us money matters - credit suisse

TRANSCRIPT

ANALYST CERTIFICATIONS AND IMPORTANT DISCLOSURES ARE IN THE DISCLOSURE APPENDIX. FOR OTHER IMPORTANT DISCLOSURES, PLEASE REFER TO https://firesearchdisclosure.credit-suisse.com.

CREDIT SUISSE SECURITIES RESEARCH & ANALYTICS BEYOND INFORMATION®

Client-Driven Solutions, Insights, and Access

US Money Matters

Does QE Really Work? The Evidence to Date QE3 is looking increasingly likely before Election Day in November. While an

announcement is possible as soon as August 1, the FOMC probably will choose to wait until its September 13 meeting.

This raises a natural question: Will additional QE work? After all, few would argue that US interest rates are too high or that banks in the US need still more excess reserves.

Empirical studies on the effectiveness of the Fed's balance sheet operations suggest that asset purchases designed to address general economic malaise are less potent than programs targeted at specific market disruptions. Even QE proponents stress that asset purchases are not the silver bullet that will cure all that ails the US economy.

The negative effects of unconventional monetary policy have received scant attention in the research literature and are not well understood. Costs should be weighed against the value of asset purchases for macro stabilization.

Monetary Policy Review/Preview Minutes of the June 19-20 FOMC meeting (July 11)

Fed Chairman Bernanke’s Semiannual Monetary Policy Testimony (July 17-18)

Beige Book (July 18)

Fed Balance Sheet Update The Fed’s securities portfolio shrank with a $3.8bn drop in T-bill holdings.

The ECB’s use of the central bank dollar liquidity swap line is edging higher.

Money Supply Update M1 rose $21.5bn in the week ended July 2; M2 increased $43.2bn.

Plunging velocity suggests money supply is not signaling worrisome inflation.

Bank Balance Sheet Update C&I loans are recovering fastest from the crisis, growing at a 14.5% yoy pace.

Branches of foreign banks in the US are back to holding more cash assets than domestically chartered commercial banks.

Selected Empirical QE Studies

15 July 2012Economics Research

http://www.credit-suisse.com/researchandanalytics

Contributors

Neal Soss+1 212 325 3335

Dana Saporta+1 212 538 3163

15 July 2012

US Money Matters 2

Does QE Really Work? The Evidence to Date Less than four weeks ago, the Federal Open Market Committee voted to continue its maturity extension program (Operation Twist) for another six months. But the sluggishness of US economic activity has the key decision-makers on the FOMC considering a more aggressive easing move.

In our view, another round of large-scale asset purchases (“QE3”) is looking increasingly likely before Election Day in November. While an announcement is possible as soon as the July 31-August 1 meeting, the FOMC probably will choose to wait until its September 12-13 meeting.

Having forecast that the FOMC will buy more assets, we address the next natural question: Will additional QE work? After all, few would argue that US interest rates are too high or that banks in the US need still more excess reserves.

To find the answer, we consulted empirical studies within and without the Federal Reserve system on the effectiveness of the previous two rounds of QE and the balance sheet neutral Operation Twist program. There are many complications that arise in the evaluation of the programs’ results, and opinions differ among economists even within the Fed. However, a review of the empirical literature yields some common themes:

1. QE1 was more effective than QE2.

2. It is easier to find and quantify QE’s effect on Treasury yields than to identify and measure QE’s effect on real economic performance.

3. QE also lowered nominal interest rates on agencies, MBS, and corporate bonds, with magnitudes differing across bond types and maturities.

Results of the studies we reviewed were less uniform on QE effects on equities, the dollar, and commodity prices.

How is QE supposed to work?

QE1 was the expansion of the Fed’s balance sheet achieved mostly through large-scale asset purchases of agency debt and mortgage-backed securities. To a considerable extent, that program was aimed at rehabilitating a particular financial market that was functioning poorly at the time. From that perspective, the report card reads favorably. Lingering issues in the mortgage market (e.g., the foreclosure confusion) are not related to the original malfunction the Fed sought to cure.

In QE1 (Nov 2008-Mar 2010), the expansion of the Fed balance sheet, and especially the provision of a large amount of bank reserves, was incidental.

QE2 (Nov 2010-Jun 2011) was not about a poorly functioning piece of the financial system. The Treasury market had been functioning just fine. QE2 was about the Fed doing large-scale asset purchases to boost aggregate demand and eventually create more jobs.

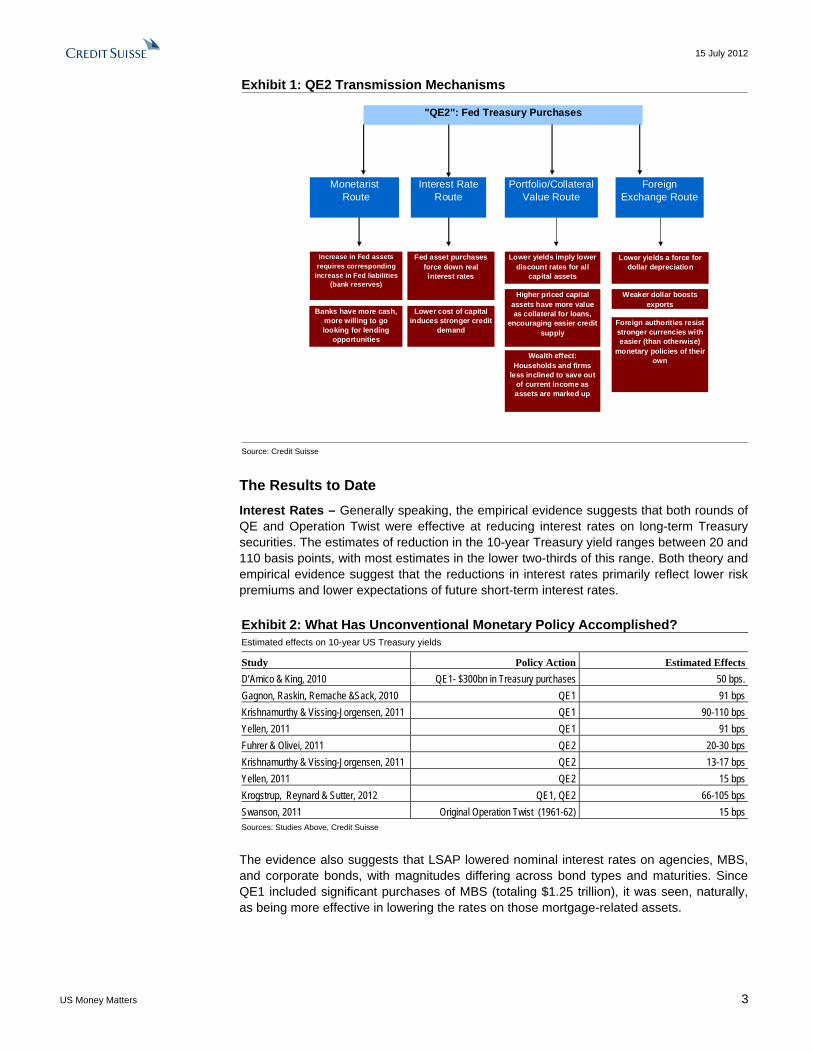

How do we get from expanded central bank balance sheets to real economic performance? There are four broad policy transmission paths economists have theorized about over the years as follows:

A money supply effect, which one might identify with old-fashioned (although perhaps again more timely) monetarism.

An interest rate effect, which one might identify with a Keynesian marginal efficiency of investment analysis.

A portfolio or credit channel or collateral value effect, which one might identify with the scholarly contributions of “Professor Bernanke” himself, among others.

A foreign exchange effect that, in current circumstances, may be more a matter of “forcibly enrich thy neighbor” global capital flows than “beggar thy neighbor” competitive devaluation.

15 July 2012

US Money Matters 3

Exhibit 1: QE2 Transmission Mechanisms

"QE2": Fed Treasury Purchases

Monetarist Route

Interest Rate Route

Portfolio/Collateral Value Route

Foreign Exchange Route

Increase in Fed assets requires corresponding

increase in Fed liabilities (bank reserves)

Banks have more cash, more willing to go looking for lending

opportunities

Fed asset purchases force down real interest rates

Lower cost of capital induces stronger credit

demand

Lower yields imply lower discount rates for all

capital assets

Higher priced capital assets have more value as collateral for loans,

encouraging easier credit supply

Wealth effect: Households and firms

less inclined to save out of current income as assets are marked up

Lower yields a force for dollar depreciation

Weaker dollar boosts exports

Foreign authorities resist stronger currencies with easier (than otherwise)

monetary policies of their own

Source: Credit Suisse

The Results to Date

Interest Rates – Generally speaking, the empirical evidence suggests that both rounds of QE and Operation Twist were effective at reducing interest rates on long-term Treasury securities. The estimates of reduction in the 10-year Treasury yield ranges between 20 and 110 basis points, with most estimates in the lower two-thirds of this range. Both theory and empirical evidence suggest that the reductions in interest rates primarily reflect lower risk premiums and lower expectations of future short-term interest rates.

Exhibit 2: What Has Unconventional Monetary Policy Accomplished? Estimated effects on 10-year US Treasury yields

Study Policy Action Estimated Effects

D’Amico & King, 2010 QE1- $300bn in Treasury purchases 50 bps.

Gagnon, Raskin, Remache &Sack, 2010 QE1 91 bps

Krishnamurthy & Vissing-Jorgensen, 2011 QE1 90-110 bps

Yellen, 2011 QE1 91 bps

Fuhrer & Olivei, 2011 QE2 20-30 bps

Krishnamurthy & Vissing-Jorgensen, 2011 QE2 13-17 bps

Yellen, 2011 QE2 15 bps

Krogstrup, Reynard & Sutter, 2012 QE1, QE2 66-105 bps

Swanson, 2011 Original Operation Twist (1961-62) 15 bps Sources: Studies Above, Credit Suisse

The evidence also suggests that LSAP lowered nominal interest rates on agencies, MBS, and corporate bonds, with magnitudes differing across bond types and maturities. Since QE1 included significant purchases of MBS (totaling $1.25 trillion), it was seen, naturally, as being more effective in lowering the rates on those mortgage-related assets.

15 July 2012

US Money Matters 4

In addition, QE1 provided liquidity support to a largely dysfunctional market, and therefore its impact was probably larger than that of QE2 and Operation Twist, which were conducted in more normal environments.

Macroeconomic Effects – Research dedicated to the effects of LSAP on GDP and employment is limited, but they do generally find these programs to be effective at promoting GDP growth, though to different extents. One study (Fuhrer and Olivei, 2011) found that $600bn Treasury purchases would increase real GDP by about 40-120bps while another study (Chen et al., 2011) suggested that the effects on GDP growth are not very likely to exceed 50bps. By using Okun’s law, the Fuhrer and Olivei study also theorized that the unemployment rate would drop by 30-45bps.

It should be noted that the estimated (as opposed to observed) effects on GDP and the unemployment rate are more gradual, usually taking place over the course of about two years.

The unconventional measures were generally seen as effective in preventing deflation at the zero lower bound through the signaling effect. However, economists do have contrasting opinions on the magnitude of QE’s price impact.

One study (Krishnamurthy and Vissing-Jorgensen, 2011) found that QE1 increased 10-year expected inflation by 96-146bps and that QE2 raised it by 5-16bps. On the flip side, one study (Chen et al., 2011) concluded that the inflationary consequences of QE1 and QE2 were less than 50bps. The Federal Reserve Bank of New York noted that inflation actually trended lower over the period when QE1 was in progress, though it probably fell less than it would have done without the asset purchases.

* * *

Empirical studies of the effects of the Fed's balance sheet operations suggest that QE designed to address general economic malaise is less potent than a program targeted at a specific market dysfunction. Even QE proponents on the FOMC stress that asset purchases are not the silver bullet that will cure all that ails the US economy.

Meanwhile, the drawbacks of additional easing may be rising. In his press conference on June 20, Chairman Bernanke explained that unconventional policy has costs and should not be used without serious consideration. Among the costs he cited were (1) potentially making the Fed’s exit strategy more difficult, (2) potentially creating negative implications for market functioning, and (3) financial stability issues (about which he was very vague).

The minutes of the June 19-20 FOMC meeting suggested that other Fed officials are also considering the potential limits and drawbacks of large-scale asset purchases:

“A few members observed that it would be helpful to have a better understanding of how large the Federal Reserve’s asset purchases would have to be to cause a meaningful deterioration in securities market functioning, and of the potential costs of such deterioration for the economy as a whole.”

Paraphrasing comments from San Francisco Fed President John Williams, the negative effects of unconventional monetary policy have received scant attention in the research literature and are not well understood.

Future studies should weigh these costs against the value of asset purchases for macroeconomic stabilization. In the meantime, in the face of decidedly inadequate job growth and low inflation, Fed policymakers are likely to conclude that QE3 will do more good than harm.

* For links to selected empirical studies on the effectiveness of unconventional monetary policy, click here.

15 July 2012

US Money Matters 5

Monetary Policy Review/Preview Minutes of the June 19-20 FOMC meeting (released on July 11)

Fed Chairman Bernanke’s July 17-18 Semiannual Monetary Policy Testimony

This week’s Beige Book (July 18)

Review: June 19-20 FOMC Meeting Minutes

Release date: July 11, 2012

The minutes of the June 19-20 Federal Open Market Committee meeting indicated the majority of voting members on the FOMC would support additional easing should the loss of momentum in the US economy be sustained:

“A few members expressed the view that further policy stimulus likely would be necessary to promote satisfactory growth in employment and to ensure that the inflation rate would be at the Committee’s goal. Several others noted that additional policy action could be warranted if the economic recovery were to lose momentum, if the downside risks to the forecast became sufficiently pronounced, or if inflation seemed likely to run persistently below the Committee’s longer-run objective.”

In the Federal Reserve vernacular, a “member” is a voting member of the FOMC, and a “participant” is on the committee but may or may not have a vote. So, doing the math, a few members (3?) plus several others (4 to 6?) would equal more than half of the 12 voting members on the FOMC.

There was some suggestion in the minutes, however, that Fed officials are also considering the potential limits and drawbacks of large-scale asset purchases:

“A few members observed that it would be helpful to have a better understanding of how large the Federal Reserve’s asset purchases would have to be to cause a meaningful deterioration in securities market functioning, and of the potential costs of such deterioration for the economy as a whole.”

The FOMC minutes were dovish, but not dovish enough to put the chances of QE as soon as August 1 over 50%, in our opinion. A September 13 announcement seems more likely to us.

In discussions of downside risks, Europe and US fiscal policy figured prominently. The FOMC discussed the so-called year-end fiscal cliff directly:

"If an agreement was not reached to address the expiring tax cuts and scheduled spending reductions in current law, a sharp tightening of fiscal policy would occur at the start of 2013. A few participants reported hearing that defense contractors were making contingency plans to reduce their workforces if potential spending cuts go into effect; one reported that some firms already had begun to make such reductions.”

Uncertainty was also a key theme:

“Contacts in some parts of the country also indicated that firms had become more cautious in their hiring and investment decisions, with most capital investment being undertaken to improve productivity and reduce costs rather than to expand capacity. Some participants cited examples of business contacts saying that heightened uncertainty about future tax and regulatory policies had led them to put potential investment projects on hold until the uncertainty is resolved.”

(For a related discussion, see the July 12, 2012 “Market Focus: Has Uncertainty Peaked?”)

15 July 2012

US Money Matters 6

Preview: Fed Chairman Bernanke’s Semiannual Monetary Policy Testimony

Release date: July 17-18, 2012

Chairman Bernanke will deliver the semiannual Monetary Policy Report to the Senate Banking Committee at 10am ET on July 17 and to the House Financial Services Committee at 10am on July 18. Market participants will be listening carefully for any strong hints of an imminent QE3 operation. They may be disappointed.

Those with a certain tenure in the business may occasionally still refer to these Congressional appearances as the Fed’s “Humphrey-Hawkins testimonies.” Before October 2007, the Humphrey-Hawkins testimonies were the first opportunity the public had to see the FOMC's newest economic projections. Also, public appearances by the Fed Chairman were rarer in that era. Now that the Fed releases its projections four times a year and holds press conferences immediately after the associated policy meetings, these semiannual testimonies have lost some of their market relevance.

FOMC Economic Projections as of June 20, 2012 GDP and PCE price indexes (Q4/Q4%), unemployment rate (Q4 average)

Source: Federal Reserve, Credit Suisse

That said, there are still good reasons to tune in this week. While we already have seen the FOMC projections that Bernanke will be presenting, we have not yet heard the Chairman’s reaction to the disappointing June employment data released on July 6.

Also, these Congressional appearances will give Bernanke an opportunity to underscore some key points from his June 20 press conference: (1) the extension of Operation Twist was a “substantive” easing move; (2) the Fed is not out of ammunition when it comes to providing additional accommodation; and (3) the FOMC would consider a resumption of large-scale asset purchases (QE3) if more easing seems warranted.

There may also be discussion of other unconventional policies, besides QE, the Fed might be contemplating (although Jackson Hole is the more typical venue for such topics). Bernanke is not likely to show his hand regarding the probability of QE3, or other action, as soon as the July 31-August 1 FOMC meeting, however.

15 July 2012

US Money Matters 7

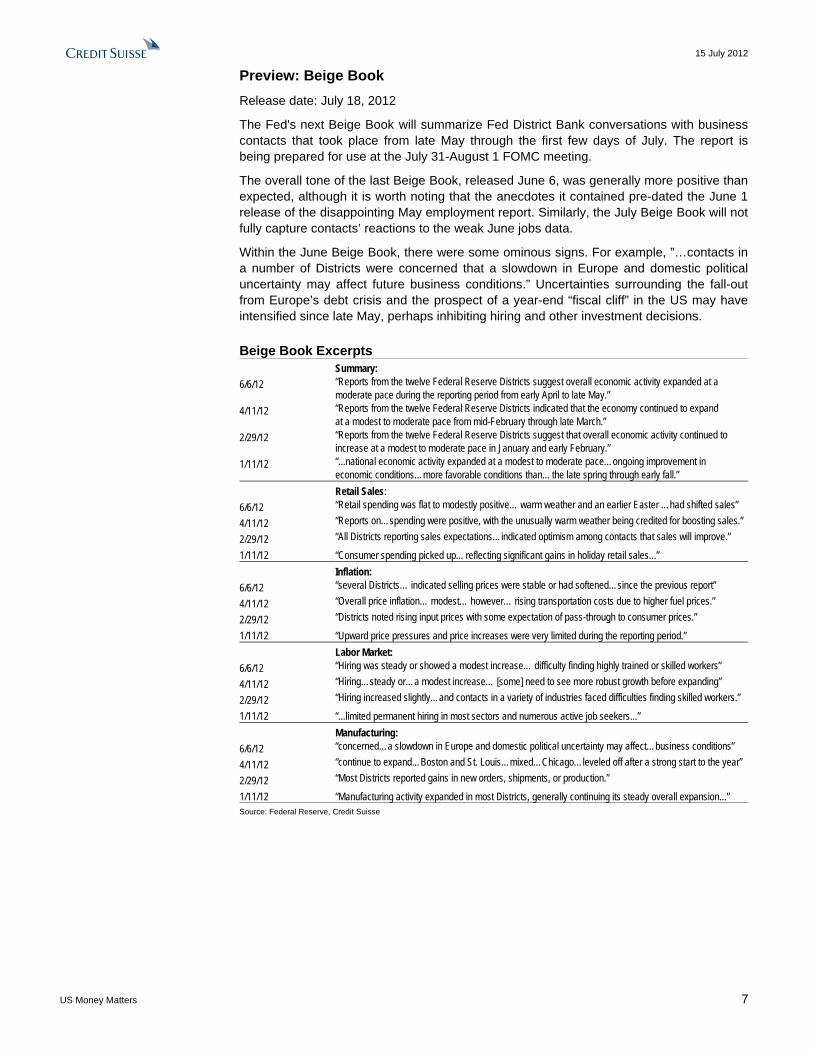

Preview: Beige Book

Release date: July 18, 2012

The Fed's next Beige Book will summarize Fed District Bank conversations with business contacts that took place from late May through the first few days of July. The report is being prepared for use at the July 31-August 1 FOMC meeting.

The overall tone of the last Beige Book, released June 6, was generally more positive than expected, although it is worth noting that the anecdotes it contained pre-dated the June 1 release of the disappointing May employment report. Similarly, the July Beige Book will not fully capture contacts’ reactions to the weak June jobs data.

Within the June Beige Book, there were some ominous signs. For example, ”…contacts in a number of Districts were concerned that a slowdown in Europe and domestic political uncertainty may affect future business conditions.” Uncertainties surrounding the fall-out from Europe’s debt crisis and the prospect of a year-end “fiscal cliff” in the US may have intensified since late May, perhaps inhibiting hiring and other investment decisions.

Beige Book Excerpts Summary:

6/6/12 “Reports from the twelve Federal Reserve Districts suggest overall economic activity expanded at a moderate pace during the reporting period from early April to late May.”

4/11/12 “Reports from the twelve Federal Reserve Districts indicated that the economy continued to expand at a modest to moderate pace from mid-February through late March.”

2/29/12 “Reports from the twelve Federal Reserve Districts suggest that overall economic activity continued to increase at a modest to moderate pace in January and early February.”

1/11/12 “...national economic activity expanded at a modest to moderate pace…ongoing improvement in economic conditions…more favorable conditions than... the late spring through early fall.”

Retail Sales:

6/6/12 “Retail spending was flat to modestly positive… warm weather and an earlier Easter …had shifted sales”

4/11/12 “Reports on…spending were positive, with the unusually warm weather being credited for boosting sales.”

2/29/12 “All Districts reporting sales expectations…indicated optimism among contacts that sales will improve.”

1/11/12 “Consumer spending picked up... reflecting significant gains in holiday retail sales...”

Inflation:

6/6/12 “several Districts… indicated selling prices were stable or had softened…since the previous report”

4/11/12 “Overall price inflation… modest… however… rising transportation costs due to higher fuel prices.”

2/29/12 “Districts noted rising input prices with some expectation of pass-through to consumer prices.”

1/11/12 “Upward price pressures and price increases were very limited during the reporting period.”

Labor Market:

6/6/12 “Hiring was steady or showed a modest increase… difficulty finding highly trained or skilled workers”

4/11/12 “Hiring…steady or…a modest increase… [some] need to see more robust growth before expanding”

2/29/12 “Hiring increased slightly…and contacts in a variety of industries faced difficulties finding skilled workers.”

1/11/12 “...limited permanent hiring in most sectors and numerous active job seekers...”

Manufacturing:

6/6/12 “concerned…a slowdown in Europe and domestic political uncertainty may affect…business conditions”

4/11/12 “continue to expand…Boston and St. Louis…mixed…Chicago…leveled off after a strong start to the year”

2/29/12 “Most Districts reported gains in new orders, shipments, or production.”

1/11/12 “Manufacturing activity expanded in most Districts, generally continuing its steady overall expansion...” Source: Federal Reserve, Credit Suisse

15 July 2012

US Money Matters 8

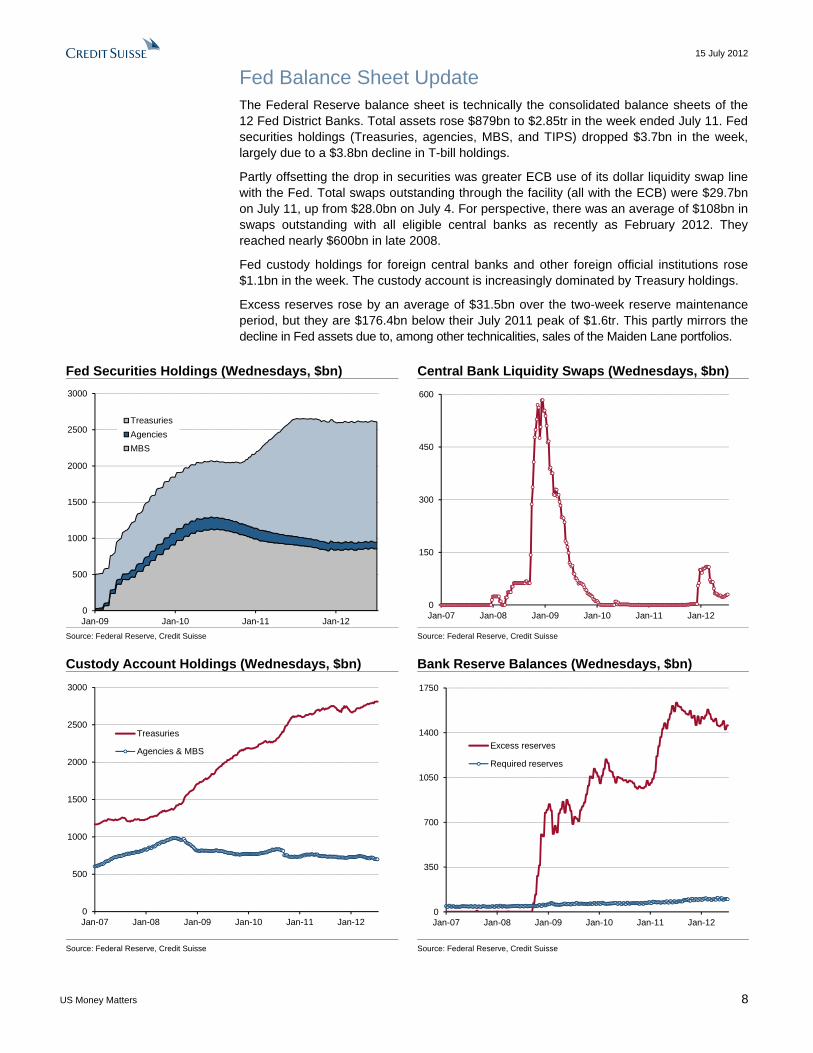

Fed Balance Sheet Update The Federal Reserve balance sheet is technically the consolidated balance sheets of the 12 Fed District Banks. Total assets rose $879bn to $2.85tr in the week ended July 11. Fed securities holdings (Treasuries, agencies, MBS, and TIPS) dropped $3.7bn in the week, largely due to a $3.8bn decline in T-bill holdings.

Partly offsetting the drop in securities was greater ECB use of its dollar liquidity swap line with the Fed. Total swaps outstanding through the facility (all with the ECB) were $29.7bn on July 11, up from $28.0bn on July 4. For perspective, there was an average of $108bn in swaps outstanding with all eligible central banks as recently as February 2012. They reached nearly $600bn in late 2008.

Fed custody holdings for foreign central banks and other foreign official institutions rose $1.1bn in the week. The custody account is increasingly dominated by Treasury holdings.

Excess reserves rose by an average of $31.5bn over the two-week reserve maintenance period, but they are $176.4bn below their July 2011 peak of $1.6tr. This partly mirrors the decline in Fed assets due to, among other technicalities, sales of the Maiden Lane portfolios.

Fed Securities Holdings (Wednesdays, $bn) Central Bank Liquidity Swaps (Wednesdays, $bn)

0

500

1000

1500

2000

2500

3000

Jan-09 Jan-10 Jan-11 Jan-12

Treasuries

Agencies

MBS

0

150

300

450

600

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

Custody Account Holdings (Wednesdays, $bn)

Bank Reserve Balances (Wednesdays, $bn)

0

500

1000

1500

2000

2500

3000

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Treasuries

Agencies & MBS

0

350

700

1050

1400

1750

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12

Excess reserves

Required reserves

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

15 July 2012

US Money Matters 9

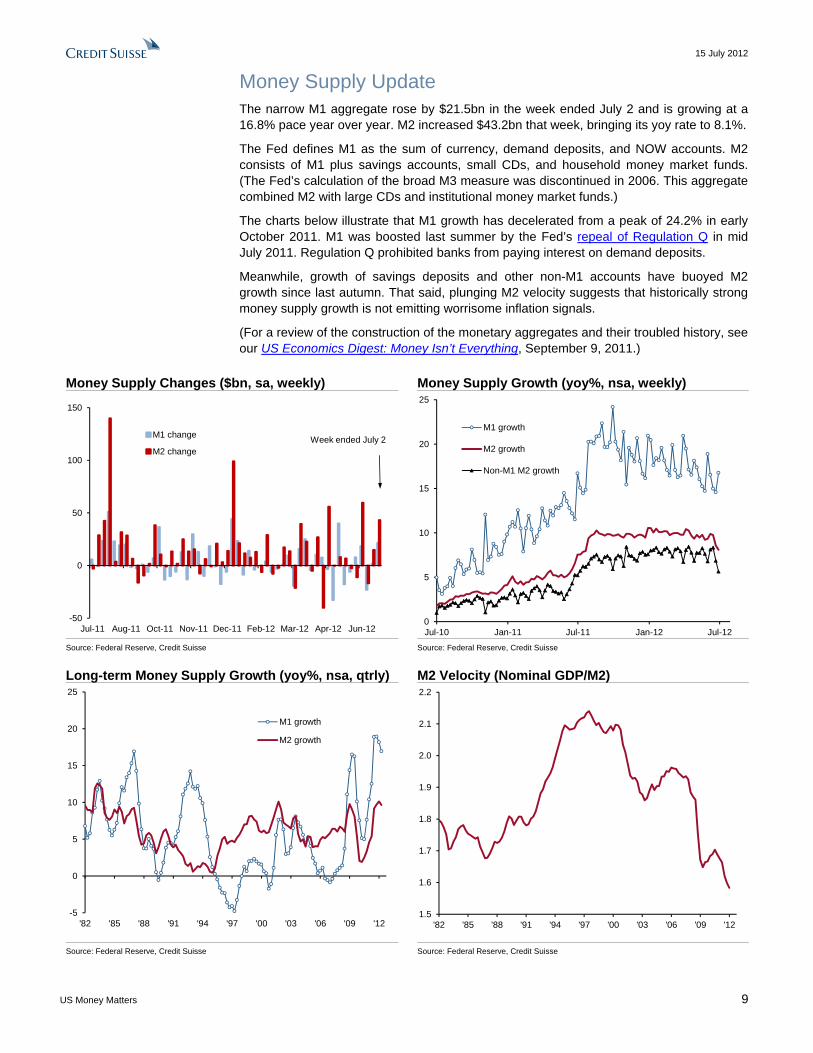

Money Supply Update The narrow M1 aggregate rose by $21.5bn in the week ended July 2 and is growing at a 16.8% pace year over year. M2 increased $43.2bn that week, bringing its yoy rate to 8.1%.

The Fed defines M1 as the sum of currency, demand deposits, and NOW accounts. M2 consists of M1 plus savings accounts, small CDs, and household money market funds. (The Fed’s calculation of the broad M3 measure was discontinued in 2006. This aggregate combined M2 with large CDs and institutional money market funds.)

The charts below illustrate that M1 growth has decelerated from a peak of 24.2% in early October 2011. M1 was boosted last summer by the Fed’s repeal of Regulation Q in mid July 2011. Regulation Q prohibited banks from paying interest on demand deposits.

Meanwhile, growth of savings deposits and other non-M1 accounts have buoyed M2 growth since last autumn. That said, plunging M2 velocity suggests that historically strong money supply growth is not emitting worrisome inflation signals.

(For a review of the construction of the monetary aggregates and their troubled history, see our US Economics Digest: Money Isn’t Everything, September 9, 2011.)

Money Supply Changes ($bn, sa, weekly) Money Supply Growth (yoy%, nsa, weekly)

-50

0

50

100

150

Jul-11 Aug-11 Oct-11 Nov-11 Dec-11 Feb-12 Mar-12 Apr-12 Jun-12

M1 change

M2 changeWeek ended July 2

0

5

10

15

20

25

Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

M1 growth

M2 growth

Non-M1 M2 growth

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

Long-term Money Supply Growth (yoy%, nsa, qtrly)

M2 Velocity (Nominal GDP/M2)

-5

0

5

10

15

20

25

'82 '85 '88 '91 '94 '97 '00 '03 '06 '09 '12

M1 growth

M2 growth

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

'82 '85 '88 '91 '94 '97 '00 '03 '06 '09 '12

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

15 July 2012

US Money Matters 10

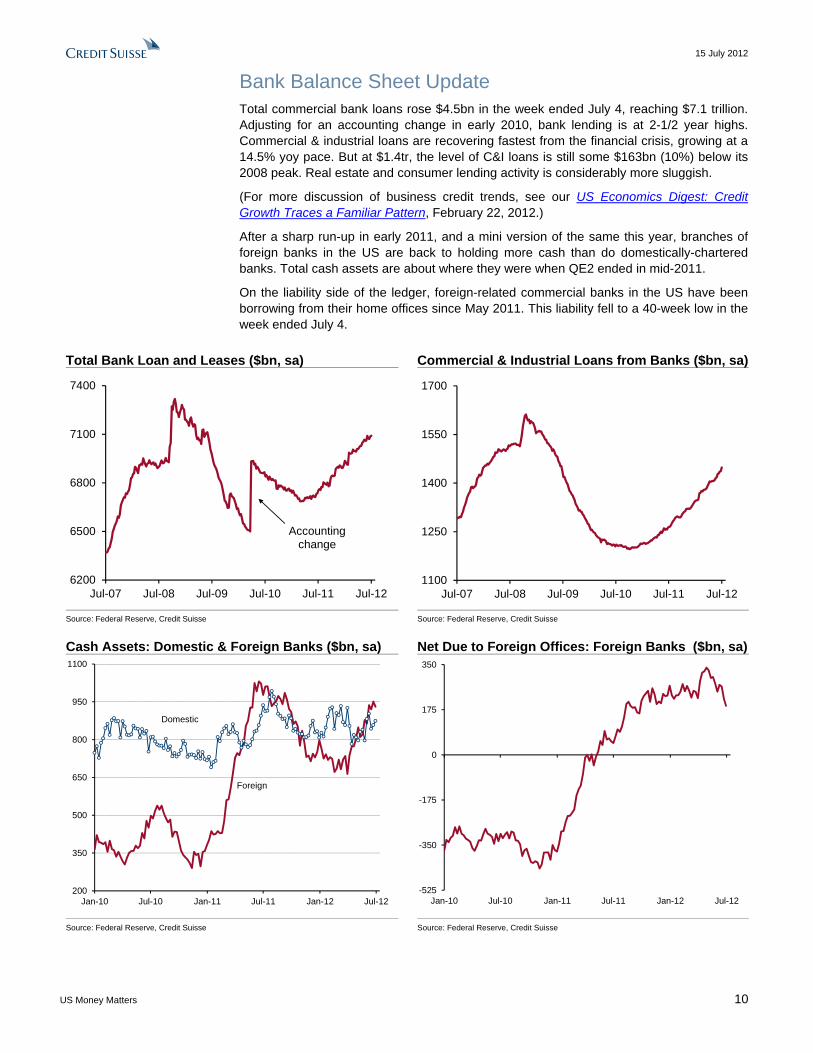

Bank Balance Sheet Update Total commercial bank loans rose $4.5bn in the week ended July 4, reaching $7.1 trillion. Adjusting for an accounting change in early 2010, bank lending is at 2-1/2 year highs. Commercial & industrial loans are recovering fastest from the financial crisis, growing at a 14.5% yoy pace. But at $1.4tr, the level of C&I loans is still some $163bn (10%) below its 2008 peak. Real estate and consumer lending activity is considerably more sluggish.

(For more discussion of business credit trends, see our US Economics Digest: Credit Growth Traces a Familiar Pattern, February 22, 2012.)

After a sharp run-up in early 2011, and a mini version of the same this year, branches of foreign banks in the US are back to holding more cash than do domestically-chartered banks. Total cash assets are about where they were when QE2 ended in mid-2011.

On the liability side of the ledger, foreign-related commercial banks in the US have been borrowing from their home offices since May 2011. This liability fell to a 40-week low in the week ended July 4.

Total Bank Loan and Leases ($bn, sa) Commercial & Industrial Loans from Banks ($bn, sa)

6200

6500

6800

7100

7400

Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12

Accounting change

1100

1250

1400

1550

1700

Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

Cash Assets: Domestic & Foreign Banks ($bn, sa)

Net Due to Foreign Offices: Foreign Banks ($bn, sa)

200

350

500

650

800

950

1100

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Domestic

Foreign

-525

-350

-175

0

175

350

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

15 July 2012

US Money Matters 11

Selected Empirical Studies on the Effectiveness of Unconventional Monetary Policy1 Chen, Han, Cúrdia, Vasco, and Ferrero, Andrea (2011). “The Macroeconomic Effects of Large-Scale Asset Purchase Programs,” Federal Reserve Bank of New York Staff Reports, N0. 527. http://www.newyorkfed.org/research/staff_reports/sr527.pdf

Christensen, Jens and Rudebusch, Glenn (2012). “The Response of Interest Rates to U.S. and U.K. Quantitative Easing”, Federal Reserve Bank of San Francisco Working Paper Series, 2012-06. http://www.frbsf.org/publications/economics/papers/2012/wp12-06bk.pdf

D’Amico, Stefania and King, Thomas (2010). “Flow and Stock Effects of Large-Scale Treasury Purchases,“ Federal Reserve Finance and Economics Discussion Series, 2010-52. http://www.federalreserve.gov/pubs/feds/2010/201052/201052pap.pdf

Farmer, Roger (2012). “The effect of conventional and unconventional monetary policy rules on inflation expectations: theory and evidence”, NBER Working Paper, No. 18007. http://www.rogerfarmer.com/NewWeb/PdfFiles/Monetary%20Policy%20Rules_R.pdf

Fuhrer, Jeffrey and Olivei, Giovanni (2011). “The Estimated Macroeconomic Effects of the Federal Reserve’s Large-Scale Treasury Purchase Program”, Federal Reserve Bank of Boston Public Policy Briefs, No.11-2. http://www.bos.frb.org/economic/ppb/2011/ppb112.pdf

Gagnon, Joseph, Matthew, Raskin, Remasche, Julie and Sack, Brian (2010). “Large-Scale Asset Purchases by the Federal Reserve: Did They Work?” Federal Reserve Bank of New York Staff Report, No. 441. http://www.ny.frb.org/research/staff_reports/sr441.pdf

Glick, Reuven and Leduc, Sylvain (2011). “Are Large-Scale Asset Purchases Fueling the Rise in Commodity Prices? Federal Reserve Bank of San Francisco Economic Letter, 2011-10 http://www.frbsf.org/publications/economics/letter/2011/el2011-10.html

Hamilton, James and Wu, Jing (2011). “The Effectiveness Of Alternative Monetary Policy Tools In A Zero Lower Bound Environment,” NBER Working Paper, No. 16956. http://dss.ucsd.edu/~jhamilto/zlb.pdf

Krogstrup, Signe, Reynard, Samuel and Sutter, Barbara (2012). “Liquidity Effects of Quantitative Easing on Long-Term Interest Rates,” Swiss National Bank Working Papers, No. 2012-2. http://www.snb.ch/n/mmr/reference/working_paper_2012_02/source/working_paper_2012_02.n.pdf

Krishnamurthy, Arvind and Vissing-Jorgensen, Annettte (2011). “The Effect of Quantitative Easing on Interest Rates: Channels and Implications for Policy”, NBER Working Paper, No. 17555. http://www.tilburguniversity.edu/about-tilburg-university/schools/economics-and-management/news/seminars/finance/2011/Vissing.pdf

Lockhart, Dennis (2012). “ Monetary Policy Limits: Federal Reserve Actions and Tools,” Federal Reserve Bank of Atlanta, speech at Institute of Regulation & Risk, North Asia, Tokyo, Japan, May 21, 2012. http://www.frbatlanta.org/documents/news/speeches/120521_lockhart.pdf

Neely, Christopher (2010), “The Large Scale Asset Purchases Had Large International Effects,” Federal Reserve Bank of St. Louis Working Papers, 2010-018D. http://research.stlouisfed.org/wp/2010/2010-018.pdf

1 Credit Suisse has not reviewed the linked site and takes no responsibility for the content contained therein. This link is provided solely for your convenience and information. Following this link or any other link on the Credit Suisse Web site shall be at your own risk.

15 July 2012

US Money Matters 12

Stroebel, Johannes and Taylor, John, “Estimated Impact of the Fed's Mortgage-Backed Securities Purchase Program,” forthcoming, International Journal of Central Banking. http://www.stanford.edu/~stroebel/MBS%20Purchase%20Program%20%20Stroebel%20and%20Taylor.pdf

Swanson, Eric (2011),“Let’s Twist Again: A High-Frequency Event-Study Analysis of Operation Twist and Its Implications for QE2,” Federal Reserve Bank of San Francisco Working Paper Series, 2011-08 http://www.frbsf.org/publications/economics/papers/2011/wp11-08bk.pdf

Swanson, Eric and Alon, Titan (2011). “Operation Twist and the Effect of Large-Scale Asset Purchases,” Federal Reserve Bank of San Francisco Economic Letter, 2011-13. http://www.frbsf.org/publications/economics/letter/2011/el2011-13.html

Thornton, Daniel (2009). “The Effect of the Fed’s Purchase of Long-Term Treasuries on the Yield Curve”, Federal Reserve Bank of St. Louis Economic Synopses, No. 25. http://research.stlouisfed.org/publications/es/09/ES0925.pdf

Thornton, Daniel (2012). “Quantitative Easing and Money Growth: Potential for Higher Inflation?”, Federal Reserve Bank of St. Louis Economic Synopses, No. 4. http://research.stlouisfed.org/publications/es/12/ES_2012-02-03.pdf

15 July 2012

US Money Matters 13

FOMC Economic Projections (from June 19-20 FOMC Meeting)

Real GDP Unemployment Rate

-6

-4

-2

0

2

4

6

Q12011

Q2 Q3 Q4 Q12012

FOMC Central TendenciesQ4/Q4%

annualized QoQ%

LongerRun'12

'13'14

4

5

6

7

8

9

10

11

Jan 2010 Jan 2011 Jan 2012

FOMC Central Tendencies

Q4 avg

May

%

LongerRun

'12'13

'14

Source: BEA, Federal Reserve, Credit Suisse. 2012 central tendency is 1.9% to 2.4%, 2013 is 2.2% to 2.8%, 2014 is 3.0% to 3.5% and longer run is 2.3% to 2.5% on a Q4/Q4 basis.

Source: BLS, Federal Reserve, Credit Suisse. 2012 central tendency is 8.0% to 8.2%, 2013 is 7.5% to 8.0%, 2014 is 7.0% to 7.7% and longer run is 5.2% to 6.0% on a Q4 average basis.

PCE Inflation Core PCE Inflation

-1

0

1

2

3

4

Jan 2010 Jan 2011 Jan 2012

FOMC CentralTendencies

Q4/Q4%

YoY%

LongerRun

'12'13

May

'14

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Jan 2010 Jan 2011 Jan 2012

FOMC Central Tendencies

Q4/Q4%

May

'12

YoY%

'13 '14

Source: BEA, Federal Reserve, Credit Suisse. 2012 central tendency is 1.2% to 1.7%, 2013 is 1.5% to 2.0, 2014 is 1.5% to 2.0% and longer run is 2.0% on a Q4/Q4 basis.

Source: BEA, Federal Reserve, Credit Suisse. 2012 central tendency is 1.7% to 2.0%, 2013 is 1.6% to 2.0% and 2014 is 1.6% to 2.0% on a Q4/Q4 basis.

Appropriate Timing of Policy Firming Appropriate Pace of Policy Firming

0%

1%

2%

3%

4%

5%

2012 2013 2014 Longer Run

Target Federal Funds Rate at Year

3 3

7

6

0

1

2

3

4

5

6

7

8

2012 2013 2014 2015

Number of Participants

Source: Federal Reserve, Credit Suisse Source: Federal Reserve, Credit Suisse

GLOBAL FIXED INCOME AND ECONOMIC RESEARCH

Dr. Neal Soss, Managing Director Chief Economist and Global Head of Economic Research

+1 212 325 3335

Eric Miller, Managing Director

Global Head of Fixed Income and Economic Research

+1 212 538 6480

US AND CANADA ECONOMICS

Dr. Neal Soss, Managing Director

Head of US Economics

+1 212 325 3335

Jonathan Basile, Director

+1 212 538 1436

Jay Feldman, Director

+1 212 325 7634

Henry Mo, Director

+1 212 538 0327

Dana Saporta, Director

+1 212 538 3163

Jill Brown, Vice President

+1 212 325 1578

Isaac Lebwohl, Associate

+1 212 538 1906

Peggy Riordan, AVP

+1 212 325 7525

LATIN AMERICA ECONOMICS AND STRATEGY

Alonso Cervera, Managing Director

Head of Non-Brazil Latam Economics

+52 55 5283 3845

Mexico, Chile, Colombia

Casey Reckman, Vice President

+1 212 325 5570

Argentina, Venezuela

Daniel Chodos, Vice President

+1 212 325 7708

Latam Strategy

Nilson Teixeira, Managing Director

Head of Brazil Economics

+55 11 3841 6288

Daniel Lavarda, Vice President

+55 11 3841 6352

Brazil

Tales Rabelo, Vice President

+55 11 3841 6353

Brazil

Iana Ferrao, Associate

+55 11 3841 6345

Brazil

Leonardo Fonseca, Associate

+55 11 3841 6348

Brazil

EURO AREA AND UK ECONOMICS

Neville Hill, Director

Head of European Economics

+44 20 7888 1334

Christel Aranda-Hassel, Director

+44 20 7888 1383

Giovanni Zanni, Director

European Economics – Paris

+33 1 70 39 0132

Violante di Canossa, Vice President

+44 20 7883 4192

Axel Lang, Analyst

+44 20 7883 3738

Steven Bryce, Analyst

+44 20 7883 7360

Yiagos Alexopoulos, Analyst

+44 20 7888 7536

EASTERN EUROPE, MIDDLE EAST & AFRICA ECONOMICS AND STRATEGY

Berna Bayazitoglu, Managing Director

Head of EEMEA Economics

+44 20 7883 3431

Turkey

Sergei Voloboev, Director

+44 20 7888 3694

Russia, Ukraine, Kazakhstan

Carlos Teixeira, Director

+27 11 012 8054

South Africa

Gergely Hudecz, Vice President

+33 1 7039 0103

Czech Republic, Hungary, Poland

Alexey Pogorelov, Associate

+7 495 967 8772

Russia, Ukraine, Kazakhstan

Natig Mustafayev, Associate

+44 20 7888 1065

EM and EEMEA cross-country analysis

Saad Siddiqui, Associate

+44 20 7888 9464

EEMEA Strategy

Nimrod Mevorach, Associate

+44 20 7888 1257

[email protected] EEMEA Strategy, Israel

JAPAN ECONOMICS

Hiromichi Shirakawa, Managing Director

+81 3 4550 7117

Takashi Shiono, Associate

+81 3 4550 7189

NON-JAPAN ASIA ECONOMICS

Dong Tao. Managing Director

Head of NJA Economics

+852 2101 7469

China

Robert Prior-Wandesforde, Director

+65 6212 3707

Regional, India, Indonesia, Singapore

Christiaan Tuntono, Vice President

+852 2101 7409

Hong Kong, Korea, Taiwan

Santitarn Sathirathai, Vice President

+65 6212 5675

Malaysia, Philippines, Thailand

Disclosure Appendix

Analyst Certification I, Neal Soss and Dana Saporta, certify that (1) the views expressed in this report accurately reflect my personal views about all of the subject companies and securities and (2) no part of my compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

Disclaimer References in this report to Credit Suisse include all of the subsidiaries and affiliates of Credit Suisse AG operating under its investment banking division. For more information on our structure, please use the following link: https://www.credit-suisse.com/who_we_are/en/. This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse AG or its affiliates (“CS”) to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates. The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients of this report as its customers by virtue of their receiving this report. The investments and services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. CS does not advise on the tax consequences of investments and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. Information and opinions presented in this report have been obtained or derived from sources believed by CS to be reliable, but CS makes no representation as to their accuracy or completeness. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that such liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. CS may, to the extent permitted by law, participate or invest in financing transactions with the issuer(s) of the securities referred to in this report, perform services for or solicit business from such issuers, and/or have a position or holding, or other material interest, or effect transactions, in such securities or options thereon, or other investments related thereto. In addition, it may make markets in the securities mentioned in the material presented in this report. CS may have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the entities mentioned in this report or may be providing, or have provided within the previous 12 months, significant advice or investment services in relation to the investment concerned or a related investment. Additional information is, subject to duties of confidentiality, available on request. Some investments referred to in this report will be offered solely by a single entity and in the case of some investments solely by CS, or an associate of CS or CS may be the only market maker in such investments. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgement at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR’s, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report may have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment and, in such circumstances, you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed any such site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS’s own website material) is provided solely for your convenience and information and the content of any such website does not in any way form part of this document. Accessing such website or following such link through this report or CS’s website shall be at your own risk. This report is issued and distributed in Europe (except Switzerland) by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is regulated in the United Kingdom by The Financial Services Authority (“FSA”). This report is being distributed in Germany by Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). This report is being distributed in the United States and Canada by Credit Suisse Securities (USA) LLC; in Switzerland by Credit Suisse AG; in Brazil by Banco de Investimentos Credit Suisse (Brasil) S.A; in Mexico by Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); in Japan by Credit Suisse Securities (Japan) Limited, Financial Instruments Firm, Director-General of Kanto Local Finance Bureau (Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Securities Investment Advisers Association, Type II Financial Instruments Firms Association; elsewhere in Asia/ Pacific by whichever of the following is the appropriately authorised entity in the relevant jurisdiction: Credit Suisse (Hong Kong) Limited, Credit Suisse Equities (Australia) Limited, Credit Suisse Securities (Thailand) Limited, Credit Suisse Securities (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch, and elsewhere in the world by the relevant authorised affiliate of the above. Research on Taiwanese securities produced by Credit Suisse AG, Taipei Branch has been prepared by a registered Senior Business Person. Research provided to residents of Malaysia is authorised by the Head of Research for Credit Suisse Securities (Malaysia) Sdn Bhd, to whom they should direct any queries on +603 2723 2020. This research may not conform to Canadian disclosure requirements. In jurisdictions where CS is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements. Non-U.S. customers wishing to effect a transaction should contact a CS entity in their local jurisdiction unless governing law permits otherwise. U.S. customers wishing to effect a transaction should do so only by contacting a representative at Credit Suisse Securities (USA) LLC in the U.S. This material is not for distribution to retail clients and is directed exclusively at Credit Suisse's market professional and institutional clients. Recipients who are not market professional or institutional investor clients of CS should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK or to other matters which are not regulated by the FSA or in respect of which the protections of the FSA for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available upon request in respect of this report. CS may provide various services to US municipal entities or obligated persons ("municipalities"), including suggesting individual transactions or trades and entering into such transactions. Any services CS provides to municipalities are not viewed as “advice” within the meaning of Section 975 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. CS is providing any such services and related information solely on an arm’s length basis and not as an advisor or fiduciary to the municipality. In connection with the provision of the any such services, there is no agreement, direct or indirect, between any municipality (including the officials, management, employees or agents thereof) and CS for CS to provide advice to the municipali ty. Municipalities should consult with their financial, accounting and legal advisors regarding any such services provided by CS. In addition, CS is not acting for direct or indirect compensation to solicit the municipality on behalf of an unaffiliated broker, dealer, municipal securities dealer, municipal advisor, or investment adviser for the purpose of obtaining or retaining an engagement by the municipality for or in connection with Municipal Financial Products, the issuance of municipal securities, or of an investment adviser to provide investment advisory services to or on behalf of the municipality.

Copyright © 2012 CREDIT SUISSE AG and/or its affiliates. All rights reserved.

Investment principal on bonds can be eroded depending on sale price or market price. In addition, there are bonds on which investment principal can be eroded due to changes in redemption amounts. Care is required when investing in such instruments. When you purchase non-listed Japanese fixed income securities (Japanese government bonds, Japanese municipal bonds, Japanese government guaranteed bonds, Japanese corporate bonds) from CS as a seller, you will be requested to pay purchase price only.