update: a summary of single aisle activity€¦ · • expect keener pricing from boeing to steady...

TRANSCRIPT

Update:A summary of single aisle activity

Stuart Hatcher – CIO

• Economic View

• Traffic

• Narrowbody Market

• Rest of the year

2016 Catch-up

Economic Outlook

Signals

• Oil

• Interest Rates

• GDP

• World Trade

• USD

Regional Forecast

• Europe

• North America

• China

• Latin America

• Asia Pacific

• World

2016 2017

Pax Traffic remains steady

Source: IATA

• Passenger traffic growth up at 7.9% in February,

• Whilst economic signals look poor for China, service industry business growth continues to hold.

• Once again, India remains on top. Fastest growing economy and >20% YOY growth and growing

• Domestic Japanese & Brazilian market remains under pressure.

• Russia recovered well in March after loss in January

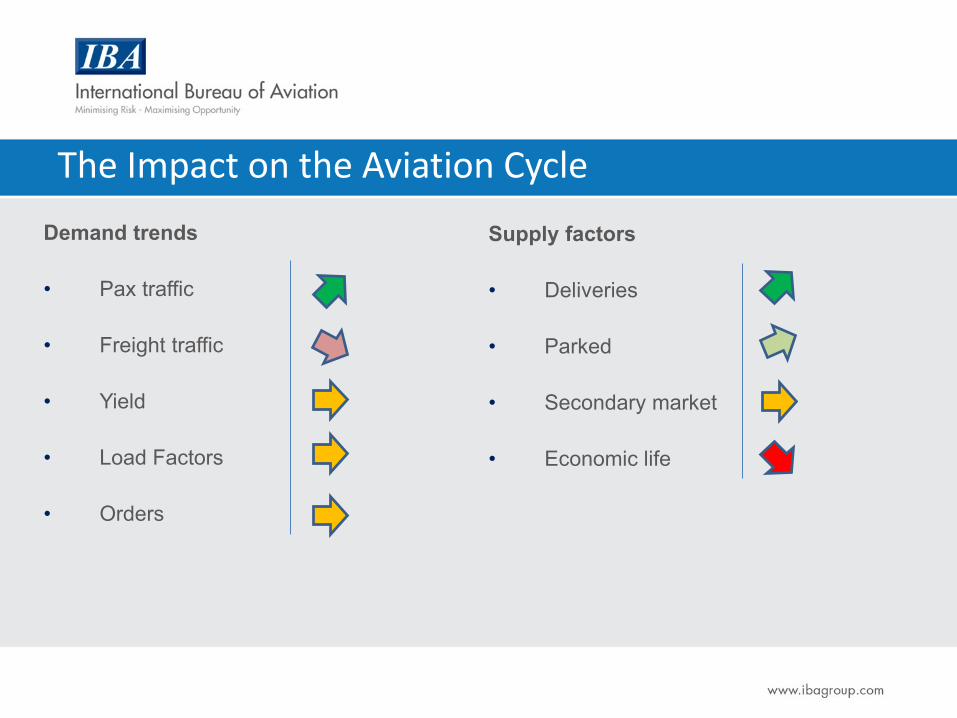

The Impact on the Aviation Cycle

Demand trends

• Pax traffic

• Freight traffic

• Yield

• Load Factors

• Orders

Supply factors

• Deliveries

• Parked

• Secondary market

• Economic life

Single Aisle

• Slow orders for 2016

• Oil may shift focus

• Fewer lessor orders with more bias

towards operators that haven’t bought yet

• Expect keener pricing from Boeing to

steady 737MAX market share

• Availability Falling

• Storage Falling

• Lease Rates under pressure – will leak

into pricing

• Market remains liquid across all ages,

but…. At a price

Sale & Leasebacks

Sales with leases attached

Lease Rate Factors

OEM pricing

Lease Term Lengths

Extensions

Potential New OrdersA320 family Operators Fleet Backlog

AMERICAN AIRLINES 363 138

CHINA EASTERN AIRLINES 250 0

EASYJET 249 174

CHINA SOUTHERN AIRLINES COMPANY 238 0

AIRASIA 174 306

JETBLUE AIRWAYS 159 87

UNITED AIRLINES 153 0

LUFTHANSA 151 126

TAM - LINHAS AEREAS 134 0

BRITISH AIRWAYS 131 35

DELTA AIR LINES 129 79

AIR CHINA 128 0

AIR FRANCE 122 3

LATAM AIRLINES GROUP 112 78

INDIGO 108 426

VUELING 106 58

UNDISCLOSED 104 676

TURKISH AIRLINES 103 100

SICHUAN AIRLINES 100 0

AIR CANADA 94 0

AEROFLOT RUSSIAN AIRLINES 87 0

SPIRIT AIRLINES 85 81

ALITALIA 79 0

SHENZHEN AIRLINES 78 0

WIZZ AIR 67 144

AVIANCA 67 136

AIR INDIA 66 0

AIR BERLIN 65 3

Potential New OrdersB737 family Operators Fleet Backlog

Southwest Airlines 599 248

Ryanair 351 223

United Airlines 312 139

American Airlines 271 134

China Southern Airlines 147 25

Delta Air Lines 141 62

Air China 138 22

GOL Transportes Aereos 134 71

Hainan Airlines 128 9

Xiamen Airlines 125 37

Alaska Airlines 129 60

WestJet 114 70

Lion Air 108 240

Shandong Airlines 90 13

Shenzhen Airlines 86 7

Turkish Airlines 92 86

SAS 85 0

Garuda Indonesia 80 50

Virgin Australia 74 45

COPA Airlines 76 70

China Eastern Airlines 76 43

Jet Airways 70 75

Qantas 67 0

Shanghai Airlines 72 0

Norwegian Airlines 59 130

Considerations – Single Aisle

• New generation engine technology reliability & reserve rates

• Economic life debate continues

• Premium of neo/MAX ‘v’ ceo/NG

• Developing economic market softness

• Lease rate factors under pressure

• Shorter lease term economics

• Order bubble

• Lots of interior flexibility but will it lead to marginalised fleets

• Ramp ups on the way

Values & Rates – Single Aisle

• A320-200

• A319-100

• A321-200

• A320neo

• A320 Classics

• 737-800

• 737-700

• 737-900ER

• 737 MAX 8

• 757-200s

• 737 Classics

Other Asset comments

• Turboprops Storage rising, regional distress, falling lease rates & values

• Regional Jets Storage rising, demand remains strong for specific types, a lot of new

aircraft technology coming

• Twin Aisle Storage rising, A330 production line bridged, 777 still has some way to

go. Softness in placing speculative orders – challenged by low oil price.

Appetite remains intact on financing for new deliveries to good credits

• Freighters Out of production large freighters still in turmoil, narrowbody demand

rising

What’s coming up…

• Economy – weak growth on the horizon – generally uneasy

• Traffic – on the up, LFs holding steady, freight struggling

• Airlines – great revenue for some, strong USD squeezing profits

• Developing economies dependant on oil – airline bankruptcies ahead

• OEM Challenges: Ramp-ups, market share

• Lessors – sales in the pipeline, falling LRFs, increasing competition & new accounting

rules