using durable consumption risk to explain commodities returns - world...

TRANSCRIPT

Using Durable Consumption Risk to ExplainCommodities Returns

Deepa Dhume∗

Harvard University

November 11, 2010

Job Market Paper

Abstract

Commodities futures contracts have low correlations with market returns but highaverage returns. This is puzzling because the capital asset pricing model predicts thatassets that are uncorrelated with market returns will have low average returns. Applyingthe consumption-based capital asset pricing model does little to help, as commoditiesare also uncorrelated with nondurable consumption growth. In this paper, I show thatadding durable consumption growth to a multi-factor consumption-based asset pricingmodel can explain high commodities returns. Using a more comprehensive data setthan has been used in previous studies of commodities and asset pricing models, I showthat commodities returns covary strongly with durable consumption growth, which hasbeen shown to be an important driver of returns to other assets. Furthermore, sys-tematic durables risk can explain the cross section of returns to commodity portfoliossorted on the futures-spot spread, returns momentum, and spot price volatility. Finally,I demonstrate that commodities’ high durables risk may be explained by the businesscycle properties of commodities and durable consumption growth.

JEL Classifications: G12, G13, E21, E32, E44Keywords: asset pricing, commodity, futures, durable consumption

∗Department of Economics, Harvard University. Email: [email protected]. I am grateful toKenneth Rogoff and John Campbell for their invaluable guidance. I also thank Craig Burnside, MartinFeldstein, Jeffrey Frankel, Stefano Giglio, David Mericle, Gloria Sheu, Luis Viceira, and Motohiro Yogofor helpful comments and discussions.

1 Introduction

“Hogs, orange juice, sugar, and coffee.... It sounds like a breakfast menu as

investment plan, but it could be the best money you ever spend, particularly

if U.S. stocks continue to flounder. After all, breakfast is the most important

meal of the day.” – Jim Rogers, The Breakfast of Champions, July 3, 2002

Commodities have generated a lot of interest of late because of their high returns

and increasing importance as an asset class. Yet, returns to commodities are not

well understood or measured, and until recently, even the existence of positive returns

was debated. Given the deepening markets for commodities futures contracts and

the recent commodity price bubble, it is clear that understanding this asset class will

be helpful to both hedgers, who invest in commodities futures markets to balance

exposure to commodity price risk, and speculators, who invest in commodities futures

markets to make a financial gain. Whether or not Jim Rogers is correct to claim

that commodities are the investors’ breakfast of champions, understanding the risks of

commodities investments is as important as understanding the returns.

This paper makes three key contributions to the literature on explaining commodi-

ties returns using asset pricing models. First, I demonstrate that inclusion of durable

consumption growth as a factor improves the fit of multi-factor asset pricing models and

allows us to explain the time series and cross sectional characteristics of commodities

returns within a theoretically grounded model of systematic financial risk. Second, I

show that returns to portfolios of commodities sorted on known correlates of returns

are consistent with high durables risk. In the cross section of returns, commodities

with a low basis, high returns momentum, or high spot price volatility tend to have

higher covariance with durable consumption growth and higher returns. Finally, I show

that the high risk exposure of commodities returns to durable consumption growth may

be explained by the similar business cycle characteristics of commodities returns and

durable consumption growth.

This paper examines the return to buying a futures contract for 35 individual com-

modities over the period 1959 to 2008. On average, the index of all commodities has

earned 5.7% returns over the entire sample period. However, the return varies sub-

stantially across commodities, ranging from 22.9% per annum for propane futures to

negative 2.1% for zinc futures. By grouping commodities by type, we can see that the

portfolio of energy, animal, and metals commodities have each earned positive returns

1

of 6.1% or more, while agriculture and soft commodities have earned lower positive

returns.

To resolve the apparent contradiction between commodities’ high returns and low

correlation with equity markets, I demonstrate that the consumption-based asset pric-

ing model by Yogo (2006) is able to explain the high returns to commodities. The

model begins with an intertemporal household optimization problem with choices over

durable and nondurable consumption. When combined with portfolio choice theory,

the model predicts that the factors affecting marginal utility include nondurable and

durable consumption growth and returns to market wealth. Building upon this model,

previous empirical work has found that the inclusion of durable consumption growth

as a factor is able to explain the well-documented value premium in equity markets,

as well as the sizable returns to portfolios of high interest rate currencies (Yogo, 2006;

Lustig and Verdelhan, 2007).

The inclusion of durable consumption growth as a factor is the key to explaining

the high returns to commodities. According to the model, assets whose returns are

highly correlated with the factors affecting marginal utility should have higher returns

on average because they do not help investors hedge against downturns in consumption

growth and wealth. While commodities returns have low correlations with equity re-

turns and nondurable consumption growth, they exhibit strong correlation with durable

consumption growth. Therefore, the high returns to commodities we observe are in fact

consistent with the a multi-factor risk-based model, because they compensate the in-

vestor for exposure to durable consumption growth risk.

To test the prediction that assets with higher factor risk have higher returns, I first

estimate the model on portfolios of commodities grouped by type. To these 5 portfolios,

I add a broad cross section of potential assets in which an individual may choose to

invest, including 11 equity portfolios, 6 bond portfolios, 3 international indexes, and 6

currency portfolios. The results indicate that the model is able to predict the returns

to commodities. The generally high R2 (above 0.90) and low prediction error (less than

0.90 percentage points) indicate that the returns to commodities can be explained by

their levels of factor risk. Furthermore, the implied preference parameters of the model

are consistent with previous findings.

Given the success of the model in predicting commodities returns for portfolios

based on type, I next explore which characteristics of commodities may be driving

these returns and risk amounts. There is a long history in finance of grouping equities

into portfolios based on characteristics that successfully predict returns, including size,

2

book-to-market value, and industry type. Sorting assets into portfolios allows us to

study the relationship between the underlying sorting characteristic and asset returns

by eliminating the other idiosyncratic drivers of returns that can be diversified within

each portfolio. Motivated by recent work by Gorton et al. (2007), I focus on the

basis, the spot price volatility, and the return momentum as sorting characteristics for

commodities, to see whether portfolios formed on these characteristics have returns

that are predictable using standard asset pricing models. The results indicate that the

known high returns to low basis, high momentum, and high volatility commodities are

consistent with the high durables risk these portfolios have, both in the time series and

cross section of commodities returns.

While the model is able to measure factor risk and use it to predict commodities re-

turns, it does not provide an explanation for why commodities returns have a relatively

high covariance with durables consumption growth. To answer this further question,

I examine the business cycle properties of commodities returns. Gorton and Rouwen-

horst (2006) note that commodities returns behave differently than stock and bond

returns over the business cycle. Following their analysis of the full index of commodi-

ties and stock market returns, I add an examination of the business cycle properties of

the five commodities type portfolios and the consumption-based risk factors of durable

and nondurable consumption growth.

The results indicate that commodities follow a business cycle pattern similar to

that of durables consumption growth. While nondurable consumption growth and

market returns peak in early expansion, durable consumption growth and commodity

portfolios returns peak in late expansion. In addition, while nondurables and market

returns trough in early recession, durables and commodity portfolios trough in late

recession. According to the model, investors demand high average returns from assets

that pay poorly when marginal utility is high. Commodities have high returns on

average because they deliver low returns when durable consumption growth is low and

marginal utility is high.

There is little agreement in the literature about how to explain these high returns

to commodities. One issue is that the magnitude of average returns differs depending

on the sample period and the set of individual commodities included. However, recent

work has found that commodities have earned positive average returns over an extended

sample period including recent years. For example, both Gorton and Rouwenhorst

(2006) and Hong and Yogo (2010) find that an index of commodities earns high returns

3

with low variance when the sample period is extended to 2004 or later. However, there

is little agreement in the literature about how to explain these returns.

One strand in the commodities literature argues that commodities returns compen-

sate investors for systematic risk exposure within an integrated market. In support of

this view, Bessembinder and Chan (1992) show that many of the same variables that

have forecast power for equity and bond markets also have forecast power for agricul-

ture and metals futures markets. More recently, Bollinger and Kind (2010) have found

that the convenience yield, which is the benefit that accrues to the owner of a physical

inventory, can be explained by risk exposure to standard asset pricing factors such as

the returns to the S&P 500 index and an index of world government bonds.

While a number of papers have successfully linked commodities returns to systematic

financial risk, they have been unable to do so within the context of the Capital Asset

Pricing Model. According to the CAPM, assets which are highly correlated with market

returns should have high returns on average. In contrast, assets which have a low

correlation with market returns tend to have low returns, because they provide a hedge

for investors and reduce portfolio volatility. This model would predict that commodities,

which have high returns on average, have a high correlation with market returns. Yet,

we know that “commodities tend to zig when the equity markets zag” (Rogers, 2002).

Indeed, while the return to my index of 35 commodities futures is 5.7% per annum over

the sample period of 1959 to 2008, the empirical correlation coefficient between this

commodities index and a broad market index of equity returns is 0.07. Gorton and

Rouwenhorst (2006) similarly find that while their index of commodities has returns

comparable to those of equities, it also has a zero or negative correlation with equity

and bond returns over time.

Given these empirical facts, it is unsurprising that previous literature has found that

the CAPM is unable to explain the high returns to commodities (Bodie and Rosansky,

1980; Dusak, 1973). Using data covering fifteen years of corn, soybean, and wheat

futures, Dusak (1973) argues that commodities’ low returns and low correlation with

market wealth are consistent with the CAPM. However, this finding has not held up

over time as researchers have found that when studying more commodities and a longer

sample period, commodities continue to have a low correlation with market wealth but

earn high returns. In one such paper, using quarterly observations on 23 individual

commodities futures contracts between 1950 and 1976, Bodie and Rosansky (1980) find

a negative relationship between average returns and the market correlation for the cross

section of commodities. Finally, using data on prices for corn, soybeans, and wheat,

4

Jagannathan (1985) demonstrates that the consumption-based intertemporal CAPM is

rejected for commodities as well. However, in his conclusion he notes that one weakness

in his work is that his consumption data is limited to nondurable consumption due

to the difficulty of measuring the service flow from durable goods. He notes that if

durable goods are an important component of consumption, this data limitation could

be significant.

Because these efforts to explain commodities returns using systematic risk-based fac-

tors have met with only limited success, an older view of commodities as a segmented

market has sustained continued interest. Keynes’ Theory of Normal Backwardation

casts futures markets as a tool used by commodities hedgers to transfer risk to spec-

ulators. Since most hedgers are risk averse commodities sellers, they offer speculators

a futures price lower than the expected spot price in return for increased certainty.

Excess hedging pressure from commodity sellers can result in a futures price below the

expected spot price in equilibrium, which implies positive returns on average. However,

if speculators are risk neutral, they may bid up the futures price until it equals the

expected spot price, reducing returns to zero. The empirical finding of high returns to

commodities indicates that speculators require a positive return, or risk premium, for

assuming the exposure to spot price risk. Under the segmented markets theory, this

risk premium is impacted by commodity-specific variables such as the basis, inventory

levels, open interest, and hedging pressure.

A number of papers have tried to measure the relative importance of the two sets of

variables: the commodities-specific variables and the systematic financial risk variables.

Evidence for a segmented view of commodities markets can be found in Bessembinder

(1992), who shows that the returns to agricultural futures contracts are affected by

hedging pressure even after controlling for variables that measure systematic risk. Ad-

ditionally, Hong and Yogo (2010) show that open interest is a stronger predictor of

commodities returns than systematic risk variables such as the yield spread and the

short rate. They use this evidence to argue that market segmentation is an important

driver of commodities returns. In contrast, Etula (2009) highlights the broker-dealer

characteristic of risk-appetite to show that systematic risk factors can affect the willing-

ness of speculators to take on spot price risk, and so can affect the balance of hedging

pressure and the risk premium demanded by speculators in commodities markets.

This paper fills a gap in the literature on systematic financial risk in commodities

markets by demonstrating that a consumption-based asset pricing model can explain

commodities returns, as long as durable consumption growth is included as a factor.

5

By using a theoretically grounded model of household investment and portfolio alloca-

tion, it supports earlier findings that systematic financial risk is an important driver

of commodities returns. However, it also confirms earlier findings that the CAPM and

CCAPM are insufficient to explain commodities returns because it demonstrates that

including market returns, nondurable consumption, or even both of these as factors is

not enough to explain commodities returns without the inclusion of durable consump-

tion growth as a separate factor. Lastly, this paper also demonstrates that the finding

of systematic risk in commodities returns is consistent with the findings in the market

segmentation literature. In particular, it shows that commodities which have the prop-

erties that are well-known correlates of commodities returns, including low basis, high

returns momentum, and high volatility, also have high durables risk exposure.

The rest of the paper is organized as follows: In Section 2, I detail how commodities

returns are constructed from spot and futures prices and provide descriptive statistics

on the conditional and unconditional returns to investing in individual commodities

and portfolios. Section 3 outlines the Yogo (2006) model of household investment and

portfolio choice that results in the three factor consumption-based asset pricing model.

In Sections 4 and 5, I describe the time series and cross sectional results of the model

using commodities type portfolios and sorted portfolios. Section 7 demonstrates robust-

ness of the model and Section 8 explores the business cycle properties that may drive

the strong correlation between commodities and durable goods. Section 9 concludes.

2 Commodities Data

Despite the claim by Jim Rogers (2002) that investing in commodities could be “the best

money you ever spend,” returns to commodities are not well understood or measured.

While older literature finds mixed evidence for the existence of a risk premium, more

recent work has found that commodities have earned positive average returns over an

extended sample period including recent years. For example, Gorton and Rouwenhorst

(2006) find that an index of commodities earns high returns with low variance over the

period 1959 to 2004. Hong and Yogo (2010) find a similarly high mean-variance ratio

but use cash market spot prices, which can be unreliable. Before examining the ability

of asset pricing models to explain commodities futures returns, it is helpful to look at

the data sources and construction of commodities returns. In addition to descriptive

6

statistics, this section contains preliminary analysis of the size and predictability of

commodities futures returns.

2.1 Data Sources and Construction

A futures contract specifies on date t the quantity, quality, delivery location, and price

of a commodity to be traded on date t + h. While some commodities have contracts

expiring every month, others have contract months that are regularly spaced (every 3

months, for example) or irregularly spaced (7 months out of the year). A number of

recent papers have turned to the Commodities Research Bureau (CRB) for data on

these contracts (Gorton and Rouwenhorst, 2006; Gorton et al., 2007; Hong and Yogo,

2010). For each of these contracts, the CRB maintains a database that includes daily

prices on each contract from its opening to its expiration. This paper examines futures

contracts on 35 individual commodities that span a broad range of commodity types,

including grains, softs, metals, animal, and energy. While futures contracts became

available as early as 1959 for some grains, many futures markets did not begin until

much later. Crude oil contracts, for example, became available only in 1983, and rice

contracts began trading in 1986. Appendix A provides further details on commodities

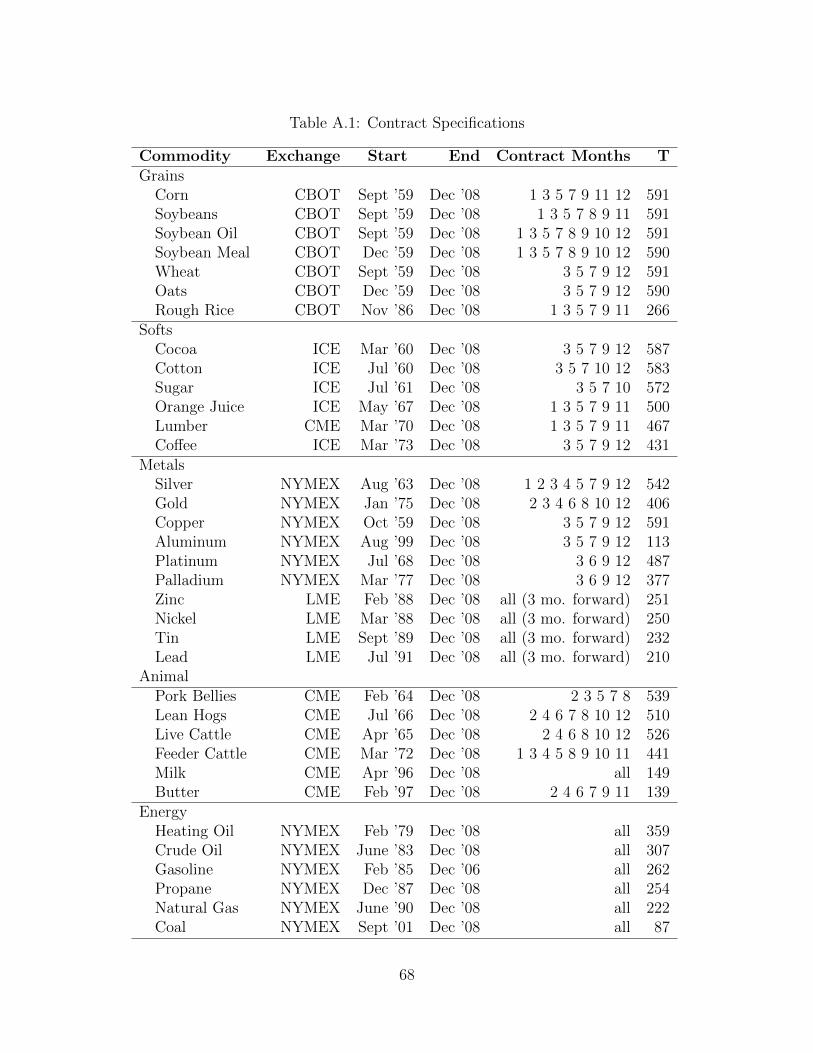

data availability and Table A.1 lists individual futures contract coverage, including the

exchange the contract is traded on, the start and end date for contract availability,

available contract months, and number of monthly observations.

Using daily price data on these individual futures contracts, I create monthly series

by extracting prices on the last trading day of each month. The monthly data for each

contract are then used to generate two main series for each commodity: a spot price

series and a 3-month futures series. While data on cash transactions are available for

most commodities, I follow Gorton et al. (2007) and use near-month futures prices as

spot prices instead. The spot price for a given month is therefore defined as the price on

the last trading day of the month for the near-month futures contract, i.e. the futures

contract which is the next to expire. Using the near-month futures price as a measure of

the spot price allows me to focus on the change in the futures price over time, unclouded

by other differences between futures and cash prices such as differences in transaction

or transportation costs, liquidity, delivery cost, or delivery location. Furthermore, since

the delivery window for a contract often overlaps with the final month of trading, the

near-month futures price should often be nearly equal to the spot price in the cash

market. One weakness in using near-month prices is that due to the irregular spacing

7

of commodities futures contracts, for a given commodity the near-month price may

reflect a contract that expires after a few months, rather than within a few days.

To extract data series for the 3-month futures price, I take the price on the last

trading day of the month for the contract which is next to expire 3 months in the

future. For example, the January 2005 price for a 3-month futures contract will be the

price on the last trading day in January 2005 of the contract that is next to expire on

the last trading day in April 2005. This contract may actually expire on the last trading

day of April 2005 or as late as May or even June, depending on contract availability

for that particular commodity.

Using these two variables, I construct three important series for the basis, the spot

return, and the excess (futures) return. The basis is defined as the percentage difference

between the contemporaneous futures and spot prices:

Basist ≡Ft,t+3 − St

St, (1)

where Ft,t+3 is the price on date t of the futures contract that is next to expire on date

t+ 3, and St is the spot (near-month) price on date t. The spot price return is defined

as the percentage difference between the current and lagged spot price:

SpotPriceReturnt ≡St − St−3St−3

. (2)

The spot price return is not a financial return that can be earned by an investor, because

an investor who holds a commodity over the period t−3 to t will pay a storage cost and

earn a convenience yield, which is the benefit earned by someone who holds physical

inventory of a commodity. Instead, the financial return that can be earned is the excess

return, which is defined as the percentage difference between the current spot price and

the lagged futures price:

ExcessReturnt ≡St − Ft−3,tFt−3,t

. (3)

We call this value an excess return because it measures the profit that can be made by

taking a long position in a futures contract at date t− 3 and holding the contract until

8

maturity at time t.1 While technically no money must change hands for an investor to

enter into such a contract, in practice, investors are often required to post margin on

these investments. Even so, this margin is generally in the form of Treasury bills, so

that the return as measured is still in excess of the risk free rate.

Often, we express these variables using the approximation that (X − Y )/Y ≈log(X)− log(Y ). Using lowercase letters to denote logs, we have:

ExcessReturnt ≈ (st − ft−3,t)

SpotReturnt ≈ (st − st−3)

Basist ≈ (ft,t+3 − st)

These approximations allow us to express the excess return as approximately equal to

the spot return minus the lagged basis:

(st − ft−3,t) = (st − st−3)− (ft−3,t − st−3) (4)

⇒

ExcessReturnt ≈ SpotReturnt −Basist−3 (5)

While this approximation helps us understand the relationship among these three vari-

ables, using log approximations for returns would require the additional step of adjusting

excess returns and portfolio aggregation by one half the variance of the returns. For

this reason, and because average simple returns are the relevant returns for investors, I

use average simple returns as expressed in equation 3 for all further estimations in this

paper.

2.2 Conditional and Unconditional Returns

To investigate the returns to investing in commodities, I examine excess returns for both

individual commodities and portfolios of commodities. Because patterns of returns can

differ widely across commodities, I aggregate commodities into portfolios based on

commodity type to better uncover common patterns. As a benchmark, Figures 1 and

2(a) depict the price index and returns for an equal weighted portfolio of commodities

1Given the structure of the futures contracts, the excess return will always be measured as thechange in price for the same contract over a horizon of 3 months. While these 3 months are intendedto be the last 3 months of the life of the contract, when there is a missing contract, the excess returnwill be measured as the 3-month return that occurs earlier in the life of the next contract to expire.

9

futures plotted against the same measures for a broad equity market portfolio.2 As the

figures show, the index of commodities futures prices has grown unevenly over time.

The commodities index has similar mean and volatility as the market portfolio, though

the two are not highly correlated.

Drawing heavily from analogous investigations in the exchange rate literature, here

I present results from two tests of forecast efficiency. The tests examine whether the

futures price Ft,t+3 is a good predictor of the future spot price St+3. Following Gilmore

and Hayashi (2008), I first perform an unconditional test, which examines whether

excess returns are statistically different from zero on average. Formally, I test:

H0 : Et

(St+3 − Ft,t+3

Ft,t+3

)= 0.

Because the overlapping forecast windows introduce serial correlation in the observa-

tions of the excess returns, the t-statistic is constructed using Newey-West heteroskedas-

ticity and autocorrelation consistent (HAC) standard errors with a maximum of 4 lags.

The results in Table 1 indicate that there are unconditional returns to investing

in commodities futures for only 8 of 35 commodities tested. While 28 commodities

have positive returns on average, the high variance of these returns prevents many

of these positive returns from being statistically significant.3 In contrast, once these

individual commodities are grouped into portfolios, we can see a stronger pattern of

positive unconditional returns. In Table 1, we can see that the index of all commodities

has positive significant returns of 5.7% per annum. In addition, the energy and animal

portfolios have significant unconditional returns of 14.3% and 6.2%, respectively, while

the metal portfolio has returns of 6.3% that are significant at the 0.10 level.

Secondly, I perform the conditional test of forecast efficiency, which examines whether

the lagged basis can be used to predict excess returns. Since excess returns are approxi-

mately equal to the difference between spot returns and the lagged basis, the hypothesis

that the excess return equals zero is equivalent to the hypothesis that the spot return

equals the lagged basis. For the conditional test, I estimate the Fama (1984) regression

2The broad equity market index is further described in Appendix C. Details on portfolios con-struction can be found in Appendix A and summary statistics for individual commodities and typeportfolios are provided in Tables A.2 and A.3.

3Unless otherwise stated, significance refers to statistical significance at the α = 0.05 level.

10

and perform the associated hypothesis tests:

SpotReturnt+3 = α + β(Basist) + εt+3 (6)

H0 : α = 0 & H0 : β = 1

Since the spot return equals the percentage change in the spot rate, we can think of this

as the gross return (before storage costs) to buying a commodity at time t, holding it,

and selling it at time t+ 3. This return should be equal to the gross return on buying

a commodity at time t and signing a futures contract at time t to sell the commodity

at time t+ 3.

The estimated parameter α is sometimes said to measure the non-time varying

risk premium, because under the assumption that β = 1, α measures the average

unconditional excess return. The hypothesis test H0 : β = 1 is called the conditional

test of excess returns because the trading strategy implied by the result is conditional

on the spot and futures prices at time t. For (α = 0, β < 1), investors should sell a

futures contract (take a short position) when Ft,t+3 − St > 0 to earn excess returns

(Ft,t+3− St+3)/Ft,t+3 at time t+ 3. Conversely, investors should buy a futures contract

(take a long position) when Ft,t+3 − St < 0 to earn excess return (St+3 − Ft,t+3)/Ft,t+3

at time t+ 3.4

The conditional test for excess returns focuses on the spot return and the basis as

the key variables. Here, I present results from the conditional test for the 35 individual

commodities in my sample, using daily price data and the maximum sample period

for each commodity. Results in Table 2 indicate that we reject H0 : α = 0 for 6

commodities, all of which have point estimates of α > 0. These results are a strong

indication of a positive excess return, or a non-time varying risk premium, for these

commodities on average. An additional 6 commodities reject H0 : α = 0 at the 0.10

level of significance, and all but 2 of the commodities have positive point estimates for

α.

While much of the analogous exchange rate literature tries to explain why estimates

for β are usually negative, this pattern does not hold for commodities. Rather, β is

between 0 and 1 for most commodities. The only negative point estimates for β are for

4 of the 10 metals (aluminum, platinum, palladium, and tin), which along with the β’s

4When α 6= 0, the trading strategy is almost the same, but the cutoff is no longer Ft,t+3 − St = 0.Instead, an investor should take a short position in commodities futures when Basist is large and takea long position in futures when Basist is small. The precise cutoff point for “large” and “small” isBasist = SpotReturnt+3, which is when Basist = α/(1− β).

11

for gold, lead, and copper are the seven lowest values for β. At the upper end, there

are 7 point estimates for which β is greater than 1, including 4 of 6 energy commodities

(crude oil, coal, propane, and gasoline). Overall, I reject H0 : β = 1 for 11 of the 35

commodities, including soybean oil, oats, rice, cocoa, lumber, coffee, copper, aluminum,

nickel, tin, and live cattle. The results provide statistical evidence of a time-varying

risk premium for these 11 commodities, and suggest that a time-varying risk premium

might exist for 8 additional commodities which have point estimates of β < 0.75 but

are not statistically significant.

To summarize, these results demonstrate statistically significant unconditional re-

turns to a number of commodities, and unconditional returns that are economically

significant (greater than 5%) though not statistically significant for an additional few

commodities. Furthermore, the conditional test of returns provides evidence that a

number of individual commodities have time-varying risk premia. Table A.2 indicates

that the correlation of returns across commodities can be low even within commodities

of the same type. Because shocks in one commodity market may not affect returns in

another, the potential to earn high returns with low volatility by investing in portfo-

lios of commodities is especially high. Indeed, the returns to portfolios of commodities

grouped by commodity type supports this hypothesis, as the grains, metal, and energy

portfolios earn positive significant returns, as does the index of all commodities. The

remainder of this paper investigates the extent to which these returns to commodity

portfolios may be associated with systematic factor risk.

3 Model of Household Consumption and Portfolio

Choice

In this section, I describe the consumption-based asset pricing model as developed by

Yogo (2006). In the model, an intertemporal household optimization problem with

choices over durable and nondurable consumption is combined with portfolio choice

theory. The resulting Euler equation is used to develop a linear factor model that is

estimated using two-step GMM.

12

3.1 Household’s Optimization Problem

The consumption-based asset pricing model derived by Yogo (2006) begins with a house-

hold optimization problem with a durable consumption good. In each period t, the

household purchases Ct units of a nondurable consumption good and Et units of a

durable consumption good. Pt is the price of the durable good in units of the non-

durable good. The nondurable good is entirely consumed in the period of purchase,

whereas the durable good provides service flows for more than one period. The service

flow from the stock of durables, Dt, is related to durables expenditure by the law of

motion:

Dt = (1− φ)Dt−1 + Et, (7)

where φ ∈ (0, 1) is the depreciation rate. Each period, the representative household

maximizes a utility function of the CES form:

u(C,D) = [(1− α)C1−1/ρ + αD1−1/ρ]1/(1−1/ρ), (8)

where α ∈ (0, 1) is the weight on durables and ρ ≥ 0 is the elasticity of substitution

between nondurable and durable consumption.

There are N+1 tradeable assets in the economy, indexed by i = 0, . . . , N . In period

t, the household invests Bit units of wealth Wt in asset i, which earns Ri,t+1 in period

t+1. The household’s intraperiod budget constraint requires that total saving in assets

equals household wealth minus that period’s expenditures:

N∑i=0

Bit = Wt − Ct − PtEt. (9)

The household also optimizes across time by maximizing intertemporal utility given

by the recursive function:

Ut = {(1− δ)u(Ct, Dt)1−1/σ + δ[Et(U

1−γt+1 )]1/κ}1/(1−1/σ), (10)

where κ ≡ (1− γ)/(1− 1σ). The parameter δ ∈ (0, 1) is the subjective discount factor,

σ > 0 is the elasticity of intertemporal substitution (EIS), and γ > 0 determines

the relative risk aversion. Finally, the intertemporal budget constraint describes the

13

evolution of household wealth:

Wt+1 =N∑i=0

BitRi,t+1. (11)

In sum, given wealth Wt and the stock of durable goods Dt−1, the household chooses

consumption and saving {Ct, Et, B0t, . . . , BNt} to maximize its utility (equation (10))

subject to the three constraints (equations (7), (9), and (11)).

After recasting this household optimization problem as one of portfolio choice, Yogo

derives the Euler equation:

Et[Mt+1(Rei,t+1)] = 0, (12)

where Rei,t+1 is the return to asset i in excess of the risk free rate5, and the stochastic

discount factor Mt+1 is the intertemporal marginal rate of substitution:

Mt+1 =

[δ

(Ct+1

Ct

)−1/σ(v(Dt+1/Ct+1)

v(Dt/Ct)

)1/ρ−1/σ

R1−1/κW,t+1

]κ(13)

where

v

(D

C

)=

[1− α + α

(D

C

)1−1/ρ]1/(1−1/ρ)

,

and RW,t+1 is the return on the market portfolio. According to the model, assets whose

returns are highly correlated with consumption growth and returns to market wealth

should have higher returns on average, because they have high returns when marginal

utility is low. Conversely, assets whose returns have low correlations with these factors

should have low returns on average, because they provide a good hedge during periods

of high marginal utility.

3.2 Estimating the Linear Factor Model

Yogo (2006) demonstrates that the above model can be approximated as a linear factor

model in nondurable consumption growth (∆ct), durable consumption growth (∆dt),

and market returns (rWt):

E[Reit] = b1Cov(∆ct, R

eit) + b2Cov(∆dt, R

eit) + b3Cov(rWt, R

eit). (14)

5In the case of commodities futures returns, Rei,t+1 is equal to the excess return on commodities asdefined in equation (3).

14

The risk prices b are a function of the preference parameters in the model:

b =

b1b2b3

=

κ[1/σ + α(1/ρ− 1/σ)]

κα(1/σ − 1/ρ)

1− κ

. (15)

Furthermore, this model can be estimated using two-step GMM. Define the vector of

factors, ft = [∆ct,∆dt, rWt]′, and its expectation µf = E[ft]. We can estimate the

model using the moment function:

e(zt, θ) =

[Ret −Re

t (ft − µf )′b(ft − µf )

](16)

and weighting matrices:

W1 =

[kIN 0

0 Σ̂−1ff

]and W2 = S−1,

where k > 0 is a constant and Σ̂ff is a consistent estimator of Σff , the variance-

covariance matrix of ft.6

The two-step GMM is solved using constrained linear minimization. Following Yogo

(2006), I impose two constraints on the risk prices that arise from their relationships

with the preference parameters of the model. Using Equation 15, we have that σ =

(1−b3)/(b1+b2), γ = b1+b2+b3, and α = b2/[b1+b2+(b3−1)/ρ].7 The first constraint,

that b1 + b2 + b3 ≥ 0, ensures that the risk aversion (γ) is nonnegative. The second

constraint, that b3 ≤ 0, ensures that the elasticity of intertemporal substitution (σ) is

nonnegative when b2 and b3 are nonnegative.8

The commodities returns in this and all further estimations of the linear factor model

are the excess returns as defined and constructed in Section 2 and as summarized in

Table A.2. The factors used in the estimation, which are described in detail in Appendix

6The initial weighting matrix W1 puts equal weight on the first N moments. The constant k =[det(Σ̂ii)]

1/N is inversely related to the variance-covariance matrix of the initial values for the firstN moments. See Yogo (2006), Appendix C and Cochrane (2005), Chapter 13 for discussions of themoment function and choices for weighting matrices.

7Because α and ρ cannot be separately identified, I follow Yogo (2006) and use ρ = 0.79.8While the results indicate that the parameters are rarely constrained in the final solutions, the

restrictions do sometimes impact the initial values for the parameters, which are calculated as theconstrained OLS estimates of the coefficients of the linear factor model in equation 14.

15

C and summarized in Table A.4, are constructed following Yogo (2006) with only slight

modification. The monthly observations are converted to overlapping quarters to match

commodities returns, so that the return associated with a given month reflects the

market return or durable or nondurable consumption growth for the three months

leading up to and including that month. The mean return on market wealth is 4.9%,

with an annualized volatility of 15.9%. In contrast, the mean returns on nondurable

and durable consumption are 2.1% and 3.9%, and the volatilities are much lower at

1.1% each. Unsurprisingly, the correlation coefficient between nondurable consumption

and durable consumption is largest among the factors, at ρ = 0.28. The correlation

between nondurable consumption and wealth is somewhat lower (ρ = 0.19), and the

correlation for durable consumption and wealth is close to 0 (ρ = 0.03).

4 Testing the Model using Commodity Type Port-

folios

To estimate the linear factor model for commodities, I use portfolios of commodities in

order to diversify away some of the commodity-specific idiosyncratic risk. There are a

number of potential sorting characteristics for commodities, just as there are for equities.

While the next section will explore characteristics of commodity portfolios sorted on

the basis, returns momentum, and volatility, in this section I focus on commodity type

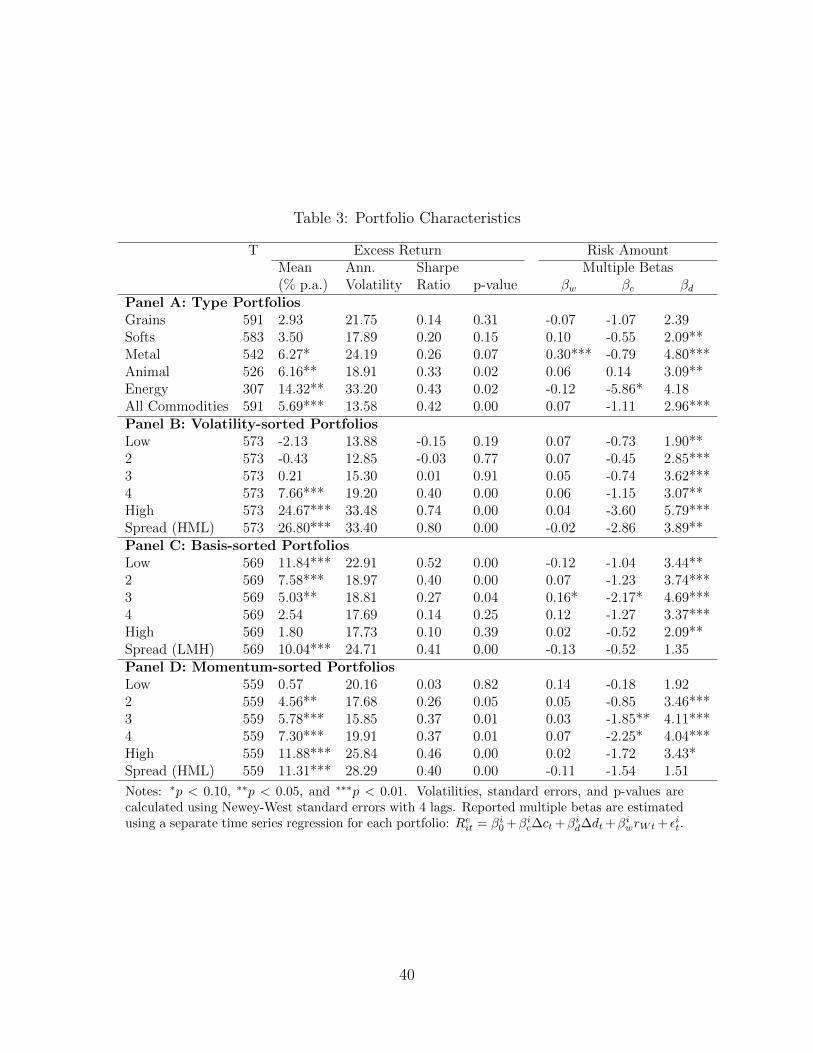

portfolios. Tables 3 and A.3 list summary statistics for commodity portfolios aggregated

by commodity type. The returns to these portfolios are examined in detail in Section 2.

Of the 5 type portfolios, energy commodities unsurprisingly have the highest average

excess return, at 14.3%, while grains have the lowest average excess returns, at 2.9%.

The full index of commodities has significantly positive returns of 5.7%. Given the high

volatility of individual energy commodities and high correlation across these contracts,

it is unsurprising that the annualized volatility of the energy portfolio is the highest, at

33.2%. In contrast, the low correlation across the full set of commodities reduces the

volatility of the index of full commodities to 13.6%. In Table A.4, we can see that over

the sample period 1959 to 2008, commodities have a higher return and lower volatility

than the return to the broad market index of equity returns.

16

4.1 Estimating Risk Exposure using Time Series Regressions

Before turning to the results of the linear factor model, I investigate the time series

properties of commodities returns by examining the multiple betas for each portfolio.

These multiple betas are estimated using a separate time series regression for each

commodity portfolio.9 The regression coefficients measure the amount of risk each

commodity has relative to each factor within the three factor model:

Reit = βi0 + βic∆ct + βid∆dt + βiwrWt + εit (17)

The magnitude and significance of the multiple betas for each commodity can indicate

which factors are most important in the asset pricing of commodities futures. The

number of observations for each regression depends upon the data availability for that

particular type portfolio, and ranges from 307 for energy to 591 for grains. As before,

I adjust for serial correlation using Newey-West standard errors with 4 lags.

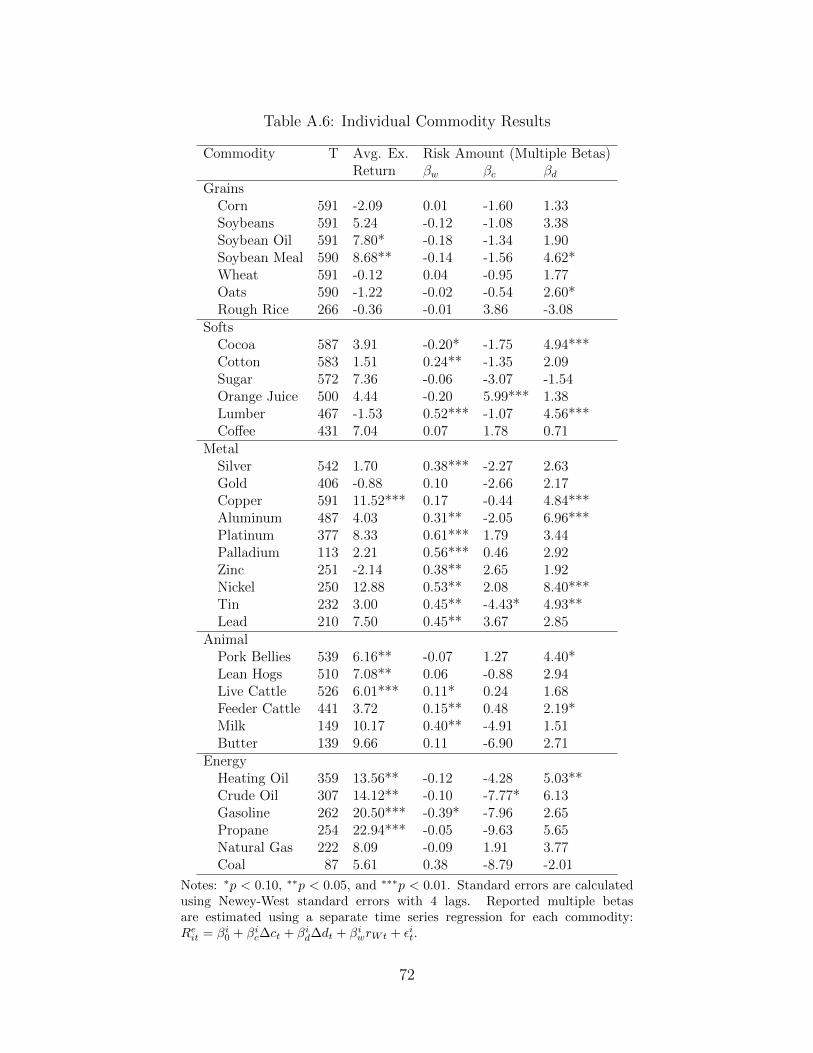

In Panel A of Table 3, we can see the first indication that durable consumption

growth is an important factor for commodities returns. For the index of all commodities,

we have a negative βc, and positive values for βd and βw. Of these, only βd is statistically

significant. The results for the five type portfolios also point to the importance of

durable consumption growth, as the estimate of βd is significant for the softs, metal,

and animal portfolios. Point estimates for βd are generally the largest in magnitude

as well, ranging from 2.09 for softs to 4.80 for metals. The only other statistically

significant factor beta is the market wealth beta for the metal portfolio (βw = 0.30).

However, there is no discernible pattern in market wealth risk, as the βw estimate is

negative for energy and grains portfolios and positive for softs, animals, and metals.

Finally, the results for the five type portfolios indicate that nondurable consumption

risk also differs quite a bit across commodity type, as the multiple beta for nondurable

consumption ranges from -5.86 for energy to 0.14 for animals.

9Though these multiple betas can also be estimated using the GMM estimation of the linear factormodel, the GMM estimates are affected by the choice of test assets used in the cross section and theprecision with which the GMM is able to estimate the population means of the factor returns. In orderto examine factor multiple betas which are free of these complicating factors, in this section I presentthe results from time series regressions instead.

17

4.2 Evidence and Evaluation for the Broader Cross Section

While examining the individual assets’ multiple betas helps us understand the amount

of risk exposure each asset has relative to the factors included, the linear factor model

allows us to determine how well these risk amounts and the estimated risk prices can

predict the average excess returns. In other words, the linear factor model allows us to

test the prediction that assets with higher betas and higher amounts of risk will have

higher excess returns.

In order to test whether this model can predict the returns of commodity portfolios,

I estimate the linear factor model using a broad cross section of potential assets in which

an individual may choose to invest. In addition to the 6 commodity portfolios, each

cross section may also include 6 Fama-French equity portfolios sorted on size and book-

to-market value, 5 equity portfolios sorted on industry characteristics, 6 bond portfolios,

3 indexes of international equities, and 6 foreign currency portfolios. A description of

portfolio construction and summary statistics for these assets can be found in Appendix

D.

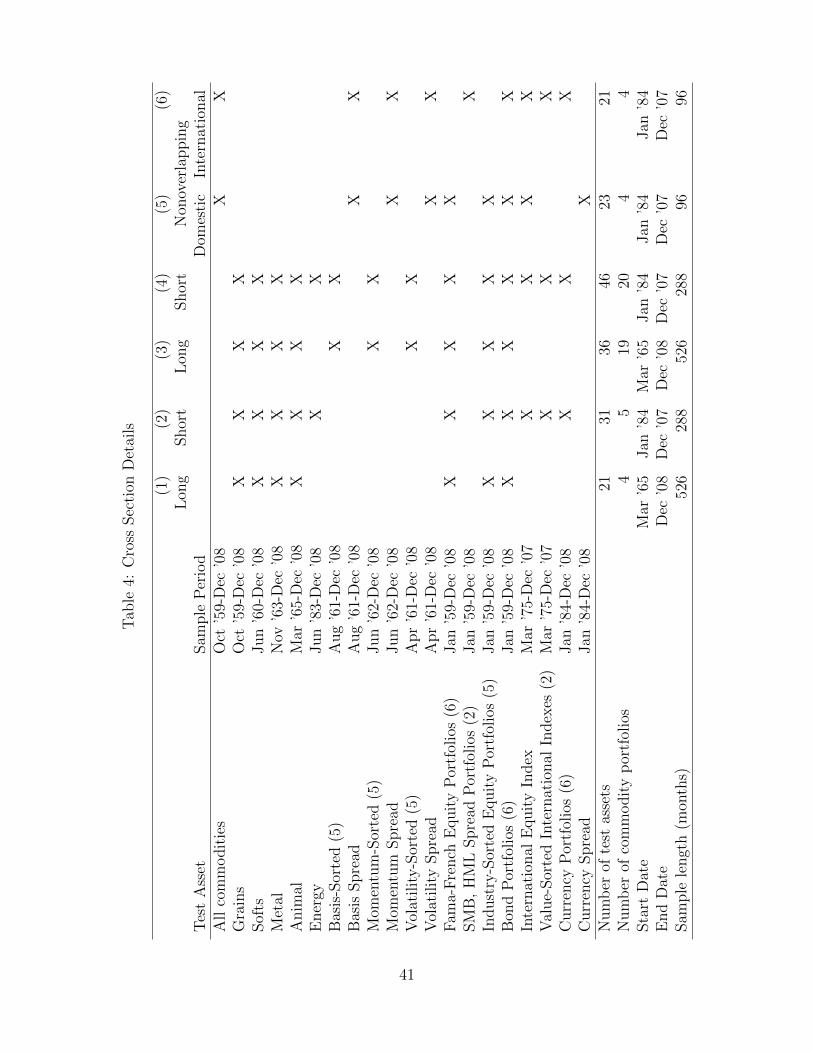

GMM estimation requires that all included test assets have data availability over

the entire sample period chosen. Therefore, a cross section that includes the energy

portfolio must be limited to the sample period June 1983 to December 2008, which

leaves over two decades of data on most other commodities unused. In order to make

maximum use of the data available, I therefore estimate the model on a long sample

that covers March 1965 (when the animal portfolio begins) to December 2008 and a

short sample that covers January 1984 to December 2007, when data on the energy

portfolio, currency portfolios, and international equities are available. For the long

sample, the set of test assets includes all test assets for which the data is available for

the entire sample period: the grains, softs, animal, and metals portfolios, the 6 Fama-

French portfolios, the 5 industry-sorted equity portfolios, and the 6 bond portfolios.

For the short sample, I add to these the energy portfolio, the 3 international indexes

and the 6 currency portfolios.

The cross sectional results of the model, which can be found in Table 5, demonstrate

that the model describes the data well. The first estimation with the long sample gives

positive significant risk prices for durable and nondurable consumption growth, but a

negative risk price for market wealth. The high R2 (0.88) and low mean absolute error

(0.87 percentage points) are based on first-stage estimates for the 21 test assets, and

are visible in Figure 3(a), which graphs the actual returns to each test asset against

18

the predicted return. Furthermore, the J-test of overidentifying restrictions does not

reject the model (p = 0.98). For the short sample, the estimated risk prices for durable

consumption growth and market wealth are positive and significant, while the risk

price for nondurable consumption growth is negative and significant. The J-test does

not reject this model either (p = 1.00), and the R2 is an even higher 0.93. Figure 3(b)

graphs the actual and predicted returns for the short sample estimation.

According to the theory, these estimated risk prices can be used to calculate the

values of the preference parameters of the model. For the long sample, the risk prices

imply an elasticity of intertemporal substitution (σ) of 0.01, a coefficient of risk aversion

(γ) of 167.68, and a weight on durables (α) of 0.35. In the short sample, the estimate

for the elasticity of intertemporal substitution is similarly low (0.01), while the estimate

for the weight on durables is higher than for the long sample (1.52). Additionally, in

the short sample, the estimate for the coefficient of risk aversion is lower than for the

long sample, but still high (48.96). Yogo (2006) explains that the high coefficient of

risk aversion is an expression of the equity premium puzzle, which is driven by the low

volatility of nondurable and durable consumption relative to asset returns.

These results indicate that the consumption-based asset pricing model including

durable and nondurable consumption growth can predict returns to commodity type

portfolios and a broad cross section of assets. This result is at odds with earlier pa-

pers on commodities, which found that asset pricing models were not able to explain

commodities returns. However, it is consistent with conventional wisdom in the fi-

nance literature that while factor models might perform poorly when trying to explain

differences among individual assets, they are generally more successful at explaining

differences in returns across broad classes of assets. By grouping commodities into

portfolios based on type and then including these assets with many assets of diverse

origin, I am able to estimate a consumption-based multi-factor asset pricing model that

successfully predicts commodities returns.

Furthermore, these results indicate that durable consumption growth is an impor-

tant factor in the pricing of commodity portfolios. In time series regressions, coefficient

on the durable goods factor has the largest magnitude and most significance for com-

modity portfolios, indicating a strong correlation between commodities returns and

durable consumption growth. In the cross section, while theory would predict all risk

prices to be positive, the risk price on durable goods is the only consistently positive

significant one. This positive risk price is consistent with the theory that durables con-

sumption growth is an important factor in explaining the cross section of asset returns,

19

because it indicates that assets with higher durables risk have higher returns. While

the high returns to commodities and low correlation with nondurable consumption and

equity returns was previously puzzling, these results demonstrate that the high returns

to commodities can be explained by their high durables risk.

5 Characteristics driving commodities returns

5.1 Theory, Motivation, Construction

Given the success of the model in predicting commodities returns for portfolios based on

type, I further investigate which characteristics of commodities may be driving these

returns and risk amounts. There is a long history in finance of sorting equities into

portfolios according to characteristics that can predict returns, including size, book-

to-market value, and industry type, as in the Fama-French test assets used above.

Sorting assets into portfolios allows us to study the relationship between the underlying

sorting characteristic and asset returns by eliminating the other idiosyncratic drivers of

returns that can be diversified within each portfolio. For example, equity portfolios that

are sorted on size should contain equities with similar distributions of book-to-market

ratios. Comparing these size portfolios, and especially the spread between the extreme

portfolios, allows us to focus on the risk-return tradeoff of the size characteristic. These

ideas have also been applied by Lustig and Verdelhan (2007), who explain the returns

to investing in currency futures by sorting currencies into portfolios based on interest

rate differentials.

To identify potential sorting characteristics for commodities, I draw on a broad set

of theories on commodities returns, backwardation, and the storage model. In partic-

ular, this work is motivated by Gorton et al. (2007), who examine the empirical link

between inventories and the risk premium. They demonstrate patterns of returns to

portfolios of commodities sorted on inventories and priced-based signals of inventories,

such as the futures basis, spot return momentum, and excess return momentum. How-

ever, they stop short of testing the relationship between these predictors of returns and

conventional asset pricing models. In this paper, I focus on spot price volatility, the

basis, and excess return momentum as sorting characteristics, to see whether commod-

ity portfolios formed on these characteristics have returns that are predictable using

standard asset pricing models.

20

The first characteristic I use for sorting is the spot price volatility. If we view the

return to buying a futures contract as a reward for taking on the risk associated with

future spot price volatility, then we should expect returns to increase in periods of high

volatility and high risk. Furthermore, if past volatility is a predictor of future volatility,

when we sort on past volatility, we should see an increase in excess returns for the high

volatility portfolios. If spot price volatility also covaries predictably with the factors in

the consumption-based model, then we would find predictable patterns in the returns

to volatility-sorted portfolios. To measure recent volatility, I calculate for the end of

each month the three month coefficient of variation, which equals the variance of the

daily spot prices over the previous three months divided by the mean of these daily spot

prices. Finally, I sort commodities each month into five portfolios using the demeaned

value of recent spot price volatility.10

Given the focus on the basis as a predictor of spot returns in the Fama (1984)

regression (equation (6)), the basis is a natural choice for the second sorting character-

istic. More recently, Hong and Yogo (2010) and Gorton et al. (2007) have studied the

basis as one of the determinants of commodity returns and note that excess returns are

generally higher when the basis is low. They argue that a low basis is often a signal

of low inventories, which cause spot prices to rise more than futures prices. Since low

inventories can result in higher spot price risk, they also require higher excess returns.

By sorting commodities into portfolios using the basis, I measure the relationship be-

tween the basis and futures returns in a cross sectional, rather than time series, setting.

I construct the set of basis-sorted commodity portfolios by sorting commodities each

month using the demeaned monthly basis for each commodity.

The final sorting characteristic is returns momentum. In addition to being an im-

portant predictor of returns for equities, Gorton et al. (2007) point out that past returns

are likely indicative of unanticipated shocks to supply or demand. Since these shocks

may have lasting effects on prices and inventories, it is reasonable to think that past

returns, to the extent that they carry information about the state of inventories, will

be a good predictor of future returns. Indeed, Hong and Yogo (2010) and Gorton et al.

(2007) find high momentum commodities have higher returns. To capture the informa-

tion reflected in the history of excess returns, I construct a set of five portfolios sorted

on the demeaned value of the average of the previous twelve months of excess returns.

10Further details on portfolio construction can be found in Appendix B.

21

In addition to the five portfolios in each of the above sets, I add a sixth portfolio to

each set to measure the returns to a trading strategy that takes advantage of the spread

in returns across the extreme portfolios. For the basis sorted portfolios, this means going

long in the low basis portfolio and short in the high basis portfolio. For the momentum

and volatility sorted portfolios, it means going long in the high momentum/volatility

portfolio and short in the low momentum/volatility portfolio.

5.2 Summary Statistics and Time Series Properties of Com-

modity Portfolios

We can learn about the returns to these sorting characteristics by examining both the

average excess returns and the pattern of betas across the five portfolios. The trends

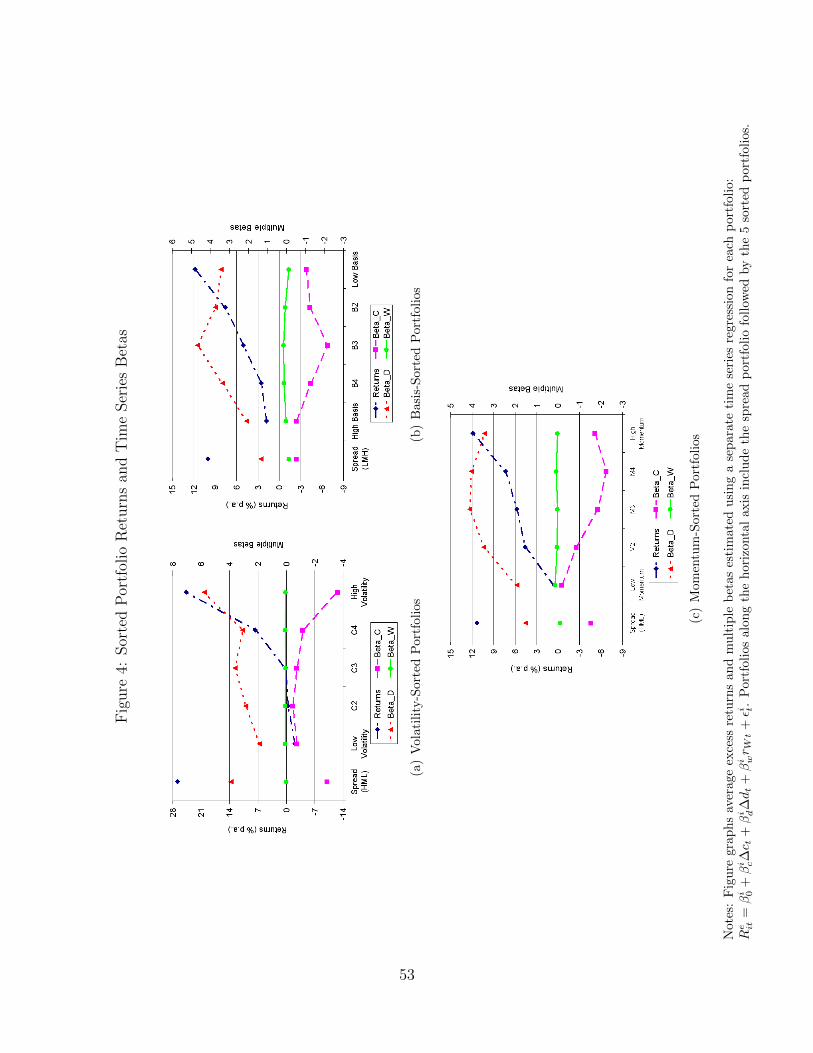

described in this section are visually represented by Figures 4(a)-4(c), which graph

the returns and time series betas for each portfolio. As shown in Figure 4(a), the

volatility-sorted portfolios indicate the patterns expected, with returns that increase

monotonically from the low volatility portfolio to the high volatility portfolio. The

high volatility portfolio has statistically significant returns of 24.7%, while the high-

minus-low portfolio generates a positive return of 26.8% and a Sharpe ratio of 0.80.

Looking at the pattern of betas across the 5 sorted portfolios in Panel B of Table 3

and Figure 4(a), it is clear that higher returns are consistent with higher durables risk,

as the positive, statistically significant values for βd increase with excess returns and

momentum. In other words, the returns to the high momentum portfolio covary more

strongly with durable consumption growth than the returns to the low momentum

portfolio. In contrast, the βw generally decrease with momentum, indicating that the

low momentum portfolio returns covary more strongly with returns to market wealth

than the high momentum portfolio returns. While none of the βw on the individual

portfolios is significant, the return to the high-minus-low portfolio, which measures the

spread in the returns to the momentum-sorted portfolios, is negative. Finally, the table

and figure show that βc does not vary consistently with the basis or returns.11

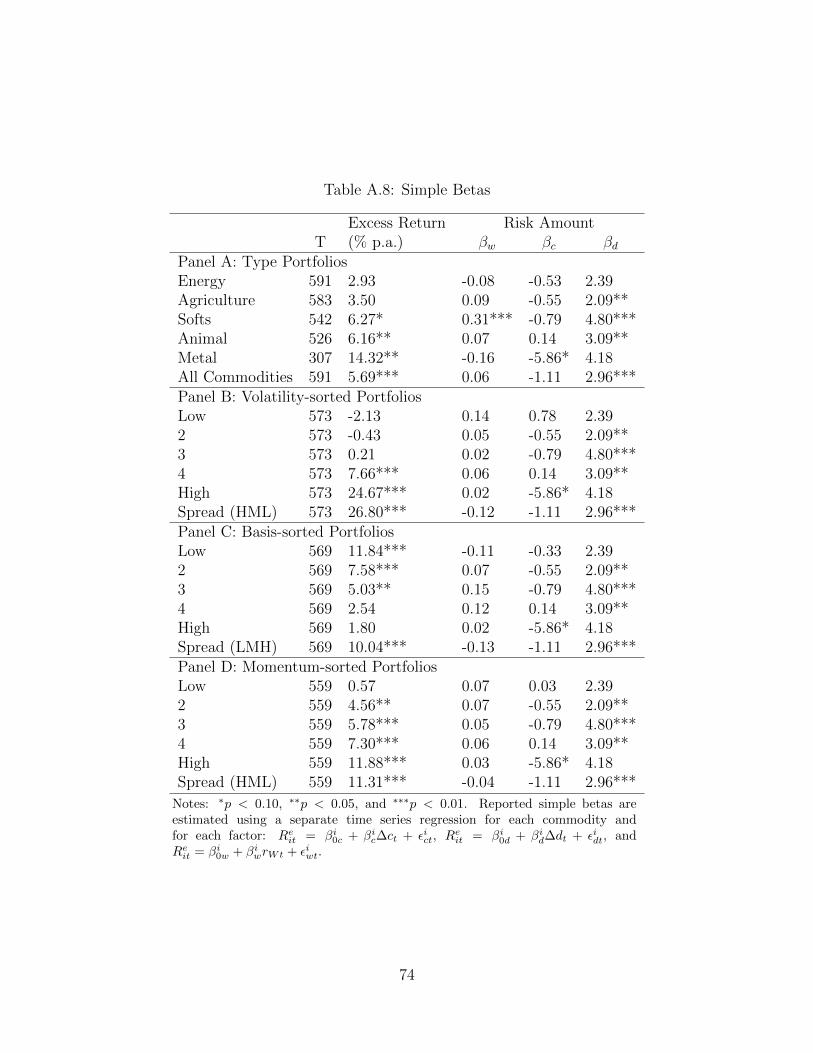

11Since nondurable and durable consumption are positively correlated, the multiple betas presentedhere could be quite different from simple betas calculated from univariate time series regressions.Simple betas are provided for in Table A.8 for comparison. While market and durables betas retainsimilar magnitudes and qualitative patterns, many nondurables betas are in fact positive in a univariatesetting where the durables factor is not included in the regression. However, since the nondurablesbetas still do not demonstrate a pattern of increasing with average returns across sorted portfolios,they remain unable to explain the cross section of commodities returns.

22

For the portfolios sorted on the basis, we can see in Panel C of Table 3 and Figure

4(b) that returns increase monotonically as the basis decreases, and the low-minus-high

portfolio has a significant positive return of 10.0%. Again, the pattern of exposure

to durable consumption risk is consistent with the pattern of returns, as βd generally

rises as the basis falls and returns increase. In addition, βd is the only positive beta

coefficient for the spread portfolio. In contrast, βc and βw are declining or U-shaped as

the basis falls, and are negative for the basis spread portfolio.

Finally, in looking at Panel D of Table 3 and Figure 4(c), which show the returns

and time series properties for the momentum-sorted portfolios, we have that returns

are monotonically increasing with momentum and are highest for the high momentum

portfolio. We also have that the values for βd are generally increasing with momentum,

while the values for βc and βw are lower for the high momentum portfolios. Finally,

we can see that for the spread portfolio, only βd is positive. All these results indicate

that for the momentum-sorted portfolios, high returns are again most closely associated

with high durables risk.

5.3 Cross sectional results for portfolios

I add these sorted commodity portfolios to the set of test assets and estimate the model

using the same long and short sample periods. The cross section of test assets used

now includes the full set of assets from the previous estimations as well as the 15 sorted

commodity portfolios (three sets of five sorted portfolios). The results in Table 5 show

that for both estimations, the risk price of durables remains positive and significant.

However, as in the estimations with only the type portfolios, the risk price on market

wealth is negative for the long sample, and the risk price on nondurable consumption

growth is negative for the short sample. As before, the models have high values for

the R2 (0.85 and 0.96) and low values for the mean absolute error (0.82 and 0.39). In

addition, neither of the models is rejected by the J-test of overidentifying restrictions.

Though these models fit the data well, the implied preference parameters are again

sometimes outside of the expected range. The elasticity of intertemporal substitution

is still close to zero (0.06 or lower), but within the expected range of σ ∈ (0, 1). While

the estimate for the weight on durables of 7.7 for the short sample is well outside the

expected range of α ∈ (0, 1), the estimate of 0.81 is within range for the long sample.

Finally, the coefficient of risk aversion γ is lower than in the estimations without the

sorted portfolios, but still very high (69.38 and 9.03).

23

A summary of these results is best represented by Figures 3(c) and 3(d), which plot

the realized average excess returns against the predicted average excess returns. While

the momentum and basis-sorted portfolios have returns that range from 1% to 12%

per annum, the realized returns for the volatility-sorted portfolios have a much larger

range, from -2% to 25%. Figure 3(c) illustrates that the model is able to accurately

predict this range of returns. Finally, Figure 3(d) demonstrates that the model also fits

well when using a short sample period.

6 Nested Special Cases and other Benchmark Mod-

els

The three factor model presented in Section 3 nests a number of well-known special

cases. In this section I present results for these linear factor models, each of which uses

only a subset of the three factors included in the main model and imposes corresponding

restrictions on the preference parameters of the model. I also present results for the

Fama-French three factor model as an additional benchmark. The results demonstrate

that durable consumption growth is an important factor in explaining the cross section

of asset returns.

Secondly, I present two robustness checks for the GMM estimations above. First,

in order to examine whether the risk prices change over time, I provide GMM esti-

mation using the same cross section of test assets over different sample periods. The

results indicate that while estimates of risk prices are not stable over time, the risk

price for durable consumption is the only one that is positive and significant in every

sample period. Finally, because consumption data may not be well-measured at the

monthly level, I present results using only nonoverlapping quarters. While data using

nonoverlapping quarters has the benefit of a lower autocorrelation across consecutive

observations, it also has the drawback of having a smaller number of observations in

the time series, which restricts further the number of test assets which may be included

in a sample of a given length. Even so, the results are consistent with those estimated

using overlapping quarterly data.

24

6.1 Nested Special Cases

The full three factor model presented in Section 3 nests a number of well-known asset

pricing models as special cases. Using the short cross section with sorted portfolios

(column 4 of Table 4), I present results for linear factor models which use one or two of

the three factors of the full model. The columns of Table 6 correspond to the following

special cases:

1. CAPM: The standard CAPM uses only market wealth as a factor. Preference

parameters are restricted such that b3 = γ, b1 = b2 = 0, σ = ρ, and σ →∞.

2. CCAPM: The consumption CAPM uses only nondurable consumption as a factor,

and restricts preference parameters to b1 = γ, b2 = b3 = 0, σ = 1/γ = ρ and α = 0.

3. DCAPM: The durable CAPM uses only durable consumption as a factor. Pref-

erence parameter restrictions are the same as those in the CCAPM, as this

model simply substitutes durable consumption growth for nondurable consump-

tion growth: b2 = γ, b1 = b3 = 0, σ = 1/γ = ρ and α = 1.

4. EZ-CCAPM: The Epstein-Zin CAPM uses nondurable consumption and market

wealth as factors. Once again defining κ ≡ (1 − γ)/(1 − 1σ), we have preference

parameter restrictions: b1 = κ/σ, σ = ρ, b2 = 0, and b3 = 1− κ.

5. CD-CAPM: The nonseparable expected utility model uses nondurable and durable

consumption as factors. Preference parameters are restricted such that σ = 1/γ,

b1 = γ + α(1/ρ− γ), b2 = α(γ − 1/ρ), b3 = 0, and ρ = 0.79 by assumption.

6. EZ-DCAPM: Results for the full three factor model are reproduced for ease of

reference. As before, b1 = κ[1/σ+α(1/ρ−1/σ)], b2 = κα(1/σ−1/ρ), b3 = 1−κσ,

and ρ = 0.79 by assumption.

Comparing the first three models which have one factor each, it is clear that the

durable CAPM has the most explanatory power. The durable CAPM is the only model

for which the R2 is higher than 0.9 and the mean absolute error is below 1%. The

relatively strong fit of the model can be seen in Figure 5(c) as compared to Figures

5(a) and 5(b). In fact, the durable CAPM with only one factor has a higher R2 and

lower mean absolute error than the EZ-CCAPM, which has nondurable consumption

and market wealth as factors.

25

Comparing the results of the DCAPM to the results in columns 5 and 6 of Table

6, we can see that the R2 falls from 0.985 to 0.977 and then rises to 0.991. Similarly,

the mean absolute error rises when the nondurable consumption factor is added, going

from 0.457 to 0.584, but then falls to 0.391 when the market returns factor is added.

When using a linear factor model to explain returns to a cross section of international

assets and commodity portfolios, these results indicate that once durable consumption

is included as a factor, the addition of nondurable consumption does not add much ex-

planatory power to the model. Additionally, these results indicate that adding durable

consumption to a model with only nondurable consumption and market returns as

factors does improve explanatory power.

One final important benchmark model is the three factor Fama-French model, which

uses market returns as well as the size and value spread portfolios as factors. The SMB

factor measures the spread in returns between equities with small and large market

capitalizations, while the HML factor measures the spread in returns between equities

with high and low book-to-market values. The results in column 7 of Table 6 show that

the three factor Fama-French model performs better than many of the nested mod-

els discussed above. However, it is outperformed by all models which include durable

consumption growth as a factor, including the one-factor DCAPM, the two-factor CD-

CAPM, and the full three-factor model with nondurable consumption, durable con-

sumption, and market returns.

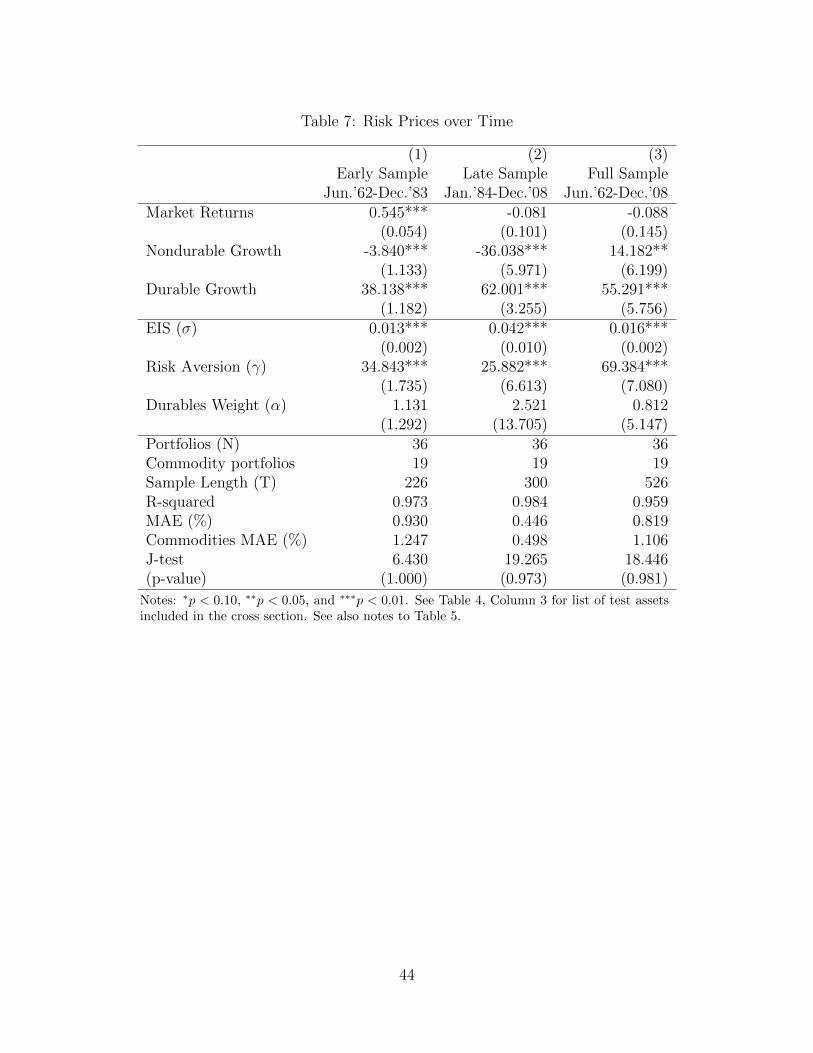

6.2 Risk Prices over Time

The cross sectional results in Table 5 show large differences in risk prices across the

four specifications. These differences could be due to either the inclusion of different

assets in each cross section or the different sample periods used for each estimation. In

order to further investigate whether the risk prices have changed over time, I estimate

the model using an early and late sample period for the same cross section.

Table 7 provides results using the set of assets that are available in the early sam-

ple period, which includes the domestic equities and bonds, and all the commodity

portfolios except for energy (column 3 of Table 4). In addition to the early and late

samples, the results for the full sample period are reproduced for ease of reference. The

estimated risk price for each factor differs across sample periods. While the changes in

parameter estimates may reflect changes in the actual risk price over time, they could

also reflect the difficulty in estimating the parameters using limited sample periods. In

26

fact, the full sample risk prices are not always an intermediate value between the two

short sample estimates. However, despite the inconsistency across sample periods, it

is important to note that the durables risk price is the only risk price that remains

significant and positive for all sample periods.

6.3 Nonoverlapping Quarters

In Table 8, I present results using nonoverlapping quarterly data. These cross sectional

estimates use the same long and short sample periods as in the estimates using over-

lapping quarterly data. However, while the cross section of test assets in the two long

sample estimations remain the same as before, the short sample estimations must be

adjusted. As noted by Burnside (2007), GMM estimation requires the number of test

assets to be relatively small compared to the sample length. When using nonoverlap-

ping quarters, the sample length for the short sample period is small (T=96), so the

cross section must be limited.

One way to limit the number of test assets is to use only the index of all commodities

rather than the 5 type portfolios. Additionally, I replace the 5 sorted portfolios for

each of the sorting variables with the spread portfolios (High-Minus-Low Momentum

and Volatility, and Low-Minus-High Basis). To demonstrate that the fit of the model is

robust to various choices in the cross section of test assets, I estimate the model on two

very different cross sections. The first is a set of primarily domestic test assets, which

adds to the 4 commodity portfolios the 6 Fama-French equity portfolios, 5 industry-

sorted equity portfolios, 6 bond portfolios, one index of international equities, and

one currency portfolio that measures the spread between high and low interest rate

currencies. The second cross section is an internationally focused one, and includes the

4 commodity portfolios as well as the Small-Minus-Big equity portfolio, the High-Minus-

Low equity portfolio, the 6 bond portfolios, 3 international indexes, and 7 currency

portfolios.

For these 4 estimations, the results are little changed from before. While the risk

price on nondurables and market wealth change signs for the long samples as compared

to the previous set of estimations, the risk price on durables remains positive and

significant for all 4 estimations. In addition, the R2 remains high (0.92 or higher),

and the mean absolute error remains roughly the same as before. The parameter

values remain of a similar magnitude: relatively small for the elasticity of intertemporal

substitution (hitting the lower bound of 0 for the short domestic sample), the coefficient

27

of risk aversion remains high, and the weight on durables is higher than the expected

range of α ∈ (0, 1). Finally, while the p-value for the J-test of overidentifying restrictions

falls to below 0.05 for the long sample with sorted commodity portfolios, the J-test fails

to reject the model for the other three estimations.

7 OLS Estimation and Out of Sample Tests

In this section, I present OLS estimates of the linear factor model. GMM estimation

has a number of advantages over OLS estimation. For example, using the moment

conditions in equation 16 allows the population means of the factors to be different

from their sample averages, and using the weighting matrix 3.2 and allows the moment

conditions to have different weights. However, the GMM estimates allow for the risk

amounts, or betas, to change at every period, inducting an extremely good fit for the

model. Additionally, the risk prices can be sensitive to small changes in estimation pro-

cedure, including choice of initial parameters or variance-covariance matrix estimator.

In contrast, the OLS estimation can provide results from a simpler procedure that is

also more comparable to a number of previous studies.

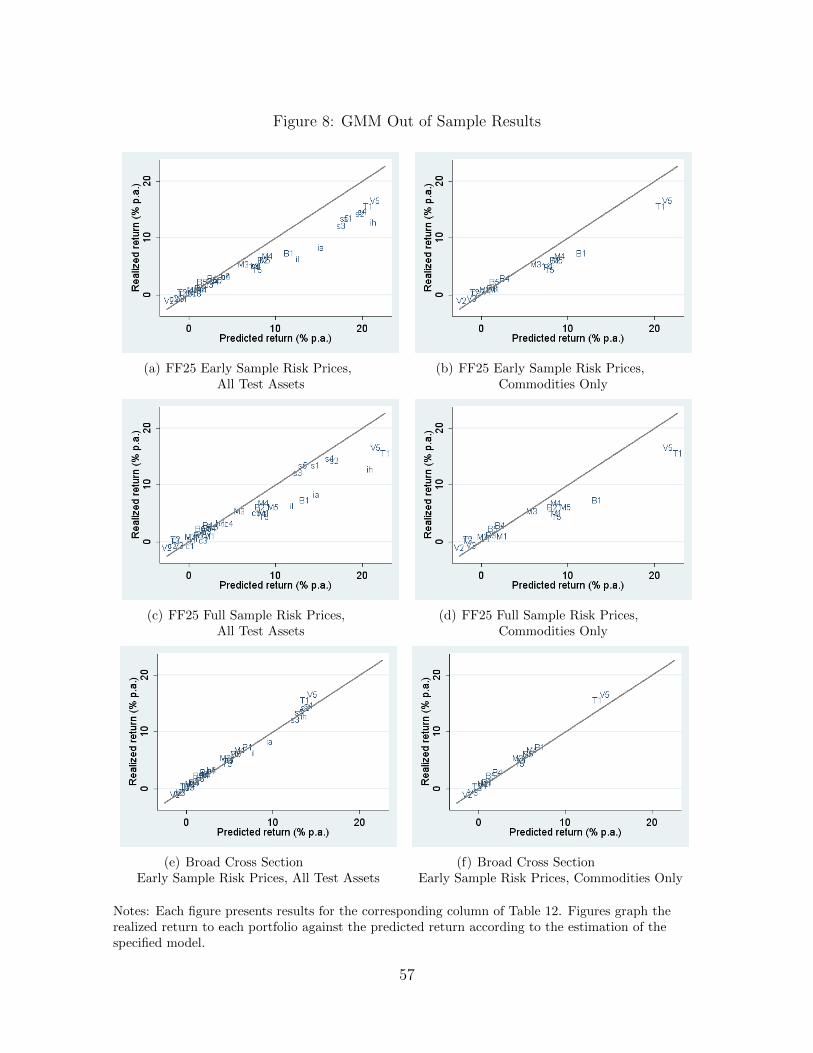

Finally, I present two types of out of sample predictions. Using the OLS estimation

procedure, I estimate either risk amounts or risk prices from an earlier sample period.

These early sample parameters are used to predict the returns to a broad cross section

of assets in a later period. Secondly, in order to provide out of sample results that

are more comparable with the main results of the model, I estimate the linear factor

model using GMM on three estimation samples. The parameters from these benchmark

estimations are then used to predict the average returns in a later sample period for

commodities and other portfolios not in the original sample.

7.1 Estimation using Ordinary Least Squares

While the estimation up to this point has followed the procedures developed by Yogo

(2006), in this section I present results for an estimation using simple ordinary least

squares regression. Using the short cross section with sorted portfolios, (column 4 of

Table 3), I first run a time series regression of each test asset on the three factors:

Reit = βi0 + βic∆ct + βid∆dt + βiwrWt + εit (18)

28

Next, I estimate the risk prices using a single cross sectional regression of the average

return to each test asset on the estimated time series betas:

Reit = λcβ̂

ic + λdβ̂

id + λwβ̂

iw + εi. (19)

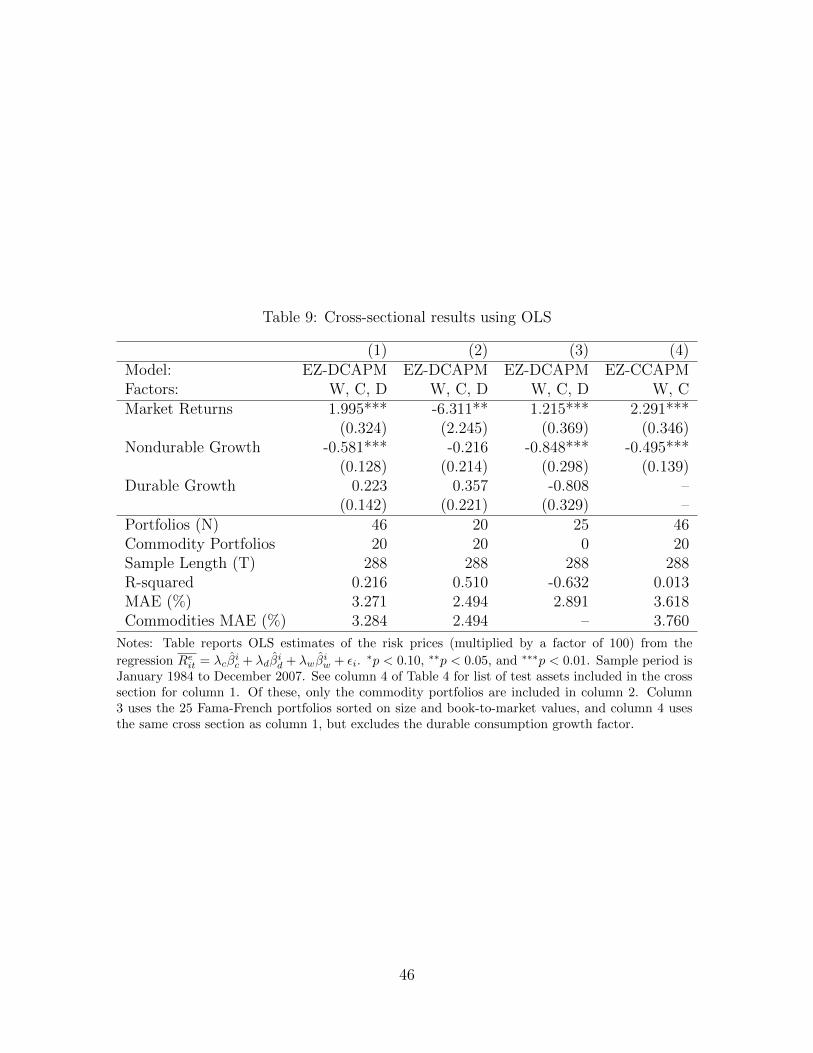

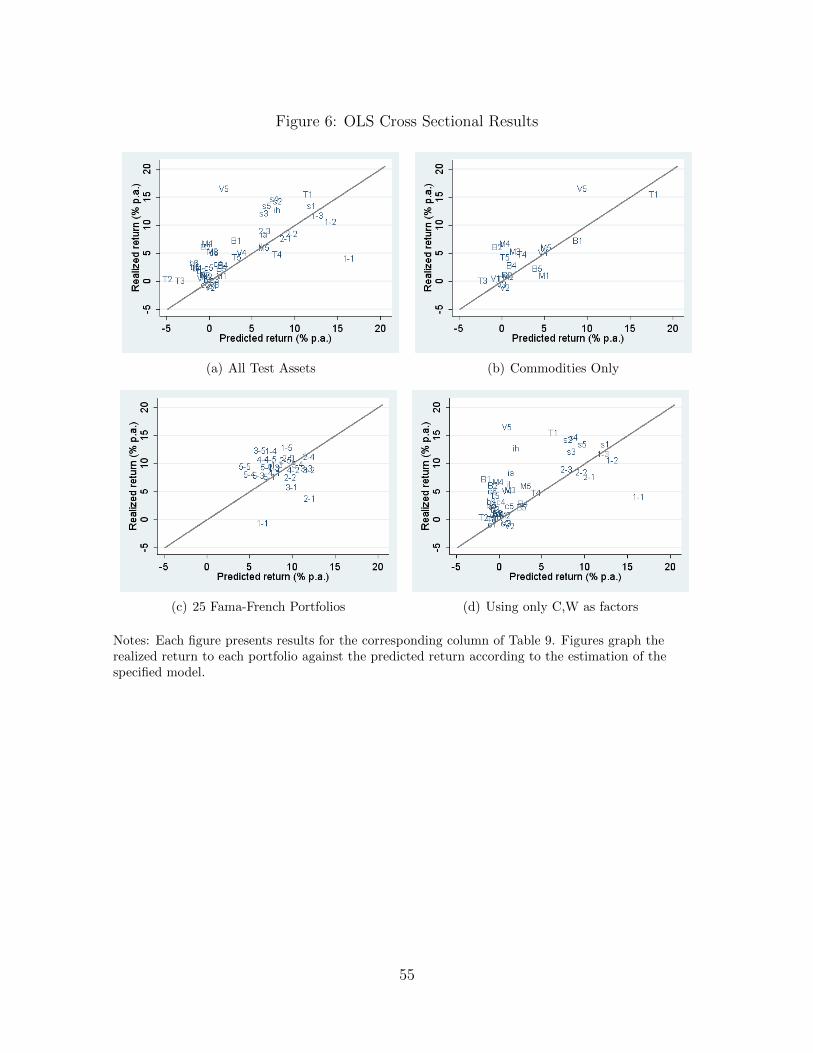

Column 1 of Table 9 presents the results of this cross sectional regression.12 While

the coefficient on durables risk is positive, it is not statistically distinguishable from

zero. Meanwhile, the risk price of market returns is positive and significant, and the

risk price on nondurable growth is negative and significant. The R-squared for this

regression is 0.22, and mean absolute error indicates that the cross sectional regression

predicts the average returns to commodity portfolios about as well as the returns to

all the test assets, on average. Figure 6(a) graphs the actual returns to each test asset

against the predicted return for the OLS estimation.

Given that the risk prices change depending on the cross section of test assets, I

also estimate the cross sectional regression using only the 20 commodity portfolios. In

the results reported in column 2, we can see that the risk price on durables is the only

positive one, though it is still not significant. Additionally, the R-squared is even higher,

at 0.51. These results provide additional evidence that while a number of assets have

returns that increase with market risk, the average returns to commodity portfolios

instead increase with durable consumption risk.

Finally, I provide two more OLS estimations for comparison. Column 3 provides

results for the cross section of 25 Fama-French equity portfolios sorted on size and

book-to-market value. For this estimation, the risk price of market returns is the only

positive one. However, the R-squared is negative. These results, along with Figure 6(c),

provide evidence that OLS estimation of the linear factor model does not perform well

even for the benchmark test assets. In comparison with these results, the OLS results

for commodities look even stronger. Column 4 and Figure 6(d) provide results for the

EZ-CCAPM, which is the nested model with only nondurable consumption and market

returns as factors. The poor fit of this model provide further evidence that even in an

OLS estimation, the durables factor helps explain the returns to commodity portfolios.

12Since the regressors here are betas, rather than covariances, the risk prices (λ) are not necessarilyequal to the risk prices (b) in the previous cross sectional analyses. Consequently, they also do nothave the same relationship with the preference parameters of the model in Section 3.

29

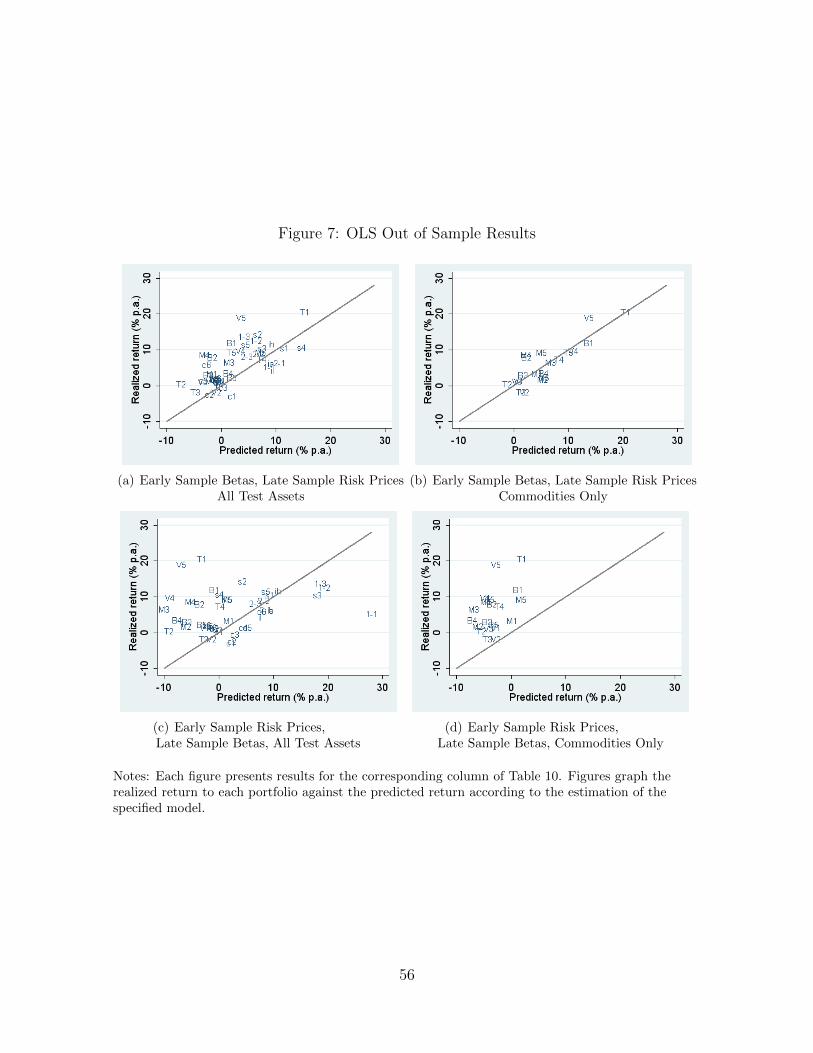

7.2 Out of Sample Tests using OLS

Another way to check the robustness of the results is to examine how the model per-

forms out of sample. In this section, I perform three of out of sample tests using OLS

regressions. For each test, either risk amounts or risk prices are estimated using an early

sample period. These early sample parameters are used to predict the cross section of

average returns in a later period. These out of sample estimations are performed using

the short cross section with sorted portfolios (column 4 of Table 4).

In the first out of sample test, I use the OLS cross sectional regression to test

whether betas from an earlier period are able to predict average returns in a later