0.047δ 0.40 200 0.402 0.154 200 0.404 0.062γ 0.40 200 0.409 0.193 200 0.401 0.095ε 50.00 200 47.852 9.450 200 49.929 0.852µ 100.00 200 99.427 4.285 200 100.194 2.323ν 150.00 200 146.982 13.883 200 150.218 2.191

29

Table 2: Variable Description for Option

Variable Description Frequency / Estimation Pe-riod

OptionOption Spread ($) Option’s ask price minus bid price from OPRA database Transaction / BiweekOption Rel Spread Option spread divide by the mid-point of the ask bid spread from

OPRA databaseTransaction / Biweek

Log(Option Volume) Natural logarithm of the option volume from OPRA database Transaction / BiweekLog(Daily Option Volume) Natural logarithm of daily average option volume from OPRA

databaseTransaction / Average Daily

∆ The data is from Optionmetrics. ∆ of the option is calculated bythe change in option premium for a $1.00 change in underlying price

Last day of period t

Θ The data is from Optionmetrics. Θ is calculated by the change inoption premium as time passes, in terms of dollars per year.

Last day of period t

V ega The data is from Optionmetrics. Vega is calculated by the changein option premium, in cents, for one percentage point change involatility.

Last day of period t

Γ The data is from Optionmetrics. Γ is calculated by the absolutechange in ∆ for a $1.00 change in underlying price.

Last day of period t

Unpriced Volatility (annu-alized)

Realized Volatility of time period t+ 1 minus Implied volatility atthe last day of time period 1 from Optionmetrics

Biweek

Implied Volatility (annual-ized)

The data is from Optionmetrics. IV is calculated for options withstandard settlement at last day of time period t.

Last day of period t

Realized Volatility (annual-ized)

The data is from Optionmetrics. Biweek at t+ 1

Abs(Unpriced Volatility)(annualized)

Absolute Value of Unpriced Volatility from Optionmetrics Biweek

30

Table 3: Variable Description for Option PIN

Variable Description Estimation Period

Option PINα The probability that an information event occurs Biweekθ The probability of volatility information happens when information

occursBiweek

δ The probability of high volatility information happens when volatil-ity information occurs

Biweek

γ The probability of high direction information happens when direc-tion information occurs

Biweek

ε Uninformed trading arrival rate. Biweekµ Volatility informed trading arrival rate. Biweekν Direction informed trading arrival rate. BiweekVol PIN The probability of option volatility information-based trading,

which is calculated by αθµαθµ+α(1−θ)ν+2ε

Biweek

Dir PIN The probability of option volatility information-based trading,which is calculated by α(1−θ)ν

αθµ+α(1−θ)ν+2ε

Biweek

31

Table 4: Variable Description for Stocks

Variable Description Estimation Period

StockReturn (Per Day) Raw return from CRSP database BiweekS&P 500 Return (Per Day) S&P 500 return from CRSP database BiweekExcess Return (Per Day) Raw return minus S&P 500 Return from CRSP database BiweekStock Spread ($) Stock ask price minus bid price from CRSP database BiweekStock Rel Spread Stock ask bid spread divide by mid-point of ask and bid price from

CRSP databaseBiweek

Log(Daily Stock Volume) Natural logarithm of biweek daily stock volume from CRSPdatabase

Average Daily

Log(Market Cap) Natural logarithm of market capital at last day of period t fromCRSP database

Last day of period t

Stock PINStock α The probability that an information event occurs. BiweekStock δ The probability of good news happens when information occurs. BiweekStock ε Uninformed trading arrival rate. BiweekStock µ Informed trading arrival rate. BiweekStock PIN The probability of stock information-based trading, which is calcu-

lated by Stock δ∗Stock µStock δ∗Stock µ+2Stock ε

.Biweek

32

Table 5: Summary Statistics for Options

Variable Obs Mean Std. Dev. Min Max

OptionOption Ask Bid Spread ($) 8062 0.105 0.310 0.014 2.947

Option Rel Ask Bid Spread (%) 8062 5.8 4.3 1.5 23Log(Option Volume) 8056 10.485 1.263 8.350 14.097

Log(Daily Option Volume) 8056 8.219 1.263 6.084 11.841

∆ 7994 0.526 0.016 0.508 0.615Θ 7994 -12.981 12.866 -83.370 -1.594

V ega 7994 5.909 5.744 0.534 39.047Γ 7994 0.137 0.109 0.012 0.613

Unpriced Volatility 7993 -0.013 0.154 -0.631 0.917Implied Volatility 7994 0.390 0.171 0.128 1.010

Realized Volatility 7995 0.377 0.223 0.081 1.265Abs(Unpriced Volatility) 7993 0.104 0.115 0.000 0.917

Option PINα 8064 0.457 0.064 0.066 0.838θ 8064 0.491 0.114 0.023 0.989δ 8064 0.613 0.203 0.013 0.988γ 8064 0.485 0.176 0.013 0.988ε 8064 158.939 876.544 4.731 27345.970µ 8064 372.193 1267.470 10.783 35709.450ν 8064 303.602 1048.574 11.013 33978.800

Vol PIN 8064 0.225 0.066 0.091 0.410Dir PIN 8064 0.202 0.066 0.078 0.396

33

Table 6: Summary Statistics for Stocks

Variable Obs Mean Std. Dev. Min Max

StockReturn (%) 8029 -0.03 0.74 -2.42 1.96

S&P 500 Return (%) 8029 -0.0044 0.303 -0.85 0.71Excess Return (%) 8029 -0.03 0.64 -2.20 1.76

Stock Ask Bid Spread ($) 8030 0.0164 0.0202 0.0089 0.1720Stock Rel Ask Bid Spread (%) 8030 0.045 0.038 0.010 0.231

Log(Daily Stock Volume) 8036 15.547 0.971 13.249 18.248Log(Mkt Cap) 8030 16.306 1.412 12.893 19.161

Stock PINStock α 8050 0.338972 0.049538 0.167751 0.574098Stock δ 8050 0.490051 0.177726 0.041407 0.928179Stock ε 8050 288674.3 642479.7 3491.761 16900000Stock µ 8050 342090.1 825344.1 6671.03 24400000

Stock PIN 8050 0.169494 0.032986 0.113421 0.28505

34

Table 7: Correlation MatrixDirPIN

VolPIN

StockPIN

Abs(UV)

ExcessRet

Log(DailyOp-tionVol-ume)

Log(DailyStockVol-ume)

Log(MktCap)

StockRelAskBid

OptionRelAskBid

IV RV IC RC

Dir PIN 1.00Vol PIN -0.05 1.00Stock PIN 0.22 0.09 1.00Abs(Unpriced Vol) 0.04 0.03 0.09 1.00Excess Return 0.02 0.00 -0.01 -0.08 1.00Log(Daily Option Volume) -0.56 -0.40 -0.14 -0.07 -0.01 1.00Log(Daily Stock Volume) -0.29 -0.12 -0.14 -0.06 0.00 0.70 1.00Log(Market Cap) -0.33 -0.11 -0.39 -0.23 0.05 0.42 0.33 1.00Stock Rel Ask Bid 0.22 0.15 0.33 0.19 -0.07 -0.16 0.11 -0.48 1.00Option Rel Ask Bid 0.39 0.22 0.29 -0.01 -0.01 -0.49 -0.30 -0.29 0.25 1.00Implied Vol 0.06 -0.02 0.03 0.33 -0.07 -0.13 0.03 -0.53 0.46 -0.11 1.00Realized Vol 0.05 -0.02 0.01 0.54 -0.11 -0.08 0.03 -0.38 0.32 -0.11 0.72 1.00IC -0.10 -0.16 0.05 0.02 0.01 0.02 -0.25 0.02 0.09 -0.01 0.03 0.01 1.00RC -0.09 -0.17 0.06 0.02 0.01 0.00 -0.27 0.01 0.10 0.00 0.03 0.01 0.98 1.00

35

Table 8: Sort by Market Cap

Log(MktCap) Log(Stock Vol) Log(Option Vol) VolPIN DirPIN StockPIN1 (Low) 14.215 15.265 7.727 0.230 0.226 0.190

2 15.605 15.266 7.784 0.236 0.220 0.1773 16.367 15.440 8.045 0.224 0.204 0.1664 17.157 15.535 8.182 0.227 0.198 0.159

5 (High) 18.184 16.234 9.330 0.210 0.162 0.156(1-5) -3.97 -.969 -1.603 0.020 0.0642 0.034

(-190.020) (-30.171) (-41.95) (8.815) (29.672) (29.437)

36

Table 9: Regression on Abs(Unpriced Volatility)

This table reports the coefficients from fixed effect panel regression of absoluteunpriced volatility. The absolute unpriced volatility is defined as the t − 1 pe-riod last day implied volatility (IV) minus the t period realized volatility (10days). VolPIN is the probability of option volatility information-based trading instock/option i of biweek t− 1, which is calculated by αθµ

αθµ+α(1−θ)ν+2εand DirPIN

is the probability of option volatility information-based trading in stock/option

i of biweek t− 1, which is calculated by α(1−θ)ναθµ+α(1−θ)ν+2ε

. The dummy is defined to

be 1 if IV>Realized Volatility(RV), 0 otherwise. Log(Market Cap) is the naturallogarithm of t−1 period last price times total shares outstanding. Log(Daily Op-tion Volume) is the natural logarithm of t−1 period daily average option volume.All the variables are winsorized at 1% level. Time and firm effects are controlledand s.e. is adjusted using robust option. T-stat is reported in parentheses with*** p < 0.01, ** p < 0.05, * p < 0.1.

(1) (2) (3) (4) (5)

VolPIN 0.113*** 0.222*** 0.120*** 0.227*** 0.199***(4.191) (7.399) (3.899) (6.863) (4.620)

I(IV > RV )*VolPIN -0.171*** -0.172*** -0.131***(-14.83) (-14.95) (-4.129)

DirPIN 0.0579** 0.0447 0.0695** 0.0541* 0.0871**(2.096) (1.632) (2.198) (1.736) (2.034)

I(IV > RV )*DirPIN -0.0498(-1.448)

Log(Market Cap) -0.0366*** -0.0368*** -0.0369***(-4.823) (-4.889) (-4.899)

Log(Daily Option Volume) 0.00861*** 0.00819*** 0.00824***(3.088) (2.959) (2.983)

Constant 0.0664*** 0.0697*** 0.588*** 0.599*** 0.601***(6.578) (6.959) (4.701) (4.828) (4.836)

Time Effect YES YES YES YES YESFirm Effect YES YES YES YES YES

Observations 7,993 7,993 7,956 7,956 7,956R-squared 0.002 0.033 0.006 0.038 0.038

No. of Tickers 481 481 479 479 479

37

Table 10: Asset Pricing Test

This table reports the average coefficients of Fama-MacBeth (1973) regression of the (daily) excess return ofstock. Rit = γ0t + γ1tβ̂p + γ2tStockPINit−1 + γ3tV olPINit−1 + γ4tDirPINit−1 + γ5tSIZEit−1 + γ6tYit−1 + ηit,

where Rit is the excess return of stock i in biweek t; β̂p is the portfolio betas calculated from the full periodusing 20 sorted portfolios; StockPINit−1 is the probability of information-based trading in stock i of biweekt− 1, which is calculated by Stock δ∗Stock µ

Stock δ∗Stock µ+2Stock ε; VolPIN is the probability of option volatility information-

based trading in stock/option i of biweek t − 1, which is calculated by αθµαθµ+α(1−θ)ν+2ε

and DirPIN is the

probability of option direction information-based trading in stock/option i of biweek t−1, which is calculated

by α(1−θ)ναθµ+α(1−θ)ν+2ε

; SIZEit−1 is the natural logarithm of market value of equity in firm i at the end of biweek

t − 1, Yit−1 is other control variables. Robust Newey-West (1987) adjusted t-stat is reported in parentheseswith *** p < 0.01, ** p < 0.05, * p < 0.1.

(1) (2) (3) (4) (5) (6) (7)

Portfolio β*104 -0.03 -0.012 -0.99 -1.42 -1.08 -1.03 -1.02(-0.00641) (-0.000) (-0.227) (-0.314) (-0.234) (-0.241) (-0.251)

Stock PIN*103 1.372 0.274(0.28) (0.0496)

VolPIN*103 1.13 1.68 0.815 1.39 1.03(0.668) (1.067) (0.442) (0.742) (0.587)

DirPIN*103 3.80** 3.98** 3.14* 4.17** 3.62*(2.384) (2.624) (1.827) (2.392) (1.901)

Log(Market Cap)*104 1.88*** 1.97** 2.50*** 1.49* 1.25 2.86*** 2.44***(3.308) (2.564) (3.604) (1.894) (1.442) (2.866) (3.323)

Stock Rel Ask Bid Spread*102 -0.757*(-1.960)

Implied Vol -0.00216**(-2.225)

Turnover*105 6.63(0.929)

Constant -0.00337*** -0.00378* -0.00528*** -0.00341 -0.00227 -0.00617** -0.00519***(-3.191) (-2.176) (-2.944) (-1.628) (-0.875) (-2.559) (-3.144)

Observations 8,029 8,024 8,029 8,029 7,964 8,029 8,024R-squared 0.035 0.043 0.050 0.061 0.094 0.055 0.058

Number of groups 26 26 26 26 26 26 26

38

Table 11: Asset Pricing Test (FE Panel Regression)

This table reports the coefficients of fixed effect panel regression of the (daily) excess return of stock. Rit =γ0t + γ1tβ̂p + γ2tStockPINit−1 + γ3tV olPINit−1 + γ4tDirPINit−1 + γ5tSIZEit−1 + γ6tYit−1 + ηit, where Rit

is the excess return of stock i in biweek t, β̂p is the portfolio betas calculated from the full period using20 sorted portfolios; StockPINit−1 is the Stock PIN, the probability of information-based trading in stocki of biweek t − 1, which is calculated by Stock δ∗Stock µ

Stock δ∗Stock µ+2Stock ε; VolPIN is the probability of option volatility

information-based trading in stock/option i of biweek t− 1, which is calculated by αθµαθµ+α(1−θ)ν+2ε

and DirPIN

is the probability of option direction information-based trading in stock/option i of biweek t − 1, which is

calculated by α(1−θ)ναθµ+α(1−θ)ν+2ε

; SIZEit−1 is the natural logarithm of market value of equity in firm i at the end

of biweek t− 1, Yit−1 is other control variables. All the variables are winsorized at 1% level. Time and firmeffects are controlled and s.e. is adjusted using robust option. T-stat is reported in parentheses with ***p < 0.01, ** p < 0.05, * p < 0.1.

(1) (2) (3) (4) (5) (6) (7)

Portfolio β*104 -5.05 -4.92 4.85 -5.13 -3.78 -4.40 -4.73(-0.855) (-0.826) (-0.819) (-0.870) (-0.644) (-0.745) (-0.795)

Stock PIN*103 7.93*** 7.41**(2.692) (2.509)

VolPIN*103 1.74 1.78 1.77 1.06 1.53(1.015) (1.029) (1.028) (0.590) (0.886)

DirPIN*103 5.18*** 5.20*** 4.62*** 4.43** 4.89***(3.097) (3.102) (2.727) (2.520) (2.915)

Log(Market Cap)*104 -50.1*** -50.3*** -47.9*** -50.1*** -71.2*** -50.1*** -48.2***(-8.976) (-8.860) (-8.708) (-7.846) (-10.27) (-8.789) (-8.612)

Stock Rel Ask Bid Spread*102 -0.614(-0.853)

Implied Vol -0.00606***(-6.733)

Turnover*105 -43.6*(-1.753)

Constant 0.0819*** 0.0808*** 0.0769*** 0.0807*** 0.117*** 0.0820*** 0.0763***(8.937) (8.692) (8.441) (7.542) (10.01) (8.421) (8.238)

Observations 8,029 8,024 8,029 8,029 7,964 8,029 8,024R-squared 0.021 0.022 0.023 0.023 0.031 0.023 0.023

No. of Tickers 483 483 483 483 479 483 483

39

Table 12: Regression on Option Rel Ask Bid Spread

This report reports the coefficients from OLS and fixed effect panel regression of option relative ask bidspread. The option relative ask bid spread is defined as the option ask bid spread divide by the average quoteprice (ask+bid

2); Stock PIN is the probability of information-based trading in stock i of biweek t− 1, which is

calculated by Stock δ∗Stock µStock δ∗Stock µ+2Stock ε

; VolPIN is the probability of option volatility information-based trading in

stock/option i of biweek t− 1, which is calculated by αθµαθµ+α(1−θ)ν+2ε

and DirPIN is the probability of option

direction information-based trading in stock/option i of biweek t − 1, which is calculated by α(1−θ)ναθµ+α(1−θ)ν+2ε

;

Initial hedging cost (IC) is the cost to set up a delta neutral position by purchasing ∆ shares of the stockat the ask price and close the position by selling at the bid price, which is calculated by kS∆; Rebalancehedging cost is calculated by νk; Log(Daily Option Volume) is the natrual logarithm of the average dailyoption volume at biweek t. Time and firm effects are controlled and s.e. is adjusted using robust option.T-stat is reported in parentheses with *** p < 0.01, ** p < 0.05, * p < 0.1.

(1) (2) (3) (4) (5) (6)

VolPIN 0.0517*** 0.0513*** 0.0516*** 0.0164*** 0.0164*** 0.0165***(6.646) (6.309) (6.294) (2.608) (2.601) (2.610)

DirPIN 0.111*** 0.110*** 0.110*** 0.0194*** 0.0195*** 0.0196***(11.82) (11.44) (11.44) (2.919) (2.917) (2.924)

Stock PIN 0.266*** 0.261*** 0.261*** 0.0698*** 0.0713*** 0.0713***(17.75) (17.19) (17.14) (5.504) (5.561) (5.565)

IC 0.0516** -0.0589**(2.444) (-2.143)

RC 0.286** -0.144(2.361) (-0.914)

Log(Daily Option Volume) -0.0113*** -0.0112*** -0.0112*** -0.00404*** -0.00401*** -0.00402***(-23.56) (-22.63) (-22.44) (-4.490) (-4.390) (-4.402)

Constant 0.0720*** 0.0717*** 0.0714*** 0.0719*** 0.0717*** 0.0716***(10.78) (10.37) (10.25) (7.512) (7.480) (7.459)

Time Effect NO NO NO YES YES YESFirm Effect NO NO NO YES YES YES

Observations 8,041 7,952 7,952 8,041 7,952 7,952R-squared 0.308 0.304 0.304 0.032 0.033 0.033

No. of Tickers 485 479 479

40

Table 13: Event Study on DirPIN, VolPIN, Stock PIN and Rel Ask Bid

This table reports the coefficients from fixed effect panel regression of the infor-mation measures. The information measures include DirPIN, VolPIN, Stock PINand Option Rel Spread. We only keep the data for biweek t−2, t−1, t, t+1, t+2,where t is the biweek with an earning announcement; Stock PIN is the prob-ability of information-based trading in stock i of biweek t − 1, which is cal-culated by Stock δ∗Stock µ

Stock δ∗Stock µ+2Stock ε; VolPIN is the probability of option volatility

information-based trading in stock/option i of biweek t−1, which is calculated byαθµ

αθµ+α(1−θ)ν+2εand DirPIN is the probability of option direction information-based

trading in stock/option i of biweek t − 1, which is calculated by α(1−θ)ναθµ+α(1−θ)ν+2ε

;option relative ask bid spread is defined as the option ask bid spread divide bythe average quote price (ask+bid

2); Pre-Earning Dummy is defined as 1 if the next

biweek has an earning announcement, 0 otherwise; Earning Dummy is defined as1 if the biweek has an earning announcement, 0 otherwise; Post-Earning Dummyis defined as 1 if the previous biweek has an earning announcement, 0 otherwise.We control the option greeks for the regressions with dependent variables DirPIN,VolPIN and Option Rel Ask Bid Spread. Time and firm effects are controlledand s.e. is adjusted using robust option. T-stat is reported in parentheses with*** p < 0.01, ** p < 0.05, * p < 0.1.

(1) (2) (3) (4)Variables DirPIN VolPIN Stock PIN Option Rel Ask Bid Spread

Pre-Earning Dummy -0.00121 -0.00130 0.00298*** -0.00182***(-0.607) (-0.641) (3.285) (-2.920)

Earning Dummy -0.0130*** -0.00636*** 0.00307*** -0.00345***(-6.709) (-3.217) (3.473) (-5.687)

Post-Earning Dummy -0.00246 -0.00435** -0.00387*** 0.00214***(-1.246) (-2.169) (-4.299) (3.475)

Constant 0.160*** 0.219*** 0.166*** 0.0673***(5.575) (7.485) (313.1) (7.479)

Control for Option Greeks YES YES NO YESTime Effect YES YES YES YESFirm Effect YES YES YES YES

Observations 5,361 5,361 5,358 5,361R-squared 0.015 0.016 0.012 0.145

Number of Tickers 412 412 411 412

41