usof the universal service obligation fund (usof) has assumed its statutory status in 2003 with the...

TRANSCRIPT

USOFUSOF

The universal service obligation fund (USOF) has assumed The universal service obligation fund (USOF) has assumed its statutory status in 2003 with the amendment to IT Act its statutory status in 2003 with the amendment to IT Act

1885.1885.USOF is a non-lapsable fund with effect from 01.4.2002.USOF is a non-lapsable fund with effect from 01.4.2002.The Rules have been framed and notified on 26.3.2004. The Rules have been framed and notified on 26.3.2004.

vide IT (Amendment) Rules 2004 The Gazette of India vide IT (Amendment) Rules 2004 The Gazette of India Extraordinary Part II-section 3-sub-section(i).Extraordinary Part II-section 3-sub-section(i).

Definitions-ITR 523Definitions-ITR 523

• Fund means the Universal Service Obligation Fund established under sub-section( I) of section 9A.

• Administrator means the Administrator of the Fund appointed by the Central Government of India for the administration of the Fund.

• Capital cost means the capital expenditure incurred on providing access as may be determined by the Administrator.

• Capital recovery means the aggregate of depreciation, interest on debt and return on equity on the capital cost annualized over a period of seven years.

• Net cost means operating expenses plus Capital Recovery minus Revenue.

• Operating expenses means the annual op-cost incurred on o&m of the specified facilities as may be determined by the Admin.

ContdContd

• Revenue means the annual charges including usage charge and rental from the specified service, without any deduction of any kind whatsoever except taxes relating to the specified service, if any, paid to the Government.

• USO means the obligation to provide access to basic telegraph services to people in the rural and remote areas at affordable reasonable prices.

• USP means the person who has entered into an Agreement with the Administrator for the purpose of implementation of USO.

• VPT means the first public telephone installed in a village.

What are the powers of What are the powers of AdministratorAdministrator

• Formulate bidding procedure/terms and conditions

• Evaluate the bids called for,• Enter into agreement with USP.• Settle the claim of USP after due verification.• Specify relevant formats, procedures and

records to be maintained and furnished by the USP.

• Monitor the performance of the USP as per the procedure specified by him from time to time.

Scope of support from USOFScope of support from USOF

• Financial support from the Fund shall be provided to meet the NET COST of providing the specified USO as per the procedure specified by the Administrator from time to time, and the period for which such support shall be provided and the services covered shall be governed by an Agreement entered in to with the USP.

India USOF in Global ContextIndia USOF in Global Context

• The USOF of India is one the few operational USO Funds in the world.

• The USOF of India has one the more complex mandates of operational USO Funds.

• The USOF of India is one of the largest operational USO Fund in the world.

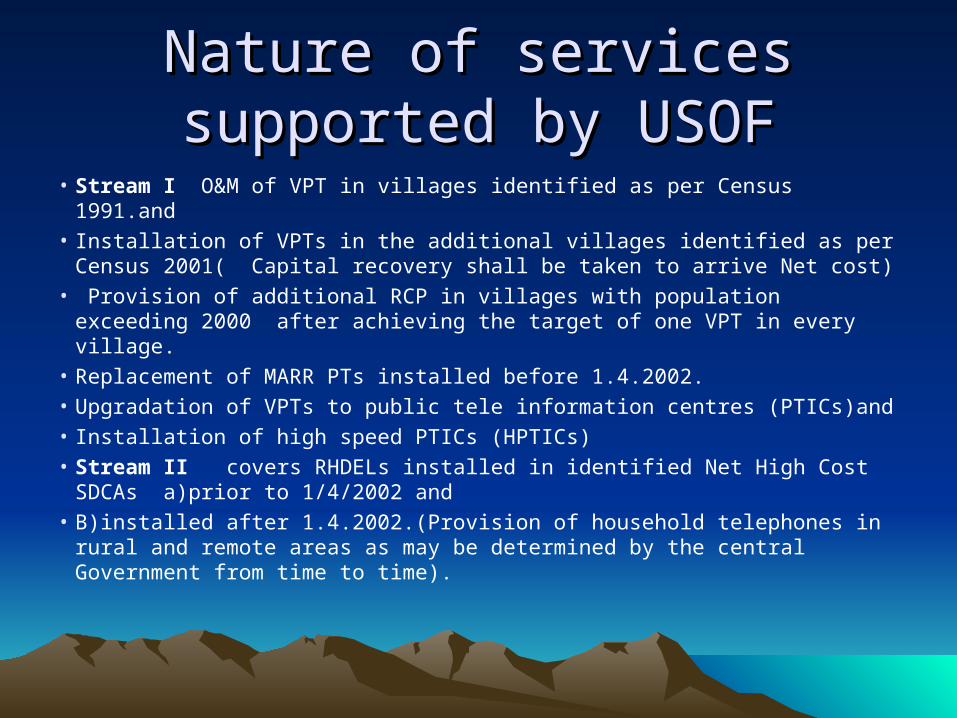

Nature of services supported by Nature of services supported by USOFUSOF

• Stream I O&M of VPT in villages identified as per Census 1991.and• Installation of VPTs in the additional villages identified as per Census

2001( Capital recovery shall be taken to arrive Net cost)• Provision of additional RCP in villages with population exceeding

2000 after achieving the target of one VPT in every village.• Replacement of MARR PTs installed before 1.4.2002.• Upgradation of VPTs to public tele information centres (PTICs)and • Installation of high speed PTICs (HPTICs)• Stream II covers RHDELs installed in identified Net High Cost

SDCAs a)prior to 1/4/2002 and • B)installed after 1.4.2002.(Provision of household telephones in rural

and remote areas as may be determined by the central Government from time to time).

Status of implementationStatus of implementation

• As a part of NTP-99 agreement signed with BSNL for 19 service area so far and six BSOs( basic service operator)

• Agreement signed with BSNL for replacement of 140210 MARR PTs installed prior to 1.4.2002

Date of effect(decentralisation)Date of effect(decentralisation)

• Date of effect is 1.10.2003

• O&m of VPTs for 2002-03 settled centrally

• Final settlement for 2002-03 and first quarter of 2003-04 will be settled centrally

• Decentralisation shall be effective from QE 31.12.2003 in r/o VPTs

USO MH circle MumbaiUSO MH circle Mumbai

• There are three USP’s in MH circle.

• M/S BSNL

• M/S TTML

• M/S RIL

Status of USP-M/s BSNLStatus of USP-M/s BSNL

• An agreement has been entered into with BSNL for provision and maintenance of VPTs,RCPs,Un-covered villages andRHDELs.

• As on 31.3.2006 the CB in respect of• VPTs--------------LL------WLL----- MARR-----• RCPs• Uncovered• RHDELs

USP-M/s TTMLUSP-M/s TTML

• Has been authorized to provide and maintain VPTs and RHDELs

• As on 31.3.2006 the CB of

• VPTs-----------LL------WLL-----GSM-------

• RHDELs

Status of USP-M/s RILStatus of USP-M/s RIL

• Has been authorised to provide and maintain RCPs and RDHELs.

• As on 31.3.2006 the CB of

• RCPs-------------LL----------CDMA----

• RHDELs

What are the obligations on the part What are the obligations on the part of USPs of USPs

• To provide telephones at the revenue villages/Rural areas as per Census 1991/2001 as the case may be as per agreement.

• To maintain those telephones and provide fault free service

• To submit claim on quarterly within 30 days from the date of closure of quarter.

• To submit claim duly singed by authorized person along with required documents.

• To certify that the claim has been submitted only for the lines installed and maintained as per agreement

• Certify that claim has been prepared at the approved rate after deducting for non-working period.

Check list for acceptance of claims Check list for acceptance of claims on submissionon submission

• The claim is received within time and in the prescribed format

• An affidavit in the prescribed proforma and a stamped pre-receipted bill are given

• Initials of authorized person are available on all pages of claim and consolidation sheet etc

• Hard copy and soft copy on CD (in read only form)

Action to be taken for non-receipt of Action to be taken for non-receipt of claimsclaims

• The claim should be submitted within 30 days of the end of a particular quarter

• Write to USP for submission within 15 days along with valid reason for delay

• On receipt of claim within 45 days inform USP that the final settlement is subject to condonation of delay by the Administrator

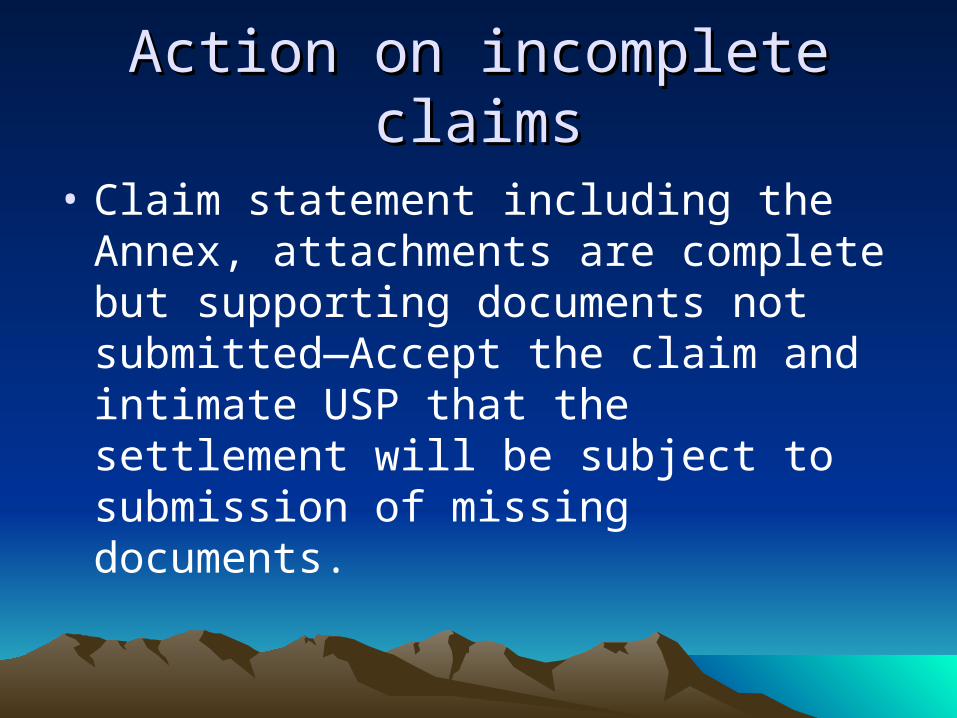

Action on incomplete claimsAction on incomplete claims

• Claim statement including the Annex, attachments are complete but supporting documents not submitted—Accept the claim and intimate USP that the settlement will be subject to submission of missing documents.

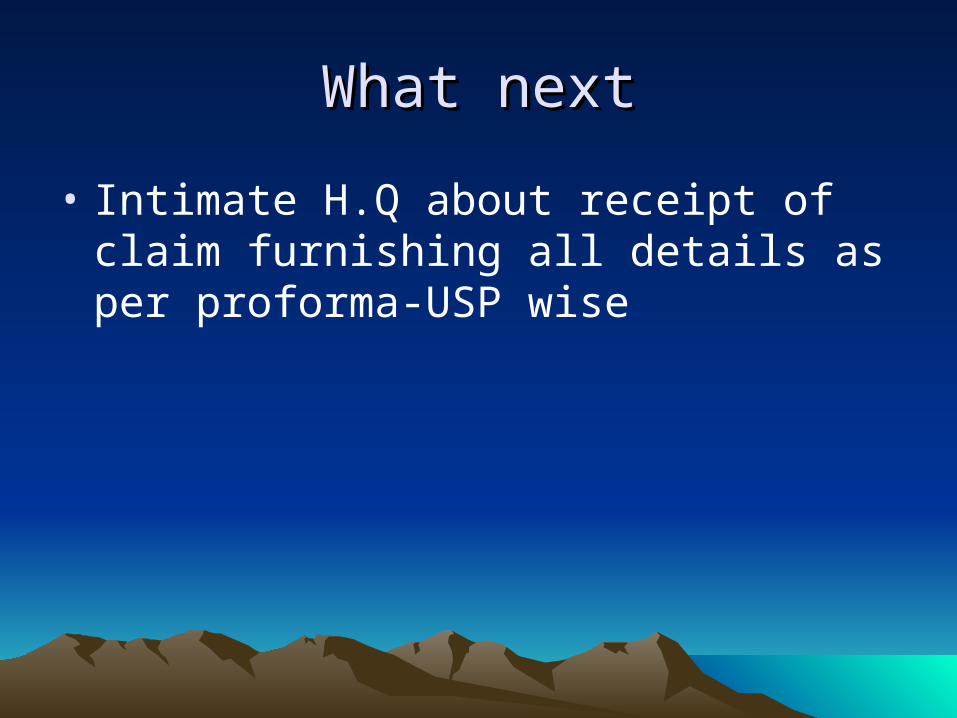

What nextWhat next

• Intimate H.Q about receipt of claim furnishing all details as per proforma-USP wise

Check list for settlement of claimsCheck list for settlement of claims

• Condition 18.2 subsidy be disbursed within 30 days of the commencement of the following quarter for vpts subject to---

• Condition 18.3 USP submit claim in the format prescribed along with Affidavit

• Condition 18.4 USP statement be audited by their auditor

• Condition 18.5 deduction for non working period• Condition 18.6 stamped pre-receipted bill• Condition 18.10 MARR VPTs on replacement shall not

eligible for subsidy from the date of replacement.

Verification of claimsVerification of claims

• Hard copy and soft copy of the claims matches. otherwise hard copy be taken as authentic

• Representative rates of the SSAs and SDCAs as the case may be

• Names of SSAs matched as per claims and agreement

• No:of days taken correctly ie 90/91/92 as the case may be

•

contdcontd

• Consolidation sheet:• Total no:of VPTs/RCPs/Rural DELs preferred

and new installation under different tech.tallies with the figure shown

• OB tallies with CB of previous quarter• Deduction for fault period (VPTs) ie

proportionate deduction for >7 days to <45days and beyond 45 days no subsidy—effective from quarter beginning 01.10.2003(includes both days ie from and to)

ContdContd

• No incremental metering and DNP shown for entire quarter – not eligible for subsidy

• Date of installation /replacement should be shown in DD/MM/YYYY

• In case of replacement of VPTs other than MARR ie LL to WLL – the representative rate of the existing or new tech whichever lower is payable

Disbursement of subsidyDisbursement of subsidy

• Payable in arrears by cheque (quarterly) after adj; if any• Head of account :FY 2004-05 onwards minor head 103

—Compensation to service provider for USO• Eg:• Dr 3275-00-103 (TACT Code)---Rs XX Cr 8670

(Cheques and Bills)---------Rs XX• After disbursement the corresponding aomunt will also

be booked as deduct entry under the head 3275 00 902—Deduct amount met from USOF by debiting the Head 8235 00 902—USOF as follows

• (-) Dr 3275-00-902 (TACT code 1508) (–Rs XX)• Dr 8235-00-118 (TACT code 2821)-------Rs XX • Refer Proforma C, Enclosure I of chapter VII

Action on transactions relating to Action on transactions relating to USOFUSOF

• Payments are made within a week of receipt of Authorization from USOF

• In case of short payment, the balance amount is surrendered to H.Q

• Payments made are not in excess of allotment

• USO subsidy are booked correctly under the concerned accounting Heads

Maintenance of recordsMaintenance of records

• The following records needs to be maintained at CCA office

• 1.Claim submission register

• 2.Subsidy disbursement register

• 3.Subsidy booking register

• Refer proforma A,B & C of Enclosure I to chapter 7

Submission of returns to USOF HQSubmission of returns to USOF HQ

• Intimation of claim receipt

• Requisition of fund

• Refer enclosure I of chapter 6

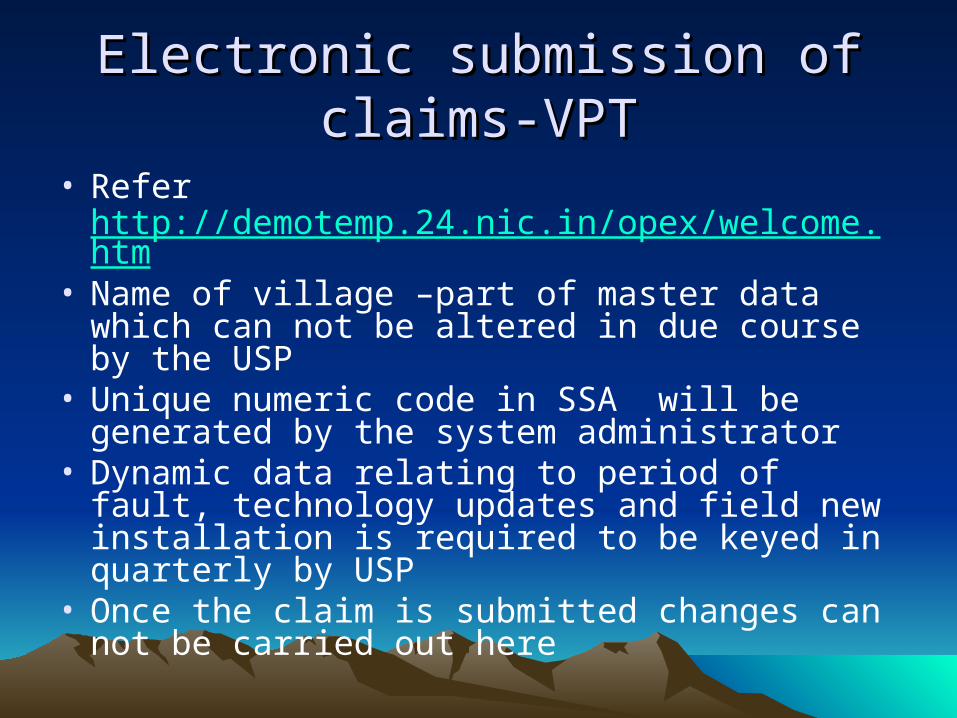

Electronic submission of claims-Electronic submission of claims-VPTVPT

• Refer http://demotemp.24.nic.in/opex/welcome.htm

• Name of village –part of master data which can not be altered in due course by the USP

• Unique numeric code in SSA will be generated by the system administrator

• Dynamic data relating to period of fault, technology updates and field new installation is required to be keyed in quarterly by USP

• Once the claim is submitted changes can not be carried out here

contdcontd

• The list of report available to CCA• Claim submission status• Consolidation sheet for individual SSA• Consolidation sheet for service area• VPT status at the end of quarter for service• Detailed claim statement of individual SSA• For more details refer chapter 5 of instruction

manual

Check list for monitoring of VPTsCheck list for monitoring of VPTs

• Technology used: subsidy rates differ –match with tech

• Installation date: after 1.4.2002—date of installation as per records should tally with claim statement

• Date of replacement of MAAR VPTs: upto one day prior to replacement at the rep rate of MARR and thereafter as per technology

• Duration of fault: upto 7 days no deduction, more than 7 days but less than 45 days proportionate and more than 45 days no subsidy for the quarter

contdcontd

• Sample size for monitoring: 5% of the numbers claimed SSA wise for all the SDCAs in the SSA ---during the year

• Each SSA should be visited for the purpose of sample check at least once a year

• The claim may be disallowed if the discrepancies are not rectified within a reasonable period

• Report on monitoring: as per format prescribed refer—enclosure I&II to chapter 8 of mannual

Powers of CCA vis-à-vis USPsPowers of CCA vis-à-vis USPs

• No action like suspension, revocation termination or extension of agreement as specified in part I, general condition shall be initiated by the o/o CCA against the USPs in terms of the conditions of the agreement and its amendments thereof.

Ref: VPT relatedRef: VPT related

• 1.File no .30-101/2002-USF(Vol-IV) dated 10.7.2003 @ inclusion of Aurangabad SSA& rep rate of MH circle. (MARR,LL,CDOT-PMP)

• 1A. File no 30-15/2002-USF dated 12.9.2003 @transfer of work relating to disbursement

• 2.File no:30-14/2002-USF dated 21.11.2003 @Outer limit for submission of claims

• 3.File no:30-111/2003-USF dated 24.11.2003 @rep rate for Wardha on GSM Tech

• 4.File no 30-107/2002-USF(Vol.IV) dated 25.11.2003 @on modification of condition no 18.6,part IV,Financial conditions—MARR replacement

contdcontd

• 5.File no:30-101/2002-USF(Vol.IV) dated 27.11.2003@ no subsidy for a VPT remaining non functional for any reason

• 6. File no 30-111/2003-USF dated 30.12.2003 @for subsidy support towards O&M---M/s TATA

• 7.same subject dt 12.3.2004 Inclusion of Latur• 7A.file no 30-15/2002-USF (vol.II) dated 5.2.2004

@transfer of work related• 8.File no 30-107/2002-USF Dated 21.10.2004

@Extension of time limit for replacement of MARR VPTs