venture capital returns

TRANSCRIPT

1 Steven N. Kaplan

What do Venture Capitalists do?

How Well Have They Done?

Steve Kaplan University of Chicago Booth School of Business

2 Steven N. Kaplan

Overview ■ Two parts to the talk:

– Performance: » How have VC funds performed?

■ How does VC compare to PE? » How will VC perform going forward?

– What do VCs do?

3 Steven N. Kaplan

How have VC funds performed?

■ Fundraising? ■ Performance?

4 Steven N. Kaplan

Fundraising (U.S.)

0

10

20

30

40

50

60

70

80

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

$ B

illio

ns

Commitments to U.S. Venture Capital Partnerships 1980 - 2015 (in $ billions)

Source: Private Equity Analysis, Steven N. Kaplan

5 Steven N. Kaplan

Fundraising (U.S.) as % of market

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.350%

0.400%

0.450%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Commitments to U.S. VC Partnerships as Fraction of Stock Market Capitalization 1980 - 2015

Source: Private Equity Analyst, Steven N. Kaplan

6 Steven N. Kaplan

Fundraising

■ Commitments to VC as a % of overall stock market has been much more stable than is commonly appreciated. – Usually between 0.10% and 0.20% of total stock market. – Big outliers were 1999 to 2001. – On the low side since 2009.

7 Steven N. Kaplan

What about performance for LPs?

■ How is performance measured? ■ Who measures performance? ■ What has performance been on average? ■ Are there good GPs? ■ Summarize results from

– Harris, Jenkinson, Kaplan (2014 and 2016) – Brown, Harris, Jenkinson, Kaplan, Robinson (2016)

8 Steven N. Kaplan

How is Performance Measured?

■ Two industry standards: – Annualized IRR (net of fees).

– Multiple of Invested Capital (MIC). » Total Value Returned / Invested Capital. » (Distributed Value + Residual Value) / (Capital in Cos. + Fees)

■ Each has its drawbacks.

9 Steven N. Kaplan

■ Each has its drawbacks:

– Net IRR: » Absolute (not relative).

■ Does not control for market movements. » Is sensitive to sequencing of investments.

– Multiple of Invested Capital: » Absolute (not relative).

■ Does not control for market movements.

How is Performance Measured?

10 Steven N. Kaplan

How is Performance Measured?

■ A 3rd method – KS PME (Public Market Equivalent). – Grow LP inflows / investments at S&P 500 (or other return). – Grow LP returns / distributions at S&P 500 (or other return). – Compare value of outflows to inflows. – If PME > 1, then LPs did better than S&P 500.

» + Does control for the market. » + Not sensitive to investment sequence.

■ Think of PME as a market-adjusted multiple.

11 Steven N. Kaplan

Does anyone use KS PME? Calpers

12 Steven N. Kaplan

Who measures performance?

■ Four commercial databases: – Burgiss – Cambridge Associates (CA) – Pitchbook – Preqin – Thomson Venture Economics (VE)

13 Steven N. Kaplan

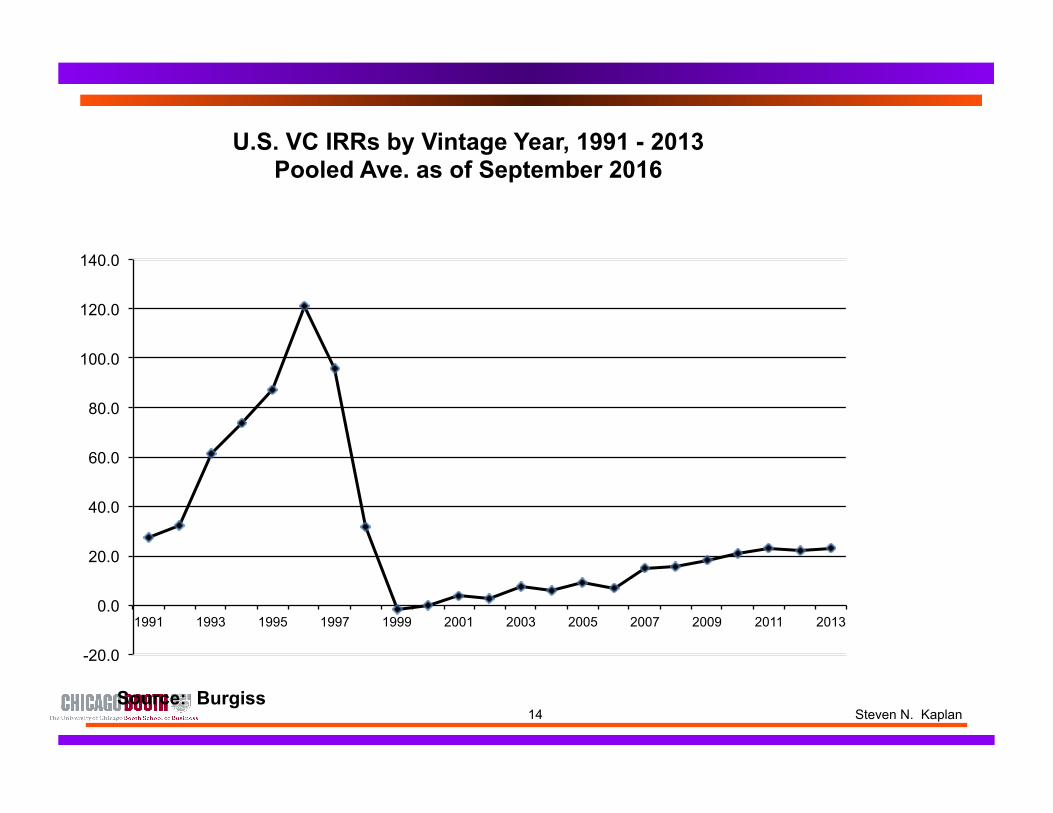

What about performance?

14 Steven N. Kaplan

-20.0

0.0

20.0

40.0

60.0

80.0

100.0

120.0

140.0

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Source: Burgiss

U.S. VC IRRs by Vintage Year, 1991 - 2013 Pooled Ave. as of September 2016

15 Steven N. Kaplan

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Source: Burgiss

U.S. VC MOICs by Vintage Year, 1991 - 2013 Pooled Ave. as of September 2016

16 Steven N. Kaplan

Question?

■ Have VC funds of vintages 2006 to 2013 beaten the S&P 500?

17 Steven N. Kaplan

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Source: Burgiss

U.S. VC PMEs by Vintage Year, 1991 - 2013 Pooled Ave. as of September 2016

18 Steven N. Kaplan

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1999 2001 2003 2005 2007 2009 2011 2013

Source: Burgiss

U.S. VC PMEs by Vintage Year, 1999 - 2013 Pooled Ave. as of September 2016

19 Steven N. Kaplan

Overall return evidence

■ IRRs, Multiples and PMEs vary substantially across vintage years. – PMEs well above 1.0 through 1998. – PMEs below 1.0 1999 to 2002. – PMEs above 1.0 since 2003.

20 Steven N. Kaplan

Question?

■ How has PE done relative to VC?

■ Have PE funds of vintages 2006 to 2013 beaten the S&P 500?

21 Steven N. Kaplan

PE vs. VC performance? PMEs

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1999 2001 2003 2005 2007 2009 2011 2013

Source: Burgiss

U.S. VC and PE PMEs by Vintage Year, 1999 - 2013 Pooled Ave. as of September 2016

VC PME PE PME

22 Steven N. Kaplan

PE vs. VC

■ How has PE done relative to VC? – For 1999 to 2005 vintages, PE did much better. – For post-2006 vintages, VC has done better.

23 Steven N. Kaplan

What will happen going forward? Returns?

24 Steven N. Kaplan

Future Performance and Fundraising:

■ Performance in VC significantly negatively related to fundraising. – Even more so. – IRR in Vintage Year =

» 43% - 75 x VC inflows in current and prior year as % of stock mkt. – Multiple in Vintage Year =

» 4.39 - 626 x VC inflows in current and prior year as % of stock mkt. – PME in Vintage Year =

» 2.48 - 279 x VC inflows in current and prior year as % of stock mkt. – On average VC inflows = 0.135% of stock market. (2 years 0.27%).

25 Steven N. Kaplan

Vintage Year PME vs. Capital Committed

26 Steven N. Kaplan

Fundraising (U.S.) as % of market

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.350%

0.400%

0.450%

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Commitments to U.S. VC Partnerships as Fraction of Stock Market Capitalization 1980 - 2015

Source: Private Equity Analyst, Steven N. Kaplan

27 Steven N. Kaplan

What will the future hold?

■ Despite all the attention to start-ups / VC, commitments to stock market value not particularly high relative to historical means.

■ Will probably be higher this year, but nowhere near tech boom. – Commitments to PE are at historically high levels.

■ Accordingly, still feel better about VC than about PE.

61 Steven N. Kaplan

Steven N. Kaplan Neubauer Family Distinguished Service Professor

Entrepreneurship and Finance [email protected]