valuing google © james dow, 2009 do not distribute without permission

Post on 21-Dec-2015

219 views

TRANSCRIPT

Valuing Google

© James Dow, 2009Do not distribute without permission

1996: Stanford

Sergey Brin and Larry Page are PhD students in computer science at Stanford University. They are working on a project to develop a better search engine.

Initial Funding

In 1998, Andy Bechtolsheim, co-founder of Sun, gives them a check for $100,000.

They incorporate in September 1998.

1999: $25 million from Sequoia Capital and Kleiner, Perkins, Caufield and Byers.

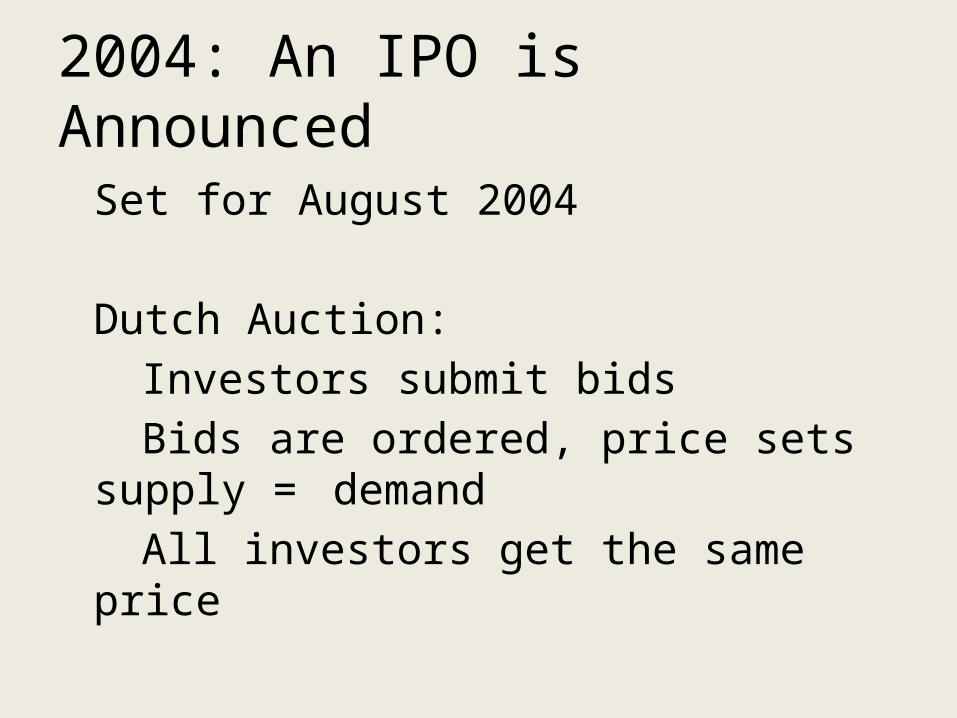

2004: An IPO is Announced

Set for August 2004

Dutch Auction:Investors submit bidsBids are ordered, price sets supply =

demandAll investors get the same price

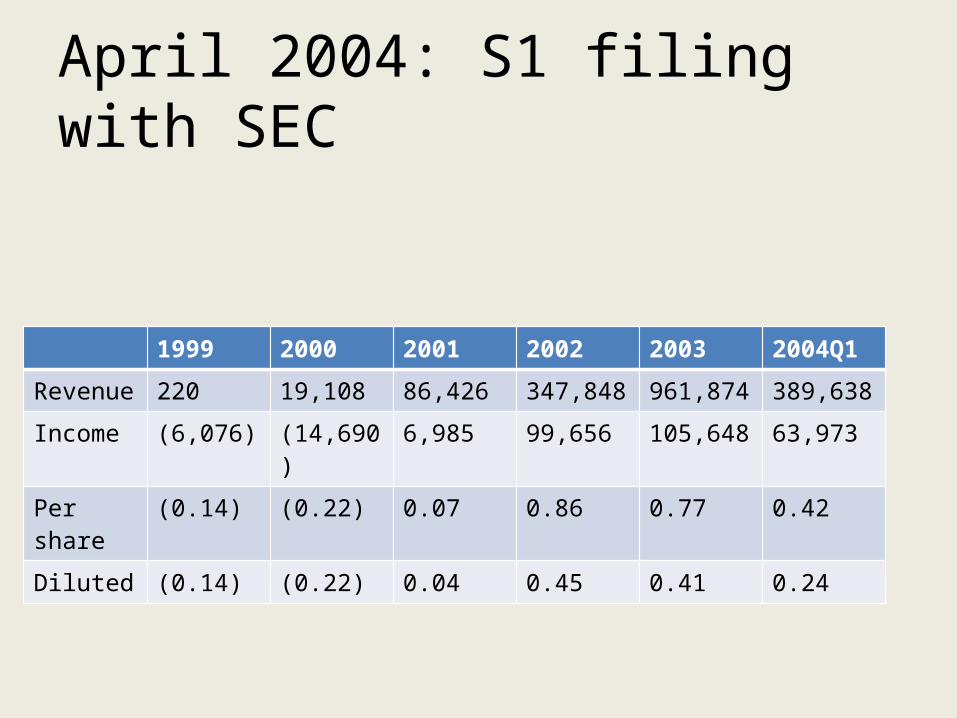

April 2004: S1 filing with SEC

1999 2000 2001 2002 2003 2004Q1

Revenue 220 19,108 86,426 347,848 961,874 389,638

Income (6,076) (14,690) 6,985 99,656 105,648 63,973

Per share (0.14) (0.22) 0.07 0.86 0.77 0.42

Diluted (0.14) (0.22) 0.04 0.45 0.41 0.24

How to forecast the rest of 2004?2003 2003Q1 2004Q1

Revenues 961,874 178,894 389,638Income 105,648 25,800 63,973Per Share 0.77 0.20 0.42Diluted 0.41 0.10 0.24

(2004Q1) x (4)

2004

1,558,552

255,892

1.68

0.96

(2004Q1) x (2003) (2003Q1)

2004

2,094,998

261,962

1.62

0.98

Actual

2004

3,189,223

839,553

2.07

1.46

Google vs. YahooGoogle 2000 2001 2002 2003 2004 (actual)

Revenue 19,108 86,426 439,508 1,465,934 3,189,223

Net Income (14,690) 6,985 99,656 105,648 399,119

Per Share(d) (0.22) 0.04 0.45 0.41 1.46

Yahoo 2000 2001 2002 2003 2004 (actual)

Revenue 1,110,178 717,422 953,067 1,625.097 3,574,517

Net Income 70,776 (92,788) 42,815 237,879 839,553

Per Share(d) 0.06 (0.08) 0.04 0.18 0.58

How do they compare in terms of revenue?

How do they compare in terms of profitability?

Pricing Google with P/E Ratios

Assume Google is just like Yahoo in 2004Yahoo shares sold for around $30Yahoo earned $0.58 per share

This gives a P/E ratio of 52$30/$0.58 = 52

Apply this to Google’s earnings of $1.46 per share.Google should trade for $76$1.46 x 52 = $76

What if we knew 2005?

Google earnings = $5.02 per share

Yahoo P/E (2004 price to 2005 earnings) = 24

At 24, Google price = $120 $5.02 x 24 = $120 At 52, Google price = $261 $5.02 x 52 = $261

What should you bid?

$76 based on 2004 information?

$120-$261 based on 2005 information?

Google’s “guidance” of $108-$135?

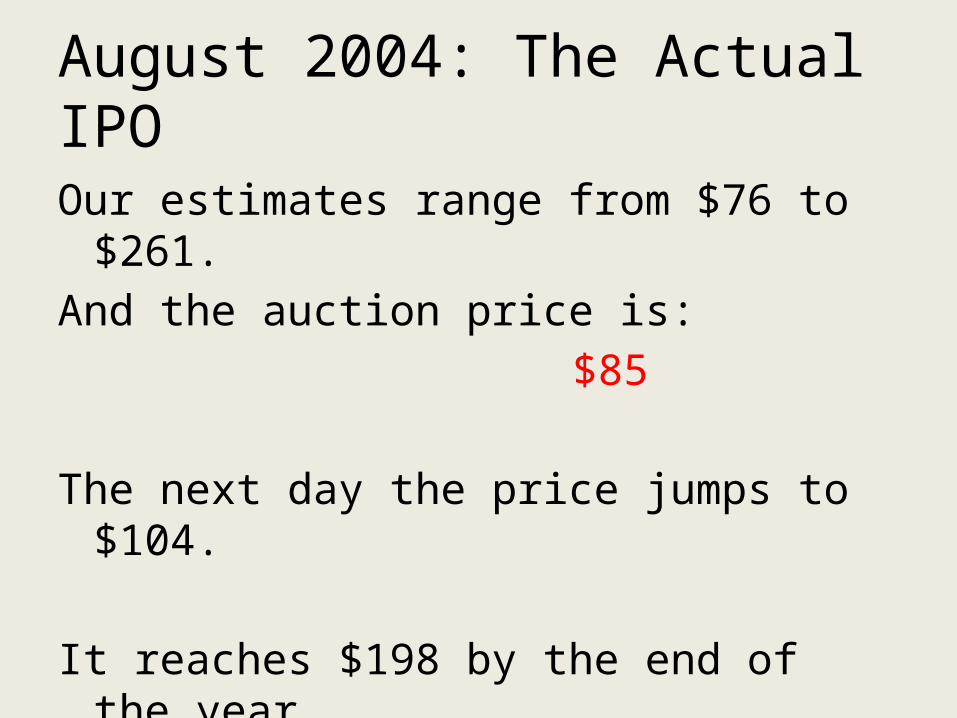

August 2004: The Actual IPO

Our estimates range from $76 to $261.And the auction price is: $85

The next day the price jumps to $104.

It reaches $198 by the end of the year.

What happened after 2004?Google Yahoo

2004 256% 222%

2005 243% 121%

2006 98% -22%

2007 34% -10%

2008 21% (est) 45% (est)

In 2008, Yahoo turned down an offer to be bought out by Microsoft and its continued existence as an independent firm is questionable.

Google is now the 15th largest company in the US by market capitalization.

Discounted Cash Flow

Why discounted cash flow?

Earnings do not grow at a constant rate. Google earnings grew 256% in 2004 34% in 2007

Using multiples assumes that other stocks are priced correctly.

The price of Yahoo fell in 2005 despite earnings more than doubling.

How to do it

Step 1: Estimate the cash flow for each year. At some point, assume constant growth.

Step 2: Determine the appropriate discount rate.

Step 3: Discount the cash flows and add them up.

Step 1: Estimate the cash flows

Year FCF Growth

2005 100%+

2006 100%+

2007 100%+

2008 ~90%

2009 ~70%

2010 ~55%

2011 ~44%

2012-2018 Down to Below 10%

2019 on 3%

Year EPS(d) Growth

2005 243

2006 98

2007 34

2008 21 (est)

Business Week, 2004 Actual

Slight of Hand

Earnings > FCF > Dividends

In long run they should grow together Not so much at the start

FCF hard for us to calculate

Handling the terminal value

Pick a growth rate (5%, 3%)

Value as a perpetuity

Discount to the present

Step 2: The Discount Rate

Base rate + risk premium

CAPM and Beta

BW: Beta of 2 and discount rate of 17.4%

Later, others use discount rates as low as 10%

Step 3. Present Value

E0= 1.46R= 0.174g= 0.05

Year 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 20141 2 3 4 5 6 7 8 9 10

Growth 243 98 34 21 15 10 5 5 5 5Earnings 5.01 9.92 13.29 16.08 18.49 20.34 21.35 22.42 23.54 24.72 Terminal Value

109.97 4.27 7.19 8.21 8.46 8.29 7.77 6.95 6.21 5.56 4.97 42.09

Sensitivity Analysis

Base price = $110

g = 0.03: price = $103

R = 0.15: price = $140

R = 0.10: price = $298

How do the values compare?

Actual price: $85 - $198

P/E estimates: $76-$261

DCF estimates: $103-$298

Warning

These are ballpark estimates.

If doing this for real you should be much more careful with the data.