var_my_presentation

TRANSCRIPT

BTRM Cohort 2 2015 2© 2015 Moorad Choudhry

Agenda

- VaR Definition

- VaR Methods

- Normal / Standard Normal Distribution

- Parameter Estimation

- VaR Calculations / Examples.

- References

BTRM Cohort 2 2015 3© 2015 Moorad Choudhry

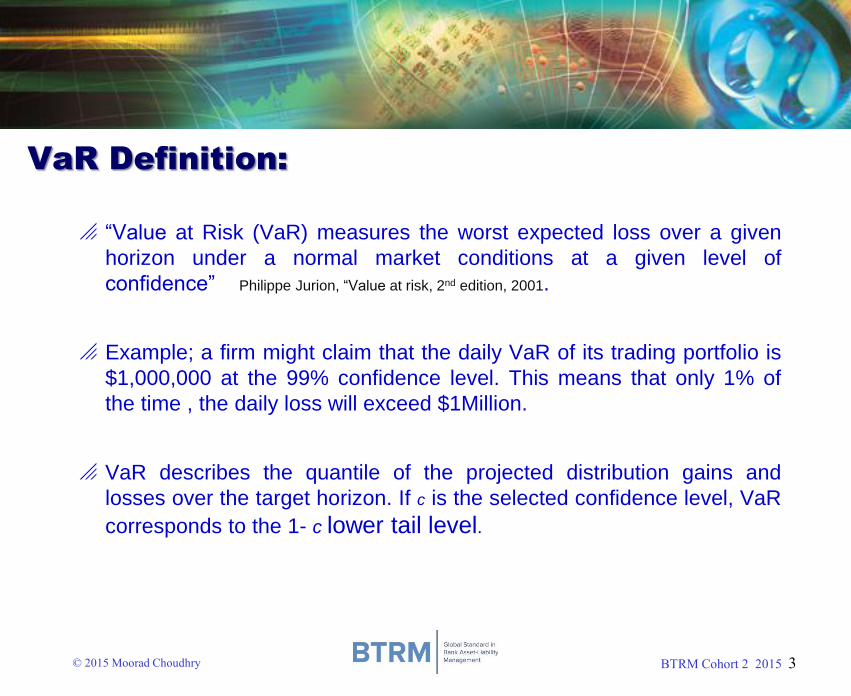

VaR Definition:

“Value at Risk (VaR) measures the worst expected loss over a given

horizon under a normal market conditions at a given level of

confidence” Philippe Jurion, “Value at risk, 2nd edition, 2001.

Example; a firm might claim that the daily VaR of its trading portfolio is

$1,000,000 at the 99% confidence level. This means that only 1% of

the time , the daily loss will exceed $1Million.

VaR describes the quantile of the projected distribution gains and

losses over the target horizon. If c is the selected confidence level, VaR

corresponds to the 1- c lower tail level.

BTRM Cohort 2 2015 4© 2015 Moorad Choudhry

VaR Definition:

“In simpler words, VaR is a single number that indices how much a

financial institution can lose with probability φ over given time horizon.

Why is it so popular ?

VaR reduces the risk associated with any portfolio to just one number,

the loss associated with a given probability.

BTRM Cohort 2 2015 5© 2015 Moorad Choudhry

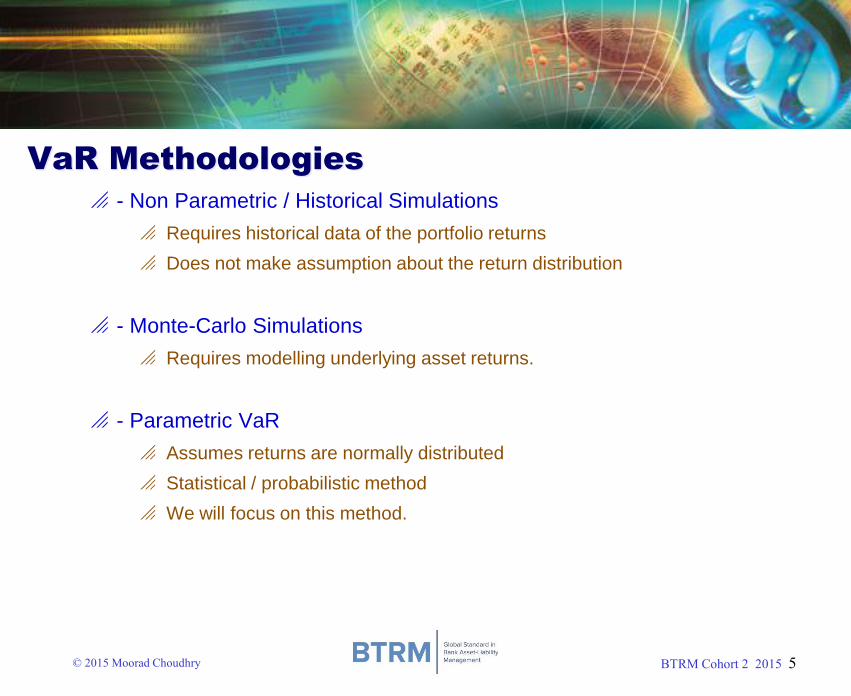

VaR Methodologies

- Non Parametric / Historical Simulations

Requires historical data of the portfolio returns

Does not make assumption about the return distribution

- Monte-Carlo Simulations

Requires modelling underlying asset returns.

- Parametric VaR

Assumes returns are normally distributed

Statistical / probabilistic method

We will focus on this method.

BTRM Cohort 2 2015 6© 2015 Moorad Choudhry

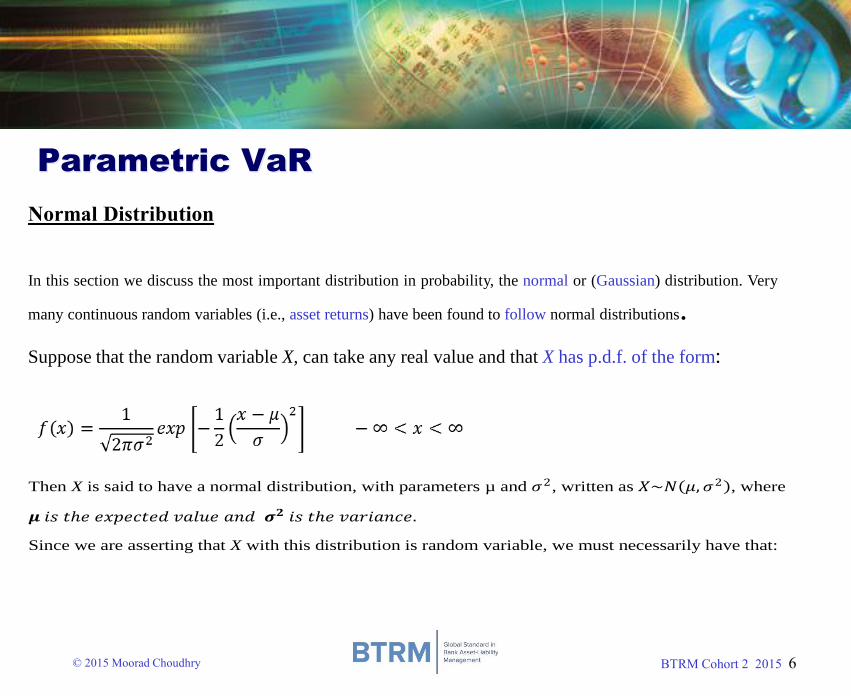

Parametric VaR

Suppose that the random variable X, can take any real value and that X has p.d.f. of the form:

In this section we discuss the most important distribution in probability, the normal or (Gaussian) distribution. Very

many continuous random variables (i.e., asset returns) have been found to follow normal distributions.

Then X is said to have a normal distribution, with parameters µ and 𝜎2, written as 𝑋~𝑁 𝜇,𝜎2 , where

𝝁 𝑖𝑠 𝑡ℎ𝑒 𝑒𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝑣𝑎𝑙𝑢𝑒 𝑎𝑛𝑑 𝝈𝟐 𝑖𝑠 𝑡ℎ𝑒 𝑣𝑎𝑟𝑖𝑎𝑛𝑐𝑒.

Since we are asserting that X with this distribution is random variable, we must necessarily have that:

Normal Distribution

BTRM Cohort 2 2015 7© 2015 Moorad Choudhry

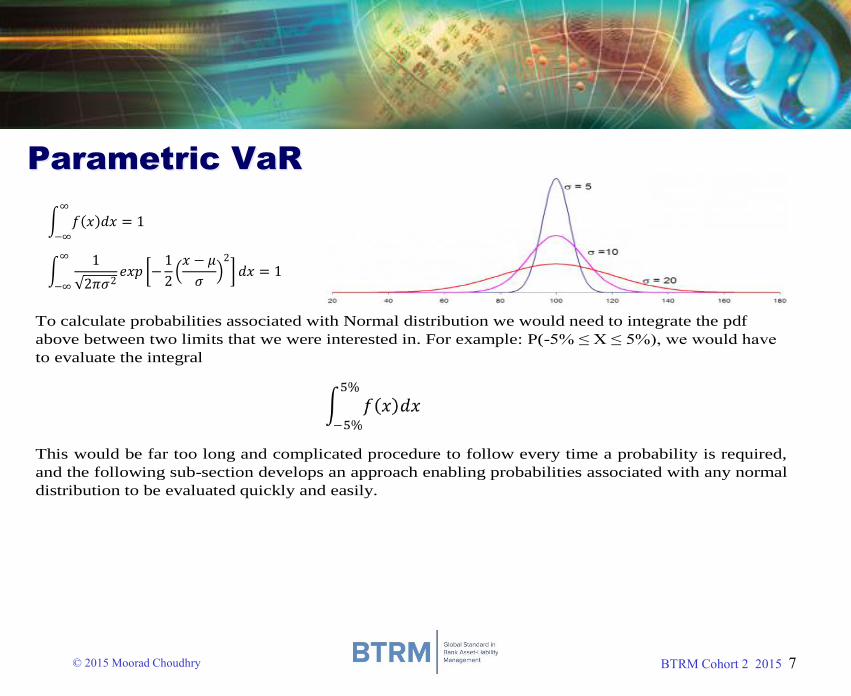

Parametric VaR

𝑓 𝑥 𝑑𝑥 = 1∞

−∞

1

2𝜋𝜎2𝑒𝑥𝑝 −

1

2 𝑥 − 𝜇

𝜎

2

𝑑𝑥 = 1∞

−∞

To calculate probabilities associated with Normal distribution we would need to integrate the pdf

above between two limits that we were interested in. For example: P(-5% ≤ X ≤ 5%), we would have

to evaluate the integral

This would be far too long and complicated procedure to follow every time a probability is required,

and the following sub-section develops an approach enabling probabilities associated with any normal

distribution to be evaluated quickly and easily.

BTRM Cohort 2 2015 8© 2015 Moorad Choudhry

Parametric VaR

Standard Normal Distribution

We do the following transformation:

A normal distribution having = 0 and 2 = 1 is called standard normal distribution.

Therefore, if 𝑍~𝑁 0, 1 , then the distribution function of standard normal function is given by;

𝜑 𝑍 = 𝑃 𝑍 ≤ 𝑧 =1

2𝜋 𝑒𝑥𝑝 −

1

2 𝑥 2 𝑑𝑥

𝑧

−∞

)1,0(N

Suppose that Z has the standard Normal distribution, Z ~ )1,0(N . Then we will use Standard

cumulative distribution table to find probabilities:

BTRM Cohort 2 2015 9© 2015 Moorad Choudhry

Parametric VaR

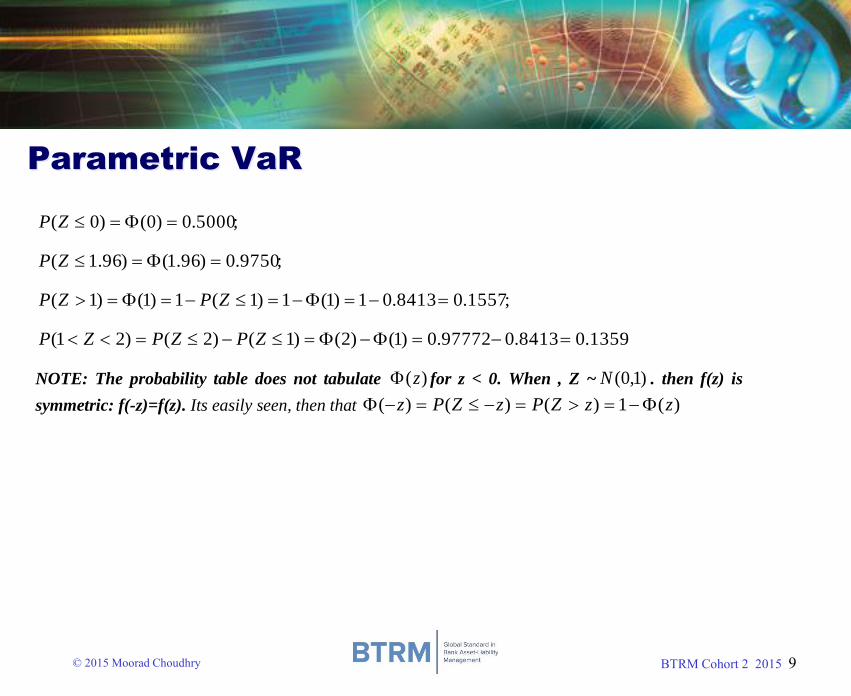

;5000.0)0()0( ZP

;9750.0)96.1()96.1( ZP

;1557.08413.01)1(1)1(1)1()1( ZPZP

1359.08413.097772.0)1()2()1()2()21( ZPZPZP

NOTE: The probability table does not tabulate )(z for z < 0. When , Z ~ )1,0(N . then f(z) is

symmetric: f(-z)=f(z). Its easily seen, then that )(1)()()( zzZPzZPz

BTRM Cohort 2 2015 10© 2015 Moorad Choudhry

Parametric VaR

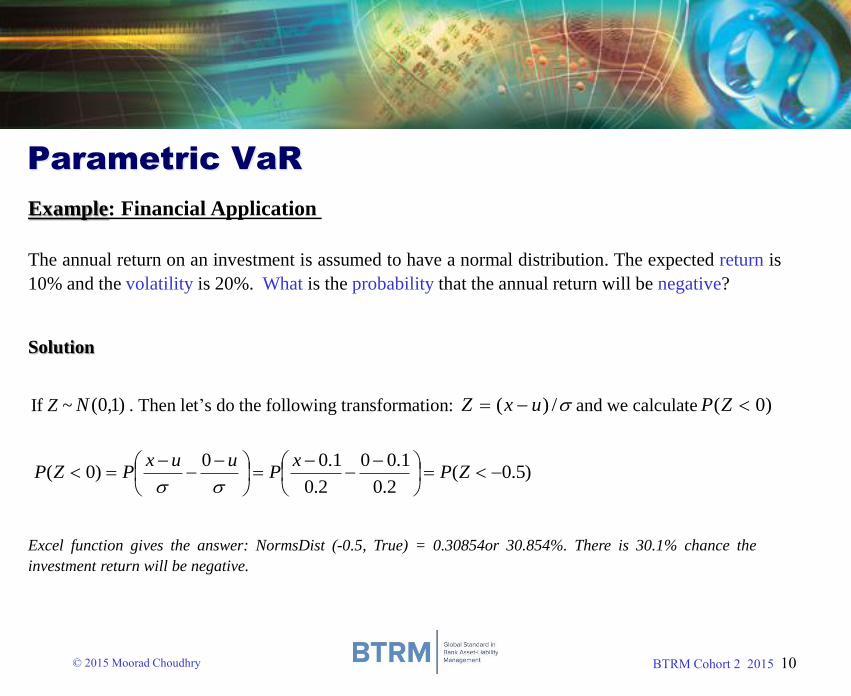

Example: Financial Application

The annual return on an investment is assumed to have a normal distribution. The expected return is

10% and the volatility is 20%. What is the probability that the annual return will be negative?

Solution

If Z ~ )1,0(N . Then let’s do the following transformation: /)( uxZ and we calculate )0( ZP

)5.0(2.0

1.00

2.0

1.00)0(

ZP

xP

uuxPZP

Excel function gives the answer: NormsDist (-0.5, True) = 0.30854or 30.854%. There is 30.1% chance the

investment return will be negative.

BTRM Cohort 2 2015 11© 2015 Moorad Choudhry

Parametric VaR

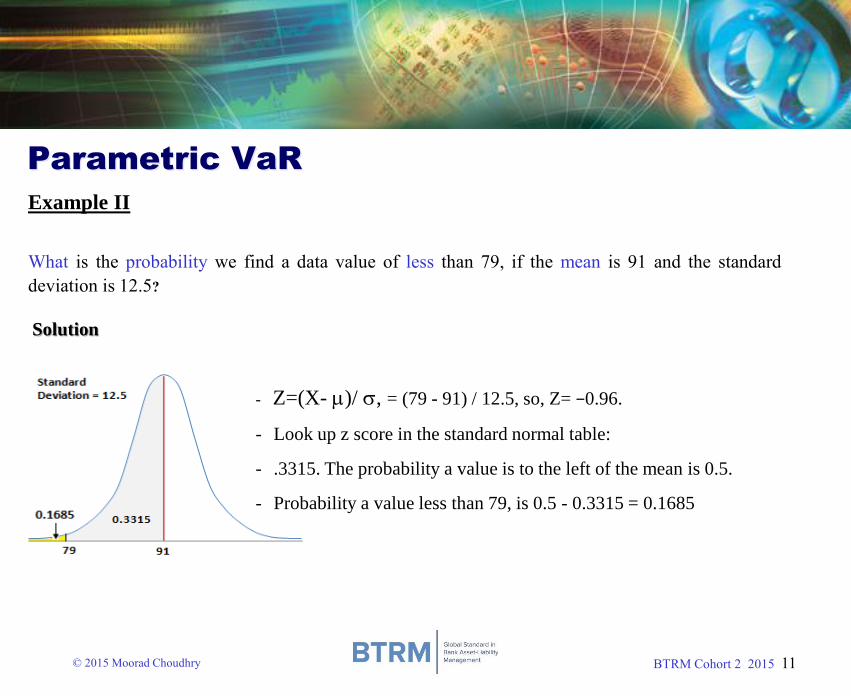

What is the probability we find a data value of less than 79, if the mean is 91 and the standard

deviation is 12.5?

Solution

- Z=(X- )/ , = (79 - 91) / 12.5, so, Z= −0.96.

- Look up z score in the standard normal table:

- .3315. The probability a value is to the left of the mean is 0.5.

- Probability a value less than 79, is 0.5 - 0.3315 = 0.1685

Example II

BTRM Cohort 2 2015 12© 2015 Moorad Choudhry

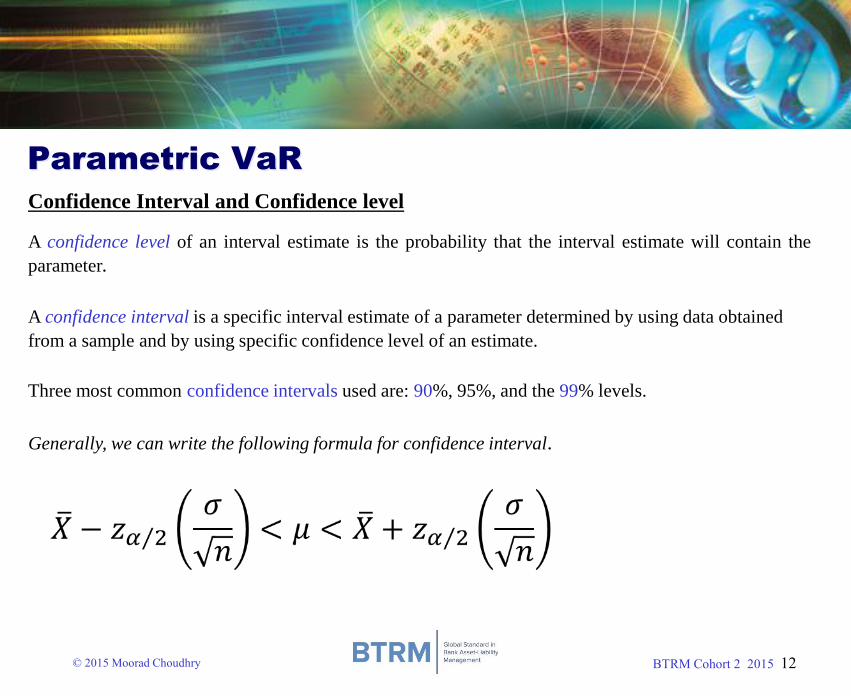

Parametric VaR

Confidence Interval and Confidence level

A confidence level of an interval estimate is the probability that the interval estimate will contain the

parameter.

A confidence interval is a specific interval estimate of a parameter determined by using data obtained

from a sample and by using specific confidence level of an estimate.

Three most common confidence intervals used are: 90%, 95%, and the 99% levels.

Generally, we can write the following formula for confidence interval.

BTRM Cohort 2 2015 13© 2015 Moorad Choudhry

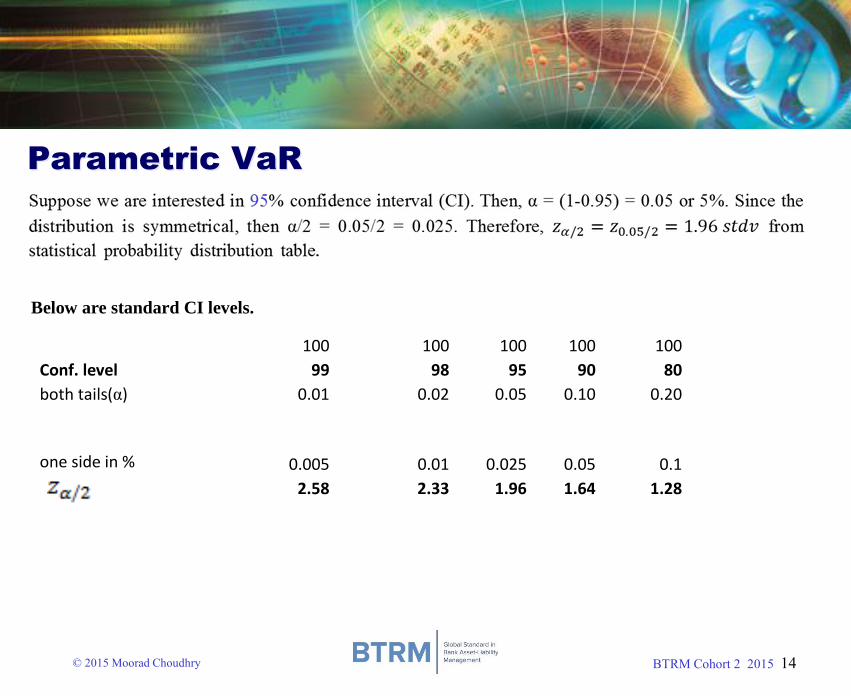

Parametric VaR

In general,

α = (1-CI). At 95% CI, then, α = (1-0.95) = 5% or 0.05. α/2 = 0.05/2 = 0.025. 𝑧0.05/2 = 1.96

α = (1-CI). At 99% CI, then, α = (1-0.99) = 0.1% or 0.01. α/2 = 0.01/2 = 0.005. 𝑧0.01/2 = 2.58

α = (1-CI). At 98% CI, then, α = (1-0.98) = 0.2% or 0.02. α/2 = 0.02/2 = 0.01. 𝑧0.02/2= 2.33

BTRM Cohort 2 2015 14© 2015 Moorad Choudhry

Parametric VaR

Below are standard CI levels.

100 100 100 100 100

Conf. level 99 98 95 90 80

both tails(α) 0.01 0.02 0.05 0.10 0.20

one side in %

0.005 0.01 0.025 0.05 0.1

2.58 2.33 1.96 1.64 1.28

BTRM Cohort 2 2015 15© 2015 Moorad Choudhry

Estimating Volatility

Volatility is a measure of capturing the variability of a given data set from its average (mean). It measures

the dispersion of the data around its mean.

Most common estimate of volatility is:

BTRM Cohort 2 2015 16© 2015 Moorad Choudhry

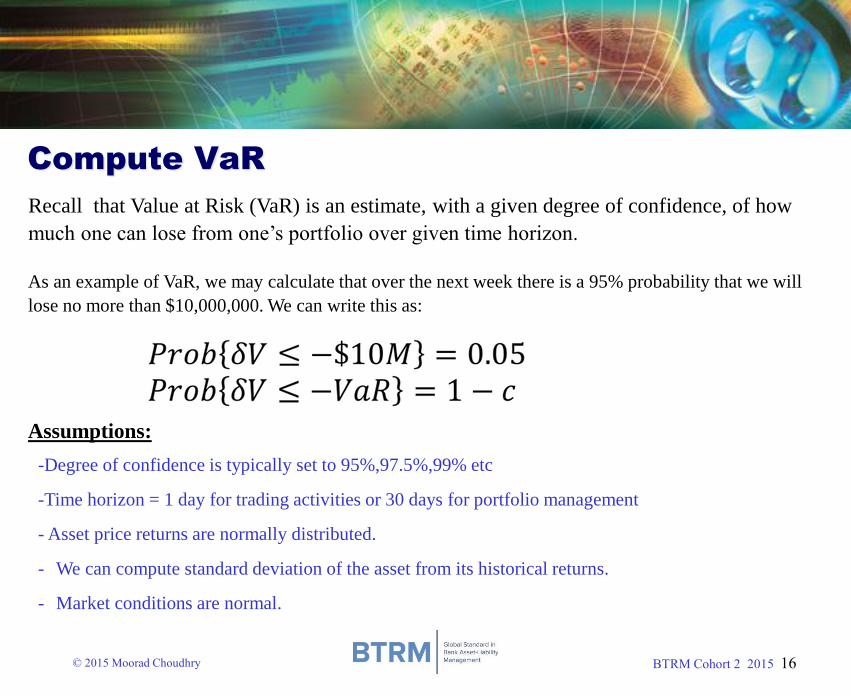

Compute VaR

Recall that Value at Risk (VaR) is an estimate, with a given degree of confidence, of how

much one can lose from one’s portfolio over given time horizon.

As an example of VaR, we may calculate that over the next week there is a 95% probability that we will

lose no more than $10,000,000. We can write this as:

Assumptions:

-Degree of confidence is typically set to 95%,97.5%,99% etc

-Time horizon = 1 day for trading activities or 30 days for portfolio management

- Asset price returns are normally distributed.

- We can compute standard deviation of the asset from its historical returns.

- Market conditions are normal.

BTRM Cohort 2 2015 17© 2015 Moorad Choudhry

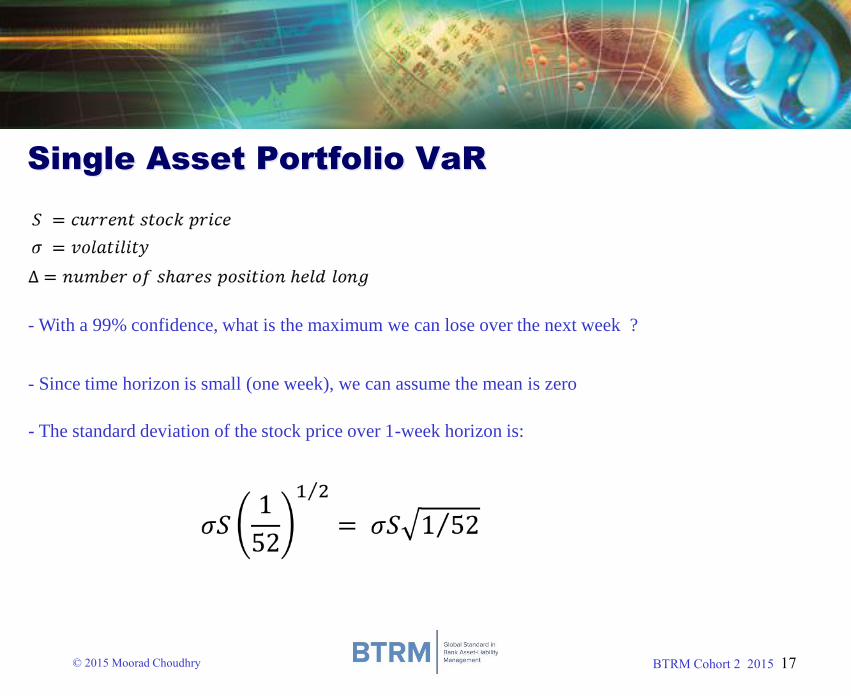

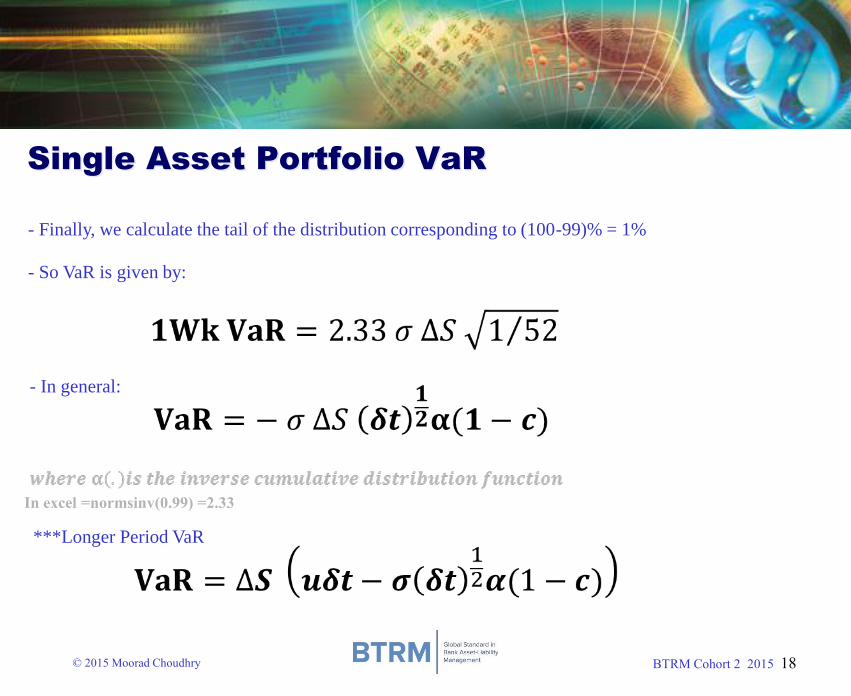

Single Asset Portfolio VaR

- With a 99% confidence, what is the maximum we can lose over the next week ?

- Since time horizon is small (one week), we can assume the mean is zero

- The standard deviation of the stock price over 1-week horizon is:

BTRM Cohort 2 2015 18© 2015 Moorad Choudhry

Single Asset Portfolio VaR

- Finally, we calculate the tail of the distribution corresponding to (100-99)% = 1%

- So VaR is given by:

In excel =normsinv(0.99) =2.33

- In general:

***Longer Period VaR

BTRM Cohort 2 2015 19© 2015 Moorad Choudhry

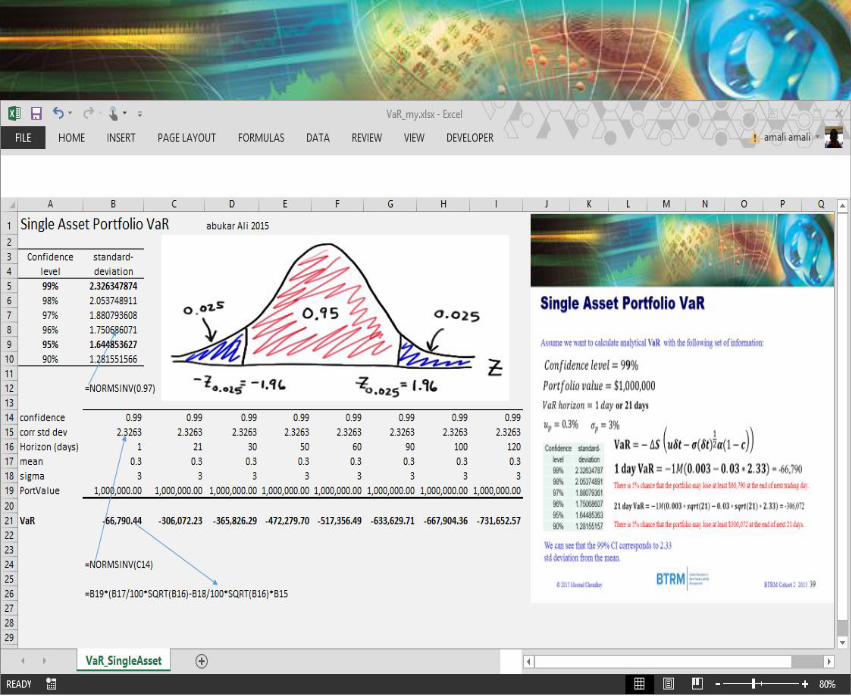

Single Asset Portfolio VaR

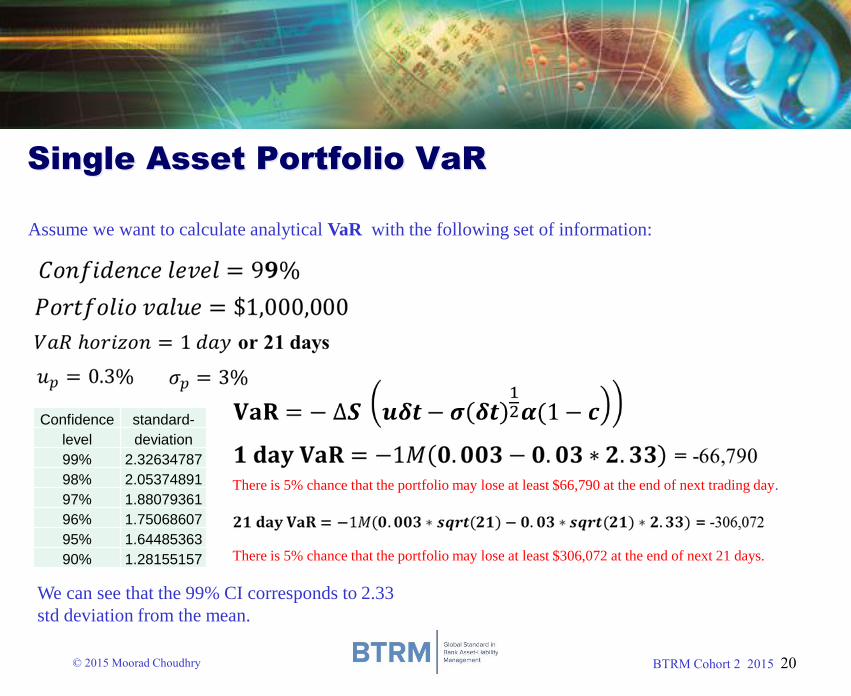

Assume we want to calculate analytical VaR with the following set of information:

Confidence standard-

level deviation

99% 2.32634787

98% 2.05374891

97% 1.88079361

96% 1.75068607

95% 1.64485363

90% 1.28155157

We can see that the 95% CI corresponds to1.64485

std deviation from the mean.

There is 5% chance that the portfolio may lose at least $46,435 at the end of next trading day.

There is 5% chance that the portfolio may lose at least $212,388 at the end of next 21 days.

BTRM Cohort 2 2015 20© 2015 Moorad Choudhry

Single Asset Portfolio VaR

Assume we want to calculate analytical VaR with the following set of information:

Confidence standard-

level deviation

99% 2.32634787

98% 2.05374891

97% 1.88079361

96% 1.75068607

95% 1.64485363

90% 1.28155157

We can see that the 99% CI corresponds to 2.33

std deviation from the mean.

There is 5% chance that the portfolio may lose at least $66,790 at the end of next trading day.

There is 5% chance that the portfolio may lose at least $306,072 at the end of next 21 days.

BTRM Cohort 2 2015 21© 2015 Moorad Choudhry

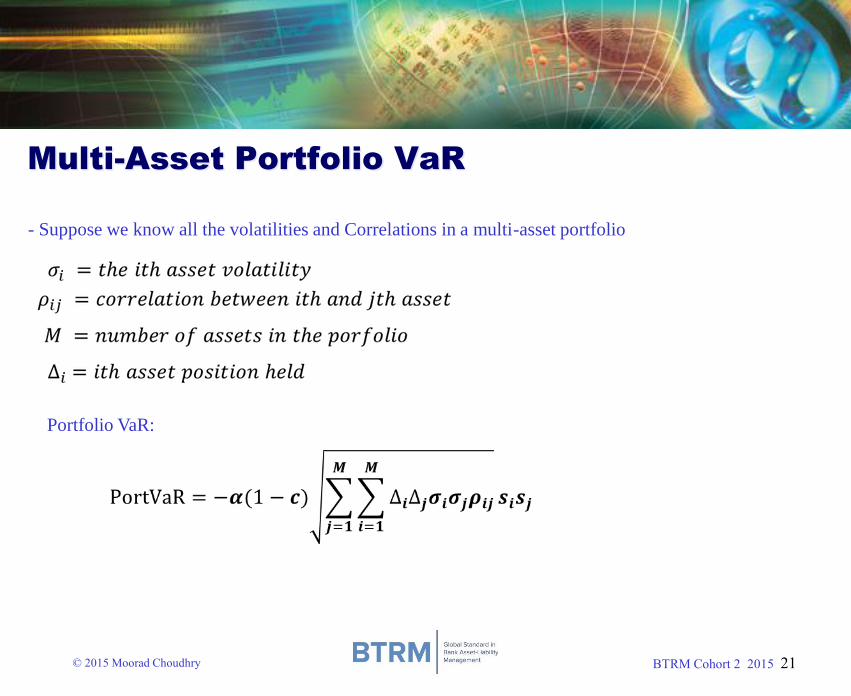

Multi-Asset Portfolio VaR

- Suppose we know all the volatilities and Correlations in a multi-asset portfolio

Portfolio VaR:

BTRM Cohort 2 2015 22© 2015 Moorad Choudhry

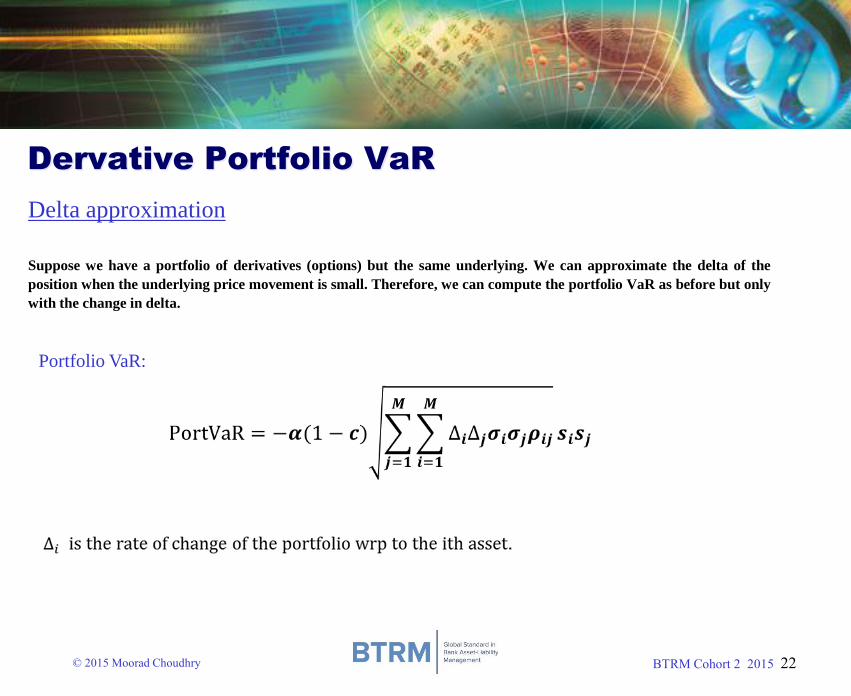

Dervative Portfolio VaR

Delta approximation

Portfolio VaR:

Suppose we have a portfolio of derivatives (options) but the same underlying. We can approximate the delta of the

position when the underlying price movement is small. Therefore, we can compute the portfolio VaR as before but only

with the change in delta.

BTRM Cohort 2 2015 23© 2015 Moorad Choudhry

Excel Calculations.

BTRM Cohort 2 2015 24© 2015 Moorad Choudhry

For discussion

What are the issues associated with understanding and “using” VaR in

the right way?

How did VaR as an estimation tool perform with respect to the 2008

crash and the JPMorgan “London Whale” episode?

BTRM Cohort 2 2015 25© 2015 Moorad Choudhry

References

John C Hull, “Options Futures and Other Derivatives”, 5th edition, 2003

Wilmott, P. “Paul Wilmott introduces quantitative finance.2001

Philipe Jorion, “Value at Risk”, 2nd edition, McGraw-Hill , 2001

Comments, any questions from this lecture or more information about full introduction to mathematical finance

lecture(s), please email me: [email protected]

BTRM Cohort 2 2015 26© 2015 Moorad Choudhry

DISCLAIMER

The material in this presentation is based on information that we consider reliable, but we do not

warrant that it is accurate or complete, and it should not be relied on as such. Opinions expressed

are current opinions only. We are not soliciting any action based upon this material. Neither the

author, his employers, any operating arm of his employers nor any affiliated body can be held liable

or responsible for any outcomes resulting from actions arising as a result of delivering this

presentation. This presentation does not constitute investment advice nor should it be considered

as such.

The views expressed in this presentation represent those of Abukar Ali in his individual private

capacity and should not be taken to be the views of any employer or any affiliated body, including

Abukar Ali as an employee of any institution or affiliated body. Either he or his employers may or

may not hold, or have recently held, a position in any security identified in this document.

This presentation is © [Abukar Ali] 2015. No part of this presentation may be copied,

reproduced, distributed or stored in any form including electronically without express written

permission in advance from the author.