vision for local governance local gover - new brunswick€¦ · round table on local governance, in...

TRANSCRIPT

Local GovernanceA Vision for

Local Governance in New Brunswick

Report of theMinister's Round Tableon Local Governance

June 2001

ACKNOWLEDGEMENTS

The Round Table members wish to acknowledge theProvincial Government for establishing a Minister’sRound Table on Local Governance, in partnership withrepresentatives of municipal associations, Local Ser-vice Districts and regional commissions. This RoundTable process provided a unique opportunity for keystakeholders to discuss and address a broad range ofissues impacting the local governance system in NewBrunswick.

Round Table members also want to acknowledge anumber of individuals that contributed to the processitself. The report could not have been completed with-out the dedication and assistance of the members ofthe Technical Committee as well as staff at the Depart-ment of the Environment and Local Government. Theseindividuals have worked countless hours in support ofthe Round Table to ensure that its members receivedrelevant information needed to develop their recom-mendations. The Technical Committee members, aswell as departmental staff involved in this process arelisted in Appendix A. Round Table members wish tothank them for their dedication, commitment and pro-fessionalism. Their tireless efforts did not go unnoticedand led to greater understanding by all members of theissues facing New Brunswick’s local governance sys-tem. As well, the effective facilitation of the meetingsprovided by Jacques Paynter was greatly appreciatedby the Round Table members.

TABLE OF CONTENTS

SECTION 1 – BACKGROUNDEstablishment of Minister’s Round Table....................................................... 1Mandate of the Round Table.......................................................................... 3Process for the Round Table.......................................................................... 3Report Overview............................................................................................. 4

SECTION 2 – CHANGES IN THE LOCAL GOVERNANCE SYSTEM SINCE 1966Changes in the System................................................................................. 5Strengths of the System................................................................................ 7

SECTIN 3 – VISION OF THE ROUND TABLE......................................................... 8

SECTION 4 – CHALLENGES FOR THE UNINCORPORATED AREASThe Unincorporated Areas: Description and Trends....................................... 9Governance Structures in the Unincorporated Regions................................. 11Issues Facing the Unincorporated Areas ....................................................... 12What Changes are Needed?.......................................................................... 16Principles Established to Guide Development of Options............................... 16

SECTION 5 – CHALLENGES FACING MUNICIPALITIESDescription and Trends.................................................................................. 20Local Government Structures........................................................................ 21Issues Facing Municipalities.......................................................................... 22What Changes are Needed?......................................................................... 24Principles Established to Guide Development of Options............................. 24

SECTION 6 – OPTIONS AND RECOMMENDATIONSGovernance in the Unincorporated Regions................................................ 26Collaboration on a Regional Basis................................................................ 33Provincial – Municipal Funding...................................................................... 38Property Taxation........................................................................................... 43

CONCLUSION........................................................................................................... 44

DEFINITIONS........................................................................................................... 45

APPENDICES:

Appendix A – Technical Committee and Departmental Staff Assisting Round Table.. 47

Appendix B – Presentations made to the Round Table................................ 49

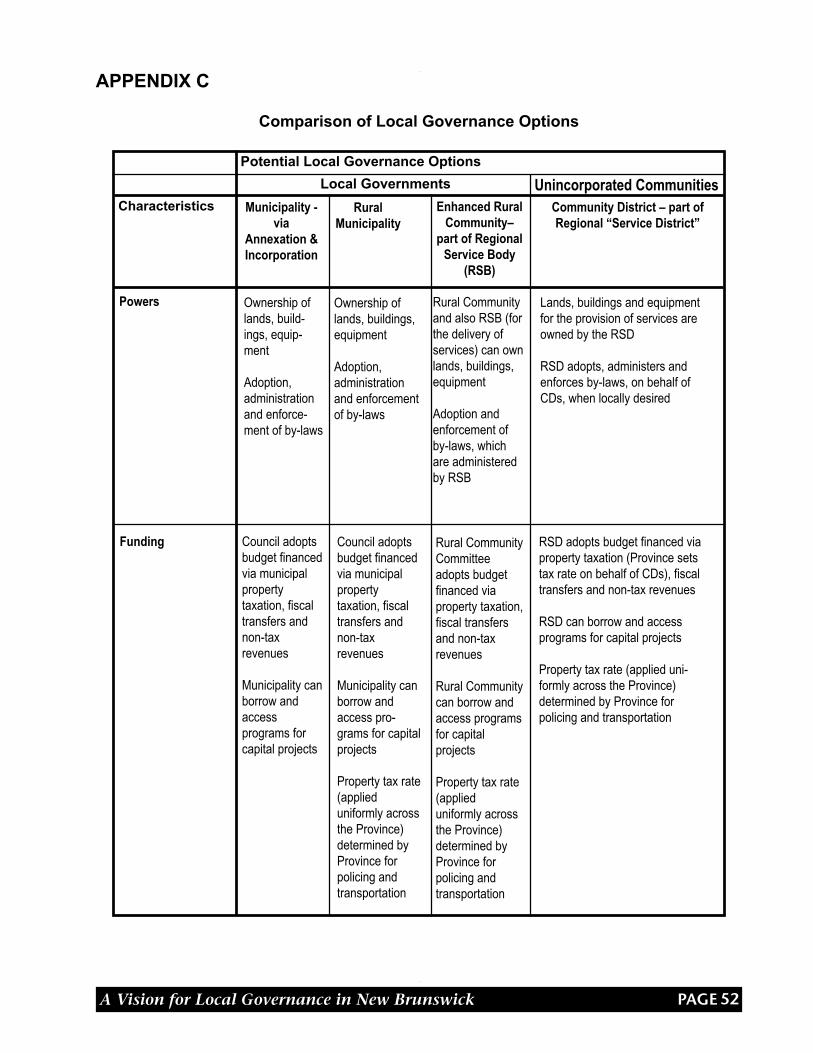

Appendix C – Comparison of Local Governance Options............................... 51

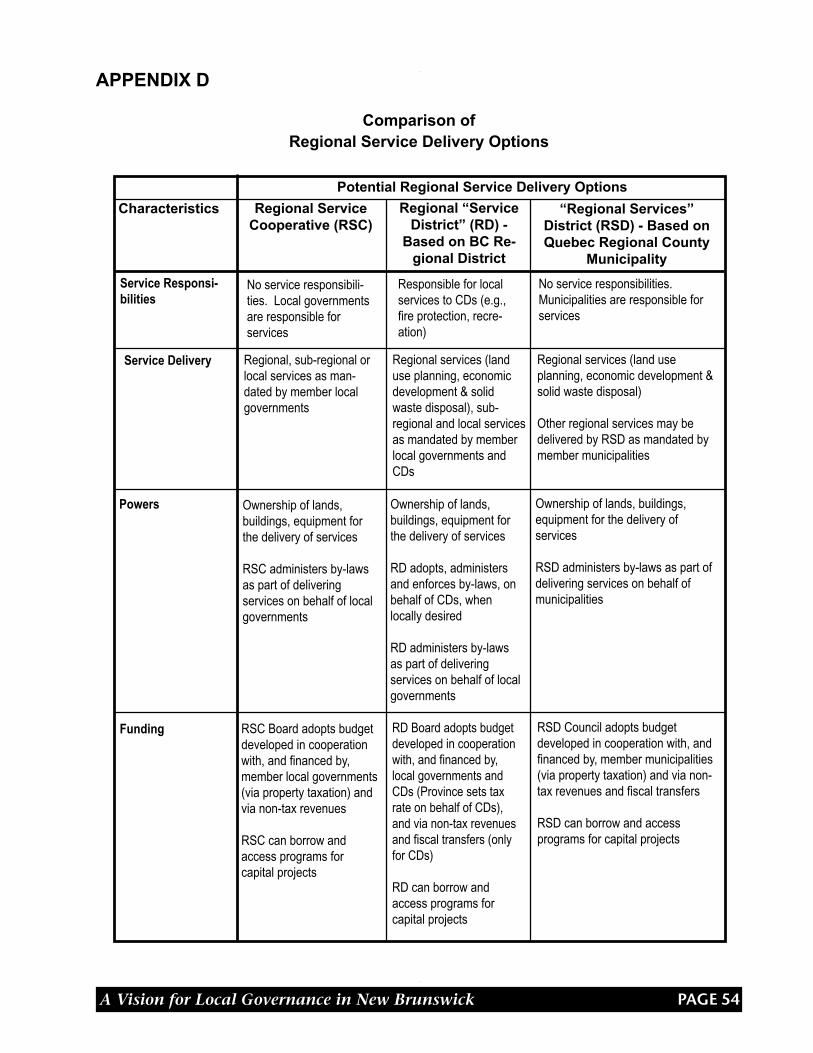

Appendix D – Comparison of Regional Service Delivery Options.................... 53

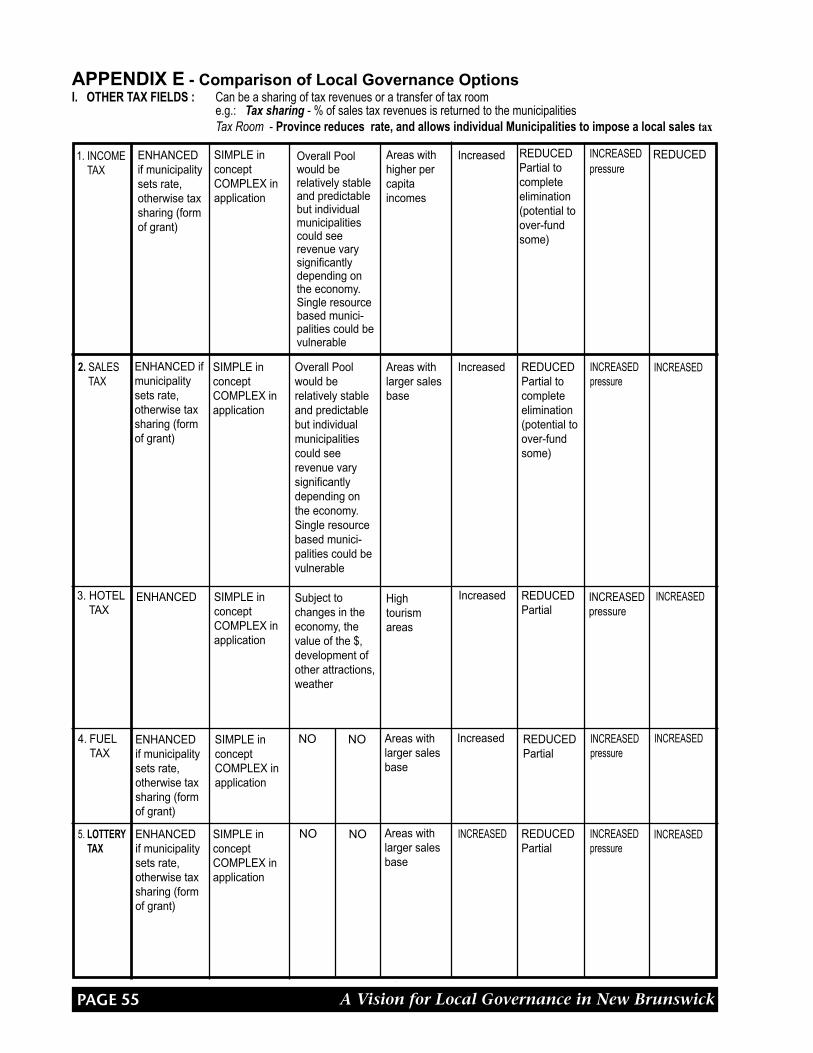

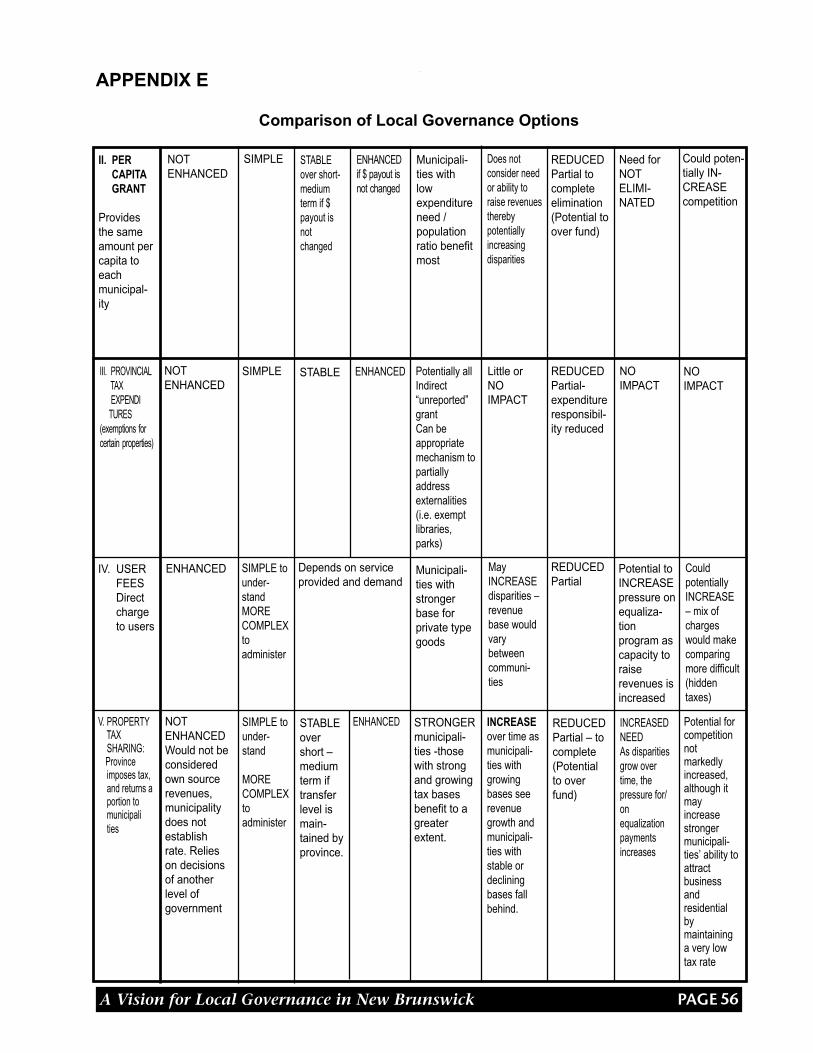

Appendix E – Assessment of Potential Revenue Sources........................... 55

PAGE A Vision for Local Governance in New Brunswick

In recent years, much has been said aboutthe need to change various aspects of thelocal governance system in New Brunswick.The issues that continue to be raised focuson: provincial fiscal transfers to municipalities;local representation, land use planning andproperty taxation in the unincorporated areas(i.e., the Local Service Districts or “LSDs”);and the relationship between municipalitiesand surrounding unincorporated areas.

In light of the changing financial climate, par-ticularly in regards to provincial-municipal fiscaltransfers, municipalities are finding it increas-ingly difficult to balance the demand for qualityservices with acceptable levels of taxation. Inunincorporated areas (suburban and rural), de-velopment continues to occur without beingproperly planned and managed, resulting in avariety of land use conflicts and environmentalimpacts. Relationships between municipalitiesand their neighboring LSDs have, in some in-stances, become strained as a result of issuesrelated to cost-sharing for services, uncontrolleddevelopment adjacent to municipal boundariesand differences in property taxation rules. Whilethese issues are not new, the need to addressthem is becoming more critical.

Given that these issues are interconnected, itwas determined that they should be addressedin an integrated manner, with input from keystakeholders, to ensure that the recommen-dations ultimately developed, whether on struc-ture or finances, would complement one an-other. On this basis, a decision was made bythe provincial government to establish aMinister’s Round Table on Local Governance.

Establishment of theMinister’s Round Table

In December of 2000, the Hon. Kim Jardine,Minister of the Environment and Local Gov-ernment, formally announced the establish-ment of the Minister’s Round Table on LocalGovernance.

In establishing the Round Table, the Ministerrequested that the three associations represent-ing municipalities (Association francophone desmunicipalités du Nouveau Brunswick, Cities ofNew Brunswick Association and the Union ofMunicipalities of New Brunswick) identify indi-viduals who could be named to the RoundTable. Once the names were received, the Min-ister appointed these individuals to the RoundTable. The Minister also appointed individualsfrom the unincorporated areas and the regionalcommissions (Solid Waste, Land Use Planning,and Economic Development) to the RoundTable.

Round Table members were appointed by theMinister, as individuals, to provide their viewsand ideas on the local governance systemas a whole and not just from the perspectiveof their respective community or associations.This approach allowed for effective and posi-tive discussions.

The following individuals were appointed tothe Round Table:

From the Cities of New BrunswickAssociation (CNBA):

Bruce MacIntoshMayor of Campbellton

Paul OuelletteMayor of Bathurst (deceased) replaced by:Jacques MartinMayor of Edmundston

1

SECTION ONEBACKGROUND

PAGEA Vision for Local Governance in New Brunswick

Peter TritesCouncillor, Saint JohnPresident, CNBA

From the Union of Municipalities ofNew Brunswick (UMNB):

Jim BlanchardMayor of Dalhousie

Yvonne GibbExecutive Director, UMNB

Raymond MurphyMayor of Rexton, President,UMNB

From l’Association francophone desmunicipalités du Nouveau Brunswick(AFMNB):

Raoul CharestMayor of Beresford, President, AFMNB

Roland J. MartinMayor of Saint Léonard,Vice-president, AFMNB

Léopold ChiassonExecutive Director, AFMNB(joined the Technical Committee)replaced by:Réginald Paulin,Mayor of Lamèque

From LSD Advisory Committees:

Réjean Bonenfant,Lac Baker LSD Advisory Committee Chair &member of COGERNO (Solid Waste Com-mission)

V. J. (Nick) Hachey,Former Allardville LSD Advisory Committeemember & member of the Nepisiguit-ChaleurSolid Waste Commission

Thomas McLaughlin,Pointe à Bouleau LSD Advisory CommitteeChair

Elizabeth Munn,Upper Miramichi LSD Advisory Committeemember

Sandra Speight,Greenwich LSD Advisory Committee Chair

From regional commissions:

Adélard Cormier,Chair, Kent District Planning Commission,President of the Association of PlanningCommissions

Wayne Flinn,Vice-Chair, Fredericton Region Solid WasteCommission & Chair of the NB Solid WasteAssociation & Chair of Estey’s Bridge LSDAdvisory Committee

Gwen Lister,Economic Development Commissions

From the provincial government:Five Ministers also participated on theRound Table.

Kim JardineMinister of the Environment and LocalGovernment (Chairperson)

Norm BettsMinister of Finance

Margaret-Ann BlaneyMinister of Transportation

Milt SherwoodMinister of Public Safety

Jeannot VolpéMinister of Natural Resources and Energy

2

PAGE A Vision for Local Governance in New Brunswick

Mandate of theRound Table

The Round Table was asked to review fourfundamental aspects of the local governancesystem in New Brunswick and to makerecommendations for improvements. Specifically,the Round Table was to:

ØØØØØ Examine the various issues resulting fromthe current gap in local governance in theunincorporated areas and examine localgovernance models to address these is-sues.

ØØØØØ Examine the relationship between localservices and property taxation levels in Lo-cal Service Districts (LSDs) and examinehow property taxation reflects the servi-ces being provided and their associatedcosts.

ØØØØØ Examine how common services providedon a regional basis such as land use plan-ning, solid waste management, economicdevelopment, recreation and libraries, andwater and wastewater management couldbe more effectively planned, coordinated,financed and delivered.

ØØØØØ Examine the various issues related to thefinancing of local governments (e.g.,property taxation, unconditional grant,user fees, etc.) and the development ofrecommendations aimed at enhancing thefinancial stability and autonomy of localgovernments.

Process for theRound Table

The Round Table met on seven occasionsbetween January and June 2001, each ofwhich was a two-day meeting. The meetingsincluded a combination of presentations anddiscussions. The information andpresentations for the meetings were prepared,for the most part, by the Technical Committeeand staff from the Department of Finance andthe Department of the Environment and LocalGovernment.

During its deliberations, the Round Tableheard from representatives of differentjurisdictions across Canada including NovaScotia, Quebec and British Columbia. TheRound Table also had an opportunity to hearacademic perspectives on municipal financingand governance. A listing of all thepresentations is outlined in Appendix B.

Round Table participants had an opportunityto share their experiences, perspectives andideas, to debate the issues and to developpotential solutions. As part of this process, avision and guiding principles wereestablished, the key issues facing the localgovernance system were identified, a varietyof options to address these issues wereconsidered and a series of recommendationswere formulated.

This Round Table approach provided a uni-que opportunity to discuss critical issuesconfronting the local governance system inNew Brunswick and to develop potentialsolutions. This approach marked the first timerepresentatives from all three municipalelected officials’ associations, from LocalService Districts, from regional commissions,as well as Cabinet Ministers jointly developedrecommendations having the potential toshape the future of the local governancesystem.

3

PAGEA Vision for Local Governance in New Brunswick

ReportOverview

The remainder of this Report includes thefollowing sections:

Section Two provides an overview of wherewe have been since the 1966 reformsrecommended by the Byrne Comission wereimplemented. A brief review of some of thestrengths of the current system is alsopresented.

Section Three outlines the vision that wasdeveloped and adopted by the Round Tableduring its deliberations. This “working” visionhelped guide members of the Round Table intheir development of options andrecommendations.

Section Four focuses on the situation in theunincorporated areas. A description of theunincorporated areas is provided (the rural /suburban picture), along with a discussion ofsome of the trends having an impact on theseareas. This is followed by a review of thegovernance structures in place, a descriptionof the critical issues confronting these areasand a summary of the changes needed toaddress the issues. In general terms, the is-sues focus on representation and localdecision-making, collaborative servicedelivery and property taxation. A series ofprinciples that guided the development of op-tions is also presented.

Section Five focuses on the municipalities.A description of municipalities is provided (theurban / suburban / rural picture), along with adiscussion of some of the trends having animpact on municipalities. This is followed bya review of the current municipal governmentstructure, the identification of the criticalissues confronting municipalities and asummary of the changes needed to addressthese issues.

Specifically, the issues deal with collaborativeservice delivery, the relationship betweenmunicipalies and the unincorporated areas,and provincial-municipal fundingarrangements. A series of principles that wereapplied in the development of options is thenpresented.

Section Six describes the options consideredby the Round Table to address the issues,followed by the recommendations of theRound Table.

4

PAGE A Vision for Local Governance in New Brunswick

Changes to the system…

Though local government in New Brunswickpredates confederation, it is perhaps mostrelevant to outline the fundamental changesthat were introduced in 1966 as a result ofthe New Brunswick Royal Commission onFinance and Municipal Taxation, otherwiseknown as the Byrne Commission, named afterits Chair, Edward G. Byrne.

Prior to 1966, local government in NewBrunswick was characterized by two forms:municipalities (primarily towns and cities) andcounties (covering, for the most part, ruralareas). The Byrne commission identifiedsignificant disparities in both the range andcosts of services provided to citizens acrossthe province. These disparities wereparticularly evident in such service areas ashealth care and education. Furthermore, anumber of county governments andmunicipalities were experiencing majorfinancial and management difficulties. It wasrecognized that a major overhaul was needed.

Many of the recommendations put forward bythe Byrne Commission were subsequentlyimplemented by the provincial government byway of the program for Equal Opportunity. Thisresulted in significant changes in terms ofresponsibility for services, property assessmentand taxation, as well as local governmentfunding and structures. The essential aim ofthese changes was to provide all citizens withan “Equal Opportunity” to access and benefit

from minimum standards of service andopportunity regardless of the financialresources of the locality in which they live.

The Creation of Local Service DistrictsThe elimination of county governments left alarge portion of New Brunswick’s populationand land mass as “unincorporated areas”, thatis, with no local government. Local servicesto these areas would be authorized andcoordinated by the provincial government.Servicing areas were to be identified throughthe creation of Local Service Districts (LSDs).The remainder of the province would becovered by incorporated municipalities: cities,towns and villages.

The Division of Service ResponsibilitiesIn terms of servicing responsibilities, the pro-vince would be responsible for the moregeneral “services to people” including health,education, social assistance and justice,thereby ensuring a greater degree ofuniformity (in terms of access and standards)across the province. Municipalities would, onthe other hand, be responsible for the morelocalized “services to property” such as fireprotection, local road maintenance, garbagecollection, policing and recreation. The intro-duction of the Municipalities Act in 1966formalized the new alignment ofresponsibilities for municipalities as well asthe village, town, city and LSD structures.

Though there have been some minoradjustments to the division of responsibilitiesbetween municipalities and the provincialgovernment over the years, it remainsessentially unchanged. In large measure, thisdivision has worked well for the province byway of promoting greater uniformity andaccessibility throughout the province for suchservices as health, education and justice,while at the same time giving localgovernments specific jurisdiction over localmatters. In fact, many other provinces acrossCanada continue to wrestle with the

SECTION TWO

CHANGES IN THE LOCALGOVERNANCE SYSTEM SINCE 1966

5

PAGEA Vision for Local Governance in New Brunswick

entanglement of service responsibilities.Along with the division of serviceresponsibilities, local government structuresare also essentially the same as whenintroduced in 1966, with the exception of theRural Community structure established in1995.

Local Government RestructuringThough the basic structures have remainedthe same, several local governmentrestructuring initiatives have taken place sincethe early 1970s. These have included 16 in-corporations, 93 adjustments to municipalboundaries (i.e., annexations or decrements),as well as 17 amalgamations.

Local Government FundingIn terms of local government funding, EqualOpportunity reforms resulted in the introduc-tion of an unconditional grant that had twopurposes:1) To provide block funding to municipalities

to help maintain property taxation at ac-ceptable levels; and

2) To equalize municipalities’ ability to payfor basic local services in comparison tosimilar municipalities.

The formula used to calculate the distributionof funding support to individual municipalitieshas changed over the years, but in generalterms, the main objective has alwaysremained the same, that is, to supportmunicipalities in financing local services.

Property Assessment and TaxationAs a result of the realignment ofresponsibilities under Equal Opportunity, theprovince now shared the property tax field withmunicipalities in order to cover some of thecosts for education. This realignment alsoincluded the province assuming theresponsibilities for assessment, property taxbilling and collection. These functions werestandardized across the province andmunicipal revenues from property taxationwere now guaranteed by the province. (The

province continues to remit the amount ofmoney levied by municipalities via the localrate, regardless of the amount actuallycollected.) While various adjustments havebeen made to the property taxation andassessment system over the years, thefundamentals of the system remainessentially the same.

Changes in Unincorporated AreasAs for the unincorporated areas, it is worthnoting that a number of studies wereundertaken to address various issues thathave arisen over the years, many of whichcould be linked to the fact that there has beenan absence of local government in theseregions. Of particular relevance was the 1976Task Force on the Unincorporated Areas ofNew Brunswick, which recommended thatLSDs be abolished and be replaced by 11 newmunicipalities covering all of theunincorporated areas. Various other reportswere prepared regarding such issues asurban sprawl. The 1993 Commission on LandUse and the Rural Environment (CLURE) alsohighlighted a variety of major problemsassociated with the absence of localgovernment in unincorporated areas thatshould be addressed. These included:conflicting land uses, ribbon development,unmanaged development just outside themajor centres, the protection of water sourcesand the management of wastewater. Oneparticular change resulting from the CLUREreports was the creation of the RuralCommunity structure, which allowed for theelection of a Rural Community Committeewith the power to adopt a land use plan.

More recently, the 1999 Municipalities ActReview Panel report entitled Opportunities forImproving Local Governance in NewBrunswick made a series of recommendationsaimed at improving the governance situationin the unincorporated areas. In making itsrecommendations, the Panel concluded “…

6

PAGE A Vision for Local Governance in New Brunswick

the [provincial government] must moveforward to develop a more effective frameworkfor local governance for unincorporatedareas...”.

The Strengths of the System…

While a variety of issues having an impact onthe local governance system will be discussedin other sections of this report, the RoundTable also felt it was important to considerand recognize the strengths of the currentsystem that can serve as a foundation for thefuture. The following summarizes some ofthese strengths.

Ø Disentanglement ofservice responsibilities

As noted earlier, one of the legacies of theByrne reforms was the division ofresponsibilities between the province andmunicipalities, which was introduced as ameans of entrenching the notion of “EqualOpportunity. “Services to people” areprovided by the provincial government(primarily education, health, justice, socialassistance) and “services to property” (e.g.,policing, fire protection, recreation, land useplanning, water and wastewater, roads, etc.)are provided by local governments. TheRound Table sees this division of serviceresponsibilities as continuing to beappropriate and important for New Brunswick.

ØØØØØ Municipalities are the cornerstone ofthe local governance system

Municipalities are very much the cornerstoneof the local governance framework in NewBrunswick. It is difficult to imagine the pro-vince without municipalities to manage localroad networks, water and wastewatersystems, recreational facilities, police protec-tion services, fire prevention and suppression

services, solid waste collection and disposalservices and land use planning services.Services provided by municipalities not onlymeet the critical needs of local communities,but they also complement those servicesadministered by the provincial government.Municipalities should remain an important partof the local governance system.

Ø Building on establishedregional colaboration

There are a variety of services to propertiesprovided on a regional or sub-regional basis.Some of these include solid wastemanagement, land use planning, economicdevelopment, fire protection, policeprotection, and recreation. The benefits thatcan be derived through regional collaborationinclude improved effectiveness and makingbetter use of resources through theachievement of economies of scale and,avoidance of duplication of effort.

ØØØØØ Funding for local governments

Though it has been an ongoing source ofdebate and controversy, there has and conti-nues to be recognition of the need to levelthe playing field amongst municipalities toensure that they can provide a reasonablelevel and quality of local services atacceptable levels of property taxation. Thereis a need to ensure that the provincial-muni-cipal fiscal transfer relationship will continueto support municipalities in a fair and equitablemanner.

7

PAGEA Vision for Local Governance in New Brunswick

One of the first tasks of the Minister’s RoundTable was to develop a vision. The visionadopted by the Round Table is as follows:

Through a comprehensive understanding ofthe roles, responsibilities and priorities of lo-cal governance, the Round Table willdevelop a governance concept, whichensures NB citizens:

may live where they want inconsideration of: an appropriatescope of locally desired services,associated costs, andrepresentative decision makingauthority;

may fully and equitably participatein decisions related to: localservices and their associated costs,formulation and application oflegislation, regulations and policyaffecting local activities, planning oflocal services and those naturalresources affecting local economicdevelopment; and

may contribute to the strengtheningof their communities and of theprovince as a whole throughenhanced collaboration on aregional basis.

SECTION THREE

VISION OF THE ROUND TABLE

8

This vision was used by the Round Table asa reference point with respect to the issuesand options that were debated. It was alsomeant to provide an overall direction andframework for the Round Table regarding thedevelopment of its recommendations. Thisvision was further refined through the adop-tion of a series of principles by the RoundTable.

PAGE A Vision for Local Governance in New Brunswick

This section focuses on the unincorporatedareas of the province. In particular, thefollowing sections are presented:

- A description of the unincorporated areas(the suburban / rural picture, population dis-tribution), along with an overview of someof the trends having an impact on theseareas;

- A review of the governance structures inplace – the LSD and Rural Communitystructures;

- A description of the critical issuesconfronting unincorporated areas;

- A summary of the changes / improvementsneeded; and

- A review of the principles that wereestablished to guide the development ofoptions.

The Unincorporated Areas:Description and Trends

The suburban / rural pictureThe unincorporated areas compriseapproximately 40% of the population and 80%of the land mass of New Brunswick. Despitebeing referred to in general terms as the“unincorporated areas”, there are significantdifferences between these areas, which haveover time been divided into Local Service Dis-tricts (LSDs). Some LSDs are located closeto, or immediately adjacent to cities or townsand are very much ”suburban”. These LSDs

are usually characterized by substantialresidential subdivisions and some commercial/ industrial development.

Some LSDs are very “rural” and are generallylocated at some distance from a city or town.They are often dominated by large farmingor woodland areas, and have a very lowpopulation density. Still other LSDs are largerthan many municipalities in terms ofpopulation and geographic area, and have alarge number of large-scale commercial andindustrial operations within their boundaries.Among LSDs there are substantial differencesin tax base and therefore varying levels offinancial capacity in offering local services.Moreover, it is more costly to serve a largeand sparsely populated area.

Another important consideration that should beemphasized is that not all areas withinunincorporated New Brunswick have the sameneeds, desires and attitudes in regard to localgovernance. Residents of some areas haveexpressed a strong interest in seekingincorporation as municipalities, in order to takebetter charge of their future. In some instances,increased interest in incorporation or someother form of governance is a reaction to aparticular situation in a community (e.g.,unwanted development, water and wastewaterproblems, land use conflicts). It should alsobe pointed out that while there may be a stronglocal desire for incorporation, this desire is oftentempered by financial realities; theestablishment of a municipality for an area thathas a low population density and limited taxbase is simply too expensive. This situationbegs the question: could there be a moresuitable option made available tounincorporated areas that would balance localdecision-making authority with financialcapacity?

In other unincorporated areas, there appearsto be very little interest on the part of residentsin moving toward a formalized local

SECTION FOUR

CHALLENGES FOR THEUNINCORPORATED AREAS

9

PAGEA Vision for Local Governance in New Brunswick

governance structure. Residents arecomfortable with the current structure (i.e., theLSD system and the provincial role of ser-vice provider / coordinator) and are veryconcerned that any changes will result inincreased taxation.

The implication of this diversity is that any newgovernance / service-delivery approachesneed to accommodate wide-rangingdifferences in fiscal capacity and in terms ofthe needs and desires of residents ofunincorporated areas.

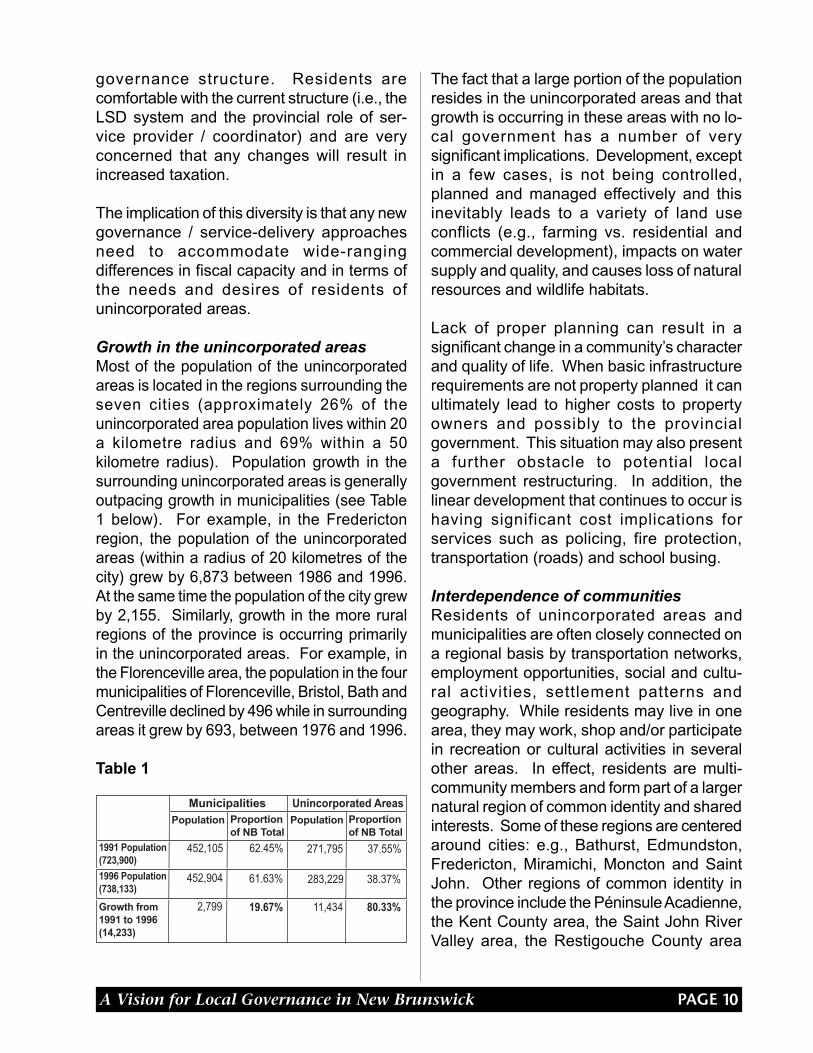

Growth in the unincorporated areasMost of the population of the unincorporatedareas is located in the regions surrounding theseven cities (approximately 26% of theunincorporated area population lives within 20a kilometre radius and 69% within a 50kilometre radius). Population growth in thesurrounding unincorporated areas is generallyoutpacing growth in municipalities (see Table1 below). For example, in the Frederictonregion, the population of the unincorporatedareas (within a radius of 20 kilometres of thecity) grew by 6,873 between 1986 and 1996.At the same time the population of the city grewby 2,155. Similarly, growth in the more ruralregions of the province is occurring primarilyin the unincorporated areas. For example, inthe Florenceville area, the population in the fourmunicipalities of Florenceville, Bristol, Bath andCentreville declined by 496 while in surroundingareas it grew by 693, between 1976 and 1996.

Table 1

Municipalities Unincorporated AreasPopulation PopulationProportion

of NB TotalProportionof NB Total

1991 Population(723,900)

1996 Population(738,133)

Growth from1991 to 1996(14,233)

452,105

452,904

2,799

62.45%

61.63%

19.67%

271,795

283,229

11,434

37.55%

38.37%

80.33%

The fact that a large portion of the populationresides in the unincorporated areas and thatgrowth is occurring in these areas with no lo-cal government has a number of verysignificant implications. Development, exceptin a few cases, is not being controlled,planned and managed effectively and thisinevitably leads to a variety of land useconflicts (e.g., farming vs. residential andcommercial development), impacts on watersupply and quality, and causes loss of naturalresources and wildlife habitats.

Lack of proper planning can result in asignificant change in a community’s characterand quality of life. When basic infrastructurerequirements are not property planned it canultimately lead to higher costs to propertyowners and possibly to the provincialgovernment. This situation may also presenta further obstacle to potential localgovernment restructuring. In addition, thelinear development that continues to occur ishaving significant cost implications forservices such as policing, fire protection,transportation (roads) and school busing.

Interdependence of communitiesResidents of unincorporated areas andmunicipalities are often closely connected ona regional basis by transportation networks,employment opportunities, social and cultu-ral activities, settlement patterns andgeography. While residents may live in onearea, they may work, shop and/or participatein recreation or cultural activities in severalother areas. In effect, residents are multi-community members and form part of a largernatural region of common identity and sharedinterests. Some of these regions are centeredaround cities: e.g., Bathurst, Edmundston,Fredericton, Miramichi, Moncton and SaintJohn. Other regions of common identity inthe province include the Péninsule Acadienne,the Kent County area, the Saint John RiverValley area, the Restigouche County area

10

PAGE A Vision for Local Governance in New Brunswick

(primarily around the municipalities ofCampbellton and Dalhousie) the KingsCounty area and the Southwest corner of theprovince (Charlotte County).

The establishment of regional serviceagencies for such services as solid waste ma-nagement, land use planning and economicdevelopment have furthered these regionalrelationships. Smaller scale inter-municipal,inter-LSD and municipal-LSD servicingagreements (e.g., for fire protection andsuppression, recreation) are also an indicationof the cooperation and inter-relationships thathave evolved over time.

There may be an opportunity to build uponthese regional and sub-regional relationshipsto address some of the issues facing bothunincorporated areas and municipalities,given that so many of these issues crossjurisdictional boundaries (e.g., protectingwater supplies).

Governance Structures in theUnincorporated Regions

There are essentially two governancestructures available to unincorporated areas:the Local Service District or the RuralCommunity.

The Local Service District (LSD)The Local Service District structure isessentially a mechanism to facilitate thedelivery and coordination of optional localservices by the provincial government inunincorporated areas (e.g., street lighting,recreation, fire protection, etc.), which areoften provided by a volunteer organization(e.g., a volunteer fire brigade or recreationcouncil).

The Local Service District is not a form of localgovernment. An LSD Advisory Committee maybe elected via a public meeting process but it doesnot have decision-making authority. It serves inan advisory capacity to the Minister of theEnvironment and Local Government on mattersof local service provision. Public meetings arealso held to vote on the establishment ordiscontinuance of services, but the final decisionon whether a service is established rests with theprovincial government.

The Rural CommunityIn 1995, the “Rural Community” structure wasintroduced, enabling unincorporatedcommunities to elect, via universal suffrage,their own representatives (referred to as aRural Community Committee). A RuralCommunity Committee’s only decision-making power is the adoption andamendment of a land use plan for the RuralCommunity it is elected to serve.

The Rural Community Committee is alsoresponsible for receiving petitions from theelectorate of the Rural Community regardingthe establishment or discontinuance ofoptional local services (such as fire protec-tion, community services and street lighting),for calling and running public meetings for avote on service establishment ordiscontinuance, and for providing advice tothe Minister following a vote at a publicmeeting.

An initial “pilot” rural community, theBeaubassin-East Rural Community(comprised of six former LSDs), wasestablished in 1995. To date, it remains theonly Rural Community in the province. Whythere is only one Rural Community in placemay be partly attributed to the lack of aprovincial implementation strategy and theneed to bring about legislative changes tofacilitate their operation. It might also beattributed to the fact that the Rural Community,

11

PAGEA Vision for Local Governance in New Brunswick

in its current form, does not offer enough tocommunities in terms of local decision-makingauthority.

NOTE: In the case of both the LSD and RuralCommunity, there are three types of services:1) Provincially provided mandatory services:

Policing, transportation (roads), adminis-tration and dog control (which are fundedpartially through a special provincial levyof 65 cents per $100 of assessment onresidential owner-occupied properties);

2) Designated services (through legislation):Land use planning, solid waste collectionand disposal, cost of assessment (paid forthrough property taxation); and

3) Elective services (optional): typically fireprotection, recreation, community servi-ces, street lighting (paid for through thelocal property tax rate).

Issues Facing theUnincorporated Areas

Unincorporated areas are facing a number ofissues, many of which can be attributed tothe lack of a formal local governancestructure. The issues described below havebeen identified through various sources and,as noted earlier, many are not new. Sourcesof information have included previous reportssuch as the 1999 Report from theMunicipalities Act Review Panel and theReport from the Commission on Land UsePlanning and the Rural Environment.Ongoing dialogue with representatives of theunincorporated areas (including theBeaubassin East Rural Community) anddiscussions with municipal officials and theirrepresentative associations have also beensources of information.

On local decision-making andgovernance…

Recognized and legitimate representationof communities:A need for a local decision-making body thatcan make decisions on behalf of a community(and be accountable for these decisions) onmatters of local concern and that is formallyrecognized by municipalities and the provincehas been identified. Currently, unincorporatedareas do not have representatives who areelected via universal suffrage (with the oneexception being the Beaubassin East RuralCommunity). The LSD Advisory Committeesthat are in place and elected through a voteat a public meeting have no authority to makedecisions. This lack of authority underminestheir ability to be a recognized and legitimatevoice within and outside their communities.

Enhancing citizen involvement in localaffairs:A desire has been expressed to enhancecitizen involvement in local issues. One wayto accomplish this might be to strengthen theirinfluence on decisions that affect their res-pective communities. Currently, there arenumerous Local Service Districts that do nothave an Advisory Committee (approximately30% of the 270). Part of the reason for thislack of interest is that these committeesultimately have no decision-making authority.While their involvement may vary from regionto region, there are many AdvisoryCommittees (including the Beaubassin EastRural Community) that feel that they do nothave influence on local matters. This feelingexists despite being elected via a publicmeeting process (or though universal suffragein the case of the Beaubassin East RuralCommunity Committee) to advise the Ministeron matters of local service provision.

Regulating local activities:

12

PAGE A Vision for Local Governance in New Brunswick

Some communities have identified problemsin regulating activities such as noise causingpublic nuisance, dangerous or unsightlypremises and outdoor exhibitions andconcerts. LSD Advisory Committees and theRural Community Committee do not have anyregulatory authority to govern activities in theircommunities. Regulation making authority inthese areas rests with the provincialgovernment.

Emphasizing the need and value of landuse planning:Approximately 20% of LSDs have some formof local land use plan in place and many ofthese plans are not adequate. The lack ofland use planning has led to land use conflicts,loss of community character, problems withwater quantity and quality, as well asunnecessary duplication of infrastructure,facilities and services. Coordinated land useplanning can help to ensure the future well-being of communities. The establishment ofa local government body could result in acommunity being able to more actively pursuethe adoption and enforcement of an effectiveland use plan that would ensure moreappropriate and sustainable development.

Local ownership of public properties andlands:Often, there is a local desire to own and ma-nage public properties that support the so-cial, cultural and economic development ofthe community. However, local publicownership and management of suchproperties is difficult because the LSD is nota body corporate (and it is not always possi-ble for a non-profit organization to assumethe ownership / management function). Inmost instances, ownership of propertiesassociated with service provision inunincorporated areas is vested with the pro-vincial government (e.g. fire halls).

In addition, lands for public purposes or money

in lieu of lands for public purposes cannot bevested in a Rural Community Committee orwith a Local Service District AdvisoryCommittee as part of a subdivision plan. Thisresults in the loss of potential publiccommunity resources such as parks, tourismattractions, or historic sites. There is a needto enable local ownership of public propertiesand the vesting of lands for public purposes.

Strengthening natural communities:Over the years, many “natural communities”have been divided into several LSDs, andsometimes into further taxing authoritieswithin the LSDs themselves. These divisionshave, in some instances, resulted in aweakened sense of community and a reducedemphasis on collective decision-making.Opportunities to make decisions that wouldbe beneficial to the community as a wholeneed to be fostered (e.g., sharing of costs fora service, development of effective land useplans). If change is to occur, there is a needto emphasize communities of interest and theimportance of collective decision-making forthe betterment of communities as a whole.

Preserving community character:A key concern that has been expressed byRound Table members is the need torecognize that communities are different andthat citizens want to preserve the characterof their communities. Citizens should be ableto influence and guide the growth anddevelopment of their communities in order toensure a desired quality of life.

On budgeting, finances and propertytaxation…

A desire to have input and control on thelocal budget:There is a desire to have local decision-making authority on budget decisions that willaffect service delivery and ultimately, local taxrates. Currently, the LSD Advisory Committee

13

PAGEA Vision for Local Governance in New Brunswick

and the Rural Community Committee onlyhave a very limited advisory role with respectto establishing local budgets for service pro-vision. In LSDs where there is no AdvisoryCommittee, there is no citizen input providedto the Minister on matters of budgetpreparation.

Access to capital financing:In many unincorporated areas, there is a pres-sing need to upgrade or replace agingequipment and infrastructure, particularly for fireprotection. The present limitations for thefinancing of capital acquisitions on behalf ofLSDs and the unfavorable terms for suchborrowing needs to be examined. (e.g.,currently, fire trucks are acquired through theProvince’s Vehicle Management Agency, whichonly permits a five-year lease purchaseagreement, while the expected useful life of thevehicle is very likely to be 15 to 20 years. ) Thisshort financing period is an obstacle, for mostLSDs, to purchasing this type of equipmentbecause of the large increase on the local taxrates required to repay the debt). Access tospecial capital funding programs by the LSDs,such as the Canada – New BrunswickInfrastructure Program, is also limited. Attemptsto access funding for water and wastewaterinitiatives are extremely limited unless the LSDis able to establish and administer a specialcommission for this purpose.

Equitable property taxation rules:In the unincorporated regions, policing,transportation, administration and dog controlservices are provided by the provincialgovernment. A provincial levy of 65 cents per$100 of assessment, which is not directlylinked to the cost of providing these services,is charged to owner-occupied residentialproperties. This levy is not charged toresidential non owner-occupied properties(e.g., cottages and apartment buildings) or tonon-residential properties (e.g., businesses).The question is – should the cost of theseservices be borne by all property owners, as

is the case in municipalities?

Linking the cost of service provision toproperty taxation:There is no direct link between the costs ofprovincially provided local services in theunincorporated areas and the 65 cent levy,which has remained at this level since 1984.It has been estimated that the gap betweenthe cost of the services and the revenueraised is at least $22 million.

Members of the Round Table have identifieda need to determine more specifically the costof provincially provided local services(policing, transportation, administration, dogcontrol) and that this cost should be reflectedin the property taxes levied.

Application of the unconditional grant tounincorporated areas:Representatives of the unincorporated areason the Round Table also indicated that thereis a need to revisit the unconditional grantformula applied to LSDs in order to ensurethat the pool available to these areas(approximately $3 million) is distributed in themost equitable manner.

On collaboration and service delivery…

There are several issues to be addressed inregards to delivery of services on a regionaland sub-regional basis, which affectunincorporated areas.

Improving accountability of regional ser-vice commissions:While they are required to pay their share ofthe operating cost of regional serviceagencies, (Solid Waste Commissions, DistrictPlanning Commissions) residents ofunincorporated areas do not feel they haveenough say as to who their representativeswill be. The Minister appoints unincorporated

14

PAGE A Vision for Local Governance in New Brunswick

area representatives which means they areneither locally chosen or elected and thereforehave no direct accountability to the citizensserved. In the case of Economic DevelopmentCommissions, there is no representation (norany funding) from LSDs, yet these agenciesserve unincorporated areas.

Emphasizing land use planning:While all unincorporated regions pay for landuse planning services through property taxa-tion, they are not necessarily receiving theservice they expect and support financially.If communities are paying for the service ofland use planning, there is a need to ensurethat they receive an equitable level of service.

Growth in unincorporated areas continues tooccur without the benefit of adequate land useplanning. Land use planning commissions,in conjunction with the provincial government,need to be proactive in promoting the benefitsof land use planning and moving toward theadoption and implementation of rural plansto cover all areas of the province. Too often,land use planning is perceived as an obsta-cle to development and not as a tool to fosterproper and sustainable development. Plansshould respond to local needs anddemonstrate sensitivity to the regionalsituation (i.e., land use plans must becomplementary).

Adequate resources to meet planningresponsibilities:For some commissions, particularly land useplanning commissions, the availability ofresources, both financial and human, is anissue. While they have been mandated toprovide land use planning services to theirmember communities, their ability to respondto community needs is being hampered bythe lack of financial resources, which in turnmakes it difficult to attract and retain planningpersonnel in the province.

A forum to address regional issues:

There are many issues that spill overjurisdictional boundaries, yet there is noformal mechanism to address them.Municipalities and unincorporated areas donot have a framework that will allow them toeffectively engage in a dialogue over issuesthat cross their boundaries (for example, pro-tection of water supplies, determining infras-tructure needs, minimizing land use conflicts,protecting natural resources and agriculturallands). Regional issues most often requireregional responses, and there is no structurein place to allow this to happen.

Matching who benefits with who pays forservices:Municipal officials have on many occasionscomplained that residents of theunincorporated areas are benefiting from ser-vices their municipalities offer (e.g.,recreational facilities, libraries). However,residents of unincorporated areas do not havea say in these services provided bymunicipalities, which happen to benefit anarea larger than the municipality’s boundaries.Moreover, a number of municipal facilitiesaround the province were built withoutsecuring the initial support of surroundingunincorporated areas. A more formalizedmechanism would facilitate partnership,collective-decision making and cost sharingwith respect to services that benefit more thanjust one community. Such a mechanism couldhelp ease some of the tensions that havesurfaced between unincorporated areas andmunicipalities regarding cost sharing forservices.

A “fair sharing” approach:While it is important to consider approachesthat will foster the sharing of costs for servi-ces of a regional nature, it is equally impor-tant to consider how the decisions regardingcosts of these services can also be shared.Fairness not only implies sharing in benefitsand costs of a service, but also sharing in thedecisions that affect the costs of the service.

15

PAGEA Vision for Local Governance in New Brunswick

What Changesare Needed?

The preceding considerations suggest thatthere are several issues to be addressed inorder to enable citizens and communities ofthe unincorporated areas to take charge oftheir futures. It is clear that the status quo isno longer an appropriate option. The currentLSD and Rural Community structures are notadequate to deal with the issues confrontingunincorporated areas. The following is a briefsummary of the changes that should beconsidered in regards to structure, servicedelivery and finances for unincorporatedareas:

ØØØØØ Provide for formally elected representation(via universal suffrage)

ØØØØØ Provide for local decision-makingauthority on matters of local servicedelivery and local activities

ØØØØØ Provide for appropriate access to capitalfinancing for purposes of service delivery

ØØØØØ Provide for local ownership of property andfor the vesting of lands for public purposes

ØØØØØ Emphasize the strengthening of naturalcommunities of interest

ØØØØØ Emphasize collective approaches todecision-making: locally and regionally

ØØØØØ Provide citizens with the tools to preservetheir communities’ character and qualityof life

ØØØØØ Emphasize land use planning as essentialto the future sustainability of communitiesand the quality of life they offer

ØØØØØ Provide a mechanism through which ef-fective cooperation can occur on aregional or sub-regional basis (on serviceprovision and issue resolution).

ØØØØØ Provide for improved accountability, andinvolvement in, regional service deliveryorganizations.

ØØØØØ Ensure that all property owners in theunincorporated areas contribute torecovering the cost of provincially providedservices through direct property taxation.

ØØØØØ Provide for a better link betweenprovincially provided services andproperty taxation levels.

Principles

The following principles were used as a basisfor developing potential options to address theissues confronting the unincorporated areas.

On local decision-makingand governance…

1. A form of local governance for all citizens with:- Elected representation- Accountability of representation- Responsibility and authority

All citizens of New Brunswick should haveaccess to a form of local government,which means choosing electedrepresentatives through formalcommunity-wide elections (i.e., throughuniversal suffrage). Those personselected should have the authority to makedecisions on behalf of their community andmust be accountable to the community fortheir decisions. Local autonomy in makinglocal decisions regarding local mattersmust be enabled and respected.

ØØØØØ LSDs want input with authority onwhat happens in their communities,without seeking permission fromsenior levels of government: Thecurrent LSD Advisory Committee doesnot have decision-making power with

16

PAGE A Vision for Local Governance in New Brunswick

respect to local service provision orother matters affecting theircommunities. This situation needs tochange. Local matters require localdecision-making.

ØØØØØ Minimum level of local governance:There should, at the very least, besome minimal form of localgovernance covering all of NewBrunswick.

ØØØØØ Local autonomy to make localservicing decisions: Localgovernments should have enoughflexibility to act as they wish on matterswithin their jurisdiction. The level,quality, and scope of services shouldbe a matter of local determination(subject to provincially establishedstandards).

ØØØØØ Communities want to take controlof development within theirboundaries: There are increasingdevelopment pressures across NewBrunswick. For many communities inthe unincorporated regions, the abilityto control this development is verylimited. Communities want to have themeans to control and managedevelopment to preserve communitycharacter and quality of life and toensure sustainability for the future.

ØØØØØ Respect from the provincialgovernment: There is a need toensure that the provincial governmentrecognizes and respects locallyelected officials. This means ensuringongoing consultation and communica-tion with local representatives.

2. Recognition of the uniqueness ofjurisdictions: Any changes that do occurshould accommodate and recognize asmuch as possible the uniqueness ofcommunities across the province. Thereare significant differences between the

various unincorporated areas of the pro-vince (e.g., not all unincorporated areasare rural, not all are interested in full-scalelocal government). Flexibility of any newapproaches would be essential toaccommodate these significantdifferences. Some areas may be readyand have the financial capacity toincorporate as a full-service municipality,while others may only have the capacityand/or desire to take responsibility for oneor two services.

ØØØØØ Choices for a variety of localgovernance models withunderstood consequences: Thereshould be a choice in the type of localgovernment a community wishes toestablish, but the consequences ofthese choices must be understood.

3. Establishing boundaries in accordancewith communities of interest:If boundaries of communities areultimately to change, the changes shouldreflect established social, cultural,recreational, employment, environmentaland economic linkages.

4. Restructuring should be Communitydriven, facilitated by Government:If changes are to occur, they should, asmuch as possible, be driven bycommunities themselves. The provinceshould play a facilitation role in making thechanges happen. As part of the process,the benefits and costs of restructuringneed to be clearly identified andunderstood. Ultimately, the changesshould benefit both unincorporatedcommunities and existing municipalities.

17

PAGEA Vision for Local Governance in New Brunswick

ØØØØØ Any restructuring should bebeneficial to both LSDs andmunicipalities: If changes are tooccur, the benefits should outweigh thecosts for both municipalities andcommunities in the unincorporatedregions. Furthermore, the benefits andcosts must be clearly identified andunderstood.

5. Communities should be proactive inworking towards local government:Establishing some form of localgovernment that will allow for localdecisions to be made on local matters isseen as a necessary step by the RoundTable. It is important for communities tounderstand the benefits and costs oftaking charge of their future through theestablishment of local governments.

On service delivery and collaboration…

6. The aim of sharing responsibilities andcosts of services between jurisdictionsshould be efficiency and quality: Theresult of sharing of services and costsshould be to provide the needed range andlevel of services at a cost each communitycan afford.

7. Communities must be part of thedecision-making process if they are toparticipate in cost-sharing: Truecooperation requires that participatingcommunities not only be willing to pay forthe services they benefit from, but shouldalso be able to directly influence decisionsthat affect the cost, quality and level of theservice provided.

8. Activities between unincorporatedcommunities and municipalities mustbe transparent: If there is to be true andpositive cooperation, there is a need for a

framework that promotes consultation,openness and access to informationamong all parties involved.

9. Land use planning on a regional basisis essential: If land use planning is to beemphasized, there should be a strong linkmade to regional considerations.Individual land use plans within a regionshould not conflict or undermine oneanother, but rather should becomplementary.

On budgeting, finances and propertytaxation…

10.Communities are prepared to pay forwhat they get but must get what theypay for: If a service is paid for by propertyowners, the level of the service they arereceiving should reflect the amount beingpaid.

11. Taxation with local representation: Ifproperty owners are to be taxed for servi-ces, they must be formally representedwhen determining what services are to beprovided, the level of the service providedand the cost of this service. Local inputmust be more than an advisory role.

12.All property owners should share in thecost of policing and transportation ser-vices: Owners of residential, residentialnon owner-occupied and non-residentialproperties should share in paying for thecosts associated with policing andtransportation in the unincorporated areas.

13.Continuation of grant funding: Grantsupport should remain as a source offunding for communities in theunincorporated areas. No matter whatstructural changes might occur, it is verylikely that some form of funding support

18

PAGE A Vision for Local Governance in New Brunswick

will be required. If the unconditional grantfor unincorporated areas is to remain,there is a need to review the formula asapplied to unincorporated areas to ensurethe most equitable distribution of thefunding pool.

19

PAGEA Vision for Local Governance in New Brunswick

This section focuses on municipalities.Specifically, the following is presented:

- A description of municipalities – the urban/ suburban / rural picture, population dis-tribution, along with an overview of someof the trends impacting on municipalities;

- A brief review of the current municipalstructure

- A description of the critical issuesconfronting municipalities;

- A summary of the changes / improvementsneeded; and

- A review of the principles that wereestablished to guide the development ofpotential options.

Municipalities –Description and Trends

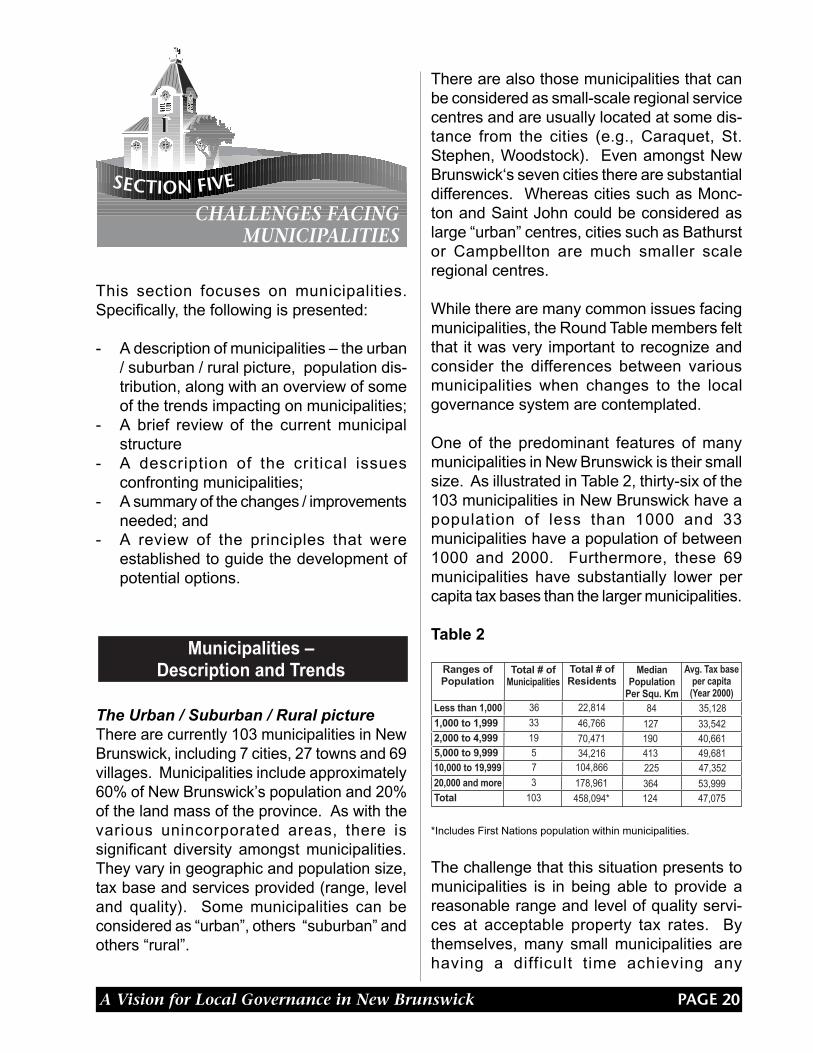

The Urban / Suburban / Rural pictureThere are currently 103 municipalities in NewBrunswick, including 7 cities, 27 towns and 69villages. Municipalities include approximately60% of New Brunswick’s population and 20%of the land mass of the province. As with thevarious unincorporated areas, there issignificant diversity amongst municipalities.They vary in geographic and population size,tax base and services provided (range, leveland quality). Some municipalities can beconsidered as “urban”, others “suburban” andothers “rural”.

There are also those municipalities that canbe considered as small-scale regional servicecentres and are usually located at some dis-tance from the cities (e.g., Caraquet, St.Stephen, Woodstock). Even amongst NewBrunswick‘s seven cities there are substantialdifferences. Whereas cities such as Monc-ton and Saint John could be considered aslarge “urban” centres, cities such as Bathurstor Campbellton are much smaller scaleregional centres.

While there are many common issues facingmunicipalities, the Round Table members feltthat it was very important to recognize andconsider the differences between variousmunicipalities when changes to the localgovernance system are contemplated.

One of the predominant features of manymunicipalities in New Brunswick is their smallsize. As illustrated in Table 2, thirty-six of the103 municipalities in New Brunswick have apopulation of less than 1000 and 33municipalities have a population of between1000 and 2000. Furthermore, these 69municipalities have substantially lower percapita tax bases than the larger municipalities.

Table 2

Total # ofMunicipalities

MedianPopulation

Per Squ. Km

Total # ofResidents

Avg. Tax baseper capita(Year 2000)

Less than 1,000

1,000 to 1,999

2,000 to 4,999

36

33

19

22,814

46,766

70,471

84

127190

35,128

33,54240,661

5,000 to 9,999 5 34,216 413 49,68110,000 to 19,999

20,000 and more

Total

7

3

103

104,866

178,961

458,094*

225

364124

47,352

53,99947,075

Ranges ofPopulation

*Includes First Nations population within municipalities.

The challenge that this situation presents tomunicipalities is in being able to provide areasonable range and level of quality servi-ces at acceptable property tax rates. Bythemselves, many small municipalities arehaving a difficult time achieving any

SECTION FIVE

CHALLENGES FACINGMUNICIPALITIES

20

PAGE A Vision for Local Governance in New Brunswick

substantial economies of scale when it comesto service provision. Their low populationdensity adds the further challenge of providingcost efficient services (many municipalitiesthat have small populations have a relativelylarge geographic area to cover). This situa-tion, combined with changes in provincial-municipal transfers, is posing significant chal-lenges to many municipalities in terms of theirlong-term viability. What are the options forthese municipalities? In some instances, oneapproach may be to increase cooperation ona regional basis for services through moreformalized means. Another approach may beto examine opportunities for more effectiveand efficient local governance throughannexation of nearby unincorporated areasor even through amalgamation with othermunicipalities.

Population Growth in MunicipalitiesAs noted earlier, the population growth isoccurring primarily outside municipalboundaries. This is generally the case in theareas surrounding urban centres, the smallerscale regional centres and around ruralmunicipalities. At the same time, populationgrowth in many municipalities is stagnant oreven declining. The implications of how growthin these regions is occurring are far-reachingand their effects are being felt bymunicipalities. The infrastructure (e.g., roads)and facilities (e.g., for recreation) are notnecessarily being used to their potential andthe costs for these services are not beingappropriately shared through property taxa-tion or fees by those who benefit from them.The costs of maintaining this infrastructure andthese facilities fall almost entirely to theresidents of the municipalities.

The Future of Urban CentresApproximately 80% of the population of NewBrunswick lives in or within 50 kilometres ofthe province’s seven cities. The reasons forthis are both historic and economic. Today,the major centres provide employment to a

high percentage of the New Brunswickworkforce. The focus on the urban centresas the job centres for the province will conti-nue and growth in the surrounding regionswill also likely continue. Given this anticipatedgrowth, it will become increasingly importantto find mechanisms through whichcommunities can share in the costs ofservices that have a regional benefit.

Furthermore, issues associated with urbansprawl (e.g., land use conflicts, water /wastewater infrastructure requirements) andlinear development must be dealt with in aproactive manner.

Aging populationAs our population ages, local governments willbe challenged to re-think how and whatservices are offered. Services such asrecreation, public safety, and land use plan-ning will need to be reconsidered in light ofthis changing demographic.

Local GovernmentStructures

Municipalities: Cities, Towns and VillagesMunicipalities are the only local governmentstructure in the province. They provide ser-vices of a local nature to a defined area. Thedecision-making body is the council that iselected via universal suffrage. The council ofa municipality has decision-making authorityon service provision, by-laws, budgets, userfees and tax rates. A council is elected tomake decisions on behalf of citizens for thebetterment of its community. While their size,capacity, services provided and needs maydiffer significantly across the province,municipalities, whether a city, town or village,have the same by-law making and serviceprovision powers.

21

PAGEA Vision for Local Governance in New Brunswick

Generally speaking, municipalities are themain local service providers for theircommunities. However, some services aredelivered by regional commissions on behalfof communities (solid waste management,land use planning, and economicdevelopment). There are also smaller scalesub-regional arrangements in place for theprovision of services between two or morecommunities (e.g., for services such aspolicing, recreation, fire protection).

Issues FacingMunicipalities

This section provides an overview of the keyissues municipalities are facing. Asmentioned earlier, while many of them are notnew, there is a sense of urgency in havingthem addressed, particularly those issuesrelated to provincial-municipal fiscal transfers.

On collaboration and service delivery...

Collaboration to maintain serviceaffordability:Service costs are continuing to escalate, whiletraditional funding sources are diminishing.At the same time, there are demands fromthe public for efficient and high quality ser-vice provision.

Service provision according to administrativeboundaries does not always result in the mostefficient and effective delivery of services. Inaddition, administrative boundaries do notnecessarily capture all those who are actuallybenefiting from services. Municipalities needto collaborate if they are to remain viable andif they are to maintain or improve currentservices at reasonable cost.

Cost-sharing with the unincorporated areas:For many years, municipal officials haveargued that residents of neighboringcommunities, particularly of unincorporatedareas, avail themselves of the services offeredby a municipality, while contributing very little,if anything, to the ongoing operational andcapital costs associated with the service (e.g.,recreational facilities). Often, the contribu-tion of residents of the unincorporated areasis through the same program fees that arepaid by residents of municipalities, or possiblythrough a slightly higher user fee. However,these fees only cover a small portion of thecosts associated with the service (usually theprogramming component). There is a needfor a mechanism that will facilitate moreeffective sharing of costs and of decisionsaffecting those costs between municipalitiesand unincorporated areas for services thathave a regional benefit.

Accountability of regional bodies:From a municipal perspective, theaccountability of regional service commis-sions needs to be improved. Municipalrepresentatives on the commissions often findthemselves in the difficult position of trying tobalance the interests of the municipalities theyrepresent with the needs of the commissionson which they serve. This situation isparticularly evident on budgetary matters andis further complicated when, in some instan-ces, the municipal representative is not amember of the municipal council.

A forum to address regional issues:There are many issues that spill overjurisdictional boundaries, yet there is noformal mechanism to address them.Municipalities and unincorporated areas donot have a framework that will allow them toeffectively engage in a dialogue over issuesthat cross their boundaries (for example, onprotection of water supplies, on determininginfrastructure needs, on minimizing land useconflicts, on protecting natural resources and

22

PAGE A Vision for Local Governance in New Brunswick

agricultural lands). Regional issues mostoften require regional responses, and thereare no structures or tools in place to allowthis to happen. An enabling mechanism isrequired that will facilitate communitiesworking and planning together to find solu-tions to regional problems.

On municipal funding andproperty taxation…

The need for adequate funding:Municipalities have the authority to provide avariety of services. While some municipalitiesmay be well positioned to provide services ata reasonable tax rate (due in large part to astrong municipal tax base), many othermunicipalities are not. These municipalitiesneed funding support beyond what is receivedthrough property taxes in order to provideservices at an acceptable tax rate for theircitizens. Currently, this funding support isprovided through an unconditional grant. Formany municipalities, the funding madeavailable through the unconditional grant,which has been substantially reduced in recentyears, is not considered to be enough toensure appropriate levels of servicing atacceptable tax rates.

Upkeep of Infrastructure:In the coming years, municipal governmentswill have to make significant investments inbasic infrastructure and facilities (e.g., roads,recreational facilities, water and wastewatersystems). There is a need to ensure thatmunicipalities are well positioned financiallyto handle these costs.

The need for stable funding:For the vast majority of municipalities, theprimary source of funding after property taxesis the unconditional grant. The unconditionalgrant pool available to municipalities is subjectto an annual review by the provincial

government. Municipalities have expressedstrong concerns regarding the unpredictableand unstable nature of such an importantcomponent of their funding. The uncertaintysurrounding the unconditional grant has madeit difficult for many municipalities to planahead. This uncertainty has been particularlyrelevant in recent years, given the significantoverall reductions to the unconditional grantpool (from $103 million in 1993 to $67 millionin 2001). Any new funding mechanism shouldbe founded on the basis of enhancedpredictability and stability and not be subjectto significant fluctuations.

Need to reconsider the application of theunconditional grant formula:The 1997 formula, which is nearing the endof its phase-in period, is creating, in the viewof many municipalities, winners and losers. Ifthe formula were to be fully applied in 2002many municipalities would experiencesubstantial reductions in revenue. In responseto these concerns, the Premier announced onJune 14, 2001 that the 2002 grant distributionwould be maintained at the 2001 levels.

Property taxation in the unincorporatedareas:In municipalities, non owner-occupiedresidential and non-residential propertyowners pay for policing, transportation, ad-ministration and dog control services as partof the local property tax rate they are chargedby the municipality. In the unincorporatedareas, owners of non owner-occupiedresidential and non-residential properties donot pay for these services through directproperty taxation. This situation creates asignificant imbalance between incorporatedand unincorporated areas in the treatment ofthese types of properties.

From a municipal perspective, the tax regimeis not neutral and provides a direct incentivefor certain types of development to occur inunincorporated areas. This imbalance

23

PAGEA Vision for Local Governance in New Brunswick

impacts the potential for development withinmunicipal boundaries. It can also be arguedthat this situation is contributing to theproblems associated with the urban sprawlphenomenon. There is a need to addressthis inequity in the property tax regime.

What Changesare Needed?

The trends and issues described indicate thatchanges are needed to ensure thatmunicipalities continue to perform their roleeffectively. Following is a brief summary ofthe changes that should be considered toensure a healthy future for municipalgovernments.

ØØØØØ Provide for a mechanism that will facilitateenhanced cooperation on service deliverybetween municipalities, and betweenmunicipalities and the unincorporatedareas, in order to achieve economies ofscale and to ensure that quality servicescontinue to be available at acceptablerates of property taxation;

ØØØØØ Provide a mechanism and the tools tofacilitate the resolving of issues that crossjurisdictional boundaries (betweenmunicipalities and between municipalitiesand unincorporated areas);

ØØØØØ Improve the accountability andeffectiveness of regional service deliveryagencies;

ØØØØØ Provide for stability and predictability ofthe provincial-municipal fiscal relationship(i.e., stable and predictable transfers);

ØØØØØ Ensure that municipalities are able toremain viable entities that can providequality services;

ØØØØØ Ensure that there is equity in the propertytaxation regime.

Principles

The following principles were used as a basisfor developing potential options to address theissues confronting municipalities.

On cooperation and service delivery…

1. The aim of sharing responsibilities andcosts of services between jurisdictionsshould be efficiency and quality: Theresult of sharing of services and costsshould be to provide the needed rangeand level of services at a cost eachcommunity can afford.

2. Activities between communities mustbe transparent: If there is to be true andpositive cooperation, there is a need for aframework that promotes consultation,openness and access to informationamong all parties involved.

3. Land use planning on a regional basisis essential: If land use planning is to beemphasized, there should be a strong linkmade to regional considerations. Individualland use plans within a region should notconflict or undermine one another, butrather should be complementary.

On funding and property taxation…

4. Adequate Funding: Local governmentshave different expenditure needs andvarying ability to finance suchexpenditures from their own resources.Adequate funding, beyond those revenuesraised primarily through property taxation,is required to fulfill service responsibilitiesat acceptable rates of taxation.

24

PAGE A Vision for Local Governance in New Brunswick

5. Equitable distribution: Equity means thatlocal governments with the same fiscalneed should be treated in a similar manner.Fiscal need is a measure of a municipality’sexpenditure needs relative to its ability toraise its own revenues. Equity does notmean that each municipality will be treatedequally, but rather that each municipalitywill be treated fairly.

6. Neutrality: The principle of neutralitymeans that the funding transfers shouldnot influence the expenditure patterns ofthe recipient. Likewise, a localgovernment should not be able to in-fluence the amount of transfer it receivesthrough its expenditure decisions.

7. Predictability / Stability: Localgovernments should be able to rely on areasonable degree of predictability andstability regarding funding transfers fromthe provincial government. Localgovernments cannot plan for the futurewith confidence if they are subject to largeor unexpected variations in revenues.

8. Respect for Local Autonomy / Choice:Local circumstances, needs and prioritiesvary amongst communities. Localgovernments must be free to determinetheir levels of service, their spending levelsand their taxation rates.

9. Accountability for financial decisions:Local governments must be accountablefor the decisions they make regardingservice provision at the local level andcorresponding property tax rates they set.To help foster this accountability, fundingfrom the provincial government should bestable and predictable.

10.Understandable and transparent: Therecannot be true accountability in the fundingtransfer system unless there is an

understanding of what the system isintended to do and how it works.

11. Access to diversified sources ofrevenue : With increasing pressures to domore with existing resources, localgovernments should have the flexibility toaccess a wider range of revenue sources.Examples of these revenue sources mightinclude additional tax room and user char-ges.

Note: There are a number of other principlesidentified in the section dealing withunincorporated areas that could also beapplied in general terms. For the purposesof the current section, however, thoseprinciples that had the most direct relevanceto municipalities were highlighted.

25

PAGEA Vision for Local Governance in New Brunswick 26

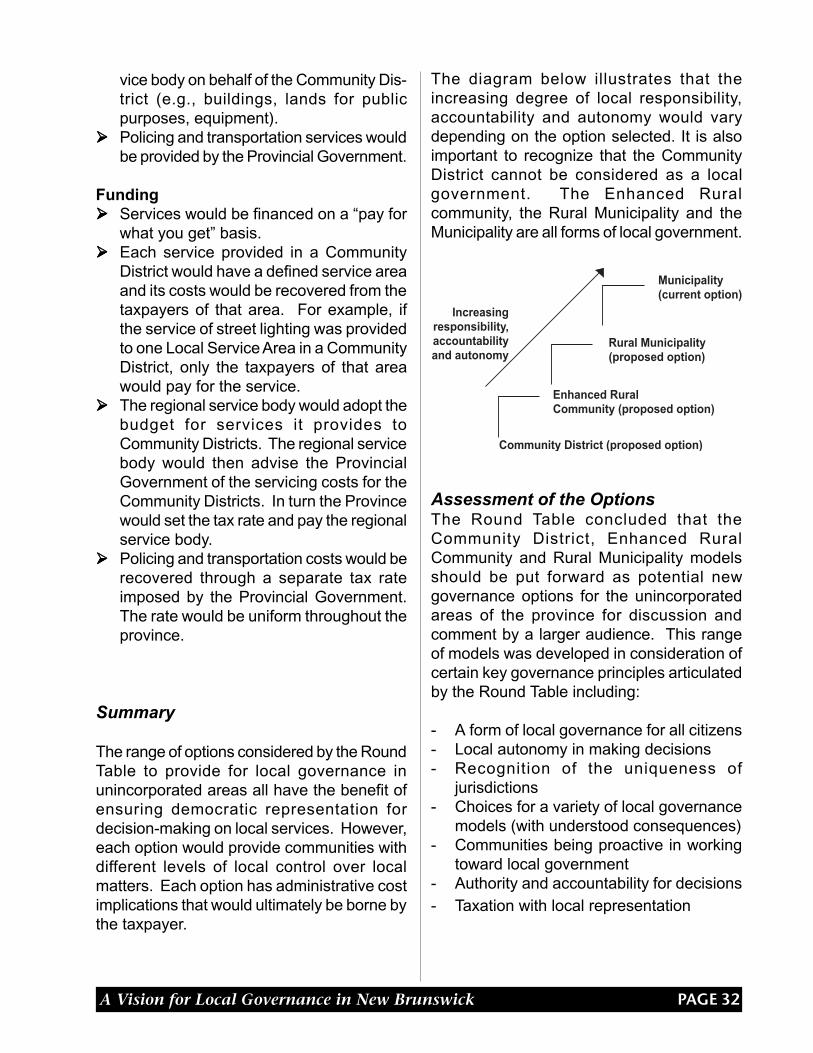

Governance in theUnincorporated Regions

To address the issues identified with respectto governance in the unincorporated areas,the Round Table examined a series of struc-tural options that could be considered for ap-plication to New Brunswick.

Specifically, the following options werereviewed:

1. Administrative adjustments to thecurrent LSD system

2. Regional municipalities (one-tier)3. Regional municipalities (two-tier)4. Incorporation as, or annexation to, a

municipality5. Rural Municipality6. Enhanced Rural Community7. Community District

1. Administrative adjustments tothe LSD system

There are several adjustments that could bemade to the current LSD system to improveit. Examples include giving the LSD AdvisoryCommittee more of a role to play in budgetdevelopment, streamlining the public meetingand service establishment process, and givingthe Advisory Committee more flexibility to

engage the community on matters of localconcern.

While these are all improvements that couldbe made either by policy changes orlegislative amendments and would bebeneficial in the short term, the Round Tablefeels that these changes do not address thefundamental issues that were identified, nordo they reflect the principles that weredeveloped. The Round Table agrees that thisapproach should not be pursued.

2. Creation of Regional Municipalities(one-tier)