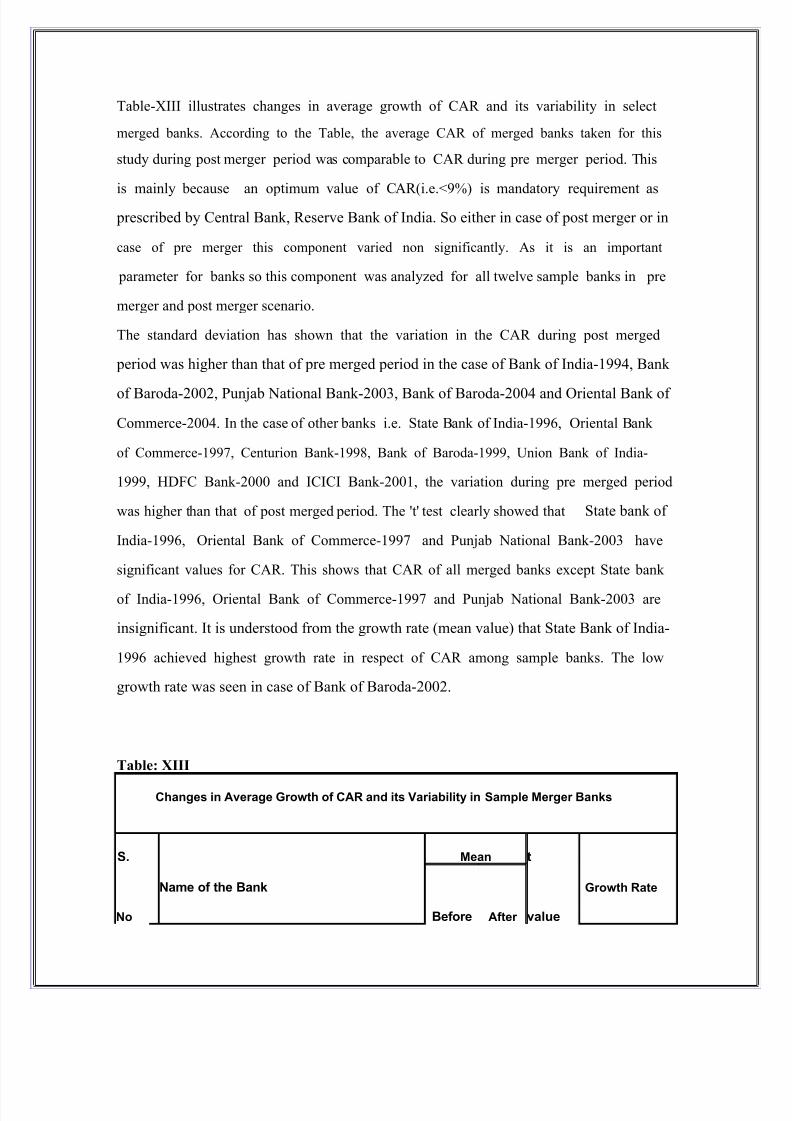

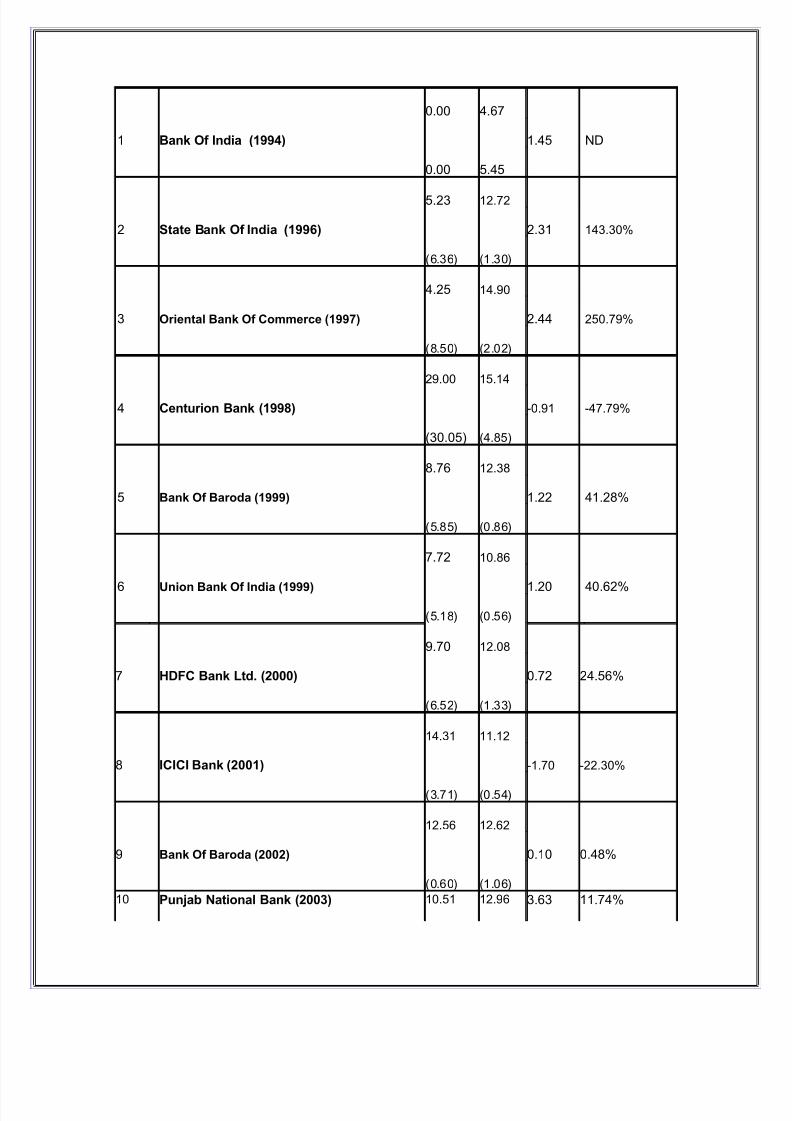

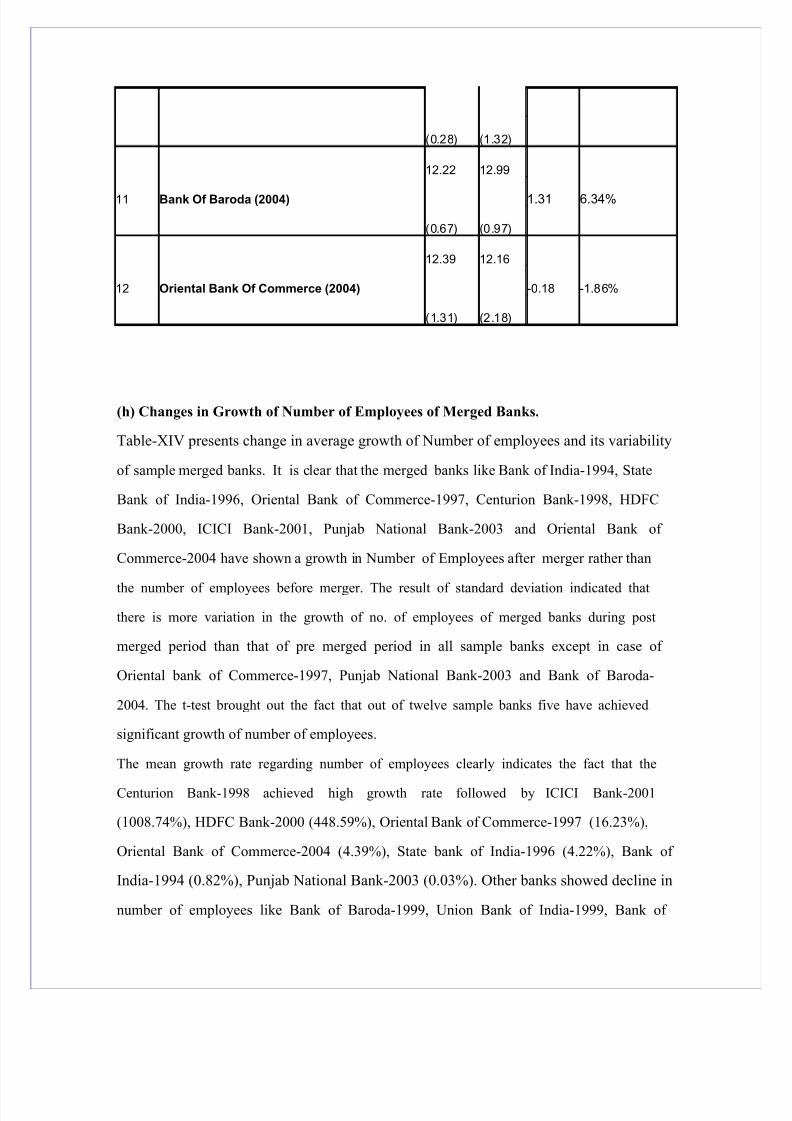

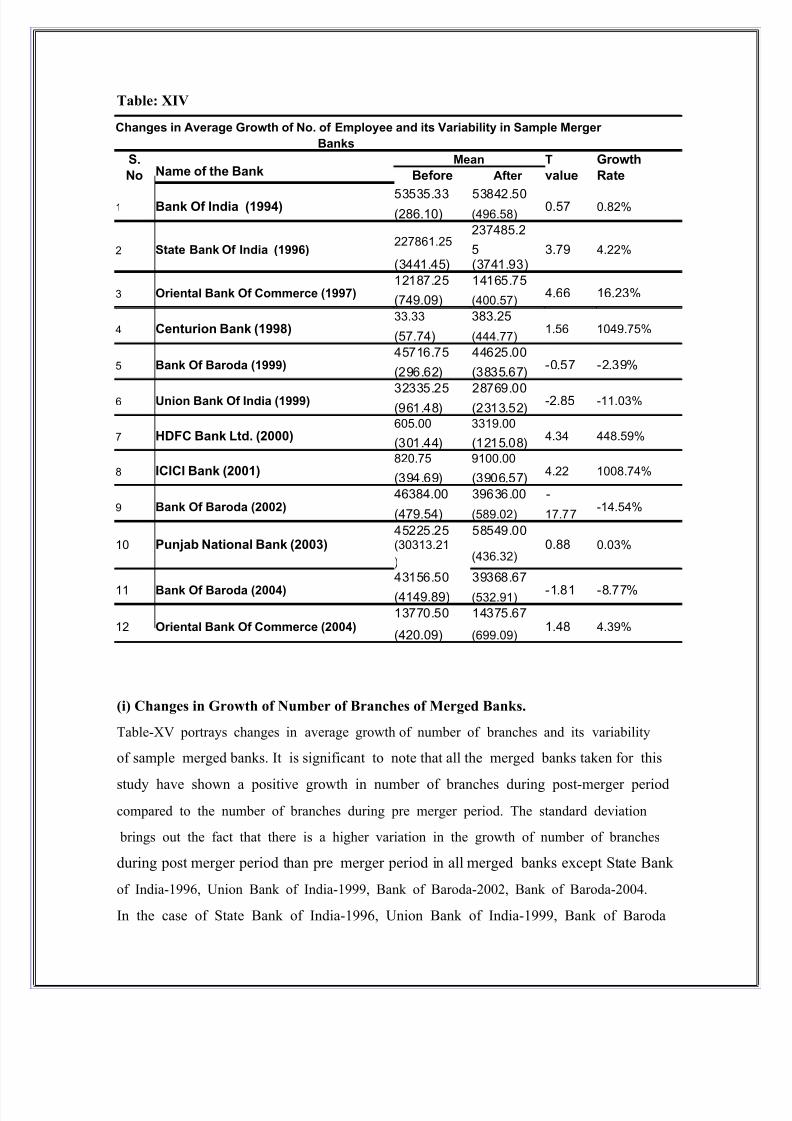

vineet - mrp report

TRANSCRIPT

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 1/83

ACKNOWLEDGMENT

It gives me immense gratification in expressing my sincere and honest gratitude to

everyone who has helped me in completing this endeavor.

I am thankful to Prof. K.V.RAO, my faculty guide (Professor at IBS Hyderabad) for

their meticulous guidance, encouragement and honest feedback that helped us to

accomplish this assignment.

My management research project helped in learning nuances of training and development.

This project has helped me in putting theory into practice. Lastly I would also like to

thank my parents, friends and almighty who blessed throughout the journey. Any

omission in this brief acknowledgement does not mean lack of gratitude.

CONTENTS

1 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 2/83

Serial No. Topic Page no.

1 Abstract 3

2 Overview Of Banking Sector 5

3 Essentials Of M&A 7

4 M&A In Banking - Present Trend 11

5 Advantages Of M&As In Banking 16

6 Factors For M&As Success 20

7 Risks Associated With Mergers 23

8 Banking Structure In India 25

9 Mergers & Acquisition In Indian Banking 28

10 Challenges For Bank Mergers In India 32

11 Pre & Post Performance Evaluation Of

M&As In Indian Banking Industry

33

12 Objective of study 34

13 Methodology Of The Study 35

14 Analysis of the study 37

15 Impact Of Mergers And Acquisition On

Human Resources

63

16 Result and Conclusion 70-74

17 Bibliography 75

ABSTRACT

2 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 3/83

Mergers and Acquisitions have become a global phenomenon in today’s free market

economies wherein companies need to constantly evolve to remain competitive. The

strategy of consolidations gained momentum in the 1980 s in the post oil-shock world

with over 55000 M&As being reported in US alone. These activities gained further

momentum in the nineties and even more so in the new millennium. This activity has

transcended geographical boundaries and made inroads in the developing world too.

Banking has become an increasingly global industry, which knows no geographic and

territorial boundaries. Banking system is deemed as the bloodline of any economy and

banks are trustees of public money. Therefore its depositors have higher stake in welfare

and growth of banks than its shareholders. The failure of a bank has more widespread

implications than a failure of a manufacturing company. Henceforth, the laws governingregulation and supervision of banks in all countries focus on protecting the interest of

depositors. Therefore boost to bank consolidations and mergers in many countries has

come through regulatory and governmental actions in public interest.

Examples:

·

United States witnessed large scale bank failures in the eighties (savings and loaninstitutions) and the government came to rescue of banking system through liberal

FDIC (federal deposit Insurance Corporation) support with estimated USD 100

billion. In the process Government encouraged mergers among banks by giving

incentives to the banks taking over assets and liabilities of failed banks.

· Asian crisis of 1997 exposed the vulnerability of banking systems in the region

and forced governments to initiate several steps for strengthening them. For

instance Hong Kong allowed 100% FDI in Banking sector and this facilitated take

over of several banks by Singapore and Taiwanese Banks.

· Japan which witnessed a virtual collapse of banking system and an economic

stagnation for over 15 years, initiated its consolidation process which has resulted

3 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 4/83

in emergence of three large banks viz. Mitsubishi UFJ, Mizuho and Sumitomo

Mitusui.

While bank consolidation in many countries in Asia and Latin America were triggered by

crisis in the economy and financial sector, some of the mega mergers seen in recent years

in America and Europe are aimed at creating Banking behemoths which can take on any

competition.

Consolidation in banking industry is crucial from various aspects. The factors inducing

consolidation include technological progress, excess retention capacity, emerging

opportunities and deregulation of various functional and product restrictions. A strong

banking system is critical for sound economic growth so it is natural to improve the

comprehensiveness and quality of the banking system to bring efficiency in the performance of the real sector.

The trend towards mergers and acquisitions in banking is also due to unprecedented

growth in competition, the continued liberalization of capital flows, the integration of

national and regional financial systems, financial innovations, etc.

In this scenario, if banks are to be made more effective, efficient and comparable with

their counterparts, they would need to be more capitalized, automated and technology

oriented, even while strengthening their internal operations and systems.

Similarly, in order to make them comparable with their competitors with regard to the size

of their capital and asset base, it would be necessary to structure the banks as early as

possible. It can be out rightly proclaimed that mergers and acquisitions are the real

strategies to achieve the requisite size and financial strength in the shortest possible time.

4 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 5/83

OVERVIEW OF BANKING SECTOR

Banking services are critical to the functioning of any economy because it offers people a

medium to exchange and provide variety of financial services which help them make

profit. A bank is traditionally defined as a financial institution that accepts deposits and

directs these funds to make loans. Traditional banking services include receiving deposits

of money, lending money and processing transactions.

Banks have a long history, and have influenced economies and politics for centuries.

Banking originated in Ancient Mesopotamia where the royal palaces and temples

provided secure places for the safekeeping of grain and other commodities. Receipts came

to be used for transfers not only to the original depositors but also to third parties.

Eventually private houses in Mesopotamia also got involved in these banking operations

and laws regulating them were included in the royal code. The earliest of the banking

services were seen in regions where trade and commerce trade and commerce thrived

including ancient China, Lydia, Phoenicia and Greece. As early as 2000 BC, Babylonian

temples provided loans from their rich treasuries.

The name bank derives from the Italian word banco, desk , used during the Renaissance byFlorentines bankers, who used to make their transactions above a desk covered by a green

tablecloth.

The first bank to provide basic banking functions emerged in Spain in 1401. It was called

the Bank Of Barcelona. Some of the other banks that served as foundations of modern

banking were:

· Bank of Venice (1587)

· Bank of Amsterdam (1609)

· Bank of Hamburg (1619)

5 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 6/83

Although the basic type of services offered by a bank depends upon the type of bank and

the country, services provided usually include:

· Taking deposits from their customers and issuing checking and saving accounts toindividuals and businesses

· Extending loans to individuals and businesses.

· Cashing cheques.

· Facilitating money transactions such as wire transfers and cashiers checks.

· Issuing credit cards, ATM cards and debit cards.

· Storing valuables, particularly in a safe deposit box.

· Cashing and distributing bank rolls

· Consumer & commercial financial advisory services.

· Pension & retirement planning.

6 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 7/83

ESSENTIALS OF M&A

Merger is a combination of two or more companies into one company. In India, mergers are

called as amalgamations, in legal parlance. The acquiring company, (also referred to as the

amalgamated company or the merged company) acquires the assets and liabilities of the

target company (or amalgamating company). Typically, shareholders of the amalgamating

company get shares of the amalgamated company in the exchange for their existing shares in

the target company. Merger may involve absorption or consolidation.

A. Merger and amalgamation: The term merger or amalgamation refers to a

combination of two or more corporate into a single entity. It may involve either;

a) Absorption one bank acquires the

other. Or

b) Consolidation two or more banks combine to form a new entity.

Other way of classifying merger is upon the basis of what type of corporate combine. It can

be of following types-

1. Horizontal merger : A horizontal merger involves a merger between two firms

operating and competing in same kind of business activity. The main purpose of

such mergers is to obtain economies of scale of production. These kind of mergers

result in decrease in the number of firms in an industry and hence such type of

mergers make it easier for the industry members to join together for monopoly

profits. The merger of Centurion bank and Bank of Punjab, Oriental bank of

Commerce and Global trust bank are horizontal mergers in banking sector.

2. Vertical merger : This is the merger of the corporate engaged in various stages of

production in an industry. They are combination of companies that usually have

buyer-seller relationships. A company involved in a vertical merger usually seeks

to expand its operations by backward or forward integration. A vertical merger

(entities with different product profiles) may help in optimal achievement of profit

7 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 8/83

efficiency. Consolidation through vertical merger would facilitate convergence of

commercial banking, insurance and investment banking.

3. Conglomerate merger : A conglomerate merger arises when two or more firms in

different markets producing unrelated goods join together to form a single firm.

The basic purpose of such combinations is utilization of financial resources. Such

type of mergers enhances the overall stability of the acquirer company and creates

balance in the company’s total portfolio of diverse products and production

processes and thereby reduces the risk of instability in the firm’s cash flows.

Conglomerate mergers can be distinguished into three types:

1) Product extension mergers: Mergers between firms in related

business activities and may also be called concentric mergers. Thesemergers broaden the product lines of the firms.

2) Geographic market extension mergers: Mergers between two firms

operating in two different geographic areas.

3) Pure conglomerate mergers: Mergers between two firms with

unrelated business activities. They do not come under product extension

or market extension mergers.

An example of a conglomerate merger is that between an athlete shoe company and a

soft drink company. The firms are not competitors producing similar products (which

would make it a horizontal merger) nor do they have an input-output relation (which

would make it a vertical merger)

B. Acquisition: This may be defined as an act of acquiring effective control by one

corporate over the assets or management of the other corporate without any combination

of both of them. For example recently Oracle, a major software firm has agreed to

acquire a majority stake in Indian banking software company I-flex Solutions. It can be

characterized in terms of the following:

a) The corporate remain independent

b) They have a separate legal entity.

8 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 9/83

C.Take Over: Under the monopolies and restrictive trade practices act, take over

means acquisition of not less than 25% of voting powers in a corporate.

Difference between Acquisition and Take Over:

Although the term acquisition and take over are used interchangeably but in fact, the term

Take over generally shows a hostile act. To put in simple words, when an acquisition is

forced or unwilling act, then it is called take over.

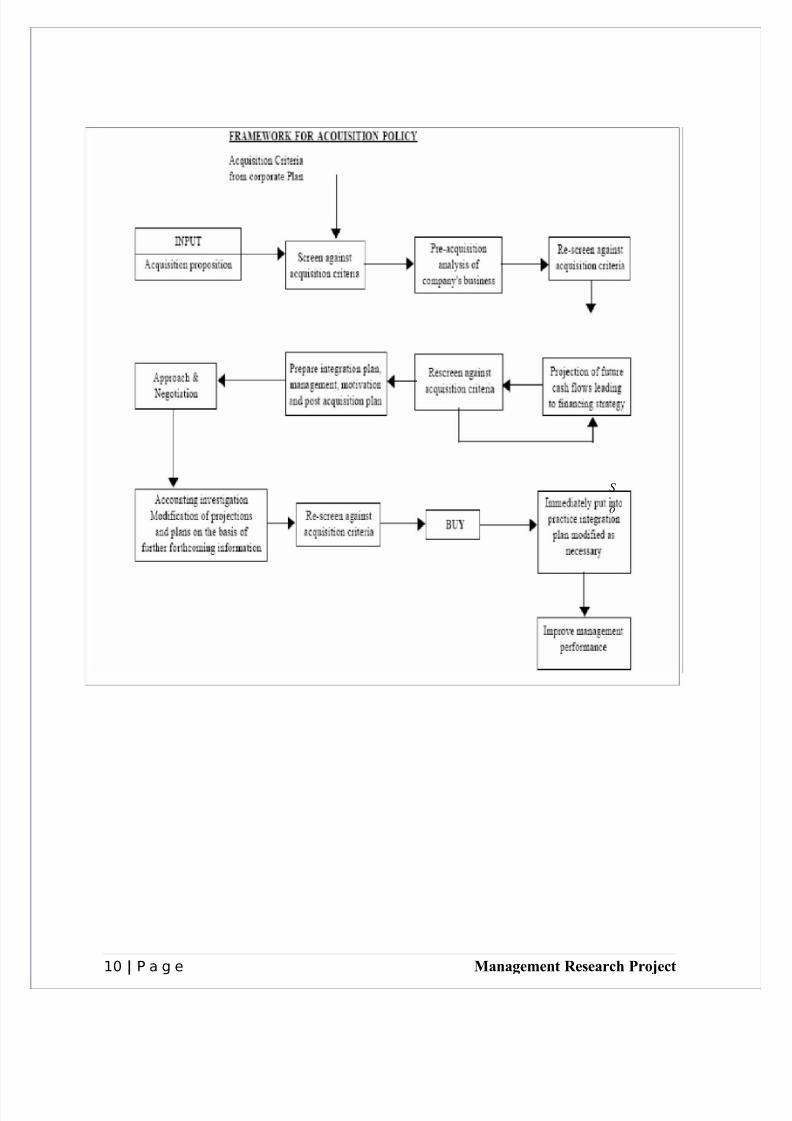

The Merger and Acquisition process:

The acquisition process can be divided into a planning stage and an implementation stage.The planning stage consists of the development of the business and the acquisition plans.

The implementation stage consists of the search, screening, contacting the target,

negotiations, integration and the evaluation activities. In short, the process of acquisition

can be summarized in the following steps:

i. Develop a strategic plan for the business (Business plan)

ii. Develop an acquisition plan related to the strategic plan (Acquisition Plan)

iii. Search companies for acquisitions (Search)

iv. Screen and prioritize potential companies (Screen)

v. Initiate contact with the target. ( first contact)

vi. Refine valuation, structure the deal, perform due diligence, and develop financing plan.

( Negotiation)

vii. Develop plan for integrating the acquired business. (Integration plan)

viii. Obtain all the necessary approvals, resolve post closing issues and implement closing.

(Closing)

ix. Implement post-closing integration (Integration)

x. Conduct the post-closing evaluation of acquisition. (Evaluation)

Figure: 1 Framework for Acquisition Policy

9 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 10/83

S

o

10 | P a g e Management Research Project

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 11/83

M&A IN BANKING - PRESENT TREND

Since more than one decade, the banking industry has been transformed throughout the

world from a highly protected and regulated industry to a competitive and deregulated

one. Especially, globalization coupled with technological development has shrunk the

boundaries by which financial services and products can be provided to the customers

residing at different parts of the world. Further, due to innovations and improvements in

service delivery channels, the trend of global banking has now been marked by twin

phenomena of consolidation and convergence.

The trend towards consolidation has been driven by the need to attain meaningful balance

sheet size and market share in the face of intensified competition, whereas the trendtowards convergence is driven across the industry to provide most of the financial services

such as banking, insurance, investment, cash management etc. to the customers under one

roof. Consolidation has become dominant feature of the banking sector in most countries.

Most large banks in the world have acquired repeatedly and integrated successfully.

· Malaysia has reduced number of banks from 55 to 10

· Taiwan aims to bring down the number of banks from 12 to 6

· Singapore government guided the system down to three players with DBS beingsupported to become a regional leader.

· M&A initiatives are happening in Indonesia, South Korea and Japan.

· European Union experienced M&A activity in banking.

· US mergers count to about 100 since 2000.

Banking system is the bloodline of any economy and banks are trustees of public money.

The depositors therefore, have more stakes in the welfare of banks than the share holders.

Failure of a bank has more systemic implications than say, the failure of a manufacturing

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 12/83

company. Laws governing regulation and supervision of banks in all countries therefore

focus on protecting the interests of depositors. Naturally, fillip to bank consolidation in

many countries came through regulatory and governmental actions in public interest.

Large scale public funding has also taken place in a number of countries to prevent failure

of banks/banking system.

United States witnessed large scale bank failures in the eighties (saving and loan

institutions) and government came to the rescue of banking system through liberal FDIC

(federal deposit insurance corporation) support. An estimated USD 100 billion was sent

on the rescue. In the process the government encouraged mergers among banks by giving

incentives to the banks taking over assets and liabilities of failed banks. Subsequent M&A

activity in the USA in nineties and in recent years have been motivated by market forces.

Europe saw fairly hectic activity too, and would have probably seen even greater M&A

activities had not heterogeneous banking regulation held up cross border mergers. Among

recent deals are the takeover of Abbey National (UK) by Banco Santander (Spain) in

2004, Uni Credito s (Italy) acquisition of Hypo Vereins bank (Germany), ING s

acquisition of Barings, Equitable of IOWA, and earlier, the mergers between Credit

Agricole and Banque Indosuez in France, Dresdner bank with Advance Bank and

Kleinwort Benson Iberfomento of Germany, etc.

Nearer home, we have the Asian experience in bank consolidation post 1997 economic

meltdown. The crisis brought out the vulnerability of a weak banking system to economic

shocks. Here again, the governments had come up with funding support and actively

encouraged consolidation among banks. Let us look at some of the initiatives taken in this

region for strengthening the banking system.

Hong Kong allowed 100% FDI in banking sector and this facilitated take over of several

banks by Singapore and Taiwanese banks.

Indonesia witnessed large scale infusion of public funds into the banking system through

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 13/83

a specialized restructuring agency. Regulatory forbearance was also present in good

measure to facilitate bank recovery. As against Basel Capital adequacy norm of 8%, banks

were allowed to operate with 4% as an interim measure. Only banks which had Capital

Adequacy ratio reduced to below 25% were marked for immediate closure. Consolidation

among banks was actively encouraged and FDI was allowed up to 99%. Net result was

that the number of banks in Indonesia which stood at 239 in 1996 came down to 138 in

2003. Consolidation was most visible among private banks with the number of such banks

coming down from 164 to 76 during the period. Post restructuring, the banks are now

healthier and their branch network and coverage has increased significantly in recent

years.

In Malaysia Bank Negara, the Central Bank implemented a well crafted financial master plan aimed at strengthening the domestic banks, create a level playing field for foreign

banks and open banking sector to global competition. The regulator used suasion to create

10 anchor banks through the consolidation of 22 banks and 39 finance companies. FDI

capped at 30% is expected to be increased in the second phase of reforms scheduled to

commence from later half of 2007.

In Singapore, there are three main banking groups and they have given boost to

consolidation process not only within the country, but also in South Korea and Malaysia.

Thailand has implemented a Financial sector master plan aimed at removing obstructions

to M&A and also allows FDI flow to strengthen the banking system.

Japan is a country which has witnessed a virtual collapse of the banking system along

with economic stagnation which lasted over 15 years. Japan had some of the leading

names in global banking arena. The economic slowdown saw the NPA levels going up

over the roofs and the banks virtually looking for government s support. Needless to say,

the low interest rate regime (near zero rates) would have eased their sufferings somewhat.

However, the banking system has recovered in recent years helped by liberal financial

assistance from the government and an environment of extremely loose monetary policy.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 14/83

Consolidation process which was kicked off as restructuring strategy has resulted in

emergence of three large banks viz. Mitsubishi UFJ, Mizuho and Sumitomo Mitusui.

Today NPA levels have come down to an acceptable level of 2% from a peek level of

8.4% in the year 2002. Capital adequacy ratios have improved above the Basel benchmark

of 8%. Banks have started showing profits and there is a pick-up in their credit portfolio.

Japanese banks may still have a long way to go as their ratings continue to be low and

they are heavily dependant on interest income with heavy reliance on low margin

corporate loans.

Another interesting development taking place in Japan is the government move to

privatize the postal agency, which doubles as a financial institution that holds the world s

largest pool of household savings. The Housing loan Corporation managing the advancesof the postal agency had, at one time, nearly 50% of all mortgage loans in Japan. As part

of privatization this corporation is being wound up with the assets getting transferred to

the banking system. The privatization of the postal agency would see the emergence of a

new bank (named as Yacho Bank) which could probably be one of the largest banking

entities in the world. This process is expected to be completed by 2011.

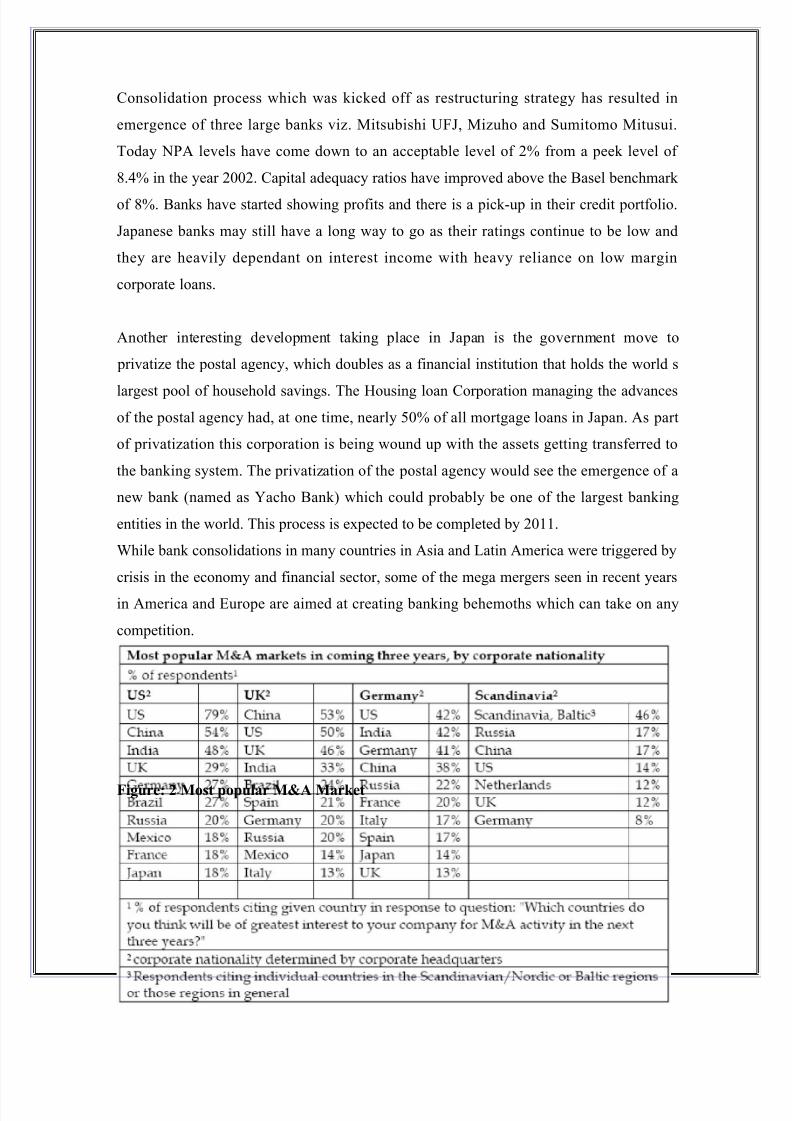

While bank consolidations in many countries in Asia and Latin America were triggered by

crisis in the economy and financial sector, some of the mega mergers seen in recent years

in America and Europe are aimed at creating banking behemoths which can take on any

competition.

Figure: 2 Most popular M&A Market

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 15/83

Source: www.accenture.com

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 16/83

ADVANTAGES OF M&As IN BANKING

A merger involves a marriage of two or more banks. It is generally accepted that

merger promote synergies. The basic idea is that the combined entity will create more

value than the individual banks operating independently. Economist refers to the

phenomenon of the 2+2 =5 effect brought about by synergy.

Various advantages of M&As can be listed as following:

Economies Of Scale: Economies of scale refers to the lower operating costs (per

unit) arising from spreading the fixed costs over a wider scale of production and

economies of scope refers to utilization of skill assets employed in the productionin order to produce similar products or services. The resulting combined entity

gains from operating and financial synergies. In a combined entity, the skill used

to produce separate and limited results will be used to produce results on wider

scale. Additional financial synergies refer to the effect of a merger on the

financial activities of the resulting company. The cash flows arising from the

merger are expected to present opportunities in respect of the cost of financing

and investment.

Economies of Scope: Economies of scope exist when the average cost falls as

more products are produced jointly rather than separately. This happens when the

banks are able to lower their cost by offering several products together as

compared to offering them on an isolated basis.

Greater Efficiency: Banks often are able to operate more effectively by

increasing their size. The costs of many functions don t double when the scale of

operation doubles. As a result, mergers are one way to keep costs and price down.

Leveraging technology: Banks and their customers have become increasingly

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 17/83

accustomed to the advantages of new and expensive technologies. Many of these

technologies are too expensive unless costs can be spread over a large number of

customers. Mergers are often necessary to allow banks to introduce and maintain

the technologies customers increasingly demand.

Managerial efficiency: This may not always be the result of bailout merger or a

hostile takeover. The value addition from the merger comes from a warranted

perception that the acquiring bank s management will be able to run the acquired

bank better even in the case of a bank that is being run well. Typically, apart from

bringing other benefits, such mergers create shareholder value.

Changing /Liberal Laws: Many countries have witnessed change in legalregulations for banking as governments have become more liberal towards this

aspect. In Indian context laws which had prevented many banks from operating in

more than one state recently have been removed or overridden. The advent of

interstate banking and branching means more opportunities for banks operating in

different states to merge with each other.

Diversification: One effective method of controlling risks inherent in bank

lending is to diversify operations across different geographic regions and different

types of customers. Mergers can help diversify such risks.

Broader arrays of products: Mergers may give banking institutions an

opportunity to offer a broader array of services. A merger of two banks with

different expertise can result in a combination more to the liking of customers

looking for one stop shopping.

Cost reduction: Consolidation helps in scaling up operations, thereby reducing

per unit cost. Cost is also reduced through economy of scope as synergy involved

in consolidation is able to offer multiple products using the same infrastructure.

Cheaper sourcing of inputs with increasing bargaining power with vendors and

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 18/83

suppliers also reduces cost.

Improved market reach and Industry visibility: Ability to enter new business

areas with reduced initial cost as compared to a new set is another benefit of

consolidation.

Reduce Competition: Through mergers and acquisitions many big companies

combine with their immediate rivals and hence reduce competition. Also with

more and more consolidations the number of players operating in open market is

reduced and hence there is reduction in competing players.

Increase Revenue: A bigger entity will be able to serve a large customer better.By offering more services and taking bigger share in the business of the customer

the bank will be able to increase the revenue per customer. A larger customer

base will generate more revenue. A bigger size and share in the market will boost

the bank s ability to raise product prices without losing customers.

Asset Building and increase size: Consolidations help in increase in Asset base

as against a new setup. Banks experience increase in number of branches,

manpower, services offered etc. when they merge with some other banks. A bank

having strong hold in particular region can increase its base by acquiring bank in

totally unexplored region.

Risk Diversification: With increase in size the merged entity can take bigger

risks and reap its reward. Risk is diversified after merger as against experienced

by single entity.

Financial Sustainability: After a merger, the strong cash flow generated can be

channeled towards meeting the cash requirements of some potential ventures that

companies are planning to take up. Consolidations can increase financial

sustainability to great extent.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 19/83

Tax Savings: Mergers are likely to bring in the tax cover by way of depreciation

on merging entity’s assets. If in a bailout merger, the distressed bank has

accumulated losses and unclaimed depreciation benefits on its books, it could eliminate

an acquirer’s liability on account of tax benefits that accrue to the latter.

Stabilization of asset quality for smaller banks: Size, a large capital base, well

rated borrowers and the ability to cater to their diverse product and service needs

through a single window are the strengths that can be acquired through a merger

and the resultant increase in size, and will lead to a sharp improvement in the

asset quality of smaller banks.

Acquiring size through the less cumbersome inorganic route to meet

competition: this decision can sometimes be impulsive, so, ideally, it needs to be

based on a concrete strategy.

Augmentation of capital base, mainly regulatory capital: Given the stringency

of Basel II regulatory capital norm compliance, this will be a major galvanizing

factor in bank consolidation.

Less cumbersome bank supervision: The RBI will find both offsite as well as

onsite supervision less cumbersome in a scenario of a few large banks. Guidelines

can be more effectively implemented.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 20/83

FACTORS FOR M&As SUCCESS

For mergers to be successful, following issues need to be given due importance:

Recovery of Bad loans

In any banking consolidation, one of the important aspects looked after at is the amount of

bad debts or the non-performing assets that has shifted hands. This definitely has an

impact on the performance of the companies. Post merger, it is imperative that this item of

the banks is recovered as much as possible which was desired by the acquiring company

at the time of going for the merger.

IT Implication

Technology increasingly lies at the heart of a modern bank and it is a critical issue that canmake or break a merger. Therefore, it is important to carefully consider prior to the merger

whether the technology platforms are similar or at least capable of talking to each other,

what the overlapping technology costs are and what are the costs of process integration.

The biggest challenge is whether the existing infrastructure of the acquiring bank can

scale up to the degree envisaged over a span of two to three years. Recently we have seen

the merger between GTB and OBC, in that merger IT implication played an important

role, because both the banks enjoyed the same platform.

With changing times technology has become so important in a merger that banks have

proved that instead of technology being an issue in merger; it can be the causal factor in a

merger. There are cases where technology merger has lead to a complete merger. Once all

the banks have the same technology, and processes, merger is just a formality.

Human Resource Issue

All over the world it is observed that after merger, very high number of employees loses

their jobs. Same theory is applicable to the Indian Banking also. It is important to sort out

this issue before merger. Human resources are another sensitive issue on the road to

consolidation.

As per a study of the Indian banking Industry by FICCI in October 2005, 88% of public

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 21/83

and private sector banks considered HRD related issues as one of the biggest challenge in

the process of consolidation.

For merger to succeed banks will have to carefully forge a cultural fit among all

employees, ingeniously devise HRD policies and concentrate not only on cost reduction

but also on enhancing revenue and profitability.

Cultural Shift

Before a merger is carried out, cultural issues should be looked into. A bank based

primarily out of North India might want to acquire a bank based primarily out of South

India to increase its geographical presence, but their cultures might be very different. So,

the integration process might become difficult. Even if there are synergies in technology,geographical presence and profile of assets, the birth of mega banks through mergers may

not be of great use unless the mindset of public sector banks changes.

A number of studies have measured the success of banking merger in terms of three

important parameters.

· Profitability

· Cost Efficiency

·

Market Power The success of a merger hinges on how well the post-merged entity positions itself to

achieve cost and profit efficiencies. It is difficult to rely on measures of economies and

diseconomies of scale in banking, whereas cost and profit efficiencies are far more reliable

and measurable indicators and create value.

Mergers elsewhere in the world have helped reduce operating expenses by 0.5 percent

(percent to total assets). That would translate into a few thousand crores of rupees for

Indian PSU banks.

One other way of measuring the success of the merger can be seen from analyzing the post

merger performance to the stated goals before the merger. This way, one can see whether

the banks were able to attain their stated objectives, which are important to realize the full

synergies of the merger.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 22/83

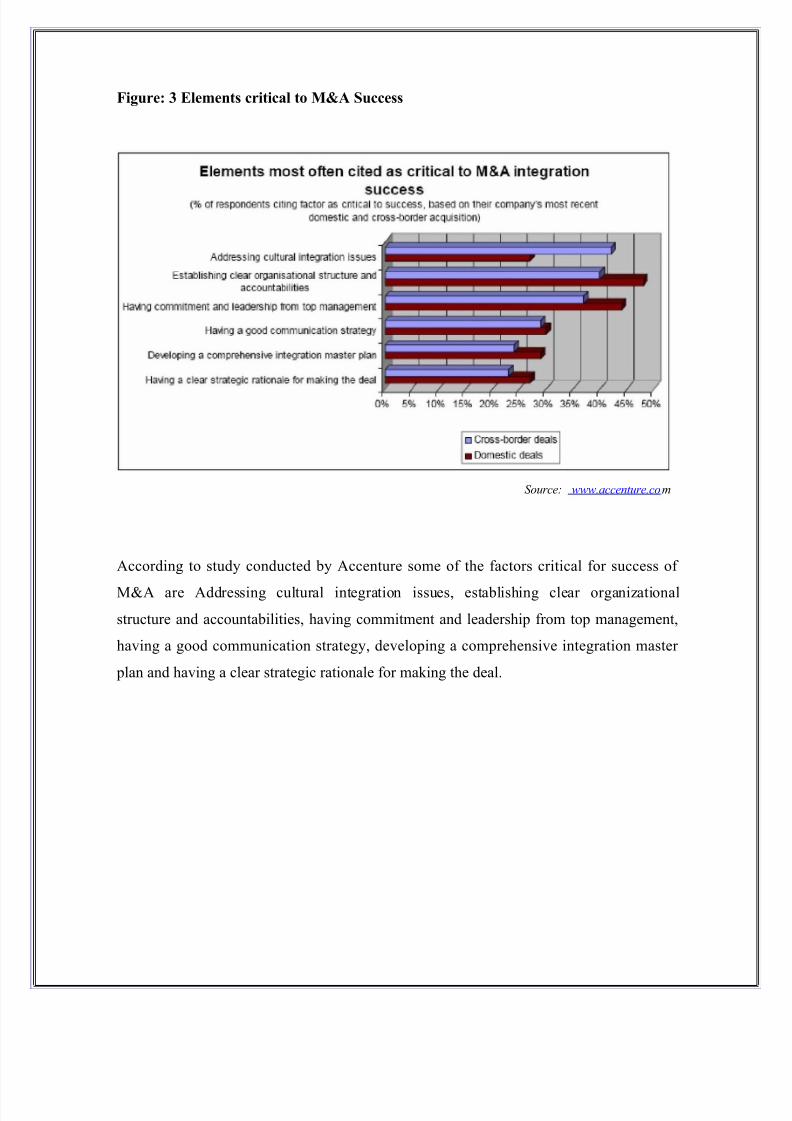

Figure: 3 Elements critical to M&A Success

Source: www.accenture.com

According to study conducted by Accenture some of the factors critical for success of

M&A are Addressing cultural integration issues, establishing clear organizationalstructure and accountabilities, having commitment and leadership from top management,

having a good communication strategy, developing a comprehensive integration master

plan and having a clear strategic rationale for making the deal.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 23/83

RISKS ASSOCIATED WITH MERGERS

Risk and return always go hand in hand, this is also true for the merger in the banks.

These are the few risks associated with the merger.

· When two banks merge into one then there is an inevitable increase in the size of

the organization. Big size may not always be better. The size may get too widely

and go beyond the control of the management. The increased size may become a

liability rather than an asset.

· Consolidation does not lead to instant results and there is an incubation period

before the results arrive. Mergers and acquisitions are sometimes followed by

losses and tough intervening periods before the eventful profits pour in. Patience,

forbearance and resilience are required in ample measure to make any merger a

success story. All may not be up to plan, which explains why there are high rate of

failure in mergers.

· Consolidation mainly comes due to decision taken at the top. It is a top heavy

decision and willingness of the rank and file of the both entities may not beforthcoming. This leads to problems of industrial relations, deprivation.

Depression and de-motivation among the employees. Such a work force can never

churn out good results. Therefore, personal management at the highest order with

humane touch alone can pave the way.

· The structure, systems and the procedures followed in two banks may be vastly

different, for example, a PSU bank or old generation bank and that of a

technologically superior foreign bank. The erstwhile structures, systems and

procedures may not be conductive in the new milieu. A through overhauling and

systems analysis to be done to assimilate both the organizations. This is a time

consuming process and requires lot of cautions approaches to reduce the frictions.

There is problem of valuations associated with all mergers. The shareholder of

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 24/83

existing entities has to be given for transfer and compensations is yet to emerge.

· Further, there is also problem of brand projection. This becomes more

complicated when existing brands themselves have a good appeal. Questions arise

whether the earlier brands should continue to be projected or should they by

submerged in favor of a new comprehensive identity. Goodwill is often towards a

brand and its sub merger id usually not taken kindly.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 25/83

BANKING STRUCTURE IN INDIA

India has an extensive banking network, in both urban and rural areas. All large Indian

banks are nationalized, and all Indian financial institutions are in the public sector. The

Reserve Bank of India is the central banking institution. It is the sole authority for issuing

bank notes and the supervisory body for banking operations in India. It supervises and

administers exchange control and banking regulations, and administers the government s

monetary policy. It is also responsible for granting licenses for new bank branches. 36

foreign banks operate in India with full banking licenses.

Indian banking System

Indian banking system has three tiers. These are the scheduled commercial banks, theregional rural banks which operate in rural areas not covered by the scheduled banks, and

the cooperative and special purpose rural banks.

Commercial banks are categorized as scheduled and non-scheduled banks, but for the

purpose of assessment of performance of banks, the Reserve Bank Of India categories

them as public sector banks, old private sector banks, new private sector banks and foreign

banks.

Scheduled and non Scheduled Banks

There are 93 scheduled commercial banks, Indian and foreign; 196 regional rural banks.

In cooperative sector nearly 2000 cooperative banks operate, which include non scheduled

banks. In terms of business, the public sector banks, namely the State Bank Of India and

the nationalized banks, dominate the banking sector.

Scheduled Commercial Banks (SCB s) in India are categorized in five different groups

according to their ownership and/or nature of operation. These bank groups are: (i) State

Bank Of India and its associates, (ii) Nationalized Banks, (iii) Regional Rural Banks, (iv)

Foreign banks and (v) Other Indian Scheduled Commercial Banks (in the private sector).

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 26/83

Regional Spread of Banking

The total number of branches of SCB s as at end-June 2004 stood at 67,097 comprising

32,207 rural branches, 15,028 semi urban branches and 19,837 urban and metropolitan

branches. In line with the regional distribution of income, the Southern region accounted

for the highest percentage of bank branches, followed by Eastern region, Northern Region,

Western Region and North-Eastern region.

The State Bank and its seven associates have about 14,000 branches; 19 nationalized

banks have 34,000 branches; the RRBs 14,700 branches; and foreign banks around 225

branches. If one includes the branch network of old and new private banks, collectively

the spread could be over 68,000 branches across the country. Besides, there are a few

thousand cooperative bank branches. On an average, one bank branch caters to 15,000 people.

India is the 4th largest economy in terms of the purchasing price parity and 10th place in

terms of the GDP. Indian economy is registering consistent 7 and above percent annual

growth for last 5 years. However, only one bank-State Bank of India-is among the top 200

banks in the world.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 27/83

MERGERS & ACQUISITION IN INDIAN BANKING

History

Mergers and Acquisitions are not an unknown phenomenon in Indian Banking. In fact, it

dates back in 1921, when Bank of Bengal (Bank of Calcutta) and two other banks (Bank

of Madras and Bank of Bombay) were amalgamated to form the Imperial Bank of India.

In 1955, the controlling interests of the Imperial Bank of India were acquired by the RBI,

and the State Bank of India was created by an Act of Parliament to succeed the Imperial

bank of India.

Indian Banking sector has been active in Merger & Acquisitions ever since Section 45 wasincorporated in the Banking Companies Act in 1960. This section empowered the RBI to

initiate the process of amalgamation of weak banks with strong ones at times when the net

realizable assets of a bank fell below 90 percent of its deposits, but with the approval of

the government. This was aimed at averting bank failures which were rampant in India as

they were in other countries in those days. The M&A wave in India dates back to 1961,

when as many as 30 sick banks were merged with well performing ones. As of today, 34

banks bailout mergers have taken place over the past 46 years, but take off on the new

generation mergers on the lines recommended by the Narsimham Committee has been

incredibly slow.

In recent times we have seen few M&As as voluntary efforts of banks. Merger of Times

bank with HDFC bank was the first of such consolidations after financial sector reforms

ushered in 1991. Merger of Bank of Madura with ICICI bank, reverse merger of ICICI

with ICICI bank, coming together of Centurion bank and Bank of Punjab to form

Centurion Bank of Punjab and the recent decision of Lord Krishna bank to merge with

Federal Bank are voluntary efforts by banks to consolidate and grow.

Consolidation fever has not been confined to the Scheduled Commercial Banks.

Consolidation process gained strength in other sectors as well. There were about 196

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 28/83

RRBs in 1989. The last year and a half saw their numbers dwindle to 103 with mergers of

RRBs sponsored by commercial banks within the same state. This move is expected to

bring most of RRBs into profit making entities capable of playing their role in the way

they were expected to do when the RRB Act was passed in 1996.

There were over 2000 Urban Co-operative Banks in the country and failure of a number of

these banks in the last few years is a matter of great concern. These banks have begun to

see the benefits of consolidation. RBI has reported receiving 17 proposals for mergers of

UCBs in past one year.

Current Scenario

Till almost the mid -1990s, M&A have not been common in most developing countriesincluding India. This was in part due to the fact that the State had been playing a dominant

role in these countries in promoting and developing economic activities, both as a

producer and a regulator. This indeed was the case in India right from the 1950 s to mid-

1991 when economic policy regime was shifted rather dramatically towards market

orientation and an incentive system. Liberalization of Indian economy in 1992 changed

the way of carrying out businesses in India. The shift in the case of the financial sector

regime took place in an effective sense only from 1992-1993 after the publication of the

report in 1992 on the reforms of the financial system chaired by M Narsimham. The need

for M&A as a strategic tool in the context of the Indian banking Industry was highlighted

by the Committee on the Financial System (Narasimham 1) in 1991, which recommended

a possible structure, towards which the banking system could evolve with 3 to 4 large

banks (including SBI) having an international presence and 8 to 10 national banks with a

network of branches throughout the country engaged in general or universal banking,

among others. In the series of reforms the Committee on banking sector reforms

(Narasimham II) in 1998 highlighted the importance of bank mergers. The committee

made certain recommendations regarding mergers between banks including public sector

banks, as well as mergers between banks and non banks. So bank mergers are in process

and they have to cover a long road ahead.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 29/83

While India has made rapid progress in other spheres of financial sector reforms, it has

made slow progress as far as bank consolidation is concerned. In India Public sector banks

form nearly 75% of Indian banking and there has been no substantial merger in this

banking sector. Mergers among banks have not taken off on a large scale in India, inspite

of the imperatives of Basel II compliance, the imminent threat of competition from foreign

banks looming up and the successive merger waves in the global banking sector.

Basel II Norms

Right now, there is a feverish activity going on in top management levels of banks and

uppermost on every mind is as small town called Basel in Switzerland. Small it may be,

but prudential norms for regulatory capital and some other areas of banking operations setthere by the Bank for International Settlements (BIS) form the ground rules that all banks

worldwide follow. The second tranche of Basel rules, which have already become

operational in many countries, has come into force in India with affect from April 1, 2007.

This time around, the rules are going to be more fine tuned, distinguishing between

various types of corporate lending risks. To that extent, the regulatory capital that has to

be kept aside for lending will no longer be uniformly 9% as before, that is, banks will no

longer keep aside Rs.9 for every 100 of risk assets. In 1988, Basel I did not discriminate

between various risks. From 2007 onwards, banks will have to set aside capital according

to the rated risk profile of each corporate borrower. This will mean a more efficient use of

capital, on one hand, but on other hand it would demand higher capital adequacy level

from the more the more aggressive lenders. It has been estimated that banks in India might

have to hike up their regulatory capital by as much as two third to meet Basel norms.

Banks today face operational risks such as competition risk, technological risk, casualty

risk, interest rate risk, market risk etc. While the 1988 Basel I rules did not take these risks

into account, Basel II stipulates that banks set aside 15% of their net income towards

coverage for operational risks.

RBI /GOI Stand On M&A in Banking in India

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 30/83

In India, the mood in the Ministry of Finance and the Reserve Bank of India is by no

means relaxed as far as the issue of bank consolidations is concerned. Government of

India and more specifically Reserve bank of India, prime regulator for banks in India has

catered to need of general public as and when required. Since independence and even

before that there have been transitions in Indian banking. In first phase of transition in

Indian Banking State Bank of India was formed in July 1955 followed by the takeover of

the strongest private bank that existed then viz., the Imperial Bank of India, by the

Reserve Bank of India. In second stage of transition there was takeover of seven princely

state banks by State Bank of India in the year 1959 in order to expand its rural outreach. In

third phase Indira Gandhi government nationalized 14 major Indian Commercial Banks on

19th July, 1969. This was followed by nationalization of six more commercial banks in

1980. GOI liberal policy in 1992 bought many changes in Indian Banking. Private players

were encouraged to participate actively in this sector. Mergers were still an efficient tool

in hand of government to save depositors of weak dying banks. Narhsimham committees

of 1992 and 1998 also encouraged mergers and acquisitions in banking. Now government

is also encouraging voluntary mergers. Basel I and Basel II norms are adhered to and after

April 2009 government of India s stand for foreign banks will also be liberalized. After

2009 Indian banks will face fierce competition from foreign banks as there operations inIndia will be easy as compared to present conditions.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 31/83

CHALLENGES FOR BANK MERGERS IN INDIA

Bank mergers in India are not as easy as it seems on the paper. No doubt everyone knows

the criticality of the issue and urgent requirement of mergers in Indian Banking sector. But

then river also have to face various rocks, pebbles and other interruptions in its natural

flow and so does Indian Banking sector has to face various challenges for mergers in

India. Various challenges like:

· Loss of corporate focus through too much size.

· Employee downsizing

· Difficulties of HR integration

· Erosion of healthy competition through concentration of a single bank/a group of banks.

· Challenges of technological integration.

· Culture mismatch.

· Erosion of shareholder value in the absence of proper planning.

· Scams and scandals in the absence of proper co-ordination between regulators(RBI and SEBI in India)

· Customer dissatisfaction, arising out of a change in the nature and quality of products. This happens even if services and products are improved.

· Small borrowers and customers often get marginalized.

· Disruptions in established banking relationships, resulting in attrition of loyalcustomers.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 32/83

PRE AND POST PERFORMANCE EVALUATION OF M&As IN

INDIAN BANKING INDUSTRY

The banking industry is an important area in which mergers and acquisitions do make

enormous financial gains. The traditional corporate customers of a banker turn away

increasingly from traditional loan. They are in favor of alternative sources of financial

instruments like commercial papers etc., As a result of changes in the expectation of the

corporate customers, banks are now constrained to rethink their business and devise new

strategies. On the other hand, competitors both from India and abroad are encroaching

upon every area of business. Therefore, Indian bankers have to struggle to survive in a

competitive environment. In the changed environment, bankers adopt different strategies.

They have no other option except to reduce their costs (both operational costs and the cost

of credit). The only way to manage competitiveness is cost reduction through acquisition,

which enables the bankers to spread its overhead cost over a large customer base. From

the current trends, one can safely predict that consolidation will also be one of the

effective strategies widely adopted by the bankers.

It is common knowledge that dramatic events like mergers, takeovers and restructuring of

corporate sectors occupy the pages of business newspapers almost daily. Further they have

become the focus of public and corporate policy issues. This is an area of potential goodand harm in corporate strategy including banking industry.

Hence it is imperative to evaluate these mergers and acquisitions. This study attempts to

assess the successfulness of Mergers and Acquisitions strategy in Indian banking industry

post liberalization. It analyses the implications of takeovers from the financial point of

view.

OBJECTIVES OF THE STUDY

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 33/83

The main objective of this study is to analyze and compare the following performance of

merged banks before and after merger with special reference to financial performance.

1. Economic parameters.

2. Financial impact.

3. Cross cultural effects.

4. Operational parameters.

5. Human Resource perspective.

6. Advancement of Information Technology and its impact.

METHODOLOGY OF THE STUDY

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 34/83

1. Study of parameters like financial/economic aspects would be more or less

secondary data analysis. It would involve pre and post analysis of financial

parameters like CAGR etc.

2. Attempt will be made to analyze profitability, total income, efficiency of branch,

deposit mobilization efficiency, working fund, performance variables, share

holding pattern etc.

3. Analysis of Operational aspects and IT transition post merger to enable unification

of various IT platform.

4. Primary Data study of HR aspects like employee motivation and issues like unionsetc.

The study is intended to examine the performance of merged banks in terms of its growth

of total assets, profits, revenue, investment and deposits, advances, capital adequacy ratio,

number of employees, business per employee, profit per employee, no. of branches and

net non performing assets.

The performance of merged banks is compared taking four years of pre merger and four years of post-merger as the time frame. The year of merger uniformly included in the post-

merger period of all sample banks. A random sample of twelve banking units (The list is

given in Table-V) was drawn from the list of about 25 banking units (Table-IV), which

have undergone mergers and acquisitions post liberalization. (The list of merged banks in

India is given in Table-II). A sample of about 50% of merged banks (12) from total

merged bank. (25) was drawn. While drawing the sample banks for this study the

availability of financial data such as financial statement, history of the companies etc. was

taken into account.

Data Collection of the Study

The present study mainly depends on the secondary data. The secondary data for financial

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 35/83

analysis were collected for four years before and four years after the merger. The required

data were obtained from the Prowess Corporate Database Software of CMIE.

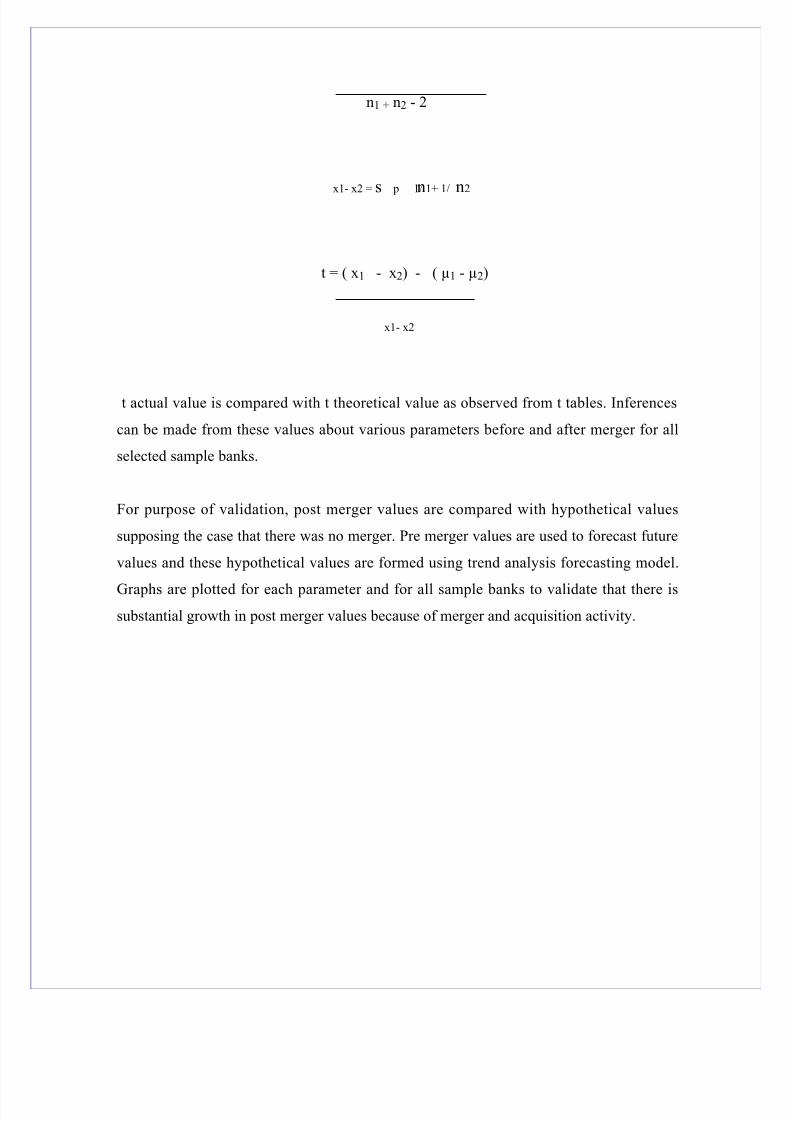

Tools used for Analysis

As stated earlier, this study has analyzed the growth of total assets, profits, revenue,

investment, deposits, advances, capital adequacy ratio, number of employees, number of

branches, business per employee, profit per employee and net non performing assets at

end of year of merged banks before and after the merger. In order to evaluate the

performance, the statistical tools like mean ,standard deviation and t-test have been used.

The statistical tool used is t- test to test difference in means of small samples. The growth

rates of sample banks for all variables (mean values of variable before and after merger)have been analyzed.

For the purpose of study null hypothesis is that there is no substantial difference in mean

value of all stated parameters before merger and after merger. And alternate hypothesis is

that there is substantial difference in mean values before merger and after merger. i.e.

mean values after merger have increased substantially from mean values before merger.

Let, Mean value before merger be X1

Mean value after merger be X2

Ho: X1 = X2 Null Hypothesis: There is no difference in mean value before and after merger.

H1: X1< X2 Alternate Hypothesis: mean value after mergers is higher than mean values before

merger

Level of significance 0.05

s p2 = ( n1- 1) s1

2 + (n2 -1) s22

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 36/83

n1 + n2 - 2

x1- x2 = s p 1/n1+ 1/ n2

t = ( x1 - x2) - ( µ1 - µ2)

x1- x2

t actual value is compared with t theoretical value as observed from t tables. Inferences

can be made from these values about various parameters before and after merger for all

selected sample banks.

For purpose of validation, post merger values are compared with hypothetical values

supposing the case that there was no merger. Pre merger values are used to forecast future

values and these hypothetical values are formed using trend analysis forecasting model.

Graphs are plotted for each parameter and for all sample banks to validate that there issubstantial growth in post merger values because of merger and acquisition activity.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 37/83

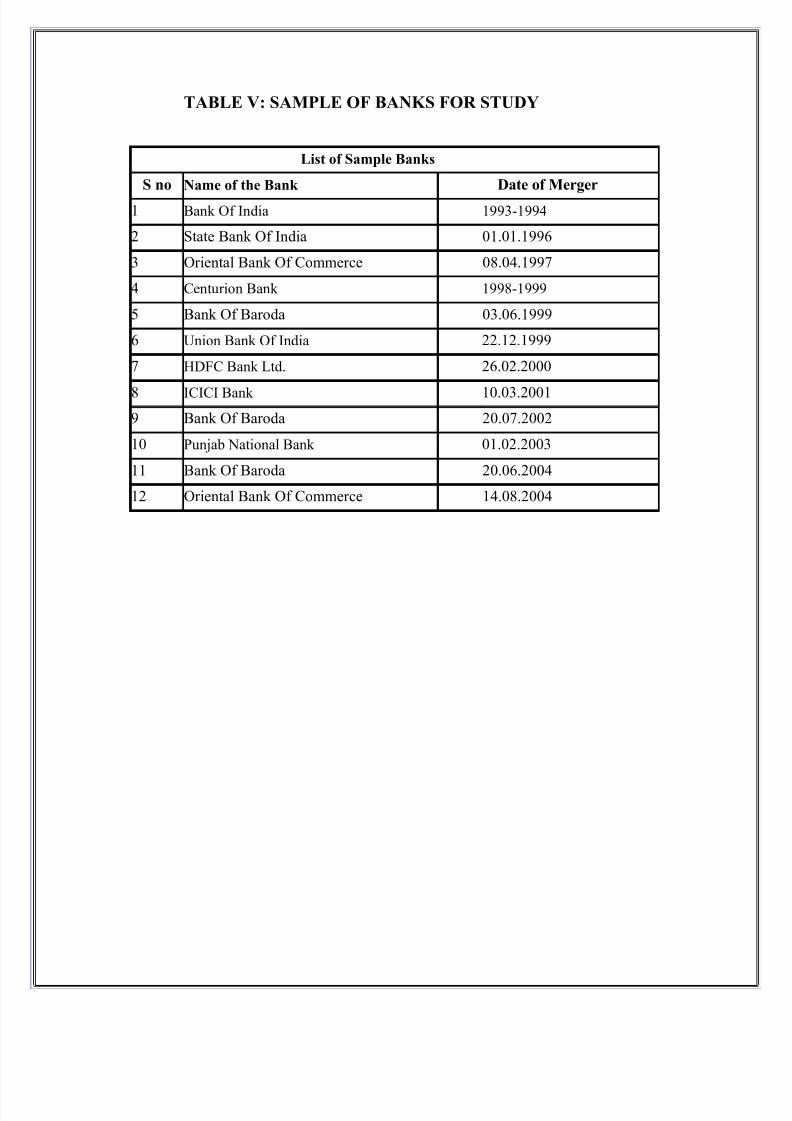

TABLE V: SAMPLE OF BANKS FOR STUDY

List of Sample Banks

S no Name of the Bank Date of Merger

1 Bank Of India 1993-1994

2 State Bank Of India 01.01.1996

3 Oriental Bank Of Commerce 08.04.1997

4 Centurion Bank 1998-1999

5 Bank Of Baroda 03.06.1999

6 Union Bank Of India 22.12.1999

7 HDFC Bank Ltd. 26.02.2000

8 ICICI Bank 10.03.20019 Bank Of Baroda 20.07.2002

10 Punjab National Bank 01.02.2003

11 Bank Of Baroda 20.06.2004

12 Oriental Bank Of Commerce 14.08.2004

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 38/83

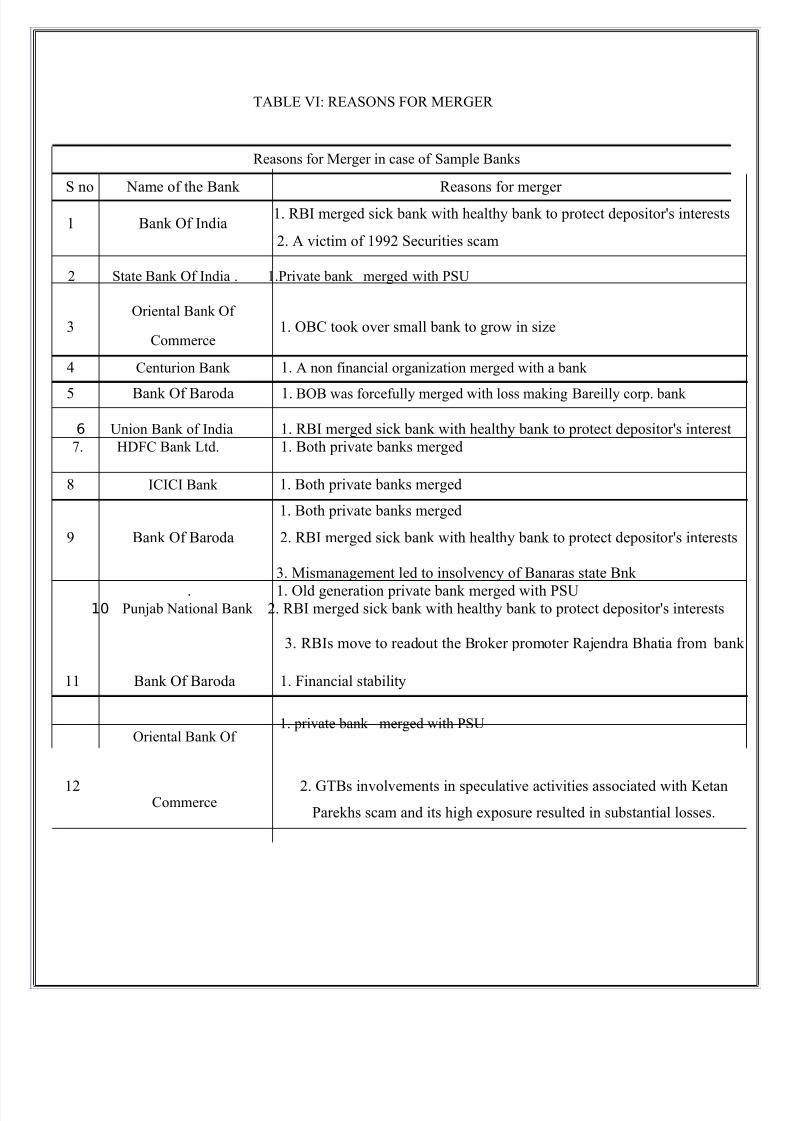

TABLE VI: REASONS FOR MERGER

Reasons for Merger in case of Sample Banks

S no Name of the Bank Reasons for merger

1 Bank Of India1. RBI merged sick bank with healthy bank to protect depositor's interests

2. A victim of 1992 Securities scam

2 State Bank Of India . 1.Private bank merged with PSU

3Oriental Bank Of

1. OBC took over small bank to grow in sizeCommerce

4 Centurion Bank 1. A non financial organization merged with a bank

5 Bank Of Baroda 1. BOB was forcefully merged with loss making Bareilly corp. bank

6 Union Bank of India 1. RBI merged sick bank with healthy bank to protect depositor's interest7. HDFC Bank Ltd. 1. Both private banks merged

8 ICICI Bank 1. Both private banks merged

1. Both private banks merged

9 Bank Of Baroda 2. RBI merged sick bank with healthy bank to protect depositor's interests

3. Mismanagement led to insolvency of Banaras state Bnk

. 1. Old generation private bank merged with PSU10 Punjab National Bank 2. RBI merged sick bank with healthy bank to protect depositor's interests

3. RBIs move to readout the Broker promoter Rajendra Bhatia from bank

11 Bank Of Baroda 1. Financial stability

Oriental Bank Of 1. private bank merged with PSU

12 2. GTBs involvements in speculative activities associated with KetanCommerceParekhs scam and its high exposure resulted in substantial losses.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 39/83

ANALYSIS OF THE STUDY

For the purpose of this study analysis was made in terms of the following variables:

(a) Changes in Growth of Total Assets of Merged Banks,

(b) Changes in Growth of Profits of Merged Banks,

(c) Changes in Growth of Revenue of Merged Banks.

(d) Changes in Growth of Investment of Merged Banks

(e) Changes in Growth of Deposits of Merged Banks.

(f) Changes in Growth of Advances of Merged Banks.

(g) Changes in Growth of CAR of Merged Banks.

(h) Changes in Growth of Number of Employees of Merged Banks.

(i) Changes in Growth of Number of Branches of Merged Banks.

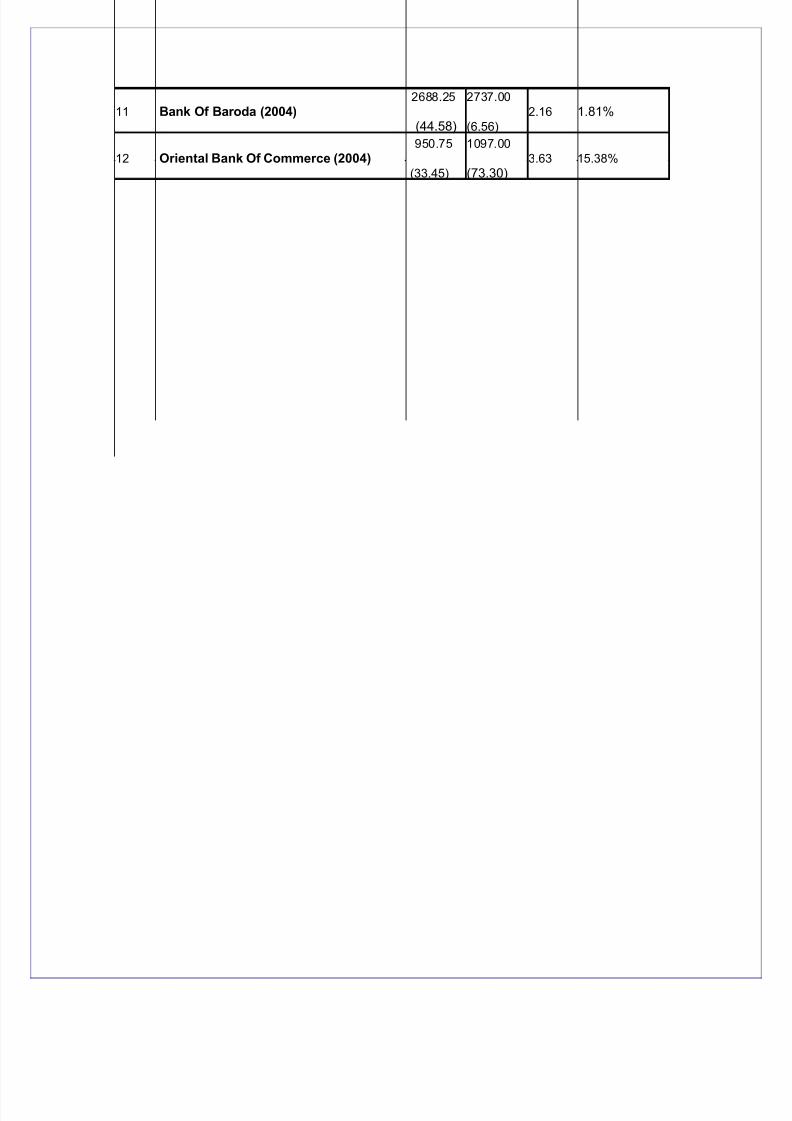

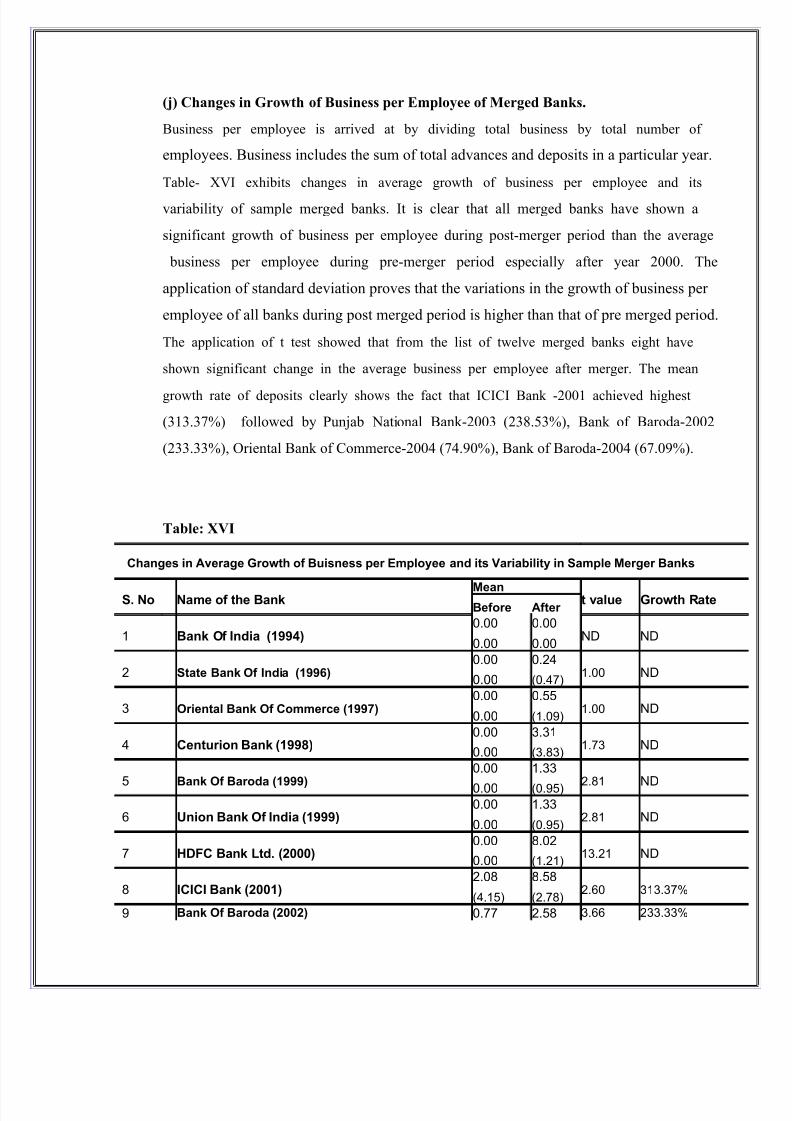

(j) Changes in Growth of Business per Employee of Merged Banks.

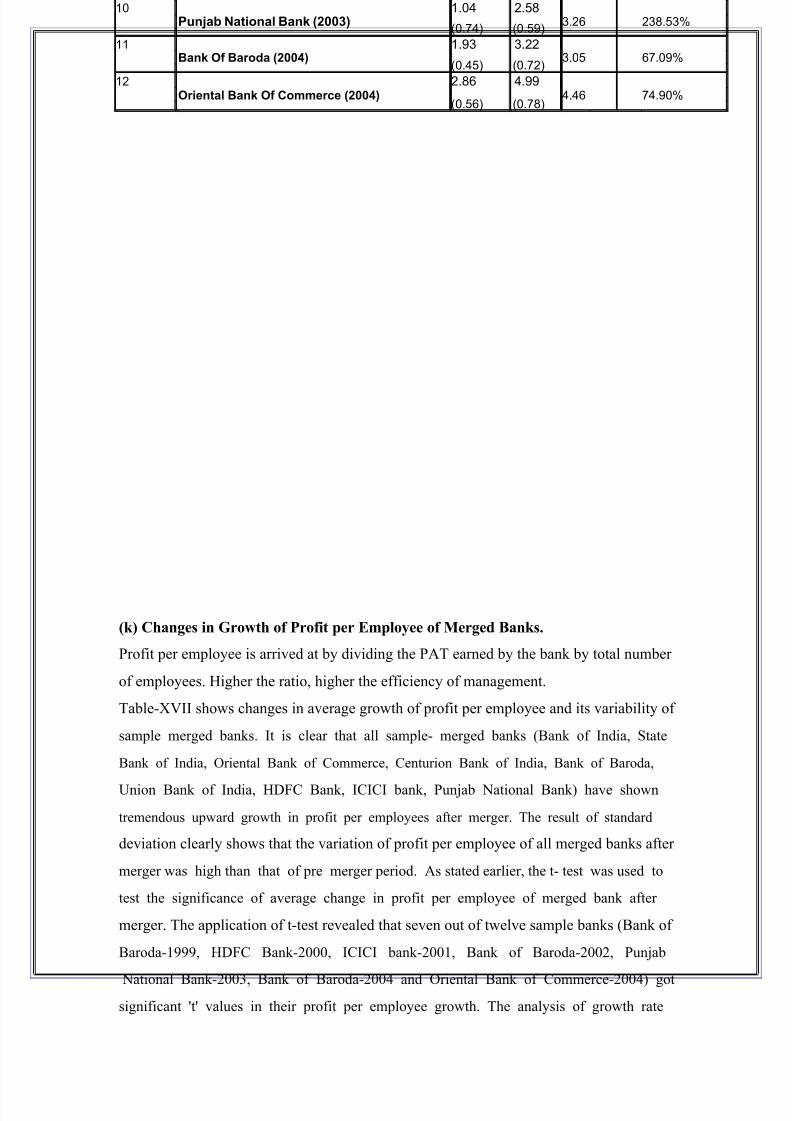

(k) Changes in Growth of Profit per Employee of Merged Banks.

(l) Changes in Growth of Net non performing Assets at end of year of Merged banks.

(a) Changes in Growth of Total Assets of Merged Banks

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 40/83

Assets represent economic resources that are the valuable possessions owned by a firm.

Assets are mainly used to generate earnings. The total assets refer to net fixed assets and

current assets. The growth of total assets indicates firm's ability to produce large volume of

sales and to earn larger revenue. One aim of business strategy namely, merger and

acquisition is the maximization of total assets of merged banks i.e., firms' ability to

produce large volume of sales. It is expected that the bank units after merger would

function efficiently.

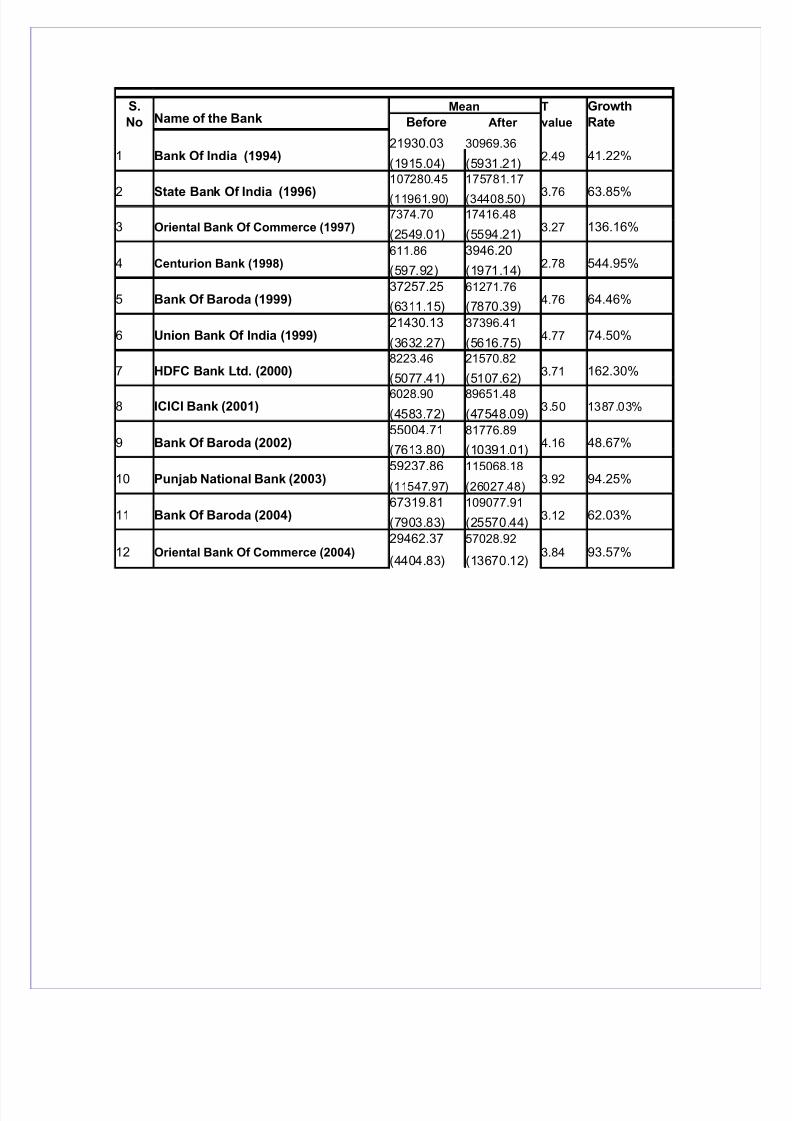

Table-VII shows changes in average total assets and its variability of sample merged

banks. It is clear that all sample- merged banks (Bank of India, State Bank of India,

Oriental Bank of Commerce, Centurion Bank of India, Bank of Baroda, Union Bank of India, HDFC Bank, ICICI bank, Punjab National Bank) have shown tremendous upward

growth in total assets after merger. The result of standard deviation clearly shows that the

variation of assets of all merged banks after merger was high than that of pre merger

period. As stated earlier, the t- test was used to test the significance of average change in

total assets of merged bank after merger. The application of t-test revealed that all

merged banks (Bank of India, State Bank of India, Oriental Bank of Commerce,

Centurion Bank of India, Bank of Baroda, Union Bank of India, HDFC Bank, ICICI

bank, Punjab National Bank) got significant 't' values in their assets growth. The analysis

of growth rate (mean value) of total assets of sample banks clearly showed that ICICI

Bank -2001 achieved high rate of growth (1387.03%), followed by Centurion Bank -

1998 (544.95%), HDFC Bank-2000 (162.30%), Oriental Bank of Commerce-1997

(136.16%), Punjab National Bank-2003 (94.25%), Oriental Bank of Commerce-2004

(93.57%), Union Bank of India-1999 (74.50%), Bank of Baroda-1999 (64.46%), State

Bank of India-1996 (63.85%), Bank of Baroda-2004 (62.03%), Bank of Baroda-2002

(48.67%), Bank of India- 1994 (41.22%).

Table: VII

Changes in Average Growth of Total Assets and its Variability in Sample Merger Banks

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 41/83

S.Name of the Bank

Mean T Growth

No Before After value Rate

1 Bank Of India (1994)30969.36

2.49 41.22%21930.03

(1915.04) (5931.21)

2 State Bank Of India (1996)

107280.45 175781.17

3.76 63.85%(11961.90) (34408.50)

3 Oriental Bank Of Commerce (1997)7374.70 17416.48

3.27 136.16%(2549.01) (5594.21)

4 Centurion Bank (1998)611.86 3946.20

2.78 544.95%(597.92) (1971.14)

5 Bank Of Baroda (1999)37257.25 61271.76

4.76 64.46%(6311.15) (7870.39)

6 Union Bank Of India (1999)21430.13 37396.41

4.77 74.50%(3632.27) (5616.75)

7 HDFC Bank Ltd. (2000)8223.46 21570.82

3.71 162.30%(5077.41) (5107.62)

8 ICICI Bank (2001)6028.90 89651.48

3.50 1387.03%(4583.72) (47548.09)

9 Bank Of Baroda (2002)55004.71 81776.89

4.16 48.67%(7613.80) (10391.01)

10 Punjab National Bank (2003)59237.86 115068.18

3.92 94.25%(11547.97) (26027.48)

11 Bank Of Baroda (2004)67319.81 109077.91

3.12 62.03%(7903.83) (25570.44)

12 Oriental Bank Of Commerce (2004)29462.37 57028.92

3.84 93.57%(4404.83) (13670.12)

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 42/83

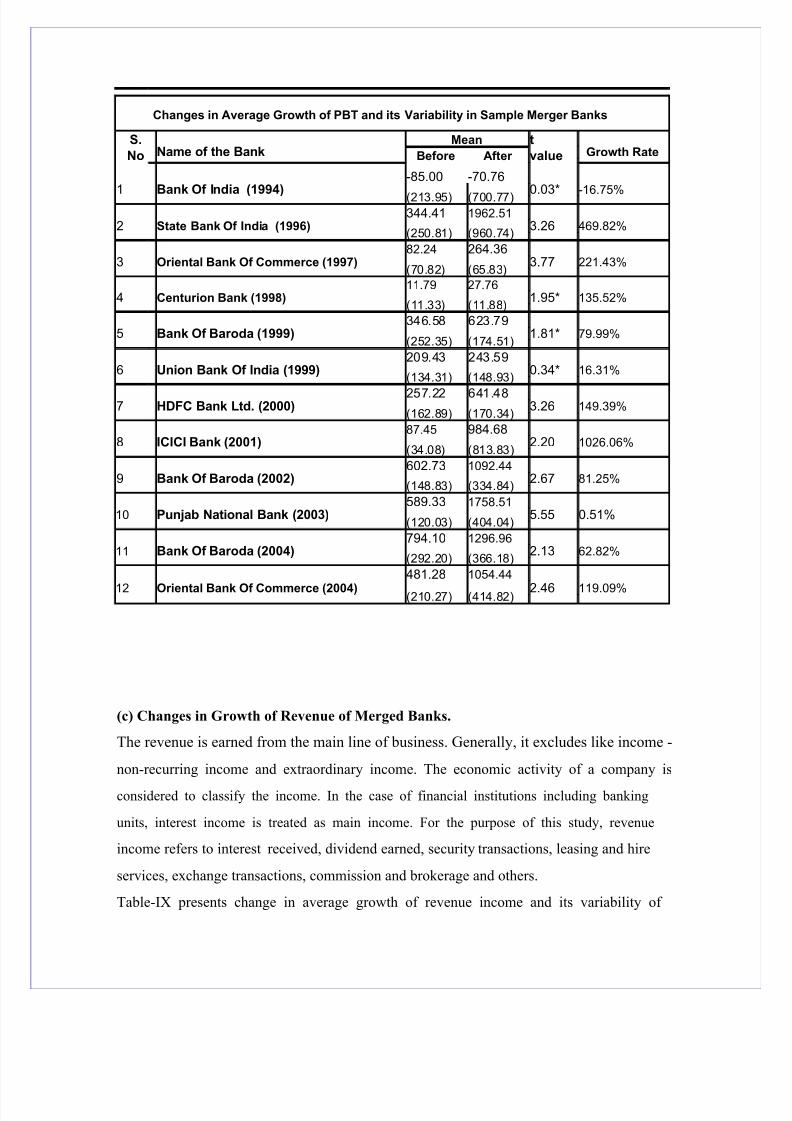

(b) Changes in Growth of Profits of Merged Banks

The profit is an indication of the efficiency with which the business operations are carried

out by corporate sector. The poor operational performance may result in poor sales leading

to poor profits. The merger intends to boost profits through elimination of overlapping

activities and to ensure savings through economies of scale. The amount of profit may be

increased through reduction in overheads, optimum utilization of facilities, raising funds at

lower cost and expansion of business. The merged banks are expected to grow fast in all

aspects and the expectations of stakeholders of both acquiring and merged banks could be

fulfilled. Here the profit refers to profit before tax.

Table-VIII illustrates changes in average profit and its variability in select merged banks.

According to the Table, the average profit earned by merged banks taken for this studyduring post merger period was higher than the profit earned during pre merger period

except for one case that of Bank of India merger in 1994.

The standard deviation has shown that the variation in the growth of profits during post

merged period was higher than that of pre merged period in the case of Bank of India-

1994, State Bank of India-1996, Centurion Bank-1988, Union Bank of India-1999, HDFC

Bank-2000, ICICI Bank-2001, Bank of Baroda-2002, Punjab National Bank-2003, Bank

of Baroda-2004 and Oriental Bank of Commerce-2004. In the case of other two banks

(Oriental Bank of Commerce-1997 and Bank of Baroda-1999) the variation during pre

merged period was higher than that of post merged period. The 't' test clearly showed that

the State bank of India-1996, Oriental Bank of Commerce-1997, HDFC Bank-2000, ICICI

Bank-2001, Bank of Baroda-2002, Punjab National Bank-2003, Bank of Baroda- 2004 and

Oriental Bank of Commerce-2004 have significant profits earned by them. This shows that

growth of profits of all merged banks except Bank of India-1994, Union Bank of India-

1999, Centurion Bank-1998 and Bank of Baroda-1999 - is statistically significant while

the growth of profits of Bank of India-1994, Union Bank of India-1999, Centurion Bank-

1998 and Bank of Baroda-1999 are insignificant. It is understood from the growth rate

(mean value) that ICICI Bank achieved highest growth rate in respect of profits among

sample banks. The low growth rate was seen in case of Bank of India- 1994.

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 43/83

Table: VIII

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 44/83

Changes in Average Growth of PBT and its Variability in Sample Merger Banks

S.Name of the Bank

Mean tGrowth RateNo Before After value

1 Bank Of India (1994)

-70.76

0.03* -16.75%

-85.00

(213.95) (700.77)

2 State Bank Of India (1996)344.41 1962.51

3.26 469.82%(250.81) (960.74)

3 Oriental Bank Of Commerce (1997)82.24 264.36

3.77 221.43%(70.82) (65.83)

4 Centurion Bank (1998)11.79 27.76

1.95* 135.52%(11.33) (11.88)

5 Bank Of Baroda (1999)346.58 623.79

1.81* 79.99%(252.35) (174.51)

6 Union Bank Of India (1999)209.43 243.59

0.34* 16.31%(134.31) (148.93)

7 HDFC Bank Ltd. (2000)257.22 641.48

3.26 149.39%(162.89) (170.34)

8 ICICI Bank (2001)87.45 984.68

2.20 1026.06%(34.08) (813.83)

9 Bank Of Baroda (2002)602.73 1092.44

2.67 81.25%(148.83) (334.84)

10 Punjab National Bank (2003)589.33 1758.51

5.55 0.51%(120.03) (404.04)

11 Bank Of Baroda (2004)794.10 1296.96

2.13 62.82%(292.20) (366.18)

12 Oriental Bank Of Commerce (2004)

481.28 1054.44

2.46 119.09%(210.27) (414.82)

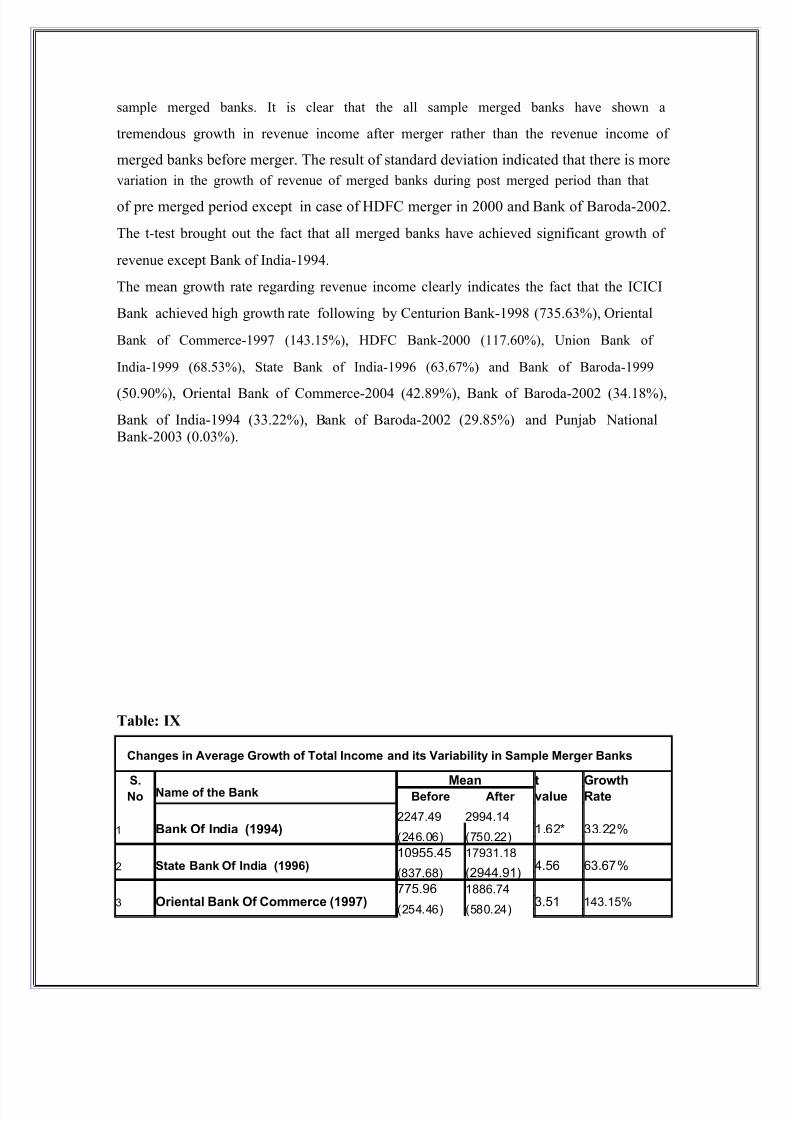

(c) Changes in Growth of Revenue of Merged Banks.

The revenue is earned from the main line of business. Generally, it excludes like income -

non-recurring income and extraordinary income. The economic activity of a company is

considered to classify the income. In the case of financial institutions including banking

units, interest income is treated as main income. For the purpose of this study, revenue

income refers to interest received, dividend earned, security transactions, leasing and hire

services, exchange transactions, commission and brokerage and others.

Table-IX presents change in average growth of revenue income and its variability of

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 45/83

sample merged banks. It is clear that the all sample merged banks have shown a

tremendous growth in revenue income after merger rather than the revenue income of

merged banks before merger. The result of standard deviation indicated that there is morevariation in the growth of revenue of merged banks during post merged period than that

of pre merged period except in case of HDFC merger in 2000 and Bank of Baroda-2002.

The t-test brought out the fact that all merged banks have achieved significant growth of

revenue except Bank of India-1994.

The mean growth rate regarding revenue income clearly indicates the fact that the ICICI

Bank achieved high growth rate following by Centurion Bank-1998 (735.63%), Oriental

Bank of Commerce-1997 (143.15%), HDFC Bank-2000 (117.60%), Union Bank of

India-1999 (68.53%), State Bank of India-1996 (63.67%) and Bank of Baroda-1999

(50.90%), Oriental Bank of Commerce-2004 (42.89%), Bank of Baroda-2002 (34.18%),Bank of India-1994 (33.22%), Bank of Baroda-2002 (29.85%) and Punjab NationalBank-2003 (0.03%).

Table: IX

Changes in Average Growth of Total Income and its Variability in Sample Merger Banks

S. Name of the Bank Mean t GrowthNo Before After value Rate

1 Bank Of India (1994)2994.14

1.62* 33.22%2247.49

(246.06) (750.22)

2 State Bank Of India (1996)10955.45 17931.18

4.56 63.67%(837.68) (2944.91)

3 Oriental Bank Of Commerce (1997)775.96 1886.74

3.51 143.15%(254.46) (580.24)

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 46/83

4 Centurion Bank (1998)53.76 449.26

4.17 735.63%(56.16) (181.24)

5 Bank Of Baroda (1999)3993.96 6026.90

4.70 50.90%(519.79) (692.31)

6 Union Bank Of India (1999)2216.33 3735.28

4.25 68.53%(424.30) (575.15)

7 HDFC Bank Ltd. (2000)1117.57 2431.85

3.37 117.60%(688.47) (365.38)

8 ICICI Bank (2001)544.09 6813.71

2.27 1152.32%(359.83) (5523.86)

9 Bank Of Baroda (2002)5464.31 7332.35

4.49 34.18%(735.07) (391.36)

10 Punjab National Bank (2003)6234.37 9955.14

4.99 0.03%(1125.83) (979.66)

11 Bank Of Baroda (2004)6516.90 8462.44

2.65 29.85%(662.45) (1308.74)

12 Oriental Bank Of Commerce (2004)

3247.63 4640.58

2.59 42.89%(527.62) (937.02)

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 47/83

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 48/83

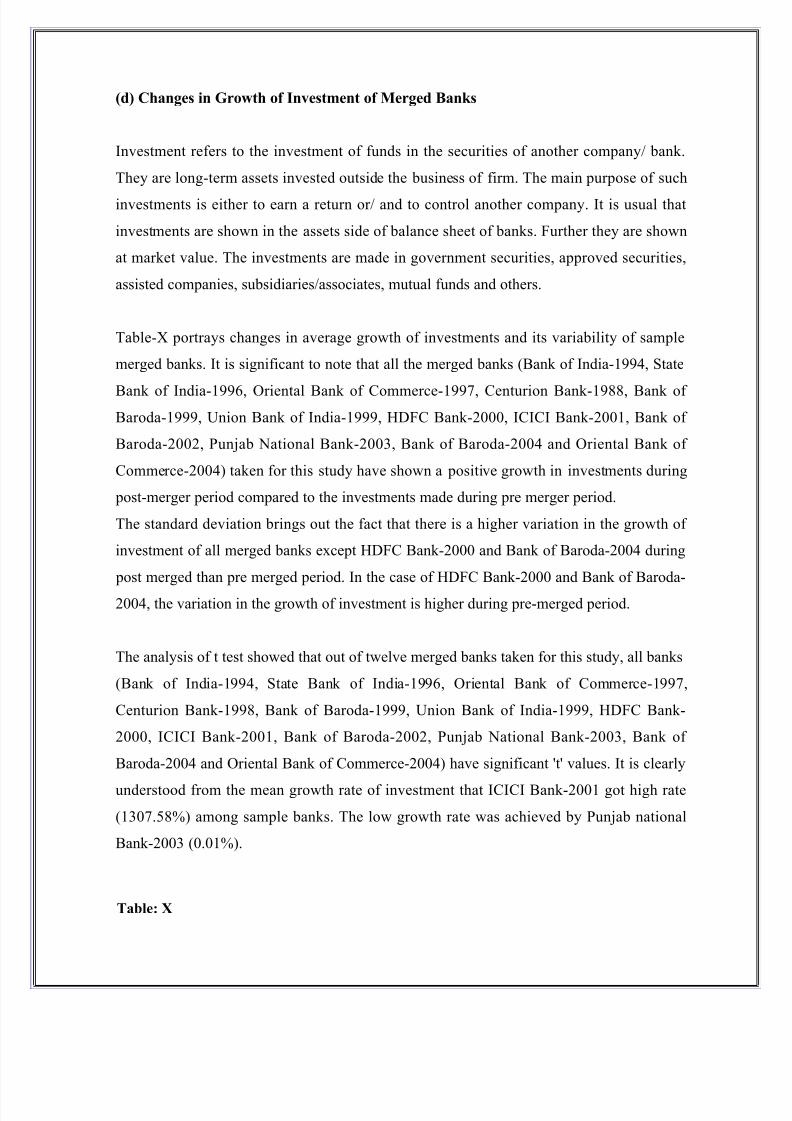

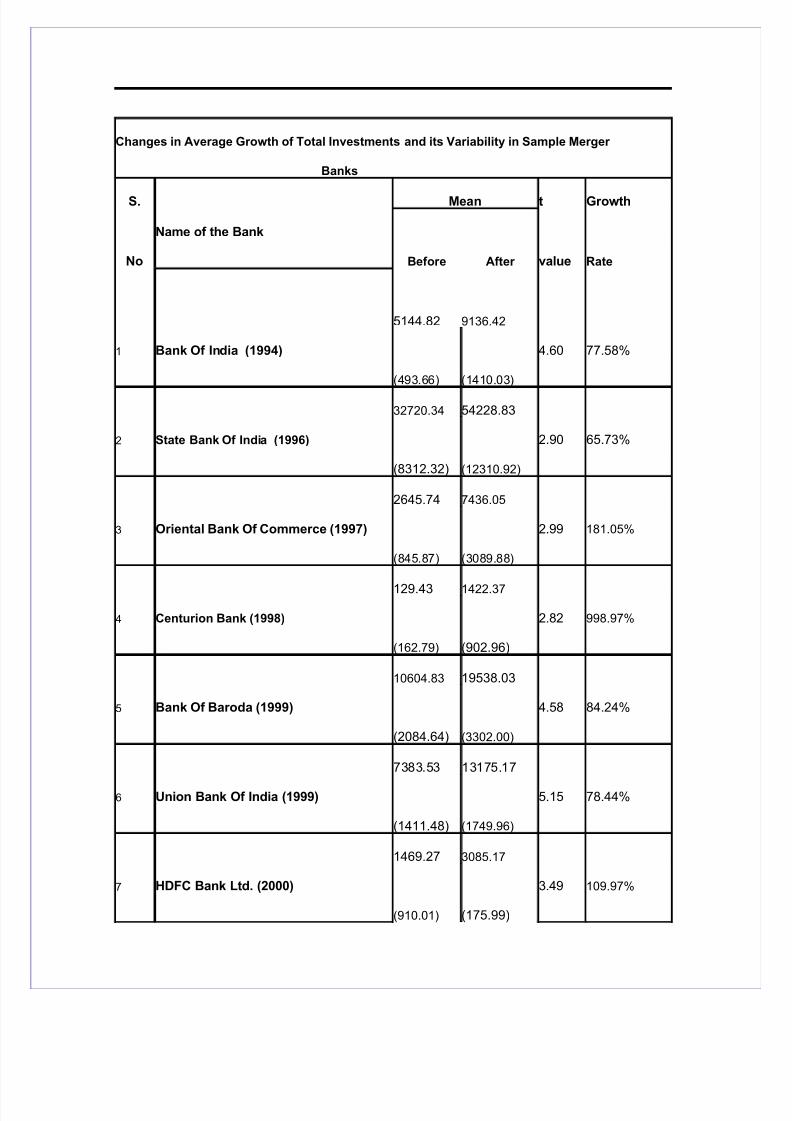

Changes in Average Growth of Total Investments and its Variability in Sample Merger

Banks

S.

Name of the Bank

Mean t Growth

No Before After value Rate

1 Bank Of India (1994)

9136.42

4.60 77.58%

5144.82

(493.66) (1410.03)

2 State Bank Of India (1996)

32720.34 54228.83

2.90 65.73%

(8312.32) (12310.92)

3 Oriental Bank Of Commerce (1997)

2645.74 7436.05

2.99 181.05%

(845.87) (3089.88)

4 Centurion Bank (1998)

129.43 1422.37

2.82 998.97%

(162.79) (902.96)

5 Bank Of Baroda (1999)

10604.83 19538.03

4.58 84.24%

(2084.64) (3302.00)

6 Union Bank Of India (1999)

7383.53 13175.17

5.15 78.44%

(1411.48) (1749.96)

7 HDFC Bank Ltd. (2000)

1469.27 3085.17

3.49 109.97%

(910.01) (175.99)

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 49/83

8 ICICI Bank (2001)

2184.16 30743.94

3.67 1307.58%

(1811.84) (15477.45)

9 Bank Of Baroda (2002)

16919.48 32276.44

4.25 90.76%

(2887.65) (6625.26)

10 Punjab National Bank (2003)

23501.96 41970.92

4.63 0.01%

(4124.95) (6822.59)

11 Bank Of Baroda (2004)

23106.54 36735.82

5.02 58.98%

(5222.22) (1481.60)

12 Oriental Bank Of Commerce (2004)

13084.24 17940.56

4.77 37.12%

(1437.20) (1440.54)

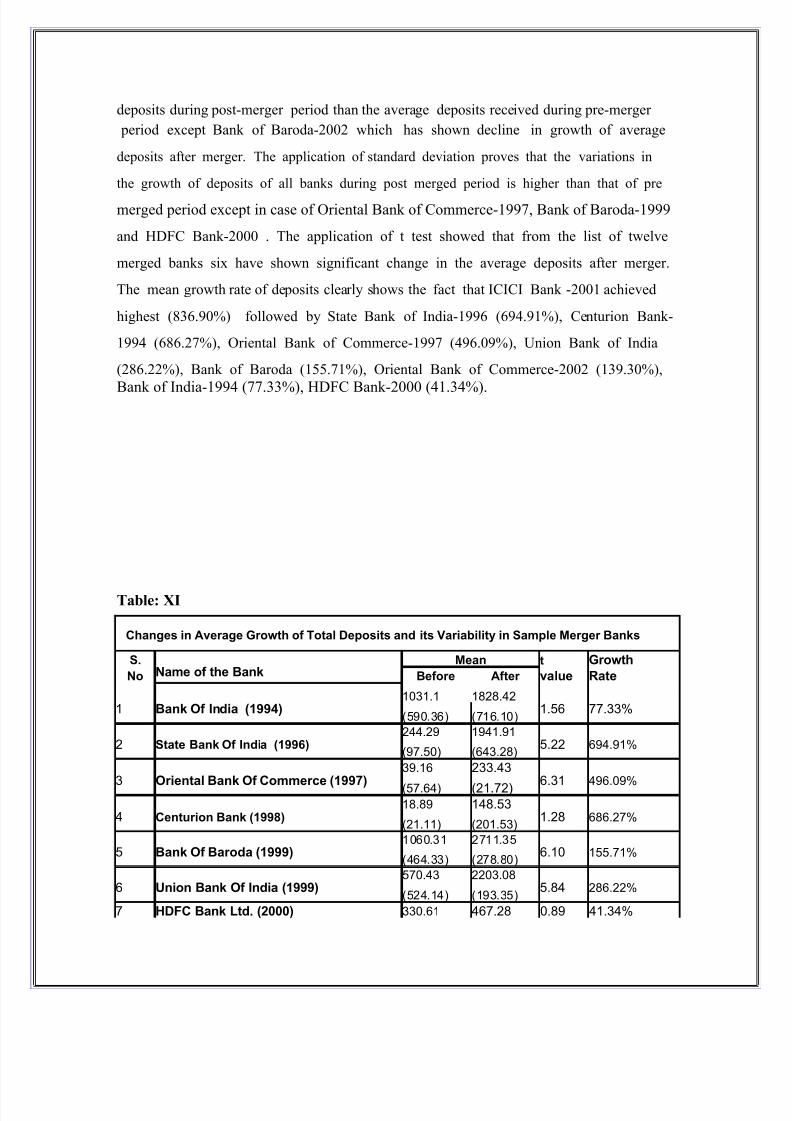

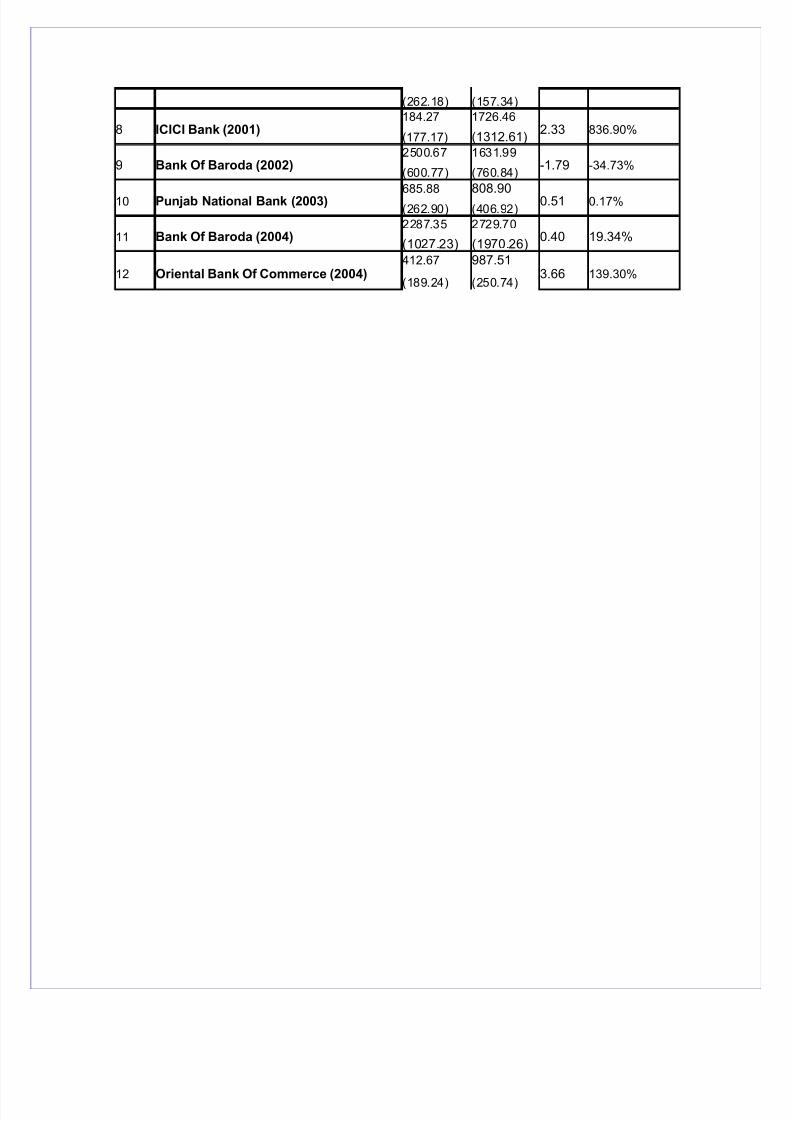

(e) Changes in Growth of Deposits of Merged Banks

The important element of conventional banking business is to accept deposits from the

customers. Now-a days manufacturing companies also started accepting deposits for

short period from their members, directors and the general public. This mode of raising

funds is popular on account of the fact that the bank credit becomes quite costlier. For the

purpose of study Total deposits refers to bank balance in deposits a/c, bank balance in

deposit a/c (abroad), deposits with government.

Table- XI exhibits changes in average growth of deposits and its variability of sample

merged banks. It is clear that all merged banks have shown a significant growth of

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 50/83

deposits during post-merger period than the average deposits received during pre-merger period except Bank of Baroda-2002 which has shown decline in growth of average

deposits after merger. The application of standard deviation proves that the variations in

the growth of deposits of all banks during post merged period is higher than that of pre

merged period except in case of Oriental Bank of Commerce-1997, Bank of Baroda-1999

and HDFC Bank-2000 . The application of t test showed that from the list of twelve

merged banks six have shown significant change in the average deposits after merger.

The mean growth rate of deposits clearly shows the fact that ICICI Bank -2001 achieved

highest (836.90%) followed by State Bank of India-1996 (694.91%), Centurion Bank-

1994 (686.27%), Oriental Bank of Commerce-1997 (496.09%), Union Bank of India

(286.22%), Bank of Baroda (155.71%), Oriental Bank of Commerce-2002 (139.30%),

Bank of India-1994 (77.33%), HDFC Bank-2000 (41.34%).

Table: XI

Changes in Average Growth of Total Deposits and its Variability in Sample Merger Banks

S.Name of the Bank

Mean t Growth

No Before After value Rate

1 Bank Of India (1994)1828.42

1.56 77.33%1031.1

(590.36) (716.10)

2 State Bank Of India (1996)244.29 1941.91

5.22 694.91%(97.50) (643.28)

3 Oriental Bank Of Commerce (1997)

39.16 233.43

6.31 496.09%(57.64) (21.72)

4 Centurion Bank (1998)18.89 148.53

1.28 686.27%(21.11) (201.53)

5 Bank Of Baroda (1999)1060.31 2711.35

6.10 155.71%(464.33) (278.80)

6 Union Bank Of India (1999)570.43 2203.08

5.84 286.22%(524.14) (193.35)

7 HDFC Bank Ltd. (2000) 330.61 467.28 0.89 41.34%

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 51/83

(262.18) (157.34)

8 ICICI Bank (2001)184.27 1726.46

2.33 836.90%(177.17) (1312.61)

9 Bank Of Baroda (2002)2500.67 1631.99

-1.79 -34.73%(600.77) (760.84)

10 Punjab National Bank (2003)685.88 808.90

0.51 0.17%(262.90) (406.92)

11 Bank Of Baroda (2004)2287.35 2729.70

0.40 19.34%(1027.23) (1970.26)

12 Oriental Bank Of Commerce (2004)412.67 987.51

3.66 139.30%(189.24) (250.74)

8/8/2019 Vineet - Mrp Report

http://slidepdf.com/reader/full/vineet-mrp-report 52/83

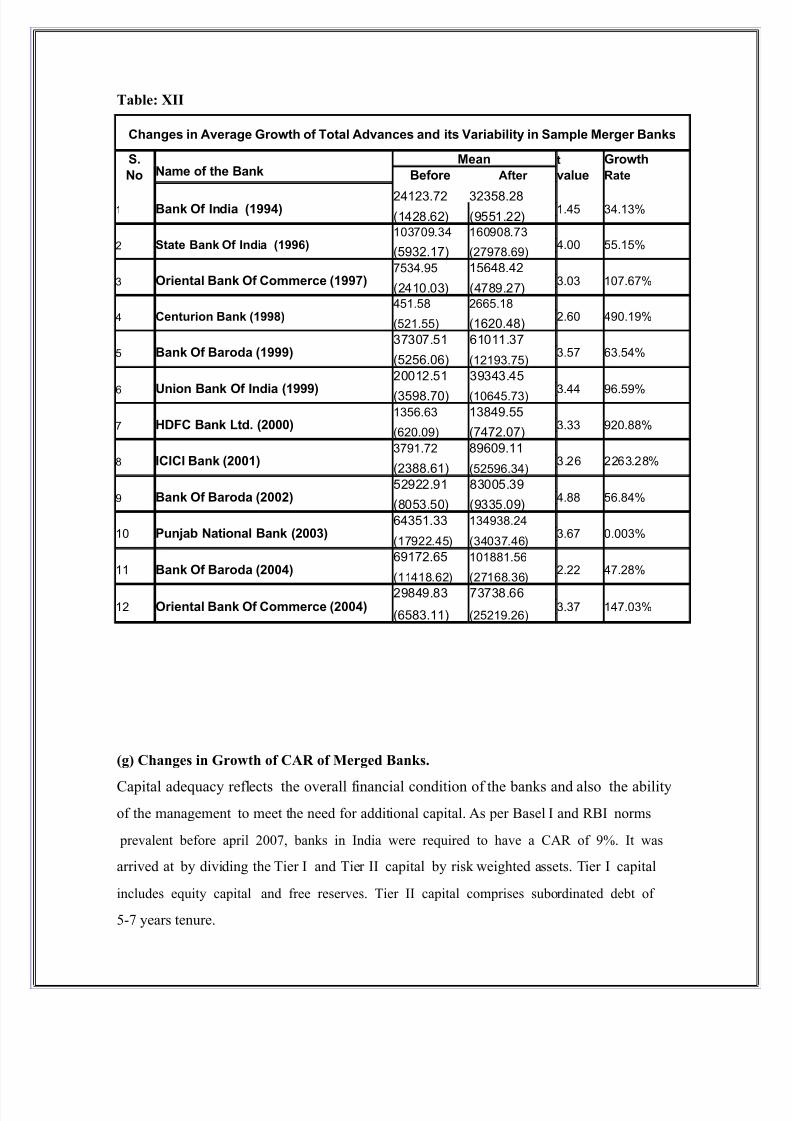

(f) Changes in Growth of Advances of Merged Banks.

Advances form another important aspect of conventional banking operations. For the

purpose of study Total Advances include Term Advances, short term advances, advances

to assisted companies, advances to bank and institutions, advances in foreign currency,

other advances, advances in priority sector, advances in public sector.

Table-XII shows changes in average growth of total advances and its variability in sample

merged banks. It is clear that all sample- merged banks (Bank of India-1994, State Bank

of India-1996, Oriental Bank of Commerce-1997, Centurion Bank-1988, Bank of Baroda-

1999, Union Bank of India-1999, HDFC Bank-2000, ICICI Bank-2001, Bank of Baroda-

2002, Punjab National Bank-2003, Bank of Baroda-2004 and Oriental Bank of

Commerce-2004) have shown upward growth in total advances after merger. The result of standard deviation clearly shows that the variation of advances of all merged banks after

merger was high than that of pre merger period.