u.s. airline business models 2006-2015: trends and key

TRANSCRIPT

U.S. Airline Business Models 2006-2015:

Trends and Key Impacts

by

Alexander R. BachwichB.S., Mechanical Engineering

South Dakota School of Mines & Technology, 2015

Submitted to the Department of Civil and Environmental Engineeringin partial fulfillment of the requirements for the degree of

Master of Science in Transportationat the

MASSACHUSETTS INSTITUTE OF TECHNOLOGYJune 2017

c©Massachusetts Institute of Technology 2017. All rights reserved.

Author..............................................................................................................Department of Civil and Environmental Engineering

May 12, 2017

Certified by........................................................................................................Peter P. Belobaba

Principal Research Scientist of Aeronautics and AstronauticsThesis Supervisor

Accepted by.......................................................................................................Jesse Kroll

Professor of Civil and Environmental EngineeringChair, Graduate Program Committee

1

2

U.S. Airline Business Models 2006-2015: Trends and Key Impacts

by Alexander R. Bachwich

Submitted to the Department of Civil and Environmental Engineering onMay 12, 2017 in partial fulfillment of the requirements for the degree of

Master of Science in Transportation.

Abstract

This thesis focuses on the evolution of U.S. airline business models from 2006-2015, and the impacts of these changes on other stakeholders in the U.S. air trans-portation system. The U.S. airline industry has been affected by increasingly volatileprofit cycles since its deregulation in 1978. This volatility has led to major changesin the industry, including cost convergence between traditional Low Cost Carriers(LCCs) and Network Legacy Carriers (NLCs), multiple rounds of consolidation, andmost recently a period of “Capacity Discipline” where high fuel prices and a reducednumber of competitors led to slower-than-average capacity growth.

The combined effects of these changes led to the emergence of a new businessmodel: the “Ultra Low Cost Carrier” (ULCC). In this thesis, we conduct an analysisof ULCCs in the U.S. and demonstrate how these carriers’ business models, costs,and effects on air transportation markets differ from those of the traditional LCCs.We also explore how the network and fleet strategies of airlines using all threebusiness models have changed, highlighting key trends such as the decline in 50 seatjet use by NLCs and the varying network strategies of ULCCs.

In the second half of the thesis, we examine how these changes in airline businessmodels have affected other stakeholders in the U.S. transportation system. Wedescribe how average fares have changed from 2006-2015 in the top U.S. markets.Then, using econometric models, we examine the effects of ULCC and LCC presence,entry, and exit on base airfares, and how these effects have changed over time.

We also explore how evolving airline business models have impacted communitiesand their local airports. We find that seat capacity has grown at large hub airportsfrom 2006-2015, whereas smaller airports have all seen declines in service levelsto varying degrees. In particular, we examine how secondary airports in majormetro areas have been affected by changing LCC strategies, and how the smallestairports have experienced significant declines in NLC service, yet some gains inULCC service. Finally, we discuss the public policy implications of these servicechanges, and what policy options airports and communities have at both a localand national level to improve their level of commercial air service.

Thesis Supervisor: Peter Belobaba

Title: Principal Research Scientist of Aeronautics and Astronautics

3

4

Acknowledgements

First and foremost, I would like to thank my advisor Dr. Peter Belobaba.From the very first time I met with him, two years before I even entered theM.S.T. program, Peter has been willing to share his extensive knowledge ofand passion for the airline industry with me. His insight into the researchproblems I faced, his continuous support of my research and academic goals,and most of all his unfailing patience with me as a student and researcher haveall been invaluable during my time at MIT. I can’t thank him enough.

I would also like to thank Mike Wittman for being an amazing mentor,colleague, and friend. Thanks for always listening to my thoughts about theaviation industry and sharing your stories from the field. Without your col-laboration on ULCC research, this thesis wouldn’t be possible.

This thesis was also made possible in part by all my colleagues at HawaiianAirlines, especially those on the Network Strategy team: Chris Keen, AngelaTseng, and Ken Lieber. During my time in HNL this past summer, I learnedhow airline analysis works in practice, and cemented my passion for this fasci-nating and dynamic industry. I’d be remiss not to also thank William Swelbar,who not only inspired me to begin work on ULCCs, but provided excellent ca-reer and life advice, and connected me with the team at Hawaiian.

I’m extremely grateful for the personal friendship and professional supportof all my ICAT colleagues, including Adam, Ben, German, JP, Matt, Oren,and Tamas. All of the airline geek banter exchanged at our lunches has beenone of my favorite aspects of the MIT experience.

I’d also like to thank all of my other MIT and Boston friends, includingAlex, Andrea B, Andrea S, Caralyn, Eli, Eytan, Henry, Jack, Joanna, John,Katie, Kim, Nate, Nick, Sid, Taylor, and numerous others (including all myTSG and Asymptones friends!) Without you, my experience at MIT would beincomplete, and I certainly wouldn’t have been able to grow as a person and aresearcher nearly as much as I did. I’m equally grateful to my South Dakotafriends for years of support, including Patrick, Scott, Beth, Paul, and Reed.

Finally, I owe much gratitude to my wonderful family, especially my sisterEmily and my parents Dale and Vera. Thank you for supporting my loveof aviation throughout life, for always sharing your wisdom and love, andespecially for always trusting me to make our family travel plans.

5

6

Contents

1 Introduction 151.1 Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151.2 Motivation for Research . . . . . . . . . . . . . . . . . . . . . 161.3 Outline of Thesis . . . . . . . . . . . . . . . . . . . . . . . . . 17

2 Evolution of U.S. Airline Business Models 212.1 A Cyclic Industry . . . . . . . . . . . . . . . . . . . . . . . . . 222.2 Cost Convergence . . . . . . . . . . . . . . . . . . . . . . . . . 242.3 Consolidation . . . . . . . . . . . . . . . . . . . . . . . . . . . 282.4 Capacity Discipline . . . . . . . . . . . . . . . . . . . . . . . . 322.5 The Emerging ULCC . . . . . . . . . . . . . . . . . . . . . . . 34

2.5.1 Characteristics of the ULCC model . . . . . . . . . . . 37

3 Evolution of U.S. Airline Network and Fleet Structures 433.1 Background and Methods . . . . . . . . . . . . . . . . . . . . 43

3.1.1 Connectivity Model . . . . . . . . . . . . . . . . . . . . 453.2 Aggregate Fleet and Capacity Statistics . . . . . . . . . . . . . 473.3 Network Legacy Carriers (NLCs) . . . . . . . . . . . . . . . . 543.4 Hybrid Low Cost Carriers (LCCs) . . . . . . . . . . . . . . . . 613.5 Ultra Low Cost Carriers (ULCCs) . . . . . . . . . . . . . . . . 67

4 Key Impacts on Traffic and Fares 754.1 Capacity and Traffic Trends . . . . . . . . . . . . . . . . . . . 754.2 Unit Revenue and Fare Trends . . . . . . . . . . . . . . . . . . 784.3 Impact of the Emerging ULCC on Fares . . . . . . . . . . . . 83

4.3.1 Models . . . . . . . . . . . . . . . . . . . . . . . . . . . 844.3.2 Data Sources and Processing . . . . . . . . . . . . . . . 854.3.3 Descriptive Statistics . . . . . . . . . . . . . . . . . . . 874.3.4 Results: Market Presence . . . . . . . . . . . . . . . . 894.3.5 Results: Entry/Exit . . . . . . . . . . . . . . . . . . . 91

7

5 Key Impacts on Airports, Communities, and Public Policy 955.1 Overview of Seat Capacity Trends by

Airport Type . . . . . . . . . . . . . . . . . . . . . . . . . . . 955.2 LCCs and Secondary Airports . . . . . . . . . . . . . . . . . . 1005.3 Impacts on Smaller Airports . . . . . . . . . . . . . . . . . . . 105

5.3.1 NLCs and Decline of the 50 Seat Jet . . . . . . . . . . 1055.3.2 ULCCs and Growth in Service to Small Airports . . . 108

6 Conclusions 1136.1 Evolution of U.S. Airline Business Models . . . . . . . . . . . 1136.2 Impacts on Fares and Communities . . . . . . . . . . . . . . . 1166.3 Future Work . . . . . . . . . . . . . . . . . . . . . . . . . . . . 119

8

List of Figures

2.1 Classification of select major U.S. carriers in 2006 . . . . . . . 212.2 U.S. Airline Industry Net Income Since 1978 - Source: Airlines

for America . . . . . . . . . . . . . . . . . . . . . . . . . . . . 222.3 Cost per equivalent available seat mile, excl. transport-related

expenses, by carrier type, 2006-2015 . . . . . . . . . . . . . . . 252.4 Labor cost per equivalent seat mile by carrier type, 2000-2015 262.5 Year-over-year change in available domestic seat miles by carrier

type . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272.6 Types of partnerships between airlines organized by level of in-

tegration and profitability improvement . . . . . . . . . . . . . 292.7 Comparison between changes in GDP and changes in U.S. do-

mestic capacity (ASMs) 2006-2016 . . . . . . . . . . . . . . . . 332.8 Changes in U.S. domestic capacity by carrier type 2010-2015,

indexed to 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . 342.9 Allegiant and Spirit traffic and capacity, in billions of RPMs

and ASMs, 2005-2015 . . . . . . . . . . . . . . . . . . . . . . . 362.10 System CASM ex transport-related expenses & fuel vs. mean

stage length (2014) . . . . . . . . . . . . . . . . . . . . . . . . 382.11 Average cost per enplaned passenger among select ULCCs and

LCCs, 3Q15 . . . . . . . . . . . . . . . . . . . . . . . . . . . . 392.12 Ticket vs. ancillary revenue per passenger segment for Spirit

and Allegiant, 2014 . . . . . . . . . . . . . . . . . . . . . . . . 402.13 Total system RASM ex transport-related revenues vs. mean

stage length (2014) . . . . . . . . . . . . . . . . . . . . . . . . 40

3.1 Key network and fleet questions with associated metrics . . . 433.2 Example schematic of Airport Connectivity Quality Index (1) 463.3 Example schematic of Airport Connectivity Quality Index (2) 463.4 Fleet size and composition of Major U.S. airlines, 2006 . . . . 483.5 Fleet size and composition of Major U.S. airlines, 2015 . . . . 49

9

3.6 Average daily narrowbody block hour utilization by airline type,2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

3.7 Average domestic stage length by airline type, 2006-2015 . . . 523.8 Evolution of the combined fleet of NLCs by equipment type . 543.9 Average narrowbody block hour utilization of NLC-operated

flights, 2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 553.10 Average stage length of NLC-marketed domestic flights, 2006-

2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 563.11 Seat departures at top 10 AA/US/HP stations by seats, 2006 . 573.12 Seat departures at top 10 DL/NW stations by seats, 2006 . . . 583.13 Seat departures at top 10 UA/CO stations by seats, 2006 . . . 593.14 Share of flights at major U.S. NLC hubs by mainline and re-

gional aircraft, 2006 vs. 2015 . . . . . . . . . . . . . . . . . . . 603.15 Percentage of total connectivity lost without NLCs by airport

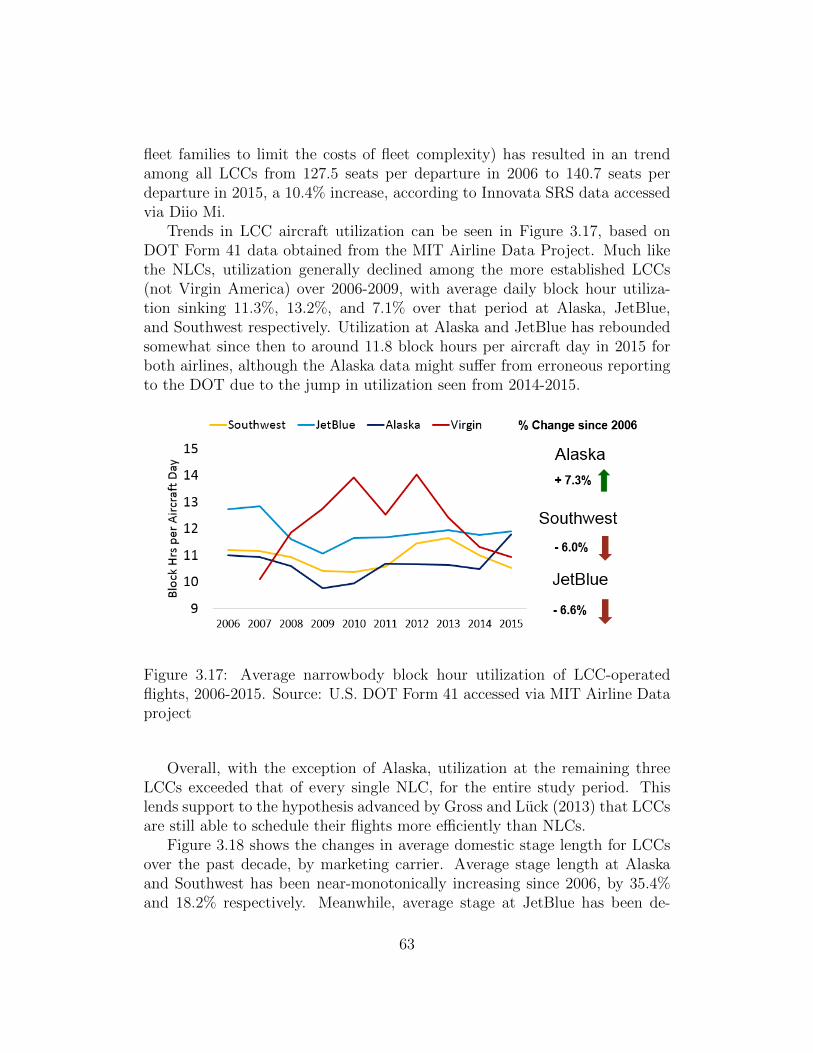

hub type, 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 613.16 Evolution of LCC narrowbody fleets 2006-2015 by carrier . . . 623.17 Average narrowbody block hour utilization of LCC-operated

flights, 2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 633.18 Average stage length of LCC-marketed domestic flights, 2006-2015 643.19 Seat departures at top 10 WN/FL stations by seats, 2006 . . . 643.20 Seat departures at top 10 B6 stations by seats, 2006 . . . . . . 653.21 Seat departures at top 10 AS stations by seats, 2006 . . . . . . 663.22 Percentage of total connectivity lost without LCCs by airport

hub type, 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 673.23 Evolution of ULCC narrowbody fleets 2006-2015 by carrier . . 673.24 Average narrowbody block hour utilization of ULCC-operated

flights, 2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . 683.25 Average stage length of ULCC-marketed domestic flights, 2006-

2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 693.26 Seat departures at top 10 F9 stations by seats, 2006 and 2015 703.27 Seat departures at top 10 G4 stations by seats, 2006 and 2015 713.28 Seat departures at top 10 NK stations by seats, 2006 and 2015 723.29 Number of destinations by carrier among ULCCs by daily fre-

quency of service, 2015 . . . . . . . . . . . . . . . . . . . . . . 733.30 Percentage of total connectivity lost without ULCCs by airport

hub type, 2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 73

4.1 Percentage of total U.S. domestic capacity by carrier type, 2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

10

4.2 Share of traffic and revenue in largest 100 O&Ds by carrier type,2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

4.3 Inflation adjusted PRESM among traditional LCCs and NLCs,2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 78

4.4 Number of top 1000 O&D markets that saw changes in fares,2006-2010 (current dollars) . . . . . . . . . . . . . . . . . . . . 80

4.5 Number of top 1000 O&D markets that saw changes in inflation-adjusted fares, 2006-2010 . . . . . . . . . . . . . . . . . . . . . 81

4.6 Average current fare by quintile over study period . . . . . . . 814.7 Average inflation-adjusted fare (in 2006 dollars) by quintile over

study period . . . . . . . . . . . . . . . . . . . . . . . . . . . . 824.8 Percentage of new markets abandoned within 1 or 2 years of

start, by carrier type . . . . . . . . . . . . . . . . . . . . . . . 88

5.1 Capacity trends by carrier type among different size airports . 975.2 Seat share trends by carrier type among different size airports 985.3 Seats per departure trends at Large and Medium Hubs . . . . 995.4 Seats per departure trends at Small and Non Hubs . . . . . . 995.5 Scheduled Southwest/AirTran seat departures by airport type,

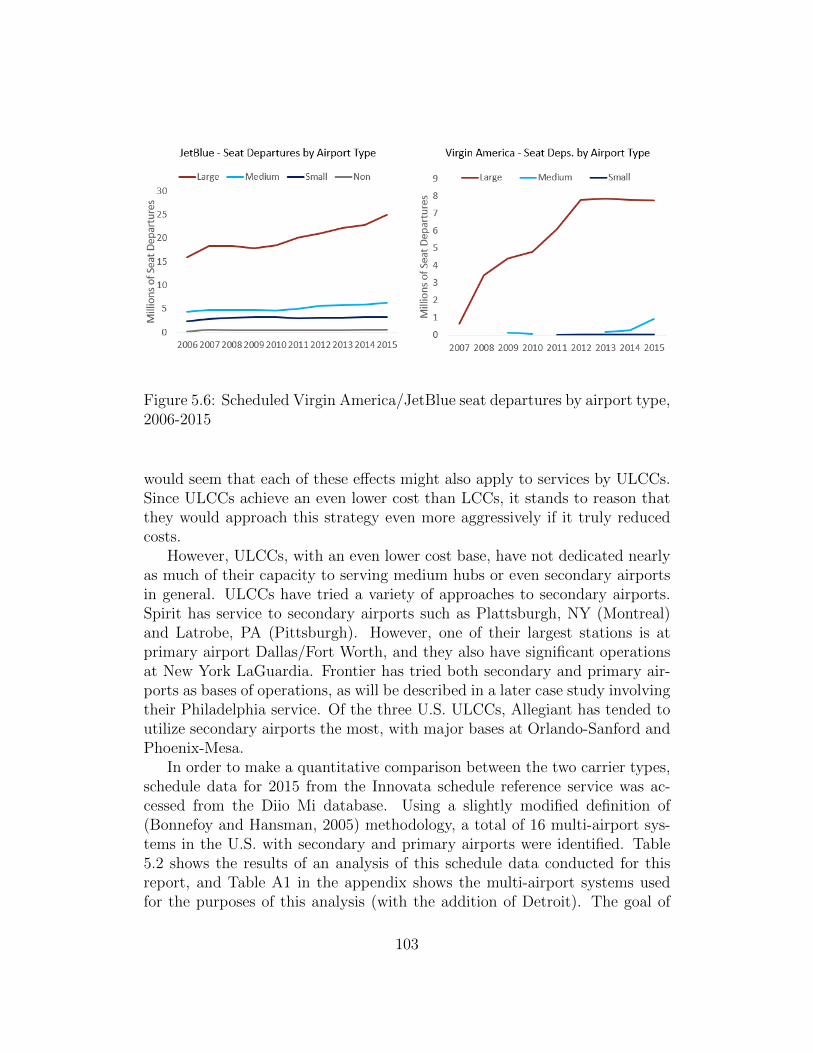

2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1025.6 Scheduled Virgin America/JetBlue seat departures by airport

type, 2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . 1035.7 Primary small (red) and non hub (blue) airports in contiguous

U.S. with more than 50,000 annual enplanements, 2014 . . . . 1065.8 Average daily departures per airport served by carrier type,

2006-2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1075.9 Frontier seat capacity at PHL-area airports, 2011-2015 . . . . 109

11

12

List of Tables

2.1 Chapter 11 bankruptcy filings by major U.S. carriers 2002-2005 232.2 Direct costs of A320-200 block hour costs by carrier, 2015 . . . 262.3 Costs and productivity of A320-200 block hour costs by carrier,

2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 272.4 Mergers and acquisitions among U.S. passenger airlines since 2006 292.5 Largest U.S. airlines in 2006 including regional partners . . . . 302.6 Largest U.S. airlines in 2015 including regional partners . . . . 312.7 Selected Major US Airlines by Category . . . . . . . . . . . . 41

3.1 Input parameters to ACQI model . . . . . . . . . . . . . . . . 473.2 Domestic/International capacity by marketing carrier type in

billions of ASMs, 2006-2015 . . . . . . . . . . . . . . . . . . . 53

4.1 Domestic RPMs (billions) by carrier type, 2006-2015 . . . . . 774.2 Descriptive statistics for markets included in fare study . . . . 794.3 Number of markets by year and type of carrier presence included

in study . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 874.4 Descriptive statistics for markets with ULCC and LCC entry

and exit events included in study . . . . . . . . . . . . . . . . 884.5 Effects of U.S. LCC and ULCC market presence on log of aver-

age one-way market fares, 2010-2015 . . . . . . . . . . . . . . 894.6 Average effect of ULCC or LCC presence on average one-way

market fares . . . . . . . . . . . . . . . . . . . . . . . . . . . . 904.7 Effects of U.S. LCC and ULCC entry and exit on log of average

one-way market fares, 2011-2015 . . . . . . . . . . . . . . . . . 914.8 Effects of U.S. carrier entry and exit on log of average one-way

market fares, 2011-2015 . . . . . . . . . . . . . . . . . . . . . . 93

5.1 FAA Airport Hub Types - Descriptive Statistics . . . . . . . . 965.2 Service breakdown in major metro areas among U.S. carriers,

2015 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 104

13

5.3 NLC changes in flights and seats, 2006 vs. 2015 . . . . . . . . 106

A1 Metro Areas Included in Entry/Exit Study . . . . . . . . . . . 126

14

Chapter 1

Introduction

1.1 Background

Since the deregulation of the U.S. airline industry in 1978, U.S. airlines havebeen competing with each other for passenger traffic on the basis of price andfrequency. As the industry has experienced a number of boom-and-bust busi-ness cycles, management strategies of airlines have been changing to competein the continuously evolving U.S. marketplace. These changes have impactedall facets of the airline business, including fare structure, network structure,labor costs, fleet composition, and fuel hedging strategies. In order to un-derstand the dynamics of U.S. airline industry, it is important to study theevolution of business models in the industry, as well as the macro-level trendsthat led to the development of these models.

The business models of today’s Network Legacy Carriers (NLCs) - Ameri-can, Delta, and United - can be traced back to the immediate post-deregulationera. Before 1978, these carriers were operating interstate flights under the au-thority of the Civil Aeronautics Board (CAB). After deregulation, with pricingand network decisions no longer subject to extensive regulation by the CAB,NLCs introduced some key features of their business model that they retainto this day (Gillen and Morrison, 2003). Namely, NLCs developed 1) huband spoke networks that enabled them to offer service on a large number oforigin and destination (O&D) markets; 2) global alliances and partnershipswith regional carriers that enabled further expansion of NLCs’ effective mar-ket reach; and 3) increasingly advanced revenue management and distributioncapabilities that allowed them to more carefully segment their market.

In addition to affecting change in the strategies of established NLCs, dereg-ulation also prompted the rapid growth of a new type of business model: the

15

Low Cost Carrier (LCC). A few LCCs began as intrastate carriers prior toderegulation that expanded their operations after 1978 (most famously South-west in Texas and Pacific Southwest in California), but the majority werefounded in the newly liberalized market environment in the late 1970s andearly 80s. The freedom to compete on price and frequency without involve-ment from the CAB was a major contributing factor to the well-documentedrise of the LCC business model in the United States, starting with SouthwestAirlines’ expansion in the 1980s (Francis et al., 2006; ben Abda et al., 2008;Gross and Luck, 2013).

By streamlining operations (e.g. operating a single fleet type, developingpoint-to-point networks), LCCs were able to achieve lower unit costs thanNLCs. This enabled the LCCs to offer lower fares while, in most cases, stillmaintaining profitability. Some LCCs developed innovative policies to increaserevenue by charging for services that were provided free of charge by net-work carriers. For example, People Express, founded in 1981, introduced a $3checked baggage fee and charged for onboard snack/meal service (Gross andLuck, 2013).

More recently, a third business model has emerged: the Ultra Low CostCarrier (ULCC). In the mid 2000s, as the gap between the unit costs of LCCsand NLCs in the U.S. narrowed (Tsoukalas et al., 2008), a market opportunityemerged for a new type of carrier with a focus on low costs to undercut eventhe LCCs’ cost structure.

The U.S. airline industry is a major component of the national economy- some estimates suggest 4-6% of the U.S. Gross Domestic Product can beattributed in some fashion to the industry (U.S. Federal Aviation Administra-tion, 2014; Airlines for America, 2017). Thus, understanding the state of theindustry and identifying key trends in air service are of great public interest.As the U.S. airline industry has trifurcated into the business models introducedabove, studying the industry through the lens of this three-model structurecan help provide insight into this major economic engine. Specifically, analysesof the evolution of airline business models can help inform thoughts on futuredevelopments and resulting impacts on all stakeholders of the U.S. air trans-portation system: the traveling public, airports, communities, governmentalentities, and air carriers alike.

1.2 Motivation for Research

The interplay between the NLC and LCC business models has been the focusof much recent academic literature, e.g. (Gillen and Morrison, 2003; Gross

16

and Luck, 2013). Many of these studies have focused on the characteristics ofLCCs, and whether a given airline should be considered an LCC or an NLC.The effects of NLC vs. LCC competition on other stakeholders in the U.S. airtransportation system have also been examined. For instance, the so-called“Southwest Effect” has been examined, where fares drop in communities whereSouthwest enters a given market (Windle and Dresner, 1995; Morrison, 2001).

However, this thesis will present evidence that the U.S. industry has di-verged into three separate business models: the NLC, the “hybrid” LCC, andthe Ultra-Low-Cost Carrier (ULCC). Thus it is a useful exercise to consider thestate of the industry under this paradigm with three dominant business mod-els. As each type of carrier has a unique structure, each business model canresult in different impacts on passengers, airports, and the industry landscapeat large.

The purpose of this thesis is to investigate the evolution of these businessmodels from 2006 to the present, focusing on some key changes in the industrythat occurred over this period, such as consolidation, capacity discipline, costconvergence between the NLCs and LCCs, and the emergence of the ULCCmodel. The evolution in airline networks and fleets over the past decade is alsocovered, including an examination of hub structures, aircraft utilization, stagelength, and connectivity. Additionally, this thesis will provide an analysis ofkey impacts of these trends on the broader U.S. air transportation system. Thisincludes an investigation into any changes base fares and pricing structuresamong U.S. carriers, as well as some broader impacts on airports, communities,and public policy.

This thesis addresses two main gaps in the current literature. First, itupdates previous literature about the NLC and LCC airline business models byupdating the evolution narrative through the present day (2016), incorporatingnew data. This thesis also addresses the emergence of the ULCC model andprovides an analysis of the industry taking into account this emerging businessmodel. The result is a comprehensive overview of recent developments in theU.S. airline industry relating to the business models adopted by U.S carriers.

1.3 Outline of Thesis

In Chapter 2, a more detailed history on the evolution of these business modelsis presented, and the types of business models are defined through a seriesof qualitative and quantitative analyses. After a brief overview of the U.S.airline industry prior to 2005, a detailed chronology of the industry from 2006to 2016 is presented. Key trends such as cost convergence between LCCs and

17

NLCs, consolidation of various carriers, and capacity discipline are reviewed.Important macro-level industry metrics such as capacity, unit costs, and otherfinancial data are studied to identify the driving forces behind these trends.Using this analysis as a basis, the U.S. carriers are then classified into one ofthe three categories of business models, focusing on cost, network, fleet, andrevenue structure.

Chapter 3 focuses on the development of network and fleet structures ofcarriers. It first examines the fleet development of U.S. airlines by reviewingtrends in key metrics such as average stage length and utilization (block hoursper day) and how these metrics differ between carrier types. Additionally,key developments such as the shift among NLC regional partners towards 76seat aircraft in favor of 50 seat regional jets are examined. Next, an analysisof evolution in carrier networks is presented. Following a general review ofthe types of network strategies associated with each business model, the keydevelopments in carriers’ networks are highlighted. Some of the general trendscovered include the consolidation of hubs among NLCs, the encroachmentof LCCs into major primary airports (such as Boston Logan and ChicagoO’Hare), and the diversity of network strategies pursued by ULCCs.

Chapters 4 and 5 present more detailed analyses of key impacts of trendsthat were observed in Chapters 2 and 3. In Chapter 4, general trends in faresand traffic are explored, focusing on how trends such as cost convergence haveaffected average fares and carriers’ unit revenue. Furthermore, the changingimpacts of the ULCC and LCC business models on market fares are stud-ied. Using data on ULCC, LCC, and NLC market presence, entry, and exitoutcomes over a six-year period, and market airfares from 2010-2015, we showthat ULCC presence has a significantly greater effect on reducing average basefares in U.S. domestic airline markets than presence by the more mature LCCs.

Chapter 5 covers the impacts of industry trends on U.S. airports andthe communities they serve. First, trends in carriers’ distribution of capac-ity among various categories of airports are analyzed. Then, we present anoverview covering the tendency of ULCCs and LCCs to serve secondary ”re-liever” airports and how this has changed over time. We also examine recenttrends in air service at smaller airports, exploring how the decline of 50-seatjet service by NLCs and additional capacity provided by ULCCs have affectedthese smaller communities. This chapter also contains an overview of recentpublic policy initiatives related to the domestic U.S. airline industry, includ-ing an overview of air carrier subsidies in the U.S., such as the Essential AirService (EAS) program.

Chapter 6 briefly concludes the thesis, highlighting key developments men-tioned above, and presents suggestions for future research.

18

Note: A modified version of Chapter 4 and selections from Chapter 2 havepreviously been published as “The Emergence and Effects of the Ultra LowCost Carrier (ULCC) in the U.S. Airline Indsutry” in the July 2017 issue ofthe Journal of Air Transport Management.

19

20

Chapter 2

Evolution of U.S. AirlineBusiness Models

In this chapter, an overview of some key recent trends in the U.S. airlineindustry will be presented. There will be a focus on how these trends affectedthe two traditional airline business models, Network Legacy Carriers (NLCs)and traditional Low Cost Carriers (LCCs). Furthermore, this covers how thesetrends helped to precipitate a new business model while causing significantchanges to the LCCs and NLCs, including how “cost convergence” led to ashift in LCC structure such that modern LCCs use a hybrid model borrowingaspects from both traditional LCCs and NLCs. Finally, an overview of thethree evolved business models present by 2015 in the U.S. airline industry isgiven, which highlights some of the notable differences between the businessmodel types. The section then concludes by classifying major airlines (in 2015)as a Network Legacy Carrier (NLC), a hybrid Low Cost Carrier (LCC), or anUltra Low Cost Carrier (ULCC).

Figure 2.1: Classification of select major U.S. carriers in 2006

21

To provide some context for the reader, the classification of selected majorU.S. carriers in 2006 is shown in Figure 2.1. In this classification, traditionalLCCs generally include many similar and well-established cost-saving prac-tices in their business models, such as using common and modern aircrafttypes with high block hour utilization, a simplified fare structure, and reduceddependence on Global Distribution Systems (GDSs) for ticket sales (Gross andLuck, 2013, p. 11). Meanwhile, as mentioned in the introduction, NLCs havehigher cost but offer comprehensive hub and spoke networks with increasedoptions through alliances and codeshares.

2.1 A Cyclic Industry

Since deregulation, the U.S. airline industry has been through many busi-ness cycles of increasing amplitude. The advent of deregulation introducedincreased volatility in the U.S. airline industry, and the economic realities ofa less regulated marketplace began to set in. The sinusoidal nature of theU.S. airline industry’s business cycles, expressed as total net income, as wellas their increasing amplitude, are clear in Figure 2.2.

Figure 2.2: U.S. Airline Industry Net Income Since 1978 - Source: Airlines forAmerica

22

This volatility has been a key factor in the evolution of both the NLC andLCC business models. Through each business cycle, the upstart LCCs thatwere not able to successfully achieve or maintain low costs eventually declaredbankruptcy or were merged into other carriers (e.g. People Express, mergedinto Continental). Additionally, NLCs that didn’t possess a strong enoughnetwork or suffered high costs themselves also were often forced into Chapter 11proceedings. Since deregulation, there have been over 100 bankruptcy filingsamong Part 121 carriers in the U.S. (Airlines for American, 2016a).

One of the reasons that this volatility exists is that passenger demand iscorrelated with the general economic conditions. However, due to the largeinvestments necessary to acquire aircraft and staff the airline appropriately,it is expensive for airlines to respond to poor economic conditions by cuttingsupply quickly (Belobaba et al., 2009, p. 154, 158, 287).

Furthermore, airlines have historically tended to over-order aircraft whenfinancing was available to do so (at the top of the business cycle) leaving themwith excess capacity during the next downturn, as new planes are not gener-ally delivered until a few years after purchase. For instance, in 2007 Boeingand Airbus booked upwards of 1,200 worldwide net orders each, presumablywith some aircraft scheduled for delivery during the 2009-2011 period. Thiscompares to 400 or fewer net orders each year during 2001-2004, with manyof these aircraft presumably being delivered in time to take advantage of the2006-2007 economic boom.

Table 2.1: Chapter 11 bankruptcy filings by major U.S. carriers 2002-2005 -Source: Airlines for American (2016a)

Carrier Date of Bankruptcy

US Airways 8/11/2002United Airlines 12/9/2002

Hawaiian Airlines 3/21/2003US Airways 9/12/2004

ATA Airlines 10/26/2004Aloha Airlines 12/30/2004

Northwest Airlines 9/14/2005Delta Air Lines 9/14/2005

Throughout the late 1980s and early 90s, the industry underwent a turbu-lent period defined by a series of mergers and bankruptcies among both NLCsand LCCs. The industry then saw a period of relative stability and growth

23

during the remainder of the 90s, much like the economy at large, only to besent into a crisis caused by the downturn in travel in the post-9/11 period.During 2002-2005, the majority of U.S. NLCs declared bankruptcy, while mostLCCs such as Southwest, and the fledgling JetBlue survived. Table 2.1 showsthe major bankruptcy filings by U.S. carriers during this period. Notablyabsent is American Airlines, which suffered from higher labor costs than itscompetitor NLCs until its own bankruptcy in 2011.

Helped by the ability to discharge pensions and labor contracts through theU.S. Chapter 11 bankruptcy process, NLCs were on the road to recovery whenfuel prices spiked in early 2008. By slashing labor costs through bankruptcy,NLCs were able to narrow the gap between their costs and the costs of LCCs(see Section 2.2). However, when fuel prices increased from $2.20 per gallonin July 2007 to $4.16 per gallon a year later (EIA, 2016), many airlines couldnot cope and set off the next round of bankruptcies and mergers (see Section2.3).

2.2 Cost Convergence

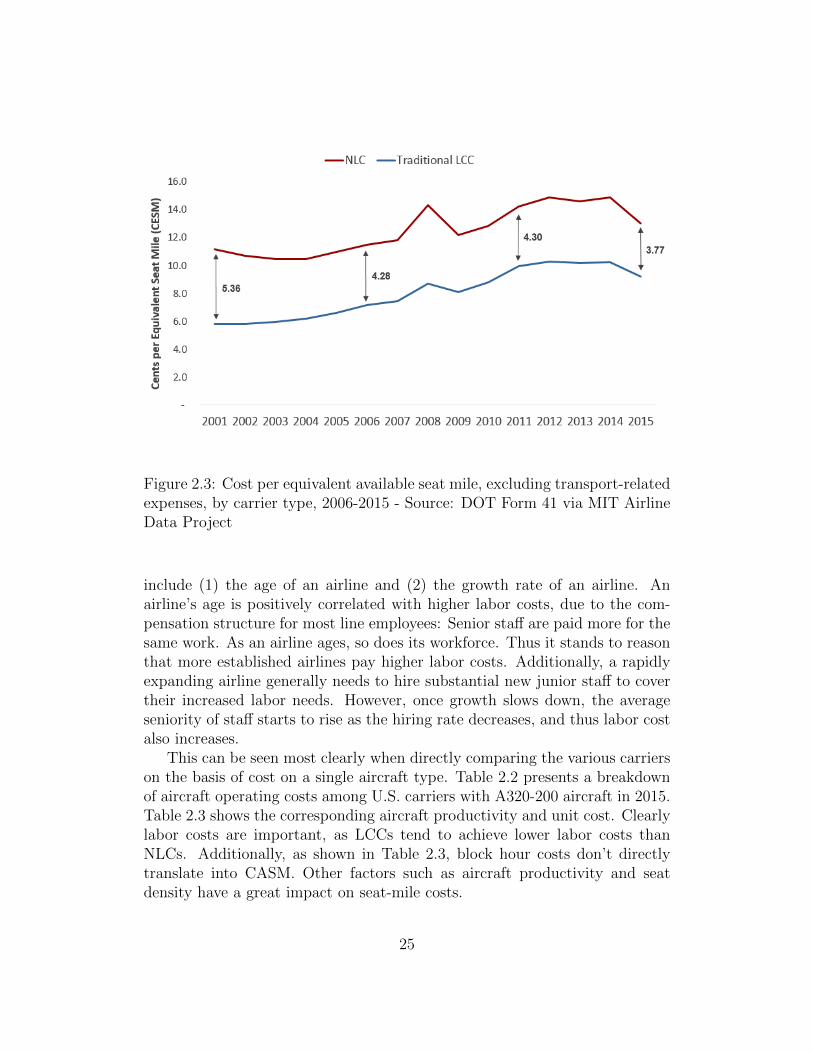

A key recent trend in the airline industry has been the cost convergence be-tween traditional LCCs and NLCs. This refers to the gradually narrowinggap in unit costs between NLCs and LCCs, which has been caused by both arelative increase in LCC unit costs and a relative decrease in NLC unit costs.Although this effect was most pronounced in the early-to-mid 2000s, there isstill some ongoing convergence between NLCs and LCCs as shown in Figure2.3.

As mentioned previously, a large portion of LCC success resulted from laborcost savings over traditional NLCs. After the rapid period of LCC expansionin the early 2000s, the legacy carriers went through a period of restructuringas part of the bankruptcy process. As a result of Chapter 11 bankruptcylaws in the U.S., the legacy carriers were able to significantly restructure laborcontracts to reduce overall cost of operation significantly.

As shown in Figure 2.4, the labor contracts negotiated in bankruptcycaused the gap between LCC and NLC costs to be reduced significantly. Thegap in labor cost per equivalent seat mile (LCESM) between NLCs and tra-ditional LCCs decreased from 2.36 cents in 2002 to 0.97 cents by 2006, whichis greater than the 0.62 reduction in the overall CESM gap between the twocarrier types over the same period. However, this does not account for thesubsequent rise in both NLC and LCC unit cost.

Tsoukalas et al. (2008) found that two of the key drivers of labor cost

24

Figure 2.3: Cost per equivalent available seat mile, excluding transport-relatedexpenses, by carrier type, 2006-2015 - Source: DOT Form 41 via MIT AirlineData Project

include (1) the age of an airline and (2) the growth rate of an airline. Anairline’s age is positively correlated with higher labor costs, due to the com-pensation structure for most line employees: Senior staff are paid more for thesame work. As an airline ages, so does its workforce. Thus it stands to reasonthat more established airlines pay higher labor costs. Additionally, a rapidlyexpanding airline generally needs to hire substantial new junior staff to covertheir increased labor needs. However, once growth slows down, the averageseniority of staff starts to rise as the hiring rate decreases, and thus labor costalso increases.

This can be seen most clearly when directly comparing the various carrierson the basis of cost on a single aircraft type. Table 2.2 presents a breakdownof aircraft operating costs among U.S. carriers with A320-200 aircraft in 2015.Table 2.3 shows the corresponding aircraft productivity and unit cost. Clearlylabor costs are important, as LCCs tend to achieve lower labor costs thanNLCs. Additionally, as shown in Table 2.3, block hour costs don’t directlytranslate into CASM. Other factors such as aircraft productivity and seatdensity have a great impact on seat-mile costs.

25

Figure 2.4: Labor cost per equivalent seat mile by carrier type, 2000-2015 -Source: DOT Form 41 via MIT Airline Data Project

Table 2.2: Direct costs of A320-200 block hour costs by carrier (U.S. units),2015 - Source: MIT Airline Data Project and US DOT Form 41

Total Aircraft Op- # inAirline Crew Fuel/Oil Maintenance Ownership erating Cost (AOC) Fleet

Delta $ 1001 $ 1629 $ 783 $ 556 $ 3969 69Frontier $ 846 $ 1657 $ 412 $ 1000 $ 3915 25United $ 927 $ 1493 $ 727 $ 551 $ 3697 97JetBlue $ 819 $ 1510 $ 762 $ 414 $ 3506 130American $ 844 $ 1220 $ 853 $ 414 $ 3331 51Virgin $ 582 $ 1314 $ 443 $ 906 $ 3246 53Spirit $ 562 $ 1258 $ 354 $ 845 $ 3019 45Allegiant $ 435 $ 1378 $ 392 $ 448 $ 2653 16

26

Table 2.3: Costs and productivity of A320-200 block hour costs by carrier(U.S. units), 2015 - Source: MIT Airline Data Project and US DOT Form 41

AirlineAOC per Average Seats per Aircraft Day

CASMBlock Hr Stage Length per A/C Departures Block Hrs ASMs

Delta $3969 924 151 3.9 8.2 544,588 0.0595Frontier $3915 1141 180 4.3 10.7 861,131 0.0488United $3697 1081 150 3.4 8.1 548,482 0.0543JetBlue $3506 1308 150 3.9 11.2 762,742 0.0513American $3331 952 150 4.3 9.6 639,418 0.0501Virgin $3246 1546 148 2.9 9.8 671,675 0.0473Spirit $3019 994 178 5.0 11.2 893,076 0.0377Allegiant $2653 907 177 4.4 9.1 706,282 0.0343

Both airline age and growth rate are partly responsible for the steady risein LCC labor unit cost observed since 2006, and is shown in Figure 2.4. Theannual systemwide year-over-year change in ASMs at NLCs and LCCs overthis period is found in Figure 2.5. That chart clearly illustrates the slowingof LCC growth around the 2006-2008 period, and subsequent annual growthrates much lower than the historical average. This is a driving factor behindthe rise in LCC labor unit costs.

Figure 2.5: Year-over-year change in available domestic seat miles by carriertype, 2000-2015 - Source: DOT Form 41 via MIT Airline Data Project

27

More broadly, the phenomenon of cost convergence between LCCs andNLCs has prompted somewhat of an evolution in both business models. Dueto the smaller differences in unit costs, LCCs are no longer able to undercutNLCs in terms of fare quite as much as they did in the past. As will beshown later in this thesis, LCCs have changed their network strategy to tryand compete more directly with NLCs for higher-yield domestic traffic.

2.3 Consolidation

Since deregulation, mergers and acquisitions have played a significant role inshaping the landscape of the U.S. airline industry. According to the nationaltrade association Airlines for America (A4A), 34 mergers and acquisitionsamong major passenger carriers in the industry have been completed since1978 (Airlines for America, 2016b). Some of the more notable instances ofmerger and acquisition (M&A) activity have included the Texas Air Corpo-ration takeover of Continental in 1982, the mergers of Delta/Western, North-west/Republic, and TWA/Ozark in 1986, Southwest’s takeover of Morris Airin 1993, and American’s acquisition of TWA in 2001.

Consolidation is especially attractive to firms in the airline industry, ashorizontal mergers in the industry have been shown to significantly increasemarket power, in addition to generating cost efficiencies (Knapp, 1990). Thisis especially true for Network Legacy Carriers (NLCs), as part of their valueproposition is offering a comprehensive network to their passengers. However,airlines have many levels of cooperation that do not necessarily incur the samecomplexity of a merger or acquisition. Code sharing, where partner airlinessell inventory on each other’s flights, or anti-trust immune joint ventures (ATI-JVs), where partner airlines coordinate schedules and pricing (and often sharerevenues/costs) are two forms of partnership short of a merger - see Figure 2.6.Some recent examples of such partnerships in the U.S. include Alaska’s codeshare agreements with Delta and American, or Hawaiian’s code shares withVirgin America and JetBlue. ATI-JVs are generally only used in situationswhere a merger is not possible, usually with a foreign partner airline (such asUnited and Lufthansa).

While these partnerships provide some benefits, they do not achieve the ef-ficiencies of a full merger or acquisition (e.g. cross-fleeting and cross-crewing).Thus, there are synergies that could not necessarily be reached by lesser formsof cooperation such as code sharing or interlining alone. This is why bothNLCs and LCCs in the U.S. have experienced another recent spike in M&Aactivity.

28

Figure 2.6: Types of partnerships between airlines organized by level of inte-gration and profitability improvement (Swelbar, 2015)

Table 2.4: Mergers and acquisitions among U.S. passenger airlines since 2006- Source: Airlines for America (2016b)

Carriers Initiated Closed Combined Carrier

Pinnacle / Colgan 1/18/2007 1/18/2007 Pinnacle / ColganSouthwest / ATA 11/19/2008 Southwest AirlinesRepublic / Midwest 6/23/2009 7/31/2009 Republic AirwaysRepublic / Frontier 8/14/2009 10/1/2009 Republic AirwaysDelta / Northwest 4/14/2008 12/31/2009 Delta Air LinesPinnacle / Mesaba 7/1/2010 7/1/2010 Pinnacle / MesabaUnited / Continental 5/3/2010 10/1/2010 United AirlinesSkyWest / ASA / ExpressJet 8/4/2010 11/15/2010 SkyWest AirlinesSouthwest / AirTran 9/27/2010 5/2/2011 Southwest AirlinesUS Airways/AMR/American 2/14/2013 12/9/2013 American AirlinesAlaska / Virgin America 4/4/2016 12/14/2016 Alaska Airlines

Notably, two of the three ”mega-mergers” in the past decade were initiated

29

in the depths of the financial crisis. The Delta-Northwest merger was initiatedon April 14, 2008, after a slew of airline bankruptcies due to a spike in fuel:Aloha, ATA, Skybus, and Frontier all declared bankruptcy (with all but thelatter ceasing operations) in the two weeks preceding the Delta-Northwestmerger announcement. The United-Continental merger was initiated in spring2010, after both carriers had report net losses the year prior. This suggeststhat these carriers merged for the increased market power which enabled theindustry to reduce overall capacity, as explored in Section 2.4.

As shown in Tables 2.5 and 2.6, after these mega-mergers the largest fourcarriers remained the same in 2006 as in 2015 (American, Southwest, Delta,and United), albeit in a slightly different order. The most notable differenceis in market concentration metrics at the bottom of each table: These fourcarriers went from carrying 56.9% of domestic traffic (as measured by share oftotal domestic O&D passengers) to 78.7%.

Table 2.5: Largest U.S. Airlines in 2006 including regional partners - Sources:US DOT T-100 & DB1B data, annual reports

2006 U.S. Summary1 American Southwest Delta UnitedRanking by seats 1 2 3 4Seat departures (millions) 154.2 148.0 139.5 119.9ASMs (millions) 186,095 92,222 145,920 153,910RPMs (millions) 148,390 67,383 114,523 125,980Load factor 79.7% 73.1% 78.5% 81.9%Fleet size (mainline/regional) 697/306 481/0 440/516 460/290Share of U.S. onboard pax 14.6% 12.6% 13.0% 11.5%Share of domestic O&D pax 13.8% 18.5% 12.9% 11.7%Total top 4 enplanement share 51.7%Total top 4 domestic O&D share 56.9%

1Data excludes flights not originating or arriving in the U.S.

30

Table 2.6: Largest U.S. airlines in 2015 including regional partners - Sources:US DOT T-100 & DB1B data, annual reports

2015 U.S. Summary2 American3 Southwest Delta UnitedRanking by seats 1 3 2 4Seat departures (millions) 244 184 211 168ASMs (millions) 267,115 139,573 241,191 246,382RPMs (millions) 221,783 116,775 205,112 205,786Load factor 83.0% 83.7% 85.0% 83.5%Fleet size (mainline/regional) 946/325 704/0 809/482 715/521Share of U.S. onboard pax 22.4% 16.6% 19.7% 15.6%Share of domestic O&D pax 21.3% 24.1% 19.2% 14.1%Total top 4 enplanement share 74.3%Total top 4 domestic O&D share 78.7%

There has been consolidation among the LCCs as well. As previously illus-trated in Table 2.4, Southwest and AirTran merged in 2011. This merger pre-sented some operational challenges, such as the integration of AirTran’s morediverse fleet. One of the key aspects of Southwest’s business model (and ofmany LCCs in general) has been a homogeneous fleet (Gross and Luck, 2013).This leads to operational advantages and cost efficiencies through simplify-ing maintenance, crewing, and scheduling. Prior to the merger with AirTran,Southwest operated one of the largest Boeing 737-only fleets in the world.However, AirTran had dozens of Boeing 717s as well as 737s. Rather thanadapting their model to two fleet types, Southwest chose to divest of the 717ssoon after the merger. However, they did expand beyond the traditional LCCdomain in the U.S. by using AirTran’s international rights as a springboardto begin service to Central America and the Caribbean.

The most recent merger (as of this writing) is the Alaska Airlines takeoverof Virgin America. As of 2015, both carriers fit within a hybridized LCCcategory that will be defined in Section 2.5, so this merger indicates that man-agement teams feel that mergers can benefit LCCs, even without as robust ahub & spoke network. Even with a merger of two smaller players, market powercan be gained, although too high of an increase in market power can result inthe denial of a merger by the U.S. Department of Justice (DOJ) on anti-trustgrounds. As a condition of approving this merger, the DOJ required Alaska

2Data excludes flights not originating or arriving in the U.S.3includes US Airways data

31

to drop its codeshare agreement with American Airlines on select routes, toensure the two carriers would compete on routes where external competitionwould be limited.

One of the most noticeable impacts of these recent “mega-mergers” hasbeen the overall effect on U.S. market concentration and carriers’ ability tofocus on profitability rather than chasing market share. This partially enabledthe emergence of another trend, known as capacity discipline.

2.4 Capacity Discipline

As mentioned in Section 2.1, due to long lead times in aircraft production,there is often a multi-year lag in phase between when new aircraft orders areplaced and delivered. Since orders for new aircraft tend to be placed nearthe top of the business cycle (when capital is available and forecasts are oftensunny), and as a result that airlines do not necessarily receive new aircraft atthe ideal economic time for expansion.

Historically, this meant that there was often a mismatch of capacity anddemand in the U.S. air travel industry, especially in periods where demandmay be slow. However, since 2006 this has not been the case. In 2008, airlinesbegan “rationalizing” their schedules: Even after a relatively slow period ofexpansion after the mid-2000s bankruptcies, airlines believed that there wasstill too much capacity in the market, especially given the occurrence of theGreat Recession and a fuel price spike (Wittman, 2014a). Thus, airlines pulledeven more capacity out of the market than changes in demand would suggest.

Figure 2.7 compares year-over-year changes in U.S. gross domestic product(GDP) – a proxy for overall changes in demand – and U.S. domestic capac-ity (in ASMs). In the period from 2008 to early 2011, the YOY reductionin capacity outpaced the decrease in GDP, clearly illustrating this period ofschedule rationalization.

After capacity had been “rationalized”, and the economy resumed grow-ing at a moderate pace, one might expect airlines to return to the previousparadigm of growing slightly faster than GDP. After all, since deregulation,airlines in the U.S. had averaged 4-6% annual capacity growth (compared toapproximately 2% GDP growth rate) (Franke, 2004). The additional capacityresulted in a slow decline in yields, which were historically somewhat offset bycost efficiencies developed over time.

However, airlines reacted differently after the economy began improvingin 2011, as shown in Figure 2.7. Higher fuel prices plus a different compet-itive environment (considering the mega-mergers mentioned in the previous

32

Figure 2.7: Comparison between changes in GDP and changes in U.S. domesticcapacity (ASMs) 2006-2016

section) allowed airlines to carefully control their capacity growth and insteadfocus more intently on increasing profitability. This resulted in a period of“Capacity Discipline” where carriers “restricted seat capacity growth, even asthe economy started to recover ... locking in capacity at lower rationalizedlevels” (Wittman, 2014a).

Although most carriers practiced some form of schedule rationalizationduring the 2007-2010 time period, capacity discipline was not evenly practicedamong the different carrier types. Figure 2.8 shows the changes in domesticcapacity by carrier type, indexed to 2010. Over the 6 year period from 2010-2015, NLCs only increased total domestic ASMs by 2.9%, whereas increasingly“hybridized” LCCs (including Alaska Airlines) and the emergent Ultra LowCost Carriers (ULCCs) grew 22.6% and 77.0%, respectively, albeit from amuch smaller base. Since NLCs generally had the lowest profit margins, werethe dominant carriers by size, and generally carried higher-yield traffic theyhad more incentive (and room) to reduce capacity, pushing yields higher. Ac-cording to data compiled by the MIT Airline Data Project, system passengeryields at NLCs increased from 12.90 cents per mile in 2010 to 14.59 cents permile in 2015 - a 13.2% increase, compared to a 10.8% increase at traditionalLCCs over the same period.

33

Figure 2.8: Changes in U.S. domestic capacity by carrier type 2010-2015,indexed to 2010

2.5 The Emerging ULCC

The trends discussed previously in this chapter, such as cost convergence, con-solidation, and capacity discipline, have affected the business models of bothtraditional LCCs and NLCs. LCCs have been moving steadily “upmarket”as they lose their cost advantages (becoming somewhat of a hybrid between“traditional” LCCs and NLCs), while NLCs have been consolidating whilecontrolling capacity somewhat to greatly increase profitability. However, thesetrends and the subsequent evolution of hybridized LCCs and NLCs have lefta gap in the marketplace for a new business model to emerge.

The term “Ultra-Low-Cost Carrier” has become increasingly commonplacein the U.S. airline industry since being popularized by Spirit Airlines’ formerCEO Ben Baldanza in 2010. U.S. carriers such as Frontier Airlines, SpiritAirlines, and Allegiant Air have been referred to as ULCCs by media outletssuch as the Wall Street Journal and Forbes (Nicas, 2012; Martin, 2016). Ina 2014 report, the U.S. Government Accountability Office (GAO) noted thatSpirit and Allegiant are often referred to as ULCCs, in part due to their lowerbase fares and their high fees for ancillary services. (GAO, 2014).

Other attempts to define ULCCs have relied on qualitative characteristicssuch as a strategic focus on price (vs. passenger experience), or lack of interlineagreements (Thomas and Catlin, 2014). However, these qualitative character-istics do not allow us to distinctly define ULCCs. For instance, Southwestdoes not maintain interline agreements, much like ULCCs, but Southwest’s

34

business model is different in other ways from ULCCs such as Spirit.In this section, we provide a brief outline of the evolution of the ULCC

business model, from its beginnings with Ryanair in the early 1990s. Wealso propose a comprehensive definition of the ULCC model, wherein: (1)ULCCs achieve significantly lower costs than LCCs or other network carriers;(2) ULCCs agressively collect ancillary revenue for unbundled services; and(3) ULCCs lag LCCs in total system unit revenue, despite their collection ofancillary revenue. Through an analysis of U.S. carriers, we find that in 2015three carriers meet these criteria: Allegiant, Frontier, and Spirit.

There is limited literature on ULCCs, and only a small subset of this workfocuses on carriers in the United States. In a study of European airlines,(Klophaus et al., 2012) recognize that there exists significant heterogeneity ofbusiness models within the LCC segment. They define a quantitative consoli-dated LCC index that can be used to classify carriers based on their adherenceto core facets of the LCC business model, e.g. fleet homogeneity, checked bag-gage fees, and simplified fare structures. The highest scoring airlines on theindex, including Ryanair and Wizz Air, were referred to as “pure LCCs,” whichwould be similar to the ULCC model in the U.S.

In the United States, one of the few papers focusing on a ULCC specif-ically is (Rosenstein, 2013), who argues in a case study that Spirit Airlineshas diverged from traditional LCCs such as Southwest Airlines on the basisof Spirit’s extremely low “unbundled” fares and their aggressive collection ofancillary revenues. (Jiang, 2014) highlights ULCCs as a separate category inan analysis of airline productivity and cost performance, but does not providea framework for the classification of carriers into the three types studied: UL-CCs, LCCs, and Network Legacy Carriers (NLCs). Only a basic qualitativeanalysis is used to classify airlines into these categories, similar to the methodsused in the GAO report (GAO, 2014).

Allegiant Air, which commenced operations in 1998, was initially focusedon the Las Vegas, Nevada and Lake Tahoe casino charter markets. Afterdeclaring bankruptcy and reorganizing in 2001, Allegiant began its transitionto the ULCC model. As part of this transition, a key priority was growingancillary revenue collection. In 2003, Allegiant collected $3.40 in ancillaryrevenue per scheduled passenger according to filings with the U.S. Securitiesand Exchange Commission (SEC). By 2007, Allegiant’s ancillary revenue hadgrown to $21.53 per passenger segment. Around this time, in late 2006, SpiritAirlines (previously a small LCC based in Detroit) also began its transitionto the ULCC model. By introducing checked baggage fees and charging foronboard food and beverage, Spirit collected $10.96 in ancillary revenue perpassenger segment in 2007. By charging for more ancillary services, these car-

35

riers could maintain passenger revenue while offering lower base fares, thusensuring their itineraries would be among the first listed on internet distribu-tion sites (e.g. Expedia), attracting more traffic (Belobaba et al., 2009, p. 458,461).

Figure 2.9: Allegiant and Spirit traffic and capacity, in billions of RPMs andASMs, 2005-2015 (Source: Innovata SRS schedule data via Diio Mi)

The first ULCC start-up in the U.S. was also founded in 2007: Skybus,based in Columbus, was explicitly founded to take advantage of the narrowingcost gap between LCCs and NLCs (Rose, 2007). The Skybus management,which had experience at Ryanair, set out to emulate that European carrier’sstyle of service in the United States. From its inception, Skybus offered fully-unbundled fares in which no optional services were included with the price ofthe ticket. While Skybus charged low base fares, with 10 seats available at $10on every flight, checked bag fees ranged from $5 for the first bag to $50 forthe third bag, and charges for onboard food and beverage items ranged from$2-$10. Skybus also lowered cost through a performance-based wage structure:for instance, Skybus’ flight attendants were only paid a base wage of $11 perhour, but also received commissions from onboard sales (Rose, 2007). Whenthe price of oil nearly doubled from late 2007 to early 2008, Skybus quicklyexhausted its initial capital of $160 million and declared bankruptcy, ceasingoperations in April 2008.

Unlike Skybus, Allegiant and Spirit were both able to survive during thistumultuous period for the U.S. airline industry. As shown in Figure 2.9, Alle-

36

giant Air continued to grow capacity and traffic every year 2005-2015, includingduring the 2008-2009 period which represented a global recession and a timeof contraction for most U.S. carriers. Allegiant also remained profitable ev-ery year over the 2005-2015 timeframe. Spirit Airlines, although experiencinga temporary cut in capacity and traffic during the recession, quickly begangrowing capacity and filed an initial public offering in 2010. The airline hassince been profitably growing traffic (exceeding 10% annual traffic growth ev-ery year since 2010) and capacity through 2015 at rates exceeding the NLCsand LCCs.

The third present-day ULCC in the U.S. is Frontier Airlines. The modernFrontier Airlines was founded in 1994 as an LCC based in Denver. Mostof its flights were oriented around its Denver hub until the carrier declaredbankruptcy in April 2008. While in bankruptcy, Frontier was acquired byRepublic Airways, a regional carrier that primarily operated feeder flights forthe NLCs. Frontier went through an extended period of restructuring byRepublic, and was eventually acquired by a private equity firm. Frontier thenbegan its transformation into a ULCC, much like Spirit five years earlier. By2014, Allegiant, Frontier, and Spirit had the lowest unit costs of the major UScarriers, as we show in Section 2.5.1, while also offering fully unbundled faresand aggressively collecting ancillary revenue (including charging for carry-onbaggage and all seat assignments).

2.5.1 Characteristics of the ULCC model

As noted in Klophaus et al. (2012), previous efforts to classify LCCs involvedevaluating carriers on the basis of a variety of mostly qualitative characteris-tics. Despite the similarities between the development of LCCs and ULCCs,qualitative characteristics alone are not sufficient to define the ULCC businessmodel. Thus, a more data-driven definition of the ULCC model is needed. Wepropose that an airline is a ULCC if:

1. It has significantly lower costs than even other “low-cost” carriers;

2. It generates a significant portion of its operating revenue through thesale of unbundled, ancillary services; and

3. As a result of lower base fares, it realizes lower unit revenues than othercarriers, even when ancillary revenues are taken into account.

A key feature of the ULCC business model is the ability to achieve lowercosts than their LCC and NLC competitors. Figure 2.10 shows a comparison

37

of the major US carriers on the basis of their unit costs, excluding fuel andtransport-related expenses.4

Figure 2.10: System CASM ex transport-related expenses & fuel vs. meanstage length (2014) Sources: (US DOT Form 41 via MIT Airline Data Project)

When considering the expected negative relationship between stage lengthand unit cost (Tsoukalas et al., 2008), the carriers can be separated into threedistinct categories: ULCCs, hybrid LCCs, and NLCs. In 2014, the ULCCs onaverage achieved 18% lower unit costs than LCCs, and 31% lower unit coststhan traditional NLCs, even without adjusting for differences in stage length.As noted by Jiang (2014), much of the cost differential between LCCs andULCCs can be attributed to differences in unit labor costs. We found that thelabor cost differences between ULCCs and LCCs described by Jiang (2014)remain, as shown in Figure 2.11. Even when considering differences in meanstage length, Spirit and Allegiant achieved substantially lower labor costs perenplanement than LCCs. Whether the ULCCs can maintain this labor costadvantage remains an open question; airlines with low labor costs have his-torically struggled to maintain this competitive advantage, as their workforceinevitably grows more senior and average pay rises accordingly (Tsoukalas etal., 2008).

4Like Tsoukalas et al. (2008), we use this adjusted measure of unit cost in order to moredirectly compare airlines’ internal cost structures, as fuel- and transport-related expensescan include inconsistent costs (e.g. NLC capacity purchase payments to regional carriers)

38

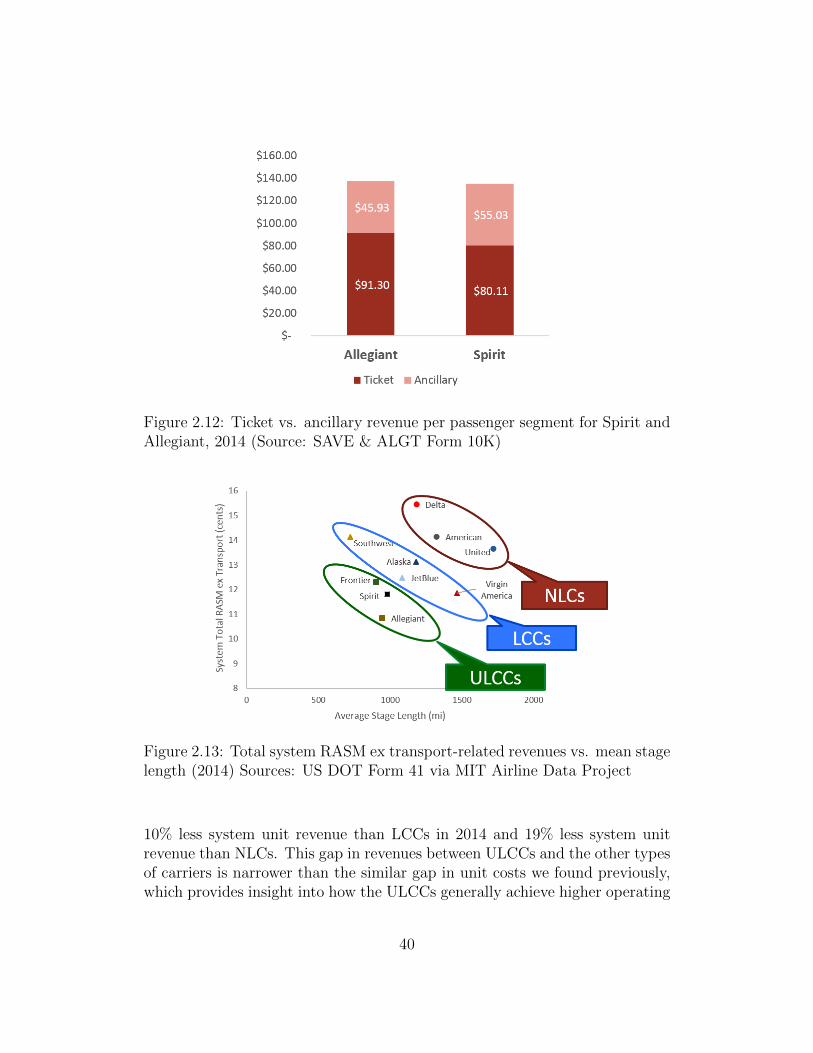

Figure 2.11: Average cost per enplaned passenger among select ULCCs andLCCs, 3Q15 (Source: ALGT investor presentations)

Another key component of the ULCC model is the collection of ancillaryrevenues after “unbundling” their fares (Rosenstein, 2013). Unbundled faresonly include a seat from origin to destination in the base ticket price; servicessuch as checked baggage, in-flight entertainment, and food & beverage are alloffered for an extra charge (Vinod and Moore, 2009). In a fully unbundledfare environment, airlines attempt to collect fees for an even wider variety ofancillary services, such as printing boarding passes at the airport and stowinga bag in the overhead compartment.

As shown in Figure 2.12, we found ancillary revenue at ULCCs Allegiantand Spirit accounted for 33% and 41% of total passenger revenue in 2014,respectively.5 A similar analysis in 2010 by the German Society of TourismResearch, as cited in Gross and Luck (2013, p. 13), found that ancillary revenueat traditional LCCs such as JetBlue and Southwest generally accounts forbetween 5-15% of total passenger revenue, a significant difference.

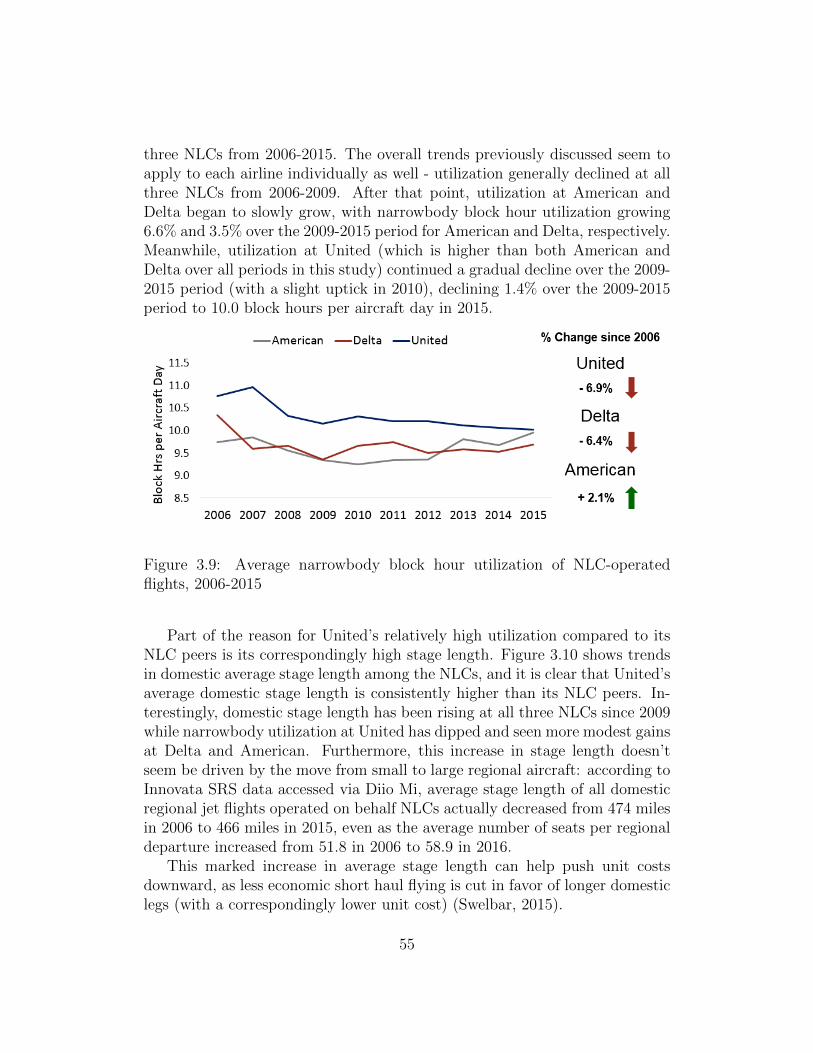

Despite the additional ancillary revenue generated by ULCCs, these carri-ers still lag LCCs and NLCs in total system unit revenue. Figure 2.13 showsthat the carriers fall into three groups based on their total system unit revenue(excluding transport-related revenues). We found ULCCs on average collected

that could skew the results.5No detailed data on Frontier ancillary revenue is available, as the company was taken

private in 2013 by Indigo Partners as it underwent its transition to a ULCC.

39

Figure 2.12: Ticket vs. ancillary revenue per passenger segment for Spirit andAllegiant, 2014 (Source: SAVE & ALGT Form 10K)

Figure 2.13: Total system RASM ex transport-related revenues vs. mean stagelength (2014) Sources: US DOT Form 41 via MIT Airline Data Project

10% less system unit revenue than LCCs in 2014 and 19% less system unitrevenue than NLCs. This gap in revenues between ULCCs and the other typesof carriers is narrower than the similar gap in unit costs we found previously,which provides insight into how the ULCCs generally achieve higher operating

40

margins than other carriers. That is, the cost advantages that the ULCCscurrently hold over LCCs and NLCs outweigh the revenue disadvantages asso-ciated with these carriers’ strategies. However, this suggests that the continuedprofitability of ULCCs depends in part on their ability to maintain their costadvantages over LCCs.

After evaluating US carriers, we found that on the basis of unit cost, unitrevenue, and ancillary generation, airlines consistently fall into one of the threecategories of carriers. As such (and based on the analyses we conducted earlierin this section), we classify the major US carriers as shown in Table 2.7 below.Throughout the remainder of this thesis, this classification scheme is used todetermine pricing effects of ULCC presence and market entry on airfares.6

Table 2.7: Selected Major US Airlines by Category

ULCCs LCCs NLCsAllegiant Alaska7 AmericanFrontier JetBlue DeltaSpirit Southwest United

Virgin America

6Carriers that have since merged over the 2010-2015 interval are considered to be in thesame category as the current, merged carrier

7Throughout this thesis, we categorize Alaska as an LCC based on its unit costs and unitrevenues as evaluated in Section 2, although its effects on market fares are more similar toNLCs, as shown in Section 3

41

42

Chapter 3

Evolution of U.S. AirlineNetwork and Fleet Structures

3.1 Background and Methods

In the previous chapter, the recent evolution of U.S. airline business modelswas discussed. At the core of every airline’s operations are its network andfleet structure. This chapter aims to provide an overview of changes in carriernetworks and fleets over the past decade, within the NLC/LCC/ULCC busi-ness model framework introduced in Chapter 2, in order to further explore thedifferences between airline business models and provide context for the rest ofthe thesis.

Figure 3.1: Key network and fleet questions with associated metrics

Figure 3.1 summarizes the two key research questions that we seek toanswer in this section:

43

1. How are airlines providing capacity? In order to understand thestructure of airline networks, it is important to understand how they gen-erate capacity. The first step is to evaluate an airline’s fleet compositionand size, as their fleet determines how much and what kinds of capacitythey can provide. Another component of this analysis is evaluating somemacro-level fleet and network trends, such as average stage length andaircraft utilization rates, as these give an overall picture of an airline’sability to provide capacity. These metrics also enable relevant time seriesanalyses that provide context for an airline’s network evolution.

2. Where are airlines allocating capacity? This is a key question inthe analysis of airline network structure. Understanding where an air-line allocates capacity provides insight into its strategic decisions, andhelps us understand what impacts those decisions may have on otherstakeholders in the U.S. air transportation system (e.g. passengers, air-ports/communities, competitor airlines). To answer this question, wewill use schedule data to show how each airline distributes its capacity(in terms of seat departures) by station, and also how airlines contributeto “connectivity” at each airport. Conducting this analysis will enabletime series comparisons to see how individual airlines’ networks and air-line business models have evolved since 2006. Furthermore, it will allowcomparison of network structures between different business models andbetween different carriers operating under similar business models.

Throughout this chapter, in an endeavor to make more relevant time-seriescomparisons, data for all carriers includes merged entities as of December2015. For example, data on American (AA) includes all legacy American,US Airways (US), and America West (HP) data for the 2006-2015 period.Additionally, the constituent entities of each carrier category (NLC, LCC,ULCC) are defined in Table 2.7. Finally, most statistics are calculated on thebasis of primary marketing carrier, as including regional operations in analysescan be of practical relevance when considering network structure. However,analyses that depend on Form 41 data (such as block hour utilization) arecalculated on the basis of operating carrier, as that is how the data is reported,and there is no way to separate Form 41 equipment statistics for regionalcarriers that operate for multiple mainline carriers. This is also noted in eachanalysis, but it is helpful to point out here.

44

3.1.1 Connectivity Model

Across all disciplines, one key metric used to evaluate a given network’s re-silience is the concept of “connectivity.” Additionally, a fundamental aspect ofan airline is the connection of airports (nodes) in a network. Thus, an investi-gation into airline networks would be remiss in excluding some quantificationof airport connectivity. In this application to airline networks, we’ll use theAirport Connectivity Quality Index (ACQI) as a proxy for true network con-nectivity. The ACQI is one of the two connectivity models for airline networksdeveloped at MIT, and is described in full in (Wittman, 2014a). The goal ofthe ACQI model is to capture the relative levels of service provided by airlinesat each node (airport) in the U.S. airline network based on the quality andquantity of non-stop and one-stop destinations served, as well as the frequencyof that service.

ACQIa = Σh∈Hfa,hda,hwh + αΣh∈Hd′

a,hwh (3.1)

Equation 3.1 describes the model, where the ACQI score of airport a isbased on the sum of the connectivity provided by nonstop flights (the firstsummation term) and the connectivity provided by one-stop flights (the secondsummation term), weighted by a desirability factor α ≤ 1, representing thepreference for nonstop service over one-stop service. In the nonstop term,for each hub type h, fa,h represents the average number of daily flights fromairport a to airports of hub type h, and da,h represents the number of airportsof hub type h with nonstop service to airport a. In the one-stop term, d′a,hrefers to the number of destinations that can be reached from airport a viaone-stop on-line or same-alliance connections. In both terms, wh representsthe relative importance of each hub type - this is used to help quantify thefact that one daily frequency to Los Angeles (LAX) is likely more conduciveto connectivity than one daily frequency to Fargo, ND (FAR), for example.

To illustrate how this model works, consider the schematic presented inFigure 3.2. In this case, airport A has two nonstop daily frequencies each toone large (L) hub H and small (S) hub G, and additionally has access to 4incremental one-stop small hubs via H. For the sake of this example, alsoassume α = 0.125, and the weights of large hubs and small hubs are wL = 1and wS = 0.05. Thus, the ACQI score of airport A can be computed as follows:

ACQIA = fA,LdA,LwL + fA,SdA,SwS + αd′A,SwS

= 2× 1× 1 + 2× 1× 0.05 + 0.125× 4× 0.05 = 2.125

Another important aspect of the ACQI model is that it does not double-

45

Figure 3.2: Example schematic of Airport Connectivity Quality Index (1)(Wittman, 2014a)

count duplicative connectivity. For example, if Des Moines (DSM) has non-stop service to Chicago (ORD), then the one-stop connectivity to Chicago(ORD) via Minneapolis (MSP) will not also be included. Furthermore, if DesMoines (DSM) doesn’t have non-stop service to San Francisco (SFO), but hasone-stop service via both Chicago (ORD) and Denver (DEN), the one-stopconnectivity to San Francisco will only be counted once. This is illustratedin a generic example in Figure 3.3. In this example, airport A has non-stopservice to an additional large hub K, as well as increased frequency of serviceto large hub H.

Figure 3.3: Example schematic of Airport Connectivity Quality Index (2)(Wittman, 2014a)

Under the same assumptions from the previous example, the ACQI scorein this case would be computed as follows:

46

ACQIA = fA,LdA,LwL + fA,SdA,SwS + αd′A,SwS

= 3× 2× 1 + 2× 1× 0.05 + 0.125× 5× 0.05 = 6.131

Domestically, the hub types used for the ACQI model are the categoriesdefined by the U.S. Federal Aviation Administration (FAA), where large hubsare the top 30 airports by enplanements in 2015 which each accounted for atleast 1% of nationwide U.S. enplanements. Medium hubs account for at least0.25% but less than 1% of nationwide enplanements, small hubs account forat least 0.05% but less than 0.25% of national enplanements, and nonhubsare airports that enplaned at least 2,500 passengers in 2015 but accountedfor less than 0.05% of national enplanements. The weights used for domesticairports roughly correspond to the relative level of enplanements handled byan average airport in each category. It should also be noted that while theFAA terminology refers to these airports as “hubs”, these definitions includeall nodes/airports in the U.S. system so the vast majority are not connectinghubs in the context of a network carrier’s hub and spoke network.

Table 3.1: Input parameters to ACQI model

Parameter α wL wM wS wN wLintl wSintlValue 0.125 1 0.21 0.05 0.01 1 0.5

For international airports, a more coarse breakdown is used due to lessavailability of reliable enplanement data. Thus large international airportsare those that were in the top 100 worldwide airports by 2015 enplanements,as defined by Airports Council International. All other international airportswere considered “small international”. Whenever the ACQI model is used inthis thesis, the weights and α value used are those shown in Table 3.1.

3.2 Aggregate Fleet and Capacity Statistics

As mentioned at the beginning of this chapter, analyzing fleet size and compo-sition is a first step towards understanding the evolution of airline networks.Figure 3.4 shows the fleet size and composition of major U.S. airlines in 2006.As noted before, carriers as shown include all merged entities as of December2015. Thus, for example, the Delta fleet includes Delta and Northwest main-line aircraft in 2006, as well as regional aircraft operating for Delta Connectionand Northwest Airlink that year.

47

Figure 3.4: Fleet size and composition of Major U.S. airlines, 2006

In this analysis, the widebody category includes any aircraft with two aislesin standard configuration, in line with standard industry nomenclature. Simi-larly, the narrowbody category includes aircraft operated by mainline carriersthat have one aisle, generally seating 100 or more passengers. Large regionalsinclude any aircraft operated by a regional carrier (on behalf of a mainlinepartner) with strictly greater than 50 seats. Small regionals are aircraft like-wise operated by regional partners but with 50 or fewer seats.

In the case of Delta and US Airways, some of the specific equipment typesof these airlines’ regional fleets are not publicly reported in their 10-Ks, andthus we are unable to determine whether these aircraft fall into the smallor large regional aircraft category. Regional aircraft reported as being part ofthese airlines’ fleets but for which seating capacity is unknown are contained inuncategorized regional aircraft. Additionally, due to the nature of the respec-tive data sources for mainline (Form 41 data via MIT Airline Data Project)and regional (10-K reports filed with the SEC) aircraft, numbers for mainlineaircraft represent a full-year average of operational aircraft based on quarterlyreports, whereas regional aircraft totals are based on a static count on Dec 31of the stated year, which might result in slight discrepancies between regional

48

and mainline fleet counts at any given time. This holds for all of the fleetanalyses throughout this chapter.

In 2006, around 5,100 aircraft were in scheduled service among the prede-cessors of today’s ten major carriers (including their regional partners). Sometrends clearly emerge: “Traditional” LCCs’ fleets were exclusively composedof mainline-operated narrowbody aircraft. Meanwhile, mainline narrowbodieswere the largest component of legacy fleets, representing 53%, 41%, and 46%of the total fleet operating under the American, Delta, and United banners,respectively.

Another notable data point is the presence of at least 1,000 small regionalaircraft in the fleets of NLCs. Use of small regional jets peaked in the mid-2000s, as airlines used these aircraft on increasingly large markets to offerhigher frequencies. However, as seen in the 2015 data (Figure 3.5), the rela-tively poor unit cost performance of these small aircraft, especially in a high-priced fuel environment, caused airlines to affect a drastic shift away from thisequipment.

Figure 3.5: Fleet size and composition of Major U.S. airlines, 2015

These small regional aircraft were mostly replaced (whether directly orindirectly) through the addition of large regional aircraft to legacy airlinefleets. The number of large regional jets in service under the legacy carriers’

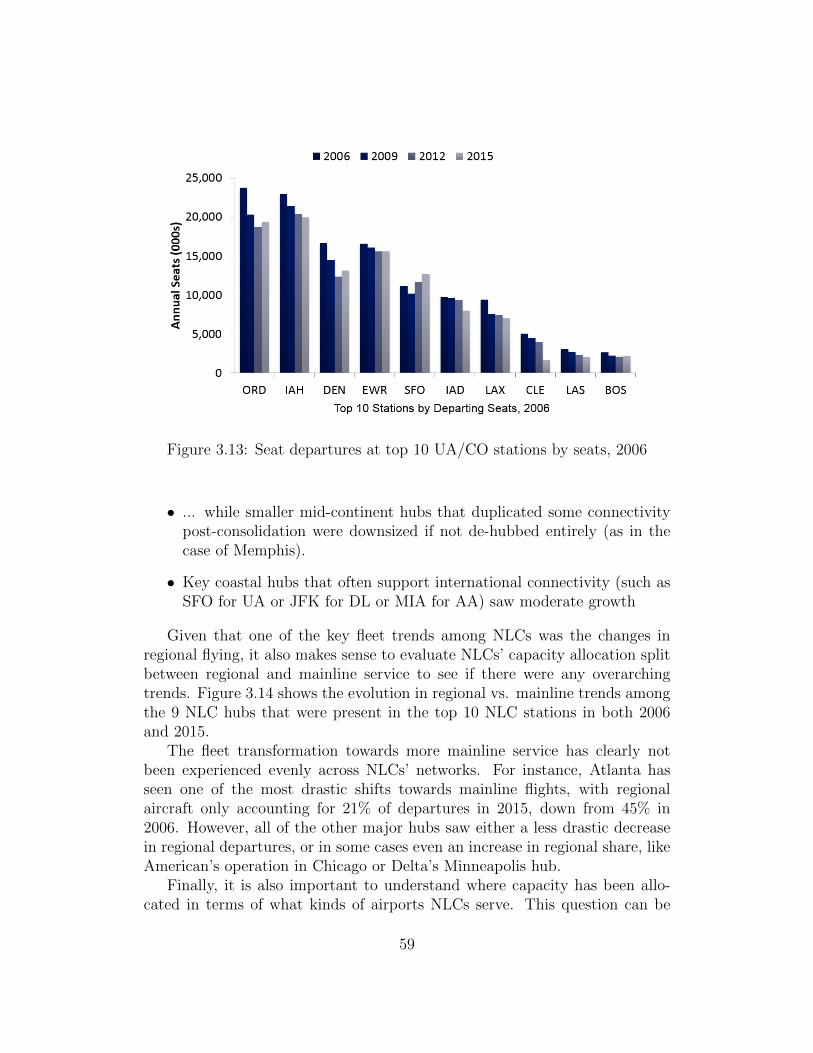

49

code more than tripled from 206 aircraft (along with some number of theuncategorized regional aircraft) in 2006 to 673 aircraft in 2015 (again, notincluding uncategorized aircraft).

The 2015 fleet stats shown in Figure 3.5 also shows the relative growthof fleets in the now-“hybrid” LCC and the ULCC sectors. As might be ex-pected, percentage growth was highest among the newest airlines over thepast decade: Allegiant’s fleet grew by 64 aircraft (585%), Spirit by 38 air-craft (122%), and JetBlue by 101 aircraft (95%). Whereas the other “hybridLCCs” also all grew their fleets, but their larger base fleet results in a lowerpercentage growth. LCC Southwest grew its fleet by 97 aircraft (17%), whilelegacy-turned-hybrid Alaska increased its fleet by 14 aircraft (8%) and alsomade upward adjustments in gauge. Traditional LCC-turned-ULCC Frontiersaw the smallest absolute growth of 7 aircraft over the 2006-2015 period, fora fleet growth rate of 13%.

Given that airlines have these fleets available to operate, another key metricinvolves block hour utilization. Since strategic flight scheduling to maximizeutilization (and thus lower unit ownership cost) is a “classic LCC hallmark”(Gross and Luck, 2013), evaluating how this metric has changed for LCCs andULCCs and comparing them to NLCs can provide insight into the evolutionof all three business models. Answering these questions requires operationaldata, so the data source used for this analysis is the formatted DOT Form 41data accessed via the MIT Airline Data Project.

Figure 3.6: Average daily narrowbody block hour utilization by airline type,2006-2015

50

Thus, the analysis is based on operating carrier, not marketing carrier.Furthermore, in order to more directly compare the different business models,we will only evaluate mainline narrowbody utilization (excluding widebodystatistics for NLCs that can skew results) to get an idea of relative utilizationof the same class of equipment. Figure 3.6 shows the results of this analysis.

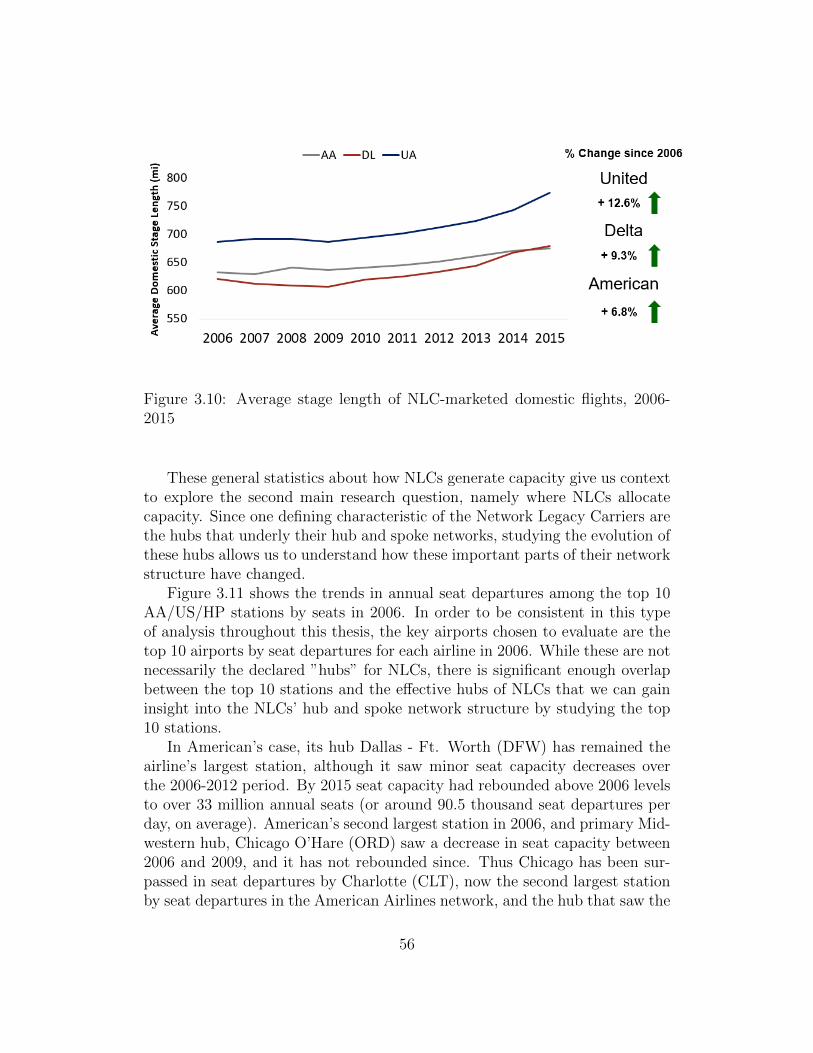

Some key trends that are interesting to note: First, all types of carriers sawa reduction in utilization from 2006-2009. This resulted from fewer scheduledflights, which was itself a response to increasing unit costs due to high fuelprices and later decreased demand during the recession. While airlines sched-uled fewer flights, they weren’t able to reduce their fleet size accordingly, thusutilization slipped 6.3%, 7.8%, and 8.7% between 2006-2009 among NLCs,LCCs, and ULCCs respectively.

After 2009, the trends in utilization vary by carrier type. As a result ofcapacity discipline, NLCs saw limited ASM growth over the 2010-2014 pe-riod, and as most of their new-build aircraft were replacing older models inthe fleet, block hour utilization correspondingly remained low but has grownslowly from its 2009 trough until 2015. As a group, LCCs tended to increaseutilization from the 2009 low until 2013 as fuel prices remained relatively highyet demand was rebounding. However, utilization slipped a bit after 2015,possibly as a result of lower fuel prices which meant that aircraft could beused less frequently while still maintaining a lower unit cost. More details onLCC utilization are covered in Section 3.4. Utilization at ULCCs continued tofall from 2010-2012, partially driven by Frontier’s transition to a full ULCCand Allegiant’s continued pursuit of low-capital-cost aircraft, before rebound-ing from 2013-2015 (driven by Frontier and Spirit). Airline specific utilizationstatistics providing more insight into this trend are found in Section 3.5.